Embed Size (px)

Citation preview

Engineers AustraliaEngineers AustraliaManagement and Engineering Branch Management and Engineering Branch

ACTACTApril 2006April 2006

An introduction to the revisedAn introduction to the revisedAustralian Standard AS 4183:2006Australian Standard AS 4183:2006

“ “ Value Management “Value Management “

Lex Clark CPEng FIEAust and Lex Clark CPEng FIEAust and Roy Barton MSc Dip Ed PhDRoy Barton MSc Dip Ed PhD

Engineers AustraliaEngineers AustraliaManagement and Engineering Branch Management and Engineering Branch

ACTACTApril 2006April 2006

An introduction to the revisedAn introduction to the revisedAustralian Standard AS 4183:2006Australian Standard AS 4183:2006

“ “ Value Management “Value Management “

PART ONEPART ONE

Lex Clark CPEng FIEAustLex Clark CPEng FIEAust

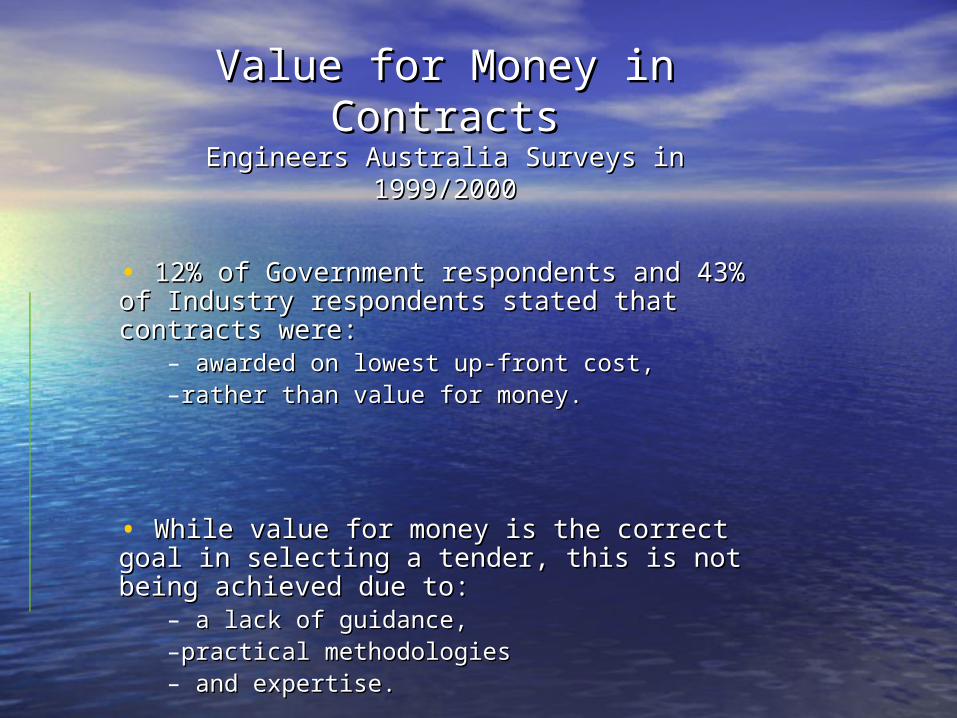

Value for Money in ContractsValue for Money in ContractsEngineers Australia Surveys in 1999/2000Engineers Australia Surveys in 1999/2000

• 12% of Government respondents and 43% of 12% of Government respondents and 43% of Industry respondents stated that contracts Industry respondents stated that contracts were:were:

– awarded on lowest up-front cost, awarded on lowest up-front cost, –rather than value for money.rather than value for money.

• While value for money is the correct goal in While value for money is the correct goal in selecting a tender, this is not being achieved selecting a tender, this is not being achieved due to:due to:

– a lack of guidance, a lack of guidance, –practical methodologiespractical methodologies– and expertise.and expertise.

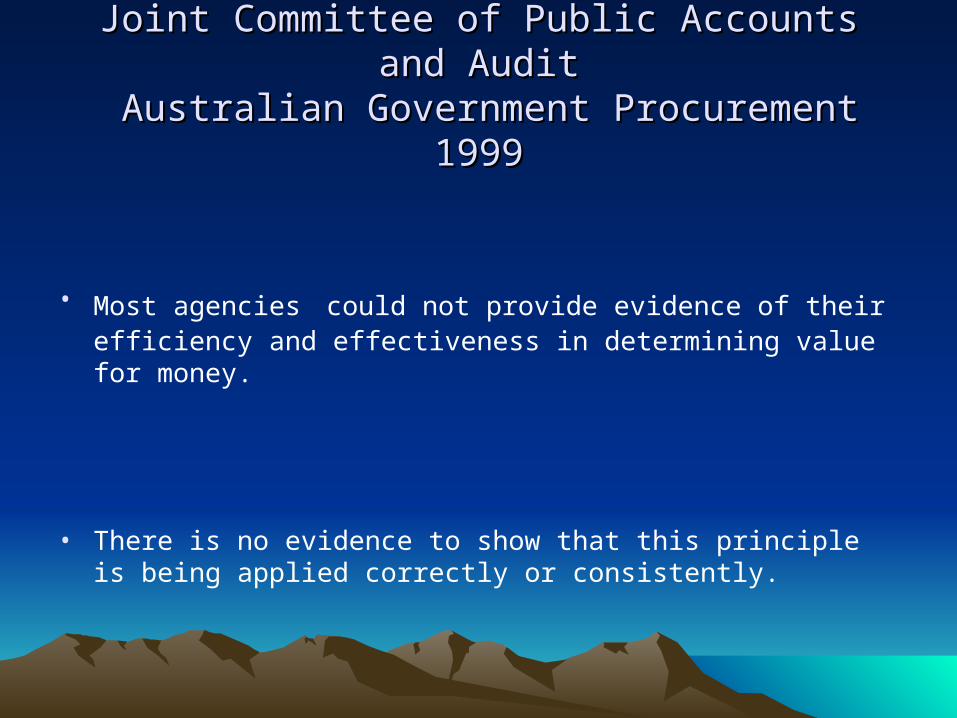

Joint Committee of Public Accounts and AuditJoint Committee of Public Accounts and Audit Australian Government Procurement Australian Government Procurement

19991999

• Most agencies could not provide evidence of their efficiency and effectiveness in determining value for money.

• There is no evidence to show that this principle is being applied correctly or consistently.

Commonwealth Procurement GuidelinesCommonwealth Procurement GuidelinesDepartment of Finance and AdministrationDepartment of Finance and Administration

20062006

The Principle of Value for MoneyThe Principle of Value for Money

• 4.1 Value for money is the core principle underpinning Australian 4.1 Value for money is the core principle underpinning Australian Government procurement.Government procurement.

• 4.3 In order to be in the best position to determine value for money 4.3 In order to be in the best position to determine value for money when conducting a procurement process, request documentation when conducting a procurement process, request documentation needs to specify logical, clearly articulated, comprehensive and needs to specify logical, clearly articulated, comprehensive and relevant conditions for participation and evaluation criteria which relevant conditions for participation and evaluation criteria which will enable the proper identification, assessment and comparison of will enable the proper identification, assessment and comparison of the costs and benefits of all submissions on a fair and common the costs and benefits of all submissions on a fair and common basis over the whole procurement cycle.basis over the whole procurement cycle.

• 4.4 Cost is not the only determining factor in assessing value for 4.4 Cost is not the only determining factor in assessing value for moneymoney

Value Analysis and Value Engineering

• Improving performance and reducing costs have long been principles of good engineering, procurement and management practice.

• World Wars I and II placed increased emphasis on these principles from combat effectiveness and availability of resources.

• Value Analysis developed in Industry in 1940/50’s as a methodology to combine these principles.

• Value Engineering expanded into Defence activities in 1950/60’s in response to growing costs and reducing resources.

Function and CostFunction and Cost

Analyse Functions (F) rather than components.Analyse Functions (F) rather than components.

Evaluate Costs (C) associated with these Functions.Evaluate Costs (C) associated with these Functions.

Value (V) was described as a relationship V = F/C.Value (V) was described as a relationship V = F/C.

Value for Money was implied but not defined in this relationship.Value for Money was implied but not defined in this relationship.

This relationship was applied within a decision making framework called the This relationship was applied within a decision making framework called the Job Plan.Job Plan.

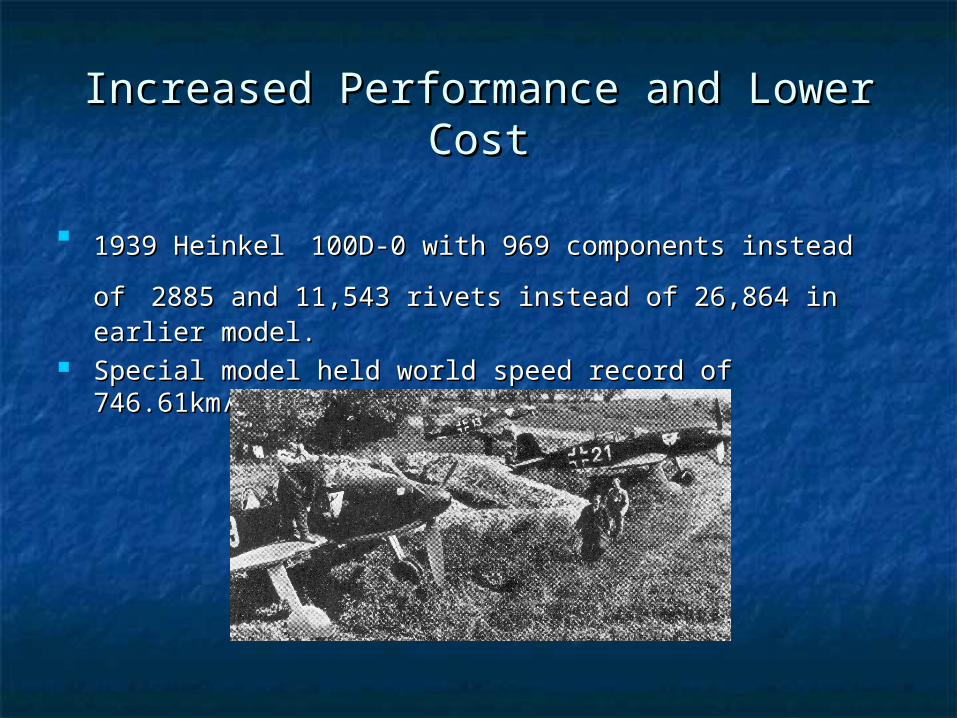

Increased Performance and Lower CostIncreased Performance and Lower Cost

1939 Heinkel1939 Heinkel 100D-0 with 969 components instead of100D-0 with 969 components instead of 2885 2885 and 11,543 rivets instead of 26,864 in earlier model.and 11,543 rivets instead of 26,864 in earlier model.

Special model held world speed record of 746.61km/hr in Special model held world speed record of 746.61km/hr in March 1939.March 1939.

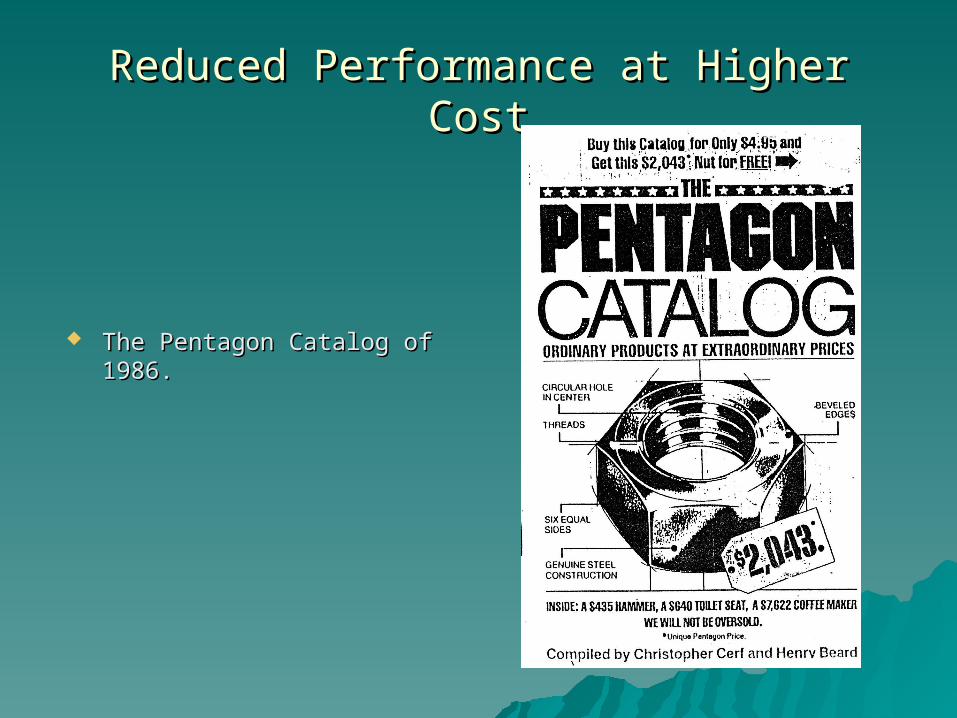

Reduced Performance at Higher CostReduced Performance at Higher Cost

The Pentagon Catalog of The Pentagon Catalog of 1986.1986.

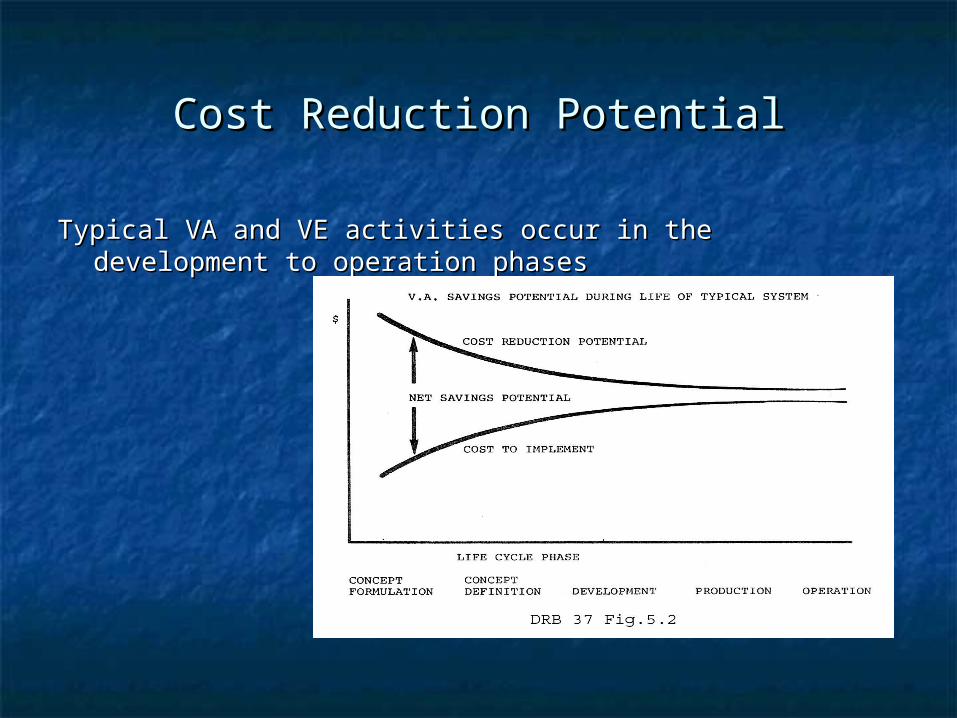

Cost Reduction PotentialCost Reduction Potential

Typical VA and VE activities occur in the development to Typical VA and VE activities occur in the development to operation phasesoperation phases

New Australian Standard New Australian Standard AS 4183:2006AS 4183:2006

AS4183:2006 redefines the concepts of Value and Value for AS4183:2006 redefines the concepts of Value and Value for Money.Money.

It increased emphasis on the application of Value It increased emphasis on the application of Value Management as early as possible by means of Value Management as early as possible by means of Value Management Studies.Management Studies.

The application of Value Analysis to ongoing activities The application of Value Analysis to ongoing activities provides continuous improvement. provides continuous improvement.

End of Part One

Engineers AustraliaManagement and Engineering Branch ACT

April 2006

An introduction to the revisedAustralian Standard AS 4183:2006

“ Value Management “

PART TWO

Dr Roy Barton

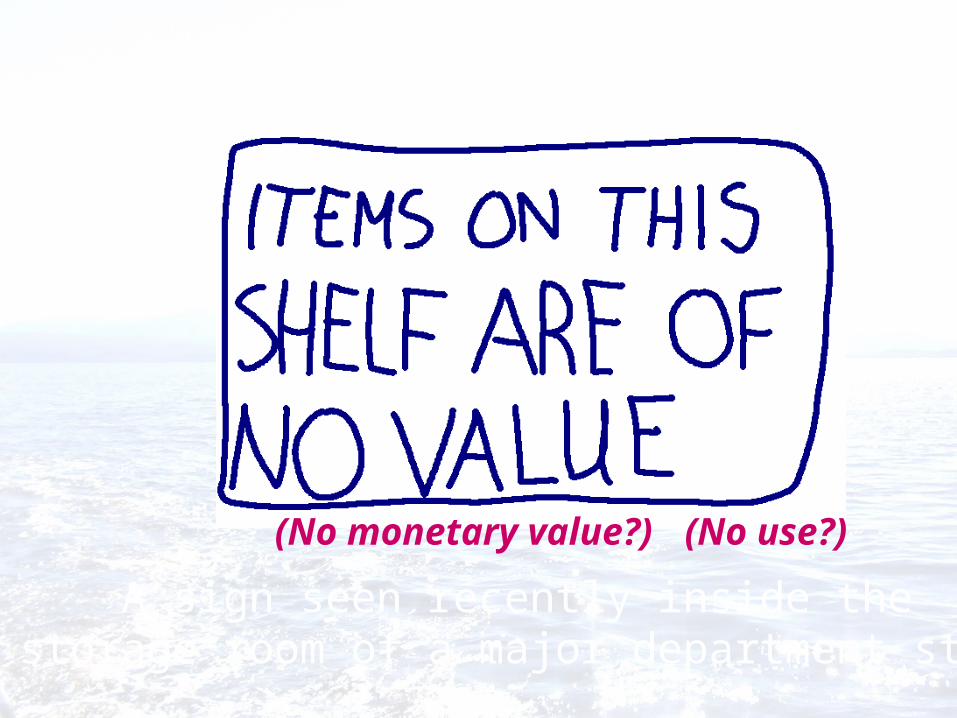

A sign seen recently inside the storage room of a major department store

(No monetary value?) (No use?)

Value for your

most valued this Mother’s Day

National Newspaper Advertisement

(Value for money)

(important one)

“Now the glass has broken, it is no longer of any value to

me” (use?)

(Benefit?)

“Having a shopping centre so close is of great value to

us” (Benefit?)

(use?)

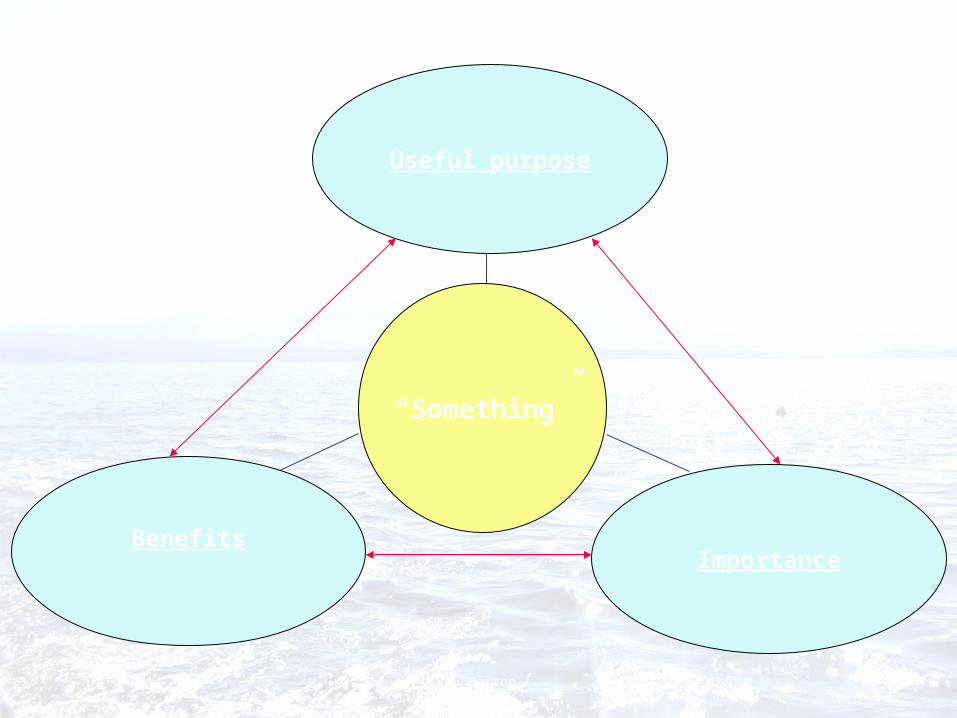

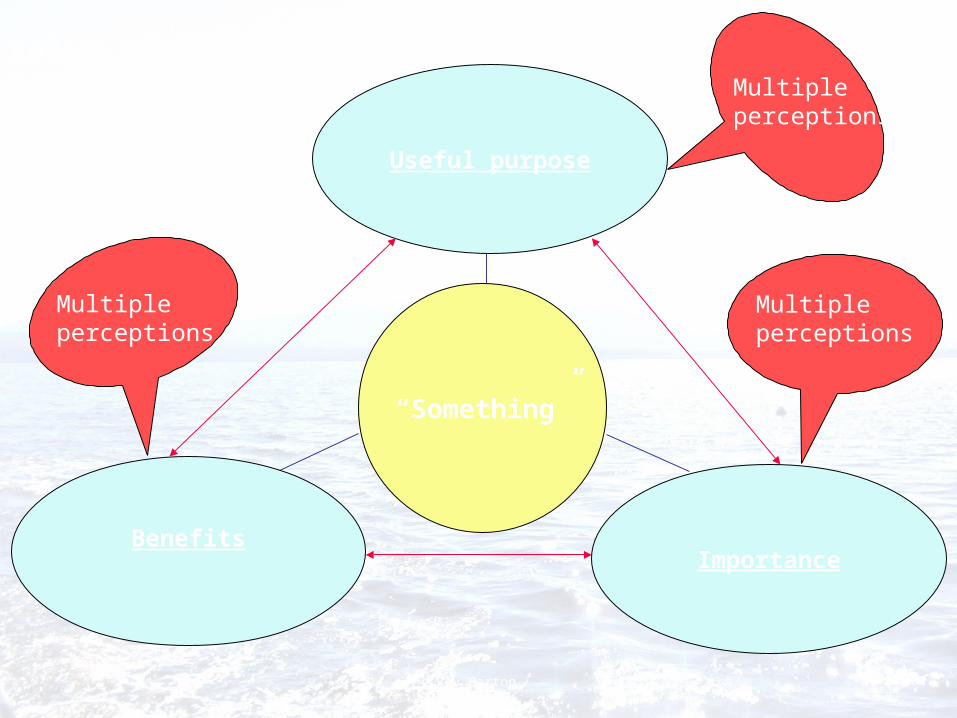

“Something”

Useful purpose

Value of “something”

BenefitsImportance

© Roy Barton 2004

“Something”

Useful purpose

Value of “something”

BenefitsImportance

© Roy Barton 2004

Multiple perceptions

Multiple perceptions

Multiple perceptions

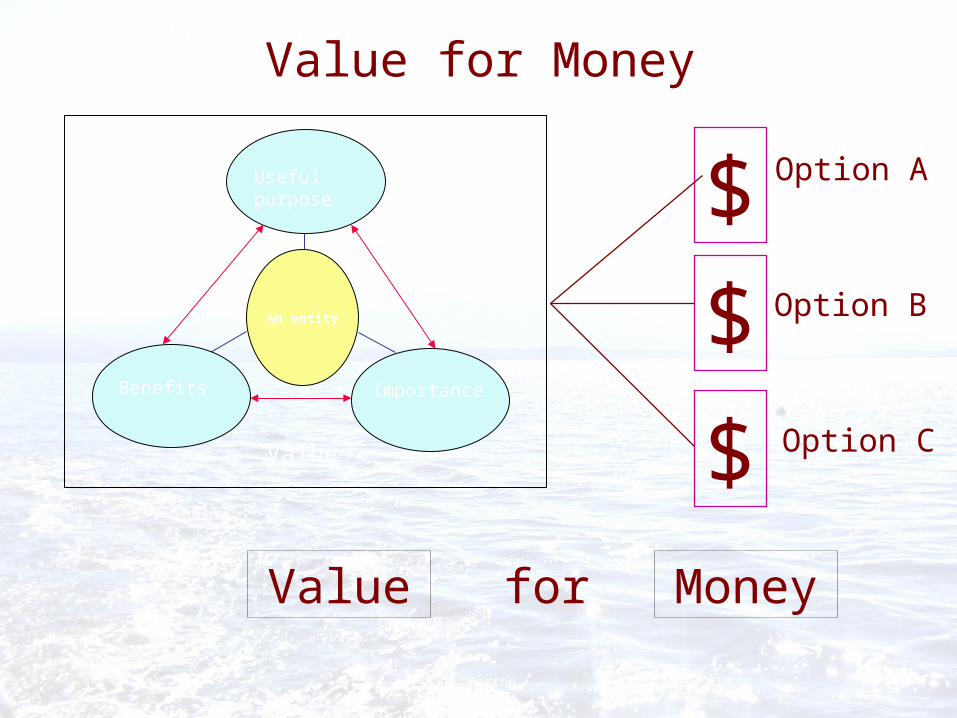

Value for Money

$

$

$ Option A

Option C

Option B

Value Moneyfor

An entity

Useful purpose

Benefits Importance

Value

© Roy Barton 2004

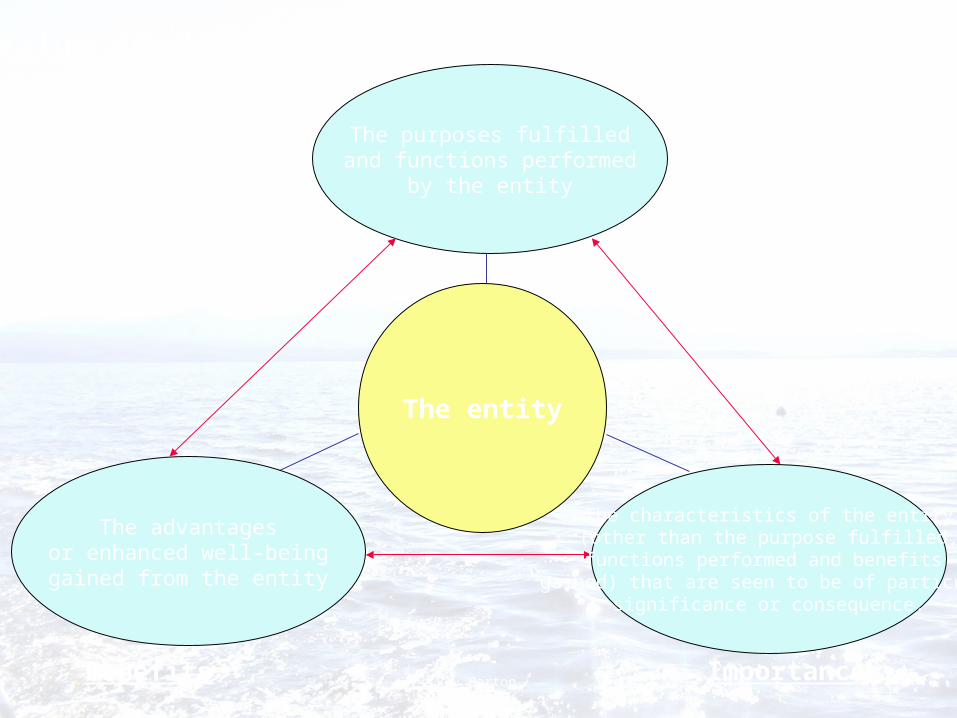

The entity

The purposes fulfilledand functions performed

by the entity

Benefits Importance

UsefulnessValue of an entity

The advantagesor enhanced well-beinggained from the entity

The characteristics of the entity (other than the purpose fulfilled, functions performed and benefits

gained) that are seen to be of particularsignificance or consequence.

© Roy Barton 2004

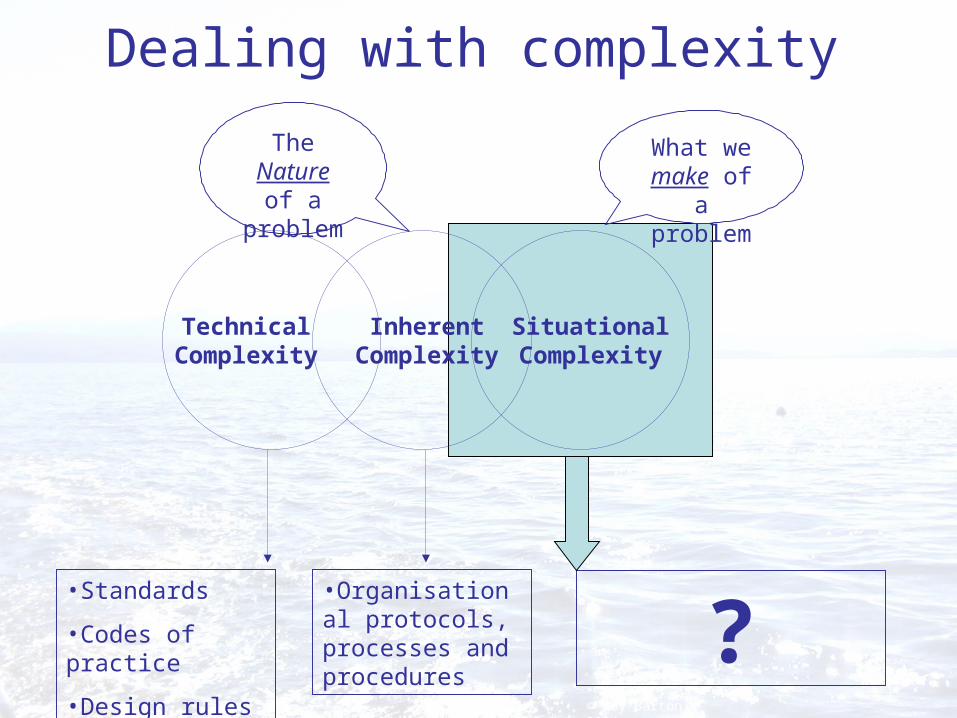

Dealing with complexity

InherentComplexity

TechnicalComplexity

SituationalComplexity

•Standards

•Codes of practice

•Design rules?

•Organisational protocols, processes and procedures

The Nature of a problem

What we make of a problem

© Roy Barton 2004

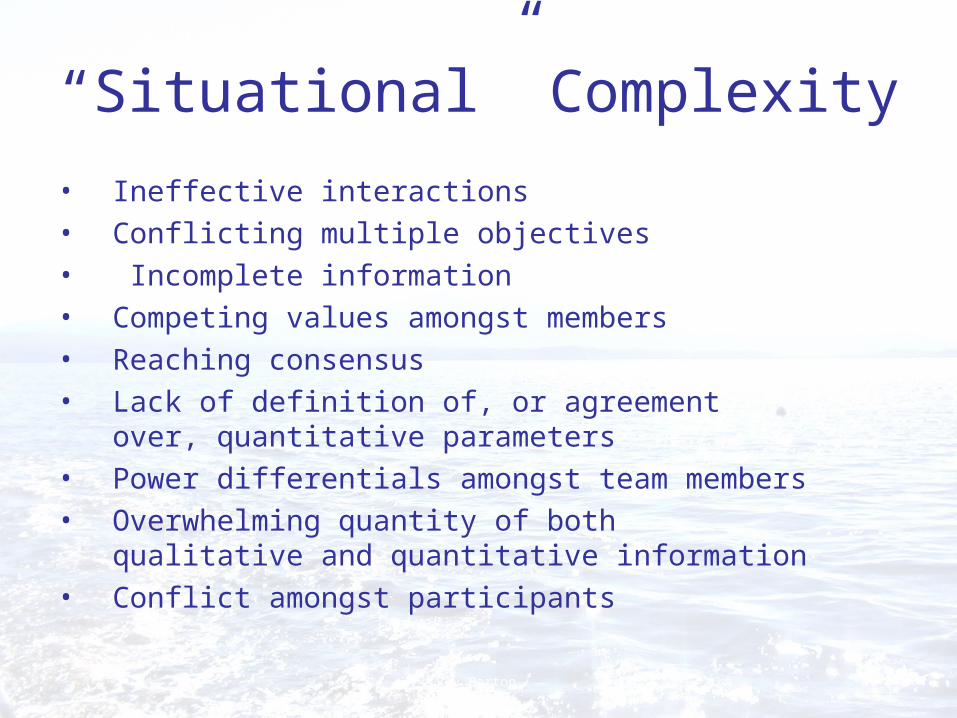

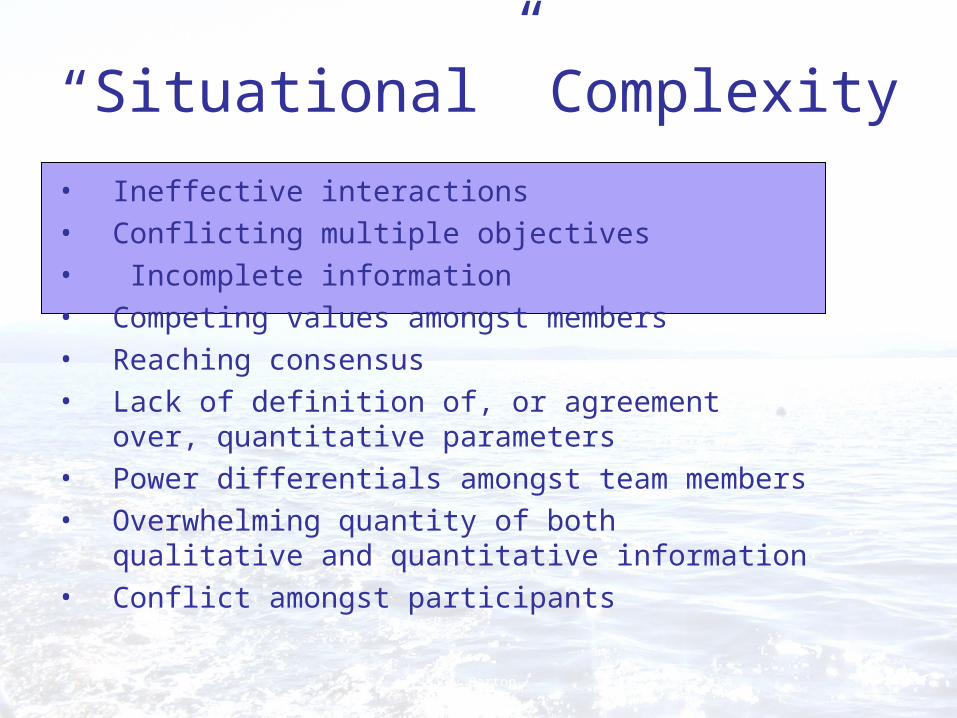

“Situational” Complexity

• Ineffective interactions• Conflicting multiple objectives• Incomplete information• Competing values amongst members• Reaching consensus• Lack of definition of, or agreement over,

quantitative parameters • Power differentials amongst team members• Overwhelming quantity of both qualitative and

quantitative information• Conflict amongst participants

© Roy Barton 2004

“Situational” Complexity

• Ineffective interactions• Conflicting multiple objectives• Incomplete information• Competing values amongst members• Reaching consensus• Lack of definition of, or agreement over,

quantitative parameters • Power differentials amongst team members• Overwhelming quantity of both qualitative and

quantitative information• Conflict amongst participants

© Roy Barton 2004

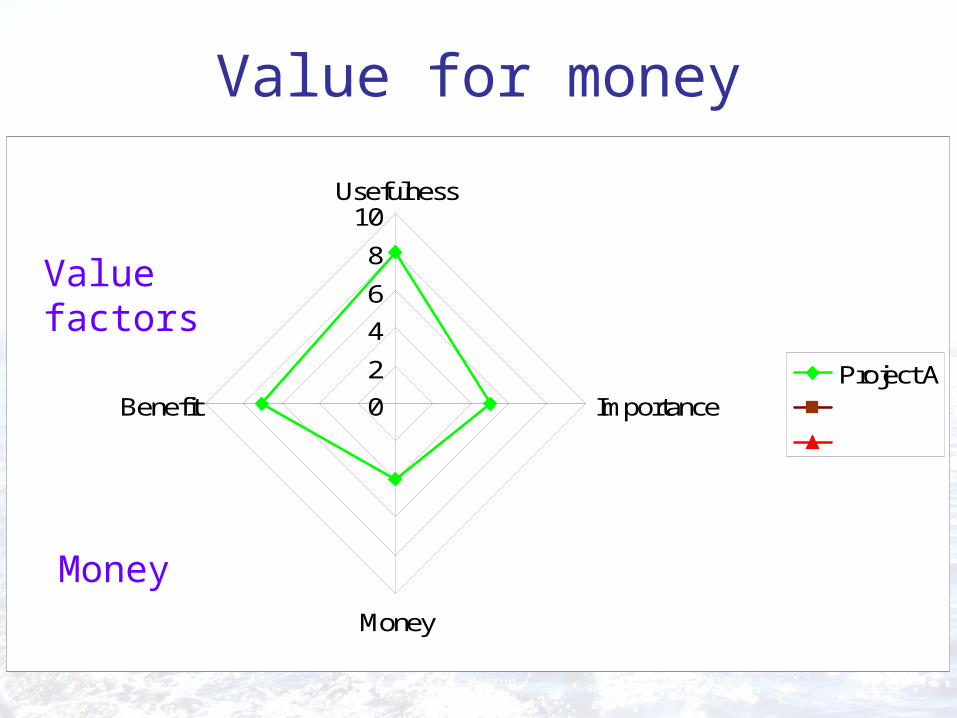

0

2

4

6

8

10Usefulness

Importance

Money

BenefitProject A

Value factors

Money

Value for money

© Roy Barton 2004

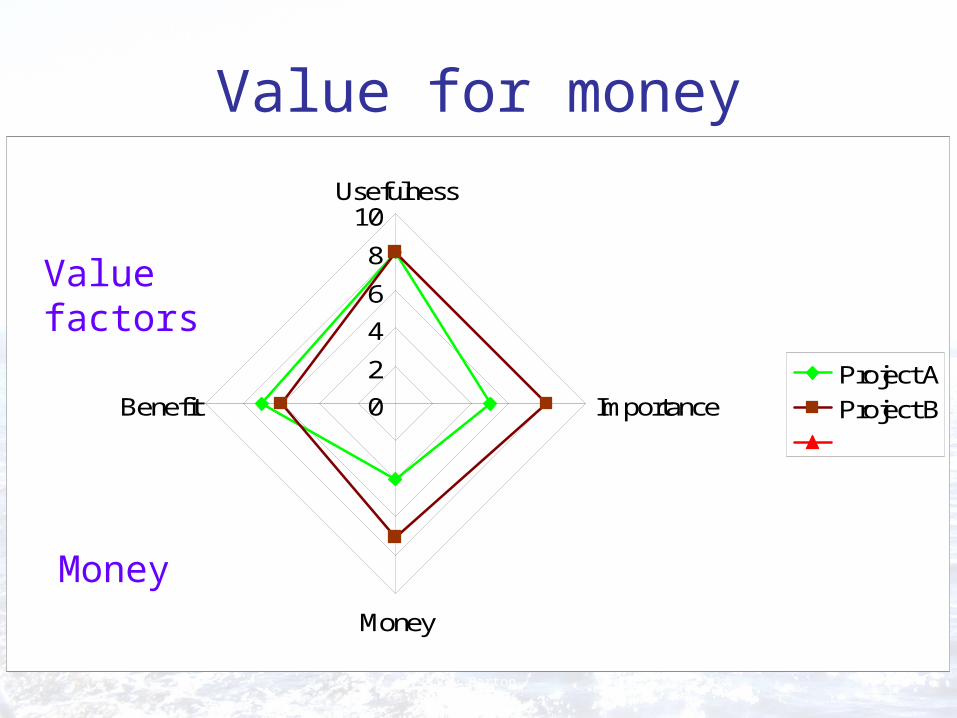

0

2

4

6

8

10Usefulness

Importance

Money

BenefitProject A

Project B

Value factors

Money

Value for money

© Roy Barton 2004

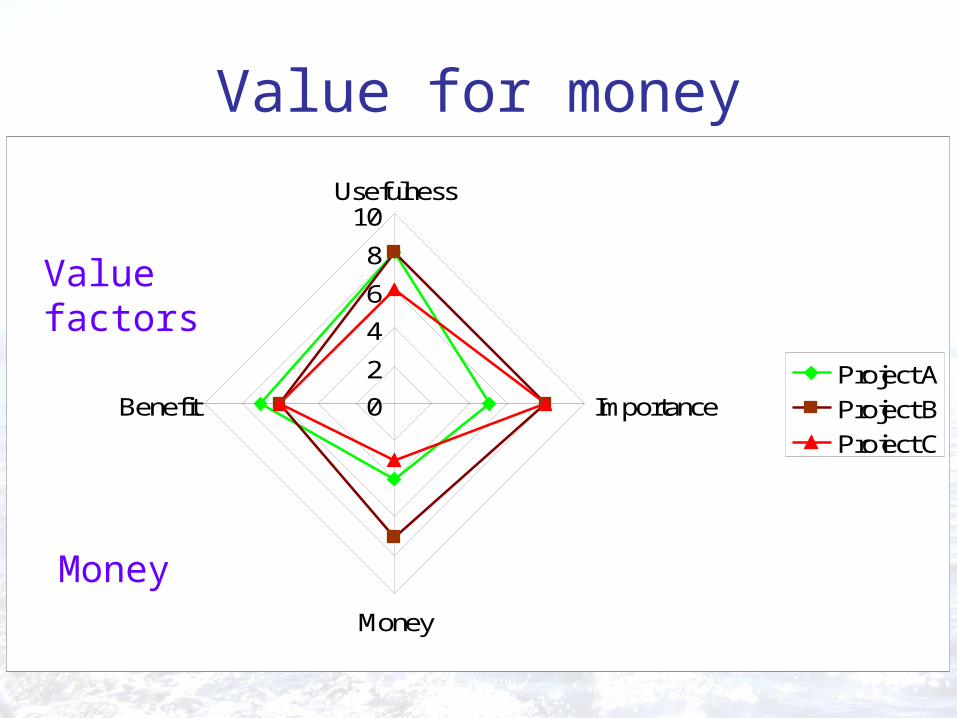

0

2

4

6

8

10Usefulness

Importance

Money

BenefitProject A

Project B

Project C

Value factors

Money

Value for money

© Roy Barton 2004

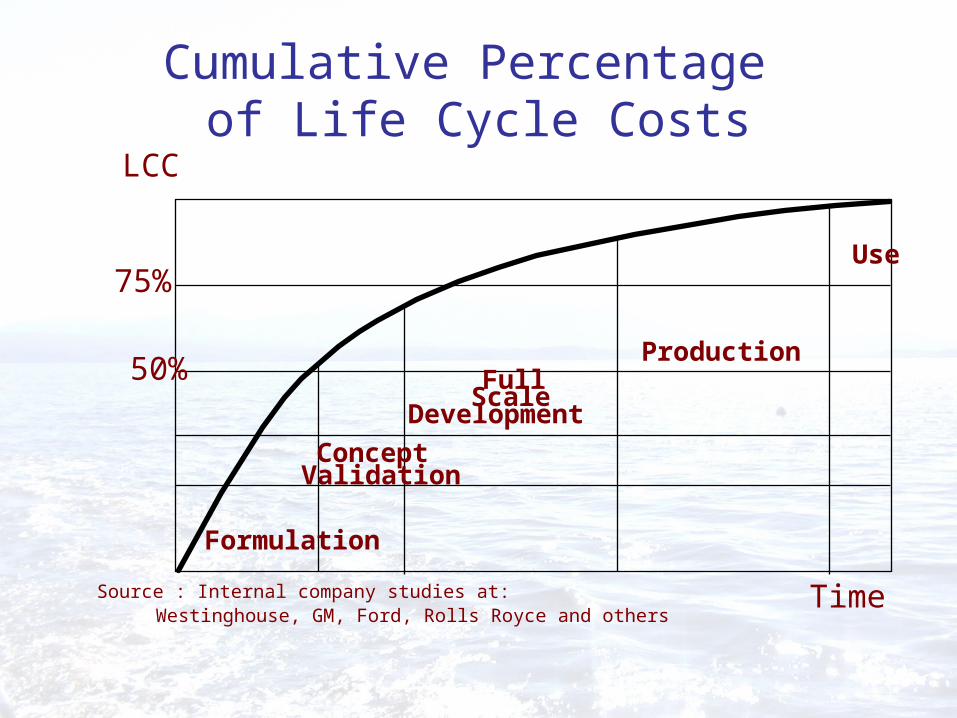

Formulation

Validation

FullDevelopment

Scale

Production

Use

Source : Internal company studies at:Westinghouse, GM, Ford, Rolls Royce and others

Concept

50%

75%

Cumulative Percentage of Life Cycle Costs

LCC

Time

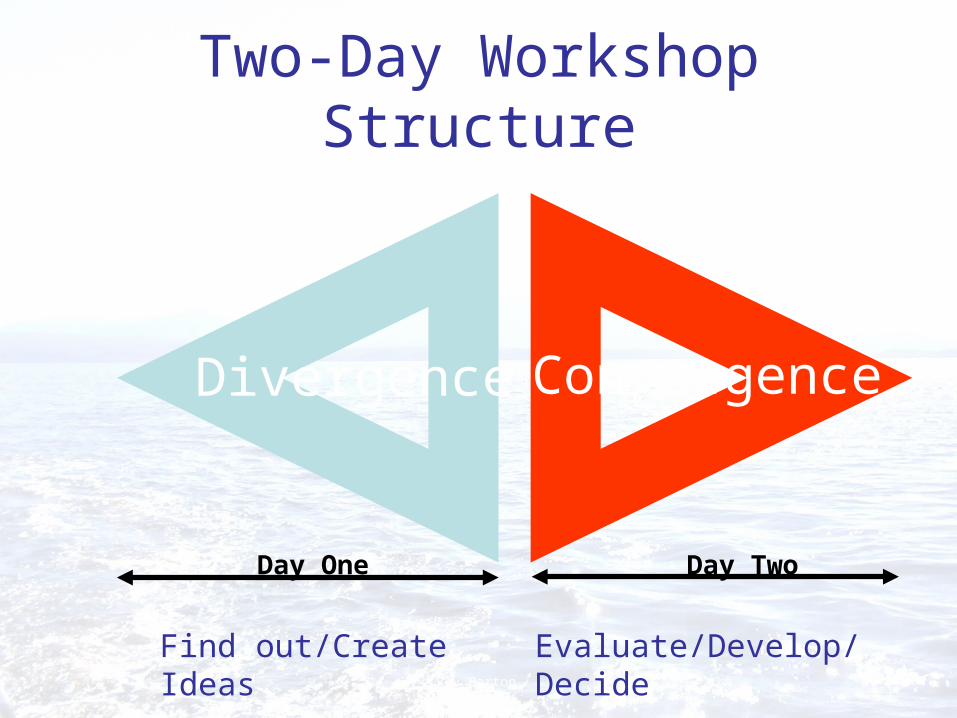

Two-Day Workshop Structure

Divergence Convergence

Day One Day Two

Find out/Create Ideas

Evaluate/Develop/Decide© Roy Barton 2004

VM Workshop

© Roy Barton 2004

VM WorkshopMedical specialists and practitioners

New definitions

Value• An attribute of an entity determined by the entity's

perceived usefulness, benefit and importance.Value for money• A measure used for comparing alternatives based on the

relationship between value and total cost.Value Management• A structured and analytical process which follows a

prescribed Work plan to achieve best value and, where appropriate, best value for money.

Contact details

• Lex Clark– [email protected]– 02 6287 4018

• Roy Barton– [email protected]– 0411 765 001

![[4183]-101€¦ · [4183]-101 B. Sc. (Hospitality Studies) (Semester-I) Examination - 2012 ... Butler Service and English Service (c) A’la Carte and Table d’hôte (B) State the](https://img.pdfslide.us/doc/110x75/5ec0d0fdffc5a904576bb377/4183-4183-101-b-sc-hospitality-studies-semester-i-examination-2012.jpg)