Embed Size (px)

Citation preview

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 1/12www.ecell-iitkgp.org/theentrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 2/12

They say choosing your spouse is the most important decision you will

make in your life. Similarly, choosing your co-founder(s) is the most

important decision you will make while building your startup, since

one could argue that at least for some period of time, you’ll be

spending more waking hours with your co-founder than your

significant other. Great partnerships are like marriages, they need a lot

of common ground, strong mutual attraction and a willingness to work

hard - especially through the inevitable issues.

You first need to dispel the delusion that you don't need a co-founder.

You do. You may have all the requisite skills, but even then, co-founders

help spread the work and make better decisions. Sure, you can talk to

your brilliant self, but that's not as effective. The selection of co-

founder(s) is one of the key determinants of long-term success in a

startup. But if you have the wrong guy, that's a hard problem to get

over with.

Knowing them beforehandThe idea is that by having gotten to know the person, you’ve already

had a chance to see how they work, how they think and whether you’re

likely to get along. This makes your college or workplace friend circle a

very useful hunting ground for a potential business partner. Consider

Chad Hurley, Steve Chen and Jawed

Karim, for instance. Chen and Karim

were classmates at the University of

Illinois, who then met Hurley at

PayPal, where all three were

employees. They then founded

YouTube, which received funding from

Sequoia Capital, whose partner Roelof

Botha, who also joined the YouTube

board of directors, was the CFO of

PayPal.

You better be good friends with them

as well, since you're going to spend a

lot of time working together. Also,

there will be times in the startup lifetime that will test your relationship

with your co-founder, so make sure you understand the stakes before

going in.

Someone you can trustMistrust can be a cancer for your startup. The good news is that you

can avoid it by choosing a

founder you trust, and then work

to foster deeper trust in your

relationship over time. Keep in

mind that it’s a never ending

process.

Play fair. You can’t expect others

to care as much about the

business when they don’t see themselves getting a fair share. This goes

hand-in-hand with trust.

Great minds think alikeThere should be aligned interest and commitment from your co-

founder. You both have to (at some level) be committed to not only

building a company, but the same company. If one of you wants to

create a company you run forever (and reap profits) and the other

wants to take a shot at a high-flying startup that gets sold or goes public

some day, you’ll have a problem.

Of course, co-founders may influence each other’s decisions in this

context. Afterall, Larry Page’s "BackRub" might just have remained a

research project on citation backlinks in research papers, with limited

commercial value, unless Sergey Brin, a fellow Stanford Ph.D. student

and close friend, had not come to the rescue and worked with him to

make it what we today know as Google.

Choose your complimentA co-founder should be strong in areas you are not. A great compliment

to your skills is someone who

loves to do things you hate,

someone who makes the

sum of your parts greater

than the whole. If Steve

Wozniak had remained the

nerd who was s imply

sceptical of the idea of selling

computers, and had not

been convinced by Steve

Jobs, the born-entrepreneur, to come up with a company so that they

could at least say that to their grandkids, neither would’ve conceived

Apple Computers independently.

Make sure at least one of the founders has the technical expertise. This

is so you don't have to try and outsource the actual product

development. Similarly, make sure at least one of you can sell. No great

idea is of any use to a startup that can’t

market it properly. Effectively, you need

to identify your “type”, and look for the

corresponding complementary skill in

your partner.

Practice, not just preachYou need a co-founder who can get

things done. If you have a great idea,

and you want to bring it to life, findsomeone who is passionate about your

vision, and who is willing to work for it.

Since startups involve lots and lots of

work (some fun, some not so fun), part

of the value of your co-founder should be that the work can be

distributed. If your co-founder is too “strategy” focused too early, you’ll

get buried because there’s too much to do.

Passion is easy to spot. Years after the two had befriended each other in

Lakeside School, Seattle, where they used to tweak the school’s

scheduling program to place themselves in classes with more female

students, and had faced several penalties for other naughty uses of

their programming skills, one of them dropped out of Washington

State University and called on the other (in Harvard then) to do the

same, for starting a venture together. Both understood each others’passion and immediately complied. They were Paul Allen and Bill gates,

and thus we have, Microsoft.

Talk the talkHave the hard discussions around equity, compensation and

responsibilities early. This stuff does not get easier over time – it gets

harder.

How should the division of shares be controlled? Who will make the

decisions? What happens if one of us leaves the company? Can any of

us be fired? By whom? For what reasons? What are our personal goals

for the startup? Will this be the primary activity for each of us? What

part of our plan are we each unwilling to change? Will any of us be

investing cash in the company? If so, how is this treated? What will wepay ourselves? Who gets to change this in the future?

Deferring these conversations is a great way to ensure problems later.

So what are you waiting for? Step out and start looking!

Two’s CompanyAuthored by Shrey Goyal , this article explores the importance of choosing the right co-founder for your dream venture, and

enumerates the various points which you may have to consider before committing to a partnership for your company.

www.ecell-iitkgp.org/theentrepreneurPage 2 The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 3/12

h t lT e recent episode of fraud by he Chairman of Satyam and a l thee s a dsev ral other fraud perpetr te by other entrepreneurs around the

l i e i T swor d s a shame on the name of entrepr neursh p. hese i olated

s a r iepisode have a tendency to m ke othe entrepreneur's l fe tougher.

h i a e l tT ey br ng a b d name to th ilk. They are usually fol owed by ougher

r nregulations, which have a tendency to rest ict freedom of busi ess

h f a e o rc oices or entrepreneurs. They m k c nduct of business mo e

e o r k r m lexpensive. Financi rsto increase the is p emiu and genera ly make

o e e g o y. b eentrepreneurs gr v l mor to et at their m ne All ecaus , someone

r n r h hgot g eedy a d unsc upulous. T e price t at genuineentrepreneurs pay

r t efo he fault of th se scamsters is so huge that it is

pworthy of a self disci lined vigil within the

mco munity itself. There is a case for them to

a t m vbecome c ive police en of themsel es and blow

h t ythe w istle when he see one of their cohorts

behaving funny.

g e n g nIn my lon exp rience fu din , raising fu ds and

v t erating the entrepreneurs o er the pas thirty y ars, I

s nhave seen two tages when the bug of cheati g

h h d sbites t e entrepreneurs ar e t for different

p n e hreasons - at the initial hase and o ce succ ss is established. When t e

t t r o m teproject is in the ini ial phase he e is a f cused pursuit of a li i d

i bobjective – may be a small project- dr ven y a passion to succeed and

i se h egambling everyth ng to increa t e prospects of success. Th re is not

i d a rmuch care g ven to forms, rules an norms, perh ps not affo dable as

l a r ewe l, s typically entrepreneurs sta t poor, are up against establish d

a e h ipl y rs who are muc more powerful. Some entrepreneurs m stakenly

h t i to e s c ,believe t at he r only way succeed is to pursu ome short uts

n t r ewhich seem to work for sometime. Unfortu ately the road tha g e ts

nt n ae repreneurs i Indi is often littered with obstacles and tempting

a o d g y to h ptach nces f r wrong oin and man fal l prey t ose tem tions and

m hcompulsions. This it seems has beco e the norm rather than t e

sexception. It is unfortunate because, tho e entrepreneurs of lesser

t i ss y a l ocompe it vene and objectivit do f l prey to this and compr mise so

s t emuch of their busine s fu ure. They nev r learn the right way of doing

s h o d s c p b e o ubusine s. T ey do n t un er tand om etition and eli ve c rr ption to

l n . d p g k lbe a egitimate part of busi ess They donot evelo stron wor cu ture

a h t n l mand le dership wit in their organiza io , fi ling the instead with

c p i r iin om etent staff that w ll lea n to man pulate rather than work smart

s f lto ensure business success. Mo t harmful o all they wi l earn for

v e ta h m nthemsel es an ill r pu tion, w ich ay be tolerated, but ever

e t r b c e nrespected and henc will no eve e the hoic partners for fi anciers

n mandbusi ess en.

h sh f The second stage when entrepreneurs go off track is w en the flu o

c s p s e isuc ess many time owers them with a ens of invincib lity. There is

i r e l c y a seither a cool ng off o a phas of comp a enc th t set in or a

a p p , smegalomani that rods them to lay 'god'. In either case focus hifts

o a u h e d t taway fr m man ging the b siness wit th e ge that ensuredi s ini ial

c d d r isuc ess, an business falters. Instea of co rect ng that in the right

n r e e s r o uma ne , entr pren ur es rt to short cuts that their newly acq ired

a s o c'power status' offer them nd et down the path of wr ngdoings whi h

n a l loften bri gs them to co lapse. Some of the we l known global

l nt l nt f phi a hropists, such as Rockafel ers we through this process o

o e r s o o r ometam rphosis, r po tedly tarting f as bo tlegge s, but wh them

e t m urede med he selves before it was too late and earned a respectf l

b l ntplace in society and history y becoming phi a hropists!

i a o t e tThe niti l period f struggle se s th tone for he character andbehaviorg i c e e s. Pr i iof entrepreneurs throu h the l fecy le of th ir v nture Azim emj n

l e te v e k a othe ear y 80s, is r pu d to ha e d clined to 'ta e c re' f some corrupt

h y r o a t l ta f officials in is h d ogenated il plant in Karnatak in he ear y s ges o

e i ehis entrepr neurial l fe. As a result, the officials closed the plant on fals

charges of flouting of excise rules. Azim Premji did not buckle down; let

the plant remain shut, while fighting the case legally. It took reportedly 3years for him to come out victorious, thanks also to the support of the

employees of the plant who were also suffering, and reopen the plant.

While it was painful, the episode surely sent a clear message to all that

Azim Premji is not to be messed around and I seriously doubt if he has

ever been harassed on that front ever after. More importantly, it is still

remembered and recounted as a legend in principle based

entrepreneurial behavior. The way I look at it, Mr Premji invested the

suffering caused by that incident, including massive financial losses in

creating a credibility capital, from which he is still reaping benefits. This

early strength in his resume ensured businessmen

and financiers around the world respect Mr Premji

as a trusted business partner, aiding him

considerably in his ventures to date.

While there are connotations of ethics and moralityassociated with the notion of integrity, I am

focusing on the competitive advantages of integrity

as a corner stone of entrepreneurial behavior. Once

an entrepreneur earns the credibility as a person of

integrity, doing business becomes that much

easier. Partners will seek to do business with such an entrepreneur who

they can trust, and might be even willing to pay a premium for that

feeling of comfort. Financiers will vie with each other to provide funds,

as they know their money is relatively safe with such an entrepreneur.

Once the entrepreneur sets the limits on acceptable behavior based on

principles of integrity, he and his team in the organization know that

they can not resort to short cuts and need to be genuinely competitive

to succeed in business. This makes them seek real competitive

advantages and conduct business to succeed against not only other

routine businesses, but also some that may 'enjoy' advantages due to

practicing business without integrity. This is not easy and I am not asking

the entrepreneur to be a monk.

Let us take a live example from the field of road contract business. Let us

assume there is one contractor (called Mr I) who behaves with

completely integrity and there are others whose integrity quotient lets

say varies from awful to 'godawful'. The challenge that Mr I faces when

he bids for a contract are that he needs to take into account the

possibility that the bidding process is perverted to favor the others

because they may ply bribes, or for someone in the bidding organization

to let these corrupting bidders know the lowest bid amount, so they can

quote a marginally lower prices and win the contract, etc. Can Mr I can

overcome this challenge while maintaining integrity? Yes. There are

many things he can do, including, finding technological solutions to

render road building less expensive and hence can quote so low that

others without that technology may find it unattractive to bid at those

prices. He could resort to the new provisions of Right To Information

(RTI) to shed the required extent of transparency in the bidding process.

He could build high quality roads on a pro-bono basis to demonstrate

the longevity and riding comfort, and hence win the support of the

users, who could be used to campaign for him. Incidentally these are

ideas I picked up from several good contractors' real life experiences.

Let us not kid ourselves. It is tough to be straight. But who said being an

entrepreneur is a cake walk? But setting your behavior right from the

beginning, though might make it tougher, straightens a lot of stuff for

the lifetime of clean, successful business. Giving into pressures or

temptations to cut corners usually sets entrepreneurs on a slippery slide

that look so inviting and harmless at the beginning and then keepsgetting harmful over time to what Ramalinga Raju calls the 'riding the

tiger, without knowing how to get out without being eaten'

phenomena.

Integrity - A Corner Stone of EntrepreneurshipBy Mr. R. Ravimohan, MD and Region Head of Standard & Poor’s South and South East Asia division , and also the appointed

chairman of the CRISIL Board of Directors. In wake of the recent Satyam scandal that has caught the entire corporate world in a

flurry of uncertainty, Mr. Ravimohan discusses about the moral issue that every entrepreneur today needs to address.

Mr. R Ravimohan (Left)

www.ecell-iitkgp.org/theentrepreneur Page 3The Entrepreneur

Contd on page #7

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 4/12

tIn a start up it’s important to maintain the balance between interes s of

operating the company within the fiscal budget and attracting,

developing, retaining, and rewarding high quality staff through wages

and salaries which are competitive with the prevailing rates for similar

employment in the labor markets.

If you have a startup, cash is not something you can afford to squander.

But at the same time you need to hire good employees, who will share

your vision about your startup and work with you to reach there.

nIn general there are four tools for employee *compensation amely,

1) Base salary

2) Short term incentives and bonuses

3) Long term incentive plans (LTIP)

4) Employee benefits

Start ups need to work on the forms of non cash compensations.

Employee stock options (ESOs) and Employee stock ownership plans

(ESOPs) come under this head. Furthermore you may frequently find it

necessary to borrow money in order to finance corporate growth. One

disadvantage of *debt financing is that repayment of the loan principal

eis not a deductible expens . An ESOP can be used to mitigate this

problem by having the company issue newly issued *stock or treasury

stock to an ESOP. The resulting tax savings can then be applied against

uthe principal payments so that tax-deductible r pees are used to pay

part, or all, of the loan principal.

An ESOP is nothing but an option to buy the company's share at a

certain price. This could either be at the market price (price of the share

currently listed on the stock exchange), or at a preferential price (price

elower than the current market price).If the firm has not y t gone public

(shares are not listed on any stock exchange), it could be at whatever

price the management fixes it at.

The ESOP is particularly advantageous for startups, whose growth

requires the reinvestment of profits, resulting in a shortage of cash

available for employee benefits.

There are many ways in which this can be done. If your company hasalready gone public, suppose you buy shares worth Rs100 in the

employees’ name when he joins and keep buying shares worth Rs100.

You can give these shares to him as a bonus after three years of his

employment. Or if your company is not public, you can tell your

employees that they will earn x number of shares for every year they

work and at the end of say 5 years he will get those shares.

There can be many more ways. This is the philosophy of sharing wealth

with the employees. It encourages an ownership feeling among them

and they work accordingly. It is also a tool to motivate employees to

perform better and to retain talented hands.

With employees owning stocks in the companies they work in, theirperformance would directly result in better prices for the stock and

dividends, not to mention better capital appreciation for employees

and dealers. Thus the story comes a full circle here.

Your startup can allocate stock options or ESOPs depending upon

various factors such as regular compensation, bonus for better

performance, etc.

Your company can either grant ESOPs to prospective employees at the

time of joining itself or the employees might become eligible on

completion of one or more years of service with the company.

Typically, the maturity period for ESOPs is three to five years - allowing

the company issuing ESOPs to retain talent and keep them motivated.

But ESOPs have also been issued by companies with a provision for

employees to offload a certain percentage of their ESOPs in the very

first year itself. The balance is then spread out over the remaining

period of maturity, with the bulk of the options to be cashed at the end

of three or five years from allotment. This lock-in period is fixed so that

it acts as a deterrent to employees wanting to change jobs. In case an

employee does jump ship, then he can at least cash in on some of his

earnings. Some companies also structure ESOP in such a manner that

no dividend is paid during the tenure of the lock-in.

How the Plan is Designed

An ESOP is an equity-based deferred compensation plan. As such, it is in

the same family as profit sharing plans and stock bonus plans. An ESOP,

however, differs from a profit sharing plan in that an ESOP is required to

invest primarily in employer securities, while a profit sharing plan is

usually prohibited from investing primarily in employer securities.

An ESOP also differs from profit sharing plans and from stock bonus

plans in that an ESOP is permitted and authorized to engage in

leveraged purchases of company stock. Consequently, an ESOP

required different accounting procedures and a different method of

allocating stocks and other investments among the employees than

other types of plans.

The ESOP, like a profit sharing plan, must cover al l nonunion employees

who are at least age 21 and have one year of service. However, an ESOP

may either include or exclude union employees.

In practical effect, share ownership under the plan is usuallyproportionate to the relative salaries of the participants in the plan.

How the plan works

The Employee Ownership Plans use a host of plans through which they

deliver the goodies. It could be a stock option scheme -- which is the

most commonly used. A stock option gives an employee the right to

purchase a set amount of shares at a fixed price for some years into the

future. It could be a stock purchase or a *restricted stock. Some types of

plans involve actual purchase and holding of stock or a phantom stock,

or could be a cashless exercise.

A phantom stock is a bonus that rewards employees based on theincrease in the value of the company's stock, the dividend performance

of the stock, or both.

Some MNCs offer global stock options for stock listed outside India. The

*vesting period, that is, the period for which the option has to be held,

Different models of sharesused by start-ups for its employees

Authored by Shikha Singh , the article explores the various share models used as a compensation by start-ups to attract

employees during the initial stages of its business. A glossary section provided at the end of the article, elaborates on certain

phrases that are marked with an ‘*’ in the article below.

www.ecell-iitkgp.org/theentrepreneurPage 4 The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 5/12

differs from 2 to 5 years depending upon the industry, company and

management policy. A company could have more than one stock

option plan.

In order to assure marketability of the stock subsequent to

distribution, the employees must be given a *“put” option, which

enables them to require repurchase of their stock at fair *market

value. The plan is administered by a committee established by thedirectors of the company. All voting rights are normally exercised by

the committee.

However, employees are allowed to vote on any matters involving

*liquidation, dissolution, recapitalization, merger, or sale of all the

assets of the corporation.

Contrary to common misconception, selling stock to an ESOP need not

result in any loss of control by the current owner. In most cases, the

existing Board of Director members serve as the ESOP Trust fiduciaries.

Thus there is no loss of voting control.

Nothing in the law requires that financial statements be shared withplan participants. The only financial disclosure that is required is the

requirement that each participant be furnished at least annually with a

benefit statement that shows the number of shares allocated to his or

her account, and the fair market value of those shares.

The other issues that need to be dealt with relate to the determination

of the total compensation cost and the period over which this needs to

be used. Experts contend that as ESOPs are still in a nascent stage in

India, they should be valued using appropriate pricing models, and the

compensation expense should be reflected in the profit & loss

account.

Lately, companies have started to treat the difference between theoption price and the existing market price as an expense to be written-

off over time. This could be the time between the granting of options

and the time when they would be allowed to be sold in the open

market.

For instance, say ABC issues ESOPs to its employees at a price of Rs 10

as against the current market price of Rs 7,000. The difference of Rs

6,990 would be written-off as an expense in the books of ABC over a

period of three years, i.e. Rs 2,330 each year multiplied by the number

of shares allotted via ESOPs.

Eli Lily Ranbaxy is an example of a pharma major which extends its

overseas ESOP to its Indian employees. Infosys, leading Indiansoftware major, has been credited as having created a large number of

Indian millionaires. The employees who received the stock of the

company have benefitted manifold by the spectacular rise in the share

price.

These are a few examples of the companies which have tried and

succeeded with this concept in India.

As the capital market watchdog on securities transactions and

issuance, the Securities and Exchange Board of India, or SEBI, has

formulated guidelines for the issue and maintenance of ESOPs. They

have been formulated under Section 11 of the SEBI Act, 1992.These

guidelines, called SEBI (Employee Stock Option Scheme and EmployeeStock Purchase Scheme) Guidelines, 1999; apply to any company

whose shares are listed on any of the recognized stock exchanges in

India. This circular and the entire text of SEBI (ESOS & ESPS) Guidelines,

including the amendments made in 2008, are available on SEBI

website at www.sebi.gov.in under the categories “Legal Framework”

and “Issues and Listing”.

Glossary

*Employee compensation means the total cost incurred by the company

towards employee compensation, including basic salary, dearness allowance,

other allowances, bonus and commissions.

*Stock, is a share in the ownership of a company. Whether you say shares,

equity or stock, it all means the same.

*Option means a right but not an obligation granted to an employee in

pursuance of ESOS to apply for shares of the company at a pre-determined

price.

* Liquidation, when a business or firm is terminated or bankrupt, its assets are

sold and the proceeds pay creditors. Any leftovers are distributed to

shareholders.

*Vesting means the process by which the employee is given the right to apply

for shares of the company against the option granted to him/her in pursuance of the ESOS.

*Vesting period means the period during which the vesting of the option

granted to the employee in pursuance of the ESOS takes place.

*Initial public offering (IPO), also referred to simply as a "public offering" or

"flotation," is when a company issues common stock or shares to the public for

the first time. They are often issued by smaller, younger companies seeking

capital to expand, but can also be done by large privately-owned companies

looking to become publicly traded.

*Debt financing is when a firm raises money for working capital or capital

expenditures by selling bonds, bills, or notes to individual and/or institutionalinvestors. In return for lending the money, the individuals or institutions

become creditors and receive a promise that the principal and interest on the

debt will be repaid.

*Restricted stocks are insider holdings that are under some other kind of sales

restriction. Restricted stock must be traded in compliance with special SEC

regulations.

*Employee stock option scheme (ESOS) means a scheme under which a

company grants option to employees.

*Employee stock purchase scheme (ESPS) means a scheme under which the

company offers shares to employees as part of a public issue or otherwise.

*Market price of a share on a given date means the closing price of the shares

on that date on the stock exchange on which the shares of the company are

listed.

*Treasury stock is the outstanding shares of stock reacquired and held by the

issuing corporation

*Capital Appreciation refers to a rise in the market price of an asset

*Lock-in period refers to the period under which a person cannot sell his shares,

generally with regards to an ESOP. Under this a person who has been granted

some stocks of the company cannot sell them immediately.

*Put option is an option contract giving the owner the right, but not the

obligation, to sell a specified amount of an underlying security at a specified

price within a specified time

www.ecell-iitkgp.org/theentrepreneur Page 5The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 6/12

SEEKING INTERNSHIPS THIS SUMMER

START-UPS ARE HIRING !

www.ecell-iitkgp.org/theentrepreneurPage 6 The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 7/12

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 8/12

u a i a . h m c e e a i n yVent re C p t l T e ter cat h s th ttent o of ever

sp r r p eu i r a l h a f r f va i ing ent e ren r l ke p ob b y no ot er. It is o m o pri atei u i g h t s p c l r b r s o t d toequ ty f nd n , t a i ty i a ly p ovided y p ofe si nal ou si ers a

g w s n s Gen r l y d c n a e o a nnew, ro th bu i e s. e a l ma e as ash i exch ng f r sh res i

e s o p y, u l nvest ent r u l i hth inve ted c m an vent re capita i m s a e sual y h g

i , t f er t po i o a o a g etu n rr sk bu o f he tent al f r b ve- vera e r r s. A ventu e

a l ( ) i a er o a ch nvest e tc pita ist VC s p son wh m kes su i m n s.

u u a l e er d n to a o er m oVent res su l y pr f VC fun i g ny th for f

nvest e t su h a o n h y g t t a d t o hi m n , c s l a s, as t e e he d ed benefi f t e

u x er h t n r a i i p vi es A hreso rces and e p tise t a a ve tu e c p tal st ro d . s t e

n r p ta st sh r a mm n es re o u c i hve tu e ca i li a es co o d i f r s c ess w th t e

o p y, e n o er th l p ss ve e , bu e th tc m an h o l ng plays e ro e of a a i lend r t mor a

a p er h l wa t r n a a i g a e r tea oof artn . T e VC wil n to b i g on a m n g n p rtn r o m t

p u t h o l us l a i h er e t ehel r n he company. T e VC's g a is ual y h g (30-40 p c n p r

a r o t o r th e o o ent n hye r) retu n n he investment ve e p ri d f his involvem i t e

o p . T u h C u h t e o l w n g rc m any h s t e V ens res t a th company f l o s a a g essive

o h r e c nt i u e t s , xp o t a dgr wt st at gy He o r b tes xper i e e erience, c ntac s, n

i l T e p c f r a i i a s s c ed b l odisc p i ne. h resen e o a ventu e c p tal st l o lend r i i ity t

e u t u a s, t o e a e i r tedth vent re. Also, if he vent re f il he l ss s r d st ibu

e h t en u w l a he rs t s h o hbetw en t e en repr e r as e l s t investo , hu cus i ning t e

to h ep r ers a y.blow t e entr reneu p on ll

u c n e i si e b f eg u i e nvest e tB t o sider th fl p d – y or oing o ts d i m n ,

e r eneu r ta a l f th i y, t s a o t r nth ent epr r e ins l o e equ t and hu ll f he cont ol, i

u en e i a ep o a vent e c l hhis vent re. Wh mon y s cc ted fr m ur apita ist, t e

m a i o l n s l th n epr r s p p y, a d hco p ny s n o ger ole y e e tr eneu ' ro ert n ence

a y w l t u ch. h s s t n o r l n i a lusu ll i l no r n as su T i hif i c nt ol a o e s compel ing

s f r ny n e r rs s f drea on o ma e tr p eneu to el -fun .

C p t c t i u l t es i vent e h th e o nV s ex ec er a n q a i i n a ur t at ey ar g i g to

u i , t w m o a b n o m g i l tea df nd n he t o most i p rt nt ei g - a go d ana er a m an a

a e m k i a st g w n s c ol rg ar et n fa - ro i g e t r.

h u h e eye o u a i a i sT ro g th s f Vent re C p t l st :

: W o C lo k f en t a h t in hQ hat d V s o or in a v ture h t t ey migh vest t eir

mo ey ?n in

A:

A M t a t erlok it al - Can an Par n s:

“ t h g e vel t q i n i a ey u l a gAt he i h st le he uest o s: c n th b i d a real l r e

b i ess l ese p p a i n n f u r ks wus n ? A l th ro os ls sitt ng i fro t o s - it b ea do n into

t ee m n s thr ai a pec s.

M k d r st u t e a e T aar et, In ust y r c ur , nd th e m.

O e s t s ze e a e . a n u l g b ses ln i he i of th m rk t You c n ot b i d lar e usines in sma l

s es. o i h he r t h s to a e, r t h s to b g ow npac S e t er t ma ke a be l rg o i a e r i g fast

en u h s h t i w l a g in t e e 3-4 e s.o g o t a t i l become l r e h n xt y ar

Th s n a ec t t k i h t u s i y h pe eco d sp t ha we loo at s ow he ind stry i l kel to s a e

u th s i g e a a w e 0 et 1 hp. Is i go n to b sp ce her 10 companies each g % of t e

m k s O i l t e n i h % a ear et h are? r w l her be o e company w t 30 - 40% m rk ts a i y o o i a o ?hare, a rel t vel c ns l d ted p sition

I h n t i a p a s h m st i p r n p r , s t tea Ist i k he th rd p rt, erh p t e o m o ta t a t i he m.

t t t a th t n k i en A l b i e s l n derhis he e m a ca ma e t happ ? l us n s p a s un go

c a g a i W n d to b f h s m t r ea sh n e and f ce cr sis. e ee e con ident t i tea has hei r

t h g u ; e h e p ss o h ve th i g w ro t e ro nd th y ave th a i n; t ey ha e stay n po e to

s e f leeth inish ine.

S i k t s a e e l h 3 i f c o r l t lo I th n ho e r r al y t e ma n a t rs. There a e o s of detai s to

ea n f th se b s i l h .”ch o e o o ut e sent a ly t at

Ba r iv s i al:laji S in a - AureosCap t

“ o, r t yo a e k n a h e r, ay n a i toS fi st hing, u r ta i g a c ll on t e s cto s i g th t th s sec r

i o a d i o e o n i a d a ta e n h ss go d n w ll c ntinu to gr w, a d Ind a has n a v n g i t i

s cto o f h o s e e b g t e.e r. Y u irst ave t be able to e th i pic ur

T en u r yi g h t i c m a h s e t em s n msh yo a e sa n t a th s o p ny a th righ el ent i ter

o us n m d l c sto r h te t es b n h sf b i ess o e , u me s -- w a ver i tak to e a player i t ii d r a d a u r t a e.n ust y n c pt re ma ke sh r

A i d y, e m s i r n t f er l t i e l l end th r l th o t mpo ta t hing a t al his s: d o you r al y ik

t p m ter h n t c m a o yo s w e ihe ro o s, t e fou ders of he o p ny? D u ome her th nk

t t h s p e a e c m a ?ha t e e peo l r o p tible

Fourth, you see the valuation - only after all this valuation comes - and it

has to be acceptable.”

Avnish Bajaj - Matrix Partners:

“I think the frameworks that investors use to evaluate early stage

companies are very simple and very consistent.

Number one: is the market opportunity large enough? When we say

large, we are looking at whether is there a current market of at least 500

million dollars or a billion dollars.

The second thing that is extremely critical is: how good are the

entrepreneur and the team? What is their understanding of the market

opportunity, and what is their track record?

We look for various clues, because it is almost impossible to predict

who will succeed or not. But typically our view is that success and

achievement are not accidents. They are the outcome of a very

methodical process followed in life, though of course there are outliers

to this. You know: what have been they been their academicachievements, what have been their professional achievements, what

do other people think of them?

Thirdly, we focus on the industry dynamics within that opportunity:

what is the state of competition, how can these guys grow. It is little bit

more about the strategy the company is following in order to be able to

take advantage of that market opportunity.

So you said great market opportunity, great people…now, are they

understanding their environment and how they will have to operate?

And do they have a differentiator by virtue of which they can create a

sustainable business?

So that is really the framework.”

Russell Siegelman (HBS MBA '89) - Partner, Kleiner Perkins Caufield &

Byers :

“The most important requirement is a large market opportunity in a

fast-growing sector. We like a company to have a $100 million to $300

million revenue stream within five years. This means that the market

potential has to be at least $500 million—or more, eventually—and

that the company needs to achieve at least a 25 percent market share.

The second factor involves a competitive edge that is long lasting. It is

usually an engineering challenge that is tough enough to give the

company an edge, resulting in several years lead or longer, if we're

lucky. We look for a tough problem that hasn't been solved before.

The third thing is team. We look for engineering vision and execution,

sales, and entrepreneurship in a team. Entrepreneurs have to have a

clear sense of the opportunity and how to build the business. But the

best ones are willing to re-examine their assumptions and are willing to

veer left or right or pivot all the way around when the data suggests

they're headed in the wrong direction.So overall it's a funny mix. When we review an investment opportunity,

entrepreneurs have to have a pretty good story to tell about what they

want to do. I think it helps to be cocky, there's no doubt about it, but if

you're not sufficiently confident, you're not going to be successful in

selling your idea.”

Sonja L. Hoel (HBS MBA '93) - Managing Director, Menlo Ventures:

“I always look at the market first. By that I mean a strategic view that

includes evaluating market growth, market size, competition, and

customer adoption rates.

We have a process here called SEMS, or Systematic Emerging Market

Selection. We do a SEMS project for every investment we make. Twice

a year at our planning meeting, we talk about new markets or problems

that need to be solved.

We track four things and relate them to the success of our investments:market size, the team, unique technology, and whether the product is

developed at the time we invest. We found proprietary technology is

important but doesn't make much of a difference as a unique

differentiator for significant returns. Market size and a developed

From a Venture Capitalists perspectiveAuthored by Hridya Ravimohan , the article focuses on analyzing what exactly Venture Capitalists (VC) look for while investing in

a new venture. It comes straight from a VC’s perspective, containing excerpts of a number of VC interviews conducted via online.

www.ecell-iitkgp.org/theentrepreneurPage 8 The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 9/12

o ct t e t. We h be te k r du is tapr du ma t r mos have muc t r luc if the p o ct in be

s ippin , lt ou w inv t in a ps w t a de lop dor h g a h gh e do es st rt-u ithou ve e

o t. fte h s gre c log , s 't k dpr duc O n someone a a at new te hno y but ha n loo e

a rk t h e hn gy ing o e.t the ma e t e t c olo is go t serv

I orde re a rrie , te hn y a go to be ha d on r to c ate ba r the c olog h s t r t

e ut c nies pate d e ou axec e. Some ompa have nts; some on't. We nc r ge

th m o have p a e beca lit ious vironment thae t t nts use it's a more ig en n it

w s t y goa en ears a .

We a loo t the ma ge a . I w 'v got fou wlso k a na mentte m f e e a nder ho's in itfo the s or unw u de h a if neces ry, we ar life tyle illing to pgra t e te m sa have

c er n out illing ss to te m mem e .onv satio ab the w ne hire new a b rs ”

R b Si n t r, A r eo ert mo - Direc o lta Pa tn rs:

“ he a e o s h ug in e a t g ne op t nitie nT re r tw c ools of tho ht v lua in w por u s. I

the f st h ve pitalist in s on pe ple w k nir , t e nture ca ve ts in ly smart o ith a ee

se s o rtunity I t e t e , ent r pitalist only c rn e of ppo . n h o h r the v u e ca a es

a ut mark ts. I m n nt is ' h ma vebo e f a ageme n t up to t e rk, the nture

c pit lis w ix it. he ru h is ob io w e be e ba a t ill f T t t v usly some h re in tw en, ut I

te t pla e r e n the ma ortun y ve u h t mnd o c mo e w ight o rket opp it rs s t e ea .

I o e perie e, rket t ump t p op nd ech logy.n ur x nc ma s r bo h e le a t no

W e na sing the rk t f r a new p o t r s e e toh n a ly ma e o r duc o ervic , w try

d t w ther produ t a r c me fo a ist ge ermine he the c is epla e nt r n ex in

p o t o h the the prod t is of ring th ne ndr duc r w e r uc fe some ing w a

p ev usly unse T e p e ct c n b c tt rr io en. h re lac ment produ a e alled the be e ,c pe , fa t de ith se o rt nitie y n sthea r s er mo l. W the ppo u s ou ca e imate

ma e siz y k g at r e ue e is ctrk t e b loo in the ev n s of the x ting produ

ship ntsme .

C r ly, c provides new un na y viou lyonve se a produ t that f ctio lit pre s

u e , we ll br e orld m del. H e, t e ma e s e dnse n ca the ave n w w o er h rk t iz an

d ma a a nkno n. T se o n re in con u r c oe nd re re lly u w he fte a the s me se t r.

N ts a , Y ho , d So y W lkma a e mple h r nee c pe a o! an the n a n re xa s. T e b ave w

w model cert inly ha r er mar risk but no n c ss rilyorld a s a g eat ket t e e a

mo e te hni l r k.r c ca is

Ad ally, ther a ma - s. I we' too early, ther sdition e re rket timing issue f re e'

n rk t de nd nd e v to sur e nt t e d re c so ma e ma , a w ha e viv u il h deman a he

u . I that o time e have two r blem av k e hs n period f , w p o s: We h e to e p t e

d op n n fe e ryb d e may e susc ptible o be goors e a d ed ve ody, an w b e t in

leapf ge e hn gy. So w on t wa t e oo ear , b wrog d by t c olo e d ' nt o b t ly ut e

d a be t o .on't w ntto o lateWe a o ok a e h gy to ee how pr priet ry a dif ul hls lo t the t c nolo s o a nd fic t t e

solu io t the problem is. he id a ase is fou . s solvingt n o T e l c r Ph D. a

p o m h y' b e w g for w y a , an h y'r ble t e ve e n orkin on t o e rs d somehow t e ve

s ck pon the ma t n. An it' tw order o ma it de t rtru u gic solu io d s o s f gn u be te

tha h ev r lse ut t e . ally, nt the a on w at e e is o h re Fin we wa te m t have

c . We get l t co e e he e epre e m inonviction a it le nc rn d w n the ntr n ur co es

a say "I m i lip ye r. So if e ge ss nnd s, ' n this to f it in a a " w t the impre io

the in r h ou time then 's f ely a problem.”y're not it fo t e t gh s, it de init

Q: W l yo irst- e entrepren uou d u back a f tim e r?

A:

Ba a i in va - u Capi ll j Sr i s A reos ta

“ w ld ck f st time e epre . u o m irI ou ba a ir ntr neur B t t day y f st time

e t p ene r are d re y e u t ntial x nn re r u s iffe nt: the hav s bs a e perie ce.

T a no f ing o h ir bu in ss ; he r theirhey re t igur ut t e s e es rather w thec ny w suc d, beca y n h ir s e .ompa i ll cee use the k ow t e bu in ss

I n illing o live ith the t e pt n, hic I n't w hat'm ot w t w o h r o io w h is: do kno w

I oing ut w fig ut. h is no c a me'm d b I ill ure it o T at t a cept ble to .

Tod h is a c pt ble o usine nd I av onay w at c e a t me is: I know my b ss a h e d e

this f r X number of e rs an I e is hic ho y a , d now hav th idea w h is t e

e t h usine d know w h r w w or not, butx ension of t is b ss. I on't het e it ill ork I

kno big t r nd I kn at have e nts T isw the pic u e, a ow th I all the leme . his

w t Iba k t day.”ha c o

A o M l n a rtl k itta - Ca a n Pa ners:

“ 0% of ou busines in S rom epe t ent neurs his4 r s the U comes f r a repre . T

implies h la ger pa c s from pe ple h f stthat t e r rt ome o w o are ir time

e p ene rntre r u s.

An e ve open to b king ir ime e pre e t e nd nd w 're ry ac f st t ntre n urs in h I ia

c e t. re y se f t t ntre u s tha the We tont x He ou e more irs ime e prene r n in s

simply e au e hole de f bu a fa t-g o ing e rpb c s the w mo l o ilding s r w nte rise

a then in is fa ne .”nd exit g irly w

Avnish Bajaj - Matrix Partners:

“I was a first time entrepreneur when I got funded by ChrysCapital. I

don't think the issue is first time entrepreneurs. In fact, if you look at

some of the world's most successful entrepreneurs, they are all first

time entrepreneurs: Bill Gates, Steve Jobs, Larry Ellison.

Indeed, if you look at the track records of entrepreneurs who have

succeeded in their first venture, they typically don't succeed after that.

But yes, absolutely we would look to back first time entrepreneurs. I

think it comes back to whether they have a track record of achievementin their lives. It doesn't have to be as an entrepreneur.”

So to encapsulate the views of the above VCs, most of them

are looking for a good technology, backed by an efficient managerial

team to launch the product into a large market at the right time,

irrespective of whether or not the person is a first-time entrepreneur.

Another source of outside investors are 'angel investors'.

These investors differ slightly from VCs. The largely accepted difference

between the two modes of funding is essentially that angel funding is

more of 'emotional money', whereas venture capital is 'logical money'.

Many angel investors are successful entrepreneurs who want to help

other entrepreneurs get their business off the ground and usually

expect a lower rate of return than a VC. Usually they are the link from

the self-funded stage of the business to the point where the businessneeds the level of funding that a VC would offer. 'Angels' typically offer

expertise, experience and contacts in addition to money. Not much is

known about angel funding due to the individuality and privacy of their

investments.

Venture Capitalism is one of the most popular forms of

funding available to entrepreneurs today. It is one of the few doors that

one could unlock in order to enter the actual entrepreneurial world.

INTERESTING FACTS

?

Etymology of 'venture': "to risk the loss" (of something),shortened form of aventure, itself a form of adventure. General

sense of "to dare, to presume" is recorded from 1559. Noun sense

of "risky undertaking" first recorded 1566; meaning "enterprise

of a business nature" is recorded from 1584. Venture capital is

attested from 1943.

?ARDC (American Research and Development Corporation)

was the first venture capital firm to be in existence. Its main

purpose was to encourage private sector investments in

businesses run by soldiers, who were returning from World War

II.

?.Georges Doriot is known as the 'father of venture capitalism'.

He, along with Ralph Flanders and Karl Compton, founded ARDCin 1946. He is also co-founder of INSEAD Business School (1957).

?In 2007, U.S. venture capitalists invested $1.4 billion in China

and $1.0 billion in India.

?The origin of the Angel Investors occurs at the beginning of

the era of Broadway Productions to define those individuals who

used to fight all odds to put up the high risk and early stage seed

money to launch Broadway shows.

?Angel Investors accept an average of 3 deals for every 10

considered, whereas VCs accept 1 for every 400.

?According to a Wells Fargo survey in 2007, 73% of a ll ventures

in the USA are self-funded.

www.ecell-iitkgp.org/theentrepreneur Page 9The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 10/12

Company RegistrationRegistering a company is an obligation which every entrepreneur has to undergo. This article written by Rahul Kumar , is aimed

at providing complete information about the various nitty-grittys of the procedure involved and the costs incurred in getting your

company registered.

The selection of right business entity is very useful for the

success of an entrepreneur. The choice of entity depends on the

circumstance of each case. A company is a separate legal entity as

compared to its members. In a company, liability of shareholders is

limited to the extent of unpaid share or to the tune of the unpaid amount

guaranteed by the shareholder. On the other hand, a partnership is a sum

total of persons who have come together to share the profits of the

business carried on by them or any of them. It is not a separate legal

entity. The major disadvantage of partnership is the unlimited liability of

partners for the debts and liabilities of the firm. If property of

partnership firm is insufficient to meet liabilities, personal property of

any partner can be attached to pay the debts of the firm. Registration of

partnership firm is not compulsory up to the extent of 20 partners,

though registration has extra advantages.

Registration of companies under the Companies Act 1956 is

under the categories of private and public limited companies. The mostcommon form is Private Limited Company.

Private Limited Company: It is a company limited by shares in

which there can be maximum 50 shareholders, no invitation can be made

to the public for subscription of shares or debentures, cannot make or

accept deposits from public and there are restrictions on the transfer of

shares. The minimum number of shareholders is 2. It must have at least 2

directors. Minimum share capital is INR 1 lakh.

Public Limited Company: It is a company limited by shares in

which there is no restriction on the maximum number of shareholders,

transfer of shares and acceptance of public deposits. The minimum

number of shareholders is 7.It must have at least 3 directors. Minimum

share capital is INR 5 lakhs.

Recently the concept of Limited Liability Partnership (LLP) has

been introduced in India. LLP is an alternative corporate business entity

that provides the benefits of limited liabil ity of a company but allows itsmembers the flexibility of organizing their internal management on the

basis of a mutually-arrived agreement, as is the case in a partnership

firm. LLPs are intended as an alternative business organisation for small

scale industries and service sector enterprises, such as lawyers,

chartered accountants etc, which at present, are primarily constituted as

partnership firms in India.

A Sole Proprietorship is the most common type of business (like

the small grocery stores). It is a business entity owned and managed by

one person. It requires almost no legal formalities. For liability purposes,

the individual and the business are one and the same.

Steps of incorporation of a company:

1. Purchase (Digita l Signature Certificate) for Directors: It

is used on the documents submitted in electronic form in order to ensure

the security and authenticity of the documents filed electronically.2. Obtain (Director Identification Number) for proposed

directors: It is obtained by filling .

3. Name approval of the company: Availability of names could

be checked at (Ministry of Corporate Affairs) portal. Apply to the

concerned RoC (Registrar of Companies) to ascertain the availability of

name in by logging in to the portal. A fee of INR 500 has to be

paid alongside and the digital signature of the applicant proposing the

company has to be attached in the form. Select, in order of preference, at

least one suitable name up to a maximum of six names, indicative of the

main objects of the company. Ensure that the name does not resemble

the name of any other already registered company. The names can be

the coined name from the objects of the proposed company or even the

name of the directors, and of such kind. Whatever be the case, it should

be indicative of the main object of the proposed company. The name

justification is required to be specified along with the application.Further, the last words in the name are required to be "Private Ltd." in the

case of a private company and "Limited" in the case of a Public Company.

DSC

DIN

eForm DIN-1

MCA

eForm1A

Availability of names requires authorised capital for certain key

words:

Keywords Requierd Authorised

Capital (INR)

(1) Corporation 5 Crores

(2) International, Globe, Universal, 1 Crore

Continental, Inter-Continental, Asiatic,

Asia, being the first word of the name.

(3) If any of the words at (2) above is 50 Lakhs

used within the name (with or without

brackets)

(4) Hindustan, India, Bharat, being the 50 Lakhs

first word of the name.

(5) If any of the words at (4) above is 5 Lakhsused within the name (with or without

brackets).

(6) Industries/Udyog 1 Crore

(7) Enterprises, Products, Business, 10 Lakhs

Manufacturing.

4. After the name approval file for registration of new

company by filing the required forms (1,18,32) within 60 days of

name approval

Memorandum of Association (MoA): It is a document that sets out the

constitution of the company. It contains, amongst others, the

objectives and the scope of activity of the company besides also

defining the relationship of the company with the outside world. It has:

1) Name clause: The name of the company is mentioned in

the name clause.2) Situation of registered office.

3) Objects clause: It specifies the activities which a company

can carry on and which activities it cannot carry on. The company

cannot carry on any activity which is not authorised by its MoA.

4) Liability clause: A declaration that the liability of the

members is limited in case of the company limited by the shares or

guarantee must be given. The MoA of a company limited by guarantee

must also state that each member undertakes to contribute to the

assets of the company such amount not exceeding specified amounts

as may be required in the event of the liquidation of the company. The

effect of this clause is that in a company limited by shares, no member

can be called upon to pay more than the uncalled amount on his

shares. If his shares are already fully paid up, he has no liability towards

the company.

5) Capital clause: The amount of share capital with which thecompany is to be registered divided into shares must be specified

giving details of the number of shares and types of shares. A company

cannot issue share capital greater than the maximum amount of share

capital mentioned in this clause without altering the memorandum.

Articles of Association (AoA): It contains the rules and regulations of

the company for the management of its internal affairs. While the

Memorandum specifies the objectives and purposes for which the

Company has been formed, the Articles lay down the rules and

regulations for achieving those objectives and purposes. The

important items covered by the AoA include:-

1) Powers, duties, rights and liabilities of Directors

2) Powers, duties, rights and liabilities of members

3) Rules for Meetings of the Company

4) Dividends

5) Borrowing powers of the company

6) Calls on shares

www.ecell-iitkgp.org/theentrepreneurPage 10 The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 11/12

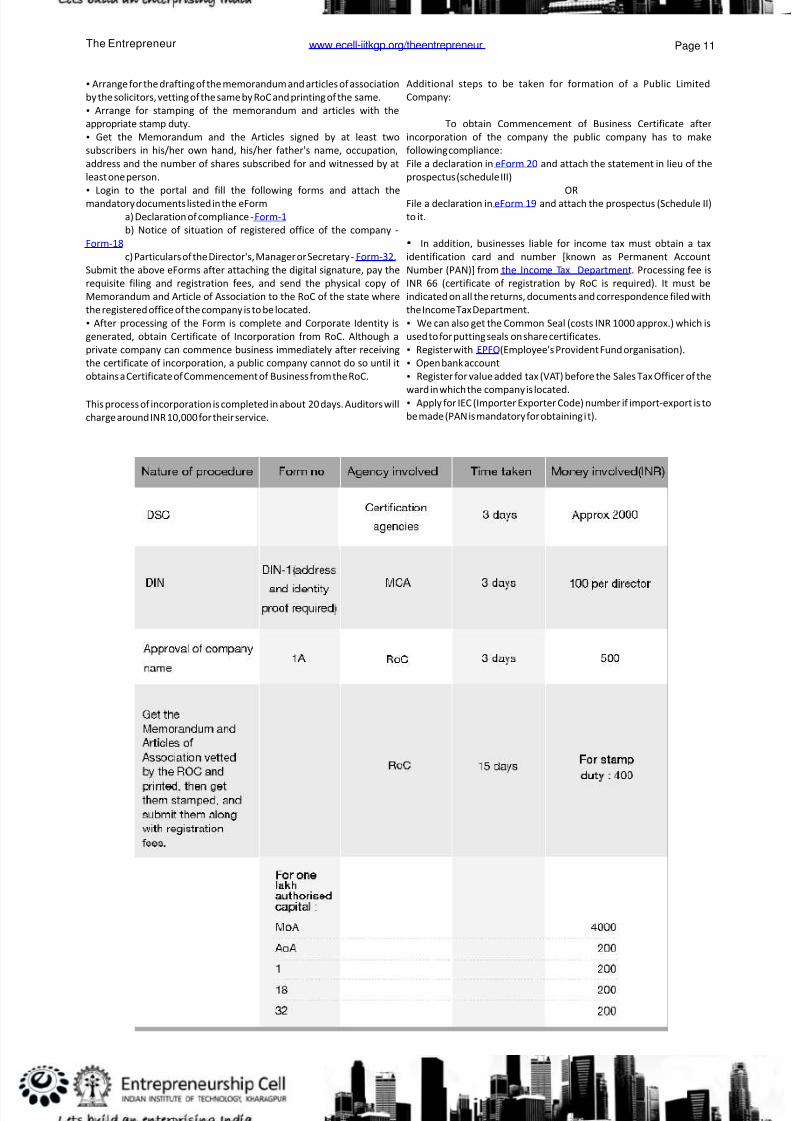

?Arrange for the drafting of the memorandum and articles of association

by the solicitors, vetting of the same by RoC and printing of the same.

?Arrange for stamping of the memorandum and articles with the

appropriate stamp duty.

?Get the Memorandum and the Articles signed by at least two

subscribers in his/her own hand, his/her father's name, occupation,

address and the number of shares subscribed for and witnessed by at

least one person.

?Login to the portal and fill the following forms and attach the

mandatory documents listed in the eForm

a) Declaration of compliance -

b) Notice of situation of registered office of the company -

c) Particulars of the Director's, Manager or Secretary -

Submit the above eForms after attaching the digital signature, pay the

requisite filing and registration fees, and send the physical copy of

Memorandum and Article of Association to the RoC of the state where

the registered office of the company is to be located.

?After processing of the Form is complete and Corporate Identity is

generated, obtain Certificate of Incorporation from RoC. Although a

private company can commence business immediately after receiving

the certificate of incorporation, a public company cannot do so until it

obtains a Certificate of Commencement of Business from the RoC.

This process of incorporation is completed in about 20 days. Auditors will

charge around INR 10,000 for their service.

Form-1

Form-18

Form-32.

Additional steps to be taken for formation of a Public Limited

Company:

To obtain Commencement of Business Certificate after

incorporation of the company the public company has to make

following compliance:

File a declaration in and attach the statement in lieu of the

prospectus (schedule III)

OR

File a declaration in and attach the prospectus (Schedule II)

to it.

?In addition, businesses liable for income tax must obtain a tax

identification card and number [known as Permanent Account

Number (PAN)] from . Processing fee is

INR 66 (certificate of registration by RoC is required). It must be

indicated on all the returns, documents and correspondence filed with

the Income Tax Department.

?We can also get the Common Seal (costs INR 1000 approx.) which is

used to for putting seals on share certificates.

?Register with (Employee's Provident Fund organisation).

?Open bank account

?Register for value added tax (VAT) before the Sales Tax Officer of the

ward in which the company is located.?Apply for IEC (Importer Exporter Code) number if import-export is to

be made (PAN is mandatory for obtaining it).

eForm 20

eForm 19

the Income Tax Department

EPFO

www.ecell-iitkgp.org/theentrepreneur Page 11The Entrepreneur

8/14/2019 Entrepreneur April 2009

http://slidepdf.com/reader/full/entrepreneur-april-2009 12/12

Entrepreneurship Cell [E-Cell] is a non-profit student organization with theaim of fostering the spirit of entrepreneurship among college students in India and

nurturing young people with bright ideas. With a team of highly motivated group of

IITians from Kharagpur and the support of encouraging faculty, E-Cell boasts to be

one of the most active student bodies in India - with more than 15 start-ups from IIT

Kharagpur itself within its three years of inception.

We, at E-Cell, strive to make all the worthwhile support available to

budding entrepreneurs and also present successful examples by conducting guest

lectures by eminent people. Case study competitions, Knowledge Camps, patent

workshops, and other focused business plan events are conducted throughout the

year to involve students in activities that help them gain an entrepreneurial bent of

mind.

Our annual competitions include:

Concipio: An exclusive in-house business plan competition, aimed at transforming

the raw ideas that are born here into full fledged business models

Pensez: A unique case study competition, with problem statements designed to

inculcate innovative thinking in topics relating to entrepreneurshipEclairez: A social entrepreneurship challenge aimed at those individuals who have

the gumption to empower those at the bottom of the pyramid

Envision: A product design competition, catering to those visionaries who have it in

them to impact our present, and revolutionize our future

Negocio: A web and mobile services based business plan competition that focuses

on individuals aspiring to startup in this very popular sector of today

Clean Tech Challenge: An event that aims at tapping the immense potential of this

promising sector of the future

ABOUT US

Editor: Naveen YS

Asst. Editors: Rahul Kumar, Hridya Ravimohan, Shikha

Singh

Write to us at [email protected]

Entrepreneurship Cell

www.ecell-iitkgp.org/ theentrepreneur

www.ecell-iitkgp.org/theentrepreneurPage 12 The Entrepreneur