Embed Size (px)

Citation preview

Enhancing Operational Performance while Building Confidence: The Case

for Stress Testing

Presented by Kevin Greenidge (CBB) & Jide Lewis (BOJ)

CAIB 37th Annual Conference

"Repositioning the Region: The Role of the Financial Services Industry"

11 November 2010

2

OVERVIEW1. Lessons from financial crises.

2. What is stress testing?

3. Stress Testing at the level of the individual FI –Guideline

4. Stress Testing at the System level

3

Lessons from financial crises Insufficient consideration of extreme events

– “It is hard for us without being flippant, to even see a scenario within any kind of realm of reason that would see us losing one dollar in any of those transactions.” August 2007, Joseph Cassano, a former AIG executive

– “Almost no one expected what was coming. It’s not fair to blame us for not predicting the unthinkable.” Daniel Mudd, former chief executive of Fannie

4

What is stress testing? Stress Testing: Risk management technique used

to evaluate the potential effects on an institution’s financial condition, of a set of specified changes in risk factors, corresponding to exceptional but plausible events. It is a rough estimate of how the value of a portfolio changes

not a precise tool that can be used with scientific accuracy. Originally developed for use at the portfolio level, to

understand the latent risks to a trading book from extreme movements in market prices.

Now applied a broader context, with the aim of measuring the sensitivity of the entire financial system to common shocks

5

What is stress testing? Stress testing the entire financial system has

several important differences with portfolio-level stress tests. First, the ultimate intent of focusing on the system as a whole

is to identify common vulnerabilities across institutions that could undermine the overall stability of the financial system.

Second, it is more macroeconomic in nature, as we are interested in understanding how major changes in the economic environment may affect the financial system.

Third, there is a difference in the complexity and degree of aggregation. System-focus tests involve aggregation or comparison of more

heterogeneous portfolios, -apples & orange problem.

6

What is stress testing?System focused stress tests should complement the regular stress testing done by individual financial institutions. They are designed to complement them with a broader

understanding of the sensitivity of the overall system to a variety of shocks, and to leverage the existing expertise found in different institutions.

Stress testing at the level of the financial system can be done one of two ways: simultaneous stress tests of multiple portfolios using a

common scenario, or a single scenario applied to an aggregated portfolio or

model of the entire system.

7

What is stress testing?

Sensitivity Test: Form of stress testing which typically involves an incremental change in a risk factor to determine the impact on an insurer

Scenario Testing: Form of stress testing which uses a hypothetical future state of the world to define the changes in the risk factors affecting the insurer.

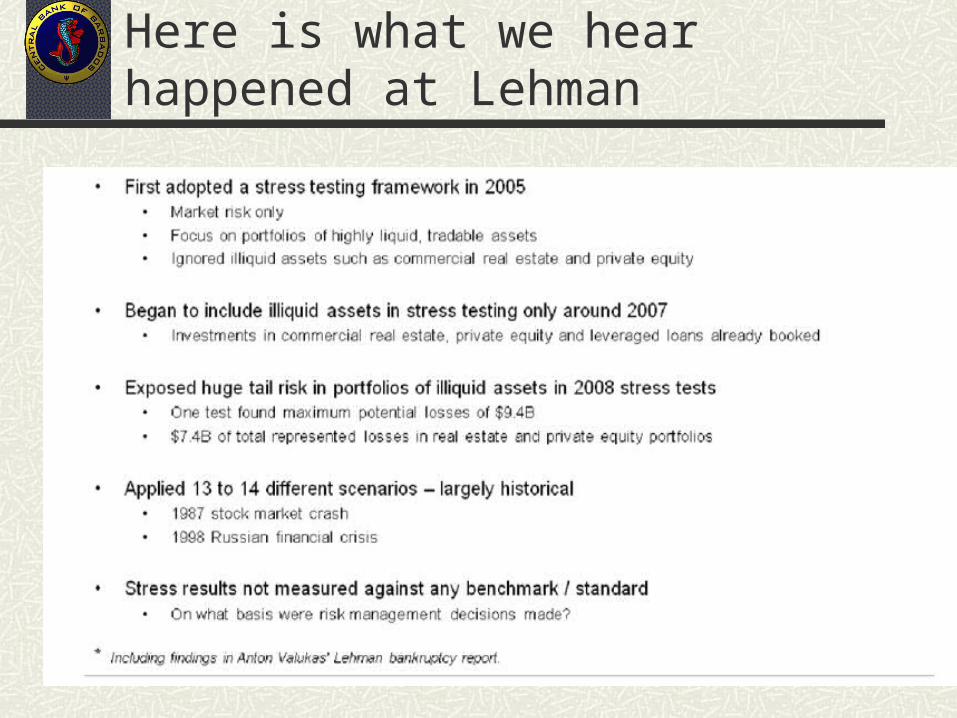

Here is what we hear happened at Lehman

Weakness in Bank Stress Testing – Pre-Crisis

Stress Testing at the level of the individual FI –Guideline

Broad purpose of stress testing– Stress testing should be embedded in enterprise

wide risk management

– It should be actionable, playing an important role in development of risk mitigation or contingency plans

– It should feed into the institution’s decision making process (e.g. setting risk appetite, exposure limits, and evaluating strategic choices)

– Stress testing should be clearly documented & available for review

Specific purposes of stress testing– Risk identification and control

– Complementary perspective to other RM tools

– Supporting capital management

– Improving liquidity management

Role of the Board and senior management– Board has ultimate responsibility for the overall stress testing

program and that it is “fit for purpose”

– Senior management is accountable for the program’s implementation, management and oversight.

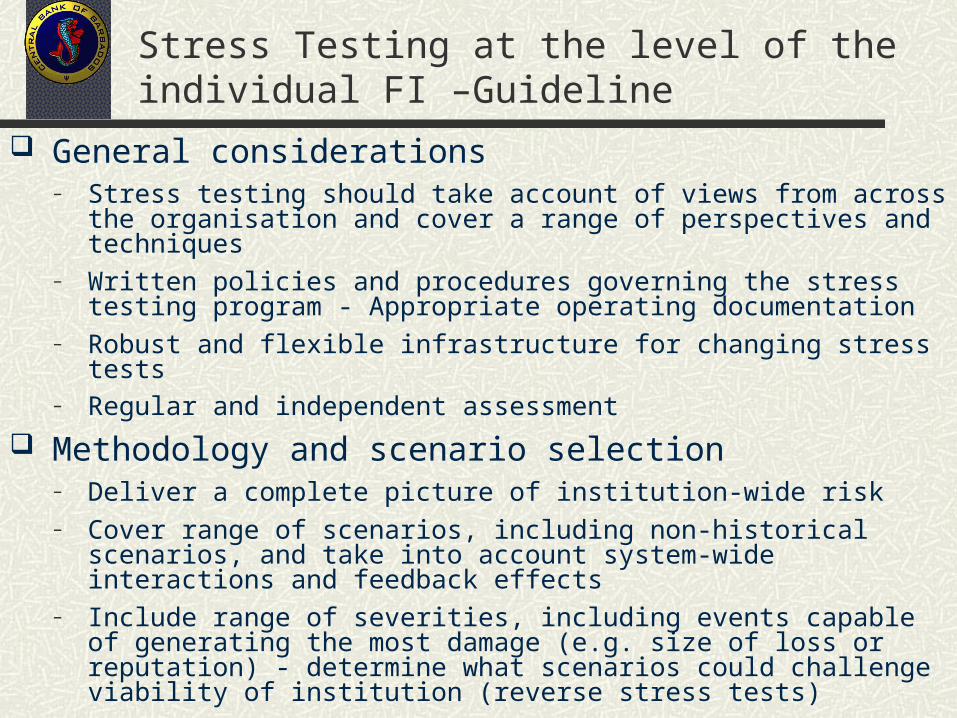

Stress Testing at the level of the individual FI –Guideline

General considerations– Stress testing should take account of views from across the

organisation and cover a range of perspectives and techniques – Written policies and procedures governing the stress testing

program - Appropriate operating documentation– Robust and flexible infrastructure for changing stress tests– Regular and independent assessment

Methodology and scenario selection– Deliver a complete picture of institution-wide risk– Cover range of scenarios, including non-historical scenarios, and

take into account system-wide interactions and feedback effects– Include range of severities, including events capable of

generating the most damage (e.g. size of loss or reputation) - determine what scenarios could challenge viability of institution (reverse stress tests)

Stress Testing at the level of the individual FI –Guideline

13

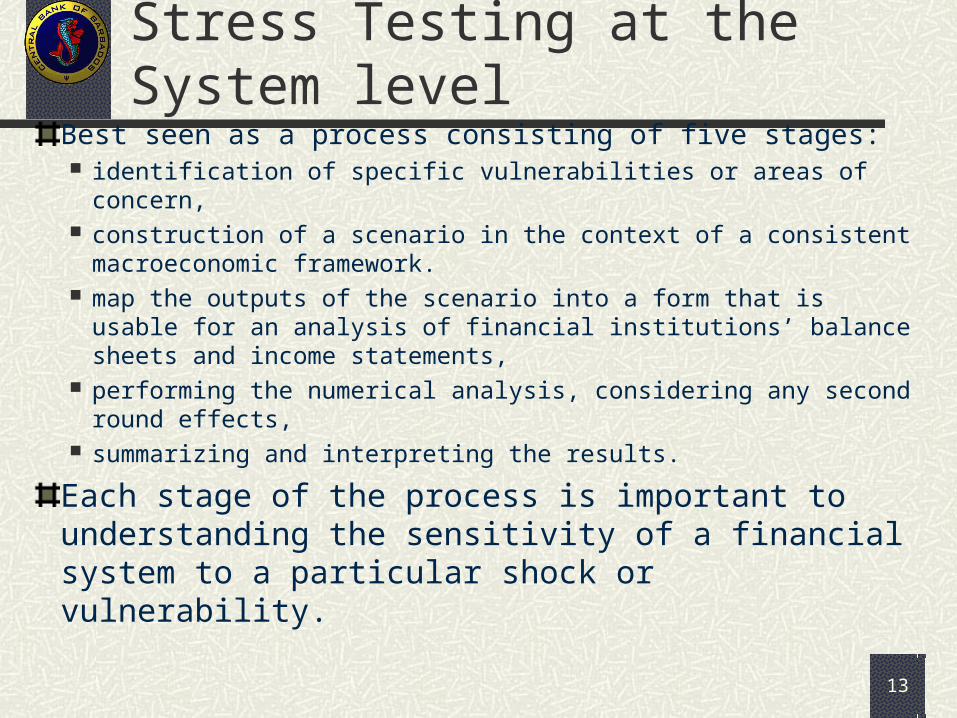

Stress Testing at the System levelBest seen as a process consisting of five stages: identification of specific vulnerabilities or areas of concern, construction of a scenario in the context of a consistent

macroeconomic framework. map the outputs of the scenario into a form that is usable for an

analysis of financial institutions’ balance sheets and income statements,

performing the numerical analysis, considering any second round effects,

summarizing and interpreting the results.

Each stage of the process is important to understanding the sensitivity of a financial system to a particular shock or vulnerability.

14

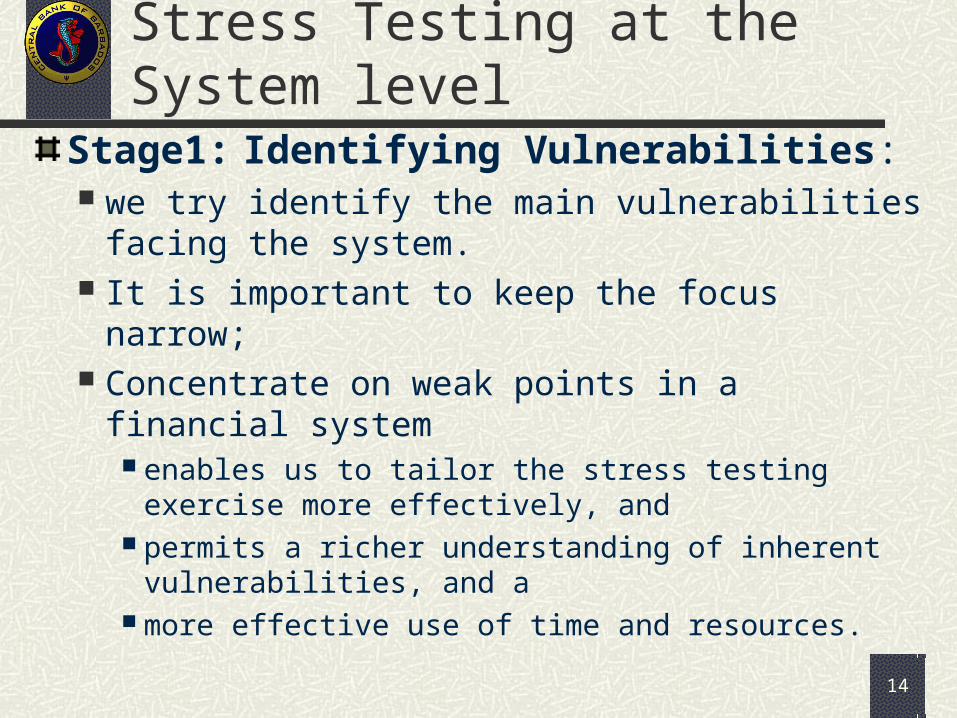

Stress Testing at the System levelStage1: Identifying Vulnerabilities: we try identify the main vulnerabilities facing the

system. It is important to keep the focus narrow; Concentrate on weak points in a financial system

enables us to tailor the stress testing exercise more effectively, and

permits a richer understanding of inherent vulnerabilities, and a

more effective use of time and resources.

15

Stress Testing at the System levelStage1: Identifying Vulnerabilities: we try identify the main vulnerabilities facing the system. It is important to keep the focus narrow; concentrate on weak points

in a financial system enables us to tailor the stress testing exercise more effectively, and permits a richer understanding of inherent vulnerabilities, and a more effective use of time and resources.

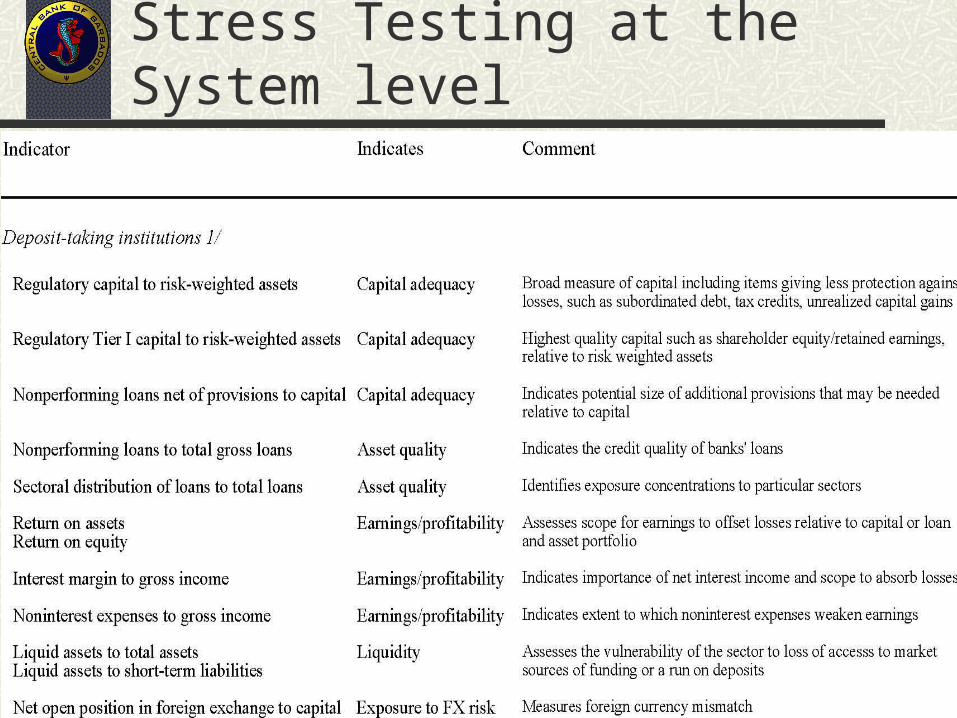

We also make use of a range of numerical indicators to help isolate potential weaknesses,

macro-level indicators, broad structural indicators,

Ownership and Market structure Balance sheet structures

and institution-focused or micro-level indicators (FSIs).

16

Stress Testing at the System level

17

Stress Testing at the System level

18

Stress Testing at the System levelStage 2: Construct a scenario: Once the key questions or main vulnerabilities of interest have

been identified, the next stage is to construct a scenario that will form the basis of the stress test.

It is recommended that some macroeconomic framework or model be employed.

The objective of using an explicit macroeconomic model is to link a particular set of shocks to key macro and financial variables in a consistent and forward-looking framework.

The key reason for using this approach is to bring the discipline and consistency of an empirically-based model and an explicit focus on the link between the macroeconomy and the main vulnerabilities.

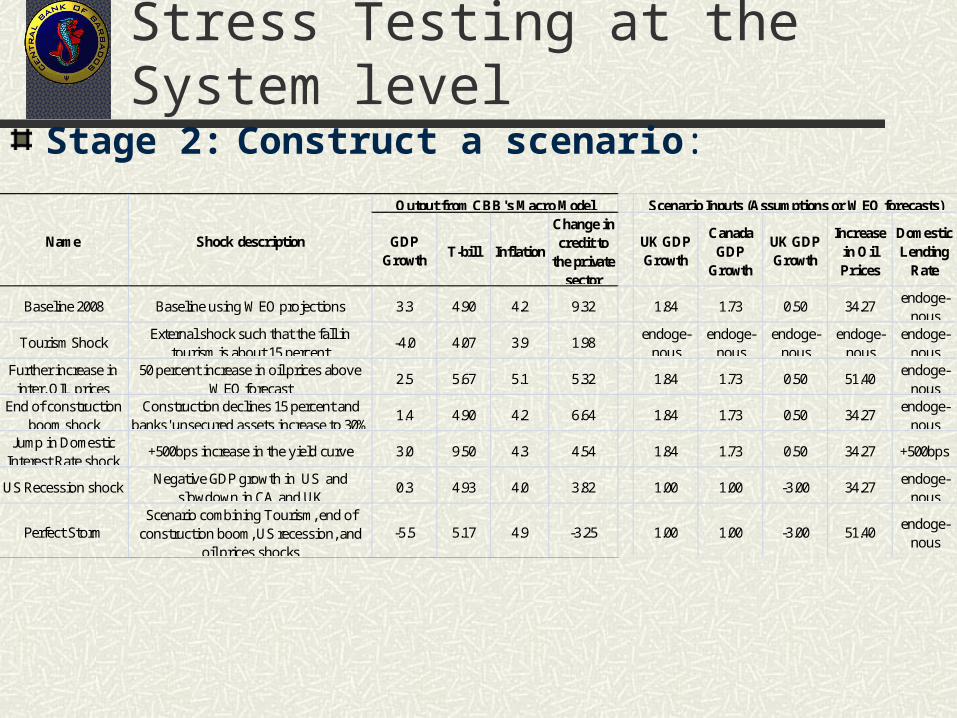

Stage 2: Construct a scenario:Stress Testing at the System level

GDP Growth

T-bill Inflation

Change in credit to

the private sector

UK GDP Growth

Canada GDP

Growth

UK GDP Growth

Increase in Oil Prices

Domestic Lending

Rate

Baseline 2008 Baseline using WEO projections 3.3 4.90 4.2 9.32 1.84 1.73 0.50 34.27endoge-

nous

Tourism ShockExternal shock such that the fall in

tourism is about 15 percent-4.0 4.07 3.9 1.98

endoge-nous

endoge-nous

endoge-nous

endoge-nous

endoge-nous

Further increase in inter. OIL prices

50 percent increase in oil prices above WEO forecast

2.5 5.67 5.1 5.32 1.84 1.73 0.50 51.40endoge-

nousEnd of construction

boom shockConstruction declines 15 percent and

banks' unsecured assets increase to 30%1.4 4.90 4.2 6.64 1.84 1.73 0.50 34.27

endoge-nous

Jump in Domestic Interest Rate shock

+500bps increase in the yield curve 3.0 9.50 4.3 4.54 1.84 1.73 0.50 34.27 +500bps

US Recession shockNegative GDP growth in US and

slowdown in CA and UK0.3 4.93 4.0 3.82 1.00 1.00 -3.00 34.27

endoge-nous

Perfect StormScenario combining Tourism, end of

construction boom, US recession, and oil prices shocks

-5.5 5.17 4.9 -3.25 1.00 1.00 -3.00 51.40endoge-

nous

Name Shock description

Output from CBB's Macro Model Scenario Inputs (Assumptions or WEO forecasts)

20

Stress Testing at the System levelBalance-Sheet Implementation: the next step is to translate the various outputs into the balance

sheets and income statements of financial institutions. There are two main approaches to translating or “mapping” scenarios into balance sheets:

the “bottom-up” approach, where estimates are based on data for individual portfolios, which can then be aggregated, and

the “top-down” approach, which uses aggregated or macro-level data to estimate the impact.

21

Stress Testing at the System levelBalance-Sheet Implementation:

22

THANK YOU!