Embed Size (px)

Citation preview

Energy Security; Qatar Crisis and Global Gas Security

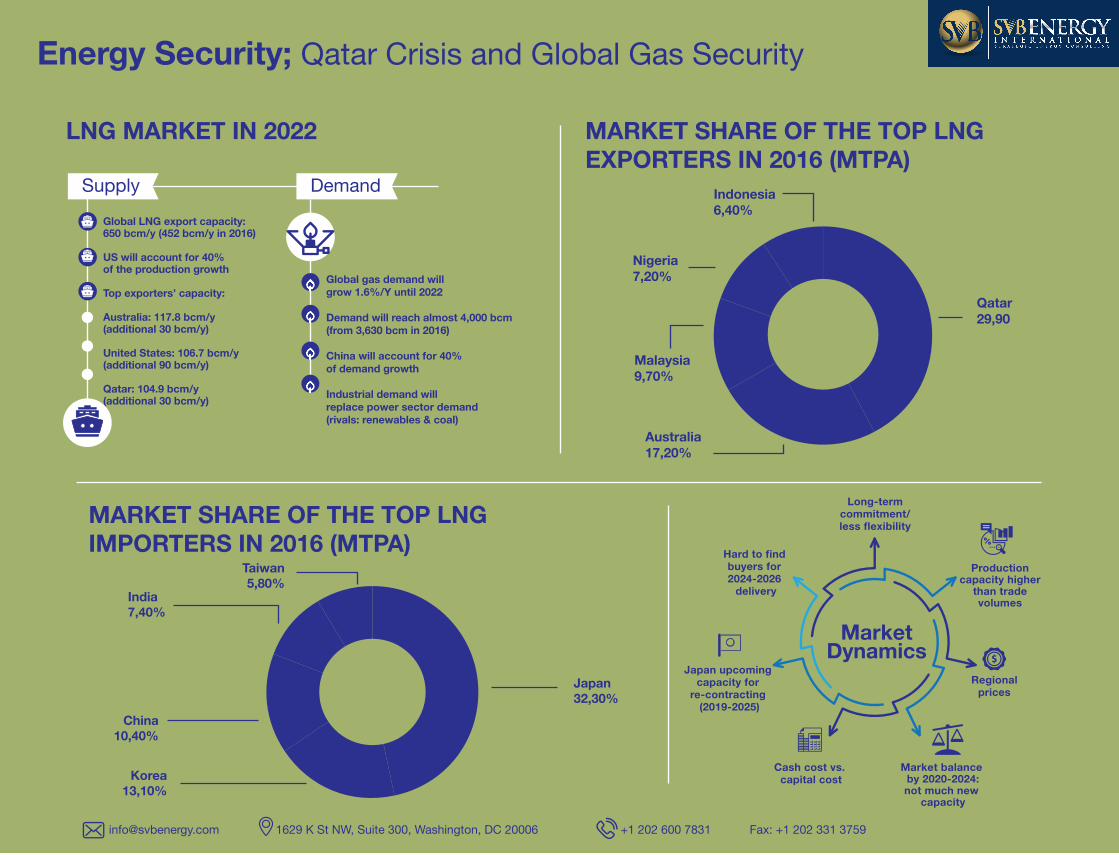

LNG MARKET IN 2022

MarketDynamics

Long-term commitment/ less flexibility

Production capacity higher

than trade volumes

Regionalprices

Market balance by 2020-2024:not much new

capacity

Cash cost vs. capital cost

Japan upcoming capacity for

re-contracting (2019-2025)

Hard to find buyers for 2024-2026

delivery

[email protected] 1629 K St NW, Suite 300, Washington, DC 20006 +1 202 600 7831 Fax: +1 202 331 3759

Supply DemandGlobal LNG export capacity:650 bcm/y (452 bcm/y in 2016)

US will account for 40%of the production growth

Top exporters’ capacity:

Australia: 117.8 bcm/y(additional 30 bcm/y)

United States: 106.7 bcm/y(additional 90 bcm/y)

Qatar: 104.9 bcm/y(additional 30 bcm/y)

Global gas demand willgrow 1.6%/Y until 2022

Demand will reach almost 4,000 bcm(from 3,630 bcm in 2016)

China will account for 40%of demand growth

Industrial demand willreplace power sector demand(rivals: renewables & coal)

MARKET SHARE OF THE TOP LNG EXPORTERS IN 2016 (MTPA)

MARKET SHARE OF THE TOP LNG IMPORTERS IN 2016 (MTPA)

Japan32,30%

Taiwan5,80%

India7,40%

China10,40%

Korea13,10%

Qatar29,90

Indonesia6,40%

Nigeria7,20%

Australia17,20%

Malaysia9,70%

Energy Security; Qatar Crisis and Global Gas Security

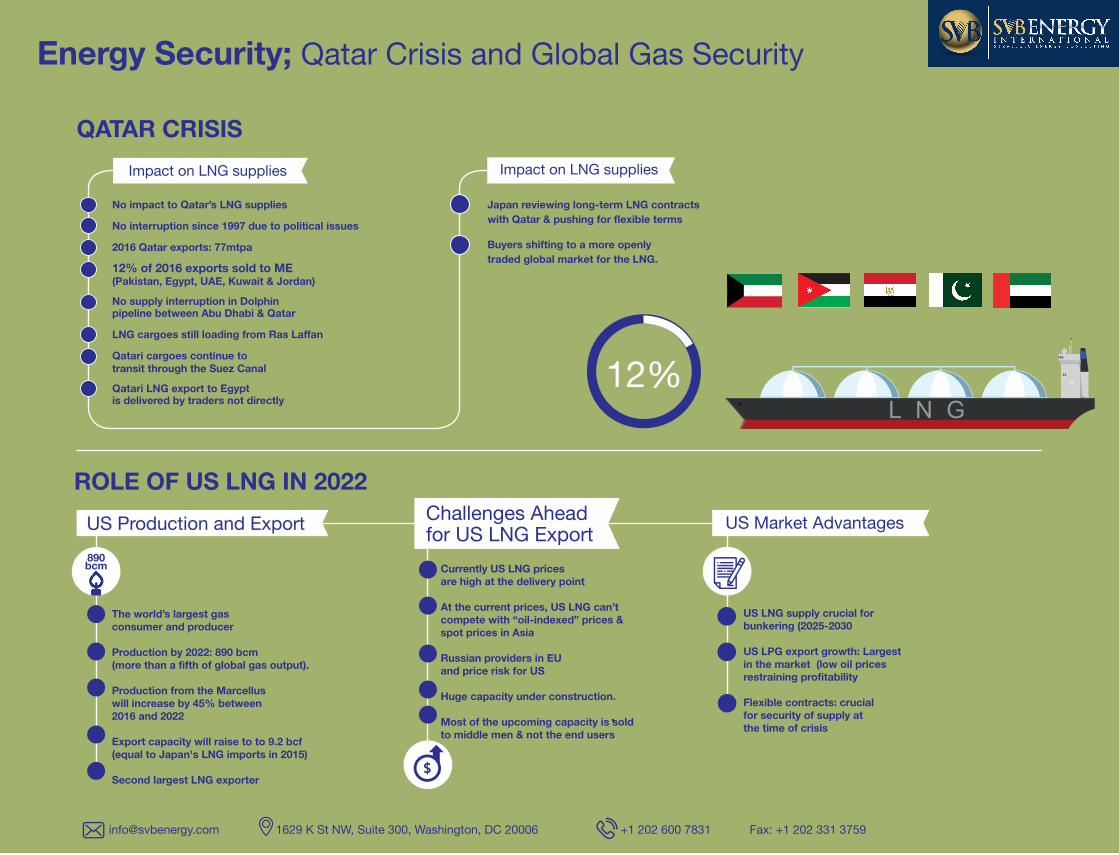

ROLE OF US LNG IN 2022

QATAR CRISIS

Currently US LNG pricesare high at the delivery point

At the current prices, US LNG can’t compete with “oil-indexed” prices & spot prices in Asia

Russian providers in EUand price risk for US

Huge capacity under construction.

Most of the upcoming capacity is sold to middle men & not the end users

US LNG supply crucial for bunkering (2025-2030

US LPG export growth: Largest in the market (low oil prices restraining profitability

Flexible contracts: crucialfor security of supply atthe time of crisis

[email protected] 1629 K St NW, Suite 300, Washington, DC 20006 +1 202 600 7831 Fax: +1 202 331 3759

US Production and Export US Market Advantages

The world’s largest gasconsumer and producer

Production by 2022: 890 bcm(more than a fifth of global gas output).

Production from the Marcelluswill increase by 45% between2016 and 2022

Export capacity will raise to to 9.2 bcf (equal to Japan's LNG imports in 2015)

Second largest LNG exporter

No impact to Qatar’s LNG supplies

No interruption since 1997 due to political issues

2016 Qatar exports: 77mtpa

12% of 2016 exports sold to ME(Pakistan, Egypt, UAE, Kuwait & Jordan)

No supply interruption in Dolphinpipeline between Abu Dhabi & Qatar

LNG cargoes still loading from Ras Laffan

Qatari cargoes continue totransit through the Suez Canal

Qatari LNG export to Egyptis delivered by traders not directly

Impact on LNG supplies

Japan reviewing long-term LNG contractswith Qatar & pushing for flexible terms

Buyers shifting to a more openlytraded global market for the LNG.

Impact on LNG supplies

Challenges Aheadfor US LNG Export

890bcm

12%

![Performance Evaluation and Analysis of Sparse Matrix and ... · sparse matrix-matrix multiplication (SpGEMM) algorithms [32,30] for hetero-geneous processors. Said et al. [40] demonstrated](https://img.pdfslide.us/doc/110x75/60429ca42c0b8a1ecf5cdafd/performance-evaluation-and-analysis-of-sparse-matrix-and-sparse-matrix-matrix.jpg)