Embed Size (px)

Citation preview

1

ENEH, SYLVIA NNENNA

PG/MSc/2010/55146

ACCESSIBILITY OF CREDIT FACILITY

FROM FINANCIAL INSTITUTIONS BY

SMALL AND MEDIUM SCALE

ENTERPRISES: EVIDENCE FROM

NIGERIA

FACULTY OF BUSINESS

ADMINISTRATION

DEPARTMENT OF ACCOUNTANCY

Azuka Ijomah

Digitally Signed by: Content manager’s Name

DN : CN = Webmaster’s name

O= University of Nigeria, Nsukka

OU = Innovation Centre

2

ACCESSIBILITY OF CREDIT FACILITY FROM

FINANCIAL INSTITUTIONS BY SMALL AND MEDIUM

SCALE ENTERPRISES: EVIDENCE FROM NIGERIA

BY

ENEH, SYLVIA NNENNA

PG/MSc/2010/55146

DEPARTMENT OF ACCOUNTANCY

FACULTY OF BUSINESS ADMINISTRATION

UNIVERSITY OF NIGERIA,

ENUGU CAMPUS

3

FEBUARY, 2015

ACCESSIBILITY OF CREDIT FACILITY FROM

FINANCIAL INSTITUTIONS BY SMALL AND MEDIUM

SCALE ENTERPRISES: EVIDENCE FROM NIGERIA

BY

ENEH, SYLVIA NNENNA

PG/MSc/2010/55146

IN PARTIAL FULFILLMENT OF THE REQUIREMENT

FOR THE AWARD OF MASTERS DEGREE IN

DEPARTMENT OF ACCOUNTANCY FACULTY OF

BUSINESS ADMINISTRATION

UNIVERSITY OF NIGERIA, ENUGU CAMPUS

4

SUPERVISOR: PROF. (MRS) UCHE MODUM

FEBRUARY, 2014

DECLARATION

This is to certify that this dissertation by Eneh, Sylvia Nnenna with registration number

PG/Msc/10/55146, submitted to the department of Accountancy, Faculty of Business

Administration, University of Nigeria, Enugu campus (UNEC) is the original and has not

been submitted in full for award of any diploma or degree in this university.

__________________

___________

Eneh, Sylvia Nnenna Date

(Student)

PG/Msc/10/55146

5

APPROVAL PAGE

This is to certify that Eneh, Sylvia Nnenna a post graduate student of the Department of

Accountancy, Faculty of Business Administration, University of Nigeria , Enugu

Campus(UNEC),with registration number PG/Msc/10/55146, has satisfactorily completed

the requirement for the award of the Msc. Degree in Accountancy of Nigeria.

_______________________

_____________

PROF. (MRS) UCHE MODUM

DATE

SUPERVISOR

6

_______________________

______________

DR, (MRS) G.N.OFOEGBU

DATE

HEAD OF DEPARTMENT

DEDICATION

To God the Father, the Son and the Holy Ghost are all honour and

glory.

7

ACKNOWLEDGEMENT

My warm and heartfelt appreciation goes to my supervisor Prof.(Mrs) Uche Modum for

her patience, attention, care and love she showed in the course of this work. In fact, mum

8

you are a rare gem to be found in this present age where almost all persons want to be in

the fast lane, but you gradually drew me to your side where I learnt to do things the right

way and naturally stand out to defend such thing anywhere. The best qualification for you

is nothing but “A REAL MOTHER”. Thanks a million times for making me outstanding

right from the class works, seminar presentations unto this stage. My prayer is that God

will strengthen you with good health and may his mercies abound for you in all things,

I am also grateful to my able, Head of Department and professional colleague Dr. (Mrs)

G.N. Ofoegbu for her encouragement and support. She will always ask how far I was

moving on with this work. Thank you so much ma and May God bless you. Special

appreciation goes to Dr R.O. Ugwoke. I was brave to face this program after a one on one

discussion with you. May God bless you. Prof. (Mrs.) R.G Okafor, Dr.(Mrs.) E.O.Onyeanu

are higly appreciated. All of you are blessed all round. All the elites, senior lecturers and

staff in the Department of Accountancy of this great university, your names are written in

gold and I love you all.

My warm regards goes to my friend for her wonderful encouragement: Dr. (Mrs) Ima

Nnam-(the youngest Doctor and my professional colleague), you made me to understand

that my supervisor is the best thing that has ever happened in my academics when I was

grumbling. Thank you dearly. Others worthy of mention are Mrs. Ngozi Nwekwo who is

my class mate and mentor. I appreciate your care and love. Let God strengthen you in all

your own endeavours. Dr. ( Mrs.) Grace Okafor of the Accountancy Department, NAU

Awka must be remembered at least for your advice and encouragements. Thanks dear.

This list will not be exhaustive if the names of my colleagues at Radio Nigeria Enugu

National Station are not mentioned, because of their immense help and care. They are :

Mrs. Chika Okafor, Mrs. Amaka Onaga, Peace Ijomanta, Mr Chris Okorie, Mrs. Helen

Ochin, Mrs. Vero Nwigwe, Justina Ude. A big thank you to all of you and May the good

Lord bless you all. I will not fail to remember Mr. Ekechukwu Sonie, Mr.Ken Eneh,

Mr.Frank Okoli, Mr.Chris Ukegbu and my Bosses Mr. Oscar Okoroafor and Mr.Alfred

Onyekwere.Thanks to all of you and may God bless you abundantly for your diverse

goodness towards me. My friends are part of this laudable achievement. They are: Mrs Joy

Eze , Nkem Anyaogu, Mrs Adaora Owoh, Mrs Vera Nwankwo and Dr Jekwu Nwabueze.

Thanks for all your encouragements.

A special and warm feeling goes to my sweetheart and ever abiding Darling Mr. Chinedu

Eneh who has been a pivot of my innumerable successes in life. As per this work when I

complain about the slow pace with which it was going, he would take side with Prof. and

tell me that I am lucky to have her as a supervisor. He will usually say that if it were in the

medical field that it will not be easy for me to see her one on one. Naturally, I will feel so

bad that he is supporting someone he had never seen in life but I will eventually reason

alongside his own thought and things started moving quite easier. Thank you so much

dear. My children: Joy. Godleads, Nmesomachukwu and Peace are all wonderful. All your

angelic assistance is highly appreciated. My mum is also appreciated for you are always

there to assist me at all times. For sure mum, I can count on your prayers. Thank you so

9

much and may the good Lord keep you in abundance of his grace. Finally, I thank my

siblings – Mrs Rose Egeson and Engr. Justin for all your care, support, kindness and love.

Eneh,Sylvia Eneh

PG\MSc\10\55146

10

Abstract

This study tries to look at the accessibility of credit facility from financial institutions by

small and Medium Scale Enterprises: Evidence from Nigeria. Small and Medium Scale

Enterprises have been faced with poor funding when developing nations like ours are

considered. This however distorts the outstanding function of SMEs as the engine and

pivot for the economic growth and national development. No wonder Nigeria has

continued to experience high level of emergence of new enterprises that would only exist

for two to three years and fizzle out. This study has a broad objective of determining the

degree of accessibility of credit facility by SMEs from the financial institution in Nigeria

with such variables like government policies, collaterals, tax incentives etc. The study

adopted the analytical survey method to gather information on the variables. The

population was made up of all the financial controllers in the 360 manufacturing

enterprises in the three states under study. We in turn used judgmental sampling technique

to select the financial controllers in these manufacturing enterprises. Data were collected

by means of questionnaires with response option graduated into a five- likert scale

designed to capture information on the variables that affect SMEs. The linear regression

analysis was used to test hypotheses one, three and four. One sampled t-test was used to

test hypothesis two while a multiple regression analysis was used to test the multiple

effects of three independent variables on credit accessibility. The result obtained using the

test statistics shows a positive relationship between government policies, access to credit

as the greatest problems facing SMEs, tax incentives, availability of collaterals as regards

the accessibility of credit facility by SMEs. The research questions proved that

international financial assistance abounds for SMEs. The study also showed that the level

of the operation of SMEs has not improved when compared with other developed nations.

SMEs in Nigeria are faced with numerous challenges and such has affected their

performances. We therefore recommend that attention and support be given to the sub-

sector so as to enhance their performance as the engine of growth and catalyst for socio-

economic transformation in Nigeria. The study has provided opportunities for further

research into other factors that could affect SMEs credit accessibility, in order to ascertain

if such factors actually affect them in equal measures or not.

11

TABLE OF CONTENTS

Title page i

Declaration ii

Approval page iii

Dedication iv

Acknowledgement v

Abstract vi

Table of content vii

List of tables x

List of figures xi

CHAPTER ONE: INTRODUCTION

1.1 Background to the study 1

1.2 Statement of the Problem 3

1.3 Object of the study 5

1.4 Research questions 5

12

1.5 Hypothesis of the study 5

1.6 Scope of the study 6

1.7 Significance of the study 6

1.8 Limitations of the study 6

1.9 Explanation of Acronyms 7

Reference 8

CHAPTER TWO: REVIEW OF RELATED LITERATURES

2.10 Conceptual review 9

2.1.1 Relevance of SMEs in Economic Development 11

2.1.2 Sources of finance for SMEs 13

2.1.3 Venture capital Financing/Business Agents 13

2.1.4 Pension reform Act & SME financing 14

2.1.5 SME Financing issues and the bank 15

2.1.6 The role of Banks in SME development 16

2.1.7 The existence of SME Financing gap 17

2.1.8 Concept and causes of Financing gap 17

2.1.9 Imperatives of Good Banking habits for

13

Successful SMEs operations 18

2.1.9.1 Appraisal of some sources of financing

SME’s in Nigeria 21

2.1.9.2 Current financing initiations and the way

Forward 27

2.1.9.3 Some countries expenses in SME development 30

2.1.9.4 Problems of SME in the development process 32

2.1.9.5 Ten commandment of small Business Finance 33

2.1.9.6 Closing the financing gaps for SMEs in Nigeria 34

2.1.9.7 Prospects of SMEs in Nigeria 35

2.1.9.8 SMEs and the living standard of people 37

2.2 Theoretical Review 38

2.2.1 Agency Theory 38

2.2.2 Signaling Theory 39

2.2.3 The Pecking order frame work/Theory 39

2.2.4 Access to capital theory 40

2.2.5 Equity Theory 40

2.2.6 Entity Theory 40

14

2.3 Empirical review of Related literature 41

2.3.1 The impart of Access to finance on SMEs 43

2.3.2 Constraints to SMEs financing 47

2.3.3 Government and CBN Policy options 48

2.3.4 SMEs and Tax Incentives 49

2.4 Summary 50

References 51

CHAPTER THREE: METHODOLOGY

3.1 Research design 62

3.2 Population of the study 62

3.3 Sampling/sample size 62

3.4 Data Collection instrument 63

3.5 Techniques of data Analysis 63

3.7 Nature and sources of Data 64

3.8 Validity, of the Instrument 64

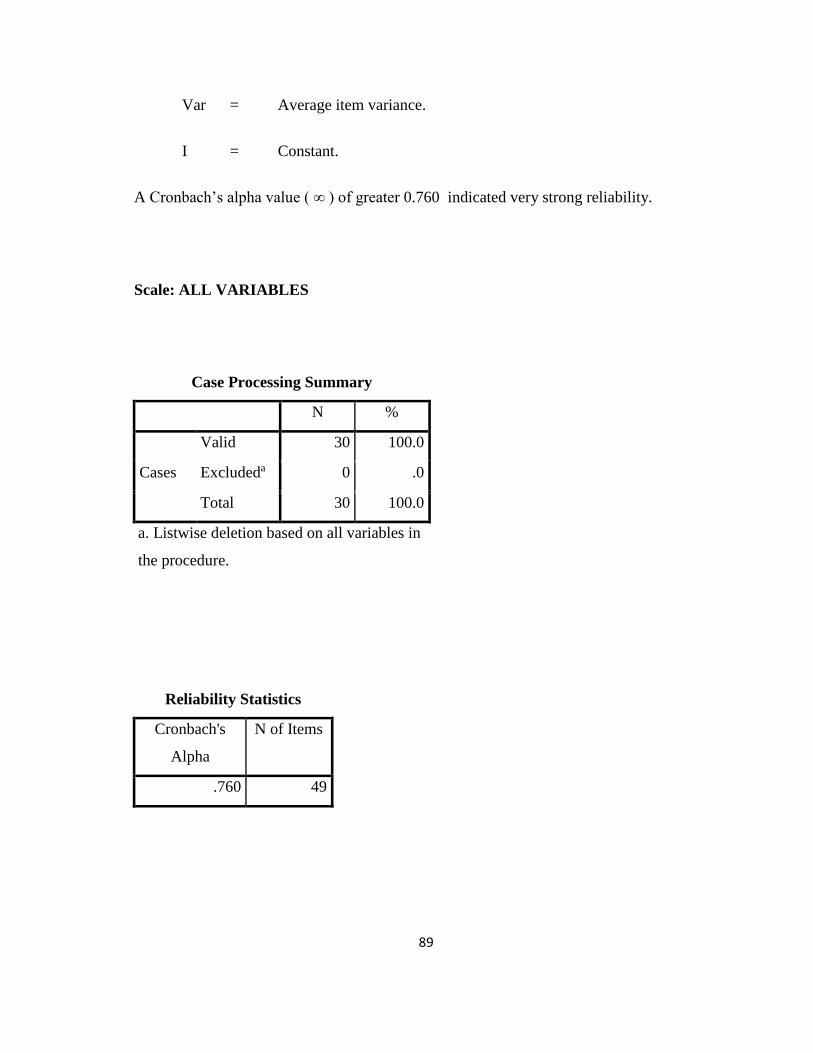

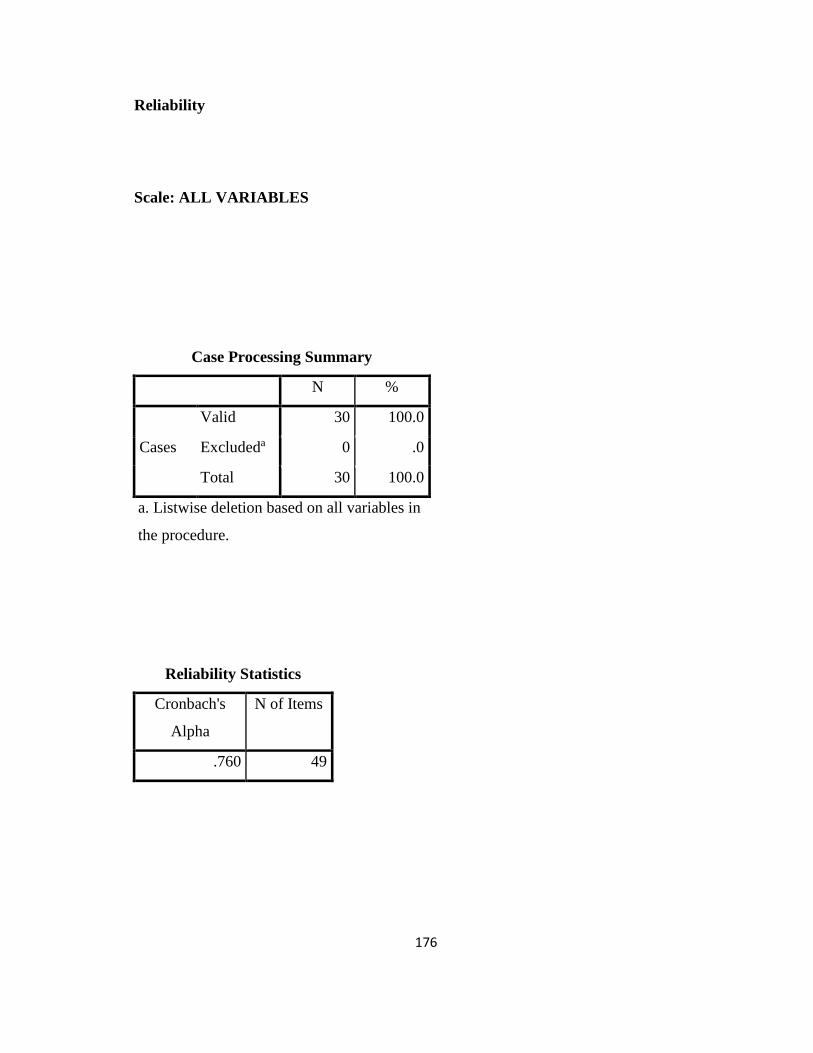

3.9 Reliability of the instrument 64

15

3.9.1 Description of Research Variables 65

3.9.2 Anticipated Problems/Limitations of the study 67

References 68

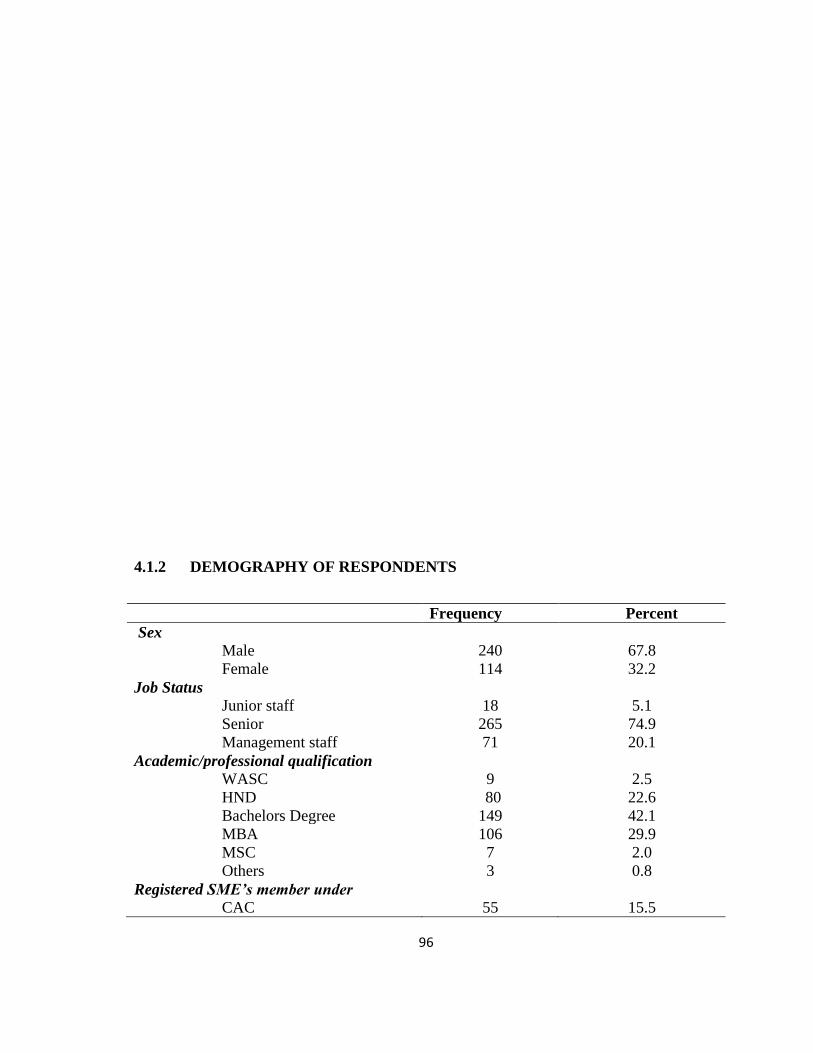

CHAPTER FOUR: DATA PRESENTATION AND ANALYSIS

4.1 Introduction 69

4.2 Hypotheses Testing 84

4.2.1 Hypothesis 1 84

4.2.2 Hypothesis 2 86

4.2.3 Hypothesis 3 77

4.2.4 Hypothesis 4 88

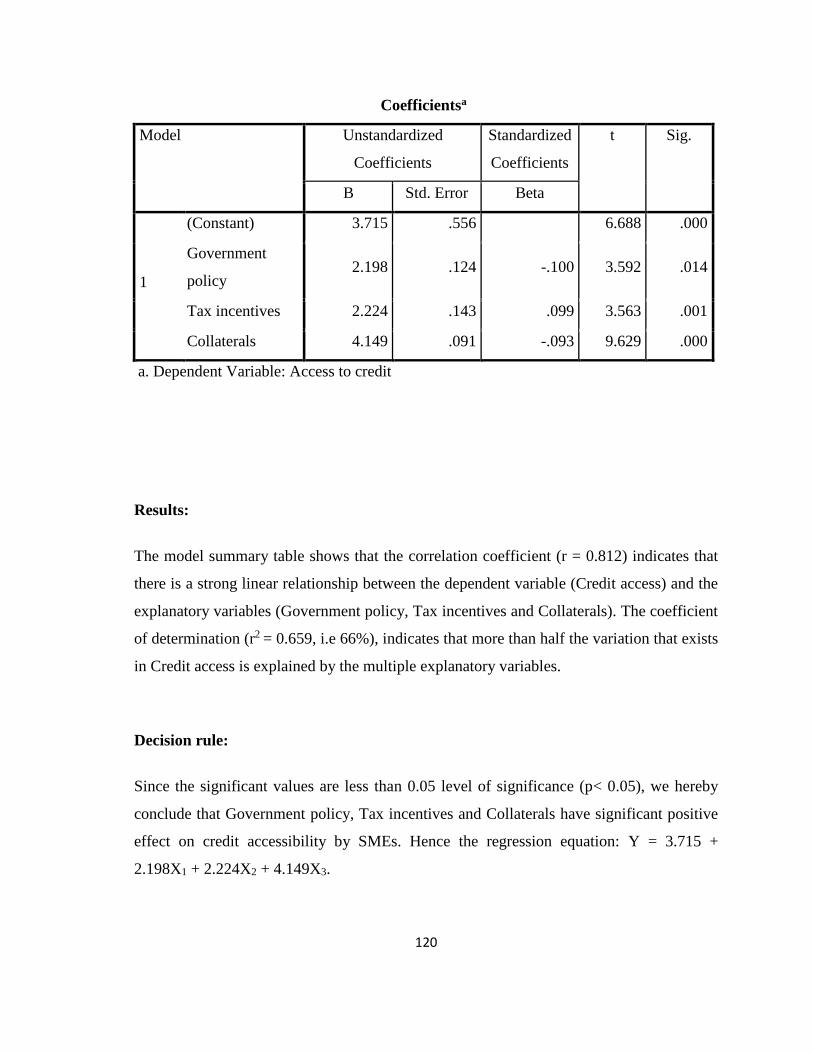

4.2.5 Multiple Regression Analysis result of effect of Government

policy, Tax incentives and Collaterals on Accessibility of credit

facilities by SMEs 90

CHAPTER FIVE: DISCUSSION OF FINDINGS, RECOMMENDATIONS AND

SUMMARY

5.0 Introduction 92

5.1.1 Discussions on findings of hypothesis 1 92

16

5.1.2 Discussions on findings of hypothesis 2 93

5.1.3 Discussions on findings of hypothesis 3 94

5.1.4 Discussions on findings of hypothesis 4 86

5.2 Conclusion 95

5.3 Recommendation 96

5.4 Contribution to knowledge 97

5.5 Further studies 97

Bibliography

Appendix

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

A business whether small or big, simple or complex, private or public is created to either

provide competitive prices make profit, provide social services or add value (Ayozie

,1999). Business in Nigeria has been classified as small, medium and large. However,

(SMEs) Small and Medium Enterprises does not have a one way definition rather, its

definition is best understood from its characteristic features; level of project costs,

turnover, number of employees, ownership composition and capital outlay

(Akinsurile,2006).

The Federal and State Ministries of Industry and Commerce have adopted the criteria of

value of fixed capital to determine what Small and medium scale enterprises (SMEs)

definition would be. The National Council of Industries defined SMEs as those businesses

whose capital base excluding land is not more than N2m only and employee ranges from

17

10 to 300 persons (Akimade,1991). However, this value rose from N60, 000 in 1972,

N159, 000 in 1975, N250, 000 in 1986 before rising to N2m in 1991. On the other hand,

small and Medium Scale Industries development Act 2003 specified that SME employee

rages from 10-199, Assets excluding land and building fall between (5 and 499) million

Naira only.

Small and Medium Scale Enterprises in Nigeria constitutes a greater percentage (75%) of

all the registered companies in Nigeria. They have been in existence for quite a long time

as majority of SMEs’ grew from Cottage Industries. The operations of SMEs’ are found in

all the areas of human endeavours: Manufacturing, Production, information, Services,

Agriculture, Hotel and Restaurants, Financial Intermediation, Real Estate, Education,

Building and Constructions, Mining and Quarrying.

For SMEs’ to operate in these sub-sectors of the economy, they are not left without

controls. Federal government through the apex bank (CBN) monitors the activities of

SMEs to ensure that they work in line with the set standards in other countries. The

government set several agencies like small and medium scale industries equity investment

schemes (SMIEIS),small and medium enterprise development agency(SMEDAN),Nigerian

agricultural cooperative and rural development bank,(NACRDB),Bank of industry(BOI),

Nigerian bank for commerce and industry(NBCI),Nigerian industrial development

bank(NIDB). They are set to moderate, monitor, finance and control SMEs’ to ensure that

they are resurrected to be the major driver of our economic development and growth

(Onugu, 2005).

On the other hand, the Federal government liaises with international agencies and

organizations World Bank, International Finance Corporation (IFC), United Kingdom

Department for International Development (DFID), United Nations Industrial

Development Organizations (UNIDO), and Europeans Investment bank (EIB) .The essence

is not only to invest heavily on SMEs but to make them work vibrantly.

Wide attention and support given SMEs is not far-fetched from the obvious reasons that

they are job and wealth creators. Small and Medium Enterprises (SMEs’) occupy a very

18

vital position in the economy’s various sub-sectors and thus have several significant roles.

SMEs’ have been referred to as the “Engine of Growth” and “Catalysts for Socio-

Economic Transformation of the country. SMEs’ represents a veritable vehicle for the

achievement of National Economic objectives: Employment generation, value added, rural

development acceleration, stimulation of entrepreneurship, vital links between agriculture

and industries, supply parts and components to large scale industries (LSI), contribute to

domestic capital formation (Anyanwu,2001).

(Salam,2012), the Deputy Director Development, Finance Department of CBN in his

workshop paper “Stakeholders responsibility in SMIEIS” opined that despite the

incentives, policies, programmes and support aimed at revamping SMEs’, they have

performed rather below expectations in Nigeria. Different opinion abounds as to why

SMEs have not been able to perform; Some said it was lack of access to credit facilities,

others think otherwise arguing that inappropriate management skills, difficulty in accessing

global market, lack of entrepreneurial skills, poor infrastructures, insecurity challenges etc

are largely responsible.

However, one observes that the bane of SMEs’ in Nigeria is lack of long term finances

bearing in mind that most Nigerian Financial Market have much of short term funds which

may not allow SME to grow and become really successful.

Onugu,(2005) opined that there are challenges and problems which frustrate SMEs’ in

Nigeria. These problems either make them to die within their first two years of existence or

perform below standard even after surviving in their early years. Some of the key ones are

inadequate infrastructural facilities (road, water, electricity) insecurity of lives and

property, inconsistent regulations, fiscal and industrial policies, limited access to market,

multiple taxes and levies, data inadequacies, fragile capital base, and harsh operating

environments. The problems and challenges of SMEs’ in Nigeria are also induced by the

operating environment (Government Policies, Globalization effects, financial institutions,

19

attitude to work, other challenges are driven by inherent characteristics of SMEs’

themselves.

In spite of the above challenges, government can still provide good infrastructure, enabling

environment, legal framework and other incentives that would aid SMEs’ to operate more

efficiently in Nigeria just like other developed countries. This will help SMEs’ to be in the

fore-front of economic growth and development in Nigeria.

1.2 Statement of Problem

SMEs in Nigeria can never be severed from the challenges and key variables that

characterize the nation as a developing one. We know that the nation has been faced with

several challenges like economic and political instability, corruption, insecurity, high rate

of poverty, poor infrastructures. SME by extension as a sub-sector of the economy must

definitely get a fair share of these problems. In addition, to the general challenges (Cole,

2008; Udell,2003;Blum&Laurie,1995; Burch & Claudia,2004; Birly,1996; Bates,2007)

who studied the problems and challenges facing SMEs, found out that one of the greatest

problem facing SMEs was access to credits. Also, (Watson& Kunt, 2002; Vos,Yeh,Carter

& Tagg, 2007; Beck & Kunt,2008; Chittenden & Hall, 1996) in their studies examined the

extent to which limited access to finance has affected the performance and growth of

SMEs. They observed that funding pose serious impediment to growth of SMEs. In the

same vein, (Abereyo & Fayomi,2005; Dagogo & Ollor,2012; Gbandi & Amissah,2012;

Anyawu,2010) have studied the appraisal of some sources of finances available for SMEs,

and observed that most sources of finance attracts huge costs of capital with the exception

of retained earnings that are cost free though may be too meager for the effective growth of

SMEs.

Furthermore, financial institutions are demanding unattainable conditions and terms (high

interest rate) for the granting of loan. They are claiming that SMEs are not presenting

bankable project (good project proposal), inadequate collaterals, lack of trained

personnel’s, lack good accounting system that would give rise to audited annual accounts,

20

coupled with high enterprise mortality. Thus, it would appear that greatest problem facing

SMEs could be lack of accessibility of credit facilities.

Still worrisome is the position of Federal Government in the implementation of SMEs

policies. How far the apex bank has gone in the enforcement and control of the laws that

guide SMEs even after the emphasis on budgetary allocation? How have she ensured that

the 10% profit before tax set aside by the commercial banks is made available to SMEs? It

would appear that the commercial banks even prefer to pay a penalty of 20% to CBN

instead of choosing the option of granting loans to SMEs.

But, despite the general vigorous marketing of these facilities by the financial institutions, SMEs

have little or no access to them. The big question then is “why is it that SMEs are not able to access

these credit facilities from the financial institutions’’?

1.3 Objectives of the Study

The main objective of this study is to determine the degree of accessibility of credit

facilities from financial institution by Small and Medium Scale Enterprises: Evidence from

Nigeria.

While the specific objectives of the study are as follows- To:

i. examine the extent to which government policies favour SMEs in Nigeria.

ii. ascertain whether access to credit facilities represents the greatest problem

facing SMEs.

iii. determine whether tax incentives affect the accessibility of credit facilities

by SMEs.

iv. determine whether having collaterals have effect on the accessibility of

credit facilities by SMEs.

v. ascertain the extent to which SMEs are funded by international agencies: -

World Bank, IFC.

1.4 Research Questions

In the course of this research study the following research questions were raised:-

(i) How far has government policies favoured SMEs in Nigeria?

21

(ii) To what extent is access to credit facilities the greatest problem facing

SMEs?

(iii) Has tax incentives affect the accessibility of credit facilities by SMEs?

(iv) To what extent does having collaterals affected credit facilities accessible

by SMEs?

(v) What is the extent to which SMEs are funded by international agencies?

1.5 Hypotheses of the Study

After a critical evaluation of the objectives the following hypotheses were developed.

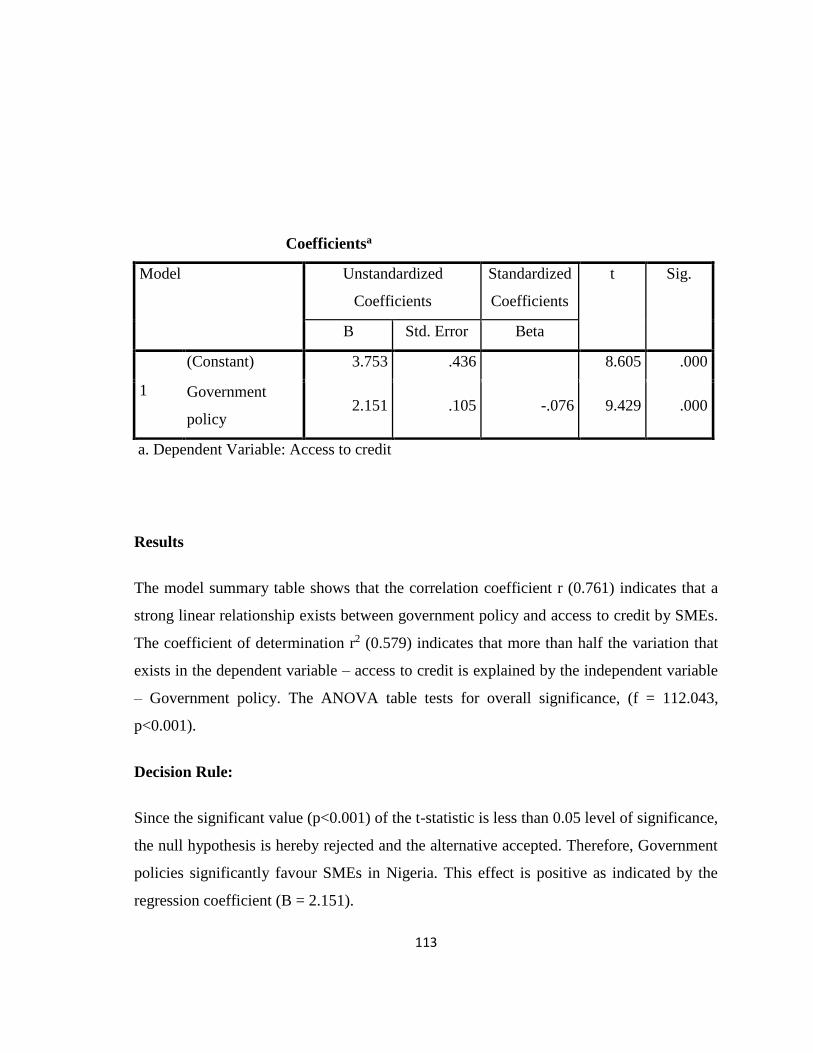

i. Government policies do not significantly favour SMEs in Nigeria.

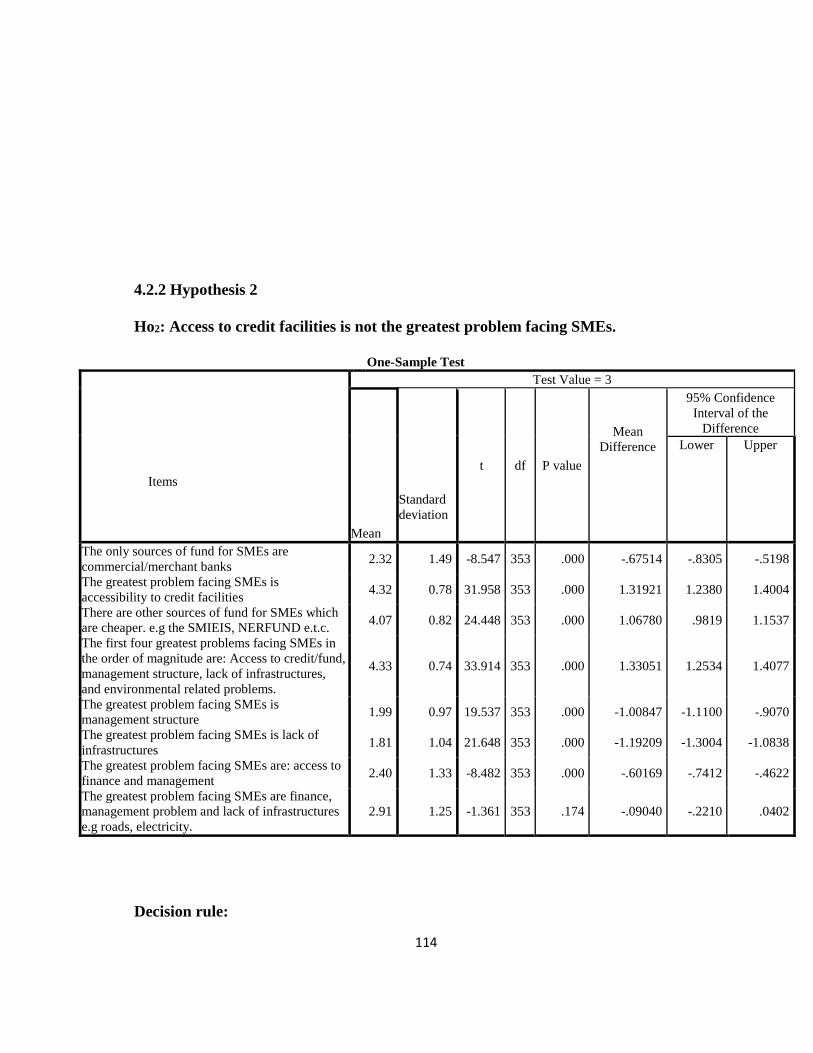

ii. Access to credit facilities is not the greatest problem facing SMEs.

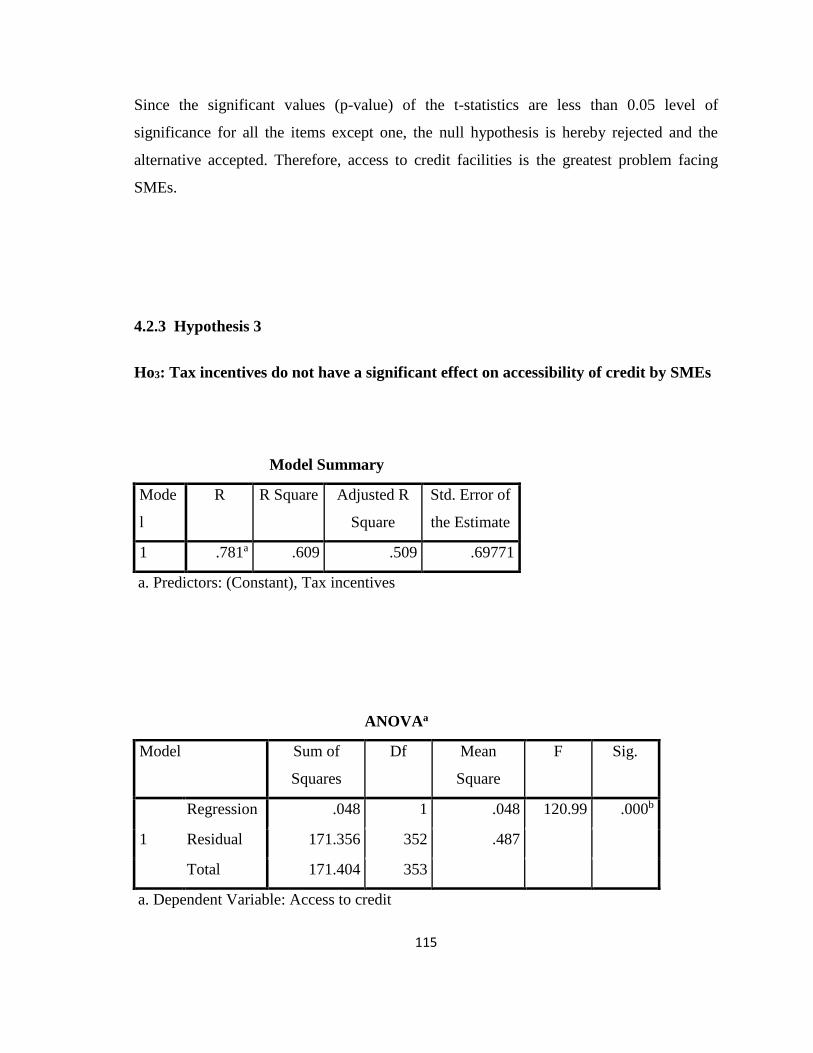

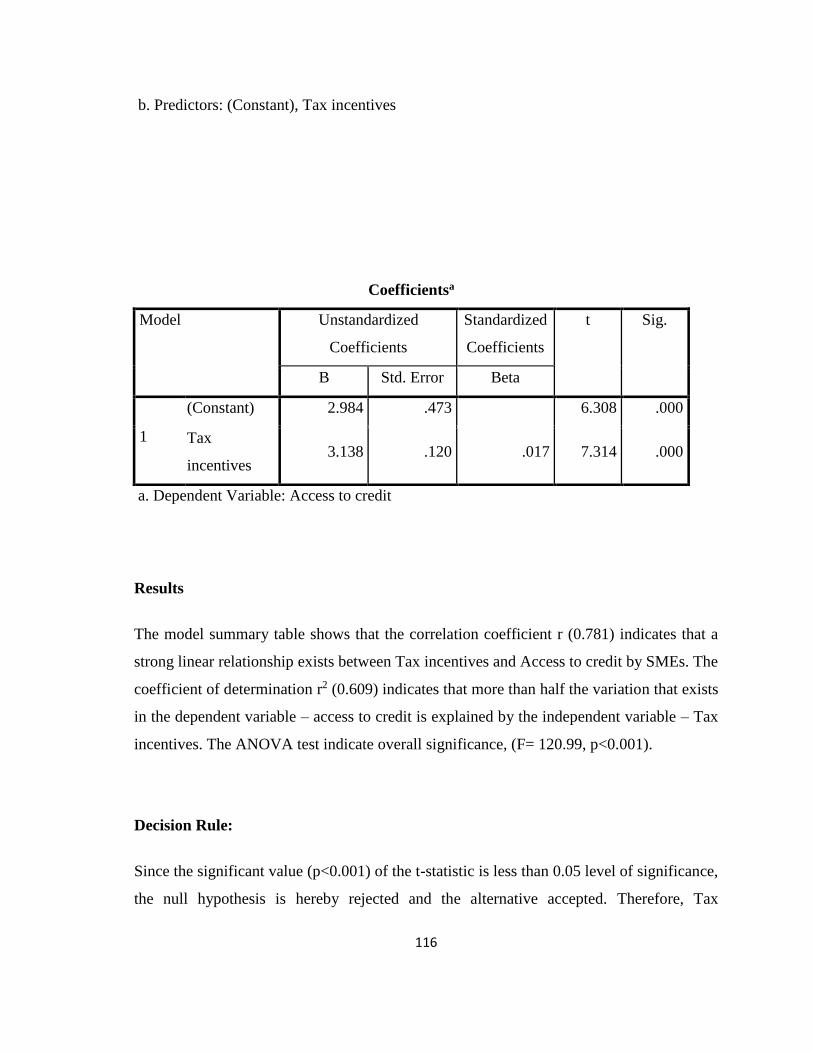

iii. Tax incentives do not have a significant effect on accessibility of credit by

SMEs.

iv. Having collaterals does not significantly affect accessibility of credit by

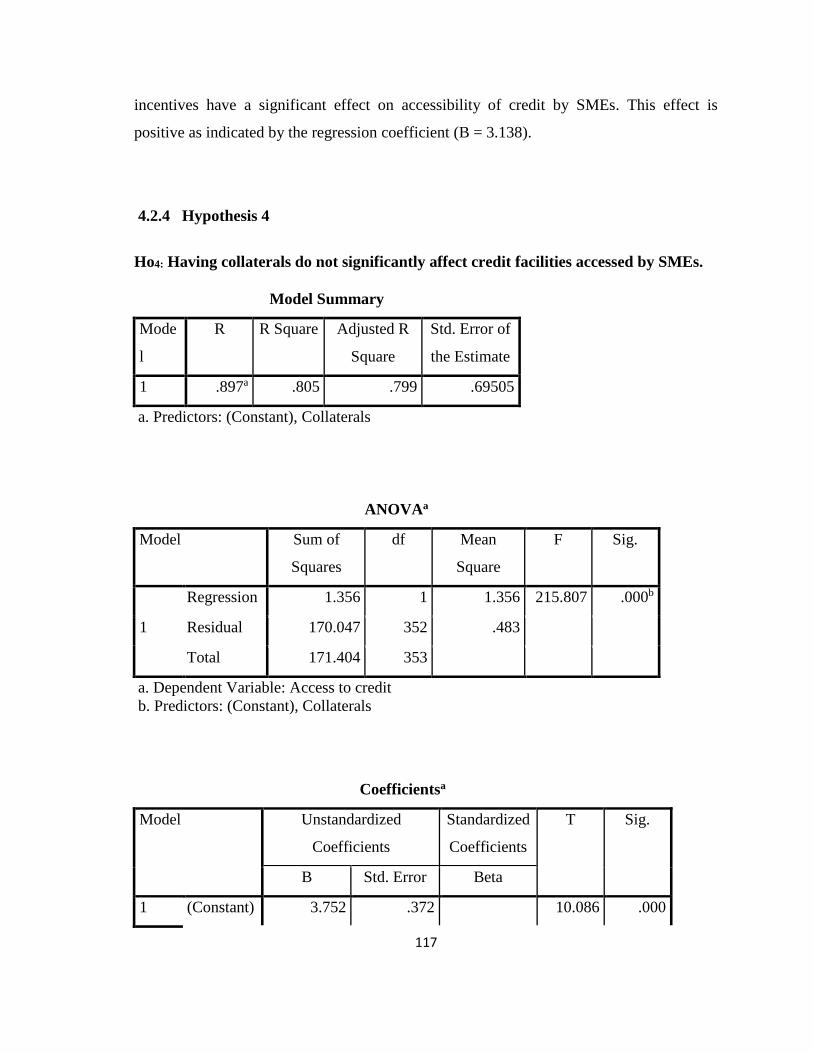

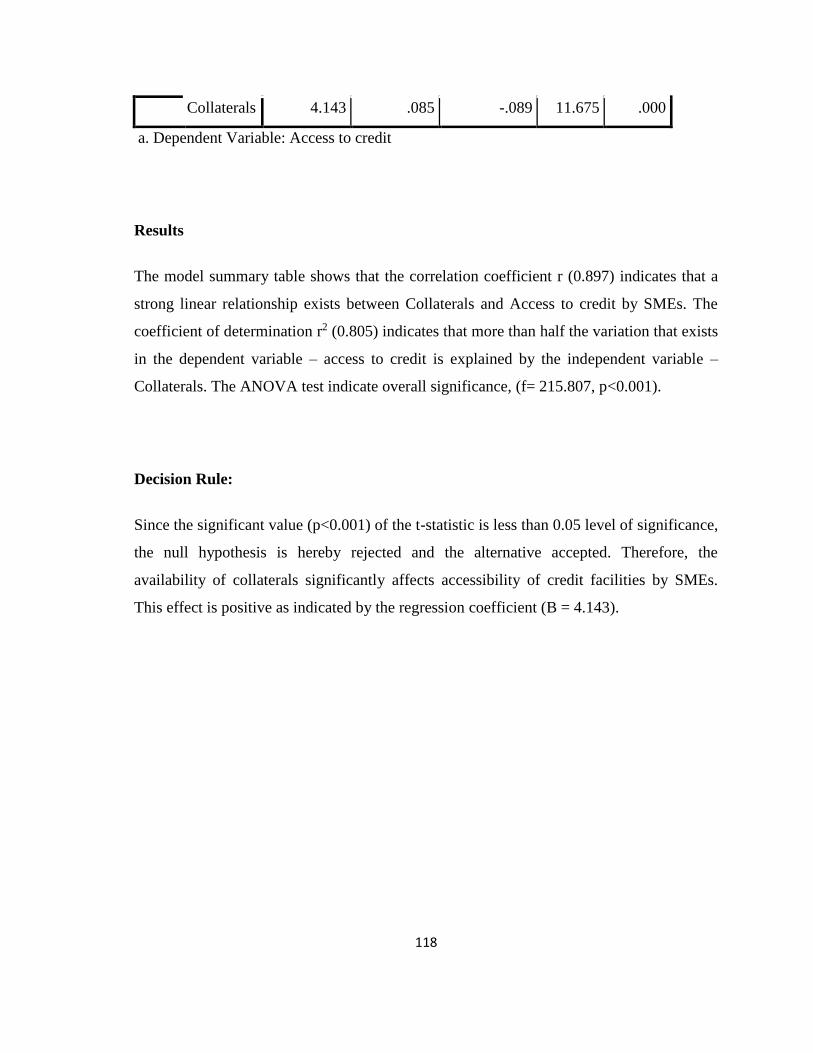

SMEs.

1.6 Scope of the Study

The researcher used all the registered enterprises under the umbrella of Small and medium

Enterprises Development Agency (SMEDAN). However, for a realistic study to be made,

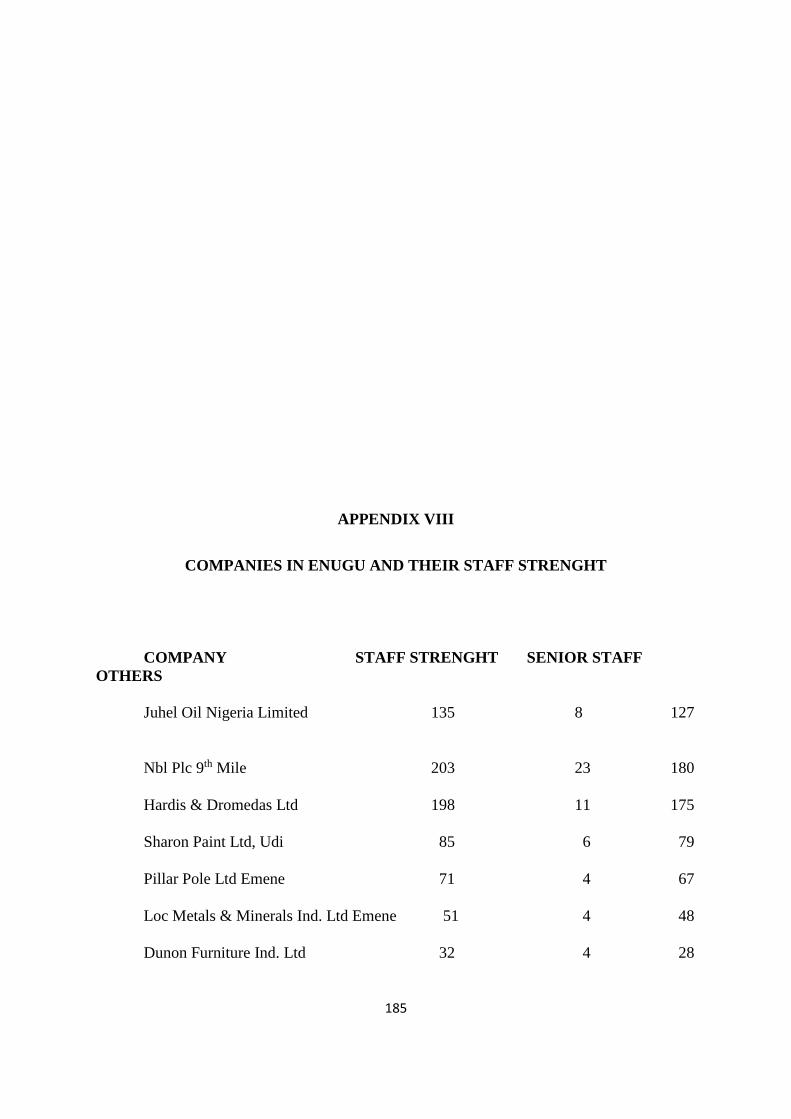

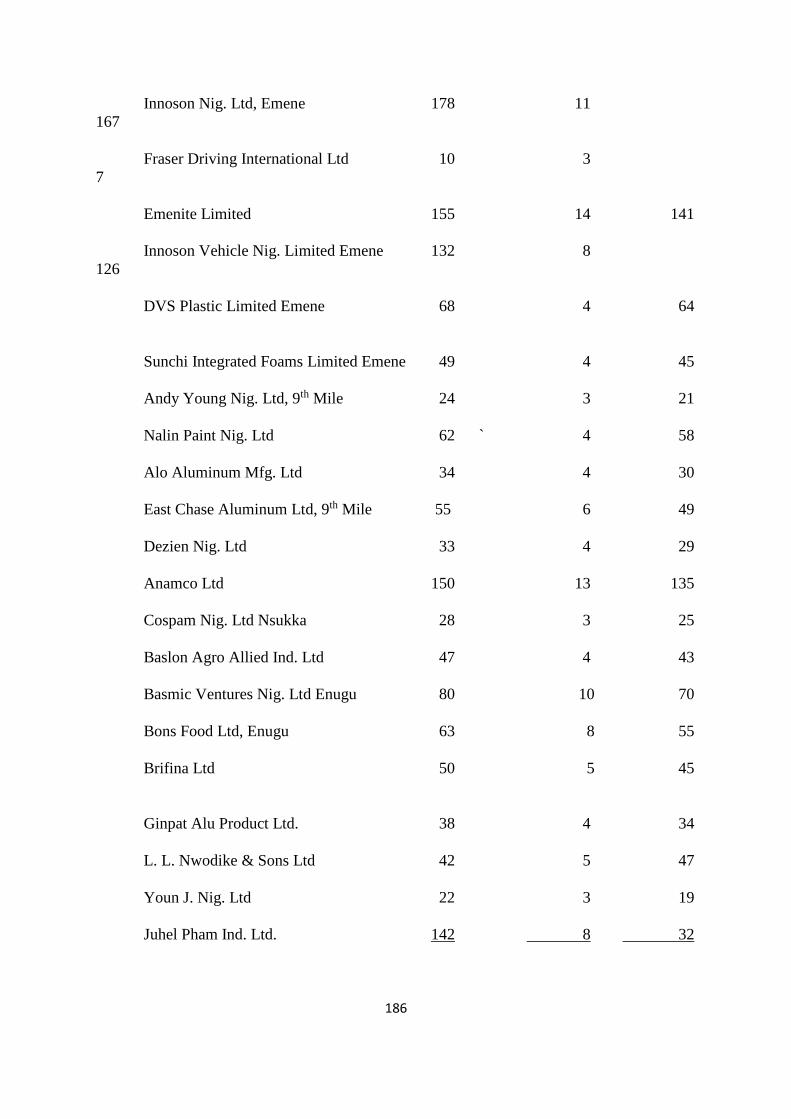

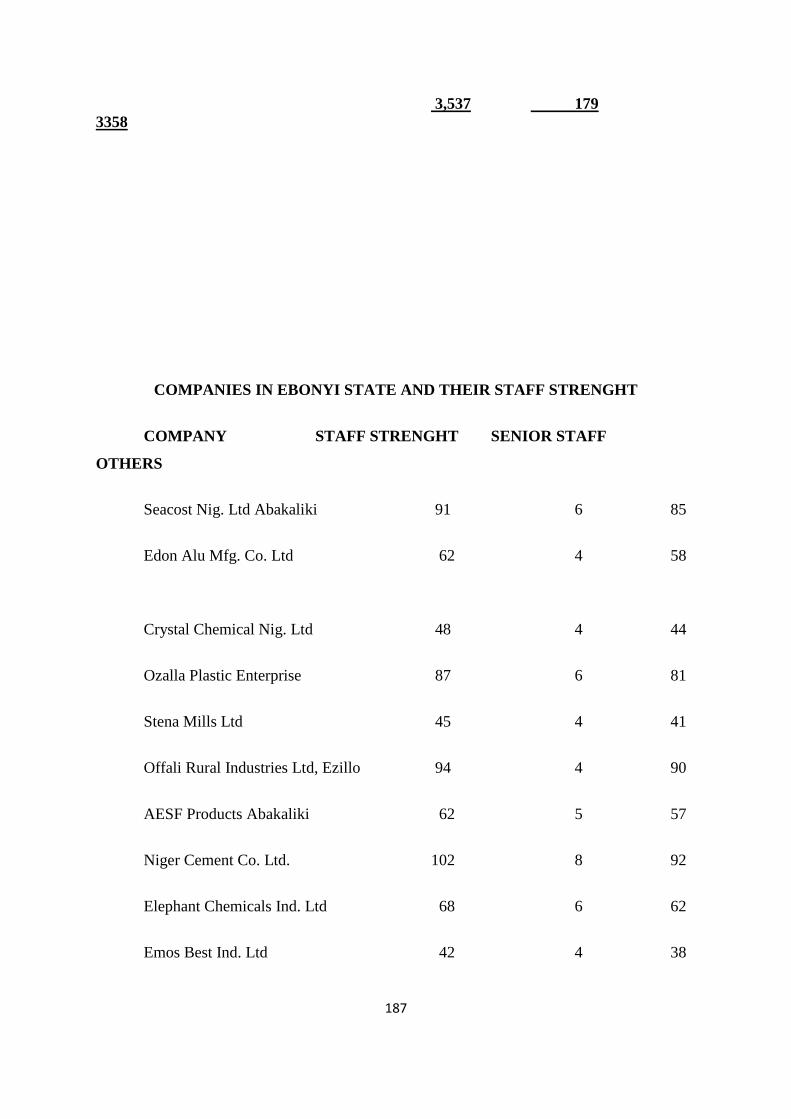

only the three states of the south-east were chosen, Anambra, Ebonyi and Enugu. The three

states were chosen because of proximity advantage. The population was the senior

accounting officers (managing directors) in the enterprises operating under Manufacturing

Association of Nigeria (MAN) in the three states as at 31st march, 2012. Manufacturing

enterprises was chosen because they have wider need for finance, optimum capacity

utilization and good records that can allow studies to be carried out on them.

1.7 Significance of the Study

To SME Operators:

Operators in the SME Sub-sector would have more insight into the various sources of

credit and tap them to achieve better result. They would be aware that government through

her agencies SMEDAN, BOI, NACRDB can protect them.

To Government

22

In addition to moderating the affairs of financial institutions, government would see the

need to provide enabling environment for SME to thrive so as to actually become the

driver of our economic growth and development.

To Public and Economy

The public will know that SME Sub-sector is a vibrant one which they can gainfully

venture into and thus make the economy of the nation most viable and enviable to foreign

investors.

1.8 Limitations of the Study

Certain limitations were encountered in the course of this study viz:-

i. Limited sample size:

The researcher found it difficult to increase sample size so as to have a

good representation of the entire population but we ensured that this did not

affect our study.

ii Respondents Resistance:

Most people are not willing to respond to oral questions as well as

questionnaires. This is because they feel that instant gain or benefits are not

attached.

iii Coverage:

In studies of this nature, coverage is usually a peculiar constraint. This

would limit the area of coverage but we ensured that they did not frustrate

our efforts.

1.9 Explanation of Acronyms.

SMEs - This means Small and Medium Scale Enterprises.

CBN - Central Bank of Nigeria which is the Apex bank for regulation of

the financial institutions affairs.

BOI - Bank of Industry

NBS - National Bureau of Statistics

NBCI - Nigerian Bank for Commerce and Industry.

NIDB - Nigerian Industrial Development Bank

NACRDB - Nigerian Agricultural, Cooperative and Rural Development Bank.

23

SMIEIS - Small and Medium Industries Equity Investments Schemes.

SMEDAN - Small and Medium Enterprises Development Agency.

Lending Infrastructures – The information environment, legal and judicial setting, tax

incentives etch. Rules and laws set by government.

REFERENCES

Anyanwu, C.M. (2011).“Financing and Promoting SSI, Concepts, Issues and Prospects”

Bullion Publication of CBN. Vol. 25, No. 3.

Allen, N.B. (2004). “Small and Medium Enterprises: Overcoming Growth Constraints”

World Bank Conference Paper Presentation ([email protected])

Ayozie, D.O. (1999). “A handbook on Small Scale Business for National Diploma

Students”. Danayo Inc. Coy. Ilaro.

24

Bates, F. (1997). Financing small business creation: The case of Chinese & Korean

immigrant entrepreneurs. Journal of business venture, vol. 12 pp109-124.

Birly, S. (1996).Start up in small business and entrepreneurship, eds, Bums and Dewhust,

Macmilian Press.

Buch, C.M. (2004)..Information versus Regulations:What drives the international

activities of commercial Banks? Journal of money credit and Banking No:51-69.

Blum, L. (1995).Free money for SMEs.4th edition, John Williams & Sons inc.

FBN Plc Bi-annual Review of SME Financing in Nigeria (1993) Vol. 2 No. 4.

Onugu, B.A. (2005). SMEs in Nigeria:”Problems & Prospects” Dissertation paper

presented to St. Clement University Lagos.

Olorunshola, J.A. (2001). “Industrial Financing in Nigeria: Some Institutional

Arrangement” CBN Economic and Financial Review. Vol. 24, No. 4.

Oye, A. (2006). Financial Management, page 578. El-Toda Ventures Ltd, Mushin, Lagos

Olu, A.O.(1999). A paper presented at the First Bank Business and Economic Report

Summit p1-5.

SMEDAN/NBS 2010 National Collaborative Survey

www.cenbank.org/out/publicaton/dfd/2004/smi

CHAPTER TWO

REVIEW OF RELATED LITERATURE

INTRODUCTION

The review of literature is arranged as follows:

2.1 Conceptual review

25

2.2 Theoretical review

2.3 Empirical studies

2.4 Summary

2.1 CONCEPTUAL REVIEW

HISTORICAL DEVELOPMENT OF SMEs IN NIGERIA

Small Scale Industry orientation is part and parcel of Nigeria. Evidence abound in our

respective communities of what success our great grandparents made in their respective

trading concerns; yam barns, iron smelting, farming, cottage industries and the likes. So

the secret behind their success (of a self- reliant strategy) does not lie in any particular

political philosophy, so much as in the people’s attitude to enterprise and in the right to

which the right incentive is enough to make risk worth taking are provided

(Anyawu,2011).

Economic history is well stocked with enough insights into the humble beginning of

present day giant Corporation. Evidence abound that almost all of the multinational giant

corporations were cottage enterprises, growing as their industry grew, and through their

own sheer ability either reproduce existing products more cheaply or improve their quality.

The respective government policies accorded and gave priority to the country’s small

scale enterprise. Abudu (2009),said that they constitutes the fountain head of vitality for

the variation economy and consequently their problems have been viewed as those of the

nation, by virtue of their number, diversity, penetration in all sectors of production and

marketing, contribution to employment and to the prosperity of the particular areas in

which they operate.

In concrete terms, CBN (2010) stressed that small scale industries constitute a greater

percentage of all registered companies in Nigeria, and they have been in existence for quite

a long time, majority of the small scale industries developed from cottage industries and

from small scale to medium and large scale enterprise. Prior to Nigeria’s Independence, the

business climate was almost totally dominated by the Colonial and other European

26

Multinational companies like United African company (UAC), GB Olivant, Uniliver Plc,

Patterson Zechonics, Leventis, etc. These companies primarily engaged in bringing into

Nigeria finished goods from their parent companies overseas. The government in those

days encouraged them to become stronger by giving incentives at favourable terms and tax

concessions (CBN, 2010).

A major/remarkable breakthrough in small scale business came about through the

indigenization Decree 2002 and later in Nigeria Enterprise Promotion Act 2007. These

were genuine attempts by the Federal Government to make sure that Nigerians play an

active and worthwhile role in the development of the economy. In the National

Development Plan, the Federal government gave special attention to the development of

small scale industries particularly in rural areas. This was in recognition of the roles of

small and medium scale industries, as the seedbeds and training grounds for entrepreneurs

(Mungcal, 2011). Nigerians need to take a cue from economic history, which is well

stocked with enough insight into the humble beginnings of the present day giant

conglomerates which started as small scale outfits.

Within this decade, the government policy measures placed emphasis on the technological

development of small scale industries in Nigeria. Various governments embarked on

corrective measures to focus efforts towards the maximum exploitation of natural

resources, and tried to discourage capital intensive mode of production in the light of the

abundant resources available Mungcal et al (2011).

The federal and state governments have both contributed to the growth of small scale

industries in Nigeria especially in the rural areas. In recent time, various fiscal and non-

fiscal incentives have been established for investors and entrepreneurs in the small scale

sectors of the economy. Of special mention was the strategy adopted by the federal

government for the training and motivation of the unemployed graduates, to be gainfully

employed in out of school entrepreneurship development programmes. Thus, on the

27

presentation of viable feasible projects, approved loans are disbursed through pre-selected

commercial banks assisted by the National Directorate of Employment CBN (2010).

To show its seriousness, the federal government through its educational agencies like the

National Board for Technical Education (NBTE), the Nigerian University commission

(NUC), and the National youths Service Corps (NYSC) programme gave directives that

entrepreneurial development courses be incorporated into the curricular of tertiary

institutions and NYSC programme.

2.1.1 Relevance of SMEs in Economic Development

The link between SMEs activity and economic growth and development is important

considering the relative larger share of SMEs sector in most developing countries and

because of substantial international resources that have been channeled into SMEs sub-

sector of these nations (Beck & Kunt, 2003).

One observes that SMEs is the major driver of the economic growth .The SMEs sector is

the backbone of the economy in high income countries, but is less developed in less

income countries OECD (2005). No wonder (Adelaja,2003) opined that SMEs have a lot

of important contributions to make to the economic development of the country. He

further posits that SMEs aid in the provision of employment, innovation, marketing of

goods and services. No wonder youth’s retirees and out of school graduates are now

gainfully employed thereby reducing crime, robbery and white collar jobs.

(Olorunshola,2001) opined that SMI assumed a heightened significance in the

development of literature and became a focal point of discussion at the global level. This in

fact makes the title of this paper, germane at this stage of Nigeria’s development. That is

why it captures the interest of government and other interest groups especially now that the

issue of poverty alleviation is on board.

28

Nigeria, just like most developing economies has always been faced with a choice between

two basic industrialization strategies, viz, large scale and small-scale industrialization. The

large-scale industries approach to development prefers attaining development through the

establishment of heavy industries. Such industries will then give rise to small industries

that will service them. This strategy is therefore designed to produce a backward linking

effect whereby the growth and expansion of a few large-scale industries would generate a

number of small-scale enterprises thereby making the gains of industrial growth to

permeate the rest of the economy. This link would lead to an advanced success in the

economy Onwumere & Ige,(2000).

(Allen, 2004) posits that any strategy of industrial development must consider the goals,

the resources, and the constraints facing an economy. The perception of the economic

planners may lead to differences in the strategies considered appropriate in any given

economy. Indeed radical changes in strategies may be called for over time because of

changes in goals or resource availability.

The superiority of small-scale industrialization strategy in promoting economic growth is

generally acknowledged. As a matter of fact, a positive correlation between the emergence

of an active small-scale industrial sector and the commencement of rapid economic growth

and development can always be established. A practical illustration is the recent

transformation of some South-east Asian economies from rudimentary states to highly

industrialized ones in the second half of the last century. That manifested the dynamic

potentials of small-scale industrialization option for developing economies.

SMEs will play a dominant role in dictating the pace of growth of the Nigerian economy

given an enabling environment. Such industries maintain a very strong and ubiquitous

presence in almost every sector of the economy Uche,( 2008).

29

SME Sub-sector therefore plays key roles towards moving the economy forward in the

following areas: capacity building, employment generation, promoting growth, service to

large scale industries, technology acquisition, even and industrial development and poverty

alleviation (Toyo, 2004; Venkataraman, 2004).

2.1.2 SOURCES OF FINANCE FOR SMEs

Sources of fund for SMEs are many and varied, but what determines the entrepreneurs

choice is dependent upon many factors, availability of credit or its accessibility, cost of

funds, and conditions to be met on one hand, and the stage at which the fund is needed on

the other hand (Adams,2002).

For a business that is starting newly studies has shown that the best type of financing

should be oneself, banking, thrift, asset sales, contributions from friends and neighbours,

non-governmental organizations, investor funding, interest sources (Binley,2006).

However, for an existing business, some of the sources mentioned above could be used in

addition to the following: Commercial and merchant banks, equity financing, debt

financing, venture capital financing (Kesava, 2002; Bates, 2007; Stevev & Jarillo, 2000).

2.1.3 VENTURE CAPITAL AND BUSINESS ANGELS

Venture capital involves the provision of investment finance to private, Small or Medium

Enterprises in the form of equity or quasi-equity instrument not traded on the stock

exchange (Abereijo & Fayomi, 2005). Venture capital is also referred to as risk capital.

Venture capital focuses on high growth business in early stages of development. The

stages of venture capital are basically:

a) Seed capital.

b) Start-up and early stage capital.

30

The venture capitalist may however provide funds for expansion and development, buyout

etc. A study on “the effect of venture capital financing on the economic value added profile

of Nigerian SMEs” (Dagogo & Ollor, 2012), found that venture backed SMEs contributed

more to society in terms of taxes to government, provision for corporate social

responsibility and staff welfare. The SMIEIS which is essentially a pool for venture capital

has not done very well in terms of providing equity funds for the SMEs Terungwa, (2011).

Recently, two new sources of funds have been unlocked for investment in growth business

in Nigeria through private equity and venture capital. They are the pension fund assets and

sovereign wealth fund (SWF) (Gbandi & Amissah, 2012).

2.1.4 PENSION REFORM ACT AND SMEs FINANCING.

The pension reform act of 2004 established the contributory pension Scheme (CPS). The

act has been largely adopted by the Federal government and the private sectors. However,

only 17 out of the 36 state governments have passed bills to adopt and implement the CPS

as at the end of 2004 CBN,( 2010). One of the duties of the National Pension Commission

(Pencom) which is the apex regulator is the establishment of standards, rules and issuance

of guidelines for the management and investment of pension funds under the act.

Under the pension act, the funds may be invested in private equity funds and venture

Capital subject to a maximum of 5% of pension assets. The funds can also be invested in

money market and equities. The pension asset funds were N2.029 trillion as the end of

2010. This means that more than N100 billion can be available for investment in private

equity and venture capital. This amount will grow as pension funds grow by an estimated

20-30 percent per annum in the next few years (James & Achua, 2010). SMEs will benefit

directly from pension funds investment in private equity funds (CBN,2010). But the

31

pertinent remark is that there has not been disbursement to the SMEs sub sector as at the

period of this review.

2.1.5 SME FINANCING ISSUES AND THE BANK

Compared with the position of large enterprises, the provision of finance to SMEs by

lending institutions can be problematic for a number of reasons (Berger and Udell. 2006;

Frank and Goyal, 2003). First, such institutions need to be able to effectively monitor the

performance of the enterprise and ensure that: the enterprise is abiding by the initial terms

of the contract; the enterprise is making satisfactory business progress; the necessary

means are available to ensure that the interests of the lender are being respected.

Such monitoring, however, is difficult due to a lack of transparency in the operation of

SMEs, which are less likely to follow expected norms of corporate governance. This is

compounded by the fact that SMEs experience greater volatility in profitability, growth

and earnings in comparison to larger firms, and their survival rate is much lower (Storey

and Thompson,et al 2005). SMEs also suffer from principal-agent problems, and

asymmetric information, which can lead to investment in more risky projects and present

lenders with the difficulty of distinguishing good loans from bad loans. In these

circumstances banks find it rational to engage in credit rationing (e.g. not extending the

full amount of the credit requested, even when the borrower is willing to pay a higher

interest rate).

In addition, it can be difficult to disentangle the financial position of the owner from that of

the firm. SMEs tend to have a much less developed bank-client relationship, which can be

32

important for successful access to finance. These difficulties can be further compounded in

the cases of start-up and young enterprises, which can have difficulties in providing the

collateral, employment of trained personnel and may be seen as potentially offering high

returns but at high potential risk (Nofsinger and Wang, 2011). The financial system may

not provide range of products and services to meet the needs of SMEs adequately.

However, there may be a ‘pecking order’ in terms of firm lending, with larger firms

favored by lending institutions (Seifert and Gonenc, 2008; Watson and Wilson, 2002).

SME problems in accessing finance are further exacerbated by rigidities in macro level

policy, institutions and the regulatory environment. At the macro-economy level,

government policy may require access to large amounts of finance, crowding out access to

finance for SMEs.

Government policies could also favor implementing industrialization and/or import

substitution development strategies that result in large domestic firms being given

favorable access to finance to the exclusion of other smaller enterprises. The domestic

legal system may not adequately protect lending institutions from delinquent payments and

bankruptcy, nor protect property rights, thus increasing the risk inherent in lending to

SMEs.

2.1.6 THE ROLE OF BANKS IN SME DEVELOPMENT

The statement that SMEs sector is the engine of growth for emerging economies like

Nigeria cannot be more appropriate than now when the fabrics of several sectors in the

country have deteriorated very well due to the financial meltdown (Sanusi,2010).The truth

remains that many institutions including the banks has continued to treat issues relating to

the SMEs with levity. The reason adduced is that the banks feel that the sector is a high

33

risk sector. Banking sector’s lack of commitment to the sub-sector could be drawn from

the revelation in 2008 that Banking sector credit to SMEs in 2010 was less than 4% of its

estimated N7.8trillion claims to the private sector.

However, the essence of the Bankers committee was to boost the credit advancement to

SMEs. That was why they mandated the banks to set aside 10% before profit to SME sub-

sector through the equity investment schemes. The question that is pertinent is to ascertain

how far the banks are willing and involved in the advancement of such funds to SMEs.

The (CBN2010) conclusively compared Nigeria’s SMEs with those of other countries like

India. He posits that Indian SME accounts for 39% of manufacturing output and 233% of

total export thereby registering higher growth rate when compared to the other sectors.

2.1.7 THE EXISTENCE OF SME FINANCING GAP

Some studies found out that SMEs face a deficiency in obtaining the finance that they

require, and that this will act as major inhibitor in terms of their performance; growth,

employment, and productivity (Torre et al 2010). This section discusses the existence of

‘financial gaps’ for SMEs. From a conceptual perspective, it was considered for a long

time that it was not meaningful to talk about a financing gap, except where the authorities

deliberately kept interest rates below the market clearing level. As risks increased financial

lenders would be required to increase interest rates to bring market demand into

equilibrium with market supply.

However, (Stiglitz and Weiss 2001; Gertler and Gilchrist 2004) showed that under certain

conditions financing gaps can exist for all firms, as banks respond in a rational fashion by

34

imposing credit rationing. While the arguments were not specifically targeted at explaining

credit rationing for SMEs, these enterprises possess characteristics that make them more

prone to credit rationing than larger enterprises. This position has been applied more

generally to problems encountered in emerging market and developing economies in

particular.

2.1.8 CONCEPT AND CAUSES OF A FINANCING GAP

The issue of access to finance by firms in general, and the theoretical recognition that

financing gaps can exist for firms, can be traced back to the theory of imperfect

information in capital markets (Stiglitz and Weiss 2001 et al). Banks are likely to adopt

more stringent lending policies favoring those who are able to provide more collateral

assets, or who have a more established credit record. In other words banks adopt credit

rationing measures to minimize problems. The financing gap here could be measured by

the difference between desired access to finance and actual access to finance, and by the

cost and terms of access to finance.

The potential for credit rationing is thought to be greater for small firms. On the demand

side, as argued by (Petersen and Rajan, 2004), the amount of information that banks could

acquire is usually much less in the case of small firms, because banks have little

information about these firms’ managerial capabilities and investment opportunities. The

extent of credit rationing to small firms may also occur simply because they are not usually

well-collateralized (Gertler and Gilchrist,2004). The most recent paper by (Torre et

al.2010) also attributes hindrances to SMEs’ access to finance to ‘‘opaqueness”, meaning

that it is difficult to ascertain if firms have the capacity to pay (have viable projects) and/or

the willingness to pay (due to moral hazard).

35

This opaqueness particularly undermines lending from institutions that engage in more

impersonal or arms-length financing, requiring hard, objective, and transparent information

(Hytinen and Pajarinen, 2008). Thus the problem of a mismatch between the supply of

funds (loans) and the demand for funds (loans) leads to the notion of “financial gaps”.

The gaps exist if particular categories of firms that ought to receive financing are unable to

obtain it, despite a willingness to pay higher interest rates, (indicating market failure)

particularly if such business opportunities are profitable. A mismatch between demand for

finance and supply of finance can arise due to asymmetry in information and consequent

difficulty in distinguishing between good and bad loans, leading to the application of credit

rationing. This is potentially more severe for SMEs than for large enterprises (Berger &

Udell et al 2006).

2.1.9 IMPERATIVES OF GOOD BANKING HABITS FOR SUCCESSFUL SMEs

OPERATIONS

The need for banks to possess outstanding qualities when SMEs operations are concerned

cannot be over-emphasized.(Ogubunka,2003), states that there is no doubt that sustainable

industrial development in an economy is germane to national economic growth and

development. For one thing, industrial development has been credited with creating

productive opportunities for positive economic and social growth and development. This

is why governments all over the world are concerned about the state, stage and level of

industrial development in their countries. They are always interested in measures that

would not only improve but also sustain such developments, especially as the level of

industrial development differs in developed, developing and under-developed nations.

It is the drive to reduce some of such socio-economic problems that efforts, including the

on-going Millennium Development Goals, are being pursued across the globe. Whether

36

such efforts would realistically reduce or eliminate the challenges will depend on a variety

of issues, one of which ought to be the roles to be played by various stakeholders including

SMEs and banks (Seers, 2002).

There is no-gain-saying that banks, because of their distinct and unique place in the

economy as financial intermediaries, are important and necessary agents in the

transformation of national economies to the path of growth and development (Afolabi ,

2004).

Consequently, both SMIs and banks can be seen as critical socio-economic transformers,

especially if there is good synergy between them. This will create and widen the path to

successful industrial operations. (Lamido, 2010).

Whereas, there are evidences to indicate that SMIs and banks have, in Nigeria, been having

operational relationship over the years, the question sometimes asked is whether such

relationship has helped in any meaningful way to bring about sustainable industrial

development within the economy. While there may be varying responses to the question,

suffice it to state that irrespective of where the relationship has led to date, it can

significantly be improved upon, if the country must achieve sustainable industrial

development. This is very important because while banks had often fingered lack of good

banking habits of SMIs as a key reason for banks’ inability to provide assistance to them,

the SMIs on the other hand, had accused banks of insensitivity to their needs and high-

handedness in providing services. Thus, as the country matches forward to becoming one

of the largest 20 economies in the world and the African Financial Centre by the year

2020, it is necessary that banks and SMIs should relate most appropriately to facilitate

successful industrial operations and development. (Zuvekas , 200s9).

.

37

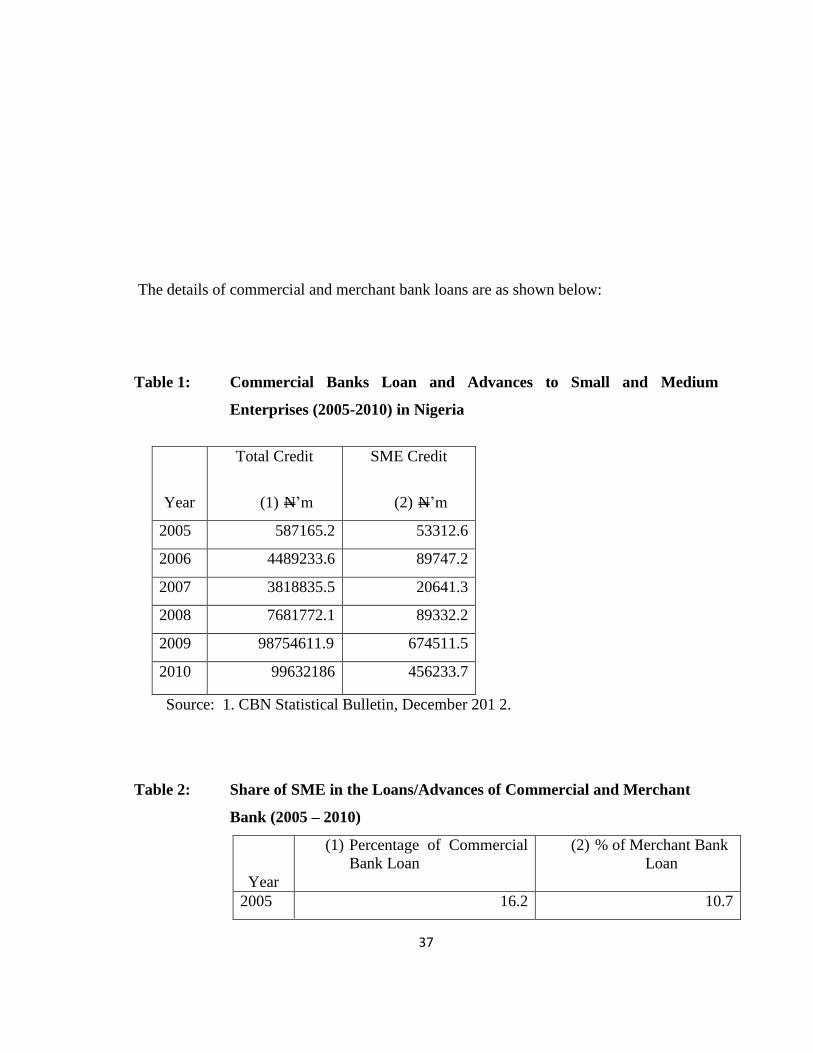

The details of commercial and merchant bank loans are as shown below:

Table 1: Commercial Banks Loan and Advances to Small and Medium

Enterprises (2005-2010) in Nigeria

Year

Total Credit

(1) N’m

SME Credit

(2) N’m

2005 587165.2 53312.6

2006 4489233.6 89747.2

2007 3818835.5 20641.3

2008 7681772.1 89332.2

2009 98754611.9 674511.5

2010 99632186 456233.7

Source: 1. CBN Statistical Bulletin, December 201 2.

Table 2: Share of SME in the Loans/Advances of Commercial and Merchant

Bank (2005 – 2010)

Year

(1) Percentage of Commercial

Bank Loan

(2) % of Merchant Bank

Loan

2005 16.2 10.7

38

2006 10.8 16.4

2007 22.1 18.2

2008 18.8 13.0

2009 23.7 11.2

2010 11.2 14.6

Source: CBN Statistical Bulletin, Various Issues 2012

2.1.9.1 APPRAISAL OF SOME SOURCES OF FINANCING SMEs IN NIGERIA

The availability of the various sources of finance are meaningless without the appropriate

appraisal of some of the sources that are of paramount importance to SMEs. No wonder

government established a coordinating umbrella organization called “Small Scale

Industries Corporation” in 1971 saddled with the responsibility of promoting SMEs. This

is acquired through the establishment of some institutions and programmes to provide

development capital to the SMEs. Notable amongst these institutions and programmes are

as follows:-

Small Scale Industries Credit Scheme (SSICS)

SSICS was as a revolving grant by the federal and state government to assist in meeting

the credit needs of the sub-sector on a more liberal condition than in private lending

institutions such as commercial banks. The problem of financial resources especially at the

state level coupled with rampant mismanagement of meager funds by both the

administrator of the loans as well as the benefiting SMEs killed the scheme.

The First Bank of Nigeria plc bi-annual review December 2003, Federal Government

decided to look for several other available options to bring up SME to at least acceptable

level to enhance economic development and growth employment generation, wealth

39

creation etc. Federal Government extricated itself from the scheme and then launched

another scheme called Nigerian Bank for Commerce and Industry (NBCI).

Nigerian Bank for Commerce and Industry (NBCI)

(Anyanwu, 2011) in his workshop paper titled “The Role of CBN in SME Financing”

appraised SME financing thus: NBCI was set up to provide financial services to the

indigenous business community, particularly SMEs. NBCI was operated as the apex

financial body for SME and also administered the SMEs World Bank loan scheme, World

Bank (2000). It approved a total of 797 projects with a credit value amounting to N965.5

million between 2001 and 2004. They disbursed N141.82m between 2006 and 2008. The

bank also financed a total of 126 projects under the World Bank loan scheme, some of

which were cancelled due to the failure of project sponsors to contribute their counter-part

funding. The NBCI suffered from operational problems, culminating in a state of

insolvency though, it is now part of the newly established Bank of Industry (Oputa,2011).

Central Bank of Nigeria (CBN)

(Olorunshola, 2001) agreed that CBN is the apex regulator of the financial institutions.

“The CBN has since 1990 been instrumental to the promotion and development of

enterprise particularly in the SME sub-sector. The CBN credit guidelines requires that

commercial and merchant banks allocate a minimum stipulated credit to sectors classified

as preferred including SME CBN stipulated differential interest rates for sect oral credit

allocations with varying moratorium on the repayment of loans and advances. For

instance, since 1990s CBN directed that at least 10% of the loans advanced to indigenous

borrowers should be allocated to SMEs (CBN, 2012).

However, given the cumbersome administration of such loans, banks preferred to pay

prescribed penalties rather than channel credit to the SMEs. The failure of banks to meet

the prescribed credit allocation led the CBN to mandate such defaulting banks as from

1987, to make such lending shortfalls available to it for onward transfer to the relevant

40

sub-sector. The worrisome aspect of this is that banks are still not comfortable to make

credits accessible to SMEs and this has led to serious setbacks for SMEs to date.

STATE GOVERNMENTS

(Udechukwu, 2003) opined that state governments are not left out in the move to make

SMEs work. State government through their ministry of commerce and industries also

promote the development of SMEs. In this regard, some state governments promote the

SMEs through State-owned finance and investment companies which provide technical

and financial assistance to SMEs. However, owing to numerous constraints, some were

less active than others. The state government has ventured into many schemes and

programmes to strengthen and control SMEs through: centre for management development

(CMD), SSICS, NERFUND, SMIEIS etc.

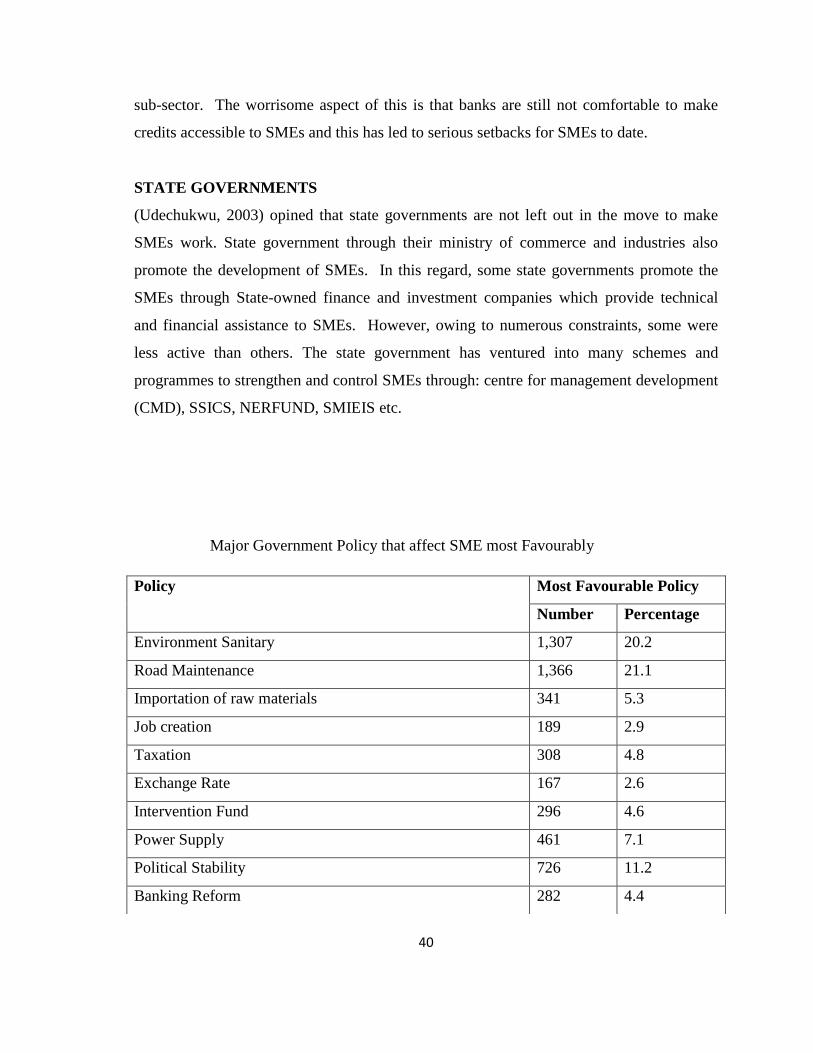

Major Government Policy that affect SME most Favourably

Policy

Most Favourable Policy

Number Percentage

Environment Sanitary 1,307 20.2

Road Maintenance 1,366 21.1

Importation of raw materials 341 5.3

Job creation 189 2.9

Taxation 308 4.8

Exchange Rate 167 2.6

Intervention Fund 296 4.6

Power Supply 461 7.1

Political Stability 726 11.2

Banking Reform 282 4.4

41

Source: SMEDAN/NBS(2012)

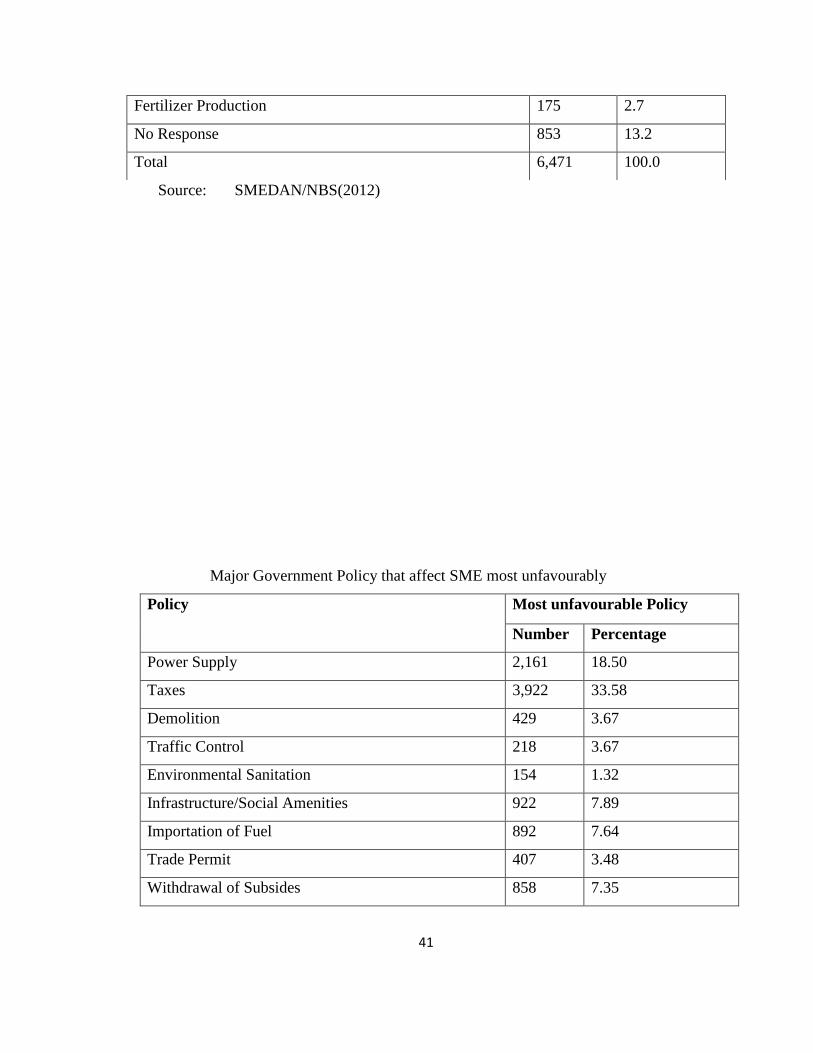

Major Government Policy that affect SME most unfavourably

Policy Most unfavourable Policy

Number Percentage

Power Supply 2,161 18.50

Taxes 3,922 33.58

Demolition 429 3.67

Traffic Control 218 3.67

Environmental Sanitation 154 1.32

Infrastructure/Social Amenities 922 7.89

Importation of Fuel 892 7.64

Trade Permit 407 3.48

Withdrawal of Subsides 858 7.35

Fertilizer Production 175 2.7

No Response 853 13.2

Total 6,471 100.0

42

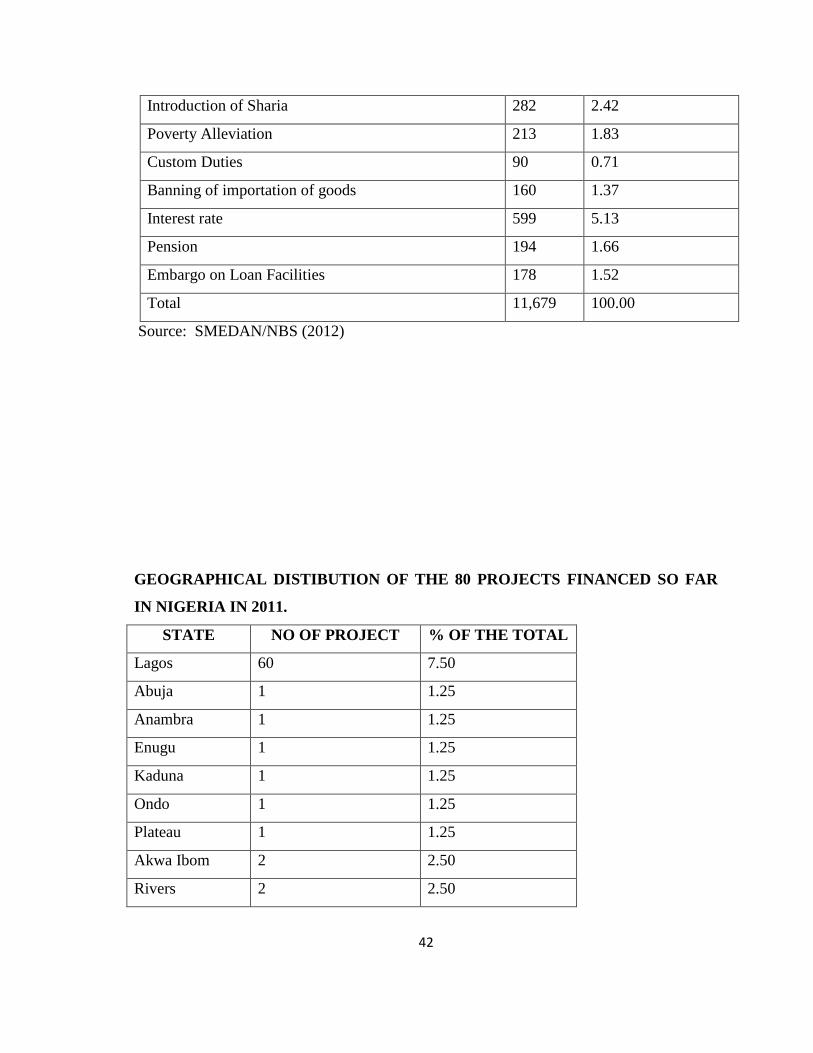

Introduction of Sharia 282 2.42

Poverty Alleviation 213 1.83

Custom Duties 90 0.71

Banning of importation of goods 160 1.37

Interest rate 599 5.13

Pension 194 1.66

Embargo on Loan Facilities 178 1.52

Total 11,679 100.00

Source: SMEDAN/NBS (2012)

GEOGRAPHICAL DISTIBUTION OF THE 80 PROJECTS FINANCED SO FAR

IN NIGERIA IN 2011.

STATE NO OF PROJECT % OF THE TOTAL

Lagos 60 7.50

Abuja 1 1.25

Anambra 1 1.25

Enugu 1 1.25

Kaduna 1 1.25

Ondo 1 1.25

Plateau 1 1.25

Akwa Ibom 2 2.50

Rivers 2 2.50

43

Ogun 3 3.75

Oyo 3 3.75

Delta 4 5.00

Total 80 100

Source: Federal Office of Statistics

NATIONAL ECONOMIC RECONSTRUCTION FUND (NERFUND)

(Olorunshola,2011) agreed that the main focus of is the provision of soft medium to long

term funds for wholly Nigerian owned SMEs in the manufacturing, agro-allied, mining &

quarrying and equipment leasing. It provides enterprises as SMEs with fixed assets plus

cost of new investment (land excluded, not exceeding N36m and sourcing not less than

60% of their raw materials locally in the case of manufacturing projects.

NERFUND interest rates are slightly lower than market rate CBN (2012). Furthermore,

the rates payable by the participating banks (Pbs) are limited to 1% above NERFUNDs’

cost of borrowing. Pbs are allowed a spread of not more than 4% over their cost of fund.

For all types of facility, and irrespective of the ability of the beneficiary to pay maturing

obligations, it is required that a Pbs repays NERFUND, failing which the CBN will

automatically debit the bank’s account with such an amount.

Small and Medium Enterprise Development Agency of

Nigeria (SMEDAN)

SMEDAN has continued search for solutions towards a vibrant and virile small and

medium enterprises sector, and to entrench the sector into the main stream of the Nigerian

economy. The Agency is a “one stop shop” for nursing and nurturing SMEs in Nigeria.

Consequently, SMEDAN has since inception been in the forefront of developing and

promoting SMEs and entrepreneurs in Nigeria. Some of the functions of the Agency are as

follows:

1. Initiating and articulating policy ideas for SMEs growth and development.

2. Stimulating, monitoring and coordinating the development of the SMEs sector;

44

3. Promoting and facilitating development programmes, instruments and support

services to accelerate the development and modernization of SMEs;

4. Serving as a vanguard for rural industrialization, poverty reduction, and job

creation and thus facilitating enhanced sustainable livelihoods;

5. Linking SMEs to internal and external sources of finance, appropriate

technology, technical skills as well as to large enterprises;

6. Monitoring implementation of government directives, incentives and facilities

for SMEs development;

7. Recommending to government required amendments to business regulation

frameworks for ease of enterprise development.

8. Mobilizing internal and external resources, including technical assistance, for

the development of SMEs.

However the roles of the agency are enhancing SMEs access to finance, sustainable

national development and rural enterprise development. They have impacted on many

businesses like: Cane weaving in Lagos, Fish and irrigation farmers Alao in Borno State,

Cassava Cluster in Taraba State, Ginger in Kwoi Local Government in Kaduna State, Shea

butter cluster in Agbaeku eji, Black soap cluster in Osun State, Aba leather cluster in Abia

State,Women Mat Weavers in Ekiti State, and Abakaliki rice cluster in Ebonyi State.

Community Bank (CB)

The programme for the establishment of Community banks was announced in the 1990

Federal Government Budget. This category of banks is expected to carry out banking

businesses but at purely local community level. Their role is to provide effective financial

services for the rural area as well as micro-enterprises in the urban centres. Towards the

end of that year, government established the Community bank Implementation Committee

(CBIC) with responsibility; among others, for appraising application and issuing

provisional licenses to incorporated Community banks. Formal licenses were ultimately

issued by the Federal Ministry of finance, upon application presented to it by the CBIC

45

through the Central Bank of Nigeria. The bulk of community bank clients fall under the

SMEs’. Unfortunately, the banks are not wide spread enough to make the desired impact

on SMEs’ access to credit.

2.1.9.2 Current Financing Initiatives and the Way Forward

In order to make the SME more vibrant, the Central Bank of Nigeria has evolved new

initiatives, which are geared towards improving accessibility of credit to the SMEs through

the following:

The Small and Medium Industries Equity Investment Scheme (SMIEIS)

Bothered by the persistent decline in the performance of the industrial sector and with the

realization of the fact that the small and medium scale industries hold the key to the revival

of the manufacturing sector and the economy in general, the Central bank of Nigeria

successfully persuaded the Bankers’ Committee in 2010 to agree that each bank should set

aside 10 percent of its annual pretax profit for equity investment in small and medium

scale enterprises. To ensure the effectiveness of the programme, banks are expected to

identify, guide and nurture enterprises to be financed under the scheme. The activities

targeted under the scheme include agro-allied, information technology,

telecommunications, manufacturing, educational establishments, services, tourism and

leisure, solid minerals and construction. With the introduction of the scheme, it is expected

that improved funding of the SMEs will facilitate the achievement of higher economic

growth. As at August 2000, the sum of N11.572 billion had been set aside by 77 banks.

Out of this amount, N1.692 billion had been invested in the small and medium scale

enterprises. Federal government through CBN ensured that even in 2013, banks set aside

N420bn each to some states in the federation with the intent to pedal SMEs to the forefront

in enhancing national development Waziri, (2013).

Nigerian Agricultural, Cooperative and Rural Development Bank (NACRDB)

The Nigerian Agricultural Cooperative and rural Development Bank Limited is an

amalgam of the former Peoples bank of Nigeria, Nigerian Agricultural and Cooperative

46

bank and the Family Economic Advancement Programme (FEAP). It was set up in

October 2000, primarily to finance agriculture as well as small and medium enterprises.

The NACRDB is structured to accept deposits and offer loans/advances in which the

interest rates are graduated according to the purpose for the loan to Nigerians and their

business. The bank also offers a number of financial products including target savings;

start-up as well as small holder loan schemes.

Refinancing and Rediscounting Facility (RRF)

With effect from January 2002, the CBN introduced the Refinancing Facility at

concessionary interest rate to support medium to long term bank lending to the productive

sectors of the economy in as much as SMEs are not usually part of it. This facility was

instituted to provide liquidity to banks in support of their financing of real sector activities.

This was in recognition of the fact that aggregate credit by deposit money mainly to

general commerce and trade. Furthermore, there is need to encourage medium to long

term lending to the productive sectors of the economy, if the production base of the

economy is to be expanded and diversified. The RRF is designed to provide temporary

relief to banks, which face liquidity problems as a result of having committed their

resources to long term financing to the specified productive sectors. The sectors include

agricultural production, semi manufacturing and manufacturing, solid minerals and

information technology. Under the facility, banks shall have access up to 60% of the

qualifying loans. Qualifying loans must have been held for not less than one year.

International Financial Assistance

Government has continued to approach international financial agencies to source need

foreign capital for the SMEs. Such agencies includes World bank and its affiliates and the

African Development Bank (ADB). The Federal Government often guarantees and agrees

to monitor or co-finance the SMEs receiving such external financial support. For instance,

in 2012, the ADP granted an export stimulation loan of US344m for SMEs in Nigeria. The

47

loan is repayable in 20 years with a concessionary interest rate of 5.2% World Bank

Economic Summit (2013).

SMEs Financing By International Development Agencies

Members of the World Bank group, the International Finance Corporation, (IFC) have

made significant contributions towards SME financing in Nigeria. In 2010, the IFC more

than doubled its exposure to Nigerians’ banking sector, investing almost $400 million of

equity and loan financing in First bank of Nigeria (FBN), First city monument bank

(FCMB) and GT bank (Omorogbe,2011). The purpose of the new investment and advisory

services of IFC was to help banks reach segments of the economy that needed better

funding such as infrastructure and the SMEs (Onyeyinka, 2010). Specifically, FCMB

received $70 million in November 2010 to help it increase financing of SMEs. The

corporation is also working with the Department for International Development (DFID) to

expand its funding and advisory role programs to Nigerian banks that have incorporated

non-financial services to SMEs. In the words of IFC’S country Manager for Nigeria,

Adegbie-Quaynor

“Non-financial services such as management and advisory

support help SMEs acquire the skills they need to grow.

IFC is working with Banks in Africa to help them deliver

non-financial services, which in turn allows the banks to

build a more loyal and diverse portfolio of small and

medium Businesses” (Oladunjoye, 2012).

The African development bank (AFDB) is another international agency that plays a role in

financing of SMEs not only in Nigeria, but in many other countries in Africa. The AFDB

has approved a total of 700million worth of loan programs for Small and Medium sized

Enterprises in Nigeria. (Mungcal, 2011). Another institution used by the AFDB in its effort

to improve funding for SMEs is the African guarantee fund (AGF) (Sogunle, 2011).

48

2.1.9.3 Some Countries Experiences in SMEs Development

United State of America (USA)

In the United States of America, issues pertaining to small business financing are handled

by a government agency – Small Business Administration (SBA), which is responsible for

creating and servicing a strong partnership with the private sector for economic

development through small businesses. The agency oversees and actually administers

funds according to needs to small businesses. It creates awareness about funds available,

the categories of business that can get them and the pre-requisites to obtain them. (Buch &

Claudia, 2003). The American Small Business Administration (SBA) has several aims

viz:- Increasing opportunity for Small Business success, transforming itself into a 21st

century leading edge institution, helping businesses recover from disaster, Serving as a

voice for American Small businesses etc.

In the word of its Administrator Aaida Alvarez, the SBA is “streamlined programmes to

help today’s small business…succeed into the next millennium.”

In this regard, it provides customer-oriented, full-service programmes, and accurately

timely information to the entrepreneurial community. Besides providing the actual fund,

the SBA is involved in providing a number of facilitations to small businesses including

loan guarantees, certificate of competence, prime contracting, and breakout procurement,

research and development and business information service (Cole, 2008).

It is however pertinent to note that SBA channels all its assistance to SMEs through

appropriate institutions e.g. commercial lending institutions. This type of coordination and

effective administration of SME operation is yet to be witnessed in Nigeria. In fact, over

the years, the lack of proper coordination of SMEs in Nigeria has led to multi-prolonged

implementation of funding and other development schemes (Ihyembe, 2009).

49

The Philippines

In the 1960s, the Central bank of Philippines established an Agricultural Guarantee Loan

Fund (AGLF) which was placed as special deposits in various rural banks. These deposit

served a twin purpose: as sources of loan able funds and as a channel for providing partial

guarantee for loans granted by the rural banks. Later the AGLF was replaced by the

Agricultural Guarantee Fund (AGF) under which the level of guarantee was raised to 70%

of all losses incurred by rural banks in respect of loans granted. In order to streamline the

administration of the different guarantee funds, a single Trust Fund, administered by the

Land Bank of Philippine was introduced to guarantee up to 85% of credit granted

specifically for the production of rice, sorghum and soya beans (Deyoneg, Robert, Hunter

(2012); Udell , 2004).

India

In order to facilitate the flow of financial assistant to small scale farmers and enterprises,

India established an Agricultural Development Bank and an Industrial Development bank,

in the early 1950s and 1960s, as apex organizations to refinance credit supplied by other

financial institutions for both agricultural and industrial projects (Udell,2004).

Empirical evidence show that in India substantial credits have been granted by nationalized

commercial banks under the refinancing and guarantee scheme to agricultural and small-

scale industries. The guarantees improved access of small businesses to credit, thereby

ensuring widespread adoption at improved technologies such as small scale irrigation

schemes and high yielding varieties of seeds among peasant farmers. Worid Bank, (2005)

shows that the major strength of the Indian Credit System, however, is the overwhelming

presence of government subsidy programmes. The high probability of debt forgiveness for

political consideration has heightened the risks of loan delinquency and frequent resort to

redemption of the guaranteed loans.

50

As a result of willingness on the part of banks to channel enough credit to SMI, the

government of Mexico in 1959 created a Trust Fund in the banks of Mexico to rediscount

and guarantee industrial/agricultural loans. After many years, government re-decided to

re-organize the rural credit system. This was done by creating a central agricultural bank

called “Banc National de Credit Rural (BANCURAL) who has the onerous task of

financing agricultural/industrial sectors.

2.1.9.4 Problems of SME in the Development Process

(Onwumere, 2000), in the CIBN Journal explained that several problems are inherent in

the SMEs growth and development: Inadequacy of finance and infrastructural facilities,

low entrepreneurial skills, multiplicity of taxes, restricted market access and poor

implementation of policies.

51

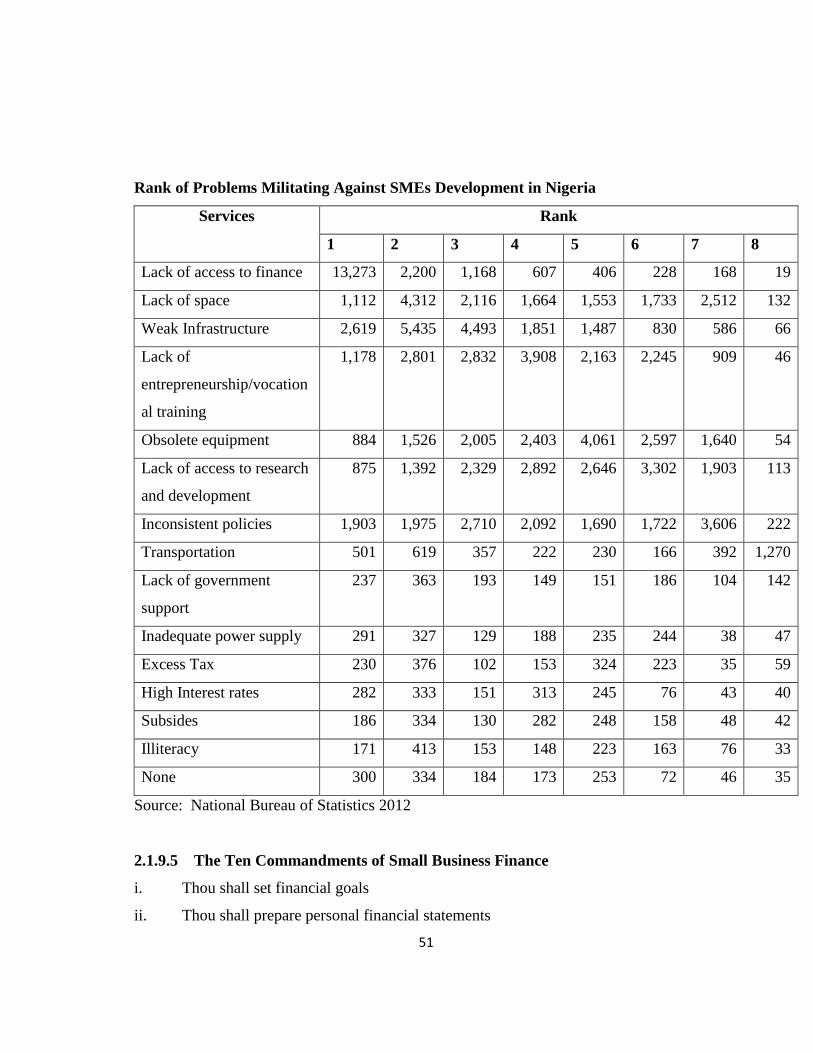

Rank of Problems Militating Against SMEs Development in Nigeria

Services Rank

1 2 3 4 5 6 7 8

Lack of access to finance 13,273 2,200 1,168 607 406 228 168 19

Lack of space 1,112 4,312 2,116 1,664 1,553 1,733 2,512 132

Weak Infrastructure 2,619 5,435 4,493 1,851 1,487 830 586 66

Lack of

entrepreneurship/vocation

al training

1,178 2,801 2,832 3,908 2,163 2,245 909 46

Obsolete equipment 884 1,526 2,005 2,403 4,061 2,597 1,640 54

Lack of access to research

and development

875 1,392 2,329 2,892 2,646 3,302 1,903 113

Inconsistent policies 1,903 1,975 2,710 2,092 1,690 1,722 3,606 222

Transportation 501 619 357 222 230 166 392 1,270

Lack of government

support

237 363 193 149 151 186 104 142

Inadequate power supply 291 327 129 188 235 244 38 47

Excess Tax 230 376 102 153 324 223 35 59

High Interest rates 282 333 151 313 245 76 43 40

Subsides 186 334 130 282 248 158 48 42

Illiteracy 171 413 153 148 223 163 76 33

None 300 334 184 173 253 72 46 35

Source: National Bureau of Statistics 2012

2.1.9.5 The Ten Commandments of Small Business Finance

i. Thou shall set financial goals

ii. Thou shall prepare personal financial statements

52

iii Thou shall prepare business financial statement

iv Thou shall support projections of future cash flows with sound logic

v. Thou shall decide upon a target capital structure

vi. Thou shall anticipate a realistic cost of capital.

vii. Thou shall recognize all current source of financing

viii. Thou shall consider alternative sources of financing

ix. Thou shall recognize exposure to business risk

x. Thou shall ensure that the financing plan fits with the overall business plans.

(From the GHANAIAN BANKER, 3rd Quarter, July – September 1997 Vol. 33)

2.1.9.6 Closing the Financing Gap for SMEs in Nigeria

From the Editorial Desk of the Nigerian banker (2000), posits that perhaps no other

development strategy has enjoyed as much prominence in Nigeria’s development plans as

the Small and Medium Scale Enterprises (SMEs) development strategy. Because

government has identified this sub-sector as a veritable engine of growth, it has

continuously put in place policies and incentive packages that will promote this segment of

the economy. However, the efforts in this direction have not paid off. But that does not

mean that we shall give up since that will imply accepting failure. The government should

not give up, but continue to come up with favourable policies and incentive packages as

well as establish an enabling environment to foster the growth of SMEs.

A major constraint identified in this segment of the economy is the financing gap and that

informed the establishment of a number of Development finance Institutions (DFIs) such

as the Nigerian Industrial Development bank (NIDB), Nigerian bank for Commerce and

Industry (NBCI) and Nigerian Agricultural and Cooperative bank (NACB) between 1960

and 1980 to bridge the funding gap. This was followed by the establishment of such

specialized instructions as the Peoples bank and community Banks to provide funding for

the sub-sector.

53

Other financing schemes designed to facilitate credit delivery to SMEs include the World

Bank Assisted Small and medium Scale Enterprises (SMEs) Apex Unit Loan Scheme; the

Export Stimulation Loan Scheme (ESL); and the Rediscounting and Refinancing Facility

(RRF) etc.

All these made minimal impacts on the economic development process of Nigeria. The

SMEs sub-sector has continued to be regarded as a high risk sub-sector. Conventional

banks thus tread cautiously when it involves credit extension to this sub-sector. A major

pitfall here has been the level of discipline of the beneficiaries of these credit facilities as

some of them see these loans as their own share of the “national cake’. This therefore

leads to mismanagement of such credit facilities. Another pitfall is the inadequacy of the

operating milieu which can now be described as hostile. The current environment cannot,

by any freak of circumstances, meaningfully support the growth of any small business

enterprise. Considering the epileptic power supply, the unreliable telecommunication

facilities, poor state of roads and even the poor attitude to work of the populace which