Embed Size (px)

Citation preview

1© 2011 The MathWorks, Inc.

Enhancing your Risk Modeling

Architecture

Steve Wilcockson

Industry Marketing – Financial Services

2

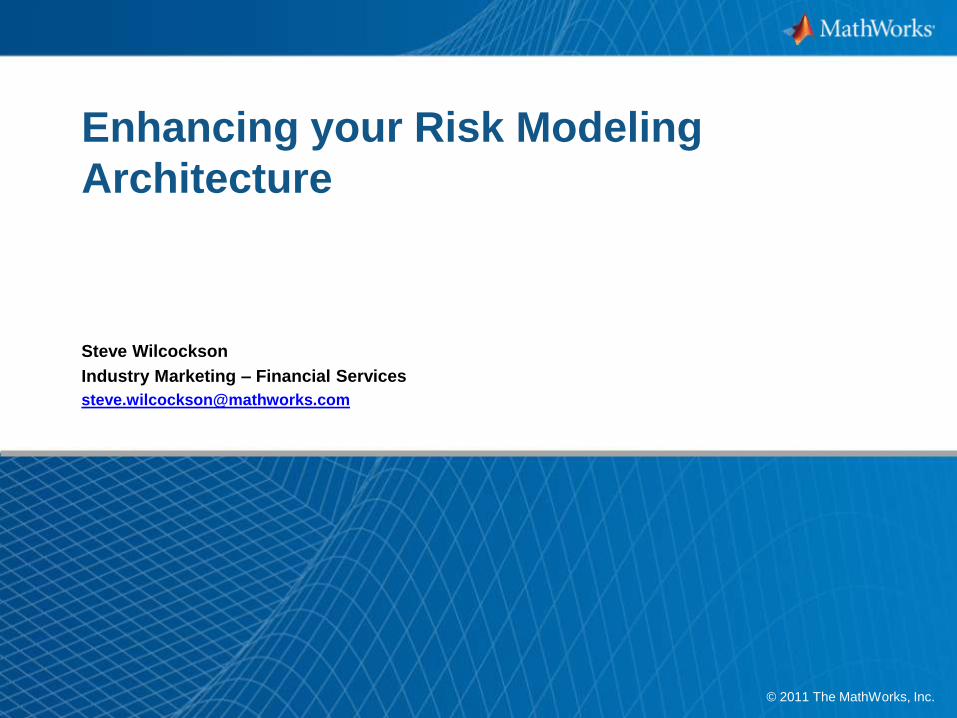

Investment Banks21%

Hedge Funds17%

Investment Managers

14%

Retail/Private Banks11%

Central Banks10%

Other9%

Other Government Regulators

6%

Insurance6%

Ratings Agencies3%

Reinsurance3%

MATLAB Use in Financial Services(2010 Customer Breakdown 2300 Companies)

•Risk

•Pricing & Valuation

•Trading

•Insurance &

Actuarial Science

•Investment

Management

•Economics &

Econometrics

•Energy

3

Agenda

Introduction

– MATLAB in the Financial Services Industry

– Computational Finance within MathWorks

Risk Modelling with MATLAB

– Examples

Portfolio Optimization & Risk Analysis

Cash flow Balancing & Scenario Analysis

RiskViewer:- Building a Risk Application

How Risk Departments across the world use MATLAB

Using MATLAB in ―Production‖ Trading (also insurance, index calculation)

Counterparty & Default Risk

4

The challenges facing you today

Analysis is growing

– More data

– Larger models

Markets are changing

– Shifting behavior

– Rapid evolution

Need for transparency is increasing

– More collaboration

– Extra oversight

5

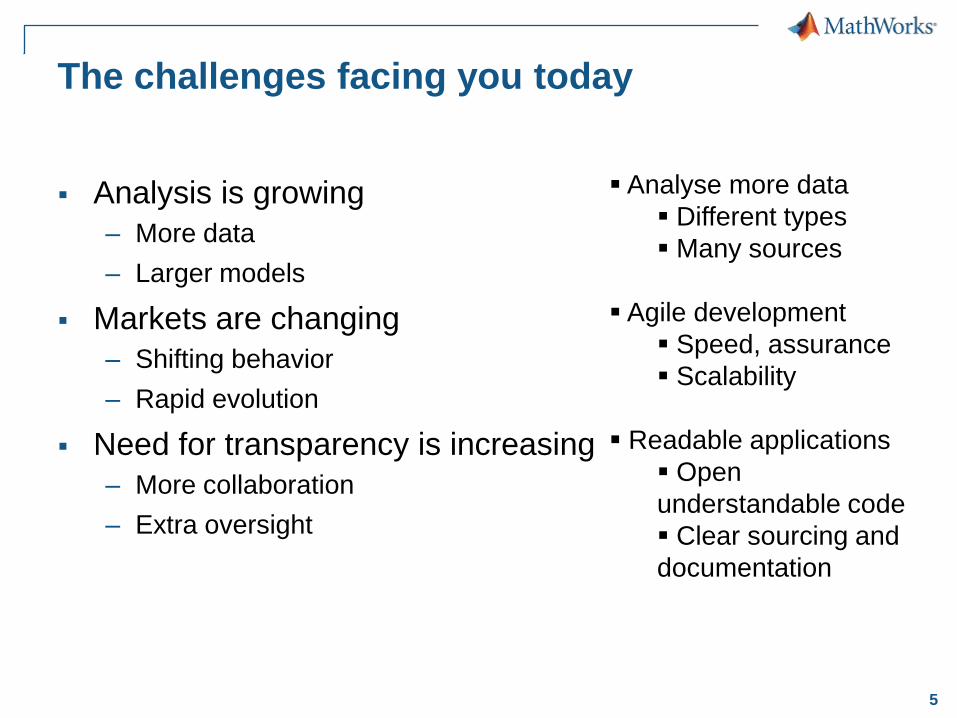

The challenges facing you today

Analysis is growing

– More data

– Larger models

Markets are changing

– Shifting behavior

– Rapid evolution

Need for transparency is increasing

– More collaboration

– Extra oversight

Analyse more data

Different types

Many sources

Agile development

Speed, assurance

Scalability

Readable applications

Open

understandable code

Clear sourcing and

documentation

6

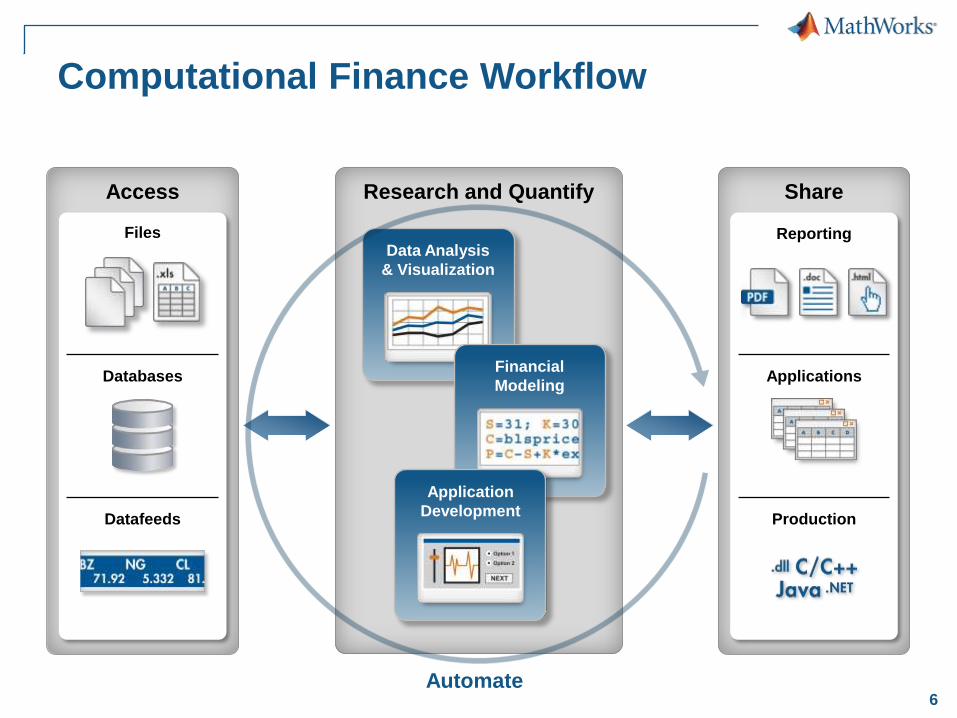

Computational Finance Workflow

Research and Quantify

Data Analysis

& Visualization

Financial

Modeling

Application

Development

Reporting

Applications

Production

Share

Automate

Files

Databases

Datafeeds

Access

7

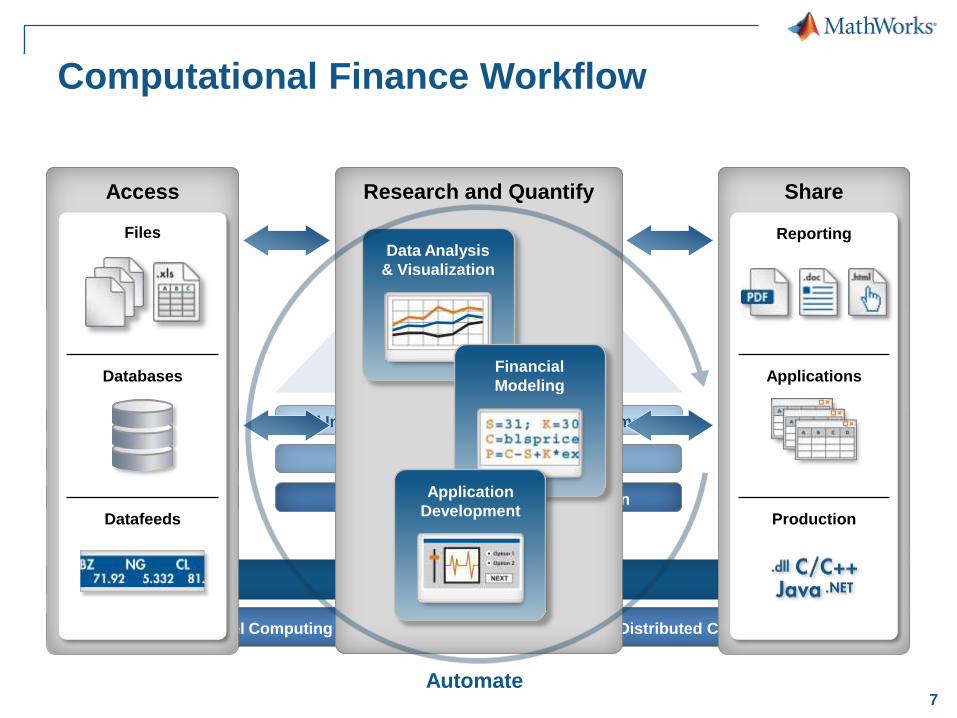

Computational Finance Workflow

Financial

Statistics Optimization

Fixed Income Financial Derivatives Econometrics

MATLAB

Parallel Computing MATLAB Distributed Computing Server

Files

Databases

Datafeeds

Access

Reporting

Applications

Production

Share

Data Analysis and Visualization

Financial Modeling

Application Development

Research and Quantify

Datafeed

Database

Spreadsheet Link EX

Builder NE

Builder EX

Builder JA

MATLAB Compiler

Rep

ort G

en

era

tor

Research and Quantify

Data Analysis

& Visualization

Financial

Modeling

Application

Development

Reporting

Applications

Production

Share

Automate

Files

Databases

Datafeeds

Access

8

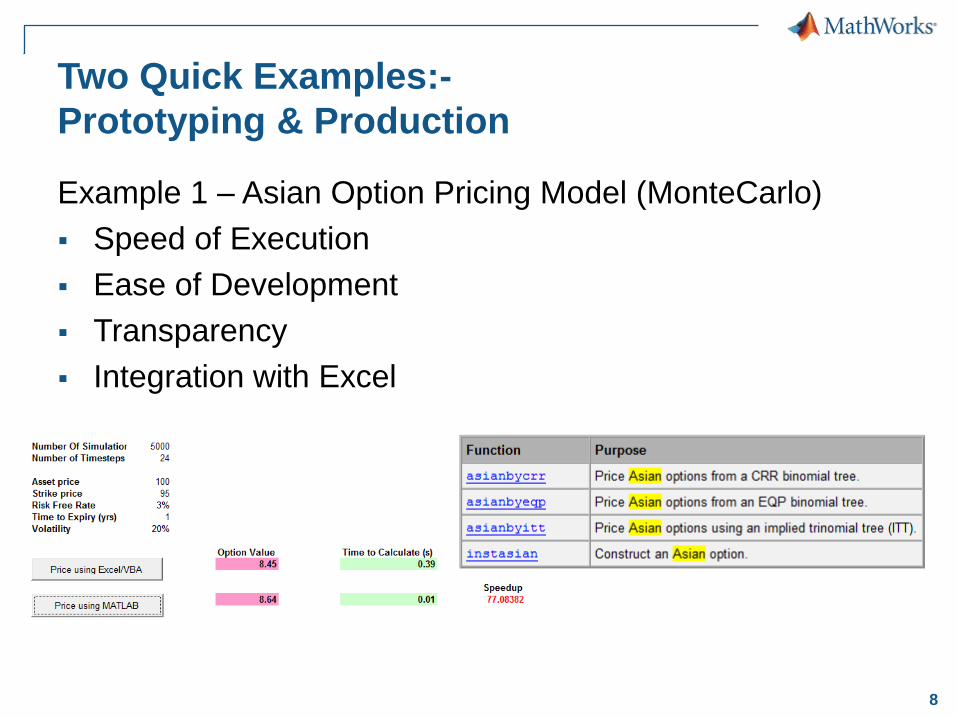

Two Quick Examples:-

Prototyping & Production

Example 1 – Asian Option Pricing Model (MonteCarlo)

Speed of Execution

Ease of Development

Transparency

Integration with Excel

9

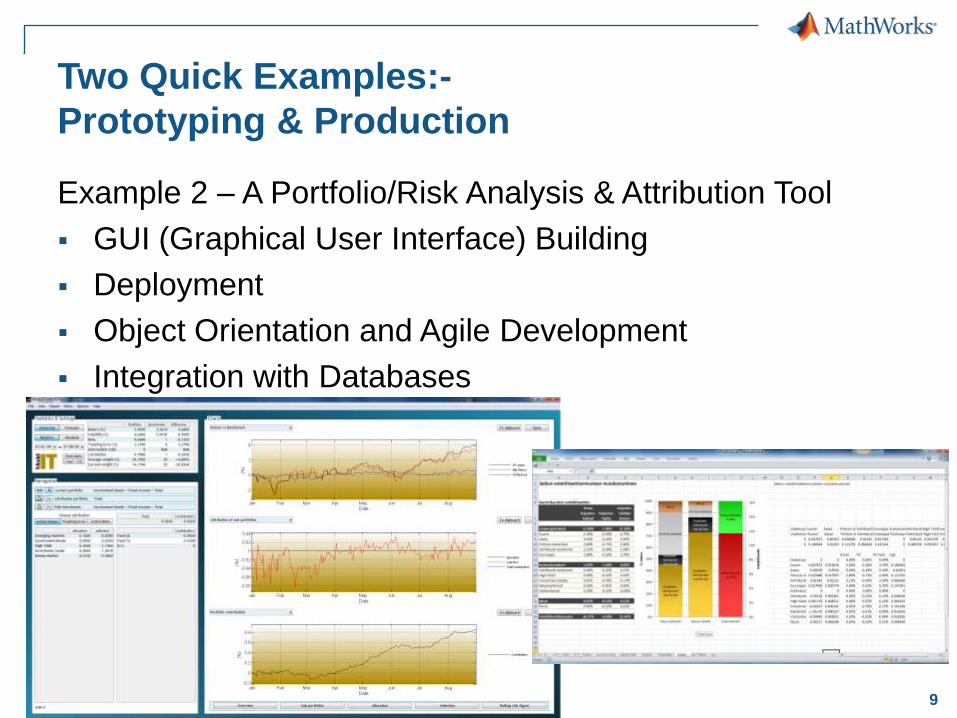

Two Quick Examples:-

Prototyping & Production

Example 2 – A Portfolio/Risk Analysis & Attribution Tool

GUI (Graphical User Interface) Building

Deployment

Object Orientation and Agile Development

Integration with Databases

10

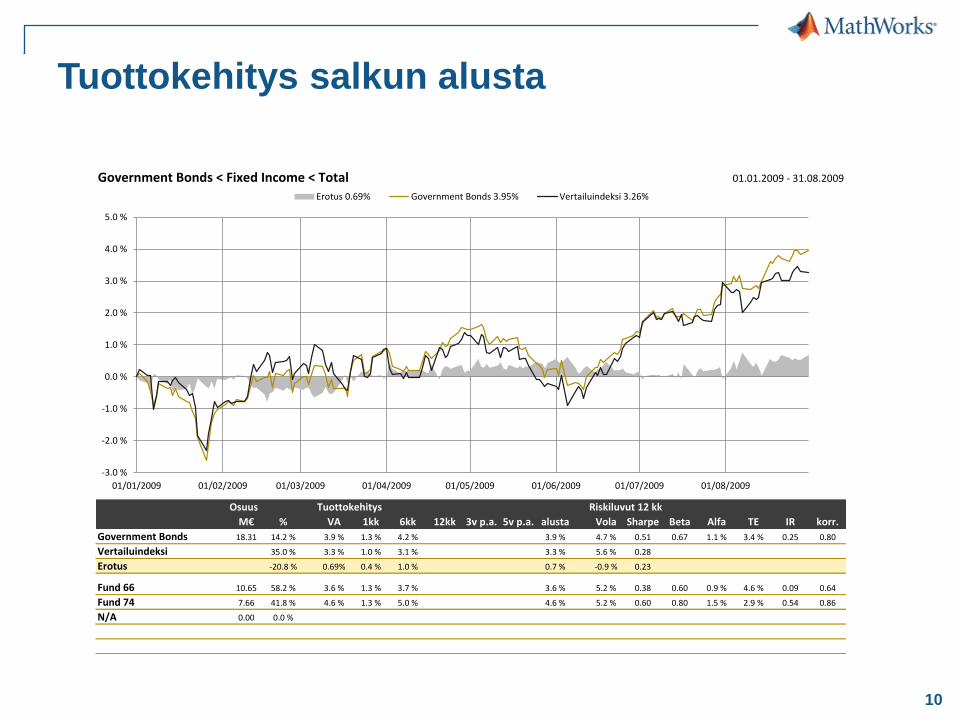

Tuottokehitys salkun alusta

Government Bonds < Fixed Income < Total 01.01.2009 - 31.08.2009

Osuus Tuottokehitys Riskiluvut 12 kk

M€ % VA 1kk 6kk 12kk 3v p.a. 5v p.a. alusta Vola Sharpe Beta Alfa TE IR korr.

Government Bonds 18.31 14.2 % 3.9 % 1.3 % 4.2 % 3.9 % 4.7 % 0.51 0.67 1.1 % 3.4 % 0.25 0.80

Vertailuindeksi 35.0 % 3.3 % 1.0 % 3.1 % 3.3 % 5.6 % 0.28

Erotus -20.8 % 0.69% 0.4 % 1.0 % 0.7 % -0.9 % 0.23

Fund 66 10.65 58.2 % 3.6 % 1.3 % 3.7 % 3.6 % 5.2 % 0.38 0.60 0.9 % 4.6 % 0.09 0.64

Fund 74 7.66 41.8 % 4.6 % 1.3 % 5.0 % 4.6 % 5.2 % 0.60 0.80 1.5 % 2.9 % 0.54 0.86

N/A 0.00 0.0 %

-3.0 %

-2.0 %

-1.0 %

0.0 %

1.0 %

2.0 %

3.0 %

4.0 %

5.0 %

01/01/2009 01/02/2009 01/03/2009 01/04/2009 01/05/2009 01/06/2009 01/07/2009 01/08/2009

Erotus 0.69% Government Bonds 3.95% Vertailuindeksi 3.26%

11

Agenda

Introduction

– MATLAB in the Financial Services Industry

– Computational Finance within MathWorks

Risk Modelling with MATLAB

– Examples

Portfolio Optimization & Risk Analysis

Cash Flow Balancing & Scenario Analysis

RiskViewer:- Building a Risk Application

How Risk Departments across the world use MATLAB

Using MATLAB in ―Production‖ Trading (also insurance, index calculation)

Counterparty & Default Risk

12

13

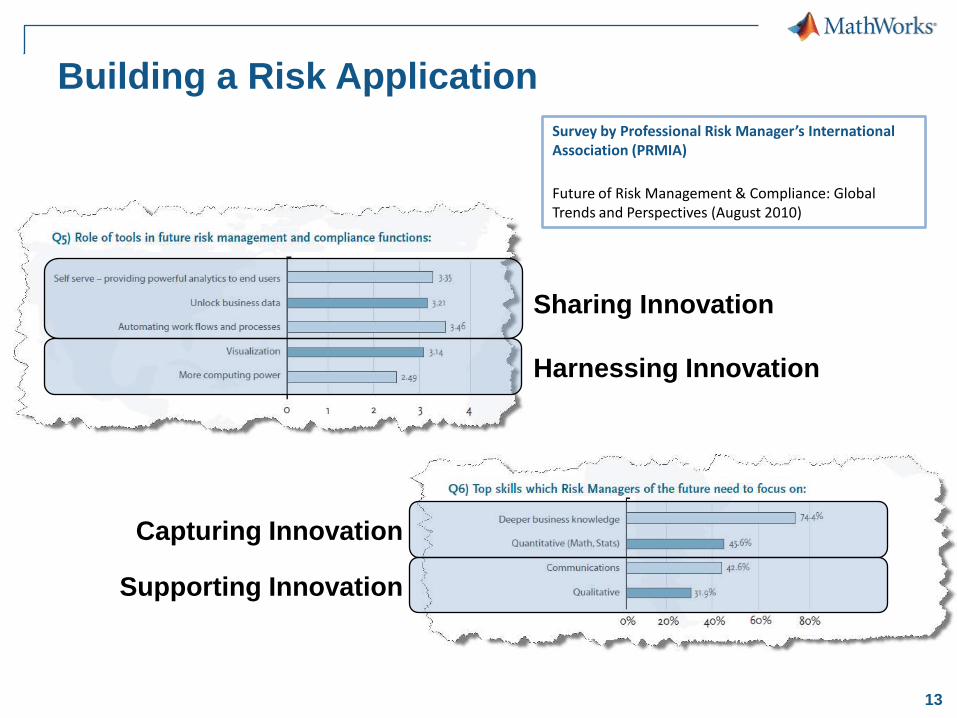

Sharing Innovation

Harnessing Innovation

Capturing Innovation

Supporting Innovation

Survey by Professional Risk Manager’s International Association (PRMIA)

Future of Risk Management & Compliance: Global Trends and Perspectives (August 2010)

Building a Risk Application

14

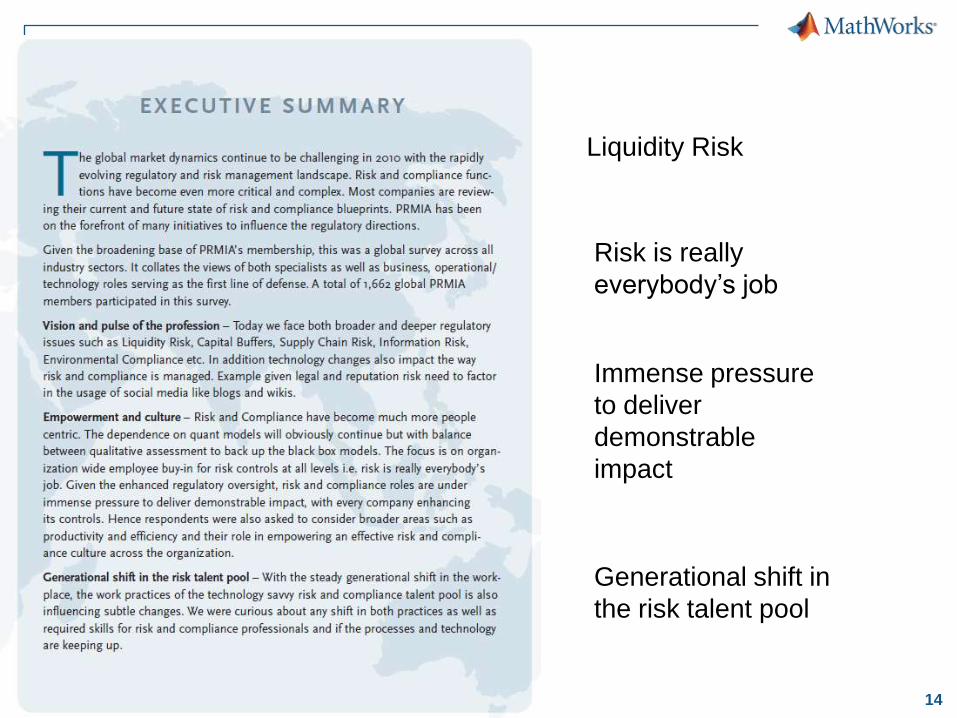

Liquidity Risk

Risk is really

everybody’s job

Immense pressure

to deliver

demonstrable

impact

Generational shift in

the risk talent pool

15

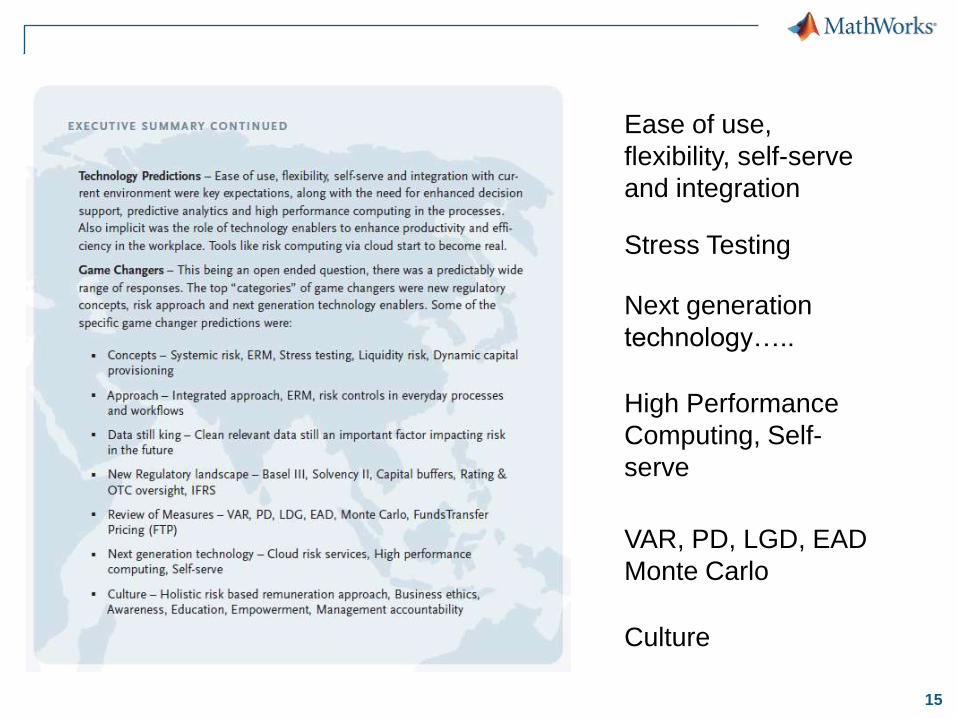

Ease of use,

flexibility, self-serve

and integration

Next generation

technology…..

VAR, PD, LGD, EAD

Monte Carlo

Culture

High Performance

Computing, Self-

serve

Stress Testing

16

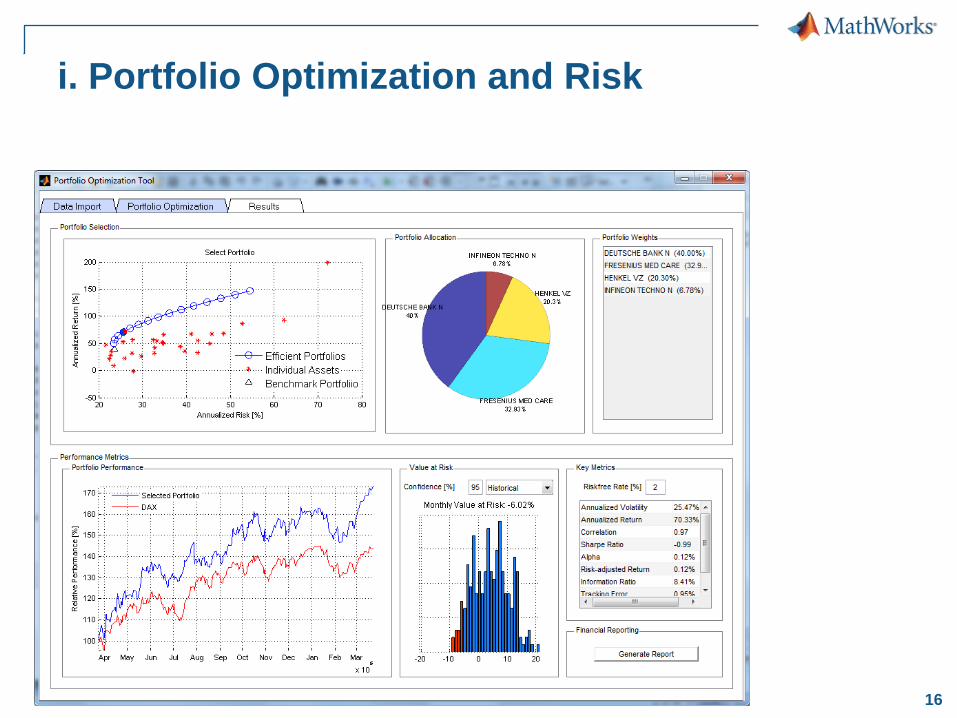

i. Portfolio Optimization and Risk

17

18

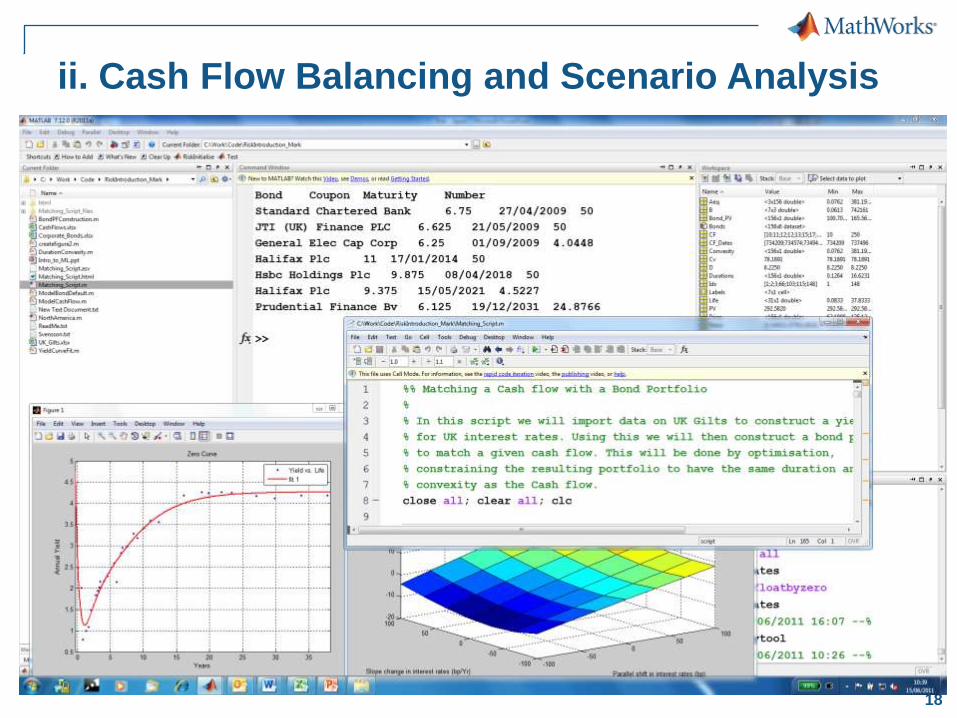

ii. Cash Flow Balancing and Scenario Analysis

19

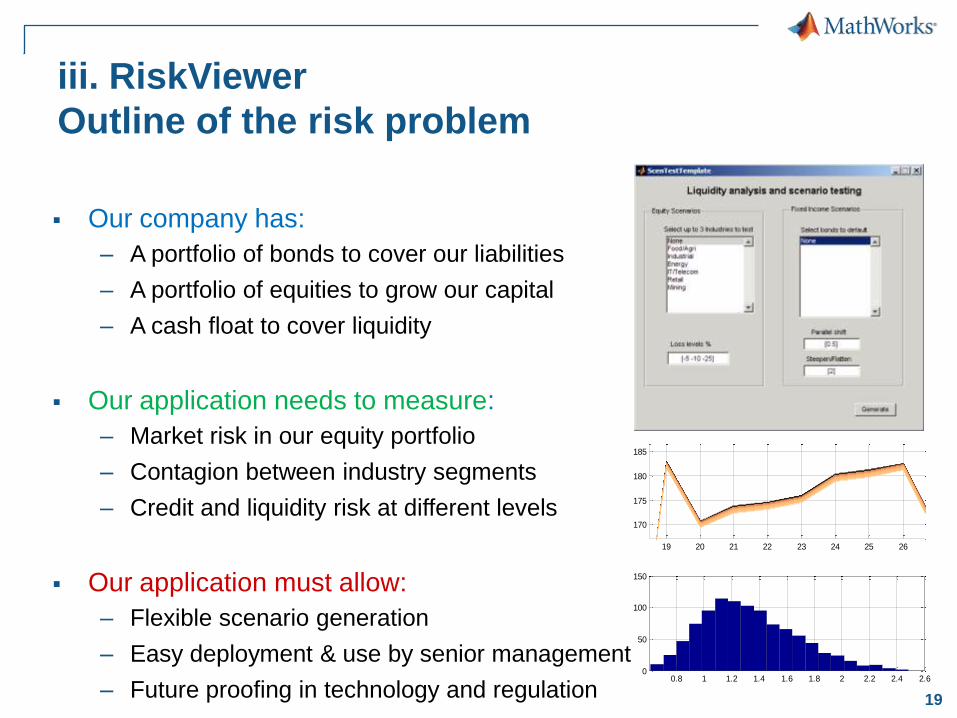

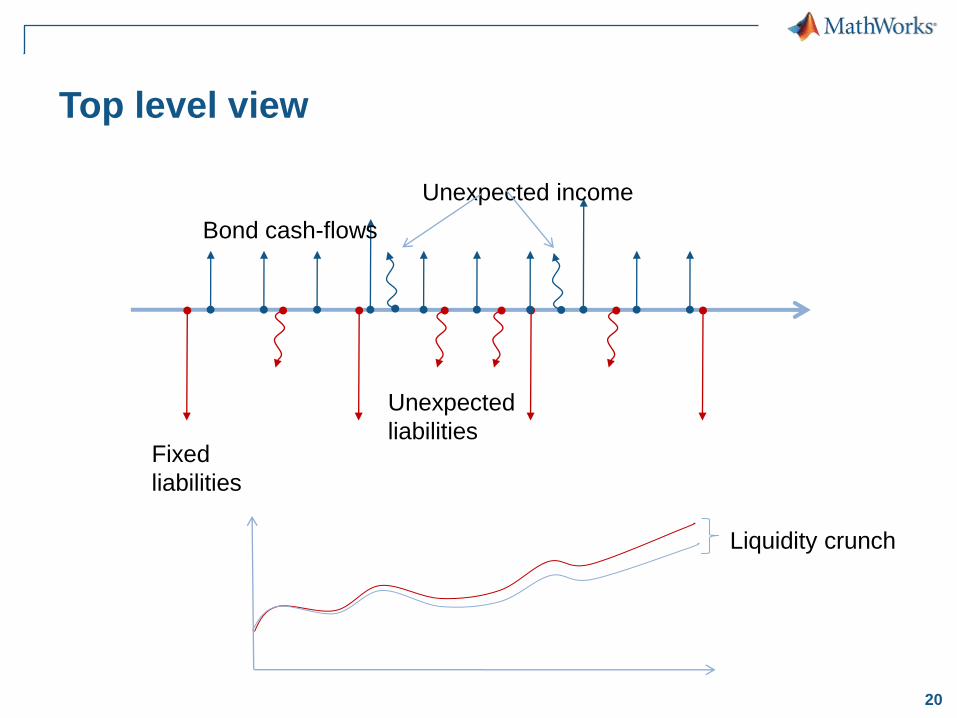

iii. RiskViewer

Outline of the risk problem

Our company has:

– A portfolio of bonds to cover our liabilities

– A portfolio of equities to grow our capital

– A cash float to cover liquidity

Our application needs to measure:

– Market risk in our equity portfolio

– Contagion between industry segments

– Credit and liquidity risk at different levels

Our application must allow:

– Flexible scenario generation

– Easy deployment & use by senior management

– Future proofing in technology and regulation

19 20 21 22 23 24 25 26

170

175

180

185

0.8 1 1.2 1.4 1.6 1.8 2 2.2 2.4 2.60

50

100

150

20

Top level view

Bond cash-flows

Fixed

liabilities

Unexpected

liabilities

Unexpected income

Liquidity crunch

21

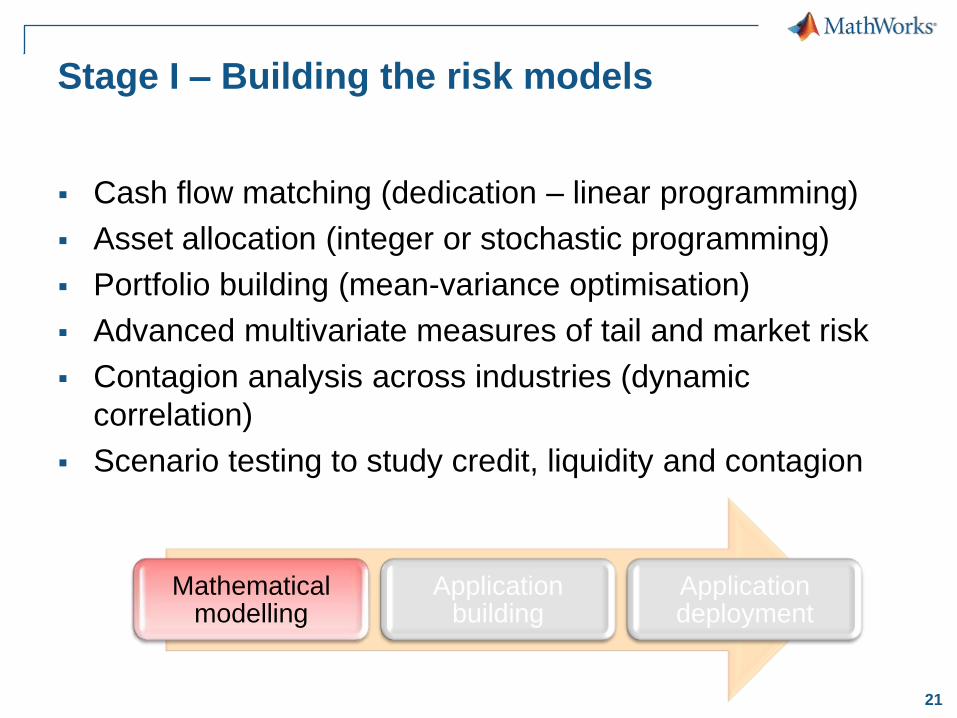

Stage I – Building the risk models

Cash flow matching (dedication – linear programming)

Asset allocation (integer or stochastic programming)

Portfolio building (mean-variance optimisation)

Advanced multivariate measures of tail and market risk

Contagion analysis across industries (dynamic

correlation)

Scenario testing to study credit, liquidity and contagion

Mathematical modelling

Application building

Application deployment

22

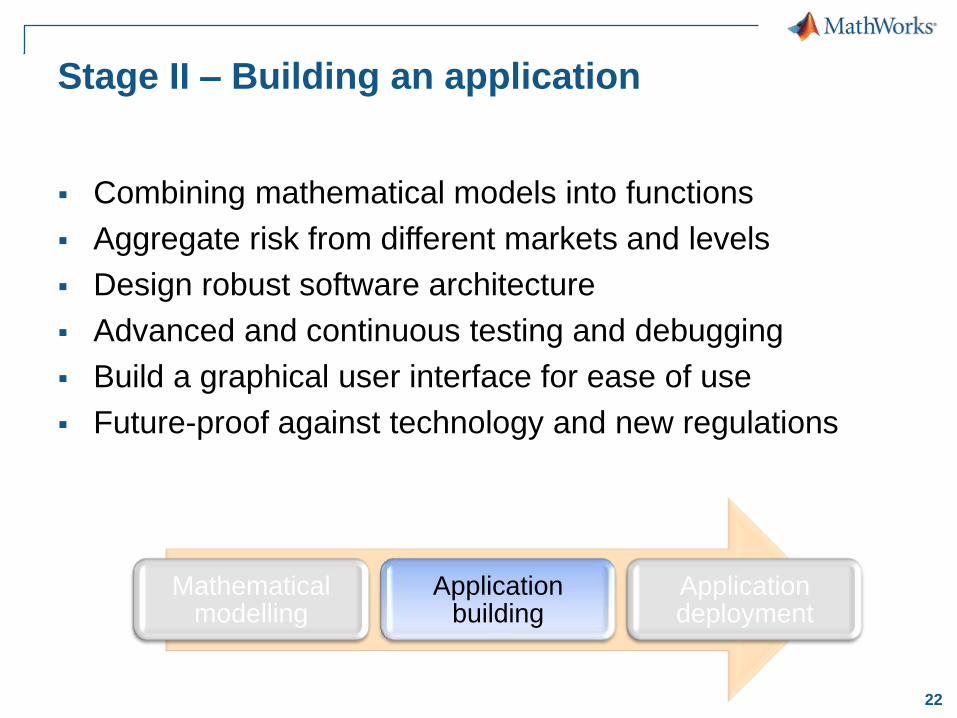

Stage II – Building an application

Combining mathematical models into functions

Aggregate risk from different markets and levels

Design robust software architecture

Advanced and continuous testing and debugging

Build a graphical user interface for ease of use

Future-proof against technology and new regulations

Mathematical modelling

Application building

Application deployment

23

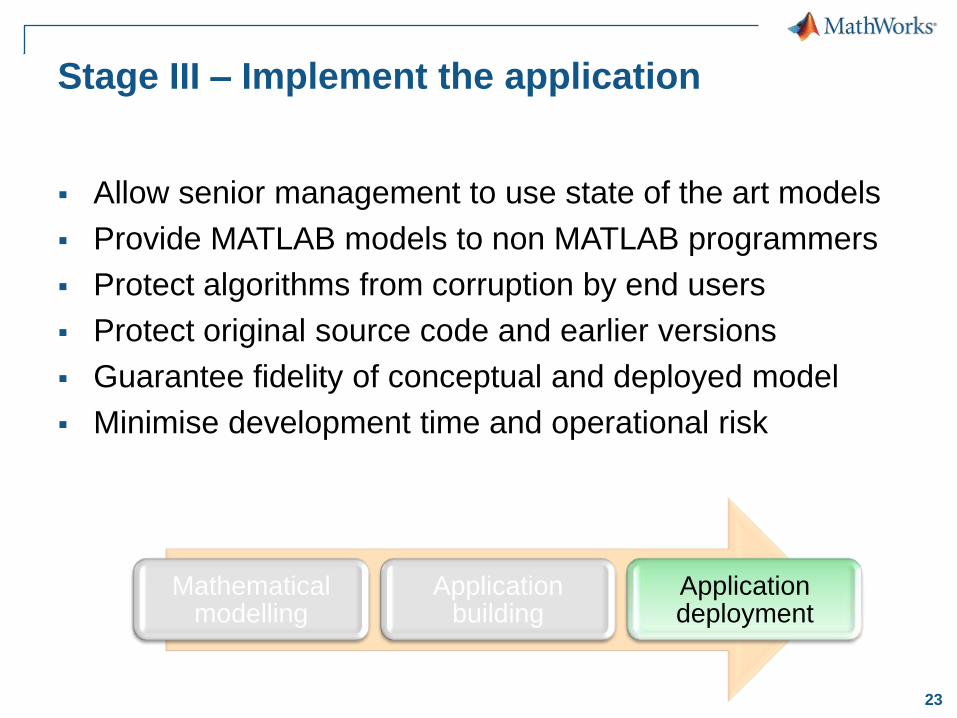

Stage III – Implement the application

Allow senior management to use state of the art models

Provide MATLAB models to non MATLAB programmers

Protect algorithms from corruption by end users

Protect original source code and earlier versions

Guarantee fidelity of conceptual and deployed model

Minimise development time and operational risk

Mathematical modelling

Application building

Application deployment

24

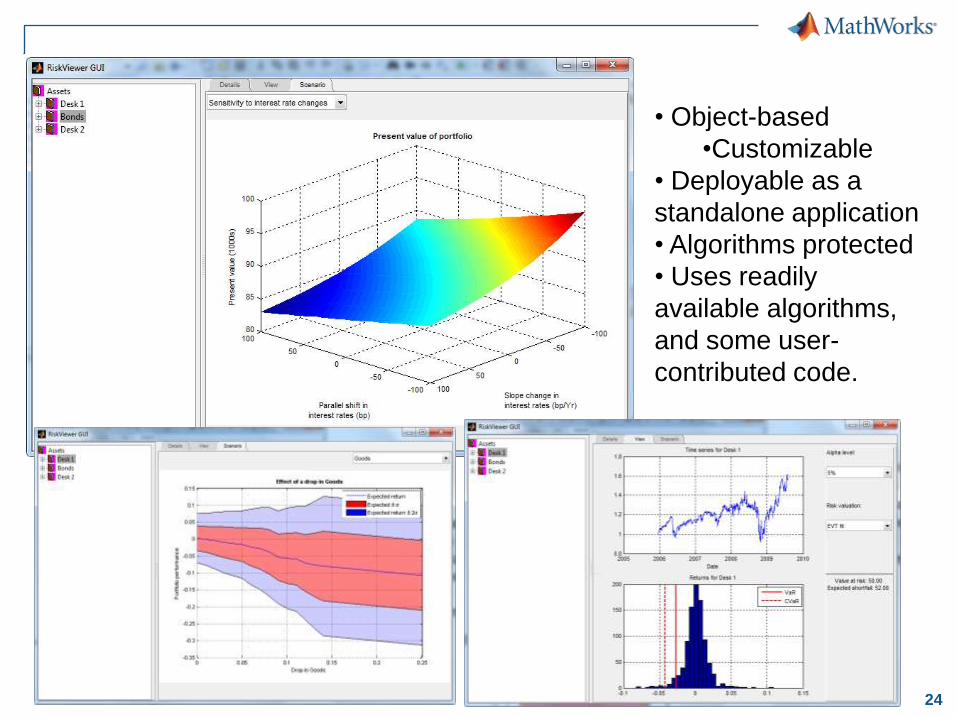

• Object-based

•Customizable

• Deployable as a

standalone application

• Algorithms protected

• Uses readily

available algorithms,

and some user-

contributed code.

25

Agenda

Introduction

– MATLAB in the Financial Services Industry

– Computational Finance within MathWorks

Risk Modelling with MATLAB

– Examples

Portfolio Optimization & Risk Analysis

Cash flow Balancing & Scenario Analysis

RiskViewer:- Building a Risk Application

How Risk Departments across the world use MATLAB

Using MATLAB in ―Production‖ Trading (also insurance, index calculation)

Counterparty & Default Risk

26

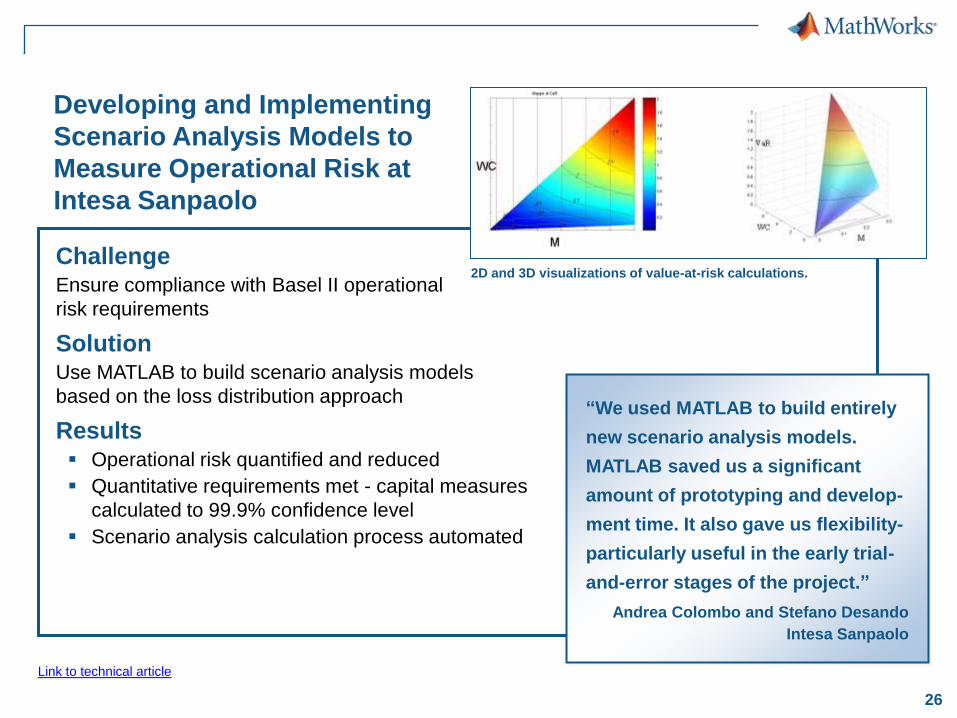

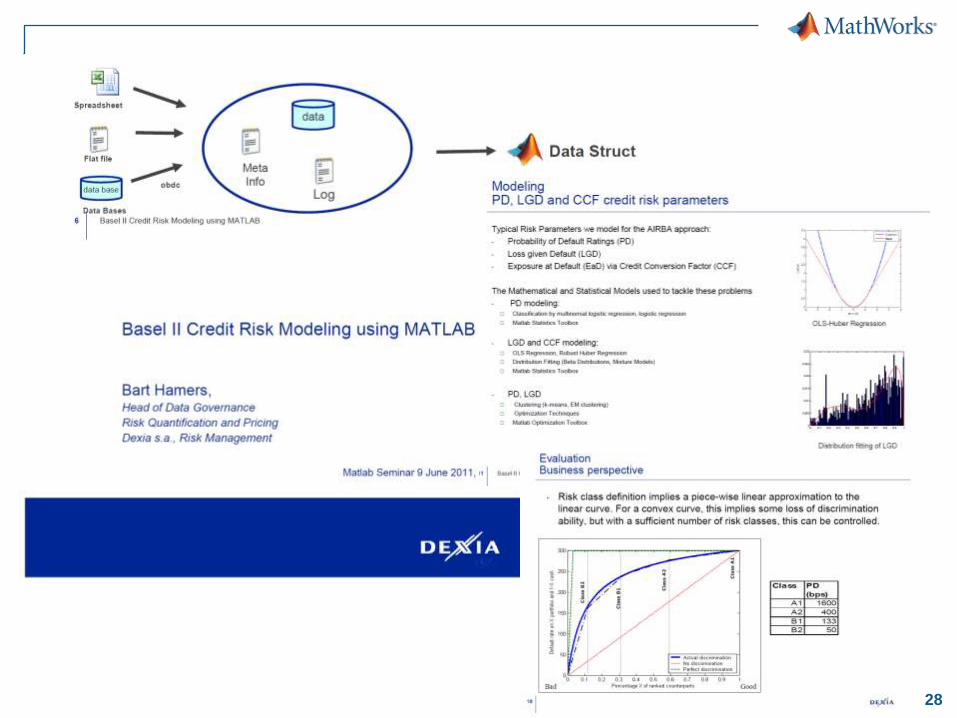

Developing and Implementing

Scenario Analysis Models to

Measure Operational Risk at

Intesa Sanpaolo

ChallengeEnsure compliance with Basel II operational

risk requirements

SolutionUse MATLAB to build scenario analysis models

based on the loss distribution approach

Results Operational risk quantified and reduced

Quantitative requirements met - capital measures

calculated to 99.9% confidence level

Scenario analysis calculation process automated

“We used MATLAB to build entirely

new scenario analysis models.

MATLAB saved us a significant

amount of prototyping and develop-

ment time. It also gave us flexibility-

particularly useful in the early trial-

and-error stages of the project.”

Andrea Colombo and Stefano Desando

Intesa Sanpaolo

Link to technical article

2D and 3D visualizations of value-at-risk calculations.

27

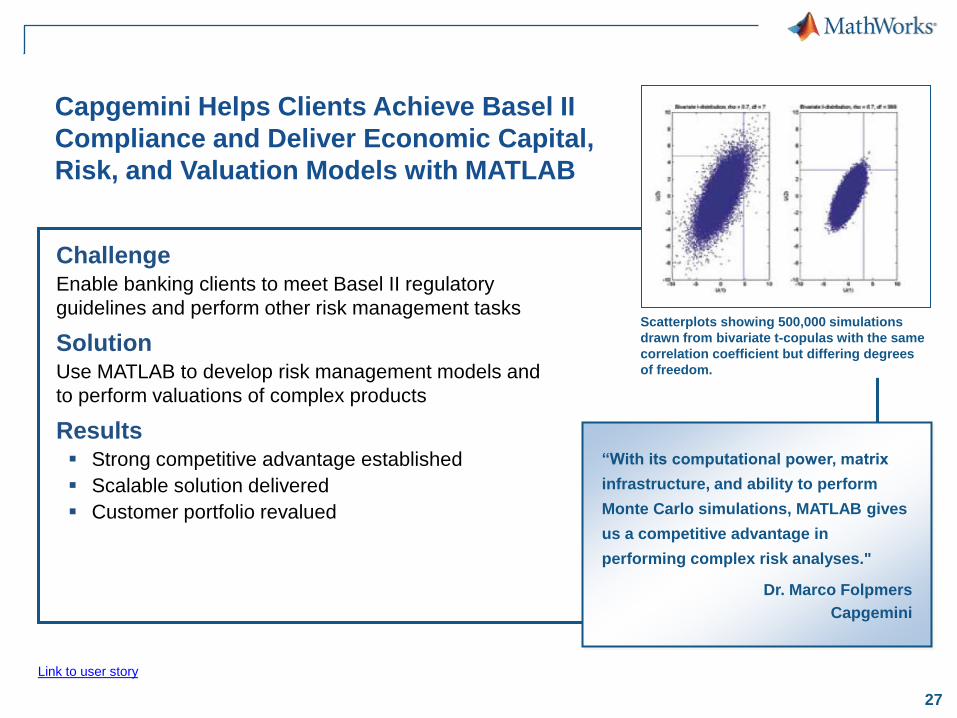

Capgemini Helps Clients Achieve Basel II

Compliance and Deliver Economic Capital,

Risk, and Valuation Models with MATLAB

ChallengeEnable banking clients to meet Basel II regulatory

guidelines and perform other risk management tasks

SolutionUse MATLAB to develop risk management models and

to perform valuations of complex products

Results Strong competitive advantage established

Scalable solution delivered

Customer portfolio revalued

“With its computational power, matrix

infrastructure, and ability to perform

Monte Carlo simulations, MATLAB gives

us a competitive advantage in

performing complex risk analyses."

Dr. Marco Folpmers

Capgemini

Link to user story

Scatterplots showing 500,000 simulations

drawn from bivariate t-copulas with the same

correlation coefficient but differing degrees

of freedom.

28

29

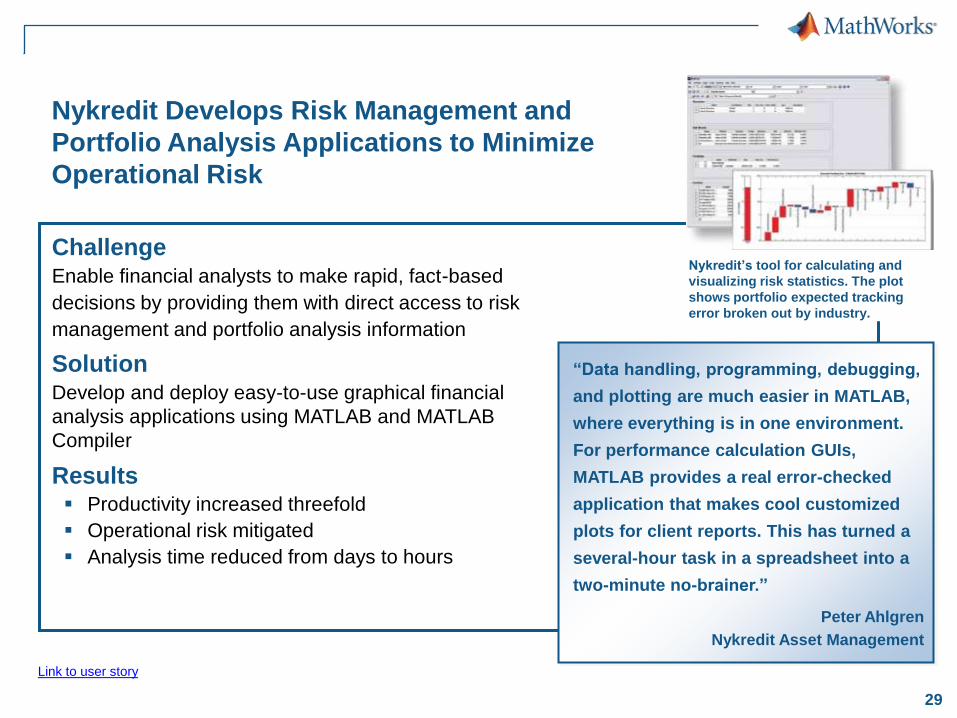

Nykredit Develops Risk Management and

Portfolio Analysis Applications to Minimize

Operational Risk

ChallengeEnable financial analysts to make rapid, fact-based

decisions by providing them with direct access to risk

management and portfolio analysis information

SolutionDevelop and deploy easy-to-use graphical financial

analysis applications using MATLAB and MATLAB

Compiler

Results Productivity increased threefold

Operational risk mitigated

Analysis time reduced from days to hours

Link to user story

Nykredit’s tool for calculating and

visualizing risk statistics. The plot

shows portfolio expected tracking

error broken out by industry.

“Data handling, programming, debugging,

and plotting are much easier in MATLAB,

where everything is in one environment.

For performance calculation GUIs,

MATLAB provides a real error-checked

application that makes cool customized

plots for client reports. This has turned a

several-hour task in a spreadsheet into a

two-minute no-brainer.”

Peter Ahlgren

Nykredit Asset Management

30

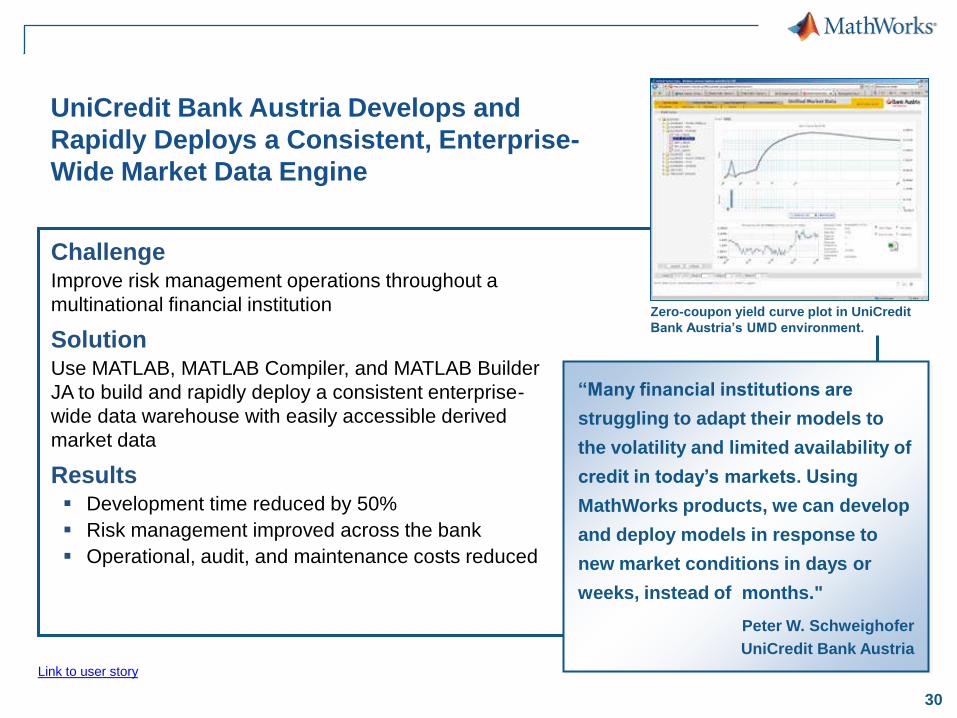

UniCredit Bank Austria Develops and

Rapidly Deploys a Consistent, Enterprise-

Wide Market Data Engine

ChallengeImprove risk management operations throughout a

multinational financial institution

SolutionUse MATLAB, MATLAB Compiler, and MATLAB Builder

JA to build and rapidly deploy a consistent enterprise-

wide data warehouse with easily accessible derived

market data

Results Development time reduced by 50%

Risk management improved across the bank

Operational, audit, and maintenance costs reduced

“Many financial institutions are

struggling to adapt their models to

the volatility and limited availability of

credit in today’s markets. Using

MathWorks products, we can develop

and deploy models in response to

new market conditions in days or

weeks, instead of months."

Peter W. Schweighofer

UniCredit Bank Austria

Link to user story

Zero-coupon yield curve plot in UniCredit

Bank Austria’s UMD environment.

31

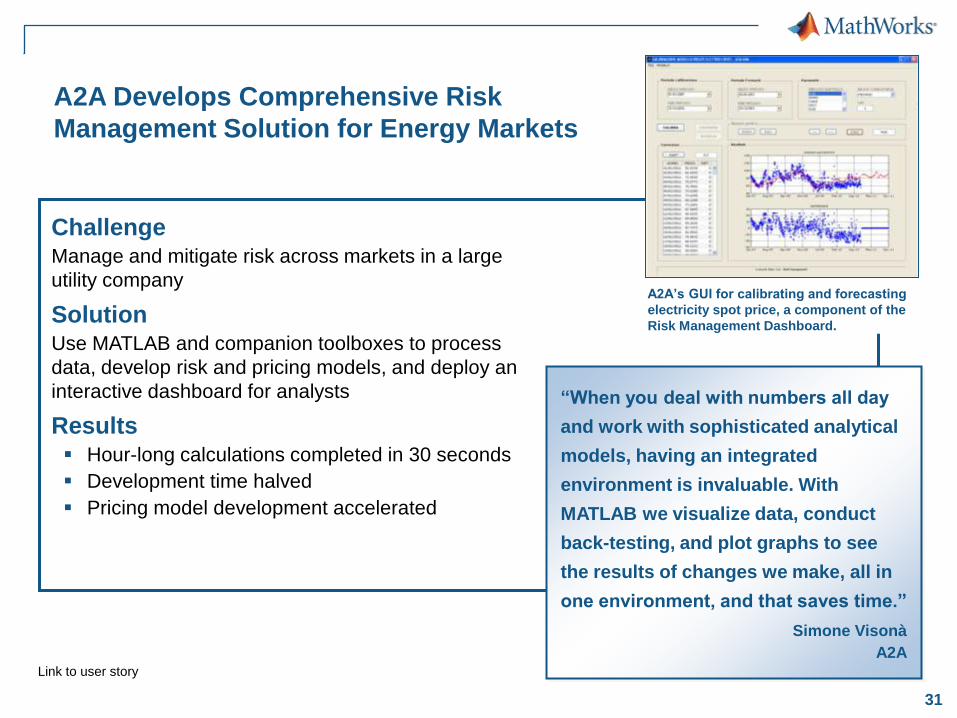

A2A Develops Comprehensive Risk

Management Solution for Energy Markets

ChallengeManage and mitigate risk across markets in a large

utility company

SolutionUse MATLAB and companion toolboxes to process

data, develop risk and pricing models, and deploy an

interactive dashboard for analysts

Results Hour-long calculations completed in 30 seconds

Development time halved

Pricing model development accelerated

“When you deal with numbers all day

and work with sophisticated analytical

models, having an integrated

environment is invaluable. With

MATLAB we visualize data, conduct

back-testing, and plot graphs to see

the results of changes we make, all in

one environment, and that saves time.”

Simone Visonà

A2ALink to user story

A2A’s GUI for calibrating and forecasting

electricity spot price, a component of the

Risk Management Dashboard.

32

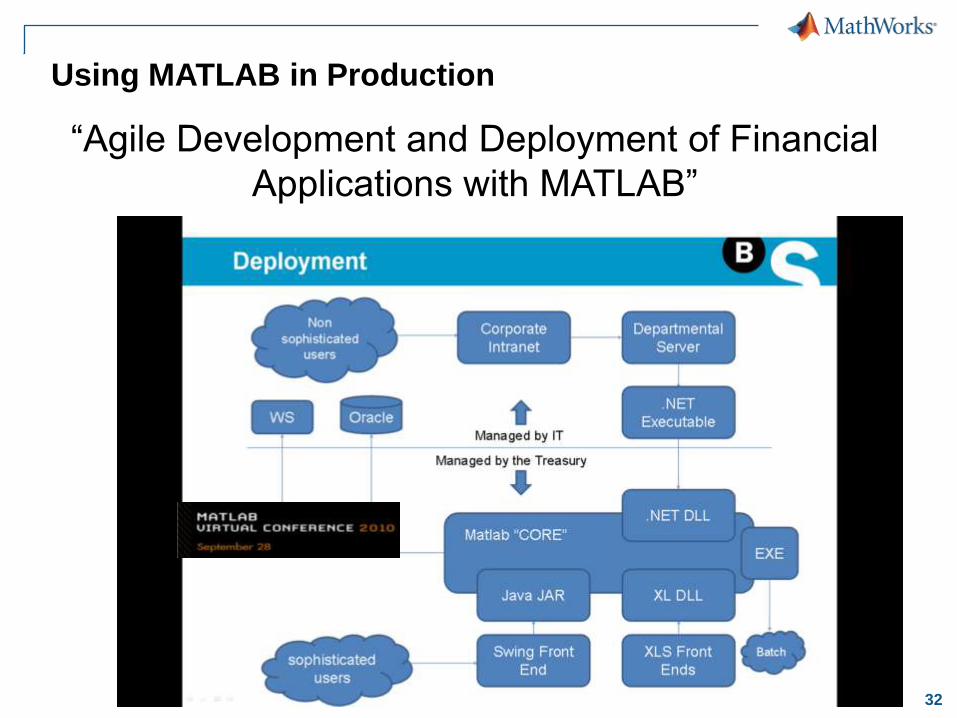

Using MATLAB in Production

―Agile Development and Deployment of Financial

Applications with MATLAB‖

33

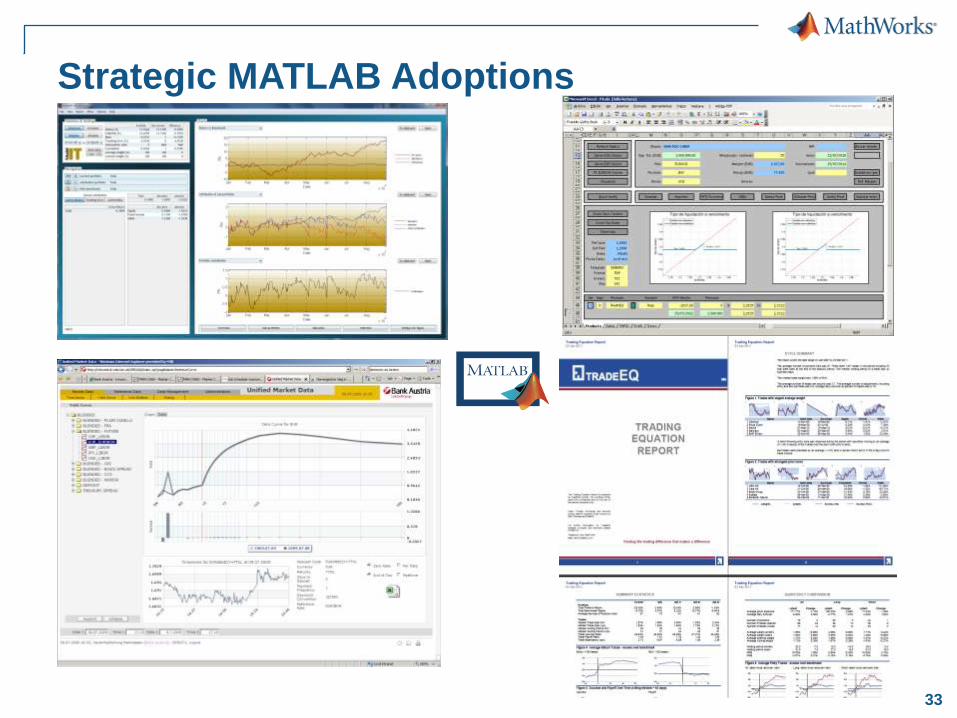

Strategic MATLAB Adoptions

34

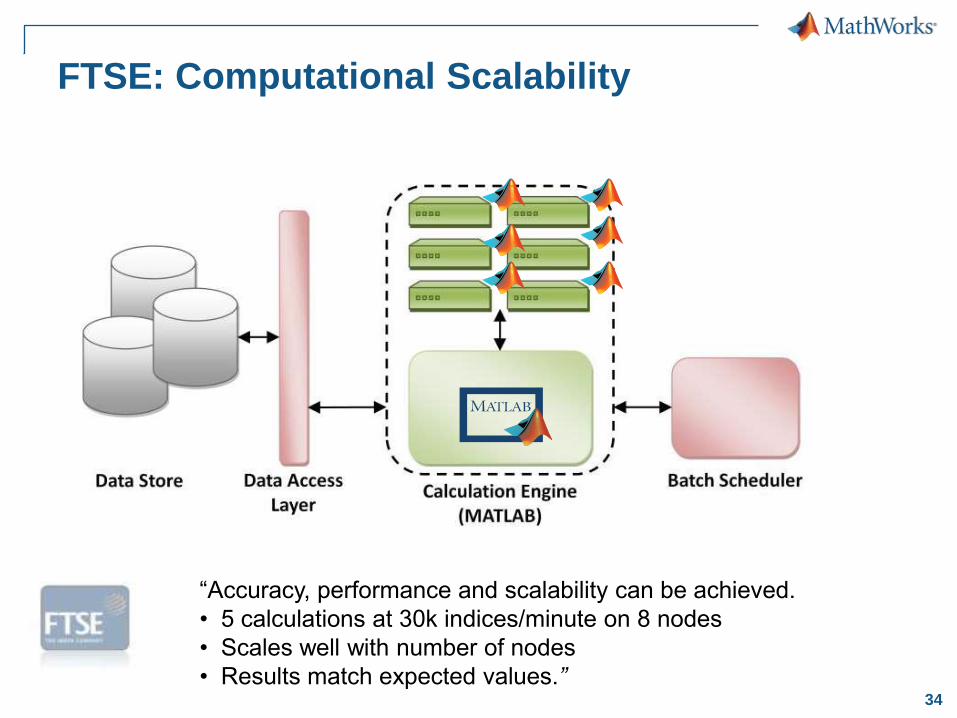

―Accuracy, performance and scalability can be achieved.

• 5 calculations at 30k indices/minute on 8 nodes

• Scales well with number of nodes

• Results match expected values.”

FTSE: Computational Scalability

35

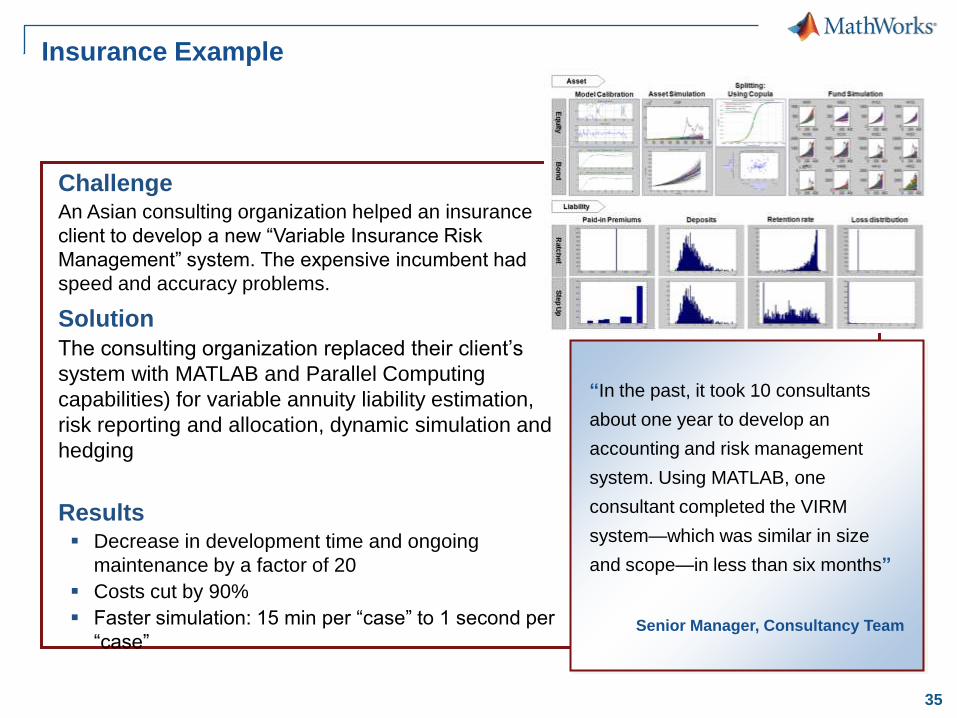

Insurance Example

ChallengeAn Asian consulting organization helped an insurance

client to develop a new ―Variable Insurance Risk

Management‖ system. The expensive incumbent had

speed and accuracy problems.

Solution

The consulting organization replaced their client’s

system with MATLAB and Parallel Computing

capabilities) for variable annuity liability estimation,

risk reporting and allocation, dynamic simulation and

hedging

Results Decrease in development time and ongoing

maintenance by a factor of 20

Costs cut by 90%

Faster simulation: 15 min per ―case‖ to 1 second per

―case‖

“In the past, it took 10 consultants

about one year to develop an

accounting and risk management

system. Using MATLAB, one

consultant completed the VIRM

system—which was similar in size

and scope—in less than six months”

Senior Manager, Consultancy Team

36

Agenda

Introduction

– MATLAB in the Financial Services Industry

– Computational Finance within MathWorks

Risk Modelling with MATLAB

– Examples

Portfolio Optimization & Risk Analysis

Cash flow Balancing & Scenario Analysis

RiskViewer:- Building a Risk Application

How Risk Departments across the world use MATLAB

Using MATLAB in ―Production‖ Trading (also insurance, index calculation)

Counterparty & Default Risk

37

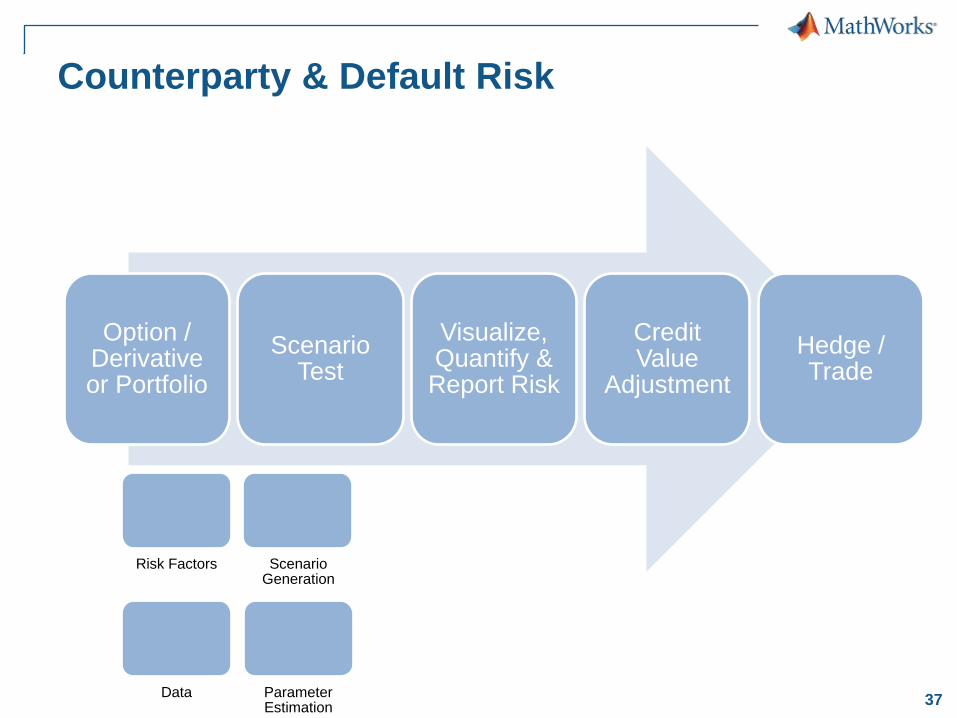

Option / Derivative or Portfolio

Scenario Test

Visualize, Quantify & Report Risk

Credit Value

Adjustment

Hedge / Trade

Counterparty & Default Risk

Risk Factors Scenario Generation

Data Parameter Estimation

38

Counterparty & Default Risk

We have already demonstrated some key capabilities:-

– VaR Calculation

– Forecasting & Stress Testing

– Rudimentary default estimation

– Object-based application building & integration

Some Disparate Examples

– Calculate PFE (Potential Future Exposure) of an FX Forward

– Credit Default Swap Modelling – Counterparty Analysis

– Hedging & Trading – A Black Karasinski Example

.

39

Counterparty & Default Risk

Calculate Potential Future Exposure (PFE) of an FX

Forward

– Determine current value of the derivative contract

Use the latest 6 month exchange rates

– Key Risk Driver is interest rate

Spot rate uses GBM, with a Term Structure of Volatility Model

Parallel shifts driven by changes in spot exchange

– Calculate PFE

Simulate for x time steps values for spot exchange rate

Volatility and drift of parameters estimated using a history of spot

exchange rates

Calculate MTM

Take 95th percentile of y simulations to yield the 95% contract-level PFE

40

Counterparty & Default Risk

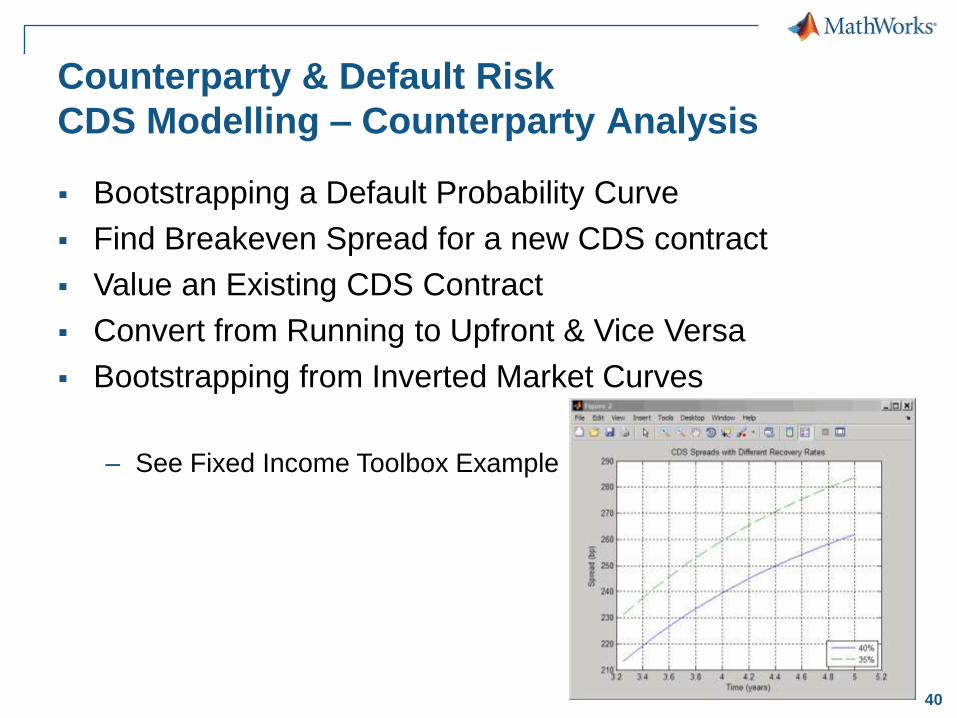

CDS Modelling – Counterparty Analysis

Bootstrapping a Default Probability Curve

Find Breakeven Spread for a new CDS contract

Value an Existing CDS Contract

Convert from Running to Upfront & Vice Versa

Bootstrapping from Inverted Market Curves

– See Fixed Income Toolbox Example

41

Hedging & Trading

This example (from Financial Derivatives Toolbox) uses

the Black-Karasinski Model

– Create the Interest Rate Term Structure Based on Reported

Data

– Specify the Volatility Model

– Specify the Time Structure of the Tree

– Create the BK Tree

– Create an Instrument Portfolio

– Price the Portfolio Using the BK Model

– Add More Instruments to the Existing Portfolio

– Hedging

– Obtain a Neutral Sensitivity Portfolio

– Adding Constraints to Hegde a Portfolio

42

43

![Enhancing the Dynamic Meta Modeling Formalism and its ... · namic Meta Modeling (DMM) [4], can be used. Dynamic Meta Modeling is a technique used to formally describe the dynamic](https://img.pdfslide.us/doc/110x75/5f6bb147a8ce9004a869923c/enhancing-the-dynamic-meta-modeling-formalism-and-its-namic-meta-modeling-dmm.jpg)