Embed Size (px)

Citation preview

ELFA Best Practices Roundtable

Industry Update

Bill Phelan – President

Tom Ware – Senior Vice President

April 4, 2017

Sponsored by:1

National

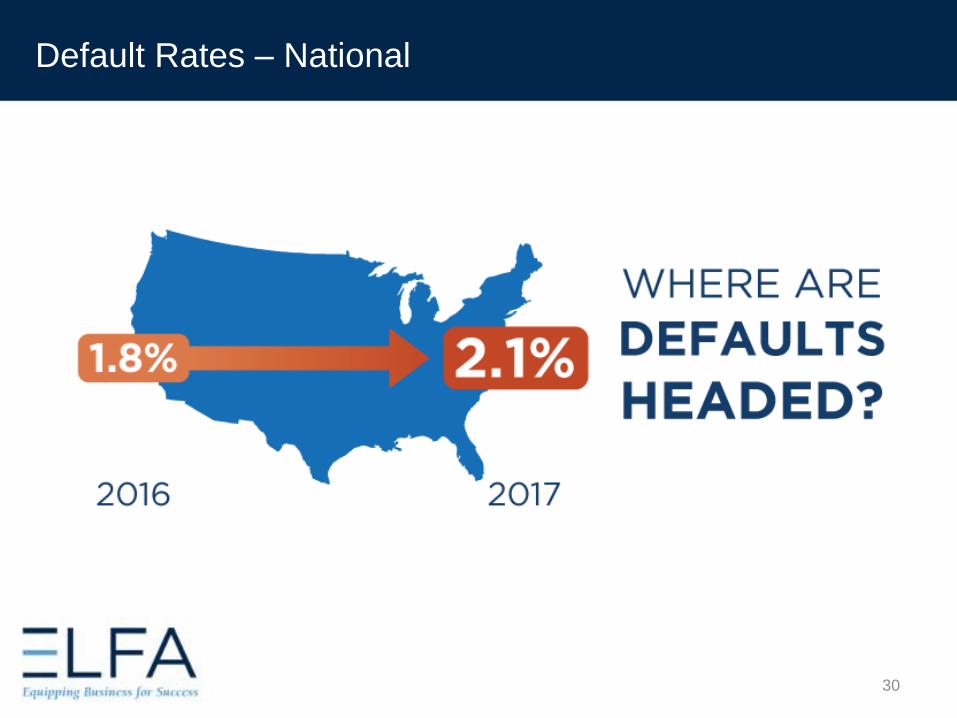

Activity

2

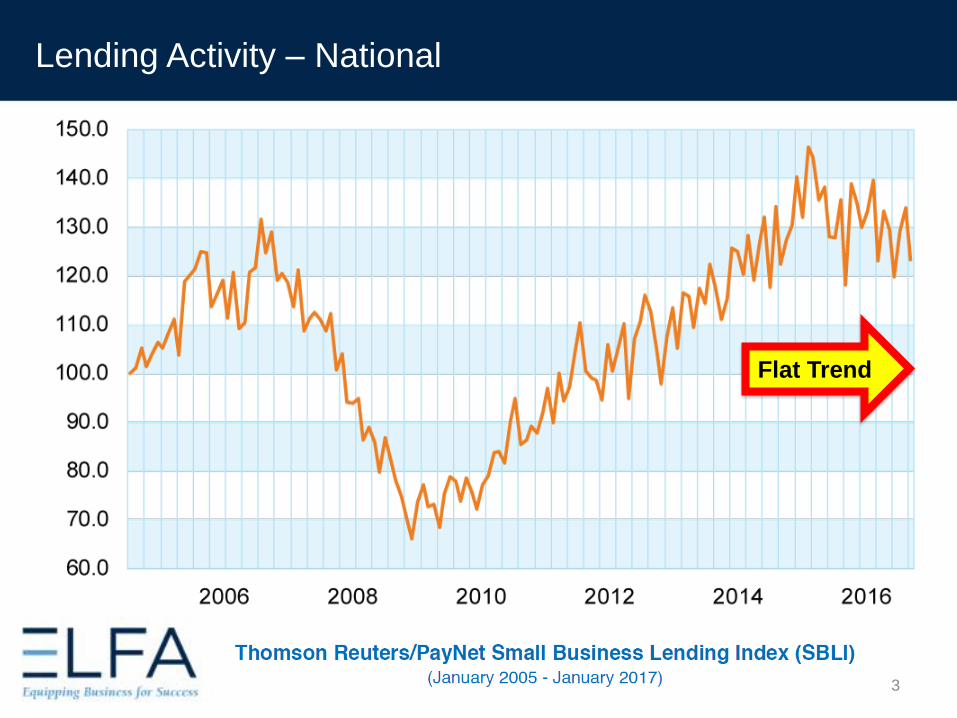

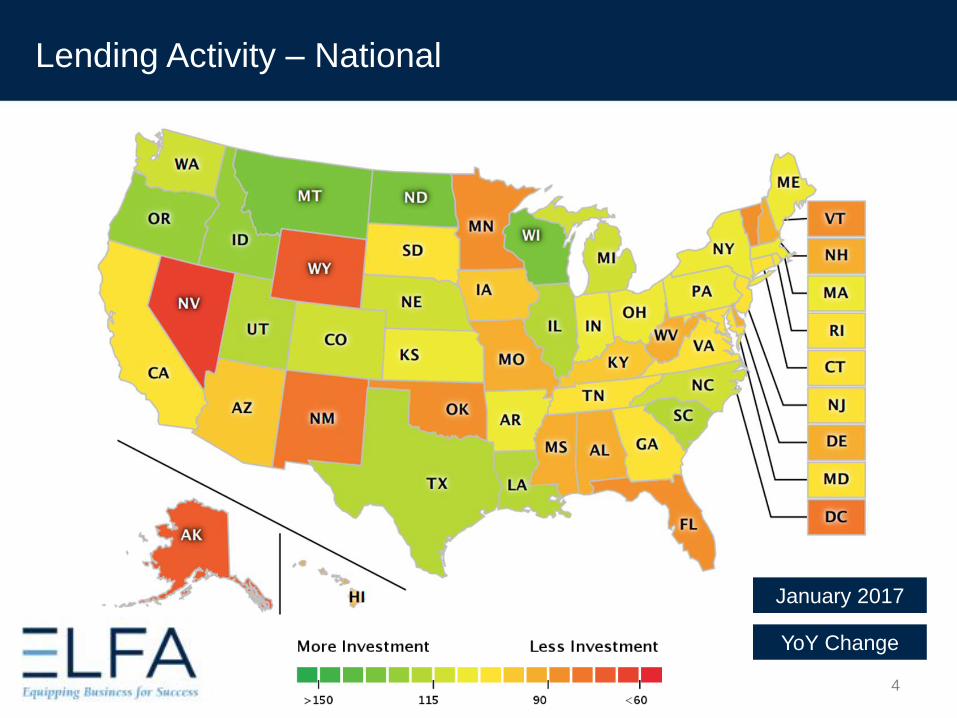

Lending Activity – National

Flat Trend

3

January 2017

YoY Change

Lending Activity – National

4

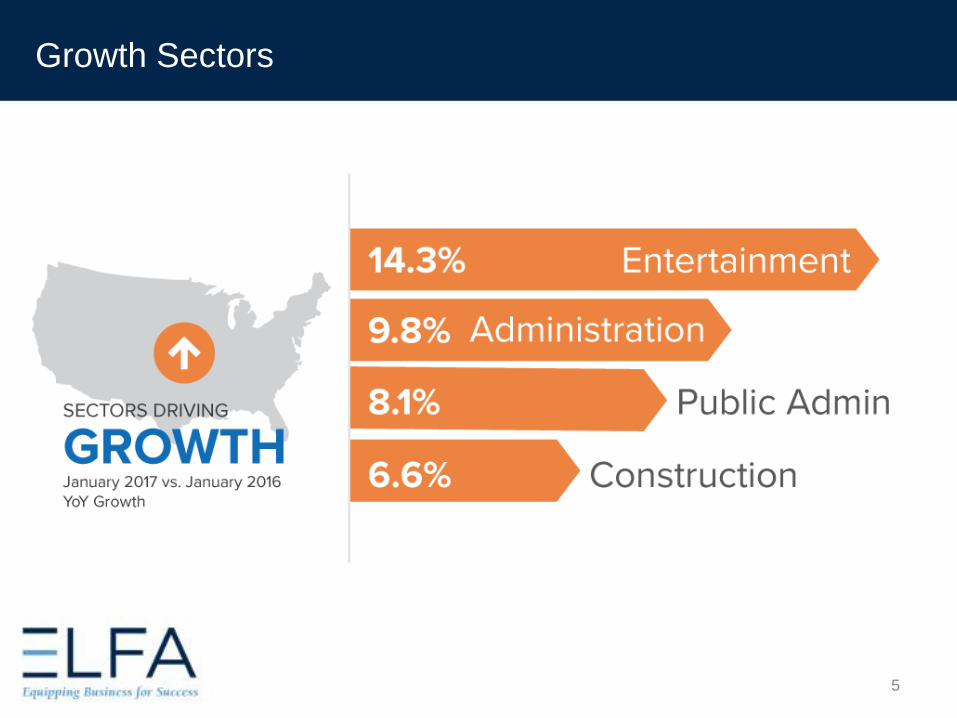

Growth Sectors

5

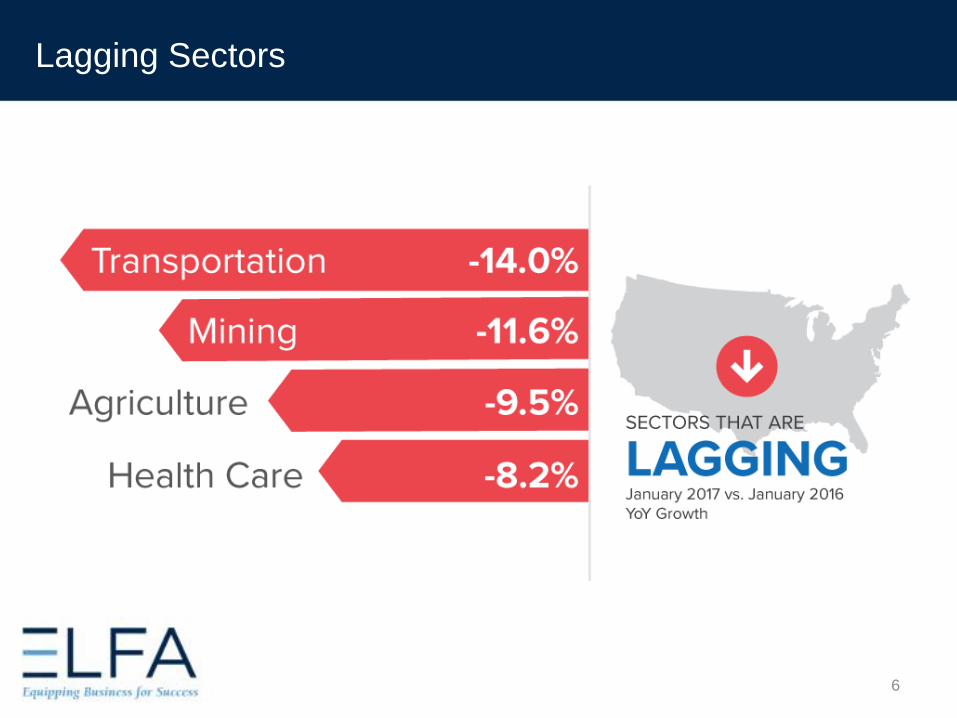

Lagging Sectors

6

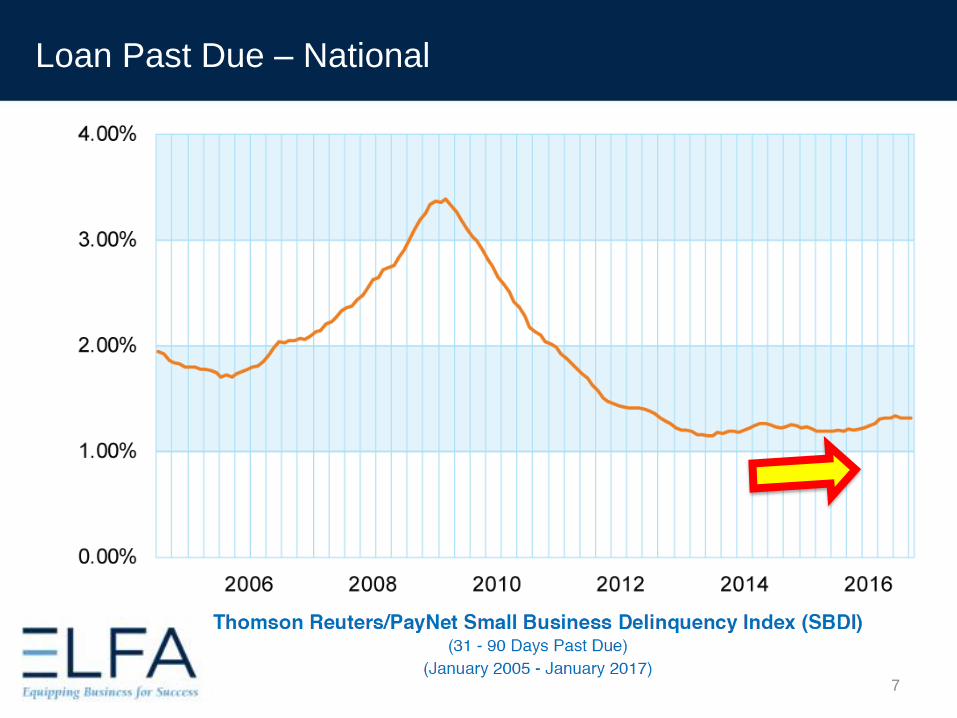

Loan Past Due – National

7

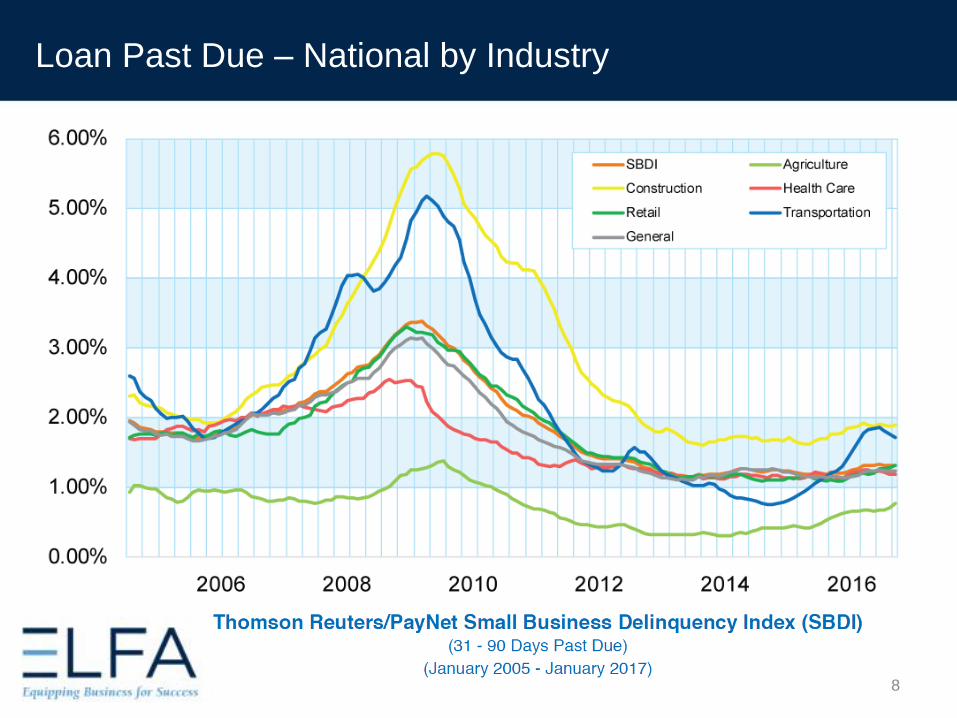

Loan Past Due – National by Industry

8

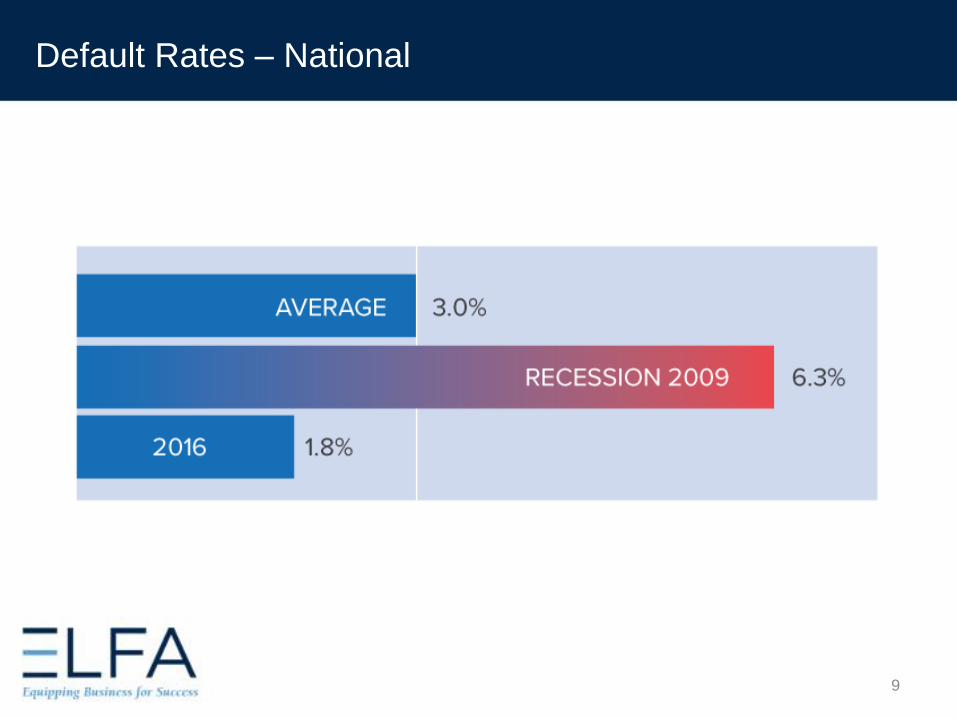

Default Rates – National

9

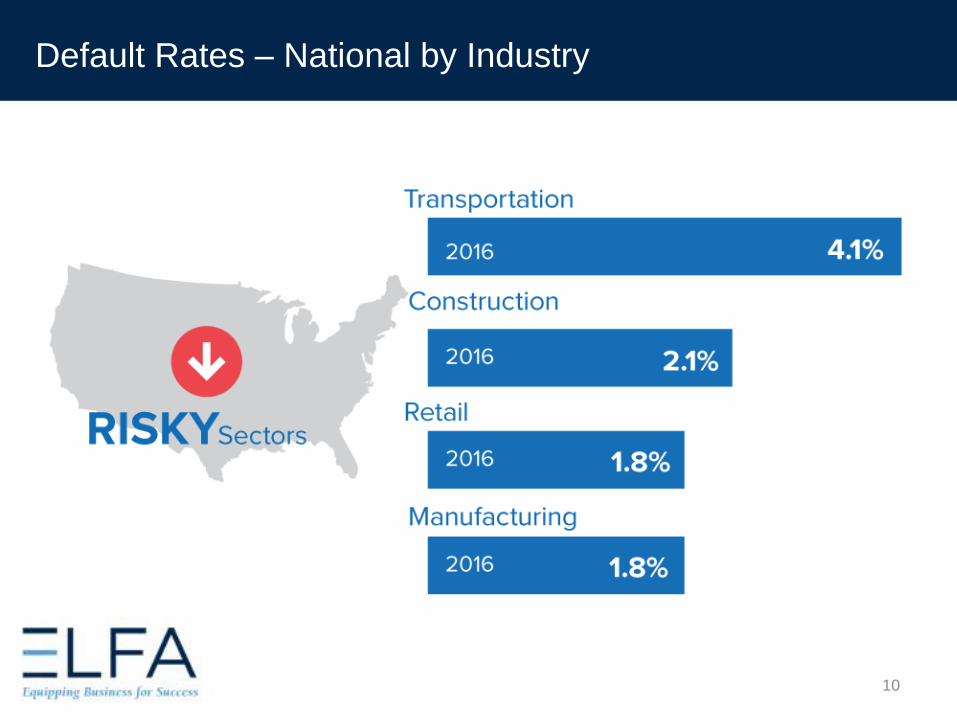

Default Rates – National by Industry

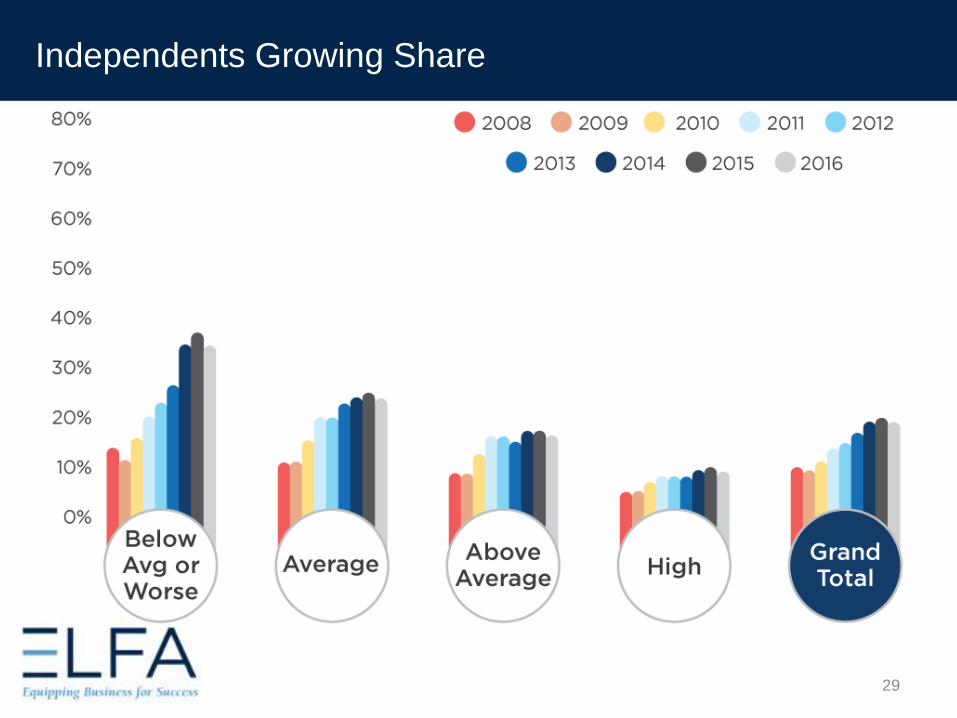

10

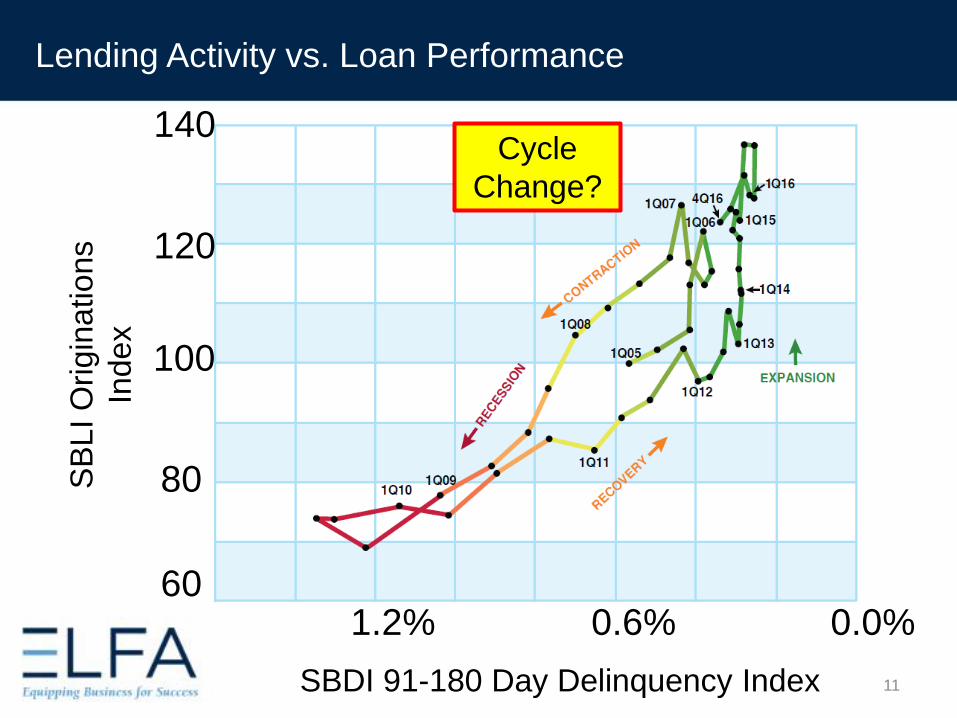

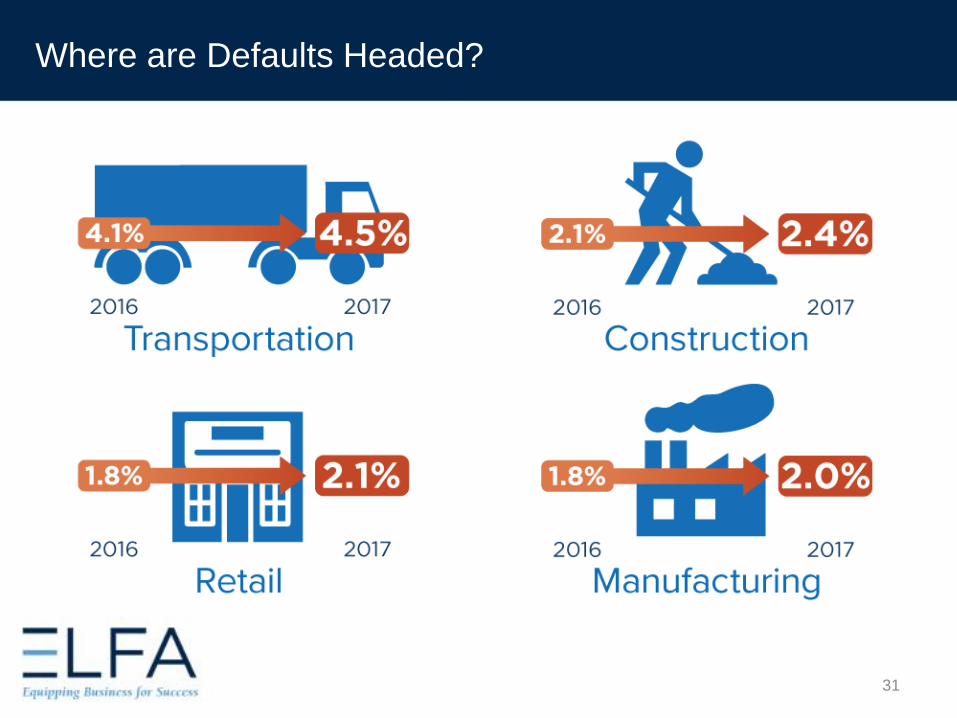

Lending Activity vs. Loan Performance

1.2% 0.6% 0.0%

SBDI 91-180 Day Delinquency Index

120

100

80SB

LI

Ori

gin

ations

Index

60

Cycle

Change?

140

11

Portfolio

Performance

12

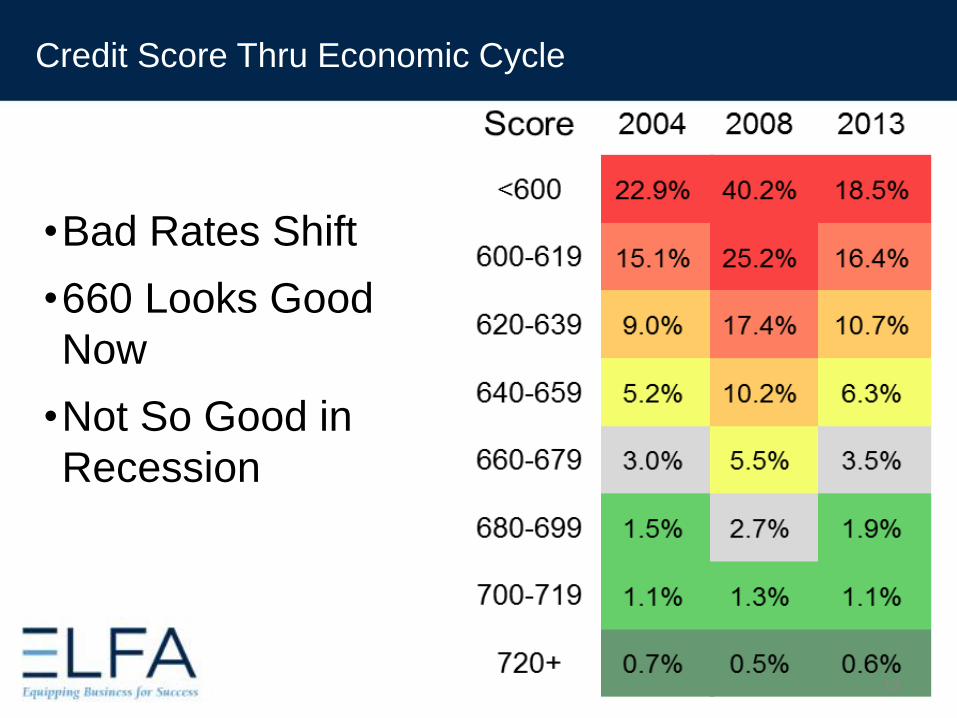

Credit Score Thru Economic Cycle

•Bad Rates Shift

•660 Looks Good

Now

•Not So Good in

Recession

13

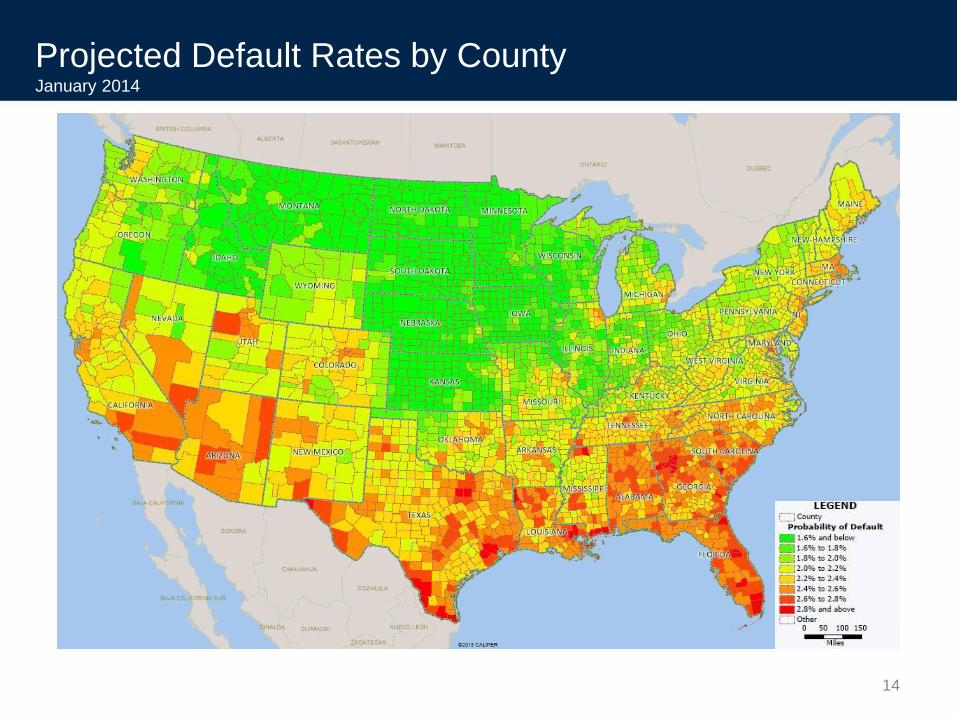

Projected Default Rates by CountyJanuary 2014

14

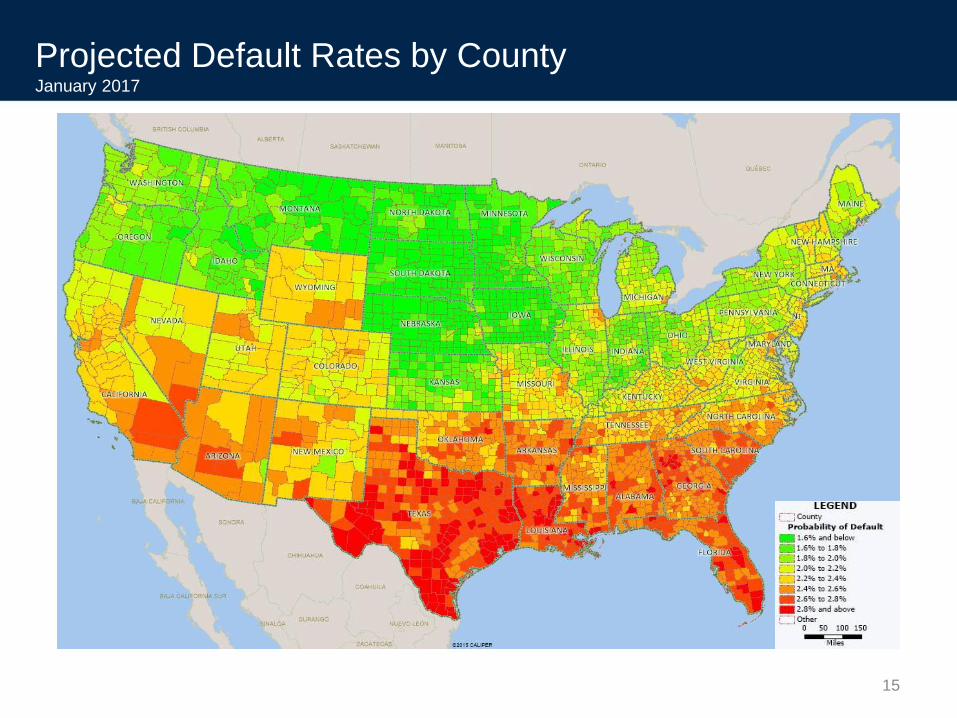

Projected Default Rates by CountyJanuary 2017

15

Changing

Regulation

16

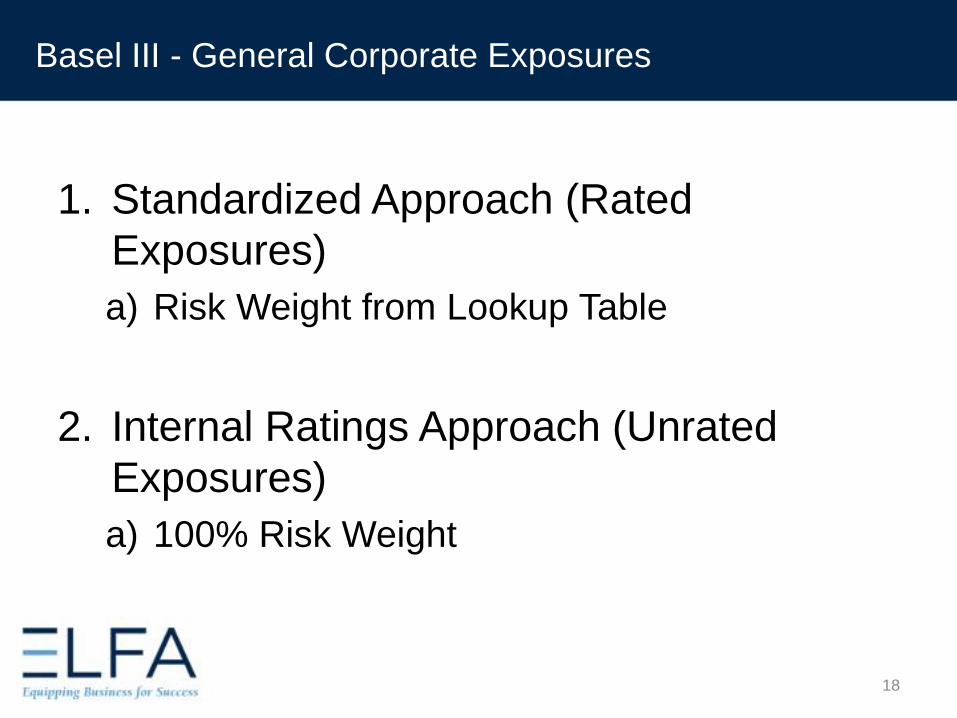

Basel III

17

1. Standardized Approach (Rated

Exposures)

a) Risk Weight from Lookup Table

2. Internal Ratings Approach (Unrated

Exposures)

a) 100% Risk Weight

18

Basel III - General Corporate Exposures

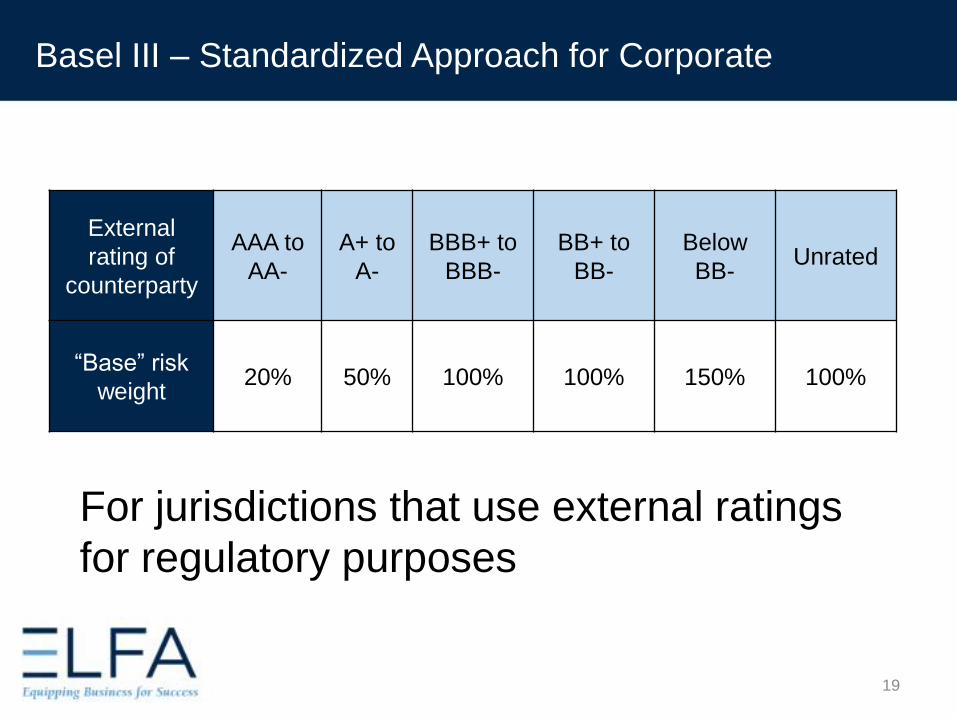

For jurisdictions that use external ratings

for regulatory purposes

19

External

rating of

counterparty

AAA to

AA-

A+ to

A-

BBB+ to

BBB-

BB+ to

BB-

Below

BB-Unrated

“Base” risk

weight20% 50% 100% 100% 150% 100%

Basel III – Standardized Approach for Corporate

Basel III – Small Medium Enterprises (SME’s)

• For Unrated Corporate SME’s

• 85% Risk Weight

• SME defined as sales <€50 million

20

• New FASB regulations• “Current and Expected Credit Loss” (CECL) will require

accounting for expected lifetime Losses

• PayNet now building models to predict lifetime Losses

(not just Defaults)

• Which requires:• Loss Given Default (LGD)

• Exposure at Default (EAD)

• Probability of Default (PD) – beyond two years

21

Expected Loss: Loss Given Default & Exposure at Default

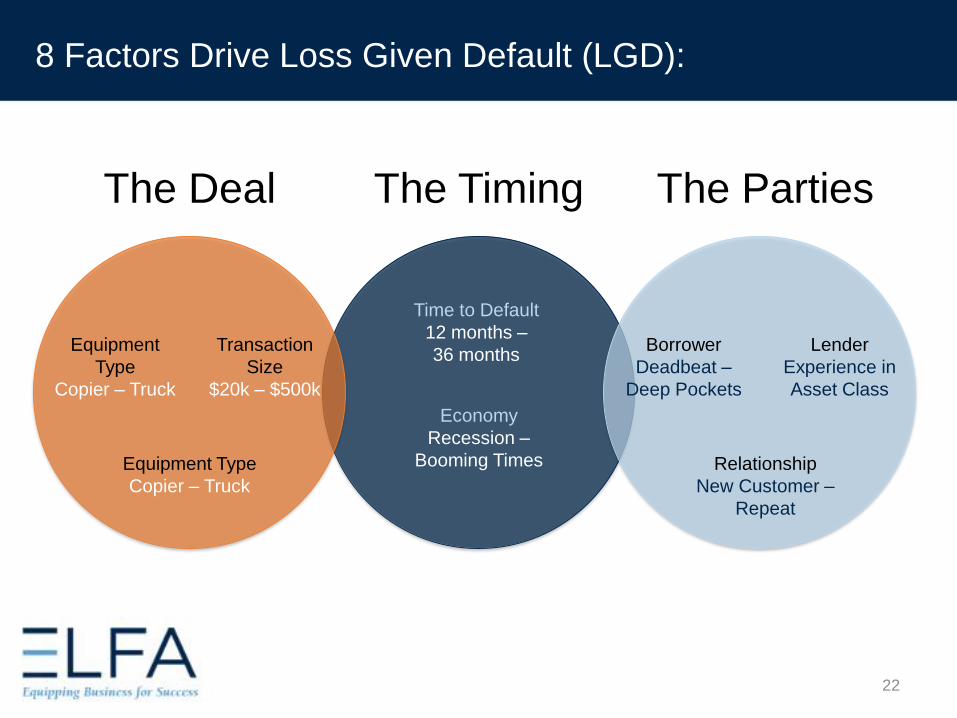

8 Factors Drive Loss Given Default (LGD):

22

The Deal The Timing The Parties

Equipment

Type

Copier – Truck

Equipment Type

Copier – Truck

Transaction

Size

$20k – $500k

Time to Default

12 months –

36 months

Economy

Recession –

Booming Times

Borrower

Deadbeat –

Deep Pockets

Relationship

New Customer –

Repeat

Lender

Experience in

Asset Class

Competitive

Environment

23

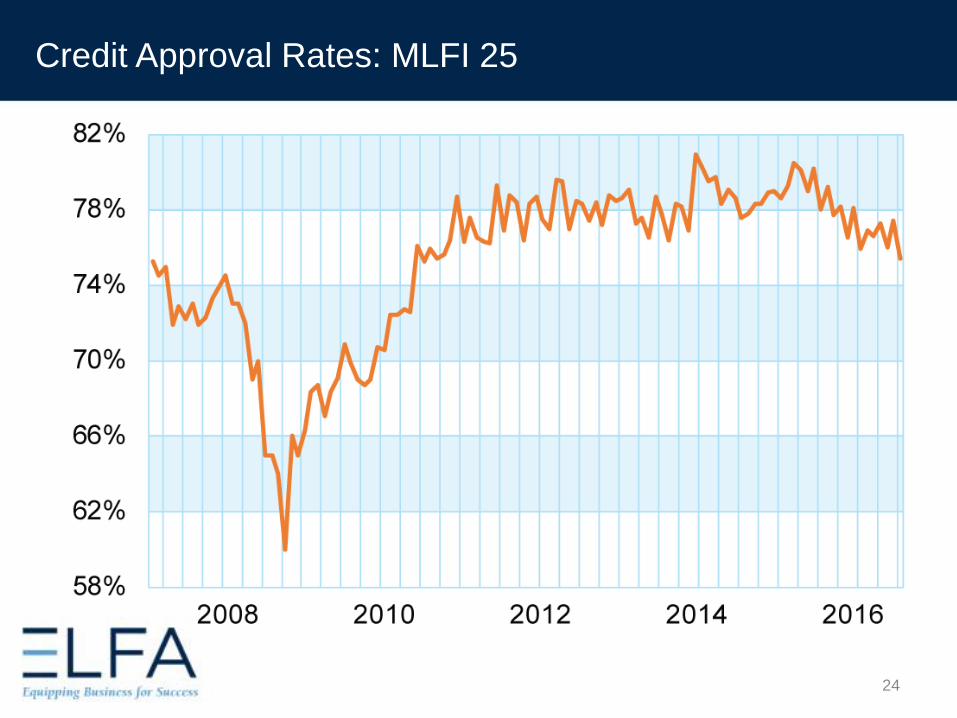

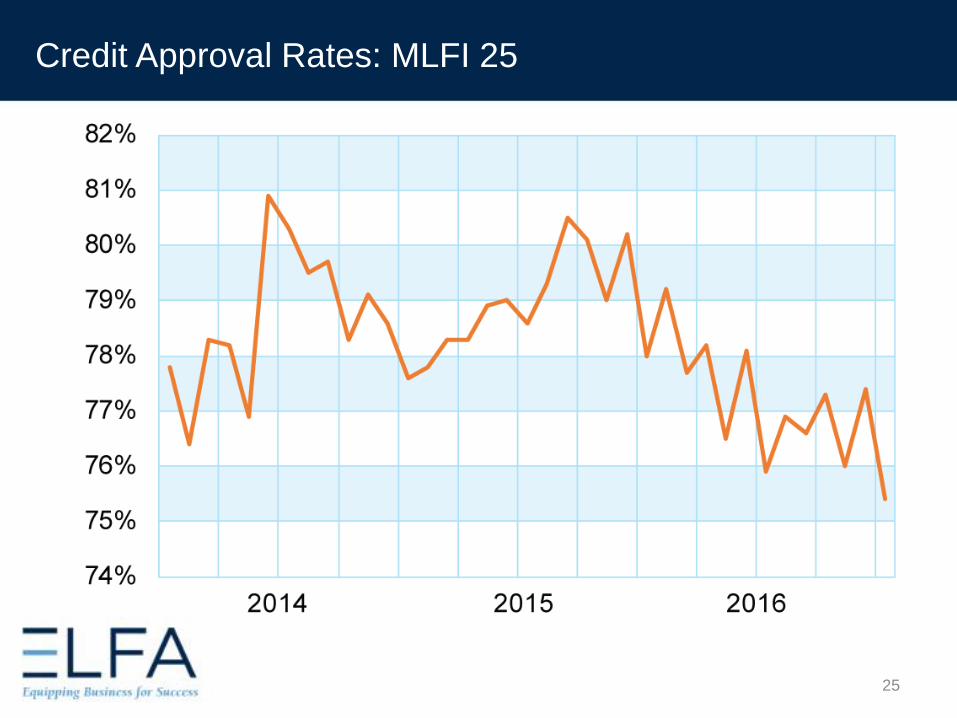

Credit Approval Rates: MLFI 25

24

Credit Approval Rates: MLFI 25

25

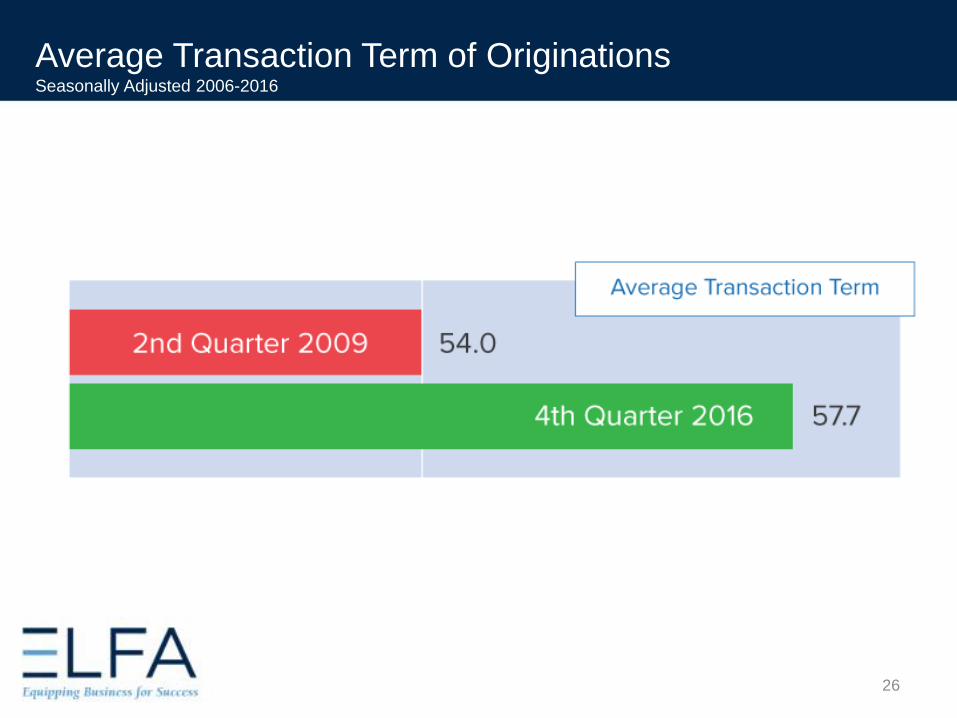

Average Transaction Term of OriginationsSeasonally Adjusted 2006-2016

26

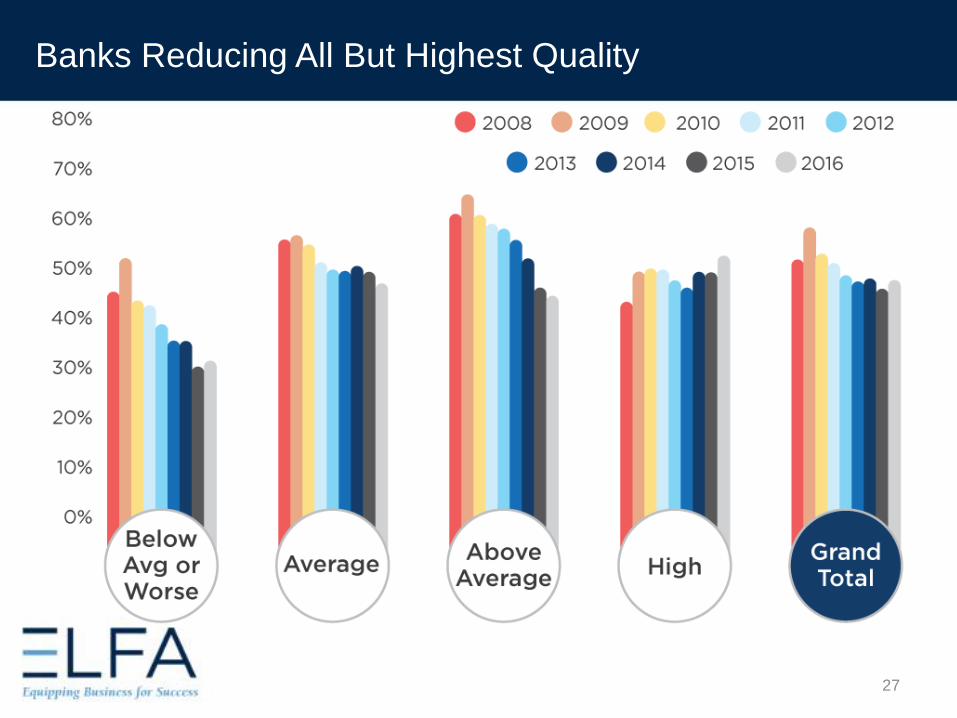

Banks Reducing All But Highest Quality

27

28

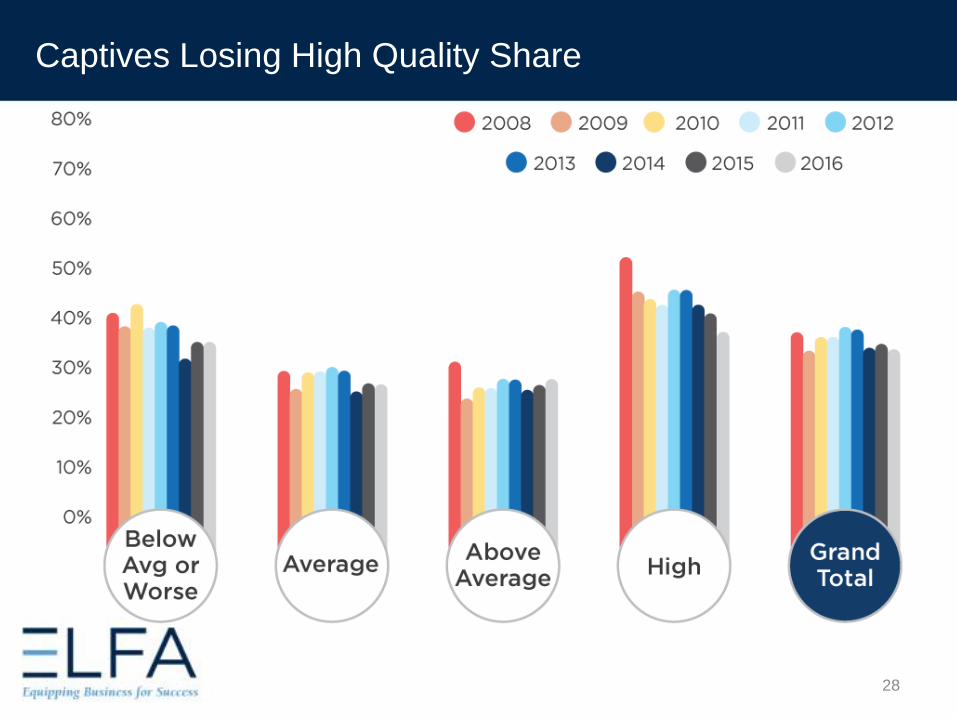

Captives Losing High Quality Share

Independents Growing Share

29

Default Rates – National

30

Where are Defaults Headed?

31

Thank

www.SBInsights.net

You

William Phelan ● Tom Ware

32