Embed Size (px)

Citation preview

EGYPTIAN AUTOMOTIVE

MARKET

SEPTEMBER 2009 REPORT

SPONSORED BY:

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

2

Sponsored By

1. Preface 3

2.. Local industry analysis 4

2.1. Total market 5

2.2. Passenger cars market 14

2.3. Buses market 32

2.4. Trucks market 43

3. Monthly news flash 15th to 15th 54

3.1. Egypt macro flash 53

3.2. Automotive industry local news clips 59

3.3. Automotive industry global news clips 61

TT Taa abb bll l ee e

oo off f

CC Coo onn ntt t ee e

nn ntt t ss s

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

3

Sponsored By

1. PREFACE The methodology, used in this report is mainly relying on the following steps:

Gathering primary and secondary data from AMIC Egypt members.

Validating missing data and cross checking of data from different

sources including Customs, JAMA, Ministry of Interior, etc..

Processing, Analyzing and presenting data in a useful way to AMIC Egypt members.

Gathering Macro Economic and Automotive industry news from:

Newspapers and Magazines, Internet, published material, etc... and

presenting them in a simple way.

Confidentiality Clause:

This report as well as the attached Excel sheet are the Exclusive property of AMIC Egypt and its members and should not be reproduced or distributed to

outsider parties.

This report was prepared and developed by:

Integrated Management Consultancy – IMC, which is a Management

Consultancy Office with specific areas of strengths in:

Marketing – Specially Business to Business,

Human Resources – Specifically in Learning Organizations,

Six Sigma Methodology - Manufacturing.

SME Upgrading and Training - World bank / Business Edge Partner

On the Job Coaching.

________________________________________________________________________________

IMC INTEGRATED MANAGEMENT CONSULTANCY

Rami Y. Camel-Toueg & Associates _________________________________________________________________________________

22 RASHID ST. OFF EL OROUBA ST. 1ST FLOOR, SUITE # 6,

11341 HELIOPOLIS, CAIRO, EGYPT. MOBILE: + (2010) 19 757 11

TEL. /FAX: + (202) 2690 1472 / + (202) 2690 1476 / + (202) 258 4015 Email: [email protected]

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

4

Sponsored By

2. LOCAL INDUSTRY ANALYSIS

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

5

Sponsored By

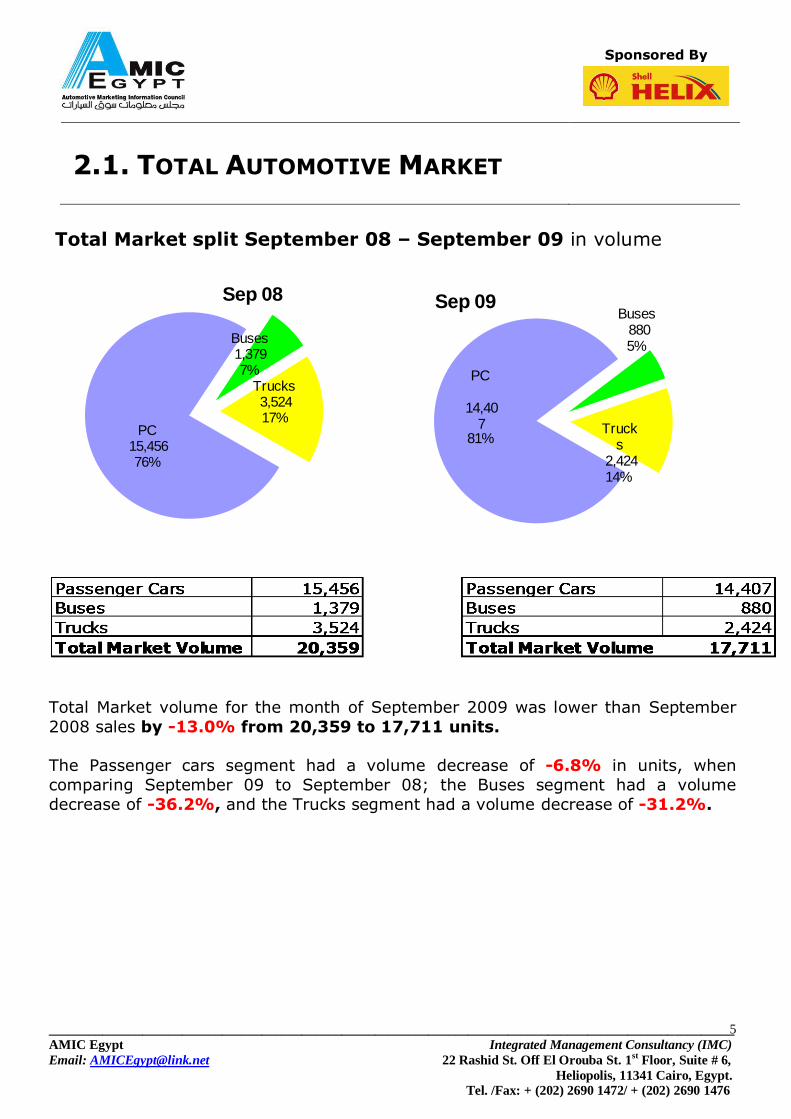

2.1. TOTAL AUTOMOTIVE MARKET

Total Market split September 08 – September 09 in volume

PC15,456 76%

Buses1,379 7%

Trucks3,524 17%

Sep 08

PC

14,407

81%

Buses880 5%

Trucks

2,424 14%

Sep 09

Total Market volume for the month of September 2009 was lower than September

2008 sales by -13.0% from 20,359 to 17,711 units.

The Passenger cars segment had a volume decrease of -6.8% in units, when

comparing September 09 to September 08; the Buses segment had a volume

decrease of -36.2%, and the Trucks segment had a volume decrease of -31.2%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

6

Sponsored By

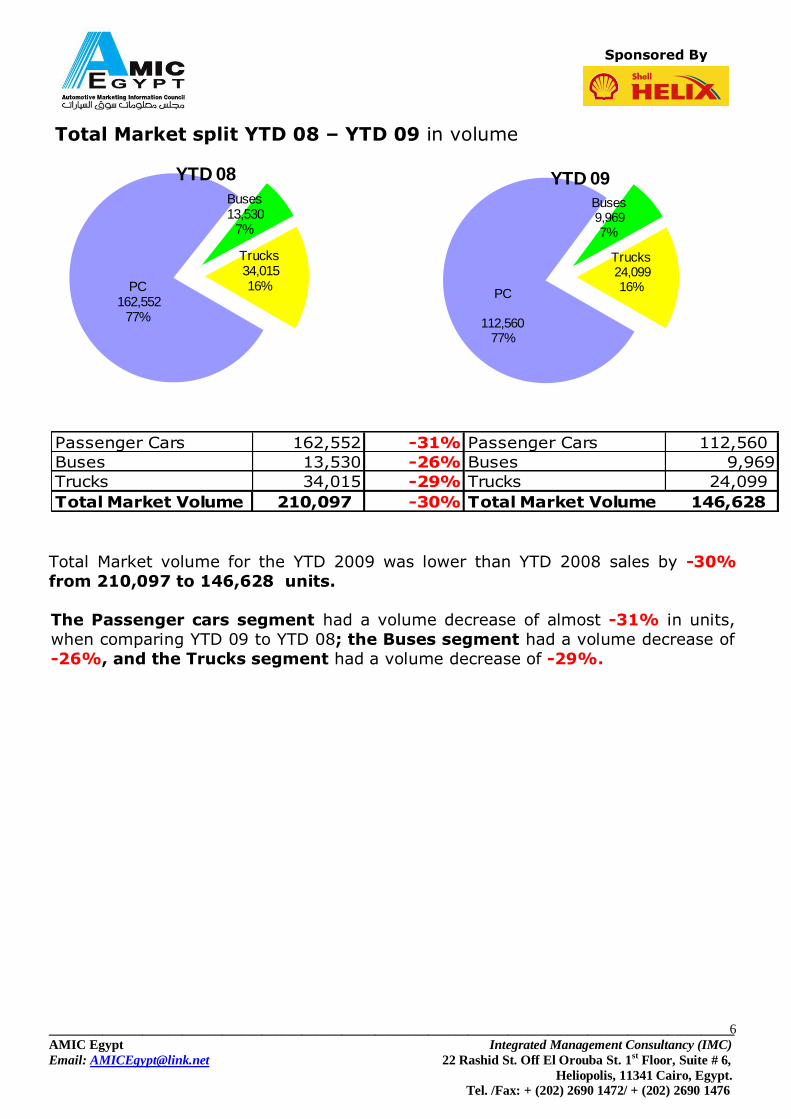

Total Market split YTD 08 – YTD 09 in volume

PC162,552

77%

Buses13,530

7%

Trucks34,015 16%

YTD 08

PC

112,560 77%

Buses9,969 7%

Trucks24,099 16%

YTD 09

Passenger Cars 162,552 -31% Passenger Cars 112,560

Buses 13,530 -26% Buses 9,969

Trucks 34,015 -29% Trucks 24,099

Total Market Volume 210,097 -30% Total Market Volume 146,628

Total Market volume for the YTD 2009 was lower than YTD 2008 sales by -30%

from 210,097 to 146,628 units.

The Passenger cars segment had a volume decrease of almost -31% in units,

when comparing YTD 09 to YTD 08; the Buses segment had a volume decrease of

-26%, and the Trucks segment had a volume decrease of -29%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

7

Sponsored By

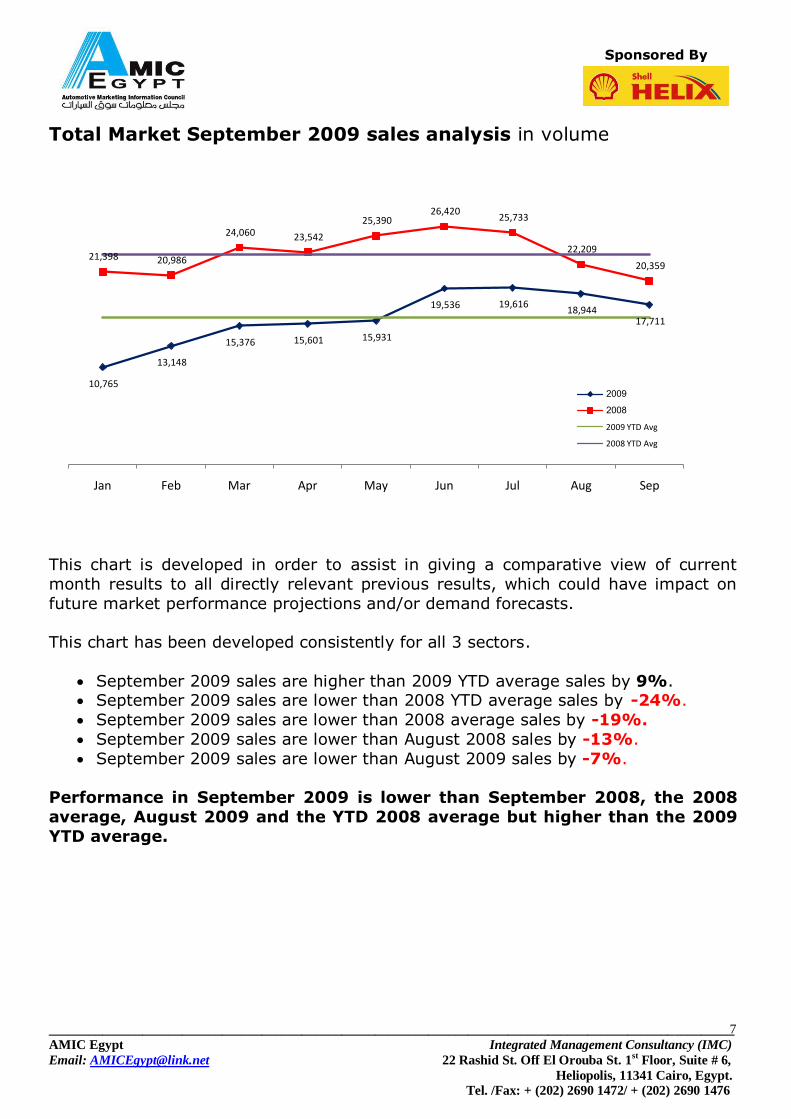

Total Market September 2009 sales analysis in volume

This chart is developed in order to assist in giving a comparative view of current

month results to all directly relevant previous results, which could have impact on

future market performance projections and/or demand forecasts.

This chart has been developed consistently for all 3 sectors.

September 2009 sales are higher than 2009 YTD average sales by 9%. September 2009 sales are lower than 2008 YTD average sales by -24%.

September 2009 sales are lower than 2008 average sales by -19%.

September 2009 sales are lower than August 2008 sales by -13%.

September 2009 sales are lower than August 2009 sales by -7%.

Performance in September 2009 is lower than September 2008, the 2008

average, August 2009 and the YTD 2008 average but higher than the 2009

YTD average.

10,765

13,148

15,376 15,601 15,931

19,536 19,616 18,944

17,711

21,398 20,986

24,060 23,542

25,390 26,420

25,733

22,209

20,359

Jan Feb Mar Apr May Jun Jul Aug Sep

2009

2008

2009 YTD Avg

2008 YTD Avg

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

8

Sponsored By

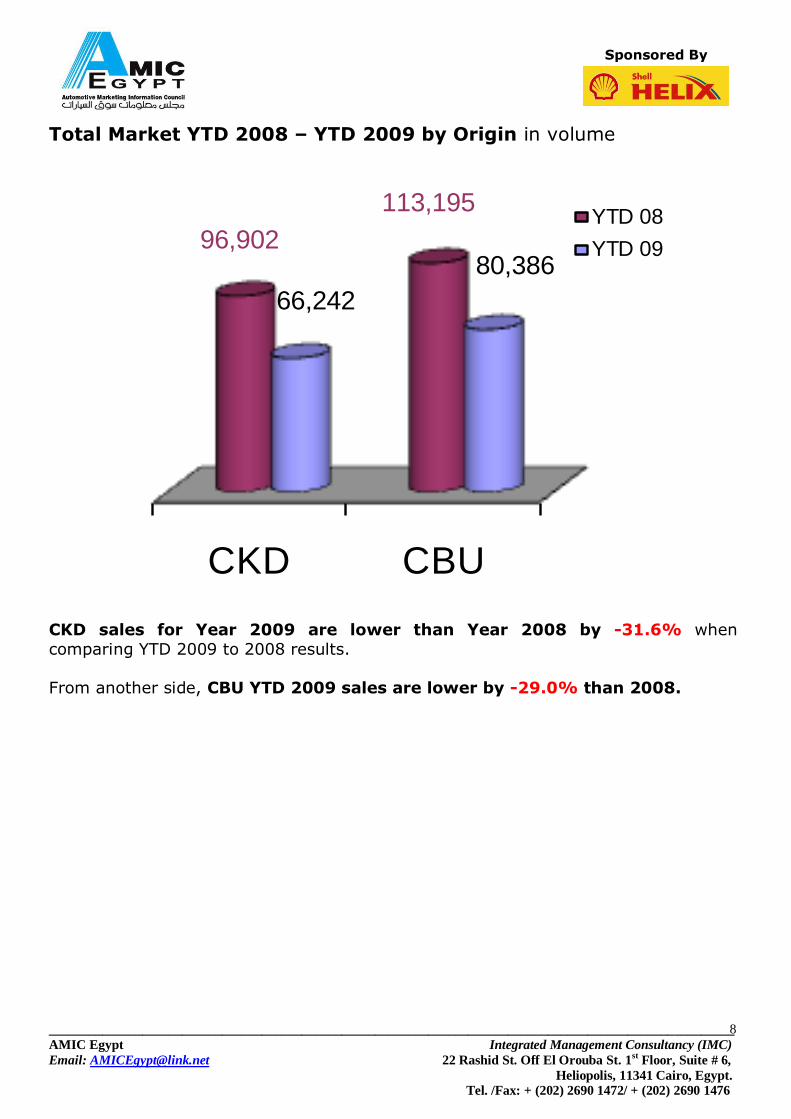

Total Market YTD 2008 – YTD 2009 by Origin in volume

CKD CBU

96,902

113,195

66,242

80,386

YTD 08

YTD 09

CKD sales for Year 2009 are lower than Year 2008 by -31.6% when

comparing YTD 2009 to 2008 results.

From another side, CBU YTD 2009 sales are lower by -29.0% than 2008.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

9

Sponsored By

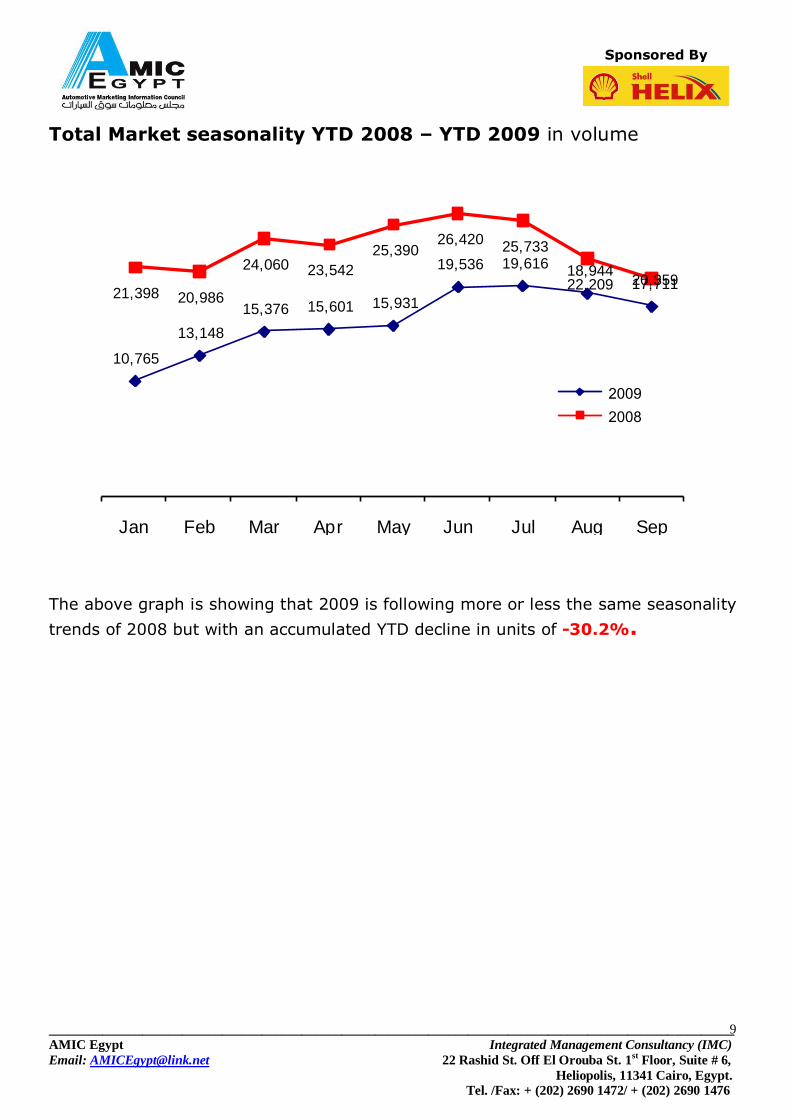

Total Market seasonality YTD 2008 – YTD 2009 in volume

10,765

13,148

15,376 15,601 15,931

19,536 19,616 18,944

17,711 21,398 20,986

24,060 23,542

25,390 26,420

25,733

22,209 20,359

Jan Feb Mar Apr May Jun Jul Aug Sep

2009

2008

The above graph is showing that 2009 is following more or less the same seasonality

trends of 2008 but with an accumulated YTD decline in units of -30.2%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

10

Sponsored By

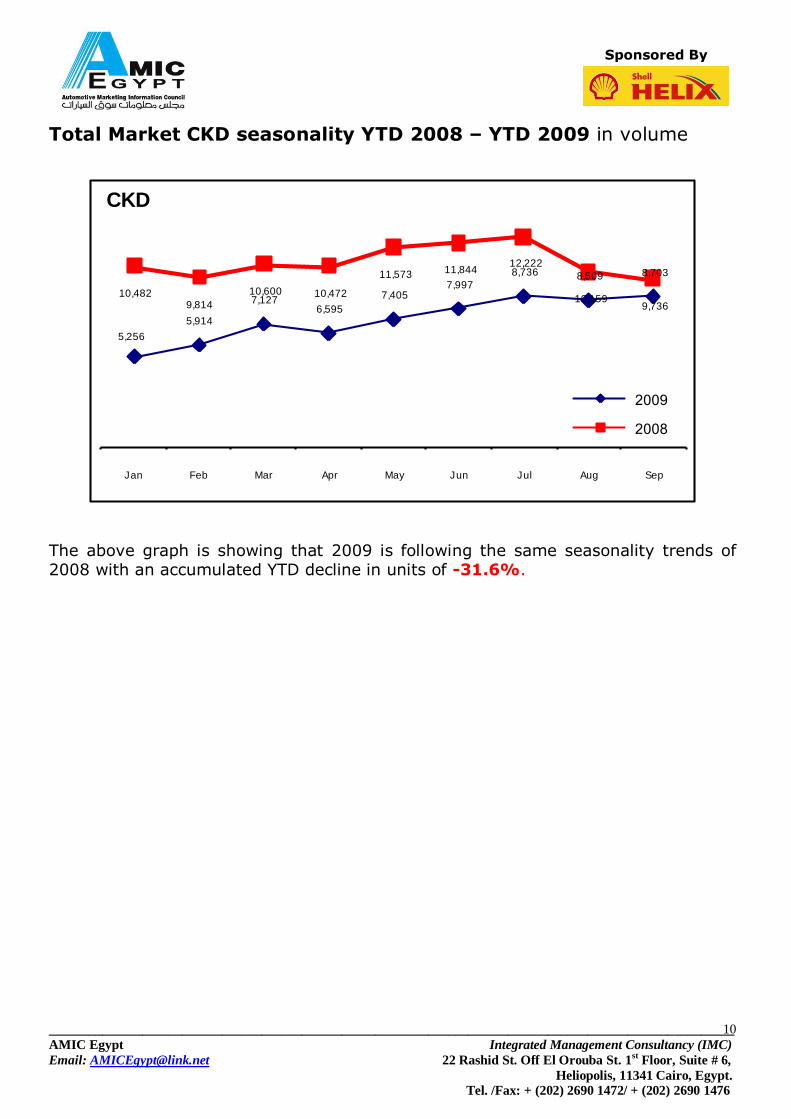

Total Market CKD seasonality YTD 2008 – YTD 2009 in volume

5,256

5,914

7,127 6,595

7,405 7,997

8,736 8,509 8,703

10,482 9,814

10,600 10,472

11,573 11,844 12,222

10,159 9,736

Jan Feb Mar Apr May Jun Jul Aug Sep

CKD

2009

2008

The above graph is showing that 2009 is following the same seasonality trends of 2008 with an accumulated YTD decline in units of -31.6%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

11

Sponsored By

Total Market CBU seasonality YTD 2008 – YTD 2009 in volume

5,509

7,234

8,249 9,006

8,526

11,539 10,880

10,435

9,008

10,916 11,172

13,460 13,070

13,817 14,576

13,511

12,050

10,623

Jan Feb Mar Apr May Jun Jul Aug Sep

CBU

2009

2008

The above graph is showing that 2009 is following more or less the same

seasonality trends of 2008 with an accumulated YTD decline in units of -29.0%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

12

Sponsored By

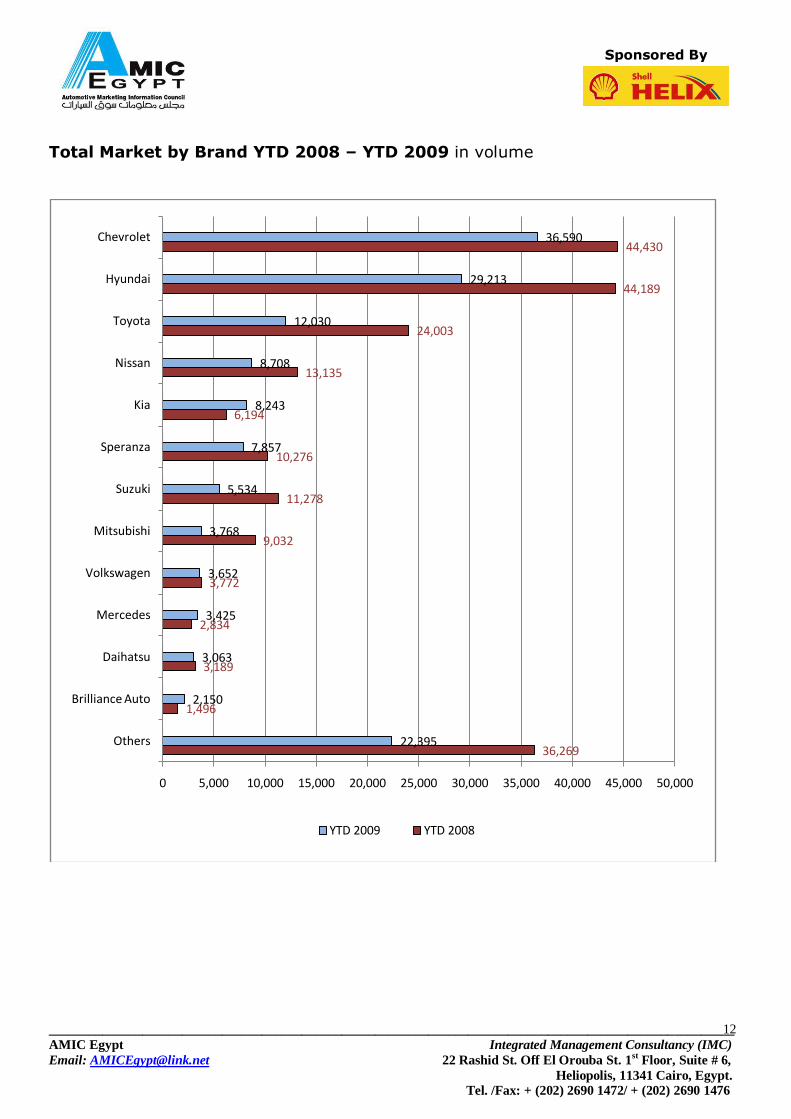

Total Market by Brand YTD 2008 – YTD 2009 in volume

36,269

1,496

3,189

2,834

3,772

9,032

11,278

10,276

6,194

13,135

24,003

44,189

44,430

22,395

2,150

3,063

3,425

3,652

3,768

5,534

7,857

8,243

8,708

12,030

29,213

36,590

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

Others

Brilliance Auto

Daihatsu

Mercedes

Volkswagen

Mitsubishi

Suzuki

Speranza

Kia

Nissan

Toyota

Hyundai

Chevrolet

YTD 2009 YTD 2008

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

13

Sponsored By

Total Market by Brand YTD 2008 – YTD 2009 in market share

17.3%

0.7%

1.5%

1.3%

1.8%

4.3%

5.4%

4.9%

2.9%

6.3%

11.4%

21.0%

21.1%

15.3%

1.5%

2.1%

2.3%

2.5%

2.6%

3.8%

5.4%

5.6%

5.9%

8.2%

19.9%

25.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

Others

Brilliance Auto

Daihatsu

Mercedes

Volkswagen

Mitsubishi

Suzuki

Speranza

Kia

Nissan

Toyota

Hyundai

Chevrolet

YTD 2009 YTD 2008

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

14

Sponsored By

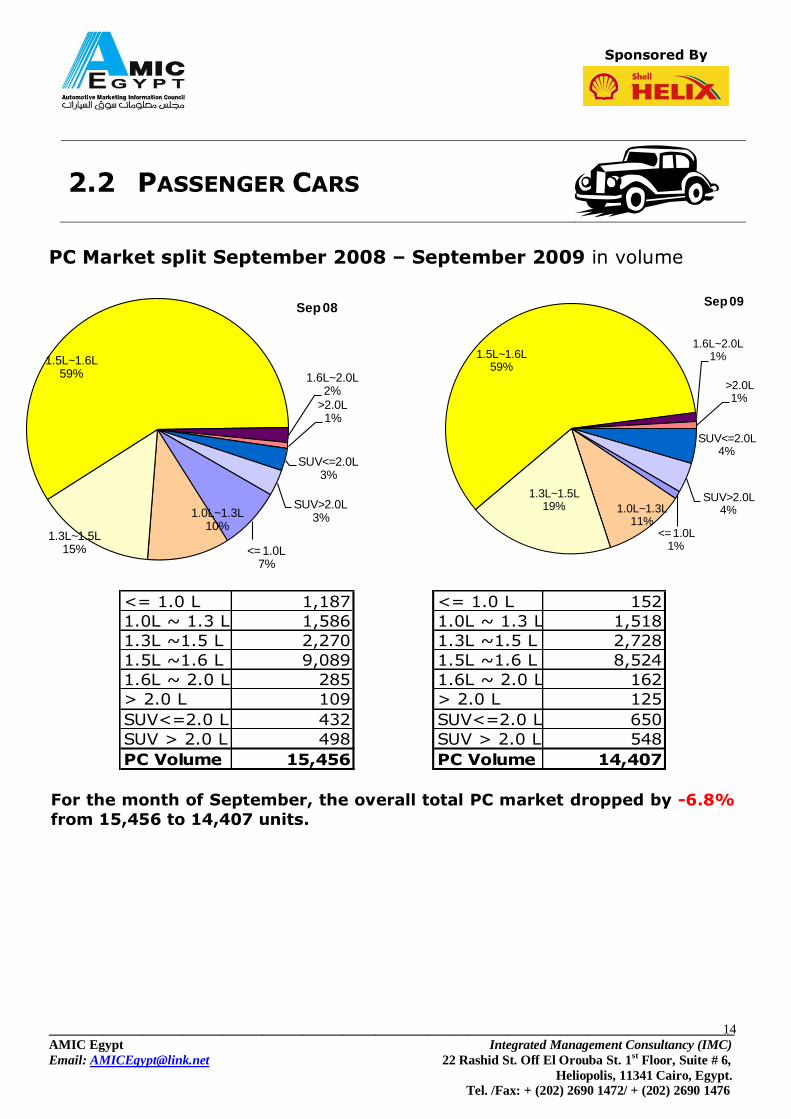

2.2 PASSENGER CARS

PC Market split September 2008 – September 2009 in volume

<= 1.0L7%

1.0L~1.3L10%

1.3L~1.5L15%

1.5L~1.6L59% 1.6L~2.0L

2%>2.0L1%

SUV<=2.0L3%

SUV>2.0L3%

Sep 08

<= 1.0L1%

1.0L~1.3L11%

1.3L~1.5L19%

1.5L~1.6L59%

1.6L~2.0L1%

>2.0L1%

SUV<=2.0L4%

SUV>2.0L4%

Sep 09

<= 1.0 L 1,187 <= 1.0 L 152

1.0L ~ 1.3 L 1,586 1.0L ~ 1.3 L 1,518

1.3L ~1.5 L 2,270 1.3L ~1.5 L 2,728

1.5L ~1.6 L 9,089 1.5L ~1.6 L 8,524

1.6L ~ 2.0 L 285 1.6L ~ 2.0 L 162

> 2.0 L 109 > 2.0 L 125

SUV<=2.0 L 432 SUV<=2.0 L 650

SUV > 2.0 L 498 SUV > 2.0 L 548

PC Volume 15,456 PC Volume 14,407 For the month of September, the overall total PC market dropped by -6.8%

from 15,456 to 14,407 units.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

15

Sponsored By

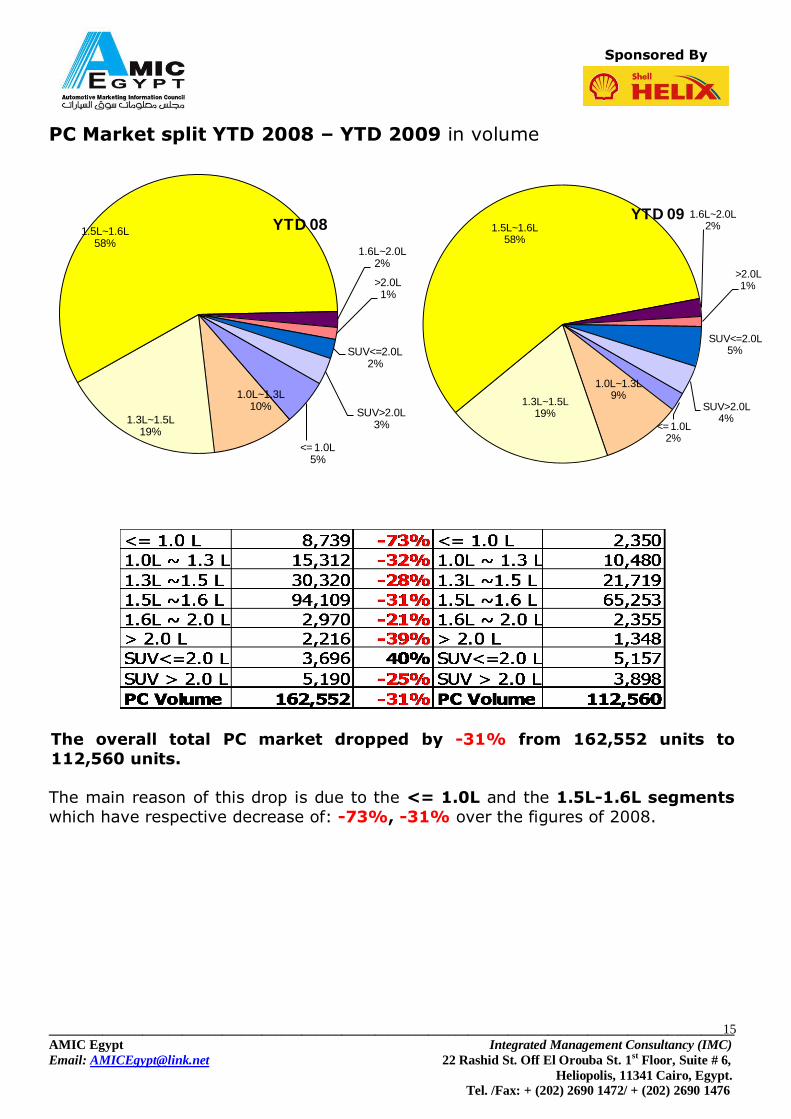

PC Market split YTD 2008 – YTD 2009 in volume

<= 1.0L5%

1.0L~1.3L10%

1.3L~1.5L19%

1.5L~1.6L58%

1.6L~2.0L2%

>2.0L1%

SUV<=2.0L2%

SUV>2.0L3%

YTD 08

<= 1.0L2%

1.0L~1.3L9%

1.3L~1.5L19%

1.5L~1.6L58%

1.6L~2.0L2%

>2.0L1%

SUV<=2.0L5%

SUV>2.0L4%

YTD 09

The overall total PC market dropped by -31% from 162,552 units to

112,560 units.

The main reason of this drop is due to the <= 1.0L and the 1.5L-1.6L segments

which have respective decrease of: -73%, -31% over the figures of 2008.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

16

Sponsored By

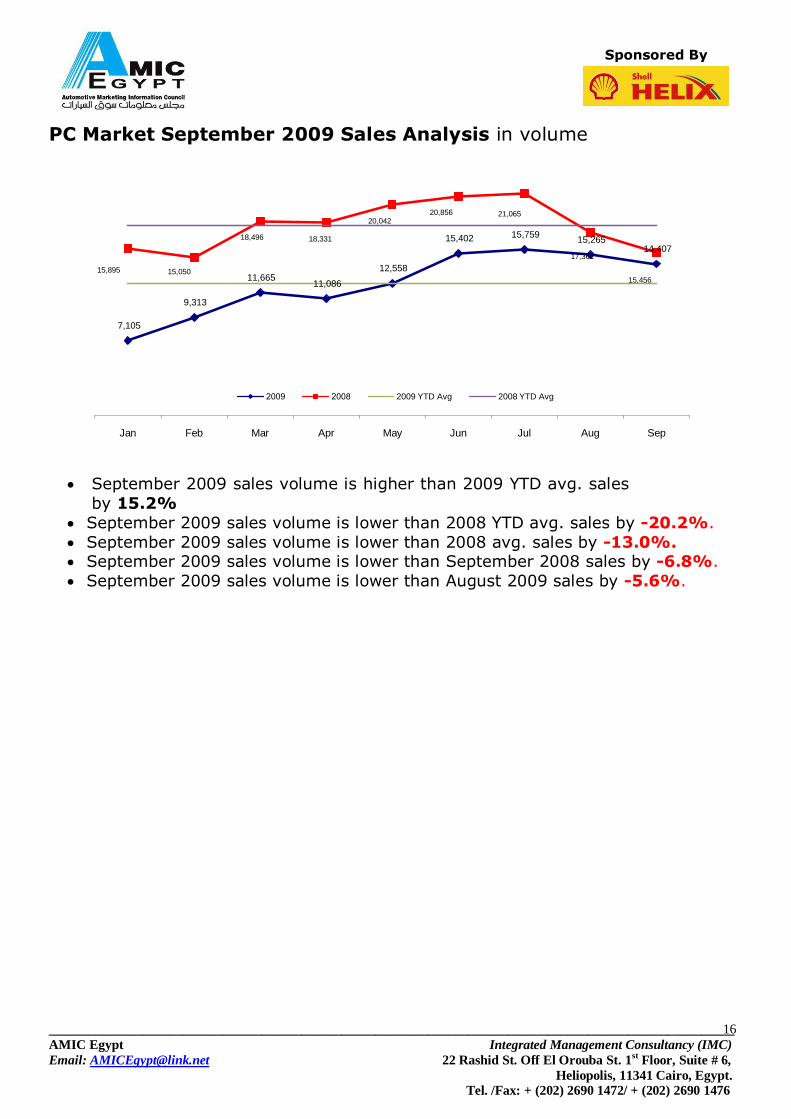

PC Market September 2009 Sales Analysis in volume

September 2009 sales volume is higher than 2009 YTD avg. sales

by 15.2%

September 2009 sales volume is lower than 2008 YTD avg. sales by -20.2%.

September 2009 sales volume is lower than 2008 avg. sales by -13.0%. September 2009 sales volume is lower than September 2008 sales by -6.8%.

September 2009 sales volume is lower than August 2009 sales by -5.6%.

7,105

9,313

11,665 11,086

12,558

15,402 15,759 15,265

14,407

15,895 15,050

18,496 18,331

20,042 20,856 21,065

17,361

15,456

Jan Feb Mar Apr May Jun Jul Aug Sep

2009 2008 2009 YTD Avg 2008 YTD Avg

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

17

Sponsored By

PC Market seasonality YTD 2008 – YTD 2009 in volume

7,105

9,313 11,665 11,086

12,558

15,402 15,759 15,265 14,407

15,895 15,050

18,496 18,331

20,042 20,856 21,065

17,361

15,456

Jan Feb Mar Apr May Jun Jul Aug Sep

2009

2008

The above Trend analysis graph is showing that for PC; 2009 is following more or

less the same seasonality trend of 2008 with an accumulated YTD decline of

-31%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

18

Sponsored By

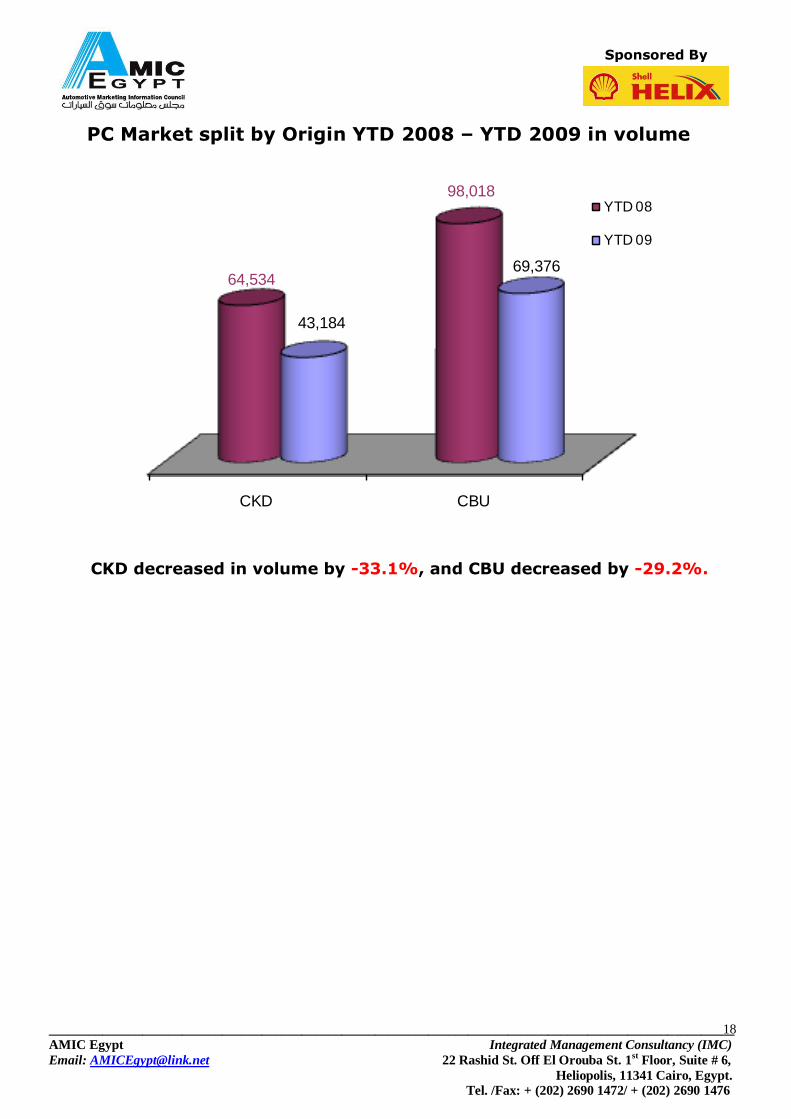

PC Market split by Origin YTD 2008 – YTD 2009 in volume

CKD CBU

64,534

98,018

43,184

69,376

YTD 08

YTD 09

CKD decreased in volume by -33.1%, and CBU decreased by -29.2%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

19

Sponsored By

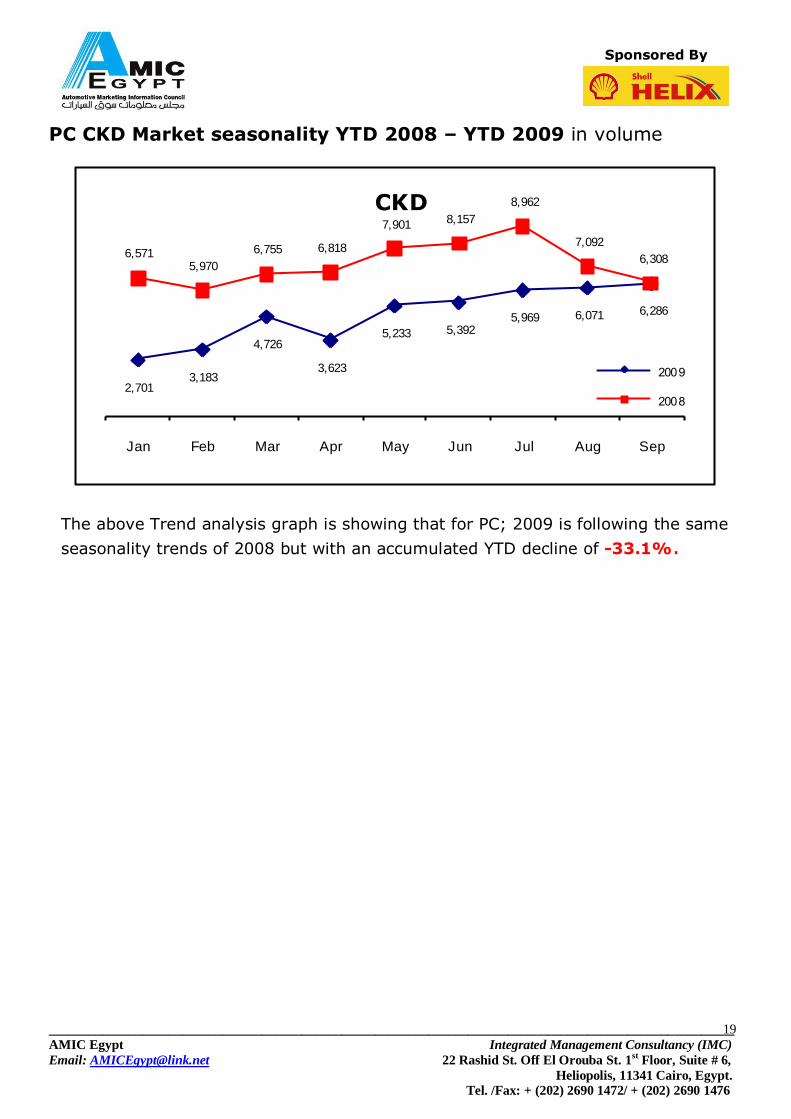

PC CKD Market seasonality YTD 2008 – YTD 2009 in volume

2,701 3,183

4,726

3,623

5,233 5,392 5,969 6,071 6,286

6,571 5,970

6,755 6,818

7,901 8,157

8,962

7,092

6,308

Jan Feb Mar Apr May Jun Jul Aug Sep

CKD

2009

2008

The above Trend analysis graph is showing that for PC; 2009 is following the same

seasonality trends of 2008 but with an accumulated YTD decline of -33.1%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

20

Sponsored By

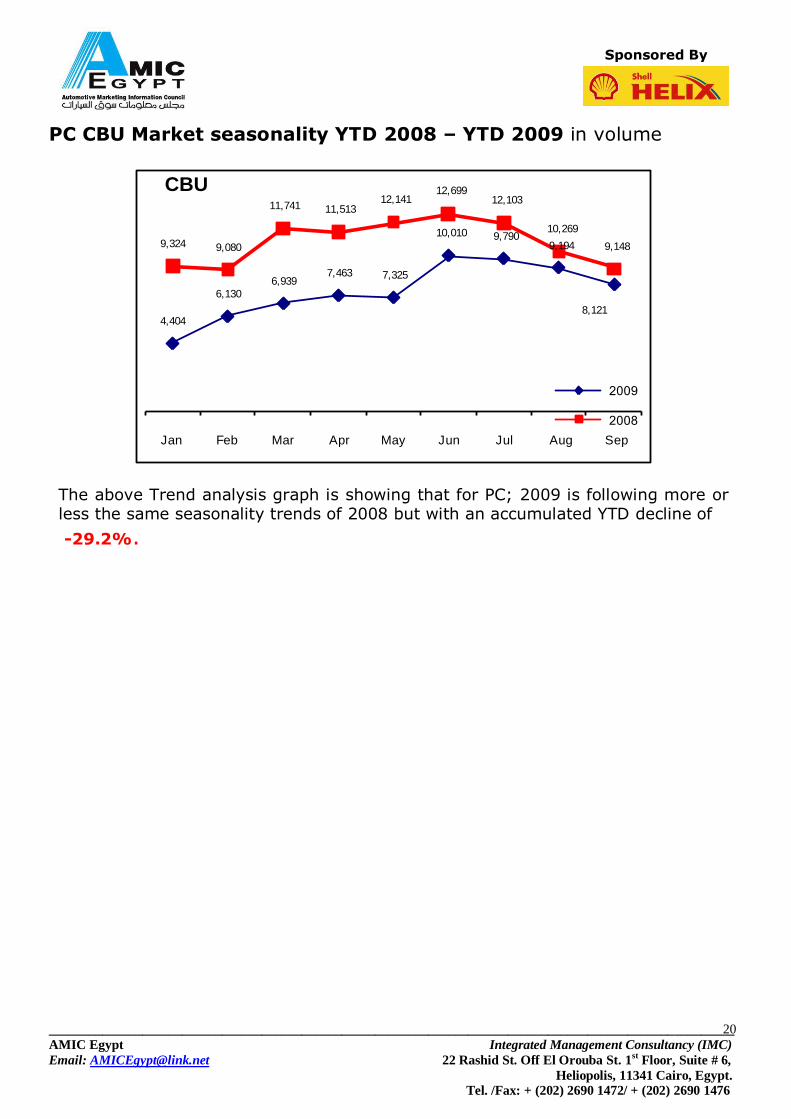

PC CBU Market seasonality YTD 2008 – YTD 2009 in volume

4,404

6,130

6,939 7,463 7,325

10,010 9,790 9,194

8,121

9,324 9,080

11,741 11,513 12,141

12,699 12,103

10,269

9,148

Jan Feb Mar Apr May Jun Jul Aug Sep

CBU

2009

2008

The above Trend analysis graph is showing that for PC; 2009 is following more or less the same seasonality trends of 2008 but with an accumulated YTD decline of

-29.2%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

21

Sponsored By

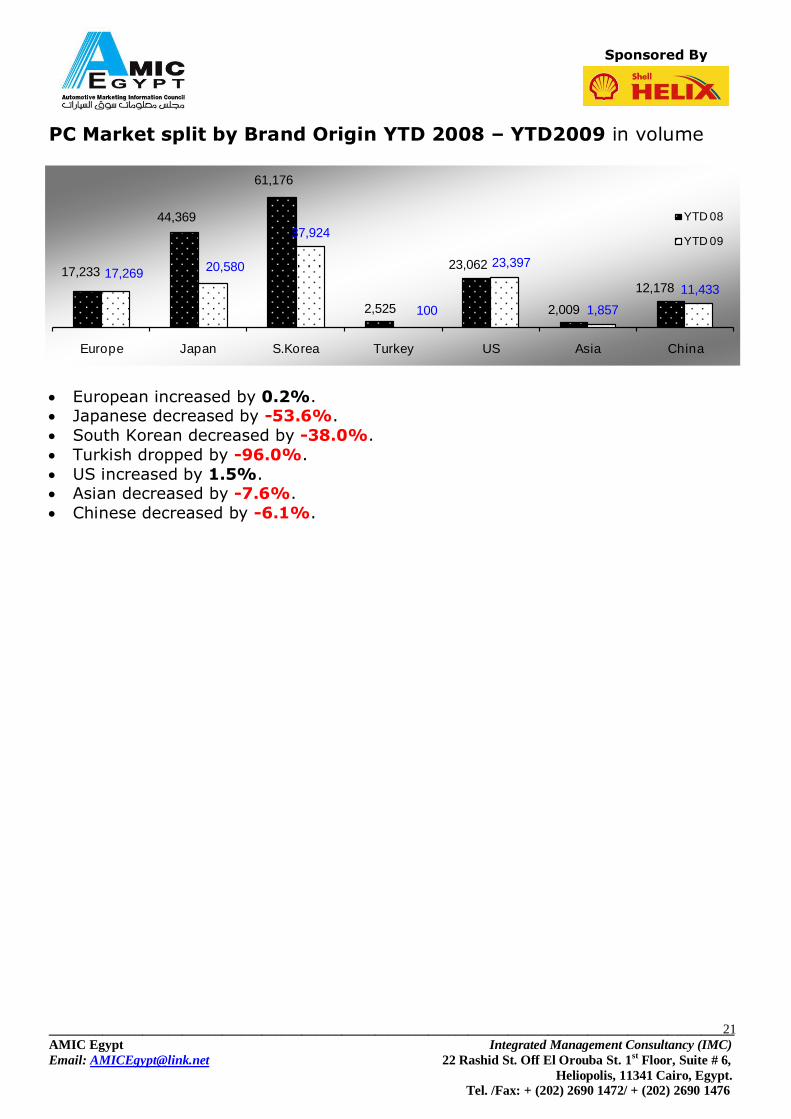

PC Market split by Brand Origin YTD 2008 – YTD2009 in volume

17,233

44,369

61,176

2,525

23,062

2,009

12,178 17,269

20,580

37,924

100

23,397

1,857

11,433

Europe Japan S.Korea Turkey US Asia China

YTD 08

YTD 09

European increased by 0.2%. Japanese decreased by -53.6%.

South Korean decreased by -38.0%.

Turkish dropped by -96.0%.

US increased by 1.5%. Asian decreased by -7.6%.

Chinese decreased by -6.1%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

22

Sponsored By

PC Market by Brand YTD 08 – YTD 09 in volume

8,278

2,525

11,494

606

2,311

953

1,380

1,879

7,582

3,704

2,536

7,011

1,992

1,540

3,387

1,316

13,397

9,923

10,276

6,194

20,962

43,306

6,628

100

722

942

982

1,290

1,586

1,688

1,841

2,045

2,339

2,532

2,581

2,644

3,138

3,347

5,525

6,096

7,857

8,243

21,475

28,959

Others

TOFAS

DAEWOO

FIAT

OPEL

BRILLIAN…

Proton

BMW

Suzuki

Honda

DAIHATSU

MITSUBI…

MERCED…

SKODA

VW

RENAULT

TOYOTA

Nissan

Speranza

KIA

Chevrolet

HYUNDAI

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

23

Sponsored By

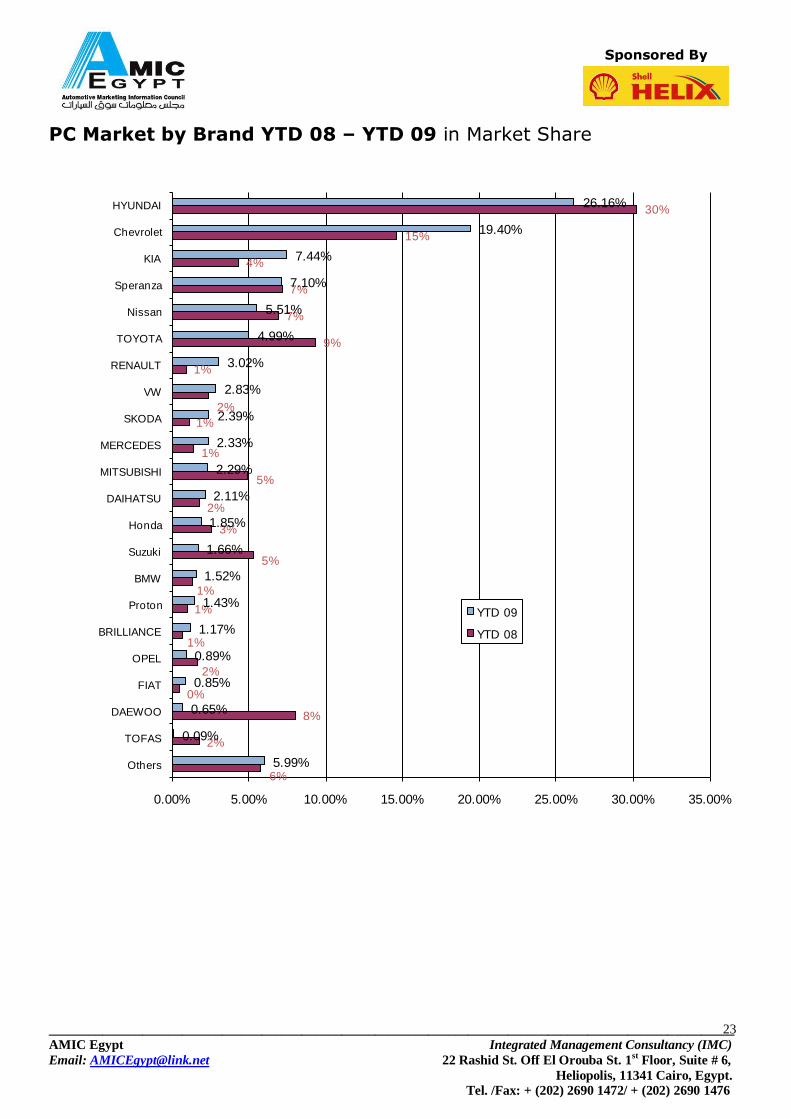

PC Market by Brand YTD 08 – YTD 09 in Market Share

6%

2%

8%

0%

2%

1%

1%

1%

5%

3%

2%

5%

1%

1%

2%

1%

9%

7%

7%

4%

15%

30%

5.99%

0.09%

0.65%

0.85%

0.89%

1.17%

1.43%

1.52%

1.66%

1.85%

2.11%

2.29%

2.33%

2.39%

2.83%

3.02%

4.99%

5.51%

7.10%

7.44%

19.40%

26.16%

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% 35.00%

Others

TOFAS

DAEWOO

FIAT

OPEL

BRILLIANCE

Proton

BMW

Suzuki

Honda

DAIHATSU

MITSUBISHI

MERCEDES

SKODA

VW

RENAULT

TOYOTA

Nissan

Speranza

KIA

Chevrolet

HYUNDAI

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

24

Sponsored By

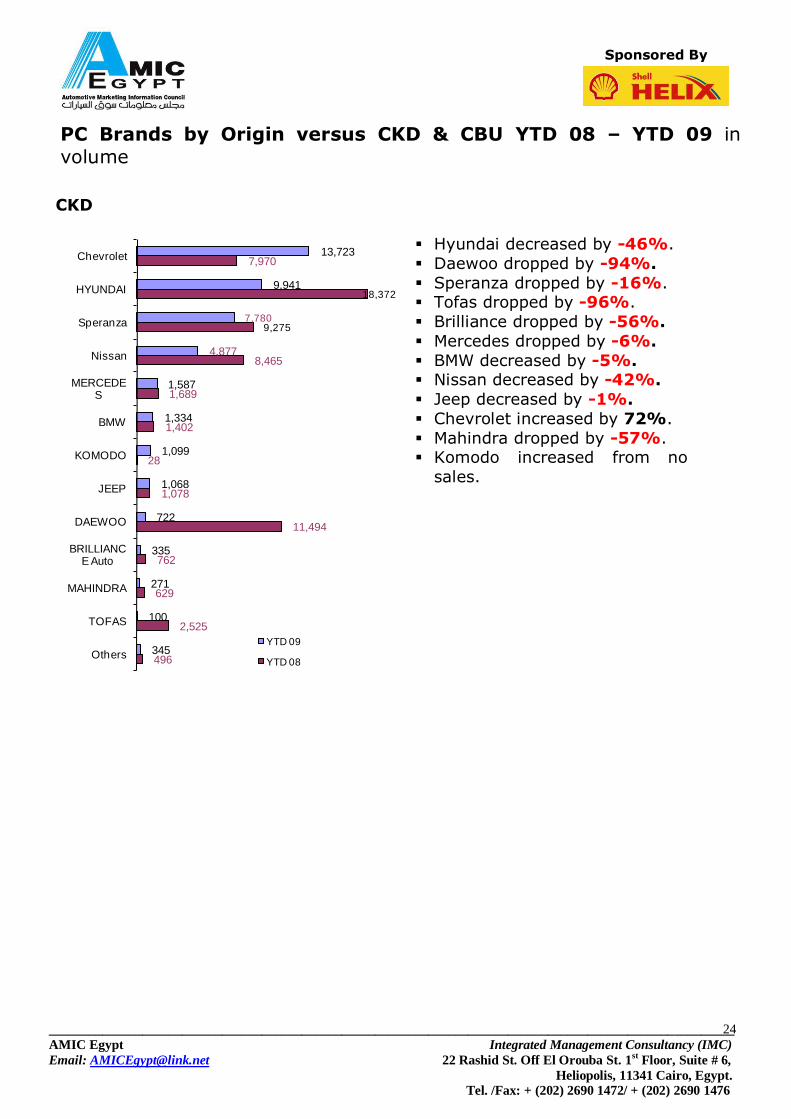

PC Brands by Origin versus CKD & CBU YTD 08 – YTD 09 in

volume

CKD

496

2,525

629

762

11,494

1,078

28

1,402

1,689

8,465

9,275

18,372

7,970

345

100

271

335

722

1,068

1,099

1,334

1,587

4,877

7,780

9,941

13,723

Others

TOFAS

MAHINDRA

BRILLIANCE Auto

DAEWOO

JEEP

KOMODO

BMW

MERCEDES

Nissan

Speranza

HYUNDAI

Chevrolet

YTD 09

YTD 08

Hyundai decreased by -46%.

Daewoo dropped by -94%.

Speranza dropped by -16%. Tofas dropped by -96%.

Brilliance dropped by -56%.

Mercedes dropped by -6%.

BMW decreased by -5%. Nissan decreased by -42%.

Jeep decreased by -1%.

Chevrolet increased by 72%.

Mahindra dropped by -57%. Komodo increased from no

sales.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

25

Sponsored By

CBU

3,876

1,001

477

1,911

606

191

2,222

303

1,458

1,380

7,582

3,704

2,536

7,011

1,540

3,387

1,316

13,397

12,992

6,194

24,934

3,045

77

354

800942

955

980

994

1,219

1,586

1,841

2,045

2,339

2,532

2,644

3,138

3,347

5,525

7,752

8,243

19,018

Others

Speranza

BMW

SEAT

FIAT

BRILLIANCE Auto

OPEL

MERCEDES

Nissan

Proton

Suzuki

HONDA

DAIHATSU

MITSUBISHI

SKODA

VW

RENAULT

TOYOTA

Chevrolet

KIA

HYUNDAI

YTD 09

YTD 08

Hyundai dropped by -24%.

Toyota dropped by -59%.

Mitsubishi dropped -64%.

Renault increased 154%.

Chevrolet dropped by -40%. VW decreased by -7%.

Honda dropped by -45%.

BMW increased by -26%.

Mercedes increased by 228%. Daihatsu dropped by -8%.

Proton increased by 15%.

Opel dropped by -56%.

Nissan dropped by -16%. Fiat increased by 55%.

Seat dropped by -58%.

Suzuki dropped by -76%.

Speranza dropped by -92%. Kia increased by 33%.

Brilliance increased by 400%.

Skoda increased by 72%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

26

Sponsored By

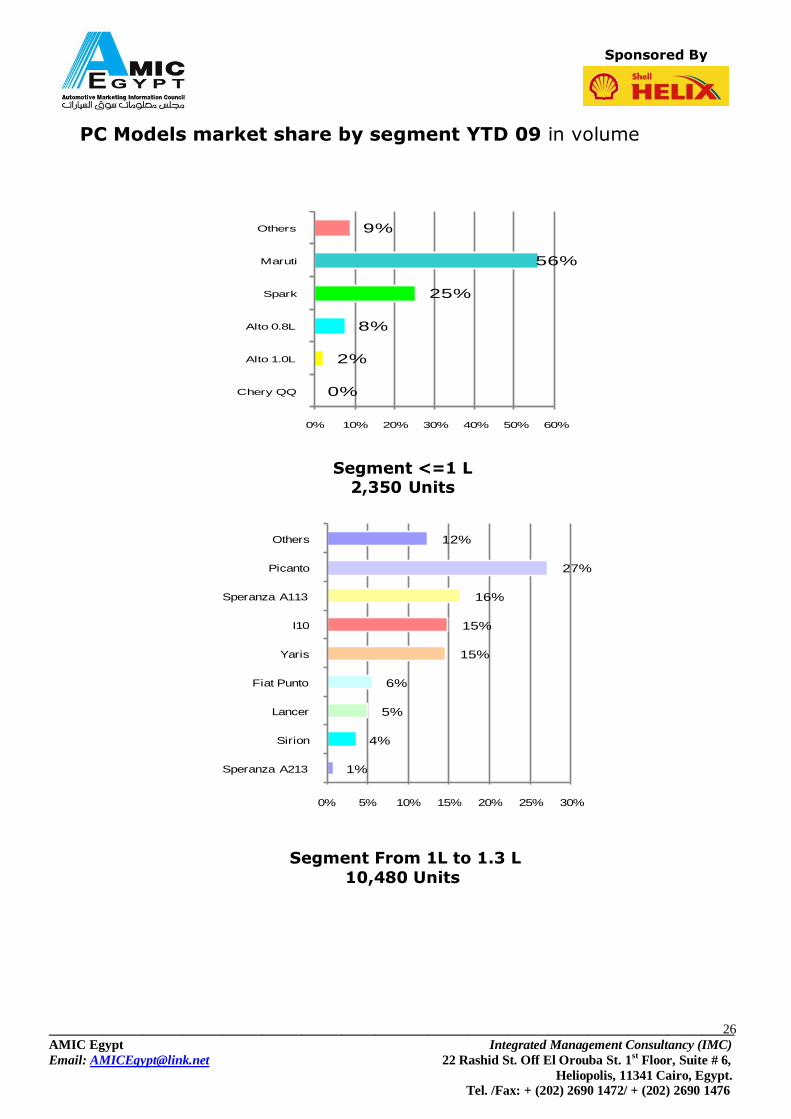

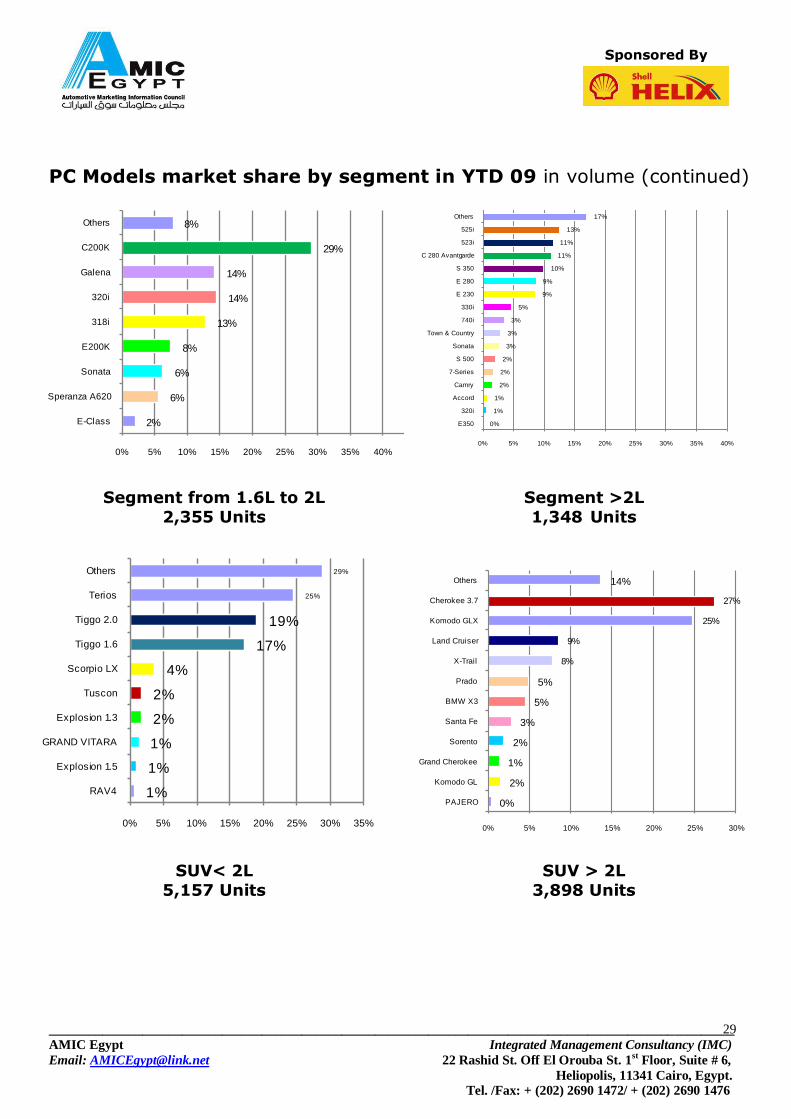

PC Models market share by segment YTD 09 in volume

0%

2%

8%

25%

56%

9%

0% 10% 20% 30% 40% 50% 60%

Chery QQ

Alto 1.0L

Alto 0.8L

Spark

Maruti

Others

Segment <=1 L 2,350 Units

1%

4%

5%

6%

15%

15%

16%

27%

12%

0% 5% 10% 15% 20% 25% 30%

Speranza A213

Sirion

Lancer

Fiat Punto

Yaris

I10

Speranza A113

Picanto

Others

Segment From 1L to 1.3 L

10,480 Units

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

27

Sponsored By

PC Models market share by segment YTD 09 in volume

(continued)

1%

2%

3%

3%

7%

11%

16%

48%

9%

0% 10% 20% 30% 40% 50% 60%

Symbol

CITY

Rio

Avanza 1.5

Verna Viva

Aveo 1.4

Aveo 1.5

Chevrolet Lanos

Others

Segment from 1.3L to 1.5L

21,719 Units

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

28

Sponsored By

PC Models market share by segment YTD 09 in volume

(continued)

0.4%

0.5%

0.8%

0.8%

0.8%

0.9%

1.0%

1.0%

1.1%

1.1%

1.2%

1.3%

1.5%

2.3%

2.3%

2.7%

2.7%

4.1%

4.4%

5.0%

5.7%

5.9%

7.6%

11.7%

15.0%

18.1%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0%

Astra

Passat

Cerato

Focus

Logan MCV

Tiida

OCTAVIA A4

Persona

Nubira

Gen2

C180

Brilliance FRV

Jetta

Civic

Getz

Matrix

Lancer 1.6

Corolla NG 1.6

New Cerato

Speranza A516

New Accent

OPTRA

Sunny1.6

Elantra

Verna 1.6

Others

Segment from 1.5L to 1.6L

65,253 Units

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

29

Sponsored By

PC Models market share by segment in YTD 09 in volume (continued)

2%

6%

6%

8%

13%

14%

14%

29%

8%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

E-Class

Speranza A620

Sonata

E200K

318i

320i

Galena

C200K

Others

0%

1%

1%

2%

2%

2%

3%

3%

3%

5%

9%

9%

10%

11%

11%

13%

17%

0% 5% 10% 15% 20% 25% 30% 35% 40%

E350

320i

Accord

Camry

7-Series

S 500

Sonata

Town & Country

740i

330i

E 230

E 280

S 350

C 280 Avantgarde

523i

525i

Others

Segment from 1.6L to 2L

2,355 Units

Segment >2L

1,348 Units

1%

1%

1%

2%

2%

4%

17%

19%

25%

29%

0% 5% 10% 15% 20% 25% 30% 35%

RAV4

Explosion 1.5

GRAND VITARA

Explosion 1.3

Tuscon

Scorpio LX

Tiggo 1.6

Tiggo 2.0

Terios

Others

0%

2%

1%

2%

3%

5%

5%

8%

9%

25%

27%

14%

0% 5% 10% 15% 20% 25% 30%

PAJERO

Komodo GL

Grand Cherokee

Sorento

Santa Fe

BMW X3

Prado

X-Trail

Land Cruiser

Komodo GLX

Cherokee 3.7

Others

SUV< 2L

5,157 Units

SUV > 2L

3,898 Units

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

30

Sponsored By

PC by Model YTD 08 – YTD 09 in volume (>800 cars)

45,750

393

8,858

1,055

1,943

2,636

1,380

1,659

-

4,800

3326

3,453

5,065

1641

2937

6,298

4,243

4,030

1,130

-

5,913

7,970

10,185

8,465

7,845

17,293

-

39,513

20

31

356

531

691

732

737

1,307

1,318

1,508

1,514

1,524

1,677

1,714

1,746

1,770

2,679

2,835

2,848

3,280

3,376

3,731

3,865

4,877

7,660

9,756

10,347

Others

SHAHIN 1.4

LANOS 1.5

New Passat

LANCER 1.3

NUBIRA

Gen 2

VECTRA

Tiggo 2.0

Suzuki Maruti

Civic 1.6

Verna Viva

Yaris

Terios

Speranza …

MATRIX

LANCER 1.6

COROLLA …

Picanto

New Cerato

Speranza …

AVEO 1.5

New Accent …

OPTRA

SUNNY

ELANTRA

Verna 1.6

Chevrolet …

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

31

Sponsored By

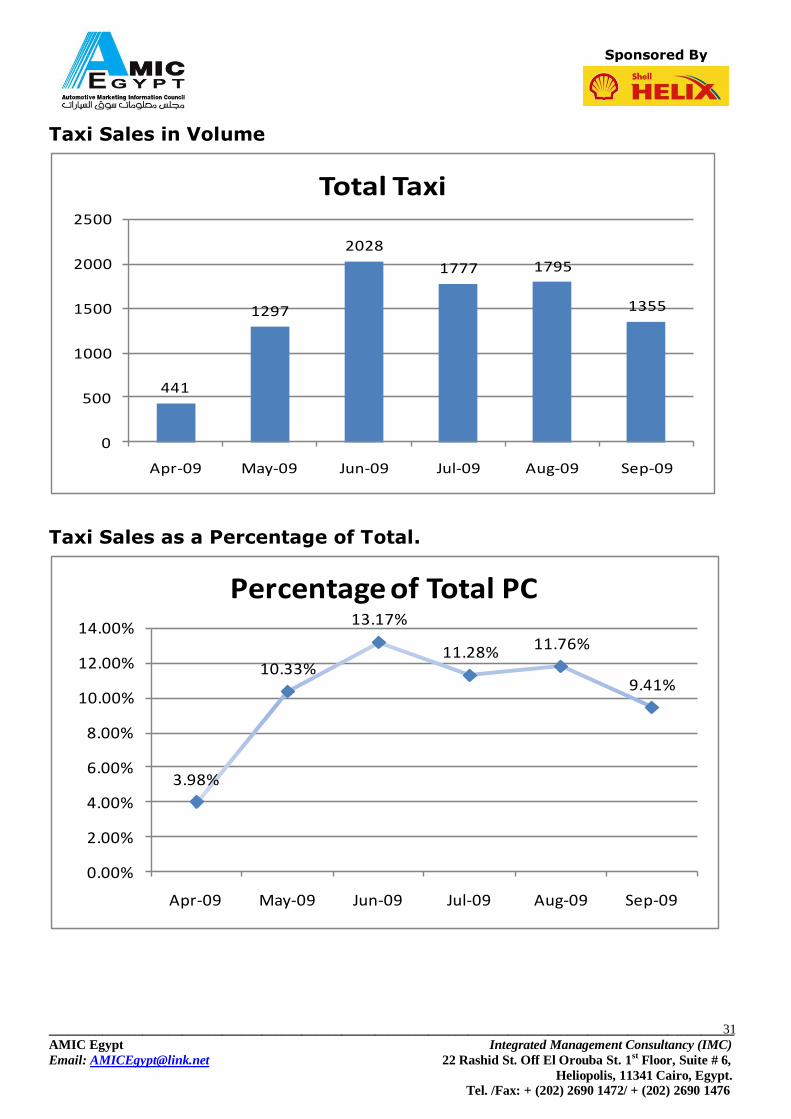

Taxi Sales in Volume

441

1297

2028

1777 1795

1355

0

500

1000

1500

2000

2500

Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09

Total Taxi

Taxi Sales as a Percentage of Total.

3.98%

10.33%

13.17%

11.28% 11.76%

9.41%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09

Percentage of Total PC

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

32

Sponsored By

2.3 BUSES

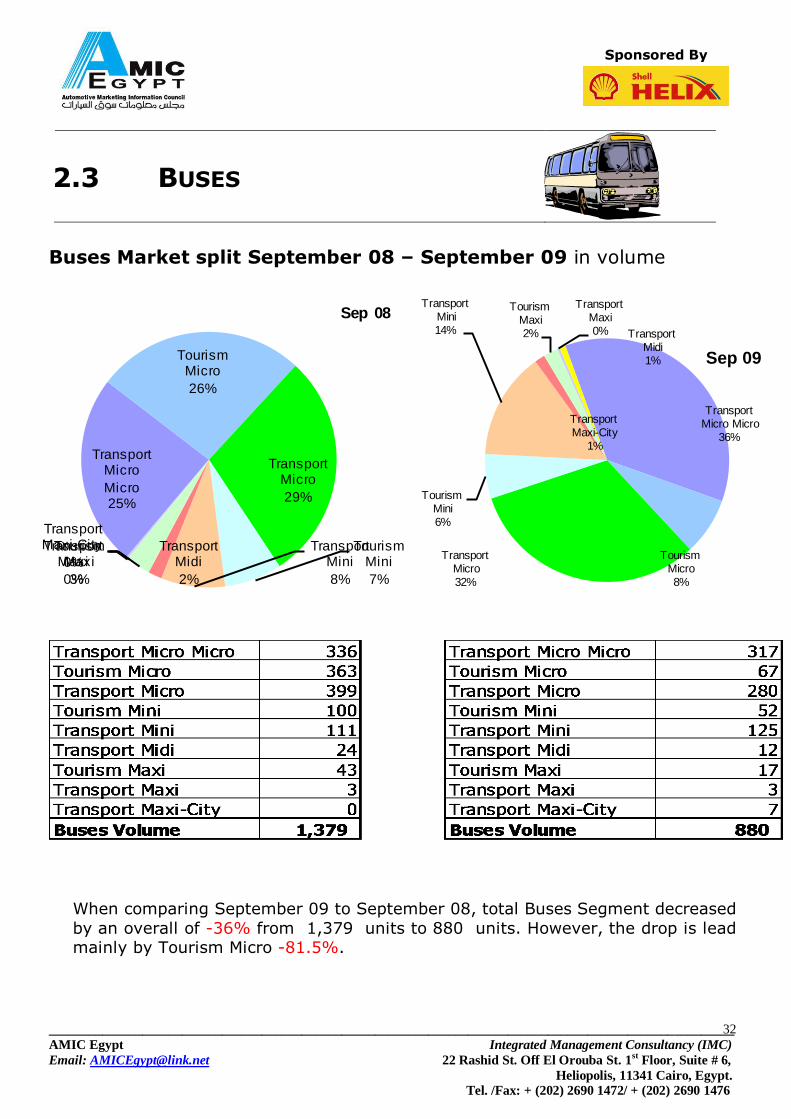

Buses Market split September 08 – September 09 in volume

Transport Micro

Micro25%

Tourism Micro

26%

Transport Micro

29%

Tourism Mini

7%

Transport Mini

8%

Transport Midi

2%

Tourism Maxi

3%

Transport Maxi

0%

Transport Maxi-City

0%

Sep 08

Transport Micro Micro

36%

Tourism Micro8%

Transport Micro32%

Tourism Mini6%

Transport Mini14% Transport

Midi1%

Tourism Maxi2%

Transport Maxi0%

Transport Maxi-City

1%

Sep 09

When comparing September 09 to September 08, total Buses Segment decreased

by an overall of -36% from 1,379 units to 880 units. However, the drop is lead mainly by Tourism Micro -81.5%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

33

Sponsored By

Buses Market split YTD 08 – YTD 09 in volume

Transport Micro Micro

21%

Tourism Micro21%

Transport Micro35%

Tourism Mini5%

Transport Mini10%Transport

Midi3%

Tourism Maxi3%

Transport Maxi2%

Transport Maxi-City

0%

YTD 08

Transport Micro Micro

33%

Tourism Micro16%

Transport Micro32%

Tourism Mini3%

Transport Mini12%

Transport Midi3% Tourism

Maxi1%

Transport Maxi0%

Transport Maxi-City

0%

YTD 09

When comparing YTD 09 to YTD 08, total Buses Segment dropped by an overall of -26% from 13,530 units to 9,969 units. Transport segments volume

decreased by -17.4%. Tourism segments volume decreased by -48.9%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

34

Sponsored By

Buses Market September 2009 sales analysis in volume

September 2009 sales volume is Lower than 2009 YTD avg. sales by -20.6%.

September 2009 sales volume is lower than 2008 YTD avg. sales by -41.5%.

September 2009 sales volume is lower than 2008 avg. sales by -39.6%.

September 2009 sales volume is lower than September 2008 sales by -36.2%.

September 2009 sales volume is lower than August 2009 sales by -23.7%.

881

1,119

1,319 1,384

1,141

1,004

1,087 1,154

880

1,465

1,721

1,558

1,479

1,441 1,377 1,436

1,674

1,379

Jan Feb Mar Apr May Jun Jul Aug Sep

2009 2008 2009 YTD Avg 2008 YTD Avg

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

35

Sponsored By

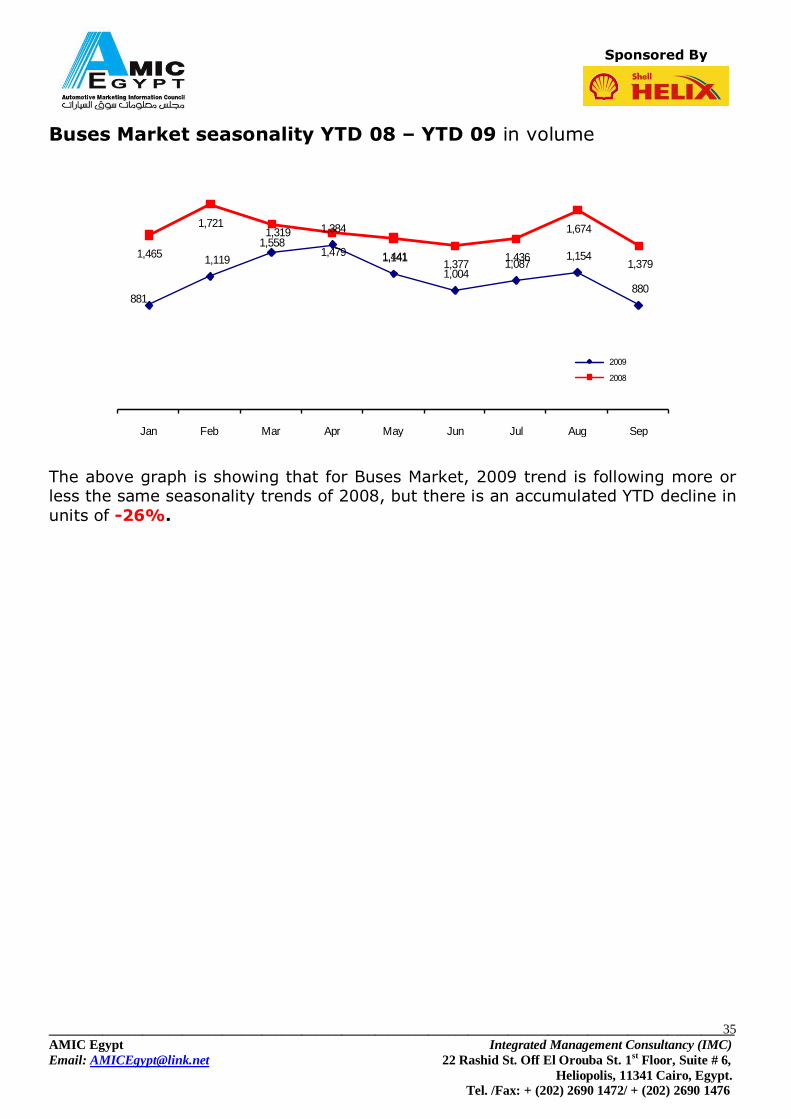

Buses Market seasonality YTD 08 – YTD 09 in volume

881

1,119

1,319 1,384

1,141

1,004 1,087

1,154

880

1,465

1,721

1,558 1,479 1,441

1,377 1,436

1,674

1,379

Jan Feb Mar Apr May Jun Jul Aug Sep

2009

2008

The above graph is showing that for Buses Market, 2009 trend is following more or less the same seasonality trends of 2008, but there is an accumulated YTD decline in

units of -26%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

36

Sponsored By

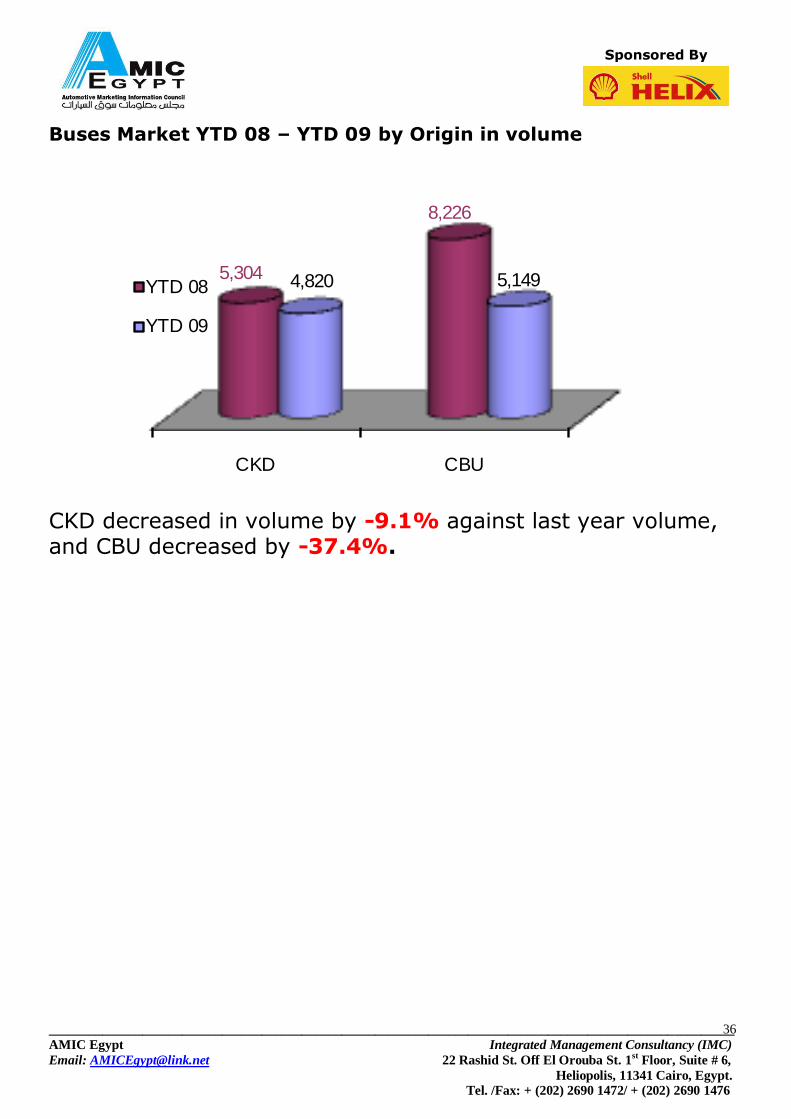

Buses Market YTD 08 – YTD 09 by Origin in volume

CKD CBU

5,304

8,226

4,820 5,149 YTD 08

YTD 09

CKD decreased in volume by -9.1% against last year volume, and CBU decreased by -37.4%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

37

Sponsored By

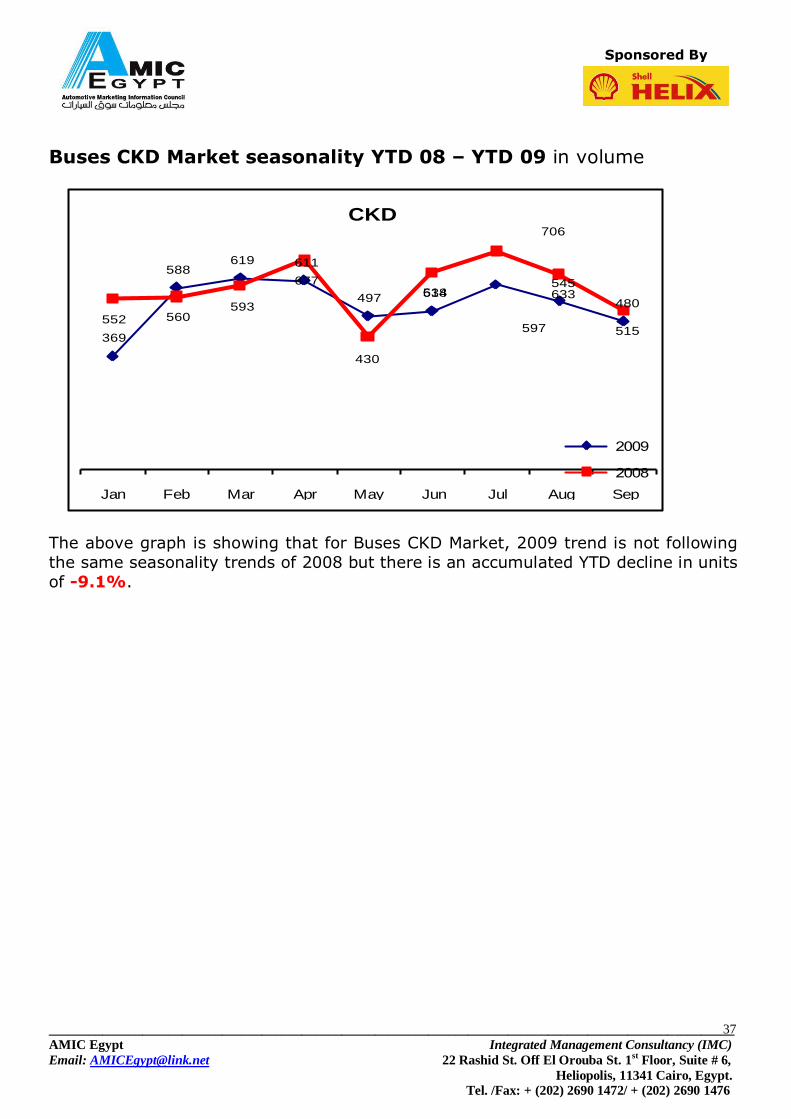

Buses CKD Market seasonality YTD 08 – YTD 09 in volume

369

588 619 611

497 514

597

545

480

552 560 593

677

430

638

706

633

515

Jan Feb Mar Apr May Jun Jul Aug Sep

CKD

2009

2008

The above graph is showing that for Buses CKD Market, 2009 trend is not following

the same seasonality trends of 2008 but there is an accumulated YTD decline in units

of -9.1%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

38

Sponsored By

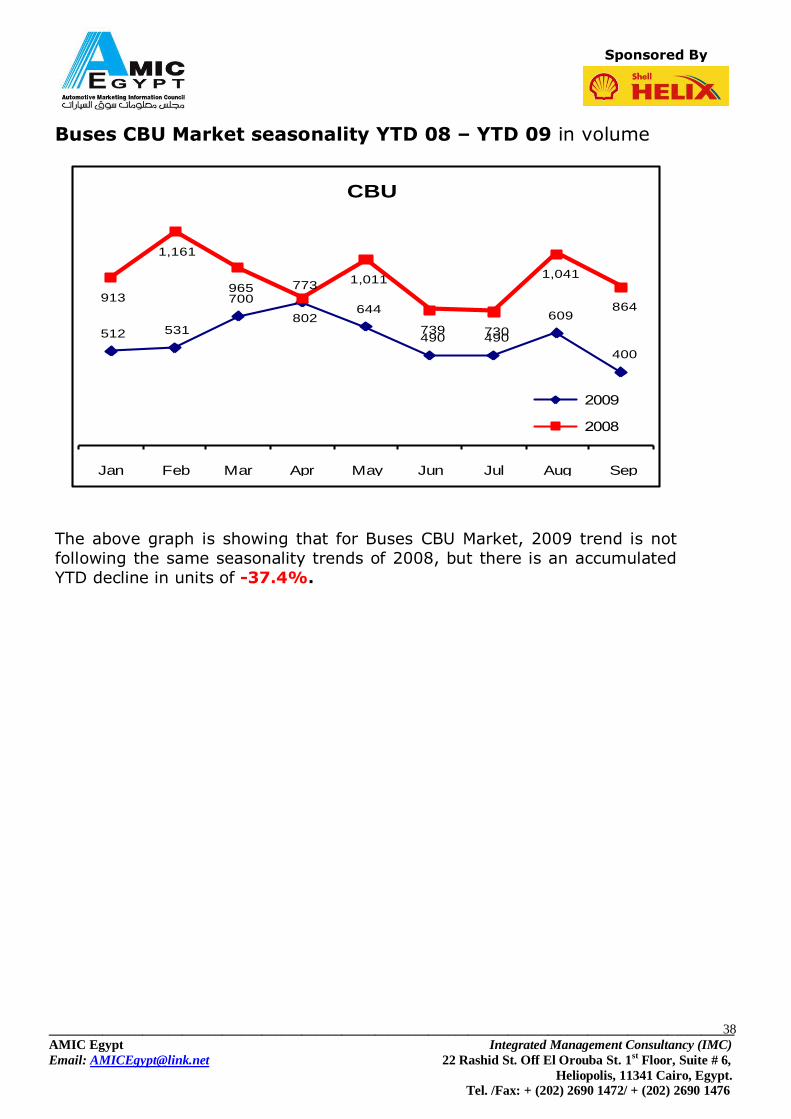

Buses CBU Market seasonality YTD 08 – YTD 09 in volume

512 531

700 773

644

490 490

609

400

913

1,161

965

802

1,011

739 730

1,041

864

Jan Feb Mar Apr May Jun Jul Aug Sep

CBU

2009

2008

The above graph is showing that for Buses CBU Market, 2009 trend is not

following the same seasonality trends of 2008, but there is an accumulated

YTD decline in units of -37.4%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

39

Sponsored By

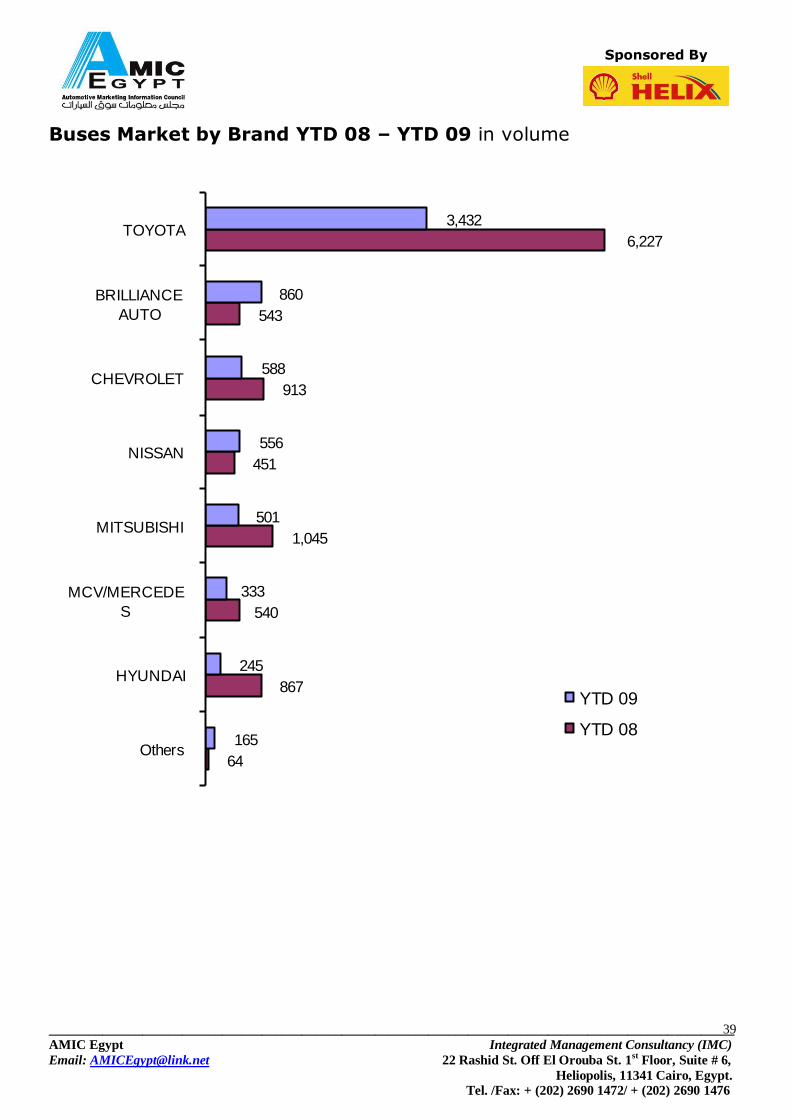

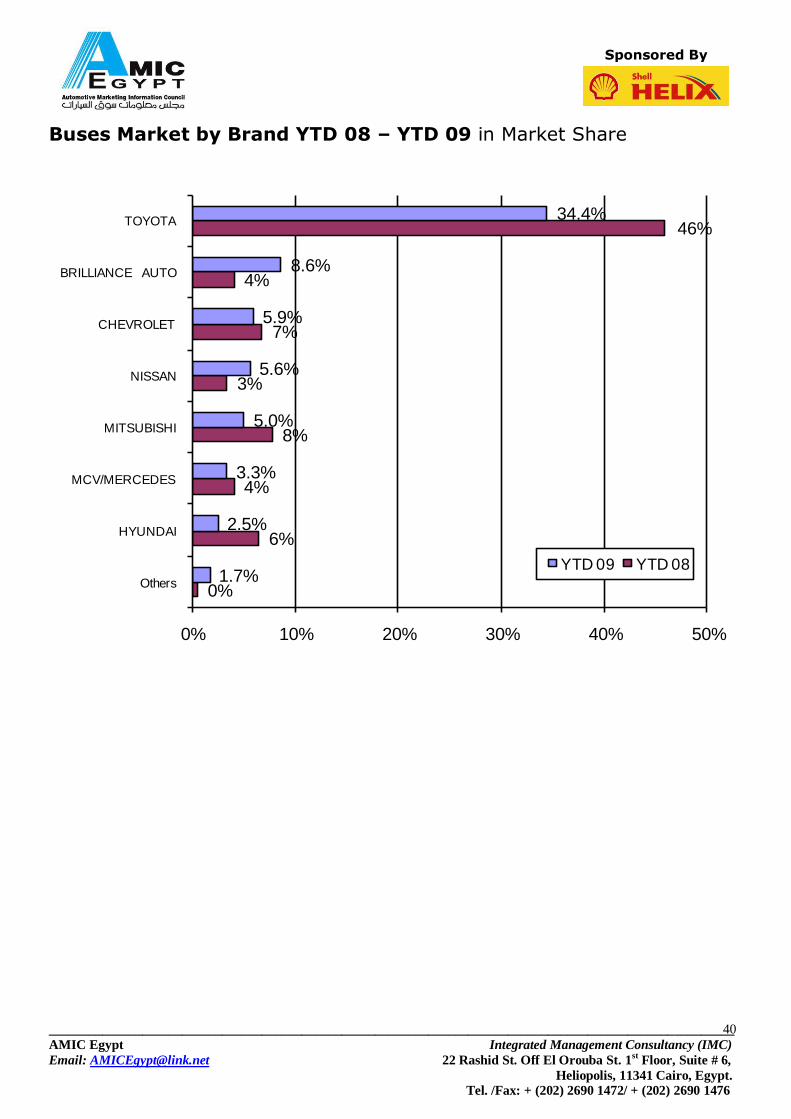

Buses Market by Brand YTD 08 – YTD 09 in volume

64

867

540

1,045

451

913

543

6,227

165

245

333

501

556

588

860

3,432

Others

HYUNDAI

MCV/MERCEDE

S

MITSUBISHI

NISSAN

CHEVROLET

BRILLIANCE

AUTO

TOYOTA

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

40

Sponsored By

Buses Market by Brand YTD 08 – YTD 09 in Market Share

0%

6%

4%

8%

3%

7%

4%

46%

1.7%

2.5%

3.3%

5.0%

5.6%

5.9%

8.6%

34.4%

0% 10% 20% 30% 40% 50%

Others

HYUNDAI

MCV/MERCEDES

MITSUBISHI

NISSAN

CHEVROLET

BRILLIANCE AUTO

TOYOTA

YTD 09 YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

41

Sponsored By

Buses Models Market Share By Segment YTD 09 In Volume

Toyota

Hiace57%

Nissan

Urvan16%

Junbei

Haise27%

Mitsubishi

L3000%

Others

0%

Toyota

Hiace84%

H-1

STAREX SVX

0%

Others

16%

Transport Micro Segment 3,199 Units

Tourism Micro Segment 1,612 Units

GM-NPR66P

2%

GB Cruiser C16%

MCV 240E12%

JNB12283%

GB Cruiser

C34%

Civilian5%

GM-NPR66L

32%

GB Cruiser C2/AD

4%

Others32%

Transport Mini Segment

1,158 Units

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

42

Sponsored By

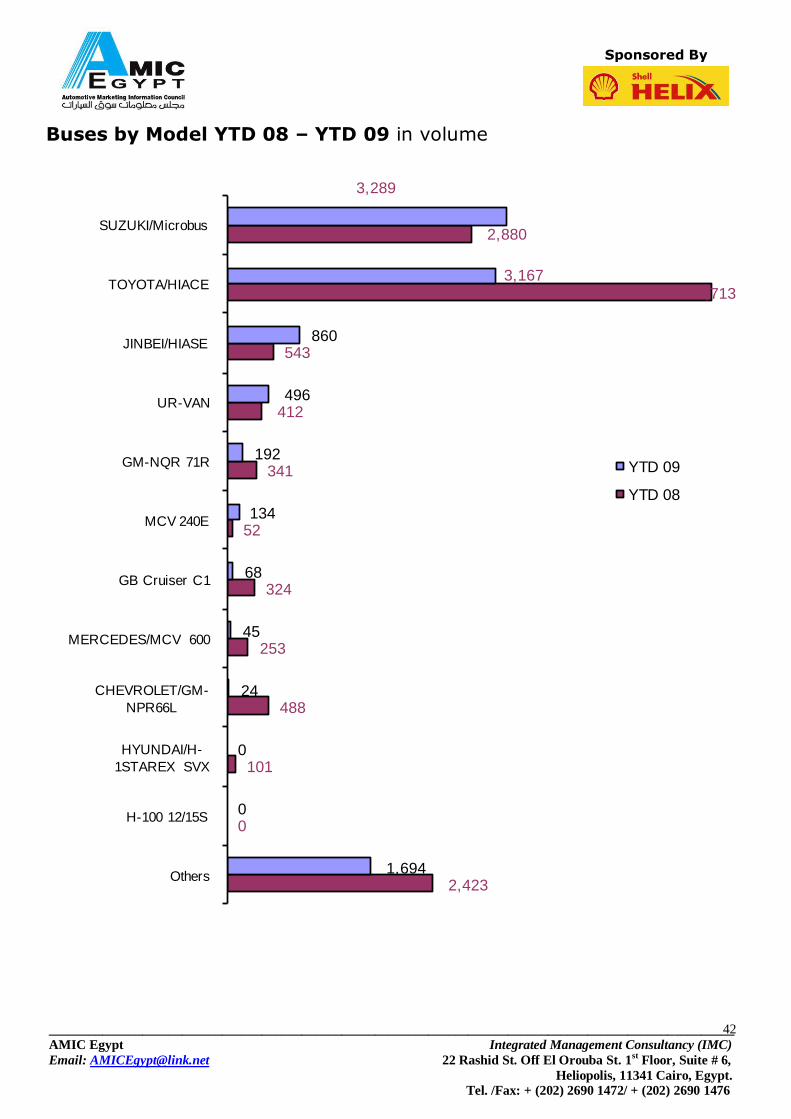

Buses by Model YTD 08 – YTD 09 in volume

2,423

0

101

488

253

324

52

341

412

543

5,713

2,880

1,694

0

0

24

45

68

134

192

496

860

3,167

3,289

Others

H-100 12/15S

HYUNDAI/H-

1STAREX SVX

CHEVROLET/GM-

NPR66L

MERCEDES/MCV 600

GB Cruiser C1

MCV 240E

GM-NQR 71R

UR-VAN

JINBEI/HIASE

TOYOTA/HIACE

SUZUKI/Microbus

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

43

Sponsored By

2.4 TRUCKS

Trucks Market split September 09 – September 08 in volume

Mini Pickup/ Van

3%

Pickup83% Light Trucks

1%

Light Medium

Trucks10%

medium Trucks

0%

Heavy Trucks

3%

Sep 08

Mini Pickup/

Van2%

Pickup73%

Light Trucks

5%

Light Medium Trucks15%

medium Trucks

0%Heavy Trucks

3%

Sep 09

Mini Pickup /Van 115 Mini Pickup /Van 57

Pickup 2928 Pickup 1772

Light Trucks 33 Light Trucks 119

Light Medium Trucks 351 Light Medium Trucks 368

Medium Trucks 4 Medium Trucks 35

Heavy Trucks 93 Heavy Trucks 73

Truck Volume 3,524 Truck Volume 2,424

Trucks segment decreased by -31%, mainly due to Pickup segment’s decrease by

-39% and the Light Medium Trucks segment increased by 5%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

44

Sponsored By

Trucks Market split YTD 08 – YTD 09 in volume

Mini Pickup /Van4%

Pickup73%

Light Trucks

4%

Light Medium Trucks

16%

Medium Trucks

0%

Heavy Trucks

3%

YTD 08

Mini Pickup /Van4%

Pickup69%

Light Trucks

6%

Light Medium Trucks15%

Medium Trucks

2%

Heavy Trucks

4%

YTD 09

Mini Pickup /Van 1,413 -29% Mini Pickup /Van 1,000

Pickup 24,701 -33% Pickup 16,654

Light Trucks 1,512 -4% Light Trucks 1,448

Light Medium Trucks 5,309 -31% Light Medium Trucks 3,658

Medium Trucks 128 154% Medium Trucks 325

Heavy Trucks 952 7% Heavy Trucks 1,014

Truck Volume 34,015 -29% Truck Volume 24,099

Trucks segment dropped by -29%, mainly due to Pickup segment’s decrease by

-33% which has the highest contribution in volume.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

45

Sponsored By

Trucks Market September 08 sales analysis in volume

September 2009 sales volume is lower than 2009 YTD avg. sales by -9.5%. September 2009 sales volume is lower than 2008 YTD avg. sales by -35.9%.

August 2009 sales volume is lower than 2008 avg. sales by -36.3%.

September 2009 sales volume is lower than September 2008 sales by -31.2%.

September 2009 sales volume is lower than August 2009 sales by -4.0%.

2,779 2,716

2,392

3,131

2,232

3,130

2,770

2,525 2,424

4,038

4,215

4,006

3,732

3,907

4,187

3,232 3,174

3,524

Jan Feb Mar Apr May Jun Jul Aug Sep

2009 2008 2009 YTD Avg 2008 YTD Avg

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

46

Sponsored By

Trucks Market Seasonality YTD 08 – YTD 09 in volume

2,779 2,716

2,392

3,131

2,232 3,130

2,770 2,525 2,424

4,038 4,215

4,006 3,732

3,907 4,187

3,232 3,174

3,524

Jan Feb Mar Apr May Jun Jul Aug Sep

2009

2008

The above Trend analysis graph is showing that for Trucks; 2009 is following more or

less the same seasonality trends of 2008 but showing an accumulated YTD decline of -29%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

47

Sponsored By

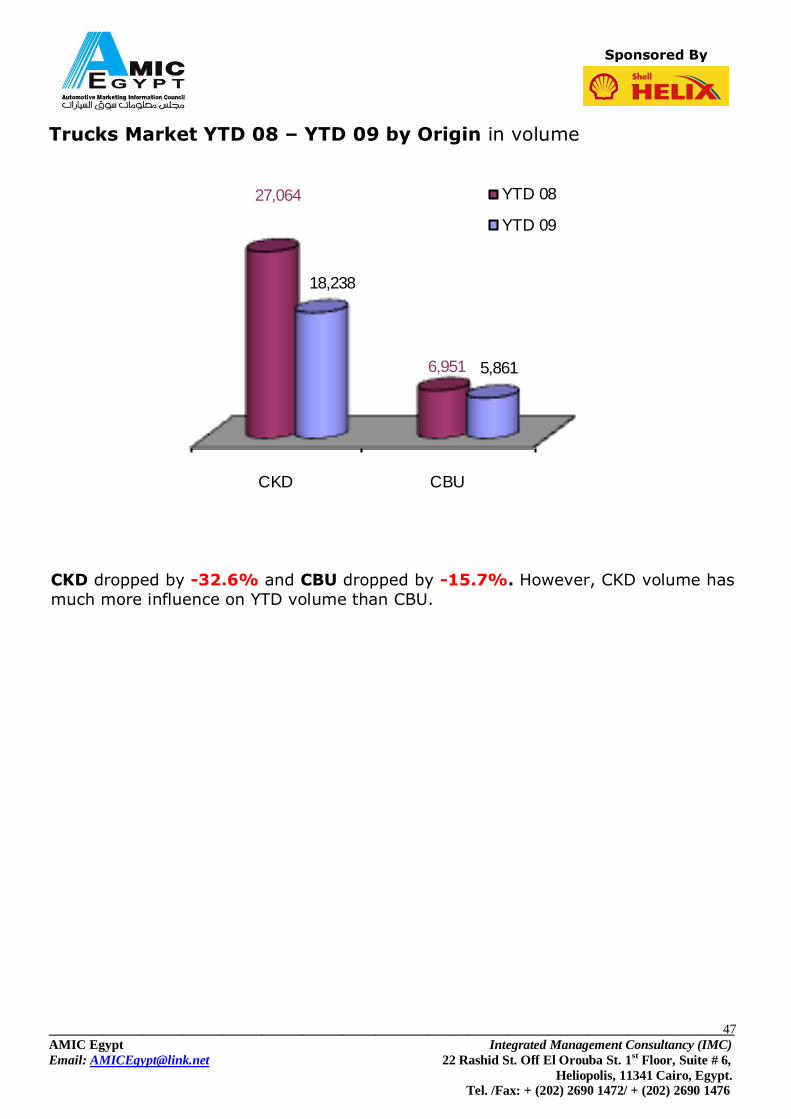

Trucks Market YTD 08 – YTD 09 by Origin in volume

CKD CBU

27,064

6,951

18,238

5,861

YTD 08

YTD 09

CKD dropped by -32.6% and CBU dropped by -15.7%. However, CKD volume has

much more influence on YTD volume than CBU.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

48

Sponsored By

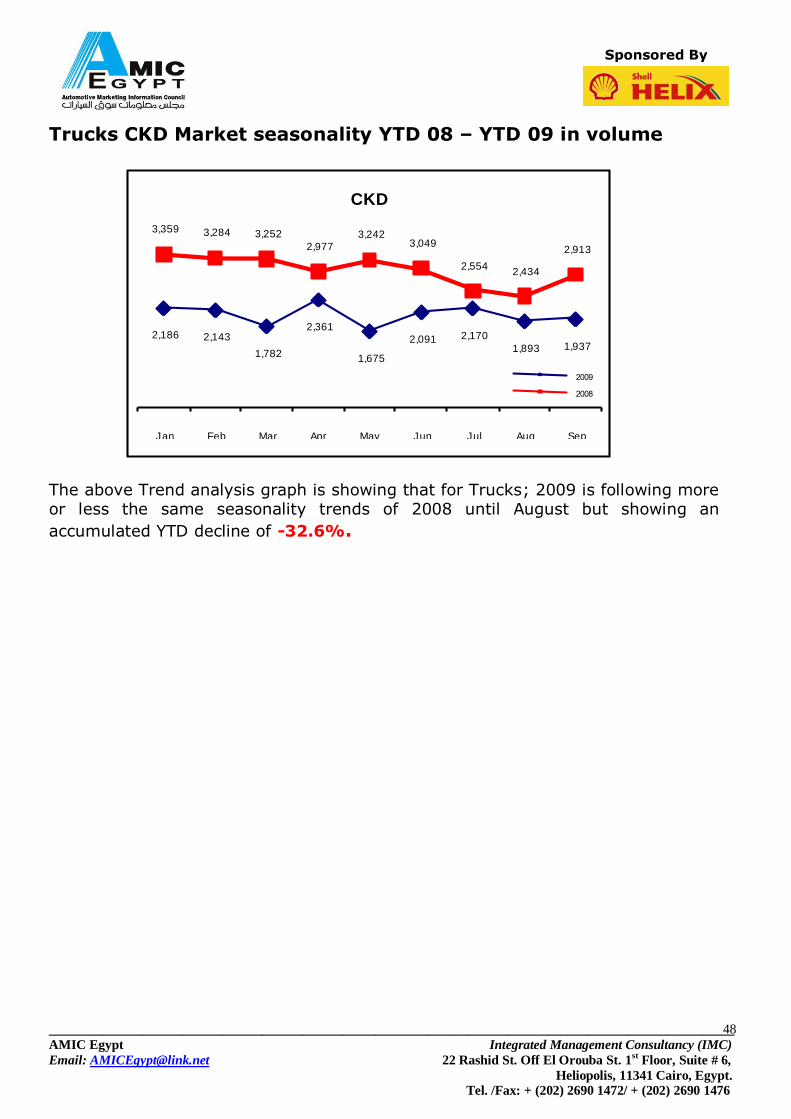

Trucks CKD Market seasonality YTD 08 – YTD 09 in volume

2,186 2,143

1,782

2,361

1,675

2,091 2,170

1,893 1,937

3,359 3,284 3,252

2,977 3,242

3,049

2,554 2,434

2,913

Jan Feb Mar Apr May Jun Jul Aug Sep

CKD

2009

2008

The above Trend analysis graph is showing that for Trucks; 2009 is following more or less the same seasonality trends of 2008 until August but showing an

accumulated YTD decline of -32.6%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

49

Sponsored By

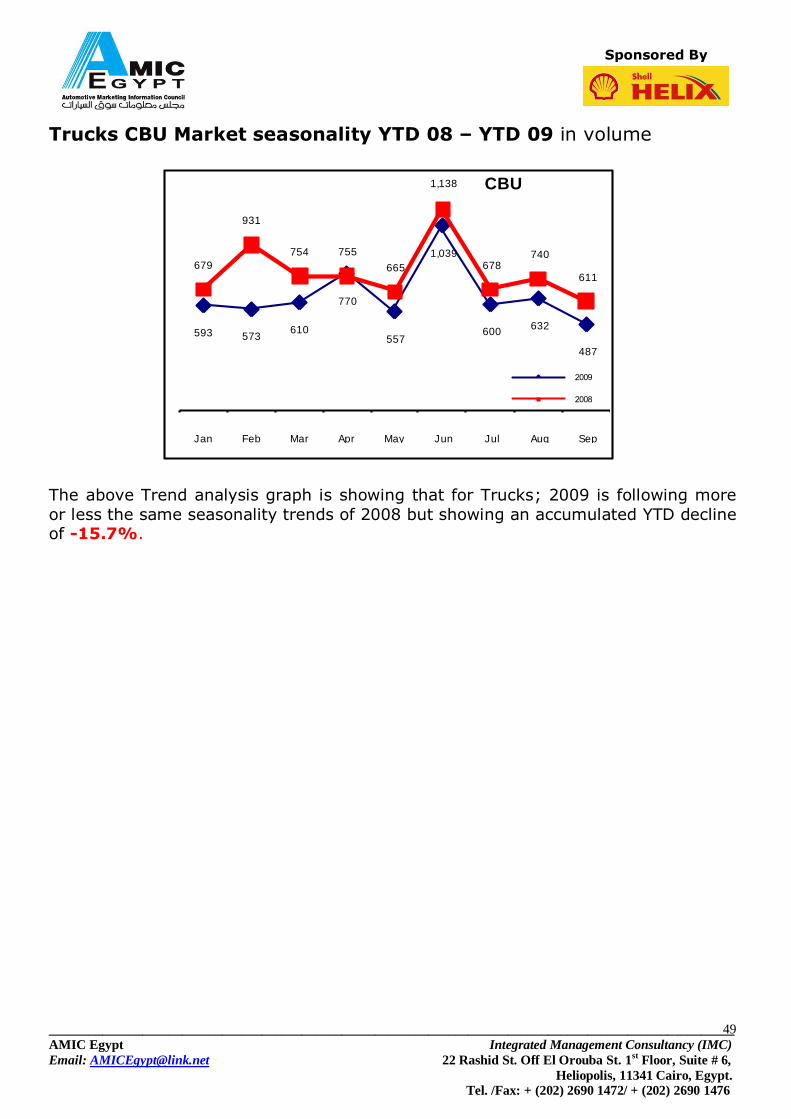

Trucks CBU Market seasonality YTD 08 – YTD 09 in volume

593 573 610

770

557

1,039

600 632

487

679

931

754 755

665

1,138

678 740

611

Jan Feb Mar Apr May Jun Jul Aug Sep

CBU

2009

2008

The above Trend analysis graph is showing that for Trucks; 2009 is following more

or less the same seasonality trends of 2008 but showing an accumulated YTD decline of -15.7%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

50

Sponsored By

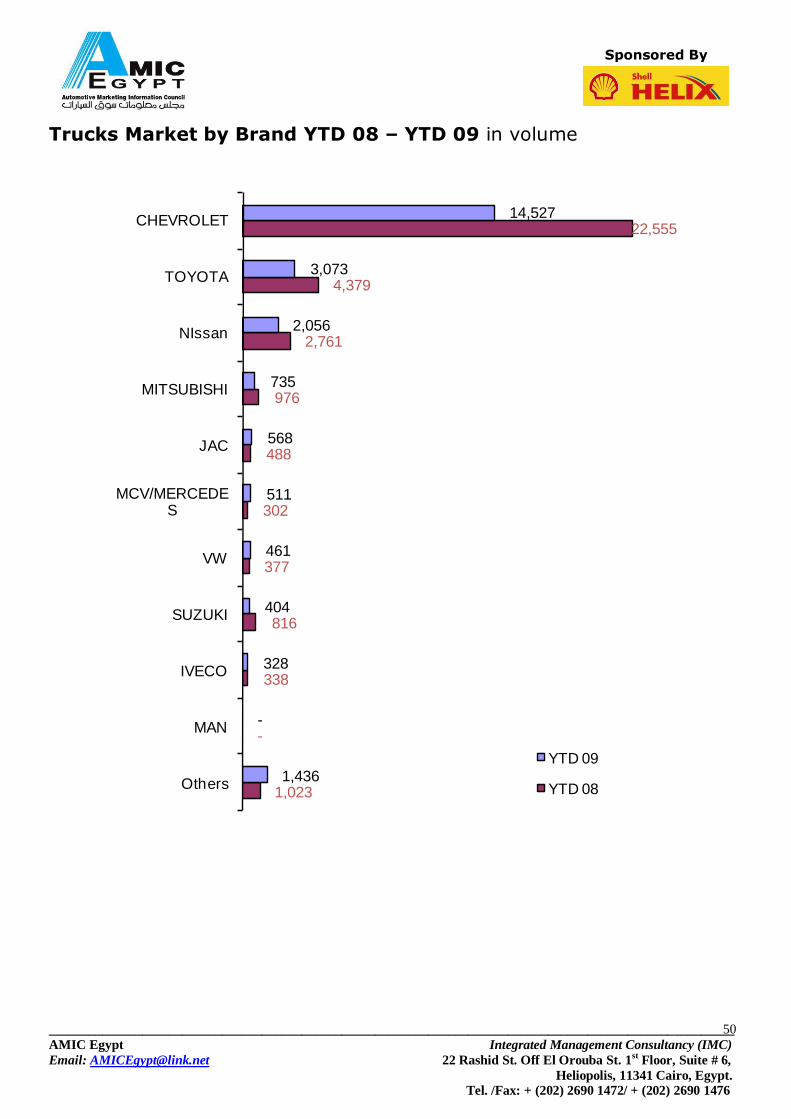

Trucks Market by Brand YTD 08 – YTD 09 in volume

1,023

-

338

816

377

302

488

976

2,761

4,379

22,555

1,436

-

328

404

461

511

568

735

2,056

3,073

14,527

Others

MAN

IVECO

SUZUKI

VW

MCV/MERCEDES

JAC

MITSUBISHI

NIssan

TOYOTA

CHEVROLET

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

51

Sponsored By

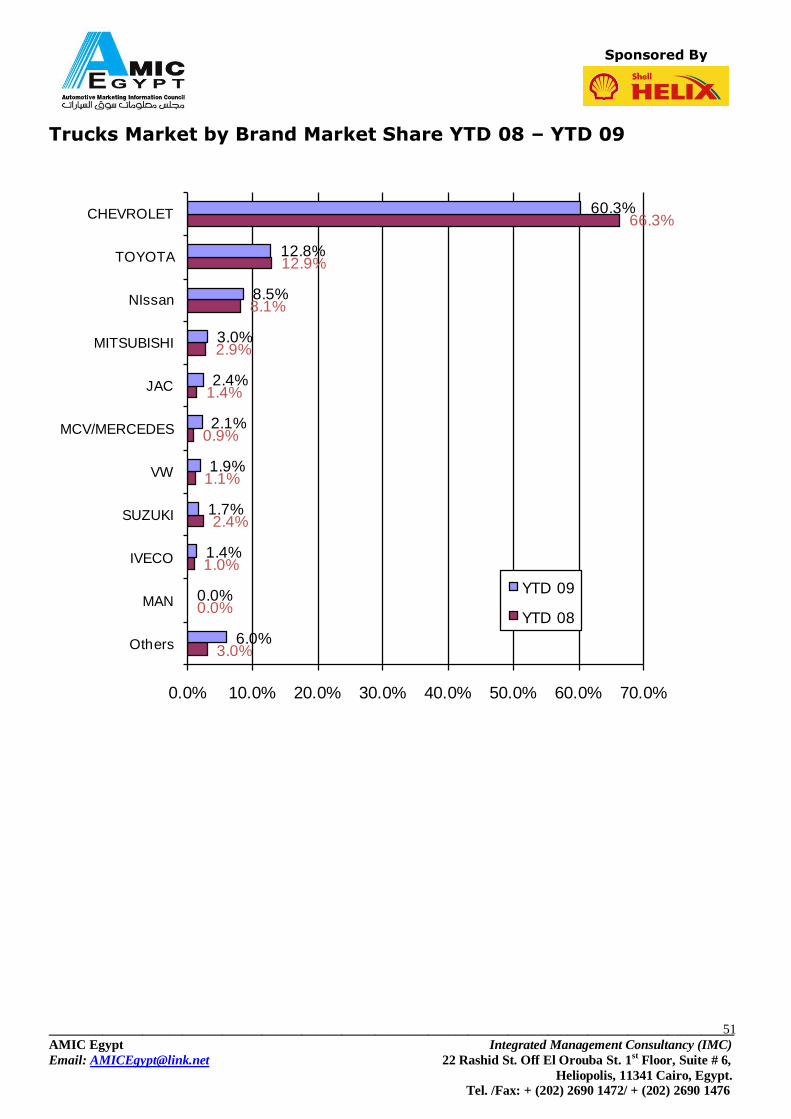

Trucks Market by Brand Market Share YTD 08 – YTD 09

3.0%

0.0%

1.0%

2.4%

1.1%

0.9%

1.4%

2.9%

8.1%

12.9%

66.3%

6.0%

0.0%

1.4%

1.7%

1.9%

2.1%

2.4%

3.0%

8.5%

12.8%

60.3%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Others

MAN

IVECO

SUZUKI

VW

MCV/MERCEDES

JAC

MITSUBISHI

NIssan

TOYOTA

CHEVROLET

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

52

Sponsored By

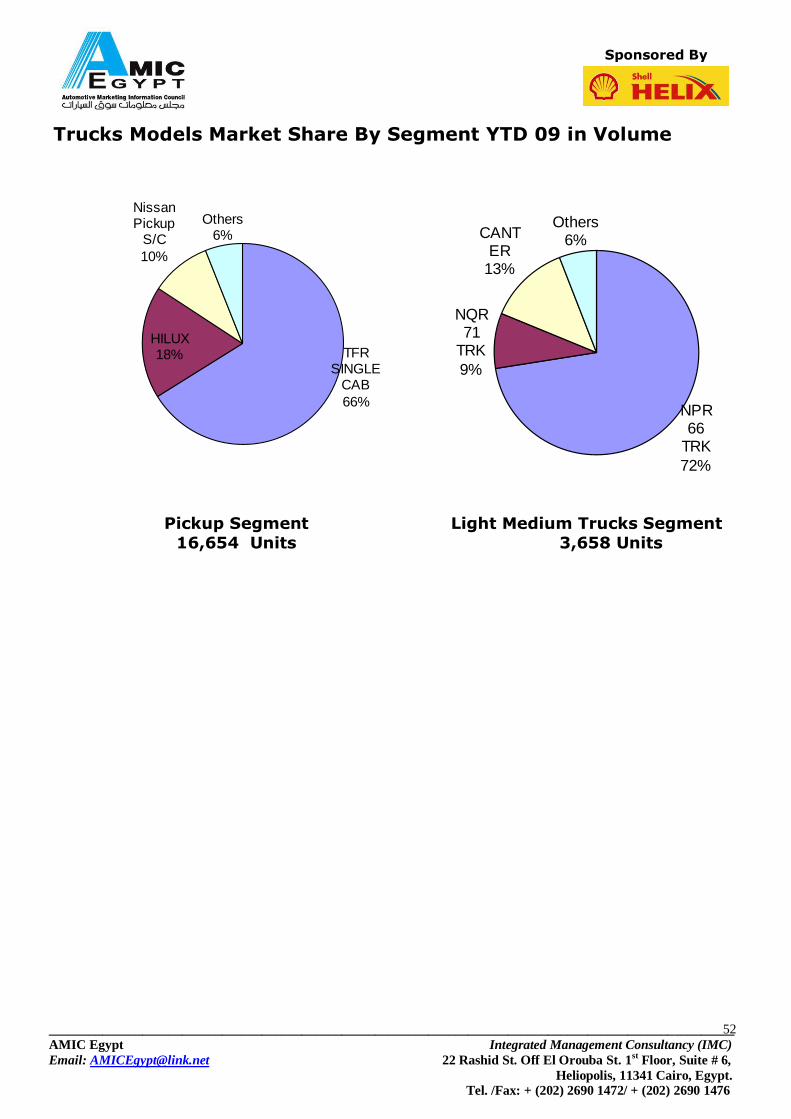

Trucks Models Market Share By Segment YTD 09 in Volume

TFR SINGLE

CAB

66%

HILUX18%

Nissan Pickup

S/C

10%

Others6%

NPR 66

TRK

72%

NQR 71

TRK

9%

CANTER

13%

Others6%

Pickup Segment

16,654 Units

Light Medium Trucks Segment

3,658 Units

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

53

Sponsored By

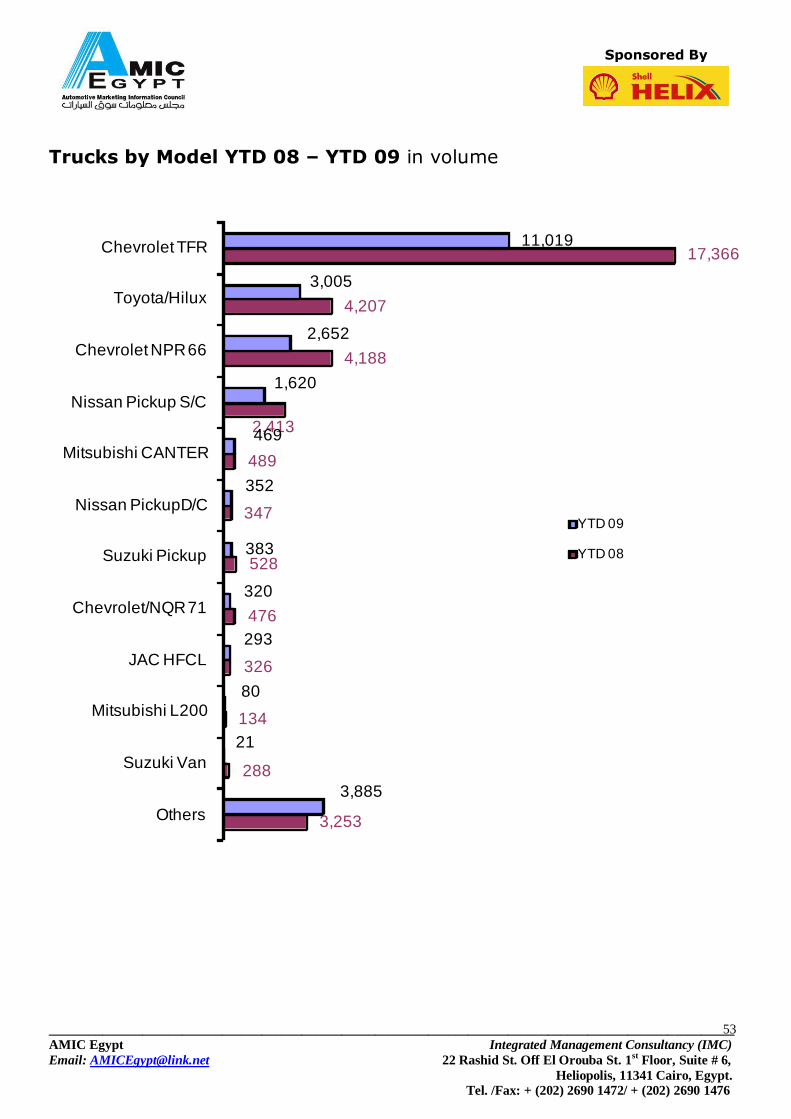

Trucks by Model YTD 08 – YTD 09 in volume

3,253

288

134

326

476

528

347

489

2,413

4,188

4,207

17,366

3,885

21

80

293

320

383

352

469

1,620

2,652

3,005

11,019

Others

Suzuki Van

Mitsubishi L200

JAC HFCL

Chevrolet/NQR 71

Suzuki Pickup

Nissan PickupD/C

Mitsubishi CANTER

Nissan Pickup S/C

Chevrolet NPR 66

Toyota/Hilux

Chevrolet TFR

YTD 09

YTD 08

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

54

Sponsored By

3. MONTHLY NEWS FLASH 15TH TO 15TH

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

55

Sponsored By

3.1 EGYPT MACRO FLASH

Africans Come Together

Al-Ahram Weekly, 22-28 Oct. 09

African trade ministers are scheduled to meet in Cairo on 27 October for three days to agree on a common position in preparation for the upcoming negotiations on the Doha Development Agenda (DDA) due to take place at the seventh WTO ministerial meeting in Geneva, 30 November. Egypt currently heads the African Group in the WTO. Also expected to take part are the trade ministers of

India, Mexico, China and Brazil. The conference will examine the effect of the global slowdown on the WTO and the liberalization of trade. African countries are expected to insist that development be at the heart of the DDA.

Transport Opportunities

Al-Ahram Weekly, 22-28 Oct. 09

INVESTMENT opportunities in the transport sector were highlighted last week by Egyptian Transport Minister Mohamed Mansour during a meeting organized by the American Chamber of Commerce in Egypt (AmCham). The minister spotlighted investment opportunities, but mentioned funding as a major challenge. Some 33 highways and 18 bridges are under construction, and work is in progress for the third line of the underground metro and 200 new railway stations are planned for coming years.

While pointing out opportunities, Mansour also mentioned achievements in the transport sector. He pointed out that some 2,300 kilometers of roads have been built across Egypt since 2005, including 360 kilometers in Upper Egypt.

Crises In The Balance

Al-Ahram Weekly, 22-28 Oct. 09

An official report evaluating the impact of the international financial crisis on the Egyptian economy was released last week. The report, entitled "A Follow Up of Economic and Social Performance During the Fiscal Year 2008/2009", said the crisis had reduced the growth rate from 7% to 4.7% in

2008/2009, with a subsequent increase in unemployment. Furthermore, less employment opportunities are expected in the coming few years.

According to the report, economic sectors that were badly affected by the crisis were those directly related to international markets, while other sectors succeeded to increase their share in growth due to the application of government policies aimed at improving the environment of internal markets. These include IT, construction, infrastructure, wholesale trade and transportation. Some other sectors remained unchanged, such as agriculture and social services, including education and health.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

56

Sponsored By

The most negatively affected sectors, according to the report, are Suez Canal revenues, tourism and oil exports. Moreover, the remittances of Egyptian workers abroad dropped from LE9.4 billion in 2007/2008 to LE7.6 billion in 2008/2009.

Due to the reduction in the international demand and price instability, Egypt's oil exports decreased by 24% in 2008/2009. Foreign direct investment was reduced by 38.7% (from $13 billion in 2007/2008 to $8.1 billion in 2008/2009), while revenues from Egyptian investments in the financial sector worldwide were also reduced by 41% due to a reduction in interest rates worldwide. Investments in the industrial sector were also reduced, from LE42 billion in 2007/2008 to LE30 billion in 2008/2009.Moreover, the report stated that successful monetary policies applied by the Central Bank of Egypt helped control the budget deficit. As a result, the negative impact on people's living standards and poverty rates was minor.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

57

Sponsored By

3.1 EGYPT MACRO FLASH

Recession Brings Inflation?

Al-Ahram Weekly, 22-28 Oct. 09

The Central Agency for Public Mobilization and Statistics (CAPMAS) announced last week that the inflation rate in Egypt increased in September 2009 to reach 10.8% compared to 8.4% in August.

CAPMAS Chairman Abu Bakr El-Guindi explained that the reason behind the increase was higher prices of basic commodities, particularly food products presenting 47 per cent of total products.

Correlatives

Al-Ahram Weekly, 22-28 Oct. 09

The findings of a new study confirm that investing in infrastructure pays off in terms of economic growth. When the Egyptian government decided it was going to inject LE15 billion into infrastructure projects to stimulate the economy out of slowdown it not only had job creation in mind but also growth. While it is assumed that investing in infrastructure promotes growth, no one had actually measured it. This is what Norman Loayza and Rei Odawara, economists at the World Bank, tried to do in their study, "Infrastructure and Economic Growth in Egypt.

The study, presented last week at the Egyptian Centre for Economic Studies (ECES) by Loayza examines the period from the early 1960s to 2005 to compare investment in infrastructure by Egypt to that of 150 other countries. It looks specifically at the areas of electricity generation, telecommunications, transportation, and water and sanitation.

In the area of transportation, the study examined road length and the quality of roads, railroads, port

facilities and air transport. In the area of electricity, energy operating capacity, power loss, access to electricity, and the reliability of the electricity supply were the focus. The authors also examine access to improved water and sanitation facilities. In all cases, Egypt was within the range of other countries of a similar income level. In some areas, like roads or cellular phone penetration, Egypt had done better than its peers.

Expenditure on infrastructure was also measured. In terms of total expenditure, Egypt was found to have spent an equivalent amount to its peers. But while infrastructure expenditure saw a large increase in the 1980s, the last 15 years saw a decline which could be normal because investment is higher at the beginning.

The study showed that a drop in sector-based investment accompanied the drop in total investment, with the largest drop registered in the electricity sector. And while the study noted increased private sector participation in transportation and telecommunications infrastructure investment, private sector participation in the electricity sector was minimal.

Comparison to Turkey showed that in both countries total expenditure on infrastructure decreased. However, in Turkey it was replaced by private investment, which did not happen in Egypt.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

58

Sponsored By

The goal of the study is to measure and quantify the impact of infrastructure on long-term growth. The study shows that infrastructure development supported and spurred growth overall. The growth effect, however, is small at the beginning. "By the end of the first decade it's 0.5%, and in the long run it adds 1.6% to the growth rate.For the best results, the authors recommend that increased infrastructure investment be measured, so as not to result in a fiscal burden. If a fiscal burden can be avoided, and if the quality of expenditure is improved, the effect of investment is proven to be larger.

Loayza further underlined that public infrastructure will not pay for itself. He pointed out that in the first five years, growth will only cover 35% of expenditure on infrastructure. That will rise to 50% by the second decade and 75% on the long run.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

59

Sponsored By

3.1 EGYPT MACRO FLASH

Business Climate Makeover

Al-Ahram Weekly 15-21 Oct. 09

A conference was held on the week of October to discuss the "Business Climate Development Strategy" to be implemented in Egypt for the first time, designed by the Organization for Economic Cooperation and Development (OECD), the World Bank and the EU.

The strategy aims to support Middle East and North Africa (MENA) countries in improving their business climates so as to raise competitiveness and growth rates. An integrated and all-inclusive system will be designed to assess, create and enforce governments' reform policies relevant to the business climate.

It also aims to attract investment by accelerating the reform process. The strategy will assess the pros and cons of the existing business climate and identify and prioritize areas for reform. It will also provide technical assistance in designing and implementing reform policies. The work will be implemented in coordination with concerned ministries, donors, international organizations, chambers of commerce, business associations and investors' federations. the strategy will as well tackle investment policies, the development of public and private sector participation, taxation and trade, small- and medium-sized enterprises, investment legislation, regulations against corruption,

human development policies, methods of project financing and infrastructure projects.

Market Report:

Al-Ahram Weekly, 15-21 Oct. 09

Foreigners' purchases have supported the market since the start of October, offsetting the effect of local investors' profit taking transactions and Arab in the average value of daily transactions remained above the LE1 billion threshold and market experts believe it will exceed it in the coming period amid expectations of a soon to be seen revival in the market on the back of better economic indicators as well as strong third quarter results.

News on the macroeconomic front is positive, with the value of Egypt's international reserves

recording an 8.8 per cent month-on-month increase to reach $33.51 billion in September. The increase comes on the back of an influx of foreign currency revenues with the decline in tourism receipts easing through the month to 6.4 per cent compared to the 9.5 per cent in the first half of the year.

The increase in inflation that reached 10.8 per cent during September from nine per cent in August, mainly due to higher food prices, was not reflected in the market. But analysts believe that if the increase persists, the Central Bank of Egypt might resort to increasing interest rates after lowering them six times since the beginning of the year.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

60

Sponsored By

3.1 EGYPT MACRO FLASH

Business Made Easier

Al-Ahram Weekly, 01-07 Oct. 09

A package of new regulations is now being studied with an aim to further facilitate business start-ups and provide a more investment-friendly climate in Egypt. Osama Saleh, the newly appointed chairman of the General Authority for Investment and Free Zones (GAFI), announced last week that electronic registration and set-up of new companies will be effective starting today.

The electronic set-up of companies is expected to further improve Egypt's position in areas related to the ease of doing business. Notably, Egypt improved its rank with regards to starting up a business in the IFC's World Bank Doing Business Report 2009, to 24th compared to 126th four years ago.

Another major improvement is decentralizing services provided by GAFI's main headquarters in Cairo. At present, the authority has opened four branches and nine offices in different governorates

that provide similar services

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

61

Sponsored By

3.2. AUTOMOTIVE INDUSTRY LOCAL

NEWS CLIPS

The All New E-Class now in Egypt: Al Sayarat, Oct. 10, 09.

Mercedes Benz Celebrates the launching of the first batch of the new E-300 Model Assembled in Egypt, available with both manual and automatic transmission (2996 CC). The 6-cylinder power-plant in the E 300 delivers a combination of smoothness and power for refined performance.

Launch of the New Chevrolet Captiva By GM and Mansour

Chevrolet. Al Ahram, Oct. 16, 09.

Chevrolet Captiva is the recently offered four-wheel drive compact SUV by both, Mansour Chevrolet and GM. Captiva system interacts with the ESP and ABS systems, enhancing driver control and

safety margins and available in 3200 cm3 engine that produces 223 in both LT and LTZ types with a 5-speed automatic transmission.

The New Porsche Panamera In Egypt: Al Ahram, Oct. 16, 09.

The new Porsche Panamera is finally launched in Egypt by SMG - the sole distributor of Porsche in Egypt. Panamera combines sporting driving dynamics, a generous and versatile interior, and a supreme driving comfort of a Gran Turismo. Joining the 911, Boxter, Cayman sports cars, and the four-wheel drive Cayenne, the Panamera is officially the fourth Porsche Sedan model series..

The Panamera comes with 1931 mm width and 1418 mm height, both wider and lower than other four-door models.

Egypt's Ghabbour Auto (GA) plans to raise 1.5 billion Egyptian

pounds ($274 million) from selling bonds to fund expansion. Egypt News, Oct 16, 09.

The bonds will have a nominal value of 100 pounds with a maturity of as long as seven years, the Cairo-based company, known as GB Auto, said in a statement to the Egyptian Exchange today. The bonds will be offered to Egyptian and foreign investors, the company said. “The purpose of issuing the bonds is to fund the capital expansions and the company’s investments in the transport sector in Egypt and countries in the region,” Ghabbour Auto said in the statement. Bassem El-Shawy, head of investor relations at the company, declined to elaborate on the expansion

plans. Ghabbour Auto sells passenger cars, buses, trucks, trailers, motorbikes and tires. It reported a 72 percent decline in second-quarter net income in August on lower car sales.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

62

Sponsored By

3.2. AUTOMOTIVE INDUSTRY LOCAL

NEWS CLIPS

Customs down to 36% on 1600cc Vehicles: Al Ahram, Oct. 16, 09.

After signing the European Cooperation Agreement 6 years ago, the first action will take place starting January 2010 where there will be a reduction of 10% from the 40% collected on 1600 cc vehicles, this means that customs will be down to 36%.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

63

Sponsored By

3.3. AUTOMOTIVE INDUSTRY GLOBAL NEWS

CLIPS

Electric Cars: A Wide-Open Race

Business Week October 19, 2009.

The electric car is likely to emerge as one of the most transformational products of the current era. Given the effect of the auto industry on the rest of the economy, mass commercialization of the electric car will fundamentally transform not just that industry but others such as petroleum, electricity generation and distribution, steel, nonferrous materials, and chemicals. By reducing the world's dependence on crude oil, the electric car will reshape the structure of global trade. Importantly too, because electric cars have zero emissions, they also could dramatically reset the debate on global warming.

It's no wonder, then, that observers and analysts are caught up in frenzied discussions about who will win the great green-car race. What makes the contest particularly interesting is the fact that an all-electric car will be the first major new product in which, right from the start, the contestants include companies from not just the developed but also the developing economies.

Asian companies are among the leaders in the electric-car race. The Chinese company BYD, for instance, is determined to roll out its all-electric E3 and E6 models this year and has announced plans to bring the E6 to the U.S. in 2010. Japan's Mitsubishi Motors has already launched its electric car, the i MiEV. The boss of another Japanese automaker, Nissan's (NSANY) Carlos Ghosn, is, through Nissan's alliance with Renault, the boldest promoter of electric cars. Tata Motors (TAMO) in India has announced that it will introduce its all-electric Indica Vista EV in Norway this year.

GM Board to Discuss Opel Sale on Nov. 3

The Wall Street Journal. October 23, 2009.

A General Motors Co. executive said that the auto maker's board will discuss a letter from Germany's economy minister and recent changes to Magna International Inc.'s bid for GM's Opel unit at its regular meeting early next month.

"Work will continue to resolve remaining open points ... and complete all preparations for the signing of binding agreements should that be authorized by GM's board at the Nov. 3 meeting," John Smith, GM's lead negotiator, wrote in his blog on the corporate Web site.

_______________________________________________________________________________________________________

AMIC Egypt Integrated Management Consultancy (IMC)

Email: [email protected] 22 Rashid St. Off El Orouba St. 1st Floor, Suite # 6,

Heliopolis, 11341 Cairo, Egypt.

Tel. /Fax: + (202) 2690 1472/ + (202) 2690 1476

64

Sponsored By

3.3. AUTOMOTIVE INDUSTRY GLOBAL NEWS

CLIPS

Peugeot, Fiat Post Lower Revenue

The Wall Street Journal. October 22, 2009.

The car-scrapping schemes that caused a jump in auto sales in Europe during the second half of this year may have boosted manufacturer's volumes, but they've done nothing to revive flagging revenues and profits.

Both France's PSA Peugeot-Citroën and Italy's Fiat both reported that their vehicle sales perked up in the third quarter, but revenues declined at both companies and Fiat's profits took a hit from the

weak top-line performance.

Magna’s plans to acquire Opel, GM’s European arm, may face a

problem

The Economist. October 19, 2009.

As the week commences when General Motors is set to conclude a deal to sell Opel, its European arm, the American car giant finds that the European Union has thrown a spanner into the engine bay. Late on Friday October 16th the European Union’s competition commissioner, Neelie Kroes, tentatively suggested what everyone else saw plainly when the bidding process for Opel concluded in early September: the winner got a big push from Germany that gave it an unfair advantage. Mr Kroes belatedly has come to the conclusion that this might fall foul of the EU’s competition rules.

The potential area of dispute is over €4.5 billion ($6.7 billion) of German state aid to Opel that was apparently only available if GM chose Magna, a Canadian car-parts maker, and its partners, Sberbank, Russia’s largest retail bank, and GAZ, Russia’s second-largest carmaker, to take over the

business. Magna’s bid was alluring to Germany’s government as the Canadian firm promised to keep open all four of Opel’s factories in Germany with minimal job losses, regardless of their efficiency. This would look appealing at any time but saving German jobs was a priority as elections loomed at the end of September. Without a favorable deal for Opel Chancellor Angela Merkel may have suffered at the polls and thus found it trickier to pull together her favored coalition.

![[EN|DE] IMC Information Management Compliance | English & German](https://img.pdfslide.us/doc/110x75/577dade11a28ab223f8fb2cd/ende-imc-information-management-compliance-english-german.jpg)