Embed Size (px)

Citation preview

Emerging US Space LaunchTrends and Space Solar Power

2015 IEEE International Conference on Wireless for Space and Extreme Environments

Orlando, FLDecember 14-15, 2015

Edgar ZapataNASA Kennedy Space Center

https://ntrs.nasa.gov/search.jsp?R=20150023507 2018-04-25T11:35:21+00:00Z

2

Contents

• Purpose• Background

• The (Slightly) Bigger Picture• The HEO Picture

• Visions of Mars• Or not…or maybe?• The Scope of the Challenge

• Needs• 1. Money?• 2. Time?• 3. Adapting?

• Visions of Launch Affordability• Affordability – How are we doing?

• Spacecraft• Competitiveness – Global• US Launch• This is Not New• In the Pipe

• Visions of Space Solar Power• Relevance to Space Solar Power

• 4. NASA as Investor • NASA as Partner• Closing

• Backup• Comparison of NASA Space Exploration

Architecture Level Assessments

3

Purpose

• Provide an overview of emerging US space launch and space systems trends that are critical to the future of new space business cases – like space solar power

• But first…some background, some visions, and some needs.

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$M

illi

on

s N

AS

A B

ud

ge

t (R

ea

l Ye

ar

Do

lla

rs)

Year

Cross Agency Support, Education & IG (+2010 fwd,Construction & Environmental)Aeronautics

Science

SFS (incl. SCaN, LSP, et al)

ISS R&D

ISS (Construction thru 2011, then Ops)

Cx ('07-'10), then SLS & Orion & Grd.Sys. ('11 Fwd)

Exploration R&D (was Shuttle Upgrades, SLI, BioSci,HSRT, et al)Space Technology

US Commercial Crew for ISS

ISS Crew (Soyuz) & Cargo (Commercial)

Shuttle

Earmarks

Rescissions (2012)

Rescissions (2012)

Purchase Power in 2003 $, NASA Inf. Index

ShuttleUpgrades +Other R&D

SFS incl. SCaN, LSP

<- US Commercial Crew ISS - Boeing & SpaceX Spacecrafts ->

Space Tech.

Decision: End Shuttle post-ISS

2005 Budget Shifts Begin ... Orion & SLS >

Last Shuttle Flight

2003 Columbia

Return To Flight

<-- ISS Cargo (US Commercial, Antares & Falcon 9 Launch, & Dragon and Cygnus Spacecrafts) & ISS Crew Soyuz -->

Actual NASA budget increases = 1.535% per year average (compound) since 2003

Science Launchers

Shuttle Production & Ops

E. Zapata NASA 8/31/2015

4

Background – The (Slightly) Bigger Picture

• The Entire NASA Budget since 2003 – and Purchasing Power

HEO

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

Life Cycle Cost Bars = All Procurement (Industry) and Government Costs as Modeled in Real Year $M2015 Human Exploration & Operations Budget = $8,185MNASA Scenario Model

2015You are Here!

100%? 50%? None?For?

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

Life Cycle Cost Bars = All Procurement (Industry) and Government Costs as Modeled in Real Year $M2015 Human Exploration & Operations Budget = $8,185MNASA Scenario Model

5

Background – The HEO Picture

• The Human Exploration & Operations (only) part of the NASA Budget

2015You are Here!

100%? 50%? None?For?

6

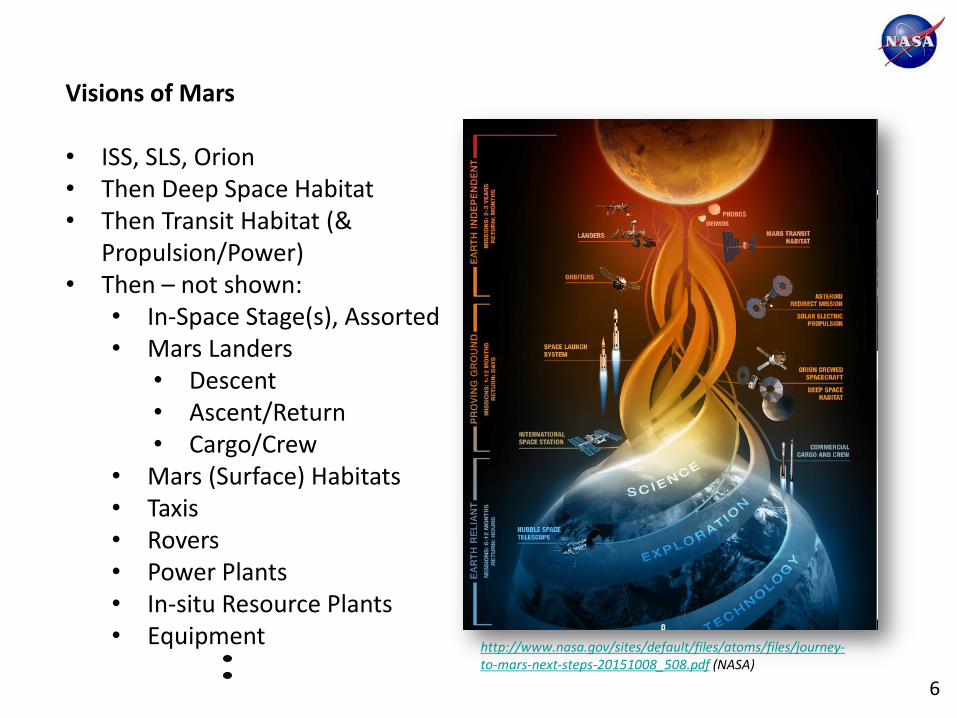

Visions of Mars

• ISS, SLS, Orion• Then Deep Space Habitat • Then Transit Habitat (&

Propulsion/Power)• Then – not shown:

• In-Space Stage(s), Assorted• Mars Landers

• Descent• Ascent/Return• Cargo/Crew

• Mars (Surface) Habitats• Taxis• Rovers• Power Plants• In-situ Resource Plants• Equipment

http://www.nasa.gov/sites/default/files/atoms/files/journey-to-mars-next-steps-20151008_508.pdf (NASA)

7

Visions of Mars – or not?

• National Research Council 2014

“Human Spaceflight Budget Projections. With current flat or even inflation-adjusted budget projections for human spaceflight, there are no viable pathways to Mars.

Potential Cost Reductions. The decadal timescales reflected above are based on traditional NASA acquisition. Acceleration might be possible with substantial cost reductions resulting from

a. More extensive use of broadly applicable commercial products and practices

b. Robust international cost sharing (that is, cost sharing that greatly exceeds the level of cost sharing with the ISS)

c. Unforeseen significant technological advances in the high-priority capabilities.”

8

Visions of Mars – or maybe?

• Jet Propulsion Laboratory 2015 – Price, Baker, Naderi

“This was the motivation for this study of a ‘‘minimal architecture’’ based on a high technology readiness level and the concept of staggered mission campaigns, in order to stay close to the current HSF annual budget adjusted for inflation.

This work was aimed at showing an example (an existence proof) that journeys to Mars could be doable using technologies that NASA is currently pursuing and on a time horizon of interest to stakeholders --without large spikes in NASA budget.”

http://spirit.as.utexas.edu/%7Efiso/telecon/Price_5-20-15/Price_5-20-15.pdf

9

Visions of Mars – the Scope of the Challenge

• SLS with Larger Upper Stage (~100+t>LEO)• 2 SLS/Year, 1 w. Orion as Payload. Other Payload TBD (No $ available)

HEO

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

Life Cycle Cost Bars = All Procurement (Industry) and Government Costs as Modeled in Real Year $M2015 Human Exploration & Operations Budget = $8,185MNASA Scenario Model

2015You are Here!

100%? 50%? None?For?

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

NASA SLS, NREC, Dev. NASA SLS, REC, Make, Fixed

NASA SLS, REC, Make, Var.

Stage, Earth Departure, NREC, Dev. Stage, Earth Departure, REC, Make NASA Orion, NREC, Dev.

NASA Orion, REC, Make, Fixed NASA Orion, REC, Make, Var.

Ground/Launch Site Ops., NREC, Dev. Ground/Launch Site Ops., REC

Government Project Management Government Program Management SLS+Orion+Ground Sys. Budget incl. Gov't Mng'mt

Post-ISS Funding Available per Scenario Selected ISS Funds (R&D & Cargo/Crew) ISS Funds All (incl. ISS Ops = ~ Mission Ops)

Human Spaceflight Total (w. SFS & R&D/"AES")

Life Cycle Cost Bars = All Procurement (Industry) and Government Costs as Modeled in Real Year $M2015 Human Exploration & Operations Budget = $8,185MNASA Scenario Model

2 X ~100t SLS a year

“challenge” No $ -

Exceeds Usual

Budget Growth

Upper Stage “challenge”

No $ -Exceeds

Usual Budget Growth

Replace SRB/SRM, “Advanced Booster” by 2030 for SLS ~130t>LEO

No $ - at Current Budget Growth/Inflation

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

NASA SLS, NREC, Dev. NASA SLS, REC, Make, Fixed

NASA SLS, REC, Make, Var.

Stage, Earth Departure, NREC, Dev. Stage, Earth Departure, REC, Make NASA Orion, NREC, Dev.

NASA Orion, REC, Make, Fixed NASA Orion, REC, Make, Var.

Ground/Launch Site Ops., NREC, Dev. Ground/Launch Site Ops., REC

Government Project Management Government Program Management SLS+Orion+Ground Sys. Budget incl. Gov't Mng'mt

Post-ISS Funding Available per Scenario Selected ISS Funds (R&D & Cargo/Crew) ISS Funds All (incl. ISS Ops = ~ Mission Ops)

Human Spaceflight Total (w. SFS & R&D/"AES")

Life Cycle Cost Bars = All Procurement (Industry) and Government Costs as Modeled in Real Year $M2015 Human Exploration & Operations Budget = $8,185MNASA Scenario Model

10

Visions of Mars – the Scope of the Challenge

• Or alternate futures? Other stakeholders.

HEO

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

Life Cycle Cost Bars = All Procurement (Industry) and Government Costs as Modeled in Real Year $M2015 Human Exploration & Operations Budget = $8,185MNASA Scenario Model

2015You are Here!

100%? 50%? None?For?

2 X ~100t SLS a year

“challenge” No $ -

Exceeds Usual

Budget Growth

Upper Stage “challenge”

No $ -Exceeds

Usual Budget Growth

Replace SRB/SRM, “Advanced Booster” by 2030 for SLS ~130t>LEO

No $ - at Current Budget Growth/Inflation

11

Needs

• Option 1: Getting More Money?

“Meaningful human exploration is possible under a less-constrained budget, ramping up to approximately $3 billion per year in real purchasing power above the FY 2010 guidance in total resources.”

-Seeking a Human Spaceflight Program Worthy of a Great Nation, by The Review of US Human Spaceflight Plans Committee

• Also NRC 2014, et al

• Option 2: Getting More Time? (& Money, & Doing Less)

• JPL 2015 et al• Mars landing by 2039• Assumption of infinite patience – if neglecting certain stakeholders

There’s a reason stakeholders are called “stake” holders

12

Needs

• Option 3: Adapting? – like Smith Corona?• For a time, saw threat as typewriters manufactured abroad

• Response: Plants moved abroad• For a time, created “personal word processors” –advanced for their time

• Why use someone else’s software?• Why use someone else’s electronics?• Why use someone else’s floppies?• Numerous advantages over those “PCs”

• Bankruptcy 1995

Adapting - right to the end

13

Visions of Launch Affordability

…Once upon a time…the Reusable Launch Vehicle program, NASA, late 1990’s

$1000/lb = $2,222/kg

14

Affordability – How are we doing?

• What do the numbers tell us?

$25,501

$3,107 $144 $222 $2,091

$14,057 $17,087

$-

$5,000

$10,000

$15,000

$20,000

$25,000

CSM-Apollo(crew/to Cis-Lunar)

CST-100 (crew/toLEO)

Cygnus (cargo/toLEO)

Dragon 1.0(cargo/to LEO)

Dragon 2.0(crew/to LEO)

LEM-Apollo(crew/to Lunar

Surface)

Orion (crew/to Cis-Lunar)

No

n-r

ecu

rrin

g $

M

NASA Non-recurring Investment / Development,Procurement $ Only, $M FY 2015$

E. Zapata NASA9/17/2015

Alphabetical Order ->

Total of Actuals to 2014, +Planned 2015-2020, +Estimates 2021-2022 to complete

Average Shown; UncertaintyLo $20B, Hi $31B

Average Shown; UncertaintyLo $12B, Hi $16B

Total of Actuals to 2014,+Planned to complete

Total of Actuals to 2014,+Planned to complete

NASA Only ShownPrivate $ add $148M

NASA Only ShownPrivate $ add $124M

$683

$420

$162 $91

$303

$699

$932

$- $100 $200 $300 $400 $500 $600 $700 $800 $900

$1,000

CSM-Apollo(crew/to Cis-Lunar)

CST-100 (crew/toLEO)

Cygnus (cargo/toLEO)

Dragon 1.0(cargo/to LEO)

Dragon 2.0(crew/to LEO)

LEM-Apollo(crew/to Lunar

Surface)

Orion (crew/to Cis-Lunar)

Re

cu

rrin

g $

M

Spacecraft Recurring Price to NASA per Unit,Procurement $ Only, $M FY 2015$

E. Zapata NASA9/2/2015

Alphabetical Order ->

Make Only.An estimate @1 unit/year.If @2 flights year, $566M/unit. Scenario if Orion less than 1 Flts/year = $1,560M/unit.

Make and Ops and Launch included (as a service).For CST-100 & Dragon 2.0, estimates / planned

Make Only.Average Shown; UncertaintyLo $300M, Hi $1,000M

Make Only.Average Shown; UncertaintyLo $400M, Hi $1,000M

0

5

10

15

20

25

30

35

40

45

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

To

tal

Co

mm

erc

ial

Sp

ace

La

un

ch

es

Da

ta U

S D

ep

art

me

nt

of

Tra

nsp

ort

ati

on

Year

United States

Russia

Europe

Sea Launch

China

India

Ukraine$28 $55 $61 $67

$88 $90

$97 $109 $184

$187 $223 $268 $295 $284

$775 $872

$1,547

580 443 13,150 13,150 13,150

43,000

13,150 4,900

28,790

9,797 17,443

11,587 12,124

28,790 24,400

70,000 70,000

$48,276

$124,153

$4,654 $5,119 $6,662

$2,093

$7,376

$22,247 $6,391 $19,087 $12,784

$23,159

$24,370 $9,865

$31,755 $12,458

$22,100

4,630 2,658

78,900 78,900 78,900 78,900

9,800

66,103

103,399 103,399

121,236

66,103

195,200

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Minotaur I,DoD/ORS

Pegasus XL, NASALSP, Sci., Class-D

Falcon 9,Commercial

Falcon 9, NASA ISS,Cargo, Block-buy,

Bundle

Falcon 9, NASA LSP,Sci., Class-C

Falcon Heavy,Commercial

Falcon 9, DoD (w.NASA & NOAA)

Antares, NASA ISS,Cargo, Block-buy,

Bundle

Delta IV Heavy, NRO(Service ONLY, No

ELC)

Atlas V 401, NASALSP, Sci., Class A/B

Atlas V 541, NASALSP, Sci., Class A/B

ULA (Atlas/DeltaAvg., ALL

Customers)

ULA (Atlas/DeltaAvg., DoD Only,Service + ELC)

Delta IV Heavy, NRO(Service + ELC)

Space Shuttle (ref.,crew excluded from

calculation; seenotes)

SLS (+grd ops, noupper stage, no

Orion, 2 flts/year)

SLS (+grd ops, noupper stage, no

Orion, 1 flt/year)

$ p

er k

g B

asis

Min

imu

m C

ost o

f E

ntry

$ M

Cost of Entry = Price of the Specific Launcher for that Customer / Application in $ Millions

Maximum Payload Capability of Launcher, kg to LEO, 200km/28.5 circ. (regardless of actual kg used by customer)

$ per kg

Best Recent Yearly "System" (All Atlas's, All Delta's, All Falcon 9's, etc.) Capability Demonstrated, Total kg to LEO in a Year

E. Zapata NASA10/14/2015

No longer operational

(2011)

Not yet operational

(2018)

RECENT COST DATA 2012-2017In Order of Cost of Entry >

Best yearly capability (6 flights) not

recent - 1998

BUT IF NASA -NOT $184M

RATHER $389.1M

Atlas best total kg/year

20149 flights

Delta best total kg/year

20124 flights

Falcon 9 besttotal kg/year

20146 flights

All 2014 data, DoD Only costs and total

kg/year

Not yet operational

(2016)

Not yet operational

(2018)

15

• Holistic view, recent/old, cargo/crew, commercial/cost-plus

$25,501

$3,107 $144 $222 $2,091

$14,057 $17,087

$-

$5,000

$10,000

$15,000

$20,000

$25,000

CSM-Apollo(crew/to Cis-Lunar)

CST-100 (crew/toLEO)

Cygnus (cargo/toLEO)

Dragon 1.0(cargo/to LEO)

Dragon 2.0(crew/to LEO)

LEM-Apollo(crew/to Lunar

Surface)

Orion (crew/to Cis-Lunar)

No

n-r

ecu

rrin

g $

M

NASA Non-recurring Investment / Development,Procurement $ Only, $M FY 2015$

E. Zapata NASA9/17/2015

Alphabetical Order ->

Total of Actuals to 2014, +Planned 2015-2020, +Estimates 2021-2022 to complete

Average Shown; UncertaintyLo $20B, Hi $31B

Average Shown; UncertaintyLo $12B, Hi $16B

Total of Actuals to 2014,+Planned to complete

Total of Actuals to 2014,+Planned to complete

NASA Only ShownPrivate $ add $148M

NASA Only ShownPrivate $ add $124M

CrewCommercial

CargoCommercial

CargoCommercial

CrewCommercial

CrewCost+/BAU

Spacecraft Cost Data - Development(Cost as Price to NASA)

Emerging Space

16

$683

$420

$162 $91

$303

$699

$932

$- $100 $200 $300 $400 $500 $600 $700 $800 $900

$1,000

CSM-Apollo(crew/to Cis-Lunar)

CST-100 (crew/toLEO)

Cygnus (cargo/toLEO)

Dragon 1.0(cargo/to LEO)

Dragon 2.0(crew/to LEO)

LEM-Apollo(crew/to Lunar

Surface)

Orion (crew/to Cis-Lunar)

Re

curr

ing

$M

Spacecraft Recurring Price to NASA per Unit,Procurement $ Only, $M FY 2015$

E. Zapata NASA9/2/2015

Alphabetical Order ->

Make Only.An estimate @1 unit/year.If @2 flights year, $566M/unit. Scenario if Orion less than 1 Flts/year = $1,560M/unit.

Make and Ops and Launch included (as a service).For CST-100 & Dragon 2.0, estimates / planned

Make Only.Average Shown; UncertaintyLo $300M, Hi $1,000M

Make Only.Average Shown; UncertaintyLo $400M, Hi $1,000M

CrewCommercial

CargoCommercial

CargoCommercial

CrewCommercial

CrewCost+/BAU

Manuf. $ Only Manuf. and Ops/Launch $

• Holistic view, recent/old, cargo/crew, commercial/cost-plus

Spacecraft Cost Data – Manufacturing - “Thru Delivery”(Cost as Price to NASA)

Manuf. $ Only Manuf. $ Only

Emerging Space

17

0

5

10

15

20

25

30

35

40

45

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Tota

l Co

mm

erc

ial S

pa

ce

Lau

nch

es

Da

ta U

S D

ep

art

me

nt

of

Tra

nsp

ort

ati

on

Year

United States

Russia

Europe

Sea Launch

China

India

Ukraine

6

6

6

0

1

0

0

Total Commercial

2015 = 19

Competitiveness2015 = 19 Commercial Launches out of 68 Total Global Major Launches

• The US is regaining commercial launch market share• Customers appear glad to return – for the right price

Emerging Space

Data through 2014 from US DOT: http://www.rita.dot.gov/bts/node/4909112015 data from assorted launch records

18

US Launch Prices (Costs to the Customers)

$4,600/kg $2,000/kg?

$28 $55 $61 $67

$88 $90

$97 $109 $184

$187 $223 $268 $295 $284

$775 $872

$1,547

580 443 13,150 13,150 13,150

43,000

13,150 4,900

28,790

9,797 17,443

11,587 12,124

28,790 24,400

70,000 70,000

$48,276

$124,153

$4,654 $5,119 $6,662

$2,093

$7,376

$22,247 $6,391 $19,087 $12,784

$23,159

$24,370 $9,865

$31,755 $12,458

$22,100

4,630 2,658

78,900 78,900 78,900 78,900

9,800

66,103

103,399 103,399

121,236

66,103

195,200

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Minotaur I,DoD/ORS

Pegasus XL, NASALSP, Sci., Class-D

Falcon 9,Commercial

Falcon 9, NASA ISS,Cargo, Block-buy,

Bundle

Falcon 9, NASA LSP,Sci., Class-C

Falcon Heavy,Commercial

Falcon 9, DoD (w.NASA & NOAA)

Antares, NASA ISS,Cargo, Block-buy,

Bundle

Delta IV Heavy, NRO(Service ONLY, No

ELC)

Atlas V 401, NASALSP, Sci., Class A/B

Atlas V 541, NASALSP, Sci., Class A/B

ULA (Atlas/DeltaAvg., ALL

Customers)

ULA (Atlas/DeltaAvg., DoD Only,Service + ELC)

Delta IV Heavy, NRO(Service + ELC)

Space Shuttle (ref.,crew excluded from

calculation; seenotes)

SLS (+grd ops, noupper stage, no

Orion, 2 flts/year)

SLS (+grd ops, noupper stage, no

Orion, 1 flt/year)

$ p

er k

g B

asis

Min

imu

m C

ost o

f E

ntry

$ M

Cost of Entry = Price of the Specific Launcher for that Customer / Application in $ Millions

Maximum Payload Capability of Launcher, kg to LEO, 200km/28.5 circ. (regardless of actual kg used by customer)

$ per kg

Best Recent Yearly "System" (All Atlas's, All Delta's, All Falcon 9's, etc.) Capability Demonstrated, Total kg to LEO in a Year

E. Zapata NASA10/14/2015

No longer operational

(2011)

Not yet operational

(2018)

RECENT COST DATA 2012-2017In Order of Cost of Entry >

Best yearly capability (6 flights) not

recent - 1998

BUT IF NASA -NOT $184M

RATHER $389.1M

Atlas best total kg/year

20149 flights

Delta best total kg/year

20124 flights

Falcon 9 besttotal kg/year

20146 flights

All 2014 data, DoD Only costs and total

kg/year

Not yet operational

(2016)

Not yet operational

(2018)

Emerging Space

19

This is Not New – and it’s not limited to launch systems

• SpaceHab Price-Water House Report 1991• SpaceHab was 1/10th the cost as commercial (as defined then) versus

business-as-usual• One of a handful of historical data points with a Business-as-Usual ~

analog (SpaceLab)• Dependent on Shuttle; very much an ECLSS system extension

shielded within the Orbiter payload bay

SpaceHab double-research module, STS-107 Columbia, NASA

20

In the Pipe

• Reusability – Falcon 1st Stage(s)?

• ULA Vulcan launcher – price drops?

• Constellations of Sat’s – Round 2? OneWeb, Google/SpaceX, etc.

• Small Launch – business plans around the business plans of ever more Small Sat capabilities

21

http://science.ksc.nasa.gov/shuttle/nexgen/Nexgen_Images/solar_power_satellite_concept.jpg (Public Domain)

By permission, John C. Mankins

“Integrated Symmetrical Concentrator” (ISC) Solar Power Satellite, late 1990s, NASA

“SPS-ALPHA” (Solar Power Satellite by means of Arbitrarily Large Phased Array),

2013, Mankins Space Technology, Inc.

Visions of Space Solar Power

22

Relevance to Space Solar Power

Are the barriers to Mars and Space Solar Power the same?

• Both need more affordable space transportation

• Both need more affordable space systems

• Will both always be 20 years away?

23

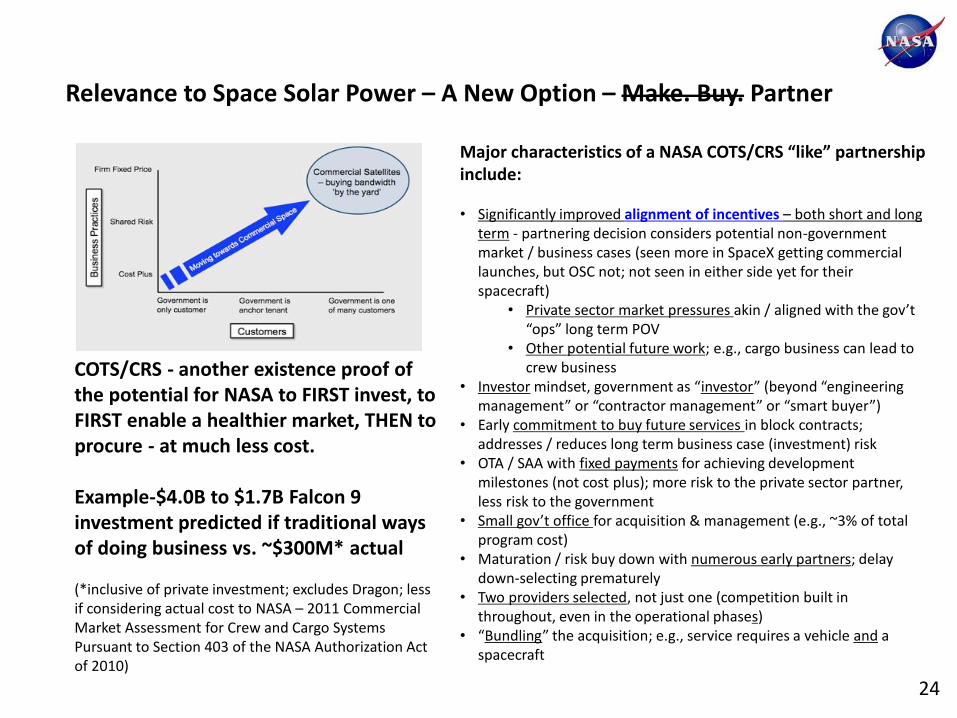

Relevance to Space Solar Power – A New Option

1. Get Money2. Get Time3. Adapt4. NASA as Investor – transforming to become “one of many customers”

NASA, http://www.nasa.gov/offices/oct/partnership/comm_space/

Space Systems-Launch-Spacecraft-Habitation

Decreasing Prices, Decreasing Costs

Highest Price, Unsustainable Costs

24

Relevance to Space Solar Power – A New Option – Make. Buy. Partner

Major characteristics of a NASA COTS/CRS “like” partnership include:

• Significantly improved alignment of incentives – both short and long term - partnering decision considers potential non-government market / business cases (seen more in SpaceX getting commercial launches, but OSC not; not seen in either side yet for their spacecraft)

• Private sector market pressures akin / aligned with the gov’t “ops” long term POV

• Other potential future work; e.g., cargo business can lead to crew business

• Investor mindset, government as “investor” (beyond “engineering management” or “contractor management” or “smart buyer”)

• Early commitment to buy future services in block contracts; addresses / reduces long term business case (investment) risk

• OTA / SAA with fixed payments for achieving development milestones (not cost plus); more risk to the private sector partner, less risk to the government

• Small gov’t office for acquisition & management (e.g., ~3% of total program cost)

• Maturation / risk buy down with numerous early partners; delay down-selecting prematurely

• Two providers selected, not just one (competition built in throughout, even in the operational phases)

• “Bundling” the acquisition; e.g., service requires a vehicle and a spacecraft

COTS/CRS - another existence proof of the potential for NASA to FIRST invest, to FIRST enable a healthier market, THEN to procure - at much less cost.

Example-$4.0B to $1.7B Falcon 9 investment predicted if traditional ways of doing business vs. ~$300M* actual

(*inclusive of private investment; excludes Dragon; less if considering actual cost to NASA – 2011 Commercial Market Assessment for Crew and Cargo Systems Pursuant to Section 403 of the NASA Authorization Act of 2010)

25

Relevance to Space Solar Power

• NASA as Investor / Partner• Smaller amounts of $ to justify• NASA (and partner contributions) $ leveraged into large effects

• Business case maturation• Strategic technology maturation / demonstration

• Modularity• Assembly• Transmission

• Encourage non-government investors• “NASA on board” (credibility of NASA)• “Virtuous cycle” – more investors ease the case for more

NASA partnering (credibility of the business)

“As was mentioned previously, a number of technology and systems level demonstrations can be accomplished without new space transportation”

-The Case for Space Solar Power, J. Mankins

26

Closing

• Space sector supply AND demand can, will and must grow together• Large scale programs – like Space Solar Power – face similar challenges

MoneyTimeAdapt

Transform

• An increased emphasis on public-private partnerships offers the most viable path forward

…when you have eliminated the impossible, whatever remains, however improbable, must be the truth? -Sherlock Holmes in The Sign of the Four

You can always count on Americans to do the right thing - after they've tried everything else. –Winston Churchill

27

Backup

28

Comparison of NASA Space Exploration Architecture Level Assessments

Study NASA Human Spaceflight Budget? (and/or inflation)

CAS, Science, Aeronautics $?STMD $?HEO SFS, M/GOps, & R&D $?

Mars Exploration Possible?

SLS,Orion?

ISS? Budget Profile incl. NASA support for Private Space Stations post-ISS?

Budget for 70t SLS to 110t? To 130t?

2014 NRC Committee on Human Spaceflight

..increases fasterthan *inflation(pp.41)

†Unaddressed

Unaddressed / **Frozen/Flat?

Yes – Phobosearly 2040s, Mars surface 2050s

Yes Ends2028

~No? Unaddressed

2015 JPL H2MMinimal Architecture

…increases at rate of *inflation

†Unaddressed

Unaddressed / **Frozen/Flat?

Yes – surface by 2039

Yes Ends2028

~No? Unaddressed

2015 Planetary Society Humans Orbiting Mars

Evolvable Lunar Architecture w. PPP

…increase athistorical budget growth…

All NASA areas increase at same rate as HEO

Lunar 1st, Mars asfollow-up study

**No n/a-> Possible - Budget set aside –ample fund split possible

n/a

Evolvable Mars Campaign

* aerospace, space systems specific inflation per se ill-defined** moves funds from X to Y† if flat, this shifts the whole NASA portfolio split

Segues off of JPL H2M Minimal Architecture

TBD

What about the 1991 Space Exploration Initiative (SEI)? Budget growth by multiples of then current. Rest ~ n/a.