Embed Size (px)

Citation preview

Ensuring Decades of Growth… �CAN WE REALLY SUSTAIN GROWTH?

23RD National Convention!

Prof. Enrique Soriano!

Resource Speaker!

Iloilo City, Philippines!

October 2014 !

• VP Greenfield Dev Corp

• Country CEO of Singapore based Electronic Realty Associates

• Chairman, Eastwood City

• Chairman, listed Sun Trust Developers

• Founding CEO, Travelers International (Resorts World)

• Founding Head, Megaworld Commercial Services Group

• President, Oceanic Realty Inc.

• Chairman, Marketing Com Phil. Retirement Inc

• Group CEO, Belo Medical Group at 38

• Semi Active from Corporate Life In 2008 at 40

• Executive Director AA Real Estate Advisory

• Turnaround Advisor Wong + Bernstein Advisory

• Book Author of

‣ Family Succession

‣ Business Turnaround Strategies

‣ Service Quality Modeling

• Corporate Receiver

• Family Business Advisor

• IPO Advisor

• Columnist, Asian Journal US

• Sought after Adviser and Speaker in Vietnam, Malaysia, Singapore, China, Indonesia

Why are investor’s shying away from China?

China’s property market is closely watched by investors. However, China real estate is in a catch-22.

Nervous Market

But when the housing market rises, with new home sales and prices increasing, the market gets nervous.

Investors think the housing bubble is out of control, and that becomes a sell signal more than a buy sign.

Nervous Market In short, housing development is a key driver of

local growth and employment. In China’s case total funds invested in real estate amounted to 19% of nominal GDP in 2012.

Economist Bell said that there are “clear signs of market weaknesses with climbing inventory, falling prices, and declining total floor space”—all of which point to a deflation in China’s property bubble.

Beijing Intervention

Systemic risk?

To contain a boom in China's housing market and keep prices affordable, Beijing imposed restrictions over the past five years. Those measures together with a slowing economy now appear to be having an impact.

Consequences of a Burst

"Sales dry up, prices fall, new [housing] starts to dry up, construction dries up, sales of construction equipment, concrete, and steel dry up, land sales dry up, local government revenues disappear and they can't pay their debts ... in other words, falling asset prices undercut the basis for both past and future lending, and you've got a real system-wide problem,”

Just like in China, our Developers, LGU’s and Regulators are the Weakest Link

If one property developer gets into trouble that could have a domino effect on the rest of the market," he said. "Without the central government taking action there will be a serious slowdown. Something has to be done and liquidity may have to be eased to help property developers

Housing Bubbles Vary

"The risks and exposure to property don't look the same as in the U.S. subprime [mortgage crisis], but new bubbles never look exactly like the last bubble (otherwise they'd be easy to recognize),”

Learning from our Neighbors "The real estate market has been the

downfall of many major economies in the past. So the worst case scenario for China's housing market is an economic crisis.

In China's case, credit expansion drives the housing market and when that slows it has a direct impact on real estate, says economists.

Lessons from my experience in Vietnam and China

When property developers can't get more credit, they have to slash prices to unload their unsold inventories (and pay back their debts), which gives investors second thoughts about whether to continue plowing their money into property,”

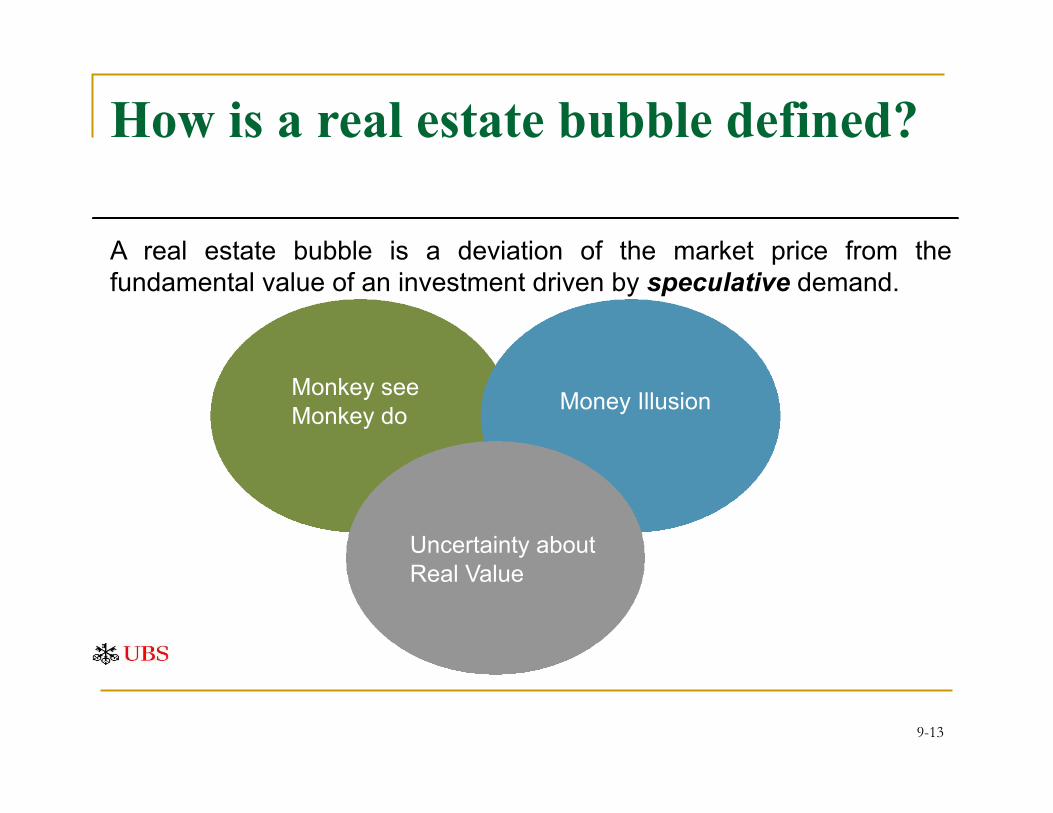

How is a real estate bubble defined?

9-13

Monkey see Monkey do Money Illusion

Uncertainty about Real Value

A real estate bubble is a deviation of the market price from the fundamental value of an investment driven by speculative demand.

Ass

et V

alue

Time

Bub

ble

Market value

Fundamental value

Rationale

Traditionally, the housing market has not been as subject to pricing bubbles as other asset markets have been because the large transaction costs of purchasing a home and the carrying costs of owning and maintaining a home discourage speculative behavior but…

Irrational Exuberance

… housing markets do go through periods of "irrational exuberance". In this talk, we'll discuss what causes housing price bubbles, the triggers that cause housing bubbles to burst and why home buyers and developers should look to long-term averages when making critical housing decisions.

We apply Physics taught in School

The laws of physics state that when any object (which has a density greater than air) is propelled upward, it will return to earth because of the forces of gravity act upon it.

Mean Reversion

Too often, homeowners (and developers) make the damaging error of assuming recent price performance will continue into the future without first considering the long-term rates of price appreciation and the potential for mean reversion.

Recalling Finance 101

The laws of finance say that markets that go through periods of rapid price appreciation or depreciation will, in time, revert to a price point that puts them in line with where their long-term average rates of appreciation indicate they should be. This is known as mean reversion.

Natural Process

Prices in the housing market follow this law of mean reversion too - after periods o f r a p i d p r i c e a p p r e c i a t i o n ( o r depreciation), they revert to where their long-term average rates of appreciation indicate they should be.

Home price mean reversion can be rapid or gradual.

Market Forces

Home prices might fall (or rise) quickly to a point that puts them back in line with the long-term average, or they might stay constant until the long-term average catches up with them.

Scarcity of Land Just as important is that the supply of housing is slow to react to increases in demand because it takes a long time to build a house, and in highly developed areas there simply isn't any more land to build on.

So, if there is a sudden or prolonged increase in demand, prices are sure to rise.

Opportunities Abound

Once you've established that an above-average rise in housing prices is primarily driven by an increase in demand, you might ask what the causes of that increase in demand are.

The next slides point to several:

Opportunities

1. An upturn in general economic activity and prosperity that puts more disposable income in consumers' pockets and encourages home ownership.

2. An increase in the population or the demographic segment of the population entering the housing market e.g. OFW Market

The International Monetary Fund foresees 6.6% GDP growth for the Philippines in 2014.

The Philippine economy grew by 7.2% in 2013, after GDP growth of 6.6% in 2012, 3.9% in 2011, and 7.6% in 2010.

According to the International Monetary Fund (IMF), from 2000 to 2009, the economy expanded by an average of 4.4% annually.

Still robust economic growth despite calamities

Opportunities

3. A low general level of interest rates, particularly short-term interest rates, that makes homes more affordable.

4. Innovative mortgage products with low initial monthly payments that make homes more affordable.

9-27

Low interest rates

Opportunities

5. Easy access to credit (a lowering of underwriting standards) that brings more buyers to market.

6. High-yielding structured mortgage bonds, as demanded by investors, that make more mortgage credit available to borrowers.

Opportunities

7. A potential mispricing of risk by mortgage lenders and mortgage bond investors that expands the availability of credit to borrowers.

8. The short-term relationship between a mortgage broker and a borrower under w h i c h b o r r o w e r s a r e s o m e t i m e encouraged to take excessive risks.

Opportunities

9. A lack of financial literacy and excessive risk-taking by mortgage borrowers.

10. Speculative and risky behavior by home buyers and property investors fueled by unrealistic and unsustainable home price appreciation estimates.

9-31

Natural Progression

All of these variables can combine to cause a housing market bubble. They tend to feed off of each other. A detailed discussion of each is out of the scope of this presentation.

We simply point out that in general, like all bubbles, an uptick in activity and prices precedes excessive risk-taking and speculative behavior by all market participants: buyers, borrowers, lenders, builders and investors.

What Causes the Bubble to Burst then?

The bubble bursts when excessive risk-taking becomes pervasive throughout the housing system. This happens while the supply of housing is still increasing. In other words, demand decreases while supply increases, resulting in a fall in prices.

This pervasiveness of risk throughout the system is triggered by losses suffered by homeowners, mortgage lenders, mortgage investors and property investors. Those losses could be triggered by a number of things, including:

9-34

The Fundamental Causes 1. An increase in interest rates that puts homeownership out of reach for some buyers and, in some instances, makes the home a person currently owns unaffordable, leading to default and foreclosure, which eventually adds to supply.

2. A downturn in general economic activity that leads to less disposable income, job loss and/or fewer available jobs, which decreases the demand for housing.

3. Demand is exhausted, bringing supply and demand into equilibrium and slowing the rapid pace of home price appreciation that some homeowners, particularly speculators, count on to make their purchases affordable or profitable.

When rapid price appreciation stagnates, those who count on it to afford their homes long term might lose their homes, bringing more supply to the market.

The bottom line is that when losses mount, credit standards are tightened, easy mortgage borrowing is no longer available, demand decreases, supply increases, speculators leave the market and prices fall.

Current Scenario: Rates are Good…

The BSP kept its policy rates at 3.5% for the overnight borrowing in June 2014, and 5.5% for the overnight lending and repurchase facility (RF).

Most borrowing is short-term. Housing loan rates charged by major commercial banks range from 5.3% to 7.8% for one-year fixed loans, and from 7% to 10% for mortgages with fixed rates for five years.

But we have Real Structural Problems?

Real problems impede the growth of the mortgage market. Few major banks offer housing loans, although loan-to-value ratios of 90% are now being offered, and loan tenors can be as long as 30 years.

Different banks’ loans have strangely similar terms and conditions, and approval of loan applications takes a long time. Land titling and registration problems are prevalent, as are delays in the foreclosure process.

Regulators Must DO more!

Property buyers also face high transaction costs, corruption and red tape, fake land titles and substandard building practices.

Plus, the large informal housing sector and their incentives, make it less attractive for low to middle income families to buy or rent properties.

Ratios look fundamentally sound

Because of these factors, the ratio of housing loans to GDP remains small, at around 2.8% of GDP in 2013. Most houses in the Philippines are sold for cash or pre-sold, with the developers offering financing.

So are we really overbuilding?

There were 57,710 condominium units in Metro Manila in 2013. Colliers anticipates 8,180 new units will come onto the market each year over the next four years.

New builds will push the stock of condominiums in Makati CBD, Rockwell, Fort Bonifacio, Ort igas, and Eastwood up to 90,436 condominium units by 2017.

Vacancy Rate is up…

Will demand be able to keep up?

The condominium vacancy rate in Makati CBD was 10.9% in Q1 2014, up from 9.8% in Q3 2013.

Is Oversupply developing?

But not 3-BR Units…

Arguably however this vacancy rate increase is artificial.

Research Agencies attributes the increase to turnover of new units. Premium three-bedroom units, it says, are still experiencing virtually full occupancy, with only a 4.6% vacancy rate.

“Little Oversupply”?

Others see a small oversupply in the short term. This “little oversupply” of homes involves property projects launched six years ago and now coming online, pulling rental rates temporarily downwards.

Again others see 2014 as the year when supply will peak; however, they see no signs of a property bubble brewing.

Metro Manila’s segmented market makes me awake on some nights If you lower down the income scale there is cause to worry.

There are three identifiable segments in Manila’s housing market:

The high end. This is the segment discussed by my research colleagues. Local high-earners and expatriates occupy this segment.

Is the Mid Market Overheating?

The middle tier. The mid-end condominium sector, with monthly amortization of around PHP 10,500 (US$ 235), presently requiring a dispensable income greater than PHP 34,962 (US$ 783), to obtain a housing loan of PHP 2 million (US$ 44,801). This segment has been targeted by many developers, and is attractive to overseas foreign workers (OFWs).

The low end. This is where the mass of the population live.

Oversupply in some Areas?

The middle tier to my mind is over-supplied. Many of these lower middle-class condominium developments will become ghost condos similar to my experience in Vietnam in 08 and China in 2013.

Let’s do the Math

According to HLURB, 452,198 condominium units were built in Metro Manila from January 2001 to March 2014.

Will we see Ghost Projects soon?

There are around 807,496 families or 27.5% of the NCR population who have a disposable income greater than PHP 34,962 (US$ 783), which is the required monthly income to be able to afford the monthly amortization of PHP 10,500 (US$ 235).

Not Really

So for all these newly-built condominiums to be occupied by those who could afford to rent or buy, 56% of locals who have the financial capacity to occupy them would need to do so

i.e., 56% of the 807,496 families with the financial capacity to do so, should purchase or rent a unit, for the available supply of condominium units to be taken up.

World Bank Estimates 10% End-users

These are problematic numbers given that many of these families already have houses in the first place. The World Bank assumes only 10% of these capable end-users as prospective end-users, indicating a gross oversupply.

But we will expect a Mismatch soon In terms of affordability, property developers are building more mid-end condominium units than locally-based Filipinos can afford to occupy.

Many of the buyers are OFWs, causing a mismatch between demand and supply.

Another Setback

The inflow of new OFW money has slowed, since the global financial crisis.

Average annual growth of remittances was only 6.9% from 2009 to 2013, compared to 16.8% annually from 2004 to 2009.

Why a slowdown on Remittances?

The World Bank believes the slowdown in remittances is due to: Stricter Implementation of the migrant

workers’ bill of rights; Political uncertainties in host countries; and The slowdown in the advanced economies.

Real Estate Bubble Index

9-59

Rule of Thumb

“Theory asserts that house prices, rents, and incomes should move in tandem over the long run. If house prices and rents get way out of line, people would switch between buying and renting, eventually bringing the two in alignment.

IMF economist Min Zhu published an article called “Era of Benign Neglect of House Price Booms is Over,”

Rule of Thumb

Similarly, in the long run, the price of houses cannot stray too far from people’s ability to afford them––that is, from their income. The ratios of house prices to rents and incomes are thus often used as an initial check on whether house prices are out of line with economic fundamentals.”

IMF economist Min Zhu published an article called “Era of Benign Neglect of House Price Booms is Over,”

Not An Option right?

Regulators can work to make sure that credit isn’t too widely available and lending standards are tightened, but sometimes the logic of a bubble can overcome even these measures.

The only reliable way to eliminate a bubble is to let it burst, which could lead to terrible consequences for the country’s economies in question.

Chris Mathews: Where Will the Next Real Estate Burst Happen? 9-62

Another Perspective: The Un-Real Estate

But what if real estate isn’t overvalued? What if there is something happening in the economy that’s causing real estate to become more valuable?

Another Perspective: The Un-Real Estate

As developed economies become less reliant on agriculture and manufacturing, and more reliant on creative industries that thrive on close collaboration for a generation of valuable ideas, land is becoming once again very important.

We can see this happening in Manila where rents are skyrocketing along with salaries. In an environment where the most productive workers are seeing rapidly rising property values, it makes sense that people would want to buy a home rather than rent. After all, what force is going to stop this trend in rising prices?

Irrational Exuberance is GREED!

With this explanation, you have reason to believe that the recent run up in real estate prices in developed countries has both a rational component (the evolution of the economy is making location more important) and an irrational component (people think that nothing will stop this trend).

Our Industry is Unpredictable

It’s difficult to say which force could be a bigger factor pushing real estate prices higher, but it’s important to realize that just because prices have always behaved a certain way in the past doesn’t mean it will continue that way in the future.

9-67

How do we manage Bubbles when they do pop…

9-68

The NEED to develop a REAL Real Estate Price Index

9-69 Monthly Price Index of Real Estate Sales, on a Month-to-Month Basis

Real Estate Input and Output: Compliance!

Site selection Guidelines

Risk Mgt Industry & Company Benchmark

Financial Benchmark

Quality Site Section

Best in class process

Optimized Portfolio

Maximize Shareholder Value

5 year Plan

Existing Locations

Competitive Market Data

Company Strategy and Data

Performance Repeating Tools

Demographic Data

Other Tools and Data Process

Control

Output

Enabler

Input

Legend

Urgent

Done

To Ensure Growth for stakeholders

Relentless BRANDING initiatives. Pursue JV opportunities Pocket developments Sustain branding Initiatives Leverage your brand in growth Cities Land banking in next wave cities Mixed use initiatives Recurring Income Stream Aggressive 360 Degree Digital Selling Campaign Best in Breed in After Sales and Excellent Property

Management

A Reminder to Stakeholders

In other words, perhaps what we think is a bubble is really just the real estate market telling us that policy makers like HUDCC and proactive private housing organizations like CREBA need to do more to allow more housing supply in a sector that needs it most…

Shift to a Sector that Matters Most

Providing Affordable and Quality Homes Plan and develop housing towns that provide Filipinos with quality homes and living environments.

9-75

Final Message…

“Success is the temporary

Suspension of Failure”

9-76