Embed Size (px)

Citation preview

ELITE Basket Bond A unique investment opportunity linked to a portfolio of Italian ELITE

Companies.

In partnership with:

Milan, 11 January 2018

ELITE CLUB DEAL

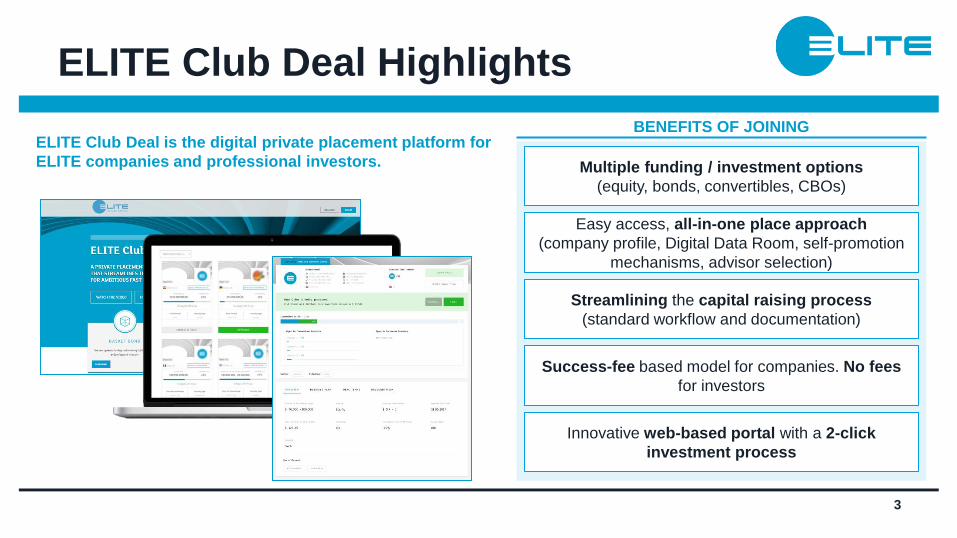

ELITE Club Deal Highlights

3

Easy access, all-in-one place approach

(company profile, Digital Data Room, self-promotion

mechanisms, advisor selection)

Multiple funding / investment options

(equity, bonds, convertibles, CBOs)

Streamlining the capital raising process

(standard workflow and documentation)

Success-fee based model for companies. No fees

for investors

Innovative web-based portal with a 2-click

investment process

BENEFITS OF JOINING ELITE Club Deal is the digital private placement platform for

ELITE companies and professional investors.

4

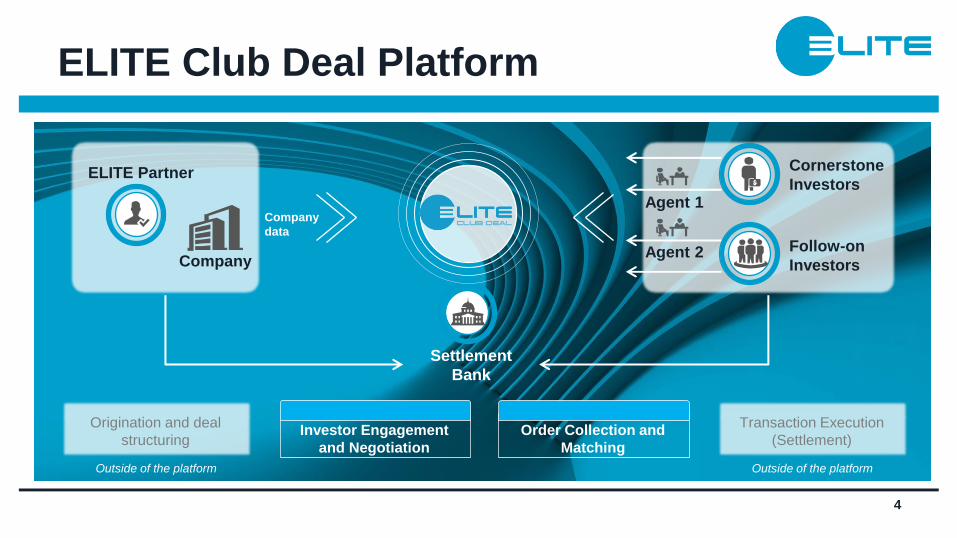

ELITE Club Deal Platform

Company

ELITE Partner

Company

data

Cornerstone

Investors

Follow-on

Investors

Agent 1

Agent 2

Settlement

Bank

Outside of the platform

Origination and deal

structuring Investor Engagement

and Negotiation

Order Collection and

Matching

Outside of the platform

Transaction Execution

(Settlement)

ELITE Basket Bond I

6

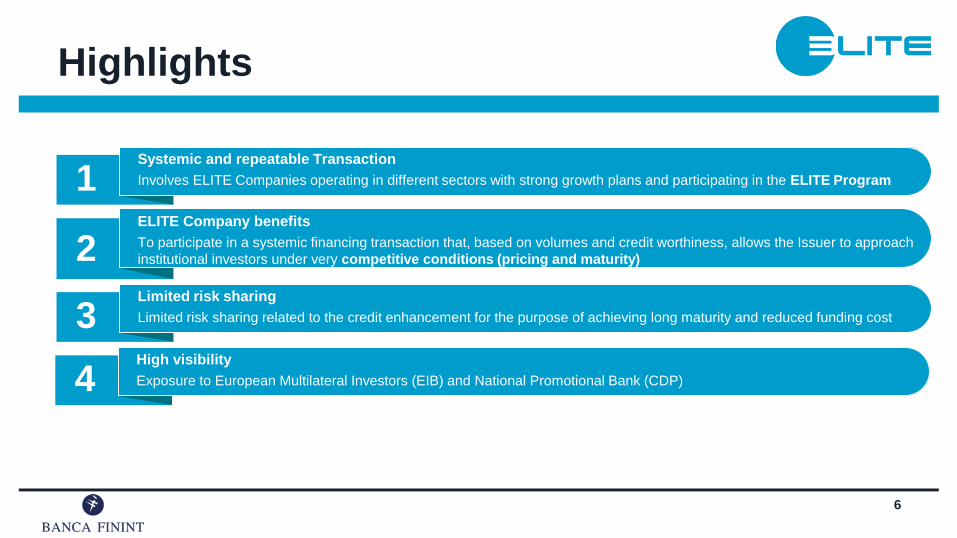

Highlights

1 Systemic and repeatable Transaction

Involves ELITE Companies operating in different sectors with strong growth plans and participating in the ELITE Program

2 ELITE Company benefits

To participate in a systemic financing transaction that, based on volumes and credit worthiness, allows the Issuer to approach

institutional investors under very competitive conditions (pricing and maturity)

3 Limited risk sharing

Limited risk sharing related to the credit enhancement for the purpose of achieving long maturity and reduced funding cost

Alignment of interest among the issuers

Risk sharing among the Issuers on the Credit Enhancement in case of non-payment or default under the bond(s)

4 High visibility

Exposure to European Multilateral Investors (EIB) and National Promotional Bank (CDP)

7

Transaction snapshot

1. Each ELITE companies (Issuers) issues a bond with same characteristics (amortisation shape, interest rate, etc.)

2. Bonds are used as collateral for the Notes relocated through the ELITE CLUB DEAL platform to Professional

Investors

1. Issuers: ELITE Companies

2. Investors: Institutional / Professional Investors

3. Arranger & Placement (issuance and structure): Banca Finint

4. Credit Enhancers: ELITE Companies

Phases

Players

ELITE Companies Professional

Investors

Bonds SPV

Notes

The ELITE Basket Bond offering is a unique way of providing debt financing to ELITE companies.

A group of ELITE companies each issue a bond with the same characteristics among themselves (other than covenants and

amounts). These individual bonds are then subscribed by a Special Purpose Vehicle (SPV). The SPV then issues an asset

backed security through the ELITE Club Deal: a private placement platform which interlinks companies and investors.

8

ELITE Basket Bond I

Amount raised: €122 Mln

Closing Date: 12th December 2017

Credit Enhancement: €18,3Mln

(15% of issued amount)

SPV Bonds issuance Notes

Other Professional Investor

CORNERSTONE INVESTOR

European Investment Bank

Other Lead Investor

Cassa Depositi e Prestiti

7 REGIONS

€1bn AGGREGATE

REVENUE

4.000+ EMPLOYEES

10 SECTORS

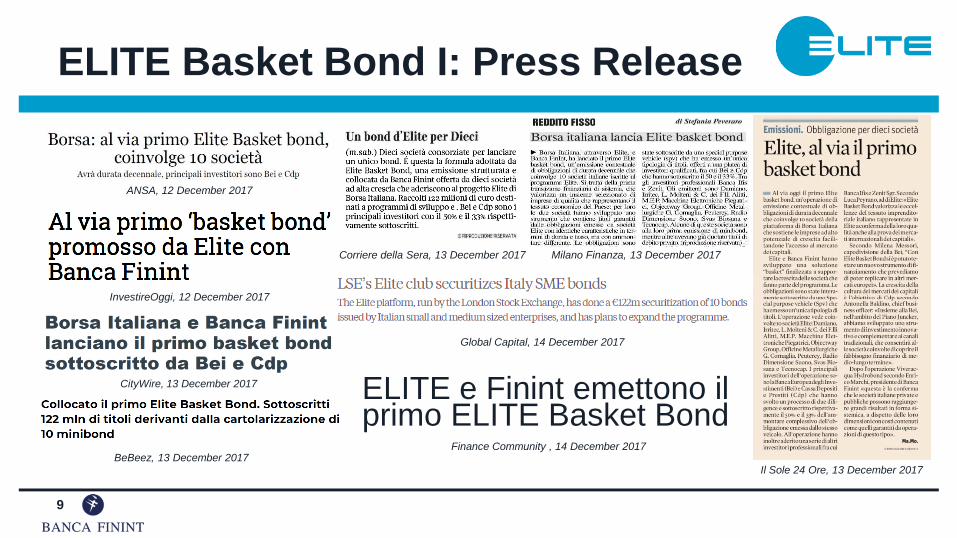

ANSA, 12 December 2017

InvestireOggi, 12 December 2017

Il Sole 24 Ore, 13 December 2017

CityWire, 13 December 2017

BeBeez, 13 December 2017

Corriere della Sera, 13 December 2017 Milano Finanza, 13 December 2017

Global Capital, 14 December 2017

ELITE Basket Bond I: Press Release

9

ELITE e Finint emettono il primo ELITE Basket Bond

Finance Community , 14 December 2017

ELITE Basket Bond I - Re opening

11

Transaction structure

New Issuer 1

New Issuer 2

New Issuer 3

New Issuer n

SPV

Credit

Enhancement

Issuance of Bonds

Remuneration and

repayment of Bonds

Excess C.E. restitution

Credit Enhancement

Services

Noteholders

Issuance

of Notes

Subscription Price

Interest and principal on the Notes

Liquidity and credit support on the notes

Representative of

the Noteholders

Subscription Price

Bonds (Phase 1)

Servicer Calculation Agent

Corporate Servicer

Agent Bank

New Series of Notes (Phase 2)

12

The Credit Enhancement in pills

• The Credit Enhancement is injected in the

structure by each Issuer as at the closing date

out of the proceeds of the Bond issuance, the

Credit Enhancement will be up to a maximum

percentage of 15% of the issued amount of

each Bond

• Credit Enhancement represents a long term

credit of the Issuers towards the SPV, and it

will be semi annually (as at any interest payment

date on the bonds) remunerated

• The Credit Enhancement starts to be

reimbursed by the SPV once the Bonds /

Notes have amortized by 50%

• The Credit Enhancement will be available in a

mutualized form among the New and Existing

Issuers which will then guarantee themselves

within the maximum limit of the available Credit

Enhancement

• The SPV will use the whole Credit Enhancement to cover any shortfall

of interest and principal on the issued Bonds (new and existing)

• In case one or more default of the New and Existing Issuers occurs,

the SPV will first use the portion of Credit Enhancement provided by

the defaulting Issuer and, if this is not sufficient to cover the default,

proquota the Credit Enhancement provided by the performing Issuers

Each Issuer does not risk anything more than its Credit

Enhancement

13

Bond Characteristics (Phase 1)

Characteristics Description

Transaction Amount • Amount of bonds different among the issuers, with the largest amount not exceeding [10%]

of the transaction amount and in any case not exceeding the Credit Enhancement

Maturity • Roughly 9.5 years

Interest Rate and

Amortisation • Fixed Interested rate (pre-amortization period of roughly 1.5 year, then amortising)

Issue Price • 100 % of the amount issued

Other • Bond issued are classified as senior unsecured debt of the Issuers

14

Notes Characteristics (Phase 2)

Characteristics Description

Transaction Amount • The amount will be equal to the sum of the principal amount under the issued Bonds (new

and existing)

Legal Maturity • In line with the series of Notes issued in respect of the Existing Bonds

Interest Rate and

Amortisation • Fixed Interested rate (pre-amortization period of roughly 1.5 year, then amortising)

Issue Price • 100 % of the amount issued

Other • Notes are limited recourse obligations of the SPV

15

Transaction costs (all-in cost)

As of today we estimate a Bonds with an ultimate interest rate of less than 4%* (“Ultimate Interest Rate”) which is

derived from the weighted average interest rates required on the Notes by different investors;

The precise rate will depend largely on the market conditions at the time in which the transaction closes and the

average credit worthiness of the participants;

The Ultimate Interest Rate includes upfront costs (lawyers fee, structuring fee, placement agent fee, ECD platform fee,

etc..) to be paid on the Bond’s issue date by the Issuer equal to 3% of the Bond issued which are to be distributed

during the transaction life (approximatively 9.5 years) – although payable upfront

*The above rate exclude the rating agency’s assignment and maintenance fees (IF requested by the investors)

for the Issuer’s rating: maximum Euro [15.000] for the assignment and maximum Euro [10.000] for the rating

maintenance per year. It also excludes other minor costs (such as notary, paying agent, etc..)

16

Company Eligibility Criteria

• Above €45M Turnover

• Last 3 years’ audited financial statements Financial

Statements

• Unlisted companies and no micro-enterprises [to be rated if requested by investors] Issuers

Ob

jecti

ve

Re

qu

ire

me

nts

• Good Standing (not subject to legal proceedings) Standing

• No start-up companies or turnaround Exclusion

Qu

ali

tati

ve

Re

qu

ire

me

nts

Use of Proceeds

• New investments (tangible or intangible assets)

• Working capital needs

For more information see the relevant slide

Financials Ratios

& Other

Covenants /

Undertakings

Qu

an

tita

tive

Re

qu

ire-

me

nts

Sectors • All sectors normally identified under international transactions completed with Multilateral

Organization and or NPBs (e.g. gambling, weapon production and selling…)

• Financial covenants:

Leverage Ratio: Total Net Debt / EBITDA

Interest Cover Ratio: EBITDA / Gross Interest

Gearing Ratio: Total Net Debt / Equity

Other undertakings may be disciplined, such as:

Max dividends distribution, below certain levels of the

Gearing Ratio

Max financial debt at subsidiaries level (unless the

subsidiaries guarantee the bond);

Others

17

Focus on Use of Proceeds

The following investment categories are eligible according to investors (in particular European Investment Bank)

requirements

Ultimately investments shall be completed within 3 years from the issue date and be at least equal to the bond issued

amount

Proceeds from the bond can be used for any corporate need (including refinancing of existing financial debts and

acquisitions of new activities)

• Investments via purchase (also through leasing), restructuring or enlargement of tangible assets, including related research

& development costs; purchase of assets different from real estate assets with the aim of renting them to third parties;

• Intangible assets: R&D costs (including the salaries of employees directly involved in R&D activities and the costs of

licenses, trade mark, industrial patent, etc..); purchase (also through leasing) of process licences, software and other similar

assets;

• Working capital: the average inventories and receivables (along with the other two items above) across the three years

period above shall be above the issued bond amount

18

Indicative Timetable

THE TIMING LARGELLY DEPEND ON THE NUMBER OF CORPORATES WHICH WILL PARTECIPATE TO THE EBB II AND AVAILABILITY OF THE VARIOUS

PARTIES SUCH AS RATING AGENCY AND INVESTORS

8 15 22 29 5 12 19 26 5 12 19 26 2 9 16 23 30 7 14 21 28

ATTIVITA' PROPEDEUTICHE

Presentazione dell'Operazione e manifestazione d'interesse delle società

Mandati alle principali parti coinvolte (legale emittenti, legale Arranger, [Issuer's Rating Agency])

LATO SOCIETA' *

Analisi statuti e documenti societari

Eventuali modifiche statutarie e/o forma giuridica societaria

Analisi contratti di finanziamento, covenants e derivati esistenti

Analisi della situazione economico finanziaria

Piano di Investimento

Revisione documentazione dell'operazione

Delibere assembleari e/o CDA

Processo di rating (se richiesto)

STRUTTURAZIONE DELL'OPERAZIONE

Fase di strutturazione dell'operazione

* In talune di queste attività le società emittenti potranno essere supportate dall'Arranger / Legale Emittenti secondo quanto previsto nel memorandum allegato al Mandato

Gennaio Febbraio Marzo Aprile Maggio

ELITE Basket Bond - Issuer Transaction Documents

20

Issuer Transaction Documents

Each Issuer, in order to finalize the Transaction, will sign the following main documents:

• “Contratto di Sottoscrizione dei Bond”, a separate agreement between, inter alia, each Issuer and the SPV, where

the SPV undertakes to subscribe the Bond and pay the relevant subscription price. Such document will contain the

Terms and Conditions od the Bond

• “Pegno Irregolare”, a separate agreement between each Issuer and the SPV, which describe the creation, purpose,

enforcement, replenishment and release of the Credit Enhancement

• “Accordo tra Creditori del Credit Enhancement”, an agreement between, inter alia, the Issuers and the SPV, which

describe the funding of the Credit Enhancement, the mechanism of using funds standing to the credit of the SPV

accounts, the replenishments of funds used, the remuneration of the Credit Enhancement;

• “Accordo Quadro”, an agreement between, inter alia, the Issuer and the European Investment Bank, which

describe the use of EIB funds (“Finanza BEI”) and discipline the retrocession of bps by the EIB to the Issuers

ELITE Trade

Receivables Bond - Preliminary Information

22

Introduction to ELITE Trade

Receivable Tool

ELITE identified a systemic solution to further support the growth of ELITE companies.

The innovative tool is represented by an Asset Backed Security collateralized by a set of underlying receivables sold

by the ELITE Companies.

Covering the ELITE Companies working capital funding need and sustain their industrial plans and

investments

Diversify the ELITE Companies’ financing sources

Creating a systemic and a standardized revolving financing facility

Pioneering a transaction involving Development Banks, Private/Sovereign investors and Institutional

Investors

Satisfying Investors’ appetite in SME’s and Mid Cap risk through a diversified portfolio

23

Highlights

Multi-Seller Platform Insolvency remote revolving sales of receivable portfolios originated by a pool of

companies. Flexibility to add new Sellers after the first closing

Risk Transfer Receivables sold on a non-recourse basis, which can help freeing up banking lines

and make it also compatible with other types of financing

Medium Term Duration Term of 5 years, renewable bi-annually or annually, providing funding certainty to

participants within a certain set of eligibility criteria for a pre-set amount

Standardised

Documentation

The portfolios will be sold under a standardised set of Transaction Documentation,

allowing for speedy renewals

Dynamic Discount Ongoing monitoring and reporting allow for a constant readjustment of the Seller

specific advance rates for each portfolio sale

Seller / Debtor

Relationship

The transfer of the portfolios will not interrupt the existing business relationship

between the Sellers and their clients. Debtors do not require to be notified of the sales

and the Sellers continue to service the sold portfolios

24

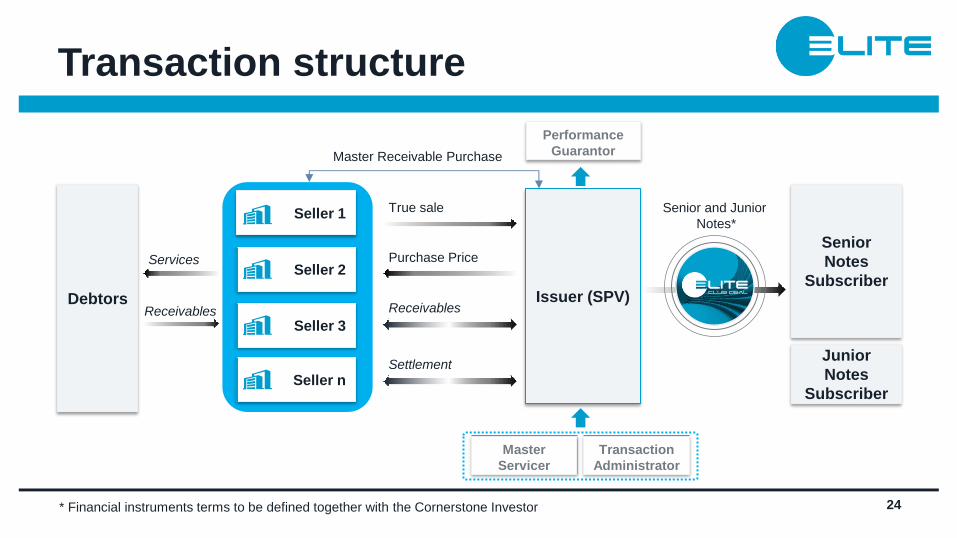

Transaction structure

Seller 2

Seller 3

Seller n

Seller 1 True sale

Receivables

Purchase Price

Master

Servicer

Transaction

Administrator

Senior

Notes

Subscriber

Junior

Notes

Subscriber

Senior and Junior

Notes*

Issuer (SPV)

Performance

Guarantor

Settlement

Master Receivable Purchase

Debtors Receivables

Services

* Financial instruments terms to be defined together with the Cornerstone Investor

25

Impact on Key Ratios

Participating in the transaction can achieve IFRS de-recognition for the Sellers and therefore have a positive impact on the key

financial ratios, and therefore also the adherence of potential covenants in other financing agreements

Debt Leverage (%)

(Total Debt / Equity)

Impact on Nominator Impact on Denominator Impact on Ratio

Debt / EBITDA (x)

Cash Flow (%)

(Funds from

Operations / Debt)

Cash Flow (%)

(Operating Cash

Flow / Debt)

Reduces Total Debt

Reduces Debt

Increases Operating Cash Flow

Reduces Debt to Equity Ratio

Reduces EBITDA1

1 Reduces EBITDA as a result of the Credit Discount

Reduces Debt

Reduces Debt

Reduces Debt / EBITDA Ratio

Increases Cash Flow

Increases Cash Flow

26

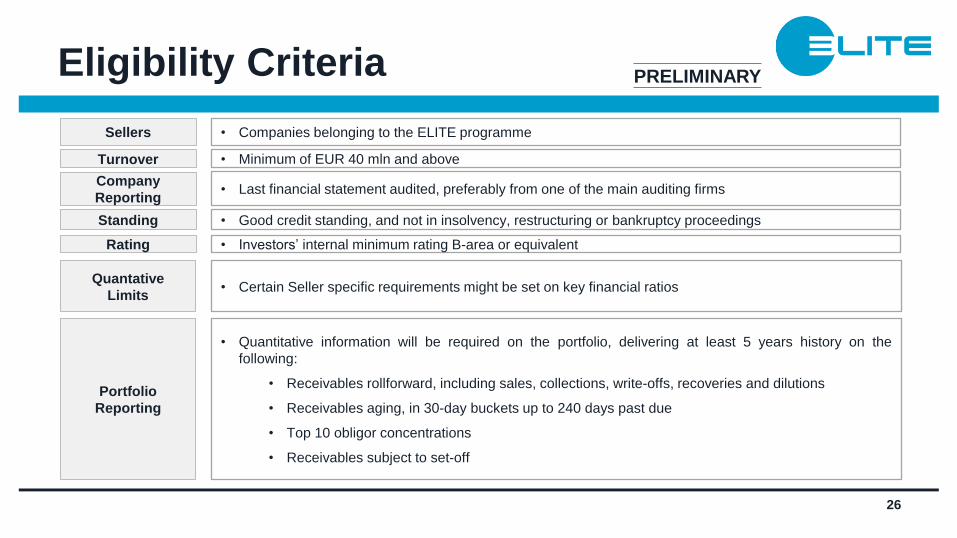

Eligibility Criteria

• Minimum of EUR 40 mln and above Turnover

• Last financial statement audited, preferably from one of the main auditing firms Company

Reporting

• Companies belonging to the ELITE programme Sellers

• Good credit standing, and not in insolvency, restructuring or bankruptcy proceedings Standing

• Investors’ internal minimum rating B-area or equivalent Rating

Quantative

Limits • Certain Seller specific requirements might be set on key financial ratios

Portfolio

Reporting

• Quantitative information will be required on the portfolio, delivering at least 5 years history on the

following:

• Receivables rollforward, including sales, collections, write-offs, recoveries and dilutions

• Receivables aging, in 30-day buckets up to 240 days past due

• Top 10 obligor concentrations

• Receivables subject to set-off

PRELIMINARY

CONTACT US

www.elite-clubdeal.com

@_ELITEGroup_

FOLLOW US

ELITE

ELITE Group

Contacts

Disclaimer

This publication contains text, data, graphics, photographs, illustrations, artwork, names, logos, trade marks, service marks and information (“Information”)

connected with London Stock Exchange Group (“LSEG”).

LSEG attempts to ensure Information is accurate, however Information is provided “AS IS” and on an “AS AVAILABLE” basis and may not be accurate or up to

date.

Information in this publication may or may not have been prepared by LSEG but is made available without responsibility on the part of LSEG.

LSEG does not guarantee the accuracy, timeliness, completeness, performance or fitness for a particular purpose of the publication or any of the Information.

No responsibility is accepted by or on behalf of LSEG for any errors, omissions, or inaccurate Information in this publication. No action should be taken or

omitted to be taken in reliance upon Information in this publication.

We accept no liability for the results of any action taken on the basis of the Information.

The publication of this document does not represent solicitation, by LSEG, of public saving and is not to be considered as a recommendation by LSEG as to the

suitability of the investment, if any, herein described.

This document is not to be considered complete and is meant for information and discussion purposes only.

LSEG accepts no liability, arising, without limitation to the generality of the foregoing, from inaccuracies and/or mistakes, for decisions and/or actions taken by

any party based on this document.

Elite Club Deal Limited is authorised and regulated by the Financial Conduct Authority

ELITE trademark and any other trademark owned by LSEG cannot be used without express written consent by LSEG having the ownership on the same.