Embed Size (px)

Citation preview

Rome – May 7, 2015

Enel Green Power 2015 Investor day

Inve

sto

r R

ela

tio

ns

2015 Investor day

Agenda

1

Introduction Francesco Venturini, CEO

1Q 2015 consolidated results Francesco Venturini, CEO - Giulio Carone, CFO

Strategic outlook Francesco Venturini, CEO

2015 - 2019 financial outlook Giulio Carone, CFO

Closing remarks Francesco Venturini, CEO

Inve

sto

r R

ela

tio

ns

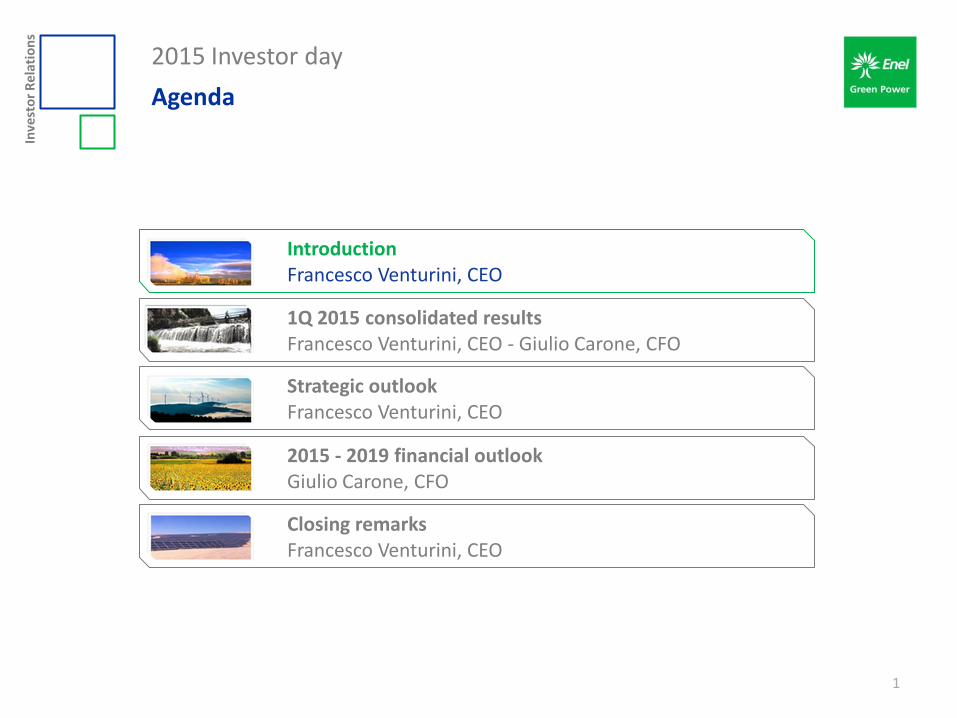

Enel Green Power today

2

Global player with a diversified footprint

2.1 GW in operation 0.4 GW in execution

North America

10 MW in operation 0.5 GW in execution 0.4 GW contracted

Africa

5.8 GW in operation 0.3 GW in execution

Europe

1.9 GW in operation 1.9 GW in execution 0.1 GW contracted

Latin America

Expertise across 5 technologies

Operations across 16 countries

Industry leading load factor at 40%

Highly efficient operations

2015 Investor day

Inve

sto

r R

ela

tio

ns

2015 Investor day

Agenda

3

Introduction Francesco Venturini, CEO

1Q 2015 consolidated results Francesco Venturini, CEO - Giulio Carone, CFO

Strategic outlook Francesco Venturini, CEO

2015 - 2019 financial outlook Giulio Carone, CFO

Closing remarks Francesco Venturini, CEO

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

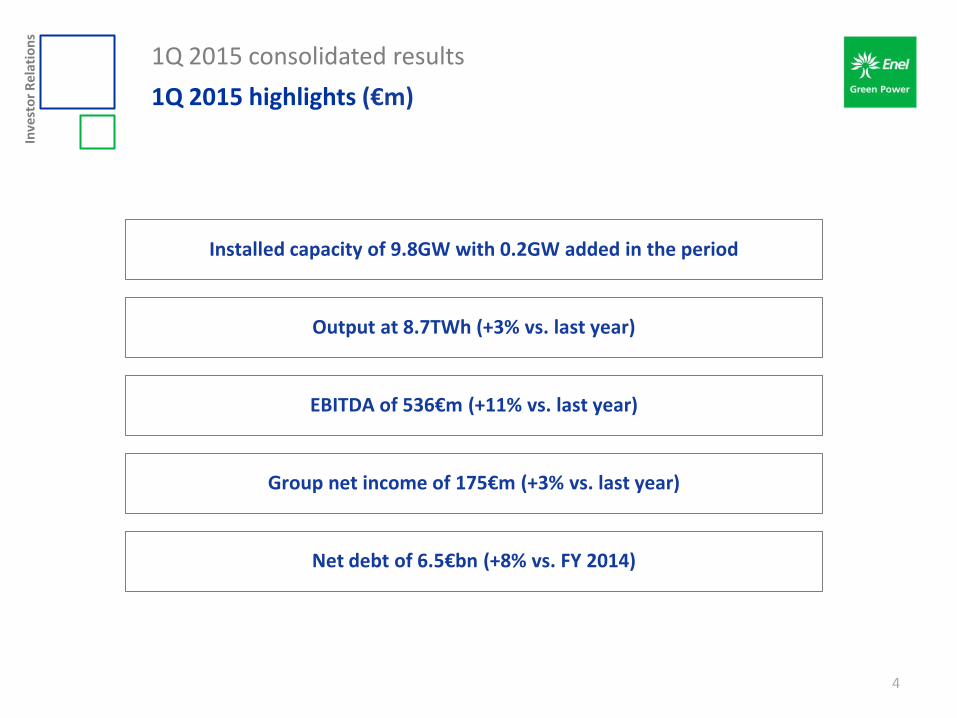

1Q 2015 highlights (€m)

4

Installed capacity of 9.8GW with 0.2GW added in the period

Output at 8.7TWh (+3% vs. last year)

EBITDA of 536€m (+11% vs. last year)

Net debt of 6.5€bn (+8% vs. FY 2014)

Group net income of 175€m (+3% vs. last year)

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

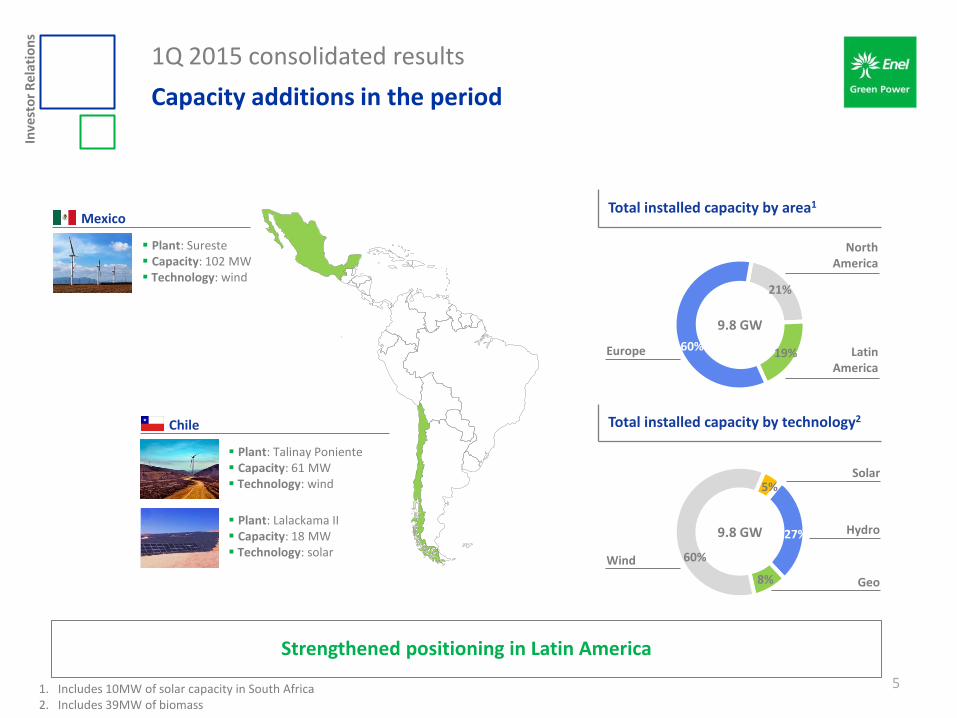

Capacity additions in the period

5

Strengthened positioning in Latin America

Chile

Plant: Talinay Poniente Capacity: 61 MW Technology: wind

Mexico

Plant: Sureste Capacity: 102 MW Technology: wind

21%

19% 60%

9.8 GW

Europe Latin America

North America

27%

8%

60%

5%

9.8 GW

Wind

Hydro

Solar

Geo

Total installed capacity by area1

Total installed capacity by technology2

Plant: Lalackama II Capacity: 18 MW Technology: solar

1. Includes 10MW of solar capacity in South Africa 2. Includes 39MW of biomass

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

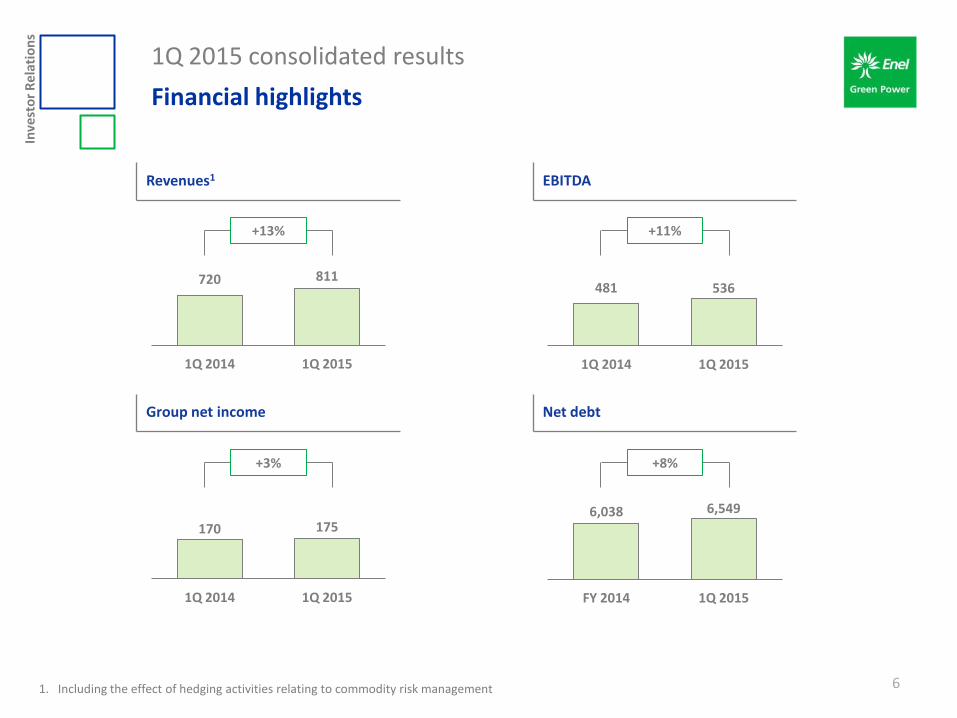

Financial highlights

6

EBITDA Revenues1

Net debt Group net income

6,038 6,549

FY 2014 1Q 2015

720 811

1Q 2014 1Q 2015

481 536

1Q 2014 1Q 2015

170 175

1Q 2014 1Q 2015

1. Including the effect of hedging activities relating to commodity risk management

+13% +11%

+8% +3%

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

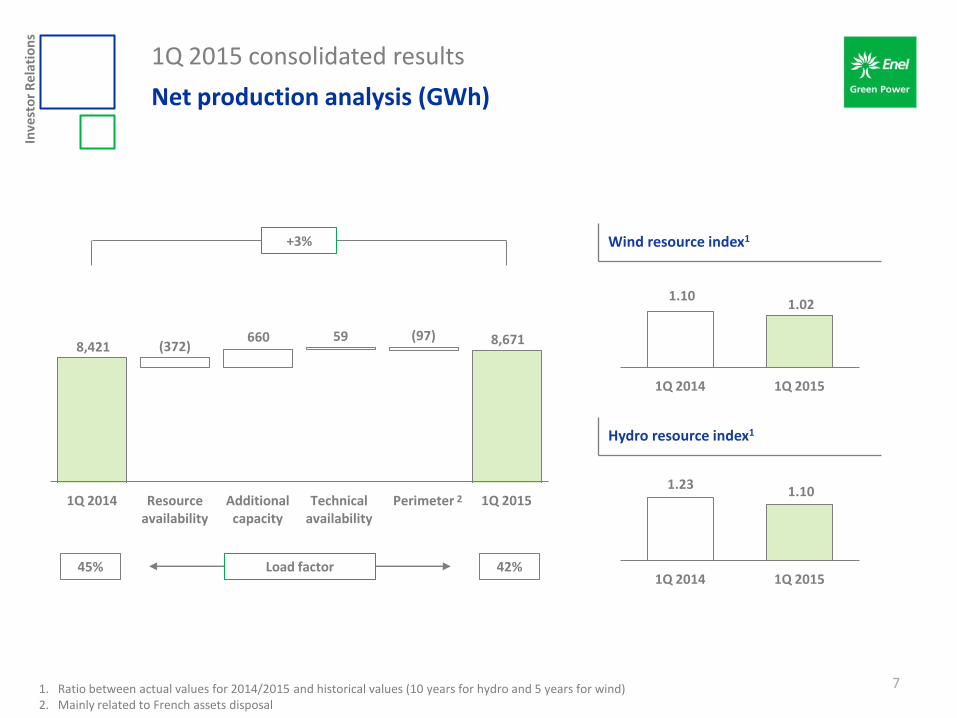

Net production analysis (GWh)

7

8,421 (372) 660 59 (97) 8,671

1Q 2014 Resource availability

Additional capacity

Technical availability

Perimeter 1Q 2015

+3%

Load factor 45% 42%

1. Ratio between actual values for 2014/2015 and historical values (10 years for hydro and 5 years for wind) 2. Mainly related to French assets disposal

1.10 1.02

1Q 2014 1Q 2015

Wind resource index1

1.23 1.10

1Q 2014 1Q 2015

Hydro resource index1

2

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

EBITDA analysis (€m)

8

EBITDA margin 66% 67%

481 1 47 (16) (7)

30 536

1Q 2014 Energy margin

Other revenues

Opex Perimeter Forex 1Q 2015

+11%

+55

1. Mainly related to French assets disposal

1

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

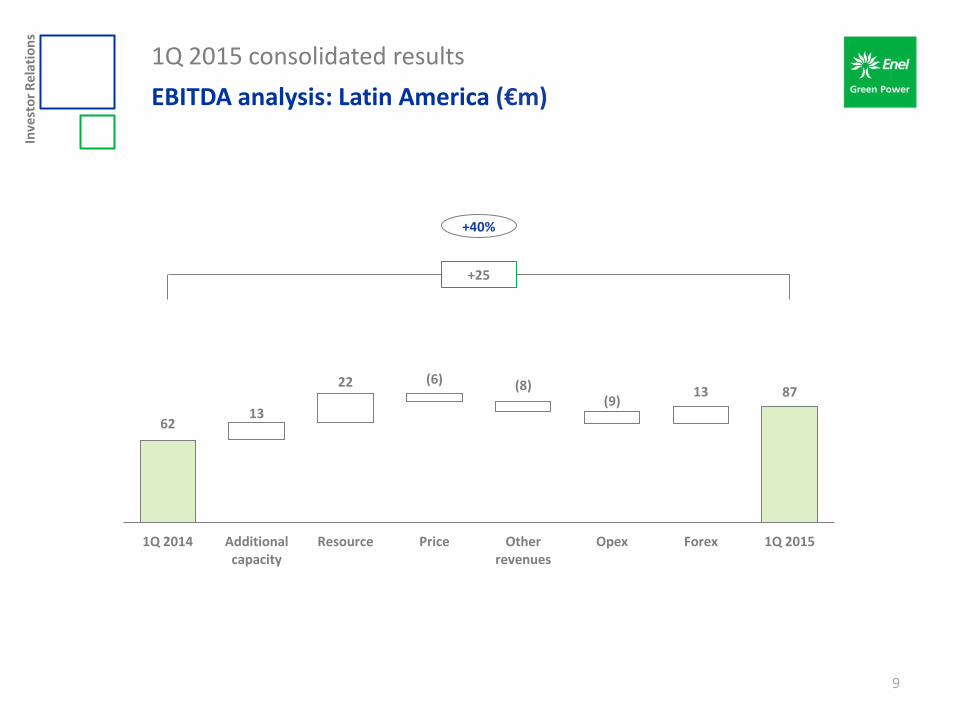

EBITDA analysis: Latin America (€m)

9

62 13

22 (6) (8) (9)

13 87

1Q 2014 Additional capacity

Resource Price Other revenues

Opex Forex 1Q 2015

+40%

+25

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

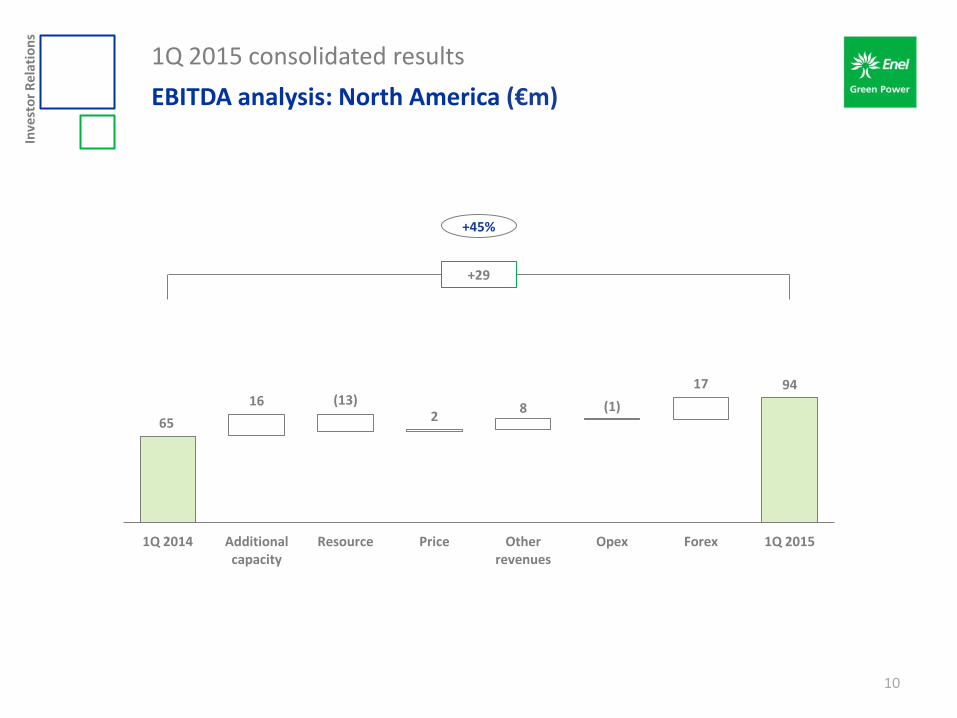

EBITDA analysis: North America (€m)

10

65

16 (13) 2

8 (1)

17 94

1Q 2014 Additional capacity

Resource Price Other revenues

Opex Forex 1Q 2015

+45%

+29

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

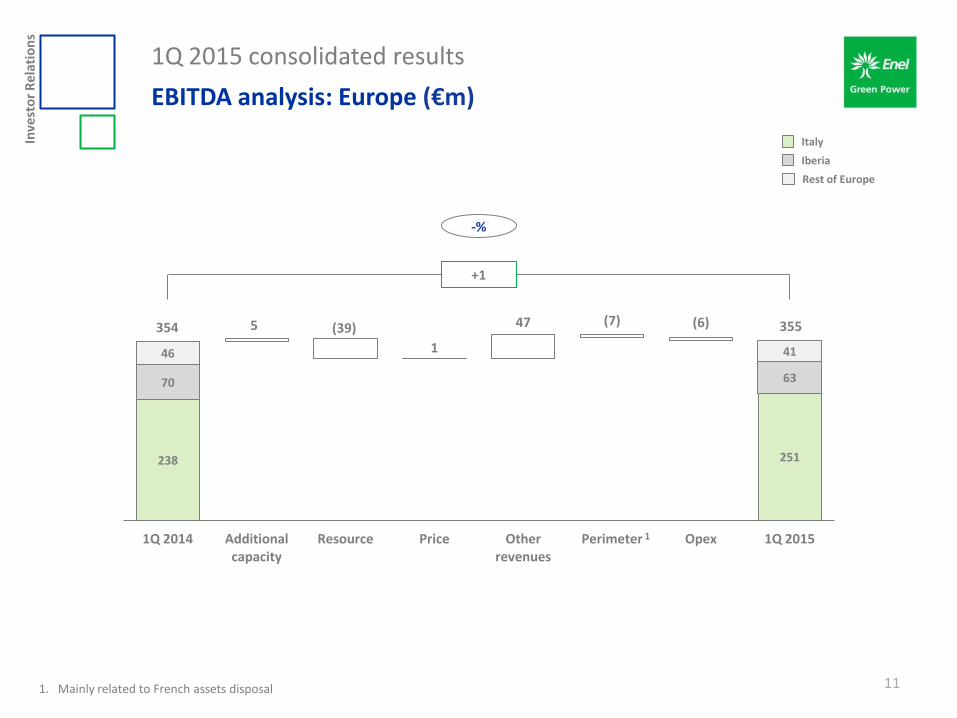

EBITDA analysis: Europe (€m)

11

-%

238 251

70 63

46

5 (39)

1

47 (7) (6)

41

1Q 2014 Additional capacity

Resource Price Other revenues

Perimeter Opex 1Q 2015

Iberia

Italy

Rest of Europe

+1

354 355

1

1. Mainly related to French assets disposal

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

Group net income

12

170

55 (28) 12 (12)

(15) (7) 175

1Q 2014 EBITDA D&A Net financial expense

Equity investment

Taxes Minorites 1Q 2015

+3%

+5

Inve

sto

r R

ela

tio

ns

1Q 2015 consolidated results

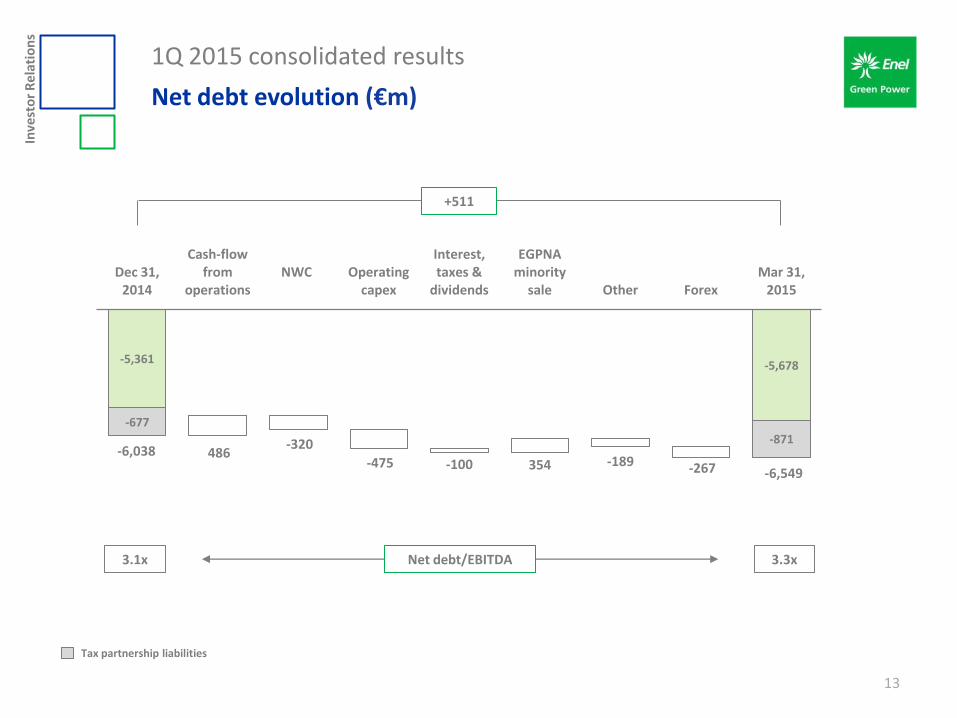

Net debt evolution (€m)

13

-5,361 -5,678

-677

486 -320

-475 -100 354 -189 -267

-871

Dec 31, 2014

Cash-flow from

operations NWC

Operating

capex

Interest, taxes &

dividends

EGPNA minority

sale Other Forex Mar 31,

2015

Tax partnership liabilities

-6,038

-6,549

Net debt/EBITDA 3.1x 3.3x

+511

Inve

sto

r R

ela

tio

ns

2015 Investor day

Agenda

14

Introduction Francesco Venturini, CEO

1Q 2015 consolidated results Francesco Venturini, CEO - Giulio Carone, CFO

Strategic outlook Francesco Venturini, CEO

2015 - 2019 financial outlook Giulio Carone, CFO

Closing remarks Francesco Venturini, CEO

Inve

sto

r R

ela

tio

ns

Strategic outlook

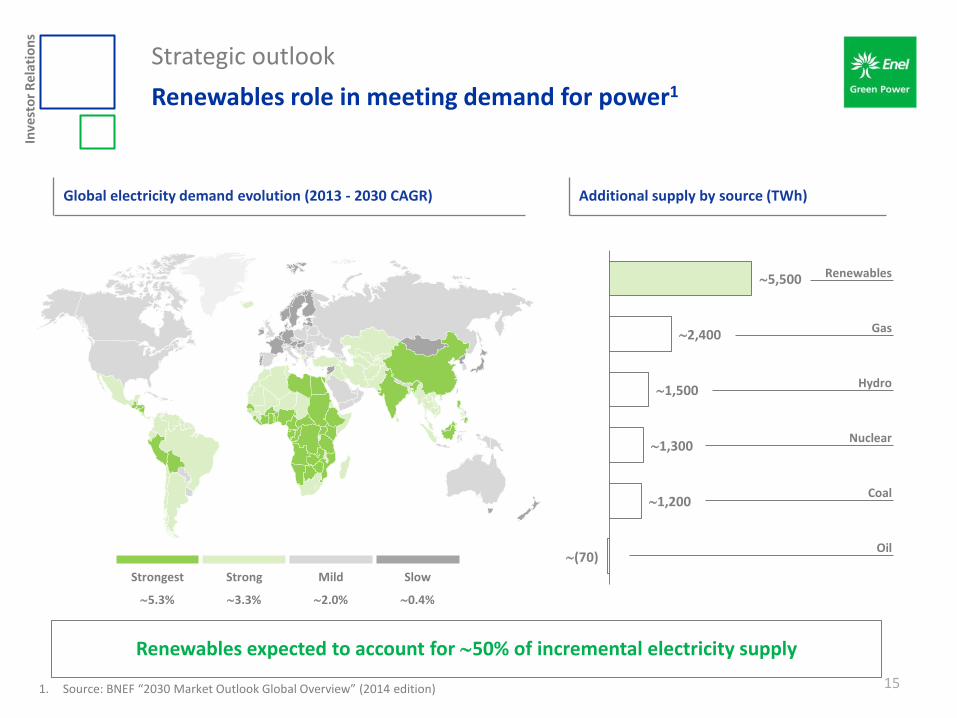

Renewables role in meeting demand for power1

15

Renewables expected to account for 50% of incremental electricity supply

1. Source: BNEF “2030 Market Outlook Global Overview” (2014 edition)

Strongest Strong Mild Slow

5.3% 3.3% 2.0% 0.4%

Additional supply by source (TWh)

(70)

1,200

1,300

1,500

2,400

5,500 Renewables

Gas

Hydro

Oil

Nuclear

Coal

Global electricity demand evolution (2013 - 2030 CAGR)

Inve

sto

r R

ela

tio

ns

Strategic outlook

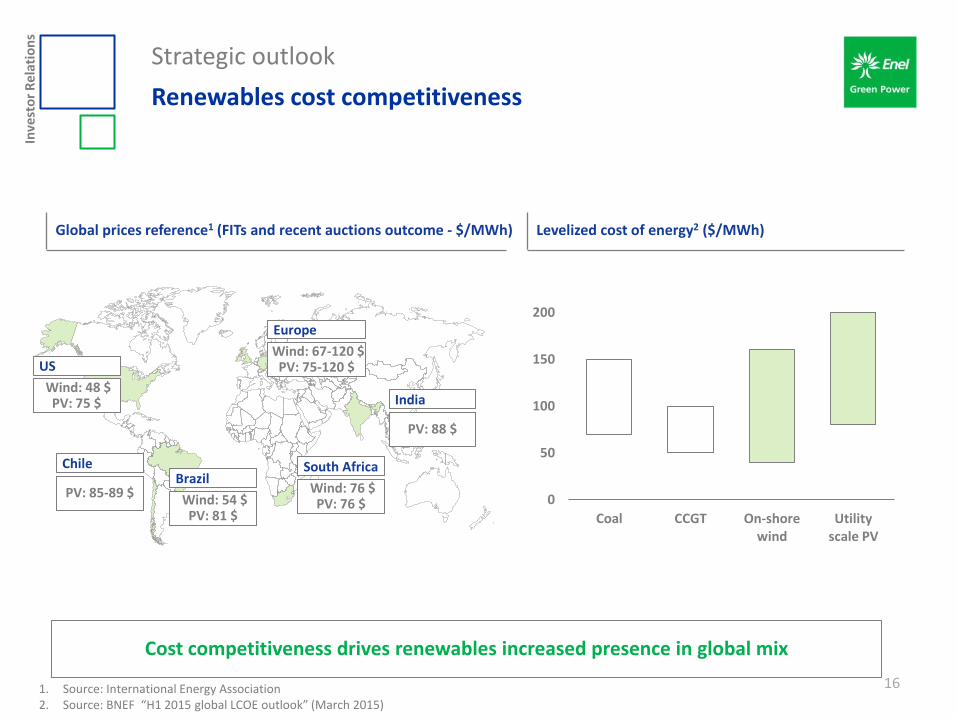

Renewables cost competitiveness

16

Global prices reference1 (FITs and recent auctions outcome - $/MWh) Levelized cost of energy2 ($/MWh)

Cost competitiveness drives renewables increased presence in global mix

0

50

100

150

200

Coal CCGT On-shore wind

Utility scale PV

1. Source: International Energy Association 2. Source: BNEF “H1 2015 global LCOE outlook” (March 2015)

Wind: 67-120 $ PV: 75-120 $

Europe

PV: 85-89 $

Chile

Wind: 48 $ PV: 75 $

US

Wind: 54 $ PV: 81 $

Brazil

Wind: 76 $ PV: 76 $

South Africa

PV: 88 $

India

Inve

sto

r R

ela

tio

ns

Strategic outlook

Renewable sector competitiveness

17

Development increasingly based on competitive tender processes

Increased appeal to financial investors

Emergence of global competitors

More reliable and long-lasting technology

Inve

sto

r R

ela

tio

ns

Strategic outlook

EGP a global player optimally positioned for success

18

Diversified geographical footprint to take advantage of opportunities globally

Maximization of asset value

Rising predictability of cash-flow

Ability to deploy multiple technologies

Proven flexibility in capital allocation

Inve

sto

r R

ela

tio

ns

Strategic outlook

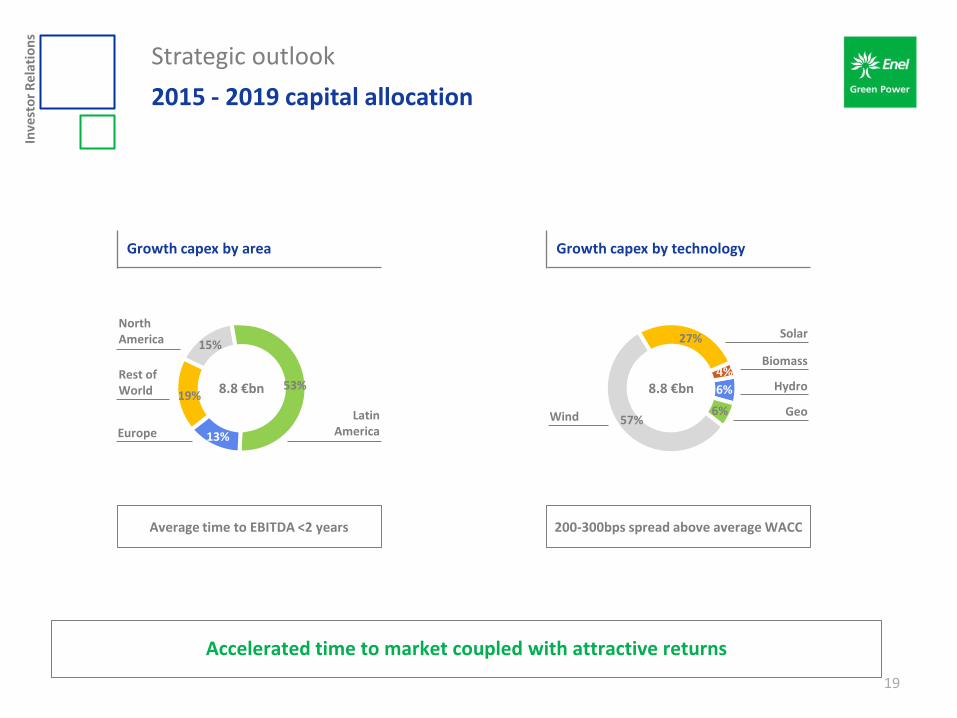

2015 - 2019 capital allocation

19

Accelerated time to market coupled with attractive returns

200-300bps spread above average WACC Average time to EBITDA <2 years

19%

15%

53%

13%

8.8 €bn Rest of World

Europe

Latin America

North America

Growth capex by area Growth capex by technology

6%

6% 57%

27%

8.8 €bn

Wind

Biomass

Solar

Hydro 4%

Geo

Inve

sto

r R

ela

tio

ns

Strategic outlook

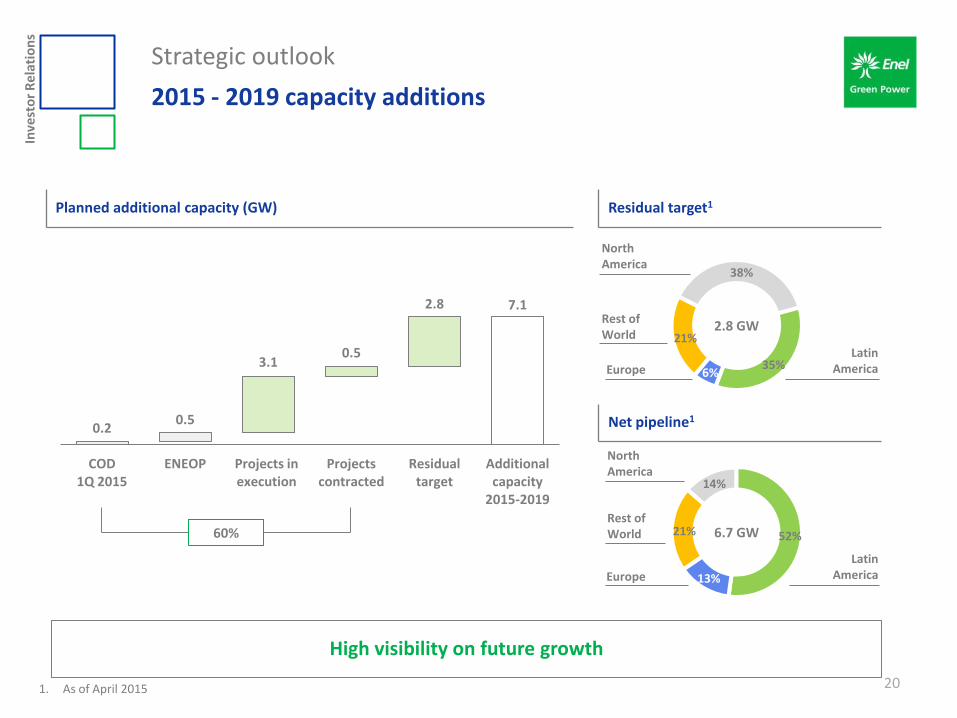

2015 - 2019 capacity additions

20

High visibility on future growth

Planned additional capacity (GW)

60%

0.2 0.5

3.1 0.5

2.8 7.1

COD 1Q 2015

ENEOP Projects in execution

Projects contracted

Residual target

Additional capacity

2015-2019

1. As of April 2015

Residual target1

Net pipeline1

21%

14%

52%

13%

6.7 GW Rest of World

Europe

Latin America

North America

21%

38%

35% 6%

2.8 GW Rest of World

Europe

Latin America

North America

Inve

sto

r R

ela

tio

ns

Strategic outlook

21

Anticipating growth trends

19%

15%

50%

16%

Latin America

Rest of World

North America

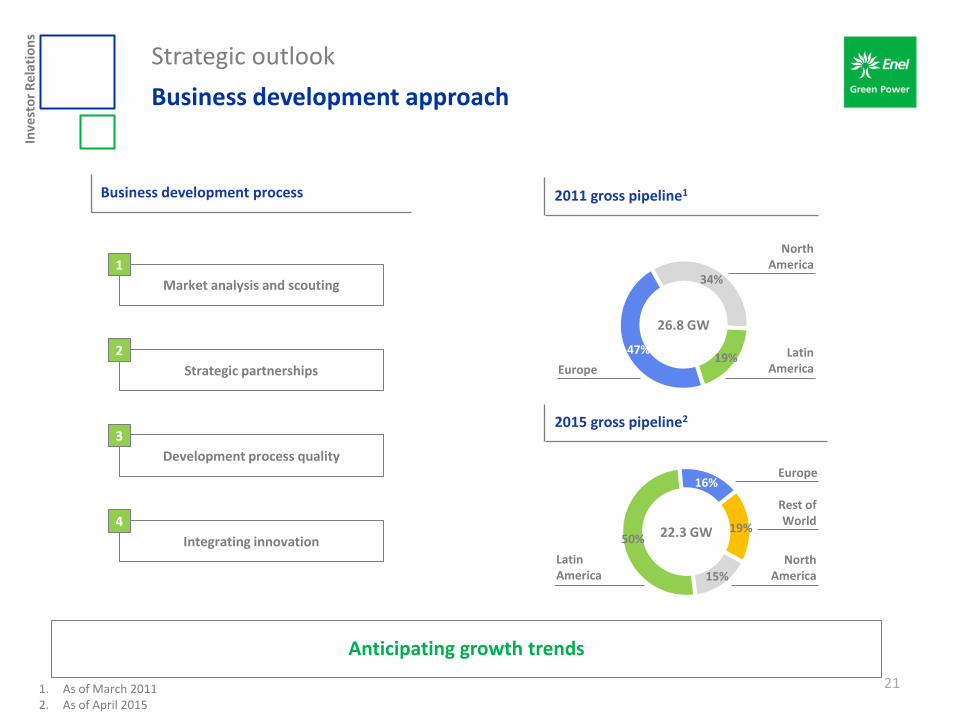

22.3 GW

Europe

34%

19% 47%

Europe

Latin America

North America

26.8 GW

2015 gross pipeline2

Business development approach

2011 gross pipeline1 Business development process

Market analysis and scouting

1

Strategic partnerships

2

Development process quality

3

Integrating innovation

4

1. As of March 2011 2. As of April 2015

Inve

sto

r R

ela

tio

ns

Strategic outlook

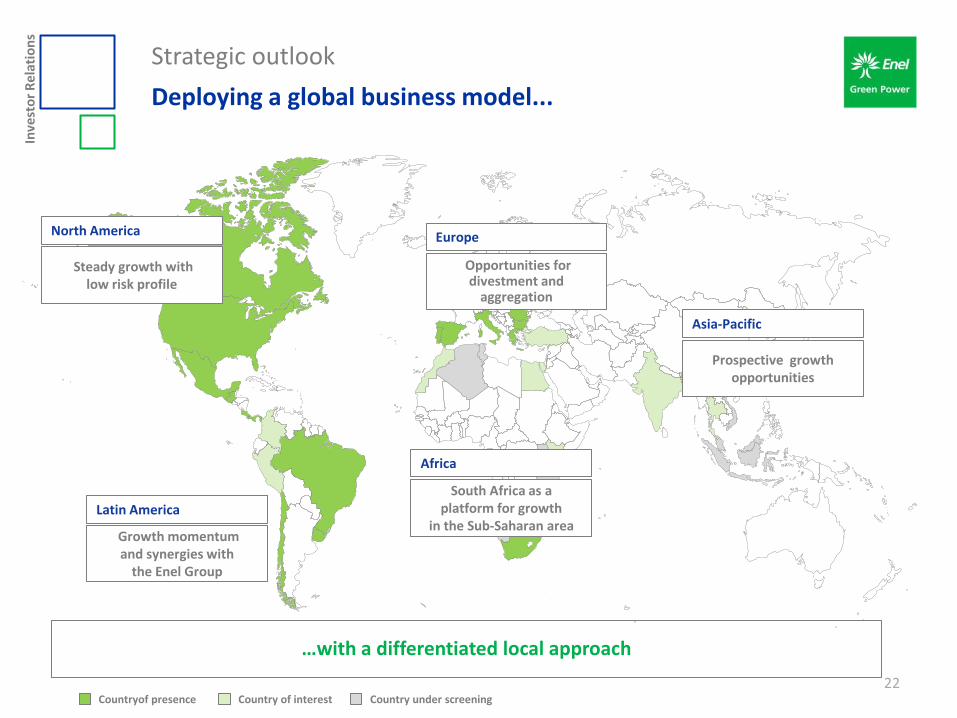

Deploying a global business model...

22

…with a differentiated local approach

Growth momentum and synergies with

the Enel Group

Latin America

Steady growth with low risk profile

North America

Opportunities for divestment and

aggregation

Europe

Prospective growth opportunities

Asia-Pacific

South Africa as a platform for growth

in the Sub-Saharan area

Africa

Country of interest Countryof presence Country under screening

Inve

sto

r R

ela

tio

ns

Strategic outlook

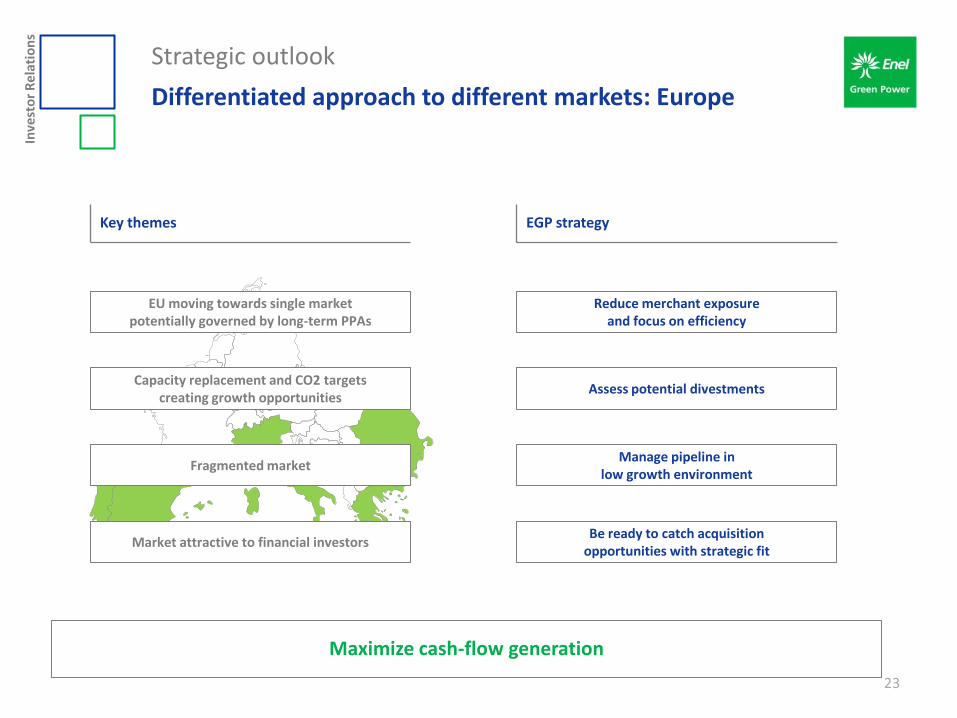

Differentiated approach to different markets: Europe

23

Assess potential divestments

Reduce merchant exposure and focus on efficiency

Manage pipeline in low growth environment

Be ready to catch acquisition opportunities with strategic fit

Key themes EGP strategy

Maximize cash-flow generation

EU moving towards single market potentially governed by long-term PPAs

Fragmented market

Market attractive to financial investors

Capacity replacement and CO2 targets creating growth opportunities

Inve

sto

r R

ela

tio

ns

Strategic outlook

Differentiated approach to different markets: North America

24

Managed growth

Long-term strategic partnerships

Greenfield development

Key themes EGP strategy

Steady progress over medium term

Coal capacity replacement and production mix diversification

Highly competitive market with a strong momentum in M&A activities

Greenfield development increasingly difficult but still offering interesting returns

Inve

sto

r R

ela

tio

ns

Strategic outlook

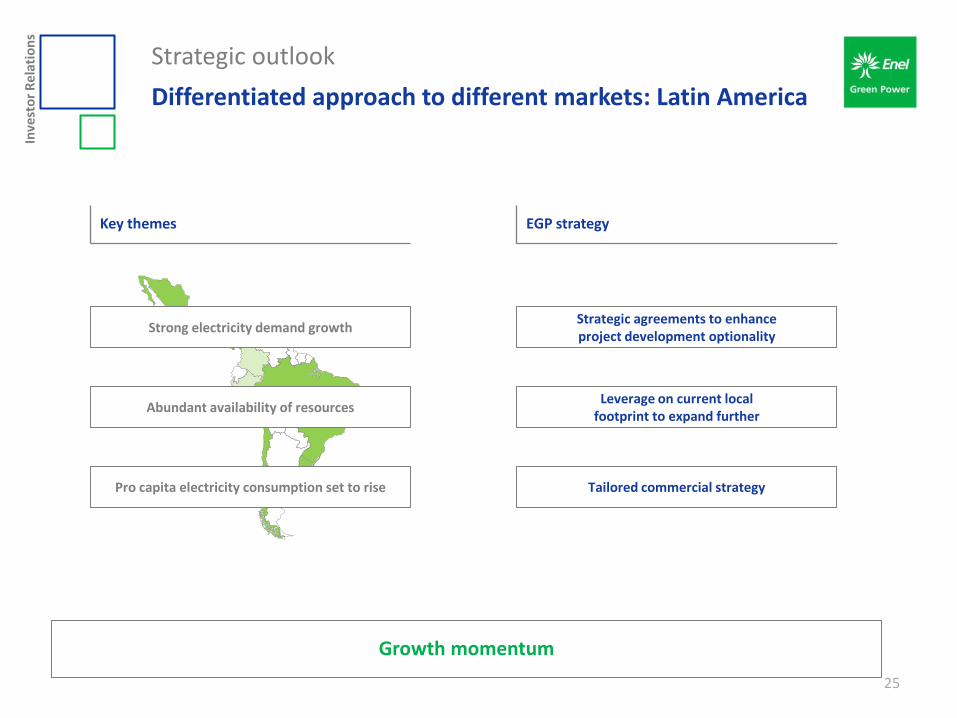

Differentiated approach to different markets: Latin America

25

Leverage on current local footprint to expand further

Strategic agreements to enhance project development optionality

Tailored commercial strategy

Key themes EGP strategy

Growth momentum

Abundant availability of resources

Strong electricity demand growth

Pro capita electricity consumption set to rise

Inve

sto

r R

ela

tio

ns

Strategic outlook

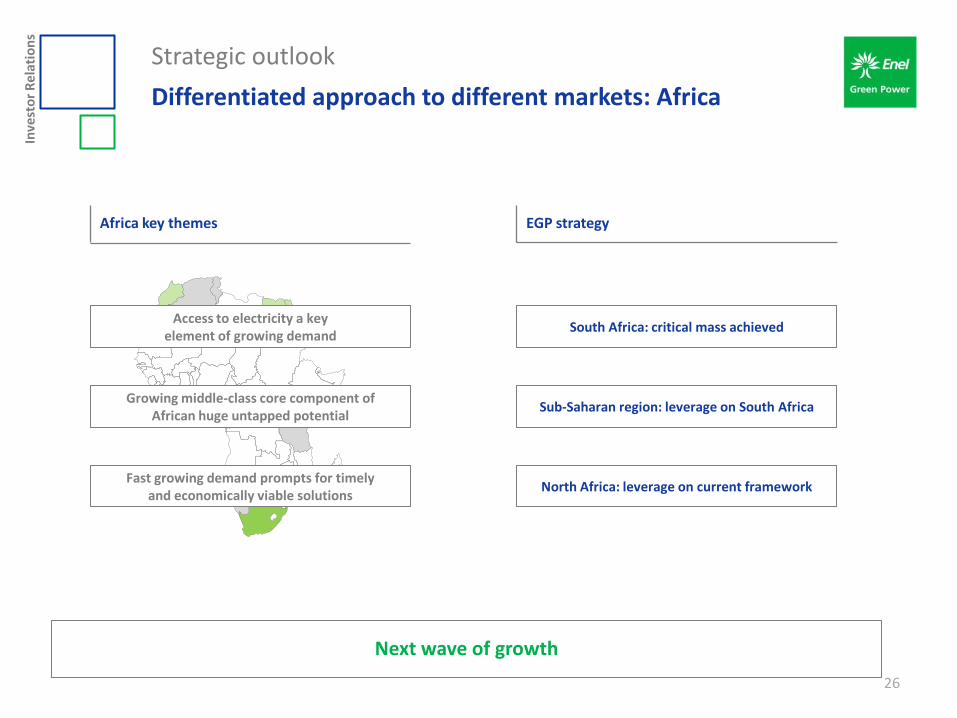

Differentiated approach to different markets: Africa

26

Africa key themes EGP strategy

Next wave of growth

Growing middle-class core component of African huge untapped potential

Access to electricity a key element of growing demand

Fast growing demand prompts for timely and economically viable solutions

Sub-Saharan region: leverage on South Africa

South Africa: critical mass achieved

North Africa: leverage on current framework

Inve

sto

r R

ela

tio

ns

Strategic outlook

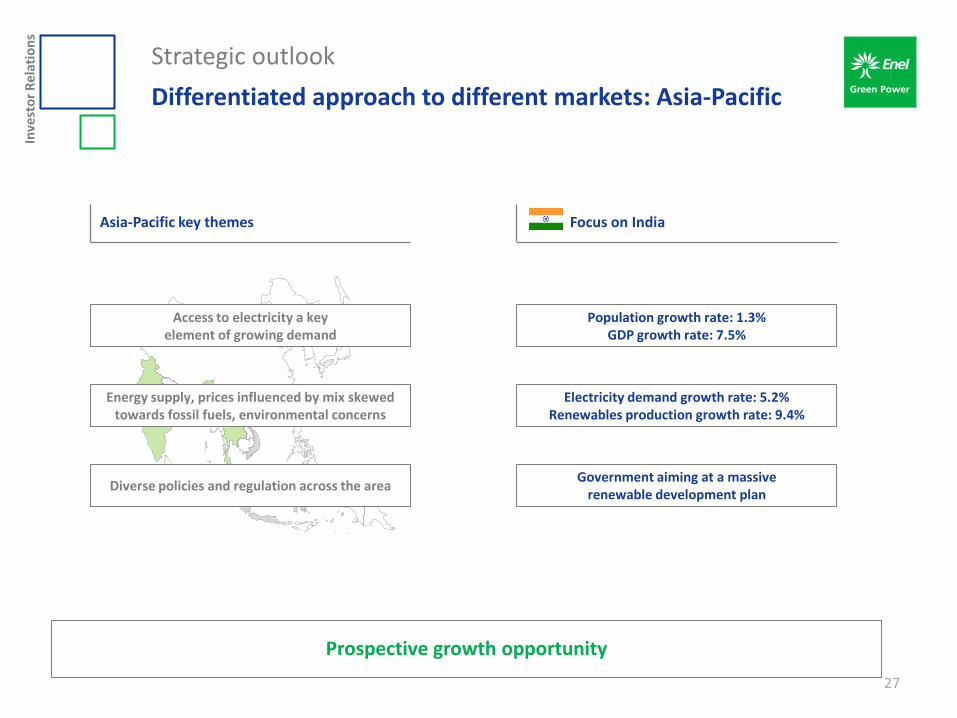

Differentiated approach to different markets: Asia-Pacific

27

Asia-Pacific key themes Focus on India

Prospective growth opportunity

Energy supply, prices influenced by mix skewed towards fossil fuels, environmental concerns

Access to electricity a key element of growing demand

Diverse policies and regulation across the area

Electricity demand growth rate: 5.2% Renewables production growth rate: 9.4%

Population growth rate: 1.3% GDP growth rate: 7.5%

Government aiming at a massive renewable development plan

Inve

sto

r R

ela

tio

ns

Strategic outlook

Asset value maximization

28

Technological leadership in EPC and O&M

Production optimization

EPC1 as a project quality accretive tool

O&M cost efficiency

1. Engineering, Procurement and Construction

Inve

sto

r R

ela

tio

ns

Strategic outlook

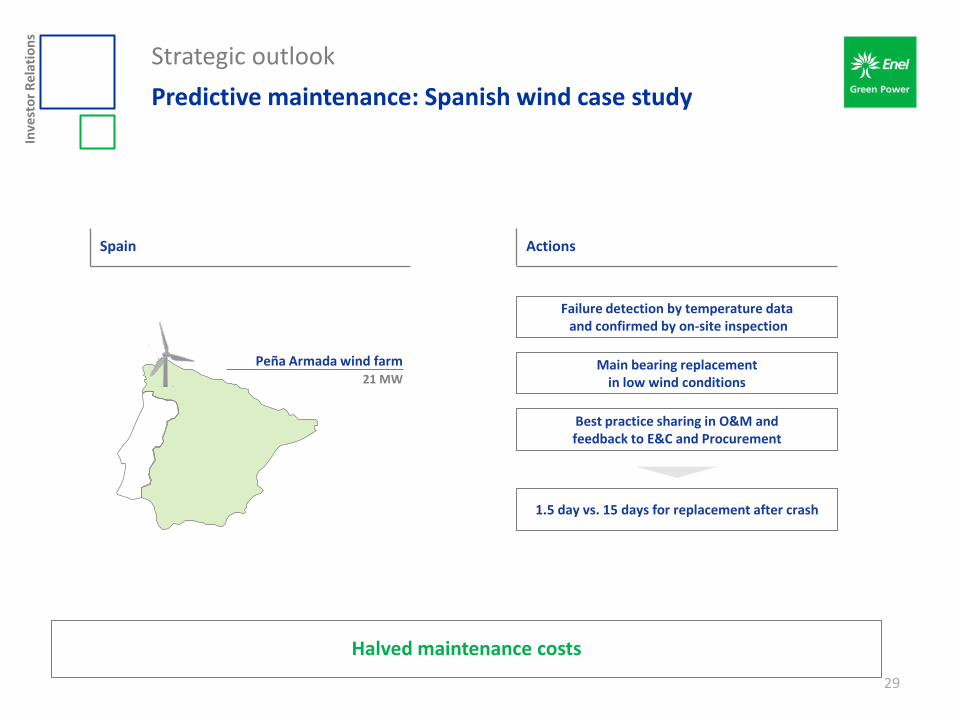

Predictive maintenance: Spanish wind case study

29

Spain Actions

Peña Armada wind farm 21 MW

Best practice sharing in O&M and feedback to E&C and Procurement

Failure detection by temperature data and confirmed by on-site inspection

1.5 day vs. 15 days for replacement after crash

Halved maintenance costs

Main bearing replacement in low wind conditions

Inve

sto

r R

ela

tio

ns

Strategic outlook

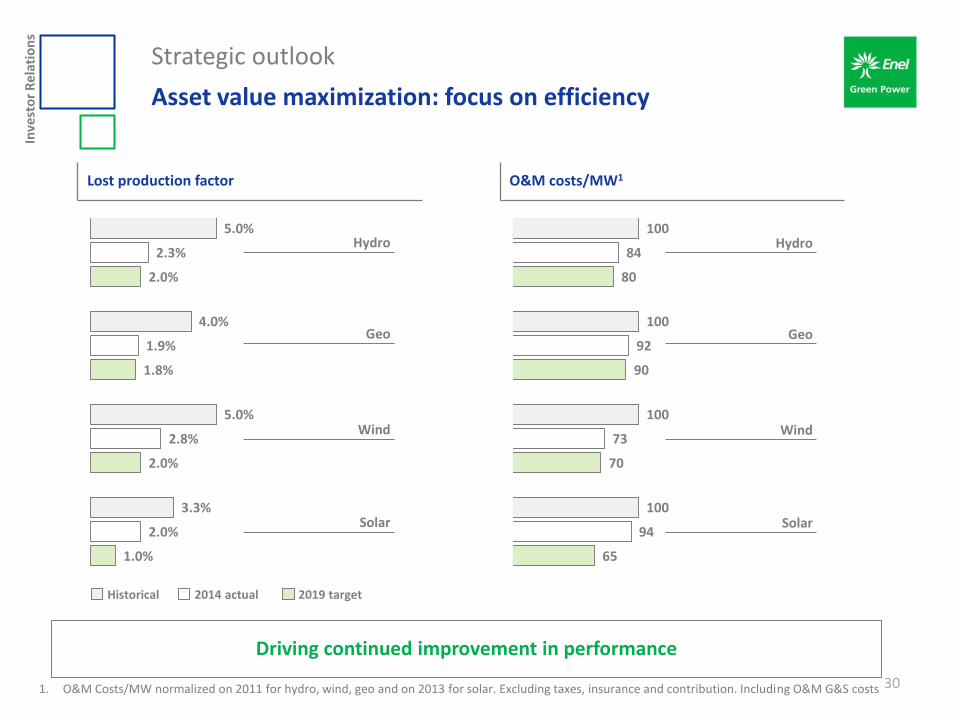

Asset value maximization: focus on efficiency

30

Driving continued improvement in performance

Lost production factor O&M costs/MW1

1.0%

2.0%

1.8%

2.0%

2.0%

2.8%

1.9%

2.3%

3.3%

5.0%

4.0%

5.0% Hydro

Geo

Wind

Solar

65

70

90

80

94

73

92

84

100

100

100

100 Hydro

Geo

Wind

Solar

Historical 2014 actual 2019 target

1. O&M Costs/MW normalized on 2011 for hydro, wind, geo and on 2013 for solar. Excluding taxes, insurance and contribution. Including O&M G&S costs

Inve

sto

r R

ela

tio

ns

Strategic outlook

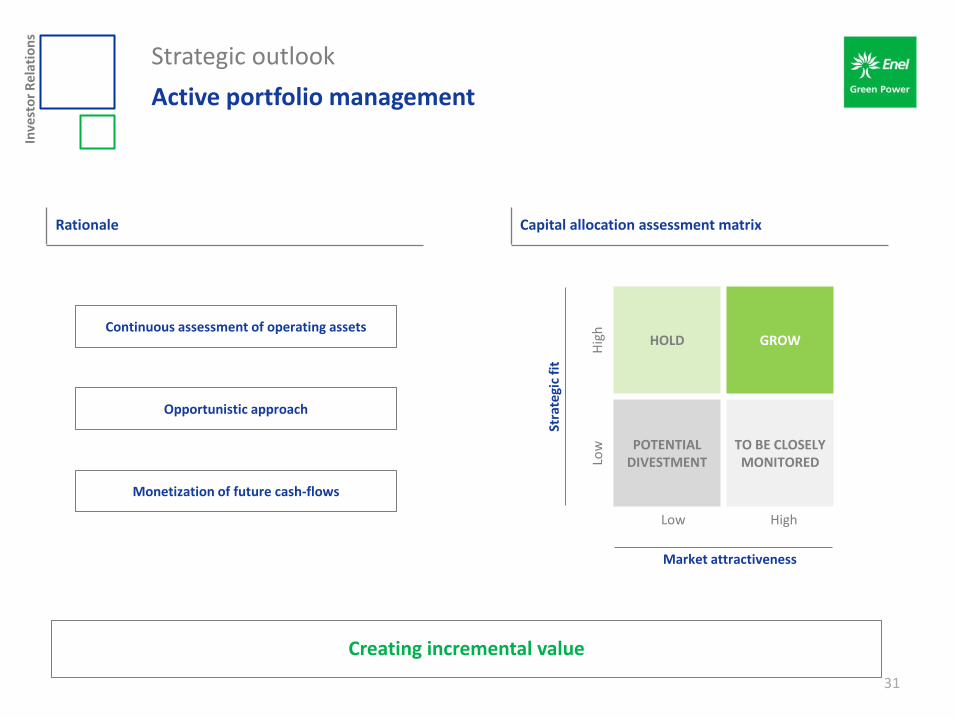

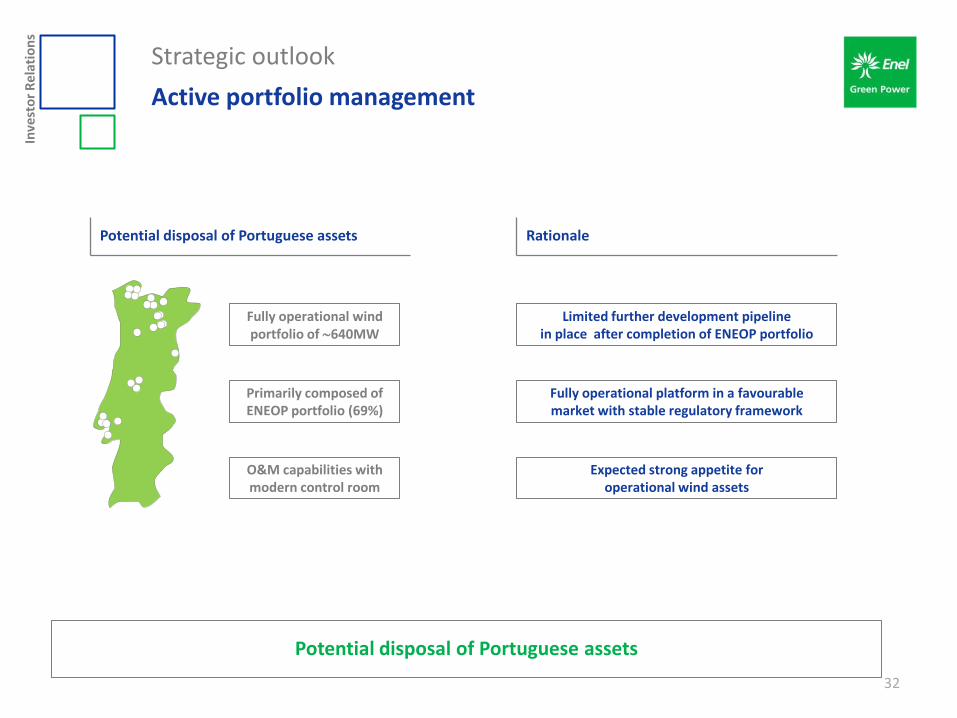

Active portfolio management

31

Creating incremental value

Rationale Capital allocation assessment matrix

Opportunistic approach

Continuous assessment of operating assets

Monetization of future cash-flows

HOLD GROW

POTENTIAL DIVESTMENT

TO BE CLOSELY MONITORED

Stra

tegi

c fi

t

Low

H

igh

Market attractiveness

Low High

Inve

sto

r R

ela

tio

ns

Strategic outlook

Active portfolio management

32

Potential disposal of Portuguese assets

Fully operational wind portfolio of 640MW

Primarily composed of ENEOP portfolio (69%)

O&M capabilities with modern control room

Fully operational platform in a favourable market with stable regulatory framework

Limited further development pipeline in place after completion of ENEOP portfolio

Expected strong appetite for operational wind assets

Potential disposal of Portuguese assets Rationale

Inve

sto

r R

ela

tio

ns

2015 Investor day

Agenda

33

Introduction Francesco Venturini, CEO

1Q 2015 consolidated results Francesco Venturini, CEO - Giulio Carone, CFO

Strategic outlook Francesco Venturini, CEO

2015 - 2019 financial outlook Giulio Carone, CFO

Closing remarks Francesco Venturini, CEO

Inve

sto

r R

ela

tio

ns

2015 - 2019 financial outlook

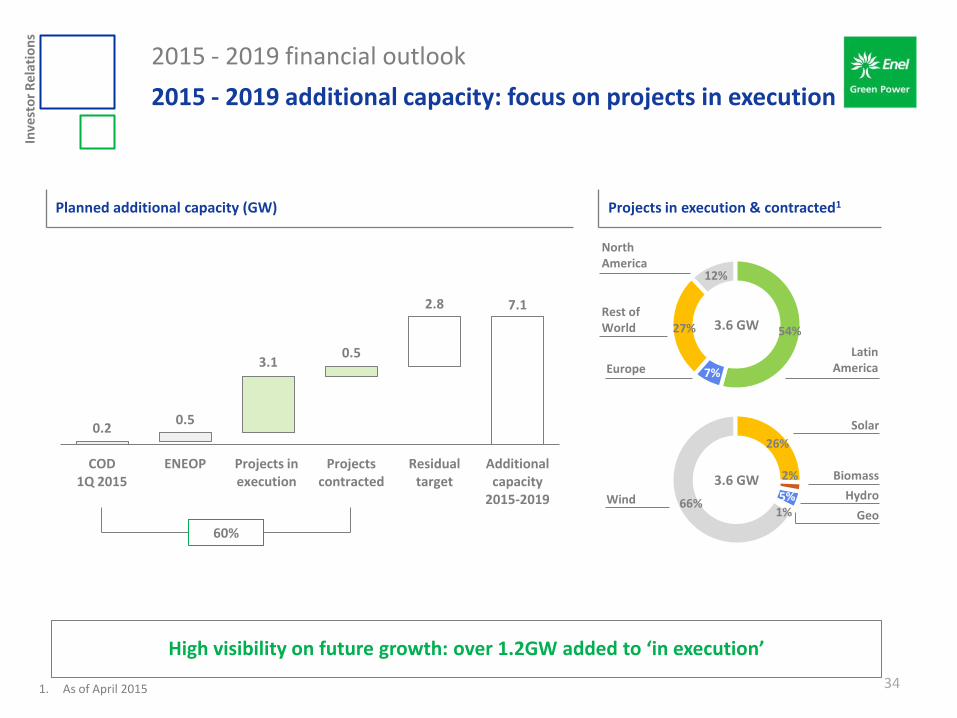

2015 - 2019 additional capacity: focus on projects in execution

34

High visibility on future growth: over 1.2GW added to ‘in execution’

Planned additional capacity (GW) Projects in execution & contracted1

27%

12%

54%

7%

3.6 GW Rest of World

Europe

Latin America

North America

60%

0.2 0.5

3.1 0.5

2.8 7.1

COD 1Q 2015

ENEOP Projects in execution

Projects contracted

Residual target

Additional capacity

2015-2019 Geo

5% 1%

66%

26%

2% 3.6 GW

Wind

Biomass

Solar

Hydro

1. As of April 2015

Inve

sto

r R

ela

tio

ns

2015 - 2019 financial outlook

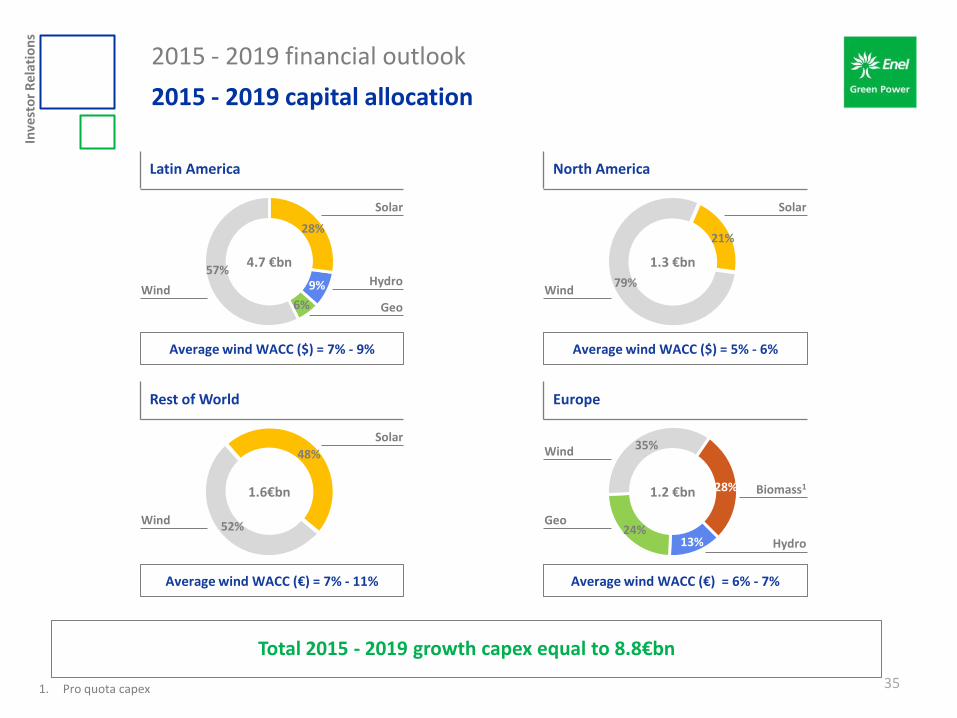

2015 - 2019 capital allocation

35

North America Latin America

Europe Rest of World

Average wind WACC (€) = 7% - 11% Average wind WACC (€) = 6% - 7%

Average wind WACC ($) = 5% - 6% Average wind WACC ($) = 7% - 9%

9%

6%

57%

28%

4.7 €bn

Wind

Geo

Solar

Hydro 79%

21%

1.3 €bn

Wind

Solar

52%

48%

1.6€bn

Wind

Solar

13% 24%

35%

28% 1.2 €bn

Geo

Biomass1

Hydro

Wind

1. Pro quota capex

Total 2015 - 2019 growth capex equal to 8.8€bn

Inve

sto

r R

ela

tio

ns

2015 - 2019 financial outlook

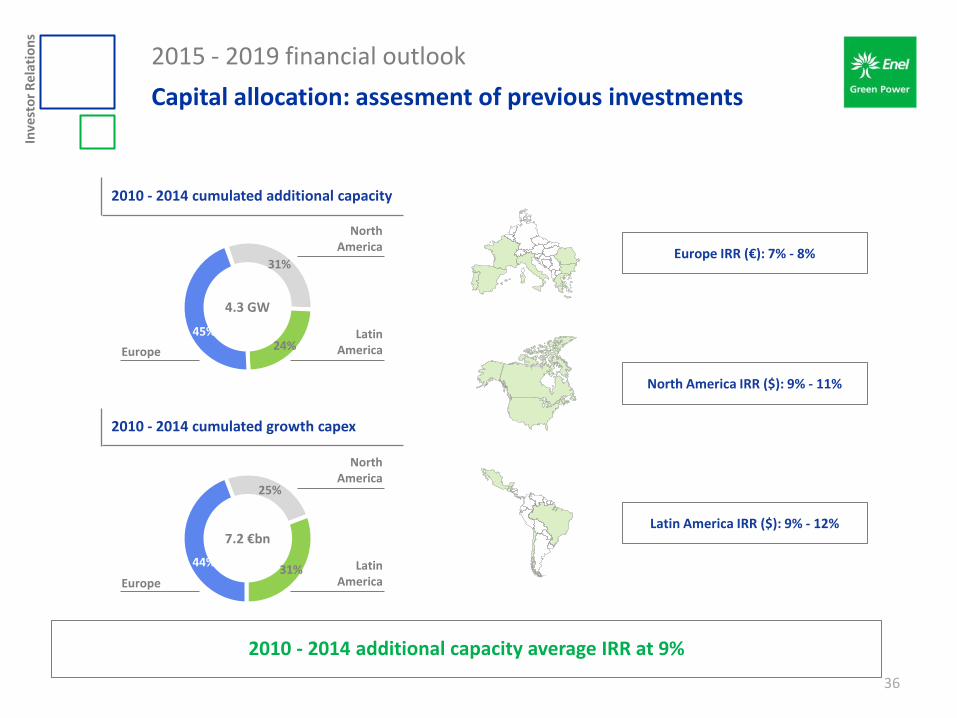

Capital allocation: assesment of previous investments

36

2010 - 2014 cumulated additional capacity

2010 - 2014 additional capacity average IRR at 9%

2010 - 2014 cumulated growth capex

North America IRR ($): 9% - 11%

Europe IRR (€): 7% - 8%

Latin America IRR ($): 9% - 12%

31%

24% 45%

4.3 GW

Europe

Latin America

North America

25%

31% 44%

7.2 €bn

Europe

Latin America

North America

Inve

sto

r R

ela

tio

ns

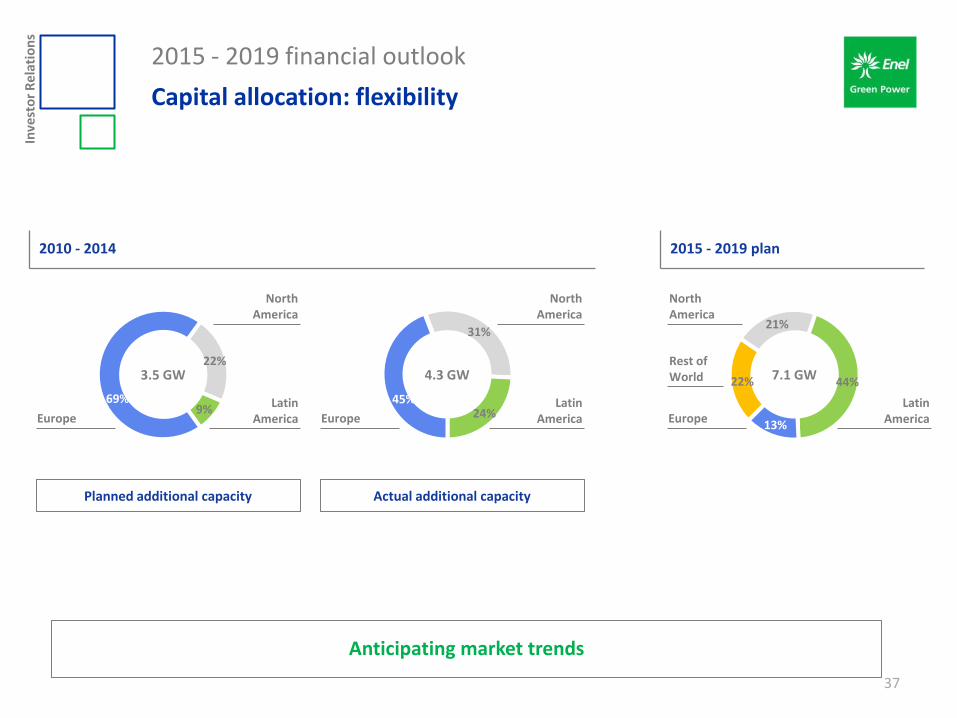

22%

9% 69%

3.5 GW

Europe Latin

America

North America

22%

21%

44%

13%

7.1 GW Rest of World

Europe Latin

America

North America

2015 - 2019 financial outlook

Capital allocation: flexibility

37

2010 - 2014 2015 - 2019 plan

Anticipating market trends

31%

24% 45%

4.3 GW

Europe Latin

America

North America

Planned additional capacity Actual additional capacity

Inve

sto

r R

ela

tio

ns

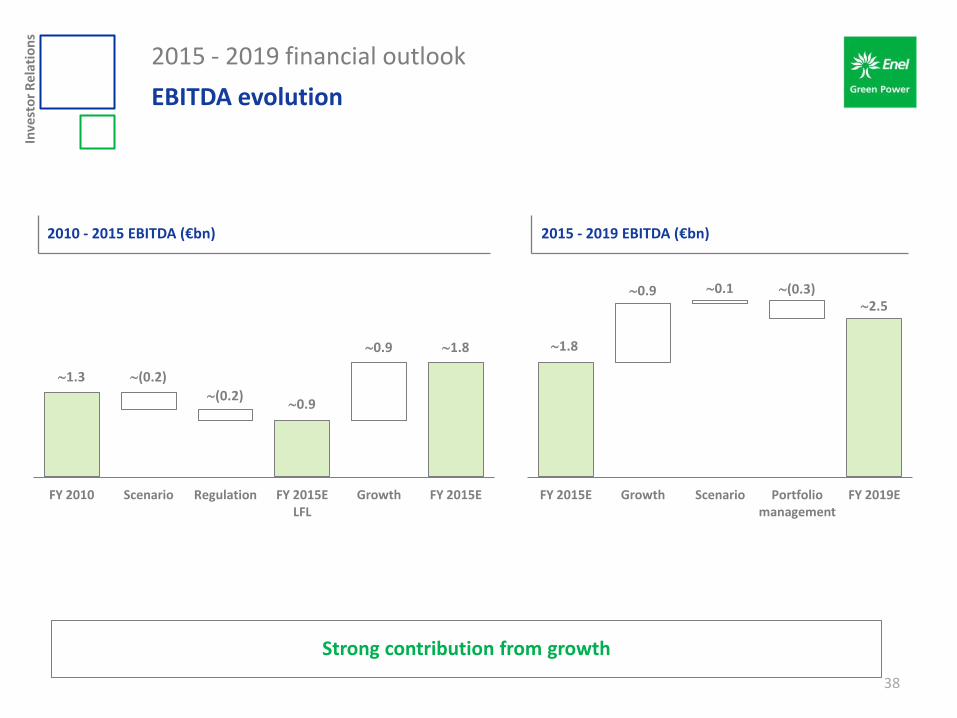

2015 - 2019 financial outlook

EBITDA evolution

38

0.9

1.3 (0.2)

(0.2)

0.9 1.8

FY 2010 Scenario Regulation FY 2015E LFL

Growth FY 2015E

2015 - 2019 EBITDA (€bn) 2010 - 2015 EBITDA (€bn)

1.8

0.9 0.1 (0.3) 2.5

FY 2015E Growth Scenario Portfolio management

FY 2019E

Strong contribution from growth

Inve

sto

r R

ela

tio

ns

2015 - 2019 financial outlook

High predictability of cash-flows

39

North America Europe

Rest of World Latin America

50%

50%

Long-term structural hedge at 70%

90% 10% 100%

90%

10%

50% 90%

90% 100%

Unhedged volumes

Hedged volumes

Inve

sto

r R

ela

tio

ns

2015 - 2019 financial outlook

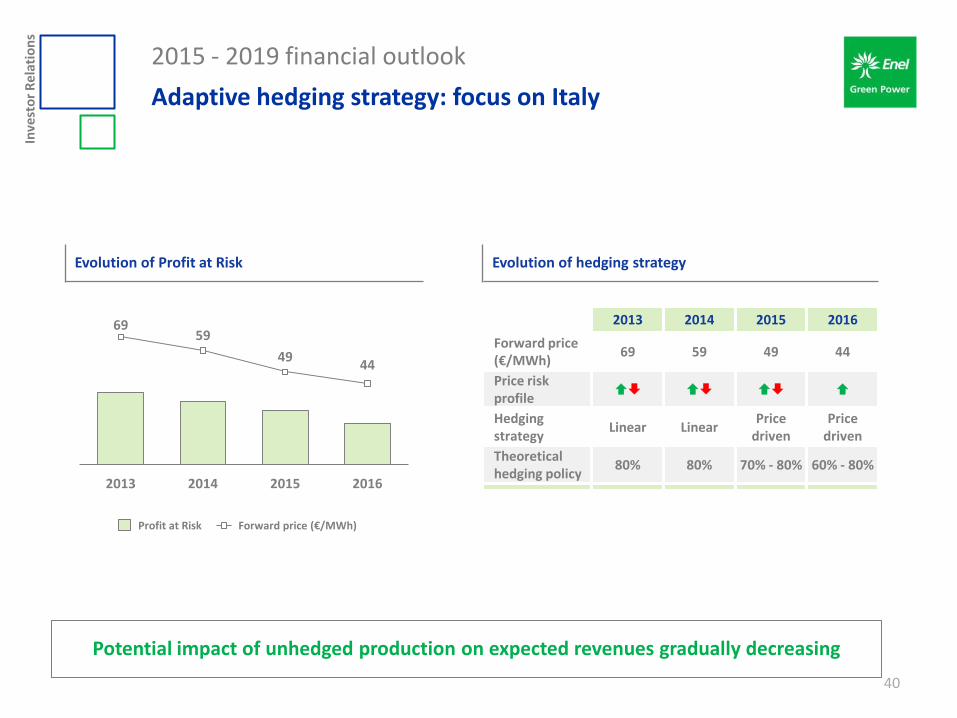

Adaptive hedging strategy: focus on Italy

40

Potential impact of unhedged production on expected revenues gradually decreasing

Evolution of Profit at Risk

69 59

49 44

0

50

100

150

200

250

300

2013 2014 2015 2016

Forward price (€/MWh) Profit at Risk

2013 2014 2015 2016

Forward price (€/MWh)

69 59 49 44

Price risk profile

Hedging strategy

Linear Linear Price

driven Price

driven

Theoretical hedging policy

80% 80% 70% - 80% 60% - 80%

Evolution of hedging strategy

Inve

sto

r R

ela

tio

ns

Forward sales

41

Spain1 Italy

North America Latin America

91% 91%

2015 2016

85% 46%

2015 2016

70%

2015 2016

95% 91%

2015 2016

1. Share of hedged production from capacity <2004

Unhedged volumes

Hedged volumes

2015 - 2019 financial outlook

Inve

sto

r R

ela

tio

ns

2015 - 2019 financial outlook

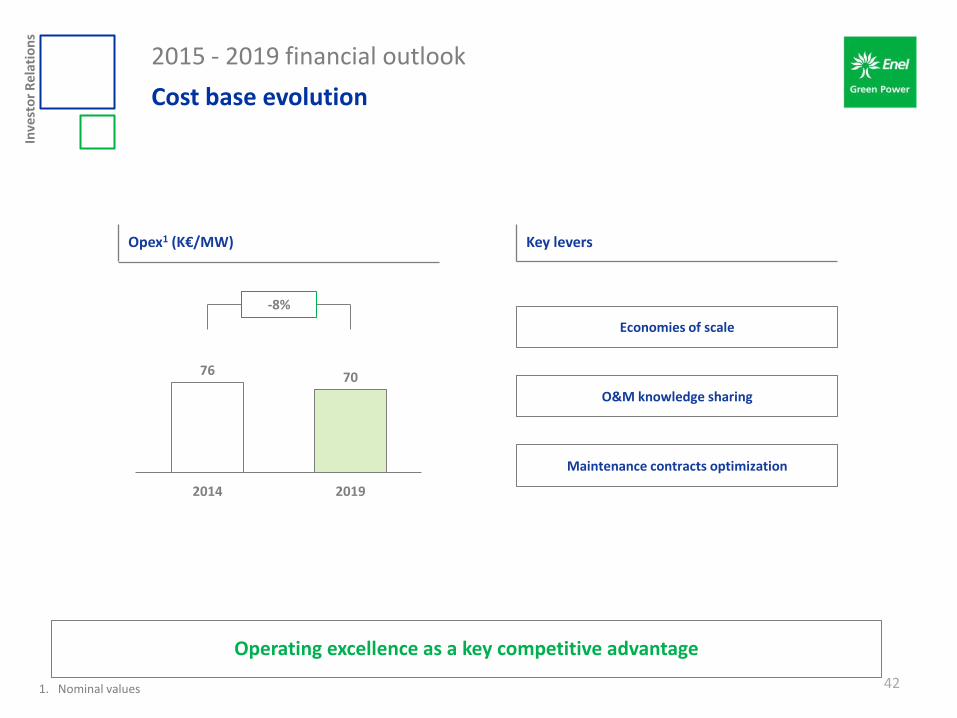

Cost base evolution

42

Opex1 (K€/MW)

76 70

2014 2019

-8%

O&M knowledge sharing

Economies of scale

Maintenance contracts optimization

Key levers

Operating excellence as a key competitive advantage

1. Nominal values

Inve

sto

r R

ela

tio

ns

2015 - 2019 financial outlook

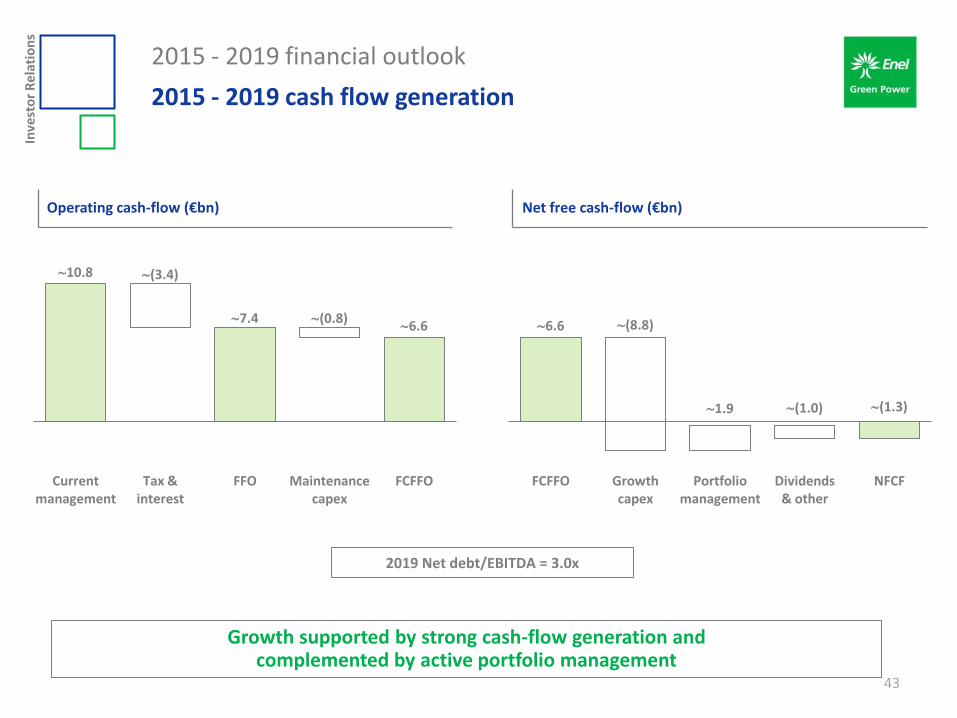

2015 - 2019 cash flow generation

43

Net free cash-flow (€bn) Operating cash-flow (€bn)

Growth supported by strong cash-flow generation and complemented by active portfolio management

2019 Net debt/EBITDA = 3.0x

10.8

7.4 6.6

(3.4)

(0.8)

Current management

Tax & interest

FFO Maintenance capex

FCFFO

6.6 (8.8)

1.9 (1.0) (1.3)

FCFFO Growth capex

Portfolio management

Dividends & other

NFCF

Inve

sto

r R

ela

tio

ns

2015 Investor day

Agenda

44

Introduction Francesco Venturini, CEO

1Q 2015 consolidated results Francesco Venturini, CEO - Giulio Carone, CFO

Strategic outlook Francesco Venturini, CEO

2015 - 2019 financial outlook Giulio Carone, CFO

Closing remarks Francesco Venturini, CEO

Inve

sto

r R

ela

tio

ns

2015 Investor day

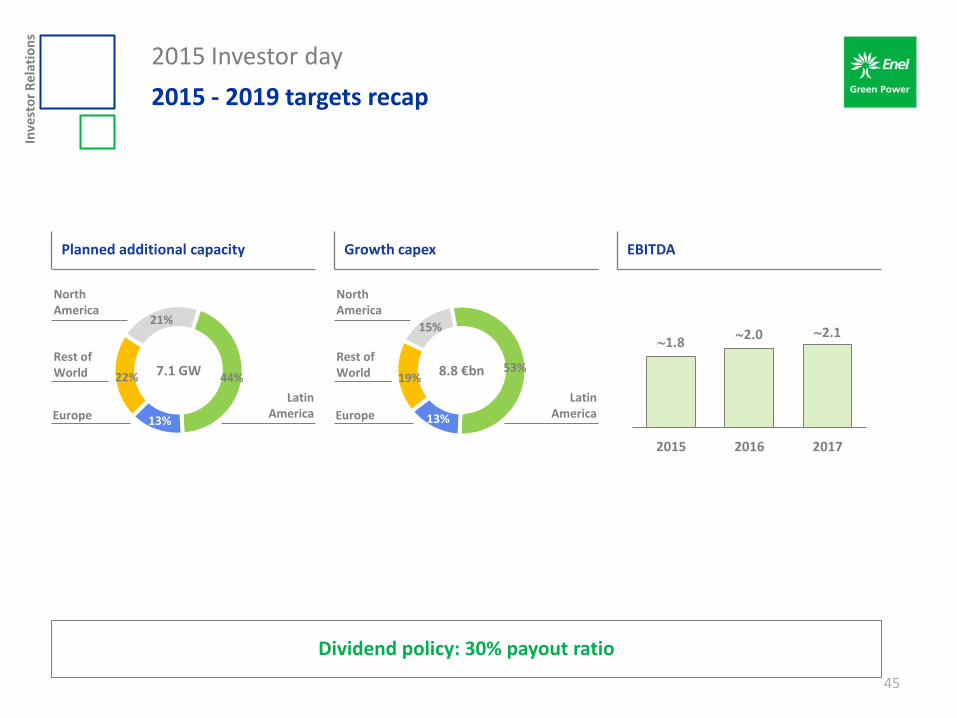

2015 - 2019 targets recap

45

EBITDA

1.8 2.0 2.1

2015 2016 2017

Dividend policy: 30% payout ratio

Growth capex

19%

15%

53%

13%

8.8 €bn Rest of World

Europe

Latin America

North America

Planned additional capacity

22%

21%

44%

13%

7.1 GW Rest of World

Europe

Latin America

North America

Inve

sto

r R

ela

tio

ns

2015 Investor day

Closing remarks

46

Global presence in attractive markets

Accelerating growth

Delivering attractive returns and predictable cash-flows

Actively managing asset portfolio

Maximizing efficiency

Rome – May 7, 2015

Enel Green Power 2015 Investor day Strategic annexes

Inve

sto

r R

ela

tio

ns

2015 Investor day - strategic annexes

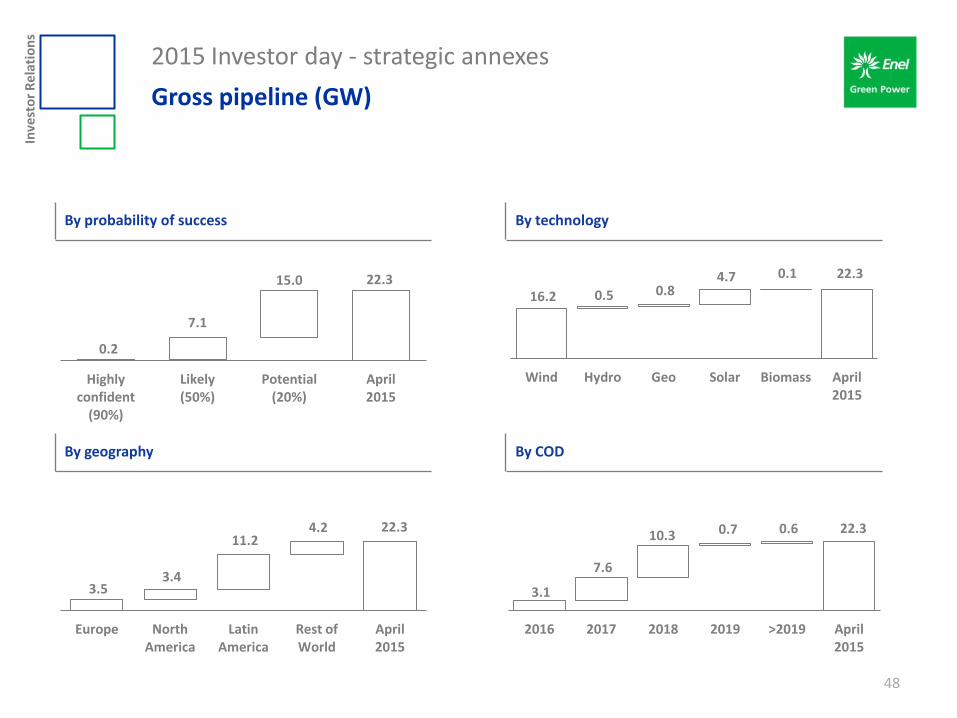

Gross pipeline (GW)

48

0.2

7.1

15.0 22.3

Highly confident

(90%)

Likely (50%)

Potential (20%)

April 2015

16.2 0.5 0.8 4.7 0.1 22.3

Wind Hydro Geo Solar Biomass April 2015

3.5 3.4

11.2 4.2 22.3

Europe North America

Latin America

Rest of World

April 2015

3.1

7.6

10.3 0.7 0.6 22.3

2016 2017 2018 2019 >2019 April 2015

By technology By probability of success

By COD By geography

Inve

sto

r R

ela

tio

ns

Business unit Wind Hydro Geo Solar Other Total

Italy 20 9 - - 75 104

Greece 154 - - - - 154

Europe 174 9 - - 75 258

Brazil 470 102 - 266 - 838

Chile 224 - 38 336 - 598

Costa Rica - 50 - - - 50

Mexico 329 - - - - 329

Panama - - - 12 - 12

Uruguay 50 - - - - 50

Latin America 1,073 152 38 614 - 1,877

USA 424 - - - - 424

North America 424 - - - - 424

South Africa 199 - - 314 - 513

Rest of World 199 - - 314 - 513

Total 1,870 161 38 928 75 3,072

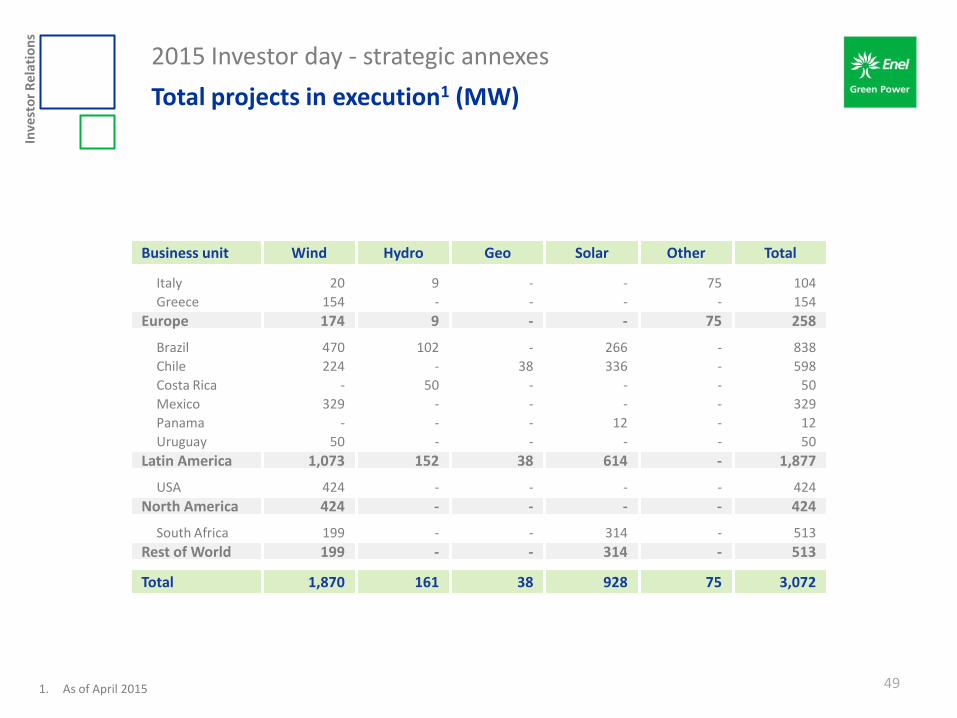

2015 Investor day - strategic annexes

Total projects in execution1 (MW)

49 1. As of April 2015

Inve

sto

r R

ela

tio

ns

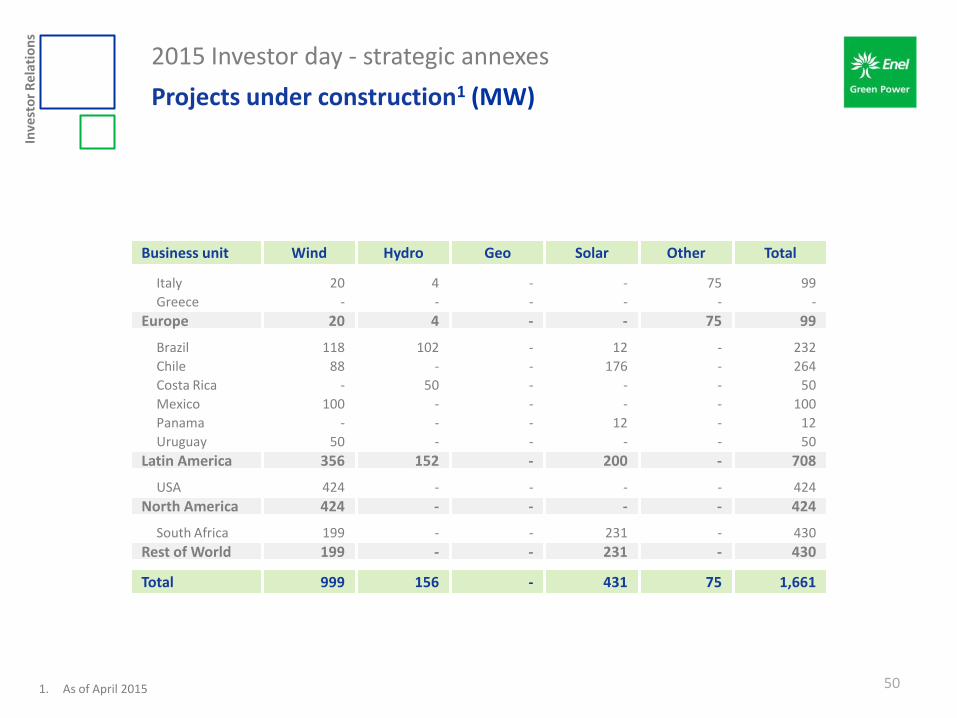

2015 Investor day - strategic annexes

Projects under construction1 (MW)

50

Business unit Wind Hydro Geo Solar Other Total

Italy 20 4 - - 75 99

Greece - - - - - -

Europe 20 4 - - 75 99

Brazil 118 102 - 12 - 232

Chile 88 - - 176 - 264

Costa Rica - 50 - - - 50

Mexico 100 - - - - 100

Panama - - - 12 - 12

Uruguay 50 - - - - 50

Latin America 356 152 - 200 - 708

USA 424 - - - - 424

North America 424 - - - - 424

South Africa 199 - - 231 - 430

Rest of World 199 - - 231 - 430

Total 999 156 - 431 75 1,661

1. As of April 2015

Inve

sto

r R

ela

tio

ns

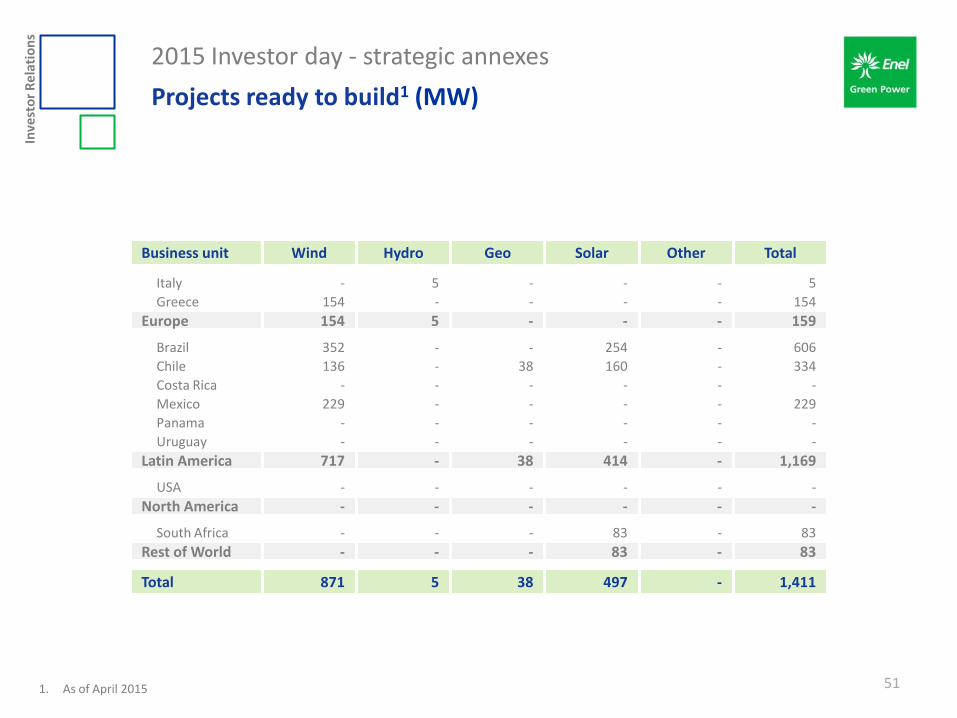

2015 Investor day - strategic annexes

Projects ready to build1 (MW)

51

Business unit Wind Hydro Geo Solar Other Total

Italy - 5 - - - 5

Greece 154 - - - - 154

Europe 154 5 - - - 159

Brazil 352 - - 254 - 606

Chile 136 - 38 160 - 334

Costa Rica - - - - - -

Mexico 229 - - - - 229

Panama - - - - - -

Uruguay - - - - - -

Latin America 717 - 38 414 - 1,169

USA - - - - - -

North America - - - - - -

South Africa - - - 83 - 83

Rest of World - - - 83 - 83

Total 871 5 38 497 - 1,411

1. As of April 2015

Inve

sto

r R

ela

tio

ns

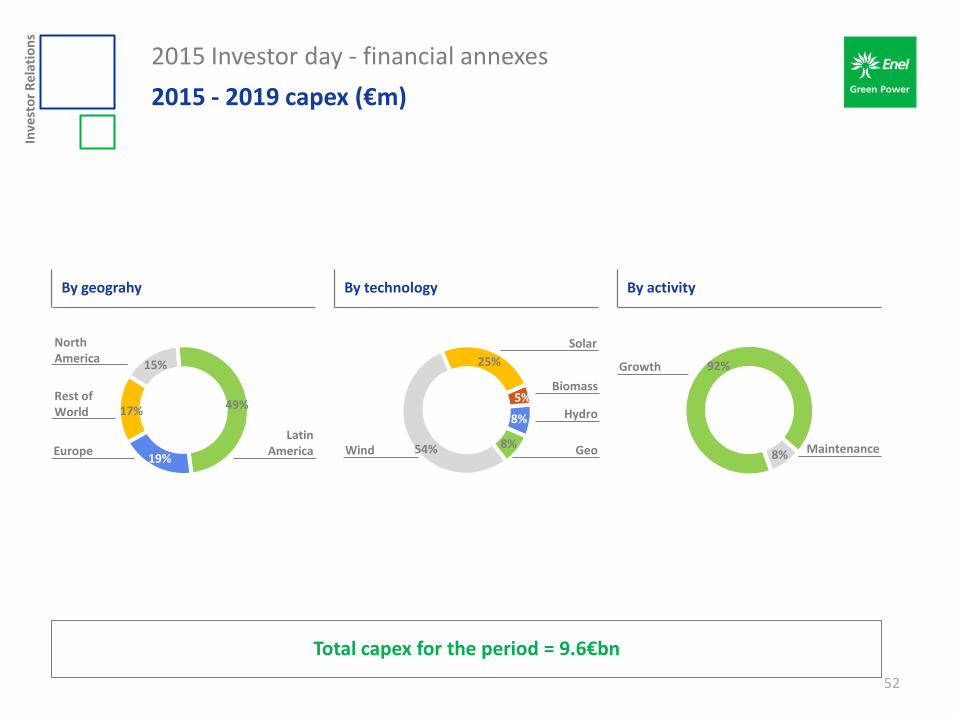

2015 Investor day - financial annexes

2015 - 2019 capex (€m)

52

Total capex for the period = 9.6€bn

By geograhy By technology By activity

92%

8%

Growth

Maintenance

17%

15%

49%

19%

Rest of World

Europe

Latin America

North America

8%

8% 54%

25%

5%

Wind

Biomass

Solar

Hydro

Geo

Inve

sto

r R

ela

tio

ns

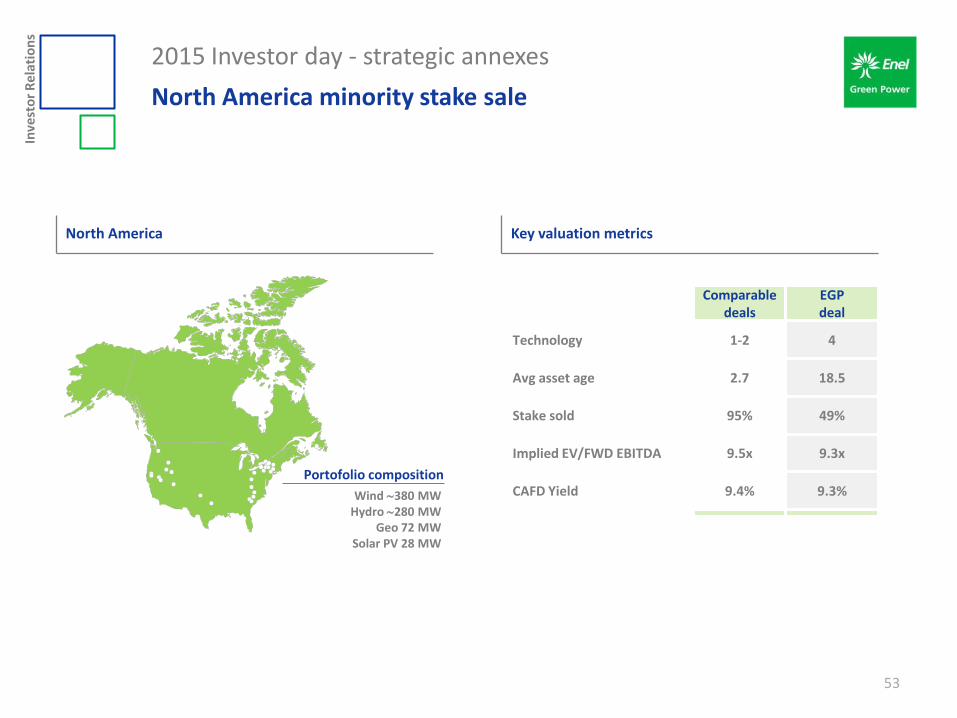

2015 Investor day - strategic annexes

North America minority stake sale

53

Key valuation metrics North America

Portofolio composition

Wind 380 MW Hydro 280 MW

Geo 72 MW Solar PV 28 MW

Comparable deals

EGP deal

Technology 1-2 4

Avg asset age 2.7 18.5

Stake sold 95% 49%

Implied EV/FWD EBITDA 9.5x 9.3x

CAFD Yield 9.4% 9.3%

Inve

sto

r R

ela

tio

ns

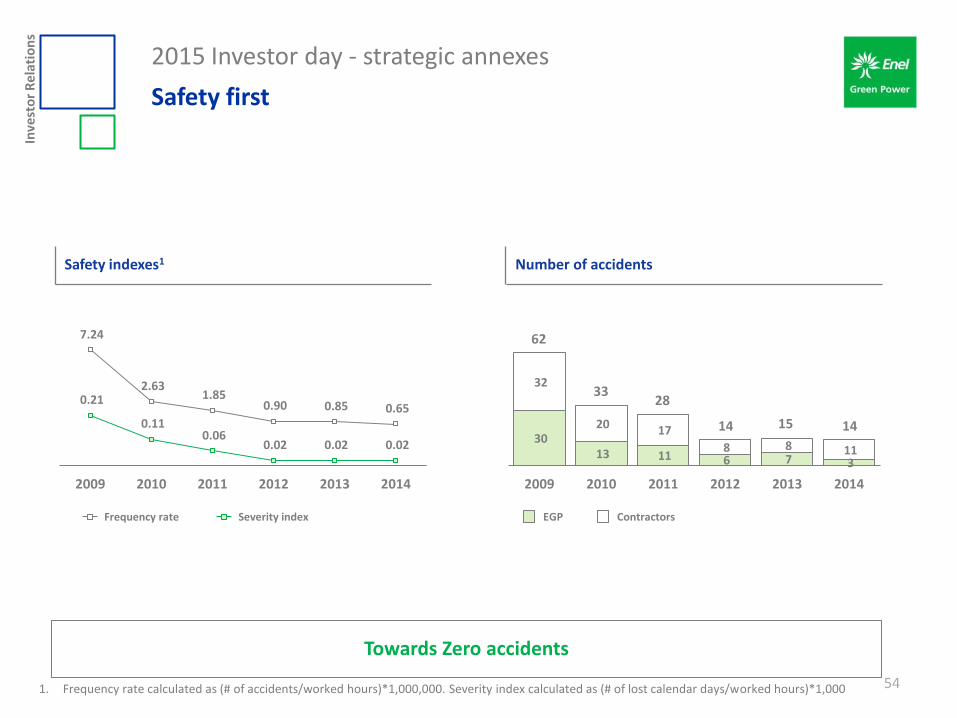

2015 Investor day - strategic annexes

Safety first

54 1. Frequency rate calculated as (# of accidents/worked hours)*1,000,000. Severity index calculated as (# of lost calendar days/worked hours)*1,000

Number of accidents Safety indexes1

Towards Zero accidents

30 13 11 6 7 3

32

20 17

8 8 11

2009 2010 2011 2012 2013 2014

62

33 28

14 15 14

7.24

2.63 1.85

0.90 0.85 0.65 0.21

0.11 0.06

0.02 0.02 0.02

-

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

2009 2010 2011 2012 2013 2014

Severity index EGP Contractors Frequency rate

Rome – May 7, 2015

Enel Green Power 2015 Investor day Financial annexes 1Q 2015 results

Inve

sto

r R

ela

tio

ns

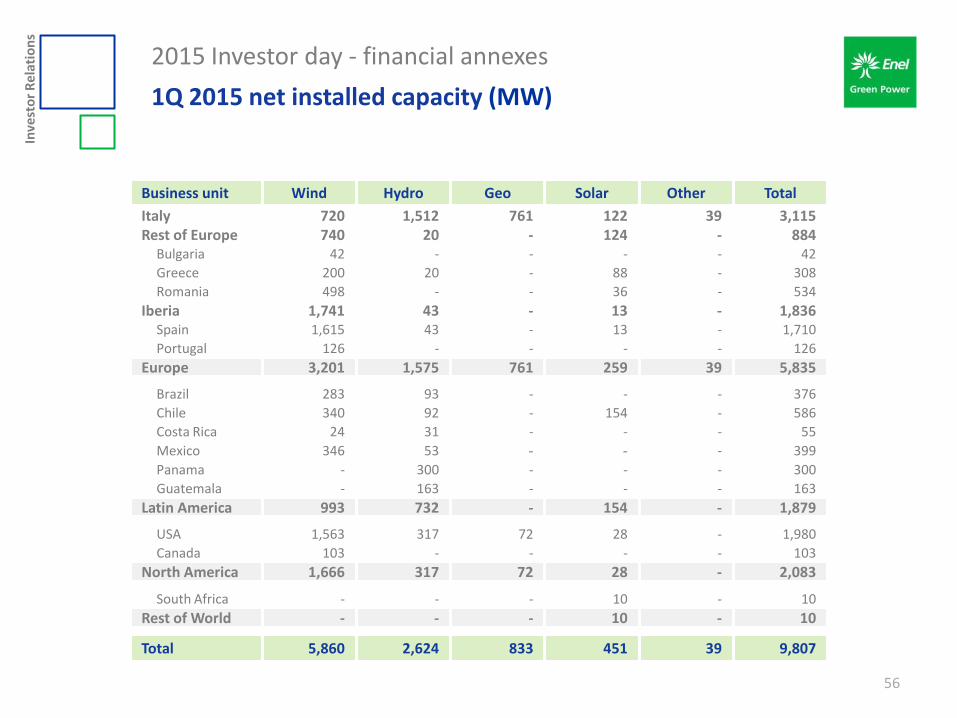

2015 Investor day - financial annexes 1Q 2015 net installed capacity (MW)

56

Business unit Wind Hydro Geo Solar Other Total

Italy 720 1,512 761 122 39 3,115 Rest of Europe 740 20 - 124 - 884

Bulgaria 42 - - - - 42

Greece 200 20 - 88 - 308

Romania 498 - - 36 - 534

Iberia 1,741 43 - 13 - 1,836 Spain 1,615 43 - 13 - 1,710

Portugal 126 - - - - 126

Europe 3,201 1,575 761 259 39 5,835

Brazil 283 93 - - - 376

Chile 340 92 - 154 - 586

Costa Rica 24 31 - - - 55

Mexico 346 53 - - - 399

Panama - 300 - - - 300

Guatemala - 163 - - - 163

Latin America 993 732 - 154 - 1,879

USA 1,563 317 72 28 - 1,980

Canada 103 - - - - 103

North America 1,666 317 72 28 - 2,083

South Africa - - - 10 - 10

Rest of World - - - 10 - 10

Total 5,860 2,624 833 451 39 9,807

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

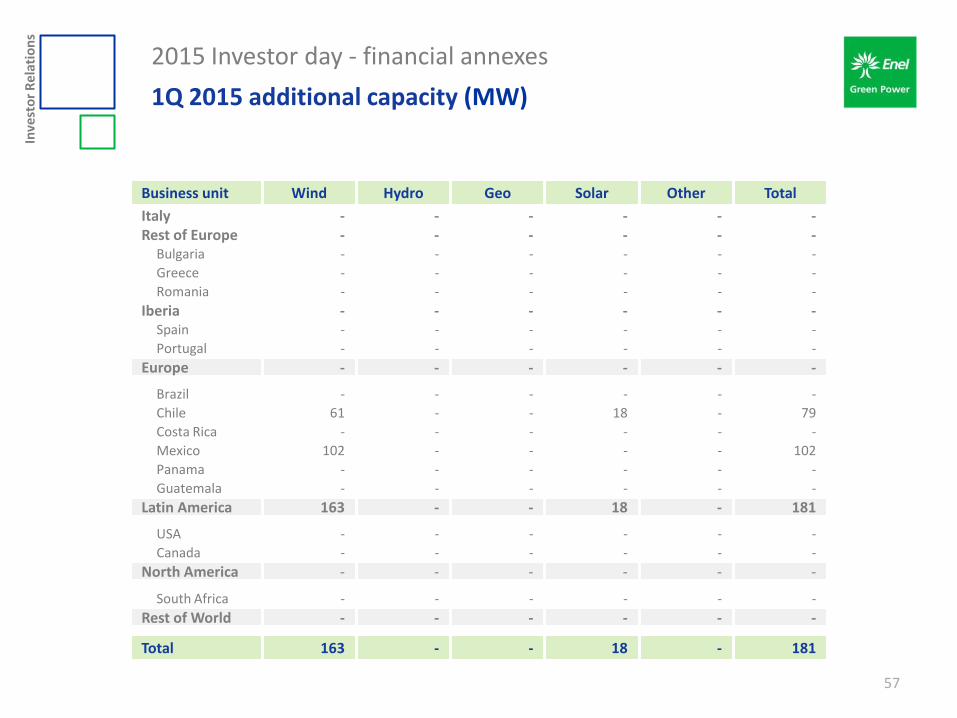

1Q 2015 additional capacity (MW)

57

Business unit Wind Hydro Geo Solar Other Total

Italy - - - - - - Rest of Europe - - - - - -

Bulgaria - - - - - -

Greece - - - - - -

Romania - - - - - -

Iberia - - - - - - Spain - - - - - -

Portugal - - - - - -

Europe - - - - - -

Brazil - - - - - -

Chile 61 - - 18 - 79

Costa Rica - - - - - -

Mexico 102 - - - - 102

Panama - - - - - -

Guatemala - - - - - -

Latin America 163 - - 18 - 181

USA - - - - - -

Canada - - - - - -

North America - - - - - -

South Africa - - - - - -

Rest of World - - - - - -

Total 163 - - 18 - 181

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

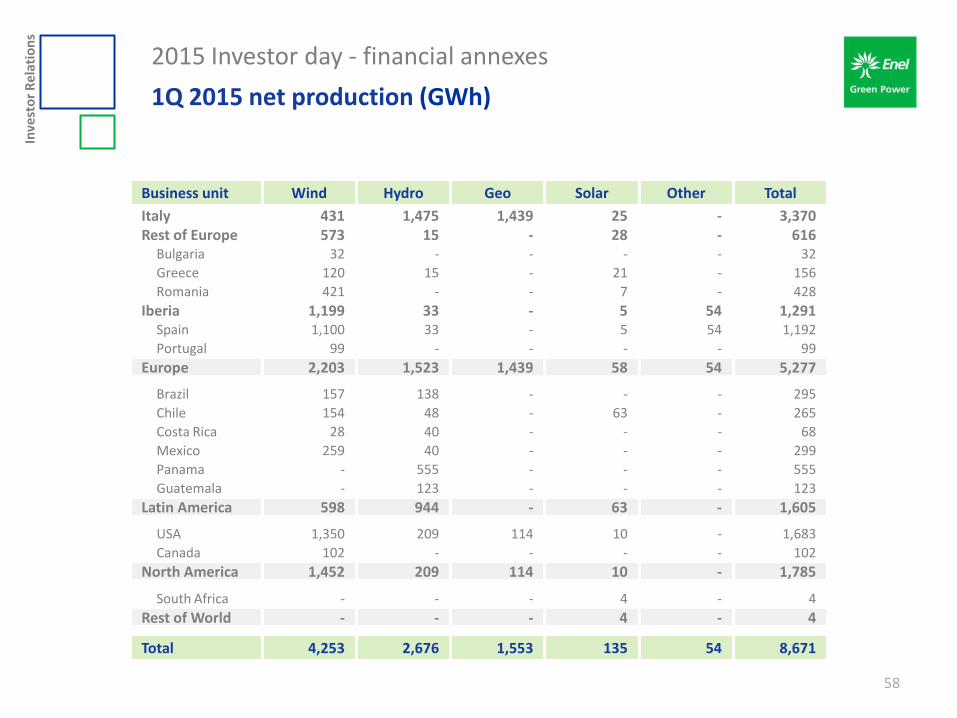

1Q 2015 net production (GWh)

58

Business unit Wind Hydro Geo Solar Other Total

Italy 431 1,475 1,439 25 - 3,370 Rest of Europe 573 15 - 28 - 616

Bulgaria 32 - - - - 32

Greece 120 15 - 21 - 156

Romania 421 - - 7 - 428

Iberia 1,199 33 - 5 54 1,291 Spain 1,100 33 - 5 54 1,192

Portugal 99 - - - - 99

Europe 2,203 1,523 1,439 58 54 5,277

Brazil 157 138 - - - 295

Chile 154 48 - 63 - 265

Costa Rica 28 40 - - - 68

Mexico 259 40 - - - 299

Panama - 555 - - - 555

Guatemala - 123 - - - 123

Latin America 598 944 - 63 - 1,605

USA 1,350 209 114 10 - 1,683

Canada 102 - - - - 102

North America 1,452 209 114 10 - 1,785

South Africa - - - 4 - 4

Rest of World - - - 4 - 4

Total 4,253 2,676 1,553 135 54 8,671

Inve

sto

r R

ela

tio

ns

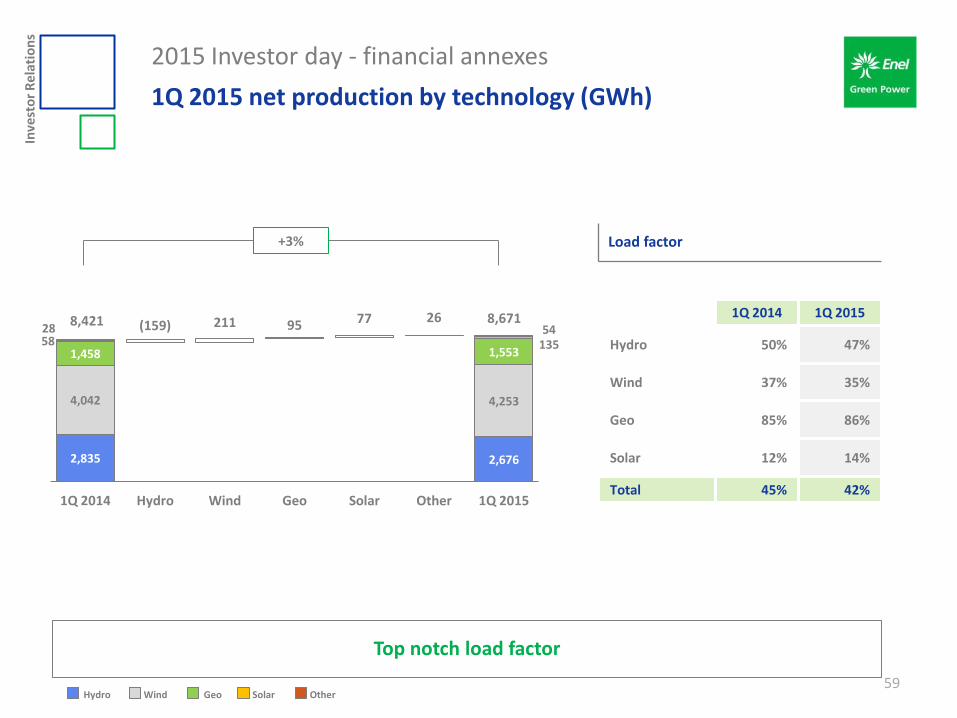

2,835 2,676

4,042

(159) 211 95 77 26

4,253

1,458 1,553 58 135 28 54

1Q 2014 Hydro Wind Geo Solar Other 1Q 2015

2015 Investor day - financial annexes

1Q 2015 net production by technology (GWh)

59

Load factor

Top notch load factor

Hydro Geo Wind Solar Other

1Q 2014 1Q 2015

Hydro 50% 47%

Wind 37% 35%

Geo 85% 86%

Solar 12% 14%

Total 45% 42%

8,421 8,671

+3%

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

1Q 2015 net production by geography (GWh)

60

+3% Load factor

5,728 5,281

1,009

(447) 596 101

1,605

1,684 1,785

1Q 2014 Europe Latin America

North America

1Q 2015

1Q 2014 1Q 2015

Europe 45% 42%

Latin America 43% 46%

North America 46% 40%

Total 45% 42%

8,421 8,671

1. Includes South Africa

1

Europe Latin America North America

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

1Q 2015 profit & loss (€m)

61

1Q 2015 1Q 2014

Energy revenues 503 456 47 +10%

Revenues from incenives 213 234 (21) -9%

Other revenues 95 30 65 n.m.

Total revenues 811 720 91 +13%

Direct costs 78 79 (1) -1% Energy & fuel puchases 52 60 (8) -13%

Transmission costs 14 11 3 +27%

Other 12 8 4 +50%

Personnel costs 57 50 7 +14% - 7 -

Operation & maintenance1 84 77 7 +9% - -

G&A and other1 56 32 24 +75% - -

Total costs 275 239 36 +15%

1Q 2015 1Q 2014

EBITDA 536 481 55 +11% 00 0

D&A (188) (160) (28) +18% 0

EBIT 348 321 27 +8% 0

Net financial expense (52) (64) 12 -19% 0

Income from equity investment 7 19 (12) -63% 0

EBT 303 276 27 +10% -

Income tax (95) (80) (15) +19% -

Net income 208 196 12 +6% -

Minorities 33 26 7 +27% 0

Group net income 175 170 5 +3%

1. 1Q 2014 includes a managerial reclassification of some G&A costs

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

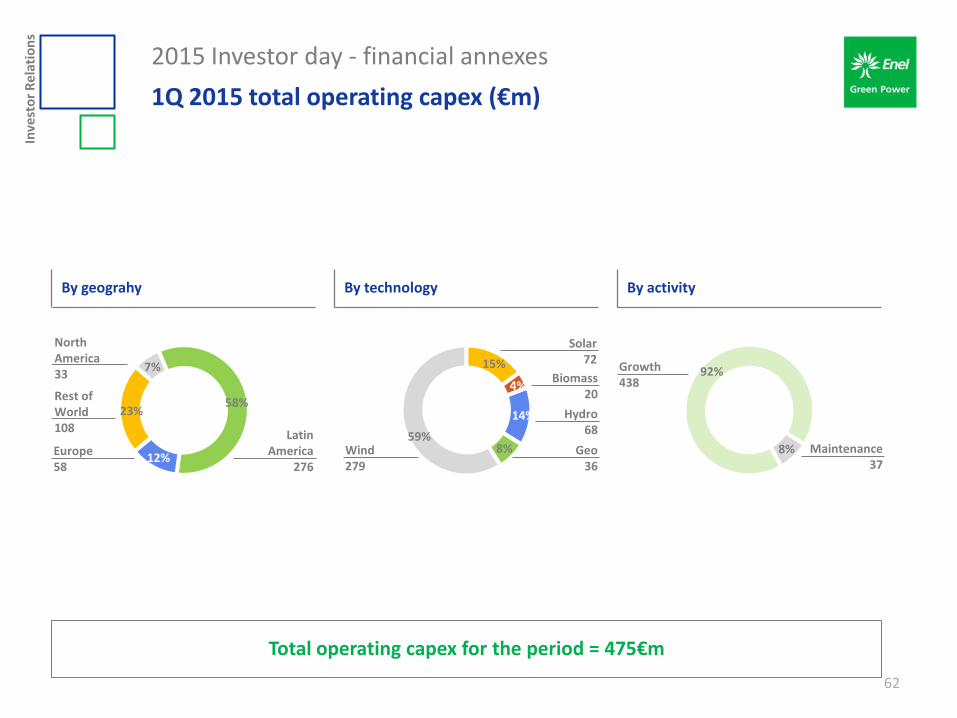

1Q 2015 total operating capex (€m)

62

Total operating capex for the period = 475€m

By geograhy By technology By activity

92%

8%

Growth 438

Maintenance 37

23%

7%

58%

12%

Rest of World 108

Europe 58

Latin America

276

North America 33

14%

8% 59%

15%

4%

Wind 279

Biomass 20

Solar 72

Hydro 68

Geo 36

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

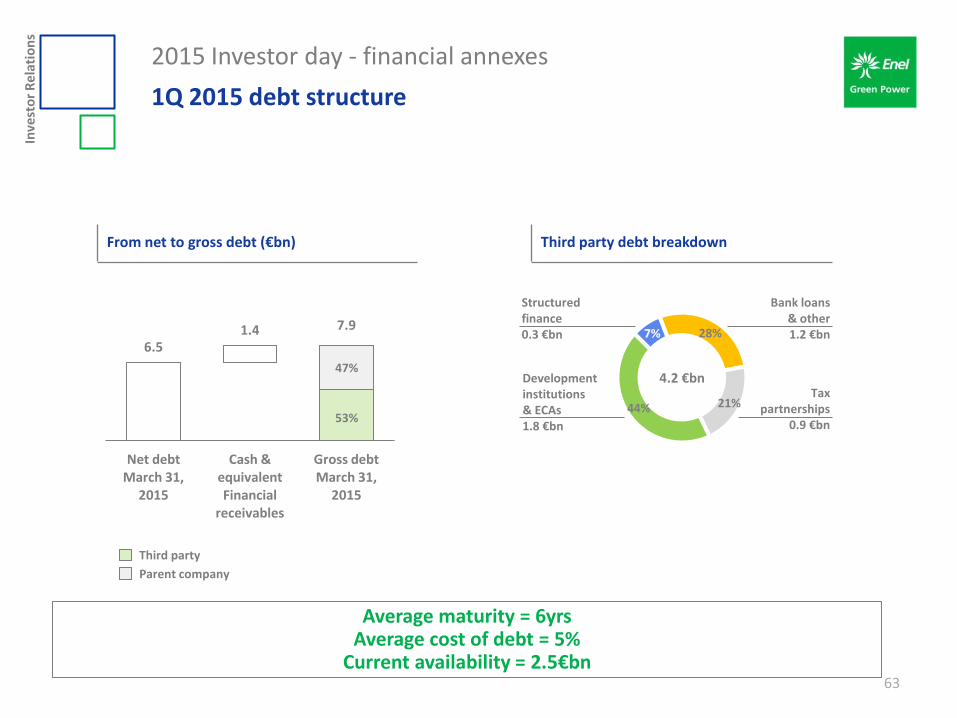

1Q 2015 debt structure

63

Average maturity = 6yrs Average cost of debt = 5%

Current availability = 2.5€bn

From net to gross debt (€bn) Third party debt breakdown

Parent company

Third party

6.5

7.9 1.4

Net debt March 31,

2015

Cash & equivalent Financial

receivables

Gross debt March 31,

2015

53%

47%

28%

21% 44%

7%

Development institutions & ECAs 1.8 €bn

Bank loans & other 1.2 €bn

Tax partnerships

0.9 €bn

Structured finance 0.3 €bn

4.2 €bn

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

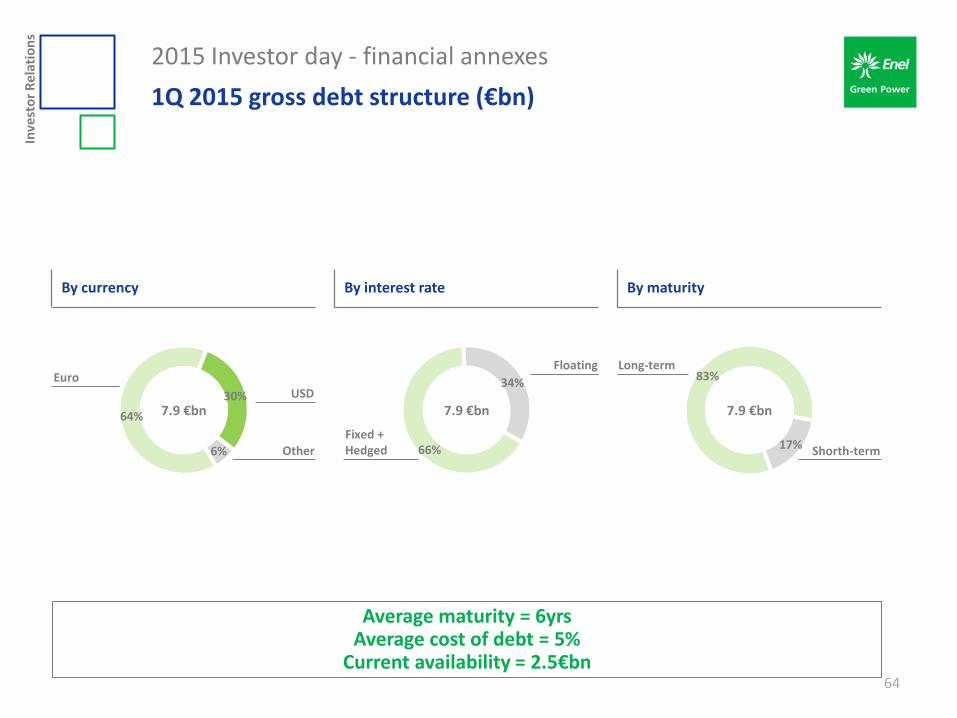

1Q 2015 gross debt structure (€bn)

64

By currency By interest rate By maturity

66%

34%

Fixed + Hedged

Floating 83%

17%

Long-term

Shorth-term

64%

30%

6%

Euro

Other

USD

7.9 €bn 7.9 €bn 7.9 €bn

Average maturity = 6yrs Average cost of debt = 5%

Current availability = 2.5€bn

Inve

sto

r R

ela

tio

ns

2015 Investor day - financial annexes

1Q 2015 long-term debt maturity (€m)

65

2015 2016 2017 2018 2019 >2019 Total

Third party 278 329 317 801 382 2,019 4,126

Parent company - - - - - 2,455 2,455

Total 278 329 317 801 382 4,474 6,581

Inve

sto

r R

ela

tio

ns

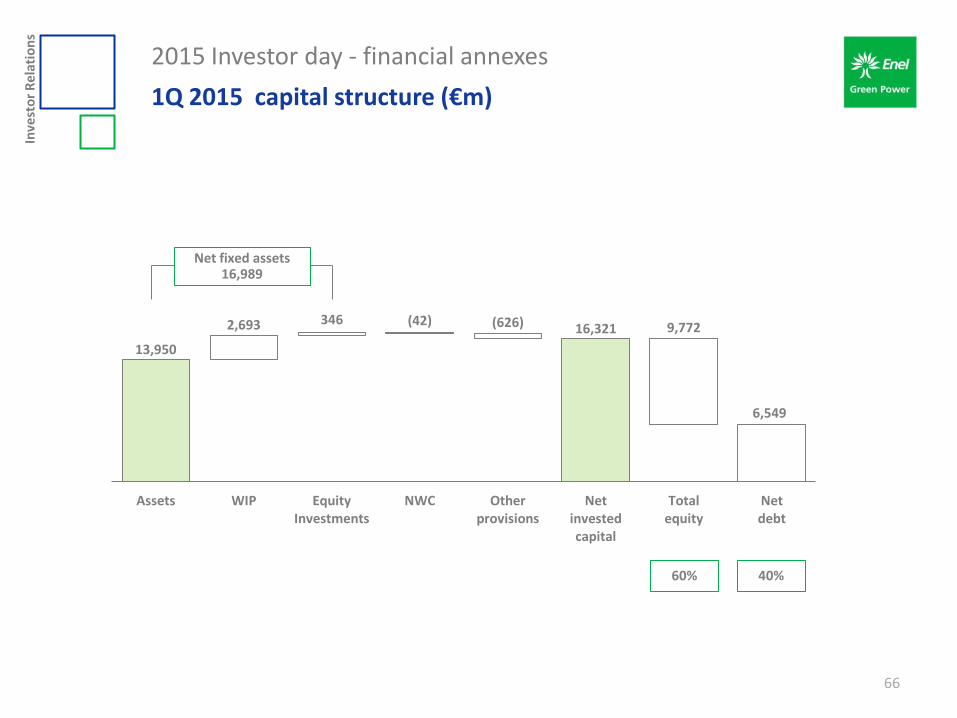

13,950

16,321 2,693 346 (42) (626) 9,772

6,549

Assets WIP Equity Investments

NWC Other provisions

Net invested capital

Total equity

Net debt

2015 Investor day - financial annexes

1Q 2015 capital structure (€m)

66

60% 40%

Net fixed assets 16,989

Inve

sto

r R

ela

tio

ns

2015 Investor day

Disclaimer

67

This presentation contains certain forward-looking statements that reflect the Company’s management’s current views with respect to future events and financial and operational performance of the Company and its subsidiaries. These forward looking statements are based on Enel Green Power S.p.A.’s current expectations and projections about future events. Because these forward-looking statements are subject to risks and uncertainties, actual future results or performance may differ materially from those expressed in or implied by these statements due to any number of different factors, many of which are beyond the ability of Enel Green Power S.p.A. to control or estimate precisely, including changes in the regulatory environment, future market developments, fluctuations in the price and other risks. You are cautioned not to place undue reliance on the forward-looking statements contained herein, which are made only as of the date of this presentation. Enel Green Power S.p.A. does not undertake any obligation to publicly release any updates or revisions to any forward-looking statements to reflect events or circumstances after the date of this presentation. This presentation does not constitute a recommendation regarding the securities of the Company.

Pursuant to article 154-bis, par 2, of the Consolidated Financial Act of February 24, 1998, the executive in charge of preparing the corporate accounting documents at Enel Green Power S.p.A., Giulio Antonio Carone, declares that the accounting information contained herein correspond to document results, books and accounting records.

Inve

sto

r R

ela

tio

ns

2015 Investor day

Contact us

68

Donatella Izzo, IR manager Elena Accorinti Federico Caggia Alessandro Marchi Etienne Martoïa

T: +39 06 8305 9104 F: +39 06 6444 2758

E-mail: [email protected] Web site: www.enelgreenpower.com