Embed Size (px)

Citation preview

EGYPT: THE ROAD AHEAD February 2016

Projects - Egypt Synopsis of Oriental Petrochemicals Company

2

Products 180,000 MTA Polypropylene

Status Operational

Acquisition Date Q4 2012

Location Suez, Egypt

SNAPSHOT COMMERCIAL STRUCTURE

xc

3

Oriental Petrochemicals Corporation Operational - 180,000 tons per annum Polypropylene Plant

4

Oriental Petrochemicals Corporation Operational Snapshots / new bagging design introduced

Private and Confidential

Projects - Egypt Synopsis of Egypt Hydrocarbon Corporation

5

Products 1,060 MTPD Ammonium Nitrate 850 MTPD Nitric Acid

Status Commissioning

Start-Up Q1 2016

Project Cost (approx.)

US$ 570 million

Location Suez, Egypt

SNAPSHOT COMMERCIAL STRUCTURE

xc

In 2010, EHC won the Euromoney Project Finance award for the Deal of Year

Egypt Hydrocarbon Corporation Commissioning – 350,000 tons per annum Mining Grade Ammonium Nitrate Plant

6

Macroeconomic Rationale GDP vs. Industrialization: Rationale for TPC development

2

The Lewis Curve demonstrates that Egypt is lagging as compared to its peers in economic development. This would suggest that capital-intensive investments offer significant national economic growth potential.

1000

10000

100000

0 10 20 30 40 50 60

Vietnam

Indonesia

India

Philippines

Egypt

Thailand

China

Turkey

Malaysia

South KoreaTaiwan

Brazil

Japan

Hong Kong

Singapore

PRIMARY

PRODUCTION

LABOUR INTENSIVE

MFG

CAPITAL

INTENSIVE

MFG

SERVICES

GDP/

CAPITA $

YEARS FROM BEGINNING OF INDUSTRIALISATION

THE LEWIS CURVE

Source: IMF 2010 nominal GDP/capita data, International eChem, ICIS Consulting

8

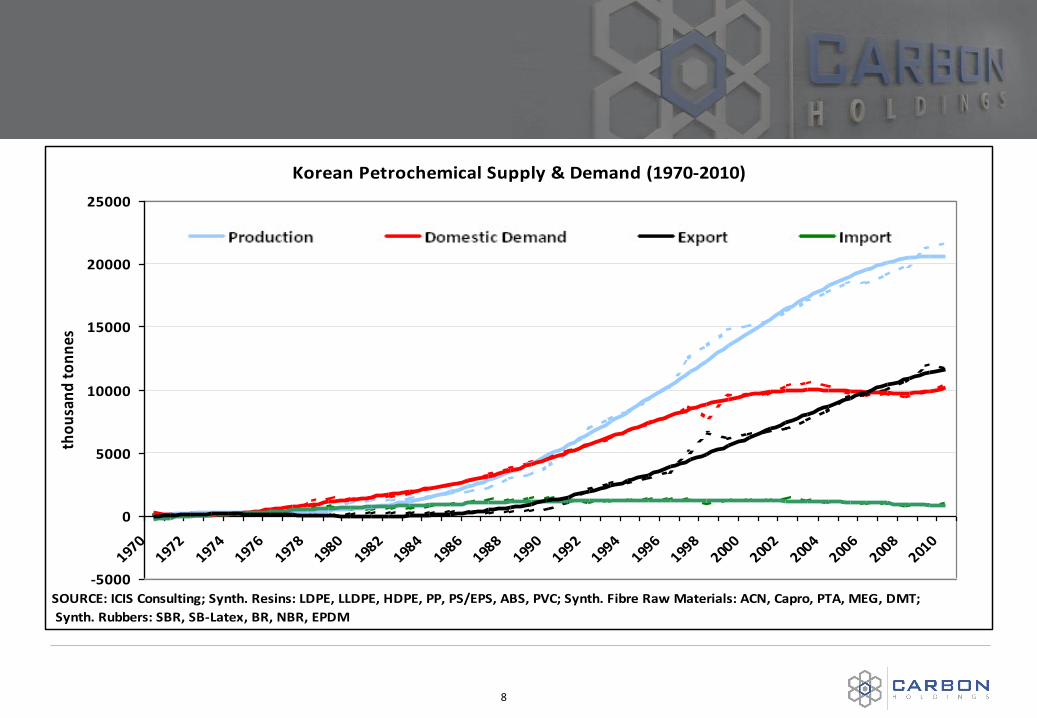

Korean Petrochemical Supply & Demand (1970-2010)

-5000

0

5000

10000

15000

20000

25000

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

tho

usa

nd

to

nn

es

SOURCE: ICIS Consulting; Synth. Resins: LDPE, LLDPE, HDPE, PP, PS/EPS, ABS, PVC; Synth. Fibre Raw Materials: ACN, Capro, PTA, MEG, DMT;

Synth. Rubbers: SBR, SB-Latex, BR, NBR, EPDM

9

Korean Petrochemical Capacity vs Net Trade Balance

-20

-10

0

10

20

30

40

50

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011N

et

Trad

e B

alan

ce (

US$

bil

lio

ns)

-10000

-5000

0

5000

10000

15000

20000

25000

Inst

alle

d r

esi

n/r

ub

be

r/fi

bre

cap

acit

y ('

00

0 t

on

ne

s)

Net trade balance (left scale)

Installed resin/rubber/fibre capacity (right scale)

SOURCE: ICIS Consulting; Synth. Resins: LDPE, LLDPE, HDPE, PP, PS/EPS, ABS, PVC; Synth. Fibre Raw Materials: ACN, Capro, PTA, MEG, DMT;

Synth. Rubbers: SBR, SB-Latex, BR, NBR, EPDM, IMF - Net trade balance.

10

Thai Petrochemical Capacity vs Net Trade Balance

-10

0

10

20

30

40

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Ne

t Tr

ade

Bal

ance

(U

S$ b

illi

on

s)

-5000

0

5000

10000

15000

20000

Inst

alle

d r

esi

n/r

ub

be

r/fi

bre

cap

acit

y ('

00

0 t

on

ne

s)Net trade balance (left scale)

Installed resin/rubber/fibre capacity (right scale)

SOURCE: ICIS Consulting; Synth. Resins: LDPE, LLDPE, HDPE, PP, PS/EPS, ABS, PVC; Synth. Fibre Raw Materials: ACN, Capro, PTA, MEG, DMT;

Synth. Rubbers: SBR, SB-Latex, BR, NBR, EPDM, IMF - Net trade balance.

11

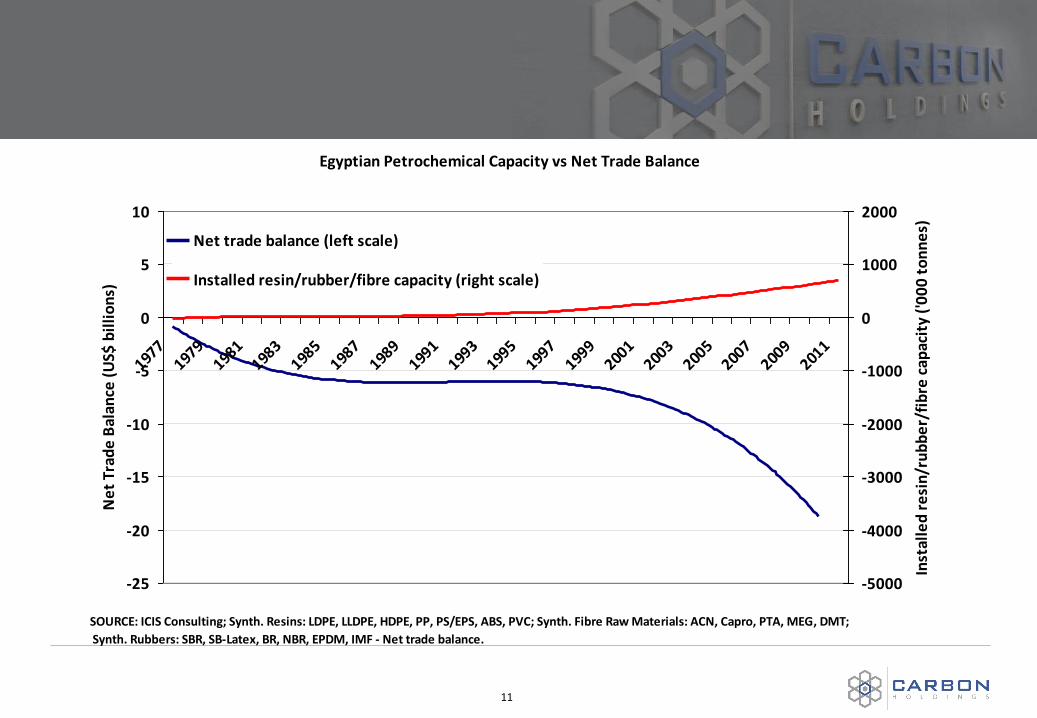

Egyptian Petrochemical Capacity vs Net Trade Balance

-25

-20

-15

-10

-5

0

5

10

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Ne

t Tr

ade

Bal

ance

(U

S$ b

illi

on

s)

-5000

-4000

-3000

-2000

-1000

0

1000

2000

Inst

alle

d r

esi

n/r

ub

be

r/fi

bre

cap

acit

y ('

00

0 t

on

ne

s)

Net trade balance (left scale)

Installed resin/rubber/fibre capacity (right scale)

SOURCE: ICIS Consulting; Synth. Resins: LDPE, LLDPE, HDPE, PP, PS/EPS, ABS, PVC; Synth. Fibre Raw Materials: ACN, Capro, PTA, MEG, DMT;

Synth. Rubbers: SBR, SB-Latex, BR, NBR, EPDM, IMF - Net trade balance.

12

Korean Petrochemical Capacity & Growth Rate (1970-2012)

0

5000

10000

15000

20000

25000

30000

19701972

19741976

19781980

19821984

19861988

19901992

19941996

19982000

20022004

20062008

20102012

Tota

l Cap

acit

y, k

t/y

Synthetic Resins Synthetic Fibre Raw Materials Synthetic Rubber

1989-1997 (Take-off period)

Large-scale expansion; launch of

Daesan complex

1979-1988 (Growth period)

launch of Yeosu complex

Government sector-led Private sector-led

1966-1978

(Development period)

launch of Ulsan complex

ethylene capacity:

505 kt/y (two companies)

ethylene capacity:

4330 kt/y (eight companies)

ethylene capacity:

5760 kt/y (seven

companies)

ethylene capacity:

7770 kt/y (six

companies)

1998-2003

(Restructuring

period)

SOURCE: ICIS Consulting; Synth. Resins: LDPE, LLDPE, HDPE, PP, PS/EPS, ABS, PVC; Synth. Fibre Raw Materials: ACN, Capro, PTA, MEG, DMT;

Synth. Rubbers: SBR, SB-Latex, BR, NBR, EPDM

38 Producing Co's.

301 Processing Co's

>5000 Finished Goods Co's

Co-ordinated start-up of multiple-world

scale crackers & foreign investment

provided the ideal basis for more rapid

growth.

ethylene capacity:

115 kt/y (one company)

= Cracker Start-up

13

Olefins Value Chain

3

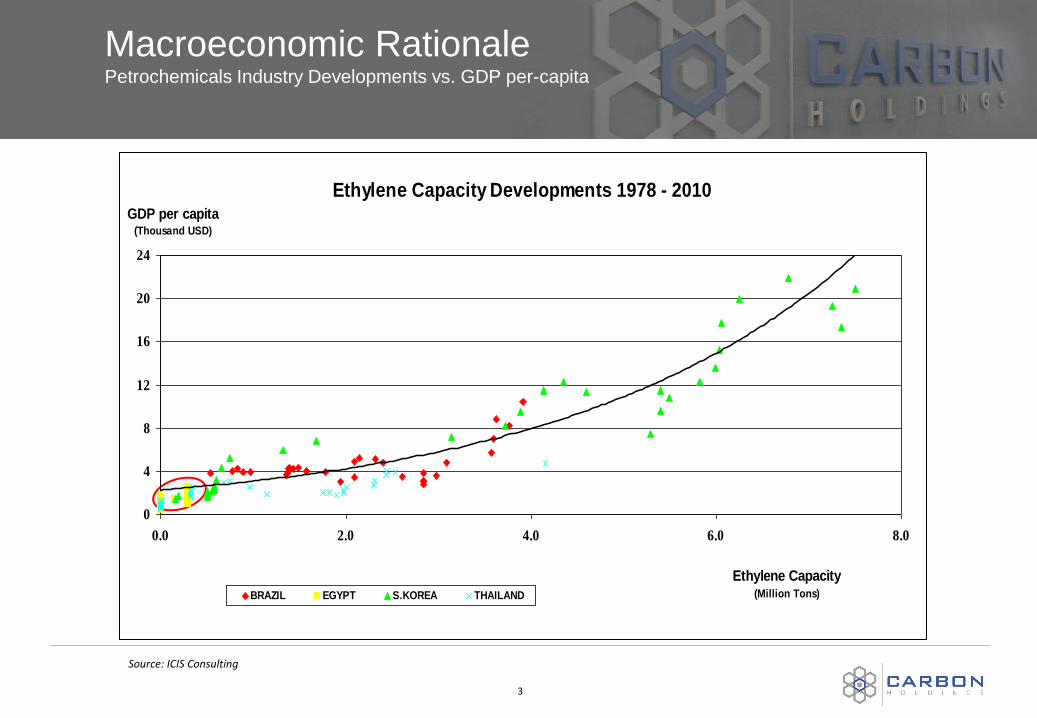

Macroeconomic Rationale Petrochemicals Industry Developments vs. GDP per-capita

Source: ICIS Consulting

Ethylene Capacity Developments 1978 - 2010

0

4

8

12

16

20

24

0.0 2.0 4.0 6.0 8.0

Ethylene Capacity(Million Tons)

GDP per capita(Thousand USD)

BRAZIL EGYPT S.KOREA THAILAND

Macroeconomic Rationale Petrochemicals Industry Developments vs. GDP per-capita

4

Petrochemical Developments 1978 - 2010(Thermoplastics, Fibres, Elastomers)

0

4

8

12

16

20

24

0 30 60 90 120 150

Petrochemical Demand(Kg per capita)

GDP per capita(Thousand USD)

BRAZIL EGYPT S.KOREA THAILAND

Source: ICIS Consulting

Projects - Egypt Master Development - Site Location, North West Gulf of Suez

16

Tahrir

Petrochemicals

Corporation

Sokhna Port 1

Operated by

Carbon Holdings

Sokhna Port 2

Operated by

DP World

700,000 MTA

Ammonia

Plant

350,000 MTA

MGAN Plant

180,000 MTA

Polypropylene

Plant Planned

SEZone Area

Pipe Easement inside SE Zone

350,000 MTA

Polypropylene

Plant

II

Projects - Egypt Synopsis of Tahrir Petrochemicals Corporation

17

Products

1,350,000 MTA Polyethylene 880,000 MTA Propylene 350,000 MTA Polypropylene 250,000 MTA Butadiene 350,000 MTA Benzene 150,000 MTA Gas Oil 100,000 MTA Hexene-1

Status

Loan package under negotiation with Export Credit Agencies (‘ECAs’) Board approval received for US$ 400m loan from the Overseas Petroleum Investment Corporation (‘OPIC’)

Project Cost (approx.)

US$ 7 Billion

Location Suez, Egypt

SNAPSHOT COMMERCIAL STRUCTURE

xc

The Project Configuration Inclusive of Polypropylene Integration

18

Naphtha 3,900 KTA

C5

Butadiene 250 KTA

HDPE 450 KTA

LLDPE/HDPE (Swing) 450 KTA

CRACKER UNIT

C4

Hexene-1 83 KTA

POLYOLEFINS

COMPLEX

LLDPE/HDPE (Swing) 450 KTA

Hexene** 17 KTA

Benzene 350 KTA

PFO/PGO*

Propylene 880 KTA

Ethylene 1,500 KTA

Polypropylene 180 KTA

180 KTA

(Propylene)

*Sent to OSBL as fuel for power generation **17 KTA will be utilized by the PE Facilities Products for export and local sales

STRICTLY CONFIDENTIAL

Polypropylene 350 KTA

350 KTA

(Propylene)

Tahrir Petrochemicals Corporation Economic impact

19

The Project shall have a total capitalized cost of approximately US$7 billion.

The Project will purchase approximately US$ 1.5 billion of goods and services from Egypt during the construction phase

Approximately 20,000 persons will be employed during its peak construction phase

It is anticipated that in excess of 15,000 indirect jobs will be created during the construction phase

The Project will employ approximately 3,000 engineers and technicians during its operational phase

It is anticipated that in excess of 25,000 indirect jobs will be created during the operational phase

The project shall increase total Egyptian exports by approximately 35%

EHC & OPC First & Second Shipments of Propylene at CH Jetty

20

350,000 MTA

MGAN Plant

180,000 MTA

PP Plant 1st Propylene

Shipment (ADNOC)

2nd Propylene

Shipment (ADNOC)