Embed Size (px)

Citation preview

0

«Engineering Retail»

MAY 2015 – LONDON VISIT

1

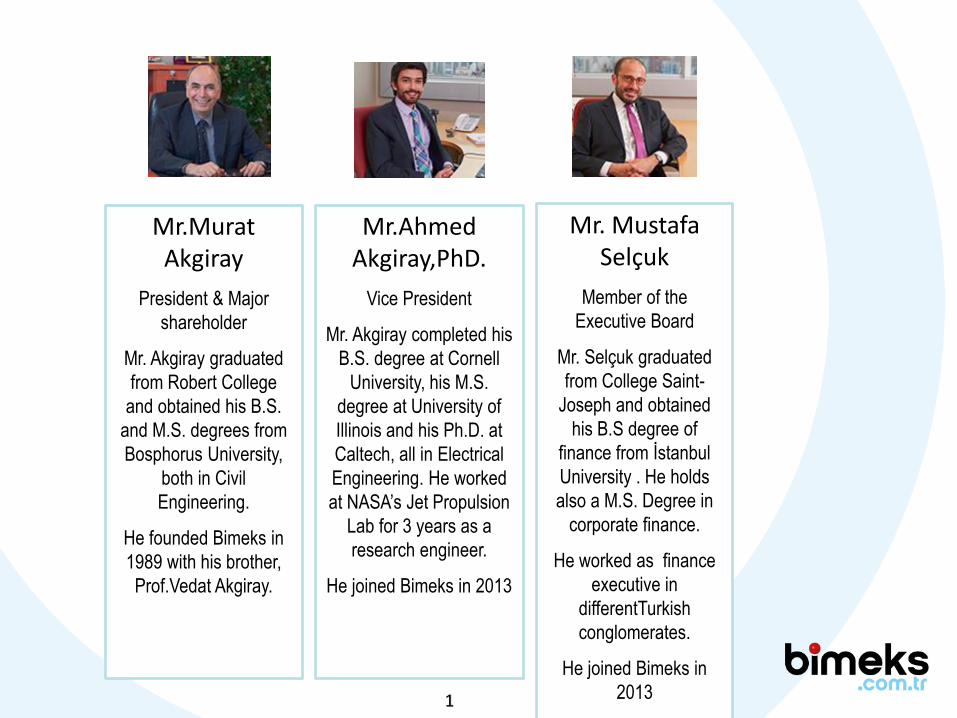

Mr.Murat Akgiray

President & Major

shareholder

Mr. Akgiray graduated

from Robert College

and obtained his B.S.

and M.S. degrees from

Bosphorus University,

both in Civil

Engineering.

He founded Bimeks in

1989 with his brother,

Prof.Vedat Akgiray.

Mr. Mustafa Selçuk

Member of the

Executive Board

Mr. Selçuk graduated

from College Saint-

Joseph and obtained

his B.S degree of

finance from İstanbul

University . He holds

also a M.S. Degree in

corporate finance.

He worked as finance

executive in

differentTurkish

conglomerates.

He joined Bimeks in

2013

Mr.Ahmed Akgiray,PhD.

Vice President

Mr. Akgiray completed his

B.S. degree at Cornell

University, his M.S.

degree at University of

Illinois and his Ph.D. at

Caltech, all in Electrical

Engineering. He worked

at NASA’s Jet Propulsion

Lab for 3 years as a

research engineer.

He joined Bimeks in 2013

2

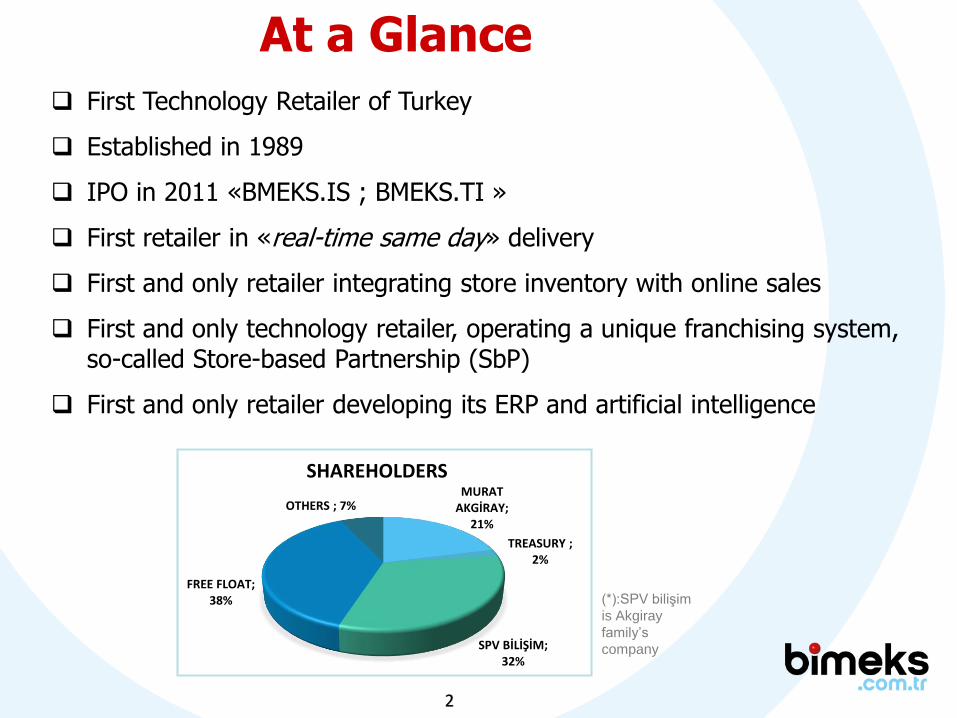

At a Glance

First Technology Retailer of Turkey

Established in 1989

IPO in 2011 «BMEKS.IS ; BMEKS.TI »

First retailer in «real-time same day» delivery

First and only retailer integrating store inventory with online sales

First and only technology retailer, operating a unique franchising system, so-called Store-based Partnership (SbP)

First and only retailer developing its ERP and artificial intelligence

MURAT AKGİRAY;

21%

TREASURY ; 2%

SPV BİLİŞİM; 32%

FREE FLOAT; 38%

OTHERS ; 7%

SHAREHOLDERS

(*):SPV bilişim

is Akgiray

family’s

company

3

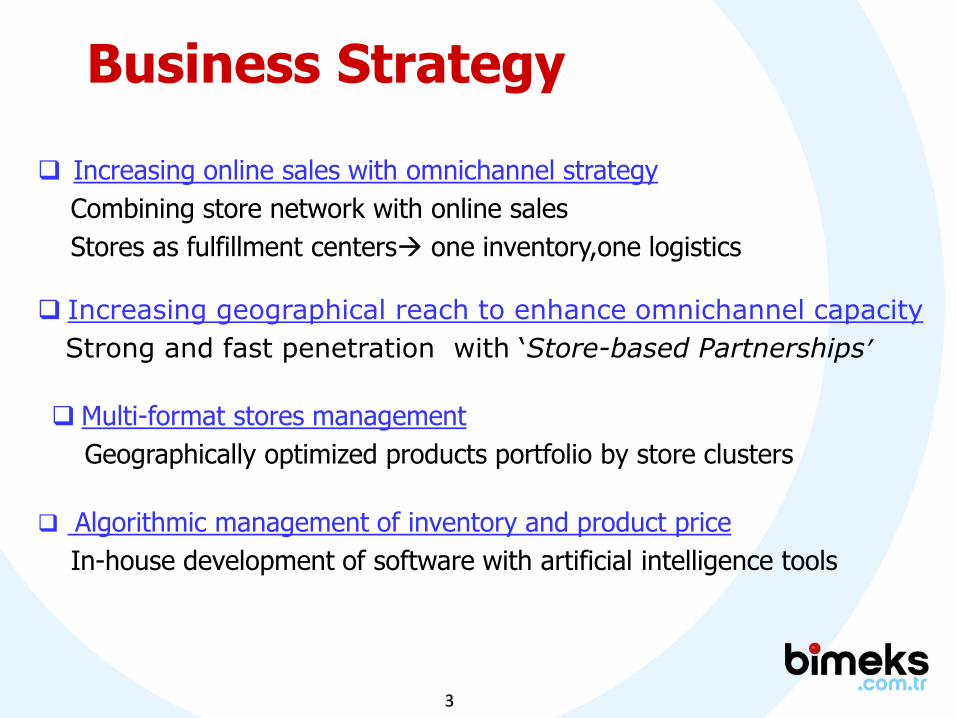

Increasing online sales with omnichannel strategy

Combining store network with online sales

Stores as fulfillment centers one inventory,one logistics

Increasing geographical reach to enhance omnichannel capacity

Strong and fast penetration with ‘Store-based Partnerships’

Multi-format stores management

Geographically optimized products portfolio by store clusters

Business Strategy

Algorithmic management of inventory and product price

In-house development of software with artificial intelligence tools

4

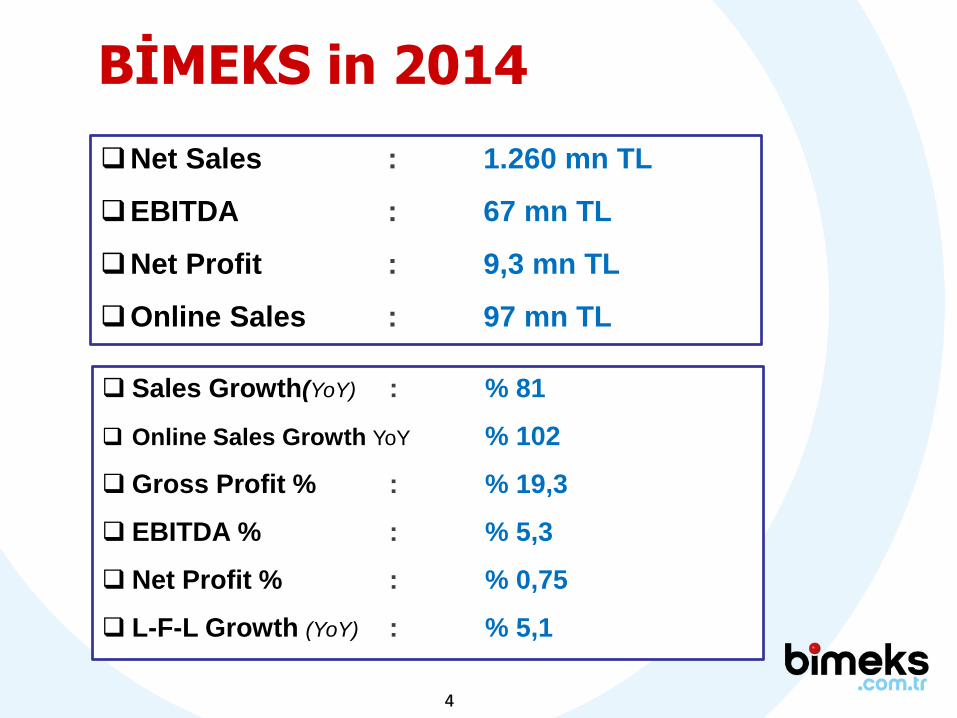

Net Sales : 1.260 mn TL

EBITDA : 67 mn TL

Net Profit : 9,3 mn TL

Online Sales : 97 mn TL

Sales Growth(YoY) : % 81

Online Sales Growth YoY % 102

Gross Profit % : % 19,3

EBITDA % : % 5,3

Net Profit % : % 0,75

L-F-L Growth (YoY) : % 5,1

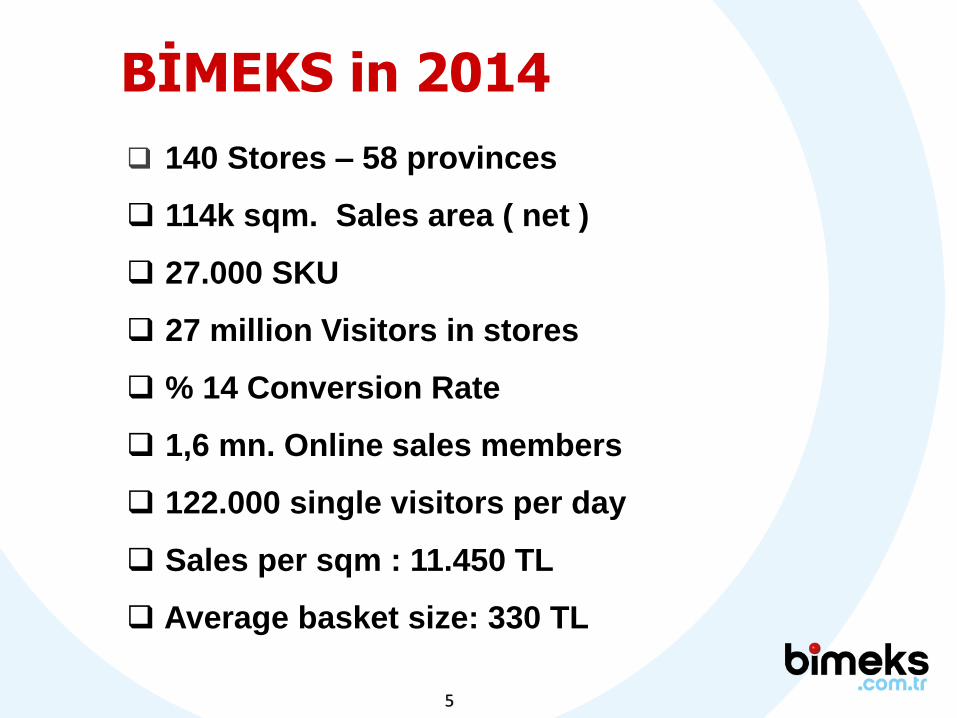

BİMEKS in 2014

5

140 Stores – 58 provinces

114k sqm. Sales area ( net )

27.000 SKU

27 million Visitors in stores

% 14 Conversion Rate

1,6 mn. Online sales members

122.000 single visitors per day

Sales per sqm : 11.450 TL

Average basket size: 330 TL

BİMEKS in 2014

6

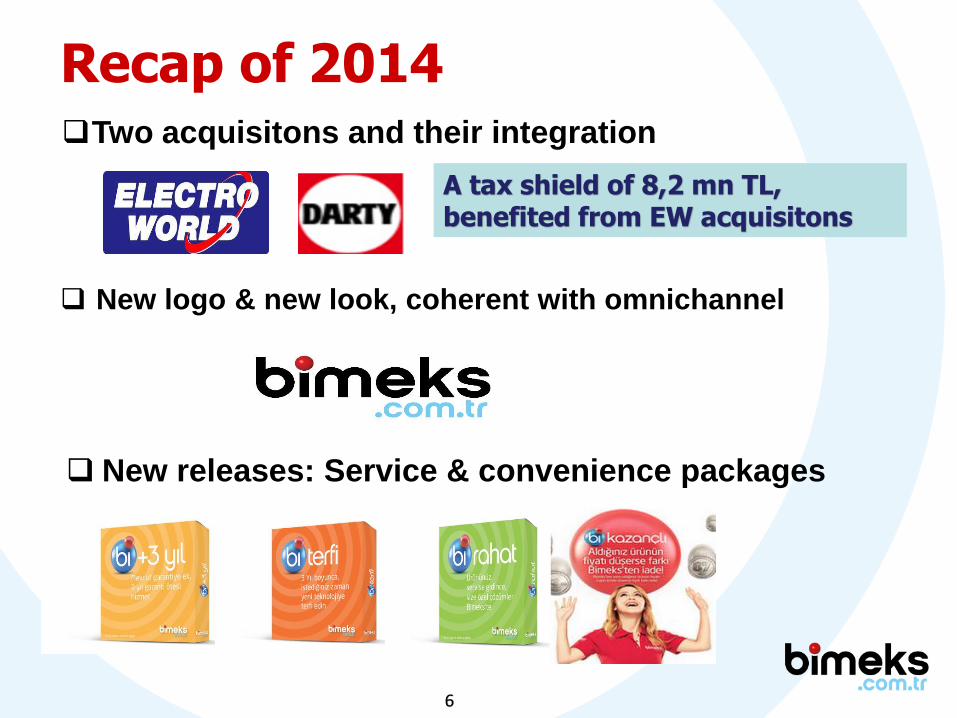

Two acquisitons and their integration

New logo & new look, coherent with omnichannel

New releases: Service & convenience packages

A tax shield of 8,2 mn TL, benefited from EW acquisitons

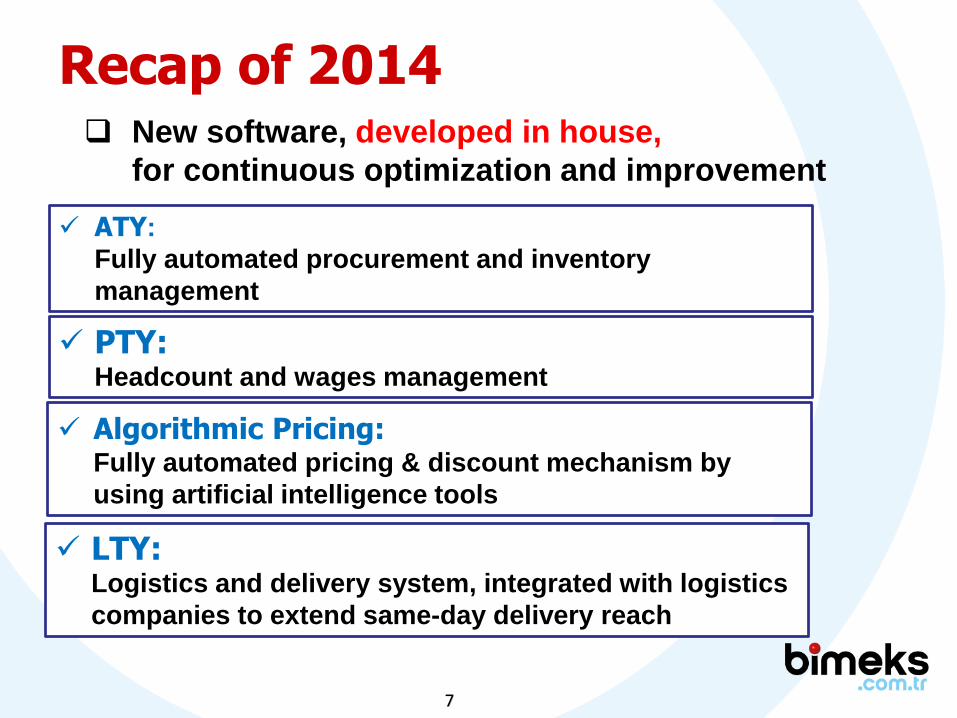

Recap of 2014

7

New software, developed in house,

for continuous optimization and improvement

ATY:

Fully automated procurement and inventory

management

PTY: Headcount and wages management

Algorithmic Pricing:Fully automated pricing & discount mechanism by

using artificial intelligence tools

LTY:Logistics and delivery system, integrated with logistics

companies to extend same-day delivery reach

Recap of 2014

8

What’s New?

Procurement & display agreement supports MDA&SDA sales

Shop-in-Shop agreement improves store costs (rental)

provides better margins

Co-sale agreement selling phones from inventory

with Vodafone contracts

selling phones from inventory

Selling soft-drinks in stores offered by Coca-Cola

valuable case study for handling/selling

non-technology & FMCG products via the Bimeks

procurement and marketing system.

Business cooperations & collaborations

9

Providing an innovative payment system to customers

First and only among technology retasilers:

powered by

payment in installments up to 24 months (with interest premium)

without requiring credit card or bank loan

secured by insurance company

What’s New?

10

What’s New?

Bimeks joined a digital and customized shopping platform:Hopi

first and only in Turkey

invented and operated by Boyner Group

vaste business members:

major retail chains,BP,Turkcell etc.

customers earn and spend virtual coins while shopping

targeted private member #

4,5 million in 2015

12 million in 2017

(*): quoted

from Hopi

corporate

presentation

11

M A R K E T

12

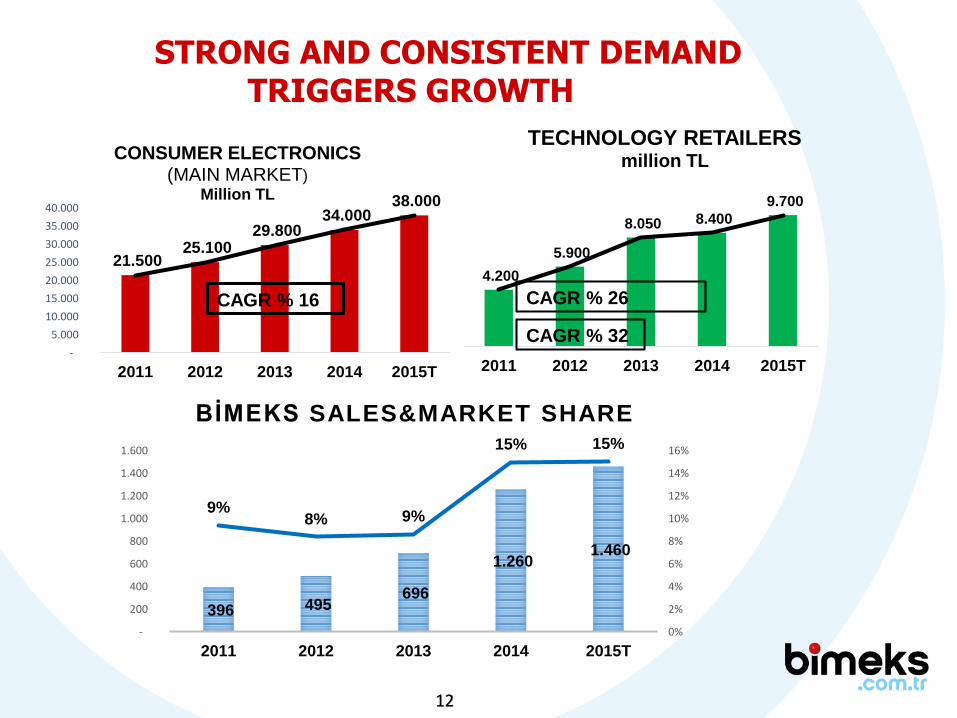

STRONG AND CONSISTENT DEMAND TRIGGERS GROWTH

396 495 696

1.260 1.460

9%8% 9%

15% 15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-

200

400

600

800

1.000

1.200

1.400

1.600

2011 2012 2013 2014 2015T

BİMEKS SALES&MARKET SHARE

21.500 25.100

29.800 34.000

38.000

-

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

2011 2012 2013 2014 2015T

CONSUMER ELECTRONICS(MAIN MARKET)

Million TL

CAGR % 16

4.200

5.900

8.050 8.400

9.700

2011 2012 2013 2014 2015T

TECHNOLOGY RETAILERSmillion TL

CAGR % 26

CAGR % 32

13

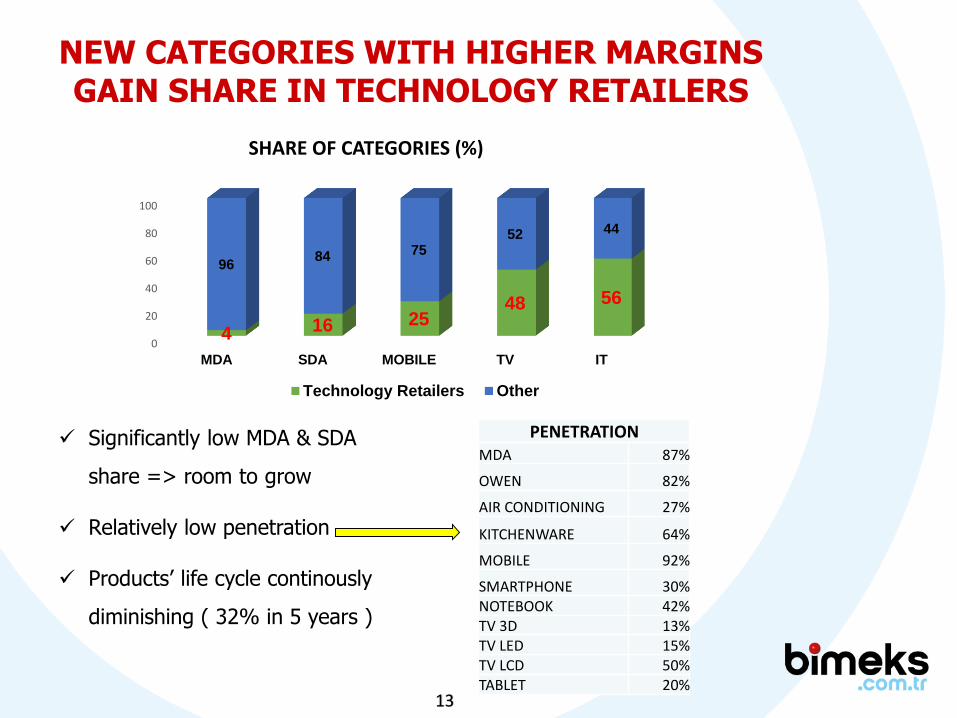

NEW CATEGORIES WITH HIGHER MARGINS GAIN SHARE IN TECHNOLOGY RETAILERS

Significantly low MDA & SDA

share => room to grow

Relatively low penetration

Products’ life cycle continously

diminishing ( 32% in 5 years )

0

20

40

60

80

100

MDA SDA MOBILE TV IT

4 16 2548 56

9684 75

52 44

SHARE OF CATEGORIES (%)

Technology Retailers Other

PENETRATIONMDA 87%

OWEN 82%

AIR CONDITIONING 27%

KITCHENWARE 64%

MOBILE 92%

SMARTPHONE 30%NOTEBOOK 42%TV 3D 13%TV LED 15%TV LCD 50%TABLET 20%

14

FINANCIALS

15

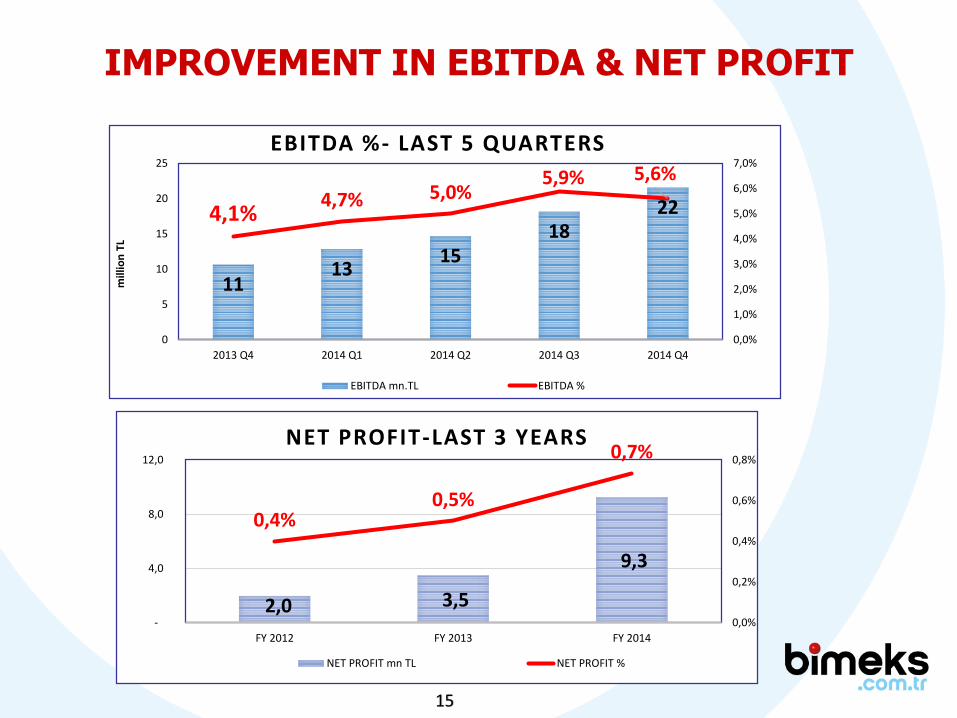

2,0 3,5

9,3

0,4%0,5%

0,7%

0,0%

0,2%

0,4%

0,6%

0,8%

-

4,0

8,0

12,0

FY 2012 FY 2013 FY 2014

NET PROFIT-LAST 3 YEARS

NET PROFIT mn TL NET PROFIT %

IMPROVEMENT IN EBITDA & NET PROFIT

1113

1518

224,1%4,7% 5,0%

5,9% 5,6%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

0

5

10

15

20

25

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

mill

ion

TL

EBITDA %- LAST 5 QUARTERS

EBITDA mn.TL EBITDA %

16

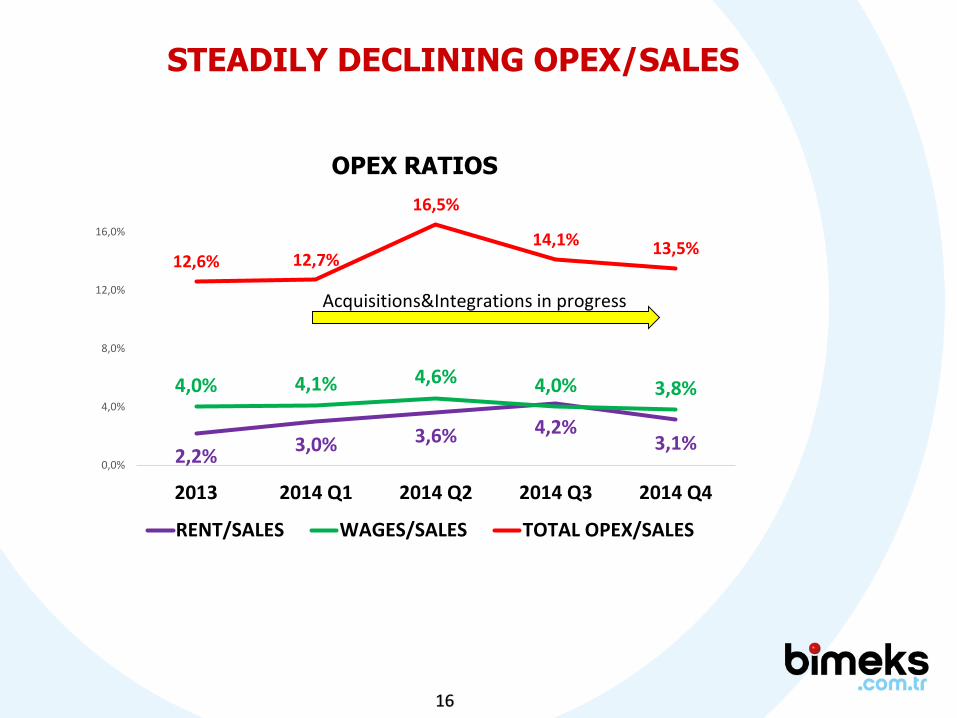

STEADILY DECLINING OPEX/SALES

2,2%3,0% 3,6% 4,2%

3,1%

4,0% 4,1% 4,6% 4,0% 3,8%

12,6% 12,7%

16,5%

14,1% 13,5%

0,0%

4,0%

8,0%

12,0%

16,0%

2013 2014 Q1 2014 Q2 2014 Q3 2014 Q4

OPEX RATIOS

RENT/SALES WAGES/SALES TOTAL OPEX/SALES

Acquisitions&Integrations in progress

17

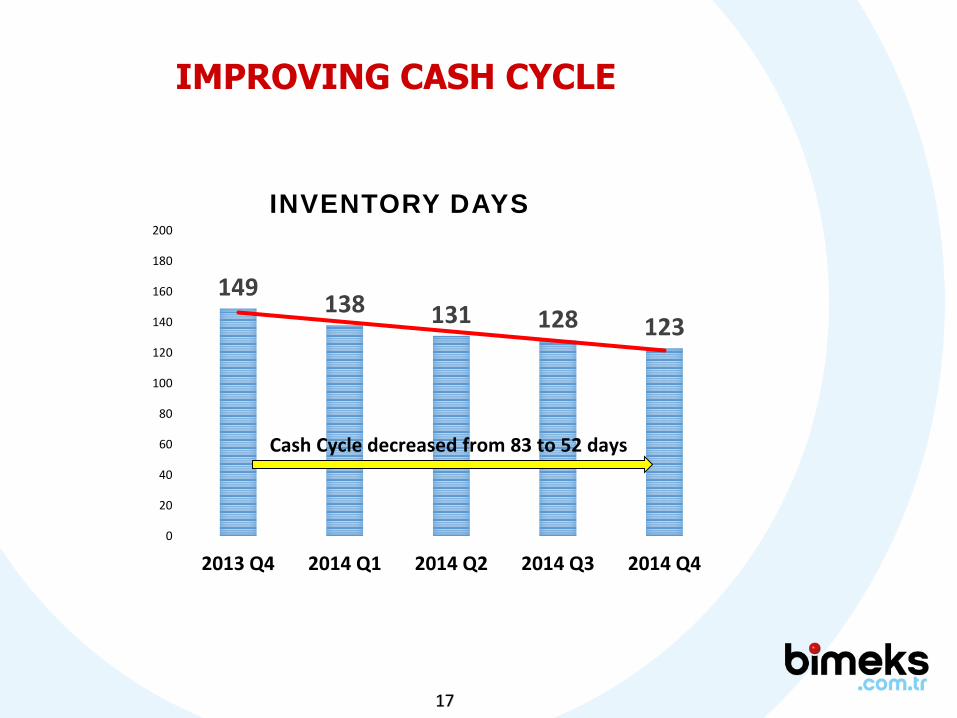

149138 131 128 123

0

20

40

60

80

100

120

140

160

180

200

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

INVENTORY DAYS

Cash Cycle decreased from 83 to 52 days

IMPROVING CASH CYCLE

18

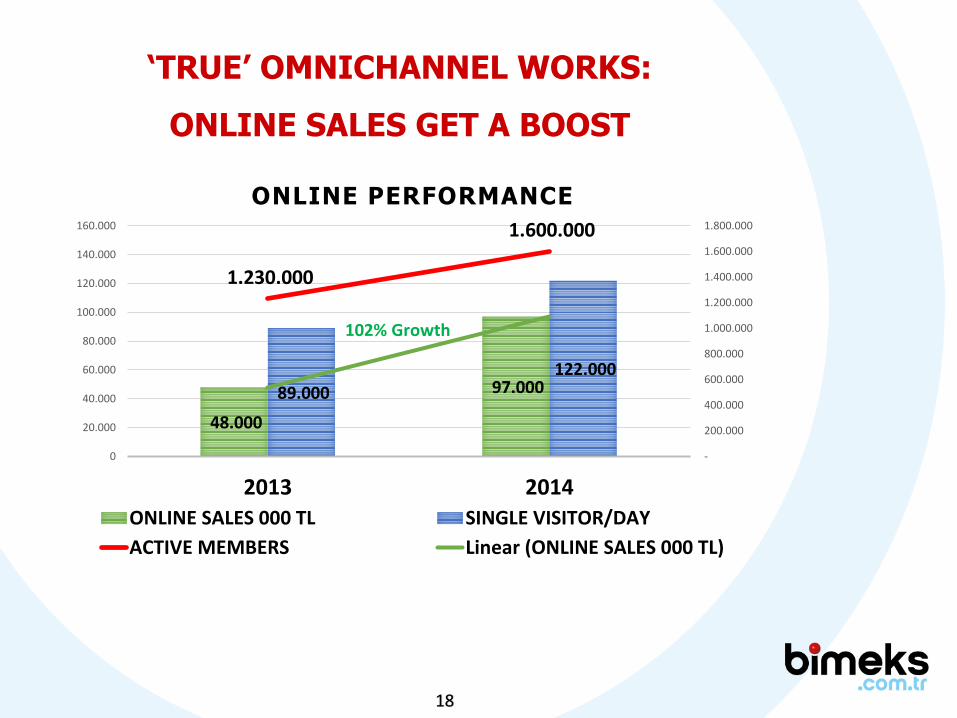

‘TRUE’ OMNICHANNEL WORKS:

ONLINE SALES GET A BOOST

48.000

97.000 89.000

122.000

1.230.000

1.600.000

-

200.000

400.000

600.000

800.000

1.000.000

1.200.000

1.400.000

1.600.000

1.800.000

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

160.000

2013 2014

ONLINE PERFORMANCE

ONLINE SALES 000 TL SINGLE VISITOR/DAY

ACTIVE MEMBERS Linear (ONLINE SALES 000 TL)

102% Growth

19

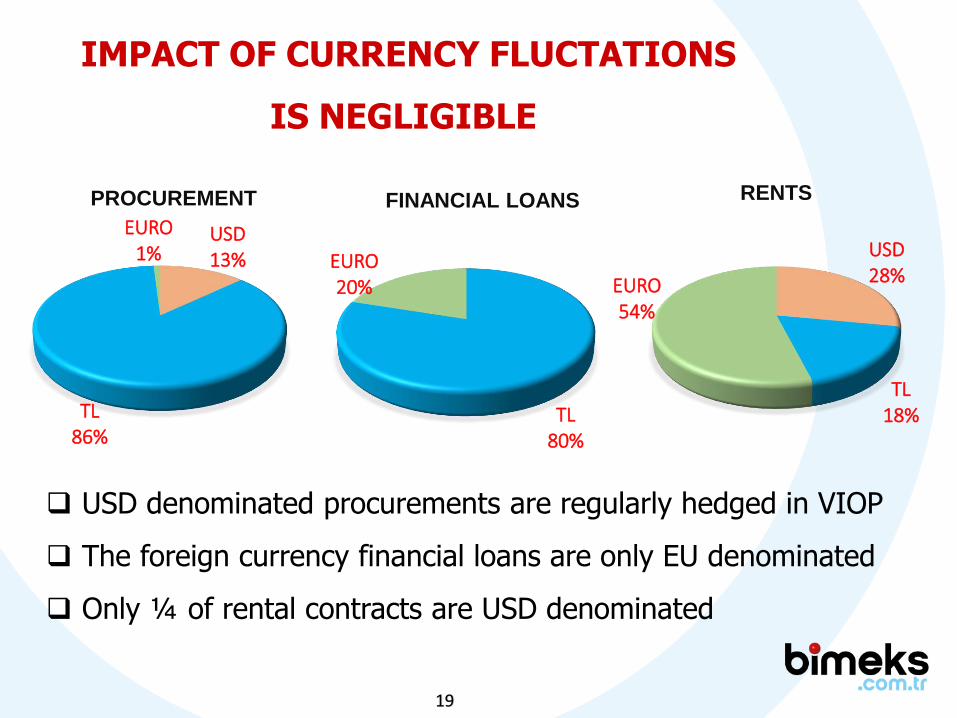

IMPACT OF CURRENCY FLUCTATIONS

IS NEGLIGIBLE

USD denominated procurements are regularly hedged in VIOP

The foreign currency financial loans are only EU denominated

Only ¼ of rental contracts are USD denominated

TL80%

EURO20%

FINANCIAL LOANS

USD13%

TL86%

EURO1%

PROCUREMENT

USD28%

TL18%

EURO54%

RENTS

20

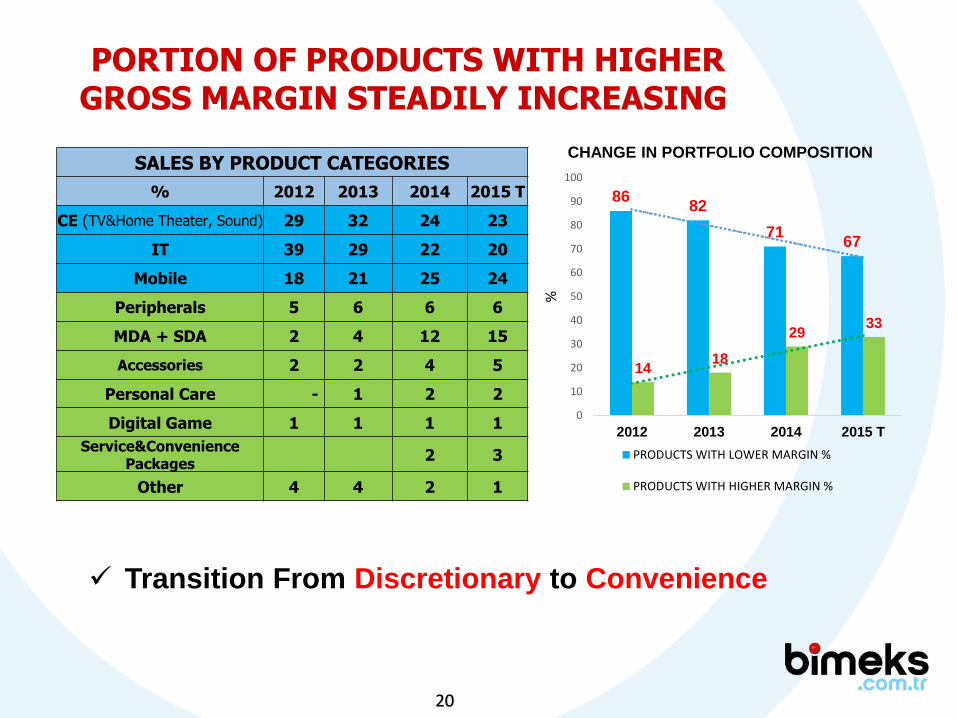

PORTION OF PRODUCTS WITH HIGHER GROSS MARGIN STEADILY INCREASING

Transition From Discretionary to Convenience

SALES BY PRODUCT CATEGORIES

% 2012 2013 2014 2015 T

CE (TV&Home Theater, Sound) 29 32 24 23

IT 39 29 22 20

Mobile 18 21 25 24

Peripherals 5 6 6 6

MDA + SDA 2 4 12 15

Accessories 2 2 4 5

Personal Care - 1 2 2

Digital Game 1 1 1 1

Service&Convenience Packages

2 3

Other 4 4 2 1

8682

7167

1418

2933

0

10

20

30

40

50

60

70

80

90

100

2012 2013 2014 2015 T

%

CHANGE IN PORTFOLIO COMPOSITION

PRODUCTS WITH LOWER MARGIN %

PRODUCTS WITH HIGHER MARGIN %

21

1Q 2015

FINANCIAL RESULTS

22

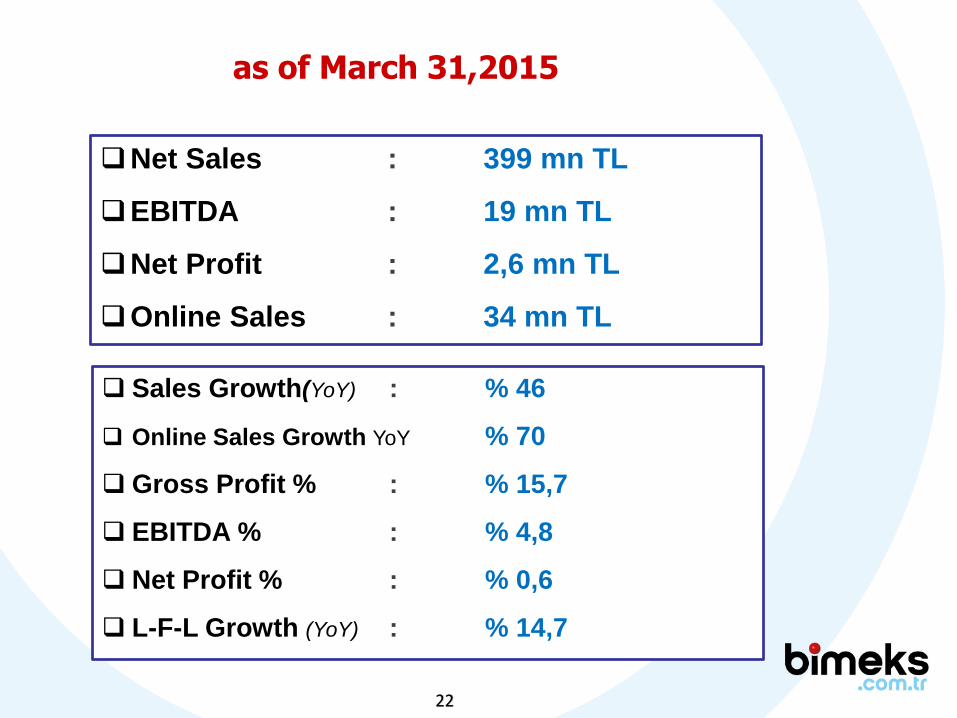

Net Sales : 399 mn TL

EBITDA : 19 mn TL

Net Profit : 2,6 mn TL

Online Sales : 34 mn TL

Sales Growth(YoY) : % 46

Online Sales Growth YoY % 70

Gross Profit % : % 15,7

EBITDA % : % 4,8

Net Profit % : % 0,6

L-F-L Growth (YoY) : % 14,7

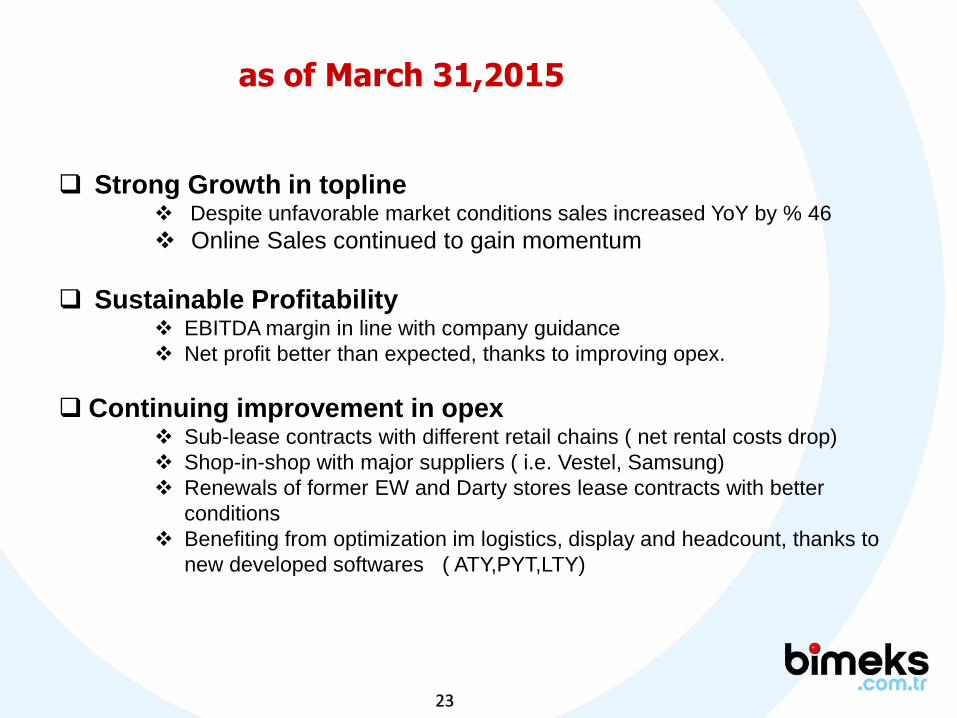

as of March 31,2015

23

as of March 31,2015

Strong Growth in topline Despite unfavorable market conditions sales increased YoY by % 46

Online Sales continued to gain momentum

Sustainable Profitability EBITDA margin in line with company guidance

Net profit better than expected, thanks to improving opex.

Continuing improvement in opex Sub-lease contracts with different retail chains ( net rental costs drop)

Shop-in-shop with major suppliers ( i.e. Vestel, Samsung)

Renewals of former EW and Darty stores lease contracts with better

conditions

Benefiting from optimization im logistics, display and headcount, thanks to

new developed softwares ( ATY,PYT,LTY)

24

2015-2017 GUIDANCE

25

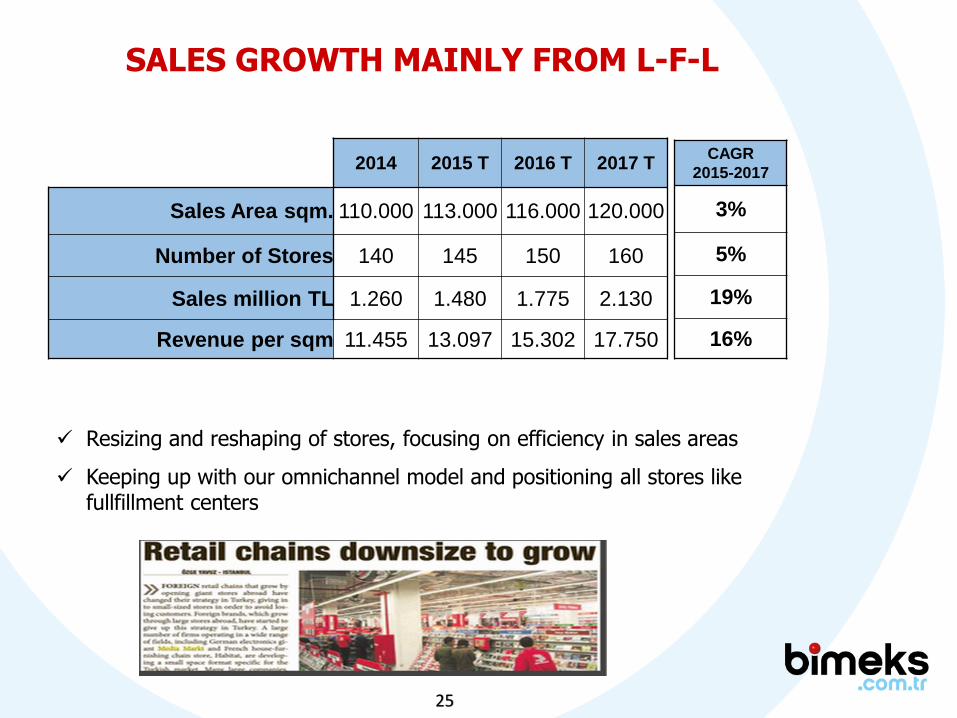

2014 2015 T 2016 T 2017 T

Sales Area sqm. 110.000 113.000 116.000 120.000

Number of Stores 140 145 150 160

Sales million TL 1.260 1.480 1.775 2.130

Revenue per sqm 11.455 13.097 15.302 17.750

CAGR

2015-2017

3%

5%

19%

16%

SALES GROWTH MAINLY FROM L-F-L

Resizing and reshaping of stores, focusing on efficiency in sales areas

Keeping up with our omnichannel model and positioning all stores like fullfillment centers

26

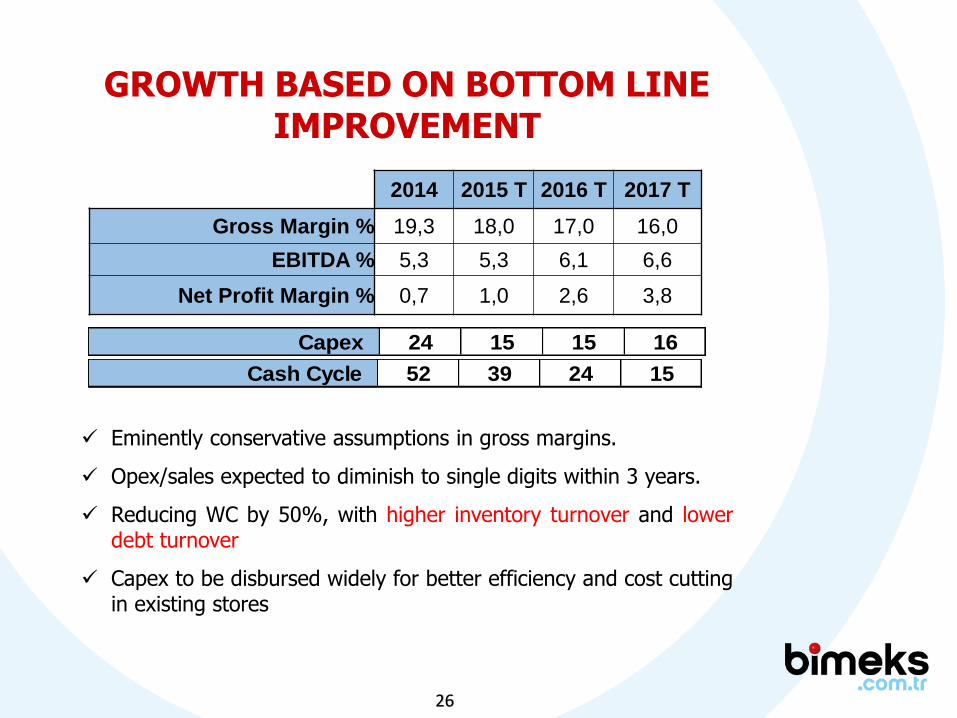

GROWTH BASED ON BOTTOM LINE IMPROVEMENT

Eminently conservative assumptions in gross margins.

Opex/sales expected to diminish to single digits within 3 years.

Reducing WC by 50%, with higher inventory turnover and lowerdebt turnover

Capex to be disbursed widely for better efficiency and cost cuttingin existing stores

2014 2015 T 2016 T 2017 T

Gross Margin % 19,3 18,0 17,0 16,0

EBITDA % 5,3 5,3 6,1 6,6

Net Profit Margin % 0,7 1,0 2,6 3,8

Capex 24 15 15 16

Cash Cycle 52 39 24 15

27

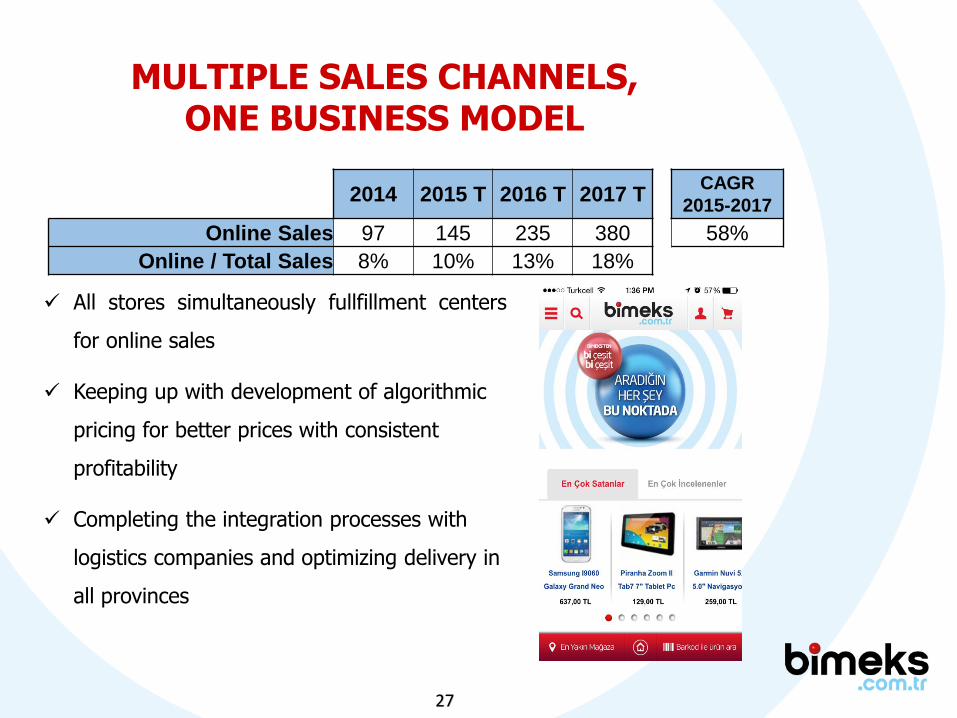

MULTIPLE SALES CHANNELS, ONE BUSINESS MODEL

All stores simultaneously fullfillment centers

for online sales

Keeping up with development of algorithmic

pricing for better prices with consistent

profitability

Completing the integration processes with

logistics companies and optimizing delivery in

all provinces

2014 2015 T 2016 T 2017 TCAGR

2015-2017

Online Sales 97 145 235 380 58%

Online / Total Sales 8% 10% 13% 18%

28

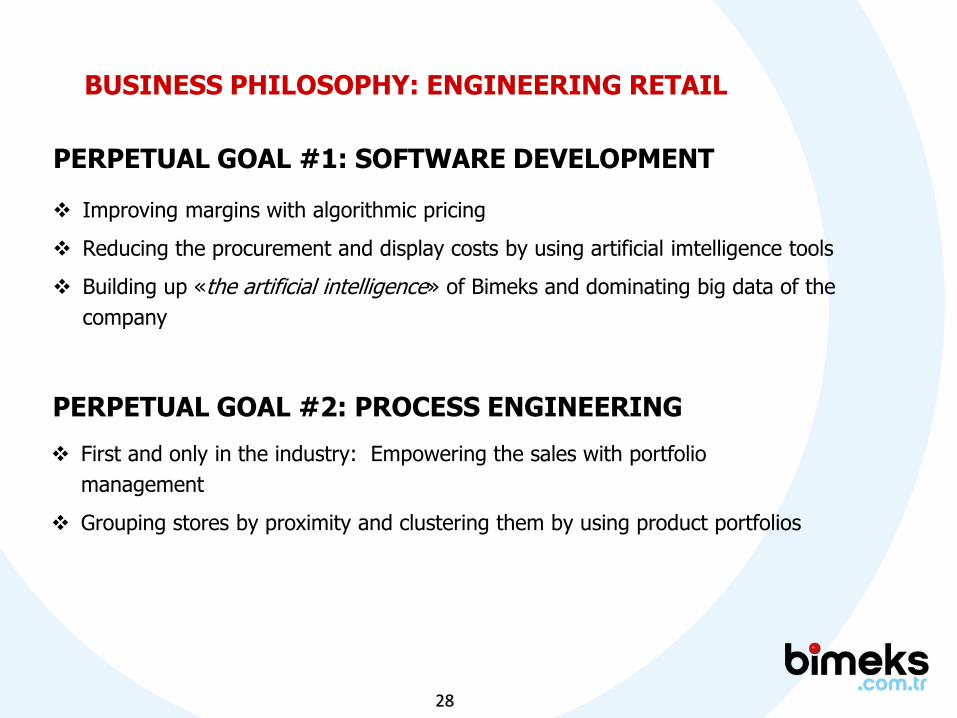

Improving margins with algorithmic pricing

Reducing the procurement and display costs by using artificial imtelligence tools

Building up «the artificial intelligence» of Bimeks and dominating big data of the

company

PERPETUAL GOAL #1: SOFTWARE DEVELOPMENT

PERPETUAL GOAL #2: PROCESS ENGINEERING

First and only in the industry: Empowering the sales with portfolio

management

Grouping stores by proximity and clustering them by using product portfolios

BUSINESS PHILOSOPHY: ENGINEERING RETAIL

29

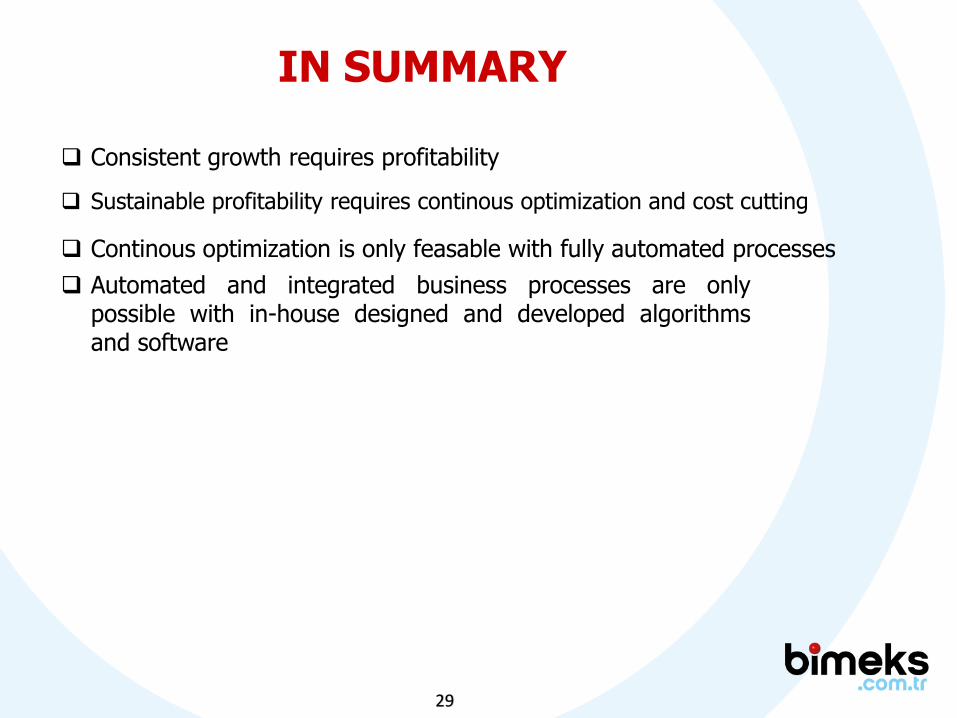

IN SUMMARY

Consistent growth requires profitability

Sustainable profitability requires continous optimization and cost cutting

Continous optimization is only feasable with fully automated processes

Automated and integrated business processes are onlypossible with in-house designed and developed algorithmsand software

30

For a complete listing of presentations and coverage reports of the company:

investor.bimeks.com.tr