Embed Size (px)

Citation preview

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 1/24

x*x,z0 u*w *u./,u} ,x-+/,vx-

B]TaVh ^dc[^^Z U^a @WX]P

{*w/-.,{u} ~u,|x.-

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 2/24

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 3/24

Energy outlook for China 1

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

Contents

1 Introduction 2

2 Hungry for power 4

3 China’s power challenges 6

4 Domestic power generation 8

5 China’s global energy hunt 15

6 Heading for a power crunch? 18

7 Sum mary 19

Appendix — China demographics 20

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 4/24

2 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

1 Introduction

Roger Munnings

The energy needs of the People’s

Republic of China (PRC) are a major

factor in the com plex global energy

demand and supply equation. Their

import ance w ill increase as the PRC’s

economy cont inues to expand and

each year larger percentages of its

population seek higher living standards.

The issues and challenges of ef ficient

energy supply to a demanding

industrial complex and an eager

population in the PRC w ill continue to

be an underlying component of

international political relationships, the

w orld’s capital market systems and

their adequacy for meeting long term

energy investment requirements and

aspirations to sustain and improveliving environments everywhere.

This paper summ aries these issues and

challenges — and I am pleased to

introduce it.

KPM G aims to contribute to the

development of the energy industries

around the w orld in our areas of

competence, which include financial

management and control, corporate

management and governance system s,

financial structuring and capital

efficiency and information presentation

and independent attestation — and

have been built over many years. We

have global coverage. Our international

credentials are based around having

strong national capabilities in over 150

countries in which we are present

together with t he ability to w ork

know ledgeably and efficiently across

international boundaries.

KPM G in the PRC has led the w ay,

w orking on privatisation and capital

markets entry with major Chinese

companies w ith the support of KPMG

colleagues from around the world from

our Global Energy and National

Resources practice.

We look forward to using our China

based capability and our international

experience to bring value to t he PRC

and its companies in the future.

Roger Munnings

Chairman, Global Energy &

Natural Resources practice and

Chairman and Chief Executive Of ficer,

KPM G in Russia/Comm onw ealth of

Independent States Region

Tel: +7 095 937 2501

e-Mail: [email protected]

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 5/24

Energy outlook for China 3

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

Nelson Fung

China’s surging economy and grow ing

prominence on the w orld stage are

increasingly shaping the econom ies

and energy markets of the Asia Pacific

region. As demand for power continues

to outstrip production at hom e, China is

fast becoming a buyer of energy, both

in the region and around the w orld. It

already has strategic pow er

partnerships w ith around 50 countries,

many of them in Asia1.

China’s emergence as a leading

economy and world power is no flash

in the pan. Four-fifths of t he w orld’s

500 largest organisations now have a

mainland presence. GDP growth

reached 9.5 per cent for the year and is

forecast to remain strong. Meanwhile,utilised foreign direct investment in China

last year reached US$60.6 billion

as multinational investor interest

gathered further m omentum 2.

China is stepping up energy production

in a bid to m eet surging demand.

According to preliminary statistics

released in late February 2005 by the

National Development and Reform

Commission (NDRC — China’s leading

economic planning agency), coal

output in 2004 climbed 17.3 per cent to

1.96 billion tons while electricity output

rose 14.8 per cent to 21.9 trillion

kilowatt (kw) hours. Meanwhile, natural

gas production climbed sharply by

18.5 per cent to 40.8 billion cubic (cu)

met res (m).

Following the continued economic

upsurge, China has embarked on a

number of signif icant energy projects

including the gigantic Three Gorges

Project, the world’s largest water

control facility. Wit h the seventh

generator of the Three Gorges Project

going into operation in November 2004,

China has its aggregate installed

capacity exceeding 400 m illion

kilowatts (kw) and now ranks second in

the w orld in terms of pow er generation

capacity3.

The Chinese government’s increasingly

cohesive energy strategy is beginning

to pay dividends, while a growing

number of foreign power companies

are gaining access to m ajor projects in

the m ainland market.

KPMG’s experience in mainland China

and the Asia Pacific region has alreadyhelped power organisations — both

mult inational and Chinese — w ith their

operations and strategies. Today, w e

have more than 3,500 professionals on

the ground in China w ith off ices in

Beijing, Guangzhou, Shanghai,

Shenzhen, Macau and Hong Kong.

Nelson Fung

Partner in charge,

Energy & Natural Resources practice and

Industrial Markets practice,

KPMG in China and Hong Kong Special

Administrative Region (SAR)

Tel: +852 2826 7215

e-M ail: [email protected] .hk

1International Energy Agency, World Energy Outlook 2004 p267; China International Business, September 2004: “ Relieving the energy tensions” ;

Agence France-Presse, 11 February 2005: “ Energy-hungry China digs deeper to boost oil reserves by 25 pct “ ; World News Connection, 28 M ay 2004:

“ Japan: Article reviews China energy short age, says China Trades ‘Weapons for Oil’”

2Associated Press Asia, 13 January 2005: “ China sees foreign investment surge t o US$60.6 billion in 2004”

3Xinhua’s China Economic Information Service, 27 December 20 04: “ China’s power short age to ease in 2006:official”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 6/24

4 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

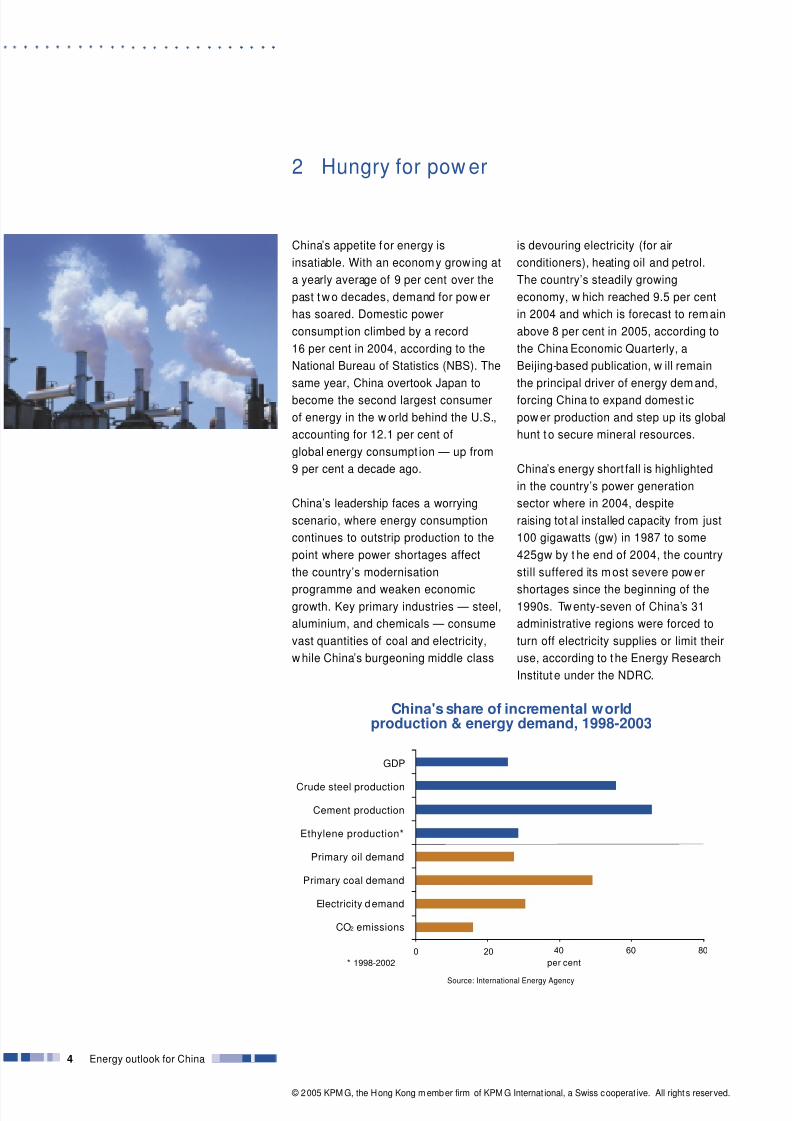

2 Hungry for pow er

0 20 40 60 80

per cent

China's share of incremental w orldproduction & energy demand, 1998-2003

GDP

Crude steel production

Cement production

Ethylene production*

Primary oil demand

Primary coal demand

Electricity d emand

CO2 emissions

Source: International Energy Agency

* 1998-2002

China’s appetite for energy is

insatiable. With an economy grow ing at

a yearly average of 9 per cent over the

past t w o decades, demand for pow er

has soared. Domestic power

consumpt ion climbed by a record

16 per cent in 2004, according to the

National Bureau of Statistics (NBS). The

same year, China overtook Japan to

become the second largest consumer

of energy in the w orld behind the U.S.,

accounting for 12.1 per cent of

global energy consumpt ion — up from

9 per cent a decade ago.

China’s leadership faces a worrying

scenario, where energy consumption

continues to outstrip production to the

point where power shortages affect

the country’s modernisation

programme and weaken economicgrowth. Key primary industries — steel,

aluminium, and chemicals — consume

vast quantities of coal and electricity,

w hile China’s burgeoning middle class

is devouring electricity (for air

conditioners), heating oil and petrol.

The country’s steadily growing

economy, w hich reached 9.5 per cent

in 2004 and which is forecast to rem ain

above 8 per cent in 2005, according to

the China Economic Quarterly, a

Beijing-based publication, w ill remain

the principal driver of energy dem and,

forcing China to expand domest ic

pow er production and step up its global

hunt t o secure mineral resources.

China’s energy short fall is highlighted

in the country’s power generation

sector where in 2004, despite

raising tot al installed capacity from just

100 gigawatts (gw) in 1987 to some

425gw by t he end of 2004, the country

still suffered its m ost severe pow er

shortages since the beginning of the1990s. Tw enty-seven of China’s 31

administrative regions were forced to

turn off electricity supplies or limit their

use, according to t he Energy Research

Institut e under the NDRC.

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 7/24

Energy outlook for China 5

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

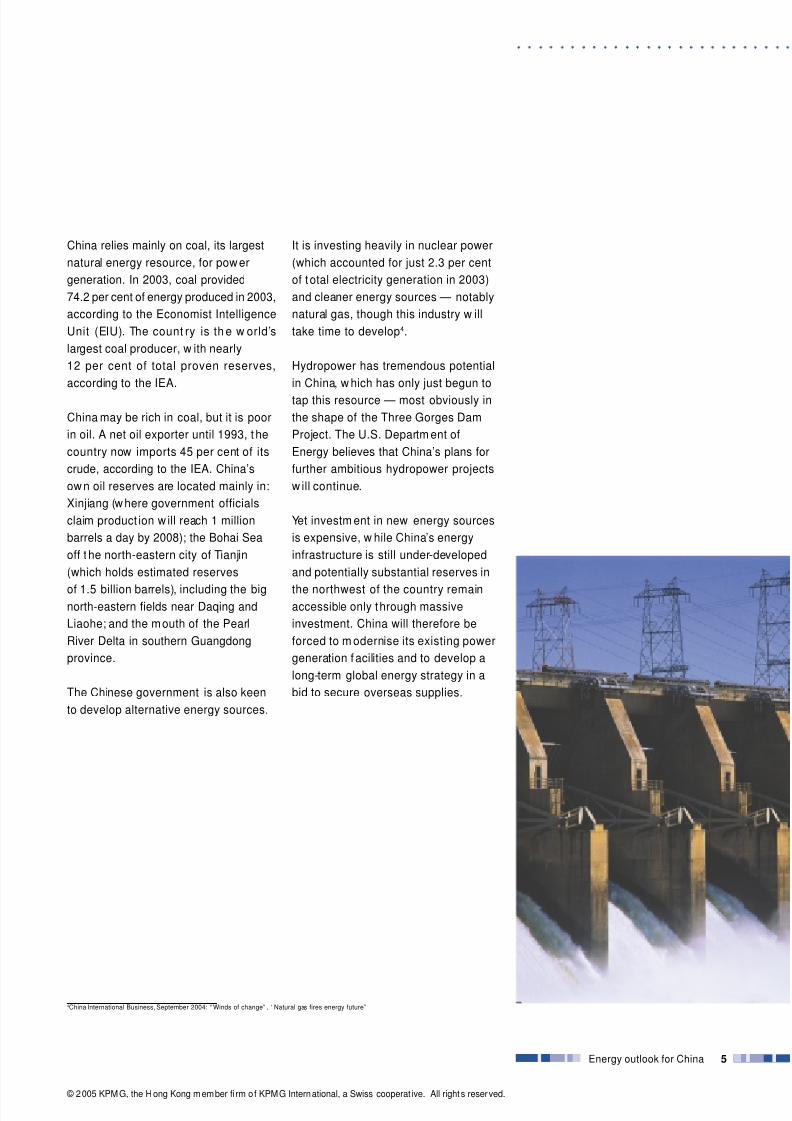

China relies mainly on coal, its largest

natural energy resource, for pow er

generation. In 2003, coal provided

74.2 per cent of energy produced in 2003,

according to the Economist Intelligence

Unit (EIU). The count ry is th e w orld’s

largest coal producer, w ith nearly

12 per cent of total proven reserves,

according to the IEA.

China may be rich in coal, but it is poor

in oil. A net oil exporter until 1993, t he

country now imports 45 per cent of its

crude, according to the IEA. China’s

ow n oil reserves are located mainly in:

Xinjiang (w here government officials

claim product ion w ill reach 1 million

barrels a day by 2008); the Bohai Sea

off t he north-eastern city of Tianjin

(which holds estimated reserves

of 1.5 billion barrels), including the bignorth-eastern fields near Daqing and

Liaohe; and the mouth of the Pearl

River Delta in southern Guangdong

province.

The Chinese government is also keen

to develop alternative energy sources.

It is investing heavily in nuclear power

(which accounted for just 2.3 per cent

of total electricity generation in 2003)

and cleaner energy sources — notably

natural gas, though this industry w ill

take time to develop4.

Hydropower has tremendous potential

in China, w hich has only just begun to

tap this resource — most obviously in

the shape of the Three Gorges Dam

Project. The U.S. Departm ent of

Energy believes that China’s plans for

further ambitious hydropower projects

w ill continue.

Yet investm ent in new energy sources

is expensive, w hile China’s energy

infrastructure is still under-developed

and potentially substantial reserves in

the northwest of the country remainaccessible only through massive

investment. China will therefore be

forced to m odernise its existing power

generation f acilities and to develop a

long-term global energy strategy in a

bid to secure overseas supplies.

4China International Business, September 2004: “ Winds of change” , “ Natural gas fires energy future”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 8/24

6 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

China faces three key challenges in

attempting to m eet growing energy

demand.

No national grid, poor transmission

Increasingly frequent and w idespread

shortages in m ajor mainland cities have

underlined the importance of creating

an effective national pow er grid and

efficient transmission network. The

Chinese government started building a

power grid by joining up the countr y’s

north and central electricity netw orks in

2003, but much work is still to be done.

In addition, pow er cables tend to be old

and not so well maintained, making

electricity transmission highly

inefficient. Effective pow er

transmission across a nationw ide grid

is essential in order to deliver elect ricity

from power plants — traditionallybased near coal and oil reserves in the

north and northeast of the

country — t o the areas of greatest

consumption, predominantly in the

south and east.

The need for a national grid w as

highlighted in mid-2004 w hen a series

of pow er cuts — previously common in

smaller cities — brought Beijing and

Shanghai to a standstill on several

occasions. Local government s resorted

to ‘cloud-busting’ — firing mortars into

clouds to c reate rain and so delay the

use of electricity-hungry air-

conditioners by m illions of urban

residents — and enforced holidays for

factories on a rotating basis. Power

shortages in some cit ies have

continued into the w inter months.

Overstretched transport network

As dem and for coal has grown, China’s

3 China’s pow er challenges

already overstretched and under-

invested-rail netw ork has suffered

hugely. Coal now accounts for m ore

than 40 per cent of all rail transport

(freight and passenger), placing w hat

w ill soon become an impossibly heavy

burden on the national system. NDRC

officials report that in the first nine

months of 2004, coal freight on the

country’s rail network rose 9 per cent

to 1.613 billion tonnes — but that

capacity m et just one-third of national

coal transport demand. In November

2004, the NDRC submit ted plans to the

State Council to construct a third coal

transport rail link (from Zhungeer in

Inner M ongolia to Tangshan in Hebei

province) to ease pressure on the

national network. In the meantime, up

to 200 million city residents were

expected to suf fer heating shortages inthe w inter of 2004-2005 because of

insufficient coal supply, according to

official media reports.

With China’s modest 73,000 kilometres

(km) rail netw ork reaching gridlock, the

country ’s 1.8 million km road system

(some 25,000km of it four-lane

highw ay) has become an option for

coal and other f reight. The government

has recognised this, investing some

US$45 billion in highw ay construction

and maintenance in 2002 alone,

according to official m edia reports. Yet

road transport has its ow n problems:

truck quality and m aintenance

standards vary w idely: although around

two-thirds of the trucks on the road in

southern China are Japanese or

European, t rucking fleets are virtually

all local. At the same tim e, government

restrictions on overloading enforced in

June 2004 have resulted in rising

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 9/24

Energy outlook for China 7

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

trucking costs — w ith the price of

highway transport between Beijing and

Shanghai almost doubling in the

second half of 2004. W hile road freight

serves to fill a gap in coal

transportation, only significant

expansion of t he country ’s railway

infrastructure w ill help China ensure a

steady supply of coal to its power

stations.

Consolidation needed in coal sector

China’s more than 2,000 mines have

low average annual production

capacities and high accident rates.

While many state-owned mines use

modern t echnology and are

comparatively safe, w ell over a

thousand are small operations ow ned

by local tow nship and village

enterprises, employing primitive miningtechnology and only the most basic

safety precautions. More than 4,500

miners died in mining accidents in

China’s coalmines in 2004, according to

official media reports. In the worst

accident of the year, 166 miners were

killed in a huge explosion in north-

w estern Shanxi province. This was

follow ed in February 2005 by the

deaths of 209 m iners in a gas explosion

in north-eastern Liaoning province.

Increasing pressure t o raise coal output

in a bid to feed surging dem and is

stretching m ining capacity and

contributing t o higher casualties. The

government is working to streamline

the industry by nurturing the

development of a handful of

homegrown state enterprises.

Rationalisation in the sector w ill see

the closure or takeover of sm aller

mines and a general improvem ent both

in production and health and safetyissues.

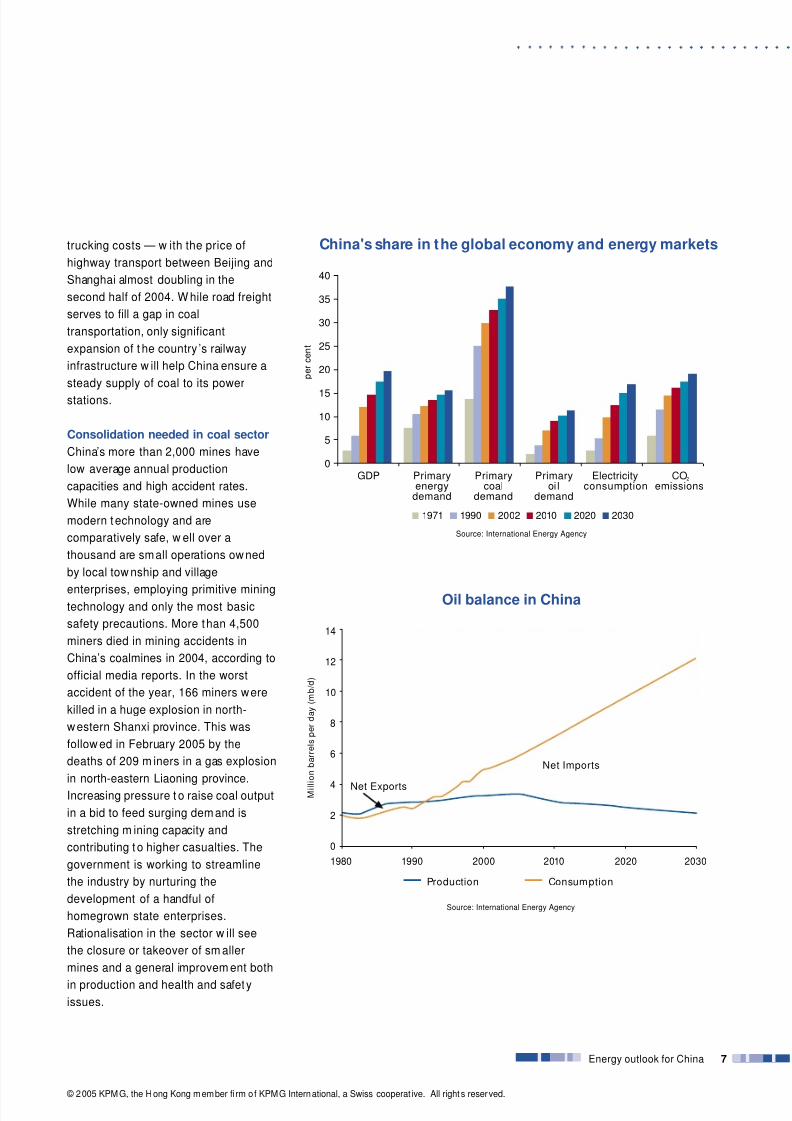

Primaryenergy

demand

Primarycoal

demand

Primaryoi l

demand

Electricityconsumption

COemissions

2

0

5

10

15

20

25

30

35

40

GDP

1971 1990 2002 2010 2020 2030

China's share in t he global economy and energy markets

p e r c e n t

Source: International Energy Agency

0

1990 2000 2010 2020 2030

M i l l i o n b a r r e l s p e r d a y ( m b / d )

1980

2

4

6

8

10

12

14

Production Consum ption

Net Imports

Net Exports

Oil balance in China

Source: International Energy Agency

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 10/24

8 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

As demand for power has grown,

China’s power industr y has sought to

keep up with m assive investment in

power plant construction over the past

five years. With a wave of new pow er

plants currently under construction,

there are concerns that the industry

could see a sharp sw ing from shortage

to oversupply. Yet a power glut is

unlikely as long as power demand

growth m aintains its mom entum — as

is likely to be the case.

In the w ake of the Asian financial crisis,

China slowed power plant construction

in anticipation of reduced pow er

consumption growth. This did indeed

happen, but a sharp rebound in pow er

demand in 1999-2000 caught the

government unaware, prompting

power shortages. Since 2000, powerconsumption growth has outpaced the

growth in power capacity, which

continued to decline until 2003, when it

climbed 9.1 per cent (compared with

4.3 per cent in 2002), according to SHK

Financial Group, a Hong Kong-based

organisation. However, in 2003 pow er

demand climbed even more rapidly by

15.8 per cent, continuing through 2004

at a similar rate of grow th.

Surging power demand prompted the

construction of coal-fire pow er plants in

2003-2004 — a development which the

Chinese government has sought to

check. In late December 2004, Beijing

announced new measures to restrict

unapproved pow er plant projects by

local administ rations. The move, w hich

follow s several previous warnings,

means that state banks w ill cease

lending money for the construction of

unapproved plants, and t he

government w ill use its pow er over

land use rights to shut down some or

all of the unlicensed plants. Although

China routinely faces pow er shortages,

government authorities are concerned

that efforts to expand capacity will

drastically overshoot the m ark creating

excess supply within a few years if all

projects currently underw ay reach

completion. Government officials

estimate that up to 120,000 megawatts

(mw ) of unauthorised capacity is now

being built.

Coal: breakneck production

China’s coal sector has raised output

enormously over the past five years,but still cannot keep up with power

demand. As demand has climbed, so

prices have risen and competit ion

increased. In January 2005, the NDRC

issued new regulations covering coal

trading. Under the new rules, coal-

trading organisations that w ish to t rade

with wholesalers and retailers must

first register w ith the State

Administration for Industry &

Commerce (SAIC) for trading licences,

w hich can be obtained only if the

applicants have a registered capital of

at least Renminbi (Rmb) 50 m illion

(US$6 m illion). This restriction w hich

should cut out many of the smaller

traders will help consolidate the m arket

and cap coal prices — or so the NDRC

hopes.

4 Domestic pow er generation

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 11/24

Energy outlook for China 9

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

Oil: less and less

As China consumes increasing

quantities of oil, so concerns over its

long-term reserves increase. In a report

released in January 2005, the IEA

stated t hat China reported a record-

breaking 16 per cent increase in oil

consumption for the previous

November.

China is working to exploit its domestic

reserves to the full. In 2004, the

country’s largest oil producer,

PetroChina (China National PetroleumCorporation, or CNPC) began

construction of tw o pipelines in the

w estern Xinjiang region valued at

Rmb14.6 billion (US$1.8 billion). The

new supplies are intended to

supplement diminishing oil reserves in

the count ry’s eastern fields. A crude oil

From coal to oil: Liquefying China’s coal

In a bid to check its grow ing reliance on import ed oil, China is turning to its

greatest energy resource — coal. Coal liquefaction (also know n as coal-to-

liquids, or CTL) involves transforming coal into refined oil t hrough a series of

processes in an environment of extreme pressure and high temperature.

China has been quick off t he m ark. The world’s largest coal liquefaction project

is already under const ruction in China’s Inner M ongolia Autonom ous Region,

and is due for completion in 2007. And in M arch 2005, Beijing is due to host aconference to discuss the potential in China for new CTL technology pioneered

in South Africa and Germany.

In the long term, Beijing hopes to replace up to 10 per cent of oil imports

through coal liquefaction. According t o the China Coal Research Institut e, it

costs around US$25 per barrel to produce a ton of coal-liquefied oil, w ith 3-5

tons of coal used in the production.

pipeline w ith an annual capacity of

20 million tons will cross 970 miles

from the Xinjiang city of Shanshan to

Lanzhou, capital of Gansu province.

China also has high hopes for its

potentially rich reserves in the high, dry

deserts of the far west . Yet gas and oil

deposits in this remote region lie much

deeper than in the northeast and w ill

cost far more to get out of the ground.

Once extracted, the oil must then be

transported via expensive pipelines to

power plants in the east of the country.

The construction of an east-west

pipeline is already underw ay.

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 12/24

10 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

0

3

6

9

12

15

1990 2000 2010 2020 2030

m b

/ d

-20%

0%

20%

40%

60%

80%

Production Demand

China oil supply balance

Imports as % of demand (right axis)

Source: International Energy Agency

China’s West-East gas pipelineChina’s West-East Natural Gas

Transmission Project officially went into

comm ercial operation on 30 December

2004, in anticipation of a boom in the

country’s f ledgling natural gas market.

The 4,000-km pipeline, which broke

ground tw o years ago, has an annual

gas transmission capacity of 12 billion

cu m — all of it already subscribed. As

oil and coal prices continue t o rise,

demand for natural gas is expected t oensure profitability for the pipeline.

A report m ade by 61 users of the w est-east pipeline project shows that by

2010, their demand for natural gas will

reach 29.8 billion cu m , and the f igure

w ill rise to 50 billion in 2020. It means

that by then there w ill be a large gap

betw een demand and supply in China’s

natural gas market.

Source: Xinhua New s Agency

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 13/24

Energy outlook for China 11

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

Gas: in the pipeline

China has big hopes for natural gas in

helping to boost energy supply. China’s

natural gas reserves amount to som e

53.3 trillion cu feet (ft), according to

the Oil and Gas Journal, or around

1 per cent of know n w orld reserves.

Natural gas has been discovered in

Xinjiang, Sichuan province and off

southern Hainan Island. Yet this is a

comparatively new industry in China,

accounting for just 2.5 per cent of

primary energy. According to the

Development Research Centre under

China's State Council, the government

aims to raise the share of natural gas in

its energy consumption from current

2.5 per cent to 5 per cent in 2010, and

7 per cent by 2020 — a forecast which

w ould see natural gas consumption

rise from 32.8 billion cu m in 2003 to251.7 billion cu m by 2020.

Whether or not it achieves this

ambitious goal w ill depend heavily on

the exploitation of gas reserves in

Xinjiang and the successful com pletion

of a 4,000-km w est-east pipeline — a

section of which opened in 2004 — to

the coastal cities. W hile increasingly

exploiting its ow n reserves, China is

seeking a short-term f ix by importing

natural gas including a plan with Kogas,

South Korea’s biggest gas organisation,

to construct a pipeline connecting

China w ith it s Siberian gas field

(operated by Kovykta, a Russian

organisation)5.

Liquefied natural gas (LNG) is also high

on the list. BP is building China’s first

ever import-fed LNG term inal (due for

complet ion by the end of t his year) in

southern China, while two more LNG

terminals are being built in Fujian and

Zhejiang provinces (both sout h of

Shanghai on the east coast). A total of

eight m ore LNG terminals are slated for

construction. In August 2002 an

Australian-based group, the Northw estShelf Venture consortium, won a

US$13 billion contract to supply LNG to

the southern Chinese terminal, while

Sinopec has signed a deal for long-term

LNG supplies from Iran6.

5Economist Intelligence Unit, Executive Briefing, 10 October 2004: “ China: Energy and electricity background ” ; Sohu.com, 2 July 2004: “ Seeking a

stable energy” (http://english.sohu.com/2004/07/02/59/article220825997.shtml)

6AP Worldstream, 18 October 2002: “Australia and China sign multibillion dollar natural gas deal ” ; World News Connection, 27 December 2004: “ China

to cooperate w ith Iran in oil, gas sectors”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 14/24

12 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

Hydropower: the next big thing

Diversification beyond coal and oil

raises expectations for hydropow er,

w hich has the additional advantage of

being a clean resource. The building of

hydropower stations has become a

priority for the Chinese government,

most visibly in the Three Gorges Dam

project. A total of 26 generating unitsw ith an output capacity of 84.7 billion

kw hours will be operational by the

time the plant is fully completed 2009,

w ith an annual output capacity of

18.2gw / 84.7 billion kw hours,

according to the State Council’s Dam

Committee, making it by far the

biggest single generating facility in the

world. About 32 per cent of the dam ’s

output w ill go to Shanghai, 16 per cent

to Guangdong, and the rest to parts ofcentral China.

But hydropower is expensive. By

end-2004, China had spent some

US$11 billion on the Three Gorges

Dam, w ith US$4.7 billion spent on

investments in dam facilities,

US$4 billion going on resett lement and

US$2.5 billion on pow er plant

construction. Final investment in the

project is likely to reach someUS$22 billion7. Despite the cost,

the U.S. Department of Energy

believes that China’s plans for further

ambitious hydropower projects will

continue. Of ficial Chinese sources

believe the country’s potential

hydroelectric capacity is as high as

300gw — with less than a third of this

potent ial exploited to date8.

2002 2030

5,573TWh1,675 terawatt hours (TWh)

72%

1%

6%

5%

16%

Coal Oil Gas Nuclear Renewables/Hydro

77%

2%

1%

3%

17%

China power generation fuel mix

Source: International Energy Agency

7 AFX Asia, 5 July 2004: “ China’s Three Gorges dam t o generate 37.5 bln kwh this yr, up 336 pct ”

8Ria Oreanda, 12 August 2004: “ China invests $11 billion in the Three Gorges Dam on the River Yangtze ” ; AFX Asia, 7 May 2004: “ China’s Three

Gorges Dam to generate 37.5 bln kwh this yr, up 336 pct”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 15/24

Energy outlook for China 13

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

Nuclear power: build, build, build

China’s modest nuclear power industry

is still young. Construction of the

country’s first t w o nuclear plants (at

Daya Bay just across the border f rom

Hong Kong and Qinshan near Shanghai)

began in the mid-1980s. Today, China

has nine nuclear reactors in operation,

w ith tw o more units underconstruction. Current combined

capacity t otals around 7gw , accounting

for just 2 per cent of the country ’s total

power supply in 2003 — far below the

17 per cent global average9.

How ever, China has ambitious plans

for its nuclear sector. By 2020, it wants

to raise installed nuclear generating

capacity to 36gw , according to China’s

Atom ic Energy Authority. This means

building around 27 nuclear pow er

plants by 2020. As a first step, in July

2004 the government approved the

construction of new reactors at the t w o

existing power stations — Sanmen in

Zhejiang province and Yangjiang in

Guangdong province.

Renewable energy: legislation on

the wayWith demand increasingly stretched,

renewable energy has once again

appeared in Chinese energy discussions.

Renewable energy — excluding

hydropower — currently accounts for

less than 1 per cent of China’s total

energy capacity, though the Chinese

government aims to raise this figure to

12 per cent by 202010. To t hat end, the

government is rushing through the

China Renew able Energy Utility

Promotion Law — initially scheduled

for m id-2006 — as early as this

summer. The law w ill cover the

exploitation and development of wind

energy, solar pow er and hydropow er.

Renewable pow er projects are typically

small-scale and highly localised,

intended principally to supply isolated

rural communities with no connection

to the power grid. Yet China has

massive potent ial in renew ables. A

report published jointly by the Chinese

Renewable Energy Industry

Association, European W ind Energy

Association and Greenpeace

environmental group in May 2004estimates that China is capable of

installing an impressive 170gw of wind

power by 2020.

9 AP Online, 14 December 2004: “ China to establish independent nuclear power corporation amid planned expansion of industry”

10 Aberdeen Press & Journal, 10 April 2004: “ China prepares to dom inate global renewables industry ”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 16/24

14 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

China and the environment

Environment al problems caused by the burning of fossil fuels are a grow ing concern in China. In its China Energy

Outlook, the IEA states that pollution f rom energy-related em issions of sulphur dioxide, nitrogen oxides, volatile organic

compounds and particulates has led to serious deterioration in air quality in urban areas. Air quality in rural areas has been

deteriorating because of the expansion of industrial activities there.

Coal burning is a main contributor t o ambient and indoor air pollution, producing 85 per cent of t otal SO2

emissions and

28 per cent of tot al suspended particulate emissions. The problem is exacerbated by t he generally poor quality of China’s

coal, which is high in sulphur.

Since the late 1990s, the Chinese government has sought to ease urban pollution levels through a combination of tactics.

It has installed anti-pollution equipment in pow er plants and factories; and it has shut dow n ineff icient factories, district

heating and power plants in some inner-city areas, such as central Beijing. But noxious em issions and carbon monoxide

from mot or vehicles are grow ing rapidly and will becom e a major source of urban air pollution in the com ing decades.

China’s pollution is also an international issue. China is a major contributor to global greenhouse gas emissions. It is the

world’s second-largest em itter of carbon dioxide. Power generation and industrial activities are the m ain sources of CO2

emissions, because of the low efficiency of the country ’s power plants and industrial boilers and its heavy reliance on coal.

The IEA forecasts that China’s energy-related CO2

emissions w ill reach 6.7 billion tonnes by 2030, or 18 per cent of w orld

emissions. By cont rast, the U.S. and Canada together w ill emit 8.3 billion tonnes in that year.

The biggest increase in emissions will come from the power sector, which will produce more than a half of China’s CO2

emissions in 2030. Transport ’s share w ill also increase, as rapid motorisation spurs brisk grow th in oil consum ption. The

IEA projects that total Chinese vehicle ow nership w ill reach more t han 90 per 1,000 people by 2030 — around 130

million, compared w ith 220 m illion in the U.S. today.

0

1000

2000

3000

4000

5000

6000

7000

1990 2002 2010 2020 2030

m e t r i c t o n s ( M t ) o f C O

2

Power generation Industry Transport Other sectors Other transformation

CO2 emissions by sector in China

Source: International Energy Agency

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 17/24

Energy outlook for China 15

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

5 China’s global energy hunt

China’s thirst for oil w ill continue. The

State Information Centre, a

government think tank, estimated in

November 2004 that China’s crude oil

output would peak at 200 million

tonnes annually by 2015. Production

reached 170 million tons of crude in

2003, up from just 120,000 tons at the

founding of the People’s Republic of

China in 1949. Imports have climbed

too, with figures released by the

General Administration of Custom s

showing that the country imported a

total of 99.59 m illion tons of crude oil in

the first ten months of 2004 — more

than the full-year total of 91.12 million

tons recorded in 2003.

Wit h local resources diminishing, China

knows it m ust secure long-term oil

supplies from abroad — and that thesesupplies must be diversified in case of

geo-political change. Beijing has

approached its neighbours, such as

Kazakhstan, Russia and M ongolia. It

has also sought to build relationships

with suppliers from further afield.

Today, around 60 per cent of China’s

imported oil comes f rom M iddle

Eastern countries — notably Iran and

Saudi Arabia11.

China’s heavy reliance on M iddle

Eastern oil became a cause of concern

to the Beijing leadership during the

Iraqi conflict, prompt ing Beijing to seek

to diversify its w orldw ide energy

interests t o guard against the potent ial

disruption of vital supplies. China has

moved into Af rica, concluding general

trade agreements with almost all 53

African countries, particularly m ajor oil

producers such as Gabon and Libya12. It

has also sought to sign oil deals with

Central Asian neighbours and Russia —

albeit with little success to date.

China’s oil majors

The principal executors of China’s

overseas oil strategy are its three m ain

energy organisations. These

organisations took over production and

exploration of oil from the Ministry of

Petroleum in the 1980s as the

government separated itself from the

operational side of the indust ry and

focused more on regulatory policy. All

three organisations are m ajority-state-

ow ned but have raised substantial

capital through the international listing

of subsidiaries.

PetroChina. One of the country’s

largest organisations, PetroChina (thelisted arm of China National Petroleum

Corp, or CNPC) is an upst ream

production organisation based in t he

oil-rich north, though it cont rols nearly

80 per cent of all local oil pipelines,

more than 90 per cent of t he domestic

gas market and around 40 per cent of

the retail oil market, according to

organisation estimates. In the first

half of 2004, PetroChina produced

388 m illion barrels of oil and 410 billion

cu ft of gas, and the organisation ow ns,

controls or f ranchises over 15,000

petrol service stations across the

country. In February 2005, PetroChina

w on approval for t he US$3.3 billion

expansion of Dushanzi petrochemical

facility in north-w estern Xinjiang

Autonomous Region — a move which

w ill enable China use the pipeline to

import up to 10 million tons of oil from

Kazakhstan by 200813.

11Axcessnews.com: http://www .axcessnews.com/business_100804.shtml; Energy Information Administration, July 2004: http://ww w.eia.doe.gov/

emeu/cabs/china.html

12World News Connection, 28 May 2004: “ Japan: Article reviews China energy short age, says China Trades ‘Weapons for Oil’” ; Platts Oilgram New s,

Vol. 82, 10-26-2004: “Africa is staging ground for push by China, India to control more output ” ; International Herald Tribune, 19 February 2005: India

joins Chi na in a w orldw ide rus h for oil and gas ”

13 Financial Times, 16 February 2005: “ PetroChina to expand Dushanzi refinery”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 18/24

16 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

International partnerships

China is learning that it m ust m ove

quickly and decisively if it is to develop

a secure and diversified global energy

strategy. Yet CNOOC, PetroChina and

Sinopec have already com e a long w ay

over the past decade. Industry insiders

estimate that Chinese oil organisations

have already spent som e US$5 billion

in nearly 30 projects across Af rica,

South Am erica and Aust ralia —

supplementing the lion’s share of oil

imports from the Middle East (and

specifically Iran, Oman and Saudi

Arabia). Notable partnerships outside

the M iddle East include the follow ing:

Algeria. Chinese president Hu Jintao

visited Algeria in February 2004 t o

sign an energy and mining

framework agreement, according tooff icial Chinese media reports.

Australia. CNOOC purchased a 5.5

per cent st ake in Australia’s North-

West Shelf gas project in 2002 — at

the time, a new strategy ensuring

long-term supply contracts through

equity stakes17.

Canada. China is talking to Canadian

oil pipeline organisations —

specifically Enbridge, Canada’s

second-largest pipeline organisation

— about securing oil supplies from

the t ar sands in north Alberta and the

northwest coast of British Columbia.

Canada is the largest im porter of oil

into the U.S., with an average of 1.6

million barrels per day in 200418.

Sinopec. China Petrochemical Corp, or

Sinopec, has a smaller upstream

business than PetroChina but a bigger

presence in midst ream and

dow nstream operations such as

refining and retailing — particularly in

its traditional stronghold in southern

and eastern China, w here over 30,000

service stations in China carry the

Sinopec brand. In the f irst half of 2004,

Sinopec produced 136 m illion barrels of

oil and 100 billion cu ft of gas. In the

middle of last year, Sinopec committed

a further Rmb10 billion (US$1.2 billion)

in new projects across North and West

Africa, Russia, the M iddle East and

South-east Asia14.

CNOOC. The China National Offshore

Oil Corporation (CNOOC) specialises in

offshore exploration and production.Incorporated back in 1982, CNOOC is

the leading operator and partner for

offshore exploration projects in Bohai

Bay, the Yellow Sea, East China Sea

and South China Sea. CNOOC also has

international ambitions: it is now

Indonesia’s largest offshore oil

producer, following the takeover for

US$585 million of Repsol Indonesia in

200215.

China’s big three oil organisations have

signed oil or natural gas exploration

deals around the w orld: in Australia,

Indonesia, Iran, Kazakhstan, Nigeria and

Papua New Guinea. So far, these deals

represent just 10 per cent of China’s oil

imports16.

14 China Daily, 12 August 2004: “ Sinopec to continue diversifying and cut costs ”

15 CNOOC website link http://www.cnoocltd.com/cnoocltd/front/html/resultspre-12-3.html

16Business Week, Vol. 3908, p60 15 November 2004: “ The great oil hunt”

17Asia Pulse, 11 April 2002: “ Profile: Australia’s Petroleum Industry”

18The Oil Daily, Vol. 55, Issue 11, 18 January 2005: “ Enbridge close to China deal” ; Vancouver Sun, 19 January 2005: “ China emerges as energy market

to rival U.S.”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 19/24

Energy outlook for China 17

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

Gabon. Under a deal signed in

February 2004, Sinopec w ill explore

three oil blocks nearly Port Gentil

before deciding whether to accept an

exploration and production-sharing

contract. The tw o sides have also

agreed to cooperate in oil

exploration, development , refining

and exports19.

Kazakhstan. Construction of a

3,000-km oil pipeline between

Kazakhstan and China’s western

Xinjiang Autonom ous Region started

in September 2004. The two sides

are also co-operating over gas. In

February 2005, KazMunaiGas,

Kazakhstan’s state organisation, w as

reported to be considering building a

pipeline to China that could begin

shipping gas from 2008. An initialdeal is expected mid-year.

Kazakhstan’s gas production

increased 46 per cent year-on-year to

20.5 billion cu m in 200420.

Russia. China’s energy relations with

Russia turned sour in 2004 w ith the

collapse of Russian oil giant Yukos

and Moscow ’s decision to build a

pipeline to the Pacific coast to f eed

Japanese and U.S. oil containers

rather than sending the oil to

China. In February 2005, Russian

state-owned oil organisation

Rosneft — the new ow ner of the

main production subsidiary of

Yukos — began deliveries of oil t o

China. Russia intends to supply

4 m illion tons of oil to China by 2006,

and 50 million tonnes of oil by

201021.

Venezuela. President Hu Jintao

visited Venezuela in 2004, signing

energy deals w ith Venezuelan

president Hugo Chavez, w ho hasadopted an increasingly anti-U.S.

stance. This is worrying for t he U.S.,

since Venezuela is its fourth-largest

supplier of crude oil. President

Chavez has talked openly of diverting

as much oil as possible t o China22.

19Asia Africa Intelligence Wire, Africa Research Bulletin, 16 November 2004: “ Continental Developments: Africa-China - From strength t o strength ”

20BBC International Reports (Central Asia), 12 February 2005: “ Kazakh oil to be shipped to China via new pipeline in M ay 2006”

21Nikolai Gorelov Denis Rebrov, 22 February 2005: A Pipeline to China

22English IPS News, 18 February 2005: “ Oil: Venezuela looks to China to diversify its oil m arkets”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 20/24

18 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

China’s voracious hunger for energy

w ill continue, driven by an economy

which — despite repeated talk of a

hard landing — is set to m aintain high

single-digit figures for the next decade.

Power demand in the short term w ill

remain acute. China’s State Grid

Corporation announced in December

2004 that national consumpt ion of

electric power w ould rise to some

2,425 billion kw/hour in 2005 — up

12 per cent on 2004. Similarly, in the

long term, t he IEA forecasts that

China’s tot al primary energy demand

w ill grow by 2.6 per cent per year until

2030. Coal w ill continue to dom inate the

fuel m ix, particularly in pow er

generation, but it s share in overall

consumption will drop slightly, from

57 per cent today to 53 per cent in

2030. Primary oil consumption willincrease by 3.4 per cent per year,

driven largely by surging t ransport

demand as vehicle ownership rises to

up to 90 per 1,000 by 2020. (Already by

2010, China w ill have some 56 m illion

mot or vehicles on its roads — w ell over

tw ice the number today.)

The U.S. Energy Department predicts

similar sharp growt h. It forecasts

that China will be importing some

75 per cent of its crude oil by

2025 — nearly twice the percentage

today — and consuming 10.6 per cent

of the world’s oil. The U.S. Energy

6 Heading for a pow er crunch?

Department also sees China’s demand

for oil almost doubling to 11 m illion

barrels per day by 2020, w ith natural

gas consumption tripling to 3.6 trillion

cu ft a year and coal consumpt ion

surging 76 per cent to 2.4 billion tons a

year.

Can the Chinese government meet this

surging demand? Beijing hopes to bring

more pow er generating capacity

onstream in 2005, but will still

experience a shortfall of some

20 million kw during the peak summer

season.

In the longer term , China’s efforts to

meet its pow er needs w ill be

hampered by the absence of a fully

developed national pow er grid.

Although som e 40 per cent of allinvestm ent in the electric power sector

betw een 1995 and 2003 went into

power grid construction, the netw ork

remains unfinished23.

23Comtex, 24 January 2005: “ China suffers blackouts due to severe power shortage in w inter” ; AFX Asia, 25 January 2005: “ China’s State Grid

forecasts 2005 profit up 18.5 pct at 11.5 bln yuan” ; AFX Asia, 21 January 2005: “ China southern provinces to face 7.8 mln kw power shortage this yr ”

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 21/24

Energy outlook for China 19

© 2005 KPM G, the Hong Kong m ember fi rm o f KPMG International, a Swiss cooperat ive. All right s reserved.

7 Summary

Although crude oil imports fell

24 per cent to 7.8 m illion tonnes in

January 2005 after a year of sharp

growth in 2004, underlying demand

for energy is expected to rem ain

strong throughout 2005 and impact

international oil m arkets.

The number of cars on China’s roads

will continue to bolster demand for

petrol in 2005.

Following an expected shortf all in

pow er generation in 2005, China

should be able to m eet dem and as

new capacity comes on-stream from

2006. Despite massive development

in pow er generating capacity,

oversupply is unlikely as long as

economic growth remains robust.

China w ill continue to invest heavily

in its rail and road netw orks as part

of the Eleventh Five-Year Plan (2006-

2010), its blueprint f or national

economic development.

Consolidation in the m ining sector

w ill most likely see the emergence of

five m ajor homegrow n players as

thousands of sm all mining operators

are forced out of business. The

introduction of modern technology

and safer m ining techniques w ill help

improve safety standards across the

board and establish m ore secure

supply.

China will encourage foreign

investment in its nuclear power

plants in a bid to m odernise and

expand the sector.

The anticipated release of a

renew able energy law in m id-2005

w ill spur growth in renewables.

The contribution of hydropower tothe overall mix w ill increase

proportionately as new phases of the

Three Gorges Dam com e on-stream.

Further investment in hydropower,

though cost ly, is highly likely.

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 22/24

20 Energy outlook for China

© 2005 KPM G, the Hong Kong m ember firm of KPM G Internat ional, a Swiss cooperat ive. All right s reserved.

Appendix — China demographics

Population: 1.3 billion

Geographic size: 9.6 mil lion square km

Number of states: 22 provinces, five autonomous regions and fourmunicipalities

Major cit ies: Beijing (capital, 16 mill ion* ), Shanghai (20 mill ion* ),

Guangzhou (15 m illion* )

* independent estimates including transient populations

Urban populat ion: 485 mill ion

Rural populat ion: 815 mill ion

Ethnic groups: Han Chinese (92 per cent), 55 minority nationalit ies (8 per

cent)

Languages: M andarin Chinese (putonghua ); several other Chinesedialects.

Religions : Off icially atheist ; Buddhist communit ies in Tibe t, Yunnan,

Sichuan and Qinghai; Muslim comm unities in Xinjiang,

Gansu and Ningxia; Christianity, Daoism and Confucianism

enjoying a resurgence, particularly in coastal cities.

Clim at e: Diverse ranging f rom subt ropical in sout h t o sub-zero

northern temperatures.

Key memberships: United Nations Security Council; World Trade Organization;

World Intellectual Property Organization; Asia-Pacific

Economic Co-operation f orum; Association of South-EastAsia Nations — dialogue partner; International Atom ic

Energy Agency; International Labour Organization; and World

Health Organization.

Source: U.S. World Factbook 2 004, China Statis tical Yearbook 2004

Beijing

Shanghai

Guangzhou

Shenzhen

Hong KongMacau

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 23/24

The views and opinions are those of the authors and do not ne cessarily represent t he view s and opinions of KPMG in China and Hong Kong SAR. All inform ationprovided is of a general nature and is not intended to address the circumstances of any particular individual or entity.

7/31/2019 Energy Outlook for China 2005

http://slidepdf.com/reader/full/energy-outlook-for-china-2005 24/24

fff1Z_\V1R^\1R]

fff1Z_\V1R^\1WZ

lpormnr sq

~47>68 z=48

:cW C[^^a/ N^fTa B4/ JaXT]cP[ K[PiP

3 BPbc @WP]V >] >eT]dT

?TXYX]V 32295:/ @WX]P

NT[ < .:8 ,32- :73: 7222

T0HPX[< \T[eX]1VdT]=Z_\V1R^\1R]

*9:24:< ~4?:685

72cW C[^^a/ K[PiP 88

3488 IP]YX]V OTbc L PS

MWP]VWPX 422262/ @WX]P

NT[ < .:8 ,43- 757; 6888

T0HPX[< ]^aQTac1\ThaX]V=Z_\V1R^\1R]

,98173 -@4

4;cW C[^^a/ DdP]ViW^d F]cTa]PcX^]P[

B[TRca^]XRb N fTa

625 EdP]bWX A^]V L^PS

DdP]ViW^d 7322;7/ @WX]P

NT[ < .:8 ,42- :954 4:54

T0HPX[< a^]P[S1biT=Z_\V1R^\1R]

,98173 -@4

L^^\ 3238/ MWd] EX]V M`dPaT

AX OP]V @^\\TaRXP[ @T]caT

7224 MWT]]P] BPbc L^PS

MWT]iWT] 73:22:/ @WX]P

NT[ < .:8 ,977- :468 55;:

T0HPX[< a^]P[S1biT=Z_\V1R^\1R]

*47;98 y=85

:cW C[^^a/ KaX]RTAb ?dX[SX]V

32 @WPcTa L^PS

@T]caP[/ E^]V G^]V

NT[ < .:74 4744 8244

T0HPX[< ]T[b^]1Ud]V=Z_\V1R^\1WZ

,98173 -@4

45aS C[^^a A/ ?P]Z ^U @WX]P ?dX[SX]V

>eT]XSP A^dc^a HPaX^ M^PaTb

HPRPd

NT[ < .:75 9:3 2;4

T0HPX[< a^]P[S1biT=Z_\V1R^\1R]

NWT X]U^a\PcX^] R^]cPX]TS WTaTX] Xb ^U P VT]TaP[ ]PcdaT P]S Xb ]^c X]cT]STS c^ PSSaTbb cWT RXaRd\bcP]RTb^U P]h _PacXRd[Pa X]SXeXSdP[ ^a T]cXch1 >[cW^dVW fT T]STPe da c^ _a^eXST PRRdaPcT P]S cX\T[h X]U^a\PcX^]/cWTaT RP] QT ]^ VdPaP]cTT cWPc bdRW X]U^a\PcX^] Xb PRRdaPcT Pb ^U cWT SPcT Xc Xb aTRTXeTS ^a cWPc Xc fX[[

X Q X W U I W [S W X U X X W X

j 4227 GKHD/ cWT E^]V G^]V \T\QTa UXa\ ^UGKHD F]cTa]PcX^]P[/ P MfXbb R^^_TaPcXeT1 >[[ aXVWcbaTbTaeTS1 KaX]cTS X] E^]V G ]V1 GKHD P]S cWTGKHD [ X S S Z U GKHD