Embed Size (px)

Citation preview

Retirement plan sponsor resourcesExperience MassMutual

FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

E M P LOY E R

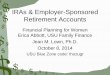

From meeting your fiduciary requirements to educating your employees on investing for their future, there are a series of fundamental actions every plan sponsor can follow to help ensure that its plan is being managed successfully. This guide outlines those actions and provides you with some checklists and

calendars as well as additional resources to help you.

Your financial professional/plan consultant and your MassMutual client service team can assist you with implementing all these keys to successful plan management.

Keys to successful plan management

FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

One of the most complex and challenging responsibilities in business today is the successful management of your company’s retirement plan. And not every retirement plan sponsor has the time and resources to stay on top of it all. Experience our retirement plan resources; we’ve developed tools and services to keep you on track.

A C T I O N T O O L / R E S O U R C E AVA I L A B L E

C O M P L E T E D /I N P R O C E S S

1. Document your fiduciary process. Consider forming a plan committee; establish and monitor procedures for plan decision-making, including a retirement plan committee charter and Investment Policy Statement (IPS), as applicable.

• Annual plan meeting agenda

• Sample IPS• Sample Retirement Plan

Committee Charter

2. Document your actions. Take minutes of all meetings, including alternatives reviewed, factors evaluated, and decisions reached. Limit your minutes to an overview of salient points. “Sometimes, less is more.”

N/A

3. Conduct investment and fee reviews at least annually. Evaluate plan investments according to your established processes, including an IPS. Examine plan fees to ensure reasonableness, taking into account the totality of all fees according to the value of the services the plan receives.

• Your IPS• Investment review

checklist• Required 408(b)(2)

disclosures from each covered service provider

4. Leverage the expertise of the plan’s professionals. Call on the experience of the plan’s financial advisor, plan consultant, and counsel, as applicable.

• Your plan’s advisors

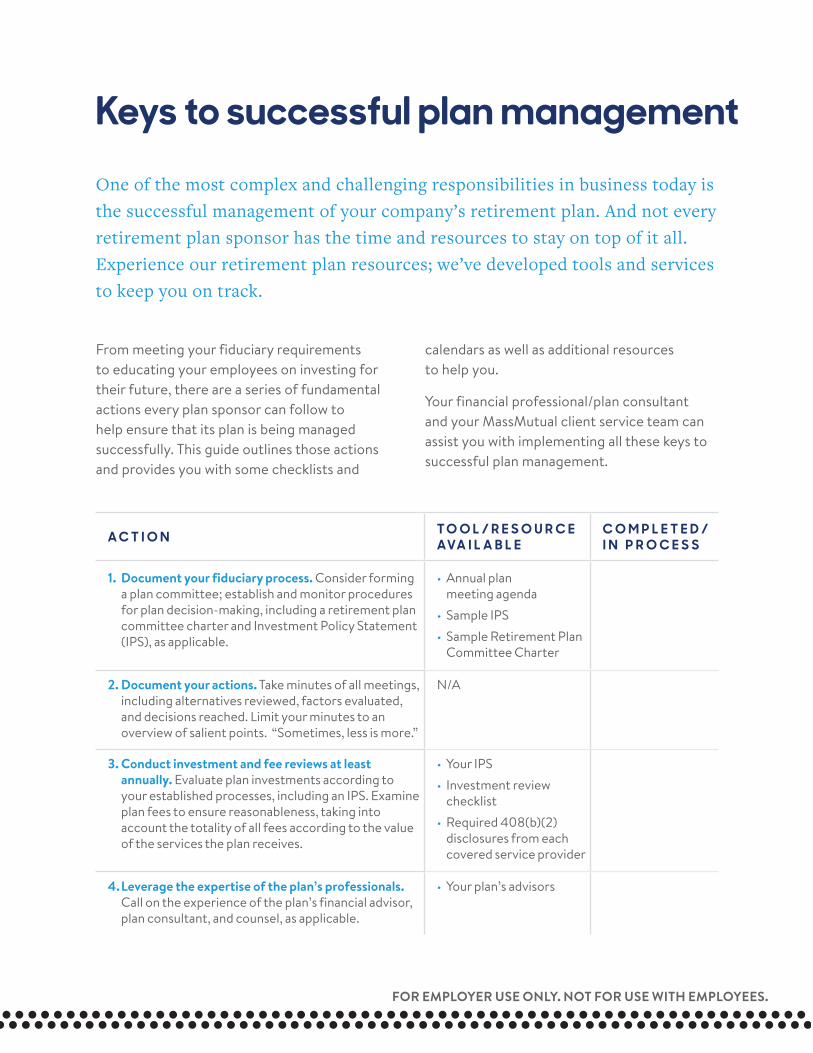

Please realize that in order to effectively mitigate your risk, you need to act according to your plan’s procedural documents which can include a retirement plan committee charter, an investment policy statement and other items.

FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.1

A C T I O N T O O L / R E S O U R C E AVA I L A B L E

C O M P L E T E D /I N P R O C E S S

5. Examine your plan. Review plan design to ensure that it meets your organization’s needs, workforce, and budget. Determine whether recent legal and regula-tory changes offer new opportunities.

• Plan service review• Your MassMutual

Service Team

6. Evaluate the plan’s success. Review key participant ratios, including participants’ retirement readiness, participation, and contribution rates.

• Plan service review• Your MassMutual

Service Team

7. Know the tools available. Familiarize yourself with the wealth of sponsor and participant tools provided by MassMutual and your financial professionals.

• MassMutual’s participant website

• Your MassMutual service team

8. Develop a strategy for participant education and communication. Develop and implement a schedule to employ MassMutual’s tools and resources to help your participants understand the plan and what they need to do to boost their retirement readiness. Document the results of these actions.

Sample plan calendar

9. Check and Adjust. Realize that plans are fluid and should react to changes in participant demographics, organizational priorities, regulatory changes, and other factors. Don’t be afraid to make logical changes according to a prudent process.

N/A

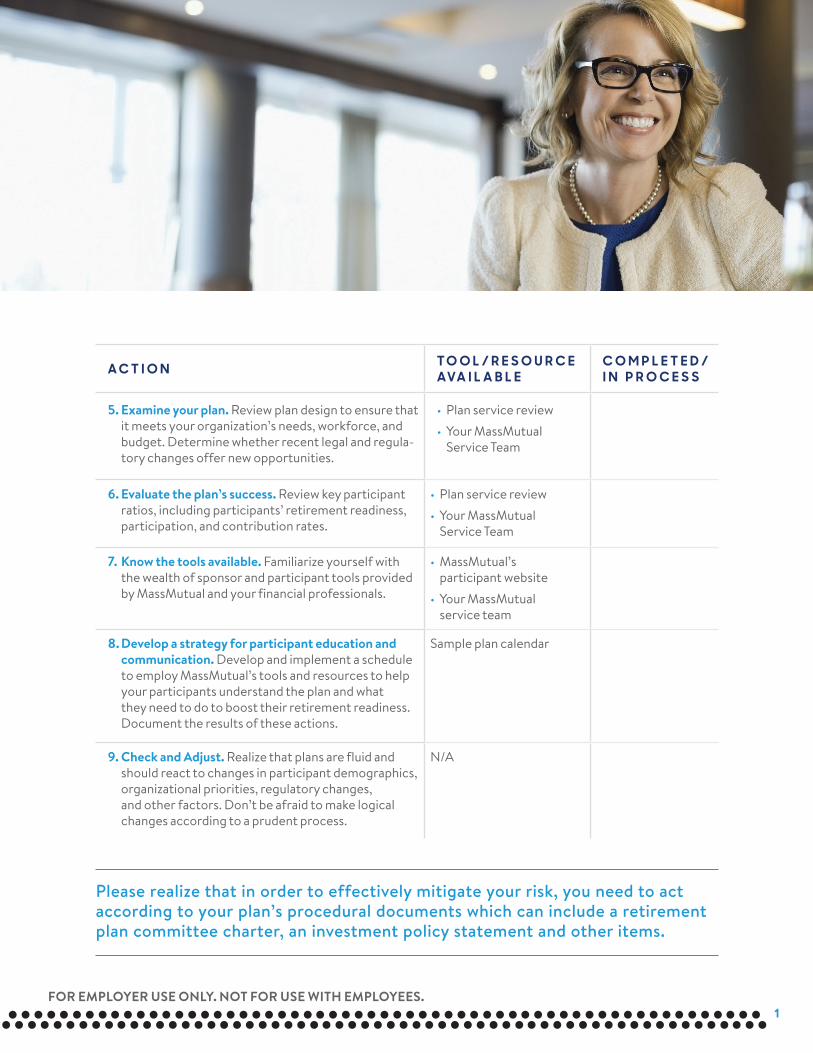

1. Roll call of attendees to ensure the presence of a quorum.

2. Review and approve minutes from previous plan meeting.

3. Review plan investments, including:

• The IPS, to ensure that it serves the plan• Potential changes to the IPS• Compliance with the IPS• Investment performance • Recommended changes to the

investment mix

4. Conduct a plan review, including:

• Recent changes in the law that may affect the plan since the last review

• IRS, DOL, SEC, and other governmental regulations or proposals that may affect the plan

• Potential changes in plan design (Realize that costs associated with studies and other consulting work relating to potential plan changes are “settlor expenses” that cannot be paid from plan assets, either directly or indirectly.)

• Plan amendments made since the last meeting

5. Review participant education and communication, including:

• Retirement readiness (or “PlanHealth”) statistics

• Participation and deferral rates• Asset allocation and contribution data• Results of enrollment meetings and

potential changes for future initiatives• Results of any ongoing

participant educational meetings and campaigns, and potential changes for future initiatives

• Employee enrollment and participant education meeting schedules

6. Review plan operations

• Review service providers’ performance against plan needs and service provider agreements.

• Examine total direct and indirect fees and expenses to ensure reasonableness considering both market forces and the value of the services received by the plan.

• Ensure that plan contributions are being segregated and invested into the plan as soon as possible.

Sample plan meeting agenda

2FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

Your plan meetings are critical times to identify any issues that may have arisen with your plan since your last meeting and to formally implement the actions laid out earlier in this Guide. It’s also important to record topics discussed through the meeting minutes.

3

• Determine whether the plan continues to qualify for relief under ERISA Section 404(c), if applicable.

• Ensure that participants have been provided with all required disclosures including, but not limited to, Investment and Fee Disclosures and the Summary Plan Description.

• Confirm that the plan has received the 408 (b) (2) fee disclosure from all the plan’s covered service providers.

7. Final changes

• Finalize changes to the plan document in the meeting minutes for review and approval at the next meeting.

• Obtain approval from the Board of Directors for plan amendments.

• Finalize changes in responsi-bilities in the meeting minutes for review and approval at the next meeting.

Fiduciary CalendarManaging your plan is a year-round responsibility

A comprehensive retirement plan calendar is an easy way to track your participant communications schedule and important plan management events. To help you more easily track and fulfill your fiduciary obligations, you can populate your own customized calendar with key fiduciary deadlines and reminders by visiting www.fiduciarycalendar.com.

FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

4FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

1. Plan records

• Plan and trust documents, including signed amendments• Summary Plan Description• Summary Annual Report• Loan program, if applicable• Copies of plan meeting minutes

2. Employee communication and education

• Participant disclosures required by law• ERISA 404(c) communications• Plan announcements• Participant communications

3. Plan reporting

• Auditors’ statements, if applicable• Form 5500

4. Service provider information

• Provider’s plan proposal or RFP (request for proposal) response

• Service provider agreements with updates and/or amendments• Cost comparisons• Provider’s Disclosure Statement (Reasonable Contract or

Arrangement under ERISA Section 408(b)(2))

5. Service provider information

• IPS• Documentation used to select investment options• Records of ongoing investment monitoring, including updates to the IPS• Current investment performance updates• Investment review checklist

5FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

Annual due diligence checklist Formal due diligence documents should be updated annually, with the exception of the investment review, which should be updated on a more frequent basis.

6

• Description of investment performance, style shift, or other characteristics considered unacceptable

• Description of how long unacceptable results may occur before action is taken

• Criteria for placing investments on a watch list

• Required investment provider communications regarding current results and corrective action

Investment review checklistHere is a two-part checklist and summary to consider as possible parts of your plan’s investment review. Complete the Plan considerations section for your plan. Then keep a copy of the completed bottom section, Individual plan investment option considerations, for each investment option in your plan.

• Process for consideration of investment option replacement and/or termination

• Experience and qualifications of personnel providing the investment management services to the plan

• Process for consideration of investment manager replacement and/or termination

• General conditions and prevailing trends in the economy, the securities markets, and the mutual fund industry

FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

Your IPS should form the basis for your investment review, which should include contact with your financial professional/plan consultant and investment provider. In addition to the guidelines set forth in the IPS, the following criteria may be helpful:

P L A N C O N S I D E R AT I O N S

7FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

I N D I V I D U A L P L A N I N V E S T M E N T O P T I O N C O N S I D E R AT I O N S

Year to date 1 year 3 year 5 year

Investment

Benchmark 1

Benchmark 2

Peer group

Risk-adjusted returns (available at morningstar.com)

Investment option evaluation criteria• Performance vs. appropriate benchmarks• Performance vs. appropriate peer groups• Risk-adjusted returns

• Consistency of investment strategy• Fee structure and expense ratio in relation

to other alternatives

We strongly recommend you work with your plan’s investment advisor to determine criteria tailored to your specific circumstances. If you don’t use the services of an investment advisor, we believe you should consider retaining one.

For more information, contact your MassMutual service professional or call us at 1-800-874-2502.

Investment option Yes No

Are the objectives still consistent with the plan’s overall investment objectives and goals?

Does this investment option remain diversified as expected?

Does this investment continue to contribute to the overall diversification of the plan portfolio?

In addition to the guidelines set forth in the IPS, the following criteria should be considered for each investment option:

Notes:

8FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

Notes:

9FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.

FOR EMPLOYER USE ONLY. NOT FOR USE WITH EMPLOYEES.© 2017 Massachusetts Mutual Life Insurance Company (MassMutual), Springfield, MA 01111-0001. All rights reserved. www.massmutual.com.RS1743 617 C:RS-42069-00

We created massmutual@work to reach more people with the solutions, guidance, and tools they need to secure their financial

future and protect the ones who matter most. As a recognized leader in retirement and insurance solutions, we are committed

to helping you do more for your employees.

Visit massmutualatwork.com today!