Embed Size (px)

Citation preview

Employment-Based Health Benefits Among Mid-Sized

and Large Employers

Paul Fronstin, Ph.D.

Director, Health Research & Education Program

Employee Benefit Research Institute

Copyright© - Employee Benefit Research Institute Education and Research Fund, 1978-2005. All rights reserved.

The information contained herein is not to be construed as an attempt to provide legal, accounting, actuarial, or other such

professional advice. Permission to copy or print a personal use copy of this material is hereby granted and brief quotations for the

purposes of news reporting and education are permitted. Otherwise, no part of this material may be used or reproduced without

permission in writing from EBRI-ERF.

2

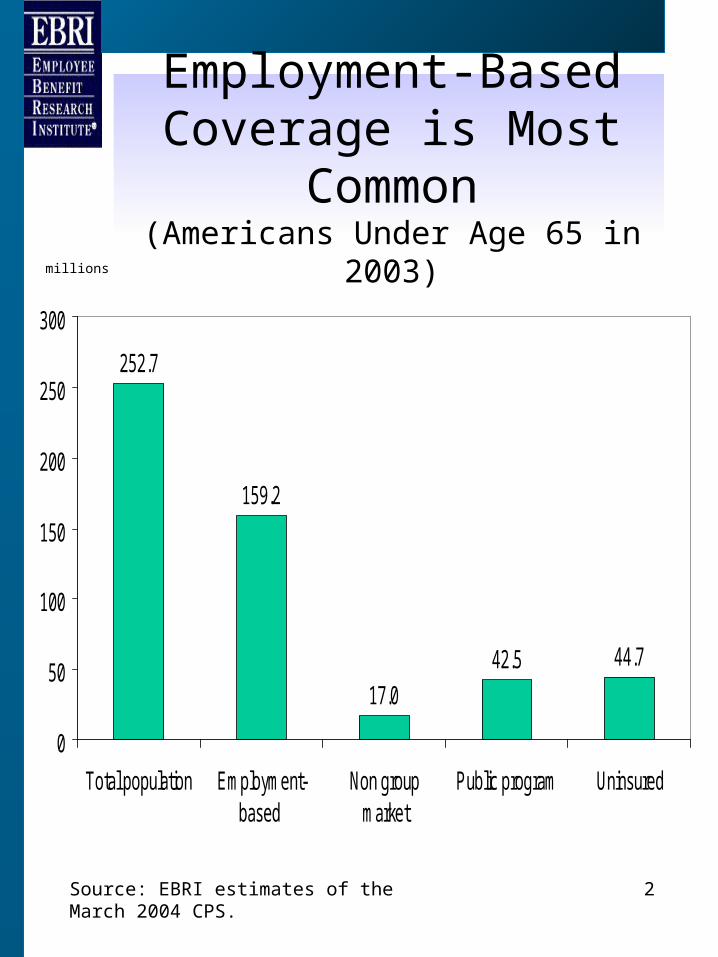

Employment-Based Coverage is Most

Common(Americans Under Age 65 in 2003)

252.7

159.2

17.0

42.5 44.7

0

50

100

150

200

250

300

Total population Employment-based

Non groupmarket

Public program Uninsured

Source: EBRI estimates of the March 2004 CPS.

millions

3

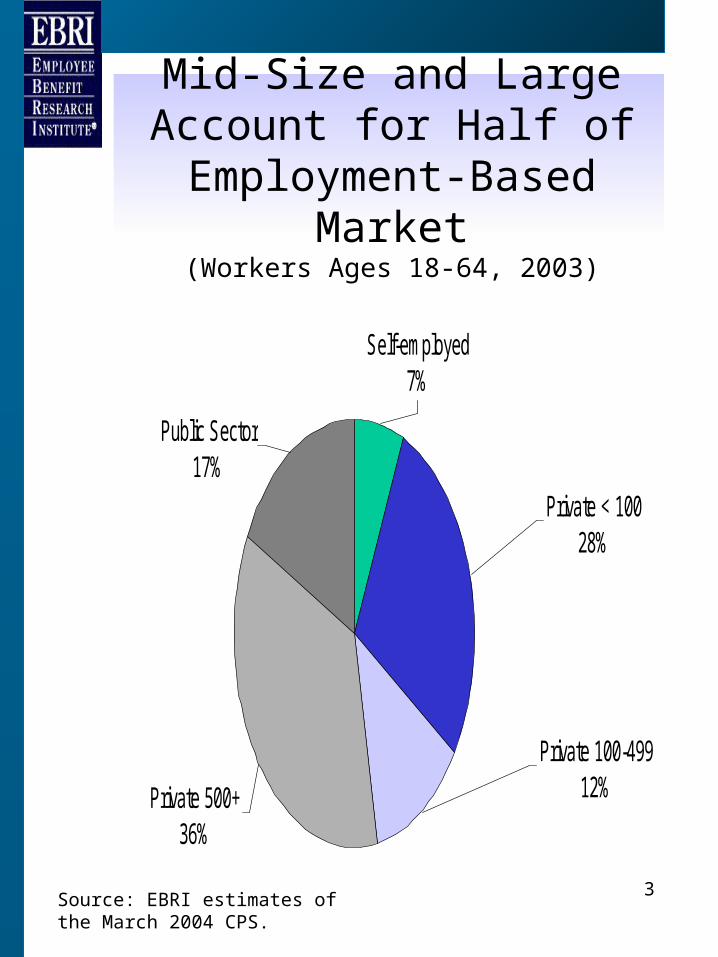

Mid-Size and Large Account for Half of Employment-

Based Market(Workers Ages 18-64, 2003)

Public Sector17%

Private 500+36%

Private 100-49912%

Private < 10028%

Self-employed7%

Source: EBRI estimates of the March 2004 CPS.

4

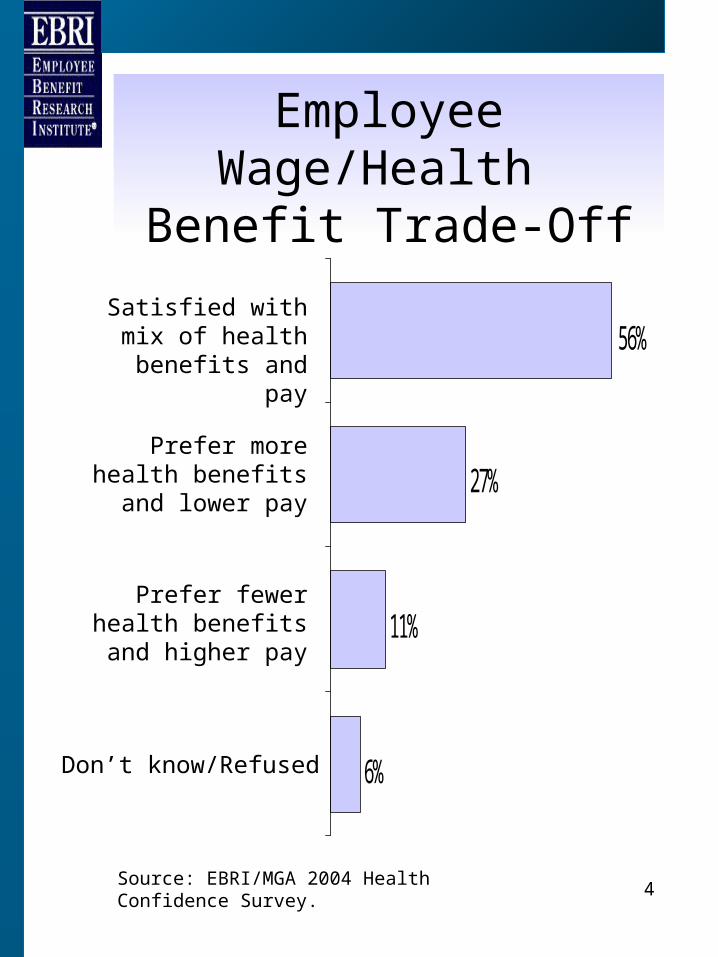

Employee Wage/Health Benefit Trade-Off

6%

11%

27%

56%Satisfied with mix of health benefits and

pay

Prefer more health benefits and lower

pay

Prefer fewer health benefits and higher

pay

Don’t know/Refused

Source: EBRI/MGA 2004 Health Confidence Survey.

5

Types of Health Plans

• FFS: Fee-for-service or traditional indemnity coverage.– No provider networks, reimbursement based on

UCR.• HMO: Owns its health care facility and

employs providers on a salaried basis.– Typically low or no cost sharing, limited

provider network.• POS: HMO with option for members to

use out of network providers.• PPO: Panel of providers who individually

contract with insurers/employers.– Limited network with out of network benefits.

Similar to FFS in many respects.• Consumer Driven Health Plans (See

below)

6

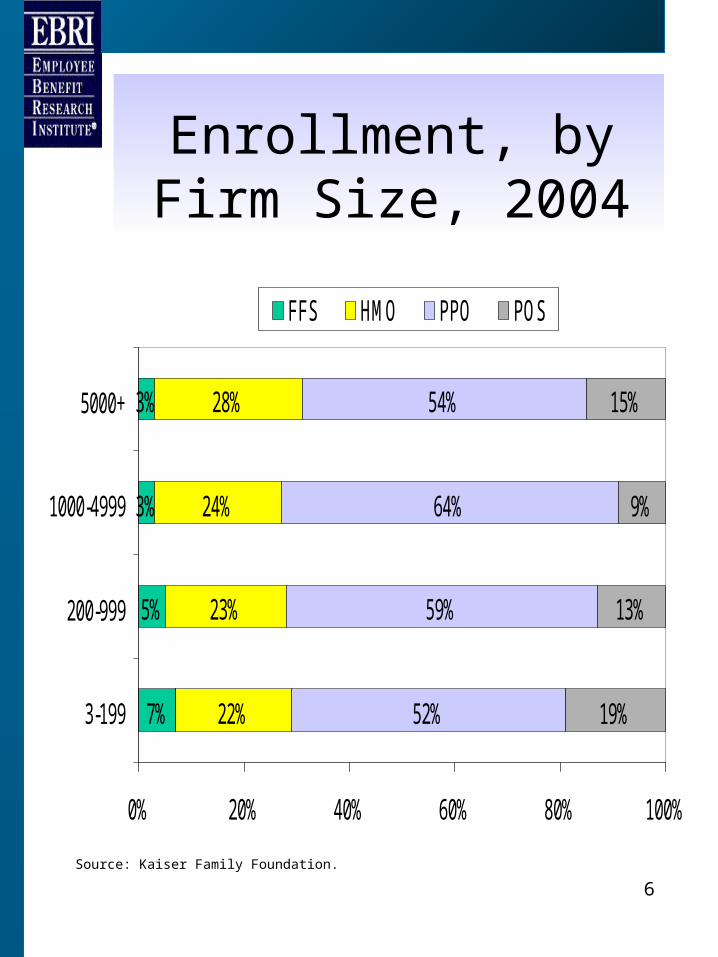

Enrollment, by Firm Size, 2004

7%

5%

3%

3%

22%

23%

24%

28%

52%

59%

64%

54%

19%

13%

9%

15%

0% 20% 40% 60% 80% 100%

3-199

200-999

1000-4999

5000+

FFS HMO PPO POS

Source: Kaiser Family Foundation.

7

Regulation of employee benefits is two-tiered:

ERISA

• ERISA is the primary regulator of private-sector employee benefit plans.– Sets forth standards on reporting and

information disclosure, claims appeal procedures, remedies for wrongfully denied benefits, and fiduciary standards.

• ERISA preempts all state laws that relate to employee benefit plans.

• ERISA specifically preserve state rights to regulate the ‘business of insurance’

8

Health Benefit Plan Regulation

• Self-funded plans: employer pays for the health care claims of its participants directly out of its own income or assets.– Regulated exclusively at the federal

level

• Fully-insured plans: employer pays premiums to purchase a commercial insurance product.– Regulated directly at the federal level

and indirectly at the state level.– State regulation includes mandated

benefits, premium taxes, and other regulation of insurance companies.

9

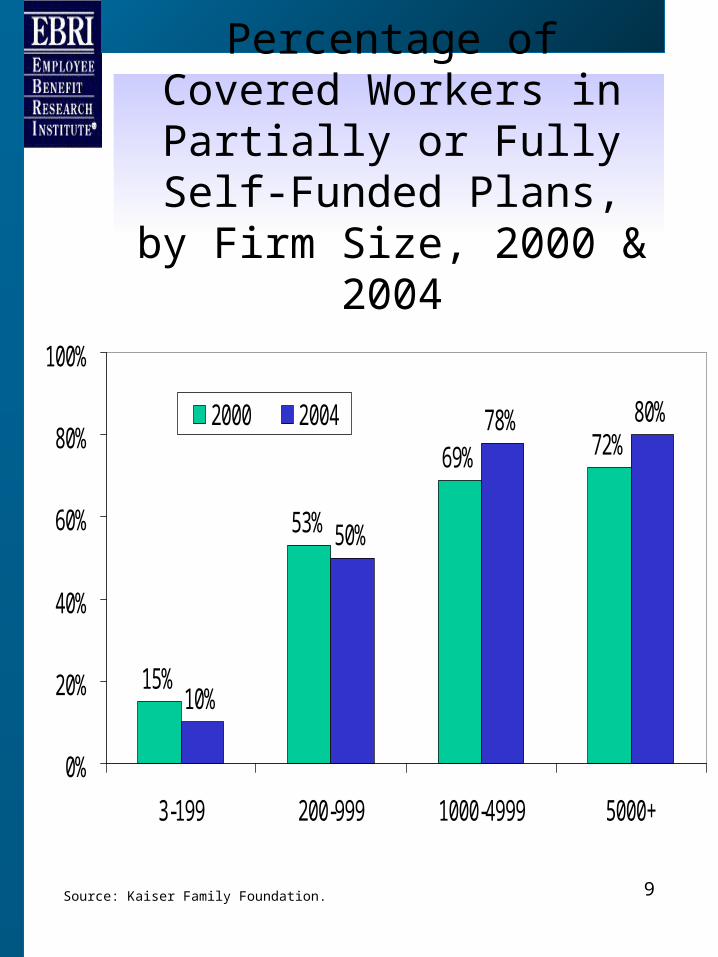

Percentage of Covered Workers in Partially or Fully Self-Funded Plans, by Firm

Size, 2000 & 2004

15%

53%

69% 72%

10%

50%

78% 80%

0%

20%

40%

60%

80%

100%

3-199 200-999 1000-4999 5000+

2000 2004

Source: Kaiser Family Foundation.

10

Health Insurance Portability and Accountability Act of

1996 (HIPAA)

• Created national standards:– Portability and access to care– Preexisting conditions– Discrimination based on health status– Timely disclosure regarding

information– Electronic transmission of health

information– Rights to privacy– Medical savings accounts

11

Other Federal Mandates

• COBRA (1985)

• Newborns’ and Mothers’ Health Protection Act (1996)

• Mental Health Parity Act (1996)

• Post-mastectomy surgery mandate (1998)

12

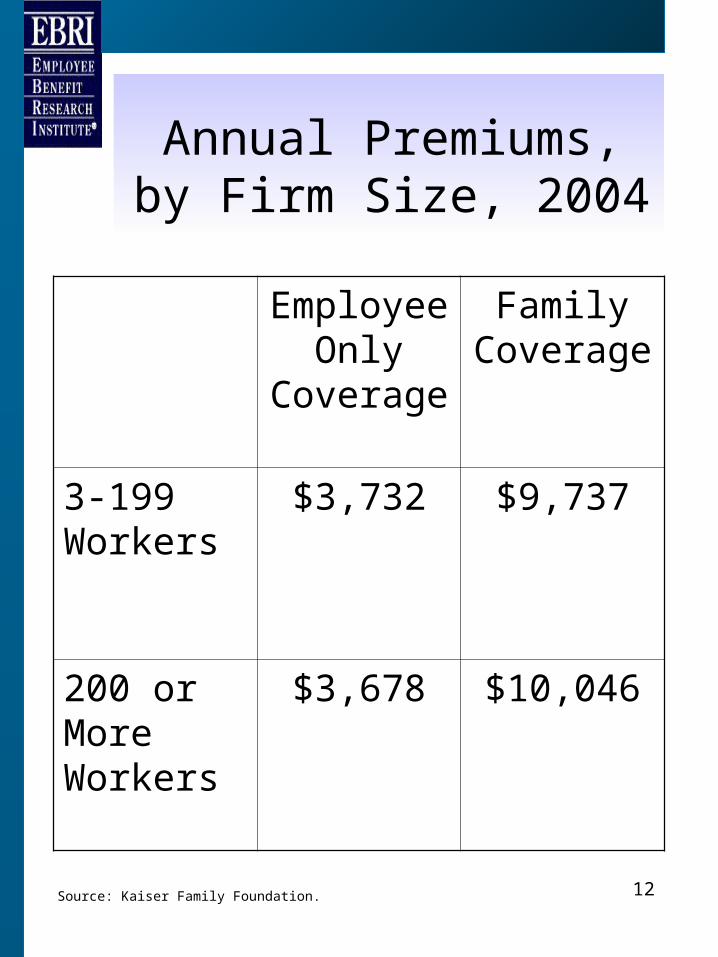

Annual Premiums, by Firm Size, 2004

Employee Only

Coverage

Family Coverage

3-199 Workers

$3,732 $9,737

200 or More Workers

$3,678 $10,046

Source: Kaiser Family Foundation.

13

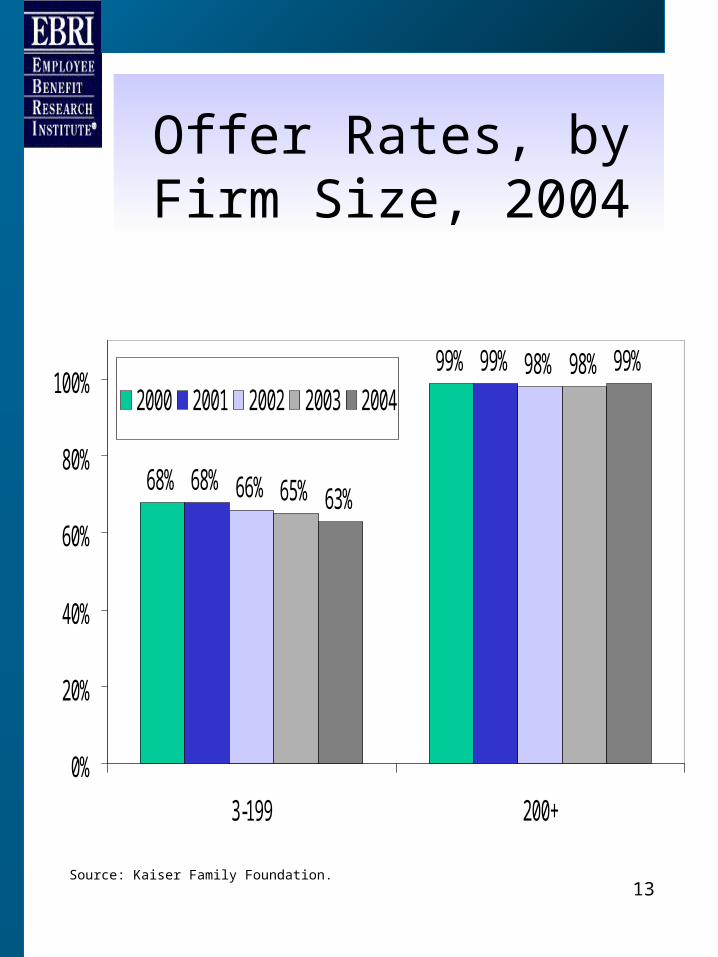

Offer Rates, by Firm Size, 2004

68%

99%

68%

99%

66%

98%

65%

98%

63%

99%

0%

20%

40%

60%

80%

100%

3-199 200+

2000 2001 2002 2003 2004

Source: Kaiser Family Foundation.

14

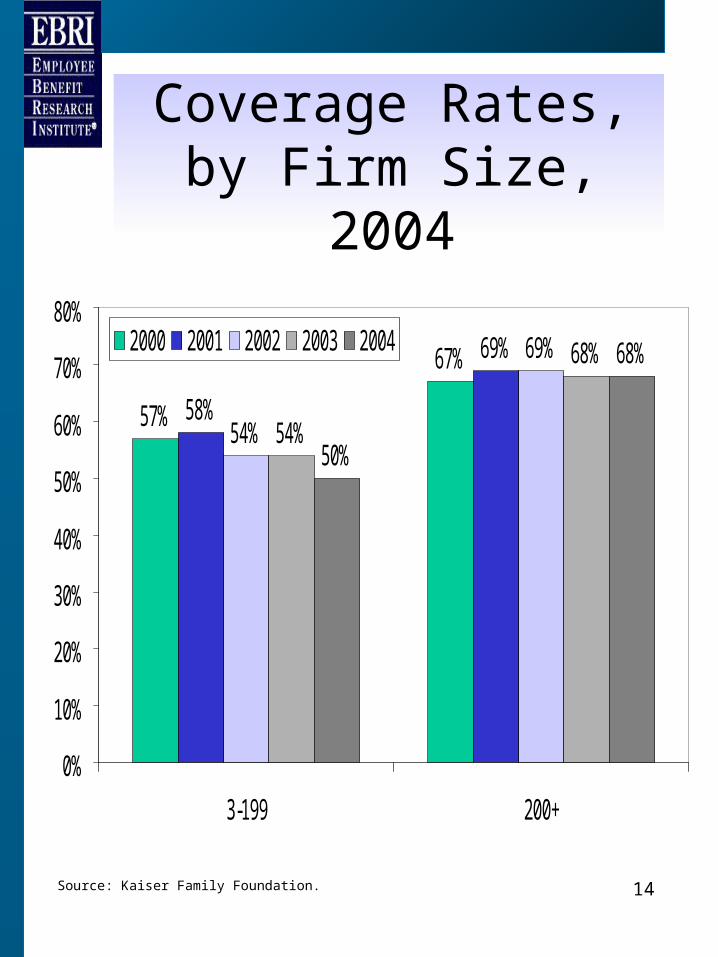

Coverage Rates, by Firm Size, 2004

57%

67%

58%

69%

54%

69%

54%

68%

50%

68%

0%

10%

20%

30%

40%

50%

60%

70%

80%

3-199 200+

2000 2001 2002 2003 2004

Source: Kaiser Family Foundation.

15

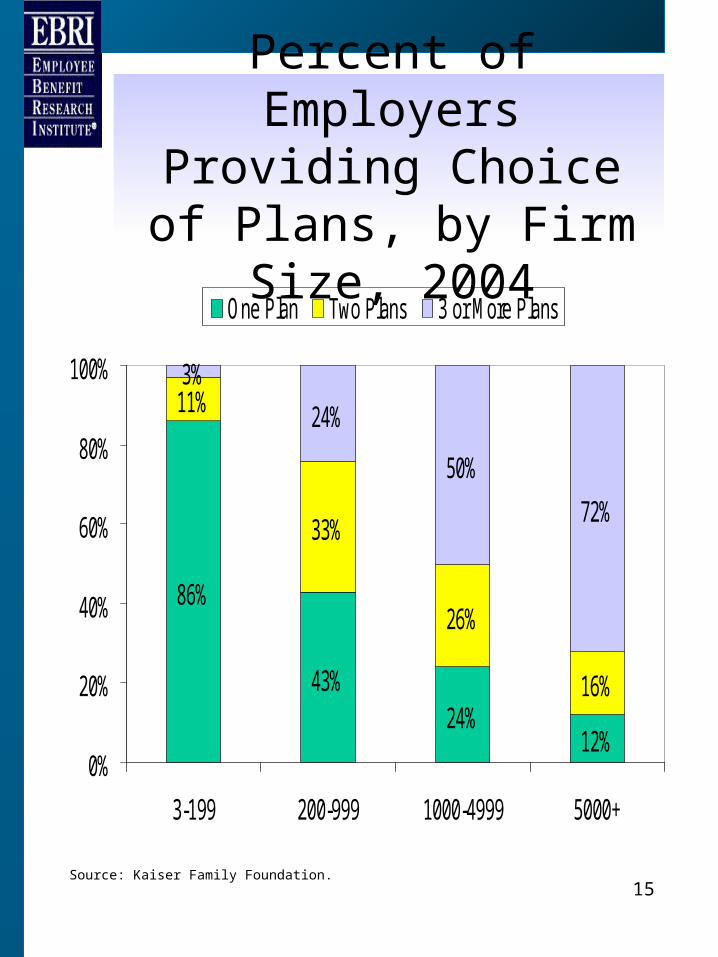

Percent of Employers Providing Choice of Plans,

by Firm Size, 2004

86%

43%24%

12%

11%

33%

26%

16%

3%

24%

50%

72%

0%

20%

40%

60%

80%

100%

3-199 200-999 1000-4999 5000+

One Plan Two Plans 3 or More Plans

Source: Kaiser Family Foundation.

16

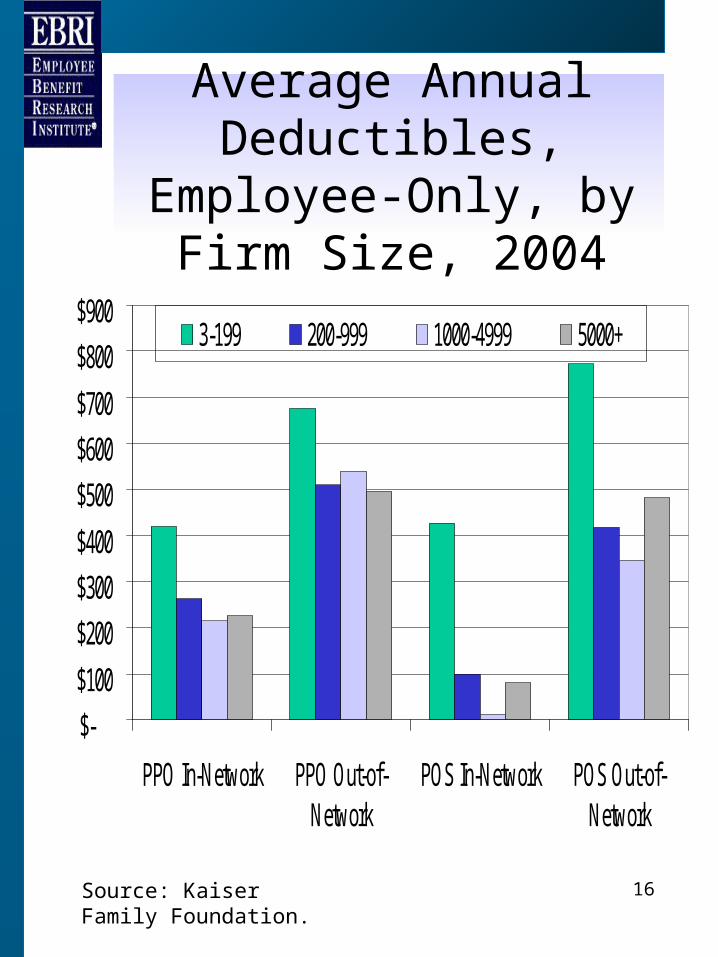

Average Annual Deductibles, Employee-

Only, by Firm Size, 2004

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

PPO In-Network PPO Out-of-Network

POS In-Network POS Out-of-Network

3-199 200-999 1000-4999 5000+

Source: Kaiser Family Foundation.

17

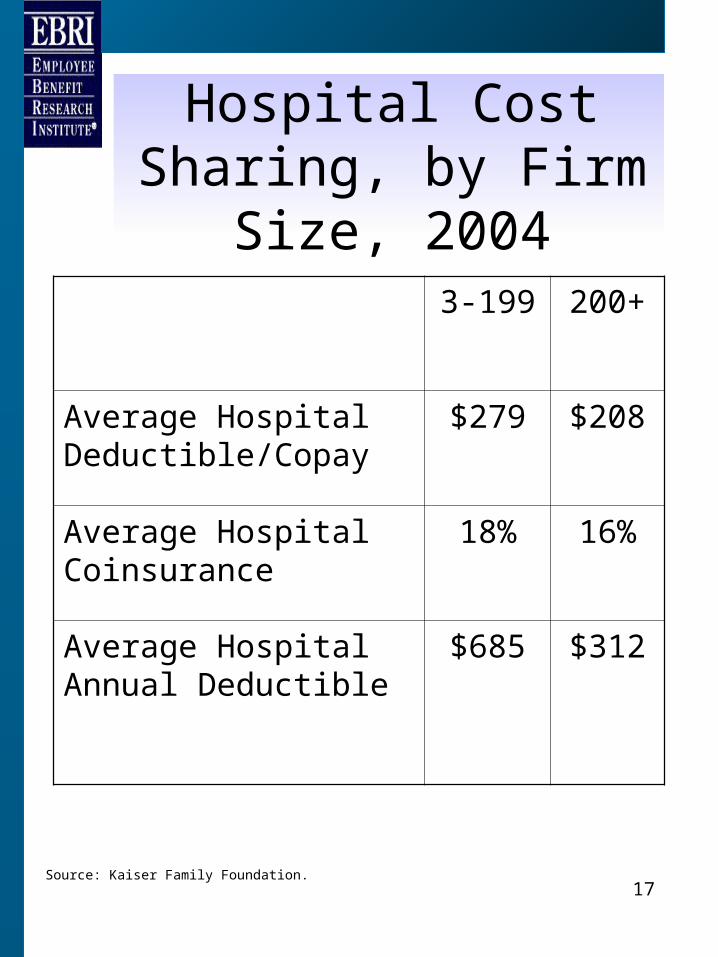

Hospital Cost Sharing, by Firm Size, 2004

3-199 200+

Average Hospital Deductible/Copay

$279 $208

Average Hospital Coinsurance

18% 16%

Average Hospital Annual Deductible

$685 $312

Source: Kaiser Family Foundation.

18

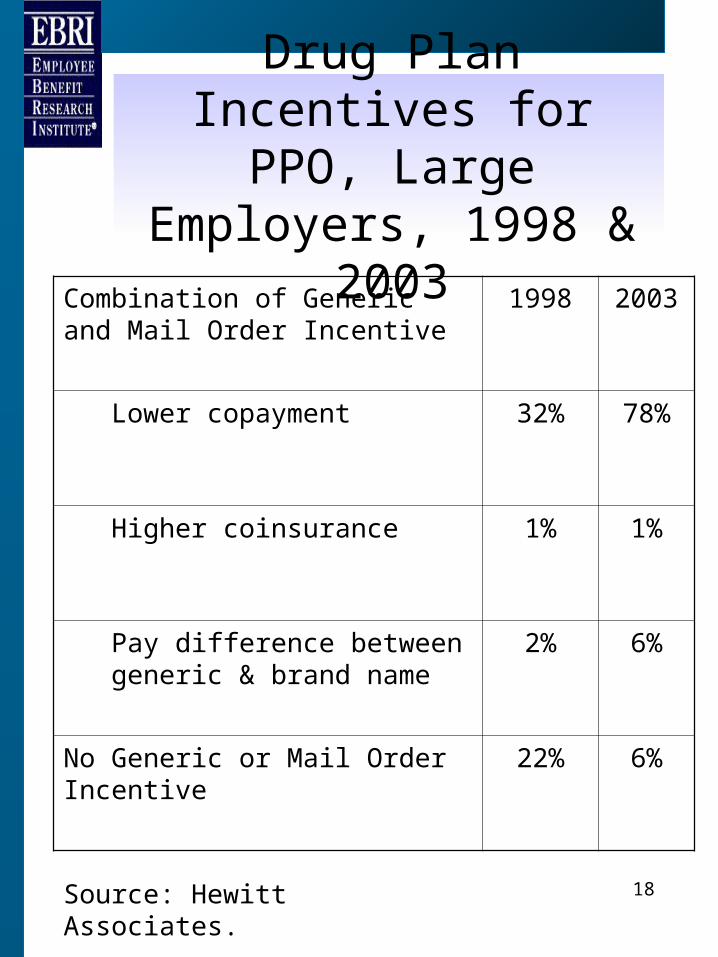

Drug Plan Incentives for PPO, Large Employers,

1998 & 2003

Combination of Generic and Mail Order Incentive

1998 2003

Lower copayment 32% 78%

Higher coinsurance 1% 1%

Pay difference between generic & brand name

2% 6%

No Generic or Mail Order Incentive

22% 6%

Source: Hewitt Associates.

19

Tiered Provider Networks

• Hospitals & doctors.• Tiers vary with cost & quality.

– Similar to PPO (in vs. out)– Similar to Rx tiers.

• Cost sharing distinctions– Co-payment per hospital day.– Coinsurance rate per stay.– Overall deductible per stay.

20

Health Reimbursement Arrangement (HRA)

• Employer provided notional account that allows for pre-tax reimbursement of medical expenses.

• Typically combined with a high-deductible health plan.

• Employee contributions not permitted.

21

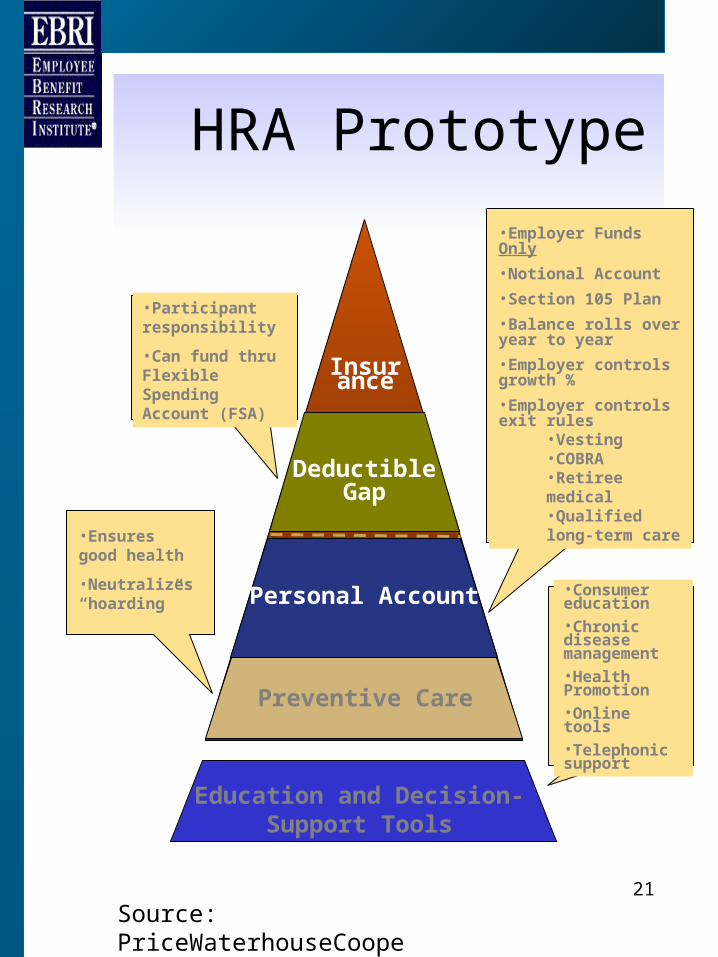

Preventive Care

Personal Account

Deductible Gap

Insurance

•Ensures good health

•Neutralizes “hoarding”

•Employer Funds Only

•Notional Account

•Section 105 Plan

•Balance rolls over year to year

•Employer controls growth %

•Employer controls exit rules

•Vesting•COBRA•Retiree medical•Qualified long-term care

•Participant responsibility

•Can fund thru Flexible Spending Account (FSA)

Education and Decision-Support Tools

•Consumer education•Chronic disease management•Health Promotion•Online tools•Telephonic support

HRA Prototype

Source: PriceWaterhouseCoopers.

22

Health Savings Account (HSA)

• Allows for tax-free accumulation of savings.– Tax free contribution.– Tax free accumulation.– Tax free withdrawals for health care services, COBRA

and LTCI premiums, retiree health premiums for Medicare-eligible retirees.

• Qualified health plan.– Self-only: Minimum $1,000 deductible, $5,100 OOP

max.– Family coverage: Minimum $2,000 deductible,

$10,200 OOP max.

• Contributions– Self-only: limited to level of deductible up to $2,650

max.– Family coverage: limited to level of deductible up to

$5,250 max.

• Catch-up contributions allowed once age 55 of $1,000.– Phased-in by 2009.

23

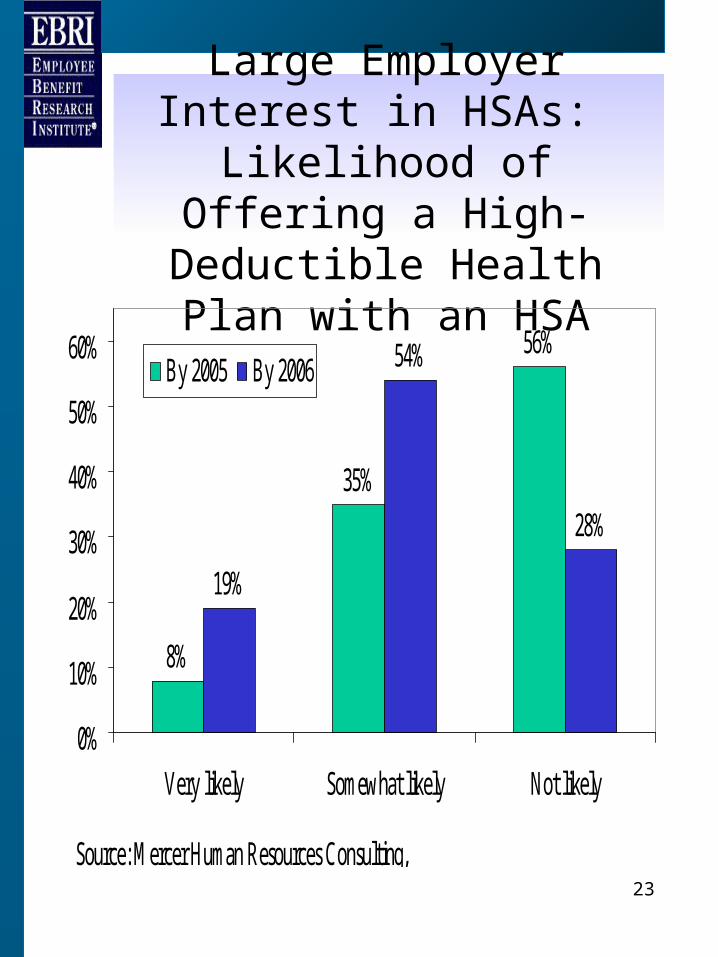

Large Employer Interest in HSAs:

Likelihood of Offering a High-Deductible Health Plan

with an HSA

8%

35%

56%

19%

54%

28%

0%

10%

20%

30%

40%

50%

60%

Very likely Somewhat likely Not likely

By 2005 By 2006

Source: Mercer Human Resources Consulting,

EBRI

2121 K Street NW, Suite 600

Washington, DC 20037

Phone: 202-659-0670

Fax: 202-775-6312

www.ebri.org