Embed Size (px)

Citation preview

Engine leasing, financing and investment

Airline EconomicsSchool

Hong Kong 2016***

Jon SharpPresident and CEO

Engine Lease Finance Corporation

Spare engine leasing

• Introduction

• Marketsize

• Businessmodels

• Shortandlongtermleasingconsiderations

• Economiclifecycle

• ImpactofOEMmarketinfluence

• Endoflifeexits

• Conclusions

121

Theworld’sleadingspareenginelessor

c.300engines$2.5bnportfoliovalue

130customers5jointventurepartners

Engine Lease Finance Corporation

This image cannot currently be displayed.

Company Structure

MitsubishiUFJLease&FinanceCompanyLimited(“MUL”)

ELFCSingaporePte. Ltd.

ELFLondonLimited

AviationLeaseFinanceLLC

EngineLeaseFinanceCorporation

SPCs&JVs

Market Overview – engine operating leases

123

• Howmanyaircraft?

• Whatnumbersleased?

• Howmanyspareenginesleased?

• Howmanyspareengines?

• Whatdollarvalue?

• Potentialmarket

EngineOperatingLeasingMarketSize– Analysismethodology

Market Overview – engine operating leases

124

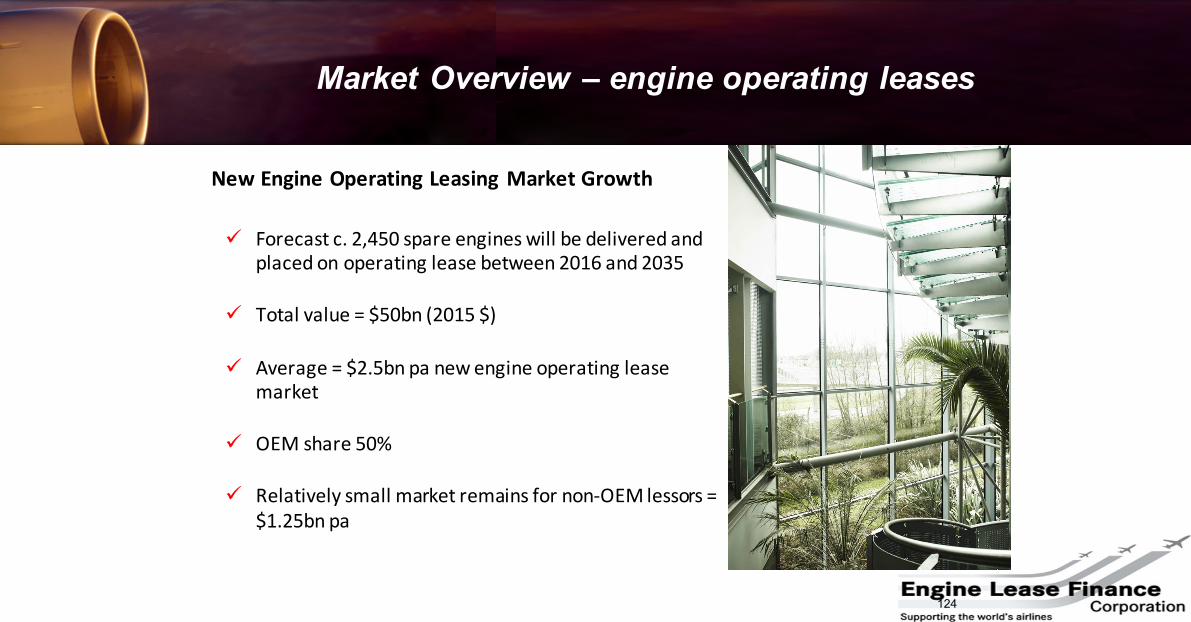

ü Forecastc.2,450spareengineswillbedeliveredandplacedonoperatingleasebetween2016and2035

ü Totalvalue=$50bn(2015$)

ü Average=$2.5bnpanewengineoperatingleasemarket

ü OEMshare50%

ü Relativelysmallmarketremainsfornon-OEMlessors=$1.25bnpa

NewEngineOperatingLeasingMarketGrowth

125

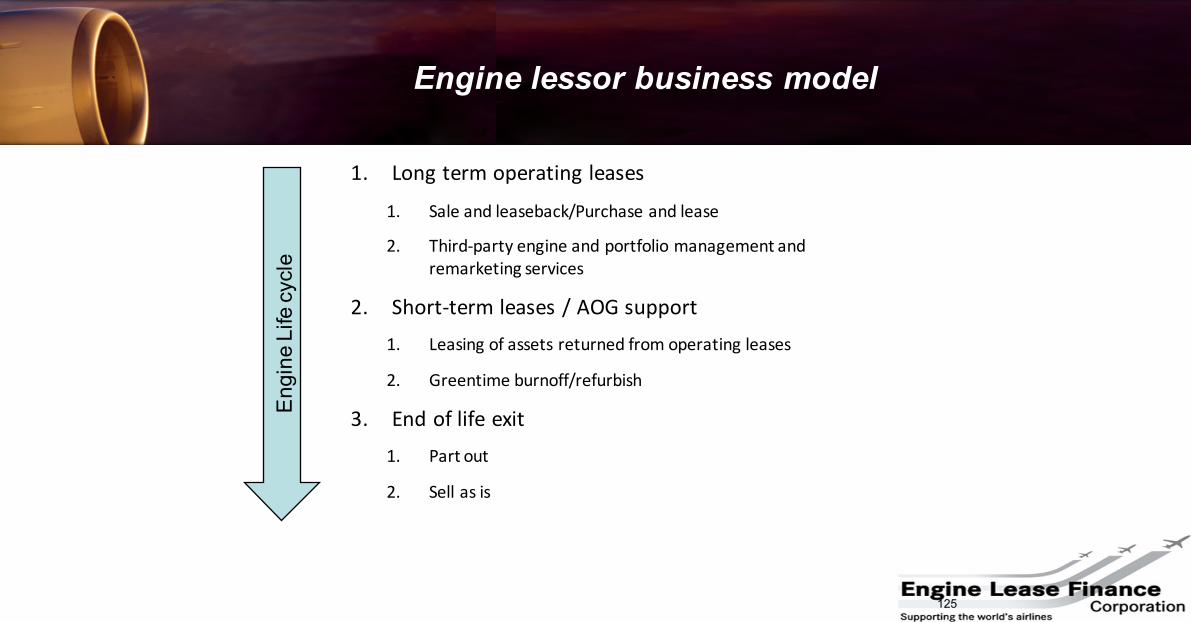

1. Longtermoperatingleases

1. Saleandleaseback/Purchaseandlease

2. Third-partyengineandportfoliomanagementandremarketingservices

2. Short-termleases/AOGsupport1. Leasingofassetsreturnedfromoperatingleases

2. Greentimeburnoff/refurbish

3. Endoflifeexit1. Partout

2. Sellasis

Engine lessor business model

Eng

ine

Life

cyc

le

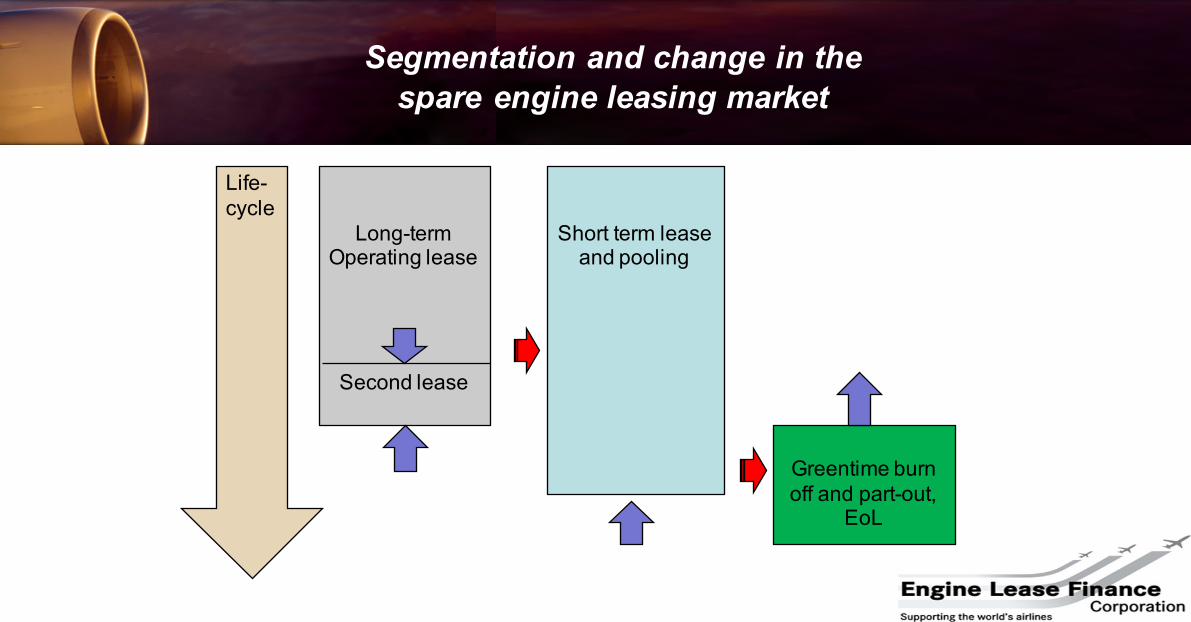

Segmentation and change in the spare engine leasing market

Long-termOperating lease

Second lease

Short term leaseand pooling

Greentime burn off and part-out,

EoL

Life-cycle

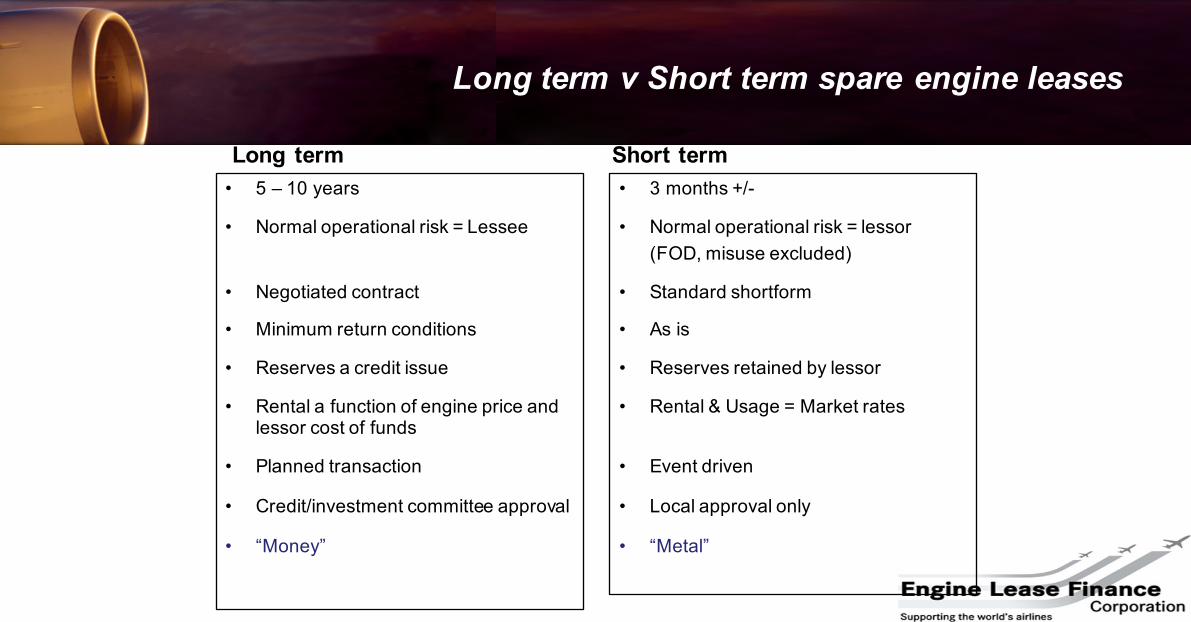

Long term v Short term spare engine leases

Long term• 5 – 10 years

• Normal operational risk = Lessee

• Negotiated contract

• Minimum return conditions

• Reserves a credit issue

• Rental a function of engine price and lessor cost of funds

• Planned transaction

• Credit/investment committee approval

• “Money”

Short term• 3 months +/-

• Normal operational risk = lessor(FOD, misuse excluded)

• Standard shortform

• As is

• Reserves retained by lessor

• Rental & Usage = Market rates

• Event driven

• Local approval only

• “Metal”

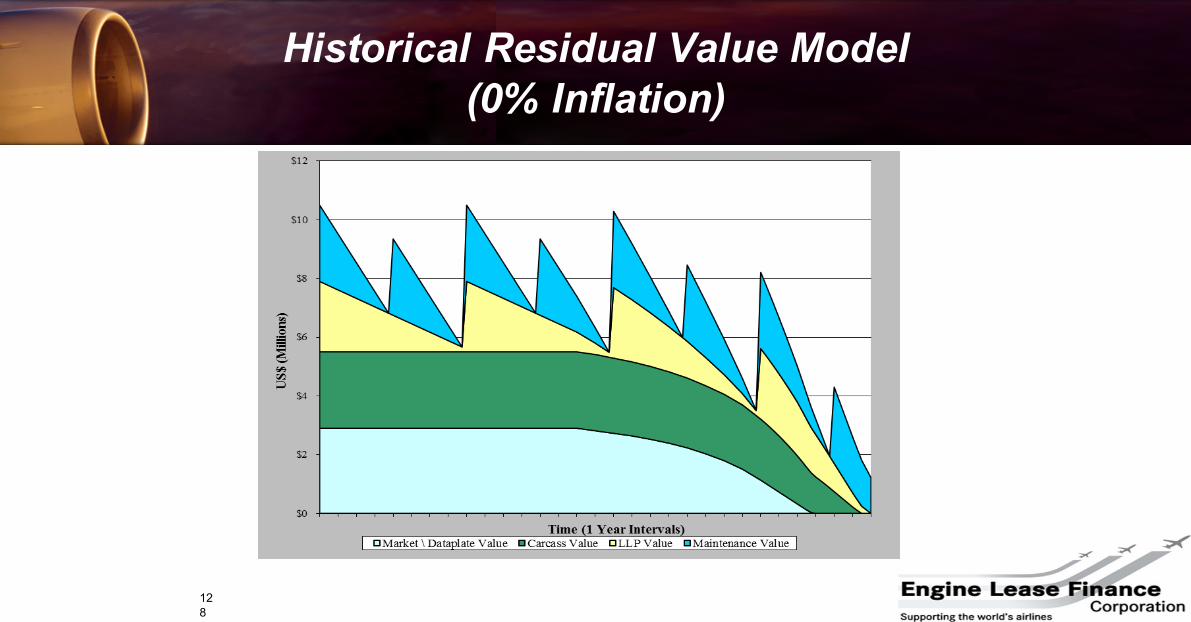

128

Historical Residual Value Model (0% Inflation)

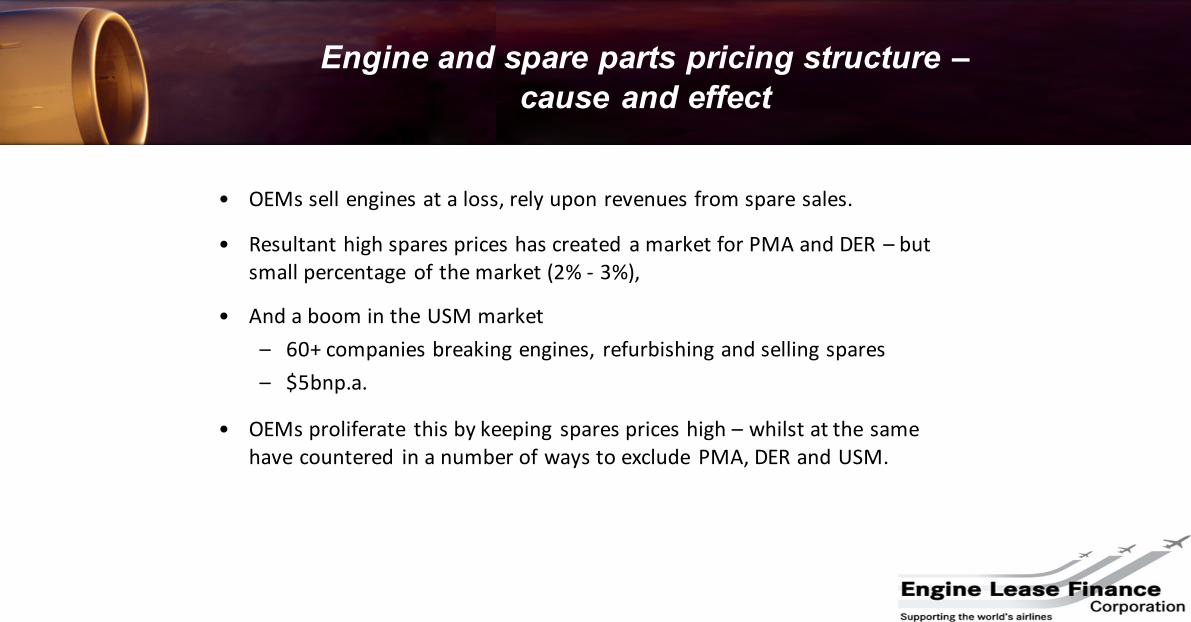

Engine and spare parts pricing structure –cause and effect

• OEMssellenginesataloss,relyuponrevenuesfromsparesales.

• Resultanthighsparespriceshascreated amarketforPMAandDER– butsmallpercentageofthemarket(2%- 3%),

• AndaboomintheUSMmarket– 60+companiesbreakingengines, refurbishingandsellingspares– $5bnp.a.

• OEMsproliferate thisbykeeping sparespriceshigh– whilstatthesamehavecountered inanumberofwaystoexcludePMA,DERandUSM.

130

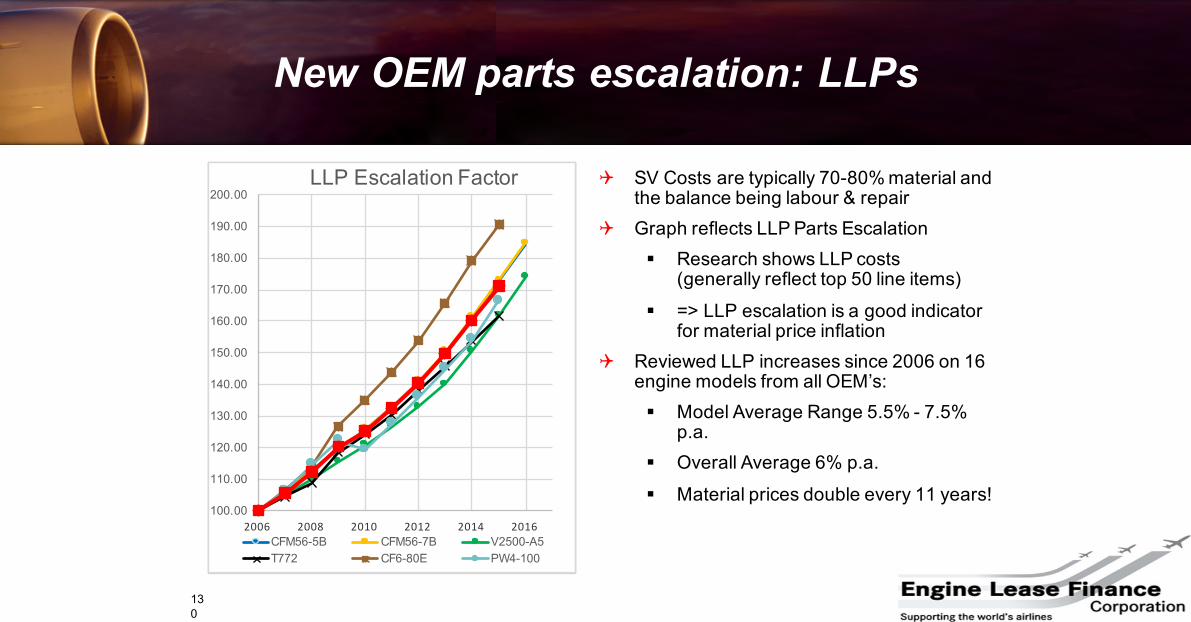

New OEM parts escalation: LLPs

Q SV Costs are typically 70-80% material and the balance being labour & repair

Q Graph reflects LLP Parts Escalation§ Research shows LLP costs

(generally reflect top 50 line items)

§ => LLP escalation is a good indicator for material price inflation

Q Reviewed LLP increases since 2006 on 16 engine models from all OEM’s:§ Model Average Range 5.5% - 7.5%

p.a.§ Overall Average 6% p.a.

§ Material prices double every 11 years!

100.00

120.00

140.00

160.00

180.00

200.00

220.00

240.00

260.00

280.00

2000 2005 2010 2015

LLP Escalation Factor

CFM56-5B CFM56-7B V2500-A5

100.00

110.00

120.00

130.00

140.00

150.00

160.00

170.00

180.00

190.00

2006 2008 2010 2012 2014 2016

LLP Escalation Factor

CFM56-5B CFM56-7B V2500-A5

100.00

110.00

120.00

130.00

140.00

150.00

160.00

170.00

180.00

190.00

200.00

2006 2008 2010 2012 2014 2016

LLP Escalation Factor

CFM56-5B CFM56-7B V2500-A5T772 CF6-80E PW4-100

100.00

110.00

120.00

130.00

140.00

150.00

160.00

170.00

180.00

190.00

200.00

2006 2008 2010 2012 2014 2016

LLP Escalation Factor

CFM56-5B CFM56-7B V2500-A5T772 CF6-80E PW4-100

OEM’s have used a multi faceted approach to achieve a dominant aftermarket position:-

1.Increase in OEM owned MRO supply

2.Proliferation of flight hour agreements

3.Reduction in repair availability and restrictions on performing repairs

4.Effective elimination in use of PMA & DER in gas-path

5.Continuous enhancements, modifications and upgrades

6.Control of new parts prices and increased presence in used serviceable material market

7.Discounting of value for Non OEM maintained engines e.g. “TruEngine” and “Pure-V”

131

OEM Control – Multiple Counters

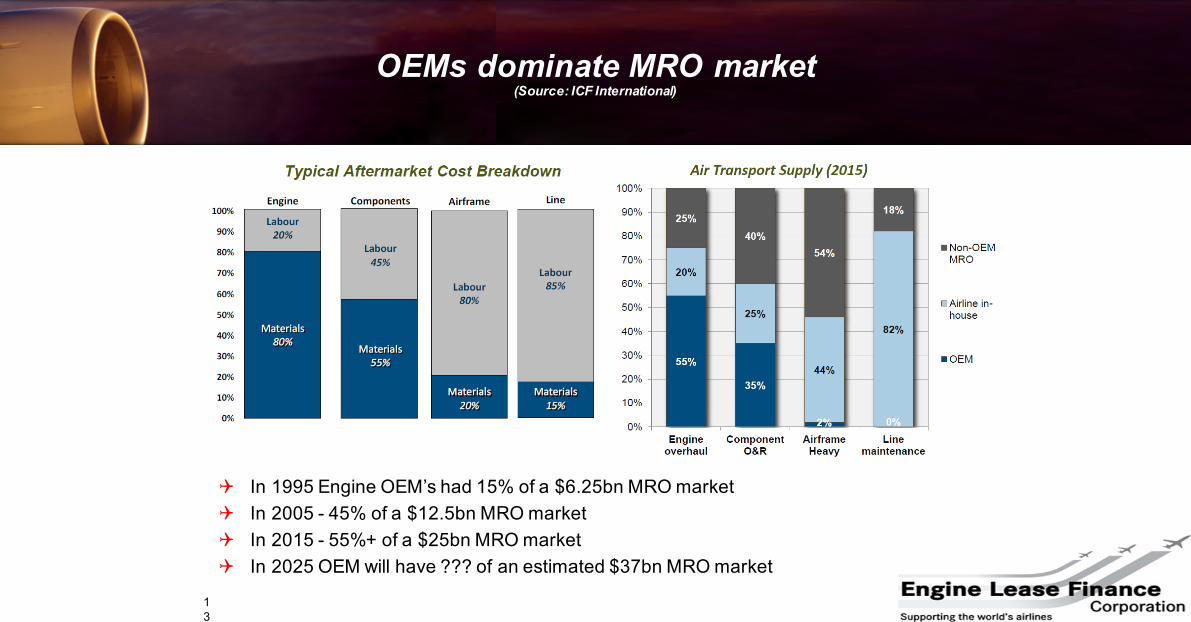

Q In 1995 Engine OEM’s had 15% of a $6.25bn MRO marketQ In 2005 - 45% of a $12.5bn MRO marketQ In 2015 - 55%+ of a $25bn MRO marketQ In 2025 OEM will have ??? of an estimated $37bn MRO market

132

OEMs dominate MRO market(Source: ICF International)

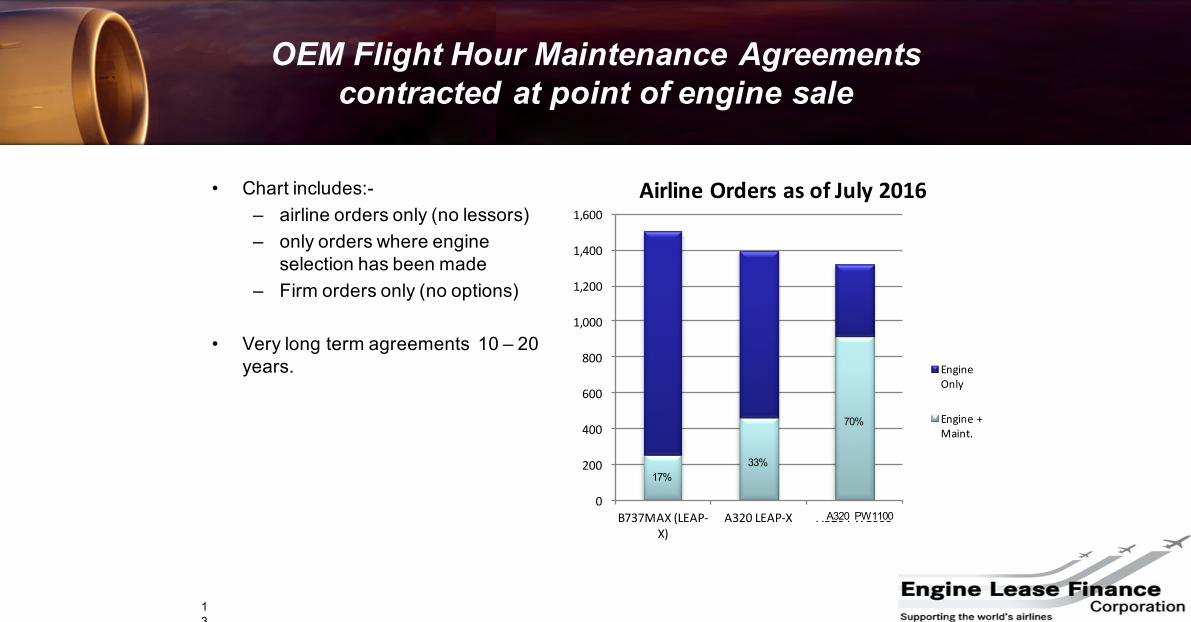

• Chart includes:-– airline orders only (no lessors) – only orders where engine

selection has been made– Firm orders only (no options)

• Very long term agreements 10 – 20 years.

13

OEM Flight Hour Maintenance Agreements contracted at point of engine sale

0

200

400

600

800

1,000

1,200

1,400

1,600

B737MAX(LEAP-X)

A320LEAP-X A320PW1000

AirlineOrdersasofJuly2016

EngineOnly

Engine+Maint.

17%33%

70%

A320 PW1100

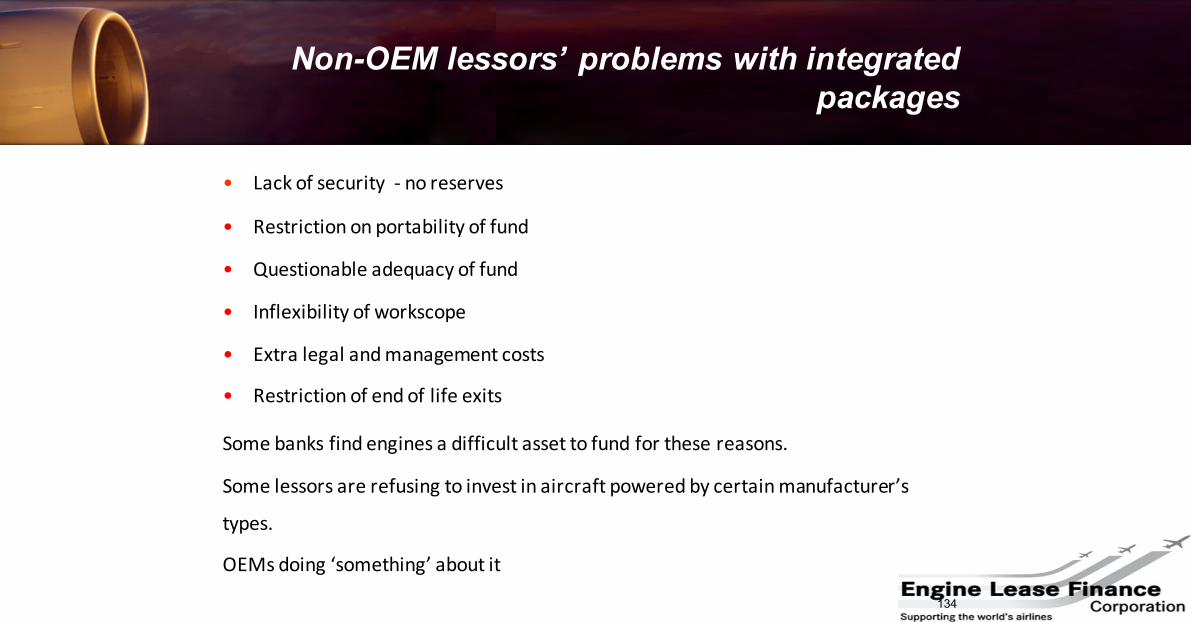

Non-OEM lessors’ problems with integrated packages

• Lackofsecurity- noreserves

• Restrictiononportabilityoffund

• Questionableadequacyoffund

• Inflexibilityofworkscope

• Extralegalandmanagementcosts

• Restrictionofendoflifeexits

Somebanksfindenginesadifficultassettofundforthesereasons.

Somelessorsarerefusingtoinvestinaircraftpoweredbycertainmanufacturer’s

types.

OEMsdoing‘something’aboutit

134

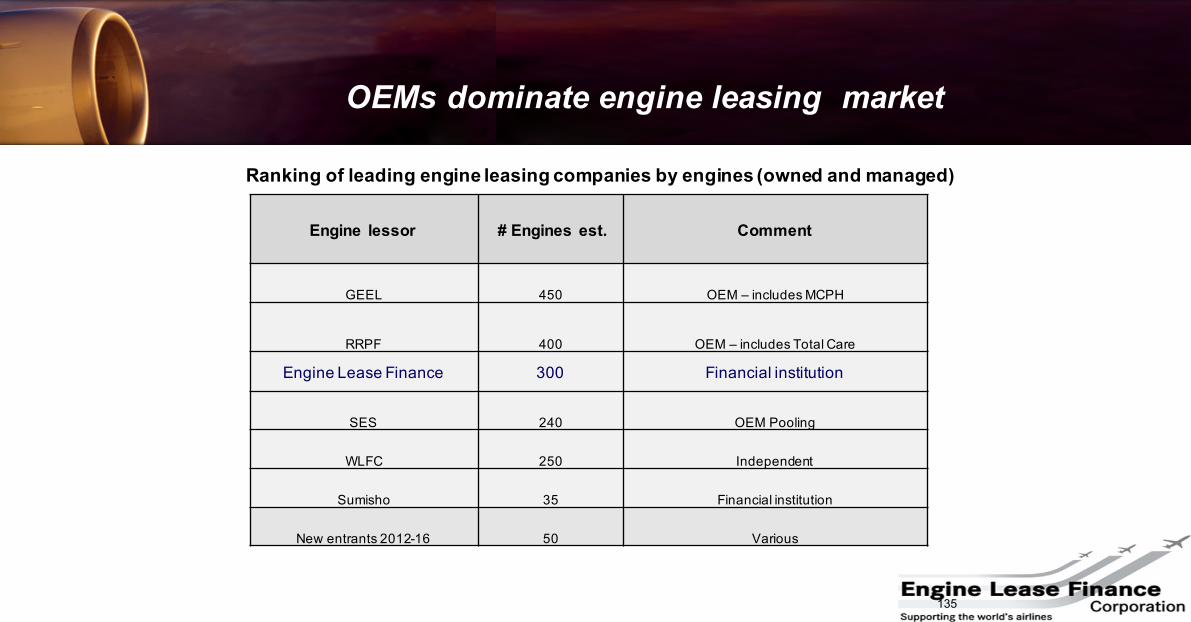

OEMs dominate engine leasing market

135

Ranking of leading engine leasing companies by engines (owned and managed)

Engine lessor # Engines est. Comment

GEEL 450 OEM – includes MCPH

RRPF 400 OEM – includes Total Care

Engine Lease Finance 300 Financial institution

SES 240 OEM Pooling

WLFC 250 Independent

Sumisho 35 Financial institution

New entrants 2012-16 50 Various

End of life solutions vitally important

• Theleasingcommunityemploysmanydifferent businessmodels.

• All thosebusinessmodelshavetwocommonelements–

• Buytherightassetattherightprice(andleaseitmakingmoneyover

money)and

• Ultimately,monetarisetheassetattheoptimumtimeinitslifecycle.

• Decisionsandconstantlymade:refurbishorsell?Itisamarketjudgement.

• Ultimately,Lessorsselltheirendoflifeassets(engines) toMROsorparts

companies.

136

Challenges regarding traditional end of life solutions

• OEMsintroducingschemessuchas‘TRUEngine’ /‘Pure-V’ retrospectively.

• BuyersofEoLengines(andpartsfromthem)selltoOEMcontrolledMROs.

• TheydemandBacktoBirthtracecertifyingno‘influencingparts’.

• EfforttotraceBtoBiscostlyevenifpossible,schememayhavebeenintroducedmanyyearsafter theassetwasacquired.

• Lessor’sassetthereforehaslostvalueoratworstisunsaleable.

• Morecrucialwithearlierbreakingofaircraft.

137

“TheErosionofChoice”.

• OEMsdominanceoftheaftermarket–– Engineleasing– MRO– Partssupply

• Airlinesandlessorsarefacing“The ErosionofChoice”.

• IATAisonthecaseofpotentialanticompetitivebehaviourandnowtheEUCommissionerforCompetitionisinvestigatingatIATA’srequest.

• Independent serviceprovidersmustformpartofthesolution.

Some conclusions

1. Theengine leasemarketisrobustbutsmallinscale.

2.Theshorttermandlongtermengineleasemarketsareverydifferent propositions:-1. Theyhavedifferentmarketdynamics.2. Theyhavetobemanagedseparately.

3.Leasingofengines andaircrafthavedifferent dynamics.

4.Businessmodelsforenginesneedmoreemphasisonmanagementof‘metal’ thanoncreditorfinance.

5.TheOEMshavedrivenradicalmarketchange, airlines’choiceshavebeeneroded,butIndependents doprovideasolutiontomaintainairlines’choice.

www.elfc.com