-

7/28/2019 Emergency Retirement

1/16

By Larry Grossman

The first of the Baby Boomers turned 60this year. I happen to

fall right into themiddle of this group (those born between1946 and

1964), so Im pretty familiar withthe financial challenges facing

many of my peers. For many, right at the top of the listIS the fact

theyre grossly unprepared forretirement.

Survey after survey shows that many graying boomers still have

no idea how much money theyll need to retire comfort-ably. Worse,

in a country with a negativepersonal savings rate, millions are

farbehind on their wealth accumulation goals.

If you or someone you know is headedfor a severely under-funded

retirement, fearnot. Ill show you how you can create theretirement

you wanteven if youve fallenfar behind on building your nest

egg.

What Do You MeanIm Broke?

The standard rule is you need 60% to90% of your pre-retirement

income tomaintain a similar standard of living post-retirement. Now

that is a pretty widespread, and it depends on whether youinclude

things like radically increasing health care costs, energy prices

and othernecessary items.

For the sake of argument, well use a number somewhere in

between, say 75%. And well run though some examples.

Lets assume you are 50 years old earning US$150,000. You want to

retire at age 65 with 75% of your current income. Now without too

many mental calculations, weare also going to assume youre making a

10% rate of return and youre putting away 10% of your income into a

retirement plan.

And, finally, we are going to actually assume Uncle Sam will

still be around totake care of you so you can draw SocialSecurity.

Oh and one last thing, lets assumeyou have already accumulated

US$100,000in a retirement plan along the way.

With this plan, you will run out of money when you hit age 72.

Thats right. You lasted a whopping 7 years before youexhausted your

savings! To meet your goalyou have a couple of options. You can

increase your rate of return from 10% to18.5%. We know thats not

going tohappen! You can reduce your requiredincome at retirement to

40% of your finalyears income. Hmmm, reducing yourincome by 40%

probably doesnt sound likean appealing retirement after you

workedyour whole life. Or you can always delay retirement until age

76. Ouch! I dont think any of us want to work that long. And

ACCESSto International Asset Protection and Investment

Opportunities

A P U B L I C A T I O N O F T H E S O V E R E I G N S O C I E T

Y

The Baby Boomer EmergencyRetirement Repair Plan

How a Defined Benefit Plan Can Turn an Under-FundedRetirement

Account into a Superfund

Whats Wrong with theFourth of July . . . . . . . . . . p. 3

Defensive Investing withGlobal Titans . . . . . . . . . . . p.

5

Worse than Worthless:3 Asset Protection ScamsExposed . . . . . .

. . . . . . . . . p. 7

The New OffshoreBankNo Longer Justfor Millionaires . . . . . . .

. . . p. 9

Your New Country In aMatter of Months: EconomicCitizenship for

Sale . . . . . p. 10

The Scourge ofExit Taxes . . . . . . . . . . . . . p. 11

Four of the Best Ways toProfit in theGlobal Marketplace . . . .

. p. 12

The World of TheSovereign Society . . . . . . p. 13

Global Correction to CreateEventual Bargains . . . . . . p.

14

TSI Portfolio . . . . . . . . . . . p. 15

Come Explore Four AncientRegions of Wealth . . . . . . p. 16

A Constitution of Governmeonce changed from Freedom,never be

restored. Liberty, onis lost forever.

John Ad

In This IssueJuly 2006 | Vol. 9 No. 7

Website PasswordThe password for the mem-bers- only section of

TheSovereign Societys website atwww.sovereignsociety.com is:zurich

(no quotes).

-

7/28/2019 Emergency Retirement

2/162

Massive Market Correction:A Midsummers Nightmare

for the Unprepared

The Sovereign Individual is published monthly (12 times a year)

for $145 per year by The Sovereign Society, 5 Catherine Street,

Waterford, Ireland. POSTMASTER: Send address changeto: The

Sovereign Society, PO Box 925, Frederick, MD 21705. For information

about your membership in The Sovereign Society, contact Member

Services at 888-358-8125 or fax 410-230-1253. Our e-mail address

is: [email protected]. Managing Director: Erika Nolan.

Associate Publisher & Marketing Director: Shannon Crouch.

Editor : Mark NestmannLegal Counsel & Editor: Robert Bauman.

Investment Director: Eric Roseman. Ecommerce Manager: Matthew

Barrett. Membership Director: David Newman. GraphicDesigner:

Jennifer Costigan. Contact the editor through the Society or by

e-mail at [email protected]. All contents of this issue are

copyright 2006 by The Sovereign Society. Allrights reserved:

reproducing any part of this document is prohibited without the

express written consent of The Sovereign Society. Protected by U.S.

Copyright Law {Title 17 U.S.C. Section101 et seq., Title 18 U.S.C.

Section 2319}: Infringements can be punishable by up to 5 years in

prison and $250,000 in fines. LEGAL NOTICE: This work is based on

SEC filings, currentevents, interviews, corporate press releases

and what weve learned as financial journalists. It may contain

errors and you shouldnt make any investment decision based solely

on whatyou read here. Its your money and your responsibility. The

Sovereign Society expressly forbids its writers from having a

financial interest in any security they recommend to our

sub-scribers. All The Sovereign Societys (and affiliated entities)

employees and agents must wait 24 hours after an initial trade

recommendation is published on the Internet, or 72 hours aftera

direct mail publication is sent, before acting on that

recommendation. The information herein is not intended to be

personal legal or investment advice and may not be appropriate

orapplicable for all readers. If personal advice is needed, the

services of a qualified legal, investment or tax professional

should be sought.Chairman John A Pugsley, U.S. Medical Expert

Jonathan Wright, M.D., U.S. Council of Experts Mary Anne Aden,

Costa Rica Pamela Aden, Costa Rica Colin Bowen, Isle of ManMichael

Chatzky, U.S. Michael Checkan, U.S. Thomas Fischer, Denmark Neil J.

George, Jr., U.S. Stuart Goldsmith, UK Ed Gunther, France, U.S.

Larry Grossman, U.S. Adrian Hartmann,Canada Doug Hendler, Canada

Ron Holland, U.S. Hubert Jongen, Belgium Rita Jongen, Belgium

Christian H. Kalin, Switzerland Rainelda Mata-Kelly, Panama Michael

Ketcher, U.S. Pierre Lemieux, Canada David S. Lesperance, Canada

Kathy Lien, U.S. Leon Louw, So. Africa David Melnik QC, Canada

Vince Miller, U.S. Brian OKane, Ireland Humberto Pacheco,Costa Rica

Dr. Jose V. Pascar, Uruguay Norman Rentrop, Germany Eric Roseman,

Canada Gideon Rothschild, U.S. Rick Rule, U.S. Derek Sambrook,

Panama Boris Schlossberg, U.S. Timothy Scrantom, U.S. Marc Sola,

Switzerland Dr. Erich Stoeger, Austria Robert Vrijhof, Switzerland

Hans C. Weber, Switzerland William Woods, Bermuda Peter Zipper,

Austria

PUBLISHER S NOTE/W EALTH PRESERVATION

Its summertime again. And this year, in addition to theusual

summer annoyances from mosquitoes to sunburns,global investors are

also suffering through the worst marketcorrection since 2002. But

luckily none of us here at TheSovereign Society are panicking. In

fact, The Sovereign Soci-etys Investment Director, Eric Roseman,

has been prophesy-ing this correction for some time.

And now that the correction has arrived, were doing a lit-tle

defensive investing with the Global Titans Index. TheIndex includes

all the large companies weve come to know and love from Johnson

& Johnsonto Coca-Cola , which look to soar as emerging markets

and small cap companies sink.

But even with the present markets weighing on ourminds, were

still thinking of the future. This month, Larry Grossman reveals

how you can restructure your retirementplans to contribute as much

as US$177,000 a year to yourretirement fund.

Plus, this month, Chairman John Pugsley comments on whats

fundamentally wrong with the 4th of July celebration.Our Legal

Counsel, Robert Bauman, reveals two of the lastremaining havens on

Earth where you can essentially pur-chase citizenship. And finally,

Wealth Preservation and TaxConsultant, Mark Nestmann gives you the

top 3 asset pro-tection scams that could cost you your fortune (and

yourfreedom if you go to jail)!

In Wealth and Prosperity,

P.S. If youre concerned about your retirement, Larry Grossman

will be attending our next Permanent Wealth Pro-tection Summit in

October. Hed be happy to sit down withyou and look over your

personal retirement plan. See theconference corner page for more

information.

Erika Nolan has been Executive Director of The Sovereign Society

since its inception. She travels extensively and focuses on the

development of new business partnerships and marketing

opportunities inorder to strengthen and expand the Societys

network.

lastly, you can increase contributions to 31% of yourincome.

So clearly, most of us do not contribute enough forretirement.

Please, max out on your IRA, SEP and or 401kcontributions if at all

possible. But now lets talk about thgreatest savings plan available

called a Defined Benefit Pla.

I mentioned Defined Benefit Plans recently and wassurprised to

learn how few people know about them. I waeven more shocked how

little these life saving plans areactually discussed.

A DB plan is a plan designed to pay a target level of benefits

at retirement age. These benefits can be basedupon a fixed

percentage of your average salary, a flatmonthly dollar amount or a

formula based on years of service in a business.

Most DB plans I have seen simply state the maximumallowable

contribution limit based upon the participantsage. Going back to

the example we were using, a 50-yearold who wants to retire at age

60 can contributeapproximately US$168,000 per year.

Compare this US$168,000 to the garden variety retire-ment plans

contributions. With a 401k, you can only contribute up to US$15,000

(and if youre over 50, youcan add an extra US$5,000 a year to

catch-up). SEP retirement plans are far more generous. You can

contributeUS$44,000 or 25% of your income up to US$220,000 toyour

SEP. But that still only leaves you with a maximum oonly US$55,000

a year.

Lets take a look at some real life examples.

Contribute Even More ThanUS$168,000 a Year with a DB Plan

Recently, I met S.W. at a Sovereign Society conference.S.W. is a

retirement planners dream client. Hes a 51-yearold, self-employed

physician with no other employees.

Continued from page 1:The Baby Boomer Emergency Retirement

Repair Plan

(Continued on page

-

7/28/2019 Emergency Retirement

3/16

By John Pugsley This year marks the 230th anniversary of the

signing of

the U.S. Declaration of Independence from Great Britain,

and as is the custom, the anniversary will be feted with fire-

works, flags and parades.

Celebrating independence from foreign rule is not uniqueto

America. A few years back, I celebrated the 4th of July, inFort

Lauderdale. Crossing to the Abacos the following day, I joined the

Bahamians in celebrating their independencefrom the Brits on July

10th. I happened to be in Grenada onFebruary 7th last year, as

Grenadian soldiers and sailors, per-formed their annual ritual of

deliverance from British rule.

Its the same around the world. Mex-icans celebrate independence

from

Spanish rule on September 16th. Zairecelebrates its independence

from Bel-gium on June 24th. Algerians fromFrance on July 5th. From

the Ukraineto the Philippines, and from Vanuatuto Turkmenistan,

country after country celebrates liberation with military bands,

flags and enthusiastic crowdssinging national anthems.

Yet, to paraphrase Rousseau: Manfrees himself, but everywhere he

is in chains. If independ-

ence is cherished and celebrated worldwide, why isnt manfree?

Why do people rebel, free themselves from tyranny,then fall victim

again, in an endless cycle?

I submit the seed of the problem may lie within that

greattemplate for independence, the Declaration of

Independenceitself. No doubt you can quote its stirring words:

We hold these truths to be self-evident, that all men are

cre-ated equal, that they are endowed by their Creator with

certainunalienable Rights, that among these are Life, Liberty and

the pursuit of Happiness.

And then the muted but ominous conclusion:That tosecure these

rights, Governments are instituted among Men[W]henever any Form of

Government becomes destruc-tive of these ends, it is the Right of

the People to institute new Government.

New government? Aye, as Shakespeare would say, theresthe

rub.

Consider the American Revolution. Just a decade after

theDeclaration liberated individuals from one powerful

centralgovernment, the Constitution created another. And so it

hasbeen around the world throughout history. Today, govern-

ments formed to replace those toppled by rebellion consumtheir

citizens lives much more than their predecessors didGovernment is

like the android inThe Terminator : if thetiniest speck of it is

left after its destroyed, it reforms itsel

It doesnt matter what form of government is thrown offOne

population celebrates when a benevolent king replacetyrannical

king. Another, when a secular leader replaces a religious leader.

Or, as in America, people celebrate whenthe monarch is deposed and

the people elect their own ruleunder the concept of a republic or

democracy. No matter, itseems. Monarchy, dictatorshipcommunism,

none havelasted. Even democracy hasnt solved the problem.

Observing parliamentary electionsin England, Rousseau observed:

Th

English people believes itself to befree; it is gravely

mistaken; it is freeonly during election of members of parliament;

as soon as the membersare elected, the people is enslaved;

itnothing. In the brief moment of itsfreedom, the English people

makesuch a use of that freedom that itdeserves to lose it.

Whats wrong with the Fourth of July? It celebrates a pyrrhic

victory. People think they willfree if they exchange one set of

rulers for another. Yet, it hnt worked. The failure is people

celebrate a nations inde-pendence from foreign rule, rather than

their own individuindependence from the rule of any other person.

No man(or woman, Hillary) has a mandate from God or from

theuniverse to rule over others, whether he or she be king,queen,

czar, fuehrer, or president. No one is endowed withrights superior

to anyone else. This is the true heart of the American credo.

When the ultimate declaration of independence isdrafted, tested

and in place, it will not refer to the indepenence of one nation

within a world of sovereign nations, bu

to the independence of each individual within a world of

sovereign individuals. While nations will continue to pass and out

of the revolving door of independence and subjugation, a personal

declaration of independence is for all time When you make your

declaration that you are a sovereignindividual, that truly will be

the day for remembrance andcelebration.

John Pugsley is Chairman of The Sovereign Socthe author of many

books on economics, investi politics. John is also the editor of

The Sovereignelite investment trading service, Stealth Investo

3

Whats Wrong with the Fourth of July?

THE CHAIRMANS CORNER

Just a decade after the Declaration liberated individuals from

one

powerful central govern- ment, the Constitution

created another.

-

7/28/2019 Emergency Retirement

4/16

S.W. makes a nice living with just over US$350,000 peryear. And

S.W. was shocked when I told him he could becontributing

approximately US$177,000 into a DB plan.

Most of us wont be quite as lucky as S.W. Well eitherhave other

employees to deal with or we wont make his highincome. But,

amazingly, a DB plan can work nearly as wellfor most business

owners.

Here is another example:

Example: Owner Grabs 90% of the BusinesssRetirement Funds

Employee Age Comp. Contributions % of TotalOwner 60 $205,000

$144,034 90.1%Emp 1 40 $40,000 $7,074 4.4%Emp 2 35 $35,000 $4,371

2.7%

Emp 3 30 $30,000 $2,707 1.7%Emp 4 25 $25,000 $1,656 1.1%Total

$159,842 100.0%

Yes, the owner still has to pay out-of-pocket to cover

hisemployees, but the owner still ends up with over 90% of thetotal

contributions.

And these are very simple examples. Far more complexplans allow

you to target highly compensated employees whileexcluding others.

These plans, called Tiered Defined BenefitPlans, let you assume

different benefit levels for each partici-pant. That means you can

make greater contributions forsome employees while minimizing

contributions for others.This factor alone was once one of the

biggest deterrents to DBplans.

What does this mean to you? This means if you own yourown

business or can influence your retirement plan in any way, then it

may not be too late to save for retirement with a defined benefit

plan. Now that I have scared the heck out of you, lets talk about a

DB plans other benefits.

Tax Savings & Global Investments

A DB plan is the number one legal way to reduce yourtaxes. Thats

right I said the number one way to reduce yourtaxes. Just like any

other retirement plan, the contributionsyou make to a DB plan are

all pre-tax. So if the 50-year-olddoctor S.W. contributes the full

US$177,000 to his definedbenefit plan, he only pays taxes on his

remaining income.That means out of a US$350,000 income, he only

pays taxon US$173,000.

These defined benefit assets can also be invested virtually

anywhere in almost any kind of investment. Were not just

talking about the traditional mutual funds you see in a 401were

talking about a world of investments available atyour finger tips.

You can invest in real estate, both domestand foreign, precious

metals, foreign bank accounts, non-U.S. currencies and many, many

other investments you havread about here in The Sovereign

Individual . If properly structured, its actually quite easy to

allocate and invest yoretirement plan assets anywhere in the

world.

Plus, these assets grow on a tax-deferred basis until youstart

to withdraw them at retirement. That means the law ocompounding

work is working in your favor as you continto save assets you would

normally have to pay taxes on.

A Defined Benefit plan allows you to maximize yourretirement

savings in a way no other retirement plan does.This plan reduces

your income tax and gives you the

freedom to invest your retirement plan anywhere in the world. If

you are one of the fortunate ones who are in a position to

implement a DB plan, I would urge you toconsider it today. For more

information on DB plans,including a custom designed plan for you,

please contact moffice for additional information.

Authors Note: The development and implementation of a custom

designed retirement plan can be a complex taskas it is with all

areas of financial planning, requiring a high degree of technical

expertise. For the sake of simplicity in trying to explain a highly

complex subject, have made certain assumptions and have

roundednumbers. A full explanation of this topic or any assump-

tions made are available upon request.

Larry C. Grossman, CFP, CIMA is one of approximately 1,500 CIMAs

nationwide.He is also the Managing Director of

SovereignInternational Asset Management. In 2006, he established

Sovereign International Pension Serv

further help his clients liberate their retirement plans for

grea protection and investment opportunities. He can be

contacted727-784-4841. Email: [email protected].

Wwww.worldwideplanning.com.

Continued from page 2:The Baby Boomer Emergency Retirement

Repair Plan

4

W EALTH PRESERVATION

A DB plan is the number one legal way to reduce your

taxes (because) the

contributions you make to your DB plan are all pre-tax.

-

7/28/2019 Emergency Retirement

5/165

GLOBAL INVESTMENTS

By Eric Roseman

Big might seem boring to most investors. But, increas-ingly,

large-capitalization stocks are looking mighty attractivein the

rough market environment weve been enduring sinceMay. In fact, for

U.S. dollar-based investors and euroinvestors alike, this is the

best time since 1973 to buy globalmultinationals on the cheap.

Large caps currently sell at a major discount to small

andmid-sized companies. And as world markets continue to cor-rect

further, the biggest global brands should draw safe-haven flows

from nervous investors seeking stable andreliable earnings

growth.

There are two excellent ways to play this sector right now.Each

enables you to snatch up global category leaders atgood prices and

collect healthy dividends. The Europeanversion of this investment

also offers protection against a falling dollar to boot.

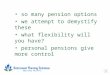

Bigger is Better in 06Over the last three years, small and

mid-sized stocks

around the world have literally gone ballistic while

large-capstocks have lagged (see enclosed chart). This divergence

hasrecently reached its highest level since 1973, when

large-capsbegan their long-term decline relative to small stocks.

Since1926, large-cap stocks have outpaced small-caps during only

one performance periodfrom 1926 to 1957.

Small stocks have historically posted fatter returns thantheir

large-cap cousins for several reasons. Namely, shortstocks provide

faster growing corporate earnings and greateragility to meet the

changes facing the global marketplace.Since 2001, small stocks have

gained 12.6% per annum

compared to just 4% per year for the S&P 500 Index, or

thbroader market. And since the bear market low in October

2002, smaller companies have zoomed ahead with a cumultive 96%

gain versus only 35% for the S&P 500 Index. Buthat trend is now

history in mid-2006 as hedge funds andinvestors are dumping the

worlds riskiest investments amthe worst reversal for global

equities since April 2004.

Time to Get Defensive as Bull FadesThe worlds largest companies,

based on their stock-mar

ket capitalization, havent looked this attractive since the

l1990s. Over the last 3.5 years, investors have neglected stable

and reliable earnings (aka boring stocks) for the highflying

emerging markets, small and mid-cap equities, realestate investment

trusts (REITs), and commodities. But asthe Federal Reserve, the

European Central Bank and evenThe Bank of Japan either accelerate

or begin a new round omonetary tightening to curb rising inflation,

corporate earnings will be revised lower for 2007. Thats especially

true smaller companies, highly tied to the global economic

cycHistorically, small-caps are the first sector to feel the squeea

result of slowing global growth and rising interest rates. this

environment of risk reduction, portfolio managersdump high-risk

equities and exchange market risk for pre-dictable earnings growth

from brand-name franchises.

The StreetTracks Dow Jones Global Titans ETF isdually listed in

New York and Frankfurt, and traded in dol-lars and euros,

respectively. The Global Titans are the worl50-largest

publicly-traded companies and include many ofthe worlds greatest

companies. As of June 1, 2006, theGlobal Titans traded at 14 times

historical earnings andyield an effective 2.7% dividendthats 35%

cheaper thanthe MSCI World Index based on price-to-earnings and

32%more in dividends.

When you buy this cheaply valued blue-chip portfolio,youre

getting world-class diversification because all of thegreat

companies derive a significant portion of their grosssales revenues

from international markets. Companies likeCoca-Cola , Nestl of

Switzerland,Toyota Motor Corpora-tion , Roche Holdings, and Samsung

Electronics are just afew of the many brand-names deriving a hefty

chunk of their sales from fast-growing foreign economies. And talk

about mega-market caps! The smallest Global Titan isDellComputer at

just US$58.4 billion. The indexs largestcompany isExxon-Mobil, a

beneficiary of the big boom inenergy prices this decade commanding

a fat US$376 billiomarket capitalization. Exxon-Mobils market

capitalization

Defensive Investing with Global TitansTapping into the Worlds

Best Brands for High Yield,

High Value and Euro Diversification

80%70%60%50%40%30%20%10%

0%

-10%-20%-30%-40%

May 01 Jan 02 Jan 03 Jan 04 Jan 05 Jan 06 May 06

S&P 600 Small-Cap Index versus S&P 500 Index

(Large-Caps): May 2001 to June 2006---- Large Caps Small Caps

Small Caps Have Soared While Cheap Large Caps Lagged

Small stocks have skyrocketedsince 2002, but now look

expensivecompared to large-caps.

Source: MSN Money

-

7/28/2019 Emergency Retirement

6/166

GLOBAL INVESTMENTS

in fact, exceeds the total gross domestic product value of many

emerging market countries!

The Dow Jones Global Titans Index currently holds19.8% in

financial services; 17.4% in health care; 16.4% inenergy; 14.5% in

information technology, and 11.8% inconsumer staples. The remaining

20% are diversified acrosscyclical, telecommunication and consumer

discretionary large-caps. Assets are heavily weighted towards U.S.

compa-nies with substantial foreign earnings exposure at 62% of

theindex, followed by 16.5% in the United Kingdom, 7.2%

inSwitzerland, 3.2% in the Netherlands, and 2.7% in Japan.

A Falling Dollar is Bullish forthe Titans

Over the last three years, the Dow Jones Global TitansETF has

gained 41.2% or 12.2% annualized. That perform-ance figure is

certainly not bad, but it badly trails the hugereturns already

generated for many international marketssince the bear market low

in October 2002. But as the mar-

ket grows more defensive this year and the dollar continuesto

fall over the next 6-12 months, many of these GlobalTitans will log

strong earnings growth as dollar-basedexporters in the United

States and Asia grow their marketshare. Lets not forget that in

1995the year the dollar fin-ished its last secular bear marketthe

S&P 500 Indexderived more than 35% of its earnings growth from

a falling American dollar. A weaker dollar does wonders for

dollar-based multinationals, and I expect more of the same aheadof

the next major U.S. dollar bear market.

Although certainly not a guarantee to future profits,insider

buying is usually a very bullish signal for investorslooking to

ride the coattails of several directors or executives. With many of

the Global Titans now trading at multi-yearor 52-week lows, its no

surprise several companies insidersare stepping up to the plate and

buying stock with cash.

For example,Dell Incorporateds founder and chairman,Michael

Dell, along with the companys chief executive offi-cer, acquired a

total of about four million company shares in

late May. Valued at approximately US$96 million, the cashbased

purchases are certainly a positive omen for future eaings growth.

The average insider purchase in the UnitedStates is US$60,000. When

two powerful executives spendalmost US$100 million of their own

cash as the stock hits 52-week low, its worth noticing.

But insider buying doesnt stop at Dell, either. AIG, the worlds

largest insurance company by market capitalizatiosaw two insiders

purchase US$200,000 worth of shares inlate May following the market

sell-off.

Another high-value Global Titan, Johnson & Johnson ,recently

increased their dividend for the 43rd consecutiveyear, raising the

latest annual payout by 15%. Many of theGlobal Titans have also

raised their payout ratios since thebear market low of 2002,

including stock buybacks, speciacash distributions and even bold

compensation plans forexecutives.

At Coca-Cola , the worlds largest soft-drinks company,the Board

of Directors recently voted to tie corporate com-pensation and

options to performance targetsone of thefirst schemes now in place

at a Fortune 500 company.

Like all ETFs, the Global Titans in the United States andGermany

are inexpensivecertainly much cheaper thanactively-managed funds.

At 0.5% per annum, a globalinvestor accesses many of the worlds

most profitable con-glomerates, all in one convenient ETF.

The German Hub for ETFsExchange-traded-funds provide low cost

indexing across

sectors, countries and even commodities, while also levyinmuch

smaller annual management fees than actively-man-aged mutual funds.

Over the long-term, ETF fees can savean investor a small fortune.

The average actively-managedfund in the United States charges 1.47%

per annum com-pared to just 0.35% for ETFs.

The United States remains the epicenter of exchange-trade-funds

with the S&P 500 Index, or SPIDERS, thehome to US$50 billion in

assets, making it the largest ETFin the world. ETFs in the United

States managed US$296billion as of December 31, 2005.

The problem with U.S.-listed ETFs, however, is that all these

products are valued and denominated in a heavily indebted currency.

The dollar remains in a secular bear maket since 1971 when the

Nixon administration effectively closed the gold standard. And

since 1987, the dollar hasplummeted more than 50% against the

worlds hardest currencies.

ETFs in Europe have boomed over the last six years.The Deutsche

Borse Groupin Frankfurt has emerged as the large

70

68

66

64

62

60

Jul Sep Nov Jan05 Mar May Jul Sep Nov Jan06 Mar May

streetTRACKS Glb Titans E.T.F. (DGT-A) as of May 31, 2006

Global Titans Are a Buy

A declining dollar combined with a major shift inearnings

momentum for large-cap stocks is very

bullish for Global Titans.

Source: Globeinvestor.com

(Continued on page

-

7/28/2019 Emergency Retirement

7/167

Worse than Worthless:3 Asset Protection Scams Exposed

A SSET PROTECTION STRATEGIES

By Mark Nestmann

At least once a week, someone contacts me to announce a new

asset protection scheme, and with near-religious inten-sity,

implores me to promote it. The schemes usually prom-ise significant

tax benefits and investment returns of 100%or more annually!

In 20 years of studying asset protection methods, I havenever

found one of these schemes effective. Indeed, the vastmajority of

these plans are worse than worthless.

In fact, some of these asset protection plans not only help you

lose your protected assets, but can also land youin prison. Or help

the IRS, rather than your creditors, seize

your assets. Year after year, the schemes never really change.

Only

their names change. As one promoter is shut down, tenmore take

its place. Some of the scams originated more than80 years ago and

are still going strong!

Thats not to say theres not a crying need to protectassets. The

U.S. is by far the worlds most litigious society, with more than

50,000 lawsuits filed eachweek.But if anasset protection promoter

tells you one on more of the fol-lowing things, RUN (dont walk)

away:

(1) My plan will result in big tax savings. With the excep-tion

of asset protection plans involving insurance, annu-ities and

certain retirement plans, asset protectionplanning is

tax-neutral.

(2) If you follow my investment advice, youll achieve great

returns plus asset protection. Those who offer invest-ment advice

are seldom asset protection experts, andvice versa.

(3) When you form this trust (foundation, corporation, etc.),

youll achieve complete secrecy and total anonymity. Since

most asset protection plans must be tax-neutral, this is a

dubious claim, because U.S. persons are taxable on their worldwide

income. Plus, most asset protection struc-tures involve extensive

IRS reporting requirements.

(4) Youll maintain total control over your assets at all times.

Virtually all asset protection techniques result in trans-ferring

legal ownership or control of assets to a thirdparty. Thats one of

the main reasons these are effective.If a promoter claims this isnt

necessary, its near-100%certain youre witnessing a fraud.

The Most CommonlyEncountered Asset Protection ScamsNevada

Corporations: Corporations are usually lousy

asset protection vehicles for individuals. (In certain

cases,corporations may offer businesses asset protection,

althouglimited liability companies are often more

effective.)Nevadacorporations are the worst offendersnot because

theresanything intrinsically wrong with them, but because of

thepromoters 25 years of false promises.

Heres the form the pitch generally takes:

Nevada is the only U.S. state that lets you use beareshares,

meaning you can anonymously transfer the ass

shares represent and no one really knows who owns youration. So,

you can give the shares to Aunt Milly beforeappear in court and

testify under oath, I dont own the And everyone, including your

creditors, your creditorsand the judge will believe you.

First, its far from clear Nevada law even permits bearershares.

Since 1942, Nevada has required a transfer of stocbetween

individuals, in order to receive recognition by thecorporation,

must be registered upon its books. That cer-tainly sounds like

registered shares to me! And creditorscan subpoena your

corporations books. Thus, simply hand

ing Aunt Milly your shares hardly constitutes a change

ofownership.

And because stock shares are personal property, all

rulesregulations and taxes which apply to personal property

tranfers also apply to bearer share transfers. So, assuming

AunMilly DOES own the shares you gave her, delivering thoseshares

will trigger a U.S. federal gift tax up to 46% of theifair market

value. When Aunt Milly gives them back,another gift tax is

triggered.

Pure Trusts: An 80-Year-Old ScamThese arrangements supposedly

allow a person to transf

all their property into the trust, never pay taxes again,

andsecure asset protection. These scams are also called commlaw

trusts, equity trusts, unincorporated business organzations (UBOs),

liberty trusts, contractual companies,colatos, and unincorporated

business companies (UBCs

These schemes seldom result in asset protection becausethe

person funding the trust generally retains complete control over

the trust and its assets, and there are serious taxproblems with

virtually all variations. You are the grantor

-

7/28/2019 Emergency Retirement

8/16

-

7/28/2019 Emergency Retirement

9/16

-

7/28/2019 Emergency Retirement

10/1610

THATS THE W AY IT L OOKS FROM HERE

Your New Country in a Matter of Months:Economic Citizenship for

Sale

By Robert E. Bauman, JD

I often get questions concerning how to acquire dual citi-

zenship and the second passport that comes with it. Folks want

to know how it can be done, and why they shouldconsider it.

I start by assuring them that dual citizenship is legal under

American law, as it is in many nations, and that the U.S.Supreme

Court upheld this right in several cases decadesago. And of course,

if the person is interested in expatria-tion, the formal act of

surrendering U.S. citizenship (also a legal right), I explain that

they certainly need a second citi-zenship to avoid becoming a man

(or woman) without a country, a modern day version of Edward

Everett Hales

disturbing novel from 1917. A second nationality is a hedge

against unforeseen events.

It provides the option to legally reside and work in

anothercountry that may offer tax advantages, although this is of

limited benefit to U.S. citizens. (If you are a U.S. citizen

orgreen card holder, you are still accountable to Uncle Sam when it

comes to reporting your taxes, no matter where youlive.)

Most countries require a foreigner to become a residentand live

there for an average of five years or more before they are granted

citizenship. But there is a quick route to a sec-ond passport in

just a matter of monthsbut it will costyou dearly.

Its known as economic citizenship and only two sover-eign

nations sell it, both tropical island tax havens in theCaribbeanthe

Commonwealth of Dominica and St.Kitts/Nevis.

Escape from AmericaUsing the excuse of drug wars and

anti-terrorism, plus

imposing excessive taxation, government controls on

privatecapital and travel restrictions are becoming more

prevalent

around the world. Smart people of wealth naturally are seek-ing

alternatives that allow them to protect their assets andincome and

to travel freely throughout the world. And, inthe case of the

United States, the only way to escape fromtaxes is to end your

citizenship.

Two Caribbean jurisdictions offer economic citizenshipunder

government-sponsored investment laws. These nations want to create

jobs, accelerate resort development and grow their tourist

industries by bringing in more money. The lawsprovide a foreigner

with instant citizenship, a new passport,

and permanent residence, if desired. And both countries

aoffshore tax havens.

Become a Saint Kittian or NevisianSt. Kitts & Nevis is an

independent English-speaking

island state situated in the northern part of the LeewardIslands

in the eastern Caribbean. The federation is made upof two islands,

St. Kitts and the smaller Nevis, separated bchannel two miles wide.

It is a former British colony, a member of the British Commonwealth

of Nations and theUnited Nations. It has a pleasant climate,

particularly durinthe cool months from December to March. Humidity

is relatively low, and constant northeast trade winds keep

theislands cool.

St. Kitts & Nevis offers good opportunities for investorsand

manufacturers. The workforce is well-educated, Englisspeaking and

friendly. Other advantages include tax breaksof up to 15 years,

repatriation of profits and the possibilityof tax-free entry of

produced goods into the U.S. market.Substantial European import

benefits also apply. There areno income taxes and no net wealth

taxes in St. Kitts &Nevis.

St. Kitts & Nevis labels their instant citizenship

plan,Citizenship-by-Investment Program. To qualify for citizeship,

the government requires a real estate investment of at

least US$250,000. The islands are an attractive place to owreal

estate, and there are some excellent real estate developments

approved under the program. The new citizen is notrequired to spend

any set period of time on the islands eacyear.

Alternatively, there is an option available to purchase

goernment bonds. Instead of real estate, one can purchaseUS$250,000

equivalent in EC$ (Eastern Caribbean cur-rency) Literacy Month

10-year Treasury bonds. Details of this program are not yet final

and no date has been set forthe next bond issue.

Additional costs include official government fees of US$35,000

for a single applicant, plus US$15,000 for eachdependant. There are

also application/professional fees of US$15,000 (same as with

Dominica) per application and aUS$2,500 due diligence fee per adult

applicant. They require a reasonable amount of documentation for

the applcation, and the application procedure itself is fairly

simple

The St. Kitts & Nevis passport is relatively well

regardesince only a relatively limited number of passports have

bissued under this citizenship-by-investment program durin

-

7/28/2019 Emergency Retirement

11/1611

its nearly 20 years of existence. As a result, St. Kitts &

Neviscitizens enjoy a passport with a good reputation and

goodvisa-free travel. For example, passport holders still have

visa-free access to Canada. Visa-free travel throughout

continen-tal Europe is also available by combining St. Kitts &

Neviscitizenship with a residence permit in European

Unioncountries.

A Passport of the Commonwealthof DominicaDominica is often

called The Nature Island of the

Caribbean. Its a small, beautiful island located in the east-ern

Caribbean between the French islands of Martinique andGuadeloupe.

Independent since 1978, Dominica is English-speaking and a member

of the British Commonwealth. Ithas a Westminster-style

parliamentary government, free elec-tions and peaceful transfer of

power. There is a strong cur-rency and almost no crime. Unlike some

other states offering economic citizenship, Dominica has a good

reputation.

The economic citizenship program has operated success-fully

since 1991, and it is based on a solid legal foundationin the

Constitution of Dominica. A limited quota of appli-cations has been

set by the government.

There are now two options for obtaining citizenship: a Family

Option and a Single Option. Under the Family

Option, the applicant pays US$100,000, which qualifies

thapplicant, his or her spouse and two children under 18 yeaold for

citizenship. An additional US$25,000 per child isrequired for each

child under 25 years old. Under the SingOption, a single applicant

pays US$75,000. In addition tothe above additional application,

agent and registration feeamount to approximately US$2,200. There

is also a US$5,000 due diligence fee per person.

Further information on each program: St. Kitts & Nevis:

www.henleyglobal.com/stkittsnevis.h Dominica:

www.henleyglobal.com/dominica.htm

You may contact a member of The Sovereign Society Council of

Experts, Mr. Christian Kalin, Executive DirectoHenley &

Partners AG, Kirchgasse 24, 8001 Zurich,Switzerland. Tel: +41

44-266-2222; Web: www.henley-global.com; Email:

[email protected].

The Passport Book covers second passports in detail. Morabout

the book at LINK: www.agora-inc.com/reports

190SGOPS/W190D342.Robert Bauman is Legal Counsel for The

SovereSociety and editor of The Sovereign Society Offshore

A-Letter. A former member of the U.Sof Representatives from

Maryland, he is a graduthe Georgetown University Law Center (1964)

a

School of Foreign Service (1959).

THATS THE W AY IT L OOKS FROM HERE

The Scourge of Exit Taxes While emigration, the right to move

freely among nations,

is a basic right confirmed by the UN Charter and in

interna-tional treaties, many countries try to impose emigration

(exit)

taxes in an effort to preserve tax claims over citizens who

leave.The most brutal of all such taxes can be traced to Nazi

Ger-many when all the assets of Jews lucky enough to escape

wereconfiscated. Apartheid South Africa imposed a similar levy on

whites who left to live abroad.

But democracies do it too. The most sweeping tax is a general

exit tax, the sort of proposal that, fortunately, recently was

rejected by the U.S. Congress. That scheme provided thatif a U.S.

person surrendered their citizenship for tax-moti-vated reasons,

they would be taxed on all unrealized gains onthe fair market value

of their entire estate. This tax graballowed, generously, a

US$600,000 exemption.

How anyone could pay such a huge tax is anyones guessin

practice, most expatriates would be forced to liquidatemuch of

their wealth to pay it. The only way to avoid paying the tax would

be to post a bond equal to the tax liabilityorto elect to continue

being taxed as a U.S. citizen, (or to sell allyour assets before

you ended your citizenship).

If this Draconian plan had become law it would haveapplied not

just to wealthy Americans, but also to hundreds of thousands who

are dual nationals: persons born abroad to a U.S. parent or born in

the U.S., many of whom live outsidethe United States. The proposal

would also catch hundreds of thousands of wealthy U.S. resident

aliens (green card holders) who are not U.S. citizens.

Only Canada imposes an exit tax similar to the proposalrejected

by the U.S. Congress. It applies when a long-termCanadian resident

becomes non-resident for tax purposes.Since Canada (along with

virtually every other country, withthe exception of the U.S.)

imposes taxes based only on physi-cal residence, and not

citizenship, Canadians do not have togive up citizenship in order

to escape taxes. They can justmove and live offshore.

A limited exit tax, which many EU nations levy, extendsonly to

certain kinds of property; typically securities. Anotherform of

emigration taxation is extended income tax liability. Your former

country taxes you even though you no longer livethere. Many EU

countries, Canada and the United States try to impose tax on this

basis. The U.S. makes a ten-year claimfor taxes when a U.S. person

ends citizenship.

Exit taxes by their nature impede the right to move freely.On

this basis, in 2004, the European Court of Justice struck down a

relatively mild French exit tax. That decision probably nullifies

the exit tax regimes of all EU members.

The U.S. Congress, however, may be moving in the wrong

direction. Its possible an American exit tax will become law inthe

next few years, perhaps sooner. U.S. citizens considering

expatriation as a tax saving measure may only have a shorttime to

act. Think about it!(This is adapted from Mark Nestmanns masters

degree thesis, Change odence by Natural Persons in Light of the EC

Freedoms, published in Aigner/Loukota, Source versus Residence in

International Tax Law [Lind

-

7/28/2019 Emergency Retirement

12/1612

BEHIND THE TRADING L INES

By David Newman You wont find a lot of The Sovereign Societys

investment

recommendations in Money magazine. You cant read aboutour best

performing offshore funds inWall Street Global . Andyoure not

likely to read about our best way to play the Japanese yen against

the British sterling even on the frontpage of theFinancial Times .

Thats because our investmentexperts tend to stray away from the

mainstream media.Instead they dig deeper to discover the

unpublicized invest-ment opportunities. They often seek out

undiscovered trendsyour broker cant even predict. And our

investment editorsare doing it again this month.

Double and Triple-Digit InvestmentOpportunities in Currencies

and Funds

For example, at our editors recommendation, select sub-scribers

sold the Laurentian Bank for a sweet 37% profit back in April after

only 14 months. This is an example of whatEric Roseman recommends

every month inGlobal Mutual Fund Investor . In his May issue, Eric

also gave subscribers a detailed chart of how they should diversify

their portfolios, with the majority in hedge funds (a full 30%). He

also

warned his subscribers of the inevitable correction coming

(which we all felt in mid-May). Check out

www.globalmutu-alfundinvestor.com for more information.

Every month in this section, Im going to give you a glimpse at

Erics best offshore mutual fund picks. And Illalso tell you about

the best way to trade currencies right now.There are no better

traders to ask thanThe Money Trader seditors, Kathy Lien and Boris

Schlossberg. As we went toprint, Kathy and Boris had just picked

eleven currency tradesin a row forThe Money Trader s subscribers.

And over thepast year,FX Magazine rated Kathy and Boris the #1

cur-rency traders for a three-month period twice.

One of the currencies Kathy and Boris are bullish on long-term

is the Canadian dollar or loonie as its called in thetrade. Right

now its at US$0.89. Boris and Kathy expect thatthe Canadian dollar

will shoot up higher than the U.S. dollarin the next 12-24 months.

You can trade that directly in thecurrency spot market. You can

play that without leverage orplay it aggressively with leverage

where a 10% move couldresult in 100% profits for you. See

www.money-trader.comfor more information.

Small-Cap Stocks & Commodities Com-pletely Off Your Brokers

Radar

And there are other great ways you can play the Canadidollar.

You can play it indirectly by owning a good Canadistock. And thats

just what John Pugsley is recommendingreaders of his trading

service,Stealth Investor . John isextremely bullish on natural

resources. He thinks certain juior resource Canada companies can

give you a double banfor your buck, appreciation for your stock and

appreciationof the currency. I cant name Jacks current gem of a

small because he often recommends such micro-cap stocks thatcould

double or more in a very short time (especially if evSovereign

Society member bought them), and thats why hlimited the excellent

service to 500 subscribers. Visit www.stealthinvestor.com if youre

interested in becoming of those 500 members.

Fortunately, we happen to have Eric Roseman on staff.Like Boris

and Kathy, hes bullish on the Canadian dollar.Not only that, Eric

is Canadian and, of course, hes long-tebullish on select Canadian

commodities. In fact, in 2001, hfounded the immensely popular and

remarkably accurateCommodity Trend Alert trading service just to

follow thosetypes of commodity trends. One of his

favoriteCommodityTrend Alert Canadian resource stocks is Strategic

Energy Fund, which youll find in your Sovereign Society

portfoliThis energy fund just corrected, giving you a great

opportunity to buy more. If youd like to play commodities

moreactively, you might want to check outCommodity Trend Abecause

Erics other 23 long positions are averaging 124%right now. Thats

even after the recent massive correction! And thats just an

average. Eric has shown readers profits 77%, 99%, 129%, 146%, and

up to 966%. Search www.commoditytrendalert.com for more

details.

Keep an eye out for this section in future issues. Wellsnatch

one or two of the best investment ideas from the edtors of The

Sovereign Society weekly investment trading sices and give you a

brief glimpse.

Until next month, keep your ear to the investmentground

David Newman is The Sovereign Society's MembDirector. He's

dedicated to helping you make the your membership. Call him today

at 561-272-53118 or email him at [email protected].

Four of the Best Ways to Profit in the GlobalMarketplace: Global

Mutual Funds,

Currencies, Commodities, and Small Caps

-

7/28/2019 Emergency Retirement

13/1613

THE W ORLD OF THE SOVEREIGN SOCIETY

more than 40% (with returns of 42%, 41%, 51%, 44%, and60%).

But Denmark doesnt offer the same level of banking pri-vacy as

Austria or Switzerland because theres no bank secrecy law. And at

the end of each year, under the EU taxdirective, all Danish banks

must turn over clients informa-tion to the Danish tax office, which

is free to share that data with foreign tax authorities.

Liechtenstein: Iron-clad AssetProtection with Safe-Haven

Currency OptionsLiechtenstein, a tiny independent enclave

nestled between

Switzerland and Austria, is a banking haven in its own

right.This Swiss neighbor uses one of the safest currencies in the

world: the Swiss franc. Plus, Liechtenstein has a reputationof

having even more bank secrecy than Switzerland. Bank secrecy may

only be lifted by a local court order and Liecht-enstein rarely

recognizes other countries mandates. TheLiechtenstein government

also insures all bank accountsno

matter how large.

However, this level of sophisticated asset protection doent come

cheap. Liechtensteins banks have no official minmum, but they try

to attract high net-worthindividualswhich means fees are high.

So as you can see, even with higher fees, banking offshocan

definitely pay off in the end (sometimes in double-digireturns).

You can bank in regions where your bankers are

bound by law to keep your assets safe. You can maintain alevel

of complete financial privacy where no onefrom exspouses to

creditors to settlement-seeking lawyers can dis-cover your assets.

Plus, you can keep your wealth in a hoscurrencies to protect

yourself should your native currency ever plummet. Everyone should

have some money outsidetheir home countrys banking system. Even if

its just as a safety net. You never know when you might need

it.

Kathlyn Von Rohr is the new managing editor of The

SovereSociety. She manages the content of both The Sovereign

Indiand the daily Offshore A-Letter.

Continued from page 9:The New Offshore BankNo Longer Just for

Millionaires

The World of The Sovereign Society

Decoding The Sovereign SocietyMembers Only Website

If you ever have a question about who we are or what we do here

at The Sovereign Society, you can quickly find

the answer to just about any question on our website. But with

so much content on our constantly updated website, wed like to

point you in the right direction of our mem-bers only content and

help you decode what each sectionentails. To access the members

only sections, go to ourhomepage at www.sovereignsociety.com and

then look forthe members tab at the top of the page. Click on

yourdesired section (see below) and then log in.

Members Only Sections:The Sovereign Individual:Read all past

issues of The Sov-

ereign Individual , with all their wealth preservation

recom-

mendations, investment advice, residency and visa information,

and privacy protection ideas.

Portfolio:Check out how your Sovereign Society invest-ments are

faring in this current turbulent market.

Your Council of Experts:Contact any member of ourcouncil of

experts for your personal financial questions with our updated

council of experts rolodex.

Your Offshore Convenient Account:Find out which off-shore bank

is right for you, how to choose an international

bank, where to set up your account, the type of accountthats

right for you, and even important information aboutbanking

fees.

White Paper Reports:Updated regularly, this currently includes

10 free reports for you to read at your leisureincluding 70 Days to

Empty ; Fab 4: The 4 Best Offshore Havens in the World ; Amazing

Annuities ; and many more.

A Brand New Section:Membership Handbook

As one of our valued Sovereign Society members, yourconstantly

receiving information from us. Ever wish weprovided a manual so you

could keep the basics straight?Now you have one. The How to Protect

Your Assets andGrow Your Wealth: The Sovereign Society Handbook

isnow available on the website. This handbook allows you tobecome a

more informed Sovereign Society member. Youcan use this handbook

to

Maximize your earning potential with The SovereignSociety's

"Rules of Thumb" for investing

Discover which conference fits your particular

financiasituation

Take a closer at each of our investment trading service Find out

how The Sovereign Society all began.Check out the new Membership

Handbook today by

visiting www.sovereignsociety.com/login.php?nid=1684.

-

7/28/2019 Emergency Retirement

14/1614

PORTFOLIO UPDATE

Global Correction to Create Eventual BargainsBuy Precious Metals

and Energy

on Intermittent Weakness

By Eric Roseman

In May, The Sovereign Individual (TSI)portfolio sufferedits

worst monthly loss in over a year as global commoditiesand stocks

plunged. The good news is we correctly preparedfor a major decline

two months agojust emerging marketsand the majority of

industrialized bourses posted significantlosses. From a universe of

38 open positions, theTSI portfolio has posted a 95.3% total return

based on ourequally-weighted strategy. Returns include dividends,

if any,and foreign currency conversions.

This month, were pruning theTSI portfolio and selling two

positions at hefty gains.

The Jyske-Invest Emerging Markets Bond Euro Fund hasgained a

cumulative 61.3% in U.S. dollars since May 2003. With emerging

markets coming undone since mid-May, itstime to book our gains and

close-out our fixed-incomepositions in this asset class. Effective

June 1,TSI no longerholds emerging market bond positions, except

Russias Mobile Telesystem, which pays a 9.75% yield and matures

inNovember 2008. In May, this bond only declined 1%.

On May 22, members received a specialTSI Profit Alert to sell

IndiasTata Motors ADR at a 72% profit since April2005. India, the

emerging markets flavor of the year, hascorrected heavily so were

ejecting Tata Motors, our lastemerging markets equity position.

Global Correction Has Arrived With global interest rates rising,

inflationary pressures

increasing and soaring input costs likely to affect earningsthis

year, its time to bury the hatchet and get defensive.

From its five-year high in early May, the S&P 500 Indexis

off 7%. Historically, corrections imply an average 10-15%decline

from index highs. This summer, further weakness forcommon stocks

will eventually create some great buying opportunities, in emerging

markets and natural resourcestocks. Seasonal stock market weakness

has now arrived and will most probably last until late summer or

early fall.

So were focusing on defensive global blue-chips, energy stocks,

precious metals, and betting against further marketdeclines with an

inverse U.S. index fund. Also, with the Fedstill raising interest

rates this summer, the oversold U.S.dollar might enjoy a short-term

bear market rally. Use any short-term dollar weakness to purchase

foreign currencies

and commodities, especially beaten-up gold and silver atthese

very low levels. As the U.S. approaches the end of thmonetary

tightening cycle later this summer or fall, thedollar will head

sharply lower. Remember to sell dollars onany intermittent strength

and add to your precious metalsholdings.

TSI Best Buys for JulyExchange/ Gain/ Buy-

Security Symbol Domicile (Loss) up-toDow Jones Global

Titans Euro DE0006289382 Frankfurt New 23Strategic Energy

Fund SEF.UN Toronto +3.75% C$13ProFunds

Ultra Bear Service URPIX USA +4.96% $18Goldcorp GG NYSE +101.44%

$30Merrill Lynch

World Energy LU0122376428 Luxembourg +14.46% $2TSI Asian

Currency Sandwich None Everbank USA +2.26% $3Pall Corporation

PLL NYSE +6.22% $31Zurich Financial ZURN Zurich +15.65% CHF

For Best Buys in July,TSI is heading to Frankfurt,

Germany, for euro-denominated, low-cost global indexing.The Dow

Jones Global Titans 50 SM EX exchange-traded-

fund is the best value in the world right now among majormarket

indices. Over the last five years, the average globalblue-chip

stock has gone nowhere. Yet this index fund,denominated in euros,

offers a host of compelling high-valattributes, including a low

multiple (13 times price-to-earnings, 2.8% yield), while trading at

a significant 35%discount to the MSCI World Index based on relative

p/e ratioThe Dow Jones Global Titans 50 should hold its own

asglobal money managers shift capital to defensive compani

with reliable earnings. Over the next several years,

blue-chstocks should return en vogue as investors search for

reliabrevenues amid a slowing world economy.

Theres no doubt CanadasGoldcorpis the best-managedgold-mining

company this decade. Goldcorps averageproduction cost is just

US$180 per ounce. With every incremental rise in gold bullions

price, her profits aremultiplying. The current gold correction

offers an excellenentry point for new and existing investors

seeking exposurto this tremendous mining company. Add to your

positionsbelow US$30.

-

7/28/2019 Emergency Retirement

15/1615

Symbol/ Exchange/ Buy Price TotalInvestment ISIN Domicile Added

Price 5/31/06 Returns Advice Notes

COMMODITIES

Anglo American ADR AAUK OTC TSI 4/04 5.79 19.34 250.69% Hold 2

for 1 stock-splitASA ASA NYSE TSI 2/00 14.89 60.32 334.65%

HoldBarrick Gold ABX NYSE TSI 2/00 15.28 29.77 104.19% HoldBema

Gold BGO AMEX TSI 8/02 1.02 5.32 421.57% Hold

Bonavista Energy Trust BNP.UN Toronto TSI 3/04 C$13.65 C$35.50

271.57% HoldCanadian General Investment Limited CGI Toronto TSI

11/05 C$19.52 C$25.50 37.23% HoldCanexus Income Fund CUS.UN Toronto

TSI 2/06 C$8.90 C$7.51 -10.18% HoldChicago Mercantile Exchange CME

NYSE TSI 4/03 47.10 433.32 828.49% HoldENI Spa ADR E NYSE TSI 11/03

28.53 59.37 126.54% HoldGold bullion none TSI 4/04 428.63 630.50

47.10% Buy Buy up to $675Goldcorp GG NYSE TSI 1/05 14.87 29.70

101.44% Buy Buy up to $30.00Merrill Lynch World Energy Fund Class A

US$ LU0122376428 Luxembourg TSI 9/05 20.40 23.35 14.46% Buy Buy up

to $25.00Merr ill Lynch World Mining Fund Class A US$ LU0075056555

Luxembourg TSI 2/04 23.80 50.51 112.23% HoldOppenheimer Real Assets

Fund Class A QRAAX USA TSI 8/03 5.11 8.12 59.42% HoldPalladium none

TSI 1/05 175.00 358.00 104.57% HoldPrimewest Energy Trust PWI.UN

Toronto TSI 3/04 C$15.36 C$32.87 224.14% HoldStrategic Energy Fund

SEF.UN Toronto TSI 5/01 C$12.52 C$12.81 3.75% Buy Buy up to

C$13.50U.S. Global Investors World

Precious Minerals Fund UNWPX USA TSI 1/06 20.32 28.93 42.37%

Hold

INTERNATIONAL VALUE

Aegon AEG NYSE TSI 1/05 13.17 16.49 31.51% HoldDiageo DEO NYSE

TSI 4/03 37.25 66.13 93.77% HoldKeppel K02 Singapore TSI 12/05

S$11.5 13.40 23.08% HoldPALL Corporation PLL NYSE TSI 2/06 28.45

30.00 6.22% Buy Buy up to $31.25SIPEF SIP Brussels TSI 3/05 129.30

170.00 36.82% HoldTata Motors ADR (India) TTM OTC TSI 4/05 9.47

16.03 71.70% Sold 5/22Zurich Financial ZURN Zurich TSI 12/01 CHF

311.85 CHF 275.5 15.65% Buy Buy up to CHF 300

CURRENCIES, BONDS, & ALTERNATIVE INVESTMENTS

TSI Asian Currency Sandwich (5 currencies) Everbank TSI 3/06

34.36 33.60 2.26% Buy Inverse IndexMan-AHL Diversified PLC

IE0000360275 Ireland TSI 2/04 50.21 64.94 29.34% Buy Long-term

BuyJyske Euro Emerging Market Bond Fund A0B726 Denmark TSI 5/03

108.00 158.70 61.34% SELLMobile Telesystem 9.75%, 11/30/08 [USD]

XS0162126287 TSI 3/04 109.69 104.00 11.79% Hold100% Capital

Protected Notes Based on the

American Stock Exchange China Index CAX AMEX TSI 12/05 9.11 9.52

4.50% Hold

Pioneer-Momentum Emerald BMG6198G3123 Bermuda TSI 11/98 102.80

206.28 100.66% Buy Long-term BuyPIMCO Foreign Bond Unhedged PFBDX

USA TSI 6/05 10.47 10.36 0.92% HoldProFunds UltraBear Investor

Class URPIX USA TSI 4/06 16.52 17.34 4.96% Buy Buy up to

$18.25Principal Protected Notes

(Basket of Asian Currencies) CAQ AMEX TSI 11/05 9.43 9.70 2.86%

Hold

GLOBAL EQUITY FUNDS

iShares FTSE/Xinhua China 25 Index Fund FXI NYSE TSI 8/05 60.54

72.88 20.38% HoldOrbis Global Equity Fund BMG6766G1087 Bermuda TSI

1/06 94.46 99.40 5.23% Hold Closed to investorsPictet PF-Biotech P

Fund LU0090689299 Luxembourg TSI 11/04 211.40 240.91 13.95%

HoldPolaris Global Value Fund PGVFX USA TSI 1/06 16.20 17.60 8.64%

Hold

AVERAGE RETURN 95.26%

BUY THE FOLLOWING NEW POSITIONS

Dow Jones Global Titans 50 SM EX (euro) DE006289382 Frankfurt

TSI 6/01 21.47 21.47 New Buy Buy up to 23.00

SELL THE FOLLOWING POSITIONS

Jyske Bank Emerging Markets Bond Fund Euro Class; Tata Motors

ADR.

Notes: The TSI Portfolio is an equally-weighted strategy and

does not include dealing charges to purchase or sell securities, if

any.Taxes are notincluded in total return calculations. Total

return includes gains from price appreciation, dividend payments,

interest payments, and stock splits forsecurities listed on

non-U.S. exchanges, total return also includes any change in the

value of the underlying currency versus the U.S. dollar.

Anglo-American ADR stock-split 2 for 1 on March 6, 2006; entry

price reflects stock-split; Oppenheimer Real Assets Class A paid

distribution of$0.04 per share on March 16, 2006; Class C paid

$0.04 on March 16, 2006.

Stop-losses: The TSI Portfolio maintains a 15% stop-loss on

every stock and bond recommendation; stop-losses are not exercised

for mutual funds.

Sources for price data: Yahoo! Finance (finance.yahoo.com),

Financial Times Portfolio Service (www.ft.com), TradeNet

(www.trade-net.ch/EN),Jyske Bank Private Banking Denmark

(www.jbpb.com), and Web sites maintained by securities issuers.

PORTFOLIO UPDAT

TSI Portfolio

-

7/28/2019 Emergency Retirement

16/16

Please note: While investing or doing business offshore is

perfectly legal for U.S. citizens and residents, there are a few

legal formalities you should keep in mind. The motant of these is

that you are responsible for paying taxes on your worldwide income.

In addition, many types of offshore investments are subject to

separate reporting requiremetransfers of US$10,000 or more in cash

or cash equivalents across U.S. borders must be reported, as well

as the formation and funding of a foreign corporation, trust or

partnerWhile its easy to comply with some of these requirementssuch

as the annual filing of the foreign bank account reporting (FBAR)

Form TD F 90-22.1, other forms (such

f l h ) l l h h l d h

CONFERENCE CORNER

Once again, The Sovereign Society will tour four of thebest

banking and asset protection havens in the world: Switzerland,

Austria, Liechtenstein, and Den-

mark. As you tour these majestic old-world nations, youll be

joined by our top international financial experts, who willreveal

their best banking and asset protection secrets during this

nine-day event.

This group of leading European experts will include

ourConvenient Account Program banking professionals and

otherpreferred financial services providers including Thomas

Fischerof Denmarks second largest bank, Jyske Bank; Peter Zipper of

Anglo Irish Bank in Austria; Robert Vrijhof of Weber, Hart-mann,

Vrijhof & Partners; and Marc Sola of NMG Interna-tional

Financial Services. Among the European money secretsthey will

reveal to you

Confidential Banking: the Swiss, Austrian and Liechten-steinian

Way, where your assets are concealed from prying eyes under penalty

of law.

First Class Estate Planning: Learn how you can accessthe

Liechtenstein-conceived and created financial vehiclethat is

completely creditor-proof and can only be accessedby your

beneficiaries.

Secret Currency Invest-ments: How you couldmake double-digit

profits trading the nine highest yiel

currencies in the world through a Danish bank. Tools to Retire

Abroad: Little-known residency andretirement programs that can

dramatically reduce yourestate tax billand help you transform your

dream of ing or retiring abroad into reality.

Taking Your Retirement Plan Offshore for asset protection,

investment diversification and greater profits.

Plus, youll meet and hear from European visa and residexperts,

international tax attorneys, investment specialists,vacy experts,

and more.

While touring these ancient wealth havens, youll stay a

best European hotels and enjoy 5-star amenities in every c Youll

enjoy VIP treatment with dinner on an oldsteamboat cruising on the

Lake Zurich, a tour of the artmuseum in Vaduz, a Gala Dinner event

in Copenhagen, anmuch more. Unfortunately, The Sovereign Society

can onlyaccommodate 40 attendees for the European Banking Tourand

seats are filling up fast. Call today to reserve your spo561-272-

0413 ext. 122. Or you can email [email protected].

Shield Your Wealth from a Lifetime ofDoubt in One Long

Weekend

Join us for the Permanent Wealth Protection Summit,October

11-15, 2006

There will be no conference rooms, microphones or podiumsat this

event. Instead, you will gather at a 5-star resort, nestledin the

Irish countryside, where you will meet one-on-one withour top asset

protection experts. Our experts will meet with youprivately to help

structure your asset protection plan. This isonly the second

Permanent Wealth Protection Summit that TheSovereign Society has

ever had and we expect Octobers summitto be just as successful as

the first. We hope youll join us for a relaxing weekend, with

plenty of time between your meetings toswim, horseback ride, golf,

play tennis, and enjoy the splendorof Irelands countryside, all

while ensuring your assets are pre-served for generations to come.

If youre interested in joining us,please contact Membership

Director David Newman by phoneat 561-272-5332 ext. 118 or email him

at [email protected] for more information.

Offshore Novices: Discover the World ofOffshore Opportunities

All At Once

The Offshore Advantage: An Introduction to the Offshore

World,

November 8-11, 2006

Interested in offshore banking but have no idea where tostart?

Does trading currencies or global securities soundexciting but you

need some advice before trading? For the time ever, The Sovereign

Society is hosting a conference spcally designed to introduce you

to the offshore world. Youlearn what an offshore trust really

entails and the best placset up one. Youll discover which banking

havens are worthtime and the easiest and safest way to set up an

offshoreaccount. A panel of our top experts will be on hand to

expthe basics for safely protecting and growing your wealth innext

year. Join us at the Sheraton Buganvillas Resort &Convention

Center in Puerto Vallarta, Mexico, to begin youfinancial adventure.

Email [email protected] for minformation.

HurryEarly Bird

Discount EndsAugust 1st

Come Explore Four Ancient Regions of Wealth Join Us for the

European Banking Tour September 20-29