Embed Size (px)

Citation preview

Engineering Economy

IEN255 Chapter 8 - Taxes

Agenda

Net Income

Corporate Income Taxes

Gains and Losses

Tax Rate in Economic Analysis

Engineering Economy

Net Income

Profit vs Loss

Revenue - Income earned as a result of providing products or services

Expense - incurred as you do business

Depreciation Expense Capital expenditures must be capitalized

Engineering Economy

Taxable Income and Income Taxes

Taxable Income = Gross Income (revenues) - expenses

Income Taxes = (Tax Rate) x (Taxable Income)

Voila!!!

Net Income = Taxable Income - Income Taxes

Engineering Economy

Example 8.1

only the table on 415

Engineering Economy

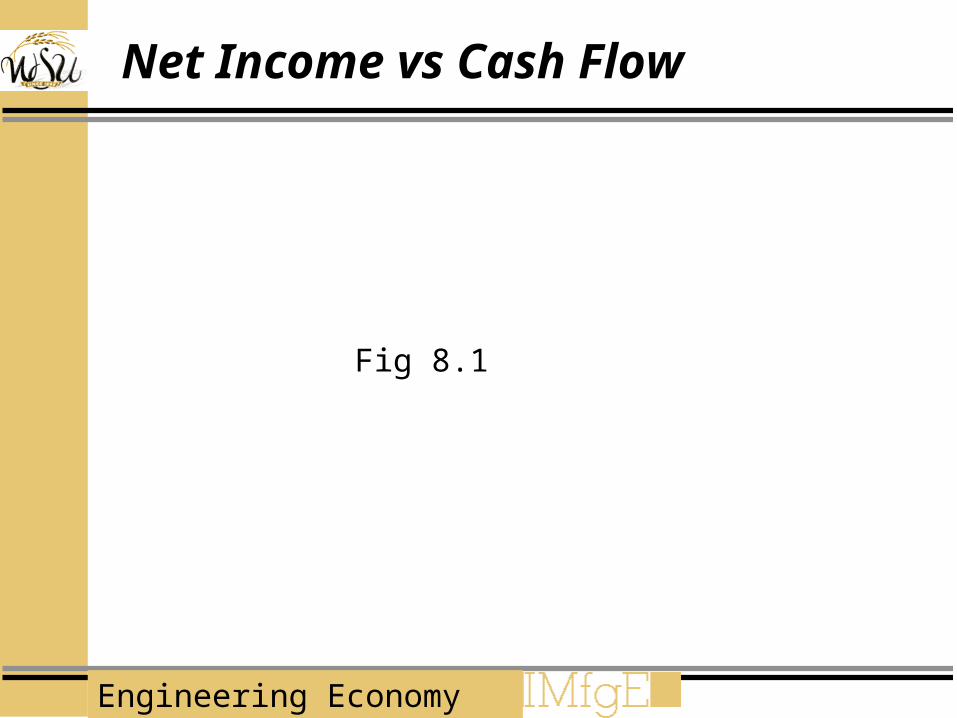

Net Income vs Cash Flow

Fig 8.1

Engineering Economy

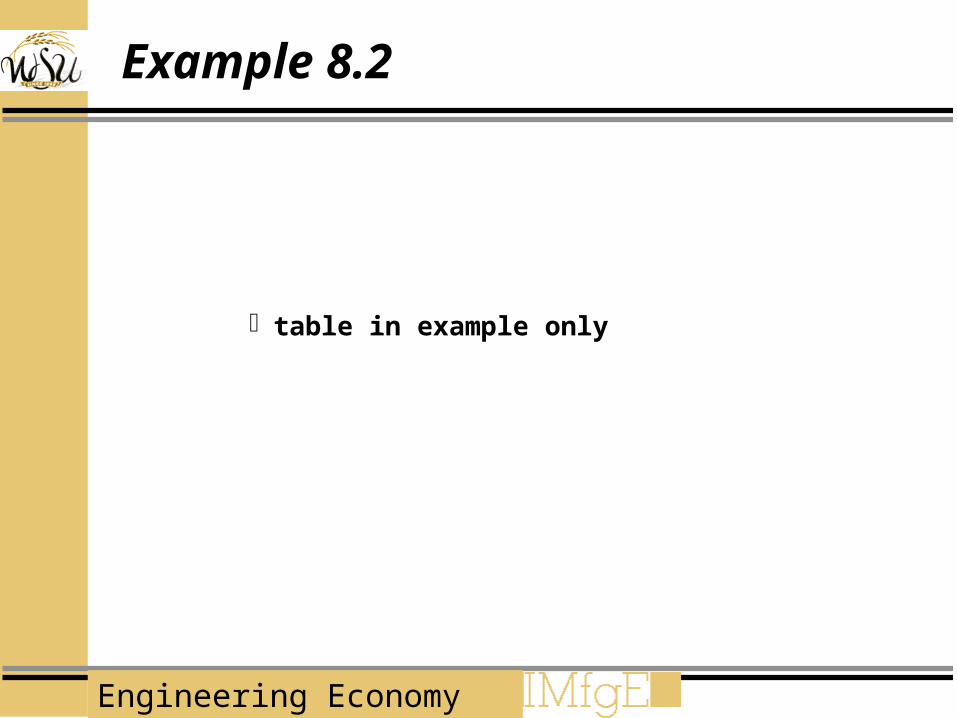

Example 8.2

table in example only

Engineering Economy

Example 8.2 (continued)

fig 8.2

Engineering Economy

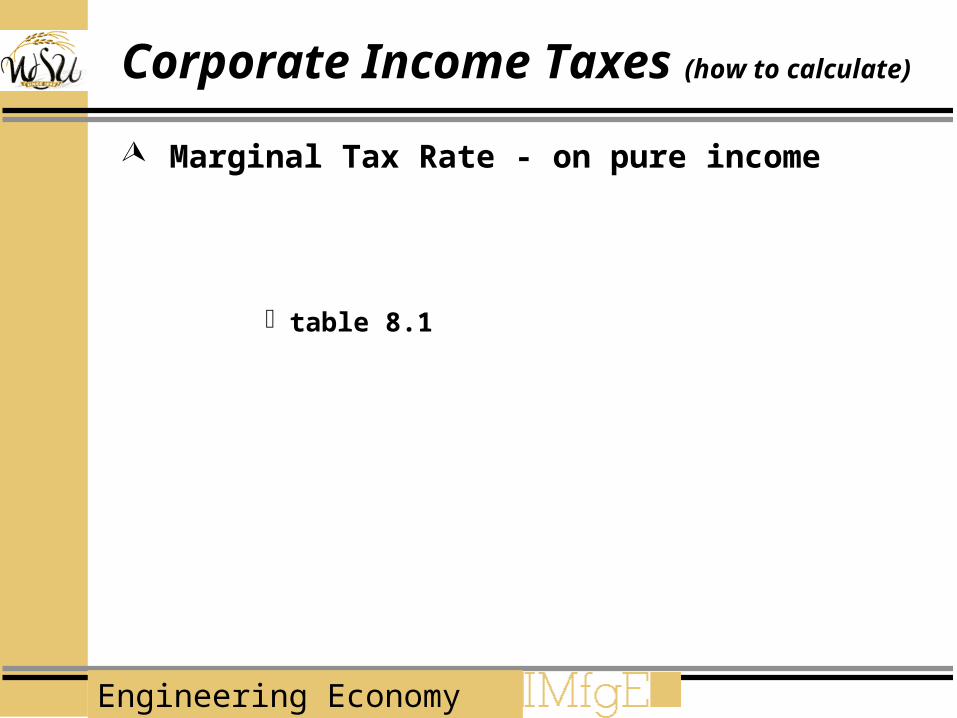

Corporate Income Taxes (how to

calculate) Marginal Tax Rate - on pure income

table 8.1

Engineering Economy

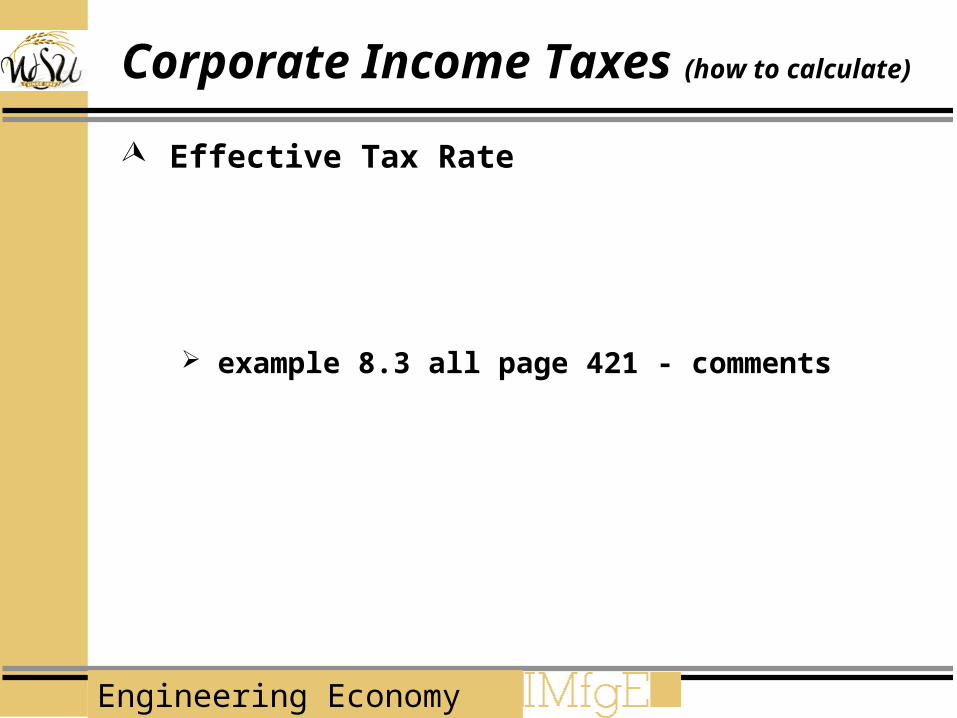

Corporate Income Taxes (how to calculate)

Effective Tax Rate

example 8.3 all page 421 - comments

Engineering Economy

Capital Gains and Losses

Gains - an asset is sold for more than its cost basis

Losses - an asset is sold for less than its cost basis

Losses cannot be used to offset operating income, but can offset capital gains (or postponed until later years)

Engineering Economy

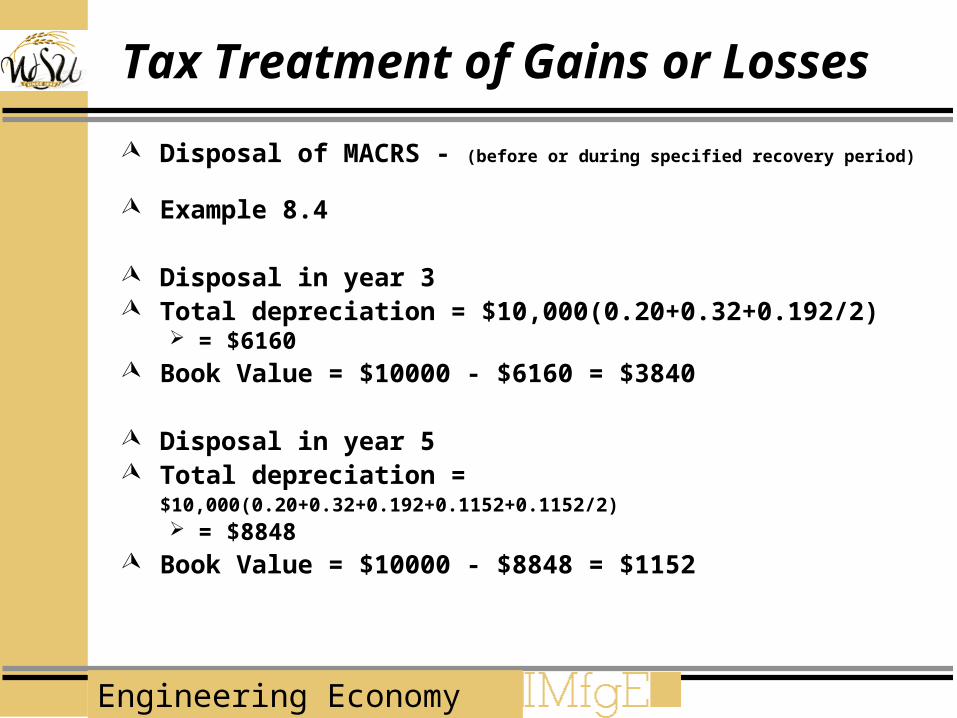

Tax Treatment of Gains or Losses Disposal of MACRS - (before or during specified recovery period)

Example 8.4

Disposal in year 3 Total depreciation = $10,000(0.20+0.32+0.192/2)

= $6160 Book Value = $10000 - $6160 = $3840

Disposal in year 5 Total depreciation =

$10,000(0.20+0.32+0.192+0.1152+0.1152/2) = $8848

Book Value = $10000 - $8848 = $1152

Engineering Economy

Tax Treatment of Gains or Losses (cont)

fig 8.3

Engineering Economy

Calculations of Capital Gains Tax Gains (losses) = Salvage Value - Book

Value (depreciation recapture)

For tax purposes

Capital Gains = Salvage Value - Cost Basis

Ordinary Gains = Cost Basis - Book Value

Only if capital gains are taxed at a different rate

Engineering Economy

Calculations of Capital Gains Tax

fig 8.4

Engineering Economy

example 8.5

Engineering Economy

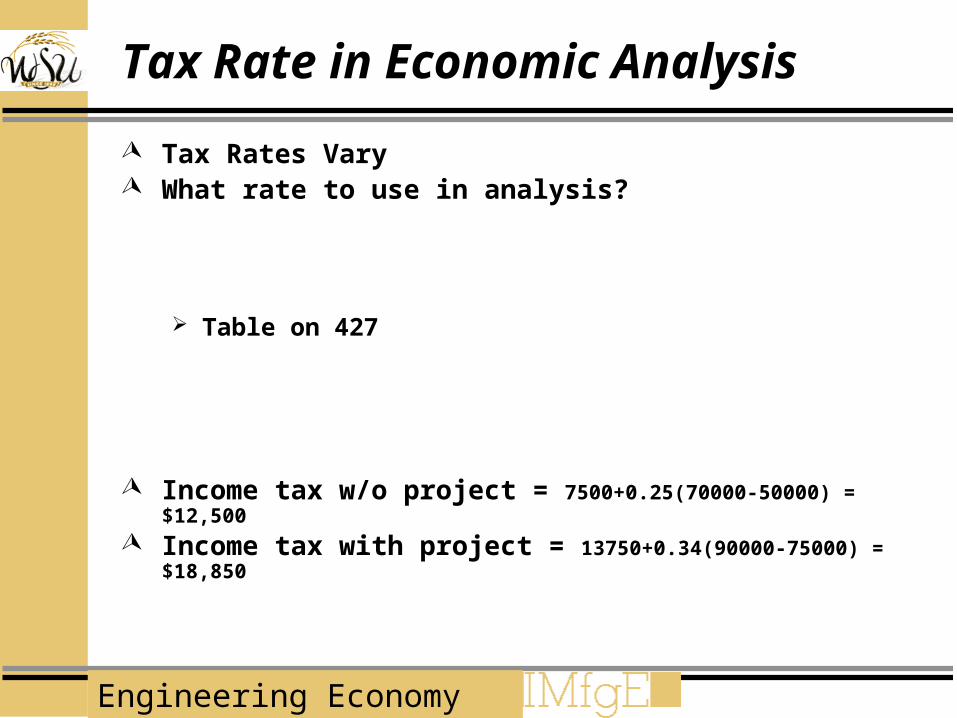

Tax Rate in Economic Analysis Tax Rates Vary What rate to use in analysis?

Table on 427

Income tax w/o project = 7500+0.25(70000-50000) = $12,500

Income tax with project = 13750+0.34(90000-75000) = $18,850

Engineering Economy

Tax Rate in Economic Analysis (cont)

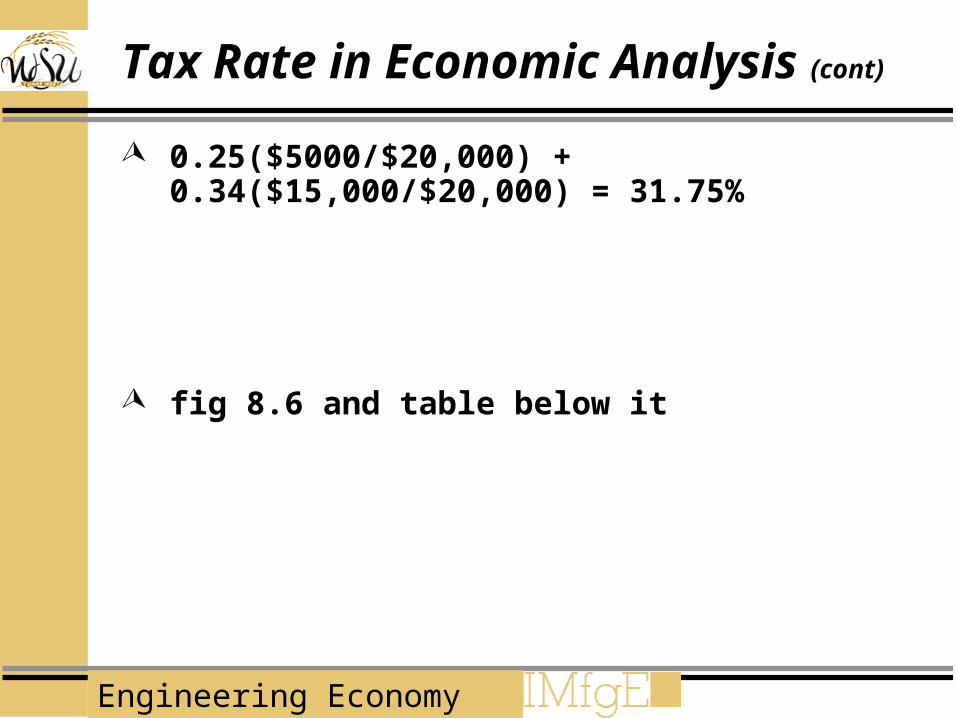

0.25($5000/$20,000) + 0.34($15,000/$20,000) = 31.75%

fig 8.6 and table below it

Engineering Economy

Example 8.6

table on 429

0.39($15,000/$50,000) + 0.34($35,000/$50,000) = 0.3550 0.39($15,000/$44,000) + 0.34($29,000/$44,000) = 0.3550

Engineering Economy

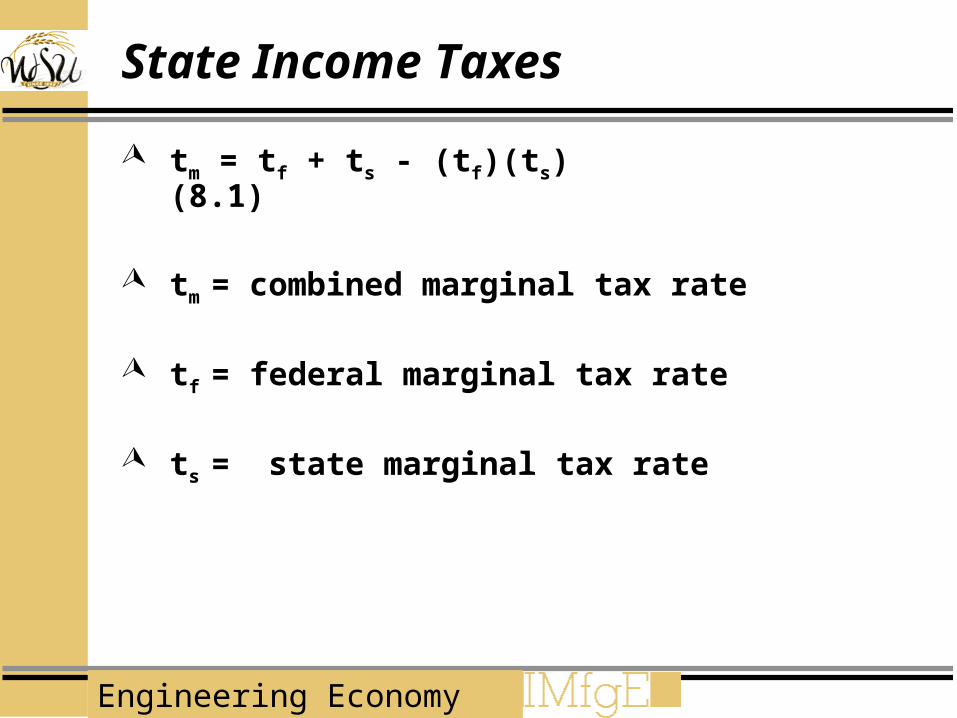

State Income Taxes

tm = tf + ts - (tf)(ts) (8.1)

tm = combined marginal tax rate

tf = federal marginal tax rate

ts = state marginal tax rate

Engineering Economy

Example 8.7

solution a and b

Engineering Economy

Consideration of Investment Tax Credits

Not now, but maybe in the future

Engineering Economy

Electing to Expense or Capitalize If your company invests < $200,000/year

in equipment

you can expense up to $17,500 of equipment each year.

Engineering Economy

IEN255 Summer’99

Test III Thursday!!!!!