Embed Size (px)

DESCRIPTION

A helpful overview of the basic considerations for EMV implementation.

Citation preview

EMV 101: Everything you need to know about EMV

E - B O O K

1

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

The Glossary of Terms provides a quick reference tool for navigating the many technical terms and abbreviations brought up when discussing EMV.

The Migration Timeline traces the history of EMVco standards, and outlines when migration steps will take effect in the US.

Lessons Learned provides a comprehensive look at economies around the world where EMV migrations are currently underway or are complete. Experiences from other countries can provide valuable insights for everyone involved in the US EMV migration.

Behind the Transaction provides a more in-depth look at why adding layers of security to our current payment ecosystem can benefit everyone within it.

Key Players takes a closer look at everyone who is involved in the US EMV migration, and how each group can be best prepared for the shift.

The EMV Checklist provides a step-by-step analysis to help you evaulate your current infrastructure and prepare for migration.

HOW TO USE THIS E-BOOK

Use this EMV chip graphic to jump to the in-depth chapter of any topic, or to go back

to the intro chapter.

IntroductionThis e-book breaks EMV down to six questions: who, what, where, when, why, and how. These topics can help you figure out what’s going on, who it will affect, when to expect changes, why this is all necessary, and how to get started. The introductory chapter, EMV 101: The Five Ws, goes through each “W” question in a brief overview, and each subsequent chapter goes in-depth on one question. Whether your EMV questions are general or specific, macro or micro, EMV 101 can get you answers.

This intro chapter is a brief introduction to all

things EMV, and answers the five classic questions:

Who? What? Where? When? & Why?

EMV 101: THE FIVE Ws

3

Where is the US payment card industry now?

Today, payment and identification cards of all types (credit cards, gift cards, loyalty cards,

membership cards, etc.) are encoded with the cardholder’s information on the back of the card

using a strip of magnetic tape, also known as the magnetic stripe.

When a consumer swipes a standard magnetic stripe card at a retailer’s point of sale (POS)

terminal, or inserts it into an ATM, the data on the magnetic stripe is captured for transmission to

an authorization system. Fraudsters have been able to put skimmers at these locations to capture

the data from the magnetic stripe, and in more sophisticated attacks, install malware on computers

connected to the POS terminal to capture the data. The prevalence of magnetic stripe cards in the

US makes card skimming and card copying easy and lucrative. In 2012, the US accounted for 47% of

global credit card fraud while only being responsible for 23% of total global credit card use.

Chip cards are different from traditional magnetic stripe cards in the way they communicate with

card reader devices. Rather than the classic swipe-to-scan method, chip cards have an embedded

integrated circuit chip which connects to the POS terminal’s chip card reader. This chip is a

EMV 101: THE FIVE Ws

23%

47%

US Share of Global Credit Transactions

US Share ofGlobal Credit Fraud

(Nilson Report, 2014)

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

4

microprocessor, which is essentially a very small computer, with the capability to encrypt transaction

data dynamically for each purchase. Because the card has a microprocessor embedded, it has the

ability to make some payment-related decisions without the need to connect to the network. That

is why this type of card is often referred to as a “smart card.” With over 1 billion cards in use, EMV is

already a burgeoning global reality.

Contact Chip Cards can be distinguished by their square metallic contact pads. These cards are

inserted into a POS terminal which has an integrated chip card reader; much like a microSD card

or flash drive is inserted into a computer. The card stays inserted in the POS terminal until the

transaction is complete. Chip cards are only activated when connected to a reader, which provides

the power source for communication. Chip cards do not have batteries and do not need to be

charged.

Additionally, Contactless Chip Cards do not require an internal power source. Embedded in the

plastic of a contactless card is an antenna. Using radio waves, the card communicates with a reader

that emits a specific radio frequency. This frequency is harnessed to power the electronic chip.

Contactless cards are especially advantageous for use as payment cards because they need only a

moment to tap or wave the card near a reader to complete the communication. Recent pilots and

rollouts indicate contactless chip cards will be widely utilized for transit payments.

Hybrid or Dual Interface cards include both a contact pad and an internal antenna. They can be

tapped, waved or inserted into many different chip card readers.

What is EMV?

EMV is an acronym for the founding companies who came together to build a common specification:

Europay (now part of Visa), MasterCard, Visa. These companies formed EMVCo in order to

Contactless Chip:EMV Card & Reader

Contact Chip:EMV Card & Reader

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

5

administer international standards to champion global interoperability for chip-based payment

cards. This includes, but is not limited to, card and terminal evaluation, security evaluation and

management of interoperability issues. Today, there are EMV specifications based on contact chip,

contactless chip, common payment application (CPA), card personalization and tokenization. These

specifications and requirements were developed with a mission to increase payment security and

efficiency, and to ensure global interoperability amid payment ecosystems. A globally accepted EMV

card with an associated PIN empowers cardholders to take out cash from an ATM in Hong Kong, buy

lunch at a deli in New York, or buy a train ticket from a Deutsche Bahn kiosk in Munich — all with the

same card. EMV specifications regarding chip size, card size, electrical use, and security features all

help make this possible. Chip cards are already widely used in Europe, Asia and other regions. The

transition of the US payment card market from magnetic stripe cards to chip cards is referred to as

the US EMV migration.

EMVCo is the association that manages, maintains and enhances EMV chip card specifications.

EMVCo has expanded its sponsoring organizations and is comprised of six backing members —

American Express, Discover, JCB, MasterCard, UnionPay, and Visa — and supported by dozens of

banks, merchants, processors, vendors and other industry stakeholders who participate as EMVCo

Associates.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

6

Who will be affected by EMV migration?

Cardholders will have to adapt to new ways of interacting with ATMs and POS terminals. Consumers

using contact chip cards will have to insert their card for the duration of the transaction, and those

using contactless cards will have to tap or wave their card over the designated area. Also, depending

on how the chip card is configured and the capabilities of the POS terminal, cardholders may have to

verify they are the actual cardholder by entering a PIN instead of verifying by signature.

Card Issuers will have their operation costs go up, as the new cards are more expensive to produce

and replace. They will also have to work with acquirers to update their payment processing and

authentication infrastructures.

Merchants will have to upgrade and certify their POS terminals so that they can communicate with

chip cards. As mobile payments rise in popularity, more and more apps will adapt to enable mobile

phones to communicate with POS terminals. Today, there are many apps and mobile phones which

can communicate with POS terminals.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

7

When is migration happening? Now, slowly but surely, major card providers in the US are beginning to offer chip-based payment

cards. Some cards are requiring PIN entry for cardholder verification, and others are requiring a

signature for cardholder verification.

The US is the last major economy in the world to implement chip-based payment technology, and

in an effort to encourage EMV deployment, the US card brands have instituted a fraud liability shift

beginning October of 2015. This means that after October 2015, all parties that make an investment

in EMV technology will be protected from being financially liable for any potential fraud losses. In

2016 this will include ATMs for MasterCard branded cards, and in 2017 it extends to automated fuel

dispensers, and ATM transactions with Visa branded cards. The liability shift is NOT a mandate.

Merchant Migration requires upgrading and certifying their point of sale devices, and training their

cashiers to use the new payment method.

Card Issuer Migration requires providing their cardholders with chip cards and educating the issuer’s

employees and their customers about the chip cards, what they are capable of, and how to use

them.

Cardholder Migration requires consumers to apply for chip cards, or request chip cards from their

current card provider. Over time, cardholders will receive chip cards as part of new card issuance or

through the normal renewal process. Cardholders will also have to adjust to new methods of using

their card with card readers.

OCT 2017Automated Fuel

Dispenser Liability Shift

OCT 2015Merchant FraudLiability Shift

APRIL 2014Acquirer Compliance

Accept Chip-BasedPayments

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

8

Why migrate now?

EMV provides better protection for cardholders. Card fraud is a huge problem in the US, largely

due to the prevalence of magnetic stripe swipe cards, which are easy to counterfeit. EMV cards

remove most opportunities for card skimming, where a magnetic stripe is scanned without the

cardholder’s consent for fraudulent use. Opportunities for card transplant fraud, where stolen

card information from EMV markets is printed onto a magnetic stripe card and used in non-EMV

markets, will be greatly reduced as more markets embrace EMV technology. In the event that data

is stolen from an EMV card, or during a transaction initiated from an EMV card, the value of that

data for counterfeiting purposes is greatly limited. Mobile markets are also on the rise, and the

current transition to chip cards will make the next transition to mobile payments safer and easier by

protecting and enabling consumers.

Today, fraud risk is making headlines like never before. Recent notable retailer data breaches have

affected millions of American consumers, and have brought credit security issues to the forefront of

public debate. Thieves have successfully stolen customer card information by observing and taking

advantage of how data is stored and moved between different areas of the payment environment.

Valuable cardholder information can be compromised not due to one weak link in the transaction

cycle, but due to joint weaknesses in the current payment system as a whole.

EMV chip card ubiquity in the US will dramatically decrease the options fraudsters will have to use

stolen account data, and it will enable cardholders to embrace new ways of making payments by

protecting and informing them. Updating the US payment system infrastructure to support EMV

will take time, investment and careful planning. It will require merchants, issuers, acquirers and

processors to evaluate and update their current security precautions. EMV Migration will not correct

every weakness within the US payment system, but it is the first clear step in a long process of

ushering the payment business into the digital age.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

This chapter provides some historical background

on EMV payment standards, and outlines major

dates and deadlines to come.

EMV 101: MIGRATION TIMELINE

10

EMV 101: MIGRATION TIMELINE

1995Europay, MasterCard and Visa issue the first EMV specification

2001-05

In an eort to improve security, a larger retailer partners with Visa to push for more

smart chip cards to be used in the US. Eorts halt due to cost management setbacks

1999Europay is acquired by MasterCard

2002

JCB (Japan Credit Bureau) joins EMVco

2005EU mandates fraud liability shift, placing pressure on card issuers and merchants to migrate to EMV

2008

Fortune 1000 Financial processor company card data breach aects 134 million accounts

2009American Express joins EMVco

2010Global circulation of EMV cards hits 1 billion

2010UK credit card fraud rates at lowest since 1999

2011MasterCard and Visa mandate fraud liability shift in CanadaEMVco publishes EMV specifications version 4.3

MasterCard, Visa and Discover announce roadmaps to bring EMV to the US

2012

US accounts for 23% of global credit card transactions and 47% of global credit

fraud. Analysts blame the shift in fraud towards the US on the comparative lack

of security in magnetic strip cards and terminals vs. EMV cards and terminals

2013Discover and China Union Pay join EMVco

US acquirer processors and sub-processor service providers are required to support, accept and process smart chip transactions

Visa, Mastercard and Discover introduce merchant/acquirer regulations

2015US implements fraud liability shift so that the party that has made an investment in EMV deployment is protected from financial liability for fraud losses

2014

Large retail customer data breach aects over 100 million

cards. Attention on US EMV migration heightened during

the aftermath

2017US fraud liability shift mandate extends to fuel dispenser machines

Visa liability shift for ATMs

2019Projected EMV ubiquity in the US

EMV 101: MIGRATION TIMELINE

Loss per £100

FRAUD LOSS RATE UK-ISSUED PAYMENT CARDS

2000£0.00

£0.02

£0.04

£0.06

£0.08

£0.10

£0.12

£0.14

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

CHIP AND PINDEPLOYMENT

2004

Europay, MasterCard and Visa form EMVco

2016

MasterCard liability shift for

ATMs

23%

47%

US Share of Global Credit Transactions

US Share ofGlobal Credit Fraud

2014

All regional debit networks to enter into agreements

with MasterCard and Visa to integrate data routing

2014-2015Regional debit networks conduct testing and certification

This chapter provides a more in-depth look

at economies around the world where EMV

migrations are currently underway or are

complete. Experiences from other countries can

provide valuable insights for everyone involved in

the US EMV migration.

EMV 101: LESSONS LEARNED FROM GLOBAL MIGRATION

12

National Migration, Global Results

Today, EMV card technology has fully replaced traditional magnetic stripe cards in virtually all

developed countries except the US. Most large economies are either fully migrated to EMV standards,

or are somewhere along a migration path. Throughout every major country’s EMV migration, each

domestic policy change affected fraud landscapes both at home and throughout the world.

As the US payment ecosystem gears up for a smart card migration, it is valuable to look back at how

other large economies made the shift, and compare how different migration patterns and policies

have affected fraud rates around the world.

Fraud 101

When measuring fraud-prevention methods, especially EMV standards, it is highly important to consider the effects EMV policies have had

on different types of fraud, and to understand the different ways card fraud is measured. This chapter will discuss global trends following

EMV migrations for several different types of card fraud, and different methods for measuring it:

FRAUD RATES are measured in incidences. Either one

fraudulent transaction, or one cardholder affected by a

fraudulent transaction equals one incident. Fraud rate is a

relatively inaccurate and sometimes deceiving method of

measuring fraud, but it is the favored method by journalists

and surveyors for its consumer-focused mass appeal.

FRAUD LOSSES are measured in currency. This statistic

totals all the money lost by cardholders, issuers, acquirers

and merchants due to fraudulent transactions over a period

of time.

FACE-TO-FACE FRAUD OR CARD-PRESENT FRAUD

consists of a fraudster finding a card, stealing a card, or

counterfeiting a card and physically using it at a store.

CARD-NOT-PRESENT (CNP) FRAUD consists of a fraudster

obtaining cardholder information, and using it to perform

fraudulent transactions without the use of a physical card.

Often, CNP fraud is performed online.

CROSS-BORDER FRAUD is where a card issued in one

country is fraudulently used in another country.

LESSONS LEARNED FROM GLOBAL MIGRATION

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

13

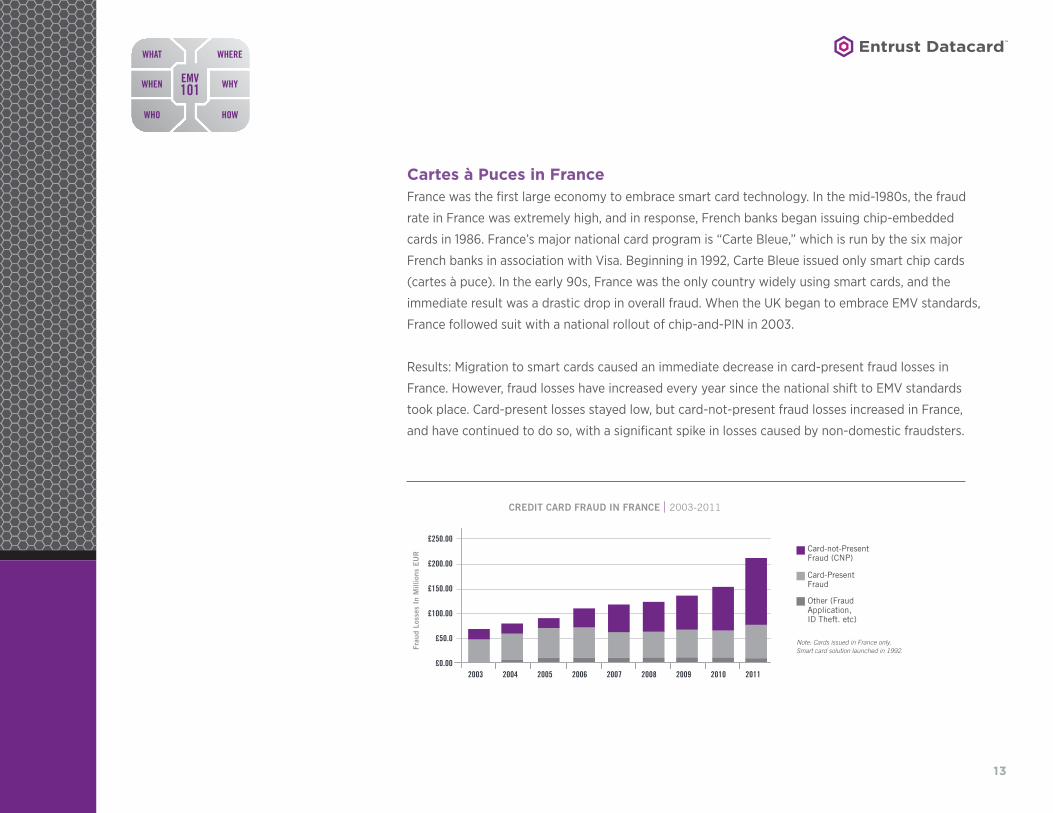

Cartes à Puces in FranceFrance was the first large economy to embrace smart card technology. In the mid-1980s, the fraud

rate in France was extremely high, and in response, French banks began issuing chip-embedded

cards in 1986. France’s major national card program is “Carte Bleue,” which is run by the six major

French banks in association with Visa. Beginning in 1992, Carte Bleue issued only smart chip cards

(cartes à puce). In the early 90s, France was the only country widely using smart cards, and the

immediate result was a drastic drop in overall fraud. When the UK began to embrace EMV standards,

France followed suit with a national rollout of chip-and-PIN in 2003.

Results: Migration to smart cards caused an immediate decrease in card-present fraud losses in

France. However, fraud losses have increased every year since the national shift to EMV standards

took place. Card-present losses stayed low, but card-not-present fraud losses increased in France,

and have continued to do so, with a significant spike in losses caused by non-domestic fraudsters.

CREDIT CARD FRAUD IN FRANCE 2003-2011

2003

Card-not-Present Fraud (CNP)

Card-Present Fraud

Other (Fraud Application, ID Theft. etc)

Note: Cards issued in France only.Smart card solution launched in 1992.

£0.00

£50.0

£100.00

£150.00

£200.00

£250.00

2004 2005 2006 2007 2008 2009 2010 2011

Frau

d Lo

sses

In

Mill

ions

EU

R

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

14

Chip and PIN in the United Kingdom Not far behind France, the UK was one of the first large economies to embrace EMV technology. The

banking industries in the UK and Ireland branded their migration efforts as “Chip and PIN” — “chip”

referring to the computer chip embedded into the new cards, and “PIN” referring to the personal

identification number that is required to authentically identify cardholders before each transaction

(requiring PIN authentication for a smart card purchase is an optional security feature, which

the UK largely favored.) After several successful trial programs launched in the mid-90s, APACS

(the Association for Payment Clearing Services) — a group of financial institutions and payment

companies — introduced a national EMV campaign in 2002, which gained serious traction in 2004. A

liability shift was put in place on Jan. 1st of 2005, and by the end of August 2006, the UK reached a

near-complete migration (99.8% of chip transactions were PIN-verified.)

Results: Overall, fraud losses in the UK have seen a significant decline. Card-present fraud loss has

decreased dramatically and stayed low, however, card-not-present (CNP) fraud loss has seen steady

increases since the EMV rollout. A large portion of UK CNP fraud is cross-border fraud, where UK-

issued cards are used in payment networks that do not require PIN verification.

CREDIT CARD FRAUD RATES IN THE U.K. 2001-2012

2006

EMV liability shift

0%

10%

20%

30%

50%

40%

70%

60%

2007 2008 20092001 2002 2003 2004 2005 2010 2011 2012

Card-not-Present

CounterfeitCard-Present

Lost/StolenCard-Present

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

15

EMV in AustraliaAustralia’s EMV shift resembles the US migration in its gradual and reluctant approach. Both

countries have seen massive spikes in fraud from abroad, due to the stricter EMV policies adopted

throughout Europe, and both economies have a complex payment ecosystem based on magnetic

stripe cards. Major financial institutions in both Australia and the US act without much influence

from a common governing body. Australian migration slowly began in 2007, and in 2009, a major

industry deadline to implement PIN-only transactions was missed due to fears over consumer

preparedness. Alongside the US, Australia has lately suffered a disproportionate share of global

fraud. Liability shifts were set for 2012 and 2013, and signature verification is currently being phased

out — with good results, so far.

Results: One result of the gradual migration approach in Australia is that positive results have been

modest in some categories, and non-existent in others. Card-present fraud is slightly down (about a

15% decrease from 2008-2010), but CNP fraud has surged (a 70% increase during the same period).

CREDIT CARD FRAUD IN AUSTRALIA 2006-2012

2006

Card-not-Present (CNP)

Card-Present

EMV Issuance ramped up

£0.00

£50.0

£100.00

£150.00

£250.00

£200.00

£350.00

£300.00

2007 2008 2009 2010 2011 2012

Frau

d Lo

sses

In

Mill

ions

AU

D

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

16

Chip Cards in CanadaInterac, the national PIN-debit network in Canada, allowed major banks and transaction processors

to work together throughout the migration process, which began in 2007 with a pilot program

launched in Ontario. This pilot program offered important insights, and is lauded as one reason why

Canada’s migration went faster and smoother, compared to other countries. The trial run alerted the

national migration effort to the lag in consumer readiness for contact cards — which was remedied

by embracing NFC-powered contactless mobile payments.

Results: Canada has seen triumphant results in reducing card-present fraud losses, especially those

produced by card skimming and cloning. In March 2013, fraud loss from skimming was at its lowest

since 2003. Like other migrated nations, however, Canada has also seen a spike in CNP fraud.

CREDIT CARD FRAUD IN CANADA 2008-2010

2008$0.00

$50.0

$100.00

$150.00

$250.00

$200.00

2009 2010

Card-not-Present

Card-Present

Fraud losses from counterfeit and lost or stolen credit cards is down 30% since the national rollout of chip-and-PIN in 2008.

Since the national rollout of chip-and-PIN in late 2008, card-not-present fraud on Canadian-issued credit cards is up 37%.Fr

aud

Loss

es I

n M

illio

ns C

AD

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

17

Lessons Learned

France’s experience displays an exaggerated trend seen in most countries after EMV migration: a

dramatic decrease in card-present fraud, followed by a significant move from card-present fraud

to card-not-present fraud alongside a shift from domestic fraud to cross-border fraud. The French

EMV migration shows us that EMV standards are very effective at eliminating certain types of

fraud, but are not a solution to eliminate fraud completely. France’s migration story also highlights

the importance of EMV ubiquity for maximum security and interoperability. If all economies had

migrated when France did, the opportunity for cross-border fraud would have been unavailable.

In the UK, PIN cardholder verification was an excellent policy for reducing card-present transaction

fraud, but fraudsters will look elsewhere for vulnerabilities, and a spike in card-not-present fraud will

likely follow a switch to safer cardholder verification measures.

Australia’s migration proves that the more you wait around, stall or disregard industry deadlines,

the larger the target on your back grows for fraudsters around the globe. As other economies crack

down on pushing for modernized cardholder verification methods, outdated methods become

weaker and weaker in comparison.

Canada can teach the US that — whether they are from a domestic pilot program, or from a deep

analysis of other country’s migration attempts — gathering as many EMV migration insights as

possible is an absolute must. Consumer and merchant education is of great importance for a smooth

migration. If brands come together and agree on common timelines, merchants will be more likely to

embrace EMV earlier on. Working together can greatly reduce unexpected migration setbacks.

Sources:

http://blog.unibulmerchantservices.com/

adoption-of-chip-based-credit-cards-pushes-up-e-

commerce-fraud/

http://digitaltransactions.net/news/story/Canada-

Puts-Down-Chip-Card-Roots

http://news.alaric.com/industry-news/payments/

closing-the-emv-gap-in-australia/

http://en.wikipedia.org/wiki/Chip_and_PIN

Chip-and-PIN: Success and Challenges in

Reducing Fraud

Douglas King

Retail Payments Risk Forum Working Paper

Federal Reserve Bank of Atlanta, January 2012

EMV Adoption and Its Impact on Fraud

Management Worldwide: A whitepaper prepared

exclusively for FICO

Mercator Advisory Group, Jan 2014

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

18

National EMV migration began in

2008

Between 2008 and 2010, fraud losses from lost/stolen

cards fell over

30%

CANADANational EMV

migration began in

2004

Between 2004 and 2010, card-present fraud fell

69%

UK

National EMV migration began in

2004

Between 2004 and 2010, card-present fraud fell

50%

FRANCE

From 2004-2010, the fraud rate

increased by over

70%Between 2007 and 2010, the

portion of fraud due to card-present fraud

increased by

20%

US

National EMV migration began in

2008

Between 2008 and 2010, card present fraud fell

15%

AUSTRALIA

EMV-Enabled Cards and Terminals by Region

Generally, a migration to EMV standards results in

a large reduction in card-present fraud.

Chip-enabled cards are very di�cult to physically

reproduce or misuse, so stolen and counterfeit

cards become significantly less valuable to

fraudsters in EMV dominant payment ecosystems.

This trend causes physical card fraud to move to

countries where EMV is less dominant.

One of the biggest advantages of EMV is the

convenience of global interoperability for card users.

For a cardholder abroad, performing a transaction

with a non-EMV payment card in a region where EMV

is dominant is more di�cult, slower to process, and

sometimes not an option at all.

41.1%CARDS

76.7%TERMINALS

CANADA, LATIN AMERICA & THE CARIBBEAN

94.4%CARDS

84.4%TERMINALS

EUROPE ZONE 1

68.1%CARDS

14.5%TERMINALS

EUROPE ZONE 2

75.9%CARDS

20.6%TERMINALS

51.4%CARDS

28.2%TERMINALS

EMV 101: EMV ADOPTION RATES BY REGION

This chapter takes a look at how EMV migration

will affect each party within the current

US payment ecosystem.

EMV 101: THE KEY PLAYERS

20

Key Player: The Industry Payment Network

The major US payment networks (Visa, MasterCard, American Express and Discover) are the main

drivers of the EMV migration. Europay (since acquired by MasterCard), MasterCard and Visa jointly

conceived the EMV specification, and have played major roles in EMV migrations all over the world.

The payment networks partner with many players throughout the US payment ecosystem, and

therefore are the ultimate champions of interoperability and cooperation. Their wide influence

makes them the go-to leaders in this large national migration push.

Key Player: The Cardholder

Cardholders will begin to receive new EMV chip cards in the mail as replacement cards to their

current magnetic stripe cards. It will be critical for issuers to educate their cardholders on how to

use the new cards at point-of-sale (POS) terminals. Other national EMV migrations (those in Canada

and Australia, for example) have experienced set backs and even missed big industry deadlines due

to concerns about cardholder readiness.

After the adoption of EMV, the way consumers physically use payment cards will be different. Not

all smart cards are the same; but they can be easily categorized into three main groups — contact

cards, contactless cards and dual interface cards. With contact chip cards, the chip is embedded into

the actual cardstock material, under a contact which is physically visible. Instead of swiping, contact

chip cards are inserted into the POS terminal for the duration of the transaction. The cardholder will

typically be required to verify their identity one of two ways: by entering in a PIN number, which

must be memorized, or by providing a signature. With contactless chip cards, the chip is embedded

into the actual cardstock material and is not physically visible. Contactless chip cards are tapped or

waved over or near a receptor space marked on the POS terminal to complete the transaction, which

only takes a moment. Cardholders might be required to verify identity by entering their signature

for contactless chip transactions. Many times now verification will be required. Dual interface

KEY PLAYERS

BANK

0000 0000 0000 0000

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

21

cards include both contact and contactless technologies and can therefore be used to complete

transactions through either inserting the card or waving the card over the POS terminal. Not all card

programs will require that their cardholders use a PIN to verify their identity, but in terms of overall

security, PIN verification is the best practice.

As the US begins its shift to EMV, all of the smart chip cards issued will also have a magnetic

stripe on the back. This way, should a cardholder encounter a POS terminal that has not yet been

upgraded by the merchant to support EMV; the cardholder can simply swipe their card the way we

do today. One of the primary goals of the switch to EMV standards is interoperability. We want to

enable all payment cards to safely work with all POS terminals across the globe.

Key Player: The Card Issuer

Financial card issuers are vital to a smooth EMV migration. Throughout the entire migration process,

educating cardholders and merchant clients about the EMV system and its standards will fall

largely on issuers’ shoulders. Becoming well versed in EMV specifications and migration education

strategies is in every issuer’s advantage.

EMV will not only change the way we physically use cards; it will change the way card programs

run behind the scenes as well. Each step in the payment process — from a card starting out as a

plain piece of plastic, to being a list of successful transactions on a statement — will include new

security features and processes. For each of those steps, issuers will need to evaluate their current

technologies and infrastructures, and invest in the necessary upgrades including hardware and

software to manage the chip card personalization, issuance, delivery and operational processes.

BANK

0000 0000 0000 0000

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

22

Key Player: The Merchant

To most merchants, the switch to EMV seems like a costly technology upgrade that their businesses

will not directly benefit from. POS terminals will need to be upgraded to meet EMV specifications,

and back-end systems must be updated and certified to be able to accept payments from the new

cards. Employees will also need to be trained to use the new technology.

These integral steps come at no small cost, and generally, merchants are the least eager key

players to migrate. Financial pressures such as card brand-enforced fraud liability shifts aim to get

merchants more on board. EMV upgrades will directly benefit their customers, which makes them a

good investment; however, EMV can also introduce many new (and potentially lucrative) payment,

loyalty, marketing and mobile commerce opportunities into the shopping landscape — possibilities

that merchants should assess and leverage early on to stay competitive in the transforming

payment market.

Key Players: The Card Manufacturer and The Software Developer

It’s up to software developers and card manufacturers to make EMV cards as efficiently and cost-

effectively as possible. Applications for the card chips, POS terminals, processors, ATMs and mobile

devices will have to be written and maintained to ensure secure, reliable interoperability across

channels to meet EMV standards.

BANK

0000 0000 0000 0000

BANK

0000 0000 0000 0000

BANK

0000 0000 0000 0000

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

23

Key Players: The Acquirer & Payment Processor

The US migration to EMV means that the entire industry is taking some time to evaluate current

payment processing and authentication infrastructures, in order to make plans and upgrades for

meeting EMV specifications. Because the market is on the cusp of a major transition, industry

leaders like Visa and MasterCard are spearheading efforts that can make the payment ecosystem

even more secure, on top of the security benefits that will come with EMV implementation. One

example of this is the possible implementation of tokenization technologies alongside EMV

upgrades. Tokenization is a practice that removes important cardholder data (i.e. the PAN) from the

servers of retailers, while still allowing them to access it if required (for a return, or a subscription).

Tokenization removes the incentive for hackers to steal card information in the thousands from

retailers, because the tokenized data which the hacker might capture would be meaningless to

them. To learn more about it, read our next chapter.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

EMV 101: BEHIND THE TRANSACTION

This chapter traces the path that payment data

will take under the new EMV standards.

25

The adoption of EMV payment systems has proven to be a worthy card fraud deterrent for

card-present transactions in every region where it has been embraced. In 2004, the UK

launched a vigorous, nationwide “Chip and PIN” card program, and 2010 marked a ten-year

low in UK payment card fraud losses. In recognition of positive EMV fraud-reduction rates

elsewhere, the major card brands have declared EMV as one way to move forward and secure

the US payment infrastructure. The US is the largest payment market where EMV has not

been adopted, making it a target for card fraud opportunities that are not viable elsewhere.

Anatomy of an EMV Chip Card Payment Transaction

There are three distinctive aspects of an EMV transaction which if implemented helps

secure different aspects of that transaction: card authentication, cardholder verification

and transaction authorization. EMV payment processes can happen online (processes are

performed by computers elsewhere on the payment network) and/or offline (processes are

performed between the point of sale (POS) terminal and the card’s chip).

EMV 101: BEHIND THE TRANSACTION

Loss per £100

FRAUD LOSS RATE UK-ISSUED PAYMENT CARDS

2000£0.00

£0.02

£0.04

£0.06

£0.08

£0.10

£0.12

£0.14

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

CHIP AND PINDEPLOYMENT

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

26

ISSUER

PAYMENTBRAND

24

AR

QC

AR

PC

AR

QC

AR

PC3

4

4

1

5

PAYMENTTERMINAL

Card authentication ensures that a payment card is not counterfeit. There are two ways a chip card

can be verified for authenticity; online or offline.

Online card authentication transactions carry dynamic data that is sent to the card issuer’s

authorization system which checks the authenticity of the card. Offline card authentication uses

chip-stored, risk assessment logic to determine if a card is authentic.

Cardholder verification ensures that the card user is the legitimate cardholder. Cardholder

verification requests that the card user provide either a signature, a valid PIN (Personal

Identification Number), or in some cases (e.g. contactless transactions) no verification is required.

Like card authentication techniques, PINs can be stored for verification either online in an issuer

authentication server, or offline on the chip.

Transaction amount authorization ensures that a purchase does not exceed the cardholder’s issued

credit limit and is within other specified limits (e.g. domestic or international purchases). As with

card authentication and cardholder verification, this authorization can also be processed online or

offline. Offline risk assessment logic offers chip cards unique protections against fraud and credit

overruns.

Within the current US payment system, merchants are the primary targets for fraudsters, who covet

the large amounts of cardholder data used, moved and stored through merchant POS devices,

networks and central servers. A truly formidable payment security standard will protect sensitive

cardholder data in each of its three states: data at rest, data in use and data in motion.

1. Based on issuer qualifications, risk assessment is performed by both the POS terminal and the chip on the card. A dynamic ARQC (Authorization Request Cryptogram) is written.

2. The ARQC is sent via the acquirer to the payment brand.

3. The payment brand then sends the ARQC to the issuer.

4. The issuer makes an authorization decision to validate the request, and responds with an ARPC (Authorization Response Cryptogram), which goes through the same channels back to the point of sale device.

5. If the chip’s request is validated, the POS terminal will request verification from the cardholder in the form of a signature, entry of a PIN, or in some cases no verification.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

27

Within a payment ecosystem, data at rest is cardholder information stored in central servers by

card issuers, for card functionality and reissuance, but also by merchants, for use in refunds, returns,

recurring charges and sales reports. Data at rest can be protected by tokenization, a process where

a payment card’s personal account number (PAN) is replaced with surrogate “token” values, and

stored with reduced risk. A stolen or breached token number cannot be used to perform an outside

transaction, but can be used by the merchant for returns, future charges, etc.

Data in use refers to the data that occupies a computer’s (or POS terminal’s) RAM (Random

Access Memory) at any given time. This is the space a computer uses to store data that it will

need to perform a task. Data in motion is data being sent from one point in a payment network to

another. Data in use and in motion can be protected with encryption, where computer algorithms

transform information from readable plain text to unreadable cipher text. Encryption does not

altogether prevent information theft, but it does reduce the likelihood that the thief would ever be

able to successfully use the stolen information. To decrypt the message, the reader must use a key

algorithm, without which the data cannot be used.

Encryption and tokenization are two security measures that collaborate with and complement EMV

security standards for protecting cardholder data in every stage of its use cycle.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

EMV 101: CHECKLIST

This chapter outlines a plan of action for a

successful EMV migration.

29

Migration Action Checklist

EMV is the future of payment; and migrating your offerings to include EMV is key to

remaining relevant in the payment card market. We want to help you capitalize on the

changes ahead. Not sure where to begin? Start by taking a phased approach to your

migration.

Phase one of any EMV migration should focus on getting familiar with EMV standards

at every level. There’s a whole new landscape of technologies, security features, best

practices and interoperability standards out there, and understanding all of your options and

constraints is key. Solid comprehensive knowledge of EMV can be leveraged to make smarter

strategic decisions about how and when to migrate.

This strategic planning makes up the focus of phase two. Evaluate your current card portfolio

and technology infrastructure. Which programs would benefit from EMV first? Which card

layouts are affected? What are your budget constraints leading up to the liability shift? Are

your solutions EMV-ready?

Phase three is all about action. It’s the time to make all the necessary upgrades to start

bringing the benefits of EMV to your cardholders. If you’re an existing Datacard® CardWizard®

software customer, use this checklist as your phase three itinerary, and Entrust Datacard as

your trusted guide. If you’re migrating central issuance operations or starting from scratch,

you’ll find the answers you need from one of our global EMV consultants.

EMV 101: MIGRATION ACTION CHECKLIST

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

30

1. Assess your technology infrastructure

Perform an audit of your existing hardware and software versions. EMV card programs

require the latest upgrades to prepare for everyday issuance.

• What version of Datacard® CardWizard® software are you running?

• What Windows operating system do you have installed?

• How many remote locations do you need to track and does every device you own have a

license for EMV card personalization?

2. Review your card gallery

Many card designs need to be altered to accommodate the placement of the chip. EMV

standards will require redesigns and layout changes within your card setups.

• What card designs will you carry over for your new program?

• How will the chip impact existing designs?

3. Evaluate your data center Migrating to EMV card issuance will likely introduce changes within your IT infrastructure.

EMV card issuance might require changes to your host and/or switch environment to

handle the additional data, security protocols and processing.

• Will EMV-related data elements be transmitted between your host and CardWizard®

software?

• Will CardWizard® software send EMV-related data to your switch?

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

31

4. Determine if you have the right Hardware Security Module (HSM)

Ensure the latest version of CardWizard® software works with your HSM since this is a

critical step in the production process.

• What is the model of your HSM?

• Is it internal or external?

• Is it FIPs Certified?

5. Upgrade your instant issuance systems

Not all instant issuance systems are EMV-ready. EMV issuance will require an instant

issuance system equipped with a contact and contactless smart card encoder.

• Which card personalization systems do you currently use?

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

EMV 101: GLOSSARY OF TERMS

This chapter defines a set of standard terminology

and enable clear understanding of all things EMV.

33

SOURCES

http://blog.unibulmerchantservices.

com/adoption-of-chip-based-

credit-cards-pushes-up-e-

commerce-fraud/

http://digitaltransactions.net/news/

story/Canada-Puts-Down-Chip-

Card-Roots

http://news.alaric.com/industry-

news/payments/closing-the-emv-

gap-in-australia/

http://en.wikipedia.org/wiki/Chip_

and_PIN

Chip-and-PIN: Success and

Challenges in Reducing Fraud

Douglas King

Retail Payments Risk Forum

Working Paper Federal Reserve

Bank of Atlanta

January 2012

EMV Adoption and Its Impact on

Fraud Management Worldwide:

A whitepaper prepared exclusively

for FICO, Mercator Advisory Group

Jan 2014

INDUSTRY TERMS

Acquirer

The acquirer is the party recognized by the network as the financial sponsor for a merchant

(typically a regulated financial institution like a bank). The network holds the acquiring

processor financially responsible for transactions processed by the merchant and helps ensure

that the merchant operates under the rules laid out by the network. Examples: Bank of America

Merchant Services, First Data, Wells Fargo, Vantiv, SHAZAM/ITS Inc.

Acquiring Processor

Acquiring Processors are third-party service providers that acquire and process payment

transactions for merchants, manage the relationship with the global and regional payment

networks on the merchant’s behalf (including interchange qualifying, chargeback disputes and

fees to networks and issuers), and manage the transaction database. The acquiring processor

connects merchant transactions to payment networks by (1) providing the POS device; and/or

(2) securely routing the transaction from the POS device or from the POS payment gateway to

the payment network; (3) managing transactions from authorization to clearing to settlement.

Application Authentication Cryptogram (AAC)

A cryptogram generated by the card at the end of offline and online declined transactions.

It can be used to validate the risk management activities for a given transaction.

GLOSSARY OF TERMS

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

34

Application Cryptogram (AC)

A cryptogram generated by the card in response to a

GENERATE AC command, providing the card decision on

the transaction. The AC is used to validate that the card has

genuinely generated the response.

The three types of cryptograms are Transaction Certificate

(TC), Authorization Request Cryptogram (ARQC), and

Application Authentication Cryptogram (AAC). The

creation and validation of the cryptogram enables dynamic

authentication.

Application Identifier (AID)

Application Identifiers are data labels that differentiate

payment systems and products. The card issuer uses the data

label to identify an application on the card or terminal. Cards

and terminals use AIDs to determine which applications are

mutually supported, as both the card and the terminal must

support the same AID to initiate a transaction. Both cards and

terminals may support multiple AIDs. An AID consists of two

components, a Registered Application Identifier (RID) and a

Proprietary Application Identifier Extension (PIX).

Authorization Response Cryptogram (ARPC)

Used during online issuer authentication, the ARPC is

a cryptogram generated by the issuer and sent in the

authorization response back to the terminal. The terminal

sends this cryptogram to the card, which allows the card to

verify the validity of the issuer response, and go ahead with

the transaction. (See ARPCs in action in EMV 101: Behind the

Transaction)

Authorization Request Cryptogram (ARQC)

This cryptogram is also used during online card authentication.

It is generated by the card and sent to the issuer in the

authorization or full financial request. The issuer validates the

ARQC to ensure that the card is authentic and card data was

not copied from a skimmed card. (See ARQCs in action in EMV

101: Behind the Transaction)

Cardholder Verification Method (CVM)

Different cards use different methods to authenticate that

the person presenting the card is the valid cardholder. EMV

supports four CVMs: offline Personal Identification Number

(PIN) (offline enciphered & plain text), online encrypted PIN,

signature verification, and no CVM.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

35

Certificate

An electronic document binding some pieces of information

together, such as a user’s identity and public encryption key.

The digital certificate is used to prove to the data recipient the

origin and integrity of the data.

Certificate Authority (CA)

A trusted central administration that issues and revokes

certificates and is willing to act as a guarantor for the identities

of those to whom it issues certificates and their association

with a given key.

Certificate Authority Public Key (CAPK)

In order to support data authentication or offline enciphered

PIN, the terminal must store one or more public keys for each

RID. When required, the card will supply a CAPK index which

is used to identify which of these keys should be used for that

transaction.

Contact Chip Card

A chip card is a card that communicates with a reader through

a contact plate. The plate must come into contact with a

terminal, usually through a chip reader into which the card is

inserted. Communication is defined by ISO 7816.

Contactless Chip Card

A chip card that communicates with a reader through a radio

frequency interface, usually through a wave or tap of the card

on the designated area on the terminal. A contactless chip card

will have an antennae embedded in the card’s plastic.

Data Encryption Standard (DES)

Data Encryption Standard is a symmetric-key algorithm for

encryption of electronic data.

Dual Interface Chip Card

A chip card that has both contact and contactless interfaces,

enabling a payment transaction with either interface.

“Dynamic” vs. “Static”

“Dynamic” data has the ability to change or update. For

example, a dynamic card security code changes for each

transaction. “Static” or “persistent” data is unchangeable.

For example, the personal account number programmed

into a smart chip card cannot be changed after the card is

personalized.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

36

Electronically Erasable Programmable

Read-Only Memory (EEPROM)

EEPROM is digital memory that can be erased and reused,

but does not require electrical power to maintain data.

It is used to store information that will change, such as

transaction counters. It is possible to load new data elements

and applications into EEPROM after a card has been

issued. Generally after personalization and issuance, limited

application data can be updated. This is linked to card

security requirements.

EMV Migration Forum (EMF)

The EMV Migration Forum is an independent, cross-industry

body created by the Smart Card Alliance to address issues

that require broad cooperation and coordination across many

constituents in the payments space to promote the efficient,

timely, and effective migration to EMV-enabled cards, devices,

and terminals in the United States.

EMV (Europay, MasterCard, and Visa)

Developed by Europay, MasterCard, and Visa, EMV refers to a

body of specifications set to ensure interoperability between

payment chip cards and terminals. Formally known as the EMV

Integrated Circuit Card Specifications for Payment Systems and

owned by EMVCo.

EMVCo

EMVCo was formed in February of 1999 by Europay

International, MasterCard International, and Visa International

to manage, maintain, and enhance integrated circuit card

specifications for payment systems. EMVCo is currently, and

equally, owned by American Express, Discover, JCB, MasterCard

Worldwide, Union Pay and Visa, Inc.

GlobalPlatform

A cross-industry membership organization created to advance

standards for multiple application smart card growth. A major

goal of GlobalPlatform is the definition of specifications and

infrastructure for multi-application smart cards, including cards,

terminals and back-end host systems. The GlobalPlatform

Specifications are based on the Open Platform Specifications,

which were donated to the consortium by Visa.

International Standards Organization (ISO)

The ISO is a global institution that maintains over 13,000

international standards for business, government and society.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

37

Issuer

Issuers are the entities that issue payment cards to customers

and perform many activities that could include, but are not

limited to, the following list. It is important to note that the

issuer may choose to outsource some, or all, of these activities:

• Cardholder customer service

• Data preparation

• Configuration set-up

• Fulfillment of personalized chip card, with all paper inserts;

preparation for mailing to customer

• Define card profile, including risk parameters

• Receive and manage card records and keys to form a

personalization record

• Generate personalization script

• Key management activities for EMV, CVV/CVC, and PINs

between card manufacturer and personalization bureau and

between issuer and personalization bureau.

Issuer Action Codes (IACs)

IACs are codes placed on the card by the issuer during card

personalization. These codes indicate the issuer’s preferences

for approving transactions offline, declining transactions offline,

and sending transactions online to the issuer based on the risk

management performed.

Issuing Processor

Issuing processors facilitate card issuance activities on behalf

of an issuer, such as process payment transactions, card

enrollment, preparing and sending the card personalization

information to the card vendor, and maintaining the cardholder

database. The issuer processor may provide other ancillary

services as well (e.g., web front-end administrative and

cardholder account management applications, customer

service, settlement and clearing, chargeback processing)

Liability Shift

When card fraud occurs, one party involved in the transaction

(the cardholder, merchant, issuer, processor, etc.) is found

liable, or at fault. A liability shift is a change in the rules that

guide which party is liable for card fraud, should it occur. Each

brand defines the rules around their liability structure.

Magnetic Stripe Card

These plastic payment cards use a band of magnetic material

to store data. Data is stored by modifying the magnetism of

magnetic particles on the magnetic material, which is read by

“swiping” the magnetic stripe through a mag stripe reader.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

38

Near Field Communication (NFC)

NFC is a standards-based wireless communication technology

that allows data to be exchanged two ways between devices

that are a few centimeters apart. NFC-enabled mobile phones

incorporate smart chips (called secure elements) that allow

the phones to securely store the payment application and

consumer account information and to use the information as a

“virtual payment card”.

“Offline” vs. “Online”

In the context of an EMV transaction, “offline” refers to actions

and processes that are performed by the card’s chip and the

point of sale terminal alone, using applications stored on one/

both devices. An “online” action or process includes data that is

sent out to other computers managed by payment processors,

issuers, or card brands.

Payment Card Industry Data Security

Standard (PCI DSS)

PCI DSS is a framework developed by the Payment Card

Industry Security Standards Council for developing a robust

payment card data security process — including prevention,

detection and appropriate reaction to security incidents.

Payment Network

A payment network provides POS and ATM services for

credit, debit, ATM and prepaid card issuers and corresponding

transaction acquirers. It establishes participation requirements,

operating rules and technical specifications under a common

brand(s) for the purpose of receiving, routing, securing

authorization for, settling and reporting domestic and

international payment transactions. Each payment network

determines the types of transactions, payment devices and

terminals that are permitted in its respective network.

Personalization

Personalization is the process by which the elements specific

to the issuer and cardholder are added to the payment card’s

magnetic stripe and/or chip.

Personal Account Number (PAN)

Often referred to as the primary account number, or the bank

card number. The PAN is often embossed onto the front or

back of a credit or debit card. The PAN is commonly 16 digits,

but can be up to 19 digits in length.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

39

Personal Identification Number (PIN)

A PIN is an alphanumeric code of 4 to 12 characters that is

used to identify cardholders at a customer-activated PIN

pad. PINs can be verified “online” or “offline”. Online PIN

verification occurs when the PIN is securely transmitted to an

issuer’s authorization system during a transaction, with that

authorization confirming whether or not the entered PIN is

correct. Offline PIN verification occurs between the chip and

the POS terminal.

Point of Sale (POS)

A point of sale terminal is a machine where card-present credit

transactions occur. POS terminals come in many varieties, and

are often embedded into automated vending machines.

Random Access Memory (RAM)

RAM is a direct-access form of computer storage. When data is

required to perform a computational task it is moved into RAM

for the duration of the task.

Read Only Memory (ROM)

ROM is permanent memory that cannot be changed once it is

programmed. It is used to store chip operating systems and

permanent data.

“Static” vs. “Dynamic”

“Static” or “persistent” data is unchangeable. For example, the

personal account number programmed into a smart chip card

cannot be changed after the card is personalized. “Dynamic”

data has the ability to change or update. For example, a

dynamic card security code changes for each transaction.

Transaction Certificate (TC)

TCs are cryptograms generated by the card at the end of all

approved transactions. The cryptogram is the result of card,

terminal, and transaction data encrypted by a DES key. The

TC provides information about the actual steps and processes

executed by the card, terminal, and merchant during a given

transaction and can be used during dispute processing.

Triple DES (TDES, 3DES)

TDES is a sophisticated implementation of DES, in which the

procedure for encryption is the same but repeated three times.

First, the DES key is broken into three sub keys. Then the data

is encrypted with the first key, decrypted with the second key

and encrypted again with the third key. Triple DES (sometimes

abbreviated TDES or 3DES) offers much stronger encryption

than DES.

EMV101

WHAT

WHEN

WHO

WHERE

WHY

HOW

©2015 Entrust Datacard Corporation. All rights reserved.

CONNECT WITH US EVERYWHERE

www.datacard.com/emv-solutions