Embed Size (px)

Citation preview

Effective Social Enterprise — A Menu of Legal Structuresby Robert A. Wexler

Robert A. Wexler

Robert Wexler is a principalwith the San Francisco lawfirm of Adler & Colvin, a LawCorporation. Rosemary Fei,also a principal with Adler &Colvin, assisted with the re-view and editing of this article.

* * * * *The new client, comfort-

ably seated at the conferenceroom table, asks: ‘‘What isthe definitive legal form fora new social enterprise — anonprofit corporation that istax exempt as an organiza-

tion described in IRC section 501(c)(3);1 a nonprofitcorporation that is tax exempt as an organization de-scribed in section 501(c)(4); a nonprofit corporation that isnot tax exempt; a for-profit corporation; a for-profit Scorporation; a B corporation; a limited liability company;a low-profit limited liability company, also known as anL3C; a combination of the above; or other?’’ The seasonedattorney, not the least bit intimidated by this complexquestion, replies with the often used, lawyerly, and in thiscase quite accurate, response, ‘‘It depends.’’

In December 2006 I wrote an article titled, ‘‘SocialEnterprise: A Legal Framework’’ (The Exempt Organiza-tion Tax Review, December 2006, p. 233). That article wasan overview of the legal issues facing the social enter-prise movement in the United States. In the two-plusyears since writing that article, I have had an opportunityto advise more and more social entrepreneurs, some whowish to form a new tax-exempt entity, others who leadestablished exempt organizations and are seeking toexpand their revenue-generating activities, and somewho have business plans in various stages of develop-ment and are not sure whether they should form afor-profit entity, a nonprofit entity, or both. Those seekingto use both a for-profit and a nonprofit sometimes refer tothe new entities as a hybrid social enterprise.

Those of us who work with social enterprises recog-nize by now that there is no legal definition of socialenterprise, and there is not even a uniformly recognizednonlegal definition, although there have been manyvaliant attempts. The Social Enterprise Alliance (http://

www.se-alliance.org) defines a social enterprise as ‘‘anorganization or venture that achieves its primary socialor environmental mission using business methods.’’ TheSkoll Foundation (http://www.skollfoundation.org) de-fines social entrepreneur, one who forms and leads asocial enterprise, as ‘‘society’s change agent: a pioneer ofinnovations that benefit humanity.’’

To me, the word ‘‘enterprise’’ implies that there is abusinesslike activity. More often than not a businesslikeactivity will seek to generate revenue. The word ‘‘social’’implies that some good is coming from the enterprise,other than merely the generation of profits. What makesa particular endeavor socially beneficial is, of course,somewhat subjective. At its core, a social enterprise,whatever else it is or is not, is a businesslike activity thatis designed, at least in part, to do good, and not simply togenerate profits.

Beyond this basic concept, I am not concerned herewith definitions, nor do I care to debate, as exemptorganization lawyers sometimes do, whether the conceptof social enterprise is good, truly differs from traditionalphilanthropy, or is just a logical extension of traditionalphilanthropy. It may well be all of the above. Personally,I believe that identifying socially motivated revenue-generating activity as social enterprise is more helpfulthan not, that social enterprise does differ, at least insome important ways, from traditional philanthropy, butthat social enterprise is not an entirely new construct. Ithas evolved from at least two sources: (1) the traditionalrevenue-generating nonprofit models, including hospi-tals, schools, and low-income housing organizations; and(2) the significant increase in for-profit venture activityduring the past 20 or more years.

Some social enterprises succeed, some fail. Our job ascounsel is to provide social entrepreneurs and socialenterprises with the best possible legal framework tohelp them try to succeed.

The purpose of this article, my second on socialenterprise, is to provide guidance to the social entrepre-neur about how to decide whether a new social enter-prise should be structured within a tax-exempt or taxablelegal entity, or whether a hybrid structure using both ataxable and an exempt entity is more appropriate. Thefirst section presents the menu of legal structures poten-tially available to the social enterprise, eliminating thosethat are hardly ever practical. Next, I pose a series ofquestions that the attorney should consider with the

1All section references, unless otherwise stated, are to theInternal Revenue Code of 1986, as amended.

The Exempt Organization Tax Review June 2009 — Vol. 63, No. 6 565

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Meat Tax FactorsManagementand Control

Capital andLoans

Distributions ofFunds Not Used

for Programs Liquidation

For-profitcorporation

Taxed on netincome.

Shareholders electboard of directors,which delegates tocommittees andstaff.

Shareholdersmake contribu-tions. The entitymay be able toaccept programrelated invest-ments (PRIs) fromfoundations in theform of loans orequity.

Dividends toshareholders. Canmake charitablecontributions, butdeductibility lim-ited to 10 percentof net income.

Net assets toshareholders, afterpaying creditors.

Limited liabilitycompany (LLC)taxed as a part-nership

Items of incomeand expensepassed through tomembers. Tax-exempt memberstreat their share ofincome as exemptor subject to unre-lated business tax-able income(UBTI), dependingon the characterof the income

The operatingagreement pro-vides for a man-agement commit-tee or a singlemanager, typicallyelected by themembers.

Membership con-tributions; pos-sible PRI funding.

Distributions tomembers. LLCcan make chari-table contribuionsand allocate themto the members toclaim on theirown returns.

Net assets tomembers, afterpaying creditors.

Low-Fat,Organic,

SubstainablyGrown Tax Factors

Managementand Control

Capital andLoans

Distributions ofFunds Not Used

for Programs Liquidation

The B corporation(a for-profit corpo-ration that alsohas a social mis-sion and is li-censed to use thetrade name ‘‘Bcorporation’’)

See for-profit cor-poration above.

See for-profit cor-poration above.

See for-profit cor-porations above.A B corporationmay be in a betterposition to attractand accept PRImoney.

See for-profitabove. May be setup to make contri-butions to chari-ties or sociallybeneficial causes,although no de-ductibility advan-tage.

Net assets usuallyto shareholders,but distributionsto charity may bepossible as well.

L3C (an LLC thatis formed as alow-profit limitedliability company)

See LLC above. See LLC above. See LLC above;plus, set up toaccept PRI moneymore easily.

Distributions tomembers andgrants for chari-table purposes.

Net assets tomembers and to501(c)(3) charities.

Vegetarian Tax FactorsManagementand Control

Capital andLoans

Distributions ofFunds Not Used

for Programs Liquidation

Nonprofit corpo-ration 501(c)(3)

Not taxed on in-come, unless it’sUBTI. Can offertax deductions todonors.

Board of directorscontrols. Somecorporations havemembers whoelect directors orappointers/designators whoappoint directors.

Charitable contri-butions andgrants. Easily eli-gible for PRIloans.

Grants for chari-table purposes.

Net assets to an-other 501(c)(3)with like exemptpurposes.

Nonprofit corpo-ration 501(c)(4)

Not taxed on in-come, unless it’sUBTI. No tax de-duction for do-nors.

See 501(c)(3)above.

Nondeductiblecontributions;grants; possiblePRI money.

Can make grantsfor charitable orpublic and socialwelfare purposes.

Net assets to an-other 501(c)(4) orto a 501(c)(3), ineither case withlike exempt pur-poses.

Special Report

566 June 2009 — Vol. 63, No. 6 The Exempt Organization Tax Review

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

client in making selections from the menu.2 Finally, Iprovide a brief framework for analyzing the informationcollected from the client in order to suggest the mostpractical legal form under the circumstances.

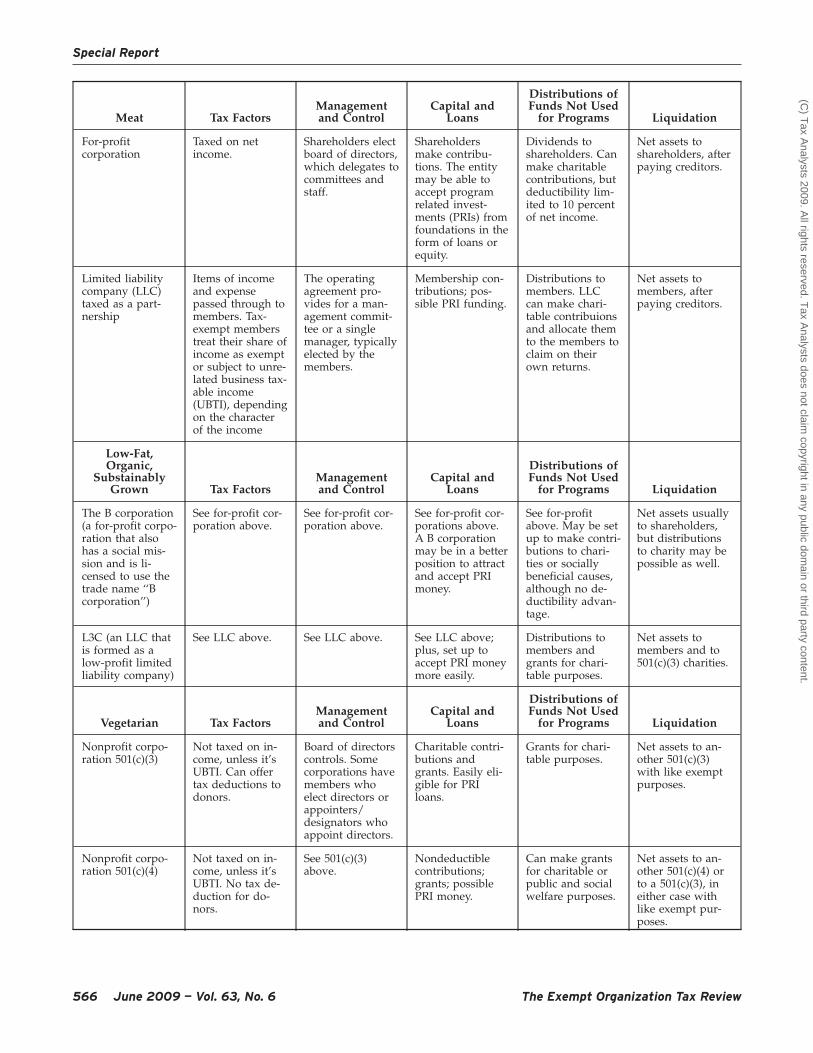

I. Menu of Social Enterprise Options

The menu (p. 2) consists of three sections: Meat;Low-Fat, Organic, Substainably Grown; and Vegetarian.Combination platters are also offered, by choosing onemenu item from meat or low-fat meat and one from thevegetarian menu.

The following items are not on our menu because theypresent no relative advantages over the choices listedabove: S corporations; trusts; unincorporated associa-tions; general partnerships; limited partnerships; LLCsthat elect to be taxed as corporations, including those thatqualify under section 501(c)(3); single member LLCs; andnonprofit corporations that do not seek to qualify fortax-exempt status.

Reading and understanding the menu:

Meat

The meat portion of the menu offers the two mostviable options for an entirely for-profit experience. Thereare many articles and treatises written on the relative taxand legal advantages and disadvantages of the LLCversus the corporation, which are beyond the scope ofthis article. Entrepreneurs who, at this point, have nointerest in the low-fat or vegetarian options and whohave no interest in seeking tax-exempt investors prob-ably need read no further.

But when a for-profit social enterprise intends to seekone or more 501(c)(3) or (c)(4) tax-exempt investors,whether in an LLC as members, or in a corporation asshareholders, the entrepreneur must understand that the

tax-exempt investor will almost always prefer to invest ina vehicle that minimizes or eliminates any unrelatedbusiness taxable income (UBTI). Generally, such a tax-exempt investor will pay no unrelated business incometax (UBIT) on dividends or capital distributions it re-ceives from a corporation (unless it is an S corporation(section 512(e)) or unless the investor has purchased itsshares using borrowed money (section 514)). A section501(c)(3) private foundation (along with its disqualifiedpersons) generally will not be able to own more than 20percent of the shares of a corporation, unless the invest-ment qualifies as a program-related investment (sections4943 and 4944).

In contrast, the tax-exempt investor in an LLC willhave to consider the character of the income derived fromits LLC investment. If the LLC, as is likely here, isgenerating UBTI, the tax-exempt investor will pay UBITon its share of net income from the LLC. In some cases,the tax-exempt investor may be able to claim that theincome is substantially related to the performance of itsexempt activity, and therefore is not UBTI. The privatefoundation investor may own no more than 20 percent ofthe profits interest in an LLC (including the shares ownedby its disqualified persons), unless the investment is avalid program-related investment (sections 4943 and4944). Any social enterprise considering an LLC will alsoneed to be aware of the tax-exempt investor’s concernsabout the line of revenue rulings and related casesdealing with whole entity and ancillary joint ventures(see Rev. Rul. 98-15 and Rev. Rul. 2004-51). A tax-exemptinvestor in an LLC should consider whether participationin the LLC might jeopardize the investor’s exempt statusor generate UBTI.

When a tax-exempt investor’s investment in an LLC orfor-profit corporation is considered to be either substan-tially related to the investor’s exempt purposes or aprogram-related investment, the tax consequences to theinvestor are generally favorable. The income from invest-ment is not UBTI; the investment does not jeopardize theinvestor’s exempt status, and, for a private foundationinvestor, none of the section 4940 series excise taxesshould apply. However, an investment in an LLC orcorporation often will not be substantially related to aninvestor’s exempt purpose, and it may not qualify as aprogram-related investment for a private foundationinvestor.

2Although they may find it useful, this article is not ad-dressed to established tax-exempt organizations that are seekingto leverage and expand a skill, product, or service that theyalready have developed within their section 501(c)(3) entities toenter into a new revenue-generating activity. Those organiza-tions might review an article published on my firm’s Web sitetitled ‘‘Revenue-Generating Activities of Charitable Organiza-tions’’ (http://www.adlercolvin.com).

Type of Entity ProfitsDistributions

to the EO

Rents, Royalties, andInterest When EO

Controls

Rents, Royalties andInterest When EODoes Not Control

Corporation Taxed at the corporatelevel only

Dividends paid by thecorporation are nottaxed to the exemptorganization share-holder, but are notdeducted by for-profit

Taxed as UBTI to theEO; deductible by thecorporation

Not taxed to the EO;deductible by thecorporation

LLC LLC provides EO with aK-1, and EO files a990-T UBIT return topay tax on its share ofincome

LLCs do not pay divi-dends and distributionsare not separately taxedto the EO

Taxed as UBTI to theEO; expensed by theLLC, effectivelyreducing other EO tax-able income

Not taxed as UBTI;expensed by the LLC,effectively reducingother EO taxable income

Special Report

The Exempt Organization Tax Review June 2009 — Vol. 63, No. 6 567

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

The following sections summarize the tax effect to anexempt investor of operating and taking distributionsfrom a corporation or an LLC, when the investment is notconsidered to be substantially related or a valid program-related investment:

A. Income From Ordinary Operations

In the course of operations, the social enterprise willgenerate funds that will be distributed to investors in avariety of forms. Sometimes the tax-exempt investor ismerely a shareholder in a corporation or a member in anLLC. In other situations, the exempt investor also willlend money to the venture and receive interest paymentsin return, license the name of the exempt entity to theventure in return for a royalty, and/or lease real estate tothe venture. If a tax-exempt entity owns more than 50percent of the stock in a corporation or 50 percent of theprofits interest in an LLC, section 512(b)(13) treats anyrental income, interest income, or royalties paid to thetax-exempt parent as UBTI (with some limited transi-tional exceptions from the 2006 Pension Protection Act).(See chart at top of p. 3 for more details.)

B. Liquidation of Entity

At some point the entity will likely terminate andliquidate or sell its assets. (See chart at top of this page formore details.)

Low-Fat, Organic, Sustainably Grown Meat

The low-fat portion of the menu presents two types ofentities, both of which are for-profit, taxable entities, butthat are designed to engage in some social benefitactivities.

The first is the low-profit limited liability company, orL3C. The L3C nomenclature can be quite frustrating toexempt organization lawyers who have been working foryears to stop their clients from expressing with allapparent confidence to members of the public that theyare exempt under ‘‘section 501(3)(c).’’ In the case of theL3C, however, the three ‘‘L’s’’ refer to ‘‘low-profit,’’‘‘limited,’’ and ‘‘liability,’’ and the ‘‘C’’ to ‘‘company.’’

As of May 15, 2009, the L3C has been adopted inseveral states, including Vermont, Michigan, Wyoming,North Dakota, and Utah, and it has been introduced in atleast a half dozen more, but anyone can, of course, forman L3C in one of these states that does business in anystate. Other states are considering adopting the L3Cform, and the Crow Indian Nation also has adopted anL3C statute. See http://www.americansforcommunitydevelopment.org for an update.

The L3C is an LLC for all legal and tax purposes, butit has some requirements built in by statute. The Vermontlaw (Sec. 1. 11 V.S.A. section 3001(23)), for example,requires that:

(A) The company:

(i) significantly furthers the accomplishment of oneor more charitable or educational purposes withinthe meaning of Section 170(c)(2)(B) of the InternalRevenue Code of 1986, 26 U.S.C. section170(c)(2)(B); and

(ii) would not have been formed but for the com-pany’s relationship to the accomplishment of chari-table or educational purposes.

(B) No significant purpose of the company is theproduction of income or the appreciation of prop-erty; provided, however, that the fact that a personproduces significant income or capital appreciationshall not, in the absence of other factors, be conclu-sive evidence of a significant purpose involving theproduction of income or the appreciation of prop-erty.

(C) No purpose of the company is to accomplishone or more political or legislative purposes withinthe meaning of Section 170(c)(2)(D) of the InternalRevenue Code of 1986, 26 U.S.C. section170(c)(2)(D).

There are two perceived advantages of being an L3C.The first is the ability to more easily attract program-related investments from private foundations. Because ofthe statutory requirements, private foundations will havean easier time making the findings required under sec-tion 4944 in order to fund a program-related investmentin an L3C than in an ordinary for-profit vehicle. Thesecond advantage is that being formed as an L3C mayprovide a branding or marketing benefit that might openup access to funding and contracts that might not beavailable to a standard LLC. It is too soon to tell whethereither of these benefits will materialize, but the L3C mayprove to be a valuable tool for social entrepreneurs.

The B corporation is a standard for-profit corporationfor all legal and tax purposes, formed under applicablestate laws, except that it has incorporated particularsocially beneficial standards into its governing docu-ments and operating principles that entitle it to licensethe brand name ‘‘B corporation’’ from a for-profit entitycalled B Labs. Many regard this certification as signifyingthat the B corporation is, while operating for profit,operating in a way that promotes favorable employmentpractices, environmental standards, and engages in somelevel of social welfare or charitable activity. See www.b-corporation.net for more information. B Labs’ Web sitestates:

B Corporations are a new type of corporation whichuses the power of business to solve social andenvironmental problems. B Corporations are unliketraditional responsible businesses because they:

Type of Entity Liquidation SaleCorporation Deemed sale of assets, taxable at for-profit

corporate level (section 336). No tax to EO onreceipt of assets.

Tax at for-profit corporate level, not at EO levelon the receipt of assets.

LLC No LLC-level tax; usually there is no tax to theEO on the receipt of property (section 731).

Gain on sale is passed through to EO. Some ofthe income may be taxable and some not to EO.

Special Report

568 June 2009 — Vol. 63, No. 6 The Exempt Organization Tax Review

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

meet comprehensive and transparent social andenvironmental performance standards;

institutionalize stakeholder interests; and

build collective voice through the power of a uni-fying brand.

Accordingly, even though the L3C and the B corpora-tion are designed to promote social good, their tax effectsfor EO investors are the same as those provided aboveunder the meat section. The debate as to the value of theB corporation brand and the L3C form is likely tocontinue for some years to come.

I also am part of a task force of volunteer attorneys inCalifornia that is drafting legislation to create a new typeof California corporation whose management would belegally permitted to operate for the benefit of labor,environmental, and charitable interests, in addition to theinterests of shareholders. If adopted, this new type ofentity will go beyond the ‘‘constituency statutes’’ thatmany other states have already adopted by, among otherthings, requiring management to measure and reporthow it has provided a social return on investment to itsshareholders. Constituency statutes are code sectionswithin a state’s corporations code that permit a board ofdirectors to consider interests other than those of theshareholders. It can be difficult, although not impossible,to qualify as a B corporation without incorporating in astate with a constituency statute.

Vegetarian

Finally, the vegetarian section of the menu offersnonprofit corporations that are tax exempt as organiza-tions described under either section 501(c)(3) or section501(c)(4). Section 501(c)(3) organizations can, of course,accept tax-deductible charitable contributions, and pub-licly supported 501(c)(3) organizations can accept privatefoundation money without the need for expenditureresponsibility. Section 501(c)(4) organizations, on theother hand, cannot accept tax-deductible contributionsbut have broader social welfare purposes that permitgreater political engagement and may conduct sometypes of social enterprise activities that are not consid-ered within the definition of section 501(c)(3). For entitiesthat do not plan to seek contributions or grants as part oftheir business model, a 501(c)(4) classification may makea great deal of sense.

Combinations

A classic combination platter would consist of a for-profit corporation coupled with a 501(c)(3) public charity.Some menus might also feature a low-calorie combina-tion platter that includes a 501(c)(3) public charity and a501(c)(4), or possibly even a 501(c)(3) private foundationcombined with a 501(c)(4) organization. While such com-binations are classically employed for tandem organiza-tions that have a lobbying arm and a charitable arm, theyare now being used more often to enable one entity toaccept charitable contributions and engage in educa-tional activities while its sister 501(c)(4) generates rev-enues from a social-welfare-style activity that might notqualify for 501(c)(3) status.

Most clients who talk about a hybrid structure, how-ever, are considering pairing a charitable organizationthat can receive grants and contributions and a for-profitthat can use investment capital to develop a product orservice and then provide that product or service to thecharity at a fair market value rate. As illustrated below,the two most complicated issues that typically arise in thehybrid model are (1) taking substantive and proceduralsteps to avoid any excess benefits, and (2) ensuring thatthe activities of the for-profit and the charity can besufficiently separated so that the activities of the businessare not attributed to the charity, thereby compromisingits tax-exempt status.

II. The Questions

With this menu in hand, how does one choose? Whenshould an enterprise consider more than one choice fromthe menu? Just as a good waiter or sommelier will ask theright questions to help the thoughtful diner make theright choice, the lawyer should make a series of inquiriesto help the social entrepreneur choose as well. Whatfollows are some of the key questions to explore with anew social enterprise client, and for a new client toconsider before speaking with the lawyer.

A lawyer who works primarily with for-profit entitiesmight be inclined to advise a new client to use a 501(c)(3)only when there is a need for charitable contributionsand grants. A lawyer who works primarily with tax-exempt entities might be inclined to look first to whethera 501(c)(3) or 501(c)(4) format might accommodate thebusiness plan, and only bring in a for-profit if the needfor private capital cannot be avoided. In contrast, thequestions that follow will assume that meat — thefor-profit option — is always on the menu, but thatvegetarian — the tax-exempt option — may or may notbe on the menu. Accordingly, the questions typically startby exploring whether a nonprofit, tax-exempt form iseven on the table. Even if the tax-exempt option isavailable, however, it is not necessarily the best choice.

1. May I see your business plan, please?

One of the most difficult situations for a lawyerinvolves the new client who has a vague idea of what heor she wants to accomplish, then comes to the lawyer tounderstand the law so that the legal considerations cangive initial shape to his or her business plan. Thisapproach is quite backwards. The client’s business plan— including a clear understanding of the goods orservices the client plans to provide, where the client plansto find capital, how the client plans to conduct opera-tions, how much control the founders expect, and con-siderations of the long-range view of the project —should come first. The lawyer should use legal constructsto shape the client’s idea. The client should not be usinglegal constructs, in the first instance, to create a businessplan based on what particular legal constructs permit.

For example, the social entrepreneur who comes inand says, ‘‘I have heard about the new L3C structure inVermont, and I want to come up with a business idea touse that new legal form,’’ is missing the point entirely, inmy view.

Special Report

The Exempt Organization Tax Review June 2009 — Vol. 63, No. 6 569

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

2. What is your fundamental program, activity,good, or service?

Almost all of my clients are tax-exempt organizations,yet I start from the premise that a for-profit structure isprobably more appropriate for most social enterprises.Nonetheless, a good waiter makes sure he fully under-stands the diner’s preferences before recommending adish. I want to know whether the client has the ability tostomach the vegetarian option, even if I might end uprecommending the meat. Accordingly, once the attorneyunderstands the core business plan, he or she shouldconsider whether the activity can qualify for tax-exemptstatus under section 501(c)(3) or 501(c)(4).

Resolving this question is usually a matter of under-standing the line of legal authority related to the specificactivity the client is proposing. When evaluating a par-ticular type of enterprise activity, it is rarely possible togeneralize based on section 501(c)(3). Each activity hasevolved its own line of authority. Let us consider sometypical examples of social enterprise activities that mightqualify for tax exemption:

A. Job Training

Many social enterprises have traditionally sought, andcontinue to seek, to operate some form of business thatemploys, and during the course of employment teachesjob skills to, a disadvantaged charitable class. Job trainingis a recognized tax-exempt activity. There are both well-known practical examples and IRS rulings on point.

We find examples of tax-exempt job training programsaround the country. In the San Francisco Bay area, wehave Delancey Street Foundation (http://www.Delanceystreetfoundation.org), which focuses on jobtraining for individuals who were previously incarcer-ated and often have drug and alcohol problems. JumaVentures (http://www.jumaventures.org) provides jobtraining to economically disadvantaged youth, and PedalRevolution, a social enterprise of New Door Ventures,helps at-risk youth learn how to develop job skills byworking in a bicycle repair shop (http://www.pedalrevolution.org). All are tax-exempt as organizations de-scribed under section 501(c)(3), and they are just three ofcountless examples from around the country.

What is the legal authority for a tax-exempt jobtraining venture? In Aid to Artisans, Inc. v. Commissioner,71 T.C. 202 (1978), the U.S. Tax Court considered theexemption of a charity that purchased and sold handi-crafts from disadvantaged craftspeople. The charity soldthe handicrafts to museums and other nonprofit shopsand agencies. The Tax Court found that the sale of theitems was related to the exempt purpose of the organi-zation, in part because the activity alleviated economicdeficiencies in communities of disadvantaged artisans. Asimilar conclusion was reached in Industrial Aid for theBlind v. Commissioner, 73 T.C. 96 (1979), in which thecorporation purchased products manufactured by blindindividuals and sold them to various purchasers.

In Rev. Rul. 73-128, 1973-1, the IRS determined that abusiness conducted for the primary purpose of providingskills training to the disadvantaged was operated forcharitable purposes. In Rev. Rul. 75-472, 1975-2 C.B. 208,a charity directly employed disadvantaged persons in its

business, which involved the production and sale offurniture made by residents of the corporation’s halfwayhouse for alcoholics.

These cases and rulings make clear that the benefits tobusinesses that obtained trained workers as a result of jobtraining programs are incidental to the primary chari-table and educational purposes of the social enterprise.The IRS agents reviewing exemption applications are, asa general rule, well acquainted with this line of authority,and we rarely encounter difficulty in obtaining exemp-tion for job training nonprofits.

B. Providing Technical Assistance

Some social enterprises seek to apply businessmethods to improve nonprofits’ operations by providingthem with technical assistance, such as managementconsulting, accounting, legal, and other services. Unlikethe job training area, it can be difficult to providetechnical assistance as a 501(c)(3) entity because there aremany for-profit entities and individuals who also consultwith exempt organizations for a fee. Accordingly, thetests for charitability are considerably more rigorous.

Many exempt organizations provide technical assis-tance as part of, or as their primary, exempt activity.CompassPoint Nonprofit Services (http://www.compasspoint.org) provides technical assistance to exemptorganizations in the San Francisco Bay area as one of itsmain exempt activities. Rockefeller Philanthropy Advi-sors (http://www.rockpa.org) is another example; it is anationally based organization that provides technicalassistance and donor services to wealthy families and toexempt organizations. Both organizations are supportedby grants and contributions as well as fees, and theyprovide other services besides technical assistance.

How are these and similar organizations exempt?Providing technical assistance to nonprofits is a recog-nized 501(c)(3) activity if the fees charged are substan-tially below cost. The IRS developed the ‘‘substantiallybelow cost’’ analysis in two revenue rulings. In Rev. Rul.71-529, an organization was formed to aid other charitiesby helping them manage their endowment or investmentfunds more effectively. The member organizations paidonly a nominal fee for those services; the organization’soperating expenses were primarily paid by grants fromindependent charitable organizations. The fees that theentity charged nonprofits for the services represented lessthan 15 percent of total costs of operation. The IRS foundthat the entity was exempt because it performed anessential function for charities at substantially below cost.

In Rev. Rul. 72-369, an organization provided mana-gerial and consulting services to charities to improve theadministration of their charitable programs. The organi-zation entered into agreements with unrelated charitiesto furnish the services on a cost basis. The IRS found thatproviding the services on a cost basis did not constitute acharitable activity, because the organization lacked thedonative element necessary to establish the activity ascharitable.

An important factor demonstrating that technicalservices are being offered at substantially below cost is toshow that the service provider raises funds from otherindependent charities or other donors, as in Rev. Rul.

Special Report

570 June 2009 — Vol. 63, No. 6 The Exempt Organization Tax Review

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

71-529, to subsidize the services. In effect, the serviceprovider is making a grant, in the form of donatedservices, to the service recipient, which must be a charity.

BSW Group, Inc. v. Commr., 70 T.C. 352 (1978), isperhaps still the leading case on this topic. In that case, anexempt organization provided consulting services to asmall number of organizations for a fee. The Tax Courtfound that even though the fee was below market, it wasabove cost and, therefore, was not sufficient to establishthe charitable nature of the provision of services. (Seealso private letter rulings 200036049, 200332046, and9414003, which cite BSW.) The IRS and the Tax Courtconfirmed this line of thinking in At Cost Services Inc. v.Commr., 80 TCM 573 (2000), in which the court held thatproviding job training and placement services for feesequal to cost was not considered to be a charitableactivity. (See also TAM 9232003, in which the IRS con-cluded that management for a fee equal to cost plus apercentage of management fee is not charitable.)

C. Producing Products for a Charitable Class

In recent years, particularly during the last 10, moreand more social enterprises have sought to develop andproduce products or services in a businesslike fashion,but then sell and distribute those products and services ata deep discount to the poor. Often the enterprises requirecharitable contributions and grants to capitalize opera-tions, but ultimately they can become barely self-sufficient. This type of social enterprise is quite prevalentin practice, but slowly evolving in legal definition. Prac-tical examples include the following organizations.

Kickstart International Inc. (http://www.kickstart.org) designs low-cost products for sale to help alleviatepoverty in developing countries. The Institute forOneWorld Health (http://www.oneworldhealth.org)helps develop new medicines to help the poor and workswith companies to help disseminate the medicines. Themission of Design That Matters (http://www.designthatmatters.org) is to create products that improvethe services of social enterprises in developing countries.

EnterpriseWorks VITA (http://www.enterpriseworks.org) also uses revenue-generating strategies to help alle-viate poverty. Design Revolution: Design for the Other90%, also known as D-Rev (http://www.d-rev.org), de-signs products at low cost to benefit the poor (the other90 percent) of the world for whom most products are notreally designed.

Despite the prevalence of those types of organizations,every exemption application that I have submitted for anorganization that seeks to produce products or developservices to benefit the poor has received several rounds ofIRS questions. Why? In my view, the IRS questions arenot at all out of line given the lack of authority in thisevolving area. IRS exemption application reviewers typi-cally have few concrete guidelines to help them whenevaluating this type of exemption application, and theycannot be blamed for being cautious.

What follows is an actual set of IRS questions on arecently approved exemption application, together withthe organization’s responses. The colloquy will helpillustrate the legal ambiguity in this area:

IRS: You explained your purposes and proposedoperations in your recent correspondence attempt-ing to justify why you engineer new products fromdesign to development with purposes to assistsmall farmers and help relieve poverty as a result ofyour products. . . . Your organization will holdpatents on designs, contract with one or more forprofit corporations to manufacture and produceproducts. Generally designing, development,patents for designs, productions and distributionsare purposes, operations and characteristics of a forprofit commercial entity, not a charitable nonprofitcorporation.[You state that your] organization is an incubatorthat brings about affordable income-generatingproducts and services to the point that they areready for full-scale dissemination through succes-sive stages of: (1) proof of concept prototype devel-opment and testing; (2) beta field tests; and (3) massdissemination. Your organization appears similar toorganizations in Revenue Rulings 68-373, 69-632,and 78-426 that were found not to be exemptbecause of commercial operations.

In Revenue Ruling 68-373, an organization wasengaged in the clinical testing of drugs for commer-cial pharmaceutical firms. Clinical testing benefitedcommercial firms and is ordinarily an incident of apharmaceutical company’s marketing operations.The organization was determined not tax exempt.

Similarly, in Revenue Ruling 78-426, an organiza-tion whose activities consisted of inspection, test-ing, and safety certification of cargo shipping con-tainers used in international and domestictransport and also conducted research, develop-ment, and reporting of information in the field ofcontainerization did not qualify for exemptionunder IRC 501(c)(3).

In Revenue Ruling 69-632, a non-profit associationcomposed of members of a particular industryformed to develop new and improved uses for theexisting products in the industry benefited its mem-bers rather than the public. The association’s re-search program enabled its members to increasetheir sales by creating new uses and markets fortheir products. The organization was held not toqualify for exemption under IRC 501(c)(3).

The Supreme Court of the United States held that abetter business bureau was not exclusively educa-tional or charitable. Its activities were in part aimedat promoting the prosperity of the business com-munity, even though there was also benefit to thepublic. This was a substantial private benefit thatprecluded exemption. Better Business Bureau ofWashington, D.C. Inc. v. United States, 326 U.S. 279(1945).

It was noted in your response you referencedGeneral Counsel Memorandum 37403. In thememorandum, it described a case that clearly in-volved a community which was impoverished,although the courts did not rely on this factor inreaching their conclusion on whether or not the

Special Report

The Exempt Organization Tax Review June 2009 — Vol. 63, No. 6 571

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

organization might otherwise qualify for exemp-tion under Code 501(c)(3). The fact that the com-munity was located in a poverty area may accountin large part for the governmental interest in help-ing it obtain a water supply, and clearly accountedfor the extent of financial assistance from the Fed-eral government. Although once the county gov-ernment became involved in such a project, in themanner and to the extent described above, theorganization qualified for exemption under Code501(c)(3) because it was lessening a burden of thatgovernment irrespective of the economic status ofthe residents of the community. It was noted thatthe exempt organization was noncommercial innature which is in contrast to your organizationthat is commercial in nature.

Charity: The Regulations provide that term ‘‘chari-table,’’ as used in Section 501(c)(3) in its generallyaccepted legal sense, can include activities thatmight also be described as educational, religious, orscientific. The term ‘‘charitable’’ includes: relief ofthe poor and distressed or of the underprivileged;advancement of religion; advancement of educa-tion or science; erection or maintenance of publicbuildings, monuments, or works; lessening of theburdens of government; and promotion of socialwelfare by organizations designed to accomplishany of the above purposes or (i) to lessen neighbor-hood tensions; (ii) to eliminate prejudice and dis-crimination; (iii) to defend human and civil rightssecured by law; or (iv) to combat communitydeterioration and juvenile delinquency.

The organization’s core mission is charitable. Therelief of poverty is a well-recognized charitablepurpose. The organization’s core activity is to de-sign products that are not being designed in thefor-profit sector, specifically to benefit the poor —those making less than $2 a day. The organizationseeks simple solutions to help alleviate poverty.

Designing products and services for the poor, whowould otherwise not be served, is a charitableactivity. These are not products that are designedfor the middle class or the wealthy. These are notproducts designed to help any industry. Thisorganization is NOT commercial in nature. It is notdesigning products in a way that looks to maximiz-ing profits or even making money at all. It islooking to design products that: (1) will help poorpeople and (2) can be sold at a very low price thatis affordable to the poor. A commercial companywould not work to incubate ideas and developproducts that are only sold at very low cost to thepoorest of the poor. We are talking about the sameindividuals who benefit from micro-finance loans— individuals making less than $2 a day.

The organization is also engaged in scientific re-search, in a manner consistent with the Regula-tions. The Regulations (1.501(c)(3)-1(d)(5)) provide:

. . . since an organization may meet the require-ments of section 501(c)(3) only if it serves a publicrather than a private interest, a scientific organiza-

tion must be organized and operated in the publicinterest. Therefore, the term scientific, as used insection 501(c)(3), includes the carrying on of scien-tific research in the public interest.

The Regulations tell us that scientific research willbe regarded as carried on in the public interestif . . . [quoting the Regs]

. . . The Regulations clarify that for purposes of thissubdivision, a patent, copyright, process, or for-mula shall be considered as made available to thepublic if such patent, copyright, process, or formulais made available to the public on a nondiscrimina-tory basis. In addition, although one person isgranted the exclusive right to the use of a patent,copyright, process, or formula, such patent, copy-right, process, or formula shall be considered asmade available to the public if the granting of suchexclusive right is the only practicable manner inwhich the patent, copyright, process, or formulacan be utilized to benefit the public.

The Organization’s research is clearly directed to-ward benefiting the public because the whole pointbehind the research is to alleviate poverty. In addi-tion, the Organization will make the results of all ofits research available to the public on a non-discriminatory basis. It will publish information onits website about all of its designs. It may, or maynot, choose to take out a patent on any particulardesign, but whether or not it takes out a patent, anycompany that wants to license the Organization’sscientific findings and designs will be afforded theopportunity to do so.

The rulings cited in the IRS inquiries all deal withentities that are designing commercial products,not intended for the poor, or that involve testingproducts for a for-profit company, at its direction.The Organization is not testing products that havebeen developed by another company; it creates itsown designs. The Organization is not designingproducts for any company, and The Organization isnot creating commercial products. The Rulingscited are simply inapplicable.

IRS cites Revenue Rulings 68-373, 69-632, and 78-426. In Rev. Rul. 68-373, the IRS ruled that anorganization set up to test drugs developed by apharmaceutical company was not exempt. The Or-ganization is not testing drugs developed by anycompany, nor is it even in the business of designingor testing drugs. However, the IRS has recognizedthat identifying and disseminating drugs to thepoor can be an exempt activity. See www.one-worldhealth.org. In Rev. Rul. 69-632, an organiza-tion was set up to evaluate products for a particularindustry. It did not do independent research. TheOrganization is not captive to any industry. It doesits own research and design based on the needs ofthe charitable class it serves — not the needs of anindustry. Rev. Rul. 78-426 deals with an organiza-tion testing ship cargo containers against federalsafety standards. This ruling bears no relationship

Special Report

572 June 2009 — Vol. 63, No. 6 The Exempt Organization Tax Review

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

to the Organization’s activities, which do not in-volve testing for public safety.

The IRS’s questions illustrate the agency’s difficultlyin approaching this area, absent clear authority, but theresponse ultimately satisfied the IRS reviewers, as itshould have.

E. Microfinance

There are both practical examples and a limited num-ber of rulings to support the tax-exempt nature of micro-finance lending. Microfinance is a social enterprise activ-ity because it involves applying a business model tolending small amounts of money to underserved popu-lations. Revenue is generated from interest, and loans canbe recycled, potentially creating a self-sustainable entity.

Kiva (http://www.kiva.org) is a 501(c)(3) charity thatfacilitates and promotes microfinance loans. Its Web sitedefines microfinance as ‘‘the supply of loans, savings,and other basic financial services to the poor’’ (citing theConsultative Group to Assist the Poor (http://www.CGAP.org)). Kiva notes further that ‘‘as the finan-cial services of microfinance usually involve smallamounts of money — small loans, small savings etc. —the term ‘microfinance’ helps to differentiate theseservices from those which formal banks provide.’’ Micro-finance loans tend to be in the $500 to $5,000 range, andthey are typically made by a microfinance institution(MFI). An MFI can be a bank or a for-profit organizationor a nonprofit entity. Kiva.org also notes that ‘‘the WorldBank estimates that there are now over 7,000 microfi-nance institutions, serving some 16 million poor peoplein developing countries. The total cash turnover of MFIsworld-wide is estimated at US $2.5 billion and thepotential for new growth is outstanding.’’ GrameenFoundation (http://www.grameenfoundation.org), af-filiated with Grameen Bank, which largely pioneered thisarea of social enterprise, and MicroCredit Enterprises(http://www.mcenterprises.org) are also examples of501(c)(3) entities that loan money to MFIs.

Despite the prevalence of MFIs and the clear charitablenature of MFI loans, new IRS applications for organiza-tions that intend to lend to MFIs or directly to the poorcontinue to receive a great deal of scrutiny. Why? Thearea of microfinance lending is relatively new, and evolv-ing, and the IRS reviewers do not have appropriateguidance, in the form of checksheets or otherwise, whenreviewing microfinance exemption applications. In arecent question, for example, a reviewer asked how anapplicant could be said to be engaged in microfinancelending when it intended to lend money to microfinanceinstitutions and not directly to the poor. We explainedthat it is not always efficient for a U.S. charity to lendmoney to individuals in another country on a person-by-person basis when there is an established MFI in thatcountry to which the U.S. can lend money and the MFIwill be able to do a better job.

What, then, is the legal authority for the charitabilityof microfinance lending? One of the most establishedcharitable purposes under section 501(c)(3) is the ‘‘reliefof the poor and distressed or the underprivileged.’’ Seereg. section 1.501(c)(3)-1(d)(2). In Rev. Rul. 74-587, 1974-2C.B. 162, for example, the IRS approved as charitable an

organization whose mission was to stimulate economicdevelopment in ‘‘high density urban areas inhabited bylow-income minority or other disadvantaged groups.’’These areas lacked capital for development and sufferedfrom a depressed economy. The IRS noted that localbusiness owners had ‘‘limited entrepreneurial skills.’’The charity sought to improve the area by providinglow-cost loans to local businesses.

The IRS also has approved loan programs to for-profitbusinesses engaged in microfinance lending as properPRIs. In LTR 200325005, the IRS ruled that an equityinvestment in foreign microfinance banks served a validcharitable purpose under section 501(c)(3). The banksused capital contributions to provide unsecured microen-terprise loans to the poor. The grantor made capitalcontributions to the banks and monitored their povertyfocus through regular reports. The IRS ruled that theinvestments differed from a typical capital venture, be-cause the banks were involved in financing microloansand providing savings services to the poor and under-served.

In LTR 200034037, a foundation proposed to make aseries of below-market-rate loans to media businesses inCentral and Eastern Europe, Latin America, SoutheastAsia, and Africa to ensure their autonomy from localgovernments. The IRS found that the loan programaccomplished a charitable purpose because it was in-tended to promote the development of independent,nonpartisan media in some regions of the world andbecause the foundation would make loans only to thosethat were not able to obtain funds through commercialsources.

Although each situation needs to be reviewed on itsmerits, there is ample precedent to show that the IRSrecognizes the relief of poverty through microfinance as acharitable activity.

Whether the business plan calls for job training, tech-nical assistance, producing products or services for thepoor, microfinance, or some other form of social enter-prise, after we have determined whether the activity canfit within a 501(c)(3), we continue the inquiry.

3. If all of the activities cannot qualify forexempt status, can the core activities bebifurcated into those that could qualify for taxexemption and those that cannot, or are theytoo closely linked?

The question surfaces whether a nonprofit/for-profithybrid might be appropriate. Again, just because part ofthe activity could qualify for exemption as charitabledoes not mean that a charitable vehicle is appropriate,but this fundamental analysis is necessary to determineexactly what is on the menu tonight.

Many of my clients over the last few years haveindicated an interest, for example, in forming a nonprofit,exempt entity to ‘‘own’’ a Web site that provides educa-tional content, and then to form a for-profit entity thatwill ‘‘manage’’ the Web site and also attract advertisingfor it. In this type of situation, the question is whetherthese two activities are too closely linked to separate intodifferent legal entities.

Special Report

The Exempt Organization Tax Review June 2009 — Vol. 63, No. 6 573

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

A second common scenario involves an entity thatseeks to form a nonprofit, tax-exempt job training entityto help a charitable class, such as the homeless, learn jobskills in the process of operating a business. At the sametime, the social entrepreneur also wants to form a for-profit business in the same line of work to provide a placefor graduates of the nonprofit and others in the commu-nity to be employed on a long-term basis, after the jobtraining is completed. Can these two activities be reason-ably separated into two entities?

A third example involves a design think tank dedi-cated to creating low-cost products for the poor. Thisentity, however, also decides to form a for-profit com-pany to sell the products that it designs. Why? Theconcern was that if the tax-exempt entity developedproducts to benefit the poorest of the poor, no establishedmanufacturing or distribution firm would be willing totake the risk of making or selling these products. Until itcan be proved that making products to help the poor canbe at least self-sustaining, if not marginally profitable,this client perceived the need to form a for-profit com-pany to make and sell some of the products that thenonprofit designed. Of course, the products would beopen for any for-profit to make and sell, but if nonewould do so, the related for-profit could at least begin theprocess and help prove sustainability.

Without more facts, I would initially surmise that theWeb site activity will be harder to separate out than thejob training activity or the product development and saleactivity, but there are examples of Web-site-based activi-ties that have successfully used a for-profit and a non-profit counterpart. One has to look no further than eBayand its nonprofit collaborator MissionFish.

4. Where do you expect to find your capital?

It clearly makes sense to set up a nonprofit entity if thebusiness model requires grants and contributions or ifthe nonprofit status will open up access to capital thatmight not be available to a for-profit business. This isperhaps the most important question when determiningwhat type of entity to form. Clearly, if an enterpriseexpects to receive most of its funding from individualdonors and foundation grants, it should seriously con-sider forming as a section 501(c)(3) entity, if legallypossible. If all of its activities cannot qualify for exemp-tion, it must consider a hybrid structure so that it can stillaccept charitable contributions to fund qualifying activi-ties.

If an enterprise expects to receive a significant part ofits capital from investors, it has no choice but to establisha for-profit entity. Whether such an entity is a corporationor an LLC will depend on other factors that are beyondthe scope of the discussion.

A hybrid structure that pairs a taxable entity with atax-exempt entity sounds ideal because the founders canattract both charitable contributions and grants, as wellas equity investments. As described above, however, careis required to ensure that the grants and contributedfunds only go to support activities that would otherwisequalify for exemption and are not funneled directly tosupport the activities that are for profit. Depending on

the type of activity, it might be easier or more difficult toseparate the different functions.

A 501(c)(4) entity might be appropriate when a singlecorporate founder or a small group of founders arewilling to forgo the tax deduction that comes with501(c)(3) status in return for greater flexibility as toactivities available to 501(c)(4) organizations. For ex-ample, salesforce.com recently established and receivedtax-exempt status for a section 501(c)(4) entity that willhelp distribute its salesforce.com Internet application tocharities in the U.S. and nongovernmental organizationsabroad. The 501(c)(4) offers many of the applicationlicenses for free, typically up to 10 per entity, while othersabove 10 are sold. Because the initial capital and thelicenses come from a single company and because theentity will not seek charitable contributions, section501(c)(4) status was deemed more appropriate.

5. What personal benefit, if any, do the founderswant or need to derive from this activity?

If the founders expect anything other than a reason-able salary for their services at a level that would passmuster under section 4958, they should consider a for-profit alternative. Some founders will expect a share ofprofits, and others will expect to be able to sell theirinterests later, neither of which works within a tax-exempt entity.

The section 4958 analysis can become exceedinglycomplex with a hybrid entity because, depending on therelationships between the two entities, the IRS mayconsider the salary or other benefits paid by both entitiesto be compensation subject to section 4958 analysis.

For a for-profit and an exempt entity to functionpermissibly within the confines of section 4958, it willalmost always be necessary for the exempt entity to havea board of directors with a majority of individuals whoare not involved with the for-profit. That board will needto follow the section 4958 procedures carefully to obtainthe benefit of the rebuttable presumption of reasonable-ness under the section 4958 regulations. Also, the exemptentity should maintain and follow solidly drafted poli-cies on conflicts of interest and disclosure. Any contractsbetween the exempt and for-profit entities should benegotiated in such a manner that the exempt entity doesnot become the captive of the for-profit. For example, theexempt entity may need to put the contract out for bid toat least solicit offers from unrelated for-profit providers.

6. How important is control to the founders, inthe short and long term?

Investors typically want a good deal of control, butabsent investors, it is quite possible to provide forfounder control in both a nonprofit and a for-profit form.If an exempt entity is involved, however, it is essential toconsider good governance practices, particularly in lightof the questions that the organization will now need toanswer in connection with parts IV, V, and VI of the newIRS Form 990. Conflicts policies, compensation approvalprocedures, and having a majority of disinterested boardmembers are probably now par for the course, at least ina 501(c)(3) public charity.

Special Report

574 June 2009 — Vol. 63, No. 6 The Exempt Organization Tax Review

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

7. What are the perceived branding issues?Sometimes, wholly apart from tax, corporate, and

other legal issues, a client perceives that being a nonprofitis essential to the success of the enterprise. We sometimesrefer to this phenomenon as the ‘‘halo effect.’’ This mayor may not be a well-considered notion, and it is worthexploring further with the client. Usually this concern islinked to the question of where the client expects toreceive funding. Exempt entities and individual donorsmotivated largely by tax deductions or by the validity ofthe cause may be disinclined to donate to or invest in afor-profit. On the other hand, venture capitalists andtraditional investors may be disinclined to work with anexempt entity or even a taxable nonprofit entity. In thatcase, the client should also consider the perceived brand-ing advantages of being formed as an L3C. Some thinkusing the B corporation model will attract particularinvestors and will also provide networking and market-ing opportunities to an entity that might not otherwise beavailable. Accordingly, if being a nonprofit entity is toomuch for a client to stomach, forming an L3C or acorporation that becomes certified as a B corporation maybe the answer.

III. The Advice

At long last it comes time to order from the menu. So,what is the best legal structure for a particular socialenterprise? Often the client seeks to implement the mostcomplicated scheme imaginable on the theory that com-plicated means sophisticated, innovative, entrepreneur-ial, and therefore better. In truth, as with cooking, com-plexity for complexity’s sake is foolish. Rather, thefollowing simple analysis should provide a practicalframework for selecting the right entity or combinationof entities.

A. Reasons to avoid the exempt organization struc-ture. The social enterprise should avoid forming anexempt organization in at least the following situations:

• No part of the proposed activities would qualify forexemption. In this case the exempt, vegetarian op-tion is off the table.

• All of the capital will be coming from investors,rather than from grants and contributions. In thiscase, there is probably no need for an exempt entityand the additional regulations that necessarily at-tach to it.

• The founders will devote significant personalenergy to the business and want to have somethingto build and sell for profit later in their careers. Anindividual cannot profit from the sale of an exemptentity or its assets.

If any of those reasons applies, the enterprise shouldselect solely from the meat or low-fat meat portion of themenu.

B. Deciding between the meat and low-fat meatoptions. Almost any social enterprise can be legallystructured as a for-profit corporation or LLC. The enter-prise should consider the L3C or B corporation status asfollows:

• Consider the L3C option if the organization hopes toobtain significant capital or loans from private foun-dations.

• Consider B corporation status when the organiza-tion will seek to attract investors who might bedrawn by more than the prospect of financial re-turns. Some investors may be truly drawn to acorporation that expresses a commitment to betterlabor practices, better environmental practices,and/or engages in more charitable activity than atypical for-profit corporation. When the corporateform is preferred, B corporation status also mayhelp attract private foundation investments.

C. Reasons to create an exempt entity. Even thoughmost social enterprises will find the meat and low-fatmeat sections more to their liking, there are clear situa-tions in which it makes sense to use an exempt entity,particularly a section 501(c)(3) entity. Assuming that wehave determined that the activity can qualify undersection 501(c)(3), the reasons include the following:

• Grants and charitable contributions are a majorcomponent of the initial capital and, possibly, offunding ongoing operations. Obtaining donations isthe main reason to consider a tax-exempt entity.

• The business model will not succeed if the organi-zation must pay taxes on its net income. This reasonwill rarely be compelling in a properly designedbusiness model.

• Potential collaborators, like government agencies,will only work with an exempt entity. For example,some student exchange organizations traditionallyhave formed as exempt entities because they mustbe exempt to contract with USAID.

D. Reasons to apply for exemption as a section501(c)(4) entity. Normally, when an organization needsdeductible contributions or requires grants, 501(c)(3)status is optimal. Section 501(c)(4) status may makesense, however, when all of the funding is coming from asingle corporation or from a single donor who, forwhatever reasons, cannot take advantage of the chari-table contribution deduction and when no outside inves-tors are needed. Also, 501(c)(4) is useful if the entitywants to engage in significant lobbying or candidate-related activities.

E. Reasons to form an exempt and for-profit combi-nation. Entrepreneurs do not always want to focus onformal boundaries and rules, but to work with a hybridentity, it is imperative to do so. A for-profit combinedwith an exempt entity to carry out a social enterprisemakes sense as follows:

• when only a portion of the activity can qualify forexemption;

• when capital is required both in the form of privateinvestment and from grants and contributions; and

• when the founders want to build a business to sell,but also are willing to dedicate some portion of theenterprise to charity in perpetuity.

Whenever an enterprise considers a hybrid structure,it must, at a minimum:

• be prepared to delineate clearly the activity that willrest in the exempt versus for-profit structure; theremust be a logical and practical way to divide theactivities;

• be cognizant of, and be prepared to comply with theprocedures to avoid, intermediate sanctions under

Special Report

The Exempt Organization Tax Review June 2009 — Vol. 63, No. 6 575

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

section 4958; the enterprise must develop and fol-low clear conflict of interest policies and disclosefinancial interests to the disinterested members ofthe nonprofit board of directors;

• give up legal control of the exempt entity to thosewho will not benefit financially from the for-profitbusiness; the disinterested members of the tax-exempt board need to be individuals who willunderstand their independent fiduciary duty andnot simply rubber-stamp the decisions of the for-profit founders; and

• ensure that the private investors, particularly anyventure capitalists, understand that they do notcontrol, and cannot control or benefit from, theexempt side of the enterprise.

Conclusion

In the end, the new social enterprise needs to select theright restaurant and the right server, study the menucarefully, and order wisely. For those who dare to do this— bon appétit!

❖ ❖ ❖

Special Report

576 June 2009 — Vol. 63, No. 6 The Exempt Organization Tax Review

(C) T

ax Analysts 2009. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.