Embed Size (px)

Citation preview

Energy Use in the Australian Manufacturing Industry: An Analysis

of Energy Demand Elasticity

Chris Hill and Kay Cao*

Australian Bureau of Statistics, Analytical Services Branch

Abstract

Price elasticities for electricity and natural gas consumption in the Australian manufacturing

industry are estimated in this paper. Energy consumption data was sourced from the

Bureau of Resources and Energy Economics’ Australian Energy Statistics publication. Price

and income data were sourced from the Australian Bureau of Statistics National Accounts

and Producer Price Index publications. Estimation results suggested that short run price

elasticities for Electricity and Natural Gas consumption in the Manufacturing Industry were

-0.24 and -0.21 respectively. A long run equilibrium relationship was found to exist between

the explanatory variables, and estimation results from Error Correction Model showed a

speed of adjustment of 61 per cent per year for electricity consumption.

Key words: energy demand elasticity, manufacturing

JEL codes: C51, L60

* Please do no quote results without authors’ permission. The authors would like to thank Phillip Gould, Ruel

Abello, Anil Kumar and Yovina Joymungul Poorun (ABS Analytical Services) for their guidance or assistance; Claire Stark and Nhu Che (BREE) for their advice on BREE data. Responsibility for any errors or omissions remains solely with the authors. The views in this paper are those of the authors and do not necessarily represent the views of the Australian Bureau of Statistics.

I. Introduction

Rising energy prices and technological advances over the years have seen a change in the

utilisation and type of fuels consumed as inputs to the production process. An area of

interest is the magnitude of the impact that certain policies will have on energy usage.

It is important to consider the short and long term effects of price changes on energy

consumption. It is also of particular interest to understand the price elasticity for different

energy types at the industry level. It has been suggested in many papers (e.g. Bernd et al.,

1981 – hereinafter, BMW, 1981), that we can expect that in the long run, the price elasticity

of energy demand to be greater than that of the short run. The reasoning being that, in the

short run, only the utilisation of capital (equipment or stock) can be changed. However in

the long run, both capital utilisation and type of capital (with improved energy efficiency)

can be changed.

Ongoing research work on energy consumption modelling at the Australian Bureau of

Statistics (ABS) suggested several datasets that could be utilised. For example, Cao et. al.

(2012 and 2013) utilised ABS survey data to estimate industry energy consumption for the

non-survey years. The authors used cross-sectional data to estimate their models. However,

there are also time series data available, one of which is published by the Bureau of

Resources and Energy Economics (BREE) in their Australian Energy Statistics publication,

which could be used for modelling purposes.

The aim of this paper is to use the industry energy consumption time series data produced

by BREE to investigate the consumption of electricity and natural gas in the manufacturing

3

industry. It will discuss in detail several time series techniques used for modelling energy

consumption and then derive the associated impacts of price and income on fuel demand.

The remainder of the paper is organised as follows. Section II describes the modelling

framework that is commonly used in modelling energy demand over time. Section III

describes the data used, including derivation of variables as well as data quality issues.

Section IV discusses in detail the model specification and model results. Section V concludes

and provides some recommendations for future work.

II. Modelling Framework

i. Energy demand over time

Business demand for energy at any given time is determined by a number of different

components, both internal and external factors. Many of these components can easily be

accounted for, whilst others are somewhat more convoluted in nature, making them in

some cases almost impossible to accurately measure. Energy, which is closely related to

labour and capital, is an important input into the production process for any firm. In

particular the demand for energy is largely determined by the type, utilisation and energy

efficiency of a firm’s stock of capital.

Since we know that energy consumption is closely related to capital stock, the ability to alter

that consumption will also be reliant on the ability to change the capital stock in some way.

There are three main ways in which the capital stock can be changed. The first is to change

the capital stock itself to a type that uses an alternative energy source. The second is to

change a firm’s utilisation of existing capital stock. The third is to change the existing capital

stock to a more energy efficient model.

In the short run, the only real option a firm has if they wish to change their energy use, is to

alter their utilisation of their existing capital. In simple terms, a firm uses more or less

energy by quickly expanding or downsizing certain projects or operations, or employing

energy saving techniques. They cannot quickly alter their actual stock of capital, only the

utilisation.

In the long run, a firm can employ any of the other two options mentioned above. They can

replace their capital with something that uses an alternative energy source, or they can

change / upgrade their capital to be more energy efficient. However, the ability to change

ones capital stock will depend on other factors such as technology advances and also the

degree of substitution between one energy source and another.

The reasons for and the ability to change energy consumption can be explained by

economic principles. Energy is a commodity, the same as labour and capital and is therefore

subject to external forces acting upon it. In particular, we expect a basic supply / demand

relationship for energy consumption; as price of energy increases, demand for energy

decreases (holding all other variables constant). An increase in price could have both short

run and long run impacts on energy demand, it could change a firms utilisation of capital

(short run), or it could be a contributing factor in the decision to change the actual stock of

capital (long-run).

5

Economic research plays a very large role in the analysis of demand for energy. Over the

last forty years, there have been vast improvements in the way in which economists and

econometricians have been able to model the relationships between energy demand and

economic factors. For modelling energy consumption over time, there are currently a

number of different techniques being utilised, and the following section will present a

summary of these.

ii. Modelling Techniques

There are a vast number of approaches that have been used over the years to look into

modelling energy consumption over time. The decision on which technique to employ

depends greatly on a number of different factors, including but not limited to; availability of

data, volatility / behaviour of time series in question, as well as output requirements for the

specific project (e.g. whether short run or long run elasticity is the focus). There is also the

matter of the aggregation level of the data itself being a very important aspect to consider

when performing any sort of energy demand analysis (Bernstein & Madlener, 2010).

Level Models

The basic model, represented below has both the dependant and independent variables

logged. This allows for the direct interpretation of coefficients 2 3 and which represent

the short run elasticities of price and income respectively:

1 2 3ln( ) ln( ) ln( ).t t tE P Y (2.1)

where E, P and Y represent energy, price and output variables respectively.

The above model can also be used with cross-sectional data. However, when there is time

series data available, it can be extended to include an AR(1)† term. The main advantages

are that both the short and long run price elasticities are easily computed using the model

coefficients:

1 2 3 4 1ln( ) ln( ) ln( ) ln( ),t t t tE P Y E (2.2)

In this model:

2

2 4

Short-run price elasticity = ,

Long-run price elasticity = / (1 ).

Stationarity‡ in a time series is a desirable property to have when it comes to the

interpretation of results. However, most economic time series data are non-stationary, and

this can mean that the interpretation of these results can be somewhat spurious if non-

stationarity is found in any of the variables.

First Difference Modelling Approach

As mentioned previously, non-stationarity can be an issue when attempting to model

economic time series data. It is often the case that there will be a strong relationship

between two variables simply because both of them are trending upward (or downward)

over time. If this is the case, then we cannot rely on the coefficients or the associated error

terms and statistical tests computed in that regression. A solution to this problem that is

†AR(1) refers to an Auto-Regressive term of lag one. The dependant variable is lagged one period and included

as an additional regressor in the model. ‡ A time series is stationary if its mean and variance are constant over time, and the value of the covariance

between two time periods depends only on the distance k (lag) between the two periods, and not the actual time t itself.

7

often used is to transform a series to be stationary by taking differences of the initial

variables:

1 2 , 3ln( ) ln( ) ln( ) .t E t t tE P Y (2.3)

Many economic time series data are non-stationary, for example, integrated of order one

(I(1)), which would become stationary after taking a first difference. The downside to taking

this approach is that the long run price elasticity can no longer be calculated using the

model coefficients. If we again assume that in the long-run 1....t tE E E , then the

differenced values would be equal to zero, and the interpretation becomes meaningless.

However, an error correction model (ECM) can often be used to overcome this issue.

Error Correction Model (ECM)

If the variables in question are I(1), there still may exist a long run equilibrium relationship

between the variables. This is known as a cointegrating relationship, which exists only if the

error term in the relationship is stationary. In this case, the error term refers to the residual

taken from model (2.1).

The error term, if found to be I(0), is defined as the deviation from the long run equilibrium

value. Its lagged values represent the deviation from the equilibrium in the previous period,

and are inserted into model (2.3) as an additional variable, and are represented by 1tEC .

(This is known as the Engle-Granger procedure)

1 2 , 3 4 1ln( ) ln( ) ln( ) .t E t t t tE P Y EC (2.4)

Coefficients 2 3and still represent the short run price and income elasticities, and 4

would represent the “speed of adjustment to equilibrium values” (Ryan and Plourde, 2009).

For example, a 4 value of -0.7 would mean that deviations from the equilibrium are

corrected at approximately 70 per cent per time period, t.

Other Models

In recent years, there were also other modelling approaches, for example, Vector Error

Correction Model (when more than one cointegrating relationship are found) or panel

VECM when there are panel datasets available. However, given the short time series of the

data used in this study, and also given that the above mentioned models require heavy

parameterisation, we did not pursue these models. Further explanation on our preferred

model is provided below.

iii. Modelling approach utilised in this study

For this study, based on an examination of the available data and the alternative modelling

approaches, the ECM method was considered the most appropriate for deriving short run

elasticities for electricity and natural gas consumption.

Testing for stationarity proved that most variables in question were in fact non-stationary,

and typically I(1) processes (see Table A2, Appendix), as is expected from economic variables

of this nature. As a result, the level models were ruled out due to their interpretability

being questionable and the possible spurious nature of the associated test statistics.

9

III. Data

i. Energy Data - Australian Energy Statistics (ABARES / BREE Table F)

BREE releases a yearly publication called “Australian Energy Statistics” (AES). Energy

consumption, by industry and fuel type, are provided in Table F of this publication (BREE,

2012). Up until 2011, these data were produced by the Australian Bureau of Agriculture and

Resource Economics and Sciences (ABARES) and published in the ‘Energy in Australia’ yearly

release. The data spans back to the 1973-74 financial year, providing 37 years of time series

data at each sub level. Energy consumption is broken into three separate components: fuels

consumed, derived fuels produced and net energy consumption. Fuels consumed data are

used in this study.

ii. Price and Income Data

ABS PPI Data - Electricity and Natural Gas

The ABS collects and publishes price data for a range of different energy types. For this

study, we utilise the ABS Producer Price Index (PPI) series, which is released quarterly (cat.

no. 6427.0). Tables 13 and 14 of this publication provide price indices for electricity and gas

used in the manufacturing industry. These indices are produced quarterly and date back to

1970. It is from these tables that the electricity and gas prices were taken. Due to energy

consumption being financial year data, an average of the corresponding four quarters of

price index data was taken to derive the financial year average price.

Gross Value Added (GVA) data

The ABS National Accounts Branch (NAB) releases a yearly publication ‘National Income,

Expenditure and Product’ (cat. no. 5206.0). Table 33 of this publication includes the

Industry gross value added (GVA) chain volume measures (CVM) for each industry. For the

purpose of this investigation the GVA for the Manufacturing industry has been used as our

measure of income. The data for the Manufacturing industry dates back to 1975.

Due to BREE data not fully available at the sub-sector level and with ABS PPI data only

available for manufacturing division and only for electricity and gas over the study period,

our analysis is mainly focused on the consumption of these fuels in manufacturing industry.

The following graphs show the data series in log form. All series demonstrate a global

upward trend. Apart from price series, electricity and value added series show a significant

dip after the global financial crisis in 2008-09.

11

Figure1. Time Series Data

Note: All variables presented are in log form. LELEC, LNAT_GAS, LELEC_PRICE, LNAT_GAS_PRICE and LGVA are electricity consumption, natural gas consumption, electricity price, natural gas price and gross value added respectively.

4.4

4.8

5.2

5.6

6.0

1975 1980 1985 1990 1995 2000 2005

LELEC

4.4

4.8

5.2

5.6

6.0

6.4

1975 1980 1985 1990 1995 2000 2005

LNAT_GAS

3.2

3.6

4.0

4.4

4.8

5.2

1975 1980 1985 1990 1995 2000 2005

LELEC_PRICE

3.2

3.6

4.0

4.4

4.8

5.2

1975 1980 1985 1990 1995 2000 2005

LNAT_GAS_PRICE

11.1

11.2

11.3

11.4

11.5

11.6

11.7

1975 1980 1985 1990 1995 2000 2005

LGVA

IV. Results

i. Cointegration and Stationarity Tests

It was decided that an ECM approach was appropriate after results of stationarity and

cointegration tests were completed. As explained in Section 2, a cointegrating relationship

represents the long run or equilibrium relationship between the variables in question

(Plourde and Ryan, 2009). We conducted Augmented Dickey Fuller (ADF) test for all

variables. Results suggested they are non-stationary - I(1).

The tables below show the results of the test for cointegration between the explanatory

variables for the consumption of electricity:

Table 1. Level Model regression - dependant variable: Log electricity consumption

Note: C, LELEC_PRICE, LGVA and LNAT_GAS_PRICE are the intercept and log of electricity price, gross value added and natural gas price respectively.

13

Whilst the variables are I(1), ADF test shows the model residuals are I(0) (i.e. stationary, as

the null hypothesis for a unit root is rejected), implying that a long run cointegrating

relationship exists between the variables in question.

Table 2. Augmented Dickey Fuller test

Note: RESID_ELEC1_3 is estimate of residual from the model in Table 1.

ii. Model Specification

Below is the specification for the final ECM models used in this paper. As mentioned

previously, data limitations constrained the analysis to only two different fuel types;

electricity and natural gas. A two stage Engle-Granger approach was used to formulate the

ECM models; the two cointegrating relationships used are:

0 1 , 2 3 , ,ln( ) ln( ) ln( ) ln( )t E t t G t E tE P Y P , (4.1)

and

0 1 , 2 3 , ,ln( ) ln( ) ln( ) ln( )t G t t E t G tG P Y P . (4.2)

The cointegrating relationships above represent the long run equilibrium for the two fuel

types, and the residuals from these relationships represent the deviation from the

equilibrium. The residuals from model (4.1) and (4.2) were lagged and included in the ECM

models for electricity and gas consumption respectively. The specification for the error

correction models are below:

0 1 , 2 3 , 4 1 5 6ln( ) ln( ) ln( ) ln( )t E t t G t t tE P Y P EC GFC T ,(4.3)

and

0 1 , 2 3 , 4 1 5 6ln( ) ln( ) ln( ) ln( )t G t t E t t tG P Y P EC GFC T ,(4.4)

where:

tE is the Electricity consumption at time t,

Gt is the Natural Gas consumption at time t,

,E tP is the price of Electricity at time t,

tY is the measure of Income (GVA) for the manufacturing industry at time t,

,G tP is the price of Natural Gas at time t,

1tEC is the error correction component for time t-1 taken from equations (4.1) and (4.2),

GFC is a dummy variable representing the time period before and after the GFC and,

T is a time trend.

15

The inclusion of the price of alternative fuels in the ECM model was based on economic

literature as well as the evidence from the model results themselves. Economic theory

suggests that the demand for a commodity may not only depend on its own price, but also

the price of its substitutes or compliments. If the coefficient of the alternative fuel price is

significantly positive, it can be considered as a substitute, and if the coefficient is

significantly negative, it can be considered as a compliment. Gas is not the only substitute

for electricity, and vice versa, however due to data limitations the inclusion of other

substitute prices was not possible.

The decision to include a dummy variable for the GFC effect was made due to the sporadic

movements of the variables in question for the 2008-09 and 2009-10 financial years. The

dummy variable has a value of one for these years, and a value of zero for all previous years.

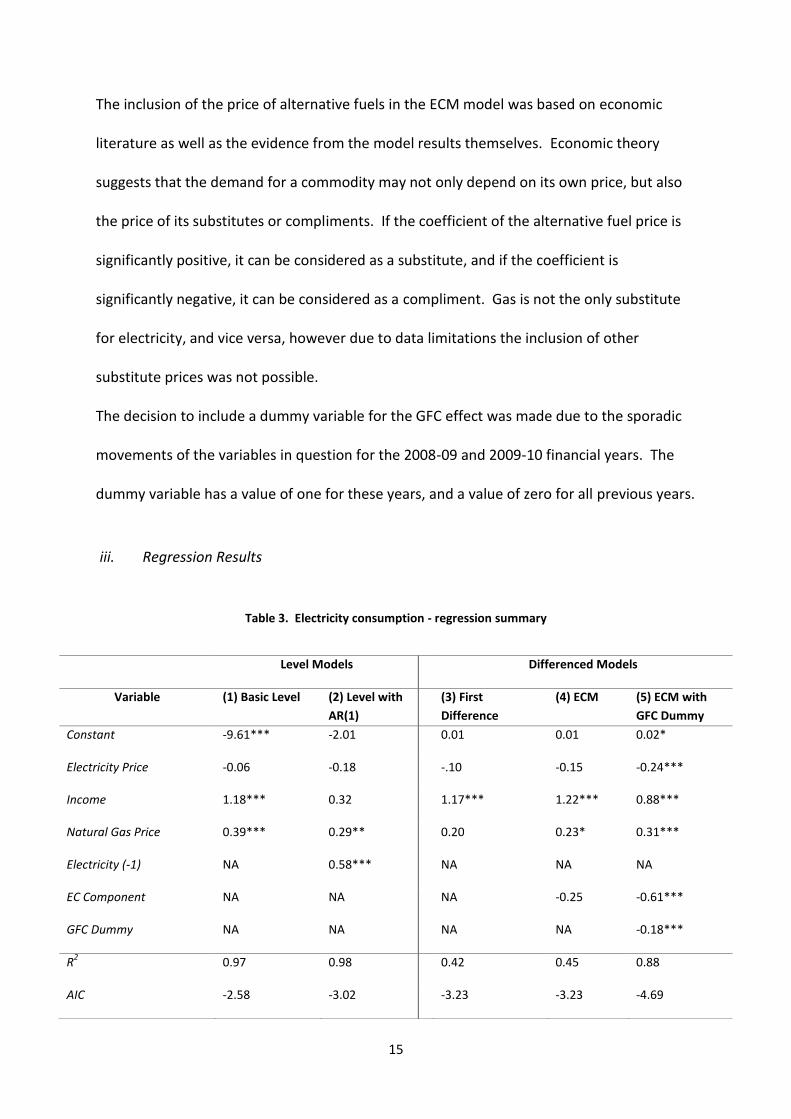

iii. Regression Results

Table 3. Electricity consumption - regression summary

Level Models Differenced Models

Variable (1) Basic Level (2) Level with

AR(1)

(3) First

Difference

(4) ECM (5) ECM with

GFC Dummy

Constant -9.61*** -2.01 0.01 0.01 0.02*

Electricity Price -0.06 -0.18 -.10 -0.15 -0.24***

Income 1.18*** 0.32 1.17*** 1.22*** 0.88***

Natural Gas Price 0.39*** 0.29** 0.20 0.23* 0.31***

Electricity (-1) NA 0.58*** NA NA NA

EC Component NA NA NA -0.25 -0.61***

GFC Dummy NA NA NA NA -0.18***

R2

0.97 0.98 0.42 0.45 0.88

AIC -2.58 -3.02 -3.23 -3.23 -4.69

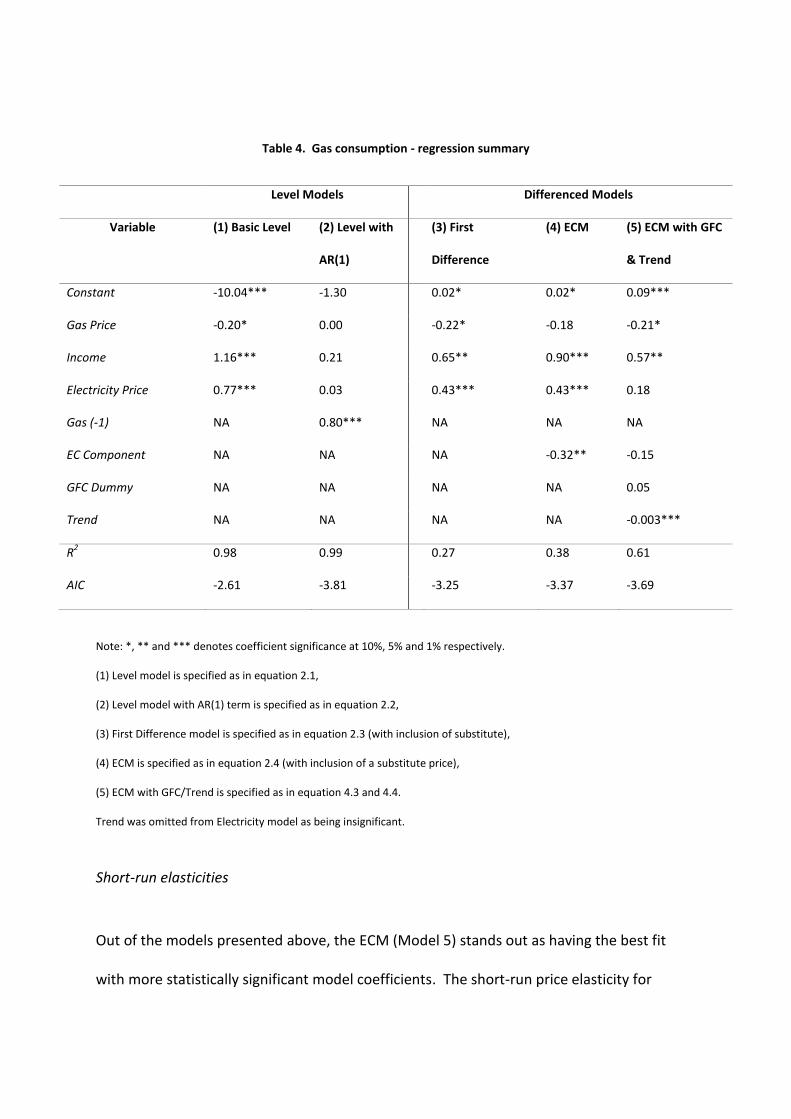

Table 4. Gas consumption - regression summary

Level Models Differenced Models

Variable (1) Basic Level (2) Level with

AR(1)

(3) First

Difference

(4) ECM (5) ECM with GFC

& Trend

Constant -10.04*** -1.30 0.02* 0.02* 0.09***

Gas Price -0.20* 0.00 -0.22* -0.18 -0.21*

Income 1.16*** 0.21 0.65** 0.90*** 0.57**

Electricity Price 0.77*** 0.03 0.43*** 0.43*** 0.18

Gas (-1) NA 0.80*** NA NA NA

EC Component NA NA NA -0.32** -0.15

GFC Dummy NA NA NA NA 0.05

Trend NA NA NA NA -0.003***

R2

0.98 0.99 0.27 0.38 0.61

AIC -2.61 -3.81 -3.25 -3.37 -3.69

Note: *, ** and *** denotes coefficient significance at 10%, 5% and 1% respectively.

(1) Level model is specified as in equation 2.1,

(2) Level model with AR(1) term is specified as in equation 2.2,

(3) First Difference model is specified as in equation 2.3 (with inclusion of substitute),

(4) ECM is specified as in equation 2.4 (with inclusion of a substitute price),

(5) ECM with GFC/Trend is specified as in equation 4.3 and 4.4.

Trend was omitted from Electricity model as being insignificant.

Short-run elasticities

Out of the models presented above, the ECM (Model 5) stands out as having the best fit

with more statistically significant model coefficients. The short-run price elasticity for

17

electricity derived from this model is -0.24 (a 1 per cent increase in the price of electricity

leads to 0.24 per cent decrease in the demand for electricity, holding other variables

constant). This value is consistent with Bernstein and Griffin’s 2005 results, in which they

found the short-run commercial price elasticity for USA to be -0.21.

It is important to note that this study uses aggregated data, and as explained by Steinbuks

(2010), there are possible associated biases that arise due to the nature of the data. For

example, aggregate data fails to account for the large differences in technological

requirements in specific industries. The substitution observed from model results could be

due to merely firm entry and exit. An elasticity of -0.24 is on the high end of the values

typically found, and this could include some upward bias in the estimate.

As expected there is a significant positive relationship between income (GVA) and the

demand for electricity, with a short run income elasticity of 0.88. Again, this value is within

the range typically found for income elasticities.

Short-run price elasticity for gas consumption is found to be -0.21 (Model 5, Table 4).

Long run equilibrium relationship

Whilst the Engle and Granger ECM model does not allow the interpretation of individual

long run elasticities, it can provide an indication of the speed at which the energy demand

reverts back to its long run equilibrium. As mentioned previously, if we assume that

1....t tE E E is the long run equilibrium demand, then the error correction term

provides information on the deviation from this equilibrium.

For the consumption of electricity, the Error Correction (EC) term is -0.61, which suggests

that deviations from the long run equilibrium are corrected at a rate of approximately 61

per cent per year. The coefficient for the EC term in the gas model is not found to be

significant; however the coefficient for the trend variable is statistically significant.

V. Conclusion

This study provides an investigation into the electricity and gas consumption by the

Australian manufacturing industry. More specifically, it looks into the associated price

elasticities of demand for these energy sources. Whilst there have been many papers

written that investigate energy consumption at industry levels, there are few papers that

use Australian energy data.

The methodological technique and selection of regression models is based largely on the

findings of European and American papers. This report investigates the pros and cons of

several energy modelling techniques, with the focus being on the Error Correction Model.

The data used has been sourced from the Bureau of Resources and Energy Economics, as

well as the Australian Bureau of Statistics. This analysis is based on yearly data ranging from

1973 to 2010.

The study has found statistically significant relationships between the dependant variables

(electricity and natural gas consumption), and the explanatory variables in question. Short

run price elasticity for electricity and gas consumption was found to be -0.24 and -0.21

respectively. Both these values were within the range of price elasticities found in other

investigations of this nature.

19

A summary of the elasticity estimates is provided in the table below.

Table 5. Summary of estimates

Variable (1) Basic Level (2) Level

with AR(1)

(3) First

Difference

(4) ECM (5) ECM with

GFC Dummy

Electricity Consumption

Electricity Price -0.06 -0.18 -.10 -0.15 -0.24***

Natural Gas Price 0.39*** 0.29** 0.20 0.23* 0.31***

Electricity (-1) NA 0.58*** NA NA NA

EC Component NA NA NA -0.25 -0.61***

Gas Consumption

Gas Price -0.20* 0.00 -0.22* -0.18 -0.21*

Electricity Price 0.77*** 0.03 0.43*** 0.43*** 0.18

Gas (-1) NA 0.80*** NA NA NA

EC Component NA NA NA -0.32** -0.15

Note: The coefficients of electricity price (in electricity consumption equation) and gas price (in gas

consumption equation) give the short run elasticity estimates. Long run adjustments are implied by the

estimates of either the coefficient of the lag price variable (in AR(1) model) or the coefficient of the EC

component.

There are other alternative approaches that have not been investigated in this study. The

use of VAR and VECM techniques can provide further valuable information regarding long-

run price elasticities as well as the causal nature of the data. Further research of this nature

will be considered in an extension to this project.

REFERENCES

Akmal, M., and Stern, D. (2001), ‘Residential Energy Demand in Australia: An Application

of Dynamic OLS’, Centre for Resource and Environmental Studies, Australian

National University (ANU).

Belke, A., Dreger, C. and de Haan, F. (2010), ‘Energy Consumption and Economic Growth:

New Insights into the Cointegration Relationship’, Ruhr Economic Papers #190,

Ruhr-Universität Bochum (RUB), Germany.

Bernstein, R. and Madlener, R. (2010), ‘Short- and Long-Run Electricity Demand

Elasticities at the Subsectoral Level: A Cointegration Analysis for German

Manufacturing Industries’, E.ON Energy Research Center, RWTH Aachen

University, Germany.

Best, R. (2008), ‘An Introduction to Error Correction Models’, Oxford Spring School for

Quantitative Methods in Social Research.

BREE, (2012), Australian Energy Statistics. Available at

http://www.bree.gov.au/publications/aes-2012.html

Cao, K., Wong, J. and Kumar, A. (2012), “Modelling the National Greenhouse and Energy

Reporting System (NGER) energy consumption under-coverage”, Australian

Bureau of Statistics (ABS) research paper, available at

http://www.abs.gov.au/ausstats/[email protected]/mf/1351.0.55.040

Cao, K., Wong, J. and Kumar, A. (2013), “Modelling the National Greenhouse and Energy

Reporting System (NGER) energy consumption under-coverage”, Australian

Economic Review, upcoming June 2013 issue.

21

Che, N. and Pham, P. (2012), ‘Economic Analysis of End-use Energy Intensity in

Australia’, Bureau of Resources and Energy Economics (BREE) research paper.

Cooper, J. (2003), ‘Price elasticity of demand for crude oil: estimates for 23 countries’,

Department of Economics at Glasgow Caledonian University working paper.

Medlock, K. (2009), ‘Energy Demand Theory’, in J. Evans and L.C. Hunt (eds),

International Handbook on the economics of Energy, Edward Elgar, Cheltenham.

Roarty, M. (2008), ‘Australia’s natural gas: issues and trends’, Department of

Parliamentary Services (DPS).

Ryan, L. and Plourde, A. (2009), ‘Empirical modelling of energy demand’, in J. Evans and

L.C. Hunt (eds), International Handbook on the economics of Energy, Edward

Elgar, Cheltenham.

Samimi, R. (1995), ‘Road transport energy demand in Australia: A cointegration

approach’ Energy Economics, Vol. 17, No. 4, pp. 329-339.

Soytas, U., Sari, R. and Ozdemir, O. (2001), ‘Energy Consumption and GDP Relations in

Turkey: A Cointegration and Vector Error Correction Analysis’, Economies and

Business in Transition: Facilitating Competitiveness and Change in the Global

Environment Proceedings, 2001, Global Business and Technology Association, pp.

838-844.

Steinbuks, J. (2010), ‘Interfuel Substitution and Energy Use in the UK Manufacturing

Sector’, EPRG Working Paper 1015, University of Cambridge.

APPENDIXES

Table A1. Energy Consumption (PJ), Manufacturing

Energy Source Other Energy Sources

Year Electricity Gas

Refinery feedstock Coke

Petroleum products

1973-74 87.6 85.7

1 230.1 139.4 169.9

1974-75 88.4 93.1

1 231.9 148.6 167.1

1975-76 90.1 103.3

1 233.7 135.3 163.9

1976-77 94.7 117.5

1 289.8 132.6 177.5

1977-78 97.6 134.2

1 331.1 130.0 182.3

1978-79 103.3 148.8

1 320.4 141.9 168.4

1979-80 109.9 179.1

1 312.8 137.1 161.6

1980-81 115.4 198.6

1 261.7 116.3 149.4

1981-82 118.0 206.1

1 276.1 124.7 144.6

1982-83 116.5 212.5

1 235.6 96.4 129.7

1983-84 133.6 215.7

1 260.9 95.3 140.3

1984-85 147.1 245.7

1 267.5 94.9 135.6

1985-86 155.6 264.3

1 247.2 89.3 136.0

1986-87 163.7 278.5

1 233.4 86.0 138.8

1987-88 177.6 284.5

1 321.6 82.3 146.8

1988-89 190.6 291.3

1 345.7 86.0 152.1

1989-90 196.7 300.2

1 386.3 114.4 142.9

1990-91 197.7 303.7

1 421.4 113.6 153.7

1991-92 198.3 303.2

NA 97.5 150.6

1992-93 204.9 309.2

NA 95.2 162.2

1993-94 213.9 327.2

NA 104.0 164.4

1994-95 214.0 338.2

NA 107.3 172.4

1995-96 213.2 336.0

NA 106.8 178.2

1996-97 219.6 354.4

NA 106.1 157.2

1997-98 238.6 356.3

NA 102.1 169.7

1998-99 249.8 356.6

1 675.1 106.7 168.5

1999-00 259.8 368.4

1 714.0 98.5 167.2

2000-01 265.6 397.8

1 695.0 83.6 157.0

2001-02 267.4 397.5

1 667.8 81.4 154.2

2002-03 275.6 422.0

1625.6 74.5 162.0

2003-04 277.4 431.1

1527.1 80.0 190.8

2004-05 293.5 405.0

1540.7 77.1 212.7

2005-06 293.1 404.5

1406.6 76.0 203.6

2006-07 300.4 417.0

1503.1 76.7 205.9

2007-08 307.4 414.8

1462.1 78.0 205.7

2008-09 242.9 423.1

1476.3 63.0 202.1

2009-10 240.9 439.1 1434.1 72.9 194.4

Source: Energy in Australia 2011, BREE.

23

Table A2. Augmented Dickey Fuller Tests Results

ADF Test

Variable Lag 1 Coefficient

Durbin Watson

P-Value Unit root

Original Series

Electricity Consumption -0.06** 1.77 0.1105 Yes

Natural Gas Consumption -0.10*** 1.86 0.0000 No*

Electricity Price -0.08*** 1.16 0.0218 No*

Natural Gas Price -0.03* 1.88 0.3894 Yes

Gross Value Added (GVA) -0.04 1.86 0.6833 Yes

1st Difference

Electricity Consumption -0.79*** 1.99 0.0012 No

Natural Gas Consumption -0.50*** 2.19 0.0172 No

Electricity Price -0.47*** 2.06 0.0383 No

Natural Gas Price -0.38*** 1.82 0.0730 No

Gross Value Added (GVA)

-0.93*** 1.93 0.0002 No

Note: The ADF tests for the Null hypothesis of having a unit root. Therefore when the P-value is smaller than

the critical value (0.05), the Null is rejected and the conclusion is no unit root or the series is stationary - I(0). In

a few cases (e.g. natural gas consumption and electricity price), although ADF test shows no strong evidence of

unit root, the diagnostics through Correlogram and other tests still suggest some evidence of non-stationarity.

For this reason, most of original series in this study are deemed non-stationary – I(1) while the first difference

series are stationary – I(0).