Embed Size (px)

Citation preview

1

Education Investment in China and its Implications

for China and East Asia

Peter E. Robertson University of New South Wales

Jessica Y. Xu*

University of New South Wales

3 December 2008

Abstract

What are the implications of China’s rapid development for East Asia? A number of studies have emphasised the competitive effects of China’s low skill-intensive manufacturing sector on East Asian exports. China, however, has recently embarked on a large scale investment in higher education with the aim of addressing skill shortages and the problem of growing wage inequality. This paper provides an analytical perspective on the implications of this policy for China and the East Asian economies. Using a computable multi-sector growth model of China and East Asia, we find that the planned spending on tertiary education generates a long run increase in skilled labour of 33 percent and a strong decline in wage inequality. Nevertheless, we find that in the short run, adjustment costs rise – due to constraints on resources for on-the-job training – wage inequality rises and income falls. The education plan also has significant effects on the structure of trade for China and East Asia, with a shift of East Asia’s exports towards less skill-intensive sectors. However, the aggregate effects on East Asia are small and the adjustment in trade patterns is gradual and involves an expansion of agricultural and low-tech manufacturing exports, with only minimal adjustments for other sectors.

Keywords Human Capital, Economic Growth, China, Computable General Equilibrium

Models

JEL: F11, J24, C68, O10

______________________

*Corresponding author: Jessica Xu, The Treasury, Langton Crescent, PARKES ACT 2600.

Email: [email protected]. Phone: (02) 6263 3748.

2

1. Introduction

In the Tenth Five-Year Plan, covering the period 2001 to 2005, the Chinese government

set a target to have 16 million students enrolled in tertiary institutions. That goal was

surpassed in 2004 with 18.9 million students.1 The current Eleventh Five-Year Plan sets

an even more ambitious target for China’s education sector with an aim to increase

government spending on education from the 1995 level of 2.4 percent of GDP to 4

percent of GDP. This represents not only a very large increase in total education spending

in China but also a significant change in the world endowment of skilled labour (Freeman,

2005; Li et al., 2008).

The projected expansion in China’s supply of skilled labour raises a host of issues

regarding the effect on China and China’s trading partners. The aim of this paper is to

evaluate the impact of this potential change in China’s skilled labour endowment on

China and its East Asian neighbours. The focus on East Asia is germane given what Lall

and Albaladejo (2004) describe as a “heightened fear of competition from China” among

the East Asian countries. Likewise, the growing literature on the effects of China’s

growth on East Asia is reflective of the intense interest in this issue. This includes, for

example, Weiss and Shanwen (2003), Lall and Albaladejo (2004), Roland-Holst and

Weiss (2004), Ravenhill (2006) and Coxhead (2007).

Whereas the recent literature focuses on China’s rapid export expansion on East Asia,

and especially on the manufactured export sectors of low wage Asian economies, the

planned up-skilling of the labour force in China is now raising protectionist sentiments in

the more industrialised economies such as South Korea (The Economist, 2008). In

addition, it may frustrate middle income countries, such as Indonesia, where policy

advice has been to avoid competition with China by investing in skills themselves

(Coxhead and Li, 2008).

1 This number includes students from regular higher education institutions, adult higher education

institutions and private institutions.

3

The implications of China’s education plan for East Asia are not obvious. On one hand,

skill-intensive industries may lose comparative advantage to resource or low skill-

intensive sectors. On the other hand, the rising endowment of skilled labour in China may

create greater trade opportunities with China, for example through increased

opportunities for specialization and trade in intermediate goods. Furthermore, given the

large mass of unskilled labour in China, it is not clear whether even this ambitious

planning response will have a significant impact on the composition of China’s labour

force or trade patterns.

To bring some quantitative perspective on these issues we consider the impact of the

expansion of tertiary education plan on China and its implications for East Asia using a

multi-sector, multi-region growth model. The model features optimal education

investment decisions and human capital dynamics allowing us to consider not only how

agents’ education decisions respond to the new government incentives in China but also

how they respond in East Asia through changes in international trade.

We find that the increase in tertiary education investment in China, as implied by the

Eleventh Five-Year Plan, generates a 33 percent increase in skilled labour in the long run

and causes a strong decline in wage inequality. Although the reduction in inequality

fulfils one of the stated objectives of the plan, there is also a substantial short term rise in

wage inequality as demand for skilled labour and adjustment costs rise.

The education plan shifts the structure of China’s production towards skill-intensive

sectors such as durables and traded services. The impact on East Asia is very small at the

aggregate level but significant changes are observed in the composition and direction of

East Asia’s trade, these changes are found to be quite gradual.

2. Background

2.1 Enrolments of Students and Supply of Skilled Labour

The legacy of the Cultural Revolution meant that, by the mid 1980s, the proportion of

skilled labour in China was well below other countries with similar income levels. During

the Cultural Revolution, from 1966 to 1976, higher education in China was essentially

4

stopped (Tsang, 2000; Chow, 2002). The national examination system for admissions

was ceased. Regular admissions of undergraduates stopped for six years and graduate

admissions also ceased for 12 years from 1966. In 1971, a quarter of the higher education

institutions were closed and the educational managers were removed from their positions

(Tsang, 2000; Hannum et al., 2007; Zhang, 2006). With students being sent to rural areas

for re-education there was also a large misallocation of skills (Hannum et al., 2007).

Deng and Treiman (1997) show that the Cultural Revolution severely depleted the stock

of educated labour in China. Since the early 1980s, enrolment rates have risen - and this

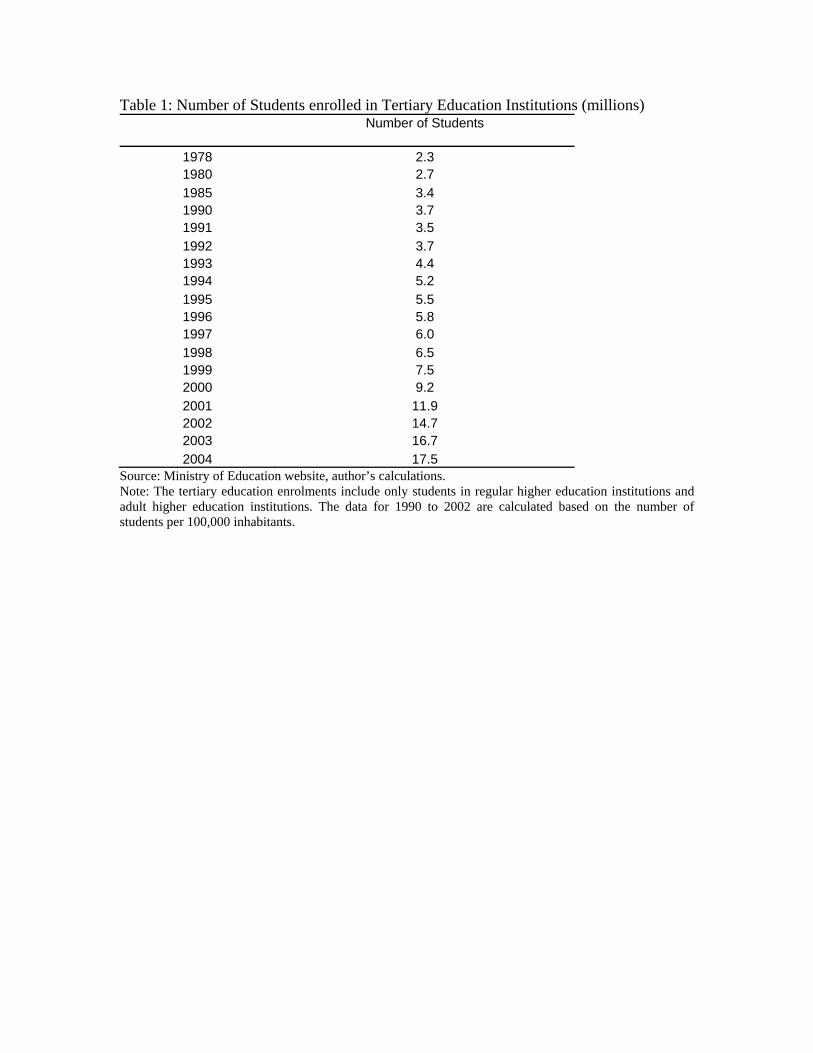

trend has accelerated in the last decade. Table 1 shows that the absolute number of

students enrolled in tertiary institutions has increased steadily since the end of the

Cultural Revolution until the late 1990s when the current education boom began. 2

Between 1997 and 2001, the number of tertiary students increased by 98 percent. The

tertiary gross enrolment ratio, which was merely 1 percent in 1985 and 3 percent in 1991,

soared to 19 percent in 2004.

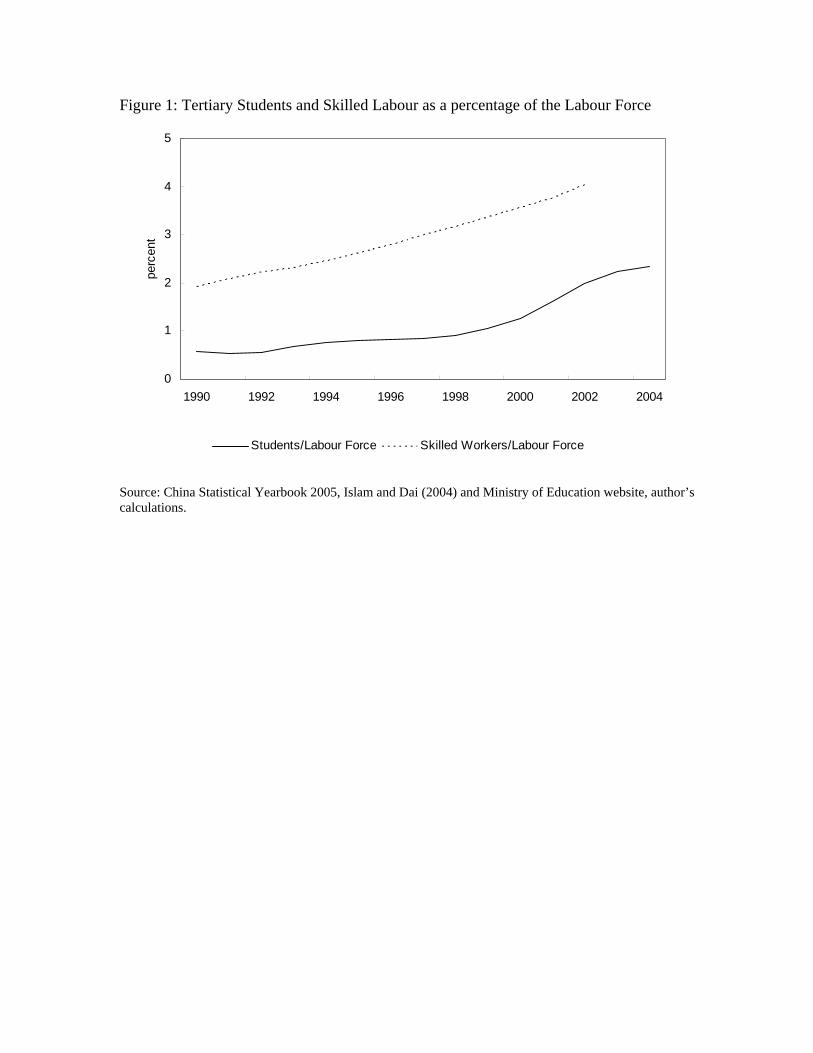

Likewise, as shown in Figure 1, the ratio of tertiary students relative to the labour force

has also grown very rapidly - from 0.6 percent in 1990 to 2.3 percent in 2004.

Consequently, the proportion of skilled labour to the total labour force has risen from 1.9

percent in 1990 to 3.6 percent in 2002.

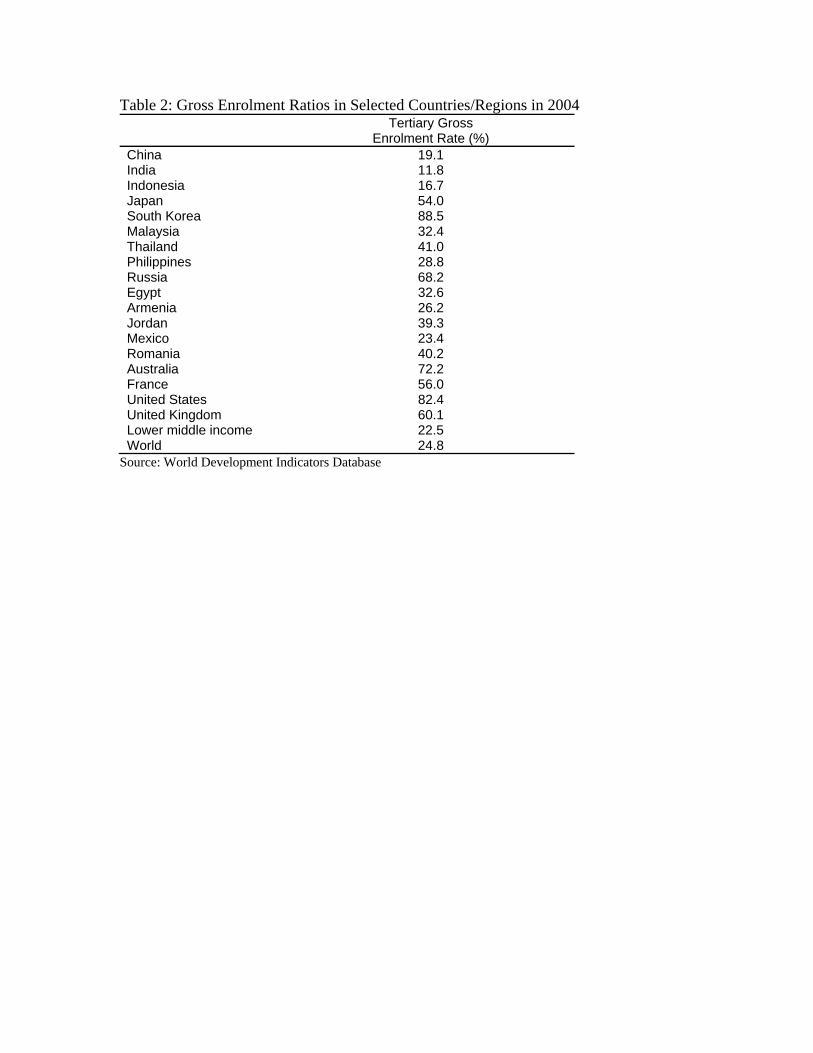

However, China’s tertiary gross enrolment rate of 19.1 percent in 2004 remains below the

world average of 24.8 percent. Table 2 shows this enrolment ratio is considerably lower

than most of its Asian neighbours and even lower than that of countries with a lower

income per capita such as Jordan (39.3 percent), Egypt (32.6 percent) and Armenia (26.2

2 The enrolments refer to students in regular higher education institutions and adult higher education

institutions.

5

percent). 3 This suggests that, in relative terms, the education plan is an accelerated

programme of catch-up to “normal” levels.

2.2 Reforms to Promote Higher Education

The rise in the enrolment rate reflects the effects of several stages of reform in the

education sector and in the labour market. A programme to implement nine years of

compulsory education was introduced in 1985. In 1999, a second reform programme, the

“Action Plan for Revitalizing Education in the 21st Century” was carried out. This set a

target on the tertiary enrolment rate (to raise the enrolment rate from 9 to 15 percent) with

the objective of providing greater access to higher education. According to Tsang (2000),

the motivation for such a large increase was that skill shortage was adversely affecting

economic growth in China. Chaudhuri and Ravillion (2007) note that skill shortage is due

to the failure in the delivery of education services and thus has led to a substantial rise in

wage inequality in China.

To supplement the expansion in public higher education, the government permitted social

organisations and private citizens to operate and finance private higher education

institutions, known as “minban” institutions. 4 The private institutions of higher education

were made possible and legally established by a succession of legislations in the 1990s.

3 For tertiary education, the gross enrolment rate is defined as the ratio of the total enrolment in higher

education to the population aged 18 to 24. National income is measured in terms per capita, purchasing

power parity from the World Development Indicators Database.

4 There are currently two types of higher education institutions in China, regular public institutions and

other institutions. The regular institutions of higher education are educational establishments that enrol

graduates straight from senior secondary schools and offer higher education training and programs. The

other institutions include both adult public higher education institutions and private institutions. The

institutions of higher education for adults refer to the establishments that usually enrol students who are in

the labour force and provide higher education courses in several forms whether full time, part time or

distance learning (Zhang, 2006). Students trained in these institutions receive a qualification equivalent to

students studying at the regular higher institutions. Privately-run tertiary institutions are a new phenomenon

and growing sector, established to support higher education development in China.

6

A new law in 2002 gave private institutions the same legal status as public institutions

and guarantees their autonomy. In 2004, private institutions numbered 226 and enrolled

1.4 million students (Zhang, 2006; Min, 2005).

The increases in education spending have been procured through non-budgetary sources

such as tuition and fees. Until 1990, universities did not charge students tuition (Zhang,

2006). After 1990, reforms in the financing of higher education meant that universities

were able to charge tuition and fees. The fees grew from 4.4 percent of educational

expenditures in 1991 to 18.6 percent in 2004 (Min, 2005; Hannum et al., 2007). Student

loan and scholarship programmes were launched by the government at the same time to

support students from low income families (Zhang, 2006).

Reforms in the labour market have also complemented the liberalisation policy in higher

education. Historically, the wage policy in China forced a low rate of return to skilled

labour and there are still distortions on the wage setting in the labour markets (Heckman,

2005). From the initiation of economic reform in 1978 to the early 1990s, wage

differences by level of schooling were very narrow. Fleisher and Wang (2004) and

Fleisher et al. (2006) suggest that these wage differences understate the return to

education by 30 to 40 percent.

The low rate of return for skilled workers is likely to have a negative effect on

individuals’ incentives to invest in education. Indeed prior to the mid 1990s, university

graduates were assigned jobs upon graduation by the government (Min, 2005). With the

gradual transition of China from a centrally planned to a market economy, the

occupational prospects and the wage structure of the graduates and skilled workers are

increasingly shaped by the labour market and recent evidence suggests that the return to

education has been rising.5

5 Chen et al. (2004) estimate that the return to tertiary education had reached 8.23 percent in 1996.

Heckman and Li (2004) use Chinese micro data to identify the return to college education and find that the

rate of return has risen to 11 percent in 2000.

7

2.3 Government Expenditure and the Eleventh Five-Year Plan

Having achieved a large degree of deregulation in the education sector in the Tenth Five-

Year Plan, the current Eleventh Five-Year Plan aims to provide the tertiary education

sector with a large injection of public funds. China’s aggregate expenditure as a

percentage of GDP grew from 3.4 percent in 1991 to 5.3 percent in 2004 as shown in

Figure 2. Of this, public spending on overall education was 2.4 percent of GDP in the

mid 1990s. As a result of the increased non-government funding in education, as

described above and by Hannum et al. (2007), the proportion of funds for education

coming from government has fallen from 85 percent in 1991 to 62 percent in 2004. This

can be seen in Figure 2 with the government spending on education relative to GDP

remaining at about 3 percent in 2004.

The Eleventh Five-Year Plan sets an explicit target to raise the public education

expenditure as a proportion of GDP to 4 percent. This represents a 66 percent increase in

public spending over the 2.4 percent level in the mid 1990s. Data from the 1990s suggest

that higher education accounts for approximately 20 percent of all education funding,

both private and public sources. The Eleventh Five-Year Plan, however, stipulates

priorities for universities and research, which suggests that the target for tertiary

education spending will be at least as ambitious, if not more so, as the target for

aggregate education spending.

3. The Model

3.1 Structure

The model used in this paper is a multi-sector, multi-region growth model developed by

Harris and Robertson (2007, 2008). The model focuses on the real side of the economy

with substantial details on sectoral output, trade flows, factor supplies and accumulation,

including human capital accumulation. In this paper we have adapted the Harris and

Robertson model (2007, 2008) to a model of China, East Asia and the Rest of the World

(ROW). The East Asian region is an aggregate of Japan and the four Asian Newly

8

Industrialised Economies of Hong Kong, Singapore, South Korea and Taiwan. The ROW

is an aggregate of all other regions.

In this section we provide a brief overview of the model’s structure.6 East Asia and China

are modelled as small open economies facing exogenous world prices. The ROW

supplies and purchases the traded commodities. Within each region, commodities are

homogenous in use irrespective of their origins but on the production side the

commodities are distinguished by market destination. The model resembles a traditional

Heckscher-Ohlin model with homogenous goods as opposed to the common Armington

assumption of differentiated good by import source.

The gross outputs of the firms are classified into eleven traded and non-traded goods.

The five non-traded goods are produced for the domestic market only. For the six traded

goods, the output is the aggregation of the three destination specific goods, one for the

home market and the other two for the foreign markets. Firms maximise revenue by

producing the optimal mix of destination specific goods. The revenue functions are

assumed to be constant elasticity of transformation functions of the prices in each market.

The seven factors of production are: the three reproducible physical capital goods

(machinery and equipment, structures, and residential housing); skilled labour; unskilled

labour; land and; natural resources. The firms’ value added technologies are specified as

nested constant elasticity of substitution unit cost functions allowing for capital-skill

complementarity. Physical capital and labour are mobile across sectors but immobile

across regions. Labour is distinguished between skilled and unskilled labour depending

on the educational level of the workers. A skilled worker possesses a tertiary degree or

comparable post-secondary qualification. To account for the differences in labour

productivity between the East Asian economies and China, labour is measured in terms of

efficiency units.

6 An appendix containing a detailed description of the model is available online at

http://www.economics.unsw.edu.au/PeterRobertson

9

The education sector transforms unskilled workers into skilled workers. The relative

supply of skilled and unskilled labour is endogenous to the model and is based on

households’ decision to invest in education with respect to the cost of the education and

the forward looking view on the return to becoming skilled. There are costs involved in

making the skilled labour useful once available; these costs can be viewed as job

matching and on-the-job training costs. Households choose the optimal current and

planned future level of schooling subject to Mincerian on-the-job training costs and a

labour time constraint, to maximise the present value of their total skilled and unskilled

labour income.7 Therefore, the costs of producing skilled labour include foregone income

from unskilled labour, training and costs of purchasing education services. The on-the-

job training costs are similar to adjustment or installation costs in the standard

neoclassical model of investment. A larger flow of graduates entering the labour force,

relative to the steady state flow, will use up unskilled labour resources.

Households own the physical capital and derive the demand for investment on these

assets to maximise the present value of the capital rental steams. The accumulation

pattern of physical capital is influenced by the endogenously determined prices of capital,

the depreciation rate and the capital adjustment costs. The adjustment costs are the units

of capital used in the installation and utilisation of the capital. The two remaining factors,

land and natural resources evolve exogenously.

An equilibrium in the model is a sequence of static competitive equilibria which satisfy

zero profits in all sectors, factor market clearing in all regions and commodity market

clearing in the world economy and the perfect foresight paths for investment, education

and consumption plans. For the education and investment plans, the perfect foresight path

of the economy is a time path of asset prices consistent with the first order conditions for

the households’ investment and education decisions, which reaches the steady state

solution in the limit as time approached infinity. In practice this is approximated by

7 See Mincer (1962) for a discussion of training costs and Mincer (1994) for some evidence on the size of

these costs.

10

requiring the path to reach the steady state after a long but finite period, usually in excess

of 100 years.8

3.2 Calibration

In assembling the benchmark data, the main data source is the GTAP database

(Dimaranan, 2006). A considerable amount of additional data was supplemented from

other sources. The GTAP dataset was re-aggregated in such a way to be consistent with

the regional and sectoral classifications used in this study. The model was calibrated to

the year 1995 as the benchmark and the initial steady state condition. The database

includes labour by skill level, as described in Liu et al. (1998) and this occupational

classification broadly corresponds with our concept of a skilled worker, as someone who

has completed a degree in higher education.

The original commodity sectors in the GTAP database are aggregated into 10 sectors

with 6 homogenous traded commodities and 4 homogenous non-traded commodities. The

traded service sector is treated differently from the other traded sectors as it consists of

both domestically supplied and imported business and recreation services and a

proportion of the public, trade, transport and utility services which is tradeable. For the

education sector, the data on the intermediate input purchase and the value added shares

for the sector was obtained separately from the Japanese and Chinese Input-Output (I-O)

tables. The data on education for Japan is used to represent the values for the East Asian

region.

The GTAP data was scaled using the Penn World Tables (PWT) version 6.2 such that the

income in each region is expressed in terms of purchasing power parity. The national

aggregate expenditure shares are derived from PWT augmented with each country’s

respective statistical yearbook for China and Japan but for the rest of the East Asian

economies, the data was gathered from the Asian Development Bank Key Indicators.

The data on capital from GTAP is disaggregated into 3 capital stocks of machinery and

8 The model is solved using numerical methods described in Wilcoxen (1988).

11

equipment, structures and residential housing. The value added flows for the sectors are

reconciled with the investment spending for the physical capital.9 The trade flows data

was adjusted to ensure a hypothetical equilibrium steady state with balanced trade.

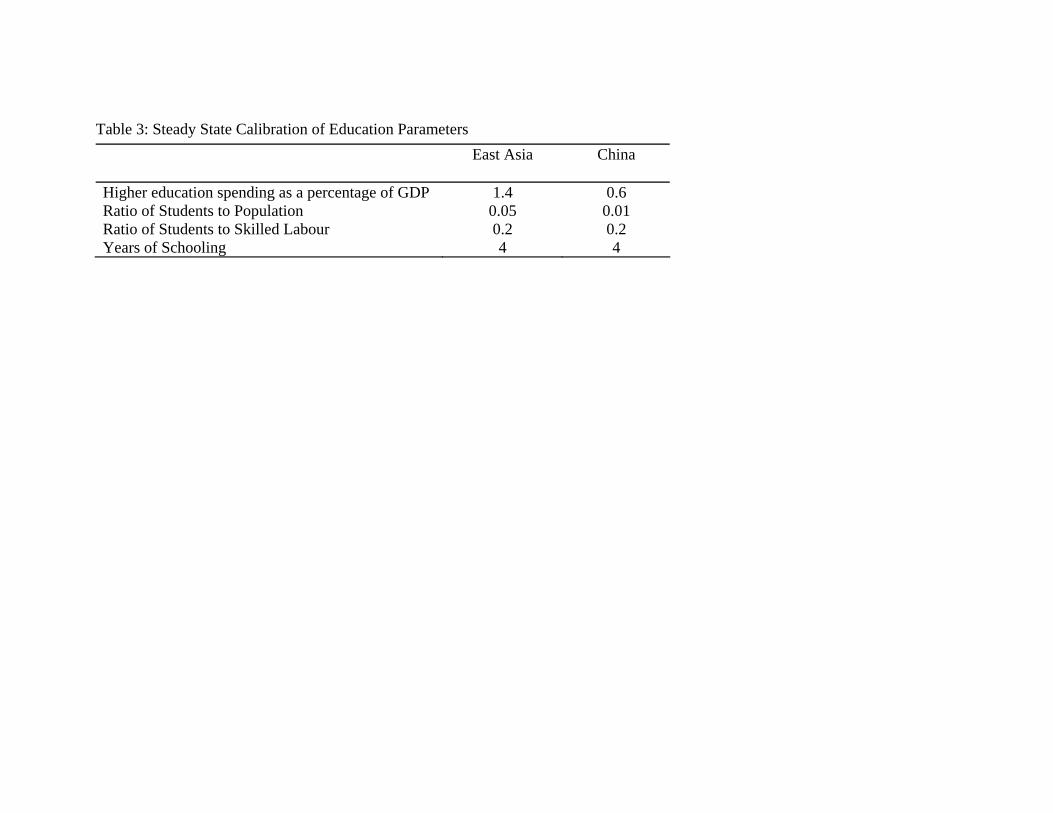

The private and public expenditure data on higher education were used to infer the

aggregate education expenditure. Total spending on higher education is 1.4 percent of

GDP for East Asia and 0.6 percent of GDP for China in 1995. The bulk of the spending

in the education sector for the East Asian economies is on the wage incomes of skilled

and unskilled labour while in China it is spent mostly on intermediate commodities.

Given that the concept of skilled labour is a worker with a university or comparable post-

secondary education, the ratio of students to working population is taken to be 5 percent

for East Asia, which is based on the data for Japan in 1995 and 1 percent for China,

which is the average for the period 1994 to 2002. The ratio of students to skilled labour is

around 20 percent for Japan in the mid 1990s, which was taken as the ratio for East Asia.

A stylised fact regarding China’s stock of university and college graduates is that it is not

on a steady state. The stock of skilled labour is growing with more young aged workers

having higher education degrees than their older counterparts. With retirement of older

workers, China could reach a steady state similar to that of East Asian economies in the

long run. This means that the current ratio of students to skilled labour in China should

fall as the stock of skilled labour is accumulated. Thus, in the benchmark the steady state

ratio of students to skilled labour for China is calibrated to that of the East Asian region.

Table 3 summarises the relevant parameters for the education sector in the model.

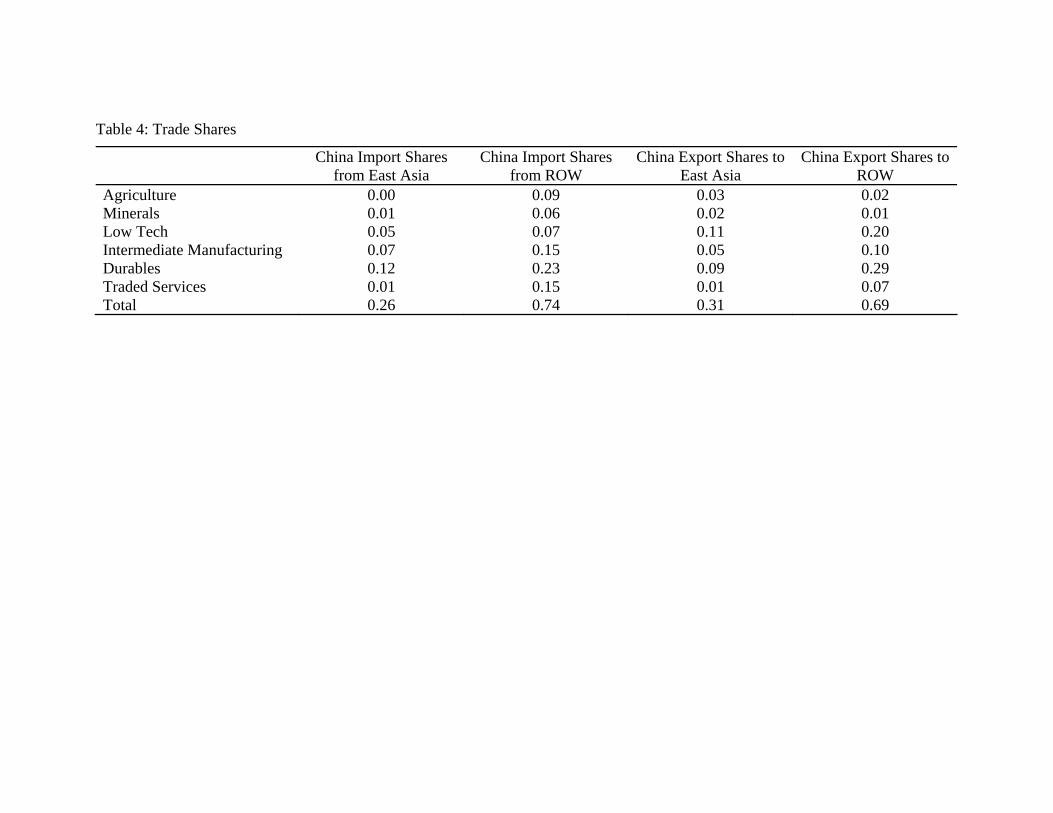

The trade flow data are taken from the GTAP database and are presented in Table 4. It

can be seen that East Asia accounts for a large fraction of China’s total trade - 26 percent

of China’s imports and 31 percent of China’s exports. With respect to the East Asian

9 The factor income shares are rescaled to ensure that the relationship between factor incomes and

investment spending for the capital holds. This means that the total value added by each sector is

proportional to total investment spending. In practice, this only required a small adjustment to the value

added shares.

region, it can be seen that China has a substantial trade deficit in durables and has trade

surpluses in the less skill-intensive sectors of agriculture, low-tech manufacturing and

minerals.

4. Simulation Results

4.1 Experiment Design

As discussed above, the Eleventh Five-Year Plan includes a large increase in tertiary

education spending in order to raise the number of skilled workers and address the

concerns regarding the effects of skill shortages on longer term economic growth. 10

Under the Plan, public tertiary education spending is to rise from the 1995 level of 0.47

percent of GDP to 0.79 percent of GDP – which is a 66 percent increase in public tertiary

education spending. Private sector spending on tertiary education represented

approximately 21 percent of total spending in 1995. Hence, the 66 percent increase in

government spending represents a 52.7 percent increase in total tertiary education

spending.

We assume that this public spending is introduced through education subsidies. The value

of this subsidy is set to be equal to the change in government spending on education

divided by total education spending. That is,

eee yggss /)( −′=−′

where is total spending on education and and ey eg eg ′ are respectively the base and the

planned levels of government spending on tertiary education.

The experiment we consider, therefore, is the effect of an increase in education subsidies

of 52 cents per dollar of education spending. For parsimony, we introduce the full

10 According to the Eleventh Five-Year Plan, the benchmark for the percentage of public spending on total

education to GDP should be 4 percent. Assuming that the share of government spending on higher

education to total education and the share of private spending to public spending on higher education

remains the same, this implies that the proportion of higher education expenditure to GDP is 1.4 percent.

12

13

subsidy in the first year, though clearly other assumptions are possible.11 The subsidy is

funded through increases in lump sum taxes such that the government budget is balanced

in every period.

4.2 Steady State Results

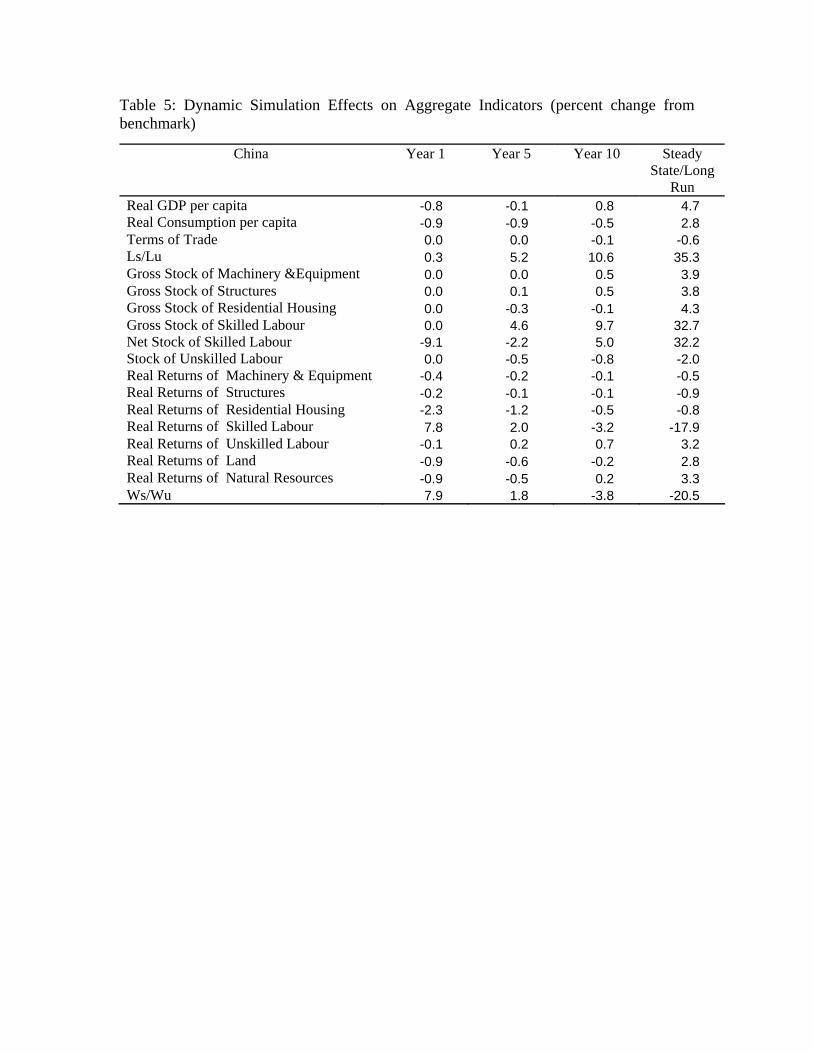

Table 5 reports the response for various aggregate economic indicators for China. It can

be seen that the effect of the subsidy is to raise the stock of skilled workers in China by

33 percent in the long run. The expansion induces capital accumulation with long run

stocks rising by about 4 percent and real GDP rising by 4.7 percent. The accumulation

generates increasing returns for unskilled labour and the fixed factors of natural resources

and land. The increase in the supply of skilled labour causes real wages for skilled labour

to decline by 17.9 percent. Real wages for unskilled labour, however, rise by 3 percent. In

the long run, the education plan addresses concerns over wage inequality.

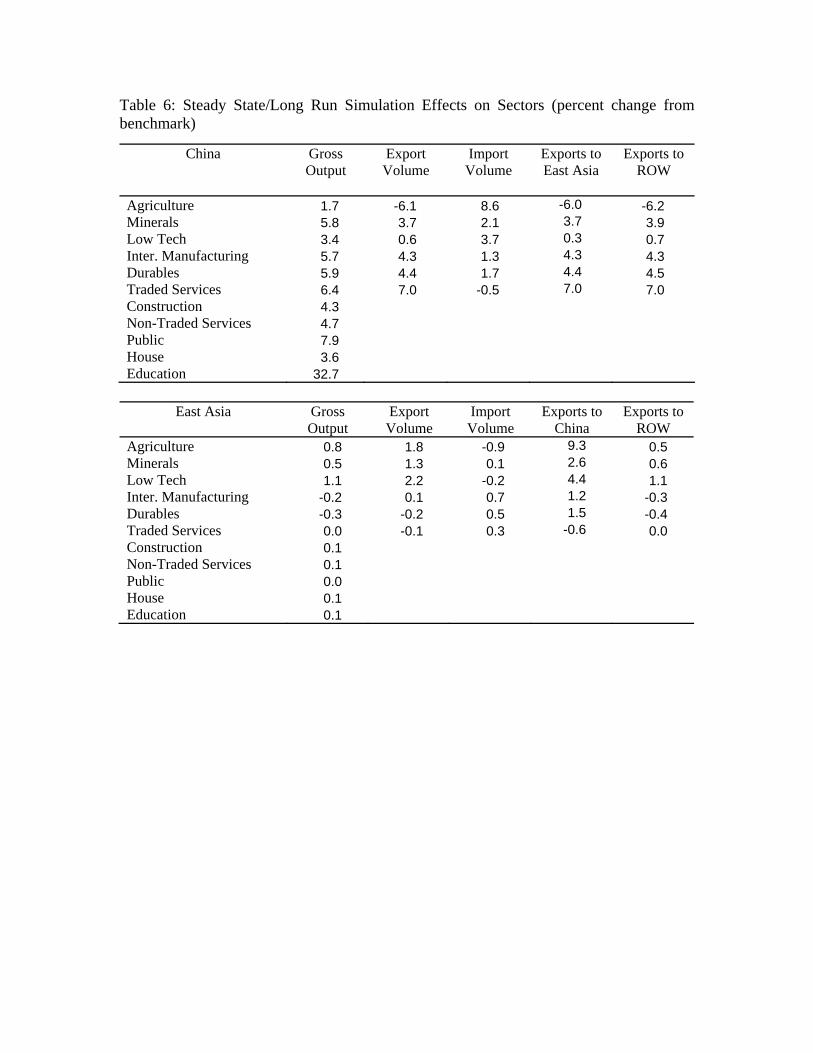

The steady state sectoral and trade results are given in Table 6. It can be seen that the

output of durables, traded services and public sectors rise significantly while the low

skill-intensive sectors of agriculture and low-tech manufacturing experience a more

modest increase in China. In contrast to what might be expected from a standard

Heckscher-Ohlin model with fixed endowments, the expansion of the stock of skilled

labour causes all sectors to experience growth in the long run.

The exports of the more skill-intensive industries of durables and traded service sectors

expand the most. Interestingly, agricultural exports fall by 6 percent and imports rise,

despite the increase in agricultural output. There is a strong long run shift in comparative

advantage away from agriculture and a large substitution in domestic production toward

domestic market rather than exports.

11 An alternative approach would be to introduce the changes gradually, which allows for anticipation

effects. We have experimented with gradual introduction of the subsidy payments so that this target is met

by the tenth year. Though this delays the onset of the transition it does not change any of the qualitative

results.

14

For East Asia, the changes on the macroeconomic aggregates are very small at around

one tenth of a percent. The simulations clearly show that the main effects of the education

plan are on China itself. However, there is a large effect on the structure of trade for East

Asia. Overall, the value of East Asia’s exports to China rise by 2.5 percent. Aggregate

exports of low-tech manufacturing rise by 2.2 percent and agriculture rise by 1.8 percent

in the long run. These changes in the total export bundle mainly reflect the increased

sales to China.

These aggregate trade figures appear to suggest that China’s increase in skill intensity has

led to an expansion of less skill-intensive exports from East Asia. This, however, hides

some interesting composition effects in East Asia’s trade patterns that are shown in Table

6. Although China’s exports of durables to East Asia rise by 4.4 percent, there is also a

rise in East Asia’s exports of durables to China of 1.5 percent. A similar pattern is

observed in intermediate manufacturing. The loss of market share of the East Asian

economies in export sales to the rest of the world in these manufacturing sectors is

approximately balanced by rising exports to China.

The long run results indicate that China’s intended programme of higher education

investment will have significant implications for East Asia’s trade patterns. In particular,

the changes in China tend to favour unskill-intensive sectors in East Asia. Nevertheless,

the increased demand growth in China also creates new export markets for durables and

intermediate manufacturing goods with East Asia’s exports markets shifting toward

China.

4.3 Transition Dynamics

The steady state results reflect changes in the economy that have occurred after the

education investment has been realised. In the short run, during the period of education

investment, the results may be very different. Table 5 also reports some of the key

variables over the transition. On impact it can be seen that the main effect is a large 8

percent rise in the return to skilled labour. Over the initial years the student enrolments

and the flow of graduates, as shown by the output of the education sector in Table 7, rises

15

rapidly, jumping by 24 percent initially and rising to 28 percent by year 10.12 Although

the education plan drives down wage inequality in the long run, the increased education

subsidies generates a short run increase in wage inequality.

The principal cause of the rise in the skilled wage premium is the loss of available skilled

labour services due Mincerian on-the-job training costs. Specifically, all investment plans

in the model are based on the standard neoclassical model of investment with installation

costs. The human capital equivalent is the costs of bringing graduates into the work force

through training programmes and internships (Mincer, 1994). Over the transition, the

increased flow of graduates reduces the effective supply of skilled labour available for

production due to these training costs. The 8 percent rise in the skill premium is

associated with a 9 percent fall in the stock of skilled labour available for production,

which in turn, is due to the 25 percent increase in the stock of students and the flow of

graduate entrants into the labour market.13

A second interesting aspect of the transition path is that, due to the stock-flow

relationship between education output (graduates) and the stock of skilled labour, the

stock of skilled labour evolves relatively slowly. After 10 years of subsidies, the skilled

labour stock has only risen by 9.7 percent. Thus, even though we have assumed that the

subsidy is fully paid in the first year, the results emphasise that there is a long delay

between the onset of subsidies and the realisation of a more skilled labour force.14

12 Alternatively if we assume that the subsidy is phased in over 10 years, then enrolments fall initially but

rise to 21 percent by year 10.

13 Mincer (1994) finds that on-the-job training costs are associated with very significant falls in labour

productivity. See Harris and Robertson (2008) for a further discussion of these on-the-job training costs and

their impact on wage inequality.

14 This result will depend crucially on the size of the adjustment costs parameter on the skilled labour on-

the-job-training cost parameters. A smaller parameter would mean that the half life of adjustment is faster.

However it would also mean that adjustment is more rapid, so that the initial jump in skilled wages is even

larger.

16

Table 7 shows the changes in sectoral outputs over the transition. The changes in the

sectoral composition of output are quite gradual and in many cases, both in China and

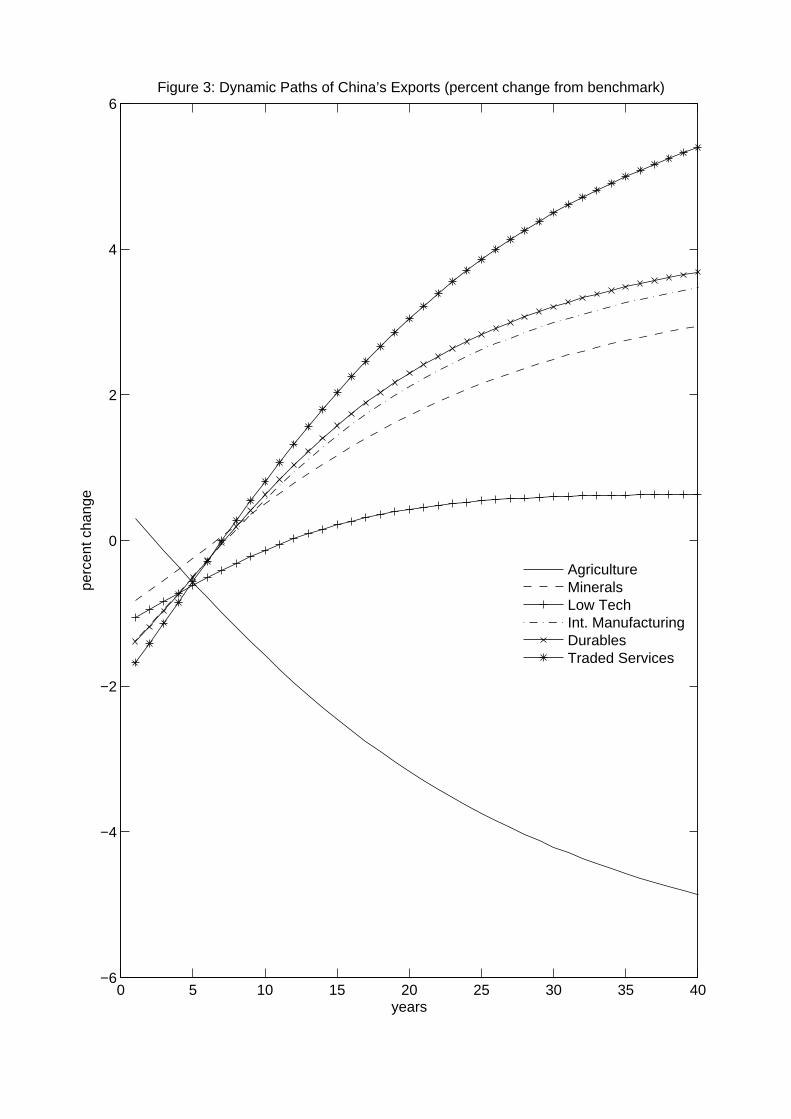

East Asia the effect on impact has the opposite sign to the long run impact. Figures 3 and

4 give a more detailed picture of the changes in the exports for China and East Asia.

Again it can be seen that adjustment is gradual. For example, although China’s exports of

traded services eventually rise by 7 percent but they fall initially and only rise by less

than 1 percent after ten years. For East Asia, it can be seen there is some moderate

growth in the exports of agriculture, minerals and low-tech manufacturing. The more

skill-intensive sectors in East Asia are largely unaffected by China’s education expansion.

Therefore, China’s education policy promotes East Asia’s exports in low skill-intensive

sectors but interestingly this is not at the expense of the other more skill-intensive export

sectors.

5. Conclusion

We have examined the implications of a large increase in higher education subsidies in

China, as set out in the Eleventh Five-Year Plan. In particular, we have attempted to

provide some insights into how such a radical plan might affect relative endowment

structures in China and how these changes will affect trade patterns in China and the East

Asian region. The implications for East Asia are of interest given the heightened concerns

in that region over the implications of China’s export expansion for their own export led

industrialisation policies.

We stress that the aim of this modelling exercise is not to provide a forecast but simply to

help organize our ideas about the effects of China’s education expansion and the

interactions for other countries through trade flows. Thus, many other factors are held

constant – most notably the relative productivity growth rates of the different regions.15

15 Moreover, we want to explore the implications of standard neoclassical trade and growth theory.

Therefore, no attempt has been made to improve the fit of the model by adding in ad-hoc adjustment

parameters.

17

Subject to these caveats and the usual data limitations of calibrated models, the results

indicate that the education subsidies may have large long term effect on the supply of

skilled labour - raising the stock by 33 percent and per capita income by 4.7 percent.

There is a significant shift in China’s trade patterns with durables and traded service

sectors benefiting from the increased endowment of skilled labour. The plan also

substantially reduce wage inequality in the long run but the adjustment costs associated

with large flows of graduates mean that wage inequality rises in the short run.

For the East Asian economies, the increase endowment of skilled labour in China leads to

significant changes in the structure of trade. It was shown, however, that for some sectors

that tend to lose export markets to the rest of the world, such as durables and intermediate

manufacturing, increasing sales to China largely counteract the loss of sales to the rest of

the world. Moreover, sectors which benefit in the longer term such as East Asia’s

agricultural exports do not experience significant growth in the medium term. Because

the stock of China’s skilled labour only changes slowly, the trade patterns also adjust

gradually.

Overall then, the results suggest that the expansion of education subsidies has a positive

effect on growth in China in the longer term, and will substantially reduce wage

inequality. In this sense, the policy effectively addresses concerns that have been raised

regarding skill shortages and wage inequality in China. Nevertheless, we also find that, in

the short-run, there are substantial adjustment costs due to constraints on the on-the-job

training, falling incomes and a rise in inequality. Finally, the results show that the East

Asian economies may face some structural adjustment as a result of the policy, but the

adjustment is slow and mainly involves the expansion of agricultural and low-tech

manufacturing export sectors without significant contraction of other sectors.

Appendix: Sensitivity of Trade Elasticities

To model trade costs we consider the revenue function faced by firms. Let

denote the three regions, where region 3 refers to the ROW region, 2 refers to China and

1 refers to East Asia. The unit revenue function describes the maximum revenue that

firms can generate by varying their supply of goods to each market at given prices,

. We assume that the unit revenue function is a constant elasticity of

transformation type and for a firm in sector i, in region R is given by:

}3,2,1{∈R

},,{ 3,2,1,Ri

Ri

Ri ppp

( ) φφδμ

13

1,, ⎥

⎦

⎤⎢⎣

⎡= ∑

=jji

Rjii

Ri pr (A1.)

By the envelope theorem, the derivative of the unit revenue function gives the firms

export and domestic supply decisions, per unit of gross output:

1

,,

−

⎥⎥⎦

⎤

⎢⎢⎣

⎡=

φ

δμ Ri

jiRjii

Ri r

px (A2.)

From which it can be seen that the elasticity of export supply with respect to the export

market price is φ−1. In the base case we use the values of φ−1=3.9 for Agriculture, 0.7

for traded services and 2.9 for all other sectors, which are taken from de Melo and Tarr

(1992).

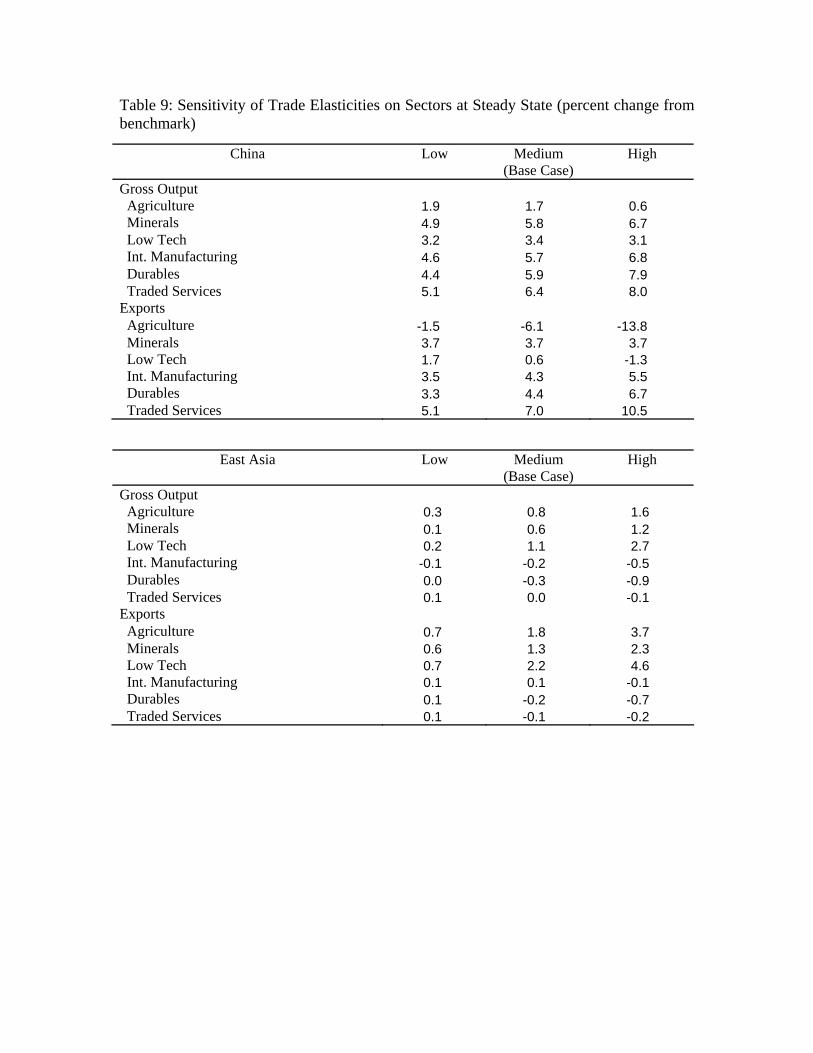

Tables 8 and 9 report the steady state results for the trade elasticity cases, where the value

of these elasticities is doubled and a low case where they are halved. It can been seen

firstly the change in the stock of skilled labour in relatively insensitive to changes in the

trade elasticities and likewise, the change in GDP for China is similar across these

scenarios. The magnitude of the trade flows is moderately sensitive to this parameter.

Nevertheless, the qualitative results remain valid. In particular, even in the high trade

elasticity case, the increased skill formation in China leads to a much larger expansion of

low-tech manufacturing and agriculture from East Asia, but only very modest falls in

exports for the other manufacturing sectors.

18

19

References

Chaudhuri, S. and Ravallion, M. (2007), ‘Partially Awakened Giants: Uneven Growth in

China and India’, in Dancing With Giants: China, India, And The Global Economy,

Winters, L. A. and Yusuf, S. (eds), The World Bank, Washington DC.

Chen, X., Ran, C. and Chen, L. (2004), Change of Rate of Return to Education in Recent

Years, paper presented at the International Conference on Economics of Education,

Beijing, China, May, 2001.

Chow, G. C. (2002), China’s Economic Transformation, Malden, MA, Blackwell

Publishers.

Coxhead, I. and Li, M. (2008), ‘Prospects For Skills-Based Export Growth In A Labour-

Abundant, Resource-Rich Developing Economy’, Bulletin of Indonesian Economic

Studies, 44, 2, 209–38.

Coxhead, I. (2007), ‘A New Resource Curse? Impacts of China’s Boom on Comparative

Advantage and Resource Dependence in Southeast Asia’, World Development, 35, 7,

1099-1119.

De Melo, J. and Tarr, D. (1992), ‘A General Equilibrium Analysis of US Foreign Trade

Policy’, MIT Press, Cambridge.

Deng, Z. and Donald J. T. (1997), ‘The Impact of the Cultural Revolution on Trends in

Educational Attainment in the People’s Republic of China’, American Journal of

Sociology, 103, 2, 391–428.

Dimaranan, B. V. (2006), Global Trade, Assistance, and Production: The GTAP 6 Data

Base, Center for Global Trade Analysis, Purdue University.

20

Fleisher, B. M. and Wang, X. (2004), ‘Skill differentials, return to schooling, and market

segmentation in a transition economy: the case of Mainland China’, Journal of

Development Economics, 73, 1, 315-328.

Fleisher, B. M., Hu, Y. and Li, H. (2006), Economic transition, higher education and

worker productivity in China, Working Paper.

Hannum, E., Jere B., Meiyan W., and Jihong L. (2007), ‘Education in the Reform Era’,

Forthcoming in China’s Great Economic Transformation, edited by Loren Brandt and

Thomas Rawski, Cambridge University Press.

Harris, R. G. and Robertson, P. E. (2007), ‘Dynamic adjustments to terms of trade shocks:

The USA Productivity Boom and Australia’, Economic Record, 83, s1, S35-S45.

Harris, R. G. and Robertson, P. E. (2008), Trade Skills and Wages in the Emerging

Giants, Mimeo, School of Economics, University of New South Wales.

Heckman, J. J. and Li, X. (2004), “Selection bias, comparative advantage and

heterogeneous returns to education: evidence from China in 2000’, Pacific Economic

Review, 9, 3, 155-171.

Heckman, J. J. (2005), ‘China’s human capital investment’, China Economic Review, 16,

50-70.

Freeman, R. B. (2005), ‘Does Globalization of The Scientific/Engineering Workforce

Threaten U.S. Economic Leadership?’, NBER Working Paper 11457.

Islam, N. and Dai, E. (2004), Role of TFP in mainland China’s growth: An investigation

using the dual approach, presented at 9th International Convention of the East Asian

Economic Association.

Kreuger, A. B. and Lindahl, M. (2001), ‘Education for growth: Why and for whom?’,

Journal of Economic Literature, 39, 4, 1101-1136.

21

Lall, S. and Manuel A. (2004), ‘China’s Competitive Performance: A Threat to East

Asian Manufactured Exports?’, World Development, 32, 9, 1441–1466.

Li, Y., Whalley, J., Zhang, S. and Zhao, X. (2008), ‘The Higher Educational

Transformation Of China And Its Global Implications’, NBER Working Paper 13849

Liu, J., van Leeuwen, N., Vo, T. T., Tyers, T. and Hertel, T. (1998), ‘Disaggregating

labour payments by skill level’, Chapter 18 in R. McDougall, A. Elbehri and T.P. Truong

(eds.), Global Trade, Assistance and Protection: The GTAP 4 Database, Purdue

University: Centre for Global Trade Analysis, December 1998.

Min, Y. (2005), Historical Perspectives and Contemporary Challenges: The Case of

Chinese Universities, unpublished manuscript, Centre of Chinese Education, University

of Columbia.

Mincer, J. (1962), ‘On-the-Job Training: Costs, Returns, and Some Implications’ The

Journal of Political Economy, 70, S5, 50-79.

Mincer, J. (1994), ‘Investment in U.S. Education and Training’, NBER Working Paper

4844.

OECD (2002), Indicators of internationalisation and trade in post secondary education,

Paris, Center for Education Research and Innovation, May.

Ravenhill, J. (2006) ‘Is China an Economic Threat to Southeast Asia?’, Asian Survey, 46,

5, 653–674.

Roland-Holst, D. and Weiss, J. (2004), ‘ASEAN and China: Export Rivals or Partners in

Regional Growth?’, World Economy, 27, 8, 1255 – 1274.

The Economist (2008), ‘The Export Juggernaut’, Sep 27, 388, 8599.

Tsang, M.C. (2000), ‘Education and National Development in China since 1949:

Oscillating Policies and Enduring Dilemmas’, China Review- an Interdisciplinary

Journal on Greater China, 579-618.

22

Weiss, J. and Gao S. (2003), ‘People’s Republic of China’s export threat to ASEAN:

Competition in the US and Japanese markets’, ADB Institute Discussion Paper No. 2,

Asian Development Bank.

Wilcoxen, P. J. (1988), The effects of environmental regulation and energy prices on US

economic performance, PhD Thesis, Harvard University.

World Education Indicator Programme (WEIP) (2002), Financing education –

investments and returns: Analysis of the world education indicators, UNESCO Institute

for Statistics and OECD.

Zhang, W. (2006), China’s higher education trade and the impact of the WTO/GATT

liberalisation, PhD thesis, University of Columbia.

Table 1: Number of Students enrolled in Tertiary Education Institutions (millions)

Number of Students

1978 2.3 1980 2.7 1985 3.4 1990 3.7 1991 3.5 1992 3.7 1993 4.4 1994 5.2 1995 5.5 1996 5.8 1997 6.0 1998 6.5 1999 7.5 2000 9.2 2001 11.9 2002 14.7 2003 16.7 2004 17.5

Source: Ministry of Education website, author’s calculations. Note: The tertiary education enrolments include only students in regular higher education institutions and adult higher education institutions. The data for 1990 to 2002 are calculated based on the number of students per 100,000 inhabitants.

Table 2: Gross Enrolment Ratios in Selected Countries/Regions in 2004

Tertiary Gross

Enrolment Rate (%) China 19.1 India 11.8 Indonesia 16.7 Japan 54.0 South Korea 88.5 Malaysia 32.4 Thailand 41.0 Philippines 28.8 Russia 68.2 Egypt 32.6 Armenia 26.2 Jordan 39.3 Mexico 23.4 Romania 40.2 Australia 72.2 France 56.0 United States 82.4 United Kingdom 60.1 Lower middle income 22.5 World 24.8

Source: World Development Indicators Database

Table 3: Steady State Calibration of Education Parameters East Asia China

Higher education spending as a percentage of GDP 1.4 0.6 Ratio of Students to Population 0.05 0.01 Ratio of Students to Skilled Labour 0.2 0.2 Years of Schooling 4 4

Table 4: Trade Shares

China Import Shares from East Asia

China Import Shares from ROW

China Export Shares to East Asia

China Export Shares to ROW

Agriculture 0.00 0.09 0.03 0.02 Minerals 0.01 0.06 0.02 0.01 Low Tech 0.05 0.07 0.11 0.20 Intermediate Manufacturing 0.07 0.15 0.05 0.10 Durables 0.12 0.23 0.09 0.29 Traded Services 0.01 0.15 0.01 0.07 Total 0.26 0.74 0.31 0.69

Table 5: Dynamic Simulation Effects on Aggregate Indicators (percent change from benchmark)

China Year 1 Year 5 Year 10 Steady State/Long

Run Real GDP per capita -0.8 -0.1 0.8 4.7 Real Consumption per capita -0.9 -0.9 -0.5 2.8 Terms of Trade 0.0 0.0 -0.1 -0.6 Ls/Lu 0.3 5.2 10.6 35.3 Gross Stock of Machinery &Equipment 0.0 0.0 0.5 3.9 Gross Stock of Structures 0.0 0.1 0.5 3.8 Gross Stock of Residential Housing 0.0 -0.3 -0.1 4.3 Gross Stock of Skilled Labour 0.0 4.6 9.7 32.7 Net Stock of Skilled Labour -9.1 -2.2 5.0 32.2 Stock of Unskilled Labour 0.0 -0.5 -0.8 -2.0 Real Returns of Machinery & Equipment -0.4 -0.2 -0.1 -0.5 Real Returns of Structures -0.2 -0.1 -0.1 -0.9 Real Returns of Residential Housing -2.3 -1.2 -0.5 -0.8 Real Returns of Skilled Labour 7.8 2.0 -3.2 -17.9 Real Returns of Unskilled Labour -0.1 0.2 0.7 3.2 Real Returns of Land -0.9 -0.6 -0.2 2.8 Real Returns of Natural Resources -0.9 -0.5 0.2 3.3 Ws/Wu 7.9 1.8 -3.8 -20.5

Table 6: Steady State/Long Run Simulation Effects on Sectors (percent change from benchmark)

China Gross Output

Export Volume

Import Volume

Exports to East Asia

Exports to ROW

Agriculture 1.7 -6.1 8.6 -6.0 -6.2 Minerals 5.8 3.7 2.1 3.7 3.9 Low Tech 3.4 0.6 3.7 0.3 0.7 Inter. Manufacturing 5.7 4.3 1.3 4.3 4.3 Durables 5.9 4.4 1.7 4.4 4.5 Traded Services 6.4 7.0 -0.5 7.0 7.0 Construction 4.3 Non-Traded Services 4.7 Public 7.9 House 3.6

East Asia Gross

Output Export Volume

Import Volume

Exports to China

Education 32.7

Exports to ROW

Agriculture 0.8 1.8 -0.9 9.3 0.5 Minerals 0.5 1.3 0.1 2.6 0.6 Low Tech 1.1 2.2 -0.2 4.4 1.1 Inter. Manufacturing -0.2 0.1 0.7 1.2 -0.3 Durables -0.3 -0.2 0.5 1.5 -0.4 Traded Services 0.0 -0.1 0.3 -0.6 0.0 Construction 0.1 Non-Traded Services 0.1 Public 0.0 House 0.1 Education 0.1

Table 7: Transitions on Gross Output (percent change from benchmark) China

Year 1 Year 5 Year 10 Steady State

Agriculture -0.8 -0.8 -0.6 1.7 Minerals -1.3 -0.4 0.8 5.8 Low Tech -1.2 -0.5 0.3 3.4 Inter. Manufacturing -1.3 -0.4 0.8 5.7 Durables -1.4 1.1 -0.5 5.9 Traded Services -1.5 -0.5 0.7 6.4 Construction -0.6 0.2 1.0 4.3 Non-Traded Services -1.1 -0.4 0.5 4.7 Public -2.2 -0.7 1.0 7.9 House -0.3 -0.5 -0.2 3.6

East Asia

Year 1 Year 5 Year 10

Education 24.5 26.4 28.1 32.7

Steady State

Agriculture -0.1 0.0 0.2 0.8 Minerals -0.3 -0.2 0.0 0.6 Low Tech 0.4 0.3 0.3 1.1 Inter. Manufacturing 0.1 0.0 0.0 -0.2 Durables -0.1 -0.1 -0.1 -0.3 Traded Services 0.0 0.0 0.0 0.0 Construction 0.0 0.0 0.0 0.1 Non-Traded Services 0.0 0.0 0.0 0.1 Public 0.0 0.0 0.0 0.0 House 0.0 0.0 0.0 0.1 Education 0.0 0.0 0.0 0.1

Table 8: Sensitivity of Trade Elasticities on Aggregate Indicators at Steady State (percent change from benchmark)

China Low Medium (Base Case)

High

Real GDP per capita 3.9 4.7 5.4 Real Consumption per capita 2.2 2.8 3.5 Terms of Trade 0.3 -0.6 -0.3 Ls/Lu 35.0 35.3 36.4 Gross Stock of Machinery &Equipment 2.4 3.9 5.0 Gross Stock of Structures 2.8 3.8 4.7 Gross Stock of Residential Housing 3.5 4.3 5.1 Gross Stock of Skilled Labour 32.3 32.7 33.7 Net Stock of Skilled Labour 32.2 32.2 32.2 Stock of Unskilled Labour -2.0 -2.0 -2.0 Real Returns of Machinery & Equipment -0.2 -0.5 -0.5 Real Returns of Structures -0.9 -0.9 -0.8 Real Returns of Residential Housing -0.9 -0.8 -0.8 Real Returns of Skilled Labour -18.4 -17.9 -17.8 Real Returns of Unskilled Labour 2.7 3.2 3.5 Real Returns of Land 2.7 2.8 2.3 Real Returns of Natural Resources 2.9 3.3 3.3

Ws/Wu -20.5 -20.5 -20.6

Table 9: Sensitivity of Trade Elasticities on Sectors at Steady State (percent change from benchmark)

China Low Medium (Base Case)

High

Gross Output Agriculture 1.9 1.7 0.6 Minerals 4.9 5.8 6.7 Low Tech 3.2 3.4 3.1 Int. Manufacturing 4.6 5.7 6.8 Durables 4.4 5.9 7.9 Traded Services 5.1 6.4 8.0 Exports Agriculture -1.5 -6.1 -13.8 Minerals 3.7 3.7 3.7 Low Tech 1.7 0.6 -1.3 Int. Manufacturing 3.5 4.3 5.5 Durables 3.3 4.4 6.7

Traded Services 5.1 7.0 10.5

East Asia Low Medium (Base Case)

High

Gross Output Agriculture 0.3 0.8 1.6 Minerals 0.1 0.6 1.2 Low Tech 0.2 1.1 2.7 Int. Manufacturing -0.1 -0.2 -0.5 Durables 0.0 -0.3 -0.9 Traded Services 0.1 0.0 -0.1 Exports Agriculture 0.7 1.8 3.7 Minerals 0.6 1.3 2.3 Low Tech 0.7 2.2 4.6 Int. Manufacturing 0.1 0.1 -0.1 Durables 0.1 -0.2 -0.7

Traded Services 0.1 -0.1 -0.2

Figure 1: Tertiary Students and Skilled Labour as a percentage of the Labour Force

0

1

2

3

4

5

1990 1992 1994 1996 1998 2000 2002 2004

perc

ent

Students/Labour Force Skilled Workers/Labour Force

Source: China Statistical Yearbook 2005, Islam and Dai (2004) and Ministry of Education website, author’s calculations.

Figure 2: Total Expenditure and Public Expenditure on Education as a percentage of GDP

0

1

2

3

4

5

6

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

perc

ent

Total Education/GDP Government Spending/GDP

Source: China Educational Finance Statistical Yearbook 2003, China Statistical Yearbook (various years)

0 5 10 15 20 25 30 35 40−6

−4

−2

0

2

4

6Figure 3: Dynamic Paths of China’s Exports (percent change from benchmark)

years

perc

ent c

hang

e

AgricultureMineralsLow TechInt. ManufacturingDurablesTraded Services

0 5 10 15 20 25 30 35 40−6

−4

−2

0

2

4

6Figure 4: Dynamic Paths of East Asia’s Exports (percent change from benchmark)

years

perc

ent c

hang

e

AgricultureMineralsLow TechInt. ManufacturingDurablesTraded Services