Embed Size (px)

Citation preview

Dealing with Duplicates

Ellen Heffner, NCP Phyllis Meyerson, AAP, CCM

ECCHO Electronic Check Clearing House Org

September 25, 2013

2 Copyright 2013, RemoteDepositCapture.com

Disclaimer This session provides an overview of various aspects of the check payments systems including legal and rules framework for check image exchange. Responsibility for compliance with image exchange rules and/or legal, operational and regulatory requirements applicable to check image exchange remains at all times with the financial institution participating in check image exchange and/or the individual or company using a check image exchange service. This presentation and the information contained herein is not intended as legal or compliance advice or recommendation to any person or company.

This document could include technical inaccuracies or typographical errors and individual users are responsible for verifying any information found in this presentation.

Financial institutions should consult with their legal counsel regarding legal and operational requirements applicable to any check image exchange program they may offer or in which they participate.

Topical Agenda • ECCHO – Who We Are • Background • Legal Considerations

– Rules and Warranties – Holder in Due Course

• Operational Considerations – Importance of Prevention and Detection – Returning vs. Adjusting Duplicates – Intermediary Duplicates – Represented Item & Duplicates

• Scenarios 3 Copyright 2013, RemoteDepositCapture.com

Who is ECCHO? • Electronic Check Clearing House Org

– Not-for-profit, created in 1990 – Owned by its membership

• Current membership – over 3,000 – Every depository financial institution is eligible for membership

• Only DFIs are eligible for membership – Only national private sector Image Rules Organization – All ECCHO members have equal coverage under rules – Vendor and Solution Independent

• Rules designed to work with all solutions – ECCHO Rules apply to Check Image Exchanges between

ECCHO Members – Three primary functions – Rules, Advocacy and Education

4 Copyright 2013, RemoteDepositCapture.com

Duplicate • Webster’s New Collegiate Dictionary – Copyright

1977 • Duplicate

– Consisting of or existing in two corresponding or identical parts or examples

– Being the same as another – Either of two things that exactly resemble or

correspond to each other – Two copies both alike – To make an exact copy of

5 Copyright 2013, RemoteDepositCapture.com

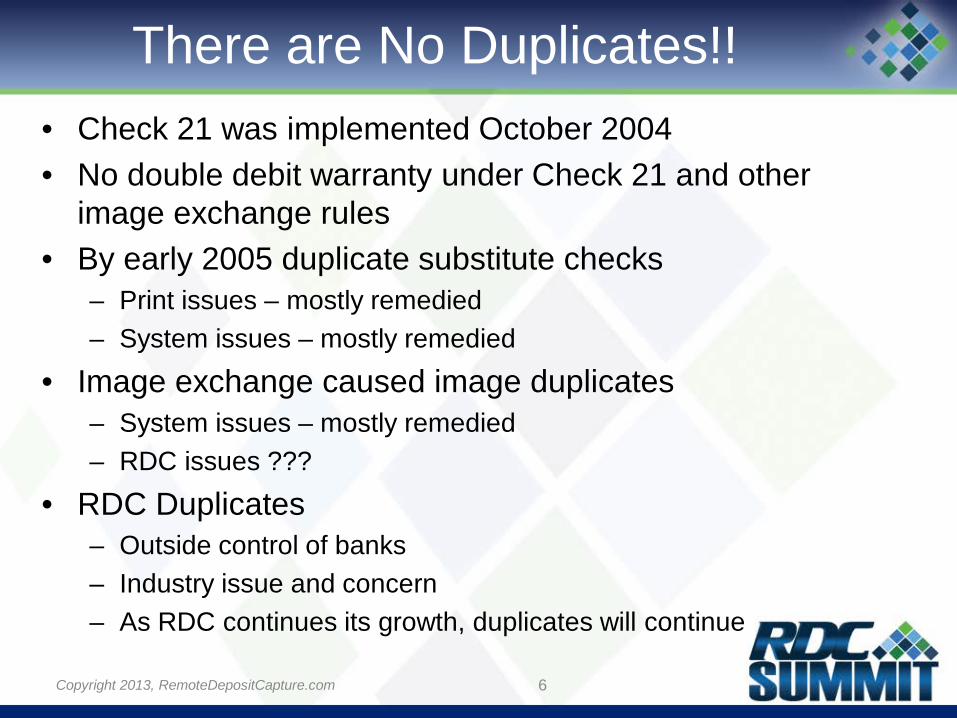

There are No Duplicates!! • Check 21 was implemented October 2004 • No double debit warranty under Check 21 and other

image exchange rules • By early 2005 duplicate substitute checks

– Print issues – mostly remedied – System issues – mostly remedied

• Image exchange caused image duplicates – System issues – mostly remedied – RDC issues ???

• RDC Duplicates – Outside control of banks – Industry issue and concern – As RDC continues its growth, duplicates will continue

6 Copyright 2013, RemoteDepositCapture.com

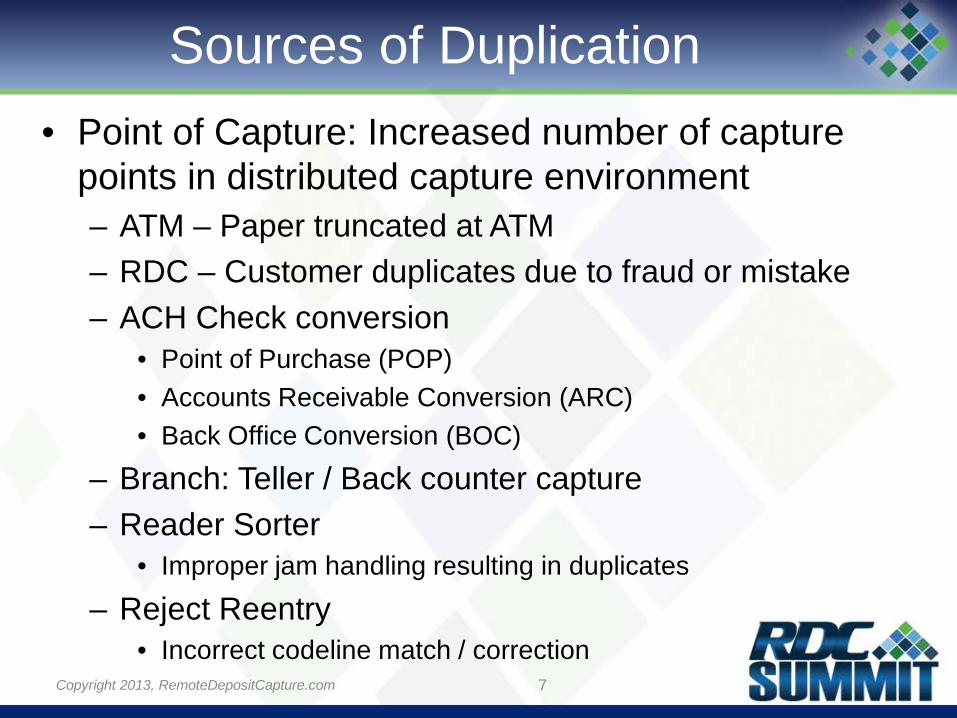

Sources of Duplication • Point of Capture: Increased number of capture

points in distributed capture environment – ATM – Paper truncated at ATM – RDC – Customer duplicates due to fraud or mistake – ACH Check conversion

• Point of Purchase (POP) • Accounts Receivable Conversion (ARC) • Back Office Conversion (BOC)

– Branch: Teller / Back counter capture – Reader Sorter

• Improper jam handling resulting in duplicates

– Reject Reentry • Incorrect codeline match / correction

7 Copyright 2013, RemoteDepositCapture.com

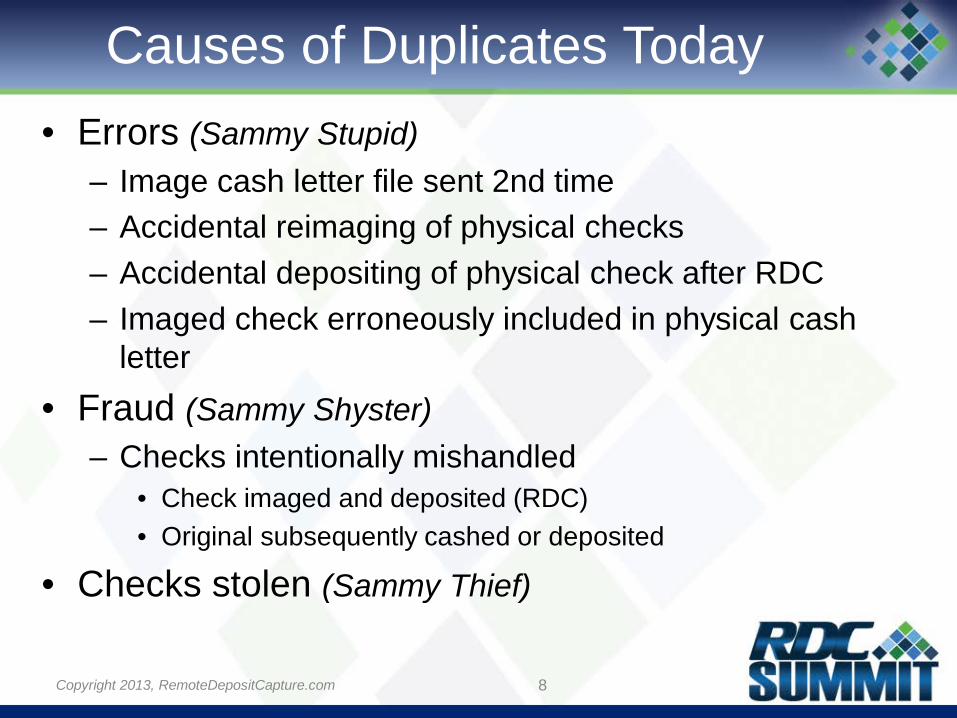

Causes of Duplicates Today • Errors (Sammy Stupid)

– Image cash letter file sent 2nd time – Accidental reimaging of physical checks – Accidental depositing of physical check after RDC – Imaged check erroneously included in physical cash

letter • Fraud (Sammy Shyster)

– Checks intentionally mishandled • Check imaged and deposited (RDC) • Original subsequently cashed or deposited

• Checks stolen (Sammy Thief)

8 Copyright 2013, RemoteDepositCapture.com

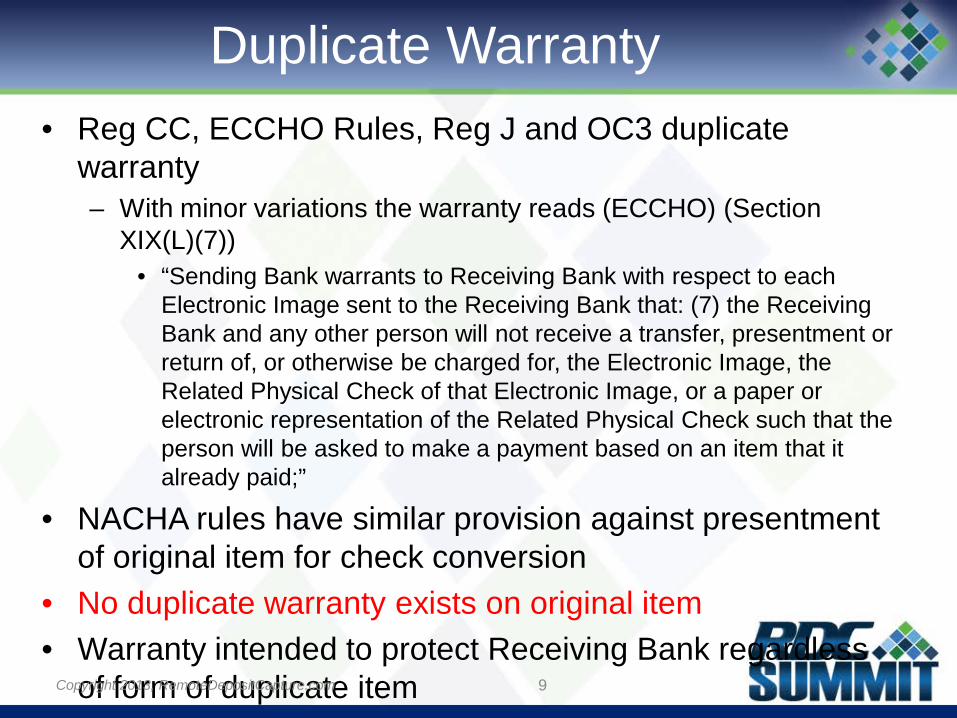

Duplicate Warranty • Reg CC, ECCHO Rules, Reg J and OC3 duplicate

warranty – With minor variations the warranty reads (ECCHO) (Section

XIX(L)(7)) • “Sending Bank warrants to Receiving Bank with respect to each

Electronic Image sent to the Receiving Bank that: (7) the Receiving Bank and any other person will not receive a transfer, presentment or return of, or otherwise be charged for, the Electronic Image, the Related Physical Check of that Electronic Image, or a paper or electronic representation of the Related Physical Check such that the person will be asked to make a payment based on an item that it already paid;”

• NACHA rules have similar provision against presentment of original item for check conversion

• No duplicate warranty exists on original item • Warranty intended to protect Receiving Bank regardless

of form of duplicate item

9 Copyright 2013, RemoteDepositCapture.com

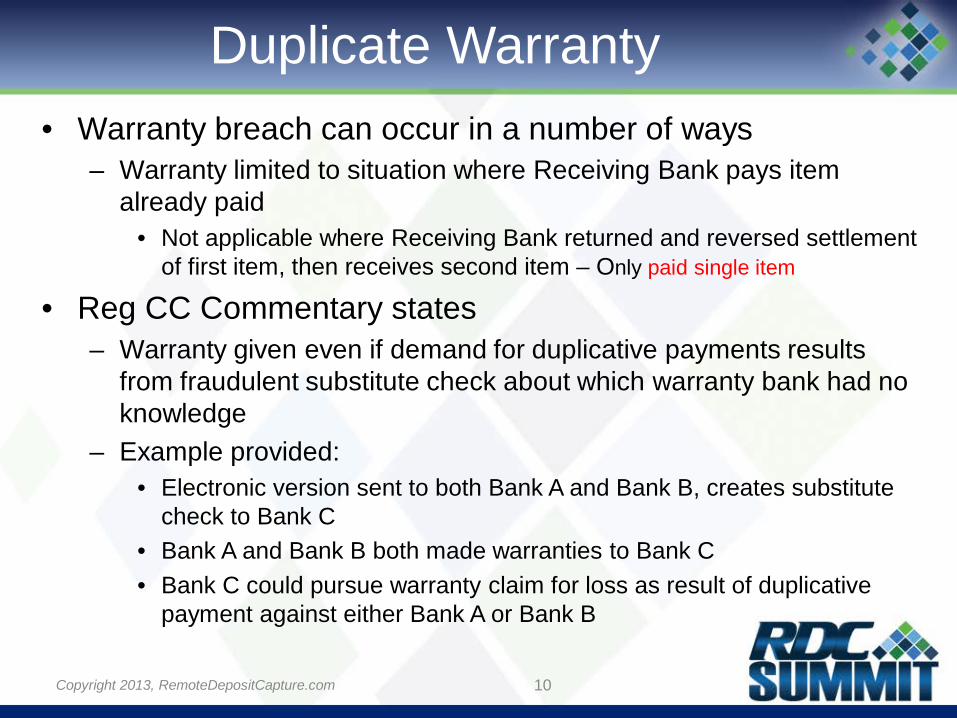

Duplicate Warranty • Warranty breach can occur in a number of ways

– Warranty limited to situation where Receiving Bank pays item already paid

• Not applicable where Receiving Bank returned and reversed settlement of first item, then receives second item – Only paid single item

• Reg CC Commentary states – Warranty given even if demand for duplicative payments results

from fraudulent substitute check about which warranty bank had no knowledge

– Example provided: • Electronic version sent to both Bank A and Bank B, creates substitute

check to Bank C • Bank A and Bank B both made warranties to Bank C • Bank C could pursue warranty claim for loss as result of duplicative

payment against either Bank A or Bank B

10 Copyright 2013, RemoteDepositCapture.com

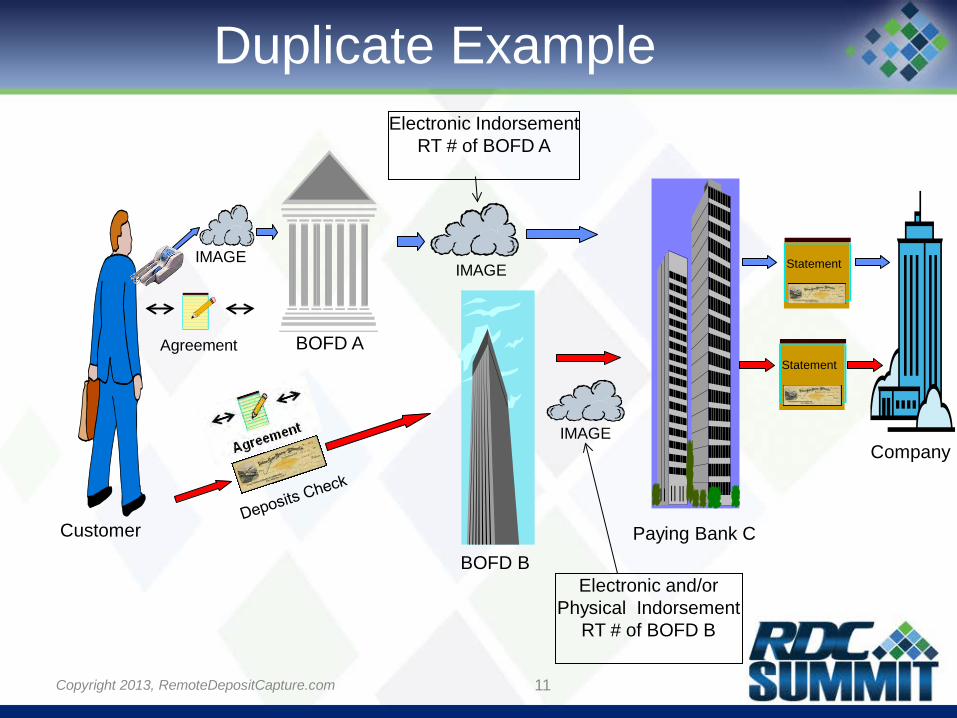

IMAGE

BOFD A

Paying Bank C

Agreement

Customer

Company

Statement IMAGE

Electronic Indorsement RT # of BOFD A

Statement

BOFD B

IMAGE

Electronic and/or Physical Indorsement

RT # of BOFD B

Duplicate Example

11 Copyright 2013, RemoteDepositCapture.com

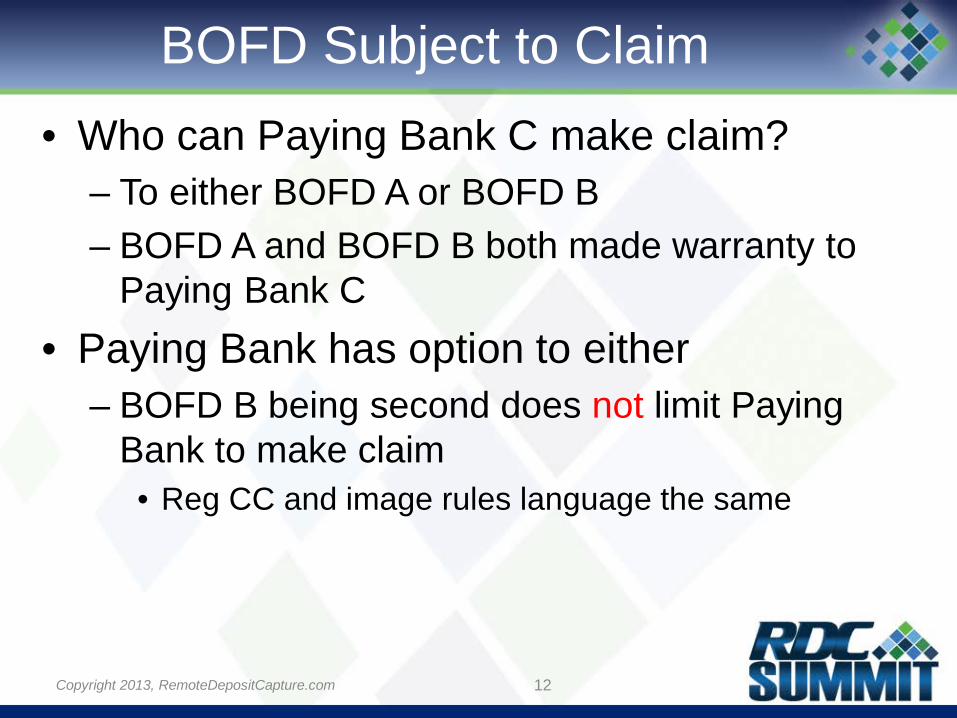

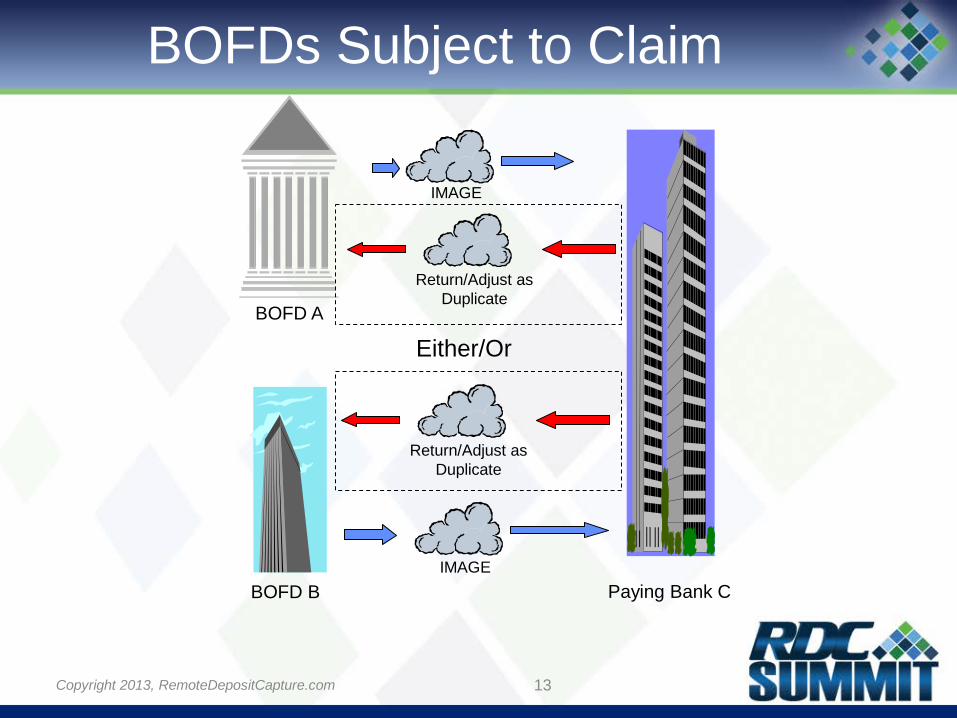

BOFD Subject to Claim • Who can Paying Bank C make claim?

– To either BOFD A or BOFD B – BOFD A and BOFD B both made warranty to

Paying Bank C • Paying Bank has option to either

– BOFD B being second does not limit Paying Bank to make claim

• Reg CC and image rules language the same

12 Copyright 2013, RemoteDepositCapture.com

BOFD A

Paying Bank C BOFD B

IMAGE

Return/Adjust as Duplicate

IMAGE

BOFDs Subject to Claim

13

Return/Adjust as Duplicate

Either/Or

Copyright 2013, RemoteDepositCapture.com

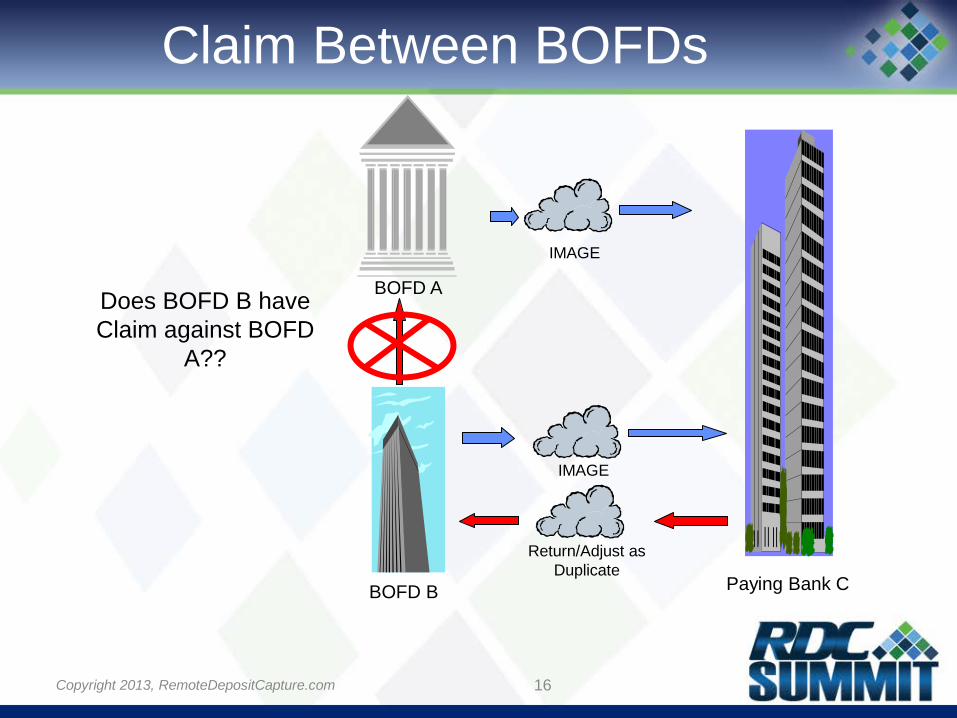

Claim Between BOFDs • Is there basis for claim between BOFDs? • Rules and check law do not address claims

between BOFDs – No exchange between BOFDs, no warranty made – Warranties arise from exchange of check images

• Reg CC does not address this for substitute checks

– Unknown if there is basis for loss sharing under other law

• Consult legal counsel • Discuss with 2nd BOFD to reduce or share loss

• Holder in Due Course issue – How is duplicate claim effected when one party has

original check?

14 Copyright 2013, RemoteDepositCapture.com

Claim Between BOFDs • BOFD A and its customer have agreement,

usually requiring customer to secure original paper check – That agreement is contract law between BOFD A and

its customer • No other party is subject to that agreement

• Nothing in any rule set regarding not “securing original paper” – For reason of BOFD B to reject claim – For reason of BOFD B to make claim to BOFD A

15 Copyright 2013, RemoteDepositCapture.com

BOFD A

Paying Bank C BOFD B

IMAGE

Return/Adjust as Duplicate

IMAGE

Does BOFD B have Claim against BOFD

A??

Claim Between BOFDs

16 Copyright 2013, RemoteDepositCapture.com

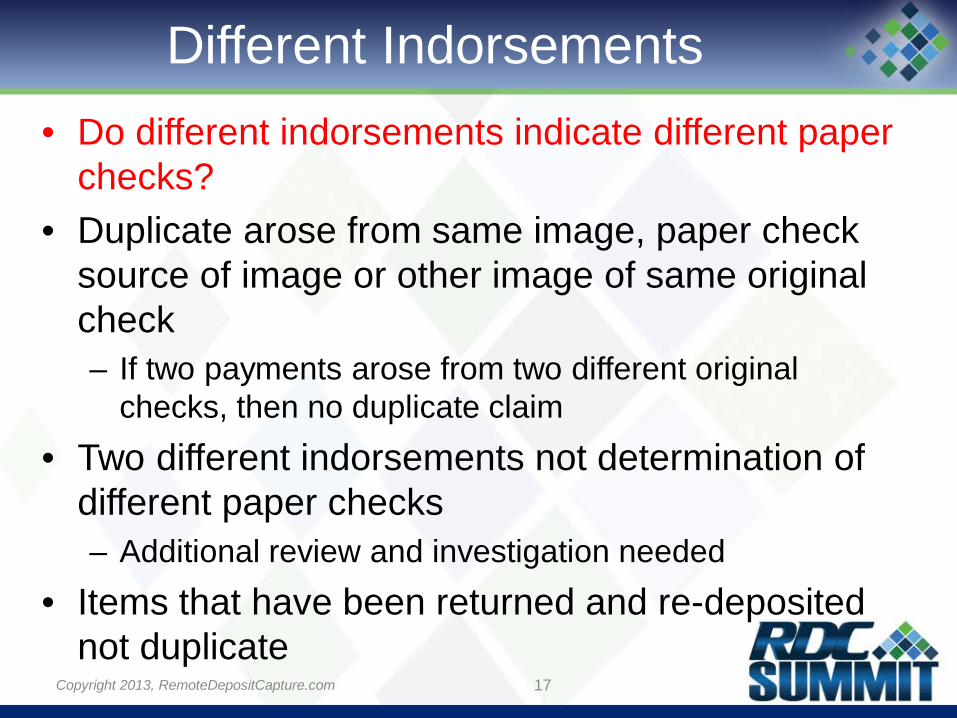

Different Indorsements • Do different indorsements indicate different paper

checks? • Duplicate arose from same image, paper check

source of image or other image of same original check – If two payments arose from two different original

checks, then no duplicate claim • Two different indorsements not determination of

different paper checks – Additional review and investigation needed

• Items that have been returned and re-deposited not duplicate

17 Copyright 2013, RemoteDepositCapture.com

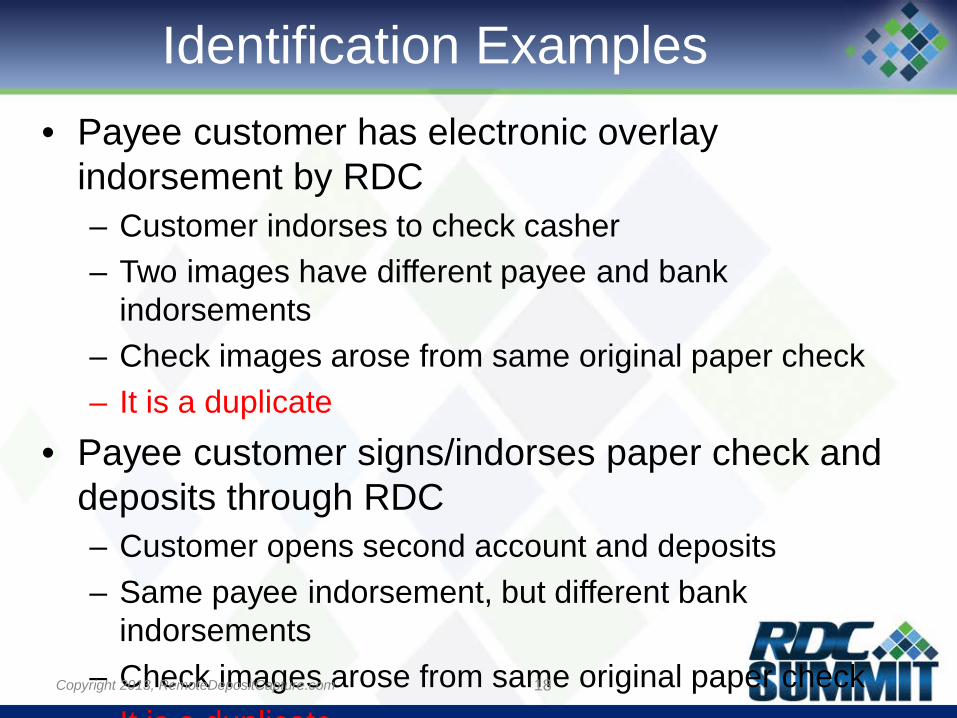

Identification Examples • Payee customer has electronic overlay

indorsement by RDC – Customer indorses to check casher – Two images have different payee and bank

indorsements – Check images arose from same original paper check – It is a duplicate

• Payee customer signs/indorses paper check and deposits through RDC – Customer opens second account and deposits – Same payee indorsement, but different bank

indorsements – Check images arose from same original paper check

It is a duplicate

18 Copyright 2013, RemoteDepositCapture.com

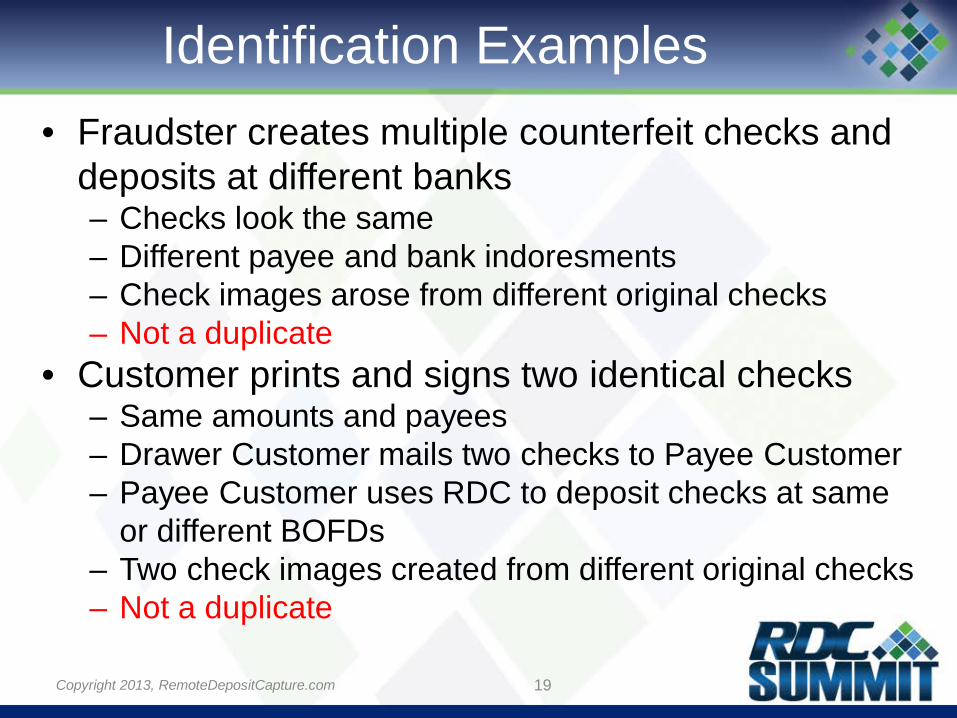

Identification Examples • Fraudster creates multiple counterfeit checks and

deposits at different banks – Checks look the same – Different payee and bank indoresments – Check images arose from different original checks – Not a duplicate

• Customer prints and signs two identical checks – Same amounts and payees – Drawer Customer mails two checks to Payee Customer – Payee Customer uses RDC to deposit checks at same

or different BOFDs – Two check images created from different original checks – Not a duplicate

19 Copyright 2013, RemoteDepositCapture.com

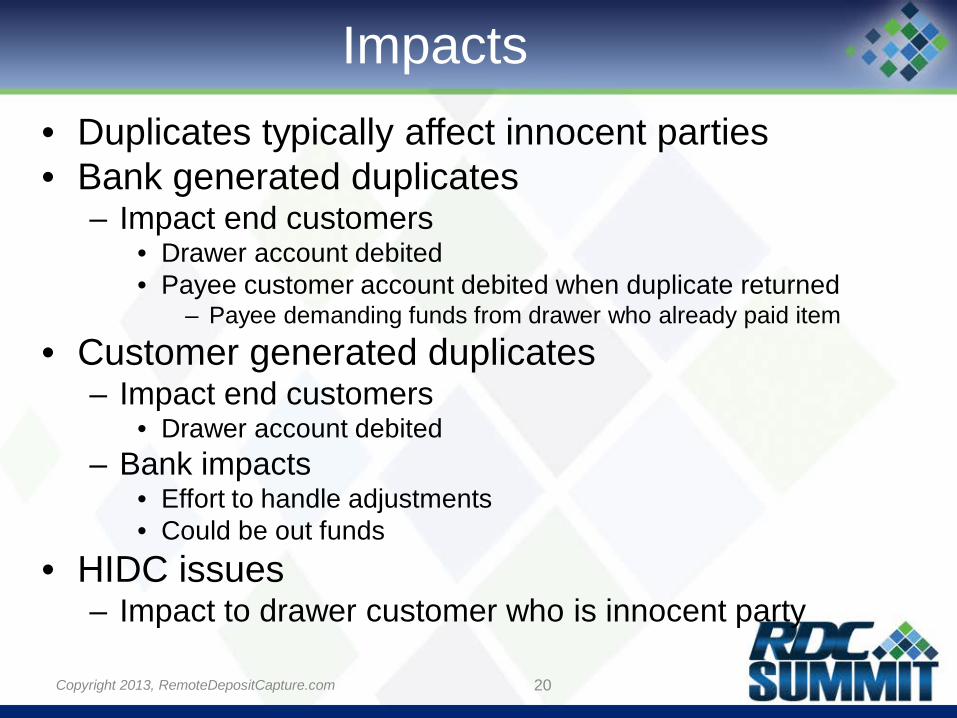

Impacts • Duplicates typically affect innocent parties • Bank generated duplicates

– Impact end customers • Drawer account debited • Payee customer account debited when duplicate returned

– Payee demanding funds from drawer who already paid item

• Customer generated duplicates – Impact end customers

• Drawer account debited – Bank impacts

• Effort to handle adjustments • Could be out funds

• HIDC issues – Impact to drawer customer who is innocent party

20 Copyright 2013, RemoteDepositCapture.com

Consumer RDC • Recently Holder in Due Course (HIDC) claims and

duplicate warranty raised • Changes to RDC landscape

– RDC volume growing as more banks offer service

• Possible sources of duplicate presentment in RDC context – Customer Errors and Fraud – Theft From Customer

• RDC duplication different from banks’ past experience – Internal Bank Duplication: Caused inside banking system

• No HIDC outside of banking system – Customer RDC Duplication: Caused outside of banking system

• HIDC may have original check and may demand payment from drawer

• Duplicate warranty covers HIDC duplicate warranty claims 21 Copyright 2013, RemoteDepositCapture.com

HIDC • If paying bank reimburses drawer or directly pays holder, bank may have

loss and warranty claim against original sending bank – Holder may demand payment from drawer when item returned unpaid by

paying bank • Claims by holder made outside of check collection process

– Breach of double payment warranty arises because drawer is asked to make two payments for same item

– Drawer customer paid claim to HIDC and also paid image presented by first sending bank

• Holder: Person that comes into possession of negotiable instrument • Holder in Due Course (HIDC): Type of holder that:

– Takes check for value, in good faith and without notice check is overdue or been dishonored

• Holder may make claim against drawer regardless of certain defenses – Not every holder qualifies as “holder in due course”

• Depends on facts and circumstances

22 Copyright 2013, RemoteDepositCapture.com

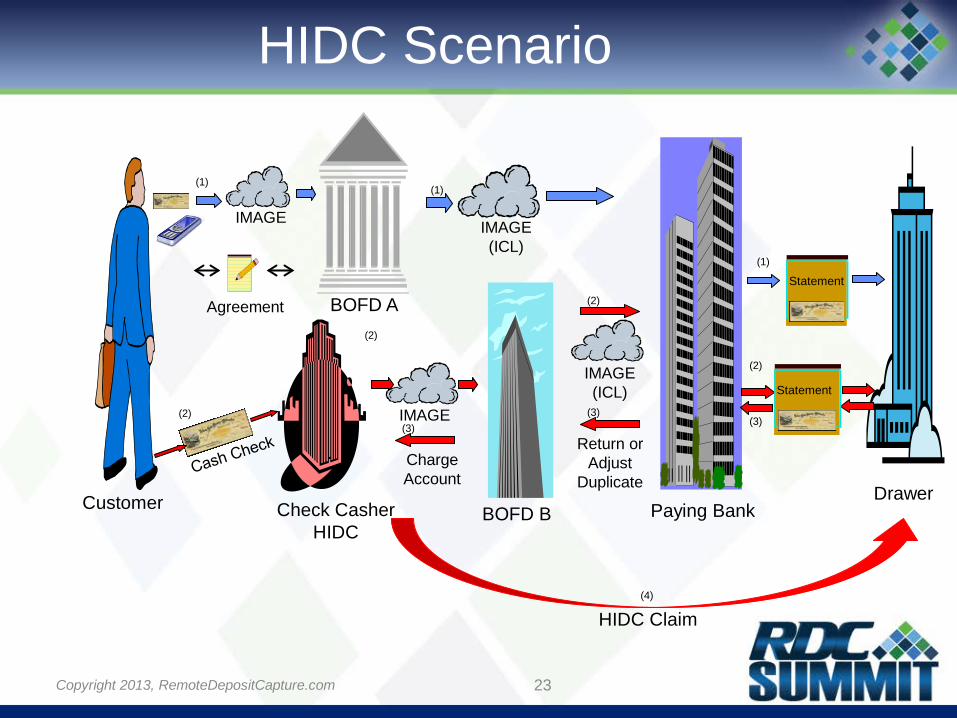

HIDC Scenario

23

BOFD A

Paying Bank

Agreement

Customer Drawer BOFD B Check Casher

HIDC

(2)

Return or Adjust

Duplicate

(3) (3)

Charge Account

(3)

HIDC Claim (4)

IMAGE

Statement

IMAGE (ICL)

(1) (1)

(1)

IMAGE (ICL)

IMAGE (2)

(2)

(2) Statement

Copyright 2013, RemoteDepositCapture.com

HIDC • Paying banks and customers encouraged not pay HIDC

claims if believe holder not have legitimate claim for payment of item – Example, customer or paying bank reason to believe holder

participated in fraud or theft

• ECCHO Rules and Fed OC 3 do not provide warranty directly to drawer – Warranty against double payment made only to Paying Bank – ECCHO Rules do not address relationship of drawer to its bank

• Application of warranty against double payment consistent with Check 21, Regulation CC and Rules – Protect Paying Bank and Drawer – Sending bank introduces risk by allowing customer to engage in

RDC • Appropriate to bear risk of loss from double payments

24 Copyright 2013, RemoteDepositCapture.com

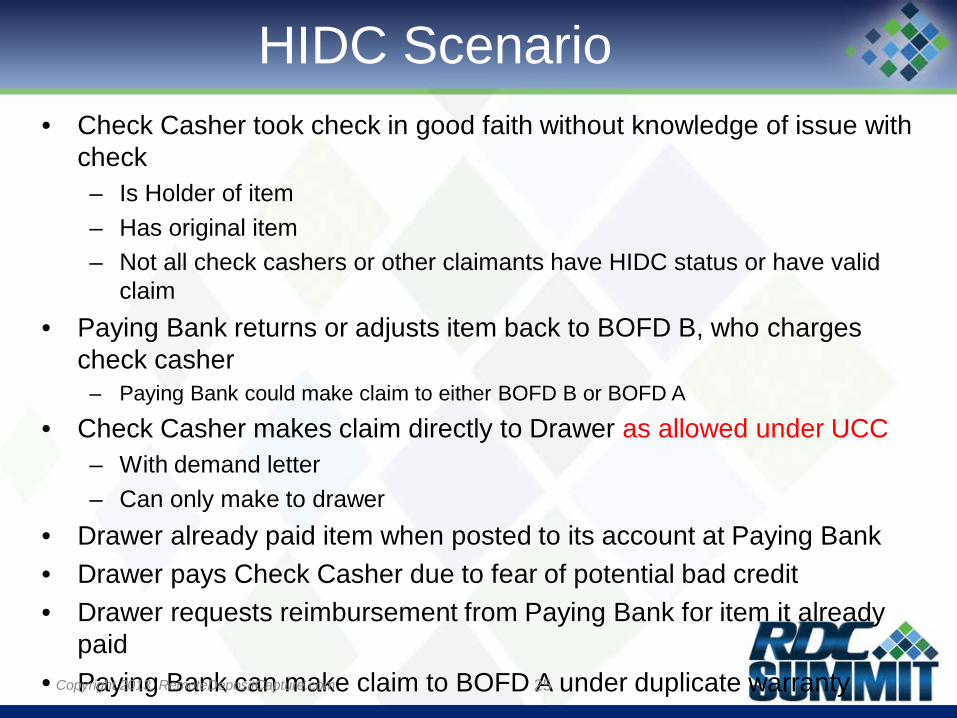

HIDC Scenario • Check Casher took check in good faith without knowledge of issue with

check – Is Holder of item – Has original item – Not all check cashers or other claimants have HIDC status or have valid

claim • Paying Bank returns or adjusts item back to BOFD B, who charges

check casher – Paying Bank could make claim to either BOFD B or BOFD A

• Check Casher makes claim directly to Drawer as allowed under UCC – With demand letter – Can only make to drawer

• Drawer already paid item when posted to its account at Paying Bank • Drawer pays Check Casher due to fear of potential bad credit • Drawer requests reimbursement from Paying Bank for item it already

paid • Paying Bank can make claim to BOFD A under duplicate warranty

25 Copyright 2013, RemoteDepositCapture.com

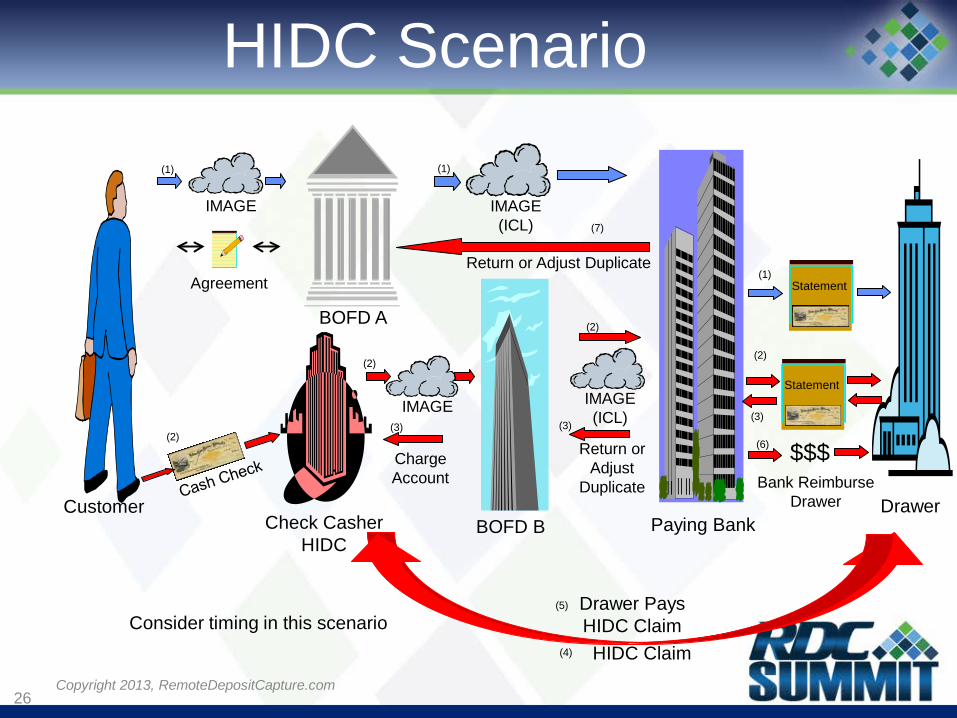

HIDC Scenario

26

BOFD A

Paying Bank

Agreement

Customer Drawer BOFD B Check Casher

HIDC

Statement

IMAGE IMAGE (ICL)

(1) (1)

(1) Return or Adjust Duplicate

(7)

Return or Adjust

Duplicate

(3) (3)

Charge Account

(3)

Statement

(2)

IMAGE (ICL)

IMAGE

(2)

(2)

(2)

HIDC Claim (4)

Drawer Pays HIDC Claim

(5)

Bank Reimburse Drawer

$$$ (6)

Copyright 2013, RemoteDepositCapture.com

Consider timing in this scenario

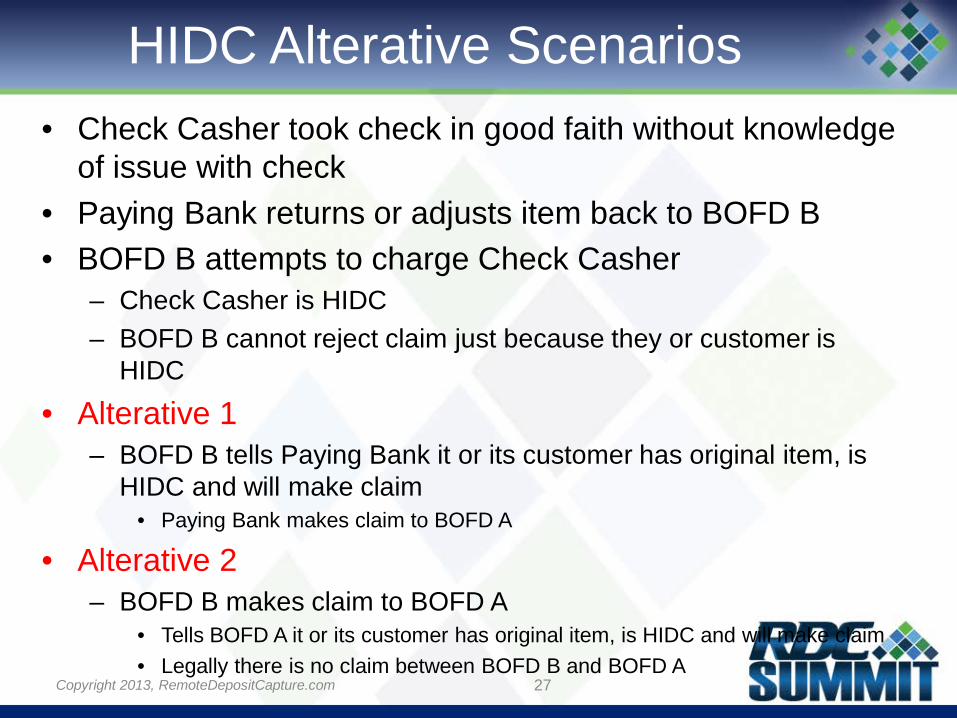

HIDC Alterative Scenarios • Check Casher took check in good faith without knowledge

of issue with check • Paying Bank returns or adjusts item back to BOFD B • BOFD B attempts to charge Check Casher

– Check Casher is HIDC – BOFD B cannot reject claim just because they or customer is

HIDC

• Alterative 1 – BOFD B tells Paying Bank it or its customer has original item, is

HIDC and will make claim • Paying Bank makes claim to BOFD A

• Alterative 2 – BOFD B makes claim to BOFD A

• Tells BOFD A it or its customer has original item, is HIDC and will make claim • Legally there is no claim between BOFD B and BOFD A

27 Copyright 2013, RemoteDepositCapture.com

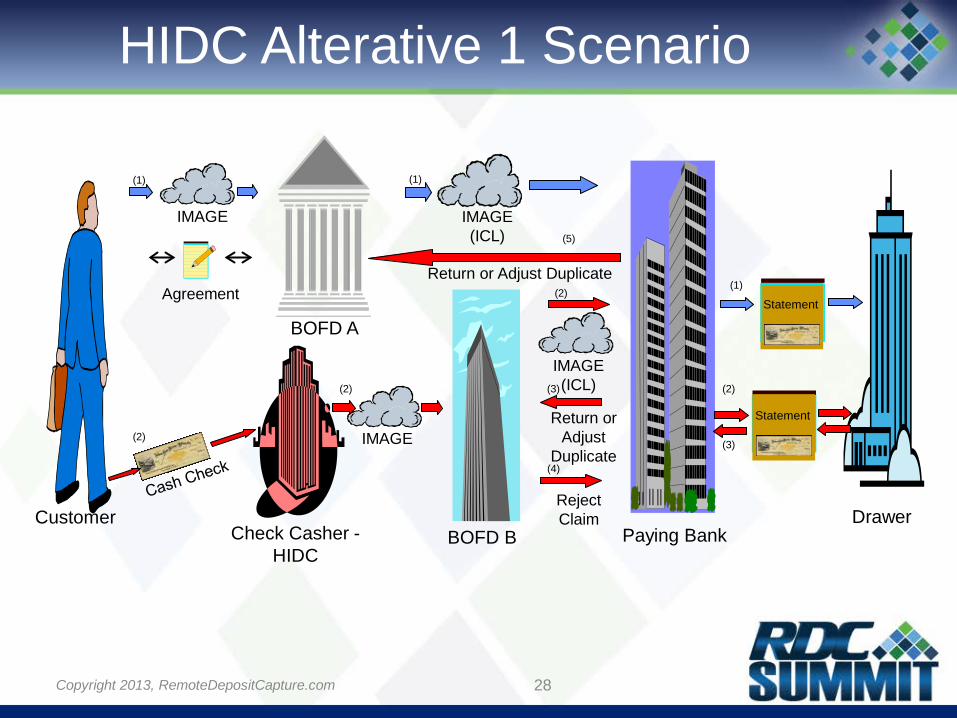

HIDC Alterative 1 Scenario

28

BOFD A

Paying Bank

Agreement

Customer Drawer BOFD B Check Casher -

HIDC

IMAGE

Statement

IMAGE (ICL)

(1) (1)

(1)

Statement

IMAGE (ICL)

IMAGE (2)

(2)

(2)

(2)

Return or Adjust

Duplicate

(3)

(3)

Reject Claim

(4)

Return or Adjust Duplicate

(5)

Copyright 2013, RemoteDepositCapture.com

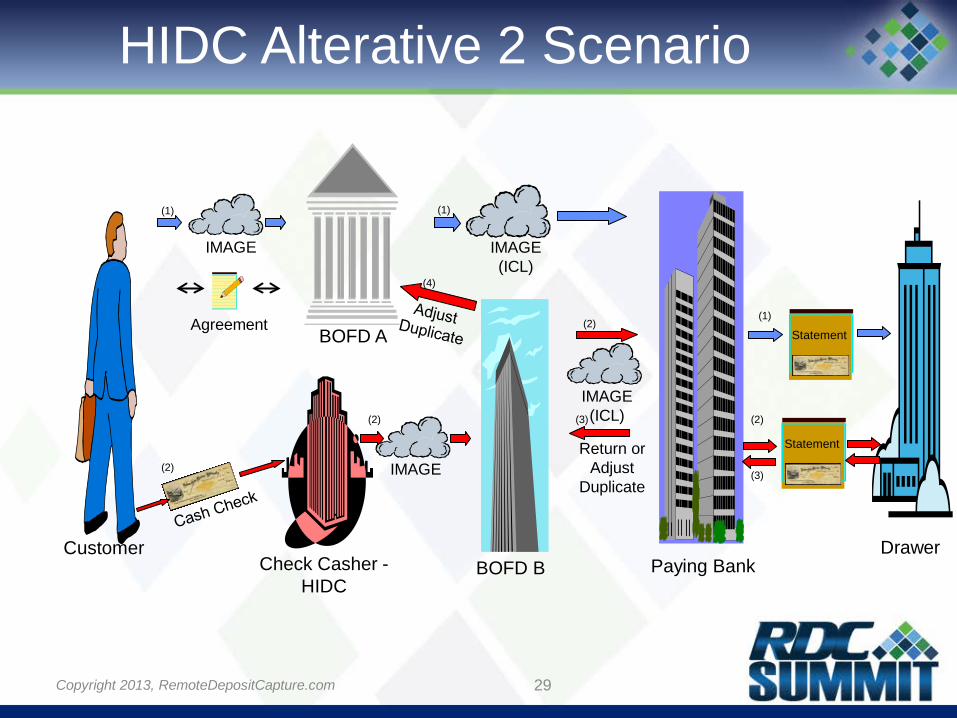

HIDC Alterative 2 Scenario

29

BOFD A

Paying Bank

Agreement

Customer Drawer BOFD B Check Casher -

HIDC

IMAGE

Statement

IMAGE (ICL)

(1) (1)

(1)

Statement

IMAGE (ICL)

IMAGE (2)

(2)

(2)

(2)

Return or Adjust

Duplicate

(3)

(3)

(4)

Copyright 2013, RemoteDepositCapture.com

Advantages to Alternatives • Scenarios could avoid some complications of HIDC

claims and subsequent warranty claims • Drawer customer does not receive direct claim from check

casher/HIDC – Resolution of duplicate payment claim handled within banking

system

• More expeditious claims process • Appropriate for BOFD A to bear risk of loss from double

payments – BOFD A introduced risk by allowing customer to engage in remote

deposit capture – Customer did not secure original paper – BOFD A in best position to collect on claim from customer

• Customer and bank typically have legal contract, protecting bank

30 Copyright 2013, RemoteDepositCapture.com

Indorsement Implications • Banks offering RDC consider indorsement language

– Help identify “status” of item already truncated • Surveyed banks and reviewed RDC agreements

– Most surveyed banks required some form of restrictive endorsement on original check such as:

• “For Deposit only” or “ For Mobile Deposit”, and/or • Deposit to name of BOFD, and/or specific account number

– Restrictive indorsement puts subsequent holder(s) of paper check on notice that item has been previously deposited

• Adjustment areas trying to determine RDC indorsements for claims

• None of agreements reviewed required depositor to “frank” the item or mark as VOID at time of deposit – Banks may want to process original paper check if image collection

fails

31 Copyright 2013, RemoteDepositCapture.com

Risk of Duplicates

• Risks to Payments System and Industry – Financial loss to bank and/or customer

• Expense of resolving duplicates – Customer dissatisfaction/lost customer

relationship(s) – Reputational risk to FIs, exchange

system (network) and banking industry • For RDC/check/image exchange

– Perception of high risk

32 Copyright 2013, RemoteDepositCapture.com

Risk Mitigation • New legislation and technologies have

changed payments collection – Substitute checks after Check 21 – Rapid growth in image exchange

• RDC and mobile payments – Changing payments delivery channels

• Increased importance in prevention and detection processes

33 Copyright 2013, RemoteDepositCapture.com

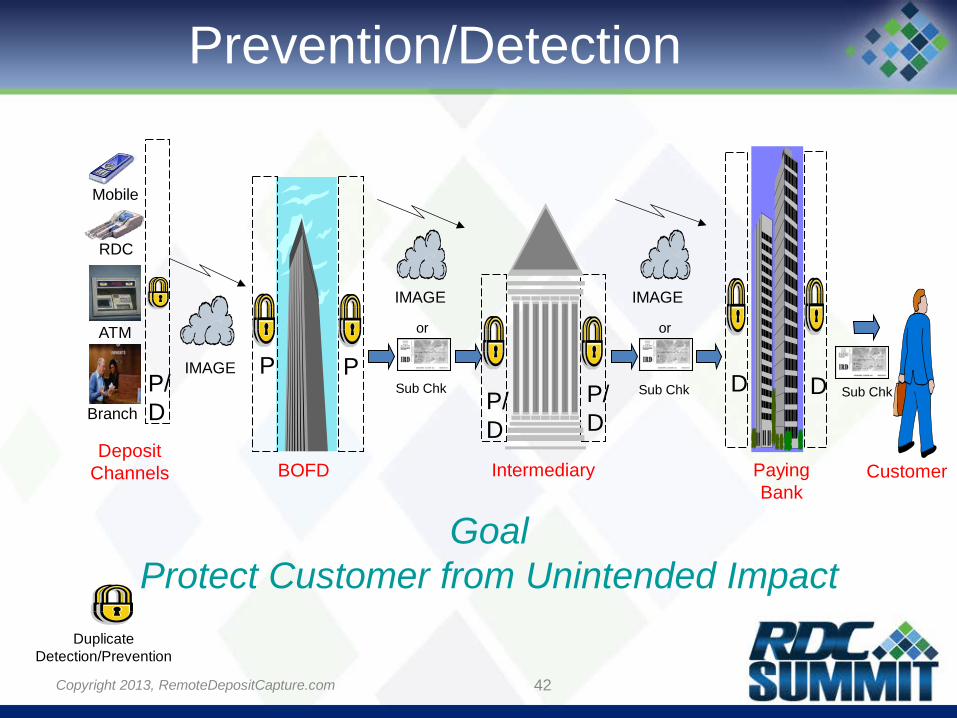

Prevention/Detection • For Forward and Return Processing • Prevention performed by institution that truncates

check and creates image or IRD – BOFD or other collecting/returning bank – Truncating institution should prevent duplicates – Capture earlier in process (customer, teller or branch)

means tighter prevention methods due to various skill levels

• Detection performed by institution receiving image or IRD

• Banks to determine level of prevention/detection needed 34 Copyright 2013, RemoteDepositCapture.com

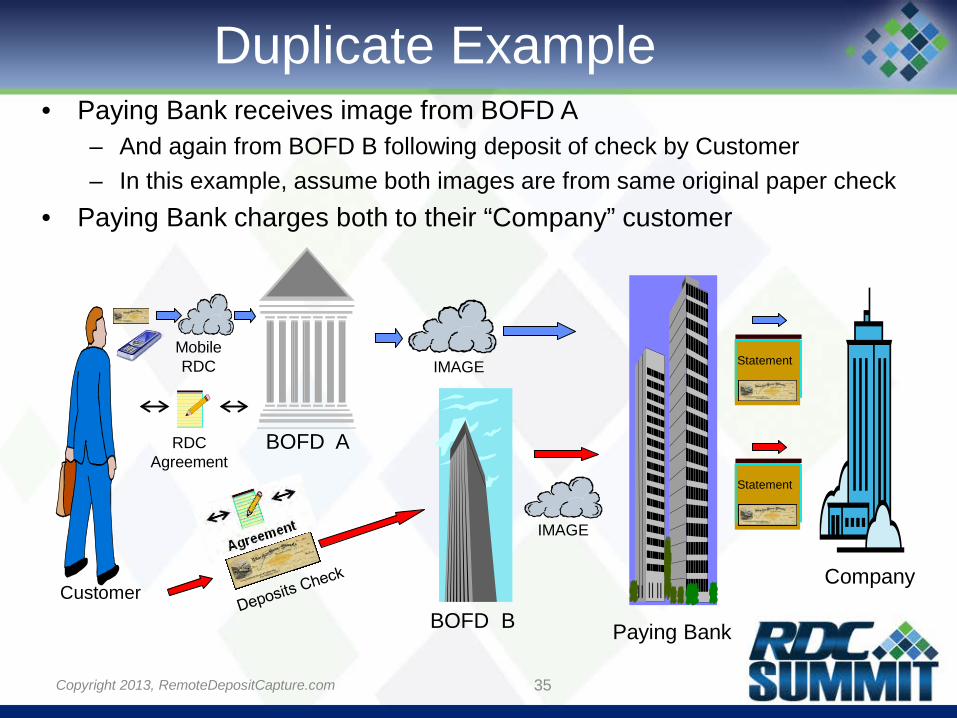

Duplicate Example

35 Copyright 2013, RemoteDepositCapture.com

Mobile RDC

BOFD A

Paying Bank

RDC Agreement

Customer Company

Statement

BOFD B

Statement

IMAGE

IMAGE

• Paying Bank receives image from BOFD A – And again from BOFD B following deposit of check by Customer – In this example, assume both images are from same original paper check

• Paying Bank charges both to their “Company” customer

ATM

IMAGE

Branch

Intermediary

IMAGE

Paying Bank

BOFD

IMAGE

or

Customer

Sub Chk

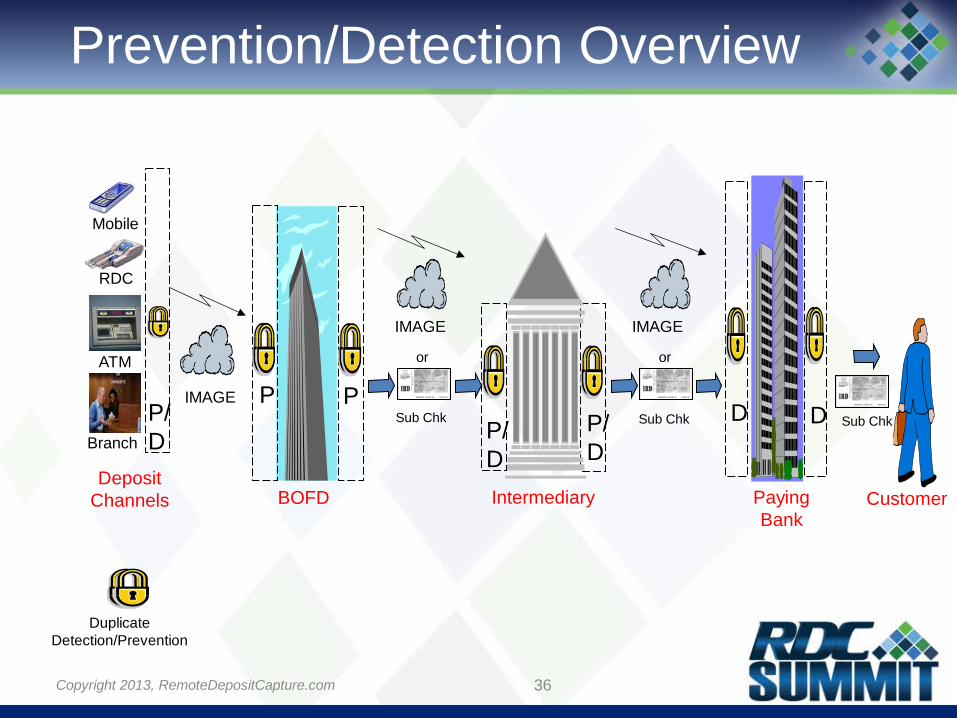

Duplicate Detection/Prevention

P P P/D

D D P/D

Prevention/Detection Overview

36

P/D

RDC

Mobile

Sub Chk Sub Chk

or

Deposit Channels

Copyright 2013, RemoteDepositCapture.com

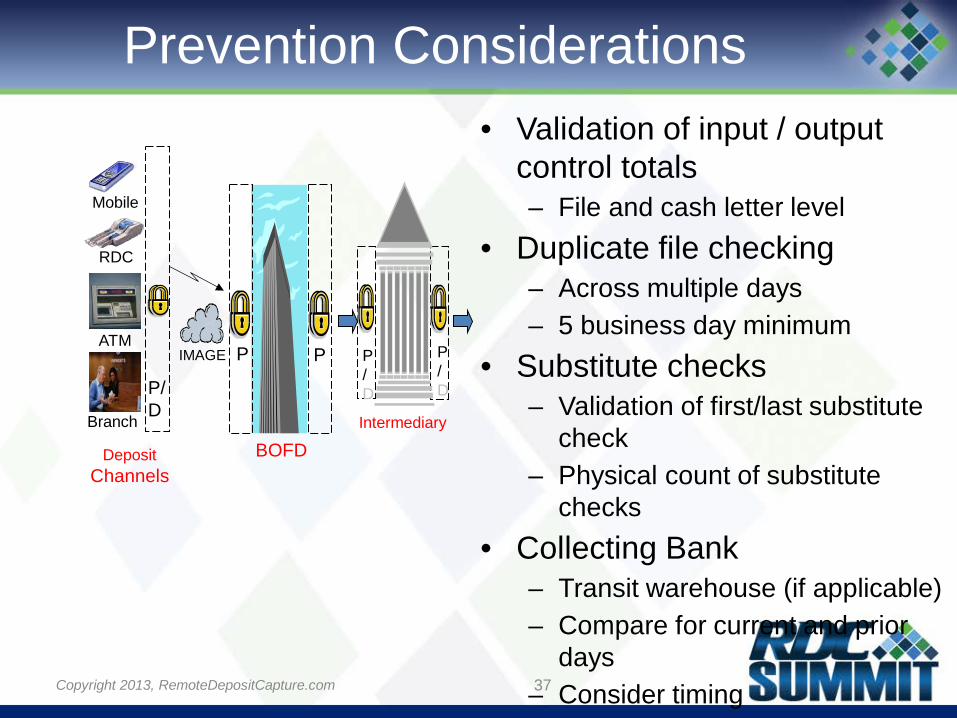

Prevention Considerations • Validation of input / output

control totals – File and cash letter level

• Duplicate file checking – Across multiple days – 5 business day minimum

• Substitute checks – Validation of first/last substitute

check – Physical count of substitute

checks • Collecting Bank

– Transit warehouse (if applicable) – Compare for current and prior

days – Consider timing

37

ATM IMAGE

Branch

BOFD

P P

P/D

RDC

Mobile

Deposit Channels

Intermediary

P/D

P/D

Copyright 2013, RemoteDepositCapture.com

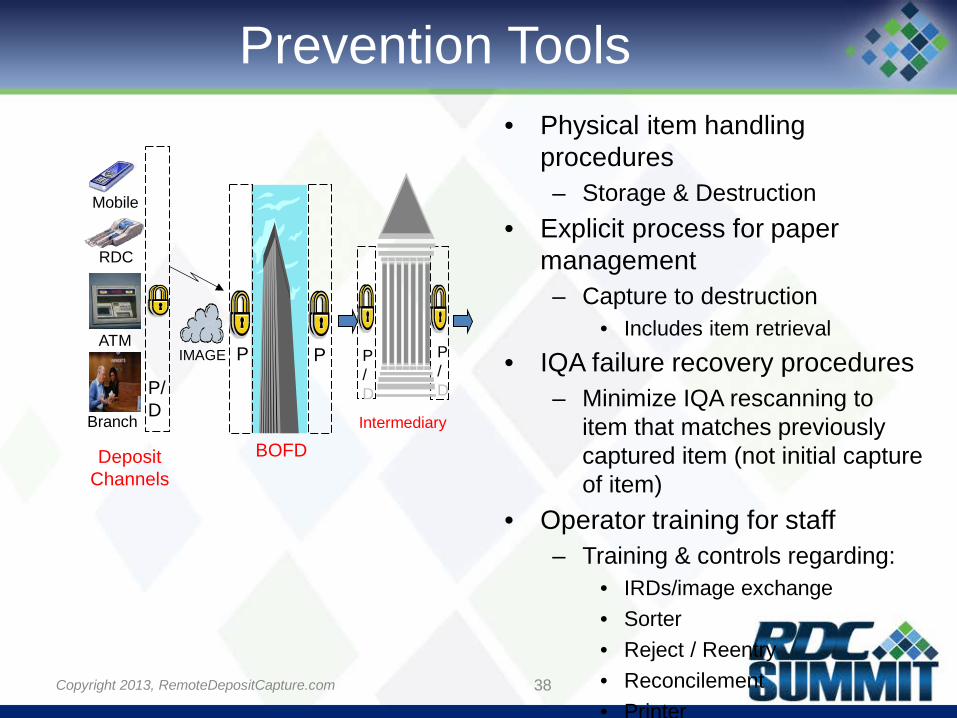

Prevention Tools • Physical item handling

procedures – Storage & Destruction

• Explicit process for paper management – Capture to destruction

• Includes item retrieval

• IQA failure recovery procedures – Minimize IQA rescanning to

item that matches previously captured item (not initial capture of item)

• Operator training for staff – Training & controls regarding:

• IRDs/image exchange • Sorter • Reject / Reentry • Reconcilement • Printer

38

ATM IMAGE

Branch

BOFD

P P

P/D

RDC

Mobile

Deposit Channels

Intermediary

P/D

P/D

Copyright 2013, RemoteDepositCapture.com

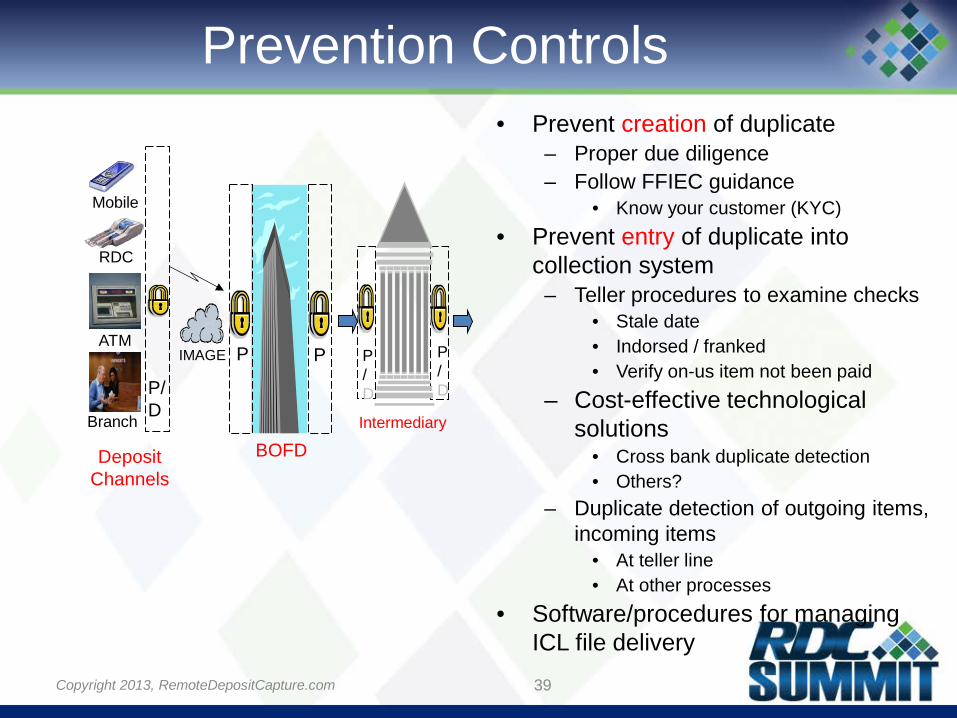

Prevention Controls • Prevent creation of duplicate

– Proper due diligence – Follow FFIEC guidance

• Know your customer (KYC) • Prevent entry of duplicate into

collection system – Teller procedures to examine checks

• Stale date • Indorsed / franked • Verify on-us item not been paid

– Cost-effective technological solutions

• Cross bank duplicate detection • Others?

– Duplicate detection of outgoing items, incoming items

• At teller line • At other processes

• Software/procedures for managing ICL file delivery

39

ATM IMAGE

Branch

BOFD

P P

P/D

RDC

Mobile

Deposit Channels

Intermediary

P/D

P/D

Copyright 2013, RemoteDepositCapture.com

Detection • Who/Where

– Paying Bank – Prior to or after posting • Prior To Posting: At file receipt • After Posting: At exception item pull or within Fraud system

– Collecting Bank – Prior to submitting file for collection • What – Methods of detection

– File Level – Generally easiest method – Cash Letter – Check headers/totals for what was

received – Item level – Most effective dup checking

• When – Across multiple days • Timing – Consider processing time

– Detection runtime vs. tradeoff/risk of letting a duplicate through to posting

40 Copyright 2013, RemoteDepositCapture.com

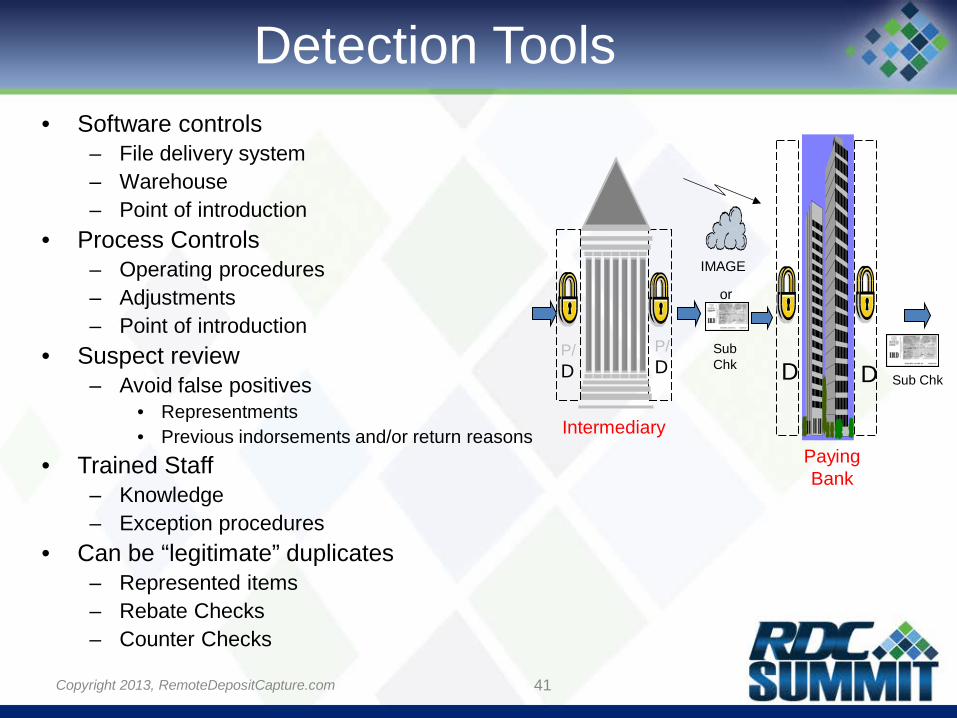

Detection Tools • Software controls

– File delivery system – Warehouse – Point of introduction

• Process Controls – Operating procedures – Adjustments – Point of introduction

• Suspect review – Avoid false positives

• Representments • Previous indorsements and/or return reasons

• Trained Staff – Knowledge – Exception procedures

• Can be “legitimate” duplicates – Represented items – Rebate Checks – Counter Checks

41

Paying Bank

Sub Chk D D

Intermediary

P/D

P/D

IMAGE

Sub Chk

or

Copyright 2013, RemoteDepositCapture.com

ATM

IMAGE

Branch

Intermediary

IMAGE

Paying Bank

BOFD

IMAGE

or

Customer

Sub Chk

Duplicate Detection/Prevention

P P P/D

D D P/D

Prevention/Detection

42

P/D

Goal Protect Customer from Unintended Impact

RDC

Mobile

Sub Chk Sub Chk

or

Deposit Channels

Copyright 2013, RemoteDepositCapture.com

Detection Implications • What happens if duplicates go undetected?

– Customer account posting • Customer ODs, wrongful dishonor

– Accounting issues • Misstated balances • Interest not applied

– Customer Reporting issues • Intra-day reporting incorrect • Overfunding of accounts

– Customer Notification • May need to provide timely notification to customers

of duplicates posted to account 43 Copyright 2013, RemoteDepositCapture.com

We Have A Duplicate! • Prevention and detection failed and you’ve

posted a duplicate item to your customer’s account – now what? – As the Paying Bank your return clocks are ticking

• UCC midnight deadline • Reg CC two-day expeditious return deadline

– Do you return the item? • What is the correct return reason code?

– Do you adjust the item? • Do you return or adjust first or second item?

• What are your options?

44 Copyright 2013, RemoteDepositCapture.com

Paying Bank BOFD

IMAGE

Image Adjustment

Image Return

or

Sub Ck

Drawer Customer

Duplicate

Sub Ck Return

Deposit Ck IMAGE

Depositing Customer

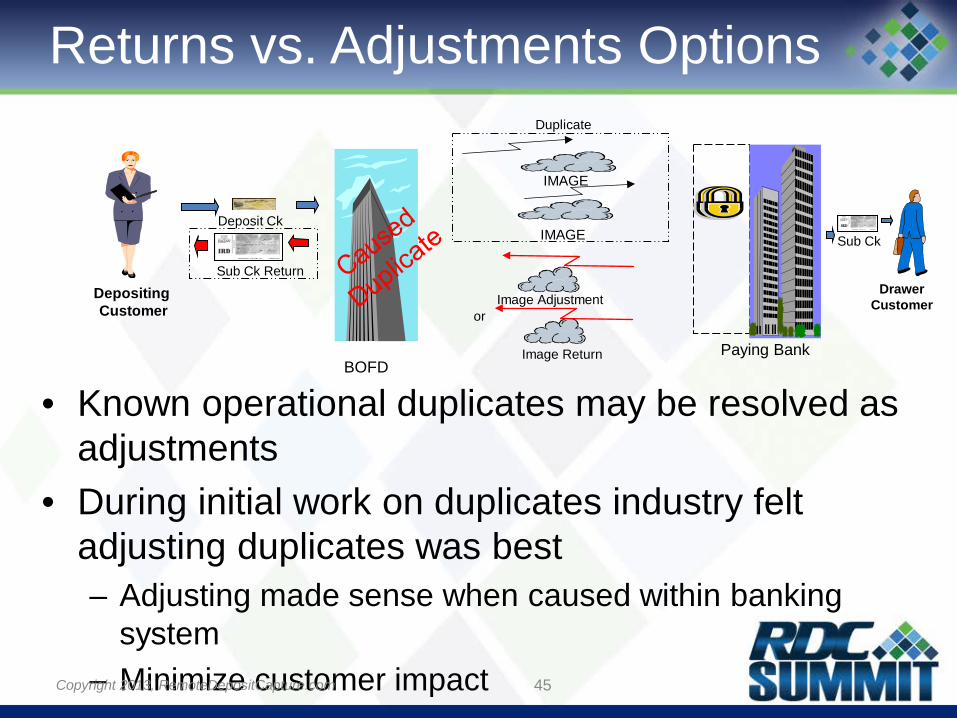

Returns vs. Adjustments Options

• Known operational duplicates may be resolved as adjustments

• During initial work on duplicates industry felt adjusting duplicates was best – Adjusting made sense when caused within banking

system – Minimize customer impact 45 Copyright 2013, RemoteDepositCapture.com

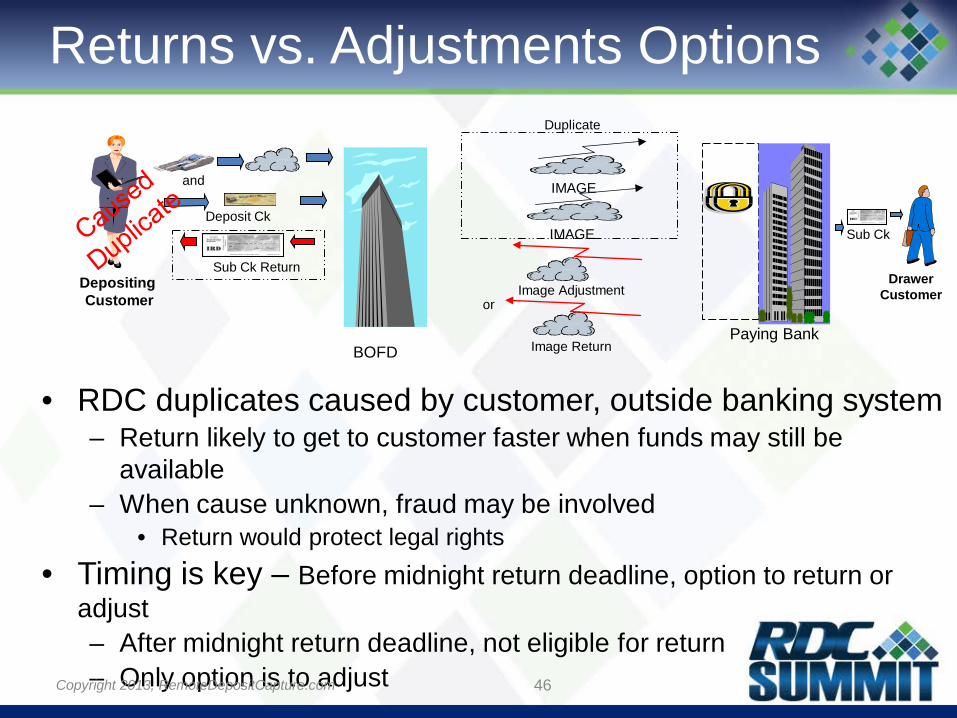

Returns vs. Adjustments Options

• RDC duplicates caused by customer, outside banking system – Return likely to get to customer faster when funds may still be

available – When cause unknown, fraud may be involved

• Return would protect legal rights • Timing is key – Before midnight return deadline, option to return or

adjust – After midnight return deadline, not eligible for return – Only option is to adjust 46 Copyright 2013, RemoteDepositCapture.com

Paying Bank BOFD

IMAGE

Deposit Ck

Image Adjustment

Image Return

and

or

Sub Ck

Drawer Customer

Duplicate

Sub Ck Return

IMAGE

Depositing Customer

Resolutions • Returns

– Faster – Timely Settlement – May have negative impact on innocent parties

(depositing customer and drawer customer) – Use correct return reason code for Duplicate

• May avoid some negative impact – Personnel not familiar with process – Do not lose right of return

• Significant issue if item is counterfeit or forged and not duplicate

47 Copyright 2013, RemoteDepositCapture.com

Resolutions • Adjustments

– Made to appropriate party – Less negative impact to customers – Handled within banking system – Personnel familiar with process

• Historically resolve these issues – Less efficient than returns

• Slower, less timely settlement • Due to timing can lose right to return

– Significant issue if item is counterfeit or forged and not duplicate • More paperwork • May have dollar limits and/or fees associated with certain

adjustments • Decision to return or adjust at discretion of bank

– Bank must perform its own risk analysis; Encouraged to seek legal counsel on potential legal risks

48 Copyright 2013, RemoteDepositCapture.com

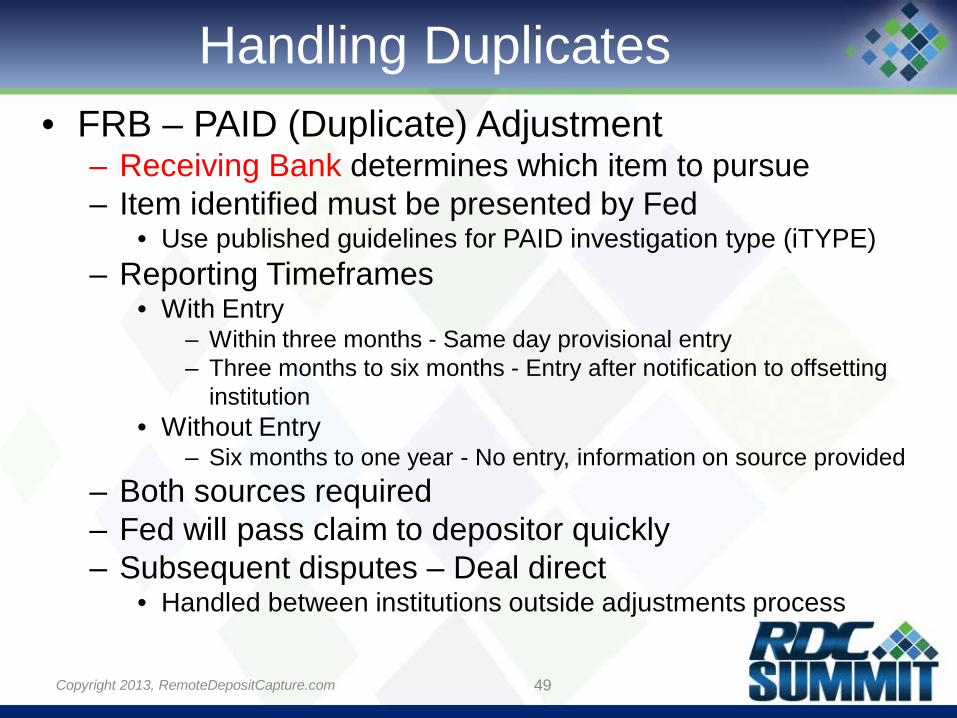

Handling Duplicates • FRB – PAID (Duplicate) Adjustment

– Receiving Bank determines which item to pursue – Item identified must be presented by Fed

• Use published guidelines for PAID investigation type (iTYPE) – Reporting Timeframes

• With Entry – Within three months - Same day provisional entry – Three months to six months - Entry after notification to offsetting

institution • Without Entry

– Six months to one year - No entry, information on source provided – Both sources required – Fed will pass claim to depositor quickly – Subsequent disputes – Deal direct

• Handled between institutions outside adjustments process

49 Copyright 2013, RemoteDepositCapture.com

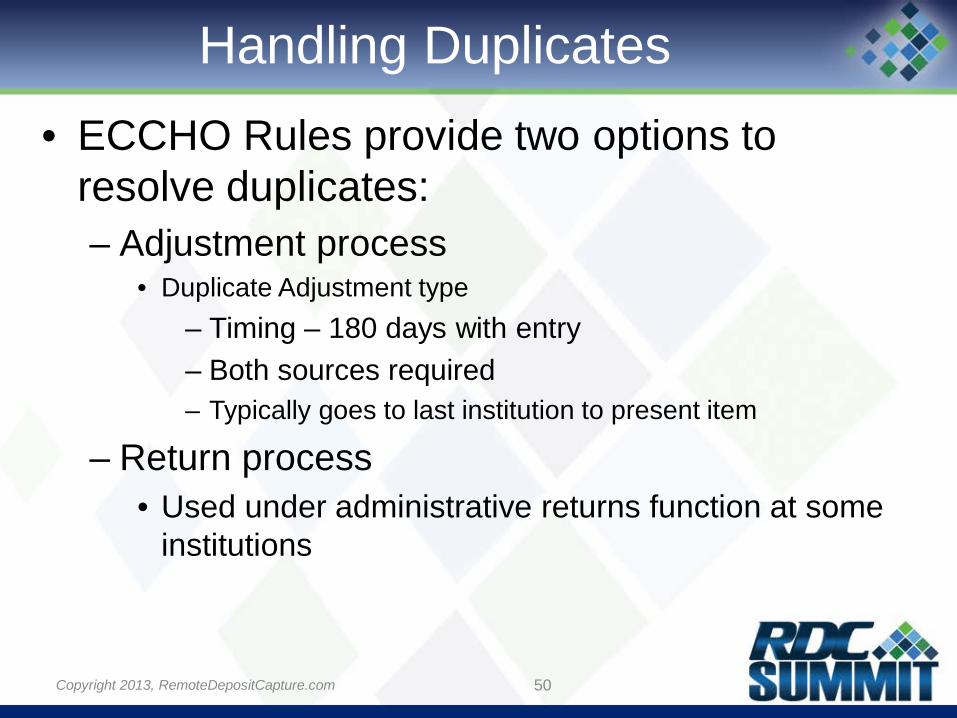

Handling Duplicates • ECCHO Rules provide two options to

resolve duplicates: – Adjustment process

• Duplicate Adjustment type – Timing – 180 days with entry – Both sources required – Typically goes to last institution to present item

– Return process • Used under administrative returns function at some

institutions

50 Copyright 2013, RemoteDepositCapture.com

Intermediary Process

51

Bank A Bank B Bank C

Duplicate Warranty

Duplicate Warranty

Duplicate Adjustment

Duplicate Adjustment

Copyright 2013, RemoteDepositCapture.com

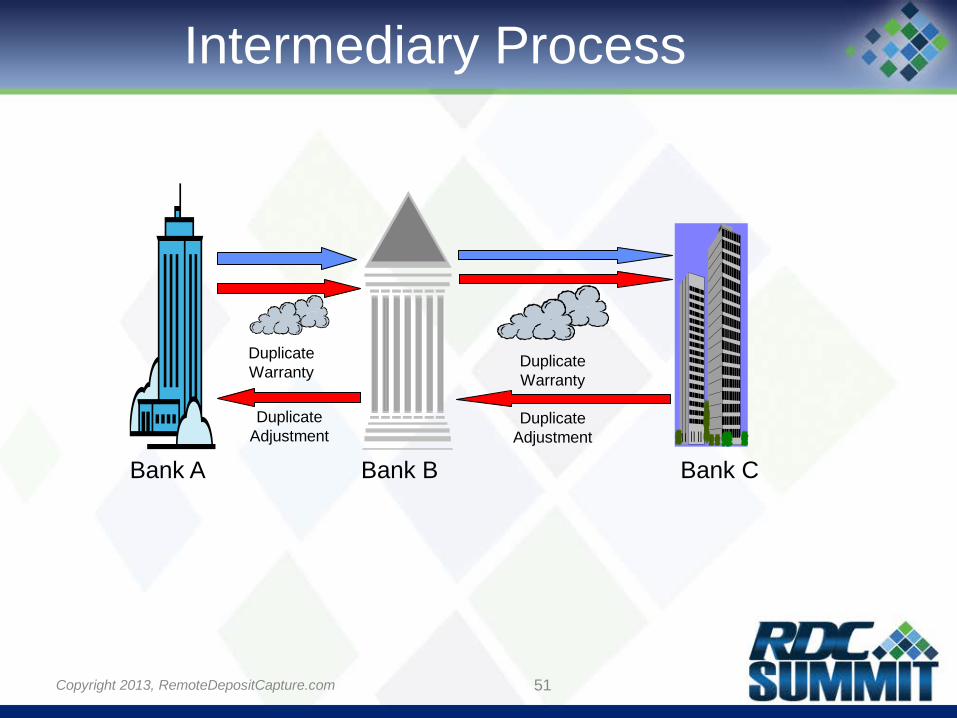

Intermediary Process • Many banks act as intermediaries for image exchange

– Intermediary institution typically has some relationship (customer) with their correspondent banks

– May have commitments regarding adjustments

• Nothing in private sector rules regarding directing Paying Bank to deal direct with BOFD – Fed makes entries based on timeframe of adjustment and directs

banks to “deal direct” at some point in time

• When image is sent from Bank A to Bank B to Bank C, Bank A made warranty to Bank B who made warranty to Bank C – Both Bank A and Bank B are liable under the warranties

• When Bank B gets claim will typically make claim to Bank A

• Bank B sometimes caught in middle because of relationship

52 Copyright 2013, RemoteDepositCapture.com

Intermediary Duplicate Checking • Some intermediary banks do duplicate checking

– May cause issues for a represented item • Following slides will illustrate the “flipping” of the

forward and return indorsement records • For more discussion on indorsements

– X9 standards “20” series and “30” series electronic indorsement records

– See document on CheckImage Central website titled, “Endorsements: Information and Usage” – link: www.checkimagecentral.org/PDF/UCD_Endorsements_Reformatted_2011_Mar_09.pdf

53 Copyright 2013, RemoteDepositCapture.com

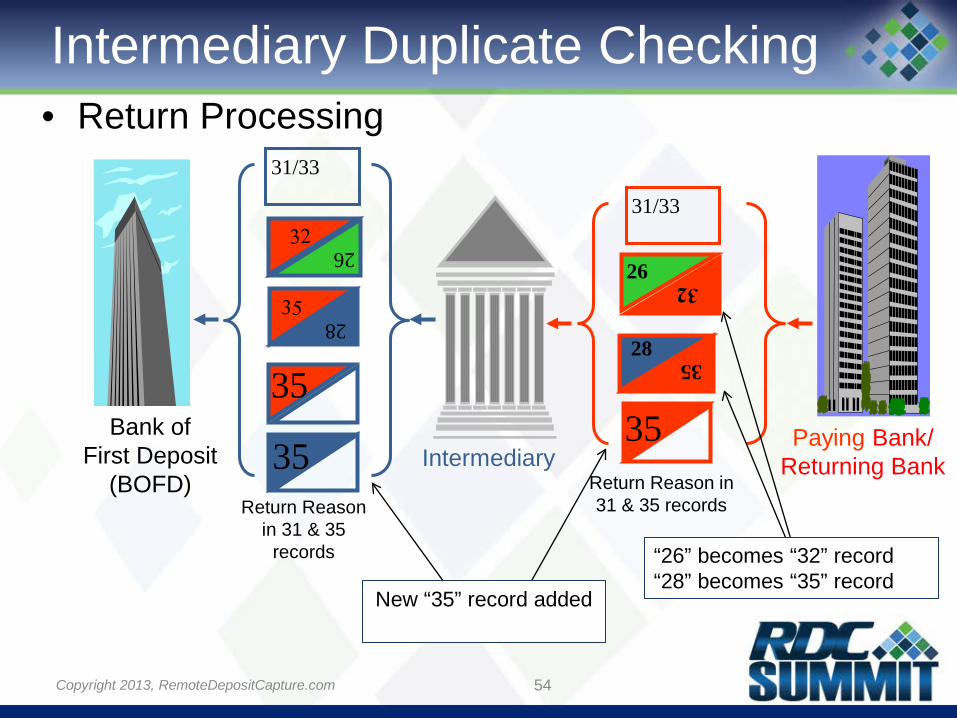

Intermediary Duplicate Checking • Return Processing

54

Paying Bank/ Returning Bank

Bank of First Deposit

(BOFD)

31/33

Intermediary

31/33

26

28 35

35 Return Reason

in 31 & 35 records

26

28 35

“26” becomes “32” record “28” becomes “35” record

35 Return Reason in 31 & 35 records

New “35” record added

Copyright 2013, RemoteDepositCapture.com

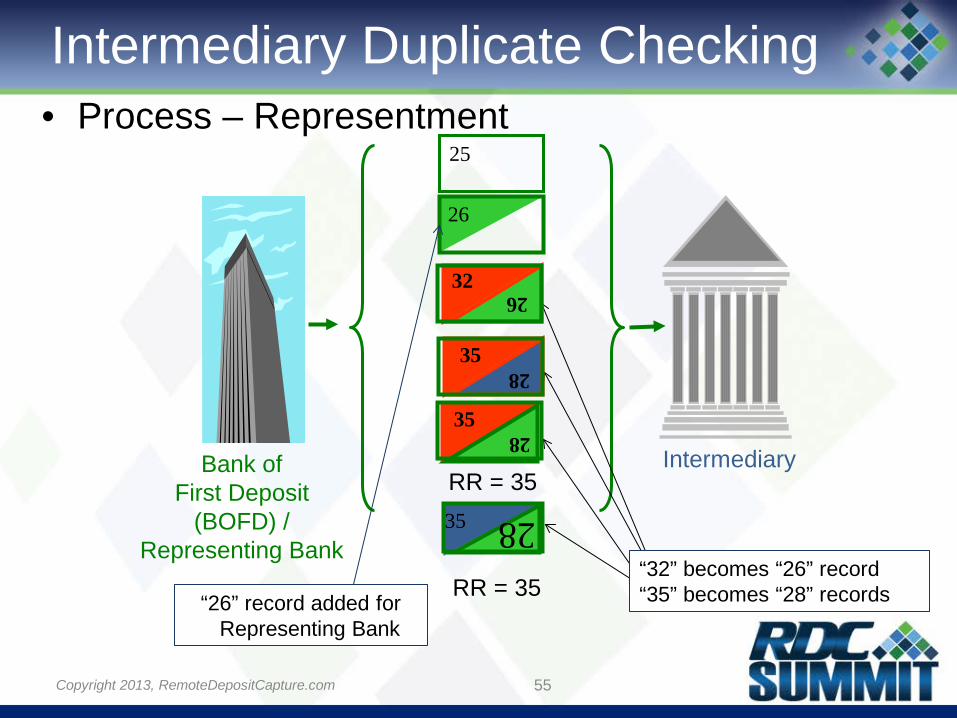

Intermediary Duplicate Checking • Process – Representment

55

25

Bank of First Deposit

(BOFD) / Representing Bank

28 35

Intermediary

RR = 35

RR = 35

26

“26” record added for Representing Bank

“32” becomes “26” record “35” becomes “28” records

26 32

28 35

28 35

Copyright 2013, RemoteDepositCapture.com

Electronic Records • Return Reason Code

– Paying Bank should add return reason to its Type 35 Record • Match Return Reason in Type 31 Record

• Other institutions in return collection chain – When adding own Type 35 record should propagate return reason

from Type 31 Record • Or last Type 35 Record received • Should be the same

– Type 28 Record should only have return reason, if created (flipped) from Type 35 Record that had return reason

• Why is this critical to the collection process? – Without return reason, item may be flagged as duplicate

• Especially Intermediary Bank with no knowledge that item was returned

56 Copyright 2013, RemoteDepositCapture.com

Represented Duplicates • Duplicate warranty limited to situation where Receiving

Bank pays item already paid – Not applicable where Receiving Bank returned and reversed

settlement of first item, then receives second item – Receiving Bank only paid single item

• Paying bank return system should interface timely with duplicate system – How long maintain items for duplicate detection

• Proper Handling of Represented Item – Avoid incorrect identification as duplicate – Proper use of return reason codes on representment in file

• Do not re-image original item – Use IRD – No longer has previous indorsements and/or return reason

57 Copyright 2013, RemoteDepositCapture.com

Represented Duplicates • Not required to use original

– Check 21 language says “Substitute check is accurate representation of original at time item was truncated”

• Original item already truncated

– Very difficult to use original and properly populate return codes in file

• Example: Using original item incorrectly – RDC customer pulls original for representment – Item returned needs some physical correction such as:

• Payee Indorsement; or • WIC stamp

– Put indorsement/required stamps on IRD

58 Copyright 2013, RemoteDepositCapture.com

RDC IRD Deposit • Question of whether customer can deposit IRDs

through RDC – Previously most banks did not allow – Now some analyzing

• Allowing customer represent returned IRD, can potentially help with duplicates – If IRD represented then return reason code and all

endorsements on it • Allowing paying bank more easily and accurately determine

represented check • When not allowed to represent IRD, customer may pull original

item and redeposit making duplicate detection more difficult

59 Copyright 2013, RemoteDepositCapture.com

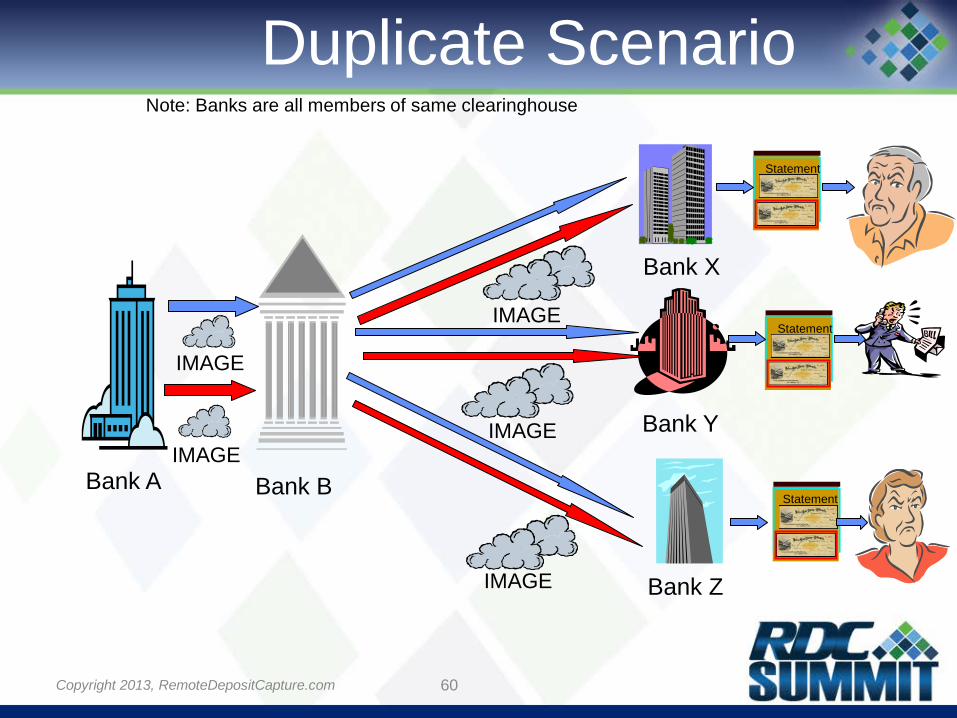

Duplicate Scenario

Bank A

Bank Z

Bank Y

Bank B

Bank X

IMAGE

IMAGE

IMAGE

IMAGE

Statement

Statement

IMAGE

Note: Banks are all members of same clearinghouse

Statement

60 Copyright 2013, RemoteDepositCapture.com

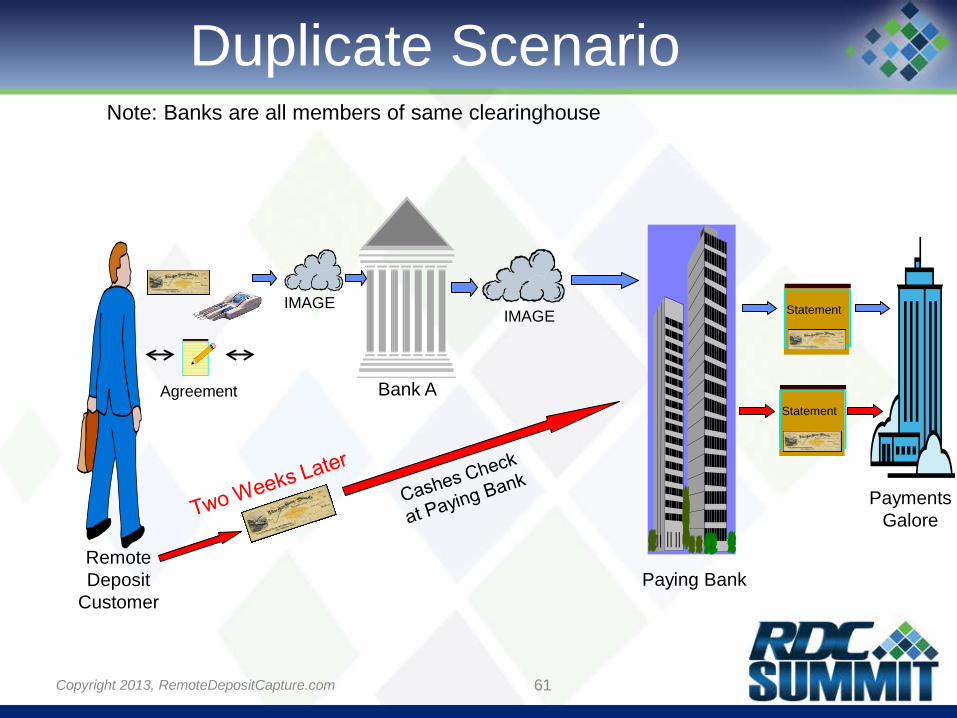

IMAGE

Bank A

Paying Bank

Agreement

Remote Deposit

Customer

Payments Galore

Statement

Statement IMAGE

Note: Banks are all members of same clearinghouse

Duplicate Scenario

61 Copyright 2013, RemoteDepositCapture.com

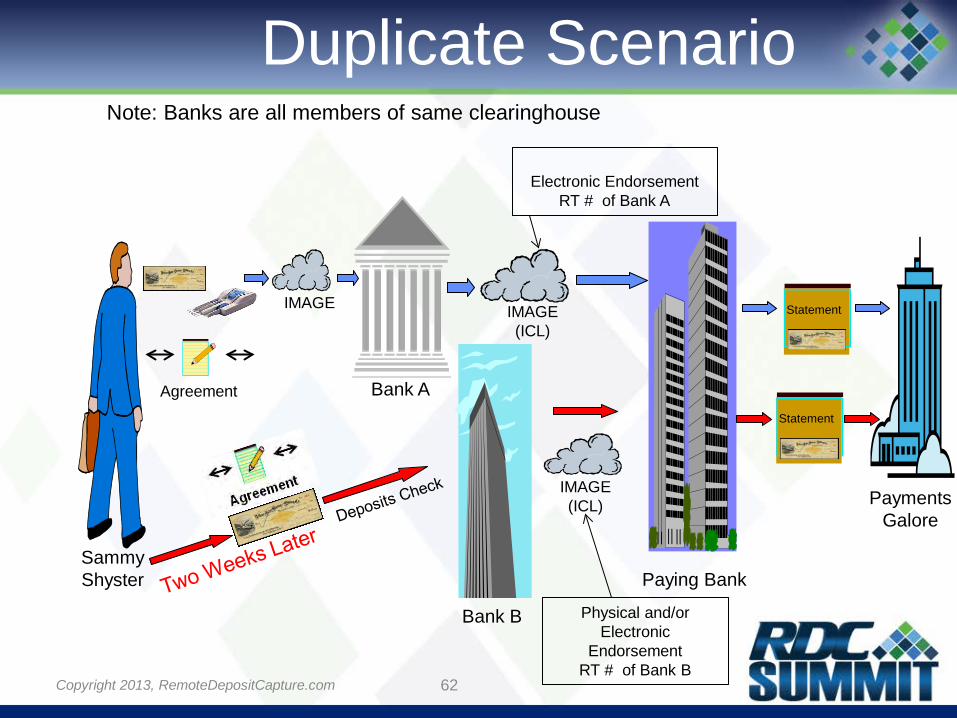

IMAGE

Bank A

Paying Bank

Agreement

Sammy Shyster

Payments Galore

Statement IMAGE

(ICL)

Electronic Endorsement

RT # of Bank A

Statement

Bank B

IMAGE (ICL)

Physical and/or Electronic

Endorsement RT # of Bank B

Note: Banks are all members of same clearinghouse

Duplicate Scenario

62 Copyright 2013, RemoteDepositCapture.com

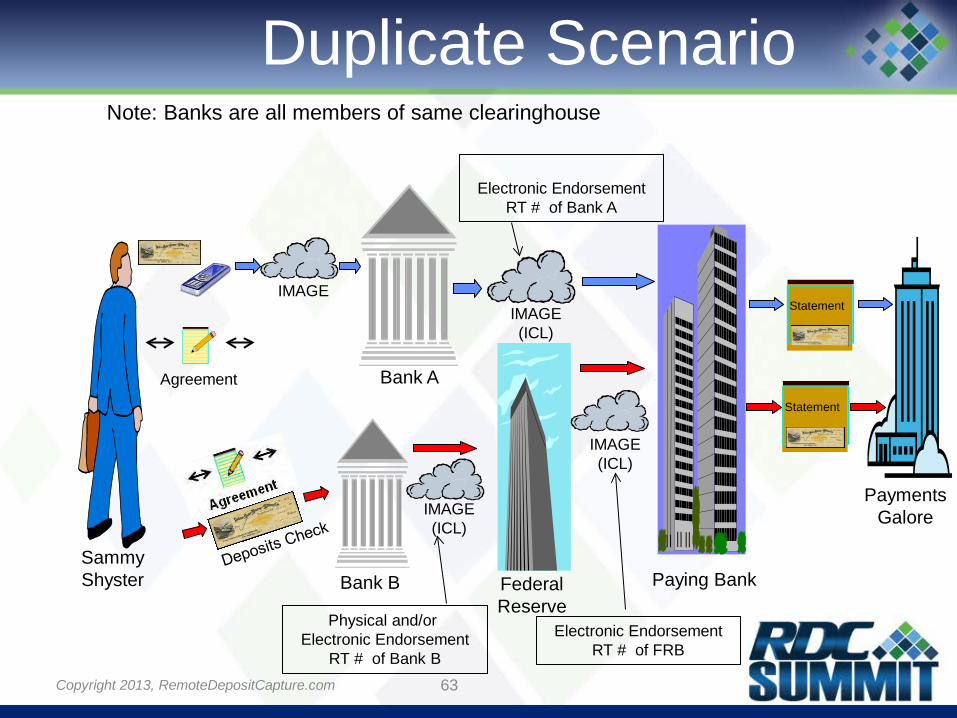

IMAGE

Bank A

Paying Bank

Agreement

Sammy Shyster

Payments Galore

Statement

Note: Banks are all members of same clearinghouse

Electronic Endorsement

RT # of Bank A

IMAGE (ICL)

IMAGE (ICL)

IMAGE (ICL)

Statement

Federal Reserve

Bank B

Physical and/or Electronic Endorsement

RT # of Bank B

Electronic Endorsement RT # of FRB

Duplicate Scenario

63 Copyright 2013, RemoteDepositCapture.com

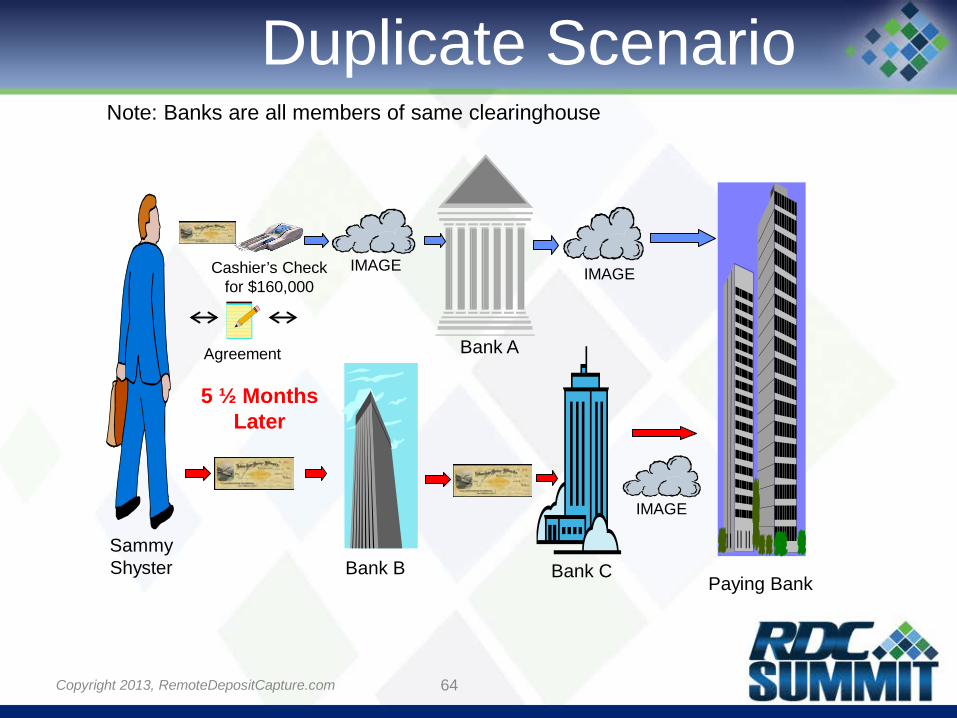

Cashier’s Check for $160,000

Bank A

Paying Bank

Sammy Shyster

IMAGE

Agreement

Bank B

5 ½ Months Later

IMAGE

Bank C

Duplicate Scenario Note: Banks are all members of same clearinghouse

64 Copyright 2013, RemoteDepositCapture.com

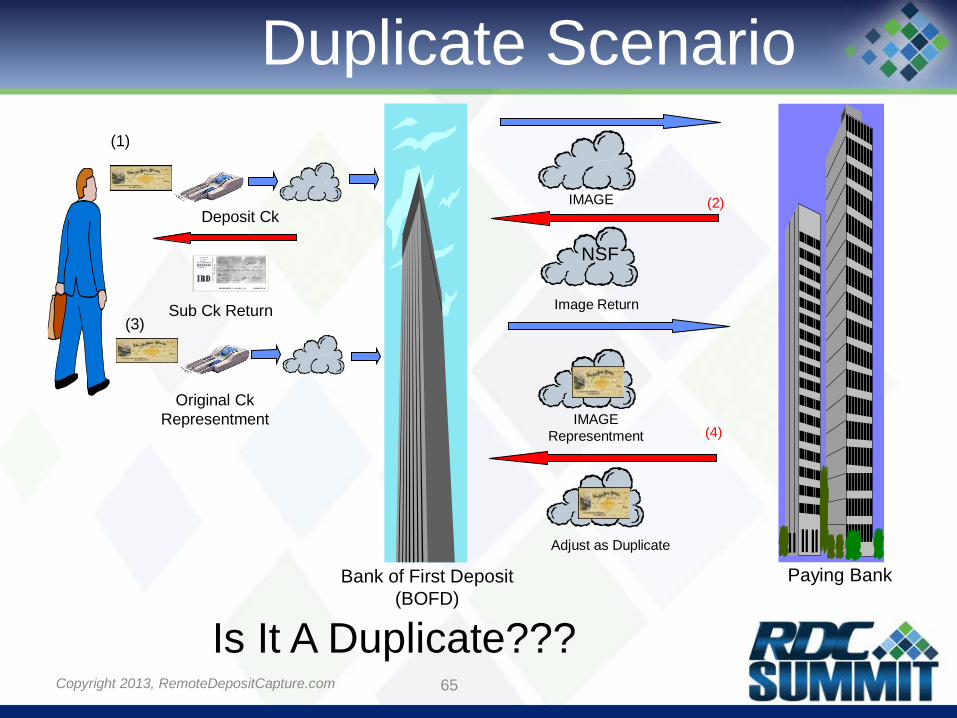

IMAGE

Paying Bank Bank of First Deposit (BOFD)

Sub Ck Return

Is It A Duplicate???

IMAGE

IMAGE Representment

Adjust as Duplicate

(4)

Image Return

(2)

NSF

Duplicate Scenario

Deposit Ck

(1)

Original Ck Representment

(3)

65 Copyright 2013, RemoteDepositCapture.com

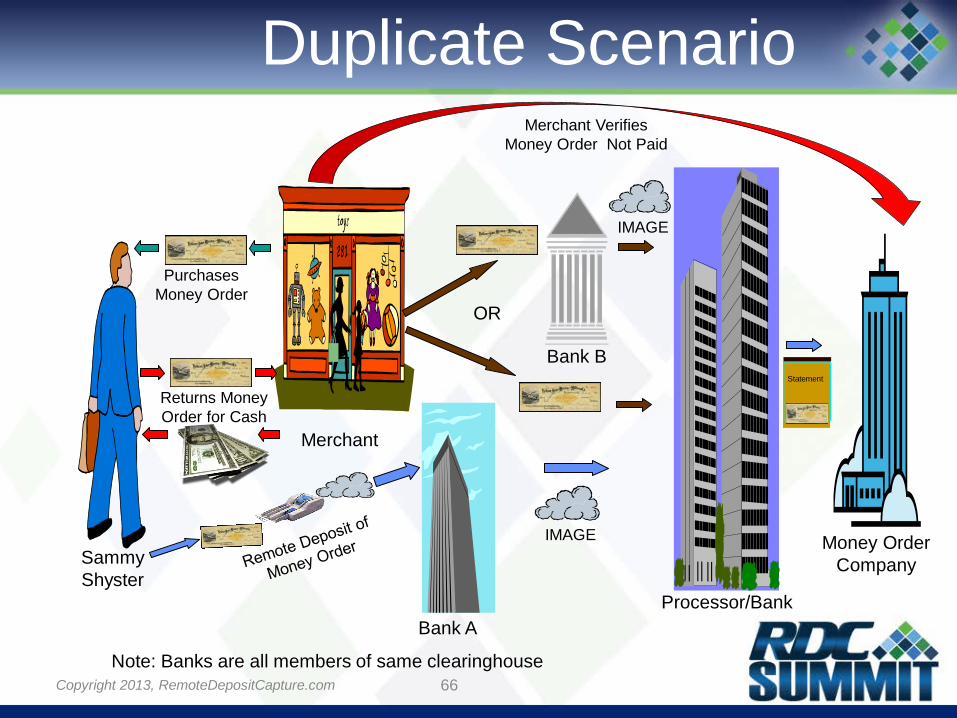

Merchant

Processor/Bank

Sammy Shyster

Money Order Company

Note: Banks are all members of same clearinghouse

Bank A

Purchases Money Order

Returns Money Order for Cash

Merchant Verifies Money Order Not Paid

Bank B

IMAGE

OR

Duplicate Scenario

IMAGE

Statement

66 Copyright 2013, RemoteDepositCapture.com

Questions?

67 Copyright 2013, RemoteDepositCapture.com

Additional Takeaways • For additional information please see the following

– Avoid Duplicates! • http://www.eccho.org/documents/Duplicates_000.pdf

– A Guideline Document on Duplicate Image/IRD Prevention and Detection • http://checkimagecentral.org/pdf/DuplicatePreventionAndDetection.pdf

– Resolving Duplicates as Adjustments versus Returns • http://checkimagecentral.org/pdf/ResolvingDuplicatesAsAdjustmentsVersusReturn

s.pdf – FIs offering RDC should review and implement FFIEC guidance on RDC

which addresses FI responsibility to identify and control risks • http://www.ffiec.gov/pdf/pr011409_rdc_guidance.pdf

– White Paper: Additional Issues Regarding Possible Duplicate Payment of Check items

• http://www.eccho.org/uploads/WhitePaperDuplicateIdentiticationVersion_08_05_2013(1).pdf

• http://www.eccho.org/uploads/HIDC%20White%20Paper%20(2)%20Aug%202013.pdf

68 Copyright 2013, RemoteDepositCapture.com

About The Presenters Phyllis Meyerson, AAP, CCM • ECCHO • Contact Info

– www.eccho.org – [email protected] – (214)273-3202

Ellen Heffner, NCP • ECCHO • Contact Info

– www.eccho.org – [email protected] – (214)273-3211

69 Copyright 2013, RemoteDepositCapture.com