Embed Size (px)

Citation preview

EGM

1 June 2012

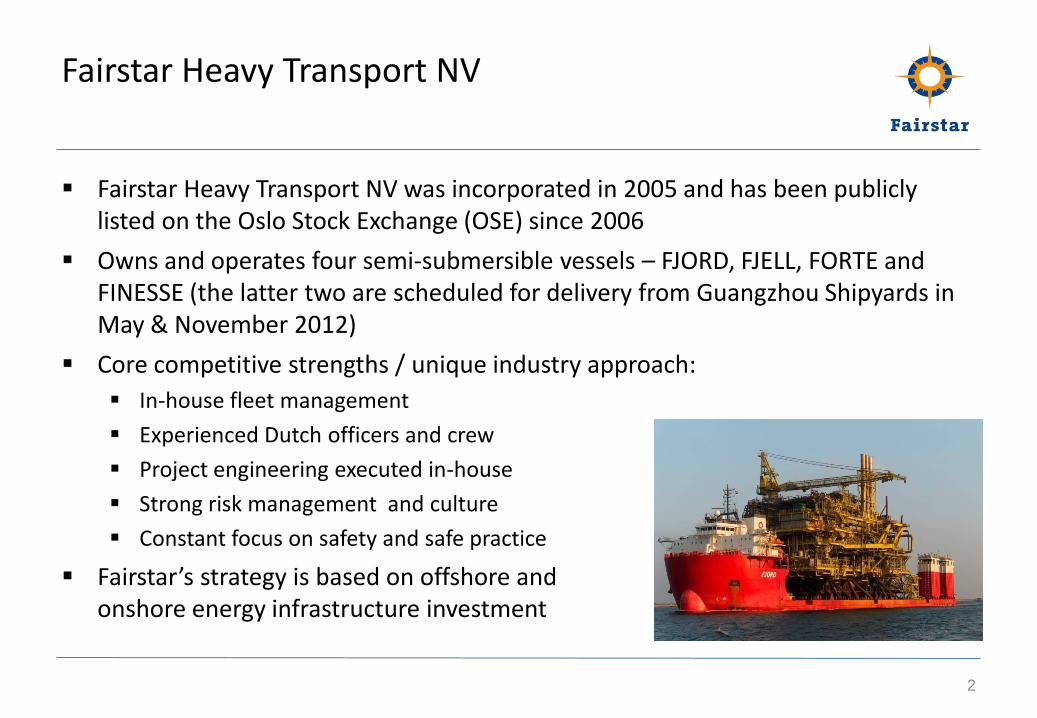

Fairstar Heavy Transport NV

Fairstar Heavy Transport NV was incorporated in 2005 and has been publicly listed on the Oslo Stock Exchange (OSE) since 2006

Owns and operates four semi-submersible vessels – FJORD, FJELL, FORTE and FINESSE (the latter two are scheduled for delivery from Guangzhou Shipyards in May & November 2012)

Core competitive strengths / unique industry approach:

In-house fleet management

Experienced Dutch officers and crew

Project engineering executed in-house

Strong risk management and culture

Constant focus on safety and safe practice

Fairstar’s strategy is based on offshore and onshore energy infrastructure investment

2

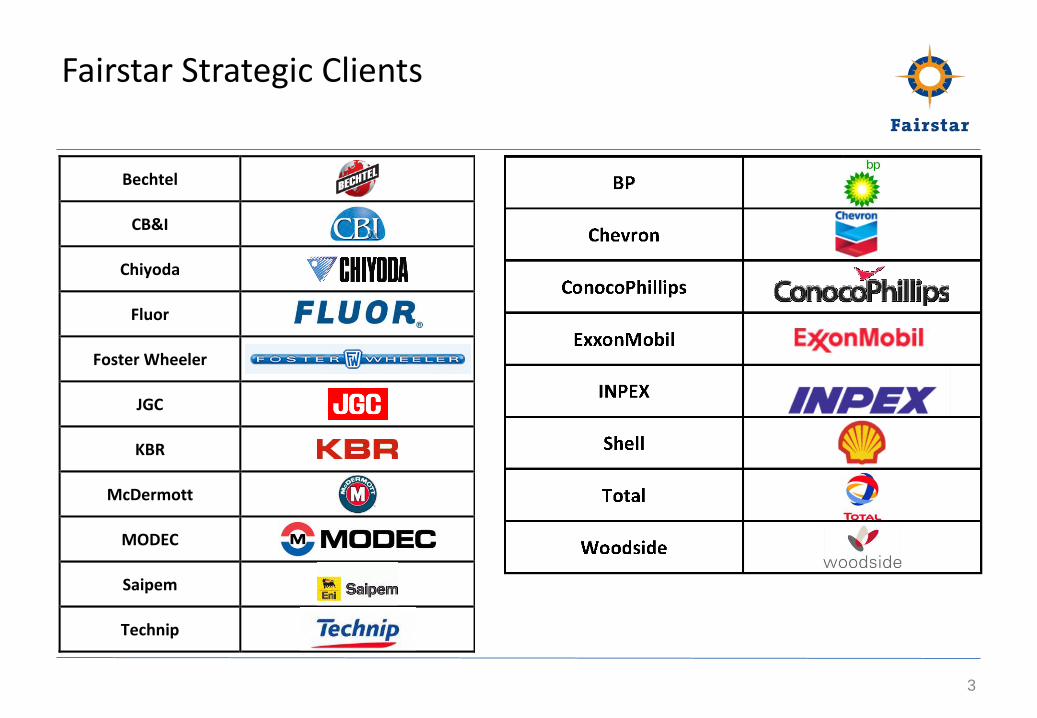

Fairstar Strategic Clients

3

Bechtel

CB&I

Chiyoda

Fluor

Foster Wheeler

JGC

KBR

McDermott

MODEC

Saipem

Technip

LNG4

MODULARIZATION

5

High value

Multiple voyage

Long term

CONTRACTSGorgon Golden Eagle Ichthys

6

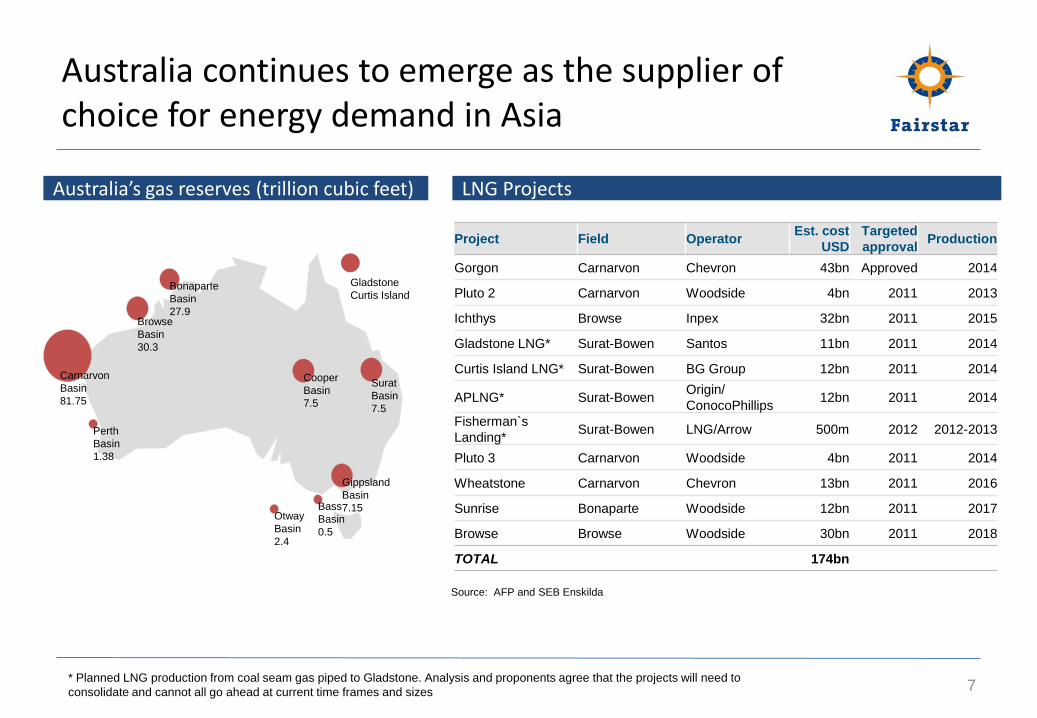

Australia’s gas reserves (trillion cubic feet) LNG Projects

Australia continues to emerge as the supplier of choice for energy demand in Asia

7

Project Field OperatorEst. cost

USD

Targeted

approvalProduction

Gorgon Carnarvon Chevron 43bn Approved 2014

Pluto 2 Carnarvon Woodside 4bn 2011 2013

Ichthys Browse Inpex 32bn 2011 2015

Gladstone LNG* Surat-Bowen Santos 11bn 2011 2014

Curtis Island LNG* Surat-Bowen BG Group 12bn 2011 2014

APLNG* Surat-BowenOrigin/

ConocoPhillips12bn 2011 2014

Fisherman`s

Landing*Surat-Bowen LNG/Arrow 500m 2012 2012-2013

Pluto 3 Carnarvon Woodside 4bn 2011 2014

Wheatstone Carnarvon Chevron 13bn 2011 2016

Sunrise Bonaparte Woodside 12bn 2011 2017

Browse Browse Woodside 30bn 2011 2018

TOTAL 174bn

* Planned LNG production from coal seam gas piped to Gladstone. Analysis and proponents agree that the projects will need to

consolidate and cannot all go ahead at current time frames and sizes

Carnarvon

Basin

81.75

Browse

Basin

30.3

Bonaparte

Basin

27.9

Perth

Basin

1.38

Cooper

Basin

7.5

Surat

Basin

7.5

Gippsland

Basin

7.15Bass

Basin

0.5

Otway

Basin

2.4

Gladstone

Curtis Island

Source: AFP and SEB Enskilda

Market trends and energy investment patterns are becoming increasingly clear

Asian demand is driving long term infrastructure investment

LNG is emerging as the preferred energy option

New discoveries of oil and gas are being found in more and more remote locations

The energy infrastructure assets required to package oil and gas into transportable bundles cannot be supplied by local industry

Modularization is the most cost efficient method of construction

Modules are becoming larger and more complex

8

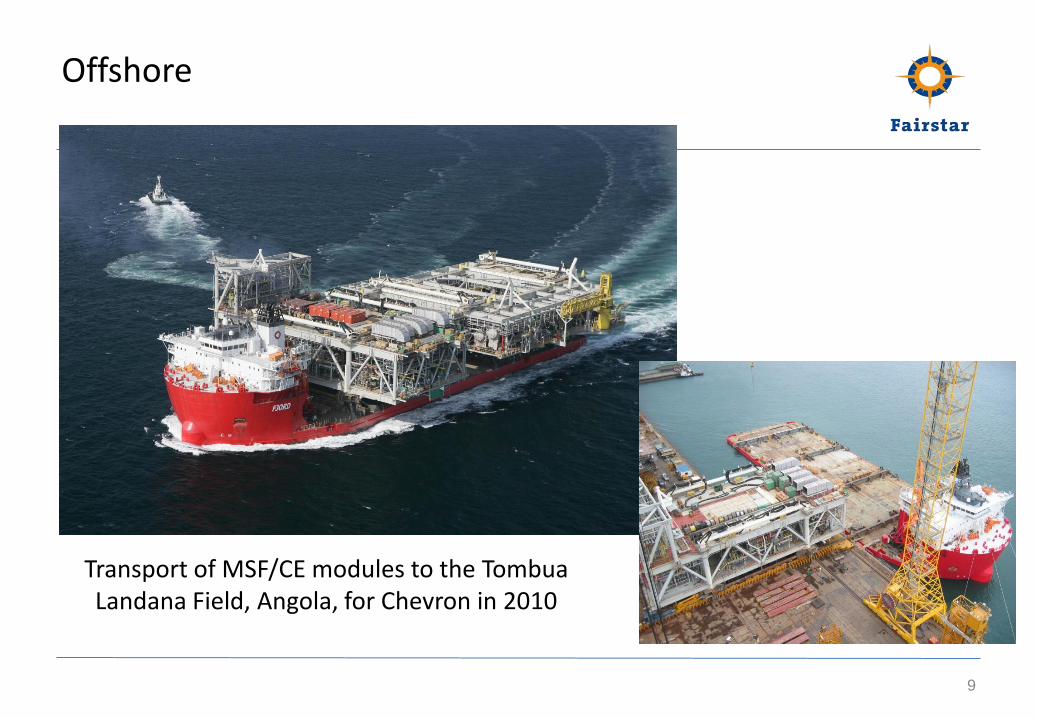

Offshore

9

Transport of MSF/CE modules to the TombuaLandana Field, Angola, for Chevron in 2010

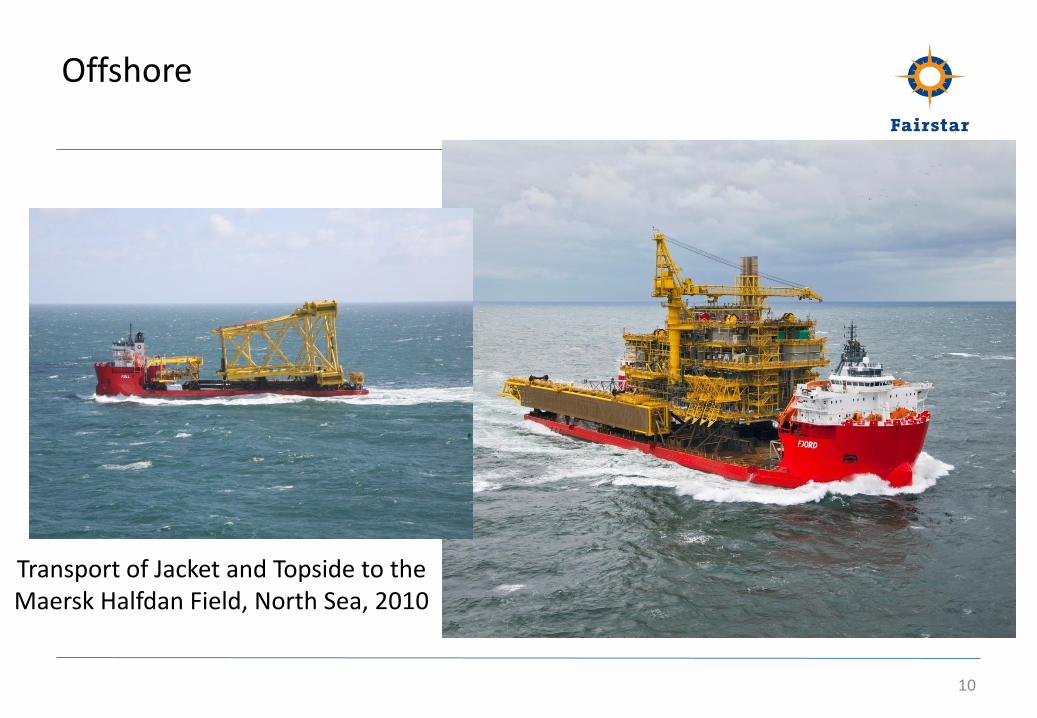

Offshore

10

Transport of Jacket and Topside to the Maersk Halfdan Field, North Sea, 2010

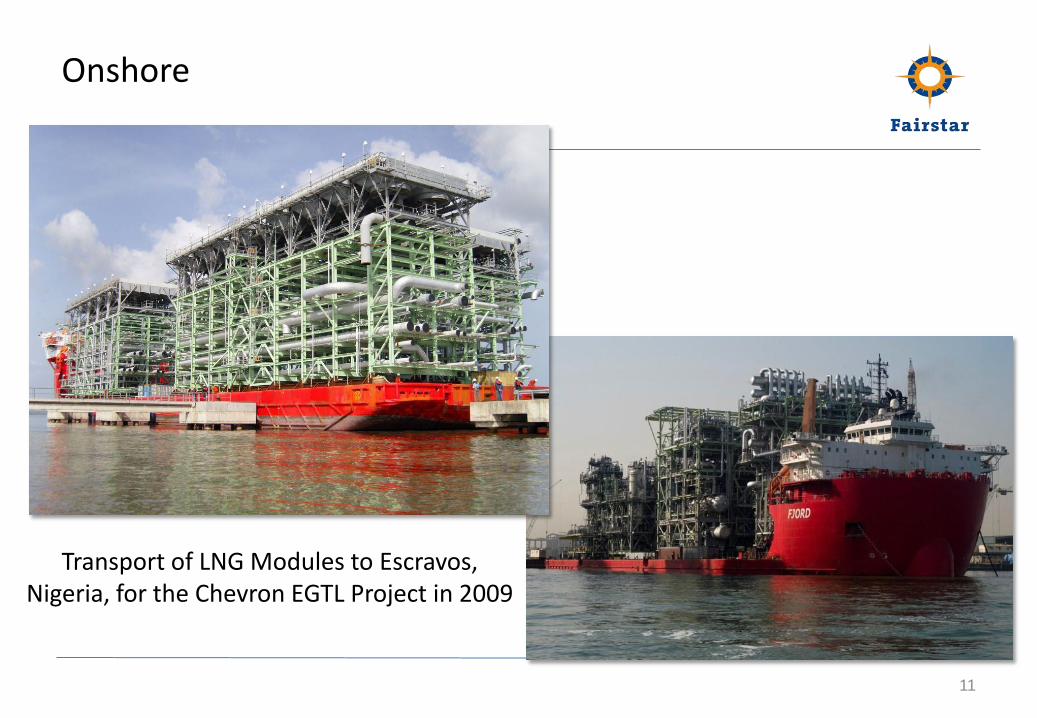

Onshore

11

Transport of LNG Modules to Escravos, Nigeria, for the Chevron EGTL Project in 2009

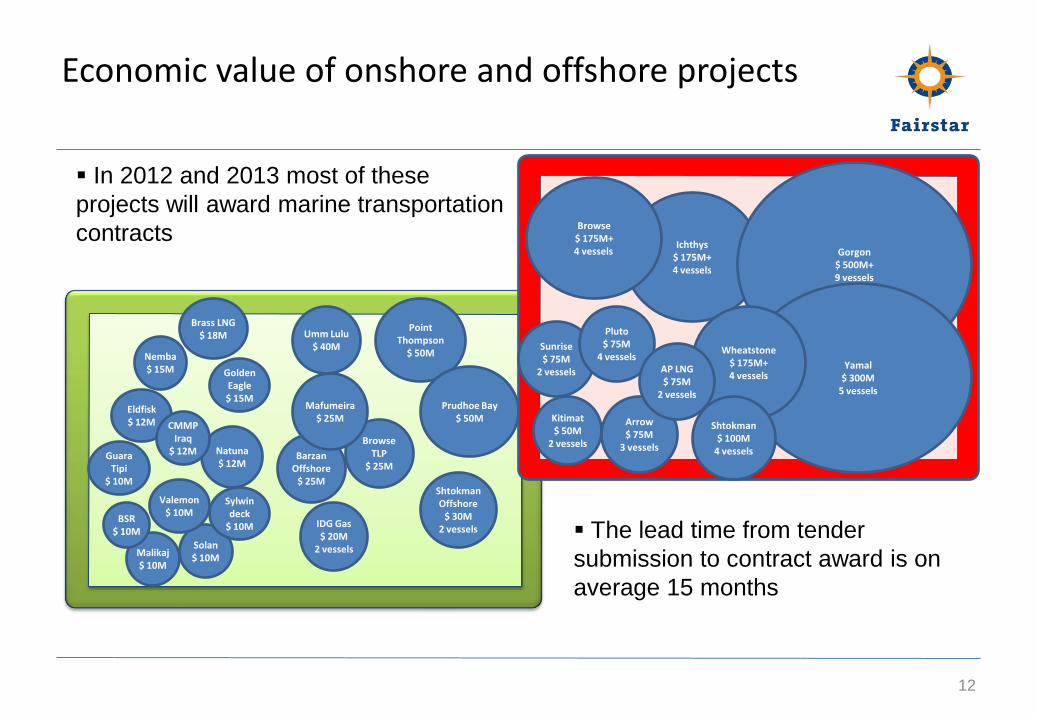

Economic value of onshore and offshore projects

12

Natuna$ 12M

Sunrise$ 75M

2 vessels

Ichthys$ 175M+4 vessels

Kitimat$ 50M

2 vessels

Browse$ 175M+4 vessels

Eldfisk$ 12M

Solan$ 10MMalikaj

$ 10M

Sylwin deck

$ 10M

Guara Tipi

$ 10M

Pluto$ 75M

4 vessels

IDG Gas$ 20M

2 vessels

CMMP Iraq

$ 12M

Golden Eagle$ 15M

Nemba$ 15M

Barzan Offshore

$ 25MShtokman Offshore

$ 30M2 vessels

Browse TLP

$ 25M

Valemon$ 10M

Mafumeira$ 25M

Brass LNG$ 18M

BSR $ 10M

Umm Lulu$ 40M

Point Thompson

$ 50M

Prudhoe Bay$ 50M Arrow

$ 75M3 vessels

Gorgon$ 500M+9 vessels

Yamal$ 300M

5 vessels

Wheatstone$ 175M+4 vessels

AP LNG$ 75M

2 vessels

Shtokman$ 100M

4 vessels

In 2012 and 2013 most of these

projects will award marine transportation

contracts

The lead time from tender

submission to contract award is on

average 15 months

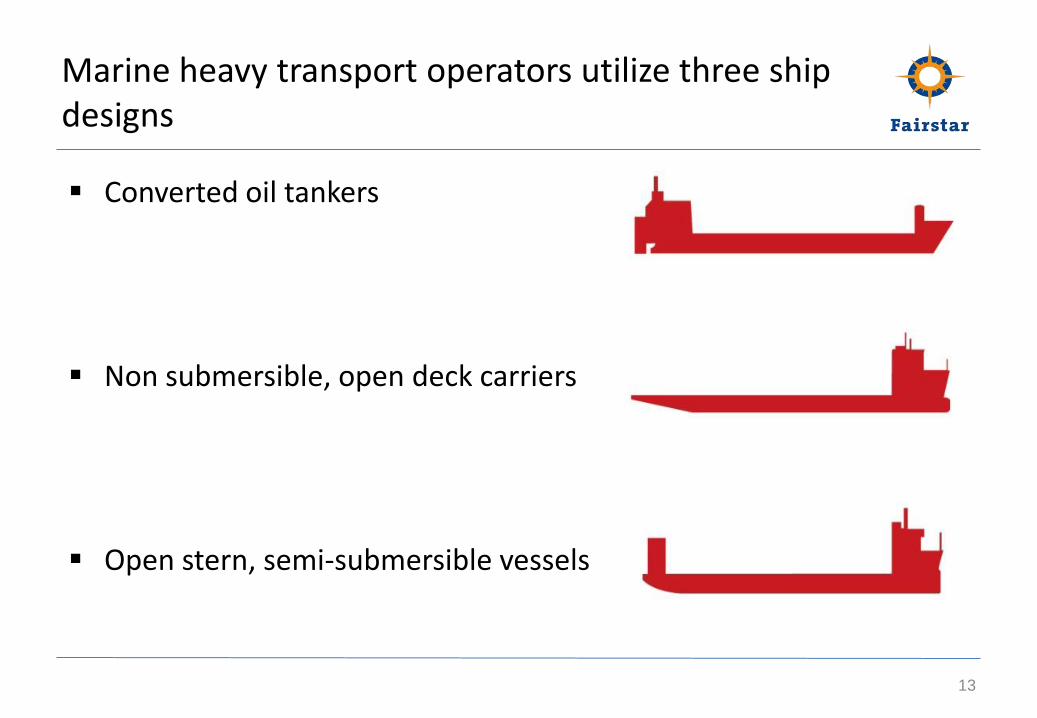

Marine heavy transport operators utilize three ship designs

13

Converted oil tankers

Non submersible, open deck carriers

Open stern, semi-submersible vessels

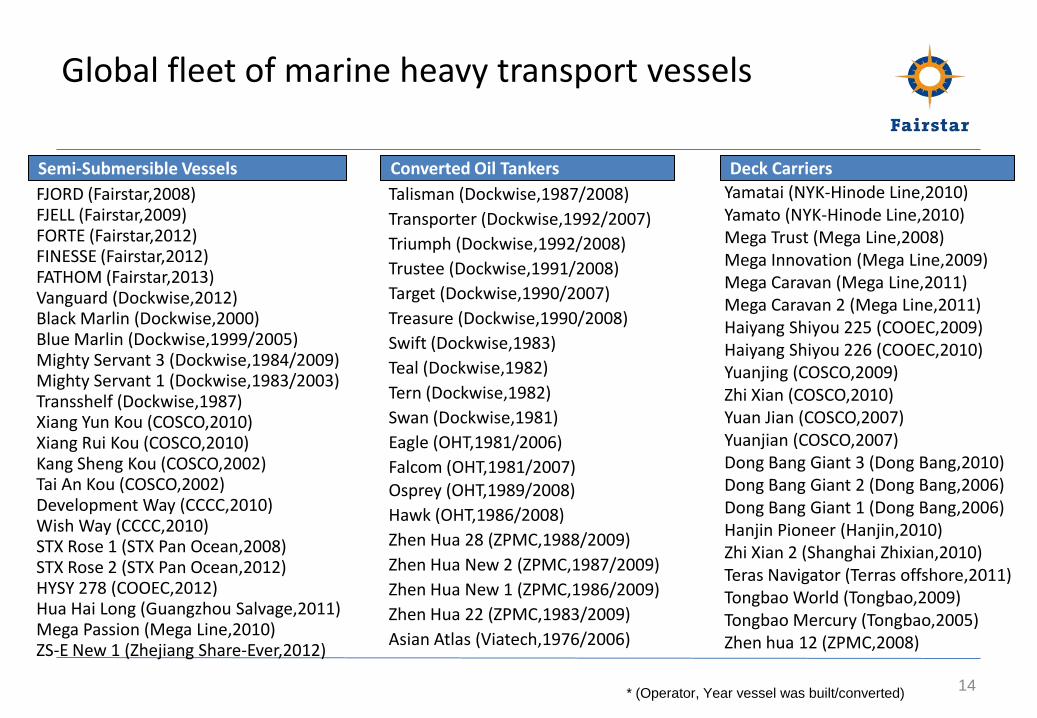

Global fleet of marine heavy transport vessels

14

Semi-Submersible Vessels Converted Oil Tankers Deck Carriers

FJORD (Fairstar,2008)FJELL (Fairstar,2009)FORTE (Fairstar,2012)FINESSE (Fairstar,2012)FATHOM (Fairstar,2013)Vanguard (Dockwise,2012)

Mighty Servant 3 (Dockwise,1984/2009)Mighty Servant 1 (Dockwise,1983/2003)

Xiang Yun Kou (COSCO,2010)Xiang Rui Kou (COSCO,2010)Kang Sheng Kou (COSCO,2002)Tai An Kou (COSCO,2002)

HYSY 278 (COOEC,2012)Hua Hai Long (Guangzhou Salvage,2011)Mega Passion (Mega Line,2010)ZS-E New 1 (Zhejiang Share-Ever,2012)

Talisman (Dockwise,1987/2008)

Transporter (Dockwise,1992/2007)

Triumph (Dockwise,1992/2008)

Trustee (Dockwise,1991/2008)

Target (Dockwise,1990/2007)

Treasure (Dockwise,1990/2008)

Swift (Dockwise,1983)

Teal (Dockwise,1982)

Tern (Dockwise,1982)

Swan (Dockwise,1981)

Eagle (OHT,1981/2006)

Falcom (OHT,1981/2007)Osprey (OHT,1989/2008)

Hawk (OHT,1986/2008)

Zhen Hua 28 (ZPMC,1988/2009)

Zhen Hua New 2 (ZPMC,1987/2009)

Zhen Hua New 1 (ZPMC,1986/2009)

Zhen Hua 22 (ZPMC,1983/2009)

Asian Atlas (Viatech,1976/2006)

Yamatai (NYK-Hinode Line,2010)Yamato (NYK-Hinode Line,2010)Mega Trust (Mega Line,2008)Mega Innovation (Mega Line,2009)Mega Caravan (Mega Line,2011)Mega Caravan 2 (Mega Line,2011)Haiyang Shiyou 225 (COOEC,2009)Haiyang Shiyou 226 (COOEC,2010)Yuanjing (COSCO,2009)Zhi Xian (COSCO,2010)Yuan Jian (COSCO,2007)Yuanjian (COSCO,2007)Dong Bang Giant 3 (Dong Bang,2010)Dong Bang Giant 2 (Dong Bang,2006)Dong Bang Giant 1 (Dong Bang,2006)Hanjin Pioneer (Hanjin,2010)Zhi Xian 2 (Shanghai Zhixian,2010)Teras Navigator (Terras offshore,2011)Tongbao World (Tongbao,2009)Tongbao Mercury (Tongbao,2005)Zhen hua 12 (ZPMC,2008)

Development Way (CCCC,2010)Wish Way (CCCC,2010)

Black Marlin (Dockwise,2000)Blue Marlin (Dockwise,1999/2005)

Transshelf (Dockwise,1987)

STX Rose 1 (STX Pan Ocean,2008)STX Rose 2 (STX Pan Ocean,2012)

* (Operator, Year vessel was built/converted)

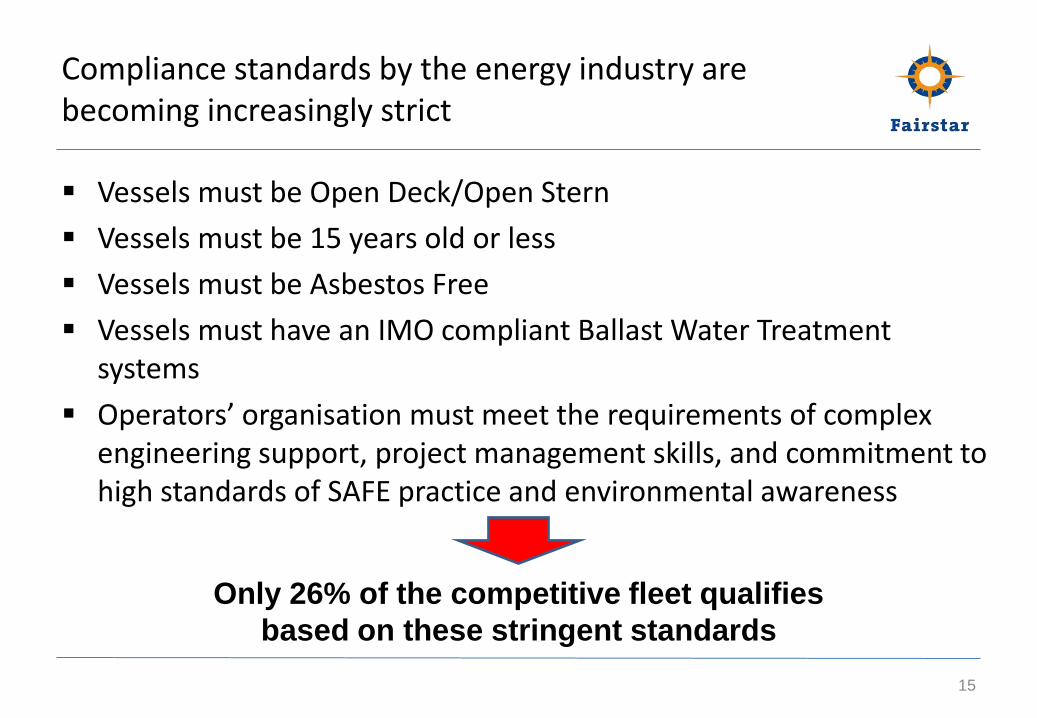

Compliance standards by the energy industry are becoming increasingly strict

Vessels must be Open Deck/Open Stern

Vessels must be 15 years old or less

Vessels must be Asbestos Free

Vessels must have an IMO compliant Ballast Water Treatment systems

Operators’ organisation must meet the requirements of complex engineering support, project management skills, and commitment to high standards of SAFE practice and environmental awareness

15

Only 26% of the competitive fleet qualifies

based on these stringent standards

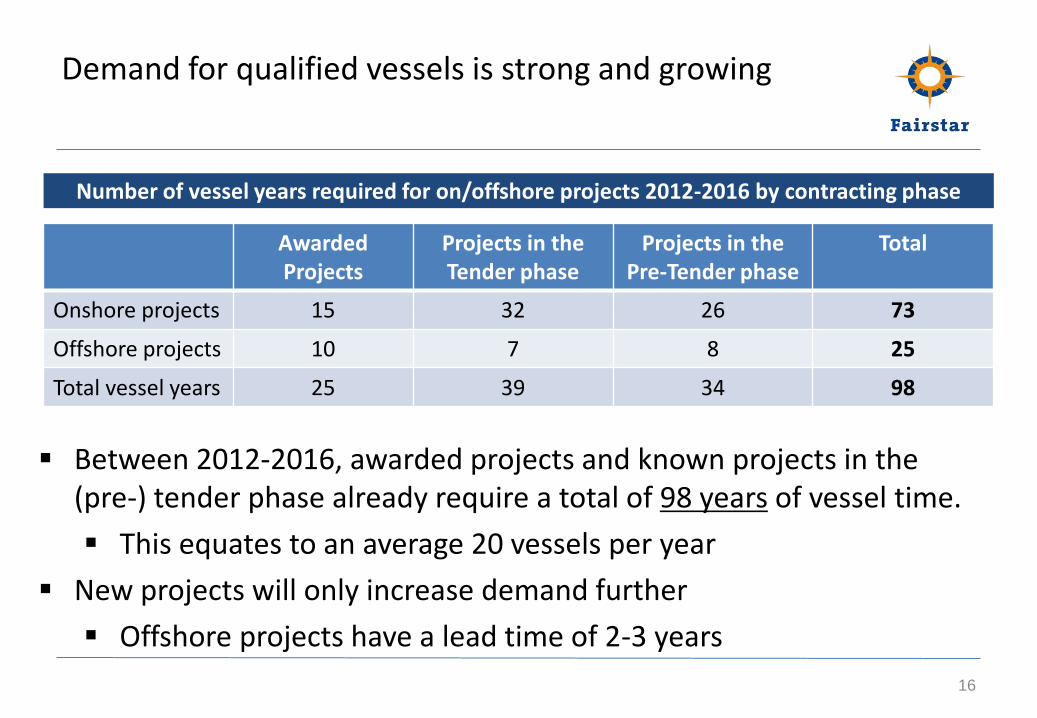

Demand for qualified vessels is strong and growing

AwardedProjects

Projects in the Tender phase

Projects in the Pre-Tender phase

Total

Onshore projects 15 32 26 73

Offshore projects 10 7 8 25

Total vessel years 25 39 34 98

16

Between 2012-2016, awarded projects and known projects in the (pre-) tender phase already require a total of 98 years of vessel time.

This equates to an average 20 vessels per year

New projects will only increase demand further

Offshore projects have a lead time of 2-3 years

Number of vessel years required for on/offshore projects 2012-2016 by contracting phase

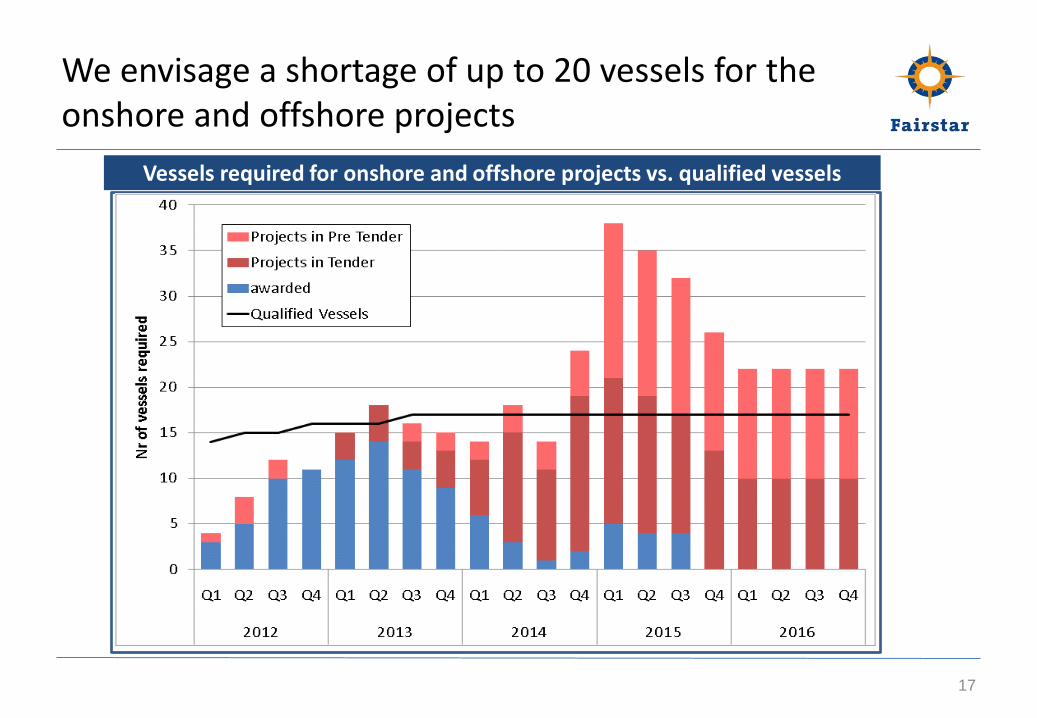

We envisage a shortage of up to 20 vessels for the onshore and offshore projects

17

Vessels required for onshore and offshore projects vs. qualified vessels

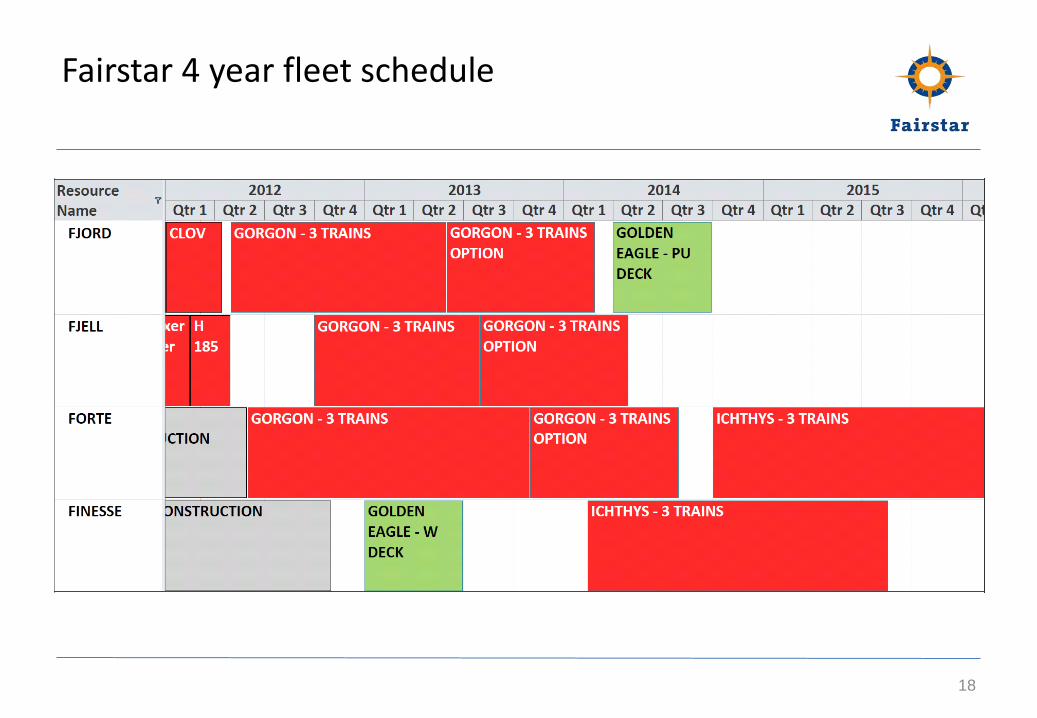

Fairstar 4 year fleet schedule

18

Contact details - Fairstar Heavy Transport NV

19

Postal address Visiting addressP.O. Box 2225 Weena 316-318, Tower A3000 CE Rotterdam 3012 NJ RotterdamThe Netherlands The Netherlands

Philip Adkins (CEO)M +44 (0)7796 681 414E [email protected]

This material has been prepared by Fairstar Heavy Transport NV (“FHT").

This material is for distribution only under such circumstances as may be permitted by applicable law. It has no regardto the specific investment objectives, financial situation or particular needs of any recipient. It is published solely forinformational purposes. No representation or warranty, either express or implied, is provided in relation to theaccuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statementor summary of the securities, markets or developments referred to in the materials. It should not be regarded byrecipients as a substitute for the exercise of their own judgement. Any opinions expressed in this material are subject tochange without notice and may differ or be contrary to opinions expressed by other business areas or groups of FHT asa result of using different assumptions and criteria. FHT is under no obligation to update or keep current theinformation contained herein. Neither FHT nor any of its affiliates, nor any of FHT’s or any of its affiliates, directors,employees or agents accepts any liability for any loss or damage arising out of the use of all or any part of this material.

© 2011 Fairstar Heavy Transport NV. All rights reserved. Fairstar Heavy Transport NV specifically prohibits theredistribution of this material and accepts no liability whatsoever for the actions of third parties in this respect.

ContactT +31 (0)10-403 5333F +31 (0)10-403 5344I www.fairstar.comE [email protected]