Embed Size (px)

Citation preview

Egypt Economic and business outlook

Quarterly update - March 2012Final analysis by Nenad Pacek

Contents

• Executive summary• Strategic business view• Political risks and political scenarios• Economic fundamentals• Corporate sales and profit trends per sector• Growth trends and drivers• Household consumption trends• Gross fixed investment trends• Government spending trends• Currency outlook• Interest rates and inflation rate outlook• Forecast table

Executive summary

• Consumer businesses have recovered reasonably well in recent months, but B2B and B2G remain weak

• If Egypt does not sign a stand-by agreement with the IMF in the next two months, it faces a prospect of chaotic pound depreciation – forex reserves are still melting at a rate of almost $2bn per month and will soon run out unless there is foreign help (first IMF and then other multilateral and bilateral lenders)

• IMF will require at least moderate austerity as a condition for the loan – this (and other factors) will prevent a quick economic bounce-back in 2012 and possibly 2013

• We think that the IMF deal worth over $3bn will be signed during March, or latest April – this is our base case scenario, but companies should have contingency plans in place in case the deal falls through

• To protect the currency, central bank raised interest rates in late 2011 to 9.25% but this is not helping growth

Executive summary II

• We expect GDP growth to reach just 1.8% this year, the same as 2011 but still far off 7%+ growth rates from 2007 or 2008

• Unemployment has increased again to 12.4%• Muslim Brotherhood has dominated both upper and lower house

elections, winning most votes in both• Presidential elections will take place on May 23 and the president will be

known by latest June 21• It is not clear yet how the new constitution will look like – the new

parliament’s constitutional assembly will draft it and then it will be clearer what kind of powers will the new president have

• The military is likely to preserve sizeable political and economic power even after the elections (officially and/or unofficially)

• The latest court ruling that questions the constitutionality of the elections is unlikely to be implemented but has caused some uncertainty

Strategic business view

• Egypt is not anymore treated as a growth market by most companies• This is in sharp contrast to pre-revolutionary days when Egypt was treated

as one of the big emerging market priorities• In the short term, executives continue to view Egypt as a politically

uncertain market with struggling sales and abundance of economic and political risks

• Those firms that were keen on building local manufacturing sites have largely put everything on hold

• Executives remain bullish about the market for the medium and long-term believing that the economy will start recovering after we get full political clarity after presidential elections

• Companies are focusing on preserving profitability, building market share, extending product portfolios, cash collection, contingency planning

Political risks and outlook

• After the removal of ex-president Mubarak, the Supreme Military council is in charge of steering the country towards new civilian government/president

• Complicated and long parliamentary elections are essentially finished• Lower house elections finished in January after some 10 weeks of voting,

with two thirds of seats going to parties and one third to individual candidates (of which half must be professionals and half farmers!)

• Elections for the upper house (the so called Shura Council) have also finished

• Muslim Brotherhood has dominated both elections – it holds 43% of the seats in the lower house and 59% in the upper house

• The next step is for both houses of parliament to meet to select 100 people for the constituent assembly which will be in charge of drafting the constitution

Political risks and outlook II

• The constitution draft will then be put up for a referendum• The army has set up an advisory council to be involved in drafting of the

new constitution• The army also wants the current cabinet (appointed by the army as a

caretaker) to be involved in drafting the new constitution• The military will therefore insists that the governemnt, the advisory

council and elected parliamentarians form the constituent assembly • This seems to be designed to prevent the moderate and less moderate

islamists from being totally in charge of writing the constitution• At this stage it is also unclear what powers will be given to the newly

elected parliament and what powers to the new president

Political risks and outlook III

• Presidential elections will take place on May 23 and if there is a second round it will be held on June 16-17

• We will know who the president is by latest June 21• This protracted electoral process with ongoing twists and turns has

contributed to ongoing unease in the business community• Lack of political clarity is hurting business and consumer confidence and it

is hurting foreign investments, tourism (as a biggest forex earner, down about one third last year), manufacturing

• 2012 will therefore be another „lost year“ in terms of economic progress and business growth (for most companies)

• Provided that presidential elections go well, Egypt should have a fully functioning civilian government in the second half of the year although there are major questions as to how pro-business the new authorities will be

Political risks and outlook IV

• To please the population the army has reshuffled the interim government several times and keeps the strict control over the army matters and judiciary

• The military establishment also does not want chaos in the future – the military and many high ranking military officials own, co-own or participate in a number of business ventures and will want to protect and expand their business interests

• Some estimates say that the military controls more than 25% of Egypt’s GDP• Ultimately the military wants Egypt that will prosper (and in which rules of

the game will be favouring domestic firms – ideally those controlled by the military interests directly or indirectly)

• The army officials are also largely seen by the business community as socialist/protectionist group from an economic point of view that could later interfere (from behind the scenes) to influence business legislation and economic policy

Political risk and outlook V

• Executives with long experience in Egypt remember the statist years between 2001 and mid-2004 when Egypt was literally falling apart, when it ran out of foreign exchange reserves, when it had constant black market exchange rate and when businesses were pulling out of the country

• The worst case scenario for companies is that some form of a statist government is elected after new elections (in the background co-ordinated by military business interests) and that we go through a number of difficult years for foreign firms with more protectionism of the domestic business interests and weak business – we hope this worst case scenario does not happen, but still companies should be aware of this possibility

• We continue to warn about the risk that the current election process will not result in a government that will be as pro-business as the one run prior to the elections by Ahmed Nazif

• The risk of relative economic statism in the near future is there despite the fact that the Muslim Brotherhood says they want strong private sector driven economy

Economic fundamentals

• As we warned in our last reports, debt levels, reserves and deficits all got worse during 2011 and early 2012 – there is now more serious threat to growth and currency unless some external funding is quickly found

• Foreign exchange reserves dropped sharply in recent months again to just $16bn (from $36bn in late 2010), falling by almost $2bn per month on average in recent months

• Local banks do not have more capacity to buy local debt • This is why the government has started talks with the IMF and we expect a

stand-by agreement of over $3bn to be signed during March or latest April• If the deal is not signed, Egypt will go through a chaotic depreciation of the

pound• The IMF deal will act as a catalyst for other financing from other multilateral

and bilateral lenders – no one will help Egypt with any serious money unless there is an IMF stamp of approval

Economic fundamentals

• Public debt has been reduced from a staggering 130% of GDP in 2005 to less than 80% (still high, but slightly lower than European Union avg.) prior to the revolution

• But public debt is now growing quickly and fast approaching 90% of GDP as Egypt budget deficit deteriorates further

• External debt is now less than 15% of GDP, one of the lowest percentages of any country in the world but at this stage this is not helping confidence much

• Egypt has sought to find external financing from various Arab nations – pledges are in place although so far only $1bn has arrived – not enough to offset the fast drop in reserves

• Some skeptical executives also remember early 2004 when the authorities claimed they had $14bn in reserves but in reality they had nothing

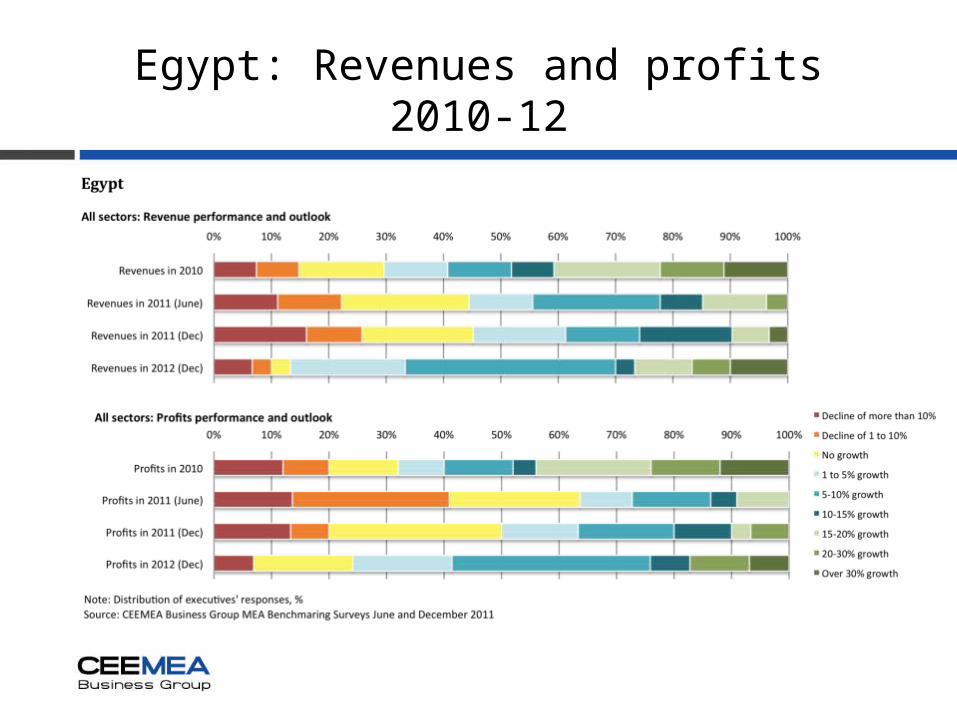

Corporate sales and profit trends

• Overall sales and profit performance by multinationals has deteriorated since our last survey in June (see charts later), although in recent months many consumer goods firms have reported a solid bounce-back

• 2011 results were weaker than 2010• Almost half of firms did not grow last year and 25% declined in terms of top

line• Corporate expectations for 2012 are better but this is probably not justified

considering expected weakness of demand • Executives should proactively manage expectations downwards and create

robust contingency plans in case the currency falls further and the country slips into a recession (this is not our base case scenario though, we think the IMF deal will come through)

• Half of all companies did not grow profits in 2011, and most expect mild improvement on this front in 2012 as their organizations got leaner

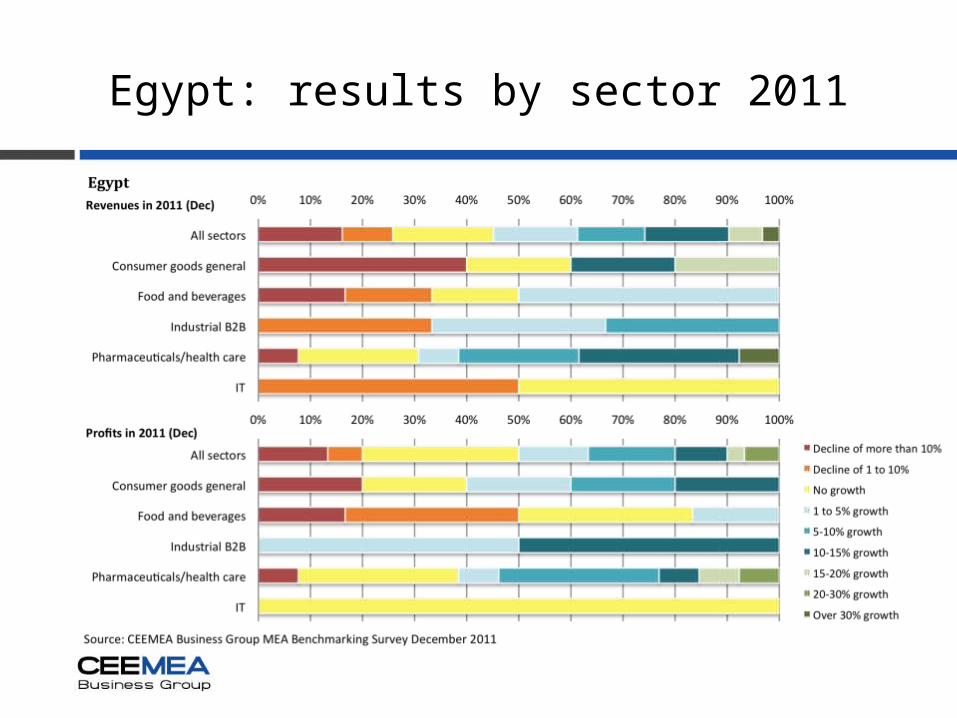

Consumer goods and food/beverages sales and profit trends

• 60% of consumer goods firms had no growth last year • 40% fell more than 10%• Firms are managing profitability aggressively largely through cost cutting

and as a result 60% of consumer goods firms achieved higher profits in 2011 than in 2010

• Food/beverage firms were doing slightly better in 2011, but not much• 50% had no growth in 2011, while the rest recorded growth between 1-

5%• Most expect improvement in 2012 but we are not sure this expectation is

justified• In 2012 only 18% of food/beverage firms expect profit growth and 50%

expect profits to fall next year

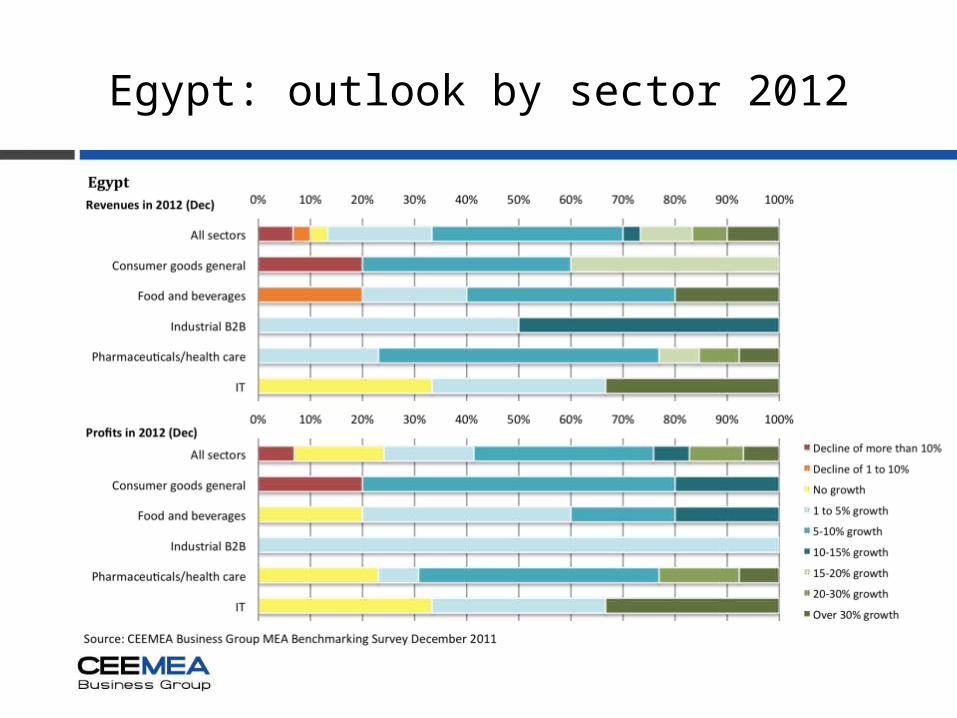

Industrial B2B and pharma sales and profit trends

• 35% of industrial firms had declining revenues by up to 10% last year• Expectations are better for 2012 but this might be too optimistic• Interestingly, most industrial B2B firms had modest profit growth last year

but anecdotal evidence suggest this was largely due to cost reductions• Pharma and health care firms had mixed results last year• For 32% there was no sales growth, but almost 40% still grew in double

digits (rest were growing in single digits)• All expect growth in 2012 which might prove to be challenging considering

fast growing budget deficit and upcoming moderate austerity program pushed by the IMF

IT sales and profit trends

• IT sector was struggling in 2011 (except the consumer side which held up better)

• 50% of companies declined up to 10% in 2011 and half were broadly flat vs. 2010

• Expectations for 2012 are mixed and cautious• Public sector business is tough and so are expectations of new purchases

by the private sector• Profits are broadly flat• Profit expectations are better for 2012 but we are not sure this is justified

considering still weak economic outlook

Egypt: Revenues and profits 2010-12

Egypt: results by sector 2011

Egypt: outlook by sector 2012

Growth trends and drivers

• Growth slowed down during 2011 – in the fiscal year it grew only 1.8% (12 months to the end of June) and the same number was achieved for the calendar year 2011

• Provided that the IMF financing deal is signed (and Egypt avoids a sharp depreciation), we expect the economy this year to perform in line with 2011 results – just under 2% growth

• We expect the IMF deal to come through in March or latest in April (base case)• This is slower than expected MENA average for 2012 of 4% and far slower than 7%+

growth recorded in 2007 and 2008• The reasons for a prolonged slow growth are linked to the aftermath of the revolution:

political uncertainty has spilled over into private and corporate confidence, big hit of major foreign exchange earner tourism, a collapse in foreign direct investment, major threats surrounding the currency

• If we get acceptable political clarity after presidential elections (see Political outlook), Egypt’s growth is likely to accelerate to 3.5% in 2013 (from a low base)

Growth trends and drivers II

• A number of factors will keep corporate sales and economic growth very slow at least in the next 2-3 quarters:– Lack of consumer and corporate confidence – Higher interest rates– Still threat of falling pound (until the IMF and other foreign financing arrives)– Capital outflows (although recent central bank measures might reduce some flows)– Sharply falling FDI and weak new FDI pipeline, low investment by local firms– Expected IMF imposed austerity program in return for financial package– A significant decline in tourism revenues (officially down by about one third vs. 2010)– Weaker export markets in the area and in the EU– Lack of government spending on infrastructure and large projects (as borrowed cash is

diverted into higher subsidies and maintenance of social peace in the short term)– Lower tax/customs revenues; booming budget deficit will reduce ability to invest also in

the next few years and high premiums on borrowing will reduce ability to spend overall– The decision of the government to raise financing locally, which means that banks will

mostly lend to the government and not companies

Growth trends and drivers III

• The government will have to borrow substantially to be able to increase spending or, if unable to borrow, will have to print money (which would lead to higher inflation rate)

• The government will need about $25-30bn just to cover the deficits which are likely in 2012 and the IMF deal is likely to be just over $3bn

• The rest of the gap will have to come from other multilateral and bilateral lenders, but all of them are waiting for the IMF green light

• G8 and other multilateral lenders are promising funds for all “Arab Spring” nations – G8 has just pledged $38bn, some of which will eventually end up in Egypt

• New loans from Saudi Arabia, UAE and Arab Monetary Fund were expected but just $1bn has arrived so far

• Any money that arrives is likely to be spent on plugging gaps and social purposes in 2012, rather than on any new investment projects – this is bad news for B2B and B2G businesses in the short term

Growth trends and drivers IV

• Over the medium term, Egypt could again become one of the most exciting emerging markets for business

• This will however depend on the final political outcome and the quality of the new government/president

• Even a moderately pro-business government/president could bring strong economic growth back

• If all goes well after both elections, growth should already start to accelerate towards the end of 2012 and gain better traction in 2013

• But the risks to this scenario are high and companies should manage expectations downwards, manage costs and receivables carefully, prioritize market share gains and have robust contingency plans

Household consumption

• Household spending was growing 5% per year until the beginning of 2011• As the revolution started, sales fell and stayed weak for most companies for

the most part of the year (see earlier slides on corporate sales and profit trends)

• Sales have started to pick up in recent months and some firms have already achieved pre-revolution volume levels

• However, the outlook for consumer goods sales growth is still weak for 2012 compared to pre-revolution days although companies that manufacture cheaper brands locally will do better than those relying on imported products

• We expect only small recovery in 2012 (mostly after the summer provided that election results are broadly acceptable)

• Moves to cheap brands but also very trusted brands will accelerate

Household consumption II

• Spending on consumer durables will suffer more than food and beverages as financing is tight and consumer confidence remains weak

• Unemployment indicators point out to weak 2012• Officially, unemployment has now jumped to 12.4%, up from just under

12% during our last quarterly report• The national employment offices says the number of advertised vacancies

dropped 7 times in the last 12 months• This is the sharpest decline of vacancies in almost 10 years – this does not

sound promising for consumer goods sales growth in 2012• Egyptian authorities counts as employed even those that work in grey

economy 4 hours per month!• Obviously, the real unemployment is much higher than officially reported

Household consumption III – corporate opinions

• “Interestingly enough, our 2011 was stronger than 2010 since most people wanted to be on social networking sites. The demand for our personal IT equipment went up and saved at least B2C part of our business. The rest is weak and will not recover until we know how the country will be run in the future. But luckily our business in Saudi is booming on all fronts and it has compensated for shortfalls in Egypt, Syria, Libya.” Regional MEA director, IT multinational

• “As of February we are back to levels where we were prior to the revolution at least in volume terms. But pricing pressures are strong and unlikely to go away any time soon. We are debating how to launch products in smaller packages, not only in Egypt but also in many other African markets and also in parts of CEE. I would be happy to see small single digit growth in Egypt this year. My expectations are low.” Regional director, consumer goods firm

Gross fixed investment

• Gross fixed investment fell by an estimated 7% last year, after growing some 8% in 2010

• In 2012 we expect no recovery of corporate spending as confidence stays low, interest rates stay up, banks remain reluctant/unable to lend, and as local and foreign investment stays low

• Companies should be aware of the risk that corporate spending could decline further especially in the first half of 2012

• Domestic and foreign conglomerates’ enthusiasm to invest has dropped and many will either sit on their cash and/or will try to keep moving it abroad in the short term

• Business uncertainty is high and corporate spending will stay weak until there is more political clarity in place

• We project flat corporate spending in 2012 and gradual acceleration in 2013 (see Forecast table)

Gross fixed investment II

• A number of planned major industrial and infrastructure projects (such as Upper Egypt, Suez, Port Said, West Alexandria...) are on hold and the previous opportunity for companies to join some of those projects under Public Private Partnership arrangements is unlikely in the short term

• The plan to spend $20bn every year in the next decade on various infrastructure projects (water plants, wastewater plants, highways, hospitals, schools, power generation etc.) will not happen in 2012 either as money is channelled into subsidies and current spending rather than investment spending

• One recent exception and hopefully a good sign for the future is the World Bank approval of $240m loan to finance the Giza electricity project

Gross fixed investment – corporate opinions

• “I was really pleased to see the date for presidential elections. There is now a timeline for most political things and if the political mess gets fully sorted by the summer, we are surely going to see at least some confidence returning in the second half of the year. Our budget is the one that protects profitability and has no growth for 2012. But we did not retrench from the market. I shipped some of our staff to work in the Gulf temporarily to help boost growth there, but I expect to bring everyone back next year.” Regional director, industrial firm

• “We have created a plan B and plan C in case there is a complete economic meltdown coupled with a sharp drop in the value of the Egyptian pound. Now it seems that external help will come and that we will avoid the catastrophe. But I am under no illusion that a quick jump in business is around the corner. This market will recover for a year or two more.” Regional director, industrial equipment firm

Government spending trends

• Both public debt and budget deficits are among the highest in the world and will require corrections in the next 3-5 years in order to achieve sustainability

• As part of the new expected IMF stand-by agreement, we expect the IMF to request a moderate austerity program in return for financial help

• This will be politically very difficult to implement, if not impossible, and if it is even partly implemented it will hurt B2G growth prospects in the short term

• Current spending has shifted more to social fire-fighting (often in the form of subsidies) and it has helped consumer goods firms at the expense of B2B and B2G firms

• We expect budget deficit to stay high this year despite a preliminary fiscal consolidation plan

Government spending trends II

• The fiscal consolidation plan (still to be seen if it will go through) calls for further cuts in the budget deficit to 8.4% in 2012 and to under 8% by late 2013

• Public debt will aim to be cut to 78% of GDP in three years• If this is approved by the IMF, it could be labelled a moderate austerity program

that would not hurt growth too much – at the same time, it is not clear if the IMF would see this as sufficient before releasing the first tranche of financing

• During 2012 and 2013 budget deficit gaps will most likely be covered by a combination of multilateral and bilateral funding, local borrowing as well as potential reduction of some subsidies, possible reforms of income taxes, VAT intro, issuance of Islamic bonds as well as planned sales of land to Egyptian expats – all these points are not entirely clear at this stage and as the year goes by we will report on the latest developments

Currency outlook

• The fate of the pound depends on the IMF deal• If it is approved, relative currency stability will be preserved in 2012, with

gradual, manageable and mild depreciation• If the deal is not approved, we are going into the worst case scenario as all

forex reserves are spent and central bank is not able to defend the currency

• Our base case scenario is based on the assumption that the IMF deal will be approved

• The pound has weakened a little bit to the $ since our last report (from 6.01 to 6.03) thanks to constant currency interventions

• To help preserve the reserves, the central bank has imposed more regulations for anyone who wants to transfer money abroad

Interest rates and inflation outlook

• Overnight interbank interest rates have gone up again a bit to 9.75% (from 9.24% six months ago)

• The central bank was forced last year to increase interest rate to 9.25% to stop the outflow out of the Egyptian pound – more increases could happen in case the IMF deal does not come through

• If it comes through, it is unlikely that interest rates will rise further since the inflation rate is now decelerating

• Inflation rate is now 8.7% yoy, down from almost 10% yoy in December last year

• Interest rates are now positive in real terms after a long time• We expect inflation rate to average 9% this year under our base case

scenario

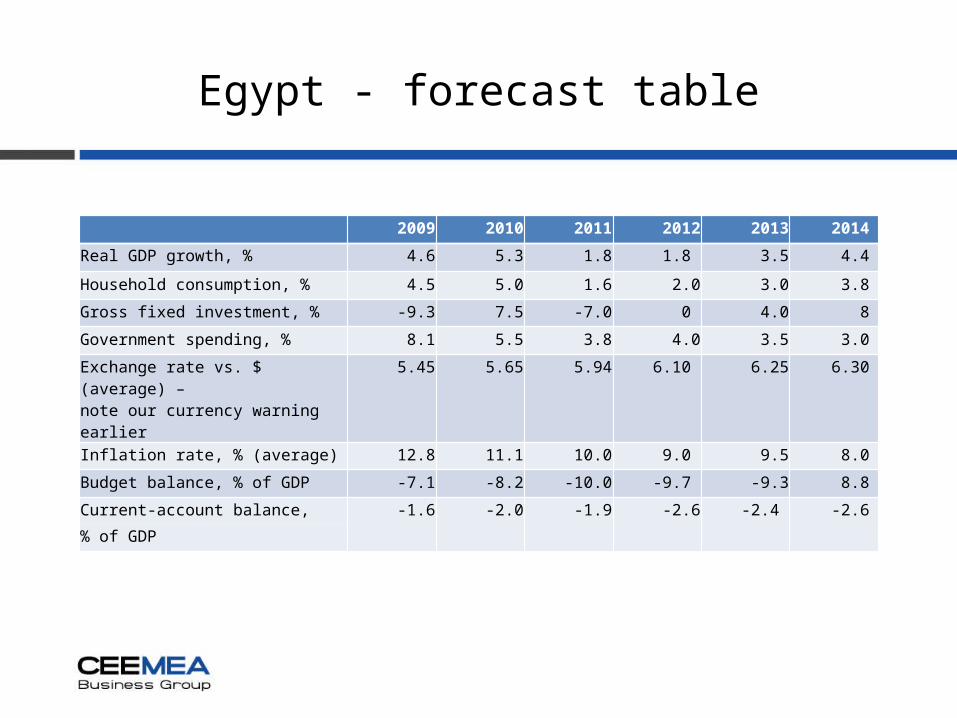

Egypt - forecast table

2009 2010 2011 2012 2013 2014

Real GDP growth, % 4.6 5.3 1.8 1.8 3.5 4.4

Household consumption, % 4.5 5.0 1.6 2.0 3.0 3.8

Gross fixed investment, % -9.3 7.5 -7.0 0 4.0 8

Government spending, % 8.1 5.5 3.8 4.0 3.5 3.0

Exchange rate vs. $ (average) – note our currency warning earlier

5.45 5.65 5.94 6.10 6.25 6.30

Inflation rate, % (average) 12.8 11.1 10.0 9.0 9.5 8.0

Budget balance, % of GDP -7.1 -8.2 -10.0 -9.7 -9.3 8.8

Current-account balance, -1.6 -2.0 -1.9 -2.6 -2.4 -2.6

% of GDP

Disclaimer, copyright, sources

© 2012 CEEMEA Business Group* *a joint venture betweenDT-Global Business Consulting GmbH, Address: Keinergasse 8/33, 1030 Vienna, Austria,Company registration: FN 331137t and GSA Global Success Advisors GmbH, Hoffeldstraße 5, 2522 Oberwaltersdorf, AustriaCompany registration: FN 331082k Source: GSA Global Success Advisors GmbH and CEEMEA Business Group researchBasic data sources come from central banks, own intelligence network, CEEMEA Business Group corporate survey, governments and other public sources. Interpretation, views, forecasts, business quotes and business outlooks by GSA Global Success Advisors GmbH and CEEMEA Business Group.

This material is provided for information purposes only. It is not a recommendation or advice of any investment or commercial activity whatsoever. The CEEMEA Business Group accepts no liability for any commercial losses incurred by any party acting on information in these materials.

Contact: Nenad Pacek, President and Founder, GSA Global Success Advisors GmbHM: +43 676 646 0607 E: [email protected]

www.ceemeabusinessgroup.com