Embed Size (px)

Citation preview

2000

Employers’ Guide

Filing the T4A Slip and Summary Form

RC4157(E) (Rev. 00)

Problem Resolution ProgramWe are always looking at ways to make it easier for you tofile your information returns, and resolve any problemsyou may have.

If you have a problem, you can call 1-800-959-5525 forservice in English or 1-800-959-7775 for service in French.

You can also write or visit any tax centre. The addresses arelisted at the end of this guide.

If, after this step, your problem is not resolved to yoursatisfaction, you should get in touch with the ProblemResolution Program co-ordinator listed in the governmentsection of your telephone book.

TTY usersIf you have a hearing impairment and use a teletypewriter(TTY), you can call our toll-free, bilingual enquiry service at1-800-665-0354.

To cancel or reinstate a mailing of theguideTo save paper, we want to reduce the number of guides wemail to you. If you receive more than one copy of this guidebecause you have more than one payroll deductions

account, and you want to cancel the extra copies, contactany tax services office. You have to provide your employername, mailing address, and Business Number to cancel amailing.

Also, if you cancelled this publication and want to receive itagain, contact any tax services office.

Ordering publicationsThroughout this guide, we mention other publications thatcover topics in more detail. You can now order thepublications you need, as well as blank copies of T4A slips,from our Web site. Complete the order form that you canfind at www.ccra-adrc.gc.ca, or call 1-800-959-2221.

Your opinion counts!We review this guide each year. If you have any commentsor suggestions that would help us improve the informationit contains, we would like to hear from you.

Please send your comments to:

Client Services DirectorateCanada Customs and Revenue AgencyVanier Place, Tower AOttawa ON K1A 0L5

Visually impaired persons can get this publication in braille orlarge print, or on audio cassette or computer diskette, by calling1-800-267-1267 weekdays between 8:15 a.m. and 5:00 p.m.(Eastern Time).

This guide uses plain language to explain the most common tax situations. If you need more help after you read this guide,you can call 1-800-959-5525 for service in English or 1-800-959-7775 for service in French.

La version française de ce guide de l’employeur est intitulée Comment établir le feuillet T4A et le formulaire Sommaire.

3

Page Page

What’s New? ....................................................................... 4

Notice ................................................................................... 4

Chapter 1 – General Information .................................... 5Who should use this guide?............................................... 5Social insurance number (SIN).......................................... 5Failure to file an information return................................. 5What should you do if your business stops

operating?......................................................................... 5Waiving penalties and interest.......................................... 5Payroll deductions tables ................................................... 5

Chapter 2 – T4A Reporting ............................................... 5Types of T4A slips available .............................................. 5How to order your blank T4A slips.................................. 6How to file information returns ........................................ 6

When to file the information return.............................. 6Where to send the information return.......................... 6Distributing copies of T4A slips .................................... 6

Customized forms............................................................... 6Do you file information returns on

magnetic media?.............................................................. 6What should you do with large returns? ......................... 6How can you amend, cancel, or replace T4A slips? ....... 6

Amending slips................................................................ 6Cancelling slips................................................................ 7Replacing slips ................................................................. 7Pension adjustment (PA) and past-service pension

adjustment (PSPA) ...................................................... 7

Completing the T4A slip..................................................... 7When to complete the T4A slip...................................... 7How to complete the T4A slip ....................................... 7Completing the boxes...................................................... 7

Completing the T4A Summary form ................................ 12How to complete the T4A Summary............................. 12

Chapter 3 – Special Payments .......................................... 13Death benefits ...................................................................... 13

Income tax......................................................................... 13Lump-sum payments .......................................................... 14

Income tax......................................................................... 14Withholding rates for lump-sum payments................. 14Retroactive lump-sum payments................................... 14Transfer of funds.............................................................. 15

Patronage payments............................................................ 15Retiring allowances ............................................................. 16

Income tax......................................................................... 16Transferring a retiring allowance to an RPP or

RRSP .............................................................................. 16How to report retiring allowances that are paid

over a number of years................................................ 17

Sample Forms ...................................................................... 18T4A slip................................................................................. 18T4A Summary form............................................................. 19

Addresses of Tax Centres .................................................. 20

Major changes that have taken place since last yearare outlined in red.

Table of Contents

4

The Canada Customs and RevenueAgency (CCRA) has a new1-800 service for employersIf you need help after you read this guide, call1-800-959-5525 for service in English or 1-800-959-7775for service in French.

Registered education savings plan(RESP)Investment earnings in an RESP can be paid to thesubscriber or, in some circumstances, can also be paid to aperson other than the subscriber. These payments are calledaccumulated income payments from an RESP.

If, as the promoter, you make accumulated incomepayments out of an RESP, you have to withhold amountsfor tax payable under Part I and Part X.5 of the Income TaxAct.

The amount subject to withholding taxes may be reduced ifboth of the following conditions are met:

n the recipient is the subscriber (or, after the death of thesubscriber, the subscriber’s spouse if there is no othersubscriber); and

n the subscriber (or, after the death of the subscriber, thesubscriber’s spouse if there is no other subscriber) hascompleted Form T1171, Tax Withholding Waiver onAccumulated Income Payments From RESPs, and asks thatyou transfer the payment directly to the subscriber’sregistered retirement savings plan (RRSP) or spousalRRSP.

If you are satisfied that the conditions explained onForm T1171 are met and you can reasonably believe thatthe recipient will deduct that amount as an RRSPcontribution for the year you paid it, you do not have towithhold any taxes on the amount transferred.

The amount subject to withholding tax is the accumulatedincome payment minus the reduction determined onForm T1171.

All payments from an RESP are to be reported on aT4A slip, Statement of Pension, Retirement, Annuity, and OtherIncome.

For more information, get the information sheet calledRegistered Education Savings Plans (RESPs), or contact anytax services office.

Disability benefitsEnter in box 16, “Pension or superannuation,” of theT4A slip, the disability benefits paid as a life annuity.

Disability benefits paid out of a superannuation or pensionplan should be declared in box 28, “Other income,” of theT4A slip.

Life income fund (LIF)Report on a T4RIF slip income paid from a life income fund(LIF). However, if a life annuity is bought from theproceeds of a LIF, there is no longer a registered retirementincome fund (RRIF) and the annuity payments have to bereported on a T4A slip. Report these payments in box 24,“Annuities,” (not in box 28, “Other income”) of theT4A slip.

Construction businessesConstruction businesses have to record amounts paid orcredited to subcontractors for goods and services renderedin connection with construction activities, and report thesepayments in a T5018, information return. They can reportpayments on either a calendar- or fiscal-year basis.Information returns have to be filed six months from theend of the reporting period.

For more information, contact any tax services office, orvisit our Web site at www.ccra-adrc.gc.ca/contract

Business Number (BN)The BN is a numbering system that simplifies andstreamlines the way businesses deal with the federalgovernment. The BN is based on the simple principle—”one business, one number.”

All new businesses will get a BN (a 15-digit number) whenthey open any of the following business accounts with us:

n corporate income tax;

n import/export;

n payroll deductions; and

n goods and services tax/harmonized salestax (GST/HST).

The BN also includes accounts for registered charities,registered Canadian amateur athletic associations, andnational arts service organizations.

Form T4A SummaryYou no longer have to provide us with two copies of theT4A Summary form. As a result, we have eliminated thecarbon-loaded summary forms. All employers should nowuse Form T4A Summary for laser or ink jet printer. You canmake a photocopy of the original T4A Summary form, anduse it as your working copy. Keep the working copy foryour records.

What’s New?

Notice

5

Other employers’ guidesThe employers’ guides called Payroll Deductions (BasicInformation), Remitting Payroll Deductions, Taxable Benefits,and the new guide called Filing the T4F Slip and SummaryForm are not sent to you automatically. If you would like toget a copy, complete the order form that you can find atwww.ccra-adrc.gc.ca, or call 1-800-959-2221.

NoteYou can also dowload these guides from our Web site.

Who should use this guide?You should use this guide if you are:

n an employer;

n a trustee; or

n a payer of other amounts (e.g., fees for services renderedby residents or non-residents, commissions toself-employed agents, or pension or superannuationbenefits).

We also provide guidelines for estate executors (orliquidators), administrators, and corporate directors.

Social insurance number (SIN)Make sure you always use the correct name and number asshown on the recipient’s SIN card.

If you cannot obtain a SIN from the recipient, file yourinformation return no later than the last day of February. Ifyou do not, you may be subject to a penalty for late filing.

For more information, see Information Circular 82-2, SocialInsurance Number Legislation That Relates to the Preparation ofInformation Slips.

Failure to file an information returnAn information return is the T4A slip and theT4A Summary form. You have to file an information returnand give information slips to the recipients by the last dayof February following the calendar year to which theinformation return applies. If you fail to do this, thepenalty for each failure is $25 a day, with a minimumpenalty of $100 and a maximum of $2,500.

NoteIf the last day of February is a Sunday, your informationreturn is due the next business day.

What should you do if your businessstops operating?Send all unremitted amounts you withheld for therecipients to your tax centre within seven days of the dayyour business ends. For more information on how to sendin deductions, see the employers’ guide called RemittingPayroll Deductions.

Complete the necessary T4A slips and T4A Summary andsend them to the Ottawa Technology Centre within 30 daysof the day your business ends. You have to calculate thepension adjustment (PA) that applies to your formeremployees who accrued benefits for the year underyour registered pension plan (RPP) or deferred profitsharing plan (DPSP). Distribute copies of the T4A slips toyour former employees. For more information on how tocomplete a T4A slip and T4A Summary form, see Chapter 2of this guide.

Prepare and give a Record of Employment (ROE) to eachformer employee. For more information, see the guidecalled How to Complete the Record of Employment (ROE) Form,which is available from the nearest Human ResourcesCentre of Canada.

Waiving penalties and interestThe fairness provisions of the Income Tax Act give us certaindiscretion to cancel or waive all or a part of interest chargesand penalties. This flexibility allows us to considerextraordinary circumstances that may have preventedemployers or payers from fulfilling their obligations underthe Income Tax Act. For more information, see InformationCircular 92-2, Guidelines for the Cancellation and Waiver ofInterest and Penalties.

Payroll deductions tablesOur payroll deductions tables or tables on diskette (TOD)contain information to help you calculate the amount ofincome tax that you have to deduct for your employees orfor retired persons.

Both versions can be downloaded from our Web site atwww.ccra-adrc.gc.ca. You can also order them bycompleting the order form that you can find on ourWeb site, or by calling 1-800-959-2221.

se the T4A slip and the T4A Summary form to reportincome you paid and amounts you withheld during

the year for the recipients.

NoteIn this guide recipient refers to a beneficiary of apayment and includes employees, ex-employees, retiredpersons, and shareholders.

The T4A slip and T4A Summary form apply to resident andnon-resident payers.

Types of T4A slips availableYou can order the two following types of slips:

n four-copy: carbon-loaded for impact printer (continuous)or hand filled; and

n single-page: 1 page (not carbon-loaded) for laser orink jet printers only.

Each type includes three T4A slips per sheet.

Chapter 1 – General Information

Chapter 2 – T4A Reporting

U

6

How to order your blank T4A slipsTo order blank copies of T4A slips, complete the orderform that you can find on our Web site atwww.ccra-adrc.gc.ca, or call 1-800-959-2221.

How to file information returnsAn information return consists of two things:

n slips; and

n the related summary forms.

A summary form alone is not an information return.

When to file the information returnYou have to file your T4A information return by the lastday of February following the calendar year to which theinformation return applies (e.g., you have to file your 2000T4A information return by the last day of February 2001).

NotesIf the last day of February is a Sunday, your informationreturn is due the next business day.

When you send us copies of the slips, keep T4As threeto a page. This will allow us to process your informationreturn faster.

Where to send the information returnAfter you complete your information return, mail it to:

Ottawa Technology CentreCanada Customs and Revenue Agency875 Heron RoadOttawa ON K1A 1G9

NoteIf, after you file your return, you need to send usamended slips, send copy 1 of the slips to any tax centre.

Distributing copies of T4A slipsCopy 1Copy 1 of each T4A slip must be appended to theT4A Summary form. If you file on magnetic media(cartridge or diskette), do not submit a paper copy of theslips or summary form.

Copies 2 and 3Copies 2 and 3 must be delivered or mailed to the recipientsby the last day of February following the calendar year towhich the slips apply.

Copy 4Keep copy 4 of the slips and a copy of the summary formfor your files.

Customized formsTo reduce the workload of those who complete largenumbers of forms, we will accept forms other than ourown. If you use your own computer-printed forms, youhave to get written approval from us before you can issuethem.

Send your proposed samples to:

Forms Management DivisionPublishing DirectorateCanada Customs and Revenue Agency17th floorAlbion Tower25 Nicholas StreetOttawa ON K1A 0L5

You will receive either our written approval or a request tomake changes to the forms before we approve them.

For more information, see Information Circular 97-2,Customized Forms – Returns and Information Slips.

Do you file information returns onmagnetic media?If you (or a representative) file more than 500 informationslips for the calendar year (the total number of T4, T4A,T4A-NR, T4RIF, T5, T5008, T4RSP, NR4, and T3 slips), youhave to file your information return on magnetic mediausing computer tape, diskette, or cartridge.

For more information on magnetic media filing, see theguide called Computer Specifications for Data Filed onMagnetic Media – T4, T4A, and T4A-NR, or call1-800-665-5164.

This publication is also available on our Web site atwww.ccra-adrc.gc.ca/magmedia

What should you do with largereturns?If you have a T4A return that contains more than 300 slips,split the return into bundles of 300 slips or less. Make sure asegment form is on the top of each bundle. The total of allamounts shown on each segment form has to agree withthe corresponding totals on the summary form.

If you would like to order segment forms, or if you needmore instructions, contact any tax services office or taxcentre.

How can you amend, cancel, orreplace T4A slips?Amending slipsAfter you file your information return, you may notice thatyou made an error when preparing the T4A slips. If so, youwill have to prepare amended slips to correct theinformation. Clearly identify the new slips as amended bywriting “amended” at the top. When you amend a slip,make sure you complete all the necessary boxes, includingthe information that was correct on the original slip.Distribute the amended slips to the recipients the same wayas the originals. Send copy 1 of the slips to any tax centrewith a letter explaining the reason for the amendment. Theaddresses of our tax centres are listed at the end of thisguide.

NoteYou do not have to file an amended summary formwhen you send in amended slips.

7

Cancelling slipsIf you are cancelling a T4A slip, send us a copy of theoriginal clearly marked “cancelled.”

If you notice errors on the T4A slips before you file themwith us, you can correct them by preparing new slips andremoving any incorrect slips from the return. If you do notprepare a new slip, initial any changes you make on theslip. Make sure you also correct the summary form.

Replacing slipsIf you issue T4A slips to replace copies that recipients lostor destroyed, do not send these copies to us. Clearlyidentify them as duplicate copies, and keep any copies youdo not distribute with your records.

Pension adjustment (PA) and past-servicepension adjustment (PSPA)You have to recalculate a pension adjustment (PA) orcalculate a past-service pension adjustment (PSPA) whenboth of the following conditions are met:

n an employee returns from a leave of absence, or from aperiod of reduced services; and

n benefits are retroactively provided for the periodconcerned.

For information on recalculating a PA, see the PensionAdjustment Guide. For information on calculating a PSPA,see the Past Service Pension Adjustment Guide.

Completing the T4A slipSee the back of this guide for a sample T4A slip.

When to complete the T4A slipYou may have to complete a T4A slip if you made any ofthe following types of payments:

n pension or superannuation (box 16);

n lump-sum payments (box 18);

n self-employed commissions (box 20);

n annuities (box 24);

n eligible retiring allowances (box 26);

n non-eligible retiring allowances (box 27);

n other income (box 28);

n patronage allocations (box 30);

n RESP accumulated income payments (box 40); or

n RESP educational assistance payments (box 42).

You have to complete a T4A slip if:

n the payment was more than $500; or

n you deducted tax from the payment.

NoteIf you provide group term life insurance taxablebenefits for former employees, you always have toprepare a T4A slip, even if the benefit is less than $500.

However, multi-employer plan administrators ortrustees that provide taxable benefits under such a planto former employees or employees, have to prepare aT4A slip only if the benefit is more than $25.

The group term life insurance benefits have to be enteredin box 28, “Other income,” of the T4A slip.

How to complete the T4A slipBefore you start to enter information on the slips, pleasekeep the following points in mind:

n Complete the slips clearly and in alphabetical order.

n Use a standard 10- or 12-character per inch font if typedor computer generated.

n Make sure the SIN you enter on the T4A slip for eachbeneficiary is the same as the one on his or her SIN card.

n Report, in Canadian dollars, all amounts you paidduring the year.

n Report all amounts in dollars and cents. However, reportthe pension adjustment (PA) in box 34 in dollars only.

n Do not show negative dollar amounts on slips. To makechanges to previous years, send us an amended slip forthe years in question.

n Do not change the headings of any of the boxes.

NoteDo not report on a T4A slip amounts paid formanagement fees, director’s fees, tips and gratuities,group term life insurance premiums paid for currentemployees, and other employment income—they mustbe reported in box 14, “Employment income,” of theT4 slip.

Completing the boxesIn many cases, we ask you to enter an explanation todescribe payments or part payments in the “Footnotescodes and explanation” area, as well as a code in box 38.You can find a complete list of these codes later in thischapter, in the section called “Box 38 – Footnote codes.”

Recipient’s name and addressIn the area next to the arrow, print or type the last name ofthe person to whom you made the payment, followed bythe first name and initials. Directly below the name, enterthe person’s address, including the province, territory, orU.S. state, Canadian postal code or American zip code, andcountry.

Employer’s or payer’s nameEnter your operating or trading name in the space providedon each slip.

8

YearEnter the four digits of the calendar year in which youmade the payment to the recipient.

Box 12 – Social insurance numberEnter the social insurance number (SIN) that is shown onthe SIN card of the person to whom you made the payment.For more information on reporting this number, see “Socialinsurance number (SIN),” in Chapter 1.

Box 14 – Recipient’s numberYou can enter an employee or payroll number. However,using this number is optional.

Box 16 – Pension or superannuationEnter the taxable part of annuity payments you paid to anemployee or retired employee out of, or under, asuperannuation or pension fund or plan includingdisability benefits paid in the form of a life annuity.Disability benefits paid out of a superannuation or pensionplan should be declared in box 28, “Other income,” of theT4A slip.

You may have paid superannuation or pension benefitsfrom an employee benefit plan for services that a personrendered in a period during which the person did notreside in Canada. If you paid the benefits periodically,report the amount in box 16. These payments cannot betransferred to a registered pension plan (RPP) or RRSP.

Unregistered pension plan – You have to identify pensionbenefits you paid from a pension fund or plan that is notregistered. In the footnotes area, enter “Box 16,Unregistered $ .” In box 38, enter code ”09.” Thesebenefits cannot be transferred to a registered plan.

Status Indian – Pension or superannuation is usuallyexempt from income tax when a person receives it as aresult of employment income that was exempt from tax. Ifpart of the employment income was exempt, then a similarpart of these amounts is also. Include the exempt part in thefootnotes area. Enter “Box 16, Status Indian (exemptincome) $________.” In box 38, enter code ”14.”

Box 18 – Lump-sum paymentsIn box 18, enter the following payments:

n the taxable part of a single payment out of a pensionfund or plan because of a:

– withdrawal from the plan, retirement fromemployment, or death of an employee or formeremployee; or

– termination of, amendment to, or modification of theplan.

n the taxable part of a single payment out of a deferredprofit sharing plan (DPSP) due to a withdrawal from theplan, retirement from employment, or death of anemployee or former employee.

If you include lump-sum payments out of RPPs and DPSPsaccrued to December 31, 1971, in the footnotes area, enter

“Box 18, Accrued to December 31, 1971 $ .” In box 38,enter code ”10.”

Direct transfers – Do not report direct transfers of RPPlump-sum payments to RRSPs, RRIFs, or other RPPs thatare transferred according to subsections 147.3(1) to (8) ofthe Income Tax Act. Similarly, do not report direct transfersof DPSP lump-sum payments to RPPs, RRSPs, orother DPSPs that are transferred according tosubsection 147(19) of the Act. You do not have to report asincome a lump-sum amount directly transferred accordingto these subsections. Also, the receiving carrier should notissue receipts. You can use Form T2151, Direct Transfer of aSingle Amount Under Subsection 147(19) or Section 147.3, todocument these direct transfers.

Amounts not eligible for transfer – Amounts that aretransferred, which are more than the amounts allowedunder subsections 147.3(1) to (8) or 147(19) of the Act areconsidered income in the year that the transfer takes place.Report such amounts in box 18. The receiving carriershould issue a receipt for these excess transfers.

When you pay a single amount out of an RPP to anindividual or you transfer such an amount that we considerto be income, in the footnotes area, enter “Box 18, RPP–noteligible for transfer $________.” In box 38, enter code ”08.”

Deferred profit sharing plan (DPSP) – Use box 18 to reportthe total of amounts you allocated or reallocated in the yearunder a DPSP or a revoked plan (to a person described inparagraph 147(2)(k.2) of the Income Tax Act) for:

n employer contributions made to the plan afterDecember 1, 1982; or

n amounts forfeited in the plan if these amounts arewithdrawn from the plan during the year.

If you allocated an amount under subsection 147(10.3) ofthe Income Tax Act in a previous year and you made thepayment in the current year, you have to report the amountof the payment. In the footnotes area, enter “Box 18,DPSP-not eligible for transfer $_______.” In box 38, entercode ”08.”

Employee benefit plan (EBP) – You may have paidsuperannuation or pension benefits from an employeebenefit plan for services that a person rendered in a periodduring which the person did not reside in Canada. If youpaid the benefits in a lump sum, report the amount inbox 18. You can transfer the amount to an RPP or RRSPunder paragraph 60(j) if the recipient or the recipient’sspouse performed the services for which you made thepayment. If you made such a transfer, in the footnotes area,enter “Box 18, Benefits for non-resident services transferredunder paragraph 60(j) $________.” In box 38, entercode ”02.”

Non-registered plan – You have to identify pensionbenefits you paid from a pension fund or plan that is notregistered. In the footnotes area, enter “Box 18,Unregistered $________.” In box 38, enter code ”09.” Youcannot transfer these benefits to a registered plan.

9

Status Indian – A lump-sum payment is usually exemptfrom income tax when a person receives it as a result ofemployment income that was exempt from tax. If part ofthe employment income was exempt, then a similar part ofthis amount is also. Include the exempt part in the footnotesarea. Enter “Box 18, Status Indian (exempt income)$________.” In box 38, enter code ”14.”

For more details, see “Lump-sum payments,” in Chapter 3.

Box 20 – Self-employed commissionsEnter the amount of commission you paid to anindependent agent.

Box 22 – Income tax deductedEnter the total income tax you deducted from therecipient’s remuneration during the year. This includes thefederal, provincial (except Quebec), and territorial taxesthat apply. Leave the box blank if you did not deduct tax.

Do not include an amount you withheld under theauthority of a garnishee or a requirement to pay whichapplies to the employee’s previously assessed tax arrears.

Box 24 – AnnuitiesEnter the total annuity payments under anincome-averaging annuity contract (IAAC), and the yearlytaxable part of other annuity payments.

Enter annuity payments from a life annuity which waspurchased from the proceeds of a Life Income Fund (LIF).

If you include IAAC payments in this box, in the footnotesarea, enter: “Box 24, IAAC $________.” In box 38, entercode ”10.”

If you include instalment or annuity payments under aDPSP, in the footnotes area, enter “Box 24, DPSP annuityor instalment payments $________.” In box 38, entercode ”15.”

When you report annuity payments from other sources onthe T4A slip, follow these guidelines:

n Report annuity payments from a superannuation orpension fund or plan (other than a life annuity) in box 16.

n In box 28, report the proceeds of disposition (or deemeddisposition) of an IAAC.

For more details, see Information Circular 77-1, DeferredProfit Sharing Plans.

NotesReport on a T5 slip the annuity payments for accruedincome from a life insurance policy that you includewhen you calculate a person’s income under theprovisions of section 12.2 of the Income Tax Act.

Report annuity payments to a non-resident on anNR4 slip.

Box 26 – Eligible retiring allowancesEnter the amount of retiring allowances (includingseverance pay) eligible for transfer to an RPP or RRSP.

Status Indian – A retiring allowance is usually exempt fromincome tax when a person receives it as a result ofemployment income that was exempt from tax. If part ofthe employment income was exempt, then a similar part ofthese amounts is also. Include the exempt part in thefootnotes area. Enter “Box 26, Status Indian (exemptincome) $________.” In box 38, enter code ”14.”

NoteFor more information, see “Retiring allowances,” inChapter 3.

Box 27 – Non-eligible retiring allowancesEnter the amount of retiring allowances (includingseverance pay) not eligible for transfer to an RPP or RRSP.

NoteAn amount of retiring allowance is not eligible fortransfer to an RPP or RRSP when it is more than the limitpermitted by the Income Tax Act. For more information,see “Retiring allowances,” in Chapter 3.

Status Indian – A retiring allowance is usually exempt fromincome tax when a person receives it as a result ofemployment income that was exempt from tax. If part ofthe employment income was exempt, then a similar part ofthese amounts is also. Include the exempt part in thefootnotes area. Enter “Box 27, Status Indian (exemptincome) $________.” In box 38, enter code ”14.”

NoteIf an employee is paid a retiring allowance of $60,000 ofwhich $40,000 is eligible for transfer, enter $40,000 inbox 26, and $20,000 in box 27 of the T4A slip.

Box 28 – Other incomeEnter the following types of payments in box 28:

1. Annuity payments from an annuity that an individualbought with a refund of premiums from a deceasedannuitant’s RRSP – For more information on this typeof annuity, see Interpretation Bulletin IT-500, RegisteredRetirement Savings Plans – Death of an Annuitant(paragraphs 27 and 28).

2. Payments under a revoked DPSP – In the footnotesarea, enter “Box 28, Payments from a revoked DPSP$________.” In box 38, enter code “23.”

3. Any fees or other amounts paid to Canadian residentsfor services from which you deducted income tax –Report any other amount from which you havededucted income tax and which you do not have toreport elsewhere on a T4A or other information return.

NoteFederal government departments, agencies, and Crowncorporations issue information slips for contractpayments of more than $500 in a year, made for servicesor mixed goods and services.

4. The proceeds of disposition or deemed proceeds ofdisposition of an income-averaging annuity contract(IAAC).

10

5. Research grants – In the footnotes area, enter “Box 28,Research grants $________.” In box 38, enter code ”04.”

Scholarships, fellowships, bursaries, and prizes – In thefootnotes area, enter “Box 28, Scholarships, bursaries, orfellowships $________.” In box 38, enter code “05.”

For more information, see Interpretation Bulletin IT-75,Scholarships, Fellowships, Bursaries, Prizes, and ResearchGrants.

6. Certain payments made under a wage-loss replacementplan, except for some payments you made under aninsured wage-loss replacement plan, even if you madea contribution to the plan – To find the types ofpayments you should report, see InterpretationBulletin IT-54, Wage Loss Replacement Plans – Changes inPlans Established Before June 19, 1971, and InterpretationBulletin IT-428, Wage Loss Replacement Plans. In thefootnotes area, enter “Box 28, Income from wage-lossreplacement plan, not fully funded by employeepremiums $________.” In box 38, enter code “07.”

Status Indian – Wage-loss replacement plan benefitsare usually exempt from income tax when a personreceives them as a result of employment income thatwas exempt from tax. If part of the employment incomewas exempt, then a similar part of these amounts isalso. Include the exempt part in the footnotes area.Enter “Box 28, Status Indian (exempt income)$________.” In box 38, enter code “14.”

7. Payments under the Labour Adjustment Benefits Act, or abenefit payable under the Appropriation Act tocompensate for loss of office or employment, such as inthe textile and leather-tanning industries.

8. The gross amount of any payment (including apayment to a surviving spouse, heir, or estate) on orafter the death of an employee to recognize theemployee’s service in an office or employment – In thefootnotes area, enter “Box 28, Death benefit $________.”In box 38, enter code ”06.”

9. Benefits from board and lodging, or transportation thata third party (a prime contractor or anothersubcontractor) supplies to employees of subcontractors(e.g., all workers on a site who share commonquarters) – The person who provides the benefits (athird-party payer) has to report them on a T4A slip,unless the benefits are non-taxable allowances forworking at a special work site or remote work location.

If an employee usually lives in a prescribed zone andworks at a special work site in a prescribed zone, reportany non-business travel assistance (including medicaltravel assistance) in box 28. Separate the medical travelfrom the non-business travel. In the footnotes area,enter “Box 28, Medical travel $________.” In box 38,enter code ”16.”

If an employee does not usually live in a prescribedzone but works at a special work site in a prescribed

zone and meets the residency requirements for thenorthern residents’ deductions, do not include in box 28the exempted portion for board and lodging benefitsthe employee receives while working at the specialwork site which is within 30 kilometres from thenearest urban area having a population of at least40,000 persons. In the footnotes area, enter “Specialwork site in a prescribed zone—exempted portion forboard and lodging benefits $________.” In box 38, entercode ”24.”

NoteInclude any GST/HST that applies to the relatedbenefits.

For more information, see “Board, lodging, andtransportation at special work sites and remote worklocations,” in Chapter 2 of the employers’ guidecalled Taxable Benefits, or Interpretation Bulletin IT-91,Employment at Special Work Sites or Remote WorkLocations.

10. Premiums you pay as a contribution to a provincialhealth services insurance plan for a retired employee –See “Premiums under provincial hospitalization,medical care insurance, and certain Government ofCanada plans” in the employers’ guide called TaxableBenefits. In the footnotes area, enter “Box 28, Medicalpremium benefit $________.” In box 38, enter code ”18.”

For more details, see Interpretation Bulletin IT-247,Employer’s Contribution to Pensioners’ Premiums UnderProvincial Medical and Hospital Services Plans.

NoteFor reporting requirements that concern paymentsfrom a retirement compensation arrangement(RCA), see the Retirement Compensation ArrangementGuide, or contact any tax services office or tax centre.

11. Payments under a supplementary unemploymentbenefit (SUB) plan.

12. Benefits of a loan that a person or partnership receivedas a shareholder or related to a shareholder – In thefootnotes area, enter “Box 28, Loan benefit undersubsection 80.4(2) $________.” In box 38, entercode ”17.”

13. Any benefit for employer-provided group term lifeinsurance when the benefit is conferred by a formeremployer or reported by another party on behalf of theemployer or former employer.

14. Disability benefits paid out of a superannuation orpension plan – In the footnotes area, enter “Box 28,Disability benefits paid out of a superannuation orpension plan $________.” In box 38, enter code ”25.”

15. A cash award or prize paid directly from amanufacturer to the employee of a dealer or other salesorganization – For more details, see InterpretationBulletin IT-470, Employees’ Fringe Benefits, and its specialrelease.

11

16. Amounts paid by a trustee in bankruptcy to employeesof a bankrupt corporation, in settlement of unpaid wageclaims filed for wages that the bankrupt employer didnot pay.

NoteThese payments are not subject to payroll deductions(CPP, EI, and income tax).

Box 30 – Patronage allocationsReport all allocations you gave to customers for theirpatronage. This includes payments you made in cash or inkind, by certificate of indebtedness, issue of shares, set-off,assignment, or any other way. Your allocations should be inproportion to the patronage.

Box 32 – Registered pension plan contributions (pastservice)Enter the contributions a former employee made to buypast service. The plan administrator usually completesthe T4A slip when an employer-employee relationship nolonger exists. Include any instalment interest paid forpast-service contributions. Instalment interest is the portionof contributions that represents the amount charged to buypast service over time. In the footnotes area, enter “Box 32,Pre-1990 past service $________.” In box 38, entercode ”26.”

Box 34 – Pension adjustmentEnter, in dollars only, the amount of pensionadjustment (PA) an employee has under an RPP during aperiod of leave or reduced services. Do this in the year forwhich you report the PA as the pension plan administratorfor a multi-employer plan (MEP). See the PensionAdjustment Guide for more information.

Box 36 – Pension plan registration numberEnter the registration number we issued for the registeredplan or DPSP in which an employee participates, and whichgave rise to the PA you are reporting. You have to reportthe pension plan number, even if your plan requires onlyemployer contributions. If you made contributions to morethan one plan for the employee, enter only the number ofthe plan under which the employee has the largest PA.

Enter registration numbers (not more than three) for anyadditional plans on lines 71, 72, and 73 of theT4A Summary form.

Footnote codes and explanationUse this area on the T4A slip to record footnotes when youreport certain kinds of income or identify transfers of fundsunder certain sections of the Income Tax Act.

Box 38 – Footnote codesWhen you enter a written footnote in the “Footnote codesand explanation” area, you have to enter the correspondingfootnote code in box 38. If there is no written footnote, leavebox 38 blank, or enter ”00.” If you have only one footnote

code, record it in box 38. If you have more than one code,enter code “13” in box 38. Also record all the relevant codesin the “Footnote codes and explanation” area at the bottomof the T4A slip.

The following is a list of the codes and the T4A slip incomeboxes to which they apply.

Code Explanation and use

00 No footnote code required.

02 Transfer of funds, paragraph 60(j)—use this codeto describe a transfer amount in box 18.

04 Research grant—box 28 only.

05 Scholarships, bursaries, or fellowships—box 28only.

06 Death benefit—box 28 only.

07 Income from wage-loss replacement plan; not fullyfunded by employee premiums—box 28 only.

08 RPP or DPSP—not eligible for transfer—use thiscode to describe an amount in box 18.

09 Unregistered plan—use this code to describe theamount in box 16 or 18.

10 Amounts reported in footnotes for lump-sumpayments accrued before December 31, 1971, andIAAC annuities—use this code to describe theamount in box 18 or 24.

13 Multiple footnotes—use this code if more than onecode applies.

14 Status Indians with exempt income—use this codeto describe any amounts shown in boxes 16, 18, 26,and 28.

15 Instalment or annuity payments under aDPSP—box 24 only.

16 Medical travel—box 28 only.

17 Loan benefit (under subsection 80.4(2))—box 28only.

18 Medical premium benefit—box 28 only.

19 Group term life insurance benefit—box 28 only.

22 RESP accumulated income payments paid tosomeone other than the subscriber or subscriber’sspouse—box 40 only.

23 Payments from a revoked DPSP—box 28 only.

24 Special work site (enter only the exempted portionthat is related to work sites which are within30 kilometres from the nearest urban area having apopulation of at least 40,000 persons)—box 28 only.

25 Disability benefits paid out of a superannuation orpension plan—box 28 only.

26 Pre-1990 RPP past-service contributions—box 32only.

12

Box 39 – Government use onlyLeave this box blank.

Box 40 – RESP accumulated income payments(If you are not a promoter, leave this box blank.)

If you are the promoter of a registered education savingsplan (RESP) and you paid RESP accumulated incomepayments (other than a refund of contributions, aneducational assistance payment, an amount transferred toanother RESP, or a payment made to a designatededucational institution in Canada generally providingcourses at a post-secondary level) to a subscriber of theplan, report this amount in box 40 of the T4A slip.

In addition, if you pay the RESP accumulated incomepayments to someone other than the subscriber orsubscriber’s spouse (if after the death of the subscriber andsubscriber’s spouse, there is no other subscriber), in thefootnotes area enter “Box 40, RESP accumulated incomepayments paid to someone other than the subscriber orsubscriber’s spouse $________.” In box 38, enter code ”22.”

NoteAccumulated income payments may be subject to boththe regular tax on lump-sum payments and anadditional tax of 20% (12% for Quebec).

For more information on RESPs, get the information sheetcalled Registered Education Savings Plans (RESPs).

Box 42 – RESP educational assistance payments(If you are not a promoter, leave this box blank.)

If you are the promoter of a registered education savingsplan (RESP), and you paid RESP educational assistancepayments (amount other than a refund of contributions) toor for an individual to help further his or her education at apost-secondary school level, report this amount in box 42of the T4A slip.

For more information on these payments, get theinformation sheet called Registered Education Savings Plans(RESPs).

Box 46 – Charitable donationsEnter the amount you deducted from the employees’earnings for donations to registered charities in Canada.

Box 61 – Business NumberEnter the 15-digit Business Number you use to send usyour employees’ deductions. This number appears in thetop left corner of the statement of account that we send toyou each month.

Your Business Number does not appear on copies 2 and 3of the T4A slip that you give to the recipients.

Completing the T4A Summary formSee the back of this guide for a sample T4A Summary form.

Use summary forms to report the totals of the amounts thatyou reported on the T4A slips.

Before you start to enter information on the summary form,please keep the following points in mind:

n If you did not receive a personalized T4A Summaryform, get a blank one from any tax services office or taxcentre. Enter your Business Number, operating ortrading name, and address.

n Report amounts in Canadian dollars and cents.

n If you file a summary form for a taxation year other thanthe one printed on the form, cross out the year in theupper-left corner, and enter the correct year directlybelow it.

n Complete a separate summary form for each one of yourpayroll deductions accounts. Ensure each summary formis in front of the related slips (do not use staples).

n Make sure the totals you report on your summary formagree with the totals you report on your slips. Errors oromissions can cause unnecessary processing delays.

n You can make a photocopy of the original T4A Summaryform, and use it as your working copy. Keep the workingcopy for your records. Send the original T4A Summaryform along with copy 1 of the related slips to the OttawaTechnology Centre. You can find the address on thesummary form.

How to complete the T4A SummaryIn the boxes at the top of the summary form, enter your15-digit Business Number, operating or trading name, andaddress.

YearEnter the two last digits of the calendar year for which youfile the return.

Line 16 – Pension or superannuationAdd the amounts in box 16 on all T4A slips. Enter the totalon line 16.

Line 18 – Lump-sum paymentsAdd the amounts in box 18 on all T4A slips. Enter the totalon line 18.

Line 20 – Self-employed commissionsAdd the amounts in box 20 on all T4A slips. Enter the totalon line 20.

Line 22 – Total tax deductions reported (per T4A slips)Add the amounts in box 22 on all T4A slips. Enter the totalon line 22.

Line 24 – AnnuitiesAdd the amounts in box 24 on all T4A slips. Enter the totalon line 24.

Line 26 – Eligible retiring allowancesAdd the amounts in box 26 on all T4A slips. Enter the totalon line 26.

13

Line 27 – Non-eligible retiring allowancesAdd the amounts in box 27 on all T4A slips. Enter the totalon line 27.

Line 28 – Other incomeAdd the amounts in box 28 on all T4A slips. Enter the totalon line 28.

Line 30 – Patronage allocationsAdd the amounts in box 30 on all T4A slips. Enter the totalon line 30.

Line 32 – RPP contributions (past service)Add the amounts in box 32 on all T4A slips. Enter the totalon line 32.

Line 34 – Pension adjustmentAdd the amounts in box 34 on all T4A slips. Enter the totalon line 34.

Line 40 – RESP accumulated income paymentsAdd the amounts in box 40 on all T4A slips. Enter the totalon line 40.

Line 42 – RESP educational assistance paymentsAdd the amounts in box 42 on all T4A slips. Enter the totalon line 42.

Lines 71, 72, and 73 – Registration numbers for RPPEnter the seven-digit registration numbers that we gaveyou, up to a maximum of three.

Lines 74 and 75 – Canadian-controlled privatecorporations or unincorporated employersEnter the social insurance numbers of any proprietors orprincipal owners.

Lines 76 and 78 – Person to contact about this returnEnter the name and telephone number of a contact personthat we can call to get or clarify information you reportedon the summary form.

Line 82 – RemittancesEnter the amount you remitted for the year under yourBusiness Number.

DifferenceSubtract line 82 from line 22. Enter the difference in thespace provided. If there is no difference between the totaldeductions you reported and the amount you remitted forthe year, leave lines 84 and 86 blank. We do not refund orcharge a difference of less than $2.

Line 84 – OverpaymentIf the amount on line 82 is more than the amount on line 22(and you do not have to file another type of return for thisaccount), enter the difference on line 84. Send us a noteindicating the reason for the overpayment and whether youwant us to transfer this amount to another account, anotheryear, or refund the overpayment to you.

Line 86 – Balance dueIf the amount on line 22 is more than the amount on line 82,enter the difference on line 86.

Amount enclosedIf you have a balance due, attach to the T4A Summary forma cheque or money order payable to the Receiver Generalfor Canada for the balance owing. If you remit yourpayment late, any balance owing may be subject topenalties and interest at the prescribed rate.

Line 88 – Number of T4A slips filedEnter the total number of all T4A slips that you areincluding with the T4A Summary form.

T4A slips with a United States addressIn the space to the right of line 88, enter the number ofT4A slips you are including for individuals with U.S.addresses. File these slips at the end of the return, after theT4A slips for individuals with Canadian addresses.

CertificationA current officer of the business has to sign theT4A information return to show that the information iscorrect and complete.

ReminderIf you file on paper, send the original summary form andcopy 1 of the related T4A slips to:

Ottawa Technology CentreCanada Customs and Revenue Agency875 Heron RoadOttawa ON K1A 1G9

If you file on magnetic media (cartridge or diskette), donot submit copy 1 of the slips or summary form.

Death benefitsA death benefit is the gross amount of any payment(including a payment to a surviving spouse, heir, or estate)on or after the death of an employee to recognize theemployee’s service in an office or employment.

Death benefits are not pensionable or insurable. Do notdeduct Canada Pension Plan contributions or EmploymentInsurance premiums. However, you have to withholdincome tax.

Income taxIf you pay a death benefit to a surviving spouse or heir, thatperson may be able to deduct part of this payment (to amaximum of $10,000) when he or she files a tax return. Donot deduct income tax from this part of the payment. Formore information, see Interpretation Bulletin IT-508, DeathBenefits.

Chapter 3 – Special Payments

14

Use the withholding rates for lump-sum payments shownlater in this chapter under the heading “Withholding ratesfor lump-sum payments,” to deduct income tax from therest of the death benefit. Report the total amount of thepayment on the T4A slip.

Lump-sum paymentsFor information on how to report lump-sum payments, seethe instructions for box 18, “Lump-sum payments,”box 26, ”Eligible retiring allowances,” andbox 27, ”Non-eligible retiring allowances,” under“Completing the T4A slip,” in Chapter 2.

Income taxYou have to deduct income tax from a lump-sum paymentthat is a retiring allowance you pay directly to anemployee:

n on retirement;

n as compensation for loss of office or employment; or

n in recognition of long service, but not out of or under asuperannuation fund or plan.

The above payments are reported in box 26, “Eligibleretiring allowances,” and in box 27, “Non-eligible retiringallowances,” of the T4A slip.

You also have to deduct income tax from lump-sumpayments that are any of the following:

n the proceeds from the surrender, cancellation, orredemption of an income-averaging annuity contract(IAAC);

n from a registered retirement savings plan (RRSP) or aplan referred to in subsection 146(12) of theIncome Tax Act as an amended plan;

n from a registered retirement plan (RPP) (the pensionincome credit does not apply on these payments); or

n more than the minimum amount you have to pay to theoriginal annuitant under a registered retirement incomefund (RRIF).

If you pay a lump-sum payment (e.g., a refund ofpremiums) to a deceased annuitant’s spouse, you do nothave to deduct income tax.

The above payments are reported in box 18, “Lump-sumpayments,” of the T4A slip.

Deduct income tax from lump-sum payments from aretirement compensation arrangement (RCA). Report thesepayments in box 16, “Distributions,” of the T4A-RCA slip,Statement of Amounts Paid From a Retirement CompensationArrangement (RCA).

Withholding rates for lump-sum paymentsUse these federal and provincial composite rates (except forQuebec):

n 10% (5% for Quebec) if the payment is not more than$5,000;

n 20% (10% for Quebec) if the payment is more than $5,000but not more than $15,000; and

n 30% (15% for Quebec) if the payment is more than$15,000.

Since the above rates are only estimates, recipients mayhave to pay additional tax on these amounts when they filetheir tax returns. To avoid this situation, if an employee orrecipient requests it, you can:

n calculate the annual tax to deduct from the recipient’syearly remuneration, including the lump-sum payment(see “Step-by-step calculation of tax deductions” inPart A of the Payroll Deductions Tables);

n calculate the annual tax to deduct from the recipient’syearly remuneration, not including the lump-sumpayment; and

n subtract the second amount from the first amount.

The result is the amount you should deduct from thelump-sum payment.

If you make payments out of deferred profit-sharing plans(DPSP), contact any tax services office or tax centre to learnhow to deduct income tax. For information on how toreport these payments, see the instructions for boxes 18, 24,and 28 under “Completing the T4A slip,” in Chapter 2.

Do not deduct income tax from a lump-sum payment if arecipient’s total earnings received and receivable during thecalendar year, including the lump-sum payment, are lessthan the “claim amount” on the employee’s Form TD1,Personal Tax Credits Return. This does not apply tonon-residents.

Retroactive lump-sum paymentsCertain lump-sum payments totaling $3,000 or more (notincluding interest) are eligible for a special tax calculation.The payments must have been paid to an individual for oneor more preceding years throughout which the individualwas a resident of Canada. The payments must have beenpaid after 1994, and relate to years 1978 and later.

Eligible sources of income are:

n Income from an office or employment received under theterms of an order or judgment of a competent tribunal,an arbitration award, or an agreement to terminate alegal proceeding (including amounts received asdamages).

15

n Employment Insurance or Unemployment Insurancebenefits.

n Superannuation or pension benefits (other thannon-periodic benefits such as lump-sum withdrawals).

n Spousal or child support payments.

n Wage-loss replacement benefits.

The payer has to provide the following information inwriting to the recipient:

n The year in which the lump-sum payment was made tothe recipient.

n A complete description of the lump-sum payment, andthe circumstances that required it to be paid.

n The total amount of the lump-sum payment, including abreakdown between the principal and the interestelement, if any, of the payment.

n The principal amount of the lump-sum payment thatrelates to the current and each of the preceding yearscovered by the payment.

The payer can provide all the information indicated aboveto the recipient by using Form T1198, Statement of QualifyingRetroactive Lump-Sum Payment.

The recipient has to send Form T1198 to us, and request thespecial tax calculation in his or her income tax return.

For more information, contact any tax services office or taxcentre.

Transfer of fundsA recipient can transfer a lump-sum payment out of an RPPor DPSP to an RPP or DPSP, or to an RRSP. If you transferthe full amount directly (not paid to the recipient) toanother RPP, RRSP, or DPSP, do not deduct income tax.

We use Form T2151, Direct Transfer of a Single Amount UnderSubsection 147(19) or Section 147.3, to instruct administratorsto directly transfer the lump-sum payment on a recipient’sbehalf. The receiving carrier should not issue receipts. Thetransferring carrier has to keep the necessary documents tosupport the transfer.

The Income Tax Act sometimes limits how much of an RPPlump-sum payment you can transfer directly to suchregistered plans. If an amount you transfer is more thanthese limits, the recipient has to include the excess transferin his or her income and you have to deduct income tax onthe amount you did not directly transfer. Report theamount in box 18 of a T4A slip. You cannot transfer thisamount to another RPP, RRSP, or DPSP. In the footnotesarea, enter “Box 18, Not eligible for transfer $ .” Inbox 38, enter code “08.”

NoteThe requirement to report excess transfers (amounts notdirectly transferred) from defined-benefit provisions ofregistered pension plans to an RRSP, RRIF, or themoney-purchase provision of an RPP applies equally inall provinces. However, the requirement for withholdingtaxes from the excess amounts you pay or transfer isdifferent in Ontario, New Brunswick, andNewfoundland.

In all provinces except Ontario, New Brunswick, andNewfoundland, provincial legislation allows you to paythe excess amounts to the beneficiaries in cash. In suchcases, you have to withhold tax from the total to be paid,and you also have to report such withholdings on theT4A slip to report the excess transfer amount.

In Ontario, New Brunswick, and Newfoundland,provincial legislation requires you to transfer the entireexcess payment into an RRSP (in the case ofNew Brunswick, into a locked-in RRSP). In thesethree provinces, we will permit such transfers to RRSPswithout withholdings. You have to issue T4A slips forthe excess amount you transferred, and inform therecipient that this amount constitutes income in the yearyou made the transfer, and that he or she must pay anytax owing on assessment. In the footnotes area, enter“Box 18, Not eligible for transfer $ .” In box 38,enter code “08.”

For more information on reporting excess amounts orwithholdings on these amounts, contact any tax servicesoffice.

You cannot transfer to an RPP any benefits and lump-sumpayments you paid after February 15, 1984, from a pensionfund or plan that is not registered under the Income Tax Act.

For more information about transferring funds betweenplans, see interpretation bulletin IT-528, Transfers of FundsBetween Registered Plans.

Patronage paymentsPatronage payments include:

n certificates of indebtedness;

n amounts credited towards the balance a recipient mayowe the payer of the patronage; and

n shares of a corporation that an individual receivesbecause of a patronage payment.

You have to apply a withholding tax of 15% on the value ofpatronage payments that Canadian residents receive in ayear. This withholding tax applies to the payment or to thetotal of several payments you made during the year that aremore than $100.

Complete the remittance voucher at the bottom ofForm PD7A, Statement of Account for Current SourceDeductions, and include it with the deducted amount youare sending to the Receiver General for Canada. Enter allpayments in box 30 of the T4A slip. Enter the income taxyou deducted in box 22.

The withholding tax does not apply to Canadian residentswho are exempt under section 149 of the Income Tax Act.

ExampleYou give Luan a $250 patronage payment. The amount onwhich you apply the 15% withholding tax is $150($250 – $100). The withholding tax is $22.50 ($150 × 15%).Her T4A slip will show the $250 patronage payment inbox 30, and the $22.50 in tax you deducted in box 22.

16

If you need more details, see Interpretation Bulletin IT-362,Patronage Dividends, and Interpretation Bulletin IT-493,Agency Cooperative Corporations.

Retiring allowancesA retiring allowance (also called severance pay) is anamount paid to officers or employees:

n when or after they retire from an office or employment inrecognition of long service; or

n for the loss of office or employment.

Retiring allowances are reported on a T4A slip.

A retiring allowance includes:

n payments for unused sick-leave credits; and

n amounts individuals receive when their office oremployment is terminated, even if the amount is fordamages (wrongful dismissal).

A retiring allowance does not include:

n a superannuation or pension benefit;

n an amount an individual receives as a result of anemployee’s death;

n a benefit derived from certain counselling services;

n payments for accumulated vacation leave not taken priorto retirement;

n pay in lieu of termination notice; and

n damages for violations or alleged violations of anemployee’s human rights awarded under human rightslegislation (these damages are not taxable).

There are situations when a person can transfer all or partof a retiring allowance to an RPP or RRSP.

NoteIf you need more details about the tax measures thataffect people planning to retire, see the pamphlet calledWhen You Retire. You can order copies of this pamphletfor your employees.

A retiring allowance is not pensionable or insurable. Donot deduct Canada Pension Plan contributions orEmployment Insurance premiums from this amount.However, you have to withhold income tax.

Income taxIf you pay a retiring allowance to a resident of Canada,deduct income tax from any part you pay directly to therecipient. Use the lump-sum withholding rates to deductincome tax. We discussed these rates earlier in this chapterunder the heading “Lump-sum payments.”

If you pay a retiring allowance to a non-resident ofCanada, you have to withhold 25% of the retiringallowance (subject to various tax conventions andagreements). Send this amount to the Receiver General forCanada on the non-resident’s behalf. For more information,see Interpretation Bulletin IT-337, Retiring Allowances, andIT-163, Election by Non-Resident Individuals on CertainCanadian Source Income.

Transferring a retiring allowance to an RPPor RRSPAn individual can transfer all or part of a retiring allowancepayment to an RPP or RRSP. The amount that is eligible fortransfer is limited to:

n $2,000 for each year or part of a year before 1996 that theretiree worked for you (or a person related to you);

plus

n $1,500 for each year or part of a year before 1989 of thatemployment in which none of your contributions tothe RPP or DPSP were vested in the employee’s namewhen you paid the retiring allowance. Determine theequivalent number of years of vesting by referring to theterms of the particular plan. The number can be afraction.

NoteIf an employee wants to transfer an eligible amount toan RPP or RRSP, he or she is no longer required tocomplete any form for tax deduction waiver.

However, if an employee wants to have a reduction intax deductions on the non-eligible amount to transfer,he or she is required to get a letter of authority from anytax services office. For more information, see “Letter ofauthority,” in Chapter 4 of the employers’ guide calledPayroll Deductions (Basic Information).

ExampleBruno is your employee. In November 2000, you pay him aretiring allowance of $42,000. Bruno worked for you from1979 to 2000 (22 years, including part-years of service).According to the terms of the pension plan, Bruno’scontributions are not vested in the pension plan, therefore,you can only reimburse his contributions to the plan.

Calculate the amount of retiring allowance eligible fortransfer, as follows:

n $2,000 × 17 years, including any part-yearsof service before 1996* (from 1979 to 1995) ......... $34,000

plus

n $1,500 × 10 years, including any part-yearsof service before 1989 (from 1979 to 1988)........... $15,000

Total eligible for transfer ......................................... $49,000

Bruno is allowed to transfer $42,000, the total amount ofretiring allowance you paid to him, to an RPP or RRSP.

Since the total amount of the retiring allowance is eligiblefor transfer, report $42,000 in box 26 of the T4A slip. Leavebox 27 blank.

*NoteYou can no longer transfer $2,000 per year of service toan RPP or RRSP for 1996 and following years.

17

How to report retiring allowances that arepaid over a number of yearsAn employee can choose to receive his or her retiringallowance payable by yearly instalments.

ExampleIn 2000, an employee is paid a retiring allowance of $60,000,of which $40,000 is eligible for transfer. If the employeechooses to receive the retiring allowance in four yearlyinstalments of $15,000, report the amounts as follows:

Year Amountpaid

Amount eligiblefor transfer

(box 26)

Amount noteligible for

transfer (box 27)

2000 $15,000 $15,000 nil

2001 $15,000 $15,000 nil

2002 $15,000 $10,000 $5,000

2003 $15,000 nil $15,000

Total $60,000 $40,000 $20,000

The employee does not have to transfer the eligibleamounts for the years in which they were received. Forinstance, in the above example the employee could chooseto not transfer any amounts in 2000 and 2001. Then, in2002 and 2003, he or she could transfer up to $15,000 to anRRSP or RPP. The maximum amount that can be deductedfor a transfer is restricted to the amount of retiringallowance received and included in income for the year.

Employees no longer have to consider deductions for RPPor RRSP contributions when calculating minimum tax. Formore information about retiring allowances, see the GeneralIncome Tax and Benefit Guide and the pamphlet called WhenYou Retire.

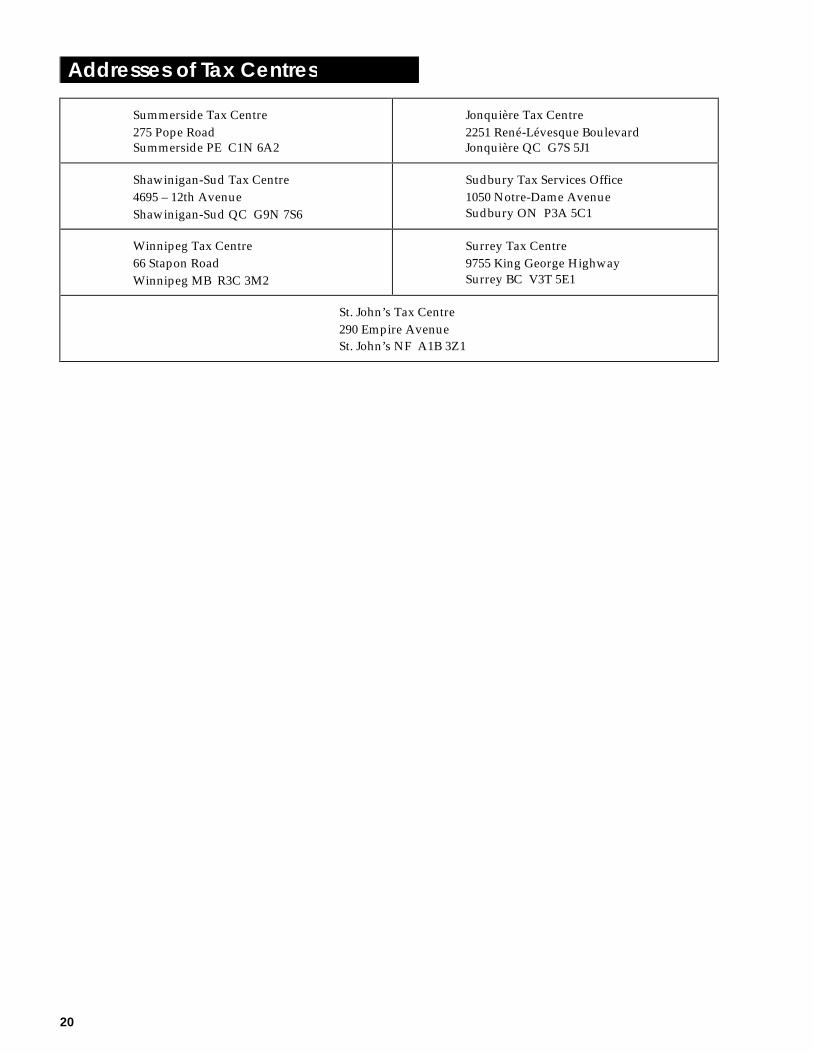

For information on how to report retiring allowances, seethe instructions for box 26, “Eligible retiring allowances,”and box 27, “Non-eligible retiring allowances,” under“Completing the T4A slip,” in Chapter 2 and InterpretationBulletin IT-337, Retiring Allowances.

20

Summerside Tax Centre275 Pope RoadSummerside PE C1N 6A2

Jonquière Tax Centre2251 René-Lévesque BoulevardJonquière QC G7S 5J1

Shawinigan-Sud Tax Centre4695 – 12th AvenueShawinigan-Sud QC G9N 7S6

Sudbury Tax Services Office1050 Notre-Dame AvenueSudbury ON P3A 5C1

Winnipeg Tax Centre66 Stapon RoadWinnipeg MB R3C 3M2

Surrey Tax Centre9755 King George HighwaySurrey BC V3T 5E1

St. John’s Tax Centre290 Empire AvenueSt. John’s NF A1B 3Z1

Addresses of Tax Centres

Notes

Notes

Notes

![[MS-DPSP]: Digest Protocol Extensions · 2 / 23 [MS-DPSP] - v20150630 Digest Protocol Extensions Copyright © 2015 Microsoft Corporation Release: June 30, 2015 Revision Summary Date](https://img.pdfslide.us/doc/110x75/5fe60c7971901a24cb29f5b8/ms-dpsp-digest-protocol-extensions-2-23-ms-dpsp-v20150630-digest-protocol.jpg)