Embed Size (px)

Citation preview

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 1

EMEA INVESTOR INTENT IONS SURVEY 2021 © CBRE , INC. | 2

EXECUTIVE SUMMARY

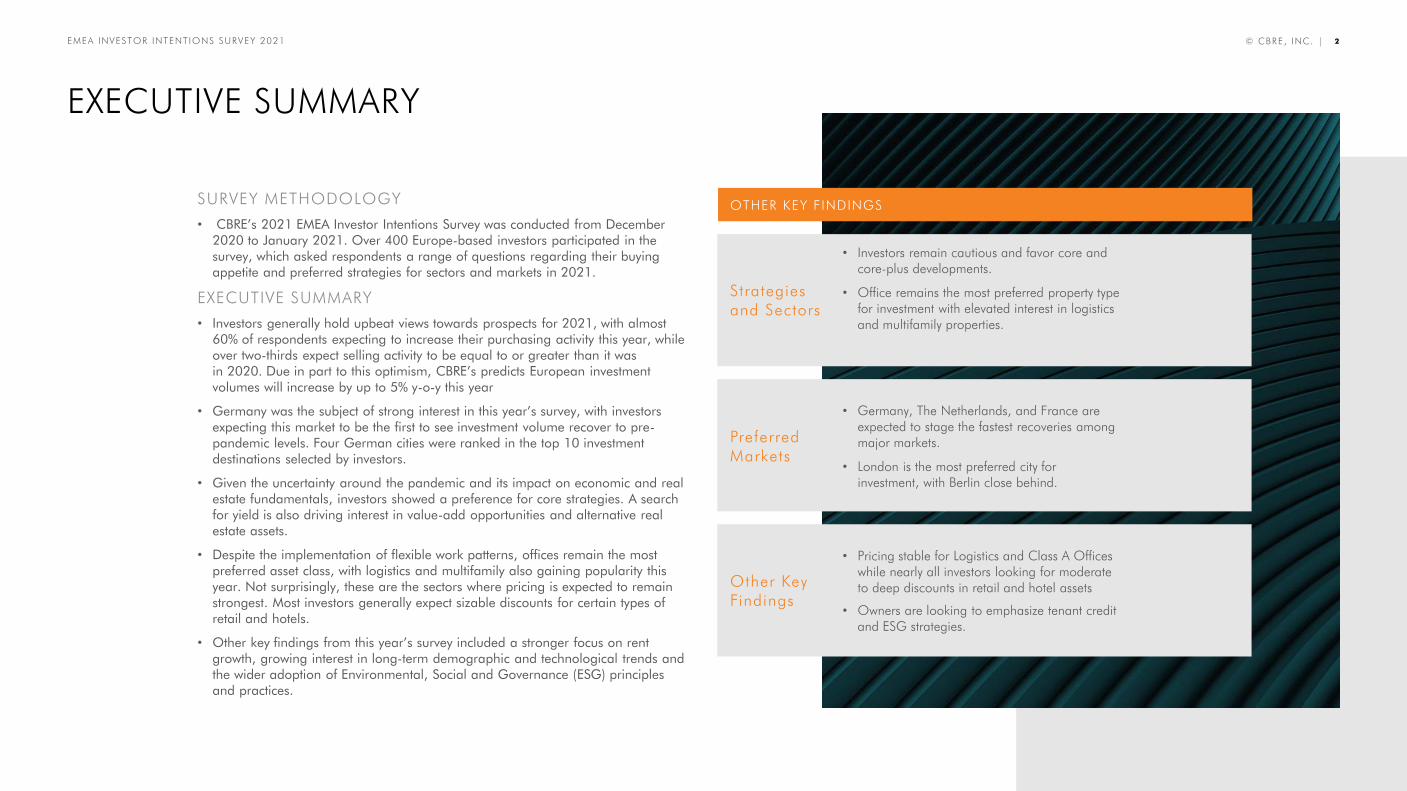

SURVEY METHODOLOGY

• CBRE’s 2021 EMEA Investor Intentions Survey was conducted from December 2020 to January 2021. Over 400 Europe-based investors participated in the survey, which asked respondents a range of questions regarding their buying appetite and preferred strategies for sectors and markets in 2021.

EXECUTIVE SUMMARY

• Investors generally hold upbeat views towards prospects for 2021, with almost 60% of respondents expecting to increase their purchasing activity this year, while over two-thirds expect selling activity to be equal to or greater than it was in 2020. Due in part to this optimism, CBRE’s predicts European investment volumes will increase by up to 5% y-o-y this year

• Germany was the subject of strong interest in this year’s survey, with investors expecting this market to be the first to see investment volume recover to pre-pandemic levels. Four German cities were ranked in the top 10 investment destinations selected by investors.

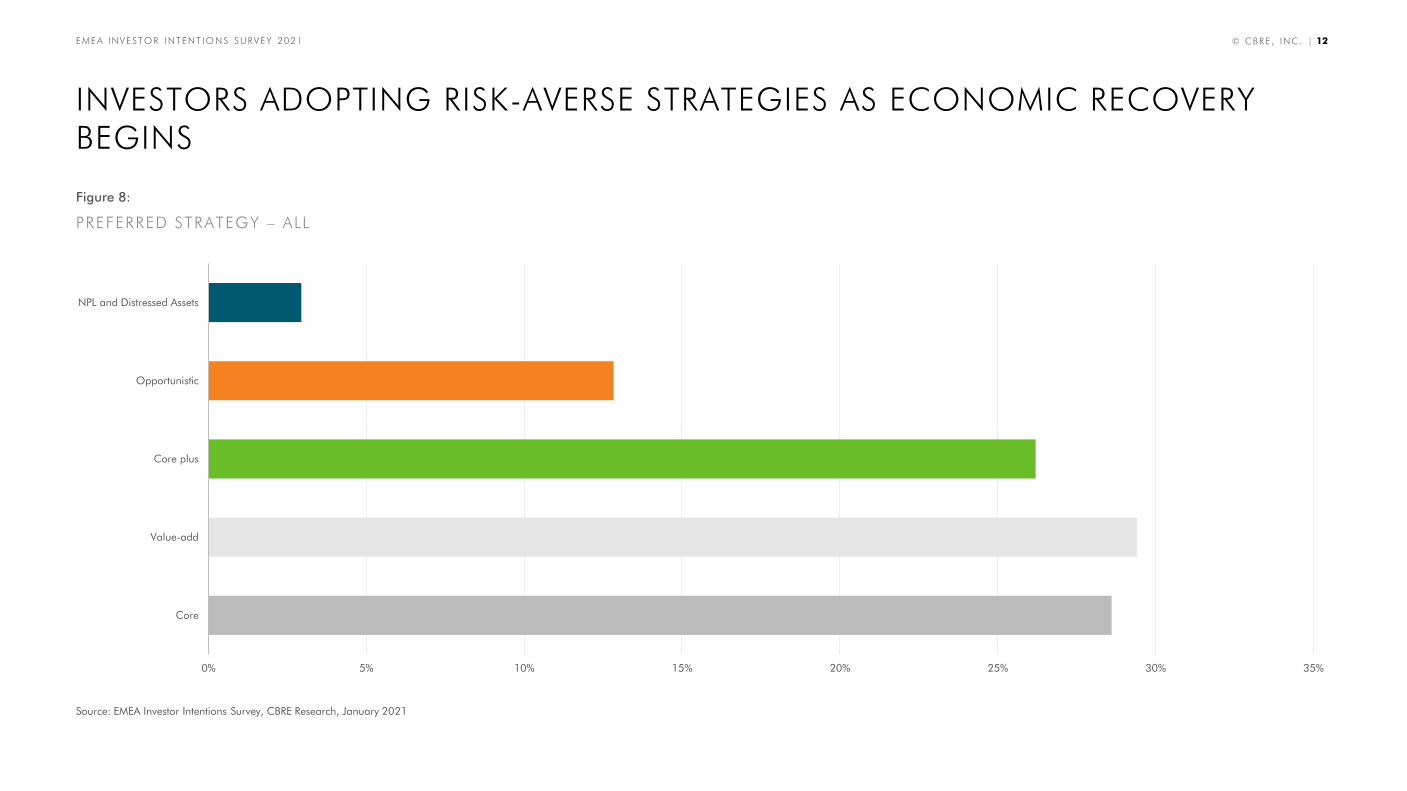

• Given the uncertainty around the pandemic and its impact on economic and real estate fundamentals, investors showed a preference for core strategies. A search for yield is also driving interest in value-add opportunities and alternative real estate assets.

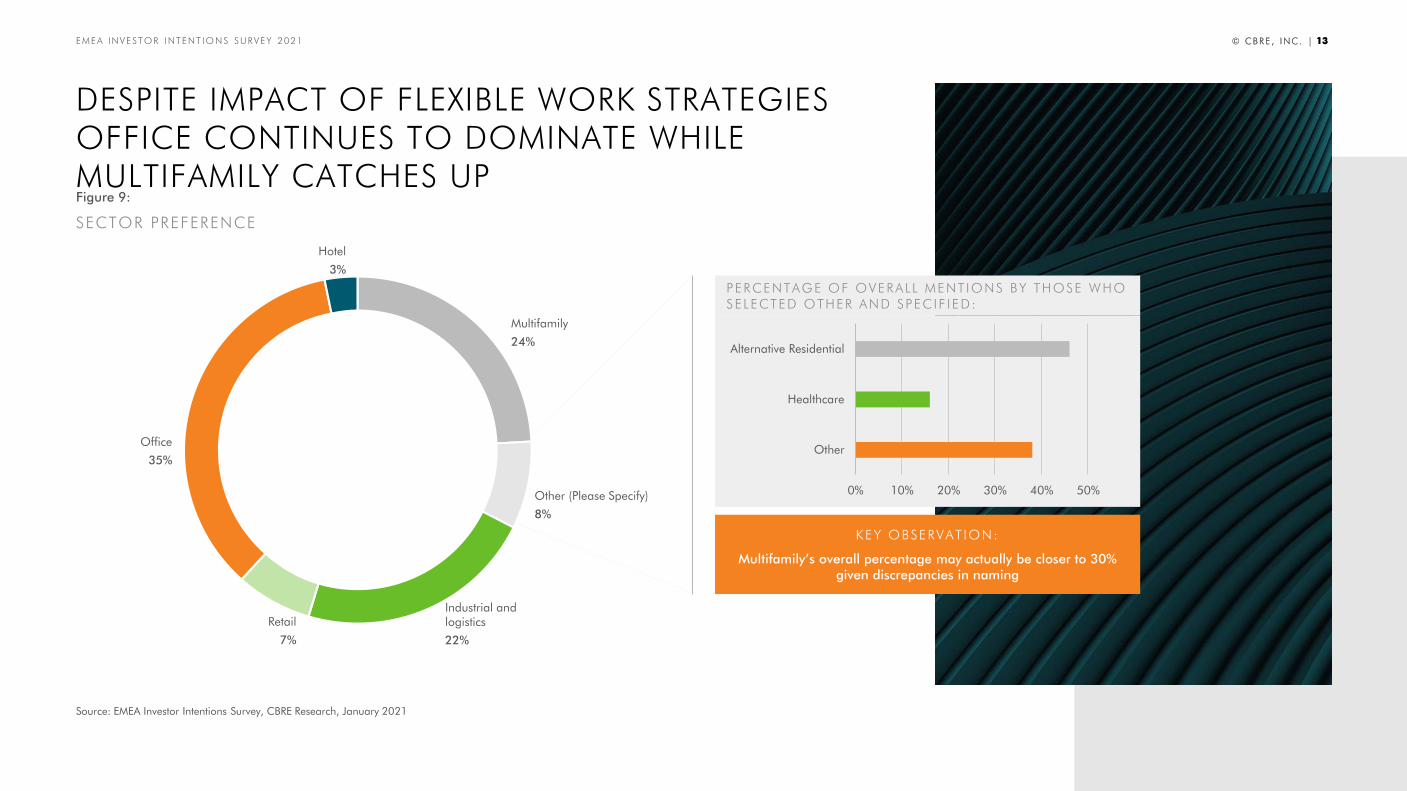

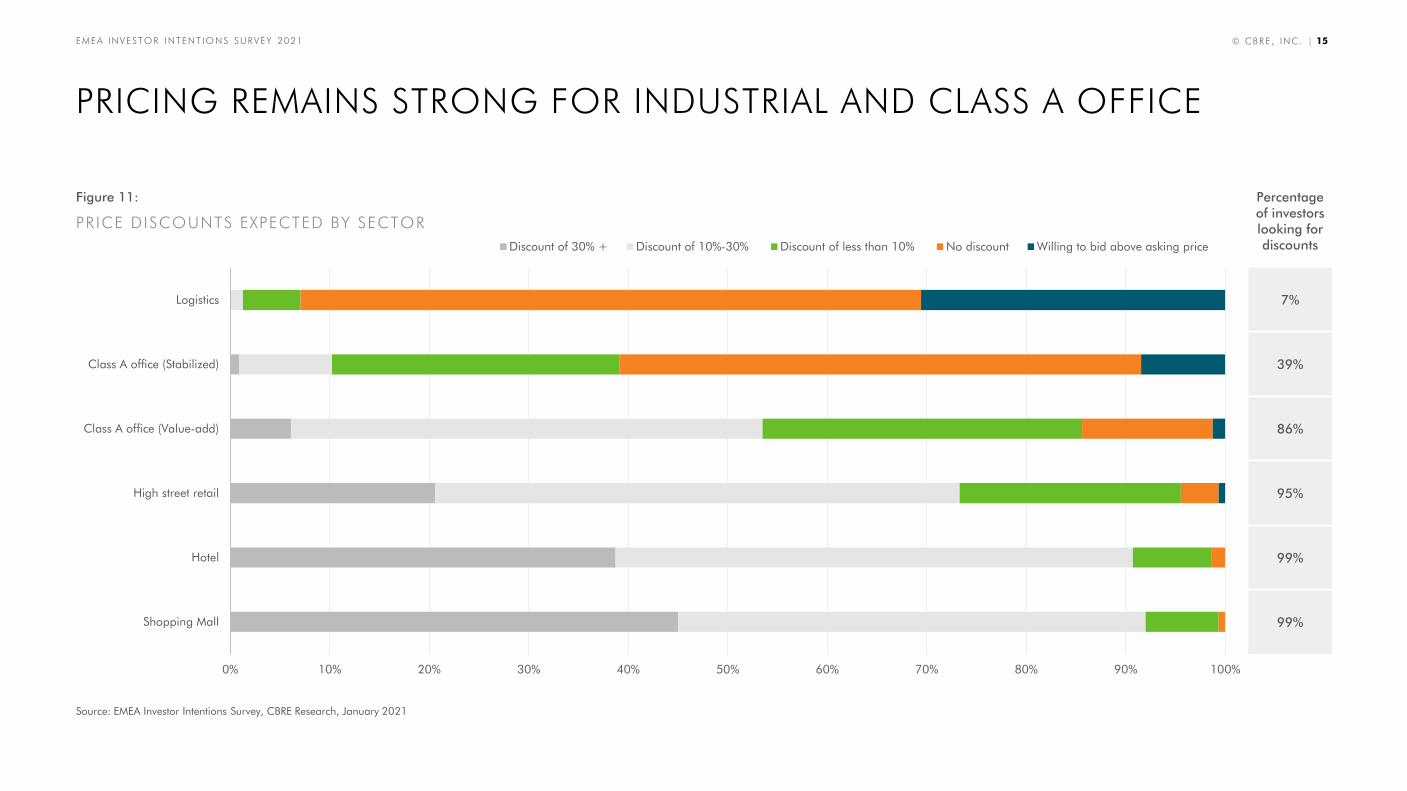

• Despite the implementation of flexible work patterns, offices remain the most preferred asset class, with logistics and multifamily also gaining popularity this year. Not surprisingly, these are the sectors where pricing is expected to remain strongest. Most investors generally expect sizable discounts for certain types of retail and hotels.

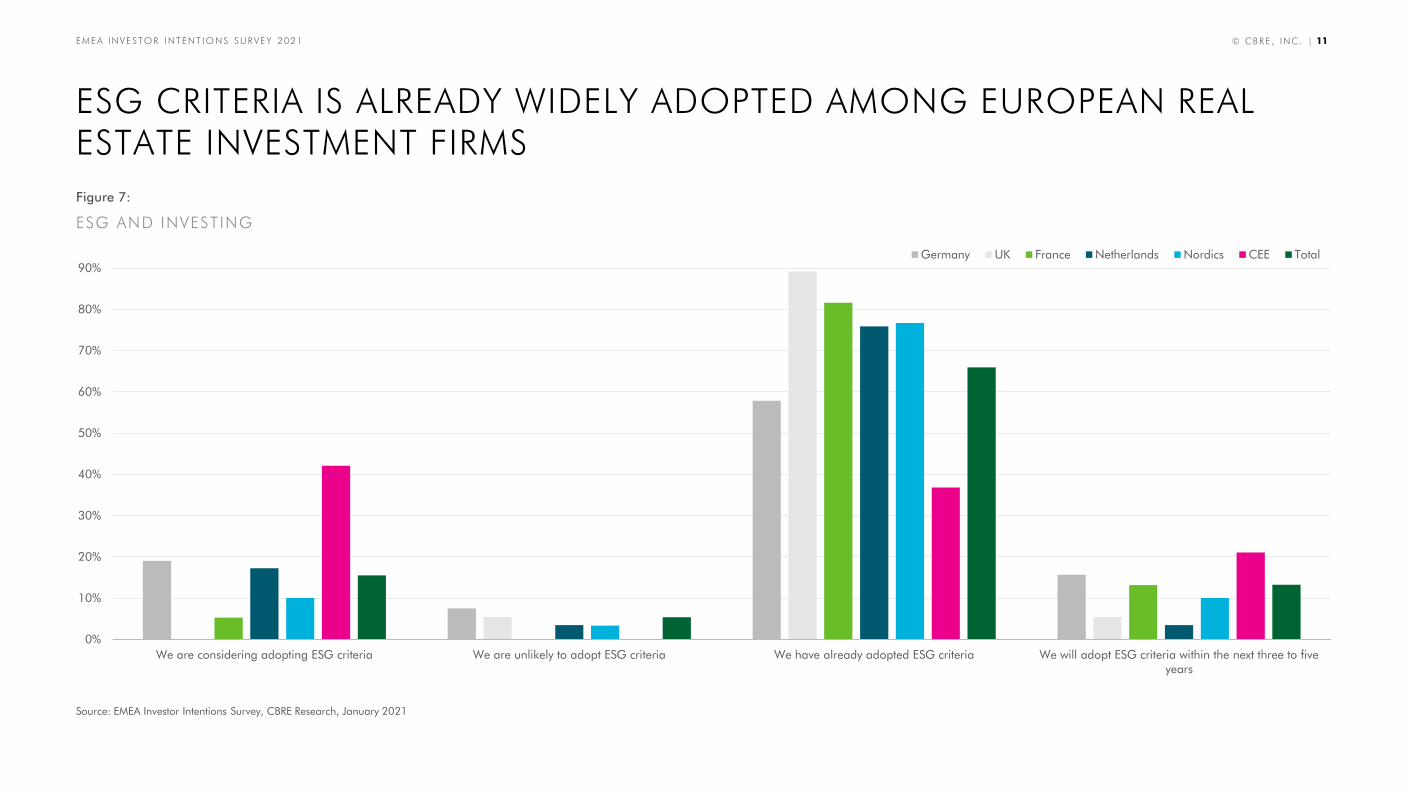

• Other key findings from this year’s survey included a stronger focus on rent growth, growing interest in long-term demographic and technological trends and the wider adoption of Environmental, Social and Governance (ESG) principles and practices.

OTHER KEY FINDINGS

• Investors remain cautious and favor core and core-plus developments.

• Office remains the most preferred property type for investment with elevated interest in logistics and multifamily properties.

Strategies and Sectors

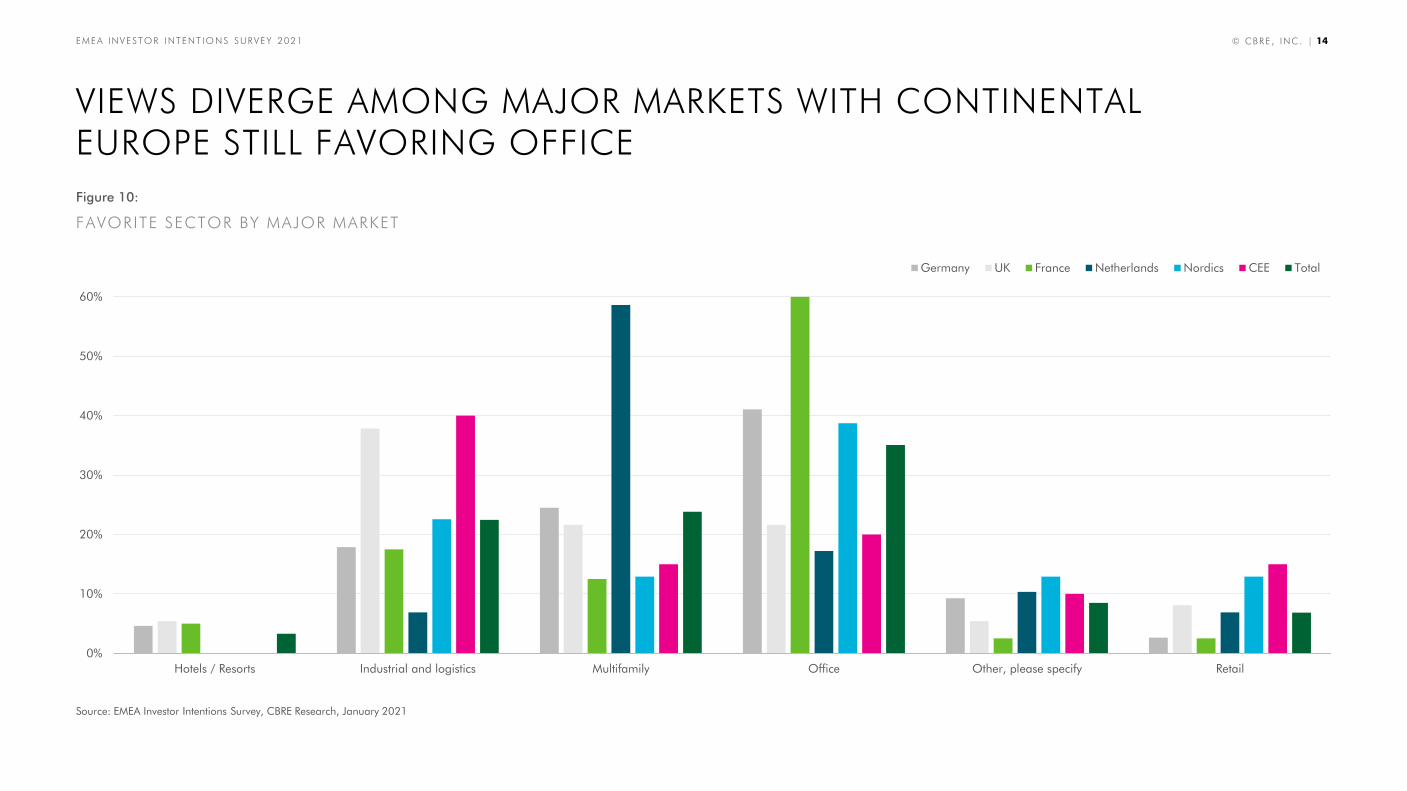

• Germany, The Netherlands, and France are expected to stage the fastest recoveries among major markets.

• London is the most preferred city for investment, with Berlin close behind.

Preferred Markets

• Pricing stable for Logistics and Class A Offices while nearly all investors looking for moderate to deep discounts in retail and hotel assets

• Owners are looking to emphasize tenant credit and ESG strategies.

Other Key Findings

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 3

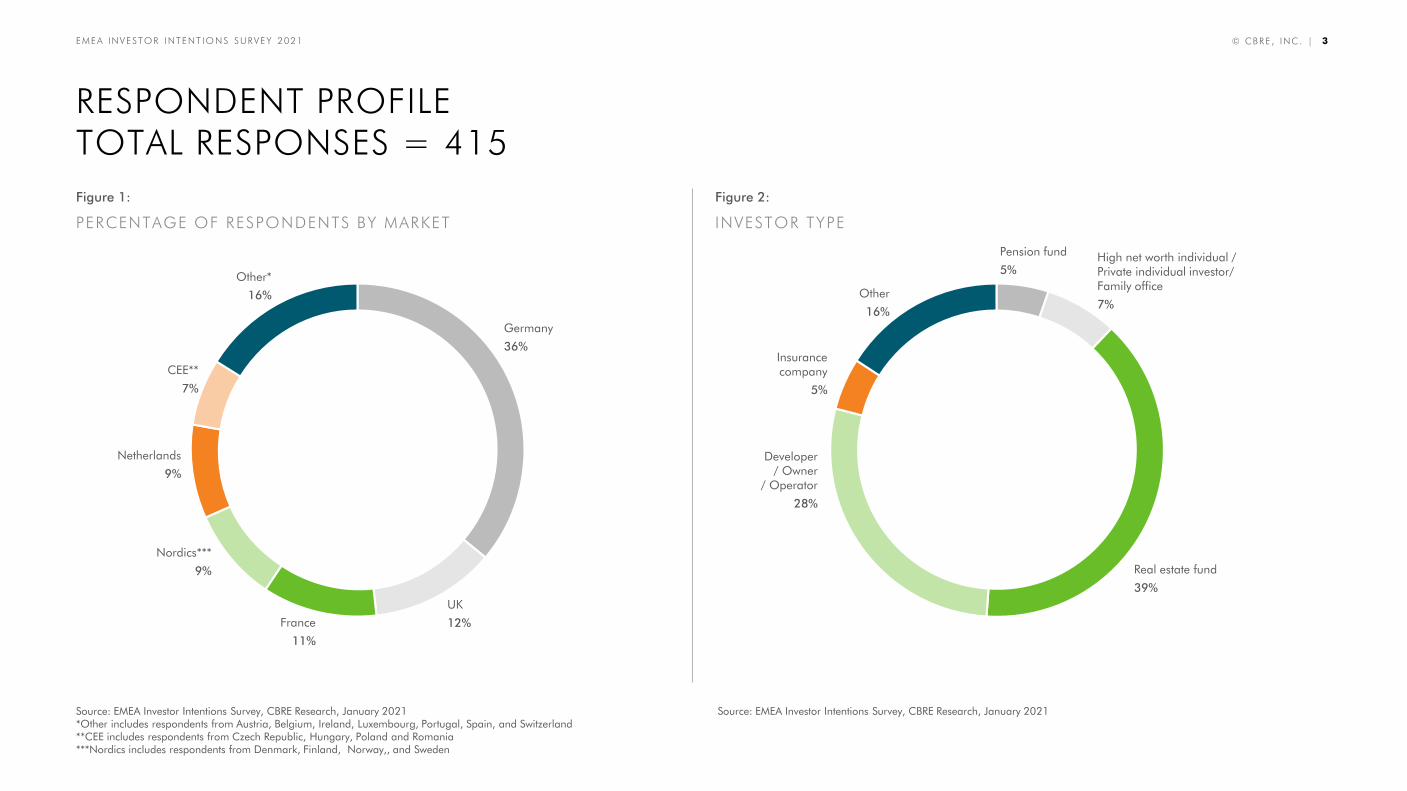

RESPONDENT PROFILETOTAL RESPONSES = 415

Figure 1:

PERCENTAGE OF RESPONDENTS BY MARKET

Figure 2:

INVESTOR TYPE

Germany

36%

UK

12%France

11%

Nordics***

9%

CEE**

7%

Pension fund

5%

Real estate fund

39%

Developer/ Owner

/ Operator

28%

Insurance company

5%

Other

16%

Netherlands

9%

Other*

16%

High net worth individual / Private individual investor/ Family office

7%

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021*Other includes respondents from Austria, Belgium, Ireland, Luxembourg, Portugal, Spain, and Switzerland**CEE includes respondents from Czech Republic, Hungary, Poland and Romania***Nordics includes respondents from Denmark, Finland, Norway,, and Sweden

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENTIONS SURVEY 2021

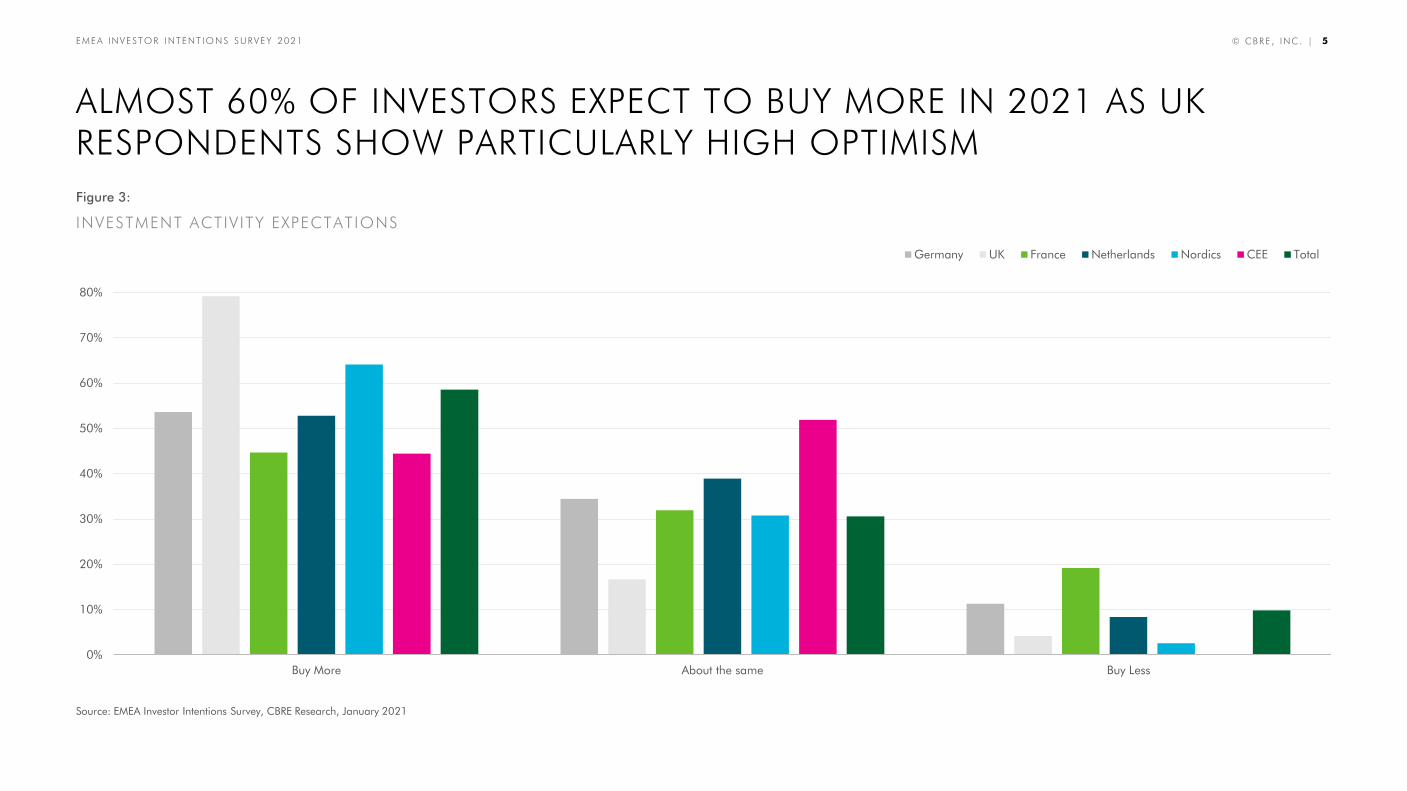

INVESTMENT ACTIVITY OUTLOOK

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 5

ALMOST 60% OF INVESTORS EXPECT TO BUY MORE IN 2021 AS UK RESPONDENTS SHOW PARTICULARLY HIGH OPTIMISM

Figure 3:

INVESTMENT ACTIV ITY EXPECTATIONS

0%

10%

20%

30%

40%

50%

60%

70%

80%

Buy More About the same Buy Less

Germany UK France Netherlands Nordics CEE Total

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 6

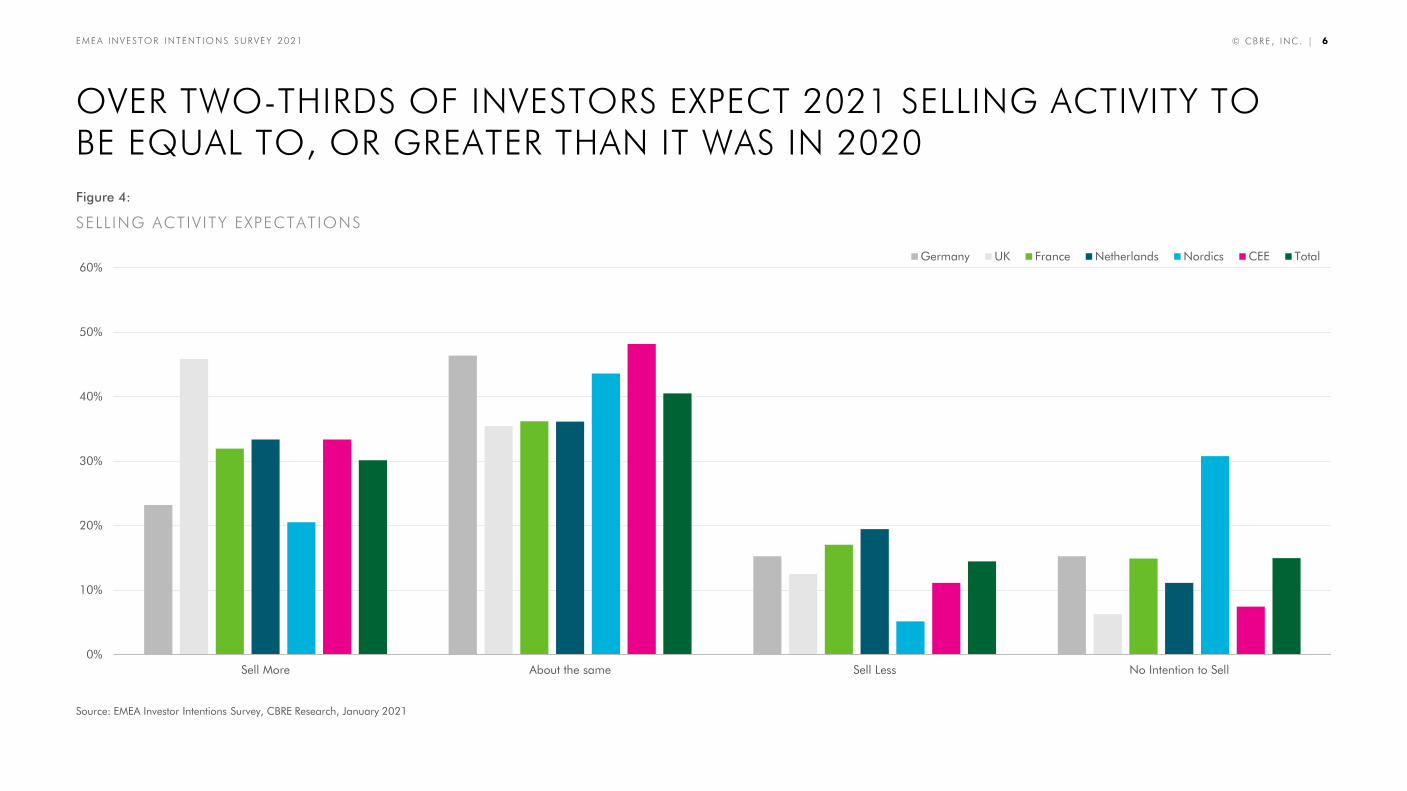

OVER TWO-THIRDS OF INVESTORS EXPECT 2021 SELLING ACTIVITY TO BE EQUAL TO, OR GREATER THAN IT WAS IN 2020

Figure 4:

SELL ING ACTIV ITY EXPECTATIONS

0%

10%

20%

30%

40%

50%

60%

Sell More About the same Sell Less No Intention to Sell

Germany UK France Netherlands Nordics CEE Total

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 7© CBRE , INC. | 7

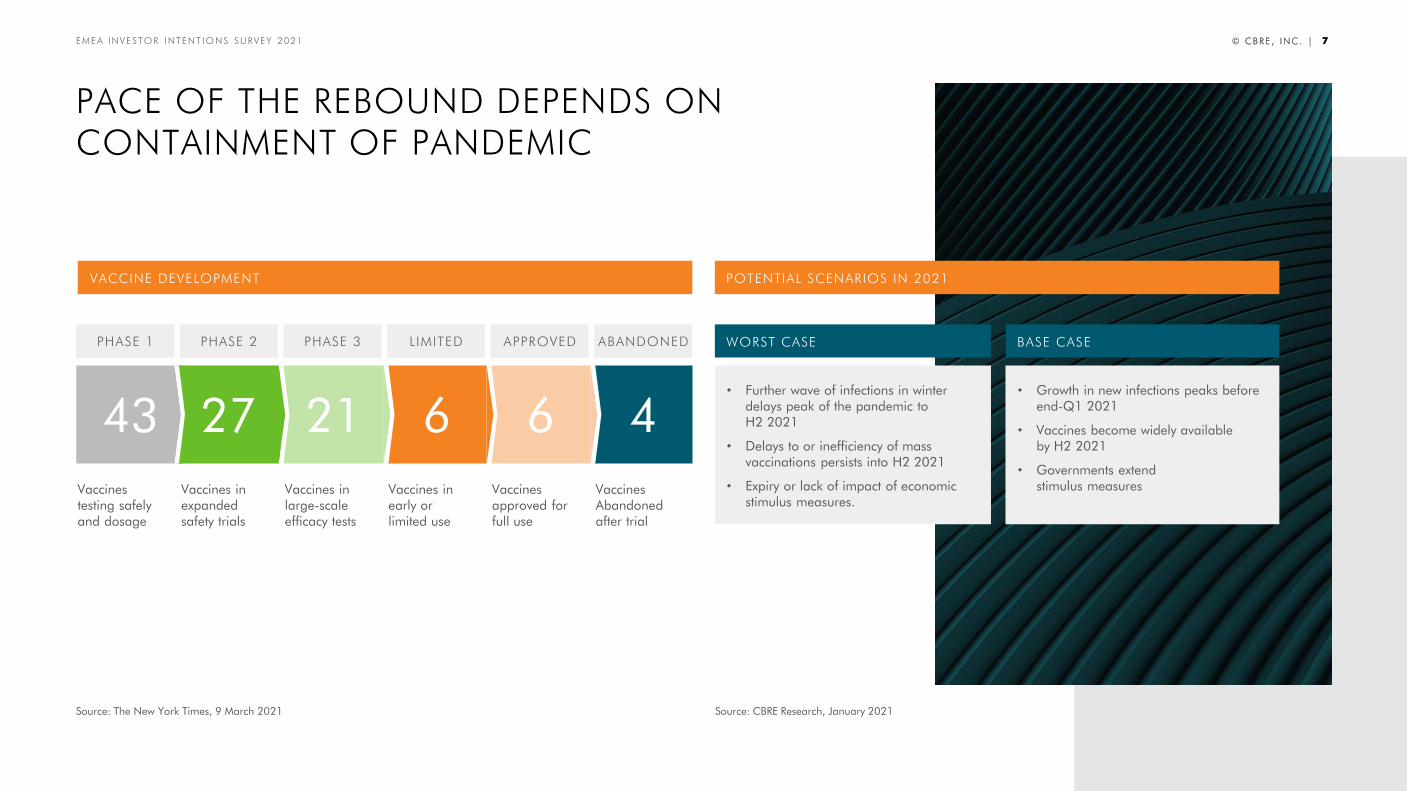

PACE OF THE REBOUND DEPENDS ON CONTAINMENT OF PANDEMIC

Source: The New York Times, 9 March 2021

PHASE 1

Vaccines testing safely and dosage

PHASE 2

Vaccines in expanded safety trials

PHASE 3

Vaccines in large-scale efficacy tests

LIMITED

Vaccines in early or limited use

APPROVED

Vaccines approved for full use

ABANDONED

Vaccines Abandoned after trial

43 27 21 6 6 4

POTENTIAL SCENARIOS IN 2021

WORST CASE BASE CASE

• Further wave of infections in winter delays peak of the pandemic to H2 2021

• Delays to or inefficiency of mass vaccinations persists into H2 2021

• Expiry or lack of impact of economic stimulus measures.

• Growth in new infections peaks before end-Q1 2021

• Vaccines become widely available by H2 2021

• Governments extend stimulus measures

VACCINE DEVELOPMENT

Source: CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 8

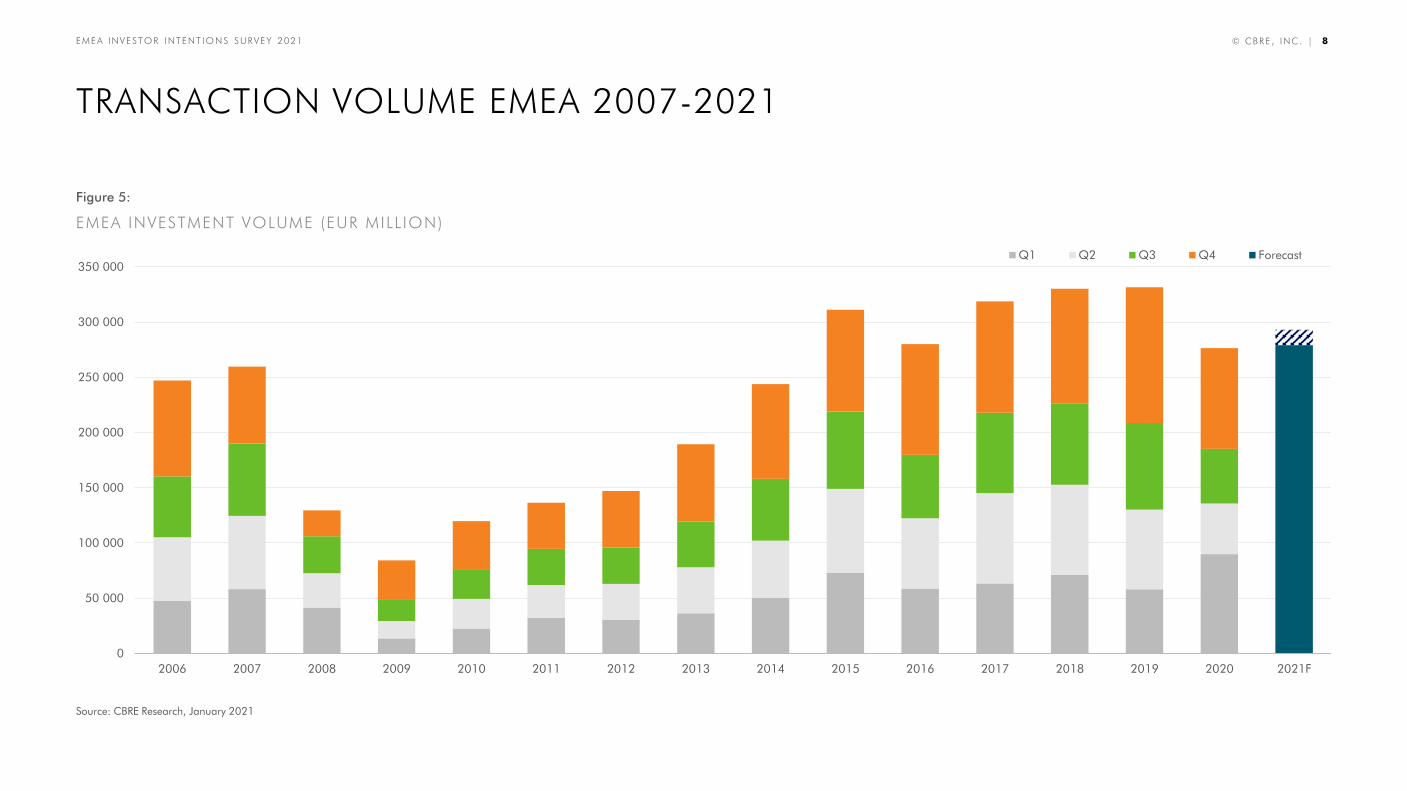

TRANSACTION VOLUME EMEA 2007-2021

Figure 5:

EMEA INVESTMENT VOLUME (EUR MILL ION)

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021F

Q1 Q2 Q3 Q4 Forecast

Source: CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 9EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 9

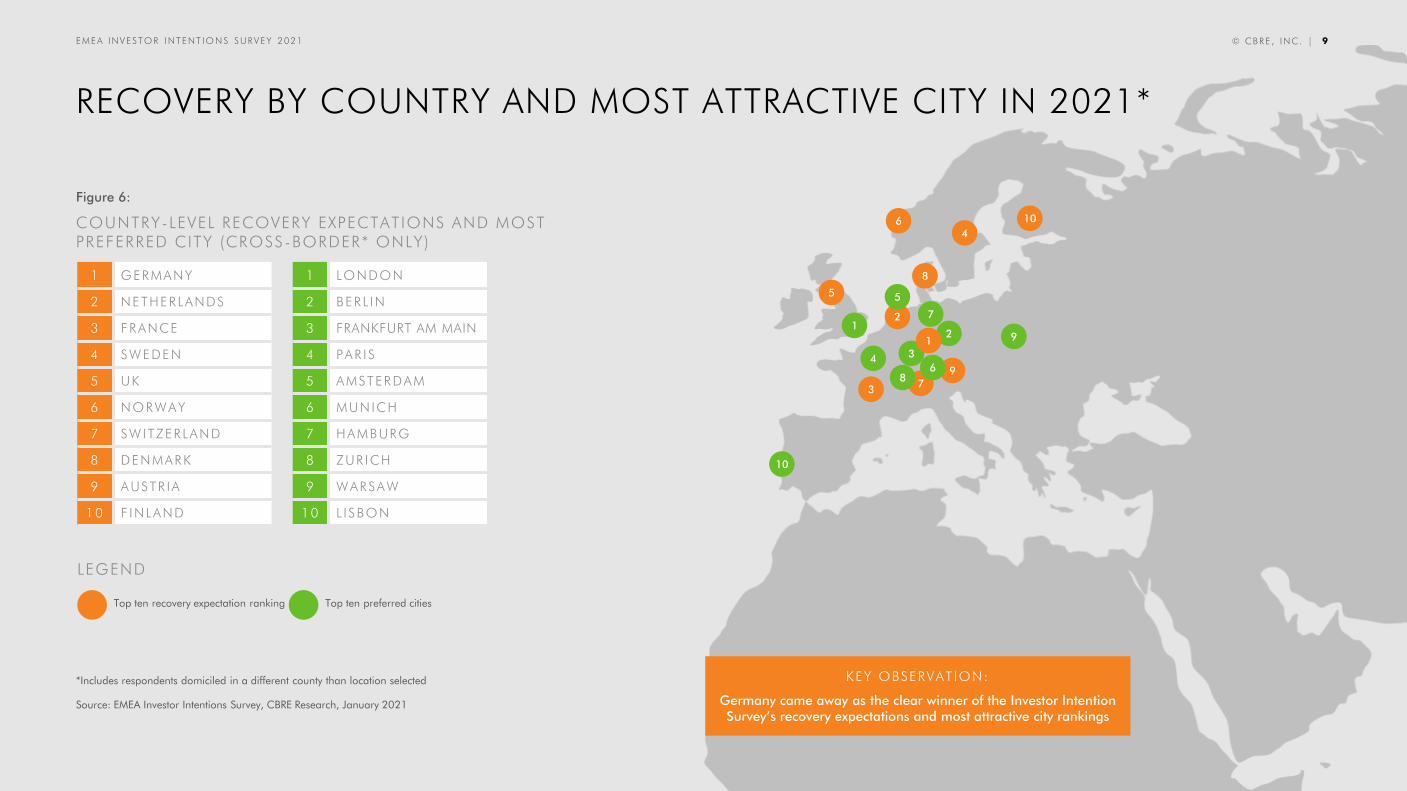

RECOVERY BY COUNTRY AND MOST ATTRACTIVE CITY IN 2021*

Figure 6:

COUNTRY-LEVEL RECOVERY EXPECTATIONS AND MOST PREFERRED CITY (CROSS-BORDER* ONLY)

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

*Includes respondents domiciled in a different county than location selected

LEGEND

Top ten recovery expectation ranking cou

1 GERMANY

2 NETHERLANDS

3 FRANCE

4 SWEDEN

5 UK

6 NORWAY

7 SWITZERLAND

8 DENMARK

9 AUSTR IA

10 F INLAND

1 LONDON

2 BERL IN

3 FRANKFURT AM MAIN

4 PAR IS

5 AMSTERDAM

6 MUNICH

7 HAMBURG

8 ZUR ICH

9 WARSAW

10 L ISBON

Top ten preferred cities

5

3

2

46

7

8

9

10

12

31

4

5

6

7

10

9

8

KEY OBSERVAT ION:

Germany came away as the clear winner of the Investor Intention Survey’s recovery expectations and most attractive city rankings

EMEA INVESTOR INTENTIONS SURVEY 2021

PANDEMIC-ERA INVESTING

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 11

ESG CRITERIA IS ALREADY WIDELY ADOPTED AMONG EUROPEAN REAL ESTATE INVESTMENT FIRMS

Figure 7:

ESG AND INVESTING

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

We are considering adopting ESG criteria We are unlikely to adopt ESG criteria We have already adopted ESG criteria We will adopt ESG criteria within the next three to fiveyears

Germany UK France Netherlands Nordics CEE Total

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 12

Core

Value-add

Core plus

Opportunistic

NPL and Distressed Assets

0% 5% 10% 15% 20% 25% 30% 35%

INVESTORS ADOPTING RISK-AVERSE STRATEGIES AS ECONOMIC RECOVERY BEGINS

Figure 8:

PREFERRED STRATEGY – ALL

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 13© CBRE , INC. | 13

DESPITE IMPACT OF FLEXIBLE WORK STRATEGIES OFFICE CONTINUES TO DOMINATE WHILE MULTIFAMILY CATCHES UPFigure 9:

SECTOR PREFERENCE

Multifamily

24%

Other (Please Specify)

8%

Retail

7%

Office

35%

Hotel

3%

Industrial and logistics

22%

PERCENTAGE OF OVERALL MENT IONS BY THOSE WHO SELECTED OTHER AND SPECIF IED :

0% 10% 20% 30% 40% 50%

Other

Healthcare

Alternative Residential

KEY OBSERVAT ION:

Multifamily’s overall percentage may actually be closer to 30% given discrepancies in naming

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 14

VIEWS DIVERGE AMONG MAJOR MARKETS WITH CONTINENTAL EUROPE STILL FAVORING OFFICE

Figure 10:

FAVORITE SECTOR BY MAJOR MARKET

0%

10%

20%

30%

40%

50%

60%

Hotels / Resorts Industrial and logistics Multifamily Office Other, please specify Retail

Germany UK France Netherlands Nordics CEE Total

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 15

PRICING REMAINS STRONG FOR INDUSTRIAL AND CLASS A OFFICE

Figure 11:

PRICE DISCOUNTS EXPECTED BY SECTOR

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Shopping Mall

Hotel

High street retail

Class A office (Value-add)

Class A office (Stabilized)

Logistics

Discount of 30% + Discount of 10%-30% Discount of less than 10% No discount Willing to bid above asking price

Percentage of investors looking for discounts

7%

39%

86%

95%

99%

99%

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 16

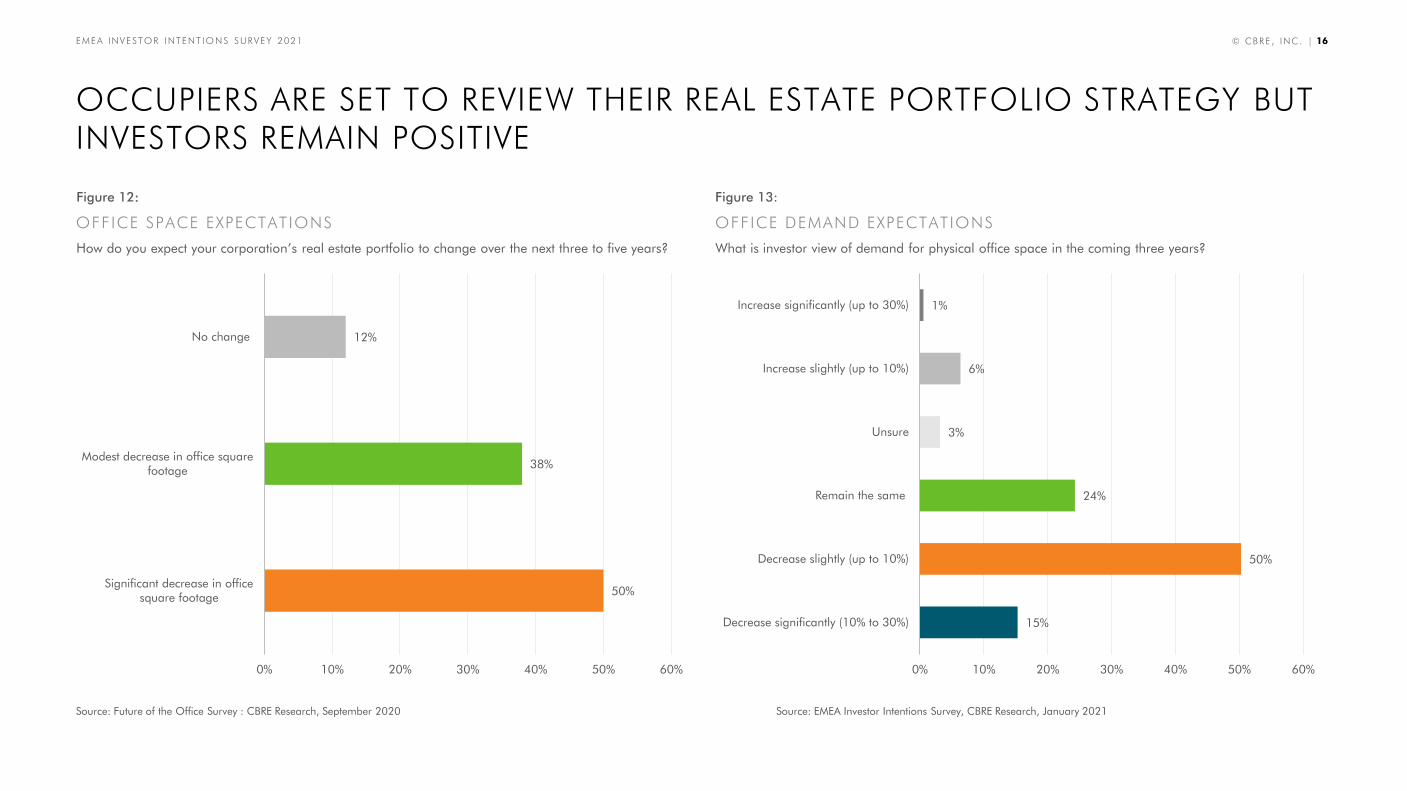

OCCUPIERS ARE SET TO REVIEW THEIR REAL ESTATE PORTFOLIO STRATEGY BUT INVESTORS REMAIN POSITIVE

Figure 12:

OFFICE SPACE EXPECTATIONS

How do you expect your corporation’s real estate portfolio to change over the next three to five years?

Figure 13:

OFFICE DEMAND EXPECTATIONS

What is investor view of demand for physical office space in the coming three years?

15%

50%

24%

3%

6%

1%

0% 10% 20% 30% 40% 50% 60%

Decrease significantly (10% to 30%)

Decrease slightly (up to 10%)

Remain the same

Unsure

Increase slightly (up to 10%)

Increase significantly (up to 30%)

50%

38%

12%

0% 10% 20% 30% 40% 50% 60%

Significant decrease in officesquare footage

Modest decrease in office squarefootage

No change

Source: Future of the Office Survey : CBRE Research, September 2020 Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 17

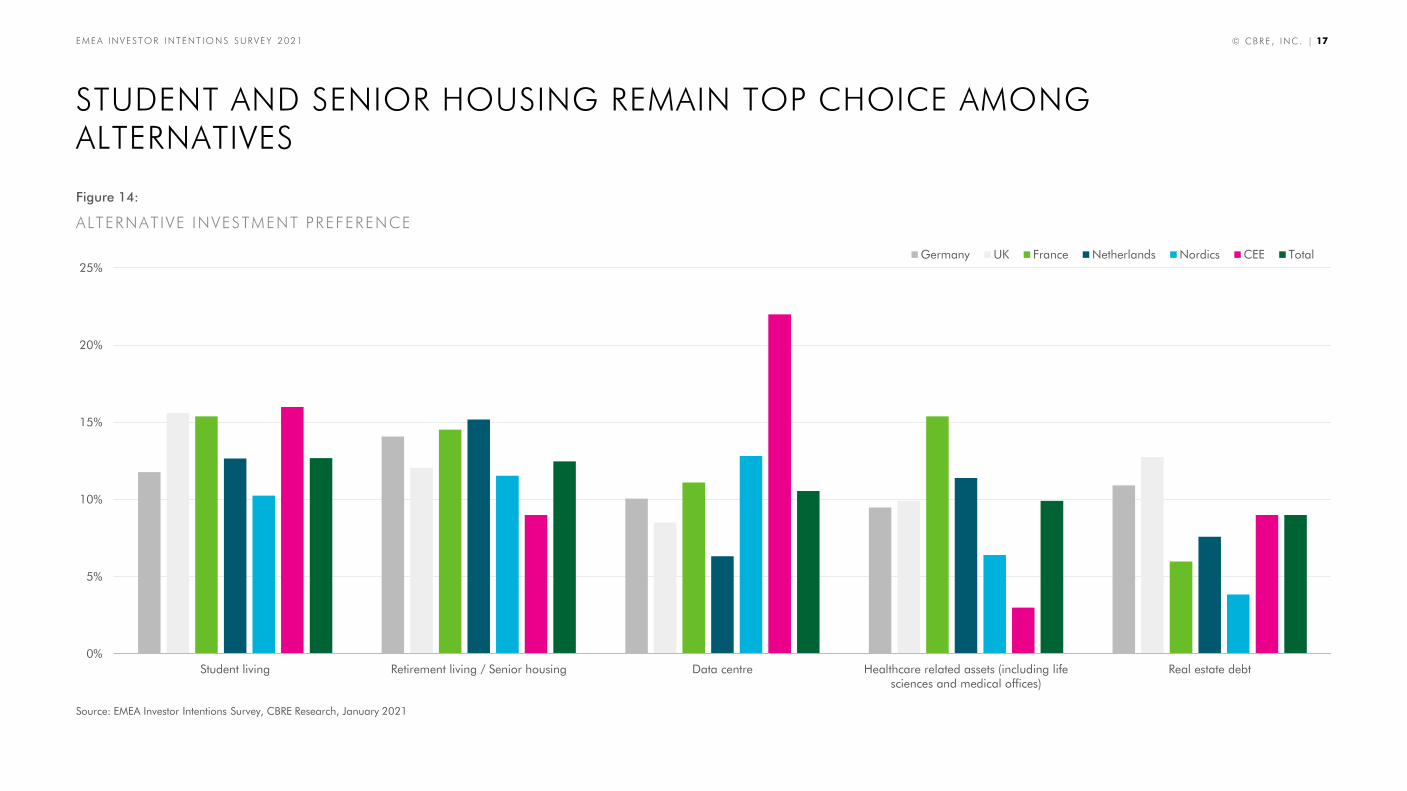

STUDENT AND SENIOR HOUSING REMAIN TOP CHOICE AMONG ALTERNATIVES

Figure 14:

ALTERNATIVE INVESTMENT PREFERENCE

0%

5%

10%

15%

20%

25%

Student living Retirement living / Senior housing Data centre Healthcare related assets (including lifesciences and medical offices)

Real estate debt

Germany UK France Netherlands Nordics CEE Total

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 18

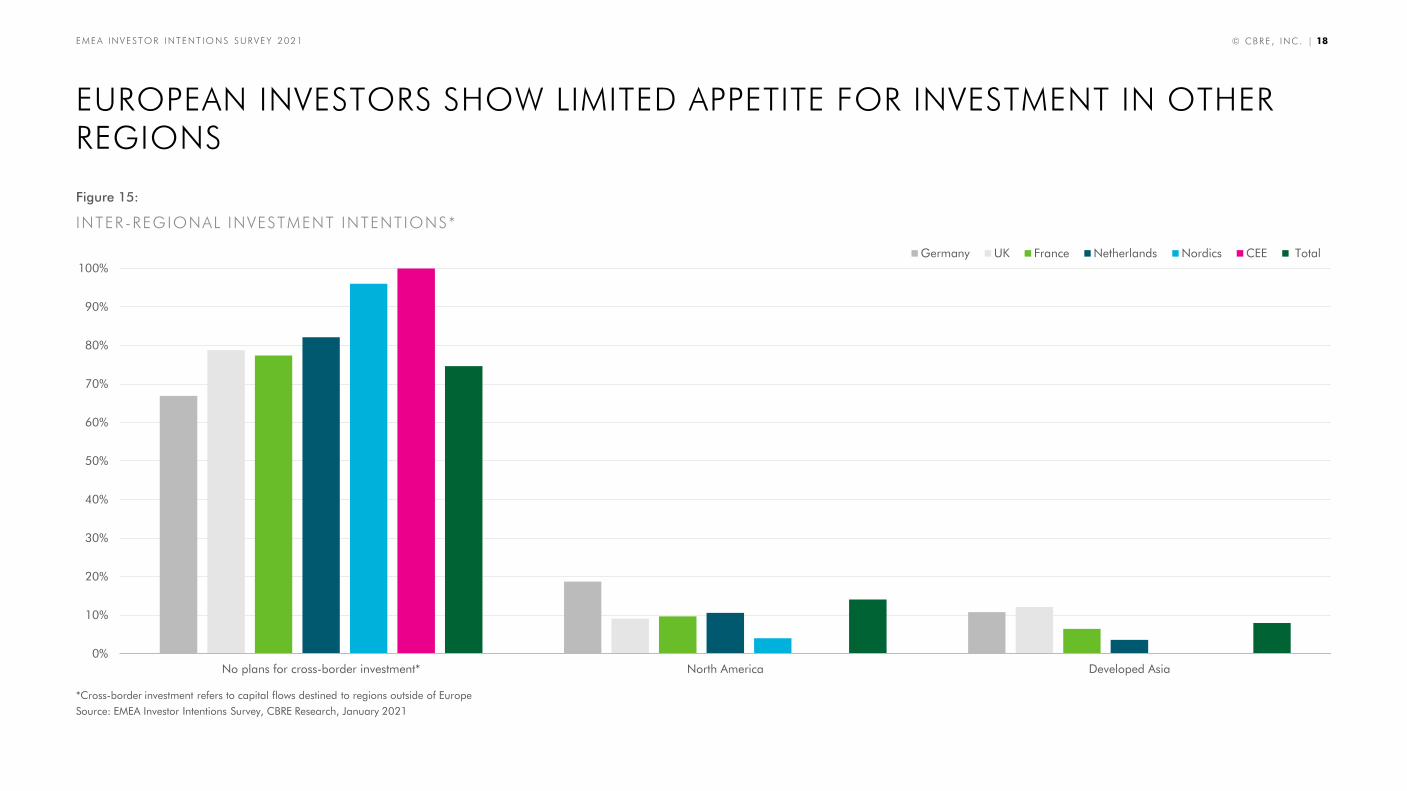

EUROPEAN INVESTORS SHOW LIMITED APPETITE FOR INVESTMENT IN OTHERREGIONS

Figure 15:

INTER-REGIONAL INVESTMENT INTENTIONS*

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No plans for cross-border investment* North America Developed Asia

Germany UK France Netherlands Nordics CEE Total

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

*Cross-border investment refers to capital flows destined to regions outside of Europe

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 19

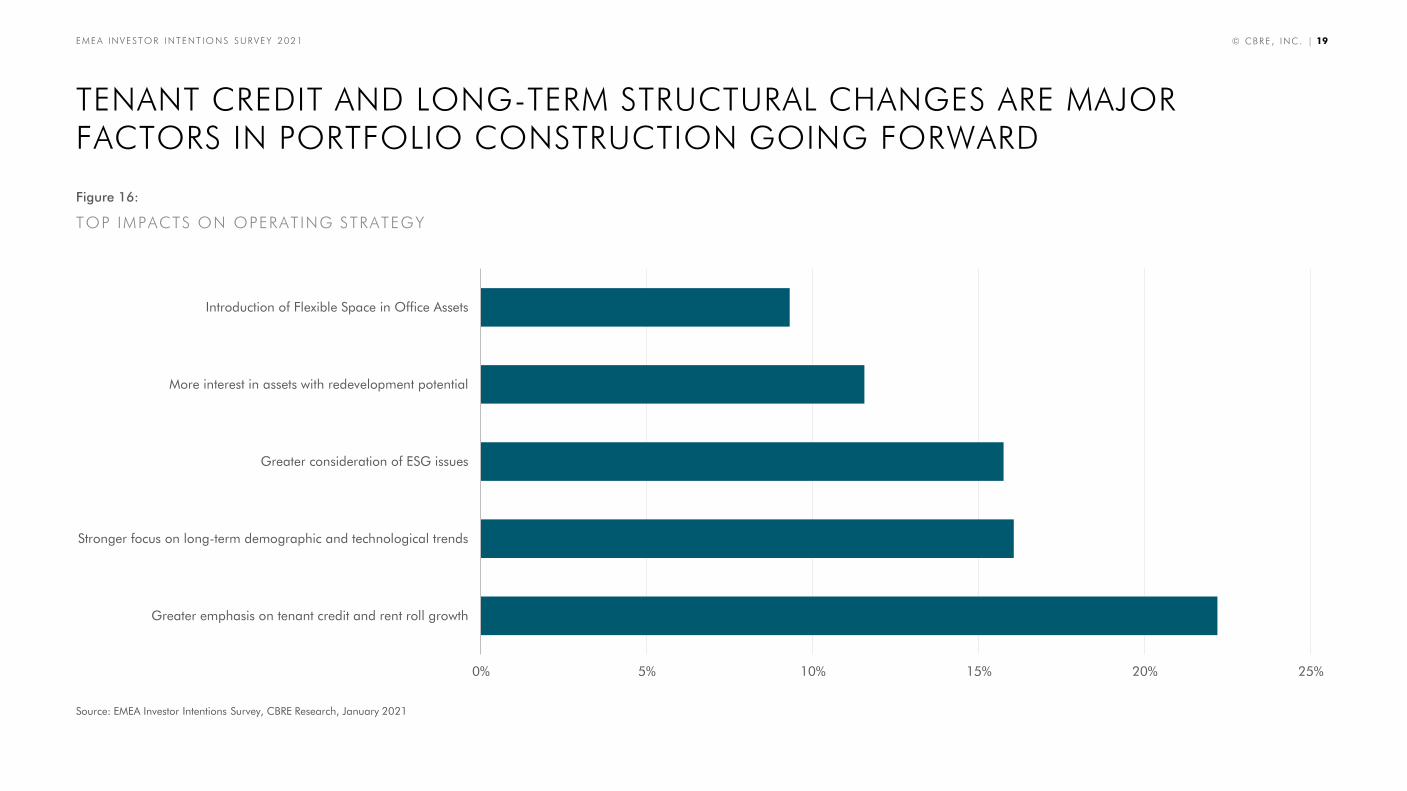

TENANT CREDIT AND LONG-TERM STRUCTURAL CHANGES ARE MAJOR FACTORS IN PORTFOLIO CONSTRUCTION GOING FORWARD

Figure 16:

TOP IMPACTS ON OPERATING STRATEGY

0% 5% 10% 15% 20% 25%

Greater emphasis on tenant credit and rent roll growth

Stronger focus on long-term demographic and technological trends

Greater consideration of ESG issues

More interest in assets with redevelopment potential

Introduction of Flexible Space in Office Assets

Source: EMEA Investor Intentions Survey, CBRE Research, January 2021

EMEA INVESTOR INTENTIONS SURVEY 2021

THANK YOU

EMEA INVESTOR INTENT IO N S SURVEY 2021 © CBRE , INC. | 21

CBRE RESEARCH

This report was prepared by the CBRE Global Investor Research Team, which forms part of CBRE Research—a network of preeminent researchers who collaborate to provide real estate market research and econometric forecasting to real estate.

All materials presented in this report, unless specifically indicated otherwise, is under copyright and proprietary to CBRE. Information contained herein, including projections, has been obtained from materials and sources believed to be reliable at the date of publication. While we do not doubt its

accuracy, we have not verified it and make no guarantee, warranty or representation about it. Readers are responsible for independently assessing the relevance, accuracy, completeness and currency of the information of this publication. This report is presented for information purposes only

exclusively for CBRE clients and professionals, and is not to be used or considered as an offer or the solicitation of an offer to sell or buy or subscribe for securities or other financial instruments. All rights to the material are reserved and none of the material, nor its content, nor any copy of it, may be

altered in any way, transmitted to, copied or distributed to any other party without prior express written permission of CBRE. Any unauthorized publication or redistribution of CBRE research reports is prohibited. CBRE will not be liable for any loss, damage, cost or expense incurred or arising by reason

of any person using or relying on information in this publication.

To learn more about CBRE Research, or to access additional research reports, please visit the Global Research Gateway at reports www.cbre.com/research-and-reports

© 2021 CBRE, Inc

I N V E S T O R I N T E N T I O N S S U R V E Y 2 0 2 1

FOR MORE INFORMATION ABOUT THIS REGIONAL REPORT PLEASE CONTACT:

Henry Chin, Ph.D.

Head of Research, Asia Pacific &Global Head of Investor Thought Leadership

Benjamin Pipernos

Research AnalystGlobal Investor Thought Leadership – Capital Markets

Darin Mellott

Director of ResearchGlobal Investor Thought Leadership

Chris Brett

Head of Capital Markets EMEA

Jos Tromp

Head of Research Continental Europe &Head of Data Strategy and Thought Leadership EMEA

Richard Barkham, Ph.D.

Global Head of Research &Global Chief Economist