Embed Size (px)

Citation preview

Employee Benefits Market Update: New solutions for a changing environment

Benefits Webinar Series June 25, 2013

Today’s agenda We’ll review the following:

Public and private exchanges

New providers and networks

Funding alternatives

New tools to manage plans and control costs

What to expect in the second half of 2013

Participant questions

Presenters

Anna Willson, Principal – EPIC Employee Benefits

Steve Vilas, Chief Operating Officer – EPIC Employee Benefits

Sarah Dodge, Benefits Technology Consultant – EPIC Employee Benefits

| 2

“Exchanges” – what are they?

On-line marketplaces for purchasing medical and other types of coverage

Public exchanges vs. private exchanges

Public

Offer four plans covering comparable benefits that vary based on % of benefits covered

Range from Bronze plan (60% of costs) to Platinum plan (90% of costs)

In CA all plans available use a closed or narrow network

Covered CA – costs for individual plans increased significantly for young males, less for older participants

Subsidies only available through public exchanges, based on income

Private

Defined contribution approach with 2013 technology

Defined contribution approach allows employer to better manage costs

Marketplace environment shifts benefit decisions from employer to employee

Subsidies not available

Decision support technology to help employees “right size” coverage based on personal needs

| 3

Decision Support Technology– what’s new?

Decision Support Plan comparisons – Ebix/Benergy, PlanSource, Enwisen

Marketplace plan recommendation model

Analyzes health, preferences and finances to recommend benefits

Employer benefits integration – Optum Health, Health Equity

> 1000 ee’s: Workable Solutions, Global Health Engines, Wealth Management Systems

Avatars – Trustnode, Code Baby

Multi-media/video communication – GuideSpark, Jellyvision

| 4

Market outside exchanges Individual and small group marketplace

Carriers Same plans outside public exchanges that are offered in Additional options outside public exchanges Small group options will be more limited due to ACA New/replacement plans being announced Grandfathered plans won’t be affected by some market

reforms Member level rating vs. current age banded rating

19 rating regions, 45 age bands in CA Cost for each family member based on their age, not

employee age Applicable to groups with 50 or fewer EEs in 2014 Applicable to groups with 100 or fewer EEs in 2016

| 5

EPIC initiatives and potential strategies EPIC’s partnership with Liazon

Medical and non-medical options

Premium reimbursement accounts

Stand alone

As an option in a comprehensive defined contribution benefits program

Expanding access

Opening an opportunity for the employer to offer a more competitive benefits package

| 6

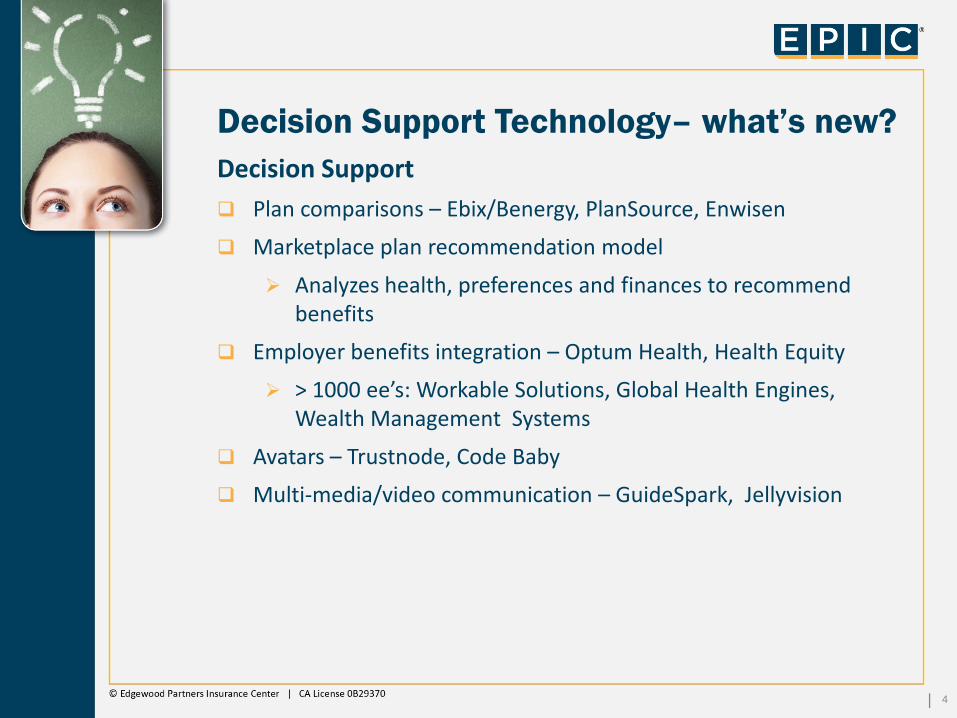

New providers and networks New options becoming available Focus on enhanced quality of care and/or controlling cost Choice vs. cost?

Accountable Care Organizations (ACOs) Groups of doctors, hospitals, and other health care providers, who

come together to give coordinated high quality care, especially to the chronically ill

Goal is to coordinate patient access to care at the right time, while avoiding unnecessary duplication of services and preventing errors

Narrow networks Offer fewer choices in health care providers Goal is to reduce costs by excluding highest cost providers from

networks Patient Centered Medical Homes (PCMH)

A health care setting that targets highest risk patients in each market, with comprehensive care replacing episodic care

Goal is to provide flexible care tailored for local delivery, aimed at patients with complex chronic health conditions

Sutter HMO

| 7

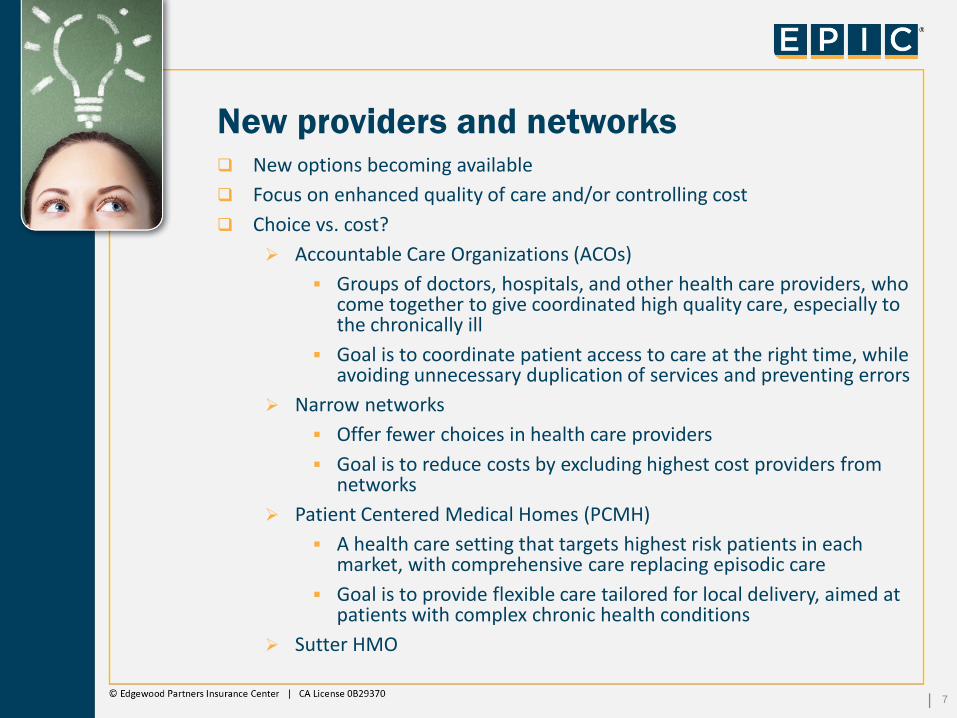

Funding alternatives Fully-insured – employer pays a fixed monthly cost, insurance

carrier maintains all the risk and receives all the profit

Self-funding – employer assumes the risk but carriers provide vehicles to cap that risk

Role and administration may be greater

Level funding – alternative for small to mid-size companies (25-250+) to smooth out the cash flows

Employer chooses the amount of risk to retain

Capping individual claims ($25k to $300k)

Capping overall claims (110% to 125%)

| 8

Advantages of self-funding Plans not bound by state mandates, subject to federal ERISA instead

Allows for more consistency for employers with multi-state populations

Plans have more flexibility over plan design under ACA

Plans not subject to some ACA taxes or state premium taxes

Employer retains plan “profit” in a good year

Employer holds on to reserves (amount set aside to pay for claims after plan termination)

Employer receives claims data allowing more proactive cost strategies

Successful wellness and cost containment efforts directly benefit employer

| 9

Disadvantages of self-funding Risk assumption – employer assumes the risk between a normal

“fully insured” rate and the maximum stop loss amount

Usually 10% - 25% additional risk

Asset exposure – employer’s assets are exposed to any liability against the self-funded plan

Fiduciary responsibility – employer is the fiduciary

Employer takes on additional administrative duties

Unpredictable monthly cash flow

Possible “bad year” with large claimants

| 10

Self-funding trends Smaller groups are embracing self-funding

Access to data

Plan flexibility

Individual and aggregate caps limit exposure

CA involvement

Benefit from successful programs that reduce cost, improve consumerism

51-99 – biggest change and opportunity?

Fully insured vs. self insured “arbitrage”

“Skinny” self-funded plans

What are they?

Will they survive?

Self funding is a multi-year strategy!

| 11

Voluntary benefits market today Health and traditional ancillary carriers entering the voluntary benefit market

Brainstorming new voluntary benefits to meet individual needs head on

Group products vs. individual products

Voluntary Life and Disability coverages continue to be the top sellers

Voluntary products on the rise

Accident

Critical Illness/Cancer

Hospital Indemnity (some HSA compatible)

Long Term Care insurance bundled with life policies

Long Term Care (individual)

Dental and Vision

Legal services/Identity Theft

Auto and Home insurance payroll deducted (one to watch)

Non-traditional voluntary benefits

Employee purchase programs

| 12

Voluntary trends Offering voluntary benefits as part of a strategic business move

In past years, voluntary products were offered mainly by larger employers as a way to increase engagement

Now, organizations of all sizes are broadening their menu of voluntary benefits to offset coverage gaps

Traditional employer paid group dental and vision moving to a voluntary option as employers further need to cut costs/focus on medical spend

Technology

Online enrollment tools (apps, iPads, etc.)

Benefits administration system integration

Enrollers developing own more sophisticated on-line enrollment systems

Private Exchanges

Defined contribution approach

Opportunity to work closely with private exchanges to add additional voluntary products in the future

| 13

New tools to manage plans & control costs Telemedicine

Use of medical information exchanged from one site to another via electronic communications to improve a patient’s clinical health status and access to medical treatment

4 of 5 doctor visits and access to medical treatment can be better handled by phone (AMA)

As little as 2 minutes average wait time to talk to a doctor by phone vs. over 3 weeks average wait to schedule a non-urgent appointment

Assures access in an environment with millions of new participants

Ideal for self-insured clients – positive ROI

Priced on a per call or PMPM basis

Anthem launched for fully insured this month ($49/call)

Available from most carriers for self-funded clients now

Consult A Doctor, TelaDoc, and other third party providers

| 14

New tools to manage plans & control costs Pricing Transparency and Comparison Tools Shop and compare pricing for medical services by location

Doctor reviews and comparisons

Cast Light, Health Care Blue Book, Change HealthCare, My Health and Money, The Leapfrog Group

Carriers have similar proprietary tools

Consumer options:

No cost (limited features)

Subscription based

Employer provided (plans/claims integration)

Ideal for self-insured clients

Identifies savings opportunities

Custom rewards programs for employees who visit in-network doctors

| 15

Benefits technology – what’s new?

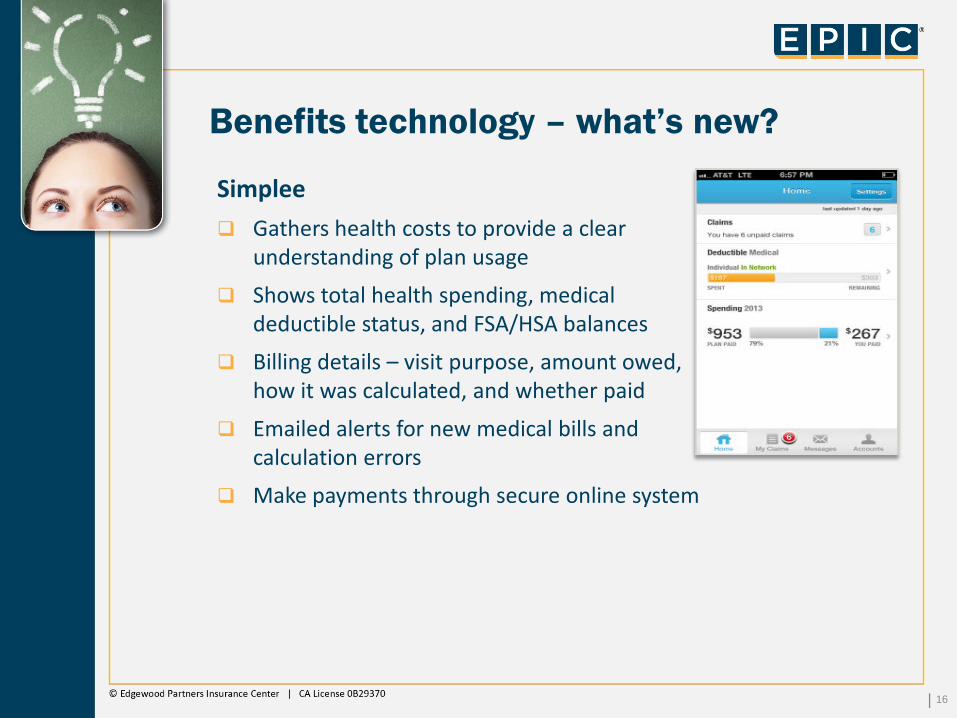

Simplee

Gathers health costs to provide a clear understanding of plan usage

Shows total health spending, medical deductible status, and FSA/HSA balances

Billing details – visit purpose, amount owed, how it was calculated, and whether paid

Emailed alerts for new medical bills and calculation errors

Make payments through secure online system

| 16

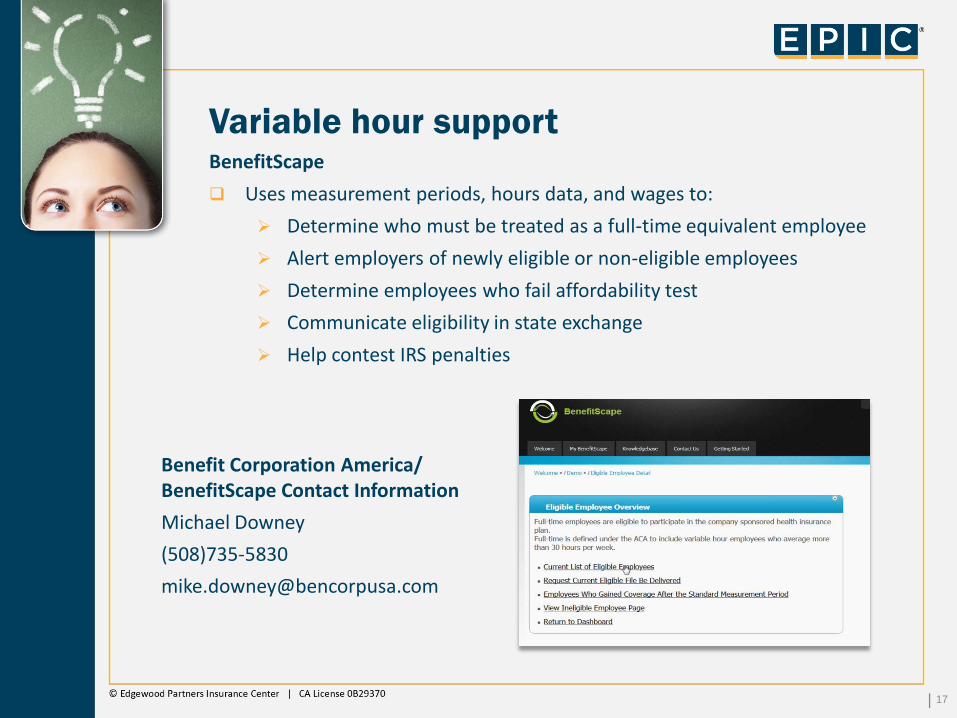

Variable hour support BenefitScape

Uses measurement periods, hours data, and wages to:

Determine who must be treated as a full-time equivalent employee

Alert employers of newly eligible or non-eligible employees

Determine employees who fail affordability test

Communicate eligibility in state exchange

Help contest IRS penalties

| 17

Benefit Corporation America/ BenefitScape Contact Information

Michael Downey

(508)735-5830

Benefits technology – what’s coming? Ben Admin ACA Compliance

Current functionality

FSA limits, 90 day waiting periods

W2 reporting of healthcare insurance costs

Auto enrollment

Decline reasons and reporting

Employee notice of exchange

Affordable coverage

ACA Enhancements

SBC acknowledgement

Variable hour eligibility management

Hours-worked data integration

Mobile Benergy

Mobile optimized Benergy employee benefits portal using responsive design

Key features of Benergy sites are designed for mobile devices (I’m Here To, Benefits Overview and Wellness)

Partnering with EPIC for initial rollout

| 18

What to expect in the second half of 2013 A LOT!

California will release SHOP plans and pricing

Carriers will release new ACA compatible plans

Expect significant revisions to small group plans

Remarketing small group for a 12/1 renewal

Avoids member level rating, other parts of ACA

Extensive market activity as a result

New tools and resources will be introduced by carriers and third party providers

| 19

Q&A and Thank You Questions?

| 20