Embed Size (px)

Citation preview

Enhancing and Protecting

Organizational Value

Introducing Sawyers 7th Edition

Objectives

• Introduce Sawyers 7th Edition – Focused on achieving the

mission of internal audit

– Setting Up and Internal Audit Shop

– Delivering IA Products and Services

• Using Sawyers to define value delivered today and

opportunities to grow value tomorrow

Sawyers 7th Edition Goals

• Mission Focused

– Enhancing & Protecting Organizational Value

• Readable by IA and Stakeholders

– Business Perspective of Internal Audit

• Relevant to today’s IA Challenges

– Growing Risk Functions, Collaboration

• Spirit of Knowing Modern Methods

- Staying Current with Leading Ideas

Enhancing and Protecting Organizational Value

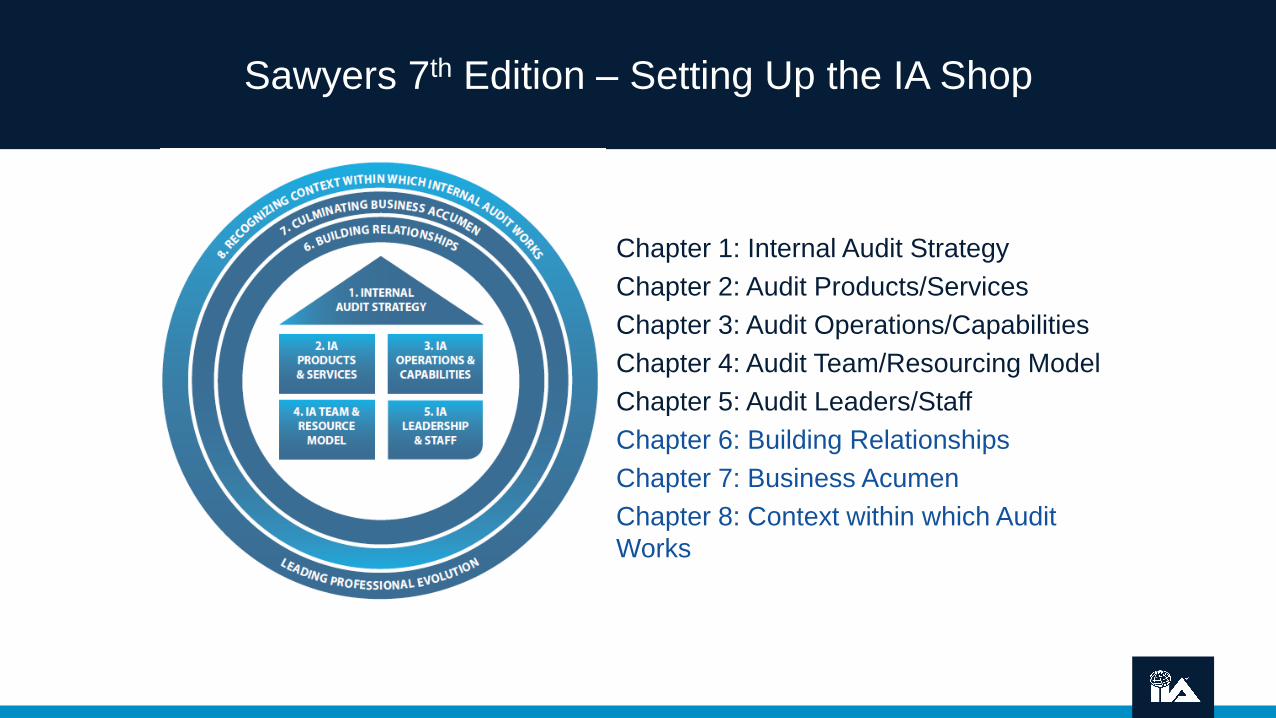

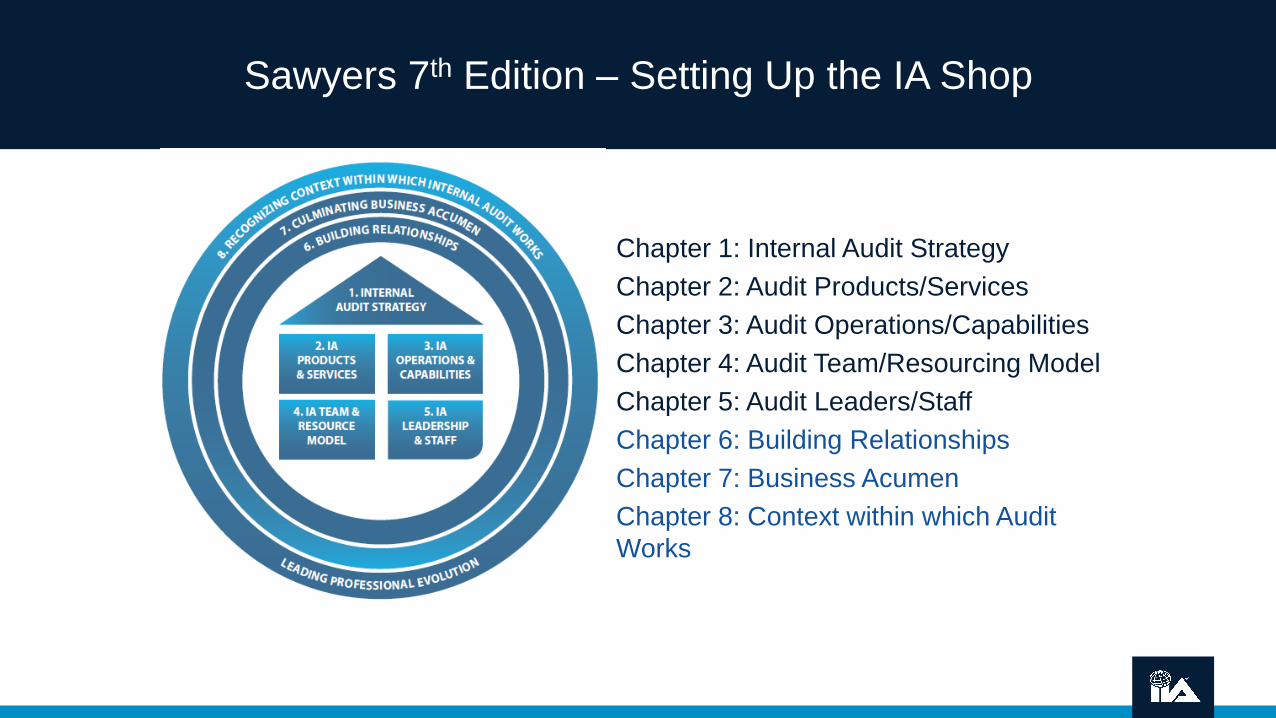

Sawyers 7th Edition – Setting Up the IA Shop

Chapter 1: Internal Audit Strategy

Chapter 2: Audit Products/Services

Chapter 3: Audit Operations/Capabilities

Chapter 4: Audit Team/Resourcing Model

Chapter 5: Audit Leaders/Staff

Chapter 6: Building Relationships

Chapter 7: Business Acumen

Chapter 8: Context within which Audit

Works

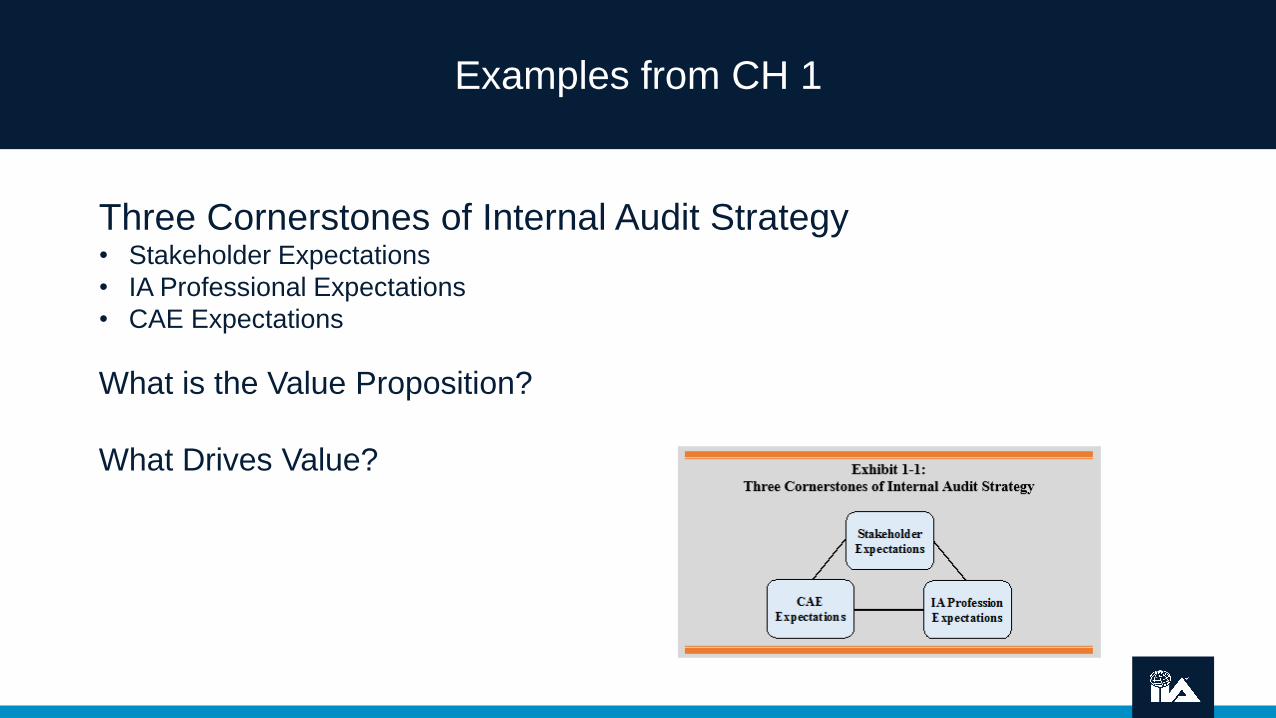

Examples from CH 1

Three Cornerstones of Internal Audit Strategy• Stakeholder Expectations

• IA Professional Expectations

• CAE Expectations

What is the Value Proposition?

What Drives Value?

Examples from CH 2

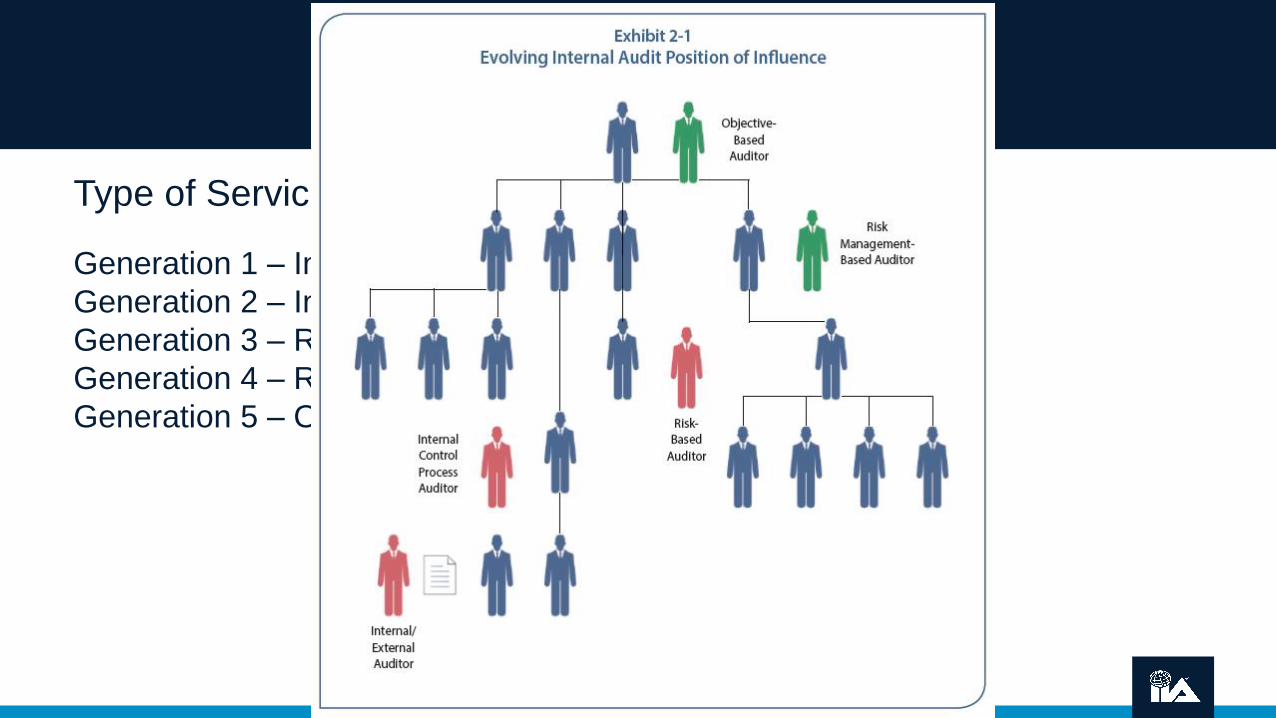

Type of Service and Expected Product

Generation 1 – Internal/External Auditor

Generation 2 – Internal Control Process Auditor

Generation 3 – Risk Based Auditor

Generation 4 – Risk Management Based Auditor

Generation 5 – Objective Based Auditor

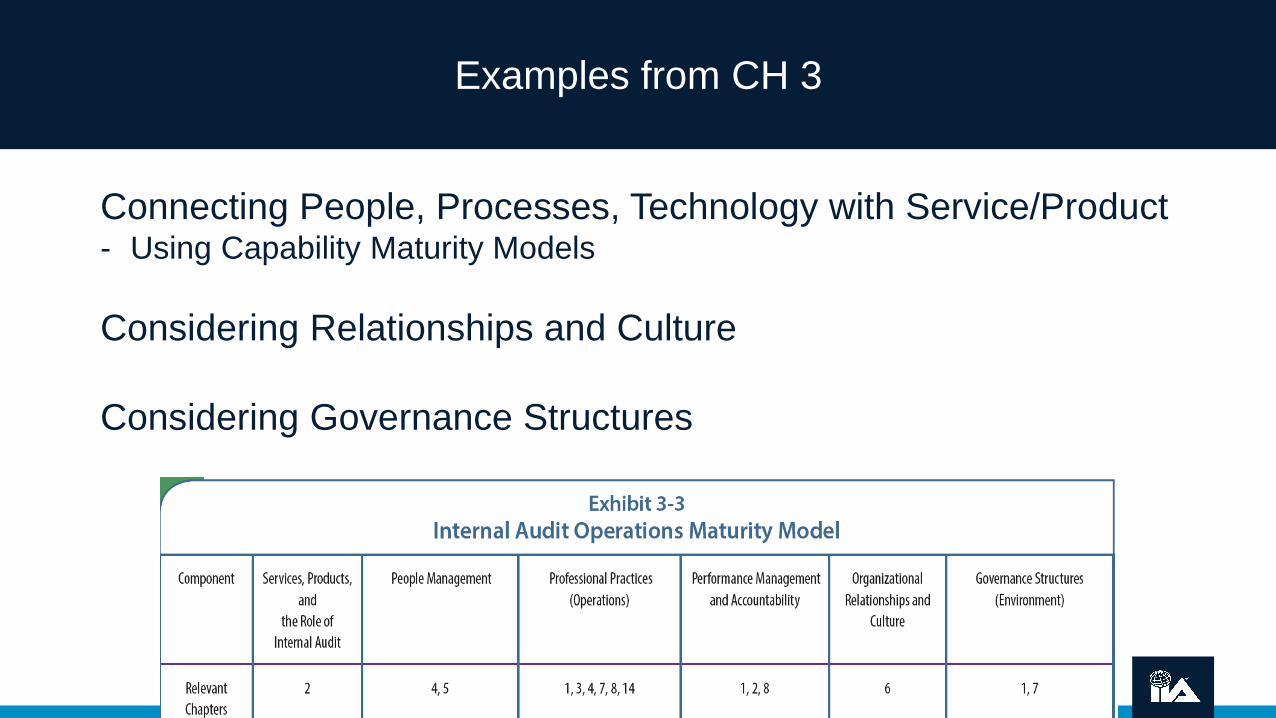

Examples from CH 3

Connecting People, Processes, Technology with Service/Product- Using Capability Maturity Models

Considering Relationships and Culture

Considering Governance Structures

Examples from CH 4-5

Implied Role of IA = The Type of Services and Products Expected

Service and Product Expectations =

Core Skills & Certifications Required

Specialty Skills & Certifications Required

Skills Required =Internal Audit Structure and Outsourcing Needs

Examples from CH 6-8

Building Relationships“Relationships with stakeholders can either contribute to the success of internal audit functions or break it.”

Business Acumen“In general business acumen means CAEs effectively align their own perspective of value with the

perspective of board and management stakeholders”

Understanding the Context for IA“It is more important than ever for internal audit to partner with SME’s and the second line of defense

functions…and define IA effectiveness”

Sawyers 7th Edition – Setting Up the IA Shop

Chapter 1: Internal Audit Strategy

Chapter 2: Audit Products/Services

Chapter 3: Audit Operations/Capabilities

Chapter 4: Audit Team/Resourcing Model

Chapter 5: Audit Leaders/Staff

Chapter 6: Building Relationships

Chapter 7: Business Acumen

Chapter 8: Context within which Audit

Works

Sawyers 7th Edition – Delivering IA Services

Chapter 9: The Internal Audit Mission and Its Risks

Chapter 10: Risk Assessment and Audit Planning

Chapter 11: Planning the Audit Engagement

Chapter 12: Assessing Internal Control

Chapter 13: Audit Communication (Reporting and Follow-up)

Chapter 14: Assembling and Supervising the Internal Audit Team

Chapter 15: Specialty Skill Areas

Chapter 16: Advisory Services

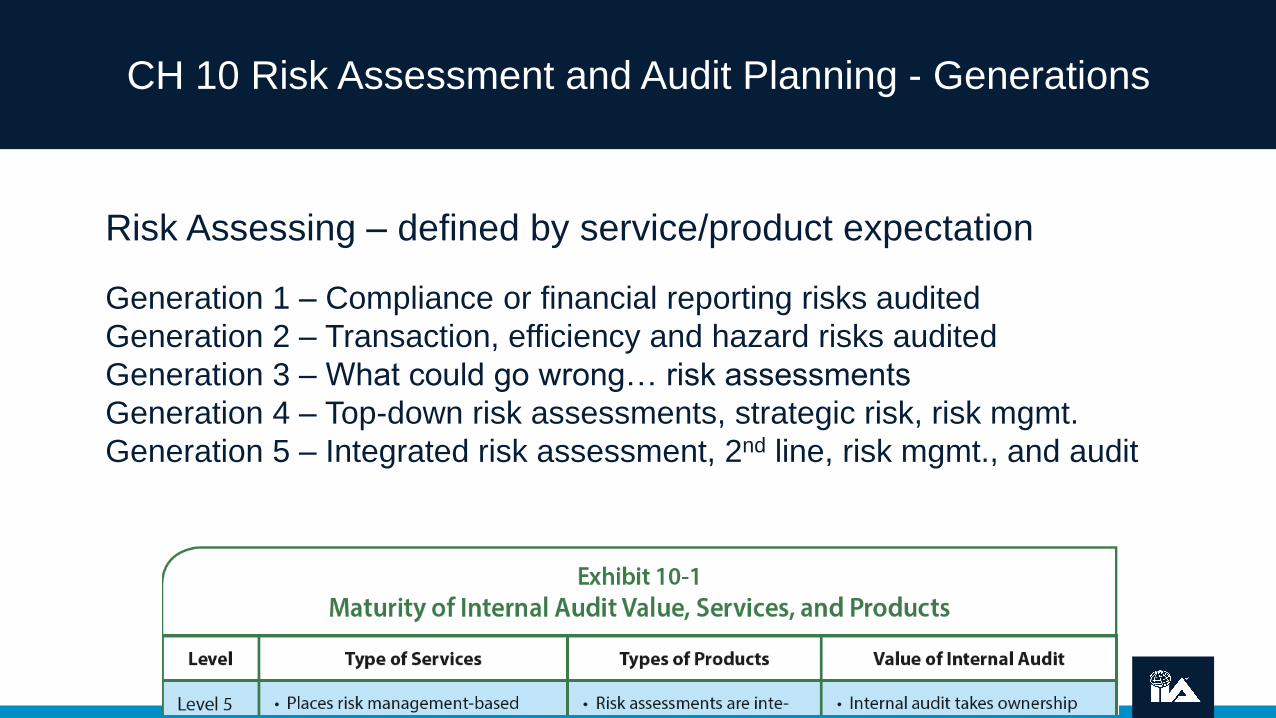

CH 10 Risk Assessment and Audit Planning - Generations

Risk Assessing – defined by service/product expectation

Generation 1 – Compliance or financial reporting risks audited

Generation 2 – Transaction, efficiency and hazard risks audited

Generation 3 – What could go wrong… risk assessments

Generation 4 – Top-down risk assessments, strategic risk, risk mgmt.

Generation 5 – Integrated risk assessment, 2nd line, risk mgmt., and audit

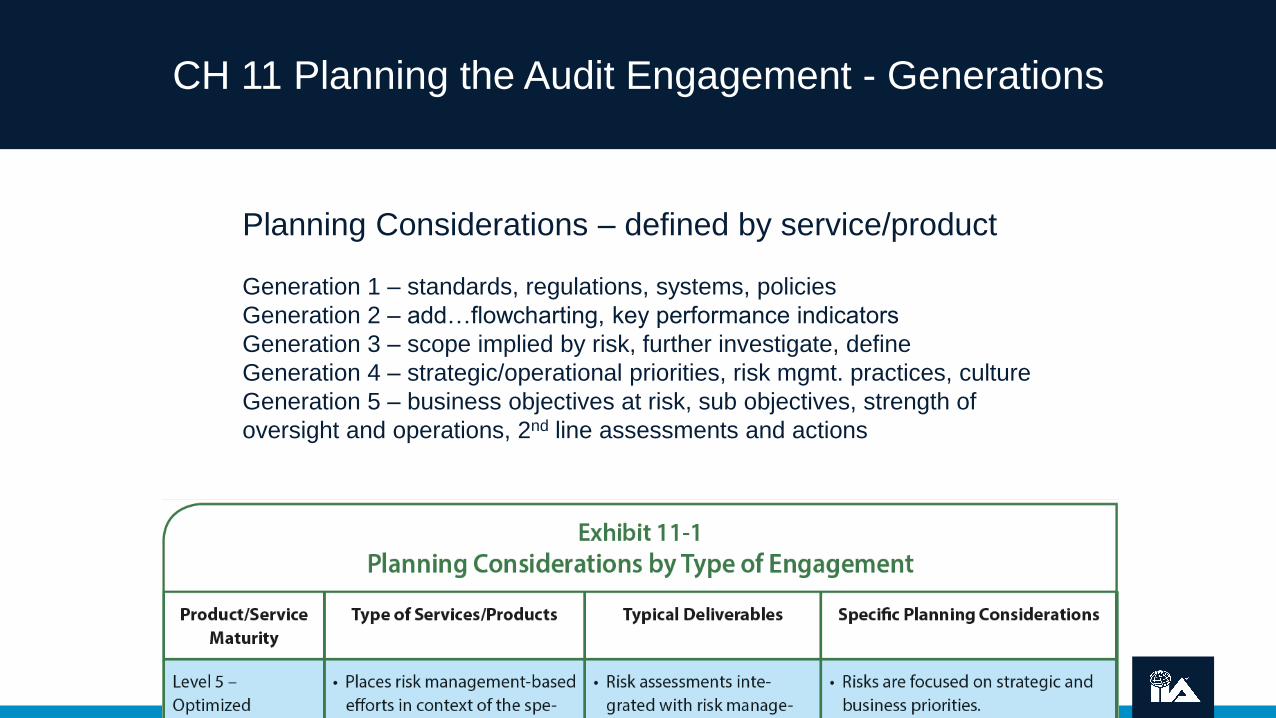

CH 11 Planning the Audit Engagement - Generations

Planning Considerations – defined by service/product

Generation 1 – standards, regulations, systems, policies

Generation 2 – add…flowcharting, key performance indicators

Generation 3 – scope implied by risk, further investigate, define

Generation 4 – strategic/operational priorities, risk mgmt. practices, culture

Generation 5 – business objectives at risk, sub objectives, strength of

oversight and operations, 2nd line assessments and actions

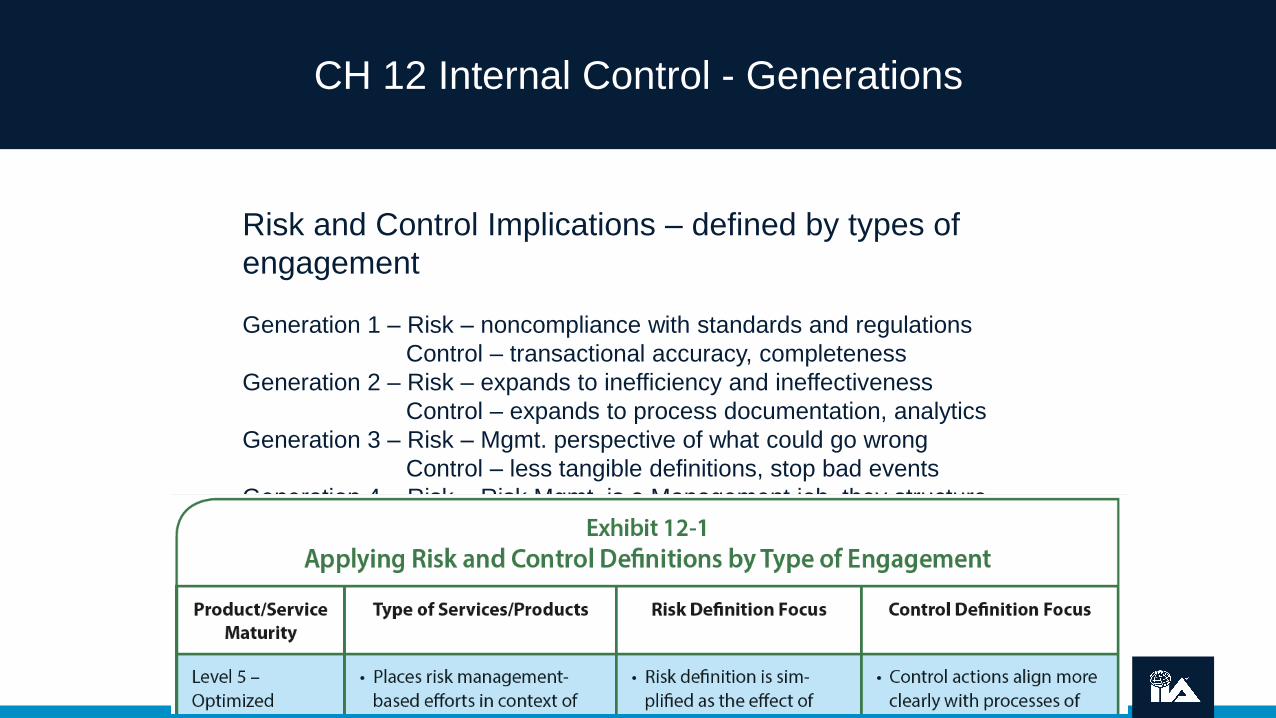

CH 12 Internal Control - Generations

Risk and Control Implications – defined by types of

engagement

Generation 1 – Risk – noncompliance with standards and regulations

Control – transactional accuracy, completeness

Generation 2 – Risk – expands to inefficiency and ineffectiveness

Control – expands to process documentation, analytics

Generation 3 – Risk – Mgmt. perspective of what could go wrong

Control – less tangible definitions, stop bad events

Generation 4 – Risk – Risk Mgmt. is a Management job, they structure

Control – Expands to include good mgmt./governance

Generation 5 – Risk – simply the effect of uncertainty on objectives

Control – actions align with mgmt process for oversight,

operations alignment of people, process, and technology

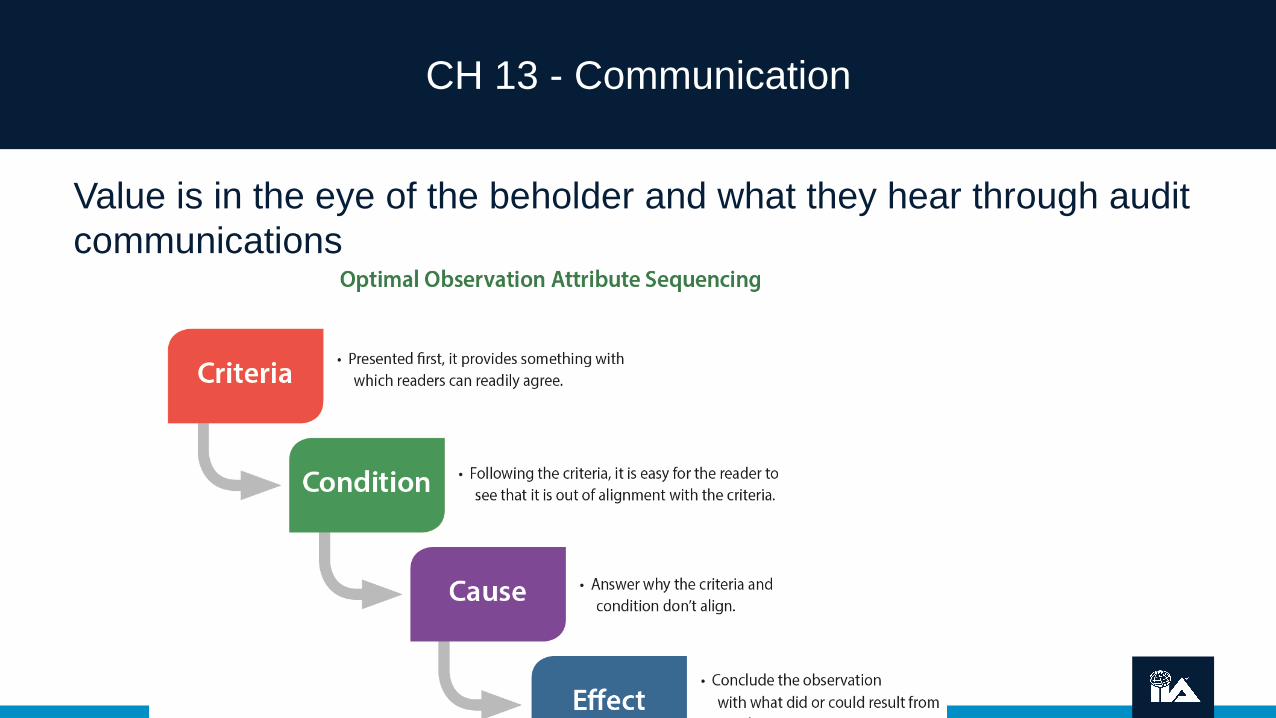

CH 13 - Communication

Value is in the eye of the beholder and what they hear through audit

communications

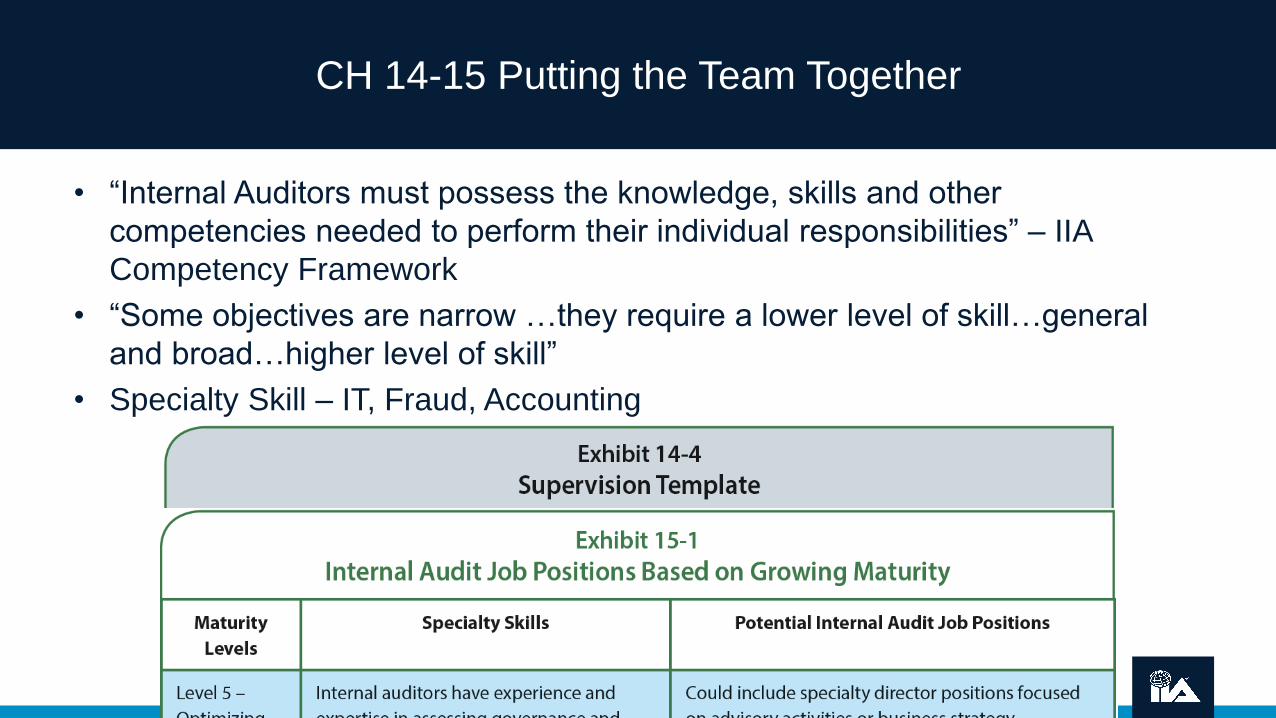

CH 14-15 Putting the Team Together

• “Internal Auditors must possess the knowledge, skills and other

competencies needed to perform their individual responsibilities” – IIA

Competency Framework

• “Some objectives are narrow …they require a lower level of skill…general

and broad…higher level of skill”

• Specialty Skill – IT, Fraud, Accounting

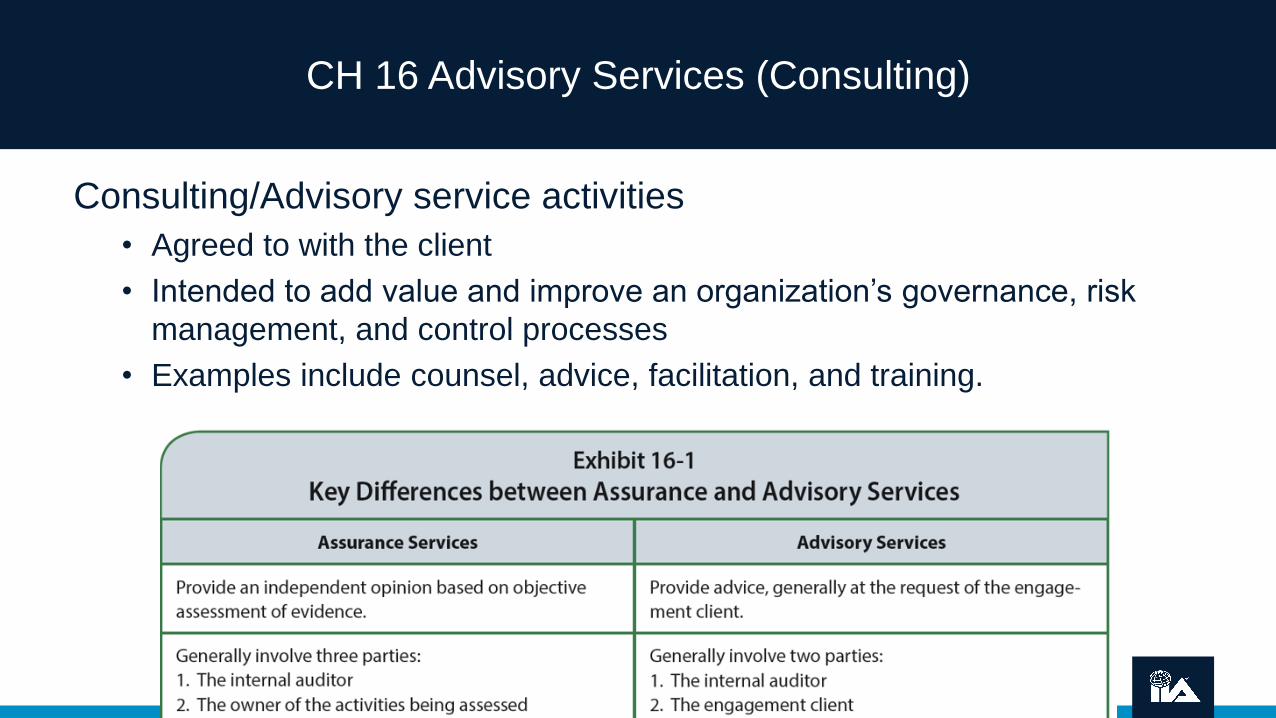

CH 16 Advisory Services (Consulting)

Consulting/Advisory service activities

• Agreed to with the client

• Intended to add value and improve an organization’s governance, risk

management, and control processes

• Examples include counsel, advice, facilitation, and training.

Conclusion

• Enhancing and Protecting Organizational Value

– Requires the CAE to understand the value their organization is

producing

– Requires the CAE to align their services and products to add to

that value

– The future is one that will include Collaborative IA connecting

with the 1st and 2nd lines of defense around assurance and

management of risk

QUESTIONS

Contributing Professionals

• Hans Beumer (Switzerland)

• Dan Clayton (USA)

• Farah Araj (UAE)

• Michael Levy (USA)

• Jenitha John (S.Africa)

• Jason Mefford (USA)

• Bruce Turner (Australia)

• Andrew Cox (Australia)

• Cris Shreve (USA)

• Angie Chin (USA/Brazil/Europe/Asia)

Contributing Authors Technical Editors

• Paul Sobel (USA)

• Dan Clayton (USA)

• Angie Chin (USA/Brazil/Europe/Asia)

• Cris Shreve (USA)

Advisory Committee

• Larry Rittenberg (USA)

• Mark Salamasick (USA)

• Angie Chin (USA/Brazil/Europe/Asia)

Thank You

The Institute of Internal Auditors

Dan Clayton

Director of Strategy & KM, System Audit Office

LinkedIn: https://www.linkedin.com/in/dan-clayton-cia-

cpa-ckm-52b2227