Embed Size (px)

Citation preview

© OECD/IEA 2012 © OECD/IEA 2012

Electricity markets Opening up to competition and investments

Lars Dittmar (TU Berlin), Dennis Volk & Matthew Wittenstein (IEA) IEA Energy Training Week

Paris, 11.04.14

© OECD/IEA 2012

© OECD/IEA 2012

Electricity is primarily a wealth creator

© OECD/IEA 2012

Asian power investment needs in good company

Power sector investments until 2035 (WEO/NPS)

16,867 bn USD 43% for grids

0

500

1,000

1,500

Generation Grids

bn

US

D

US

0

100

200

300

400

500

Generation Grids

bn

USD

Latin America

0

100

200

300

400

500

Generation Grids

bn

US

D

Africa

0

500

1,000

1,500

2,000

Generation Grids

bn

US

D

OECD Europe

2,500

3,000

3,500

4,000

Generation Grids

bn

US

D

Asia

0

200

400

600

800

Generation Grids

bn

US

D

OECD Asia Oceania

© OECD/IEA 2012

Many technologies available, which one to use?

0

20

40

60

80

100

120

140

160

180

200

Onshore Wind

Gas - OCGT Gas - CCGT Hard coal Nuclear Solar PV

USD

/MW

h

US - status quo

Investment Fuel O&M CO2 Decommissioning

-

2

4

6

8

10

12

14

16

-

20

40

60

80

100

120

140

160

Jan

-03

Jun

-03

No

v-0

3

Ap

r-0

4

Sep

-04

Feb

-05

Jul-

05

De

c-0

5

May

-06

Oct

-06

Mar

-07

Au

g-0

7

Jan

-08

Jun

-08

No

v-0

8

Ap

r-0

9

Sep

-09

Feb

-10

Jul-

10

De

c-1

0

May

-11

Oct

-11

Mar

-12

Au

g-1

2

Jan

-13

Jun

-13

Gas

pri

ce (

USD

/MB

tu)

Co

al p

rice

(U

SD/t

)

US Coal Appalachian (Monthly Average) Henry Hub (Monthly Average)

0

20

40

60

80

100

120

140

160

180

200

Onshore Wind

Gas - OCGT Gas - CCGT Hard coal Nuclear Solar PV

USD

/MW

h

US - status quo

Investment Fuel O&M CO2 Decommissioning

0

20

40

60

80

100

120

140

160

180

200

Onshore Wind

Gas - OCGT Gas - CCGT Hard coal Nuclear Solar PV

USD

/MW

h

US - high gas

Investment Fuel O&M CO2 Decommissioning

+ 15 USD/MWh

+ 10 USD/MWh

0

20

40

60

80

100

120

140

160

180

200

Onshore Wind

Gas - OCGT Gas - CCGT Hard coal Nuclear Solar PV

USD

/MW

h

EU - status quo

Investment Fuel O&M CO2 Decommissioning

+ 10 USD/MWh

+ 7 USD/MWh

0

20

40

60

80

100

120

140

160

180

200

Onshore Wind

Gas - OCGT Gas - CCGT Hard coal Nuclear Solar PV

USD

/MW

h

EU - low risk

Investment Fuel O&M CO2 Decommissioning

- 33 USD/MWh - 56 USD/MWh

- 71 USD/MWh

© OECD/IEA 2012

De-risking of generation assets

Economic

Construction Cost overruns

Time overruns

Market Inadequate prices or demand

Input cost increase

Operational Plant performance

Fuel unavailability

Macroeconomic

Significant change in exchange rates

Inflation

Interest rates

Political Regulatory

Price controls

Environmental obligations

Expropriation

Legal

Documentation and contract Terms

Validity

Jurisdictional

Choice of jurisdiction

Enforcement

Lack of dispute settlement

Force majeure

Natural disaster

Civil unrest

Strikes

© OECD/IEA 2012

De-risking of generation assets Regulated

Risk shifted to consumers Reduces or eliminates investment risks, but can lead to:

Overbuilding

“Gold-plating” – investing in more expensive technologies

Restructured Risk born by investor and third-parties

Some risks passed on in form of higher wholesale prices

Other risks can be shifted through financial/insurance products

Government interventions can reduce risk…

Guaranteed revenues through FiTs or CfDs

Loan guarantees

Market structures (e.g. capacity markets)

… or create risk

New environmental regulations

Policy uncertainty

© OECD/IEA 2012

Organisation of the electricity sector in liberalised markets

Regulated

The “markets” (different degrees of reliance apply)

© OECD/IEA 2012

Open markets and integrated system operations can deliver

Years in advance

Months in advance

Day ahead

Intraday

Real-time

Network operations

Electricity markets

Real time

Day ahead

Financial markets

Involvement of central operator

© OECD/IEA 2012

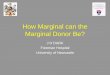

Open wholesale markets – Bids resulting in prices

Used for physical supply day-ahead and intra-day markets are used

Operational costs determines ranking order of individual plants, i.e. their competitiveness

Efficiency

Fuel costs

O & M

Price per MWh

© OECD/IEA 2012

Bids resulting in prices – operational costs count

Wholesale market (day-ahead and intra-day)

Coal @ 120 USD/t

39% efficiency

35 €/MWh

Coal plant Gas plant A - CCGT Gas plant B - OCGT

50 €/MWh

80 €/MWh

11 USD/MBtu 55%

11 USD/MBtu

35% efficiency

Ranking order: Coal, Gas A, Gas B

© OECD/IEA 2012

Wholesale markets – operation and investments

0

20

40

60

80

100

120

140

160

0 10 20 30 40 50 60 70 80 90 100 110 120

€/M

Wh

cumulated capacity (GW)

Hydro Nuclear Lignite Hard Coal Gas

Coal @ 120 USD/t

39% efficiency 35 €/MWh

Coal plant

Gas plant A - CCGT

Gas plant B - OCGT

Coal plant (35 €/MWh)

Gas A (50 €/MWh)

Gas B (80 €/MWh)

Minimal demand Max demand (average day)

Last required plant sets the market price: Marginal price @ 20 €/MWh

No

t d

isp

atch

ed

Marginal price @ 42 €/MWh

Coal plant „in the money“ (Infra-marginal rent: 42 – 35 €/MWh)

0

20

40

60

80

100

120

140

160

0 10 20 30 40 50 60 70 80 90 100 110 120

€/M

Wh

cumulated capacity (GW)

Hydro Nuclear Lignite Hard Coal Gas

Coal plant (35 €/MWh)

Gas A (50 €/MWh)

Gas B (80 €/MWh)

Peak demand (average year) Peak demand (1 in 10)

Scarcity conditions

Relevant first-order principle: • Getting the price(s) right during scarcity

• Marginal cost represents marginal service action

• Demand response (Value of Lost Load essential) • Price caps (Reliability target essential) • Co-ordination with other services (eg Balancing) • Locational differences (Underlying grid essential)

Absent perfect market conditions: Additional payments for capacity likely in the long run • PJM, NYISO, ISO NE, CAISO • ERCOT ? • UK • France • Germany?

Own set of challenges exist: • How much and which capacity? • Implications on other investments?

© OECD/IEA 2012

Q&A

Lars Dittmar | 14

Basic Characteristics of the Commodity Electricity

• Demand(t)=Supply(t): Electricity supply and

demand must be in a continuous physical balance

• Diurnal and seasonal fluctuations in demand

• Storing electricity is only to a minor degree

economically reasonable (Exception Hydro-thermal

systems such as Brazil, Colombia or Norway)

• Installed Capacity = Peak Demand + Reserve

Margin

• Short-term prices are determined according to

merit-order principles

Lars Dittmar | 15

0

10

20

30

40

50

60

70

80

Dem

an

d [

GW

]

Loads Highly Variable by Hour Day and Season

0

10

20

30

40

50

60

1 3 5 7 9 11 13 15 17 19 21 23

Lars Dittmar | 16

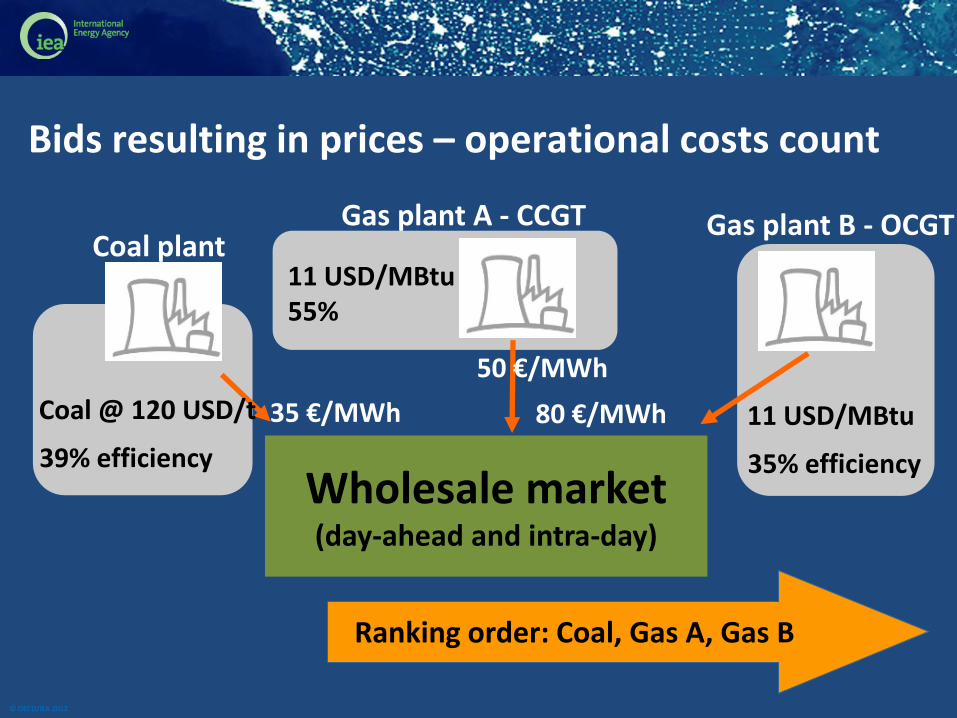

Hourly Generation of Electricity on 3rd Wednesdays in Germany 2011

-10

0

10

20

30

40

50

60

70

80

1 2 3 4 5 6 7 8 9 10 11 12

GW Solar

Wind

Charge P-Storage

Other

Discharge P-Storage

Hydro

Hydro RoR

Other Thermal

Nat. Gas

Oil

Hard Coal

Lignite

Nuclear

Source: Destatis, TSOs

Lars Dittmar | 17

Categories of costs in power production and their relevance to

Operation Decommissioning Expansion

Costs dependent on Capacity [USD/MWel]

Capital Costs P

Labor Costs P P

Fixed Operation & Maintenance P P

Costs dependent on operation [USD/MWhel]

Fuel costs P P P

Other variable costs (e.g. CO2) P P P

Lars Dittmar | 18

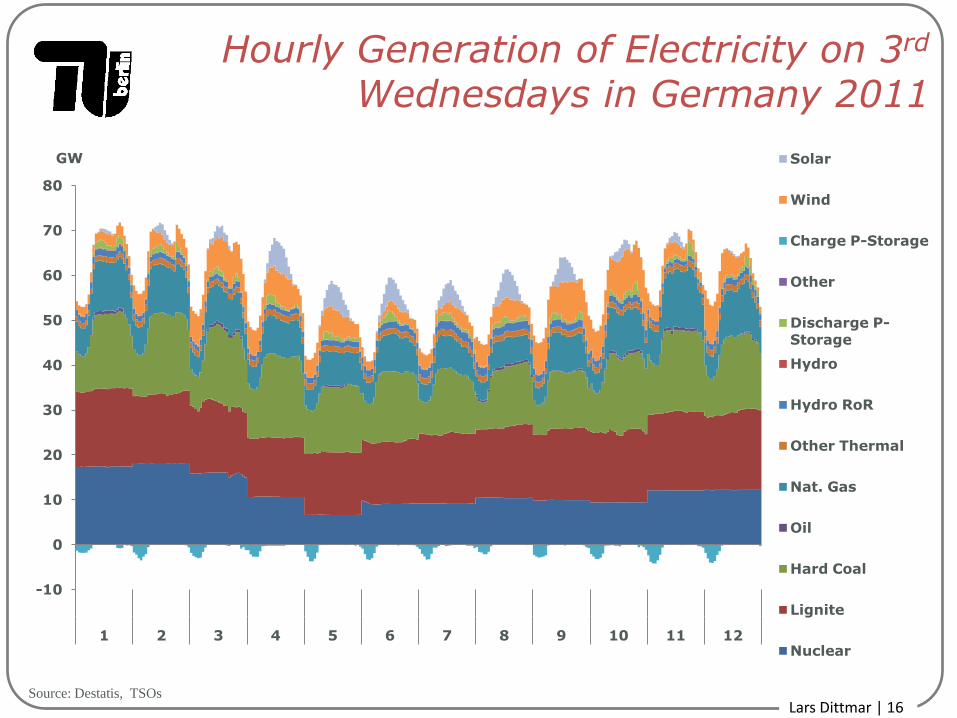

Dispatching Decision

The decision on Economic Dispatch is only based

on short-term marginal generation costs (STMC)

Dispatch if: Market price > STMC

I.e. power plants are dispatched if the contribution

margin is positive.

Lars Dittmar | 19

Short-term Marginal Generation Costs

Where:

G = Generation unit index

STMC(G) = Short-term marginal generation costs [USD/MWhel]

Fuel Price (G) = Fuel Price [USD/MWhtherm]

Eta(G) = Efficiency [-]

O&MVariable = Variable O&M costs [USD/MWhel]

EFCO2 = Emission factor CO2 [t CO2/MWhtherm]

PCO2 = CO2 [USD/tCO2]

2

2

Pr ( )( ) & ( )

( ) ( )

CO

Variable CO

EFFuel ice GSTMC G O M G P

Eta G Eta G

Lars Dittmar | 20

Stylized Merit Order

Hydro, Wind, Solar Nuclear

Coal

Gas

Tu

rbin

es

GT

Die

sel

installed capacity (GW)

CCGT

short-term marginal cost (USD/MWh)

Daily demand fluctuations

High Demand

Low Demand

Ppeak

Poff-peak

0

10

20

30

40

50

60

1 3 5 7 9 11 13 15 17 19 21 23

Lars Dittmar | 21

EEX Spot Market Prices and Merit Order vs. Residual Load 2009

-100

-50

0

50

100

150

200

0 10 20 30 40 50 60 70 80

Residual Load | Available Capacity [GW]

EEX P

rice

[Euro

/MW

h]

Sources: FG EnSys, EEX 2009

Lars Dittmar | 22

Electricity trading: Hourly Demand (red) and Supply (blue) curves EPEX

Spot Market

Sources: FG EnSys, Data EPEX 2014

Lars Dittmar | 23

Sample Market Results EPEX Spot on 16th January 2014

0

10

20

30

40

50

60

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

EUR/MWh [MW]

Demand [MW]

Price [EUR/MWh]

Sources: EPEX 2014

Lars Dittmar | 24

Load Demand and the Merit Order Shape Prices: Avg. hourly load and prices in

Germany 2011

0

10

20

30

40

50

60

70

80 12:0

0

12:0

0

12:0

0

12:0

0

12:0

0

12:0

0

12:0

0

Mo Tue Wed Thu Fri Sat Sun

Price [EUR/MWh] Load [GW]

Sources: EPEX 2012, ENTSO, own calculation

Lars Dittmar | 25

Merit Order Model: Market Power

Hydro Nuclear

Installed Capacity (GW)

Coal

Gas Turbines

GT Diesel

CCGT

sh

ort

-term

Ma

rgin

al

Co

st

(€/M

Wh

)

Demand

Marginal Cost Pricing

Coal

Gas

Turbines

GT

Diesel

CCGT

∆ Market Power?

Lars Dittmar | 26

Merit Order Model: Merit Order Effect of Renewables

REN

Installed Capacity (GW)

short-term Marginal Cost (€/MWh)

P1

PREN

∆ Merit Order Effect

Lars Dittmar | 27

Merit Order Model: Uniform Price vs. Pay-as-Bid

installed capacity (GW)

sho

rt-t

erm

mar

gin

al c

ost

(EU

R/M

Wh

)

(1) Uniform Price: Bids below PN win and get paid PN

(2) Pay-as-Bid: Bids below PN win and are paid what they bid (P1..PN)

Lars Dittmar | 28

Electricity Trading Game (Explain Online)

Lars Dittmar | 29

Exercise Electricity Trading Game

• We play 12 rounds: 9 rounds with uniform pricing

and the last 3 rounds pay-as-bid

• Maximize the profit of your team. The team

with the highest profit wins!

• Uniform pricing regime:

– Figure out how to manipulate market prices

• Pay-as-Bid auction:

– Does pay-as-bid save the customers money?

© OECD/IEA 2012

Break

© OECD/IEA 2012

And we haven’t even started talking about electricity networks…

Years in advance

Months in advance

Day ahead

Intraday

Real-time

Sufficient capacity @ peak GW

Delivery at all times GWh

Whatever you plan to do or do to deliver GW or GWh - you will have to use network services

© OECD/IEA 2012

Co-ordination of networks and generation key with unbundling

Voltage level situations @ n-1 • Individual generation location choices

• No ex ante information from the grid

•Reliability problems require trade interventions by TSO

© OECD/IEA 2012

Congestion

Balancing

Further reliability aspects

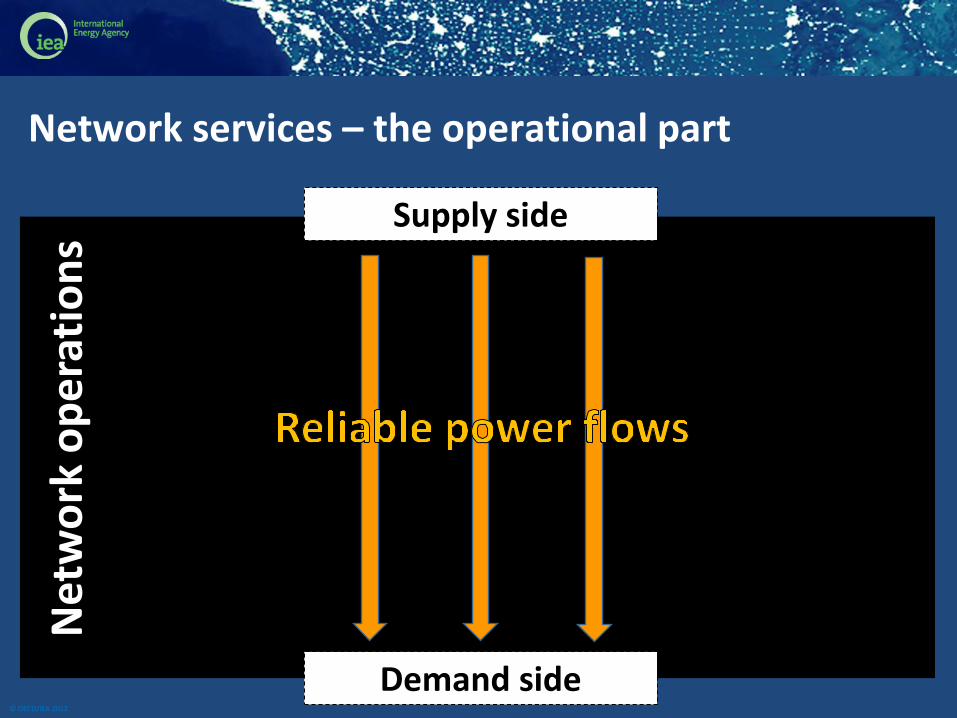

Network services – the operational part

Net

wo

rk o

pe

rati

on

s

Supply side

Demand side

© OECD/IEA 2012

Network investments – key in power until 2035

0 20 40

trillion USD

Transmission grids

Distribution grids

Conventional generation

Renewable generation

Oil supply

Gas supply

Coal supply

Biofuels

Power sector Other sectors

(IEA, 2012)

© OECD/IEA 2012

Regulated network investments – a holistic approach

Central

Central decisions

Independent planning

Information accuracy

Evaluation

Openess

Cost allocation

Network investments design-type

Planning framework

ISOITO

ITSO

Location

Prices

Fundamentals

Distribution and transmission

Demand side

StoragesGeneration

AwarenessCosts vs benefits

Beneficiaries pay

Value of renewables

Value ofreliabilityForward looking

Regulatory understanding, resolution and cost approval

Infrastructure siting

Planning interface

Environmental impacts

Need determination

Consultative planning

Adjacent systems

Merchant investments

Remote greenfield

Tenders

Market

(IEA, 2013)

© OECD/IEA 2012

Independent planning facilitation can matter

© OECD/IEA 2012

Evaluation

Network investments design-type Market

Costs vs benefits

Value of renewables

Value ofreliability

Value of trade

Setting the investment drivers – a high-level task

34

36

38

40

42

44

46

48

50

GW

Peak demand Transmission capacity

Transmission capacity under n-1

1 in 10 events

Extra transmission for 1 in 10 events Lost load over 40 years: 23 TWh

Extra costs over 40 years: 1.5 bn USD vs.

Costs for extra n-1 reliability: 66500

USD/MWh

© OECD/IEA 2012

Evaluation

Network investments design-type Market

Costs vs benefits

Value of renewables

Value ofreliability

Value of trade

Setting the investment drivers – a high-level task

0

5

10

15

20

25

13

82

76

31

14

41

52

51

90

62

28

72

66

83

04

93

43

03

81

14

19

24

57

34

95

45

33

55

71

66

09

76

47

86

85

97

24

07

62

18

00

28

38

3

Ho

url

y ge

ne

rati

on

(GW

h/h

)Germany's wind generation (2012)

© OECD/IEA 2012

Evaluation

Network investments design-type Market

Costs vs benefits

Value of renewables

Value ofreliability

Value of trade

Setting the investment drivers – a high-level task

Capture rate of wind: 50%

Capture rate of wind: 75%

Capture rate of wind: 90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 974 1947 2920 3893 4866 5839 6812 7785 8758

Win

d g

en

era

tio

n c

ap

ac

ity

uti

lis

ati

on

le

ve

l (%

)

Wind duration curve in Germany, 2012

How much of the variable generation do you want to capture?

© OECD/IEA 2012

Accurate pricing for network services support co-ordination

Costs for relevant network services consist of…

50 100 150 200 250 300 350 400

Co

sts

(USD

/MW

h)

Transportation distance (km)

Costs for network services over varying distances

CAPEX Losses

In physical reality network costs depend on transport distance

Regulatory reality often treats network costs differently

Cost-aggregation and

cost-socialisation. Easy to handle but

distorts decisions

© OECD/IEA 2012

Accurate pricing for network services support co-ordination

What is the distortion exactly?

G2

G1 L G1

Cost of production: 40 USD/MWh

G2

Cost of production: 42 USD/MWh

Cost of network losses: 5 USD/MWh

Cost of losses: 2 USD/MWh

Situation 1 (socialisation): G1 wins against G2

High network losses Total costs: 45 USD/MWh

Situation 2 (precision): G2 wins against G1

Low network losses Total costs: 44 USD/MWh

© OECD/IEA 2012

Accurate pricing for network services support co-ordination

What is the distortion exactly?

G2

G1 L G1

Cost of production: 40 USD/MWh

G2

Cost of production: 42 USD/MWh

Cost of network augmentation: 10 USD/MWh

Cost of augmentation: 2 USD/MWh

Situation 1 (socialisation): G1 wins against G2

High network CAPEX Total costs: 50 USD/MWh

Situation 2 (precision): G2 wins against G1

Low network CAPEX Total costs: 44 USD/MWh

© OECD/IEA 2012

Co-ordination with unbundling via ex ante and accurate network pricing – the US approach

Source: MISO (2013)

27 June 2013

08:30 am

© OECD/IEA 2012

Co-ordination with unbundling via ex ante and accurate network pricing – the US approach

Source: MISO (2013)

27 June 2013

08:35 am

© OECD/IEA 2012

Co-ordination with unbundling via ex ante and accurate network pricing – the US approach

Source: MISO (2013)

27 June 2013

15:30 pm

© OECD/IEA 2012

Co-ordination with unbundling via ex ante and accurate network pricing – the US approach

Source: MISO (2013)

27 June 2013

15:50 am

© OECD/IEA 2012

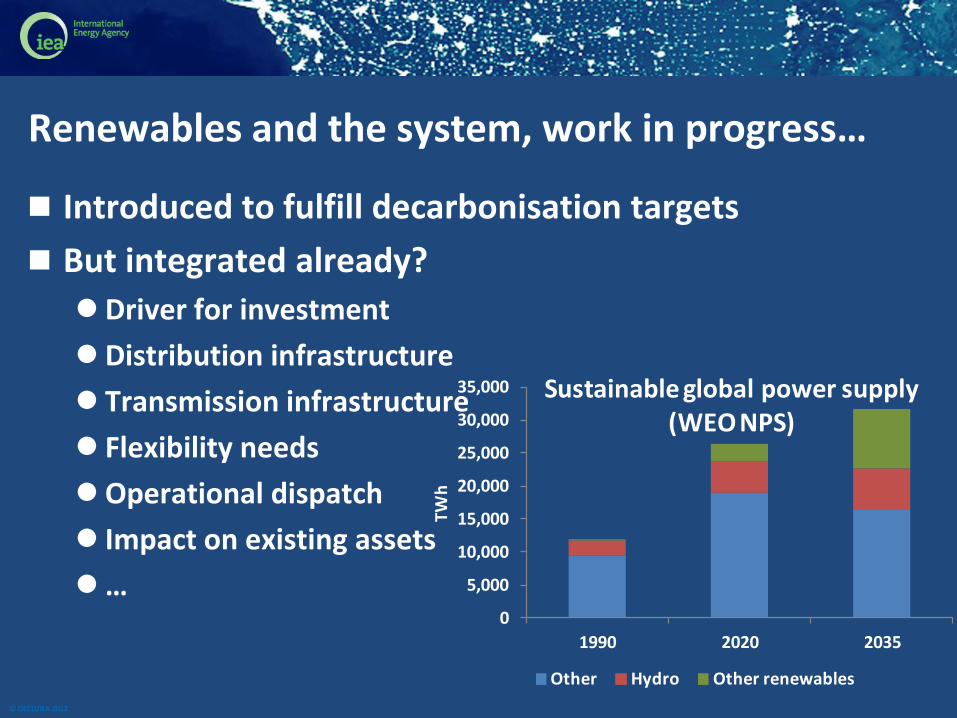

Renewables and the system, work in progress…

Introduced to fulfill decarbonisation targets

But integrated already?

Driver for investment

Distribution infrastructure

Transmission infrastructure

Flexibility needs

Operational dispatch

Impact on existing assets

… 0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1990 2020 2035

TWh

Sustainable global power supply (WEO NPS)

Other Hydro Other renewables

© OECD/IEA 2012

RENEWABLES – often shielded from the market

• Priority dispatch

• Incentives for maximizing generation

• 100% feed-in integration and compensation otherwise

• No/limited dispatch capabilities

• No network cost responsibilities

• No operational cost responsibilities

When market shares rise, these design choices have consequences for the rest

of the electricity market

© OECD/IEA 2012

Renewables in the grid – ramping needs grow

Lo

ad

& N

et

Lo

ad

(M

W)

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

9,000

00,000

04,000

08,000

12,000

16,000

20,000

24,000

28,000

32,000

36,000

40,000

Net_Load Load Wind Total Solar

Win

d &

So

lar

(MW

)

12,700 MW in 3-hours

14,000 MW in 3-hours

24,000 MW in 3-hours

© OECD/IEA 2012

Distribution network investments dominate

Projected network investments until 2035 in OECD

0

500

1000

1500

2000

2500

3000

USA Europe Total OECD

bn

USD

Distribution Transmission

© OECD/IEA 2012

Solar PV – fast, small and beyond control

400 kV

Interconnections

Interconnections

Interconnections

150 kV

60 kV

10-20 kV

400 V

Primary units

incl. Offshore wind

Ran

ge o

f

cen

tral

co

ntro

l

No

n-

dis

patc

hab

le

an

d b

eyo

nd

cen

tral

co

ntro

l 30 GW of

solar PV

© OECD/IEA 2012

Operational distribution level issues

Voltage level deviations and control

Solutions available

PV prone to under-frequency disconnection

Solutions available, but often massive retrofit required

Restoration after faults more complicated

Reliable system operation often insufficient

Real-time situational awareness and management required

Co-ordination with transmission requires common codes

Real and reactive power (feasible)

Balancing (technological progress and market-pull required)

© OECD/IEA 2012

Q&A

Lars Dittmar | 54

German Energiewende in a Nutshell –I-

• 1980: The term Energiewende (“Energy Turnaround”) was

coined by a German green think tank (Öko-Institute)

• Two main targets: (1) nuclear phase out and (2) carbon

emission reduction transition to renewable energies

• 1991: First feed-in tariffs for renewables (Chancellor Kohl)

• 2000: Renewable Energy Sources Act (EEG)

(Chancellor Schröder + Green Party)

• 2002: Decision on nuclear phase out by 2020

(Chancellor Schröder + Green Party)

Lars Dittmar | 55

German Energiewende in a Nutshell –II-

• 2010: Decision on the exit from the nuclear exit and

ambitious targets for decarbonisation, renewables and

energy efficiency (Chancellor Merkel)

• 2011: exit from the exit from the exit … In the wake of

the Fukushima disaster decision to phase out nuclear

power by 2022. (Chancellor Merkel)

• Shut-down of 8 out of nuclear power plants within a

view month

• Ambitious targets kept for emission reduction, share of

renewables and energy efficiency

• Ambitious targets + Nuclear phase out ≙ Energiewende

Lars Dittmar | 56

Gross Electricity Production in Germany 2010 ( 633 TWh)

and 2013 (633.6 TWh)

*: preliminary | Source: AGEB 2013

+11%

+6%

-31%

-25%

+5%

+45%

+91%

0

20

40

60

80

100

120

140

160

180

20

10

20

13

*

20

10

20

13

*

20

10

20

13

*

20

10

20

13

*

20

10

20

13

*

20

10

20

13

*

20

10

20

13

*

Lignite Hard Coal Nuclear Nat. Gas

Other RES Net Export

TWh

Lars Dittmar | 57

Regional Load Balance after Shut-down of 8 Nuclear Plants in 2011

Load [MW]

Before 2011 2011

Increased transmission

needs

Congestion

-5 GW

Sources: Amprion, Schiffer 2012

Lars Dittmar | 58

--

++

++

Offshore Wind

Conventional

power stations

Nuclear Phase

Out

!

!

!

Regional Power Balances 2008 and 2022

2008: Load [MW] 2022: Load [MW]

Sources: Schiffer 2012, Bundesnetzagentur/ NEP 2012

Lars Dittmar | 59

Grid Development Plan: Approval by the Federal Network Agency

• Grid extension:

– New AC-lines: 1,700 km

– Upgrade a. Enforcement of

AC-circuits: 4,100 km

– NEW DC-lines: 2,100 km

• Investment: 20 billion €

• Scenario 2022:

– Wind offshore: 13.0 GW

– Wind onshore: 47.5 GW

– Photovoltaic: 54.0 GW

– Share of RES: 50 %

Sources: Bundesnetzagentur/ NEP 2012

Lars Dittmar | 60

Development of Renewable Electricity in Germany

• Induced by the German Renewable Energy Sources Act

(EEG) the share of renewables in the German electricity mix

increased from 7 to 23 percent (≈ 117 TWh) between 2000

and 2012.

• In the same timeframe annual gross transfer payments grew

from EUR 1.2 to EUR 21 billion (≈ 342 USD/Cap/a).

• The difference between transfer payments and the market value

of renewable electricity (net burden) is apportioned to

consumers via their electricity bills as levy (“EEG levy”).

• The total EEG levy (= net burden) in 2012 amounts to EUR 17

billion (≈ 270 USD/Cap/a)

Lars Dittmar | 61

Essential Elements of the German EEG

• Grid operators (TSOs and DSOs) are obliged to provide

grid connection for EEG power plants.

• Mandatory purchase of EEG electricity by the grid

operator.

• Priority of EEG (&CHP) electricity over any other

source of power generation.

• EEG plant operators receive fixed feed-in tariffs (FiT)

for each kWh fed into the grid over 20 years.

• By 2012 about 4’000 FiT categories differentiating acc.

to energy source, vintage (decreasing rates), capacity,

technology etc.

• Additional cost of EEG electricity are apportioned to

“all” electricity consumers (“EEG levy”).

Lars Dittmar | 62

Development of Renewable Electricity Generation in Germany

Source: BMU 2013

0

5

10

15

20

25

0

20

40

60

80

100

120

140

160

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Share [%] TWh

Hydro

Wind

Solar PV

Biomass

Share of gross electricity production [%]

Lars Dittmar | 63

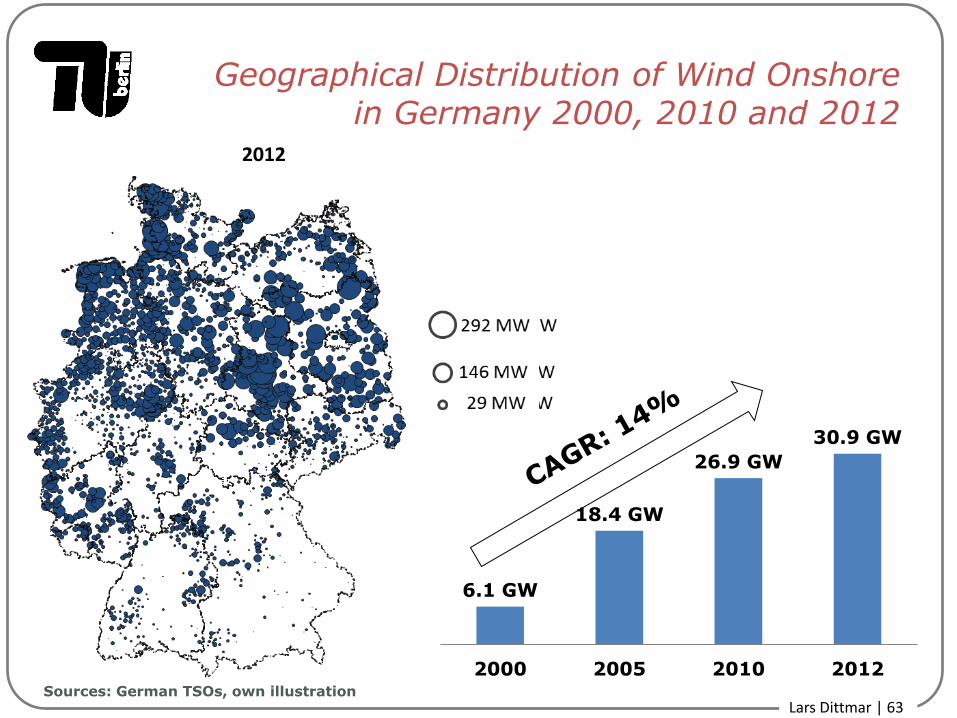

Geographical Distribution of Wind Onshore in Germany 2000, 2010 and 2012

6.1 GW

18.4 GW

26.9 GW

30.9 GW

2000 2005 2010 2012 Sources: German TSOs, own illustration

Lars Dittmar | 64

Geographical Distribution of Solar PV in Germany 2005, 2010 and 2012

0.1 GW 2.1 GW

17.6 GW

32.6 GW

2000 2005 2010 2012

Sources: German TSOs, own illustration

Lars Dittmar | 65

Relative Contribution of Costs and Electricity in 2011 by Renewable Energy Source

1

2

19

29

49

1

6

42

29

22

60 40 20 0 20 40 60

Wind offshore

Other

Wind onshore

Biomass

Solar PV

Share of REN Costs[%] | Share of REN Generation [%]

€

Lars Dittmar | 66

Energiewende and the Electricity Market

Lars Dittmar | 67

Variable Renewables and Implications for Market Prices: Merit Order Effect

Wind, PV

Installed Capacity (GW)

short-term Marginal Cost (€/MWh)

P1

PREN

∆ Merit Order Effect

Lars Dittmar | 68

Renewables and Electricity Spot Prices 2013

-150

-100

-50

0

50

100

150

0 5 10 15 20 25 30 35 40

EUR/MWh

Wind+Solar [GW ]

EEX 2013

Linear (EEX 2013)

Lars Dittmar | 69

EPEX Spot, Wind and Solar Feed-in on 26/04/2012

0

10

20

30

40

50

60

70

0

5

10

15

20

25

30

1 3 5 7 9 11 13 15 17 19 21 23

EUR/MWh GW

Wind

Sources: EPEX 2013. German TSOs

Lars Dittmar | 70

Future Prices Base Load Germany

0

20

40

60

80

100

120

2008 2009 2010 2011 2012 2013

EUR/MWh Base 2009 Base 2010 Base 2011

Base 2012 Base 2013 Base 2014

Base 2015 Base 2016 Base 2017

Base 2018 Base 2019

Shut Down of 8 Nuclear Plants

Sources: EEX

Lars Dittmar | 71

Are these returns sufficient?

Price-Duration-Curve: Power Plant Investments on Competitive Markets

0

20

40

60

80

0 1000 2000 3000 4000 5000 6000

Hourly d

ay-a

head p

rices [

Euro

/MW

h]

Marginal costs of a new plant

Expected annual operating hours

Ordered price duration curve for the planning horizon

hours of the year

Source: Erdmann 2011

Lars Dittmar | 72

Price Duration Curves Germany (EPEX)

Sources: EPEX

-100

-50

0

50

100

150

200

250

0 2000 4000 6000 8000

EUR/MWh

2011 (Ø = 51,9)

2012 (Ø = 42,8)

2013 (Ø = 37,8)

Lars Dittmar | 73

0

10

20

30

40

50

60

70

80

90

100

0 20 40 60 80 100

P/Pinstalled [%]

time per year [%]

2006

2007

2008

2009

2010

2011

2012

2007

2010

Wind Power Duration Curves for Germany 2006-2012

Sources: German TSOs

Back-up

Lars Dittmar | 74

Solar Power Duration Curves for Germany 2007-2012

0

20

40

60

80

100

0 10 20 30 40 50 60 70 80 90 100

P/Pinstalled [%]

% of time per year

2007

2008

2009

2010

2011

2012

Night

Sources: German TSOs

Lars Dittmar | 75

Contribution of Renewables to Peak Load Demand:

Germany 2006 vs. 2013

0

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

70

80

1 1001 2001 3001 4001 5001 6001 7001 8001

Delta 2006-

2013 [GW]

Residual Load

2006/2013

[GW] 2006

2013

Source: EEX/EPEX 2014, Entsoe-2013

~ 3 GW

Lars Dittmar | 76

Conclusion

• The Energiewende is a mammoth policy project

affecting the entire electricity system

• Current market prices do not cover the costs of

conventional capacities. Additionally sales volumes

decline.

• The RES-Policy-Design of „produce and forget“ has

to be changed create demand for secured

capacity

• Conventional power plants are still needed, also in

the long-run (~50GW with 80% RES)

© OECD/IEA 2012

Thank you for your attention

For further questions - please contact…

© OECD/IEA 2012

References

Besant-Jones, J., 2006: “Reforming Power Markets in Developing

Countries: What have we learned?”, available at

http://siteresources.worldbank.org/INTENERGY/Resources/Energy19.pdf.

Domah, P. D. and Pollitt, M.G., 2001: “The Restructuring and Privatisation of the Regional Electricity Companies in England and Wales: A Social Cost Benefit Analysis”, Fiscal Studies, 22 (1): 107-146.

Fabrizio, K., Rose, N. and Wolfram, C. (2007), ‘Do Markets Reduce Costs? Assessing the Impact of Regulatory Restructuring on U.S.

Electric Generation Efficiency’, American Economic Review, 97 (4): 1250-1277.

FERC, 2013: “Industry Activities”, available at

http://www.ferc.gov/industries/electric/indus-act.asp.

© OECD/IEA 2012

References

Fiorio, C. et al., 2007: “The Electricity Industry Reform Paradigm in the European Union: Testing the Impact on Consumers” Available at http://services.bepress.com/unimi/economics/art23/

IEA, 2012: “Electricity”, available at http://www.iea.org/topics/electricity/

Hattori and Tsutsui, 2004: “Economic impact of regulatory reforms in the electricity supply industry: a panel data analysis for OECD countries” Available at

http://www.sciencedirect.com/science/article/pii/S0301421503000041

Jamasb, et al., “Electricity Sector Reform in Developing Countries: A Survey of Empirical Evidence on Determinants and Performance”, available at http://ideas.repec.org/p/wbk/wbrwps/3549.html.

© OECD/IEA 2012

References

Joule Assets (2014) “The Choice Is Yours: Competition in Retail Electricity Markets”, Available at http://jouleassets.com/the-choice-is-yours-competition-in-retail-electricity-markets/

Joskow and Schmalensee, 1983: “Markets for Power: An Analysis of Electric Utility Deregulation”, Cambridge, MA: MIT Press.

Joskow, 2001: “California’s Electricity Crises”, available at

http://www.nber.org/papers/w8442.

Moore, 1992: “Privatisation Everywhere: The World’s Adoption of the British Experience” available at

http://www.cps.org.uk/files/reports/original/111027160313-PrivitisationEverywhere1992.pdf.

Nagayama, H., 2009: “Electric power sector reform liberalization models and electric power prices in developing countries – An empirical analysis using international panel data”, Energy Economics, 31:

463-472.

© OECD/IEA 2012

References

Pollitt, 2009: “Evaluating the evidence on electricity reform:

Lessons for the South East Europe (SEE) market”, available at https://www.repository.cam.ac.uk/bitstream/handle/1810/195425/0756&eprg0725.pdf?sequence=1.

PUC Texas (2014) “Power to Choose”, Available at http://www.powertochoose.org/

Steiner, 2001: “REGULATION, INDUSTRY STRUCTURE AND PERFORMANCE IN THE ELECTRICITY SUPPLY INDUSTRY”, Available at http://www.oecd.org/eco/outlook/2731965.pdf.

Triebs, T., Kwoka, J. and Pollitt, M., 2010: “The Direct Costs and Benefits of US Electric Utility Divestitures”, available at https://www.repository.cam.ac.uk/bitstream/handle/1810/242074/cwpe1049.pdf?sequence=1.

Toba, N., 2007: “Welfare Impacts of Electricity Generation Sector Reform in the Philippines”, Energy Policy, 35(12): 6145-6162.

© OECD/IEA 2012

References

AEMO, 2012: “Planning”, available at http://www.aemo.com.au/Electricity/Planning.

AER, 2013: “AER releases determination on South Australia to Victoria electricity transmission interconnector”, available at http://www.aer.gov.au/node/21633.

IEA, 2013: “Electricity Networks: Infrastructure and Operations”, available at http://www.iea.org/publications/insights/insightpublications/name,43756,en.html.

IEA, 2012: “World Energy Outlook 2012”, IEA, Paris. Joskow, 2006: “INCENTIVE REGULATION IN THEORY AND

PRACTICE: ELECTRICITY DISTRIBUTION AND TRANSMISSION NETWORKS”, available at http://economics.mit.edu/files/1181.

Pollitt, 2013: “Global Trends in Electricity Transmission System Operation: Where does the future lie?“, available at http://www.eprg.group.cam.ac.uk/wp-content/uploads/2013/05/Draft-Project-2.pdf.

Roland Berger, 2011: “Permitting procedures for energy infrastructure projects in the EU: evaluation and legal recommendations”, available at http://ec.europa.eu/energy/infrastructure/studies/doc/2011_ten_e_permitting_report.pdf.