Embed Size (px)

Citation preview

Mercosur Mercosur Energy Energy IntegrationIntegration

Hugo A. D’Angelo Hugo A. D’Angelo (h)(h) Senior Consultant Oil & Senior Consultant Oil & Natural Gas – Thompson & Knight LLP – Rio de Natural Gas – Thompson & Knight LLP – Rio de Janeiro, Brazil Janeiro, Brazil

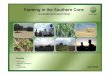

PB 100% and PB/Partners Other Companies

59 thousand bpd oil59 thousand bpd oil9.375 thousand 9.375 thousand

mm33/d gas/d gas93 thousand bpd oil93 thousand bpd oil2.383 thousand m2.383 thousand m33/d /d

gasgas

52 thousand bpd oil52 thousand bpd oil4.608 thousand m4.608 thousand m33/d /d

gasgas

52 thousand bpd oil52 thousand bpd oil5.402 thousand m5.402 thousand m33/d /d

gasgas

21 thousand bpd oil21 thousand bpd oil1.112 thousand m1.112 thousand m33/d /d

gasgas

Campos BasinCampos Basin1.447 thousand bpd oil (84%)1.447 thousand bpd oil (84%)

21.451 thousand m21.451 thousand m33/d gas (47%)/d gas (47%)1,5 thousand bpd oil1,5 thousand bpd oil1.112 thousand m1.112 thousand m33/d /d

gasgas

DOMESTIC PRODUCTION

Oil: 1.729 thousand bpd Gas: 45.563 thousand m3/d

Total: 2.016 thousand boe/d

4 thousand bpd oil4 thousand bpd oil120 thousand m120 thousand m33/d gas/d gas

Production per Basin (May/2005)

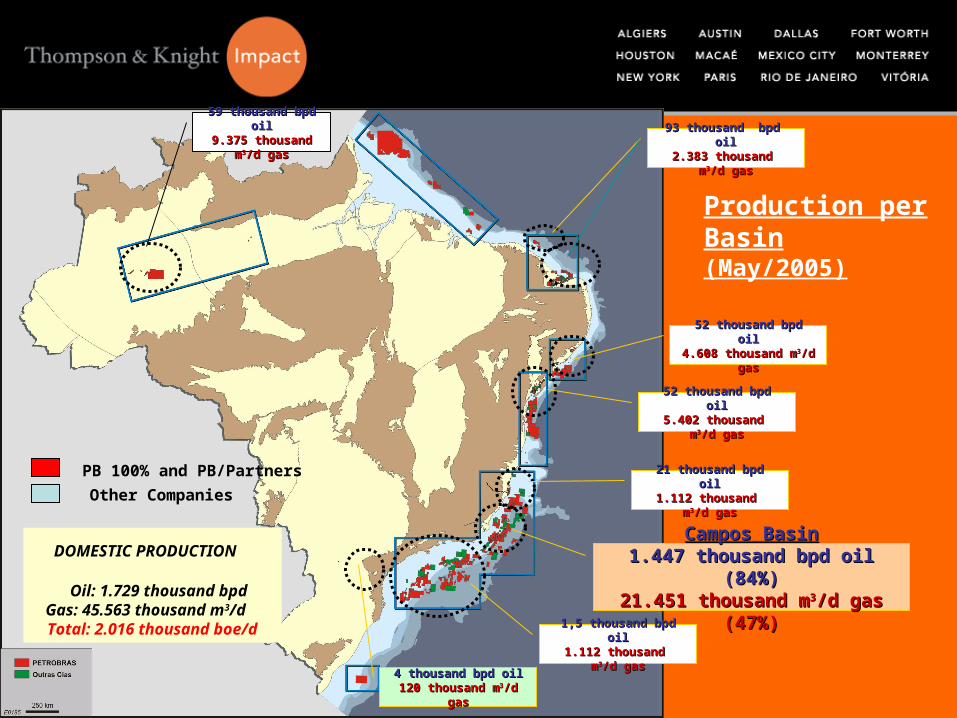

Equatorial Margin Frontier Basins Frontier Basins

Natural Gas & Light OilNatural Gas & Light Oil High Risks and Economic High Risks and Economic

ResultsResults

Basins of Espírito Santo, Campos & Santos Appraisal of the Recent Heavy Oil Findings Appraisal of the Recent Light Oil, Gas & Condensate

Findings Exploration of the Pre-Salt & Albian Carbonates

Moderate Risks & High Economic Results

Exploration Perspectives:

Solimões & Amazonas Light Oil, Natural Gas & Light Oil, Natural Gas &

Condensate GasCondensate Gas Moderate Risks and Economic Moderate Risks and Economic

ResultsResults

Basins of the Northeast Margin Natural Gas & Light OilNatural Gas & Light Oil

Moderate Risks & Low Economic Moderate Risks & Low Economic ResultsResults

Basins of the East Margin Natural Gas & Light Oil

Moderate Risks & High Economic Moderate Risks & High Economic ResultsResults

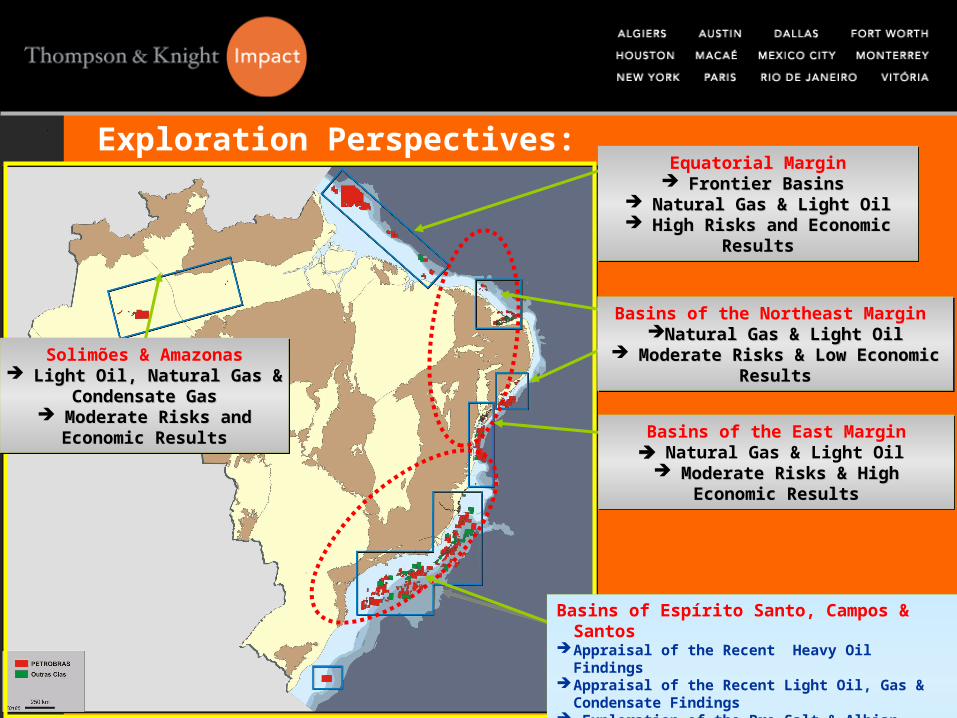

1,7 tcf

ReservesNortheast

7,7 tcf

ReservesSouth-

Southeast

1,7 tcf

Solimões Basin

Gas Proved Reserves in Brazil (Dec/2004)

11,1 tcfBRAZIL

tcf = trillion cubic feet = 28,32 billion m3

GASProved ReservesBilion m3

TOTAL

SOUTH/SOUTHEAST

NORTH

NORTHEAST 48,0

215,6

49,5

313,1

< 22º API(heavy oil)

44% 30%11%15%

Gas31 º API (light oil)

22 – 31 º API(intermediate oil)

Profile of Proved Reserves in Brazil

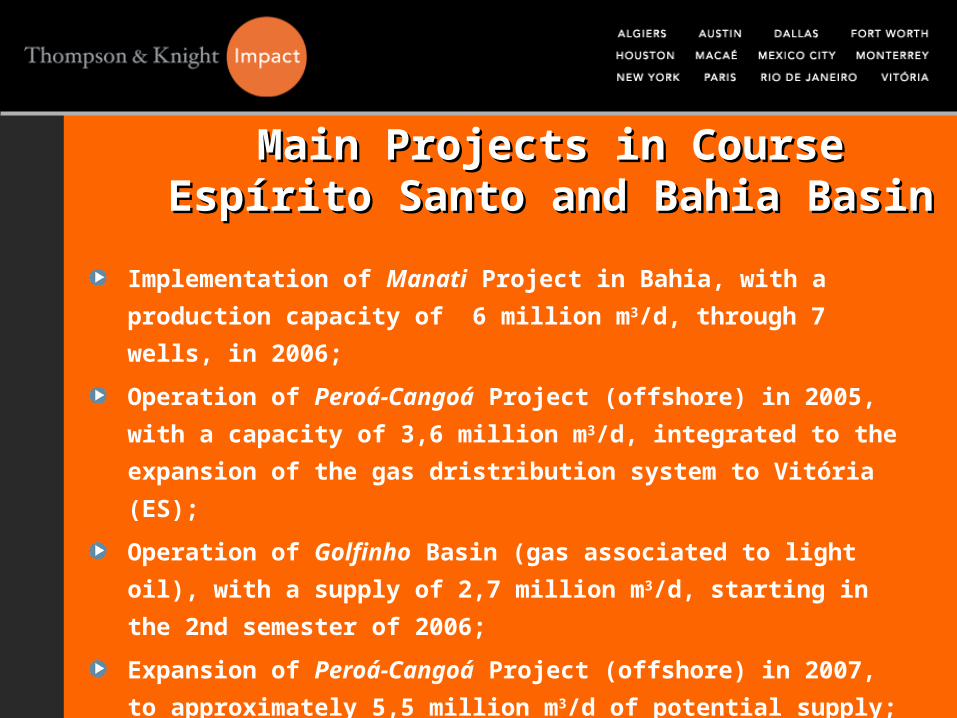

Main Projects in CourseMain Projects in CourseEspírito Santo and Bahia BasinEspírito Santo and Bahia Basin

Implementation of Manati Project in Bahia, with a production capacity of 6 million m3/d, through 7 wells, in 2006;

Operation of Peroá-Cangoá Project (offshore) in 2005, with a capacity of 3,6 million m3/d, integrated to the expansion of the gas dristribution system to Vitória (ES);

Operation of Golfinho Basin (gas associated to light oil), with a supply of 2,7 million m3/d, starting in the 2nd semester of 2006;

Expansion of Peroá-Cangoá Project (offshore) in 2007, to approximately 5,5 million m3/d of potential supply;

Optimization of gas from the Parque das Baleias Fields, associated to heavy oil in deep water, from 2010 on;

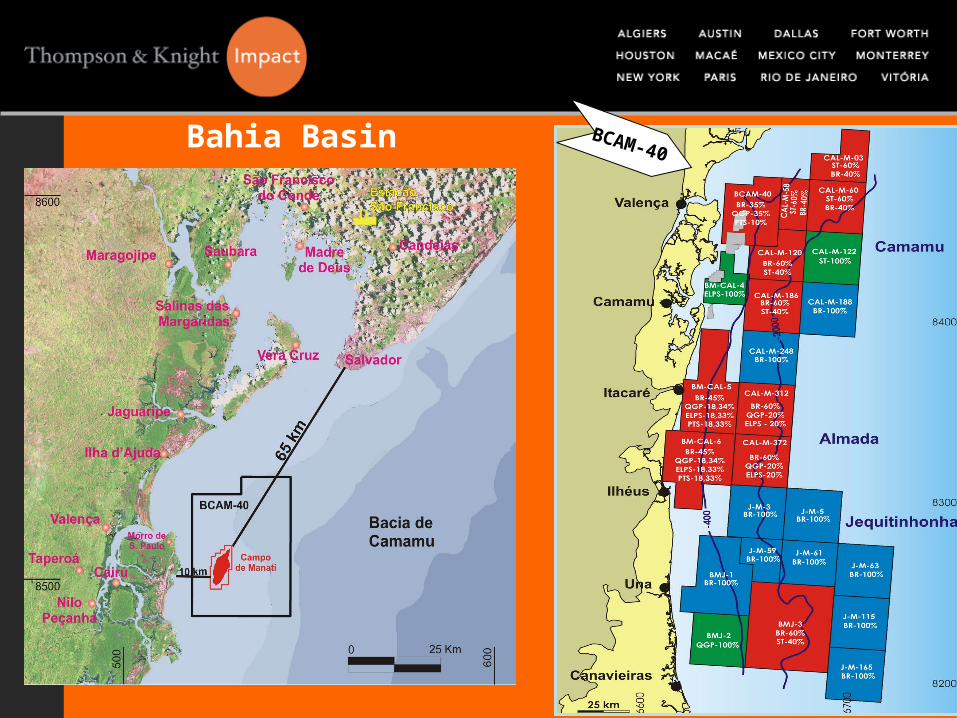

BCAM-40Bahia Basin

LIGHT OIL DEEP WATER

HEAVY OIL DEEP WATER

LIGHT OIL ULTRA DEEP

WATER

OIL SOIL

SHALLOWWATER

GAS SOIL

SHALLOW WATER

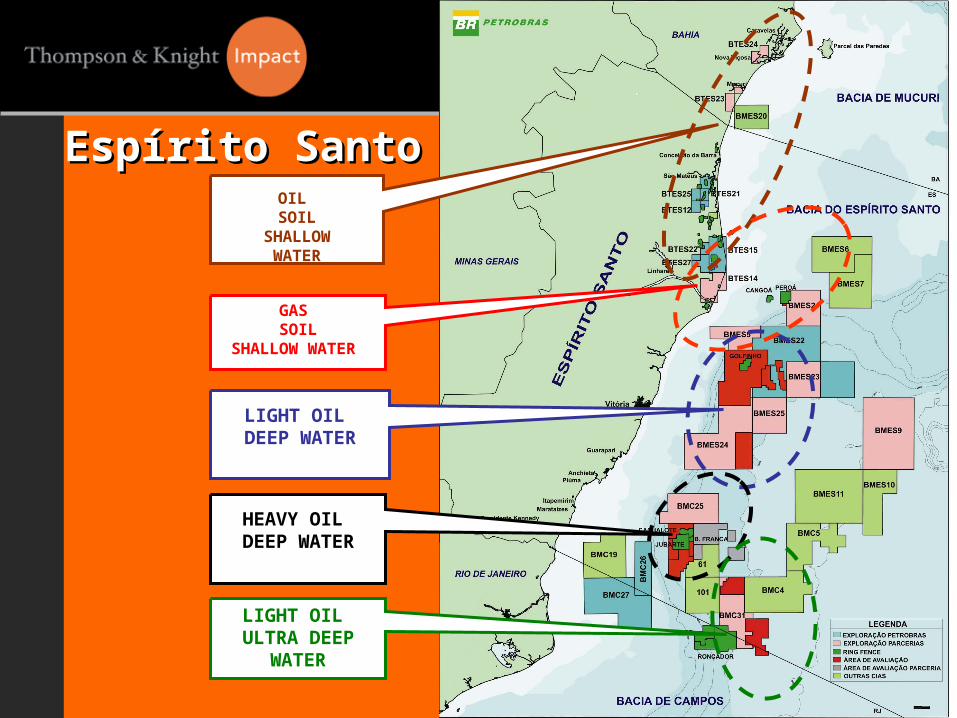

Espírito SantoEspírito Santo

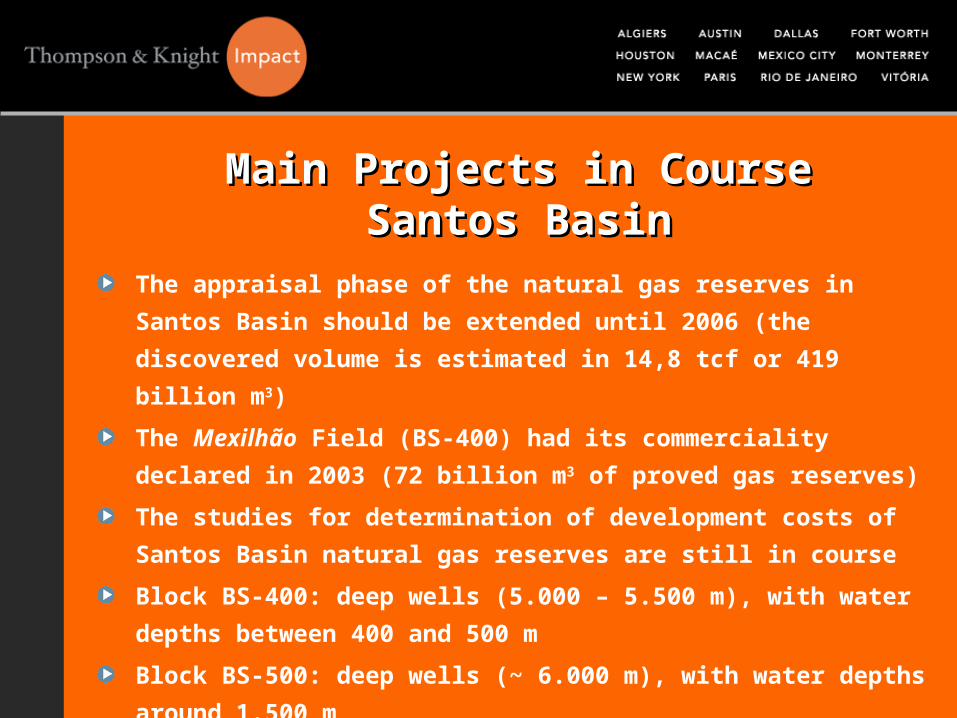

Main Projects in CourseMain Projects in CourseSantos BasinSantos Basin

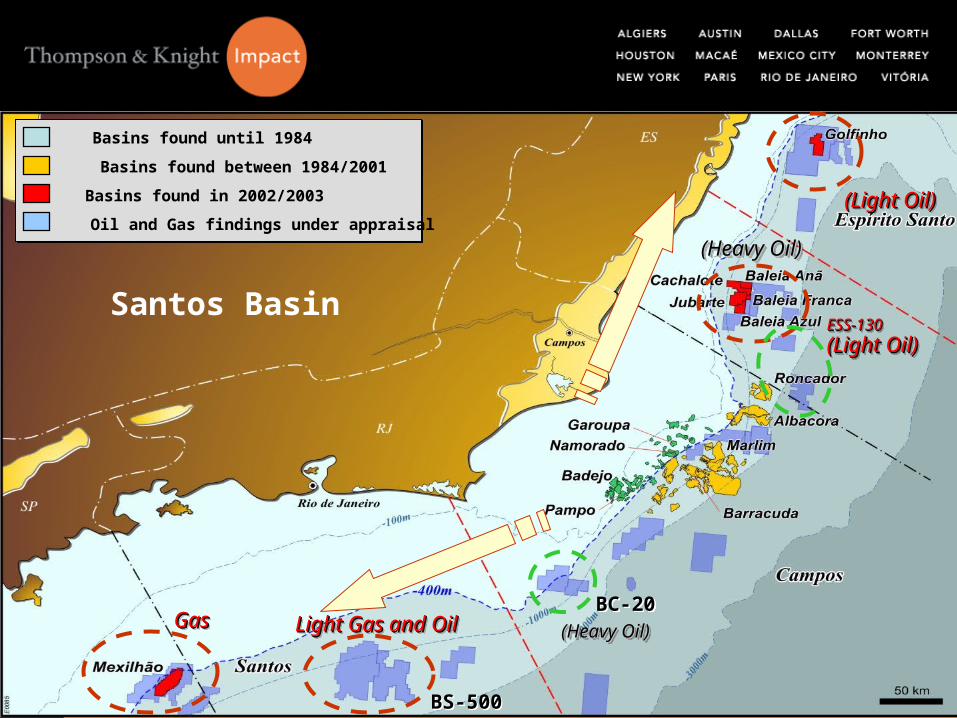

The appraisal phase of the natural gas reserves in Santos Basin should be extended until 2006 (the discovered volume is estimated in 14,8 tcf or 419 billion m3)The Mexilhão Field (BS-400) had its commerciality declared in 2003 (72 billion m3 of proved gas reserves)The studies for determination of development costs of Santos Basin natural gas reserves are still in course Block BS-400: deep wells (5.000 – 5.500 m), with water depths between 400 and 500 mBlock BS-500: deep wells (~ 6.000 m), with water depths around 1.500 m

A Expansão das Fronteiras Exploratórias Surgimento de Novas Províncias Produtoras

Basins found until 1984

Basins found between 1984/2001

Basins found in 2002/2003

Oil and Gas findings under appraisal

BS-500

BC-20Light Gas and OilLight Gas and Oil

ESS-130 ESS-130 (Light Oil)(Light Oil)

(Light Oil)(Light Oil)

GasGas

(Heavy Oil)(Heavy Oil)

(Heavy Oil)(Heavy Oil)

Santos Basin

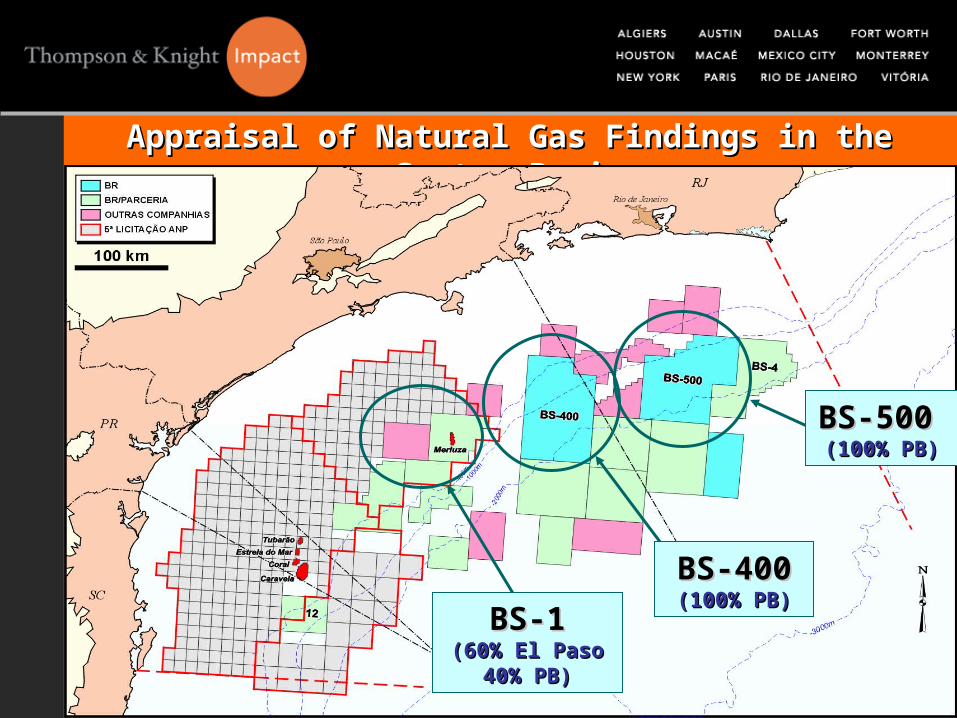

Appraisal of Natural Gas Findings in the Santos BasinAppraisal of Natural Gas Findings in the Santos Basin

BS-500BS-500 (100% PB)(100% PB)

BS-400BS-400(100% PB)(100% PB)

BS-1BS-1(60% El Paso(60% El Paso

40% PB)40% PB)

Overview of the Brazilian MarketOverview of the Brazilian Market Petrobras has been the main investor in the Brazilian natural gas Petrobras has been the main investor in the Brazilian natural gas

industry and will continue to perform high investments in order to industry and will continue to perform high investments in order to expand the supply and to develop the gas domestic market; expand the supply and to develop the gas domestic market;

The new gas discoveries have ensured increasing supply, in The new gas discoveries have ensured increasing supply, in compliance with the market growth – which is high in all compliance with the market growth – which is high in all segmentssegments;;

The participation of gas in the Brazilian energy matrix is based on The participation of gas in the Brazilian energy matrix is based on investments integrated with the capacity of ensuring the investments integrated with the capacity of ensuring the necessary scale to the development of the national gas industry in necessary scale to the development of the national gas industry in Brazil;Brazil;

The projection of expansion of natural gas into the brazilian The projection of expansion of natural gas into the brazilian energy matrix should be based on the expansion of the energy matrix should be based on the expansion of the distributing network and competitiveness;distributing network and competitiveness;

Infrastructure needs:Infrastructure needs: Market interconnection through gas pipelinesMarket interconnection through gas pipelines High costs to meet the demand expansionHigh costs to meet the demand expansion

Northeast Gas Pipeline Network GASENE Gas Pipeline (Southeast - Northeast) Southeast Gas Pipeline Network Urucu - Coari - Manaus Gas Pipeline

Main Gas Projects for Capacity Expansion

Fortaleza

Recife

Maceió

Aracajú

Salvador

Pecém

MossoróGuamaré

Açu

AcariPedra Lavrada

Campina Grande

Riacho das AlmasCaruaru

Pilar

Ipojuca

TermoPE

Carmópolis

Itaporanga

Conde

Catu

Aracati

Termoaçu

TermofortalezaTermoceará (MPX)

TermofafenTermobahia

Termocamaçari

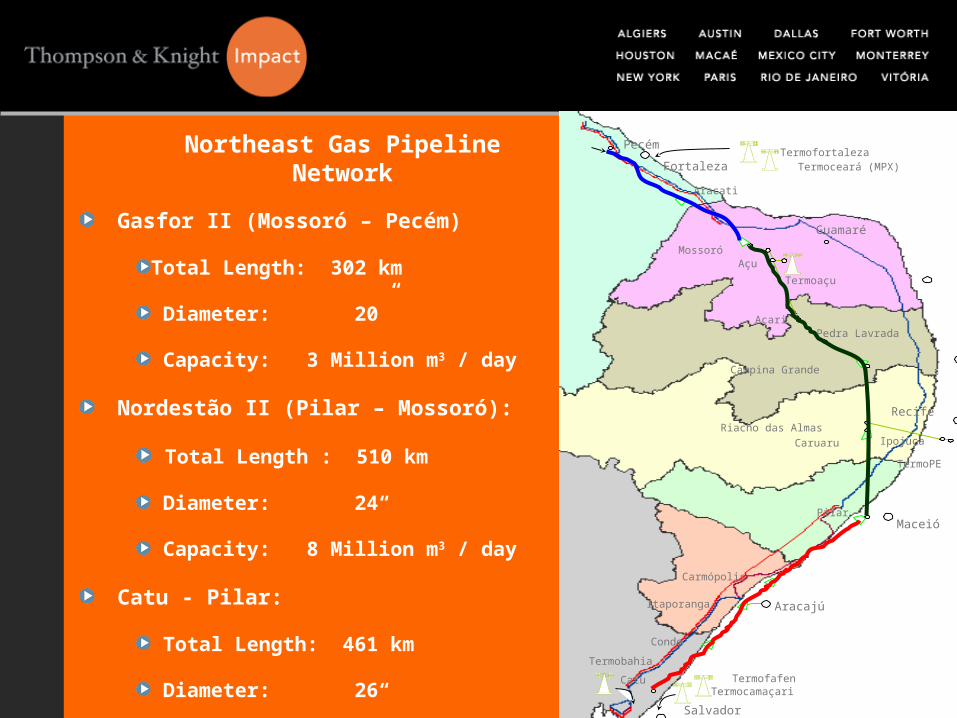

Northeast Gas Pipeline Network

Gasfor II (Mossoró – Pecém)

Total Length: 302 km

Diameter: 20”

Capacity: 3 Million m3 / day

Nordestão II (Pilar – Mossoró):

Total Length : 510 km

Diameter: 24“

Capacity: 8 Million m3 / day

Catu - Pilar:

Total Length: 461 km

Diameter: 26“

Capacity: 8 Million m3 / day

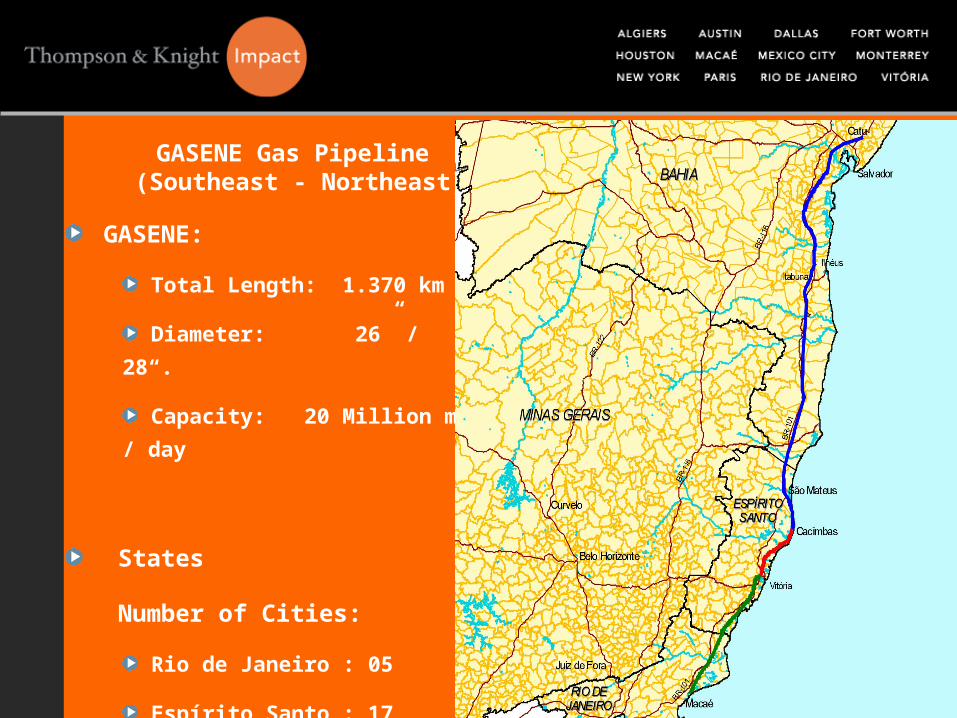

GASENE Gas Pipeline (Southeast - Northeast)

GASENE:

Total Length: 1.370 km

Diameter: 26” / 28“.

Capacity: 20 Million m3 / day

States

Number of Cities:

Rio de Janeiro : 05

Espírito Santo : 17

Bahia : 45

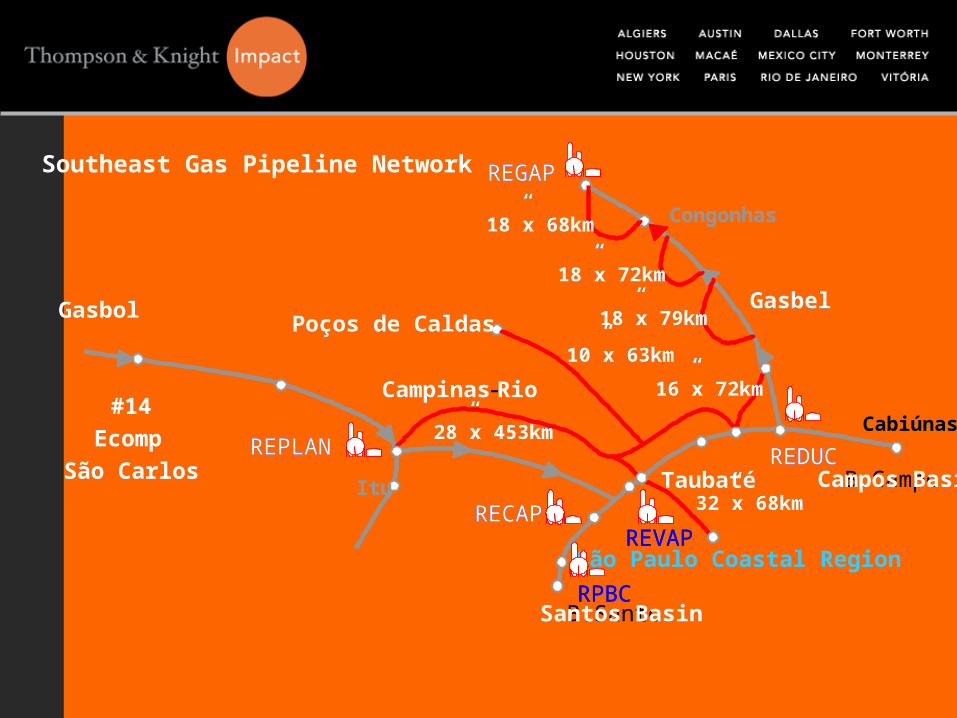

B.Campos

Gasbel

REPLAN REDUC

RPBC

REVAPRECAP

REGAP

#14Ecomp

São Carlos

Campinas -Rio

B.Santos

Congonhas

Itu

Cabiúnas

Poços de CaldasGasbol

10”x 63km

28”x 453km

16”x 72km

32”x 68km

São Paulo Coastal Region

Taubaté

18”x 79km

18”x 72km

18”x 68km

Campos Basin

Gasbel

REPLAN REDUC

RPBC

REVAPRECAP

REGAP

#14Ecomp

São Carlos

Campinas-Rio

Santos Basin

Congonhas

Itu

Cabiúnas

Poços de CaldasGasbol

10”x 63km

28”x 453km

16”x 72km

32”x 68kmTaubaté

18”x 79km

18”x 72km

18”x 68km

Southeast Gas Pipeline Network

Rio Iça

CARAUARI

Rio Negro

R i o

J a p u r á

R

i o

So l i m õ es

Rio Madeira

Rio Tapuá

Rio Ju

ruá

Rio Tefé

Rio Purus

Rio Purus

Rio Coa

ri

URUCU province

COARITEFÉ

MANAUS

RIO BRANCO

RESERVA

BALBINA

SAMUEL

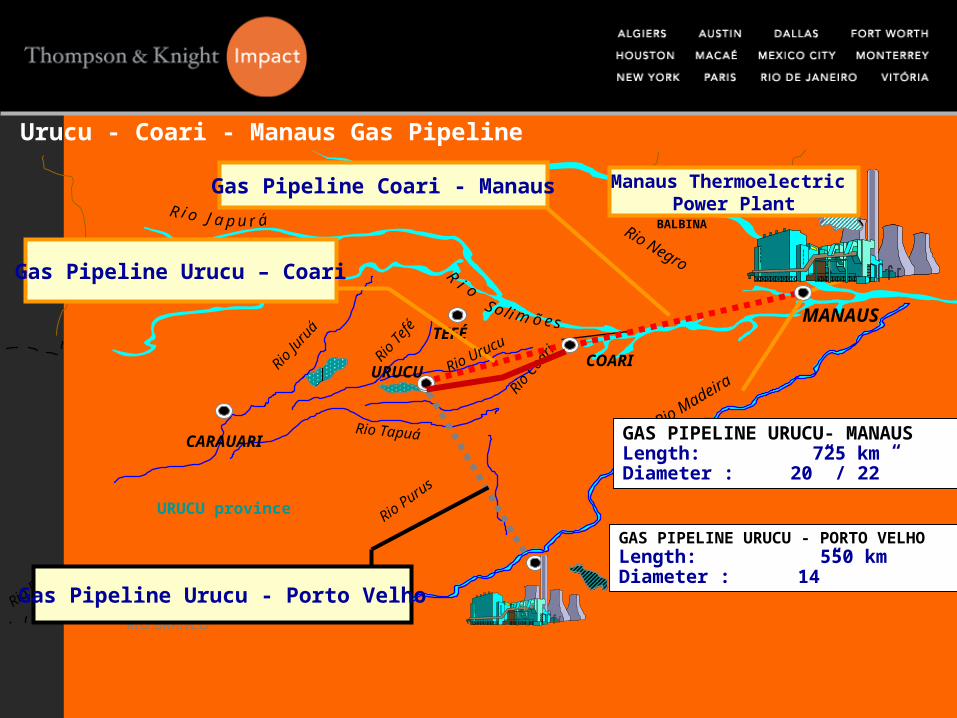

Gas Pipeline Coari - Manaus

Gas Pipeline Urucu - Porto Velho

Gas Pipeline Urucu – Coari

Manaus Thermoelectric Power Plant

URUCU Rio Urucu

GAS PIPELINE URUCU- MANAUSLength: 725 kmDiameter : 20” / 22”

GAS PIPELINE URUCU - PORTO VELHOLength: 550 kmDiameter : 14”

Urucu - Coari - Manaus Gas Pipeline

Brazilian Market ChallengesBrazilian Market Challenges IntegrationIntegration

Increase the interconnection with Latin AmericaIncrease the interconnection with Latin America MarketsMarkets

Expand thermal generation in Brazil (~ 90% domestic market is Expand thermal generation in Brazil (~ 90% domestic market is provided for Hydroelectric system)provided for Hydroelectric system)

Supply GuaranteeSupply Guarantee Ensure natural gas supply (Bolivian gas v new discoveries en Ensure natural gas supply (Bolivian gas v new discoveries en

Santos basin)Santos basin) short / medium / long termshort / medium / long term

Clear RulesClear Rules New Natural Gas Regulation New Natural Gas Regulation Transport Access (open access v. monopoly)Transport Access (open access v. monopoly) Imports/Exports rules (Tax benefit)Imports/Exports rules (Tax benefit) Market prices (Competitive prices )Market prices (Competitive prices )

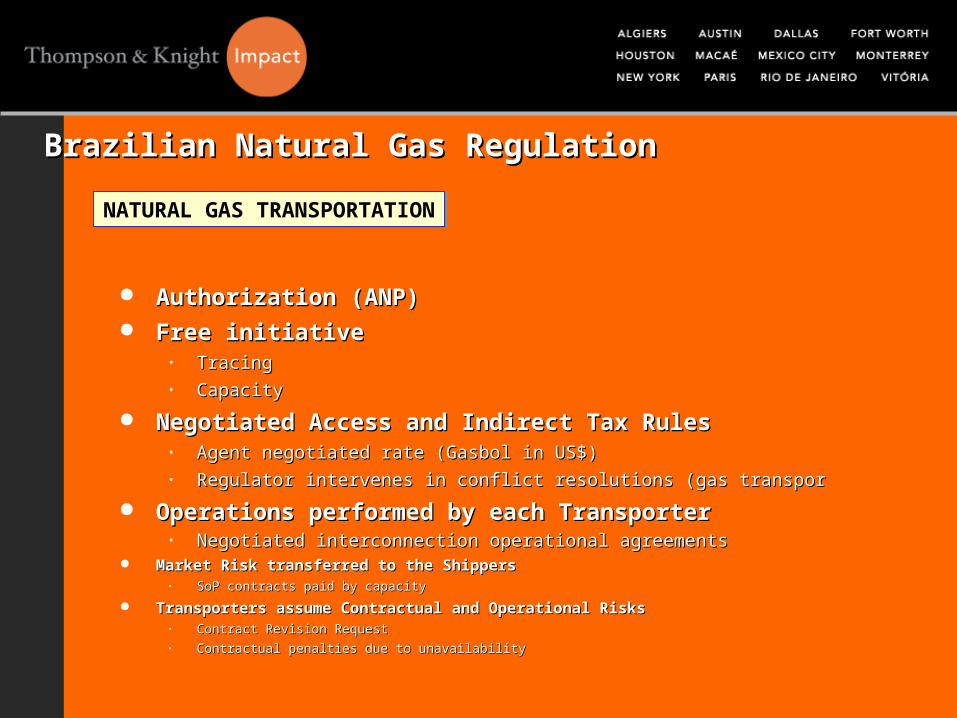

Authorization (ANP)Authorization (ANP) Free initiativeFree initiative

• TracingTracing• CapacityCapacity

Negotiated Access and Indirect Tax RulesNegotiated Access and Indirect Tax Rules• Agent negotiated rate (Gasbol in US$)Agent negotiated rate (Gasbol in US$)• Regulator intervenes in conflict resolutions (gas transporRegulator intervenes in conflict resolutions (gas transpor

Operations performed by each TransporterOperations performed by each Transporter• Negotiated interconnection operational agreementsNegotiated interconnection operational agreements

Market Risk transferred to the ShippersMarket Risk transferred to the Shippers• SoP contracts paid by capacitySoP contracts paid by capacity

Transporters assume Contractual and Operational RisksTransporters assume Contractual and Operational Risks• Contract Revision RequestContract Revision Request• Contractual penalties due to unavailabilityContractual penalties due to unavailability

NATURAL GAS TRANSPORTATION

Brazilian Natural Gas RegulationBrazilian Natural Gas Regulation

PARAGUAi

BRASIL

URUGUAI

BOLÍVIAPERU

CH

IL E

MONTEVIDEO

PORTO ALEGRE

SANTA CRUZ

SANTIAGO

BUENOS AIRES

ARGENTINA

SAO PAULO

RIO DE JANEIRO

URUGUAIANA

BAHIA BLANCA

EL CONDOR

PAYSANDU

MEJILLONESTOCOPILLA

LA MORA

LOMA LA LATA

CUIABA

CONCEPCION

CORNEJO

TUCUMAN

SAN JERONIMO

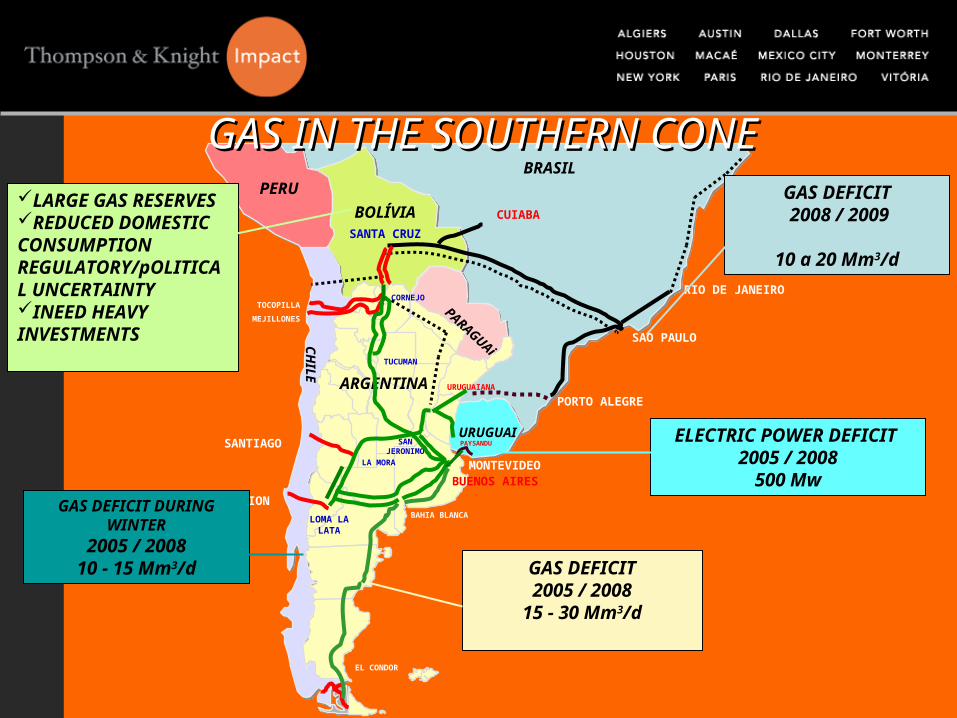

ELECTRIC POWER DEFICIT 2005 / 2008

500 Mw

GAS DEFICIT 2008 / 2009

10 a 20 Mm3/d

GAS DEFICIT DURING WINTER

2005 / 200810 - 15 Mm3/d GAS DEFICIT

2005 / 200815 - 30 Mm3/d

LARGE GAS RESERVESREDUCED DOMESTIC CONSUMPTION REGULATORY/pOLITICAL UNCERTAINTYINEED HEAVY INVESTMENTS

GAS IN THE SOUTHERN CONEGAS IN THE SOUTHERN CONE

PARAGUAi

BRASIL

URUGUAI

BOLÍVIAPERU

CH

IL E

MONTEVIDEO

PORTO ALEGRE

SANTA CRUZ

SANTIAGO

BUENOS AIRES

ARGENTINA

SAO PAULO

RIO DE JANEIRO

URUGUAIANA

BAHIA BLANCA

EL CONDOR

PAYSANDU

MEJILLONESTOCOPILLA

LA MORA

LOMA LA LATA

CUIABA

CONCEPCION

CORNEJO

TUCUMAN

SAN JERONIMO

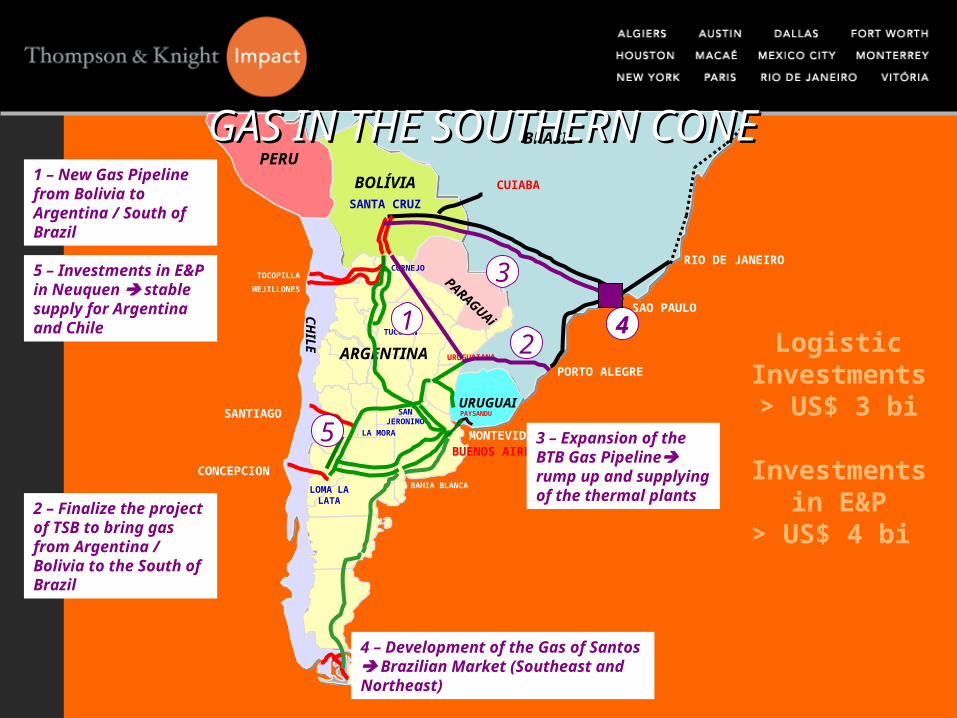

3 – Expansion of the BTB Gas Pipeline rump up and supplying of the thermal plants

3

1 – New Gas Pipeline from Bolivia to Argentina / South of Brazil

1

5 – Investments in E&P in Neuquen stable supply for Argentina and Chile

5

2 – Finalize the project of TSB to bring gas from Argentina / Bolivia to the South of Brazil

2

4 – Development of the Gas of Santos Brazilian Market (Southeast and Northeast)

4 Logistic Investments> US$ 3 bi

Investments in E&P

> US$ 4 bi

GAS IN THE SOUTHERN CONEGAS IN THE SOUTHERN CONE

ARGENTINA

COLOMBIA

ECUADOR

PERU

BRAZIL

PARAGUAY

URUGUAY

VENEZUELA

BOLIVIA Cuiabá

Belo Horizonte

Porto Alegre

Buenos Aires

Santiago

Lima

VitóriaRio de Janeiro

São Paulo

Recife

Salvador

Montevideo

La Paz

Fortaleza

Caracas

Bogotá Manaus

Porto Velho

Urucu

Pisco

Brasília

EUA EuropaMexico/EUA

Chile

NE

Pacific

Atlantic

Regas Terminal

LNG Terminal

Existing Gas pipelineExpected Gas pipeline

Alternatives for Physical IntegrationAlternatives for Physical Integration

GNEA

ConclusionConclusion

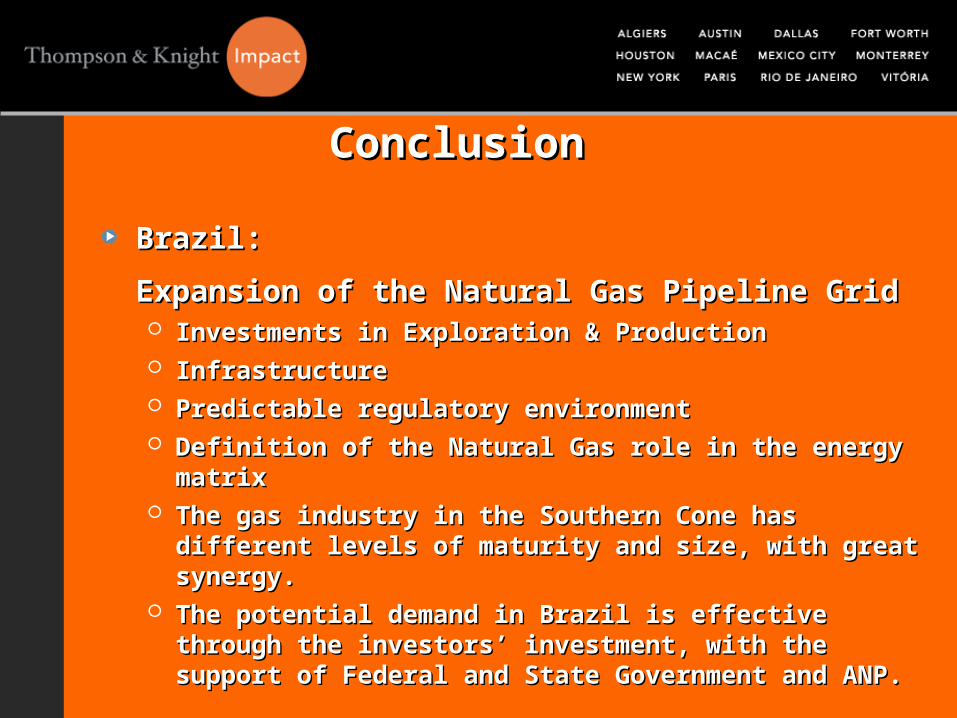

Brazil: Brazil:

Expansion of the Natural Gas Pipeline GridExpansion of the Natural Gas Pipeline Grid Investments in Exploration & ProductionInvestments in Exploration & Production Infrastructure Infrastructure Predictable regulatory environmentPredictable regulatory environment Definition of the Natural Gas role in the energy matrix Definition of the Natural Gas role in the energy matrix The gas industry in the Southern Cone has different levels The gas industry in the Southern Cone has different levels

of maturity and size, with great synergy.of maturity and size, with great synergy. The potential demand in Brazil is effective through the The potential demand in Brazil is effective through the

investors’ investment, with the support of Federal and State investors’ investment, with the support of Federal and State Government and ANP. Government and ANP.

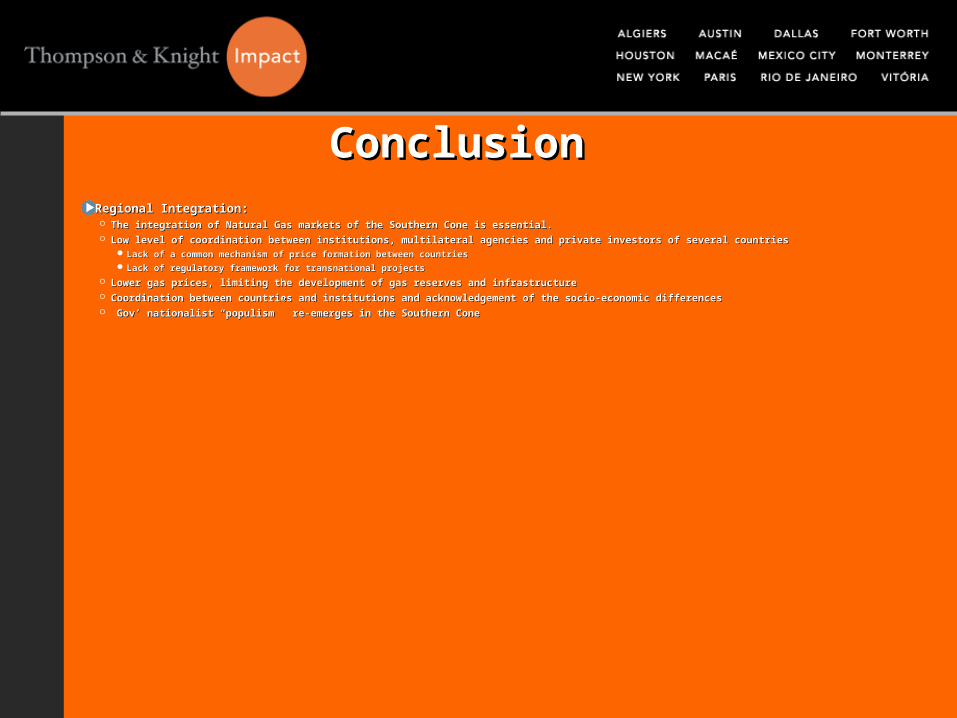

ConclusionConclusionRegional Integration:Regional Integration: The integration of Natural Gas markets of the Southern Cone is essential.The integration of Natural Gas markets of the Southern Cone is essential. Low level of coordination between institutions, multilateral agencies and private investors of several countriesLow level of coordination between institutions, multilateral agencies and private investors of several countries

Lack of a common mechanism of price formation between countriesLack of a common mechanism of price formation between countries Lack of regulatory framework for transnational projectsLack of regulatory framework for transnational projects

Lower gas prices, limiting the development of gas reserves and infrastructureLower gas prices, limiting the development of gas reserves and infrastructure Coordination between countries and institutions and acknowledgement of the socio-economic differencesCoordination between countries and institutions and acknowledgement of the socio-economic differences Gov’ nationalist “populism” re-emerges in the Southern ConeGov’ nationalist “populism” re-emerges in the Southern Cone

Hugo D’AngeloHugo D’AngeloThompson & Knight LLPThompson & Knight LLPTel.: (55-21) 2271-4210Tel.: (55-21) 2271-4210Fax: (55-21) 2271-4211Fax: (55-21) 2271-4211

E-mail: E-mail: [email protected]@tklaw.comwww.tklaw.com www.tklaw.com