Embed Size (px)

Citation preview

Energy Services Update | Q4 2017

Deloitte’s Oiland Gas Price Forecast

Page 4

Industry Transactions

Page 10

Valuation Snapshot

Page 13

Industry Activity Update

Page 18

Q4 2016

Energy Services Update | Q4 2017

4

Deloitte’s Oil and Gas Price Forecast

8

Lessons FromPrivate Equity Event

10

Industry Transactions

13

ValuationSnapshot

18

Industry Activity Update

23

DeloitteContacts

Contents

Oil and Gas Price ForecastPage 4

Lessons From Private EquityPage 8

Industry Activity UpdatePage 18

2

Deloitte, one of Canada's leading

professional services firms, provides audit,

tax, consulting, and financial advisory

services. Deloitte LLP, an Ontario limited

liability partnership, is the Canadian

member firm of Deloitte Touche Tohmatsu

Limited.

Deloitte refers to one or more of Deloitte

Touche Tohmatsu Limited, a UK private

company limited by guarantee, and its

network of member firms, each of which is

a legally separate and independent entity.

Please see www.deloitte.com/about for a

detailed description of the legal structure of

Deloitte Touche Tohmatsu Limited and its

member firms.

© Deloitte LLP and affiliated entities.

Energy Services Update | Q4 2017

THE DATA IS IN for the Q4 2017 Energy Services Update.

This update examines the current M&A environment,

transaction-based valuation multiples and key trends.

This quarter’s featured article is from Deloitte Resource

Evaluation and Advisory’s report "Deloitte’s Oil And Gas

Price Forecast December 31, 2017" and provides a forward

view of the oil and gas market.

Deloitte Corporate Finance distinguishes itself by bringing

deep industry experience and access to buyers anywhere in

the world through a global network and exposure to a

diverse range of capital providers. Our multi-disciplinary

global team combines industry-specific knowledge with

practical and valuable experience. Our corporate finance

professionals provide strategic advice and specialized

assistance with divestitures, acquisitions and capital raising

to a broad base of clients.

3

Introduction

For more information,

or if you have any

questions, please contact:

Jason Ding

Managing Director

Edmonton

Deloitte Corporate Finance

Mobile 780 803 8677

Kevin Becker

Executive Director

Calgary and Vancouver

Deloitte Corporate Finance

Mobile 778 989 8773

Energy Services Update | Q4 2017

Deloitte’s Oil And Gas Price Forecast –December 2017

4

Energy Services Update | Q4 2017

Energy Services Update | Q4 2017

The past year has seen relatively

stable oil prices, with relative

optimism for the future as OPEC

extended its current production

cuts until the end of 2018 and

global oil demand growth remains

strong. Both factors are key steps

towards rebalancing the global

crude oil market and reducing

world crude inventories. Over the

last quarter, crude oil prices rose

on news of continued compliance

by OPEC participating nations and

the expectation the cuts would

continue into 2018; however, the

differential between Brent and WTI

prices has widened over the last

year to over $6 USD/bbl, as Brent

prices have grown more than WTI.

WTI price growth has been

dampened by increased oil

production in the United States

(US), which has resulted in

transportation constraints and

continental oversupply. Rig counts

in the US have risen throughout

the year, leading to near-record oil

production rates in 2017.

Currently, tight oil plays represent

almost half of US crude oil

production, with a flurry of

development in the Permian and

Eagle Ford basins leading the way.

Long term, WTI prices should be

buoyed by the increased ability of

the US to export light sweet crude

oil to large consumer markets such

as Asia. US crude oil exports to

Asia rose in 2017 and accounted

for approximately 33 percent of all

crude oil export volumes, making

Asia the second-largest destination

for US crude. It is expected the

current differential will narrow as

US exports continue to increase to

take advantage of higher

waterborne prices.

Overall, annual crude oil import

volumes in the US are similar to

those in 2016. Canadian exports to

the US remain immobile while

heavy oil competitors Mexico and

Venezuela continue to decrease

their supply to the US. Canadian

heavy crude oil differentials to WTI

have increased over the last

quarter as increasing supply from

oil sands projects has sparked

concerns over transportation

bottlenecks. However, as the US

continues to ramp up light oil

production, and similar quality

heavy oil imports from Venezuela

and Mexico decline, the demand

for Canadian heavy crude should

continue to grow, barring any

changes to current crude slates

and refinery configurations in the

US Gulf Coast region. If Canada

can increase its market share and

access US heavy oil refining

capacity, we expect the price

differential between WCS and WTI

prices to taper or at least be

moderate when compared to the

historical differential.

Considering the increase in crude

oil prices over the last two

quarters and the increased heavy

oil price differential, Deloitte has

forecast WTI to be USD 55.00/bbl

in 2018 and WCS to be

C$46.40/bbl.

Deloitte’s Oil and Gas Price Forecast – Q4 2017

“The rearview mirror is always clearer than the windshield.”

- Warren Buffet

5

Authors: Deloitte’s Resource Evaluation and Advisory group

Source: US Energy Information Administration

Energy Services Update | Q4 2017

6

Deloitte’s Oil and Gas Price Forecast – Q4 2017continued

On the natural gas side, Canadian

prices were extremely volatile in

2017, with the differential to Henry

Hub fluctuating substantially over

the year, often to great effect on a

day-by-day basis. The summer

months saw large discrepancies

between AECO and Henry Hub

prices as Canadian producers felt

the effects of midstream

infrastructure maintenance

projects amid steady natural gas

production. AECO prices witnessed

traces of recovery in Q4 2017 due

to the resumption of transportation

systems to full capacity operations.

However, it is expected 2018

prices may have similar price

volatility in the summer months as

more maintenance projects are

planned. Historical price

fluctuations over the last 10 years

show AECO prices were on average

20 percent higher in winter months

than summer months. Deloitte has

accounted for this seasonal price

fluctuation when forecasting AECO

prices for 2018.

In addition to infrastructure issues

in Canada, AECO prices have also

been affected by increased US

natural gas production through

both shale gas plays and solution

gas from tight oil fields. Currently,

22 percent of US shale gas

production (11 percent of total gas

production) is attributed to solution

gas from the Permian, Eagle Ford,

and Bakken tight oil drilling. This

equates to over 10 Bcf/d of gas

from oil plays that affect the

supply-and-demand balance. With

increased domestic supply, the US

can export additional volumes to

Mexico by pipeline and abroad

through LNG facilities. The US

grew its natural gas export market

by 31% in 2017, with the majority

of pipeline export volumes directed

to Mexico, and an increase in LNG

export volumes more than three

times 2016 average volumes.

Henry Hub prices reflect US

optionality to export markets as

prices have remained relatively

stable throughout 2017. Natural

gas export volumes from Canada

to the US were flat in 2017,

demonstrating that the US does

not require additional volumes

from Canada to meet domestic

demand.

Canada’s limited ability to access

new markets, combined with

increased US natural gas

production, results in low AECO

pricing as the US continues to

expand its transportation

infrastructure and export markets.

Considering natural gas pricing

seasonality and increased

production in the US, Deloitte has

forecast AECO to be C$2.00/Mcf

and Henry Hub to be USD 2.80/Mcf

in 2018.

Source: US Energy Information Administration

Energy Services Update | Q4 2017

7

Deloitte’s Oil and Gas Price Forecast – Q4 2017continued

Trends to Watch In 2018:

• Q1 2017 saw a surge in

drilling activity, which led to

crew shortages and cost

escalations. More of the same

can be expected in 2018 as

producers take advantage of

stable, growing prices. Drilling

and completion costs will likely

rise as competition for rigs

increases.

• Uncertainty of AECO pricing

in a volatile environment

may hinder Canadian dry

gas producers from moving

forward with their

development plans.

Producers may be quick to shut

in production if there are

similar maintenance outages to

those that occurred in summer

2017. Companies will also likely

hedge significant volumes to

protect against price volatility.

• Light oil development,

particularly in

Saskatchewan and

southeast Alberta, should

continue at a consistent

pace. Expansion of enhanced

oil recovery operations will

most likely be an area of

increased production volumes

in certain conventional plays

such as the Viking and Midale

formations.

• Total bitumen production

may for the first time

exceed 3 MMbl/d.

Incremental production of

existing in-situ operations and

expansion projects are

scheduled to come on-stream

in 2018. The new Sturgeon

refinery, Alberta’s first new

refinery to be built in 30 years,

is scheduled to begin

operations in spring 2018 with

an upgrading capacity of

50,000 bbl/d.

• Producers will continue to

target liquid-rich gas plays

in the Deep Basin.

Condensate prices are

increasing as the domestic

condensate supply does not

meet increased demand for

expanding bitumen production.

It is expected the demand for

condensate will rise due to

increased bitumen capacity

from oil sands expansion

projects. In addition, if

proposed crude oil pipeline

projects move forward,

increased diluent will be

required to transport heavy oil.

Partial upgrading potential and

increased transport capacity by

train would slow the demand

for diluent; however, rail

transport is more costly than

pipelines and partial upgrading

is relatively new to the

industry.

Click here to view the entire forecast

Source: US Energy Information Administration

Energy Services Update | Q4 2017Energy Services Update | Q4 2017

Lessons From Private Equity Event

8

Energy Services Update | Q4 2017

Deloitte has interviewed top Private Equity (PE) firms in Alberta to gain greater insight into value creation strategies for private companies.Please join us for breakfast, networking and a panel discussion on Wednesday, February 28, 2018, where we will discuss lessons learned from PE including the key ingredients for success and how to develop a sustainable framework for your private business.

Jamie Avey and Jason Ding in Deloitte’s Corporate Finance and M&A Advisory practice will moderate an informative panel discussion which will host the following panelists:

• Gord Boersma, Vice President, Investments – Mosaic Capital Corporation

• Alan Lever, Partner –Torquest Partners

• Paul Shaw, Vice President, Private Equity – Regimen Partners

• David Sparrow, Managing Director – Forbes Bros. Capital Ltd.

• Al Stanley, CEO – Universal Rail Systems Ltd.

Top PE firms have a disciplined framework of strategies and tactics that allow them to increase the value of a private company and then exit for a significant return on investment. As a business owner, it is important to understand these perspectives to create the right strategy and structure at your company that will enhance value regardless of your investment horizon or succession plans.We look forward to seeing you on February 28!

Lessons From Private Equity Event

Deloitte is hosting a “Lessons From Private Equity” event in Edmonton on February

28, 2018, following a similar event in Calgary that was hosted last year.

9

Event details:

When: Wednesday February 28, 2018

Where: Varscona Hotel8208 106 Street NW,Edmonton, AB

Registration:7:00 – 7:30am

Breakfast: 7:30 – 8:00am

Presentation and Q&A: 8:00 – 9:00am

Click here to register for the event

Energy Services Update | Q4 2017Energy Services Update | Q4 2017

Industry Transactions

10

Energy Services Update | Q4 2017

The North American energy

services industry had closed 26

transactions in Q4, up from 22 in

Q3, and the highest in one quarter

seen since Q4 2014. Total

transaction value was also up,

from $2.0 billion in Q3 to $7.8

billion in Q4. In 2017, total

transaction value was down

slightly, from $26.2 billion in 2016

to $25.3 billion in 2017. This is

primarily due to the fact that 2016

included the landmark $22 billion

Cameron/Schlumberger

transaction which closed in April

2016. If we exclude that massive

transaction, transaction value was

up considerably – from $4.2Bn in

2016 to $25.2Bn in 2017.

Of the 26 transactions that closed

in the quarter, 12 disclosed

transaction values, which ranged

from $0.2 million to $3.0 billion,

for a combined $8.6 billion.

Two transactions were greater

than $1 billion – one at $2.3Bn and

one at 3.0Bn. The only transaction

that involved a Canadian company

and disclosed a transaction value

was the acquisition of C&J’s

Production Services Canada group

by Calgary-based CWC Energy

Services for approximately $38

million.

In addition to the transactions that

closed in Q4 2017, which are

highlighted on the following page,

a significant transaction which has

been announced in 2018 is the

acquisition of Energy Transfer

Partners LP’s CDM Resource

Management by Austin-based USA

Compression Partners (USACP) for

approximately USD 1.7 billion.

Through this acquisition, USACP

will roughly double their fleet and

expand its footprint to all major

basins in the US, including the

Eagle Ford, the Gulf Coast, and the

Rockies. While the price per

horsepower was higher than

USACP’s existing valuation, the

EV/EBITDA multiple was lower

than USACP’s, implying that CDM’s

assets are better at generating

earnings than USACP’s existing

assets.

Industry Transactions

11

Energy Services Update | Q4 2017

Select North American transactions include:

October 6, 2017Ensco plc (“Ensco”) acquired

Atwood Oceanics, Inc. (“Atwood”)

for USD 2.2 billion to create a

powerhouse ocean drilling rig

company. The combined company’s

fleet consists of 27 floating rigs

(semisubmersibles and drillships),

of which 23 are ultra-

deepwaterdrilling rigs that are

capable of drilling in water depths

of 7,500 feet or greater. The

combined fleet also comprises 38

jackuprigs, for a combined total of

65 drilling rigs.

October 30, 2017Global Infrastructure Partners

(“GIP”) purchased Medallion

Gathering and Processing

(“Medallion”) for USD 1.8 billion.

Medallion is the largest privately-

held crude oil transportation

system in the Midland Basin of

West Texas, with over 800 miles of

pipeline, approximately 670,000

dedicated acres, and total areas of

mutual interest approaching four

million acres. Medallion is widely

regarded as the leading source of

crude oil transportation in the

Midland Basin.

October 30, 2017C&J Energy Services (“C&J)

completed two transactions in

October, the first an acquisition of

O-Tex Pumping (“O-Tex”) for

USD 245.4 million, and the second

a divestiture of their C&J

Production Services Canada asset

(“Canada”) for $37.5 million.

Through the acquisition of O-Tex,

the US’s fourth largest provider of

oilfield cementing services, C&J

continued to strengthen its position

as a leading oilfield services

provider with a best-in-class well

construction, intervention and

completions platform.

Simultaneously, C&J sold Canada

to CWC Energy Services, allowing

C&J to focus their efforts on the

US.

12

26 transactions accounted for $7.8 billion in North American Energy Services

M&A activity in the fourth quarter of 2017.

Industry Transactions continued

North American Energy Equipment and Services M&A Activity

0.0x 5.6x 8.5x 4.3x 7.5x 8.4x 7.8x 7.6x 4.6x 19.7x 4.5x 4.1x 0.0x 8.9x 0.0x 0.0x 16.1x 12.5x 206.5x 5.3x

16

26

3833

4747

42 43

1924

1822 22 21

17

2421 20 22

26

1014 13 14

2218 23

14

8 9

3

9 117 6

128

11 912

0

12

24

36

48

60

0.0x

5.0x

10.0x

15.0x

20.0x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016 2017

Nu

mb

er o

f tr

an

sacti

on

s

clo

sed

Averag

e E

V/EB

ITD

A

Average disclosed EV/EBITDA Number of closed transactions Closed transactions with disclosed values

Energy Services Update | Q4 2017Energy Services Update | Q4 2017

Valuation Snapshot

13

Energy Services Update | Q4 2017

The forecast consensus median

EV/NTM EBITDA multiple (“multiple”)

for Drilling and Drilling Services

companies increased to 8.5x in Q4

2017, significantly higher than Q3’s

7.9x, and another step up from Q2’s

low of 6.4x. Q4 2017 multiples are

now a full turn above than their five-

year rolling average of 7.4x. Steady

strengthening in oil prices during the

second half of the year likely led to

the increase in share prices while

analyst NTM EBITDA forecasts

decreased slightly on average,

resulting in a higher multiple.

14

Drilling and Drilling Services (all values in CAD mm)

Valuation Snapshot

EV multiples

Company Enterprise

value (EV)

LTM

EBITDA

NTM

EBITDA

LTM

EBITDA

NTM

EBITDA

Precision Drilling Corporation 2,763 278 323 9.9x 8.6x

Ensign Energy Services Inc. 1,716 194 227 8.9x 7.6x

Pason Systems Inc. 1,387 69 112 20.2x 12.4x

Total Energy Services Inc. 1,016 51 122 20.1x 8.3x

Trinidad Drilling Ltd. 953 83 132 11.5x 7.2x

Western Energy Services Corp. 344 27 36 12.9x 9.5x

High Arctic Energy Services Inc 190 64 46 3.0x 4.2x

PHX Energy Services Corp. 157 7 34 22.5x 4.6x

Xtreme Drilling Corp. 148 (1) 15 NM 9.8x

AKITA Drilling Ltd. 128 (4) 10 NM 13.5x

Cathedral Energy Services Ltd. 84 10 14 8.1x 6.2x

McCoy Global Inc. 32 (9) 2 NM 14.4x

Adjusted average 10.2x 8.8x

Adjusted median 9.9x 8.5x

Drilling and Drilling Services Median EV/NTM EBITDA

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016 2017

Median EV / NTM EBITDA Rolling five-year average

Energy Services Update | Q4 2017

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016 2017

Median EV / NTM EBITDA Rolling five-year average

Production and Well Services Median EV/NTM EBITDADuring Q4 2017, Production and

Well Services companies’ median

EV/NTM EBITDA decreased to 7.7x,

0.5x lower than the previous

quarter. The steady decline in

multiples began in Q2 2016 when

our dataset reached a high of 14.5x,

and has now fallen well-below the

five-year rolling average of 8.9x.

While analyst consensus NTM

EBITDA estimates continued to

improve in Q4 2017, EVs remained

stable quarter-over-quarter, which

continues to decrease the multiples.

15

Driven by oil prices that continue to strengthen, well completion activity is

likely expected to be higher during the next 12 months than the last 12

months, leading to a positive EBITDA impact. As a result, median EV/NTM

EBITDA (7.7x) is lower compared to LTM EBITDA (10.3x).

Production and Well Services (all values in CAD mm)

Valuation Snapshot continued

EV multiples

Company Enterprise

value (EV)

LTM

EBITDA

NTM

EBITDA

LTM

EBITDA

NTM

EBITDA

CES Energy Solutions Corp. 2,158 111 184 19.4x 11.7x

ShawCor Ltd. 1,967 190 180 10.3x 10.9x

Calfrac Well Services Ltd. 1,749 92 265 18.9x 6.6x

Secure Energy Services Inc. 1,700 118 177 14.4x 9.6x

Trican Well Service Ltd. 1,556 107 253 14.6x 6.2x

Newalta Corporation 434 45 50 9.6x 8.7x

CWC Energy Services Corp. 138 11 - 12.4x NM

Strad Energy Services Ltd. 124 24 32 5.1x 3.9x

Essential Energy Services Ltd. 124 14 34 8.8x 3.7x

Adjusted average 10.8x 7.7x

Adjusted median 10.3x 7.7x

Energy Services Update | Q4 2017

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016 2017

Median EV / NTM EBITDA Rolling five-year average

Continuing the year’s see-saw,

Transportation and Logistics’

EV/NTM EBITDA multiples fell back

to 8.1x, from Q1’s 9.1x, Q2’s 8.1x,

and Q3’s 9.1x. The multiple still

remains higher than the five-year

rolling average of 7.8x.

Transportation and Logistics’

median EV/NTM EBITDA multiples

within our dataset have tended to

lay within a relatively tight range

from 6x - 8x and seem to have

returned towards historical

normalcy once again.

16

The Transportation and Logistics sub-sector has historically been less volatile

than the other energy services sub-sectors. The sub-sector this year has

bounced between 8.1x-9.1x, which is higher than the historical range of

6.1x-8.0x.

Transportation and Logistics (all values in CAD mm)

Valuation Snapshot continued

EV multiples

Company Enterprise

value (EV)

LTM

EBITDA

NTM

EBITDA

LTM

EBITDA

NTM

EBITDA

TFI International Inc. 4,463 508 560 8.8x 8.0x

Gibson Energy Inc. 3,695 262 332 14.1x 11.1x

Mullen Group Ltd. 2,047 169 190 12.1x 10.8x

Civeo Corporation 792 82 96 9.6x 8.2x

Horizon North Logistics Inc. 280 26 42 10.6x 6.7x

Black Diamond Group Limited 254 29 33 8.8x 7.6x

Adjusted average 10.7x 8.7x

Adjusted median 10.1x 8.1x

Transportation and Logistics Median EV/NTM EBITDA

Energy Services Update | Q4 2017

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016 2017

Median EV / NTM EBITDA Rolling five-year average

The Oilfield and Facility

Construction sub-sector median

EV/NTM EBITDA multiple has

generally remained within a

relatively narrow range. We note

that despite the narrow range of

the group median, individual

companies within our sample vary

considerably from 4.0x to 10.1x

EV/NTM EBITDA. Quarter over

quarter, the median EV/NTM

EBITDA remains relatively stable

(Q4 2017 of 6.3x compared to Q3

2017 of 6.4x) and equal to the

five-year rolling average of 6.3x.

17

In Q4 2017, oilfield and facility construction company median multiples

remained relatively flat at 6.3x EV/NTM EBITDA. The sub-sector’s valuation

is at the five-year rolling average of 6.3x, and it remains within the historical

range of 4.6x - 7.0x.

Oilfield and Facility Construction (all values in CAD mm)

Valuation Snapshot continued

EV multiples

Company Enterprise

value (EV)

LTM

EBITDA

NTM

EBITDA

LTM

EBITDA

NTM

EBITDA

Aecon Group Inc. 1,675 151 195 11.1x 8.6x

Enerflex Ltd. 1,563 195 263 8.0x 6.0x

Bird Construction Inc. 403 25 40 16.0x 10.1x

North American Energy Partners Inc. 270 54 68 5.0x 4.0x

Stuart Olson Inc. 258 22 41 11.7x 6.3x

Adjusted average 8.9x 7.0x

Adjusted median 9.6x 6.3x

Oilfield and Facility Construction Median EV/NTM EBITDA

Energy Services Update | Q4 2017

Industry Activity Update

18

Energy Services Update | Q4 2017

Energy Services Update | Q4 2017

(50%)

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18

Industry Activity Update

This is a deconstruction of the broader energy services sector into specific sub-sectors,

demonstrating monthly returns between January 1, 2017 and December 31, 2017.

19

2017 Sub-sector Returns (Dec 31, 2016 – Dec 31, 2017)

The sub-sector returns are based

on stock prices, weighted by

market capitalization, and is

adjusted for dividends.

The graph below illustrates the

importance of understanding sub-

sector fundamentals, as

performance has differed

considerably between the various

groups. Simply put, sub-sectors

matter within the larger energy

services industry.

With many oil and gas price

forecasts remaining relatively flat

in the near term, adaptation to

regulatory restraints for E&P and

midstream companies ongoing,

and the sector generally being out

of favor to investors, companies

are visibly adapting to a new

environment that is no longer

perceived as temporary.

While only two of the eight

subsectors referred to in the

graph below have experienced

positive returns in 2017, all

subsectors are beginning to trend

upwards. Even the drilling sub-

sector, which had been down each

month from January through

August, saw the freefall end.

Though the fall saw a recovery in

value, the end of the year was

mostly flat for oilfield services

providers.

Supermajors (15.7%)

Exploration and Geophysical 15.2%

Oilfield and Facility Construction 10.7%

Drilling Equipment (6.7%)

Transportation and Logistics (6.7%)

Enviro. and Waste Management (26.3%)

Production and Completion (12.7%)

Drilling (34.6%)

Energy Services Update | Q4 2017

0

200

400

600

800

1,000

1,200

1,400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

0%

10%

20%

30%

40%

50%

60%

70%

80%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

20

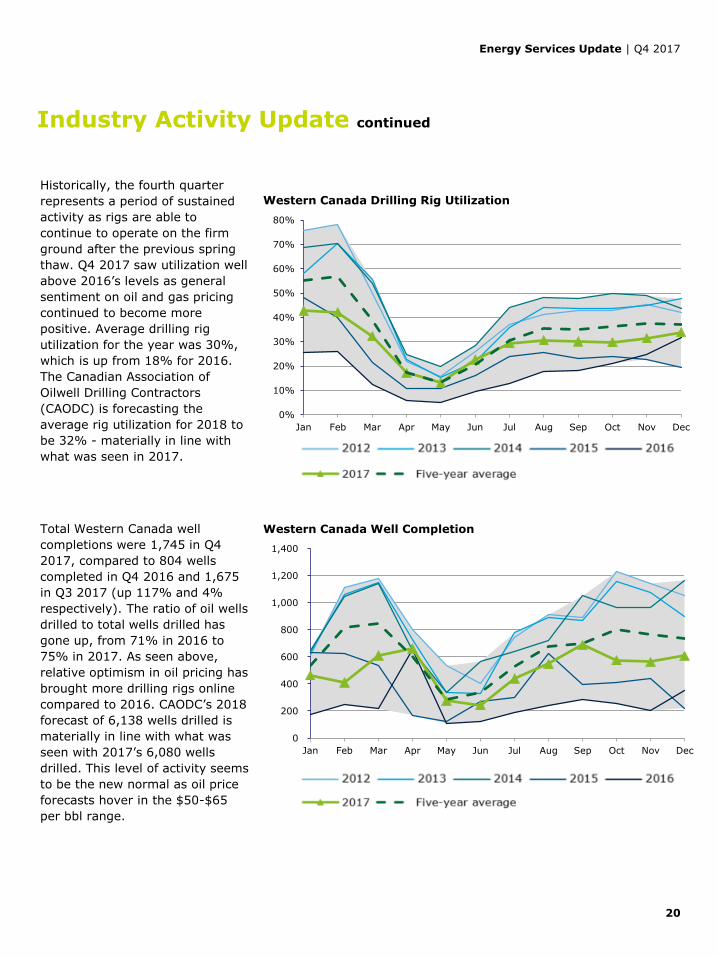

Western Canada Drilling Rig Utilization

Historically, the fourth quarter

represents a period of sustained

activity as rigs are able to

continue to operate on the firm

ground after the previous spring

thaw. Q4 2017 saw utilization well

above 2016’s levels as general

sentiment on oil and gas pricing

continued to become more

positive. Average drilling rig

utilization for the year was 30%,

which is up from 18% for 2016.

The Canadian Association of

Oilwell Drilling Contractors

(CAODC) is forecasting the

average rig utilization for 2018 to

be 32% - materially in line with

what was seen in 2017.

Industry Activity Update continued

Total Western Canada well

completions were 1,745 in Q4

2017, compared to 804 wells

completed in Q4 2016 and 1,675

in Q3 2017 (up 117% and 4%

respectively). The ratio of oil wells

drilled to total wells drilled has

gone up, from 71% in 2016 to

75% in 2017. As seen above,

relative optimism in oil pricing has

brought more drilling rigs online

compared to 2016. CAODC’s 2018

forecast of 6,138 wells drilled is

materially in line with what was

seen with 2017’s 6,080 wells

drilled. This level of activity seems

to be the new normal as oil price

forecasts hover in the $50-$65

per bbl range.

Western Canada Well Completion

Energy Services Update | Q4 2017

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$

$50

$100

$150

$200

$250

$300

$350

$400

$450

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016 2017

$ /

Hecta

re

Bonuses

(CAD

millions)

BC Total Saskatchewan Total Alberta Total

BC $ / Hectare Saskatchewan $ / Hectare Alberta $ / Hectare

21

Western Canada Land Sales

Land sales continued their robust

climb through 2017, reaching

highs in quarterly bonuses paid

not seen since 2015. This

continues the steady climb since

the beginning of 2016. The

largest land sales were in

Alberta’s petroleum and natural

gas regions, specifically in the

the Plains and Northern regions.

On a per-hectare basis across

Western Canada, the average

price paid decreased 30% to

$382/hectare as compared to

the previous quarter’s

$543/hectare, but up 30% from

a year prior (Q4 2016). In AB,

prices per hectare are at highs

not seen since Q3 2014, at

$424/hectare, up 364% since

the low of $92/hectare seen in

Q2 2015.

Companies are clearly looking to

expand, and the company that

purchased the most AB land (and

spent the most money) in the

quarter was Stomp Energy,

purchasing 43,810 hectares for a

total of $33 million. Pro West

Land Services paid the most per

hectare, at $6,180/hectare for

3,584 hectares ($22 million).

Total hectares sold in W. Canada were up 51% in 2017 compared to 2016.

Total bonus paid in W. Canada was up 289% in 2017 compared to 2016.

As a result, bonus per hectare was up 258% in 2017 compared to 2016.

Energy Services Update | Q4 2017

Abbreviations

22

Abbreviation Definition

$ Canadian dollars

USD U.S. dollars

EV Enterprise value

EBITDA Earnings before interest, tax, depreciation and amortization

LTM Last twelve months

NTM Next twelve months

QoQ Quarter over quarter - change from last quarter to this one

YTD Year to date

S&P TSX Standard & Poor's Toronto Stock Exchange Index

WCS Western Canadian Select (Alberta heavy oil price)

WTI West Texas Intermediate (oil price)

Bbl Barrel (of oil)

Ha Hectares

Energy Services Update | Q4 2017

Brian Heald Managing Director

Calgary Oil and Gas Leader

403 267 0508

Jason DingManaging Director

Edmonton Leader

780 803 8677

Contacts

23

David LamSenior Managing Director

Western Canada Leader

604 219 3878

Deloitte Corporate Finance professionals

Paul ChildersSenior Vice President

Brisbane, AU

+61 7 3308 7205

Shaun ReynoldsVice President & Director

Aberdeen, UK

+44 1224 84 7319

Global Energy Services Corporate Finance professionals

Chad Potter Assistant Director

London, UK

+44 20 7007 8952

James MillerVice President

Charlotte, NC

704 731 8230

Kong Meng YapDirector

Kuala Lumpur, Malaysia

+60 3 7610 8858

Eric AndreozziSenior Vice President

Charlotte, NC

704 333 0518

Canadian oil and gas professionals

Jamie AveyPartner

Transaction Services

403 503 1353

Paul ZonneveldPartner, Enterprise Risk Leader

Energy and Resources

403 503 1356

Kevin BeckerExecutive Director

Calgary Energy Services Leader

778 989 8773

Robert OlsenPresident

National Leader

416 726 4614

Jeff LyonsPartner

Financial Advisory

403 267 1708

Andrew LuetchfordSenior Managing Director

Debt and Capital Advisory Leader

416 601 5227

Alyson QuanVice President

Edmonton

780 421 3638

Chris LeeManaging Partner, Alberta

403 267 1751

Marc JoinerDeloitte Private leader, Prairies

403 503 1346

Andrew BotterillPartner

Resource Evaluation and Advisory

403 648 3239

Tim LynnAnalyst

Edmonton

780 686 9753

Adam FroeseAnalyst

Edmonton

780 421 3765

![Q4 FY16 Industry Update & Key Performance Highlights [Company Update]](https://img.pdfslide.us/doc/110x75/577c7f491a28abe054a3ead7/q4-fy16-industry-update-key-performance-highlights-company-update.jpg)