Embed Size (px)

Citation preview

Empowering Tomorrow’s Consumers

Consumers International World Congress 2011

5 May Hong Kong

World BankGlobal Program on Consumer Protection & Financial Literacy

Sue RutledgeGlobal Coordinator

o Consumer rights awarenesso Financial institutions (or financial industry associations)

could prepare a simple, easy-to-understand brochure about the consumer's legal rights regarding remittances

o Consumer disclosureo Financial supervisory agency could ensure that

comparable information is made available to consumers

o For example, collecting from financial institutions their standard pricing for various types of remittances

o Data should be publicly available in newspapers and internet

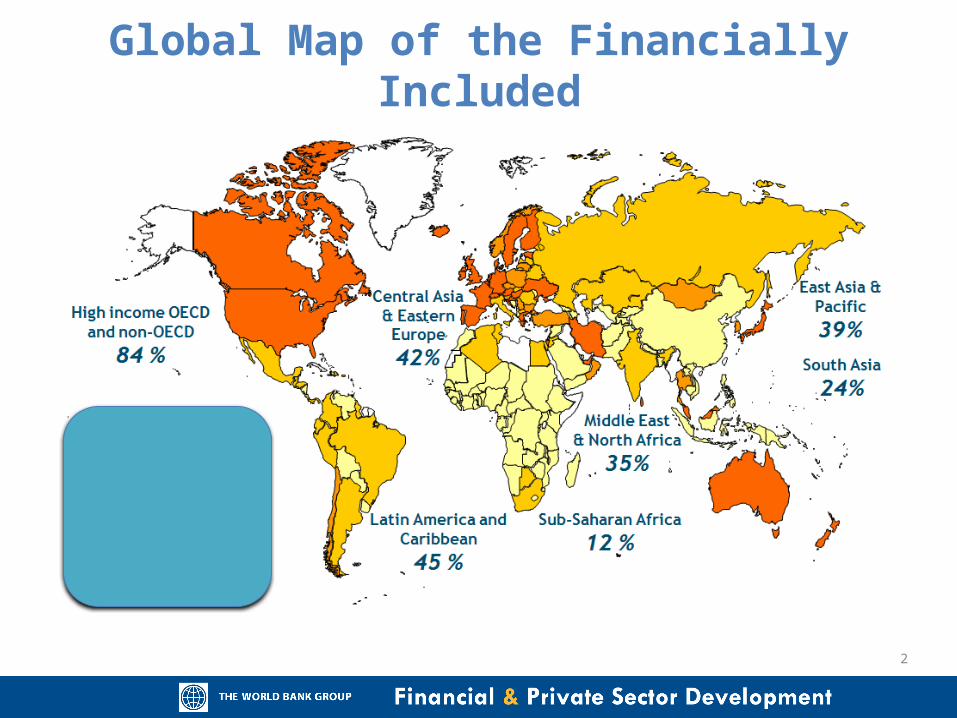

Global Map of the Financially Included

2

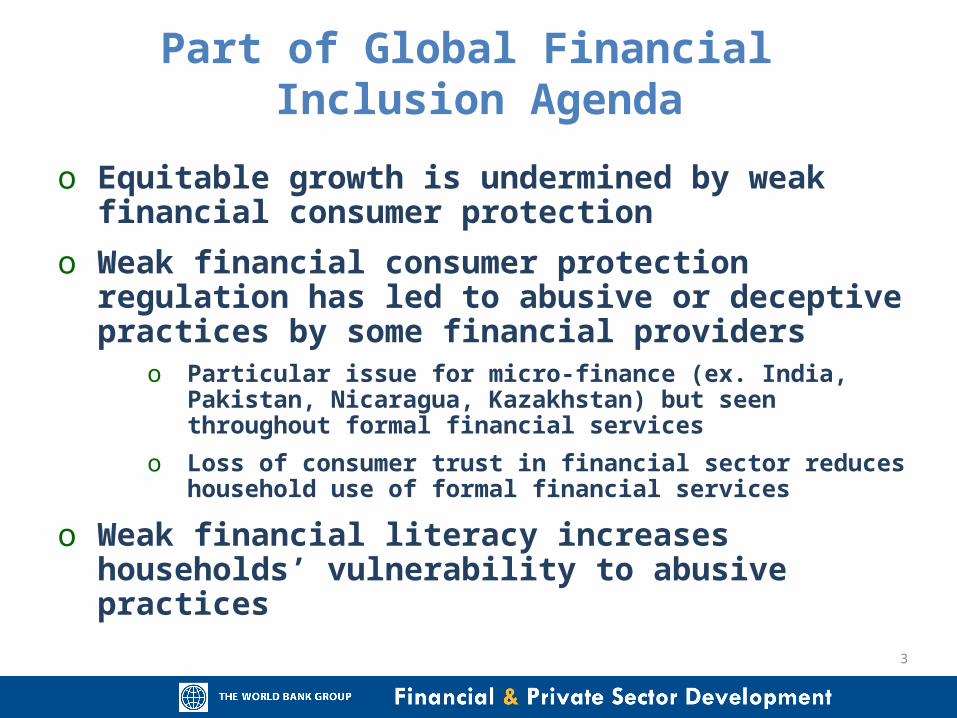

o Equitable growth is undermined by weak financial consumer protection

o Weak financial consumer protection regulation has led to abusive or deceptive practices by some financial providers

o Particular issue for micro-finance (ex. India, Pakistan, Nicaragua, Kazakhstan) but seen throughout formal financial services

o Loss of consumer trust in financial sector reduces household use of formal financial services

o Weak financial literacy increases households’ vulnerability to abusive practices

Part of Global Financial Inclusion Agenda

3

o Banking – Precondition of effective banking supervision

o Deposit insurance – Core principle

o Insurance – Core principle

o Securities – Core principle

o Private pensions - Main objective

o International remittances – General principle

o Statutory objective for financial supervisory agencies worldwide:o e.g. Canada, Colombia, Ireland, Malaysia, Singapore, South Africa,

Sweden, UK, US

Part of Global Financial Regulation & Supervision Agenda

4

o Launched Global Program on Consumer Protection and Financial Literacy

o Drafted Good Practices on Financial Consumer Protection as assessment methodology

o Published Working Paper -- Consumer Protection and Financial LIteracy: Lessons from Nine Country Studies

o Member of Financial Stability Board Consultative Group on Financial Consumer Protection

o Member of OECD Task Force on Financial Consumer Protection

o Public feedback tool: feedback.consumerprotection.worldbank.org

o Website: www.worldbank.org/consumerprotection

World Bank Contribution

5

6

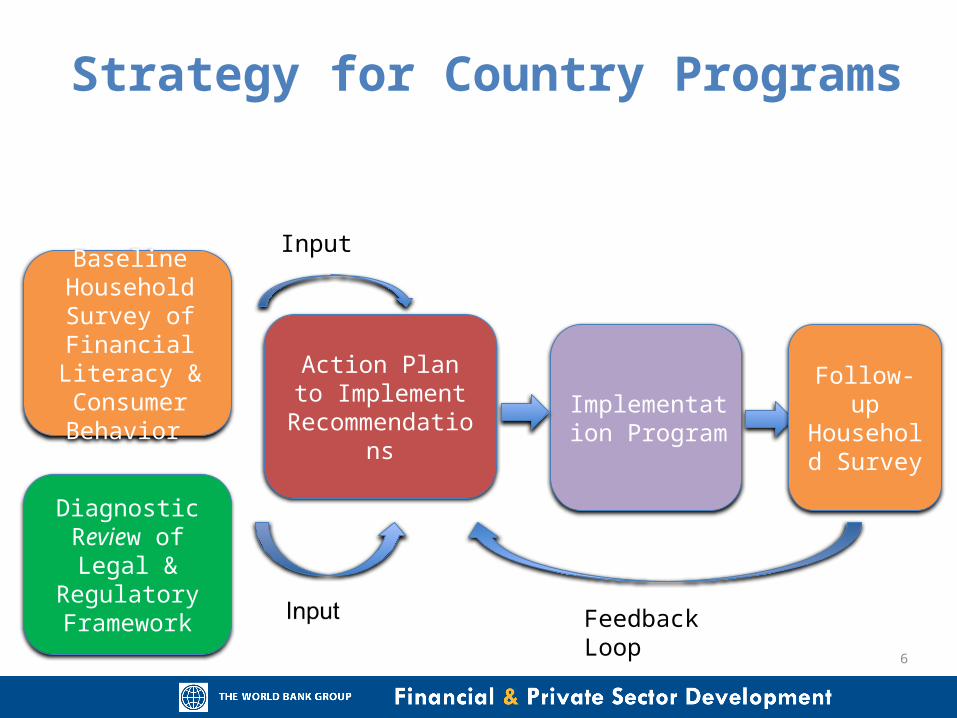

Strategy for Country Programs

Baseline Household Survey

of Financial Literacy & Consumer Behavior

Action Plan to Implement

Recommendations

Diagnostic Review of Legal

& Regulatory Framework

Implementation Program

Follow-up Household

Survey

Feedback Loop

Input

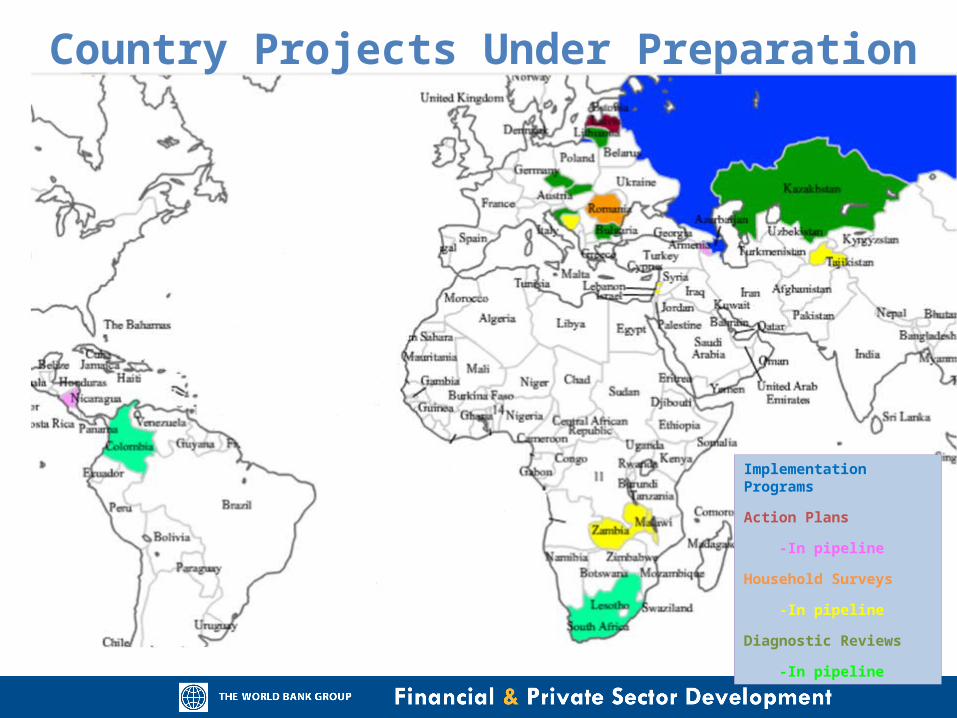

Implementation Programs

Action Plans

-In pipeline

Household Surveys

-In pipeline

Diagnostic Reviews

-In pipeline

Country Projects Under Preparation

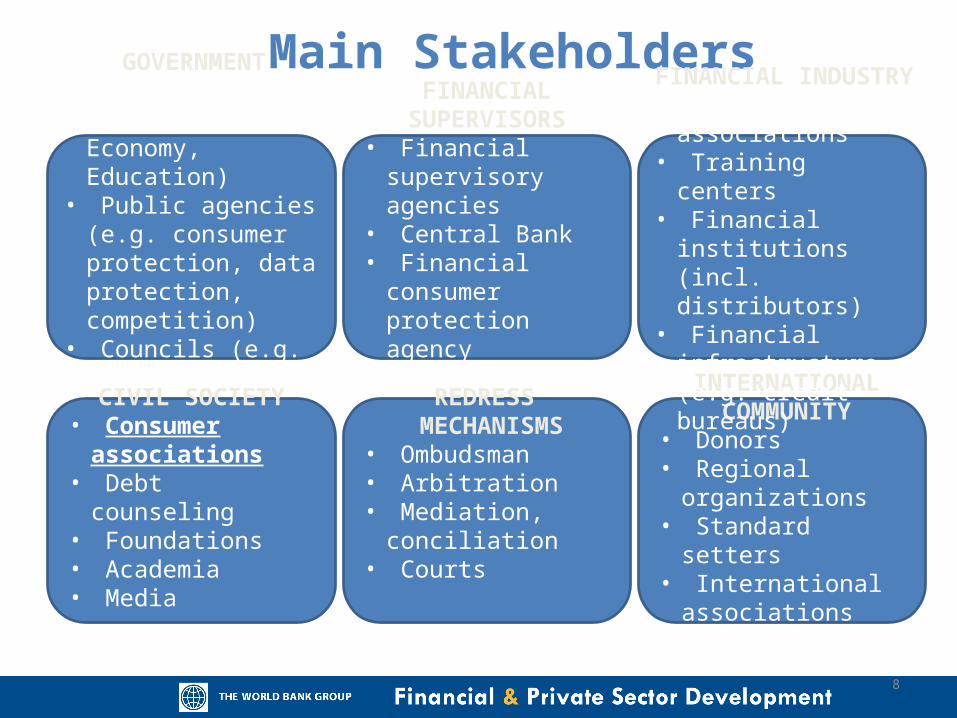

Main Stakeholders

GOVERNMENT• Ministries (e.g. Finance,

Economy, Education)• Public agencies (e.g.

consumer protection, data protection, competition)

• Councils (e.g. consumer protection, education)

FINANCIAL SUPERVISORS

• Financial supervisory agencies

• Central Bank• Financial consumer

protection agency• Compensation

schemes

INTERNATIONAL COMMUNITY

• Donors• Regional organizations• Standard setters• International

associations

REDRESS MECHANISMS

• Ombudsman• Arbitration• Mediation, conciliation• Courts

CIVIL SOCIETY• Consumer

associations• Debt counseling • Foundations• Academia• Media

FINANCIAL INDUSTRY• Industry associations• Training centers• Financial institutions

(incl. distributors)• Financial infrastructure

(e.g. credit bureaus)

8

Ins

Banking

Insurance

Private Pensions

Securities

Non-Bank Credit,

incl. MFI

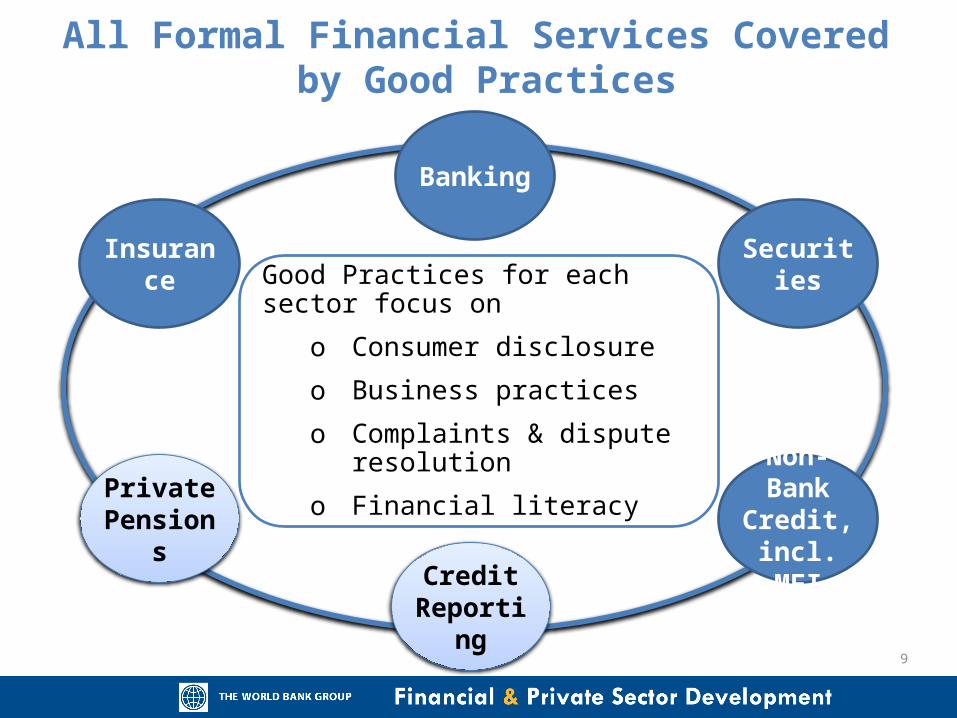

Good Practices for each sector focus ono Consumer disclosureo Business practiceso Complaints & dispute

resolutiono Financial literacy

Credit Reporting

All Formal Financial Services Covered by Good Practices

9

10

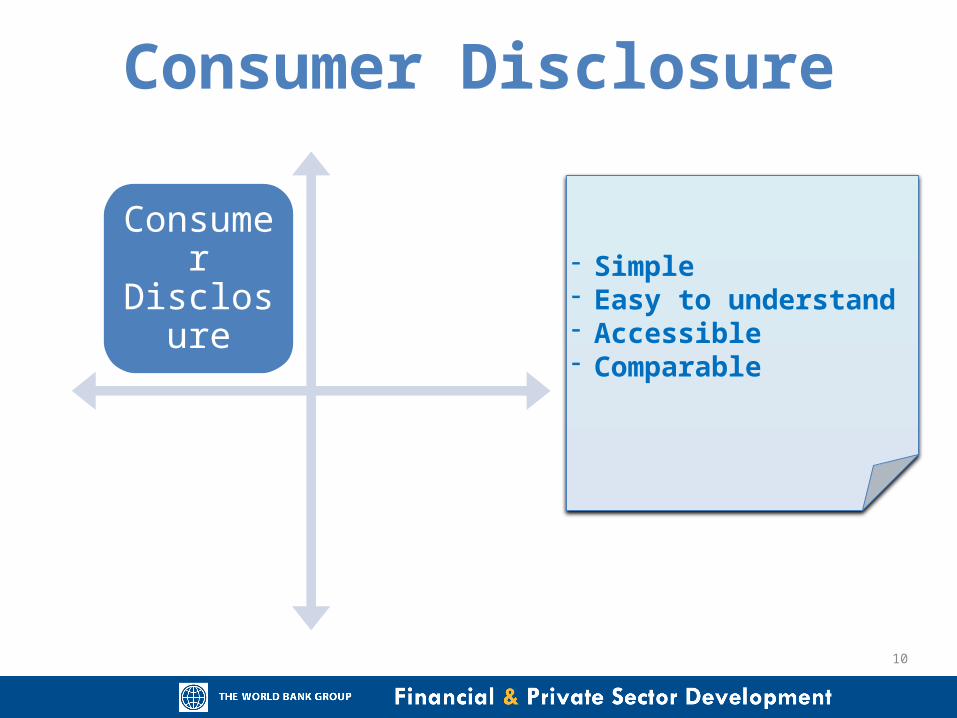

Consumer Disclosure

Consumer Disclosure

Business Practices

Consumer Redress

Financial Literacy

- Simple- Easy to understand- Accessible- Comparable

11

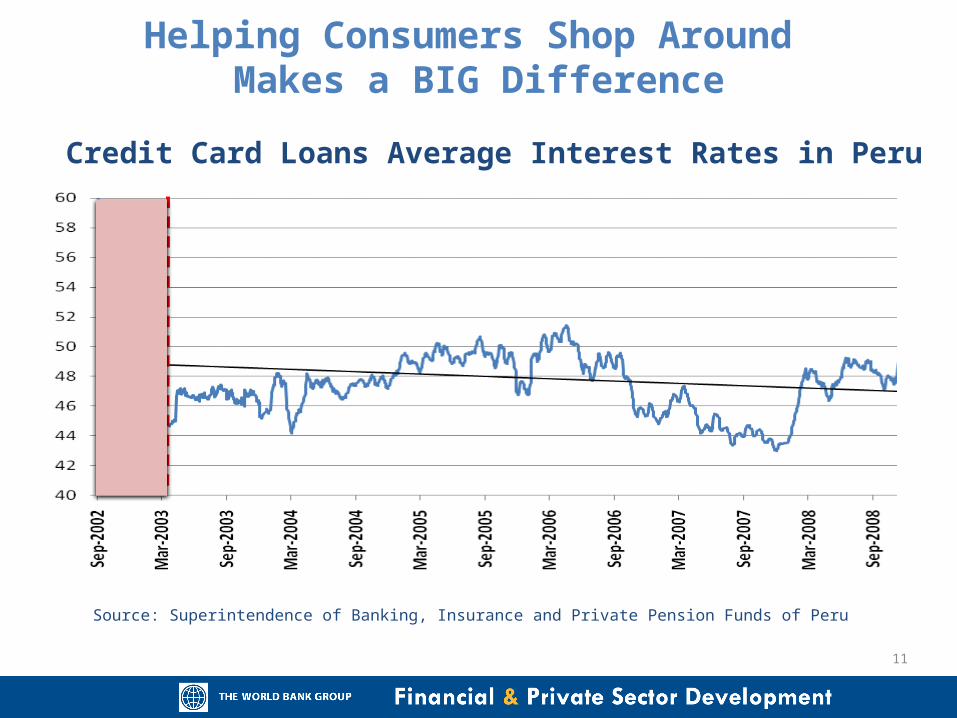

Helping Consumers Shop Around Makes a BIG Difference

Credit Card Loans Average Interest Rates in Peru

Source: Superintendence of Banking, Insurance and Private Pension Funds of Peru

12

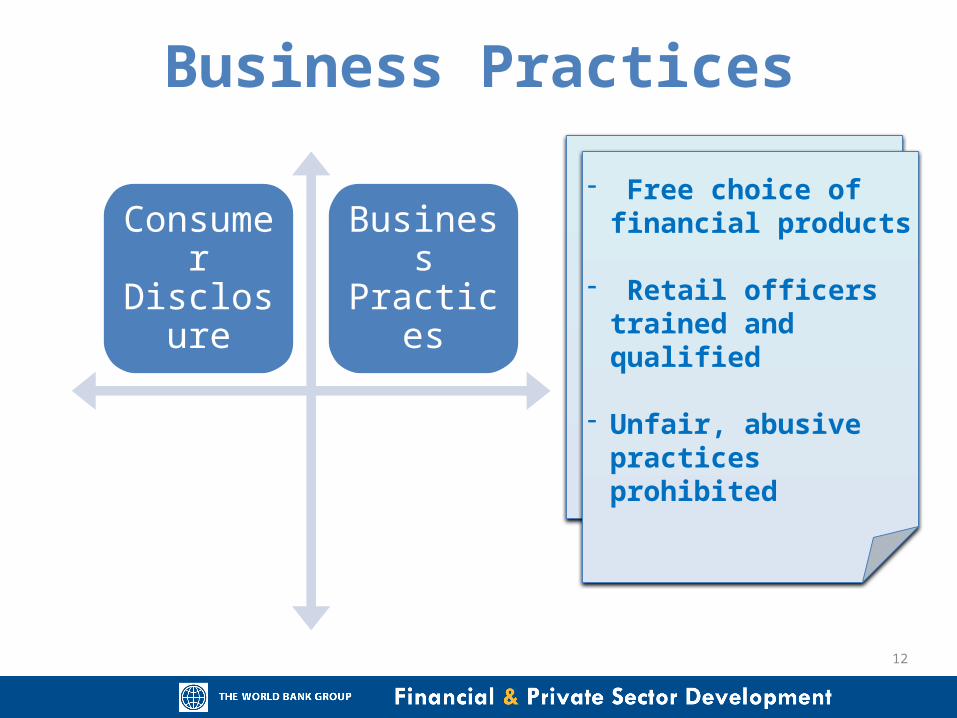

Business Practices

Consumer Disclosure

Business Practices

Consumer Redress

Financial Literacy

- Free choice of financial products

- Retail officers trained and qualified

- Unfair, abusive practices prohibited

13

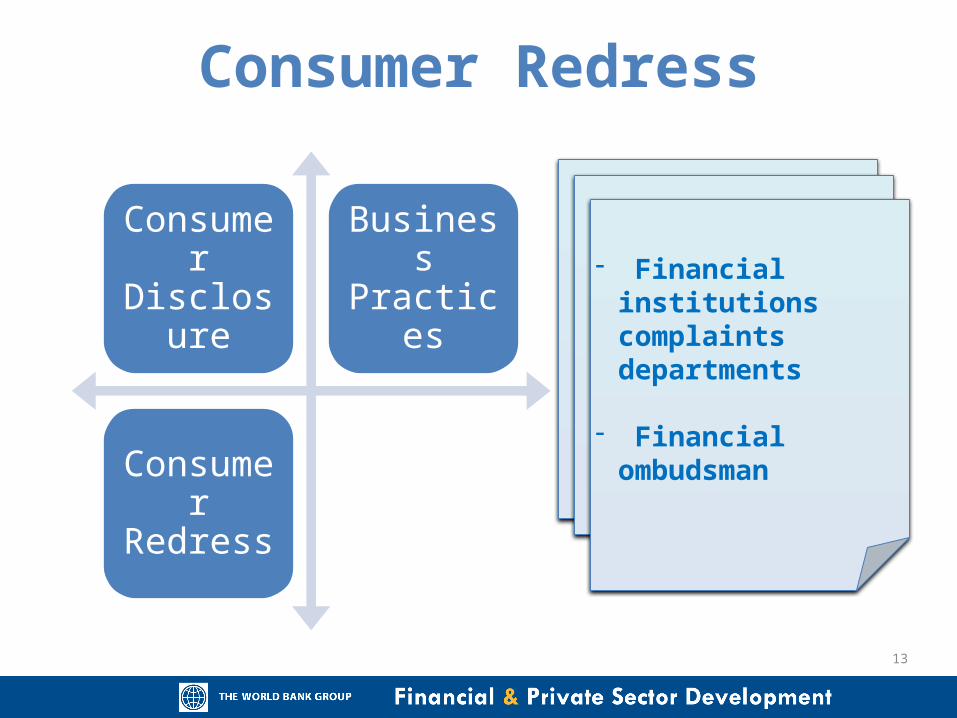

Consumer Redress

Consumer Disclosure

Business Practices

Consumer Redress

Financial Literacy

- Financial institutions complaints departments

- Financial ombudsman

14

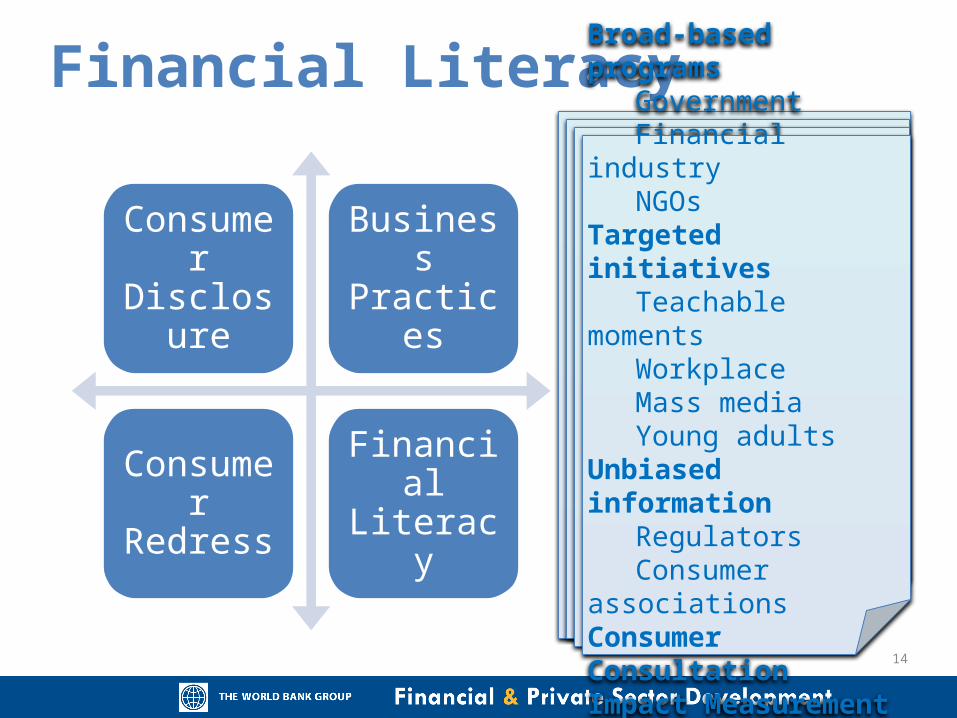

Financial Literacy

Consumer Disclosure

Business Practices

Consumer Redress

Financial Literacy

Broad-based programsGovernmentFinancial industryNGOs

Targeted initiativesTeachable

momentsWorkplaceMass mediaYoung adults

Unbiased informationRegulatorsConsumer

associationsConsumer ConsultationImpact Measurement

15

Consultation Process for Draft Good Practices

• Consultative Draft of “Good Practices for Financial Consumer Protection” available at www.worldbank.org/consumerprotection

• Public comments and suggestions feedback.consumerprotection.worldbank.org

• Direct comments and feedback to Sue Rutledge at [email protected]

• Comments due by June 30, 2011

Empowering Tomorrow’s Consumers

Consumers International World Congress 2011

May 5 Hong Kong

World BankGlobal Program on Consumer Protection & Financial Literacy

Sue Rutledge - Global [email protected]