Embed Size (px)

Citation preview

EFSE ANNUAL MEETING 2011Tirana, 6 to 8 June

Panel IIThe New Opportunity: Energy Efficiency and

Renewable Energy Lending

Panel II:The New Opportunity: Energy Efficiency and Renewable Energy Lending

Lloyd StevensDirector

Finance in Motion

Aleksandar MijailovicČačanska Banka

Yücel InanIK Banka

Olaf ZymelkaHead of Division,

Energy SEE & TurkeyKfW

Wolfgang KröpflENSO

Terry McCallionEBRD

Matthias HitzelMACS

Yücel InanGeneral Manager, IK Banka

Entering the Field of EE LendingChallenges & Opportunities

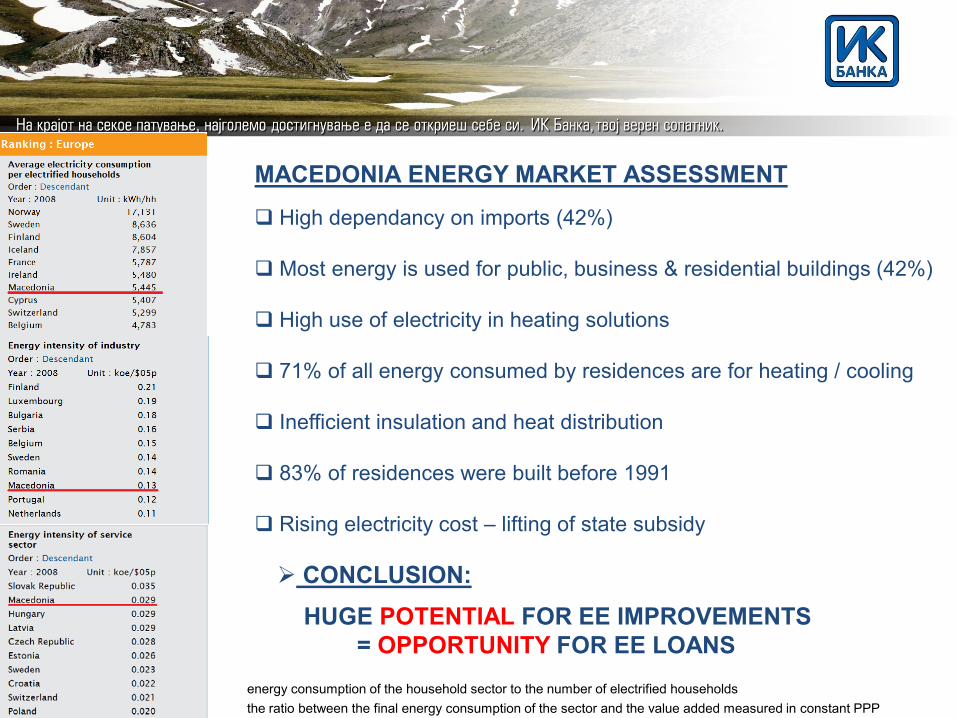

High dependancy on imports (42%)

Most energy is used for public, business & residential buildings (42%)

High use of electricity in heating solutions

71% of all energy consumed by residences are for heating / cooling

Inefficient insulation and heat distribution

83% of residences were built before 1991

Rising electricity cost – lifting of state subsidy

MACEDONIA ENERGY MARKET ASSESSMENT

energy consumption of the household sector to the number of electrified householdsthe ratio between the final energy consumption of the sector and the value added measured in constant PPP

CONCLUSION:HUGE POTENTIAL FOR EE IMPROVEMENTS

= OPPORTUNITY FOR EE LOANS

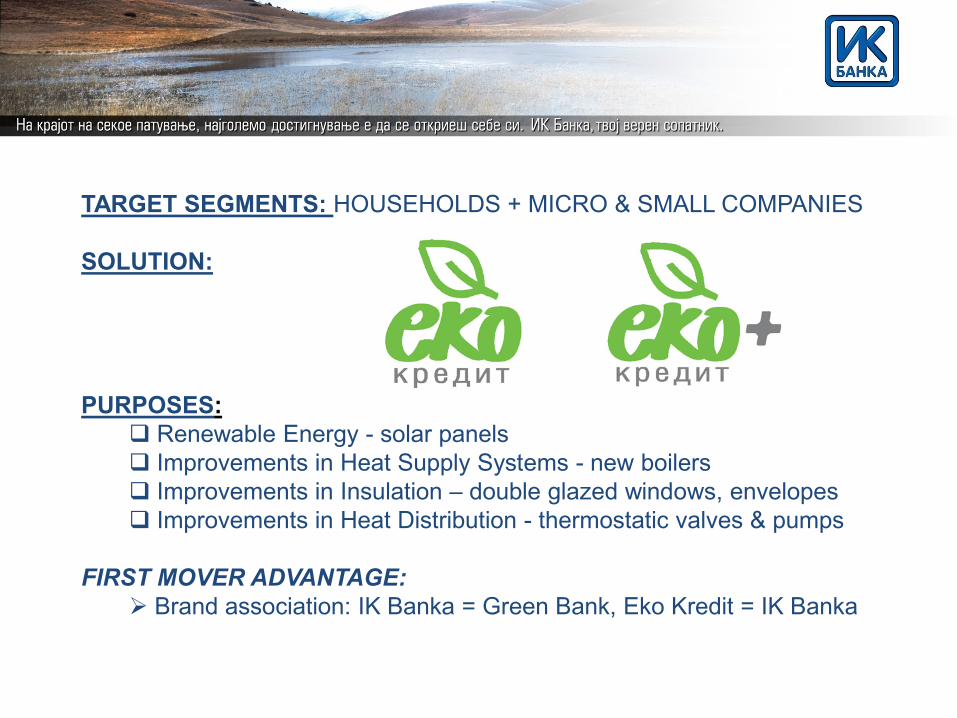

TARGET SEGMENTS: HOUSEHOLDS + MICRO & SMALL COMPANIES

SOLUTION:

PURPOSES: Renewable Energy - solar panels Improvements in Heat Supply Systems - new boilers Improvements in Insulation – double glazed windows, envelopes Improvements in Heat Distribution - thermostatic valves & pumps

FIRST MOVER ADVANTAGE: Brand association: IK Banka = Green Bank, Eko Kredit = IK Banka

CAMPAIGN

INTERNAL: STAFF UNDERSTANDING IS CRUCIALTRAINING (TECHNICAL ASSISTANCE)

What our staff learned: How to use the e-Save Tool & Calculation of the savings Increased awareness for energy savingsSales channels: direct or through sellers to individuals or companies

EXTERNAL: RAISE AWARENESSSTRATEGY:

INFORM - Multi Channel Campaign + Merchant VisitsEDUCATE - Simplify potential loan purposes through examples

RESULTS: EASIER TRANSACTIONS WITH HOUSELHOLDSMOST POPULAR EE INVESTMENTS:

RETAIL: Double glazed windows & doors, building envelopes for better isolation, solar panels for hot waterCORPORATE: Solar panels for hotels and enveloping of the business premises and roof

CHALLENGES:

Easy to “sell” to management and staff..To clients – more difficult !

FIRST MOVER DISADVANTAGE ! LOW AWARENESS - We have the job of being the first bank to increase public awareness & interest and convince that savings will pay back the EE investments

GRAY ECONOMY UNDOCUMENTED PURCHASES: Difficulties for documenting the purchases (in practice clients swap goods and services or purchase in cash without invoice avoiding taxation). Sometimes clients may prefer classical consumer loan with higher interest rate to avoid providing documentation for invoice payments.

ENERGY POLICY & LEGISLATION Still relatively low (subsidized) electricity prices.“Green Passport” not yet introduced, EU requirements not in place.

Low incentive for investment

Aleksandar MijailovicHead of SME LendingČačanska Banka

Čačanska banka a.d. Čačak

EFSE ANNUAL MEETING 2011

Energy Efficiency and Renewable Energy Lending

7 June 2011

Strategy

Enter the field of EE lending

1st Loan Agreement,

KfW, EUR 5 million

Advisor of the clients

Čačanska banka = EE/RE lending

EFSE ANNUAL MEETING 2011 – Energy Efficiency and Renewable Energy Lending – 07 June 2011

Support of EE/RE concept

KfW

Hit Energy

= EE/RE Lending

Čačanska banka a.d. Čačak

Retail segment – standardized product – 79 projectsMicro, SME, Corporate – individual approach – standard, non-standard projects

– 80 projects – EUR 4,8 million

Čačanska banka a.d. Čačak

EE Loan Poduct

Energy savings Instalment Interest

HIT ENERGY LOAN

EFSE ANNUAL MEETING 2011 – Energy Efficiency and Renewable Energy Lending – 07 June 2011

EFSE ANNUAL MEETING 2011 – Energy Efficiency and Renewable Energy Lending – 07 June 2011

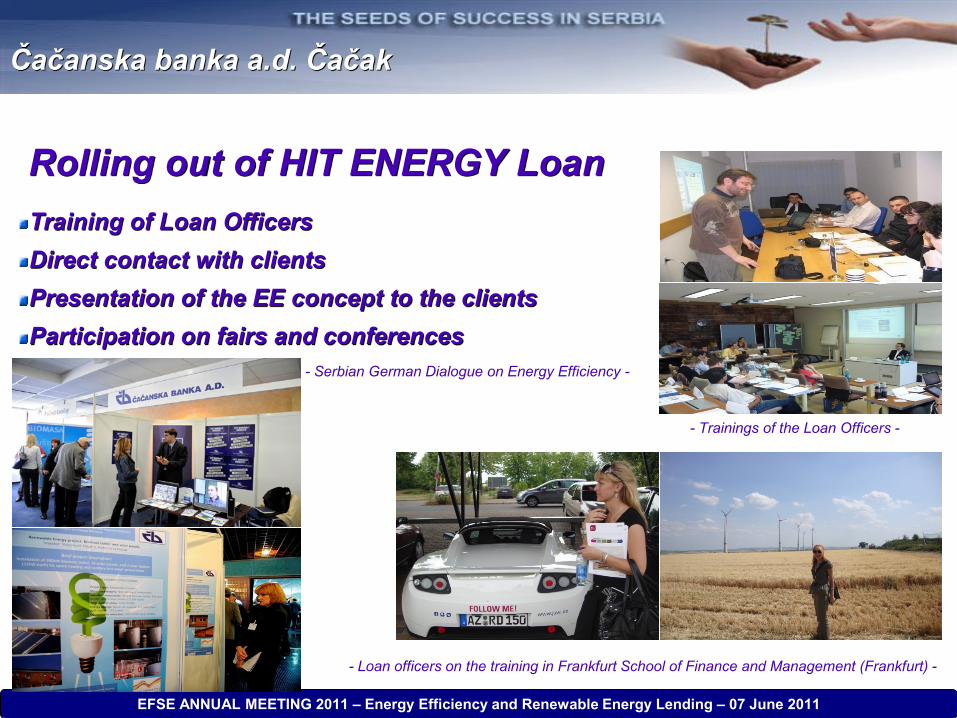

Rolling out of HIT ENERGY LoanTraining of Loan OfficersDirect contact with clientsPresentation of the EE concept to the clientsParticipation on fairs and conferences

- Trainings of the Loan Officers -

- Serbian German Dialogue on Energy Efficiency -

- Loan officers on the training in Frankfurt School of Finance and Management (Frankfurt) -

Čačanska banka a.d. Čačak

EFSE ANNUAL MEETING 2011 – Energy Efficiency and Renewable Energy Lending – 07 June 2011

Supply Chain

Information

HIT ENERGY

EE Product

Distributers and manufacturers of EE equipment were a very important sales channel and became our essential partners

We implemented relevant action plans with each supplier

We organized training sessions and promotions in cooperation with partners and created a unique product package

A large number of clients did not have satisfactory financial ratios and appropriate collateral

Čačanska banka a.d. Čačak

What we have learned

THANK YOU – QUESTIONS

EFSE ANNUAL MEETING 2011 – Energy Efficiency and Renewable Energy Lending – 07 June 2011

What we have learned

THANK YOU - QUESTIONS

The campaign started at the time of the strongest strike of economic crisis

Continuous investment in resources for improving knowledge in this area is crucial

Growing potential is extremely high, a list of measures is expanding daily

The success is inevitable if the expertise of staff is used as the main resource

Loan Agreement with GGF has been signed, we continue to finance EE/RE projects, we plan to create a product with strong brand

Čačanska banka a.d. Čačak

Matthias HitzelDirector Operations, MACS

www.macsonline.dewww.macsonline.de

Challenges and Opportunities of Energy Efficiency and Renewable Energy Finance

Panel Session II

The New Opportunity:

www.macsonline.de

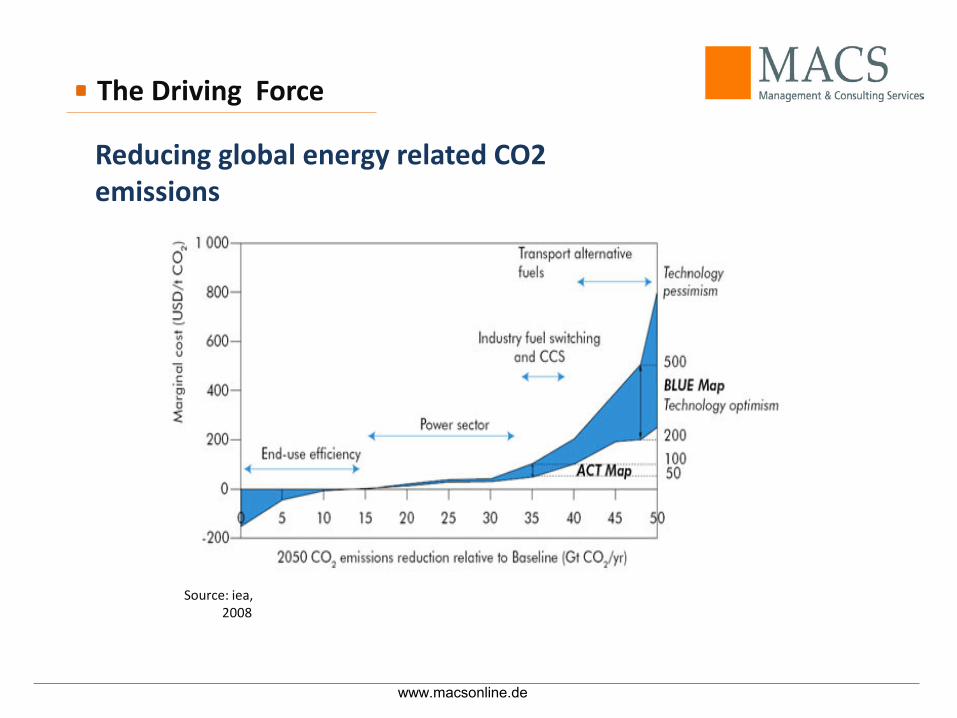

The Driving Force

Reducing global energy related CO2 emissions

Source: iea, 2008

www.macsonline.de

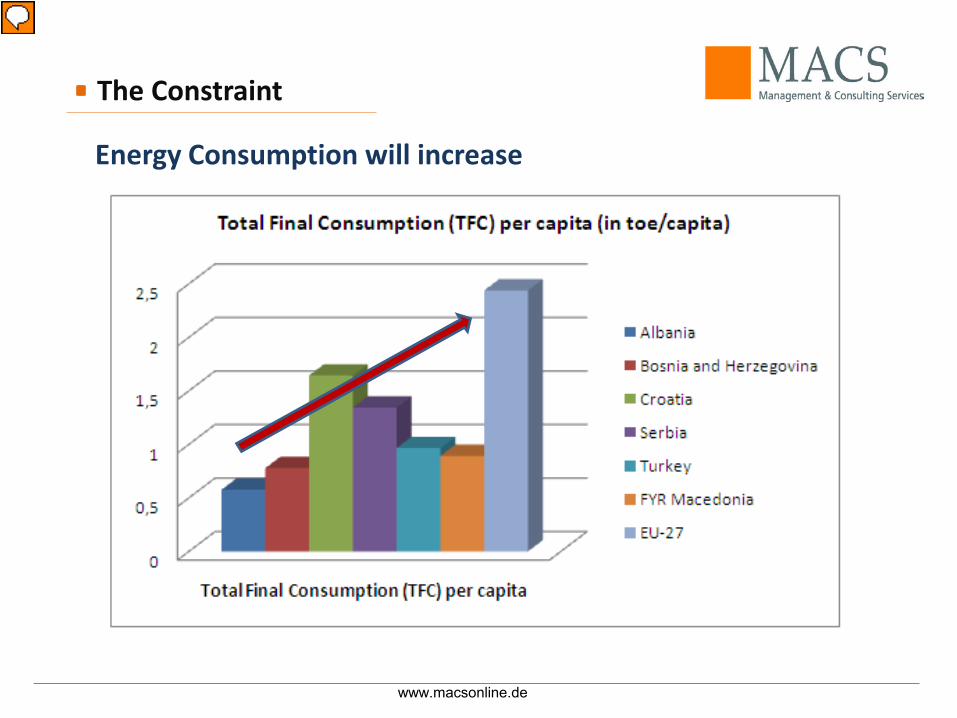

The Constraint

Energy Consumption will increase

www.macsonline.de

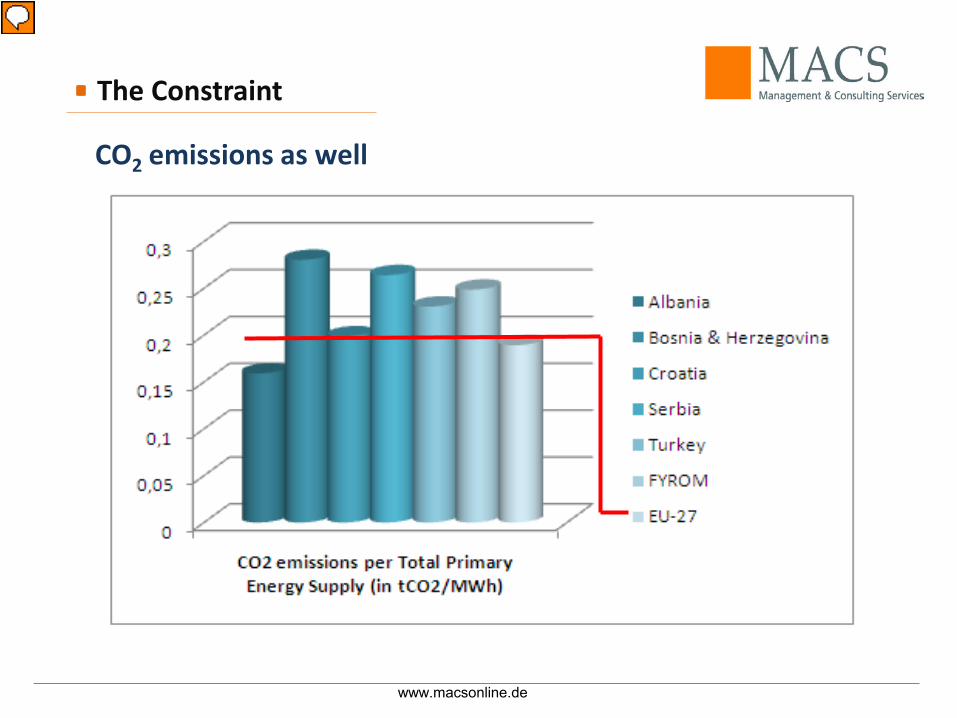

The Constraint

CO2 emissions as well

www.macsonline.de

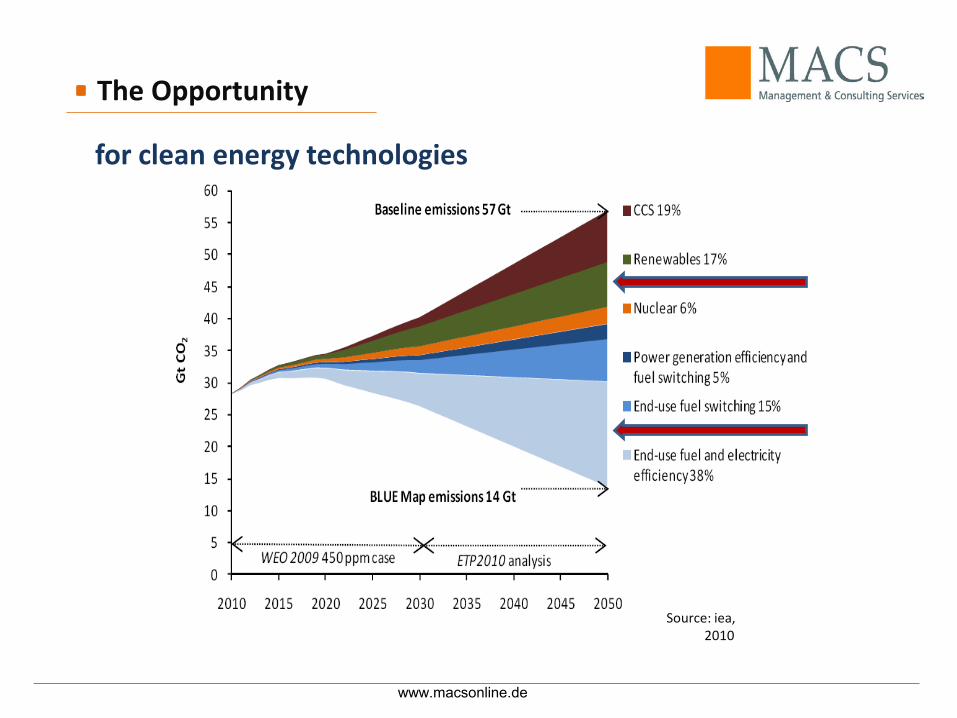

The Opportunity

for clean energy technologies

Source: iea, 2010

www.macsonline.de

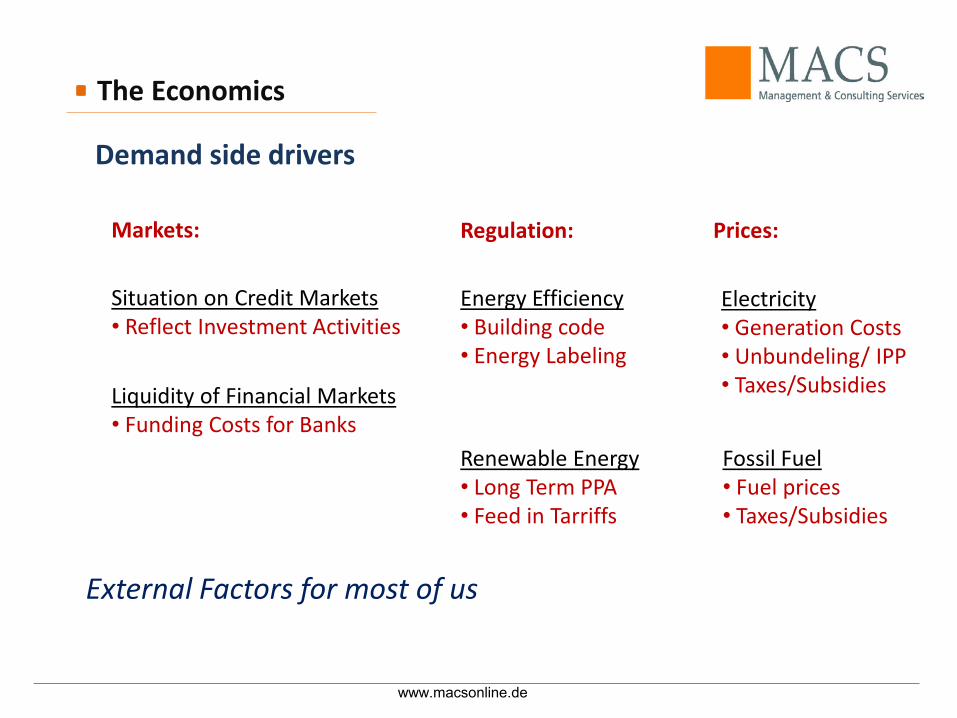

Situation on Credit Markets• Reflect Investment Activities

Energy Efficiency• Building code• Energy Labeling

Renewable Energy• Long Term PPA• Feed in Tarriffs

Liquidity of Financial Markets• Funding Costs for Banks

Markets: Regulation:

External Factors for most of us

The Economics

Demand side drivers

Prices:

Electricity• Generation Costs• Unbundeling/ IPP • Taxes/Subsidies

Fossil Fuel• Fuel prices• Taxes/Subsidies

www.macsonline.de

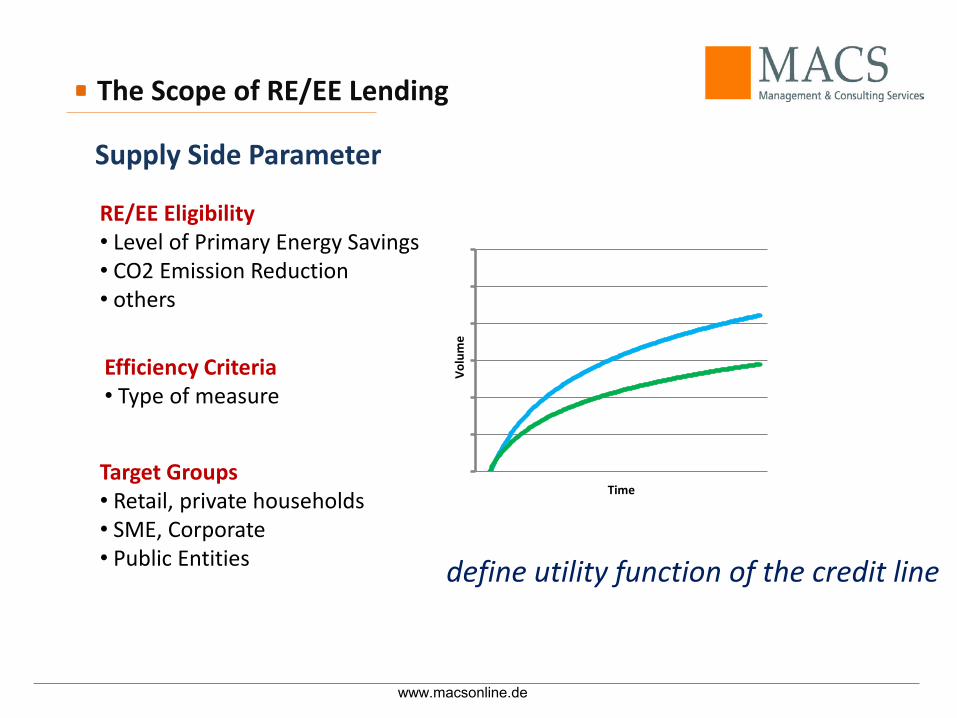

Target Groups• Retail, private households• SME, Corporate• Public Entities

RE/EE Eligibility• Level of Primary Energy Savings • CO2 Emission Reduction• others

define utility function of the credit line

Supply Side Parameter

The Scope of RE/EE Lending

Efficiency Criteria• Type of measure

0

2

4

6

8

10

12

Volu

me

Time

www.macsonline.de

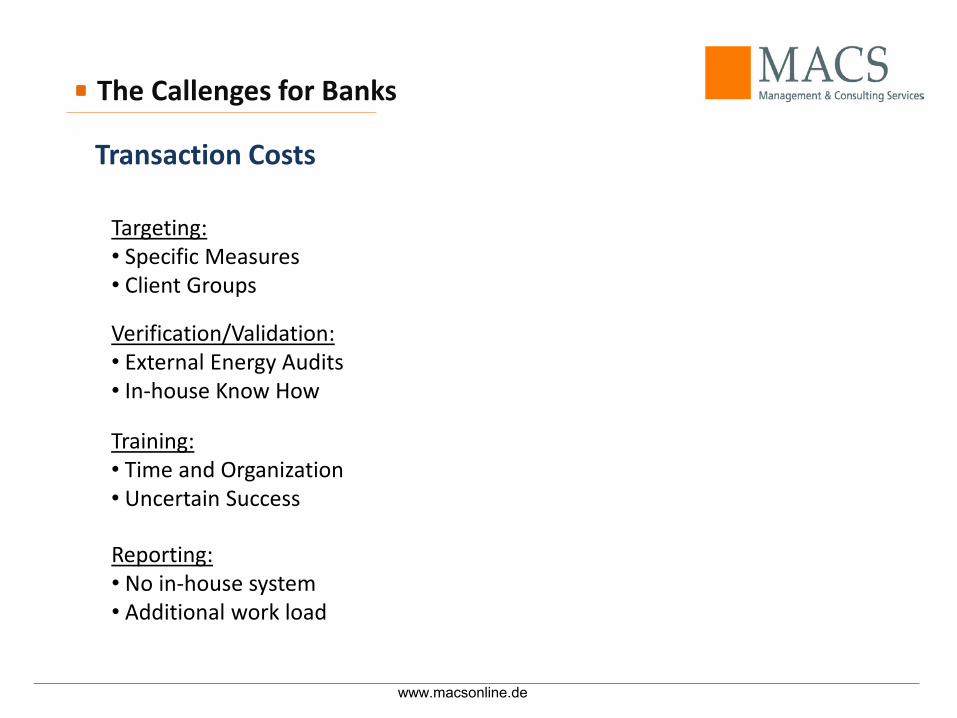

Transaction Costs

The Callenges for Banks

Targeting:• Specific Measures• Client Groups

Verification/Validation:• External Energy Audits• In-house Know How

Training:• Time and Organization• Uncertain Success

Reporting:• No in-house system• Additional work load

www.macsonline.de

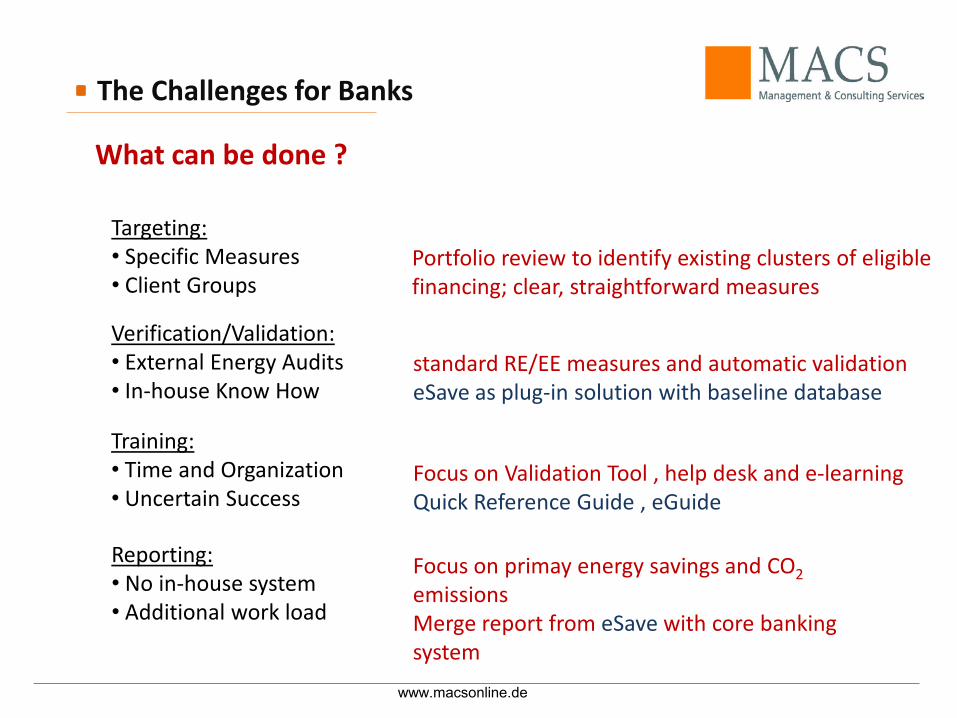

Targeting:• Specific Measures• Client Groups

Verification/Validation:• External Energy Audits• In-house Know How

Training:• Time and Organization• Uncertain Success

Reporting:• No in-house system• Additional work load

Portfolio review to identify existing clusters of eligiblefinancing; clear, straightforward measures

standard RE/EE measures and automatic validationeSave as plug-in solution with baseline database

Focus on Validation Tool , help desk and e-learningQuick Reference Guide , eGuide

Focus on primay energy savings and CO2emissions Merge report from eSave with core banking system

What can be done ?

The Challenges for Banks

www.macsonline.de

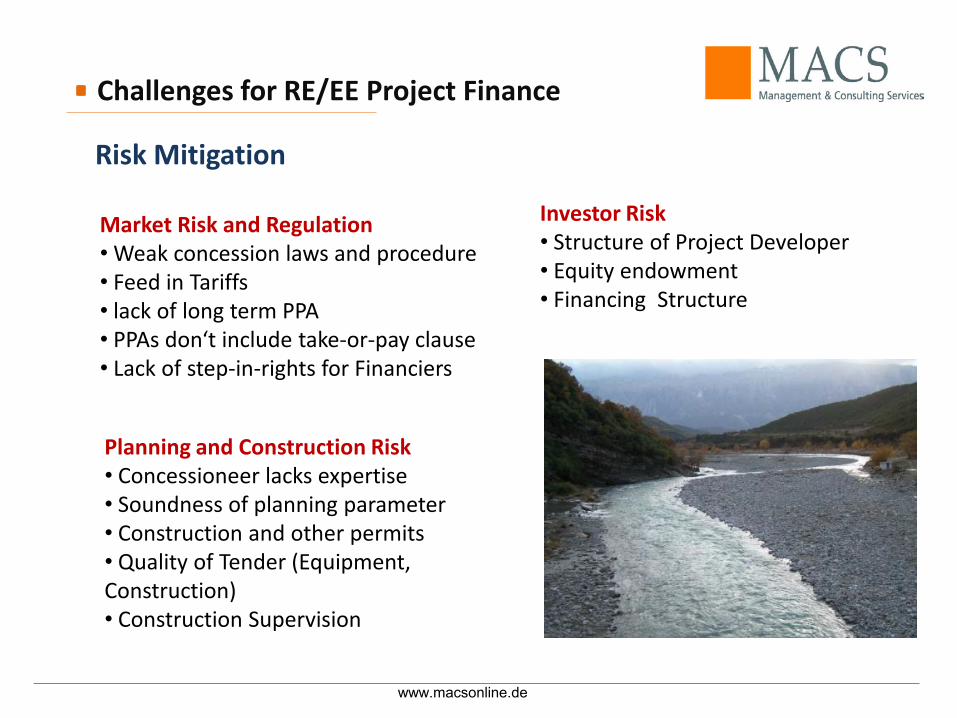

Market Risk and Regulation• Weak concession laws and procedure• Feed in Tariffs• lack of long term PPA• PPAs don‘t include take-or-pay clause• Lack of step-in-rights for Financiers

Challenges for RE/EE Project Finance

Risk Mitigation

Planning and Construction Risk• Concessioneer lacks expertise• Soundness of planning parameter• Construction and other permits• Quality of Tender (Equipment, Construction) • Construction Supervision

Investor Risk• Structure of Project Developer• Equity endowment• Financing Structure

www.macsonline.de

Thank you for your attention!

Arnsburger Str. 64, 60385 Frankfurt, GermanyTel +49-69-943188-0, Fax +49-69-943188-18e-mail: [email protected] Web: www.macsonline.de

Wolfgang KröpflManaging Director, enso GmbH

June 2011

ensoSOLID INVESTMENTS IN GREEN ENERGYEFSE meeting Tirana 07.06 – 08.06.2011

32

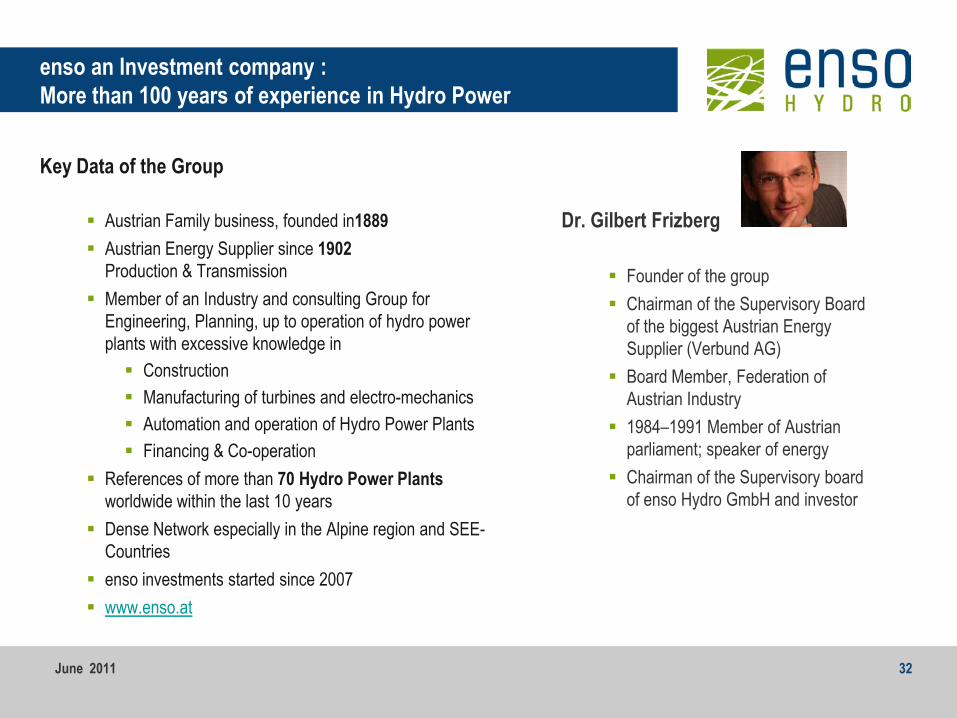

enso an Investment company : More than 100 years of experience in Hydro Power

Key Data of the Group

Austrian Family business, founded in1889 Austrian Energy Supplier since 1902

Production & Transmission Member of an Industry and consulting Group for

Engineering, Planning, up to operation of hydro power plants with excessive knowledge in Construction Manufacturing of turbines and electro-mechanics Automation and operation of Hydro Power Plants Financing & Co-operation

References of more than 70 Hydro Power Plants worldwide within the last 10 years

Dense Network especially in the Alpine region and SEE-Countries

enso investments started since 2007 www.enso.at

Dr. Gilbert Frizberg

Founder of the group Chairman of the Supervisory Board

of the biggest Austrian EnergySupplier (Verbund AG)

Board Member, Federation of Austrian Industry

1984–1991 Member of Austrian parliament; speaker of energy

Chairman of the Supervisory board of enso Hydro GmbH and investor

June 2011

33

enso - Investment

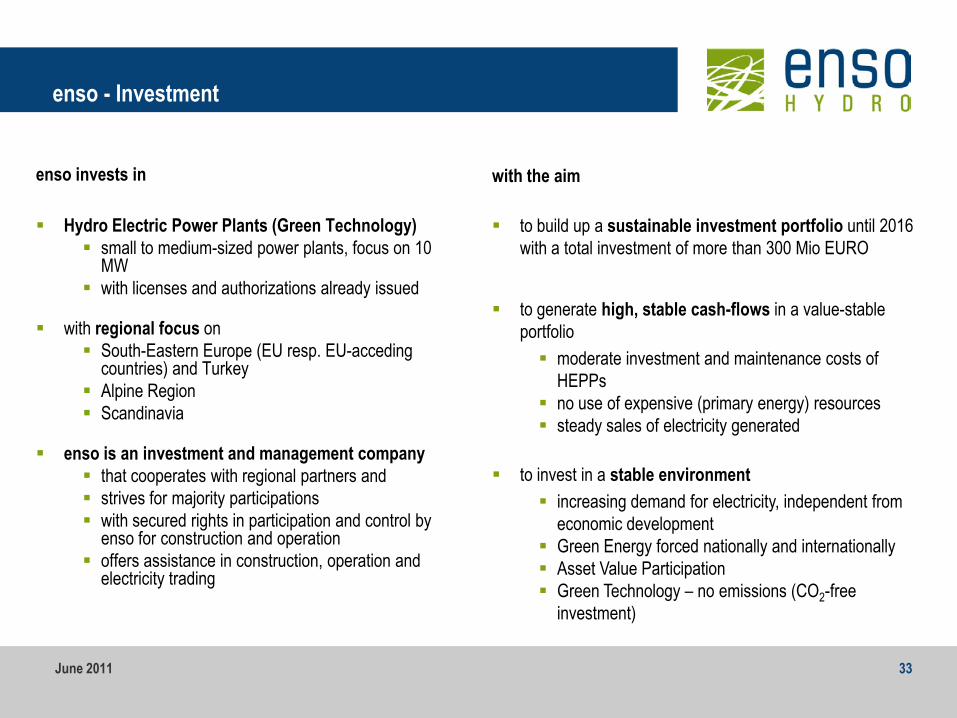

enso invests in

Hydro Electric Power Plants (Green Technology) small to medium-sized power plants, focus on 10

MW with licenses and authorizations already issued

with regional focus on South-Eastern Europe (EU resp. EU-acceding

countries) and Turkey Alpine Region Scandinavia

enso is an investment and management company that cooperates with regional partners and strives for majority participations with secured rights in participation and control by

enso for construction and operation offers assistance in construction, operation and

electricity trading

with the aim

to build up a sustainable investment portfolio until 2016 with a total investment of more than 300 Mio EURO

to generate high, stable cash-flows in a value-stable portfolio moderate investment and maintenance costs of

HEPPs no use of expensive (primary energy) resources steady sales of electricity generated

to invest in a stable environment increasing demand for electricity, independent from

economic development Green Energy forced nationally and internationally Asset Value Participation Green Technology – no emissions (CO2-free

investment)

June 2011

34

1.Attractive Potential – Market Environment

June 2011

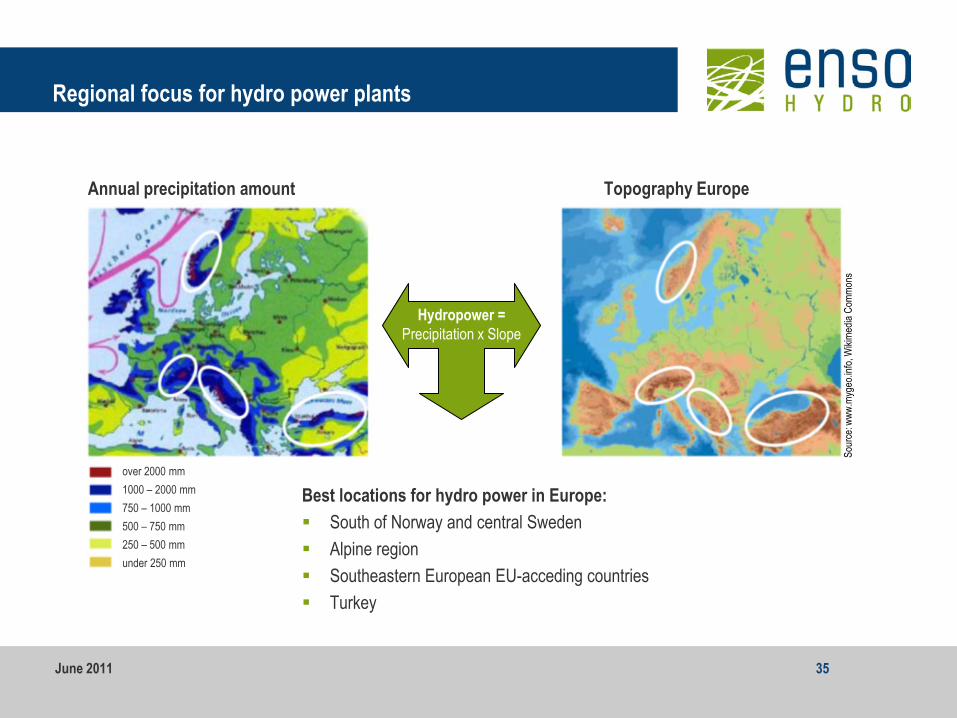

Regional focus for hydro power plants

Annual precipitation amount Topography Europe

Hydropower =Precipitation x Slope

35

Best locations for hydro power in Europe: South of Norway and central Sweden Alpine region Southeastern European EU-acceding countries Turkey

over 2000 mm1000 – 2000 mm750 – 1000 mm500 – 750 mm250 – 500 mmunder 250 mm

Sour

ce: w

ww.m

ygeo

.info,

Wiki

media

Com

mons

June 2011

36

Market Environment

Demand/Consumption Electricity consumption

increases, even in weak economic periods

need to catch up especially in South-Eastern Europe

on average increasing electricity prices

Energy supply/Electricity production Demand for electricity exceeds

electricity production Need to use green technology

to reach the climate protection requirements

Out-dated thermal power plants

Political Trend - ecology 20:20:20 targets of the EU Ownership unbundling Promotion of green energy (direct

financial aid from EIB, EBRD and other IFIs)

Europe's (and country's) independency from imports

Industrial Structure Trend to privatisation Trend to small and

medium-sized hydro energy Regulated market Guaranteed electricity sales Guaranteed minimum feed-

in-tariffs following the Euro

Marketenviron-ment

June 2011

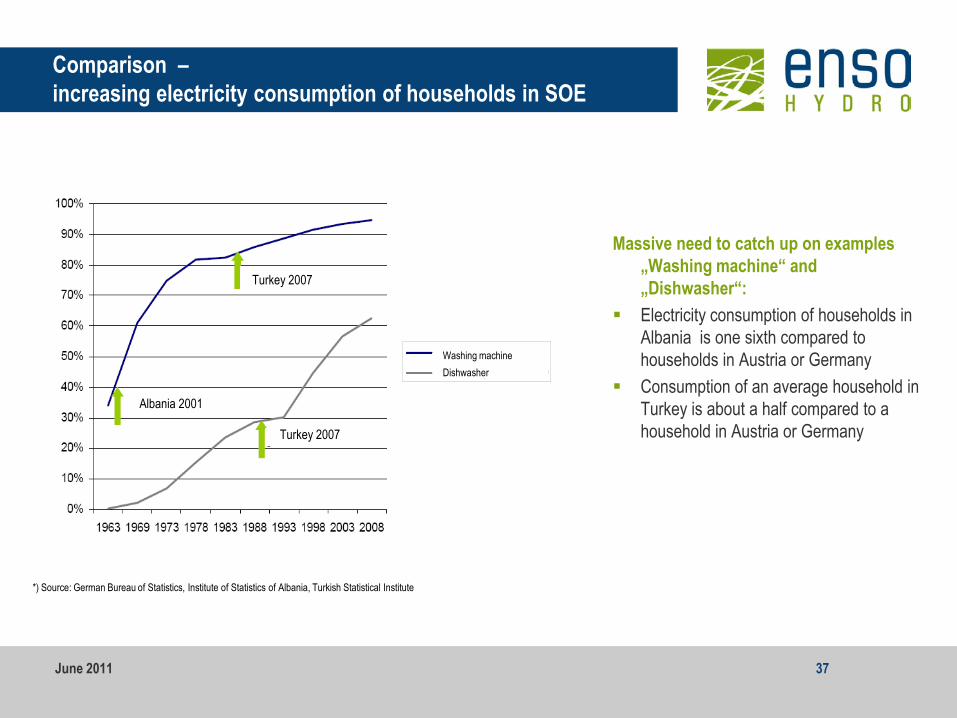

Comparison –increasing electricity consumption of households in SOE

Turkey 2007

Albania 2001

Turkey 2007

Washing machineDishwasher

*) Source: German Bureau of Statistics, Institute of Statistics of Albania, Turkish Statistical Institute

37

Massive need to catch up on examples „Washing machine“ and „Dishwasher“:

Electricity consumption of households in Albania is one sixth compared to households in Austria or Germany

Consumption of an average household in Turkey is about a half compared to a household in Austria or Germany

June 2011

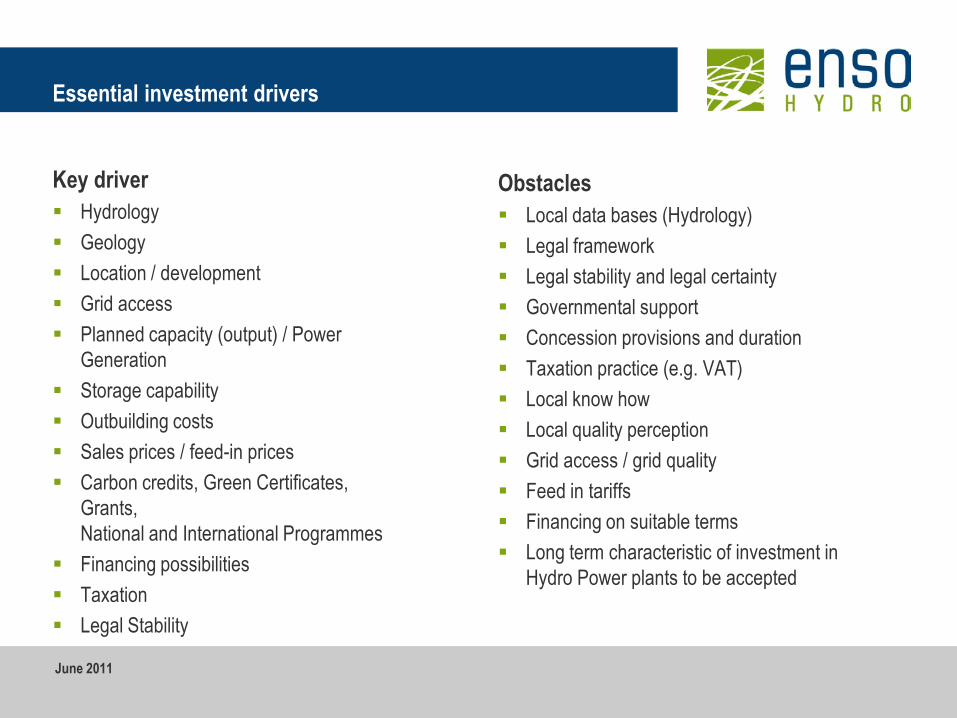

Essential investment drivers

Key driver Hydrology Geology Location / development Grid access Planned capacity (output) / Power

Generation Storage capability Outbuilding costs Sales prices / feed-in prices Carbon credits, Green Certificates,

Grants,National and International Programmes

Financing possibilities Taxation Legal Stability

June 2011

Obstacles Local data bases (Hydrology) Legal framework Legal stability and legal certainty Governmental support Concession provisions and duration Taxation practice (e.g. VAT) Local know how Local quality perception Grid access / grid quality Feed in tariffs Financing on suitable terms Long term characteristic of investment in

Hydro Power plants to be accepted

STRICTLY CONFIDENTIAL

Disclaimer

The presentation is not intended to be a legal prospectus under the capital market law. The intended recipient (hereafter referred to as ”recipient”) of this presentation (hereafter referred to as ”presentation”) agrees and accepts herewith to handle and treat all of the contents of this brochure as strictly confidential. The presentation is being provided by enso as a framework to a limited number of qualified people who in principle have an interest in investing in enso. A recipient is not the intended recipient in all cases where this document is transferred to another party by someone other than enso. The presentation is being provided to potential institutional and experienced investors (hereafter referred to as “potential investors”) solely for the purposes to support the assessment of a potential investment in enso. Furthermore, the presentation is incomplete in as much that it contains only a brief overview relevant to the potential investment. The data contained herein is not intended to serve as investment advice. Any investment decision should solely be based upon your own complete examination taken in conjunction with a qualified potential investor. The presentation does not represent an offer or a proposal, an invitation to bid, a recommendation to purchase or sell, to subscribe or underwrite or issue any other kind of securities. Nor is it a request to contribute towards such offers or such tenders or proposals and does not provide or represent the basis of an agreement with enso. Information and/or estimation contained within the presentation is liable and subject to change without further notification. By means of the transmission of this presentation enso does not assume any obligation or liability to the recipient to provide further information or accept any liability for any omissions or any adjustments or amendments that might become evident. Potential investors should only consider the possibility of an investment once they have conducted sufficient research and/or have available satisfactory knowledge with which they can correctly consider and assess any risks associated with an investment. The provision of a letter of intent or a commitment relating to the investment does not guarantee any earnings and/or maintenance of capital. Potential investors should be aware that this investment could lead to the loss of the total amount invested. Like all investments, this investment carries considerable chances and risks. Potential investors should therefore only undertake any commitment to invest following a precise and complete assessment of the presentation itself and the market situation. With regard to the anticipated duration of the investment, investors are advised to invest only a portion of their assets. Separate assessment and appraisal of legal, tax and fiscal matters plus any other potential consequences related to the investment are the sole responsibility of the potential investors and their advisors and are seen as a precondition for a commitment and the acquisition of a shareholding (including transfer of shares and application for a participation certificate). The information contained in the presentation is compiled from, and based upon, publicly available data as well as established data from internal and other sources regarded as reliable in order to be as authoritative and dependable as is possible or deemed necessary. Additionally thereupon, it should also be noted that the presentation contains estimates and prognoses based upon commonly used economic and industry trends as well as expected developments derived and compiled respectively from them. These estimates and prognoses contain a number of subjective assessments. This presentation, other written or verbal correspondence, communication or declarations of any kind do not constitute in any way whatsoever a warranty, guarantee, commitment or other acceptance of liability, whether explicit or implied, and should not be considered to be agreed and/or assumed commitments. Neither enso or their board of directors, managers, employees or representatives assume and/or take responsibility for the completeness, accuracy and/or correctness of the information contained in the presentation (including legal and fiscal), for any omission of information, for associated estimates and for any supplementary information that are provided or made available to any interested party or their advisors. By agreeing to an investment, interested parties explicitly relinquish enso of any accountability and responsibility on the basis of such information provided herein or other failure or omission. The presentation is intended for the exclusive use and assessment of a potential transaction of the addressee only.

June 2011

40

Contact

Contact - Managementenso GmbHDi Wolfgang Kröpfl, MBAFranz-Heresch-Straße 2, 8410 WildonT: +43 (0) 3182 2216-130M: +43 (0) 664 8324460E: [email protected]

June 2011

Terry McCallionDirector, EBRD

Differing approaches to EE & RE lending

Terry McCallion 6 June 2011

Shaping and Leveraging the New Reality

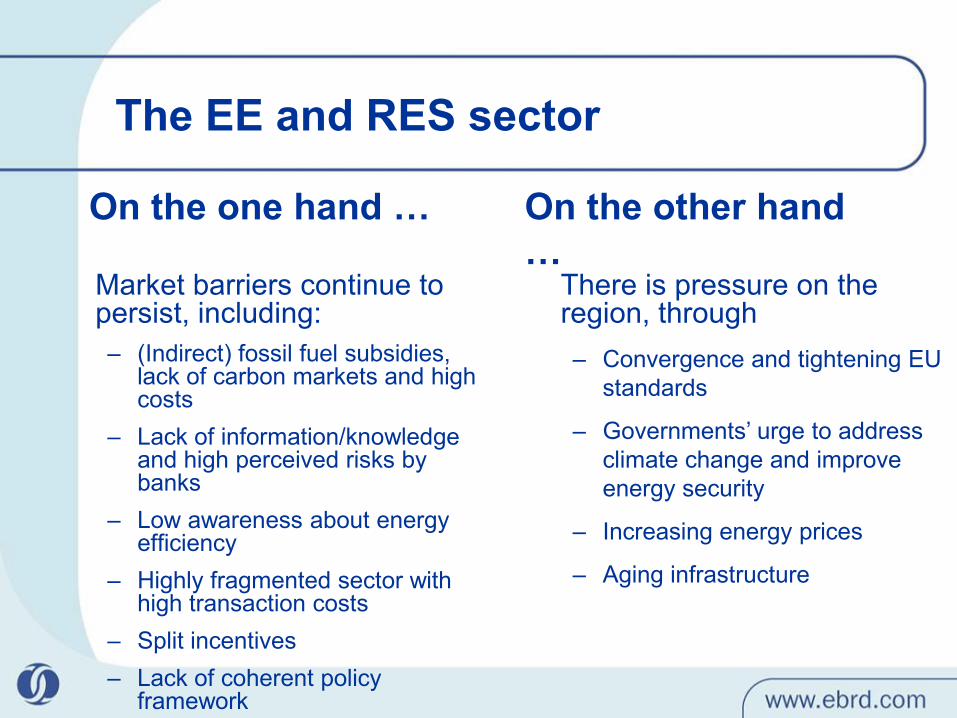

The EE and RES sector

Market barriers continue to persist, including:– (Indirect) fossil fuel subsidies,

lack of carbon markets and high costs

– Lack of information/knowledge and high perceived risks by banks

– Low awareness about energy efficiency

– Highly fragmented sector with high transaction costs

– Split incentives – Lack of coherent policy

framework

On the one hand … On the other hand …

There is pressure on the region, through – Convergence and tightening EU

standards

– Governments’ urge to address climate change and improve energy security

– Increasing energy prices

– Aging infrastructure

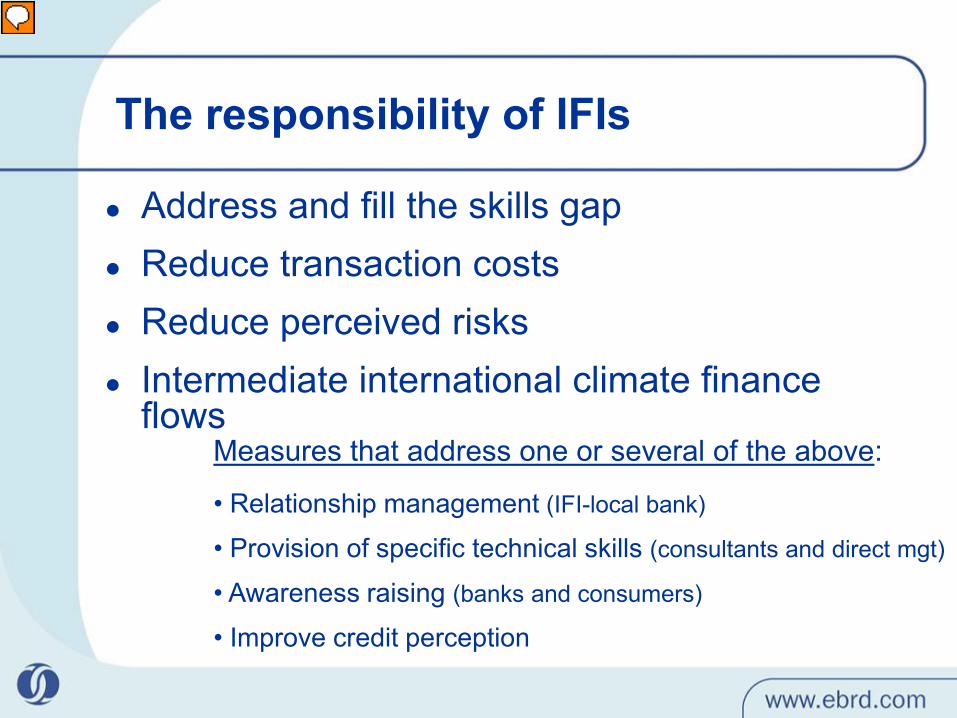

The responsibility of IFIs

Address and fill the skills gap Reduce transaction costs Reduce perceived risks Intermediate international climate finance

flowsMeasures that address one or several of the above:

• Relationship management (IFI-local bank)

• Provision of specific technical skills (consultants and direct mgt)

• Awareness raising (banks and consumers)

• Improve credit perception

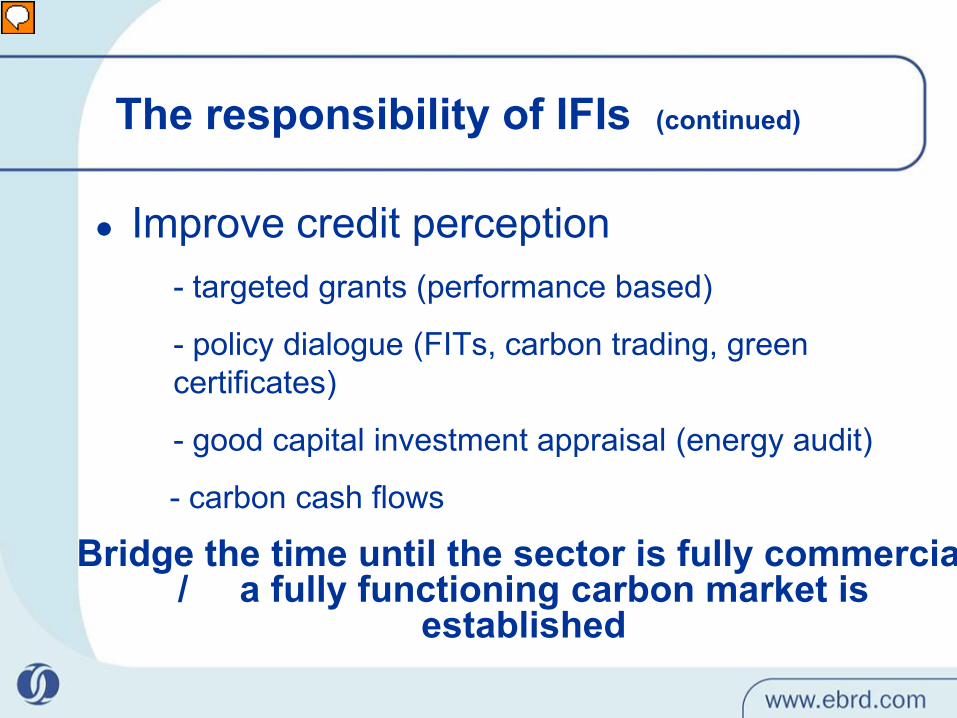

The responsibility of IFIs (continued)

Improve credit perception - targeted grants (performance based)

- policy dialogue (FITs, carbon trading, green certificates)

- good capital investment appraisal (energy audit)

- carbon cash flows

Bridge the time until the sector is fully commercia / a fully functioning carbon market is

established

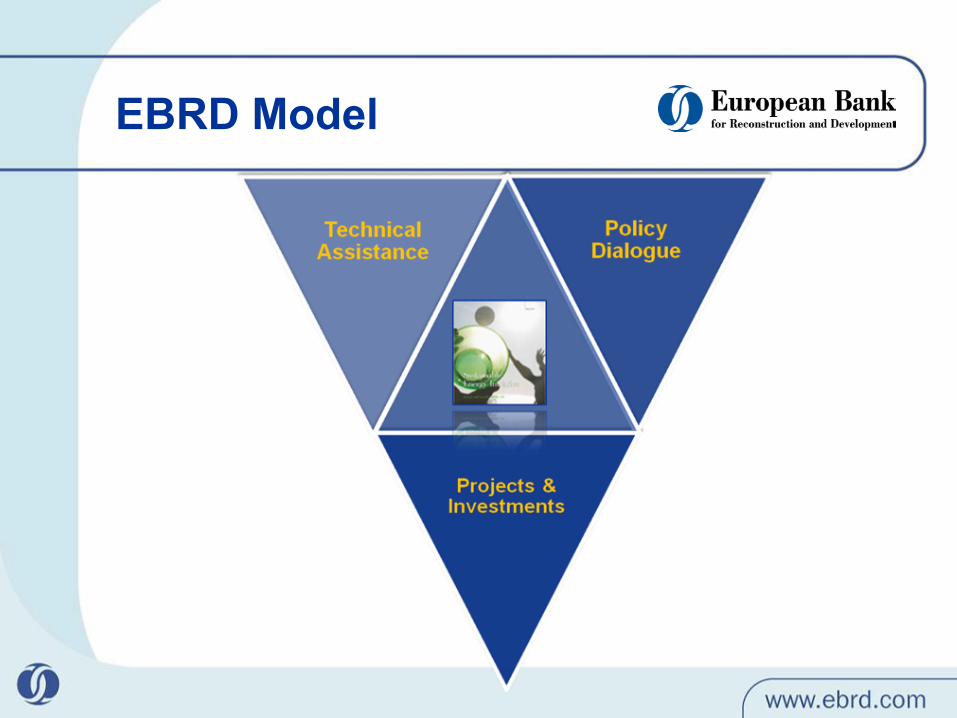

EBRD Model

47

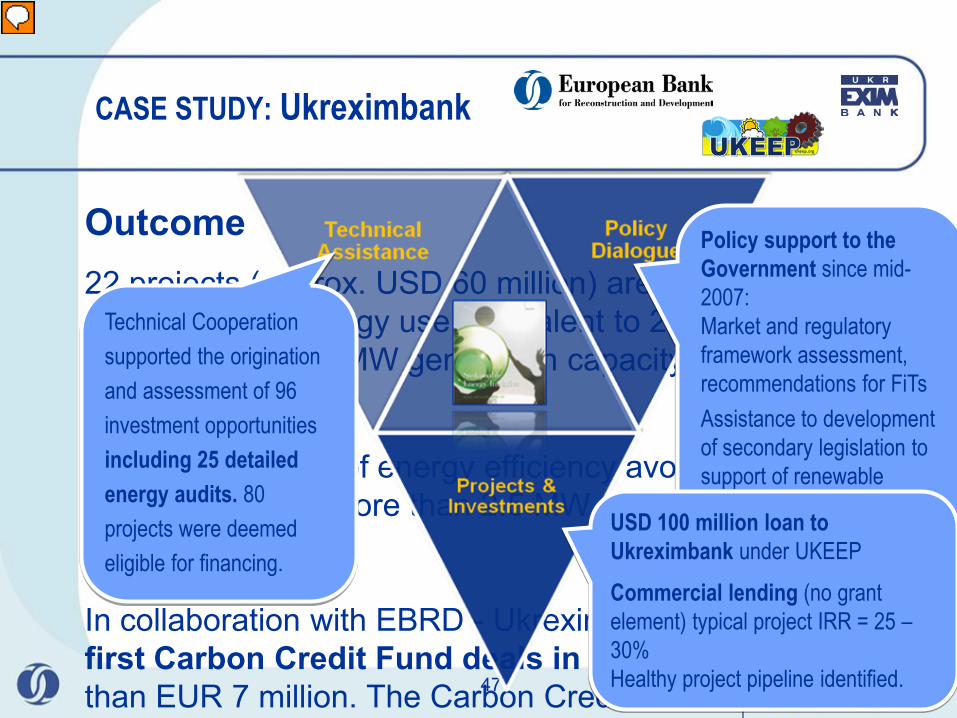

CASE STUDY: Ukreximbank

Outcome22 projects (approx. USD 60 million) are already financed; they will avoid energy use equivalent to 20 million MWh (~ 1.7mio toe or 150 MW generation capacity) and 5 million tCO2

Each million USD of energy efficiency avoids the need for the equivalent of more than 2.5 MW of electricity generation capacity.

In collaboration with EBRD - Ukreximbank pioneered the first Carbon Credit Fund deals in Ukraine, worth more than EUR 7 million. The Carbon Credits will be sold to

Policy support to the Government since mid-2007:Market and regulatory framework assessment, recommendations for FiTs Assistance to development of secondary legislation to support of renewable energy

Technical Cooperation supported the origination and assessment of 96 investment opportunities including 25 detailed energy audits. 80 projects were deemed eligible for financing.

USD 100 million loan to Ukreximbank under UKEEPCommercial lending (no grant element) typical project IRR = 25 –30% Healthy project pipeline identified.

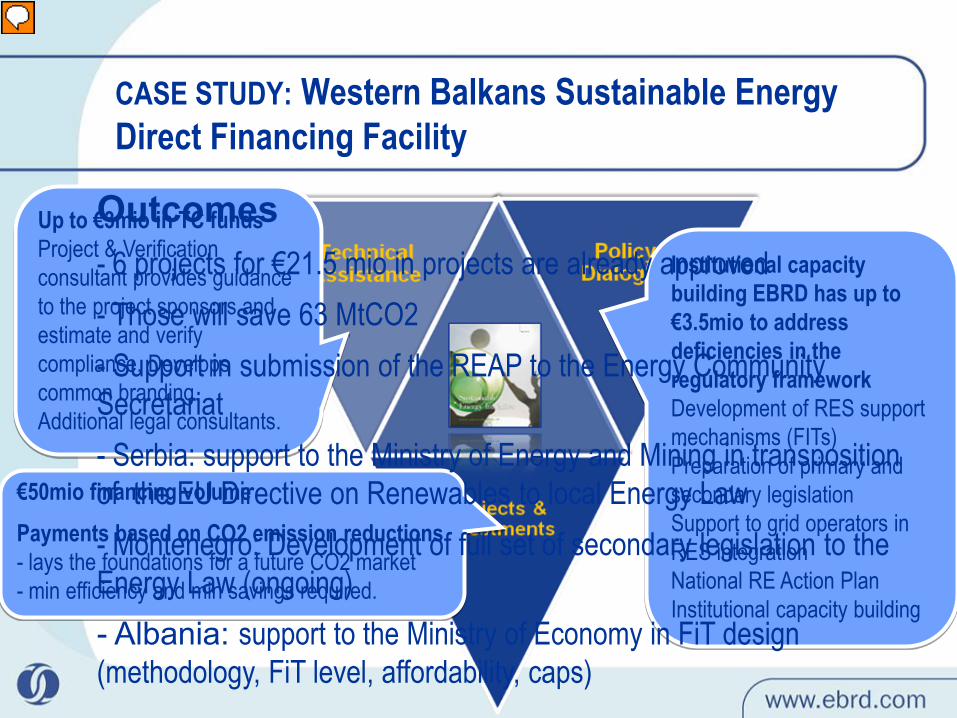

CASE STUDY: Western Balkans Sustainable Energy Direct Financing Facility

Institutional capacity building EBRD has up to €3.5mio to address deficiencies in the regulatory frameworkDevelopment of RES support mechanisms (FITs)Preparation of primary and secondary legislationSupport to grid operators in RES integrationNational RE Action PlanInstitutional capacity building

Up to €3mio in TC fundsProject & Verification consultant provides guidance to the project sponsors and estimate and verify compliance. Develops common branding. Additional legal consultants.

€50mio financing volumePayments based on CO2 emission reductions - lays the foundations for a future CO2 market- min efficiency and min savings required.

Outcomes- 6 projects for €21.5 mio in projects are already approved- Those will save 63 MtCO2 - Support in submission of the REAP to the Energy Community Secretariat - Serbia: support to the Ministry of Energy and Mining in transposition of the EU Directive on Renewables to local Energy Law - Montenegro: Development of full set of secondary legislation to the Energy Law (ongoing)- Albania: support to the Ministry of Economy in FiT design (methodology, FiT level, affordability, caps)

Panel II:The New Opportunity: Energy Efficiency and Renewable Energy Lending

Lloyd StevensDirector

Finance in Motion

Aleksandar MijailovićČačanska Banka

Yücel InanIK Banka

Olaf ZymelkaHead of Division,

Energy SEE & TurkeyKfW

Wolfgang KröpflENSO

Terry McCallionEBRD

Matthias HitzelMACS

After Coffee Break:

Concluding and Closing PanelShaping and Leveraging the New Reality

Conference Hall Illyria

Coffee Break16:00 – 16:30

EFSE Annual Meeting 2011