Embed Size (px)

Citation preview

1 © Wärtsilä

Energy Markets and LNG Fuel Business Case

LNG Fuel Forum45h Annual General MeetingCaribbean Shipping AssociationIntercontinental Hotel19-21 October 2015Cartagena, Columbia

John Hatley PE LNG Initiatives ( MBA, MSE)

Americas VP Ship PowerWartsila North America, Inc.

Cell +1 281 221 [email protected]

18 Wartsila LNG Fuel Contracted Vessels North America

3 @ BC Ferries

2 @ Seaspan

2 @ TOTE

3 @ Society Quebec Ferries

6 @ Harvey Gulf

02 November 2015

Wartsila’s #1 in LNG fuel projects

+ 2 Merchant Vessels

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Keys

Americas Shale Gale in Gas & Oil, robust / fragile ?

Global Energy Policies, market gamesmanship ?

Adoption rates, fundamentals ?

Future Ahead, structural shifts?

3 © Wärtsilä

Agenda

4 © Wärtsilä

What ? Competitive Forces Americas & EU Gas BasisEmission Areas Expansion & Owner Choices

Why ? 5 Drivers Set Investment ClockAmericas Compelling Savings3 Gas Pillars

Business Case Cargo, Investor, Banker Views1400 TEU CoasterInvestment Returns

Oil Price Shock ! Business Case: Robust or Fragile?Stress Test

Conclusions Recent Market SignalsThe Future Decade for GasBusiness Case Appendix

Agenda

5 © Wärtsilä

What ? Competitive Forces Americas & EU Gas BasisEmission Areas Expansion & Owner Choices

Why ? 5 Drivers Set Investment ClockAmericas Compelling Savings3 Gas Pillars

Business Case Cargo, Investor, Banker Views1400 TEU CoasterInvestment Returns

Oil Price Shock ! Business Case: Robust or Fragile?Stress Test

Conclusions Recent Market SignalsThe Future Decade for GasBusiness Case Appendix

Competition Model Forces

Government Legislation:Political power exercising market influence: Trade Behavior, Emissions

Porter’s 5 Forces + 1…Government Legislation exercises market influence… emissions

SHALE GALE

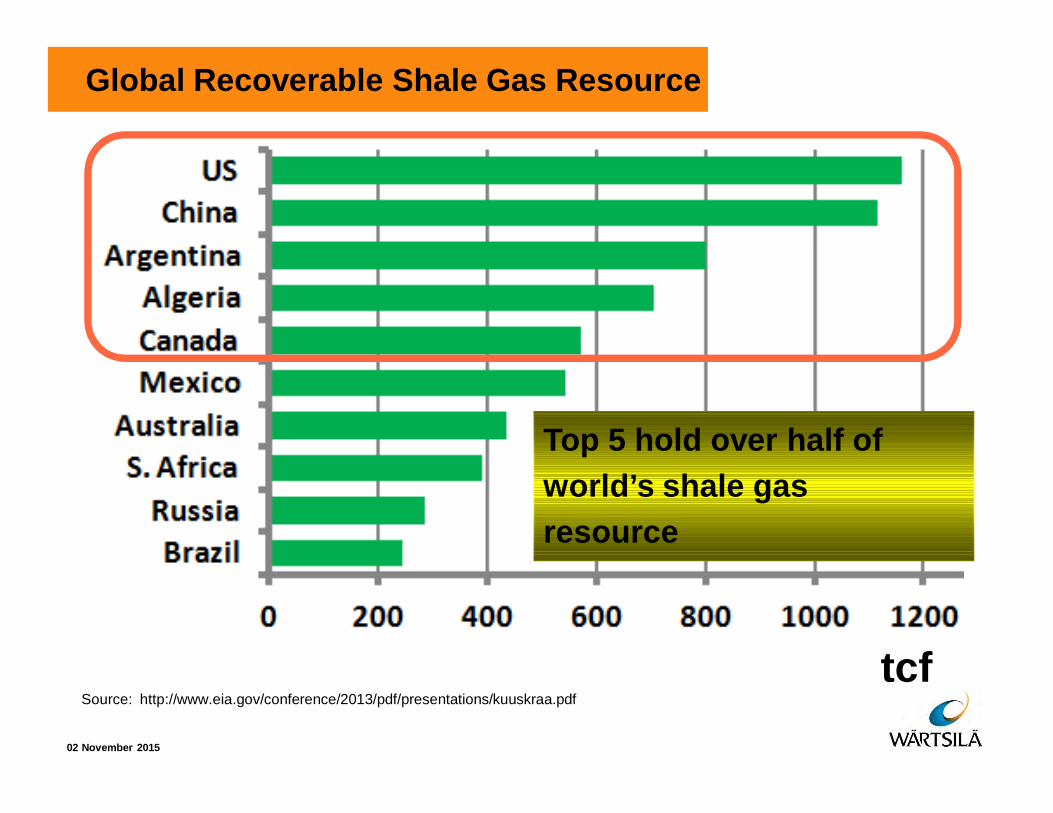

Global Recoverable Shale Gas Resource

02 November 2015

Top 5 hold over half of world’s shale gas resource

tcfSource: http://www.eia.gov/conference/2013/pdf/presentations/kuuskraa.pdf

Global Gas Production

02 November 2015

Source: LNG for Marine Transportation USA, Houston TX, June 12, 2013; David Sweet President Natural Gas Roundtable http://lngmarineevent.com/presentations/2013/David-Sweet.pdf

BILLION M3

USA is world’s #1 gas producer… US Shale gas production, by itself, exceeds all nations except Russia

Emission Control Areas

More Emission Control Areas “ECA” likely soon

Shale Gas Positioning

Americas Recent ECA casts broad &

expansive emissions regulations

Shale gas compelling economics driver amidst ever tighter Government regulatory climate.

EU Early SECA targets limited

sulfur requirements; may soon evolve into broad ECA

Shale gas parity pricing with other fuels… Government drives environmental change thru tax incentives/avoidance

02 November 2015

2012 Heralded Americas Emissions Control Area ECA broad / expansive compared to 2007 SECA specificlimits for Europe.

Marine Fuel Sulphur Content by % Weight

02 November 2015

SECA Standard

Global IMOStandard

January2012

January2020

January2025

July2010

January2015

Review2018

IMO MARPOL Annex VI Amendment October 2008 ( European Union Sulphur Directive 2012/33/EU) stepwise reductions

Shale Gas Positioning

Americas Recent invoked ECA casts

broad & expansive emissions regulations

Shale gas compelling economics driver amidst ever tighter Government regulatory climate.

EU Early adopted SECA

targets limited sulfur regulations; may soon evolve into broad ECA

Shale gas parity pricing with other fuels… Government drives environmental change thru tax incentives/avoidance

02 November 2015

Americas enjoys compelling shale gas economics…versus Europe’s absence where Government environmental inducements shape adoption.

Key: Fuel Prices on Energy Basis

02 November 2015 Peter H Jantzen

380 cStHFO

1%MGO

0.1%diesel

LNGJapan

LNGEurope

LNGUSA

0

10

20

30

$ / mmBtu

Fuel price dominates vessel OPEX… gas is cheapest & cleanest in Americas… EU price parity dampens economic incentives.

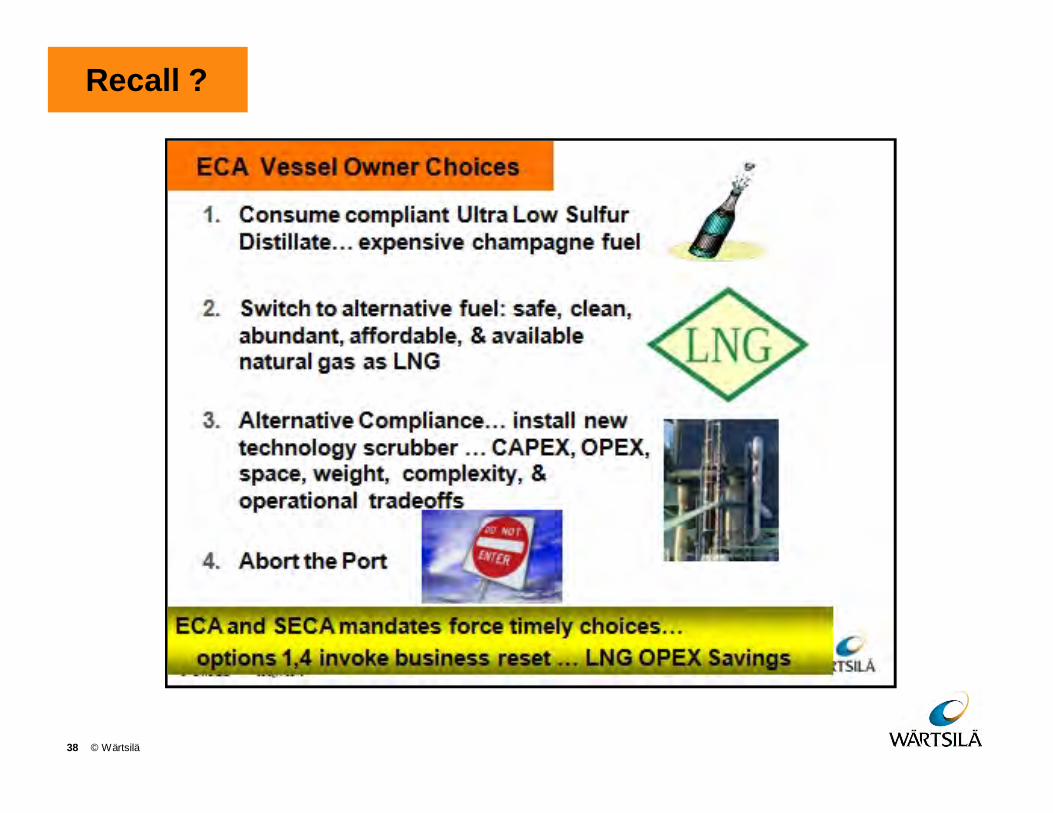

4 Pathways for Vessel Owners

1. Consume compliant Ultra Low Sulfur Distillate… expensive champagne fuel

2. Switch to alternative fuel: safe, clean, abundant, affordable, & available natural gas as LNG

3. Alternative Compliance… install new technology scrubber … CAPEX, OPEX, space, weight, complexity, & operational tradeoffs

4. Abort the Port

02 November 2015

ECA and SECA mandates force timely choices… options 1,4 invoke business reset … prepare LNG now

Agenda

15 © Wärtsilä

What ? Competitive Forces Americas & EU Gas BasisEmission Areas Expansion & Owner Choices

Why ? 5 Drivers Set Investment ClockAmericas Compelling Savings3 Gas Pillars

Business Case Cargo, Investor, Banker Views1400 TEU CoasterInvestment Returns

Oil Price Shock ! Business Case: Robust or Fragile?Stress Test

Conclusions Recent Market SignalsThe Future Decade for GasBusiness Case Appendix

Shale Gas Plays

16 © Wärtsilä

Shale …. huge reserves natural gas; nearly century supply

Abundant Gas Supply

17 © Wärtsilä

Paradigm shift to shale gas; now 25% of supply... future @ half

Annual Shale Gas Production

17% CAGR

41% CAGR

Shale production surge… 2006 frantic… 2010 strong

24% CAGR

Other US

Bakken ND

Eagle Ford TX

Marcellus PA

Haynesville LA

Woodford OK

Fayetteville AR

Barnett TX

Antrim MI, IN

Emission Control Area “ECA” US & Canada

02 November 2015

ECA bubble encapsulates… any flag ships.. 200 nautical miles… low sulfur fuel (equivalence)… enforceable August 2012

Source: US EPA, Designation of North American Emission Control Area to Reduce Emissions from Ships

Puerto RicoUS Virgin Islands 2014

20 © Wärtsilä

Source:http://www.dnvusa.com/industry/maritime/publicationsanddownloads/publications/newsletters/technical_regulatory/2012/north_american_emission_control_area.asp

Fuel Sulfur 0.10 % limit commences 1 January 2015

No. Am. ECA Fuel Sulfur Limit

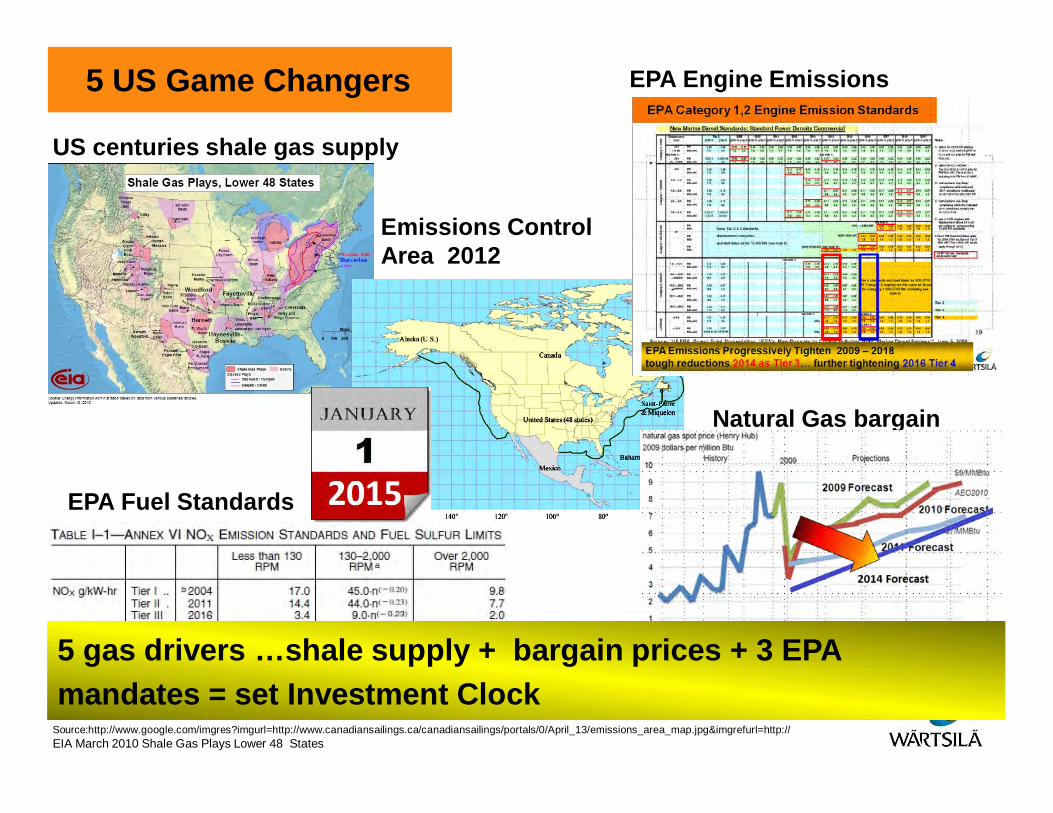

5 US Game Changers

Source:http://www.google.com/imgres?imgurl=http://www.canadiansailings.ca/canadiansailings/portals/0/April_13/emissions_area_map.jpg&imgrefurl=http:// EIA March 2010 Shale Gas Plays Lower 48 States

US centuries shale gas supply

Natural Gas bargain

Emissions Control Area 2012

EPA Engine Emissions

EPA Fuel Standards

5 gas drivers …shale supply + bargain prices + 3 EPA mandates = set Investment Clock

3 Pillars LNG Fuel Vessels

02 November 2015

ECONOMICS SAFE & RELIABLE

ENVIRONMENT SUSTAINABILITY

Proven LNG systems... reduce risk for yard, owner, & banker... extends LNG value proposition to end customer

Pillar... Environmental Sustainability

Methane has the highest hydrogen to carbon ratio = lowest CO2.

Butane[C4H10]

10:4(250%)

Propane[C3H8]

8:3(267%)

Ethane[C2H6]

6:2(300%)

Methane[CH4]

4:1(400%)

Natural gas a mixture of hydrocarbon gases associated with petroleum deposits, principally methane.

MGO 1.86:1 (186%)Natural gas… lowest carbon = cleanest burning fuel

How clean ?

CO2

NOx

SOx

ParticulatesDF Natural Gas

Engine

DieselEngine

0

20

40

60

80

100

Emissionvalues [%]

-25%

-85%

-99%

-99%

LNG provides significant emission reductions compared to traditional diesel engines

Logic… Economics !

02/11/2015

Pillar… Economics... it saves money!

LNG provides compelling savings… Business Cases demonstrate

Payback screen short term … <4 years... Strong cash flows… Higher ROIC & EBITDA

Competitive Advantage

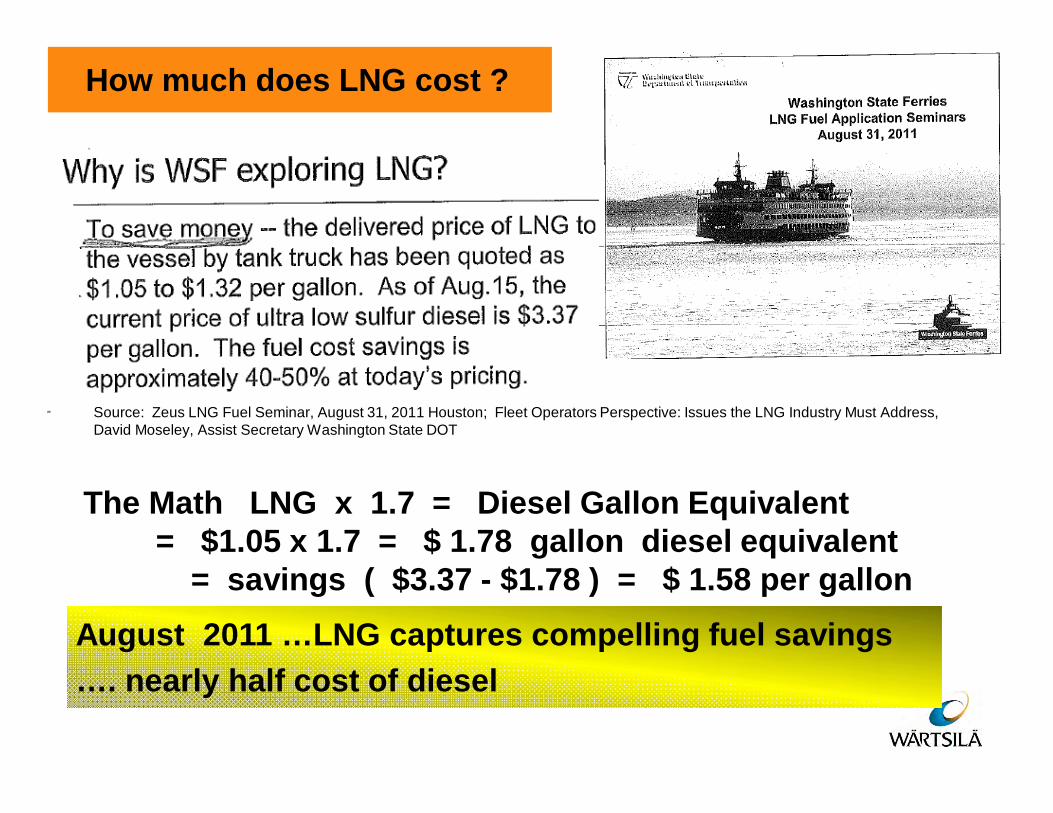

How much does LNG cost ?

The Math LNG x 1.7 = Diesel Gallon Equivalent= $1.05 x 1.7 = $ 1.78 gallon diesel equivalent

= savings ( $3.37 - $1.78 ) = $ 1.58 per gallon

Source: Zeus LNG Fuel Seminar, August 31, 2011 Houston; Fleet Operators Perspective: Issues the LNG Industry Must Address, David Moseley, Assist Secretary Washington State DOT

August 2011 …LNG captures compelling fuel savings …. nearly half cost of diesel

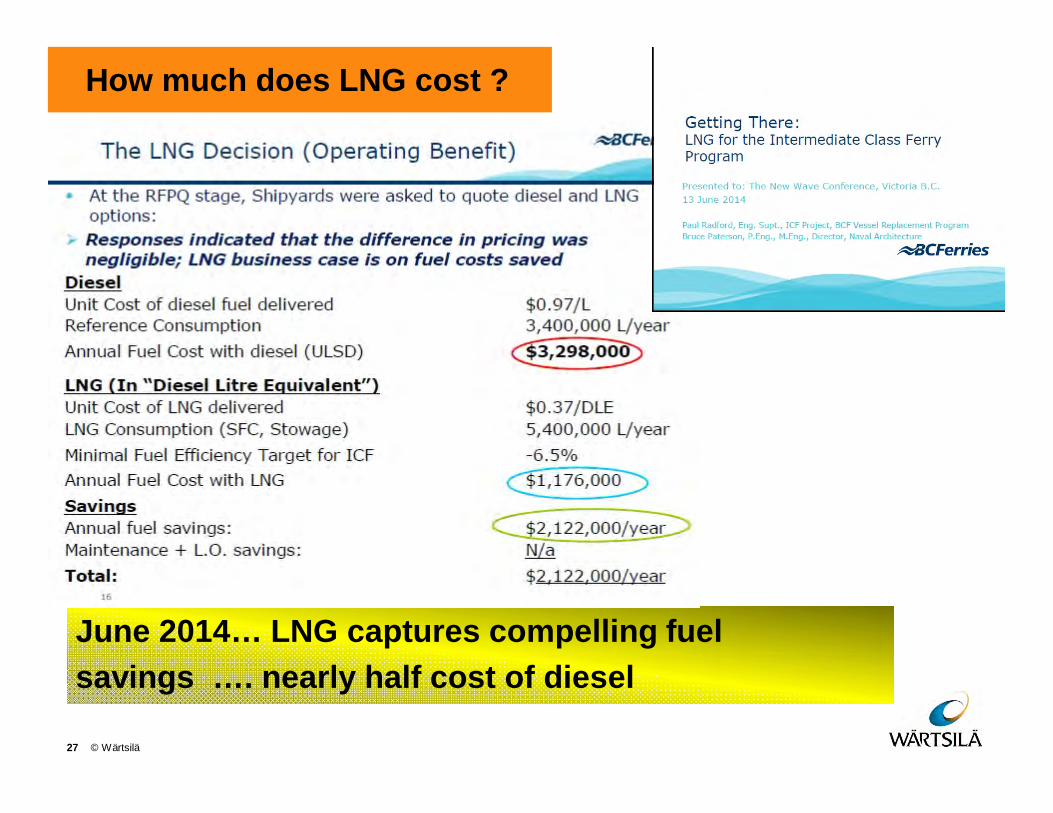

How much does LNG cost ?

27 © Wärtsilä

June 2014… LNG captures compelling fuel savings …. nearly half cost of diesel

Pillar… Safe & Reliable

Viking Energy 2003Stril Pioner 2004

Europe’s decade LNG experience began offshore North Sea vessels… proven path for technology transfer to Americas

Agenda

29 © Wärtsilä

What ? Competitive Forces Americas & EU Gas BasisEmission Areas Expansion & Owner Choices

Why ? 5 Drivers Set Investment ClockAmericas Compelling Savings3 Gas Pillars

Business Case Cargo, Investor, Banker Views1400 TEU CoasterInvestment Returns

Oil Price Shock ! Business Case: Robust or Fragile?Stress Test

Conclusions Recent Market SignalsThe Future Decade for GasBusiness Case Appendix

Cautionary Remarks

Each investment case requires careful analysis, inclusion, and weighing a broad variety of issues stemming from technical, financial, operational, regulatory, and other areas.

The purpose of this exercise is to illustrate a Business Case example and how a few of many key considerations may be transcribed into financial modeling as an aide to decision making.

Readers are advised that neither the Author nor Wartsila nor it’s subsidiaries are responsible for any errors, omissions, or updates to this information contained herein or assumptions or derivations whatsoever.

30 © Wärtsilä

This presentation is no substitute for your good and responsible decision making. Please utilize prudence and caution when making investment decisions along with securing the advice and guidance of professionals.

4 Stakeholders

31 © Wärtsilä

SHIP OWNER

BANKER

PUBLIC

George Washington (1732- 1799)

Thomas Jefferson

( 1743- 1826)

Theodore Roosevelt

(1858- 1919)

Abraham Lincoln

(1809- 1865)

CARGO OWNER

4 Stakeholders

32 © Wärtsilä

SHIP OWNER

BANKER

PUBLIC

The cargo PULL to

move a deal forward

The entrepreneur

PUSH to make a deal

The Capital Cash to

PROPELL deal

Ultimate Environment

Safety

CARGO OWNER

4 Viewpoints

33 © Wärtsilä

SHIP OWNER

BANKER

PUBLIC

Transport safely at

optimal cost reliably

At fair return capturing

risks

Are risks understood

& I’m repaid !

Ultimate Environment

Safety

CARGO OWNER

4 Key Metrics

34 © Wärtsilä

SHIP OWNER

BANKER

PUBLIC

All In Charter

Freight rate $ / ton

Return on Investment:

ROIC, EBITDA, cash flows

EBIT, Times Burden Cover,

cash flows

Ultimate Environment

Safety

CARGO OWNER

Business Case Vessel

35 © Wärtsilä

Over 100 ships annually built of similar size

The Route… Miami - Kingston - Caucedo

36 © Wärtsilä

Foreign flag 1400 TEU Container … Emission Control Area route significant “ECA” Bound…2110 Nautical Miles, cargo operations 8 hrs/port, 359 operating days, 6 weather days

37 © Wärtsilä

Foreign Flag Vessel & US Corporation

1,400 TEU Capacity ( 334 Reefers )

Speed 18 knots… single Screw … 2 Stroke

Propulsion power 13,500 HP ( 10,080 kW )

Manning SOLAS Compliant

Certified Major Class Society

1400 TEU Container Coaster

Speed provides 55 annual round trips along route… vessel size yields competitive cost tonnage delivery economics.. LNG fuel… load factor 50%

Recall ?

38 © Wärtsilä

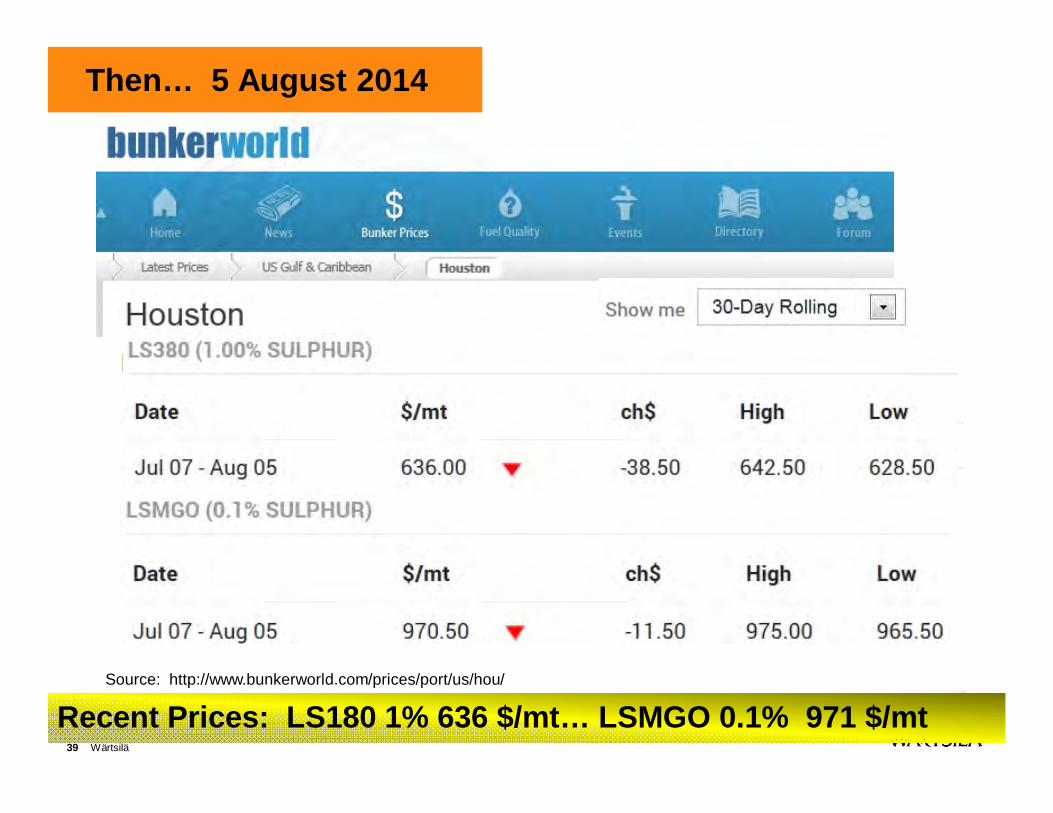

Then… 5 August 2014

39 Wärtsilä

Recent Prices: LS180 1% 636 $/mt… LSMGO 0.1% 971 $/mtSource: http://www.bunkerworld.com/prices/port/us/hou/

Cargo Owner Transport safely at optimal cost reliably

40 © Wärtsilä

Cargo owner with LNG fuel choice benefits millions transport savings… $6.7 to $13.5 million over five years per ship… times how many ships?

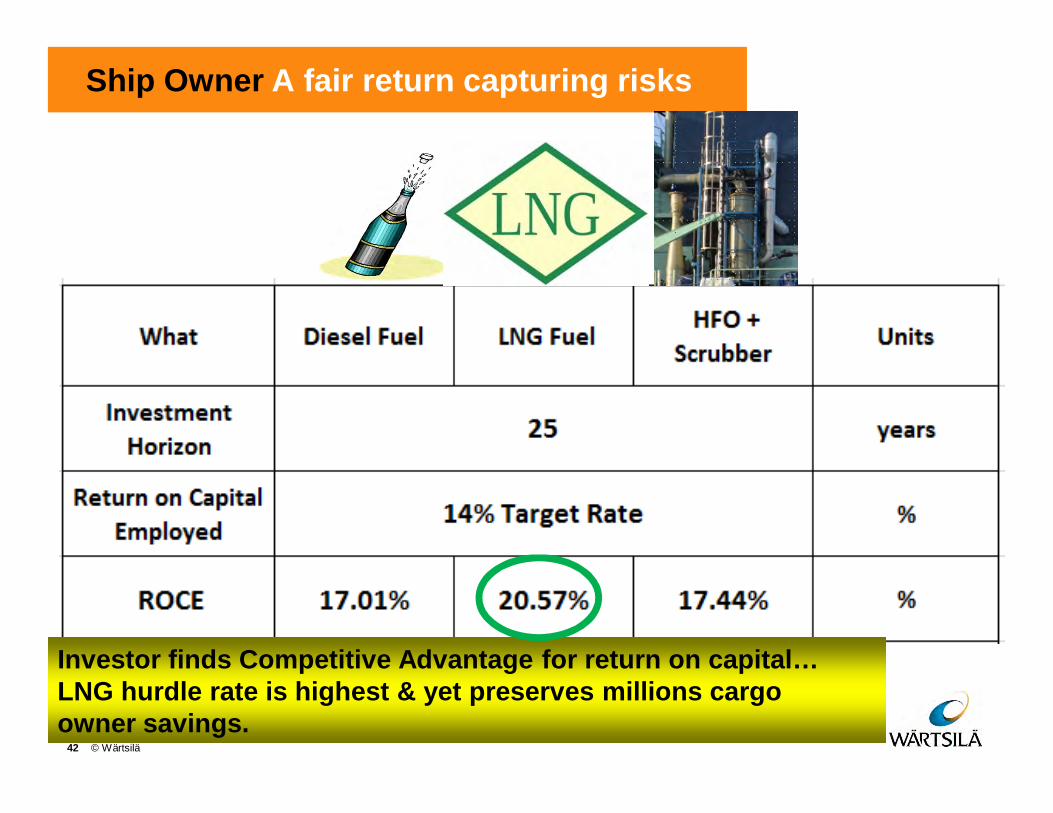

Ship Owner A fair return capturing risks

41 © Wärtsilä

Compelling fuel payback for vessels running on LNG fuel; an initial screening tool … not a good investment metric.

Ship Owner A fair return capturing risks

42 © Wärtsilä

Investor finds Competitive Advantage for return on capital… LNG hurdle rate is highest & yet preserves millions cargo owner savings.

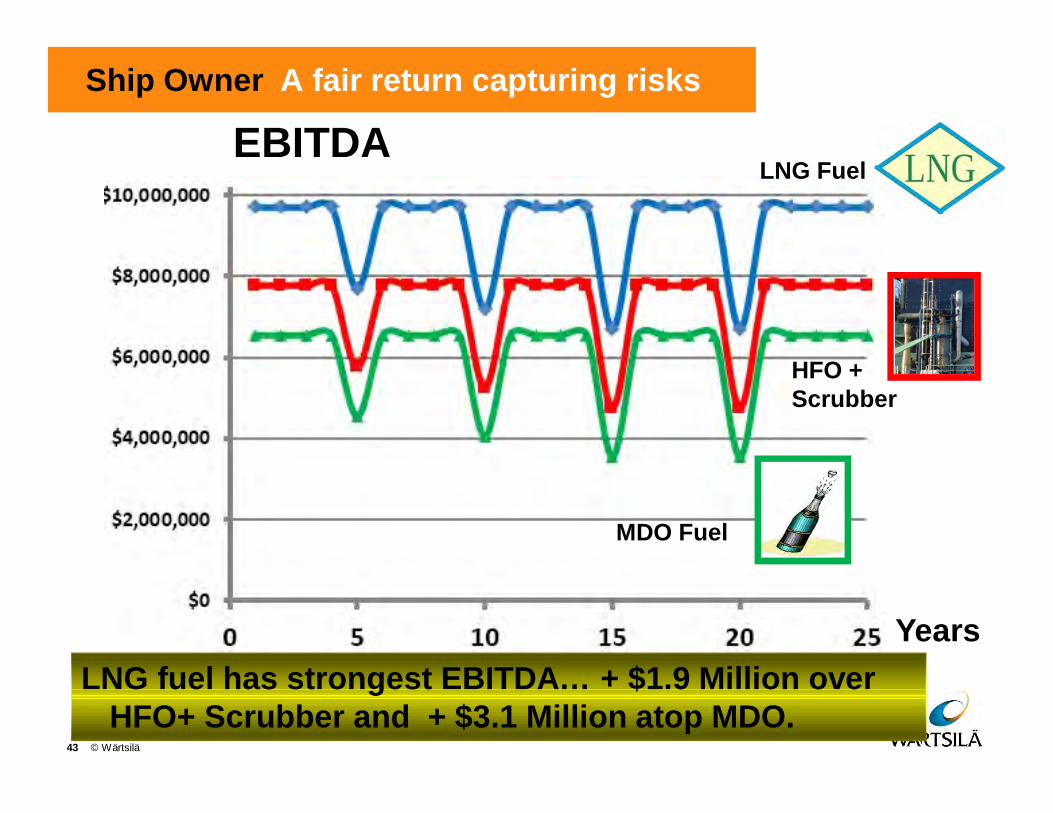

43 © Wärtsilä

LNG fuel has strongest EBITDA… + $1.9 Million over HFO+ Scrubber and + $3.1 Million atop MDO.

Years

EBITDA

MDO Fuel

HFO + Scrubber

LNG Fuel

Ship Owner A fair return capturing risks

Banker Are risks understood & I’m repaid !

44 © Wärtsilä

Banker finds debt cover is weakest on MDO fuel, favorably stronger on alternatives, LNG is strongest.

45 © Wärtsilä

Years

EBITBanker Are risks understood & I’m repaid !

LNG has strongest EBIT… Depreciation 10 Year MACRS ½ Year Convention… Dry docking years 5,10,15,20

LNG Fuel

HFO + Scrubber

MDO Fuel

Agenda

46 © Wärtsilä

What ? Competitive Forces Americas & EU Gas BasisEmission Areas Expansion & Owner Choices

Why ? 5 Drivers Set Investment ClockAmericas Compelling Savings3 Gas Pillars

Business Case Cargo, Investor, Banker Views1400 TEU CoasterInvestment Returns

Oil Price Shock ! Business Case: Robust or Fragile?Stress Test

Conclusions Recent Market SignalsThe Future Decade for GasBusiness Case Appendix

Recall Shale Gas

47 © Wärtsilä

North America Shale Oil Plays

02 November 2015Source: http://www.ogj.com/articles/print/vol-110/issue-12/processing/us-refining-outlook-rosier-than.html

US shale crude revolution; reserves exceed 120 billion BBL

49 © Wärtsilä

Source: http://www.usfunds.com/investor-library/frank-talk/one-of-the-most-notable-stories-of-the-year-energy-renaissance-in-the-usa/

5% CAGR

14% CAGR

58% CAGR

Shale crude surging… 2006 growth strong; 2010 frantic

US Shale Crude Production

5 January 2015

50 © Wärtsilä Source: http://www.forbes.com/sites/nathanvardi/2015/01/05/saudi-arabias-750-billion-bet-drives-brent-oil-below-54/

Exert Discipline in the Marketplace amongst OPEC and Non OPEC countries... Key focus on market share

Brent Crude Oil Prices

51 © Wärtsilä

Source: http://www.nasdaq.com/markets/crude-oil-brent.aspx?timeframe=1y

THEN

Crude severe price drop past year as abundant supplies face weak demand

NOW

Oil Prices Dropping

52 © Wärtsilä

Source: http://www.bloomberg.com/news/2015-01-26/oil-slides-to-near-6-year-low-as-u-s-supply-seen-worsening-glut.html

26 January 2015

Oil down 60% since June…US WTI crude closes at multi - year low… caused by oil glut from…

Strong Supply : US shale boom + Libya restarts large oilfield…& Saudi Arabia not reducing supply

Soft Demand: China strong but tapering & EU slight recession…

Discipline Target US or Russia ?

53 © Wärtsilä

Russia suffering double whammy:

Oil rich Ukraine and Black Sea burdened by politics under imposed sanctions as oil takes severe price slide…

Ruble plunges down 50% against USD

Source: http://online.wsj.com/articles/ruble-hits-new-low-as-oil-prices-drop-1417441184

Source: http://www.usnews.com/news/articles/2014/11/10/an-oil-price-cold-war-with-saudi-arabia-not-so-fast-experts-say

Source: http://www.businessinsider.com/ruble-plunging-again-2014-12p://online.wsj.com/articles/ruble-hits-new-low-as-oil-prices-drop-1417441184

1 December 2014

26 January 2015

54 © Wärtsilä

Source: http://www.cnbc.com/id/102366561#.

Recent low for crude

Source: http://www.businessinsider.com/citi-saudi-arabia-wont-win-this-oil-standoff-2014-11 55 © Wärtsilä

Profits negative… Severe Pain

Profits squeezed…Manageable Pain

45 $/BBL

Key Oil Production Cost

50$/BBL

Total Liquids Production

Brent Breakeven Price

2014 Oil Production

56 © Wärtsilä

US vaults to 3rd in world crude production in 2014

Source: http://en.wikipedia.org/wiki/List_of_countries_by_oil_production

Government Breakeven Budgets

57 © Wärtsilä

Severe shortfalls @ prices under 100$/BBL, present oil glut & soft prices challenge sustainability beyond short run

Source: https://alfinnextlevel.files.wordpress.com/2014/04/oil_breakeven_deutsche_bank_oct_14.png

50 $/BBL

What’s the impact of the steep fall in oil prices !

Is competitive advantage of LNG robust or fragile ?

58 © Wärtsilä

Recent … 12 October 2015

59 Wärtsilä

Prices : LS380 225 $/mt… LSMGO 0.1% 484 $/mt

Source: http://www.bunkerworld.com/prices/port/us/hou/

Owner At fair return capturing risks of oil fall 12 Oct 2015

60 © Wärtsilä

LNG competitive advantage retains millions savings for shipper but returns narrow for investor amidst oil glut steep price dive.

Fuel Stress Test

THEN 5 August 201420.6% @ LNG 480 $/mt 17.0% @ MDO 971 $/mt17.4% @ HFO 636 $/mt

61 © Wärtsilä

Deviation

ROCE

NOW 12 October 201522.4% @ LNG 400 $/mt 31.6% @ MDO 474 $/mt28.9% @ HFO 225 $/mt

LNG robust despite steep crude drop whose irrational conditions are not sustainable! Most volatile returns MDO, then HFO, least with LNG… holds market cargo share with compelling millions shipper savings.

Agenda

62 © Wärtsilä

What ? Competitive Forces Americas & EU Gas BasisEmission Areas Expansion & Owner Choices

Why ? 5 Drivers Set Investment ClockAmericas Compelling Savings3 Gas Pillars

Business Case Cargo, Investor, Banker Views1400 TEU CoasterInvestment Returns

Oil Price Shock ! Business Case: Robust or Fragile?Stress Test

Conclusions Recent Market SignalsThe Future Decade for GasBusiness Case Appendix

14 February 2014

63 © Wärtsilä Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=6264:harvey-gulf-breaks-ground-for-lng-fueling-facillity&Itemid=227 .

Harvey Gulf Port Fourchon LNG fueling facility operational 2015

64 Wärtsilä

18 February 2014

2 Vessels… total 94mW = North America’s largest LNG conversion undertaken !

Source: http://www.motorship.com/news101/lng/tote-goes-with-wartsila-four-strokes-for-lng-conversions

25 February 2014

65 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=6310:tote-cuts-steel-for-lng-fueled-containership&Itemid=227 .

1st LNG fuel containerships commence construction @ NASSCO

11 March 2014

66 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=6373:elliott-bay-design-group-gets-aip-for-lng-bunker-barge&Itemid=225 .

LNG bunker barge designs moving industry forward

16 April 2014

67 Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=6580:lockheed-martin-delivers-lng-tank-for-harvey-gulf-newbuild&Itemid=231

Americas industrial base expanding supply of key LNG enablers

17 April 2014

02 November 201568

Source: http://www.caribbeanbusinesspr.com/prnt_ed/crowley-extremely-positive-about-lng-units-growth-prospects-9768.html

Safe, clean, low cost LNG fuel from US shipments may lower power costs…

16 June 2014

69 © Wärtsilä Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=6853:nassco-books-another-jones-act-tanker-order&Itemid=223 .

American Petroleum Tankers “APT” orders another LNG ready tanker from NASSCO

25 June 2014

70 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=6905:crowley-seeks-title-xi-guarantees-for-lng-fueled-conro-pair&Itemid=223 .

Crowley and TOTE filing for MARAD Title 11 Loan Finance Guarantees

3 July 2014

71 © Wärtsilä Source: https://www.bcferries.com/bcferries/faces/attachments?id=856428

Now 6 LNG fuel ferries for Canada as BC Ferries (3) follows STQ

72 Wärtsilä

15 July 2014

Source: http://maritimeintel.com/maersk-warns-sulphur-regulation-will-cost-us250-million-annually/

Prohibitively expensive compliant diesel inside ECA in 2015 !

More Traditional Pain = More LNG Gain

19 November 2014

73 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=8277:seaspan-orders-two-lng-fueled-ferries&Itemid=230

Now 8 LNG fuel ferries for Canada

2 December 2014

74 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=8352:abs-approves-lng-fueled-z-drive-towboat-design&Itemid=231

River towboats 100% ECA bound consider LNG fuel.

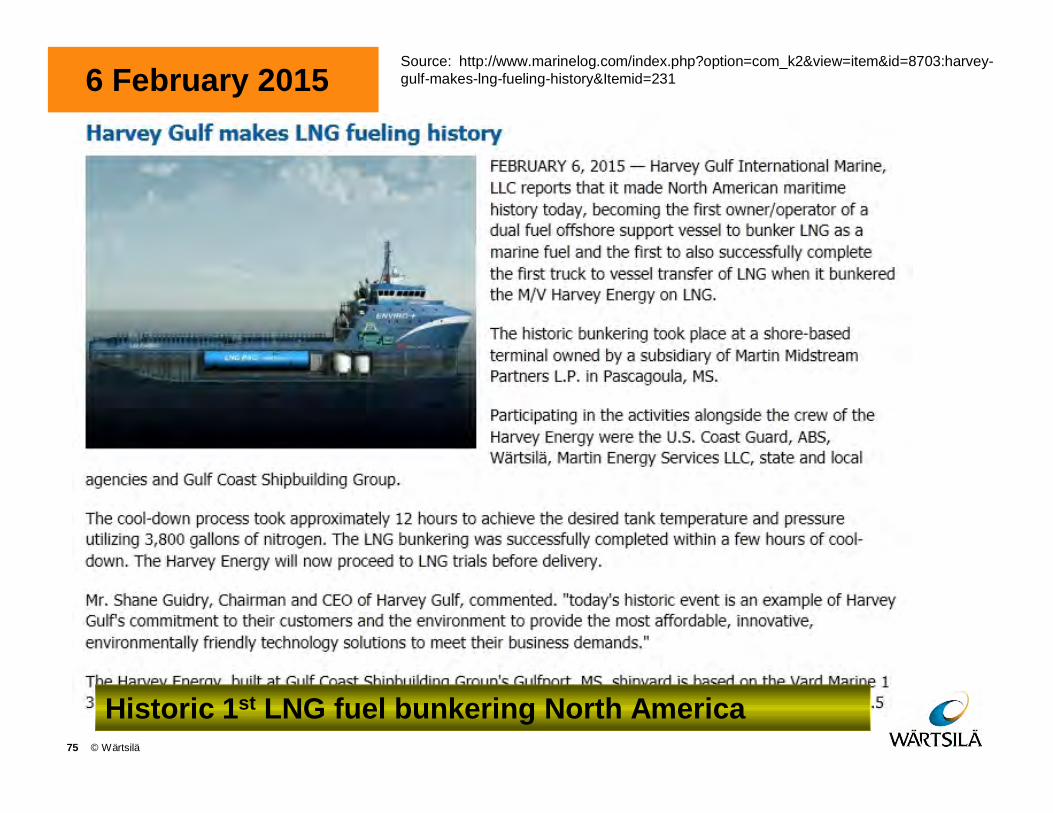

6 February 2015

75 © Wärtsilä

Historic 1st LNG fuel bunkering North America

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=8703:harvey-gulf-makes-lng-fueling-history&Itemid=231

25 February 2015

76 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=8787:conrad-shipyard-to-build-first-lng-bunker-barge-in-us&Itemid=225

1st LNG Bunker Barge for US; slated for PNW then redeployed to Jacksonville for TOTE’s Caribbean service.

5 March 2015

77 © Wärtsilä

Maritime History: Americas 1st Offshore LNG fuel Vessel enters service.

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=8822:harvey-energy-starts-working-for-shell&Itemid=231

20 March 2015

78 © Wärtsilä

STQ Ferry F. A. Gauthier on sea Trials, 1st LNG Fuel Ferry North America soon to enter service

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=8896:lng-fueled-ferry-wont-reach-quebec-until-april&Itemid=231

11 April 2015

79 © Wärtsilä

Source: http://www.wsj.com/articles/SB21439164361287373597304580572050147269116

20 April 2015

80 © Wärtsilä

Historic world wide moment: TOTE’s Marlin Class 3,100 TEU ship launched for Puerto Rico trade !

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=9035:nassco-launches-worlds-first-lng-fueled-containership&Itemid=231

9 July 2015

81 © Wärtsilä

BC Ferries short lists yards for 2 Spirit Class retrofits to Dual Fuel operation on LNG

Source: http://www.marinelog.com/index.php?option=com_k2&view=itemlist&task=tag&tag=ferry

15 July 2015

82 © Wärtsilä

Source: http://hhpinsight.com/marine/2015/07/stqs-gauthier-lng-ferry-enters-service/

North America’s first LNG ferry enters service

19 July 2015

83 © Wärtsilä

Historic Americas moment: Davies Launches first of 2 Dual Fuel Ferries for STQ

Source: http://www.marinelog.com/index.php?option=com_k2&view=itemlist&task=tag&tag=ferry

25 August 2015

84 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=9646:vt-halter-lays-keel-for-second-lng-fueled-crowley-conro&Itemid=223

2nd Crowley LNG fuel ready ConRo ship begins construction

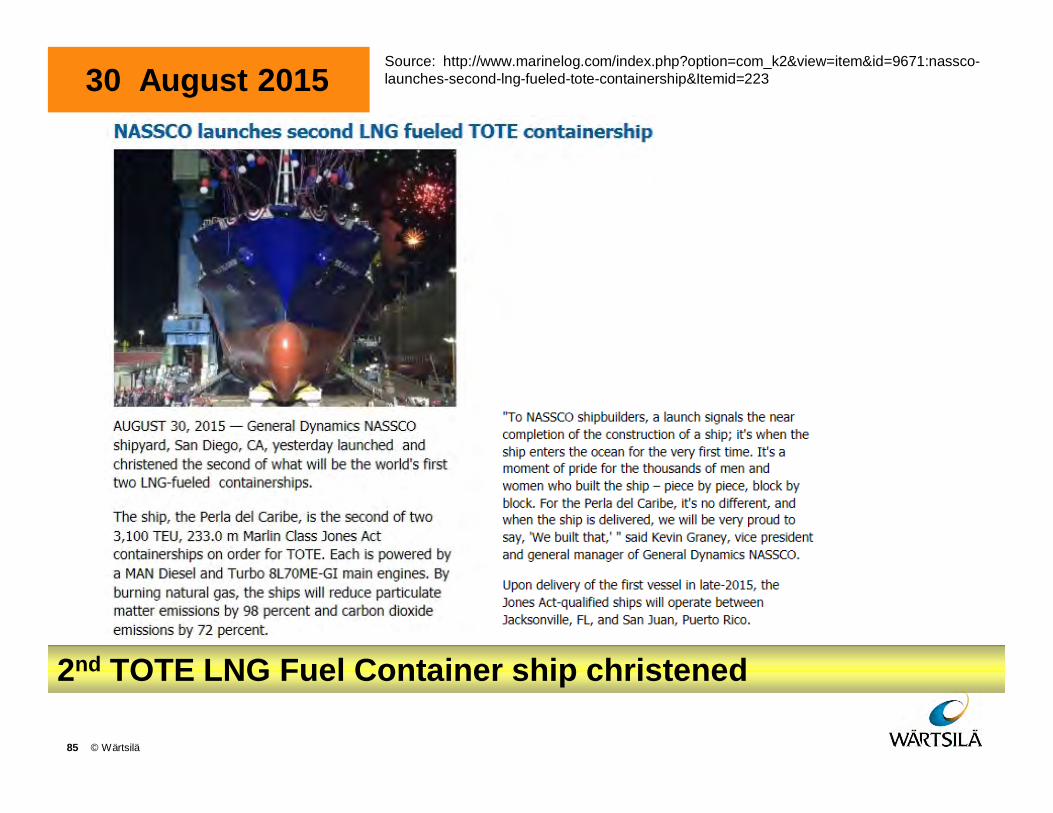

30 August 2015

85 © Wärtsilä

2nd TOTE LNG Fuel Container ship christened

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=9671:nassco-launches-second-lng-fueled-tote-containership&Itemid=223

9 September 2015

86 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=9719:keel-laid-for-first-lng-bunker-barge-at-conrad-orange&Itemid=223

Americas first LNG bunker barge begins construction

1 October 2015

87 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=9831:crowley-takes-deliver-of-first-lng-ready-jones-act-tanker&Itemid=231

First LNG ready tanker delivered to Crowley

7 October 2015

88 © Wärtsilä

Source:http://www.marinelog.com/index.php?option=com_k2&view=item&id=9864:aker-philly-cuts-steel-for-two-more-kinder-morgan-tankers&Itemid=223

3rd & 4th LNG ready tankers steel cut for Kinder Morgan

16 October 2015

89 © Wärtsilä

World’s first LNG fuel Container ship delivered

18 October 2015

90 © Wärtsilä

Source: http://www.marinelog.com/index.php?option=com_k2&view=item&id=9920:harvey-gulf-takes-delivery-of-second-lng-fueled-osv&Itemid=231

2nd LNG fuel OSV delivered for Harvey Gulf

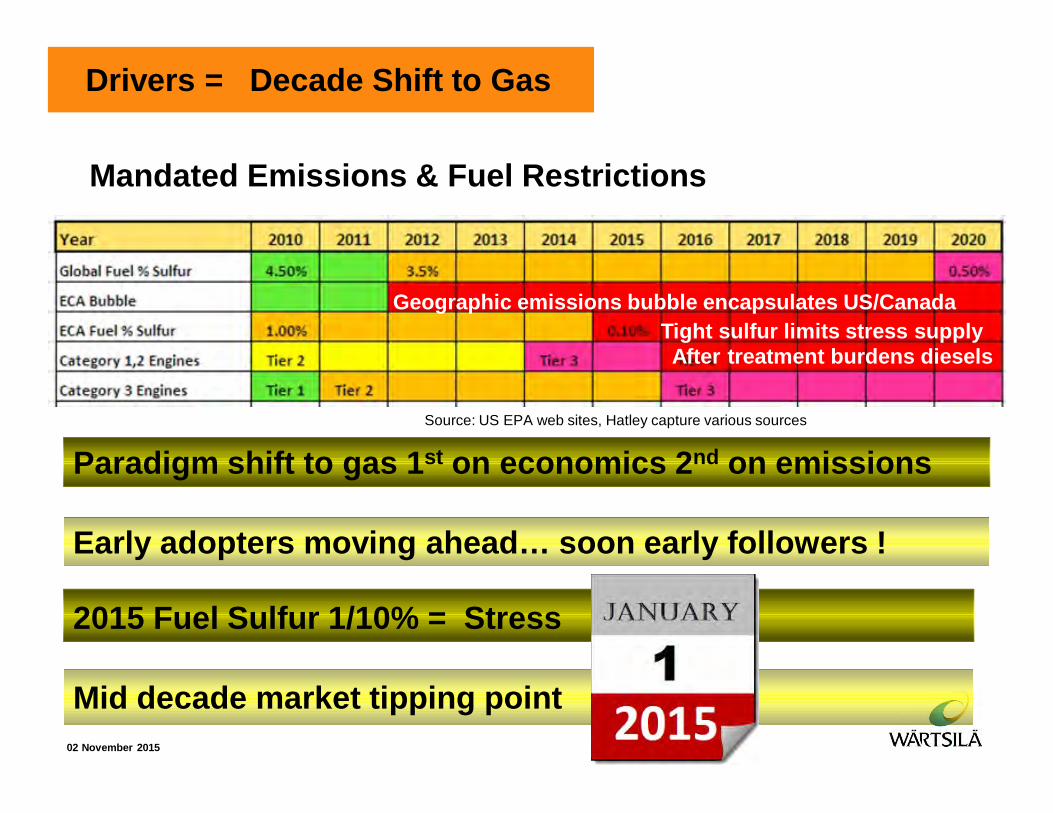

Drivers = Decade Shift to Gas

02 November 2015

Mid decade market tipping point

Source: US EPA web sites, Hatley capture various sources

Geographic emissions bubble encapsulates US/CanadaTight sulfur limits stress supplyAfter treatment burdens diesels

Paradigm shift to gas 1st on economics 2nd on emissions

Early adopters moving ahead… soon early followers !

Mandated Emissions & Fuel Restrictions

2015 Fuel Sulfur 1/10% = Stress

APPENDIXBusiness Case Details

92 Wärtsilä

Financials

93 Wärtsilä

Key Values`

94 Wärtsilä

Key Values

95 Wärtsilä

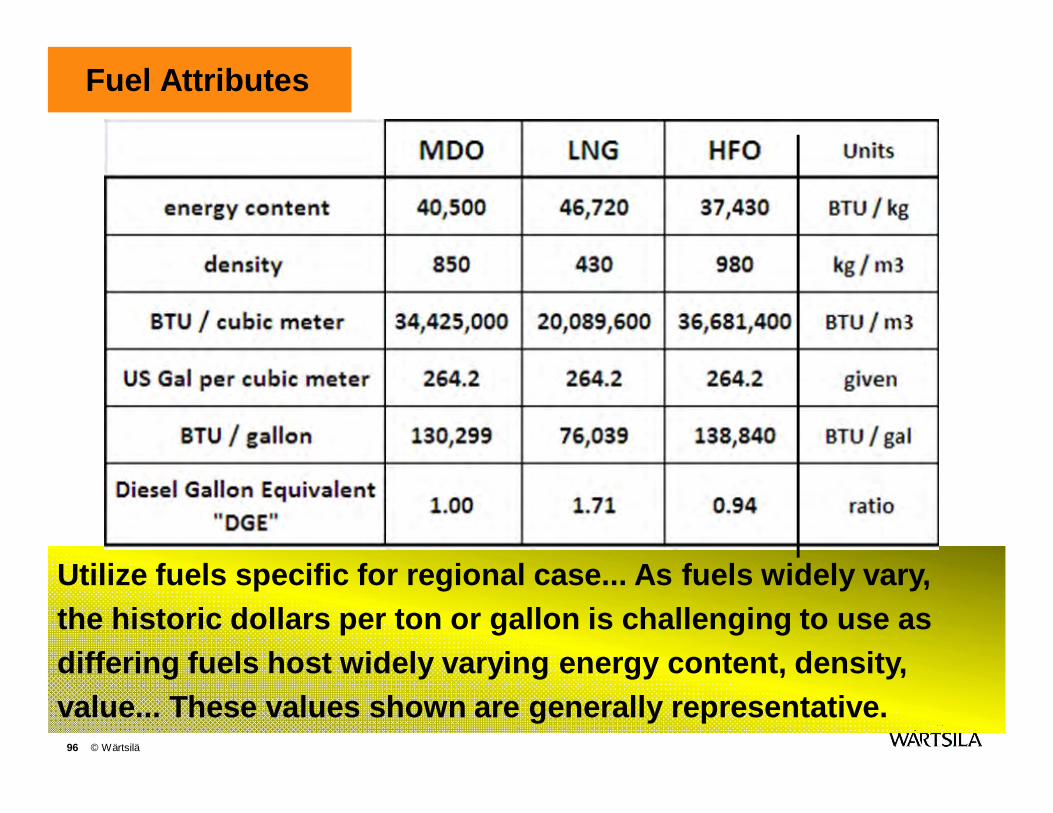

Fuel Attributes

96 © Wärtsilä

Utilize fuels specific for regional case... As fuels widely vary, the historic dollars per ton or gallon is challenging to use as differing fuels host widely varying energy content, density, value... These values shown are generally representative.

EBIT

97 © Wärtsilä

EBITDA

98 © Wärtsilä

Coverage Ratio Times Debt Burden Covered

Times Debt Burden Covered = . EBITDA .Principal Repayment.

Interest + ( 1 - tax rate )

Times Burden Covered includes both obligations of debt loan interest and principal repayment.

When including principal payment as a part of a company’s financial burden, express the figure on a before tax basis. Unlike interest payments, principal payments are not a tax deductible expense. Adjusting principal payment is “grossing up the principal.”

As replacement of maturing debt is not certain, witness the recent severe recession when creditors refused to renew maturing obligations, then debt burden becomes interest plus retiring principal payments.

Times burden covered is very conservative since it presumes a company pays existing loans down to zero without roll over.

Source: Higgens, Analysis for Financial Management 10th Edition, page 49-50 uses EBIT not EBITDA.

99 © Wärtsilä

Coverage Ratio Times Interest Earned

Times Interest Earned = . EBITDA .

Interest ExpenseTimes Interest Earned shows the available cash flow to pay debt interest

payments.

If a company is able to always roll over it’s maturing obligations with new loans, then the net burden is merely the interest expense.

However, during a financial panic replacement of maturing debt by new is not always available as credit markets tightened during the recent severe recession.

The Times Interest Earned ratio is too liberal because it assumes a company will always roll over its maturing obligations.

Source: Higgens, Analysis for Financial Management 10th Edition, page 50 uses EBIT not EBITDA.

100 © Wärtsilä

Cash Flow from Operating Activities

101 © Wärtsilä

Cash Flow from Investing Activities

102 © Wärtsilä

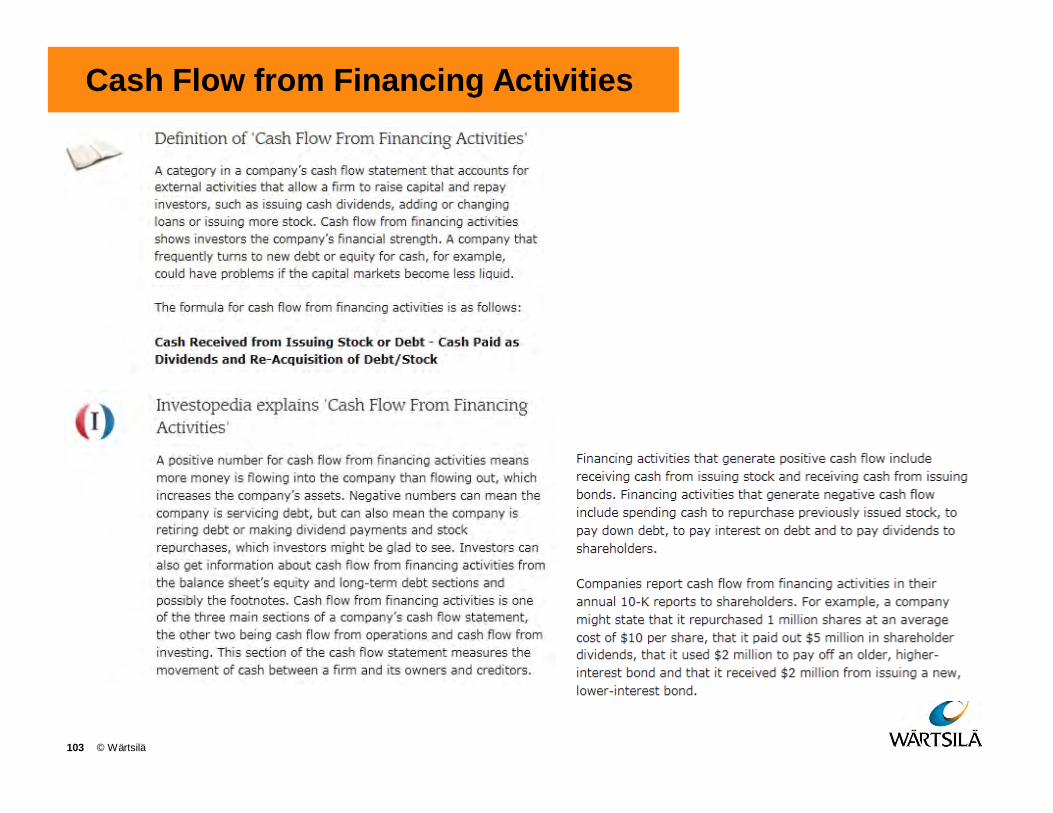

Cash Flow from Financing Activities

103 © Wärtsilä

Agenda

104 © Wärtsilä

What ? Competitive Forces Americas & EU Gas BasisEmission Areas Expansion & Owner Choices

Why ? 5 Drivers Set Investment ClockAmericas Compelling Savings3 Gas Pillars

Business Case Cargo, Investor, Banker Views1400 TEU CoasterInvestment Returns

Oil Price Shock ! Business Case: Robust or Fragile?Stress Test

Conclusions Recent Market SignalsThe Future Decade for GasBusiness Case Appendix