Embed Size (px)

Citation preview

EDITORIALShri Y.C. NandaChairmanAFC Ltd.

Shri A.K. GargManaging DirectorAFC Ltd.

Shri L.N. Vasudev RaoGeneral ManagerUnion Bank of India

Shri G.C. SharmaGeneral ManagerBank of Baroda

Shri Gobinda BanerjeeGeneral ManagerPunjab National Bank

Shri E. ShivalingamGeneral ManagerUCO Bank

Shri P.C. SrivastavGeneral ManagerCentral Bank of India

Shri N. Narasa ReddyGeneral ManagerCanara Bank

Shri P.M. KshirsagarGeneral ManagerAFC Ltd.

HonoraryAdvisory Board

Views expressed by the authors do notnecessarily reflect those of the AgriculturalFinance Corporation Ltd. No permission isnecessary to reproduce contents except

for the copyright text.

Global warming or global cooling?

The climate summit which was held in Copenhagen, Denmark from Dec 7-18, 2009was watched with great expectations as 192 countries participated to tackle theproblem of climate change. The Copenhagen Accord sets the goal of limiting globaltemperature increases to 2 degree celsius though it does not set any binding targetsfor emission reduction. Both developing and developed countries will have to informUNFCCC of its commitment to reduce emission of greenhouse gases to mitigate theeffects of climate change. The rich countries have pledged to contribute US$30billion between 2010 and 2012 and $100 billion by 2020 for developing countries,particularly vulnerable countries and small island states, to help adapt to and mitigatethe effects of climate change.

There is another viewpoint as promoted by Shri Janardhan Negi, an Indian geophysicistthat the global warming phase will change to global cooling and the temperatureanomaly will decline substantially by the year 2030. Some effects of the process arealready evident in the cold wave of 2010 which has brought about widespreadsnowfall in almost the entire northern hemisphere. According to Shri Janardhan Negi,there is a strong global cyclic weather phenomenon which is independent of thegreenhouse gas emissions.

In July 2008, some leading climatologists and meteorologists met in New York at theEnergy Business Watch Climate and Hurricane Forum. The forum strongly suggestedthat a period of global cooling is emerging, but what restrained them from spelling itout categorically was a possible concern of a political backlash.

This theory is also backed by Intergovernmental Panel on Climate Change (IPCC)scientist Mojib Latif, who in an article in Daily Mail in January this year wrote “we’rein for 30 years of cooler temperatures” which he calls it a “mini ice age”. His theoryis based on an analysis of natural oscillations in water temperatures in the oceans.However, he believes the current cold weather pattern as a pause, a “30-years-longblip”, in the larger cycle of global warming, which postulates that temperatures willrise rapidly over the coming years.

Whatever be the direction of climate change in the short-run as well as long run,what is of utmost importance is for agricultural scientists to take stock of the situationand maintain sustainability of agriculture so that the food security of the humanpopulace as well other living creatures is not jeopardised.

A.K. GargEditor-in-Chief

I N SAnnual Subscription

India, Nepal andBangladesh Rs. 600/-

Other Countries(By Air Mail) US$70

Single Copy Rs. 50/-

Agricultural FinanceCorporation Limited

Dhanraj Mahal, ChhatrapatiShivaji Maharaj Marg,Mumbai 400 001

Tel: 91-022-22028924Fax: 91-022-22028966Email: [email protected]: www.afcindia.org.in

Role of Greenhouse Technology in

Precision Farming: An Indian

Perspective ....................... 6

Issues on Management of Coastal and

Marine Biodiversity............ 9

Marketing Analysis of Milk Production

in Shirpur Tehsil of Dhule District of

Maharashtra (India) ............ 14

A Road Map to Wholesale Market

Infrastructure -PPP Mode .. 16

By K.S. Kumar and K.N. Tiwari

By K. Venkataraman

By Vijay Gorakh Patil

By Satyaveer Singh and Subah Singh Yadav

I D EEditorial Board

Published byAgricultural FinanceCorporation Ltd.Dhanraj Mahal, ChhatrapatiShivaji Maharaj Marg,Mumbai 400 001

Produced byL.B. Associates Pvt Ltd.H-108, Sector 63, Noida - 201301Tel: 91-120-2427280/82,Fax: 91-120-2427108Email: [email protected]: www.lbassociates.com

Editor-in-ChiefShri A.K. Garg

EditorG. Kalyan Kumar

Associate EditorLinda Brady Hawke

Desk EditorManish Sharma

Events & AdvertisingRitu Khanduri91-9891173723

DesignAtul Kumar

Agrarian Crisis: Distress & Suicide .. 22

Real Time Gross Settlement: Need

for Customers .............................. 28

Honesty ki Jhappi Opportunity for India’s

Social Revolution........................... 31

Statistical Overview of Agriculture

Production in India ........................ 33

News ........................................... 37

India’s Fertilizer Capacity to Expand 42

By Dr. B.B. Sahoo

By K. Kannusamy and Sathish Kumar

By Prajapati Sudhirkumar Rameshbhai

COVER STORY

6

By K.S. Kumar and K.N. Tiwari*

Introduction

India has witnessed an increase in foodgrain production from 51 million tonnes(50’s) to 206 million tonnes at the turnof the century and that has helped inachieving self sufficiency. However, quickshrinking of the agricultural landthreatens sustainable production of foodgrains and its ability to feed ever growingmouths. In this context, careful tailoringof soil and crop management practicessuitable to local needs is of greatimportance to keep up the pace ofproduction. Precision Farming otherwisecalled prescription farming or site-specificfarming helps to overcome theseconstraints by accurately assessing thevariability of crop production practices inspace-time continuum by utilizing toolslike Global Positioning System (GPS),Geographical Information System (GIS),Remote Sensing (RS) and Sensors.

Since ancient time, mankind has been

aware of the fact that a wise modification ofthe environment could improve theproductivity of crops. For instance, the factthat light transmitting shelters could createa suitable environment was certainly knownto the Romans, as Emperor Tiberius used toeat a cucumber daily. Infact, the concept ofControlled Environment Agriculture (CEA)was not a novel idea and has been in usesince a long time. Greenhouse Technologyhas been considered as the core part ofprecision farming and has a tremendous roleto play in Indian horticulture by increasingthe availability of fresh vegetables, fruits andflowers and thereby leading to betternutrition and improved standard of living.

A greenhouse can be defined as a “framedor an inflated structure with a transparentor translucent material in which crops couldbe grown under at least partially controlledenvironment and which is large enough topermit persons to work within it to carryout cultural operations”. The greenhouse isnow better understood as a system of

controlled environment agriculture(CEA), with precise control of air,temperature, water, humidity, plantnutrition, carbon dioxide and light.The inside environment(microclimate) of the greenhouse iscontrolled by growth factors likelight, temperature, humidity andcarbon dioxide concentration. Theyare scientifically controlled to anoptimum level throughout thecultivation period, thus increasing theproductivity by several folds.

Greenhouse Production

The liberalized seed policy in the lateeighties, globalization of Indianeconomy and the economic reformsinitiated in the early nineties pavedthe way for the advent of state ofthe art protected cultivationtechnology in India. The use ofgreenhouses for commercialagricultural production in India had

Role of Greenhouse Technologyin Precision Farming:

An Indian Perspective

COVER STORY

7

to wait until the technology becameadvanced enough in late nineties for theproducts to be sold at competitive prices.After the advent of plastics applicationin agriculture, greenhouse technologyevolved as a breakthrough in theagricultural production technology. It hasintegrated market driven qualityparameters with production systemprofits. Today, the expertise is such thatin principle, it is possible to let the climatecontrol computer to produce themicroclimate desired by the groweraccording to the need of a particular cropwith the benefit-cost ratio being morethan one.

Despite its late entry, Indian greenhouseindustry made rapid strides and nearly300 to 500 ha of area has been broughtunder protected cultivation ofhorticultural crops. Abundant sunshinethroughout the year especially in theautumn and winter season is perhaps thefirst blessing for year round productionand that too without depending onartificial light and the related costescalation due to additional energy input.However, necessary steps to reduce thehigh summer temperatures in thegreenhouse by adopting suitable cost-

Sl.No Country Area (ha)

1 Algeria 500

2 Australia 600

3 Belgium 2400

4 Bulgaria 1350

5 Canada 400

6 Chile 1600

7 China 48000

8 Columbia 2600

9 Egypt 1000

10 England 3500

11 France 5800

12 Greece 4240

13 Hungary 5500

14 India 500

Sl.No Country Area (ha)

15 Israel 2200

16 Italy 18500

17 Japan 42000

18 Jordan 450

19 Moracco 3000

20 Netherlands 9600

21 Poland 1500

22 Portugal 2500

23 Romania 3500

24 Spain 25000

25 South Korea 21000

26 Turkey 9800

27 USA 4250

Table1: Area under Greenhouse in Different Countries

Source: Jensen and Malter.1998. ProtectedAgriculture - A global review World BankTechnical Paper No.253.

Design of Greenhouses

India has varied climatic conditions indifferent regions, so the greenhouse andthe supporting facilities have to bedeveloped accordingly. Design of thegreenhouse should vary as per the localagro-climatic conditions keeping in viewthe economic constraint. The southernplateau and the coastal regions neednaturally ventilated polyhouses andnorthern plains with composite climaterequire both cooling and heatingfacilities. The initial cost of thegreenhouse generally depends upon thecost of the structure, cladding andtemperature control mechanism andwhere as the operational cost relies uponmainly upon the maintenance oftemperature and humidity in thegreenhouse.

Low Cost Greenhouses forNursery and Off-SeasonCultivation of Vegetables

Large scale expansion of nursery and off-season cultivation of vegetables undercost-effective greenhouse structures isnecessary to produce healthy seedlingsand for consumption of fresh vegetablesat lesser cost. Greenhouse design,structure and technology for producinghigh quality planting material need to be

effective cooling methods are necessaryto boost up the year round greenhouseproduction in India.

Fig: 1. Greenhouse designs suitable for subtropical India

8

COVER STORY

Crop Greenhouse Open field Hydroponic

Tomato 150 50 187.5

Cucumber 180 8 250

Capsicum 110 100 -

Broccolli 15 7 -

Yield (tonnes/hec)

Table 2: Comparison of yield in open field, greenhouse andhydroponic system

(Source: Chandra et al., (2003)

fine tuned to suit local climatic conditions. Efforts are also needed to develop suitabletechnology for production of healthy and well developed seedlings in plastic perforatedtrays. New growing media like soil less culture need to be standardized for optimumplant growth.

Greenhouse Floriculture Production

In view of the growing international demand for floriculture products, especially cutflowers which have been registering an annual growth of over 11 percent(Anonymous, 1997), floriculture was given a priority status for export oriented marketdevelopment in India. Cut roses accounted for 19 percent of the international cutflower trade and therefore, special attention is required in developing cut roseproduction as the major crop for export in India. However, in order to meetinternational standards for cut flowers, special greenhouse structures equipped withautomatic environmental gadgets are required. However, the promotion of “hi-techfloriculture” as a specialized industry in India requires hand to hand support fromboth greenhouse growers and the government. The state-of-the-art technologyimported from abroad for greenhouse floriculture needs substantial amendment withrespect to the design of greenhouse to achieve cost effective production and becompetitive in the global market.

Greenhouse Cultivation inPrecision Farming DevelopmentCentre, IIT Kharagpur

The precision farming developmentcentre of IIT, Kharagpur has been activelyinvolved in conducting field research,training and dissemination of developedtechnologies on greenhouse cultivationof crops for the benefit of farmers andstate government officials. A briefdescription of concluded researchactivities includes design anddevelopment of low-cost plasticgreenhouses for seedlings and offseasoncultivation of vegetables and their yieldresponses. Estimation of waterrequirement for different vegetable cropshas been documented. Apart from these,the centre has initiated an in depth studyon the design aspects of greenhousefloriculture suitable for eastern climaticconditions of India. Studies on thevariation of microclimate in thegreenhouse coupled with derivingbenefits of cost effective coolingmethods to reduce high summertemperatures for floricultural productionhave also been undertaken.

Conclusions

Greenhouse Technology has got atremendous role in keeping up the paceof precision farming in Indian Agriculture.Protected cultivation of vegetables andflowers not only increases thesustainability of agricultural productionbut also improves the standard of living.Necessary steps to maintain the glory ofthe greenhouse Industry include:

1. Improving the domestic marketsfacilities to offer high prices for theproducts of greenhouse

2. Exploring high value productalternatives such as propagatingmaterials of export oriented crops.

3. Developing vertical integration andjoint ventures that could be adoptedby Indian growers.

4. Establishing a network of supportsystems from the government,universities and the private sector willbe of immense value for growers andthe industry.

* K.S. Kumar and K.N. Tiwari

Agricultural and Food EngineeringDepartment, IIT Kharagpur

Fig: 2. Greenhouse Production of Gerbera in Greenhouse at PFDC, IIT Kharagpur

9

BIODIVERSITY

Issues on Management of Coastaland Marine Biodiversity

Introduction

Coastal zone represents 18 percent ofthe earth’s surface, providing space for60 percent of the human population,since about 70 percent of the world citieswith population more than 1.6 millionare located in the coastal zone. 90percent of the world fish catch isobtained from this zone. Interestingly,the hydrosphere of the coastal zone isonly about 8 percent but representsabout 18 to 33 percent of total primaryproduction. This zone is biogeochemicallymore important as it buries andmineralises 80-90 percent of organicmatter and the approximate carbonatedeposition is estimated to be 50 percent.This area also receives discharges ofsuspended matter associated withelevated levels of pollutants from majorrivers and this accounts for 75 to 90percent. This zone has high biologicalpotential as it serves as feeding, nurseryand spawning grounds with rich

biodiversity and as an intermediarybiotope between marine and freshwaterenvironments.

Coastal and marine ecosystems play avital role in India’s economy by virtue oftheir resources, productive habitats andrich biodiversity. India has a coastline ofabout 8000 km of which the mainlandaccounts for 5,422 km, Lakshadweepcoast extends up to 132 km andAndaman and Nicobar Islands havecoastline of 1,962 km. Nearly 250+million people live within a distance of50 km from the coast. The coastal areain particular, has been assuming greaterimportance in recent years, owing toincreasing human population,urbanisation and accelerateddevelopmental activities. The coastalregions are thus a place of hectic humanactivity and the coastal ecosystems arenow highly disturbed and very muchthreatened. Current approaches to themanagement of coastal resources are not

By K. Venkataraman

The Physical regime ofthe Indian coasts ischaracterised bydifferent types of coastaland shore ecosystemslike promontories (nearBeypore in Kerala State),sand spits (at Karnatakaand Andhra Pradesh),barrier beaches (alongKerala coast),embayment (Mirya Bayin Maharashtra),estuaries and offshoreislands

10

BIODIVERSITY

adequate for sustainable developmentand the coastal environments andresources are being rapidly degraded anderoded in India (Whittingham et al.,2003).

The Indian mainland coast is divided intotwo parts: West Coast and East Coast.The West Coast is fronted by the ArabianSea and the East Coast is by the Bay ofBengal. Other than these mainlandcoasts, there are three island groups suchas Lakshadweep in the south ArabianSea, Andaman and Nicobar in the easternBay of Bengal. The east and west coasts

islands.

Further, the coastal zone of India is alsoendowed with a very wide range ofecosystems such as estuaries, lagoons,mangroves, backwaters, salt marshes,rocky coasts, sandy stretches and coralreefs which are characterised by uniquebiotic and abiotic properties andprocesses (Venkataraman and Wafar,2005). Not realising the importance ofthe coastal and marine ecosystems andits multiple uses, the coastal populationexploit the biological resources andinterferes and modifies the basic coastalprocesses (Mehta, 1999). Traditionally,coastal areas of India are highlypopulated and developed because theyare the places where trade, transport,communication and civilisation are welldeveloped. It is estimated that, out ofthe 25 global mega cities, 15 would beon the coast. In India, out of the three

are markedly different in their geo-morphology. The West Coast is generallyexposed with heavy surf and rocky shoresand headlands. The East Coast isgenerally shelving with beaches, lagoons,deltas and marshes. It is also relativelylow lying with extensive alluvial plainsand deltas. The Physical regime of theIndian coasts is characterised by differenttypes of coastal and shore ecosystemslike promontories (near Beypore in KeralaState), sand spits (at Karnataka andAndhra Pradesh), barrier beaches (alongKerala coast), embayment (Mirya Bay inMaharashtra), estuaries and offshore

mega cities with population more than10 million, Delhi (13.2 million), Mumbai(16 million) and Kolkata 16.5 million, twoare coastal cities i.e. Mumbai andKolkata. The population density is alsomuch more in coastal areas than thenational average. For example, in thestate of Tamil Nadu, the populationdensity in coastal areas is 528 per sq kmagainst 372 per sq km which is stateaverage. In parts of coastal metros likeMumbai, Kolkata and Chennai thepopulation density ranges from 20,000to 50,000 per sq km. The increasedpopulation pressure has led to resourcedepletion and environmentaldegradation due to coastal pollution,disposal of domestic wastes and industrialwastes. As in most of the developingnations, the coastal environmentalproblems and issues in India are alsoconcerned with the following three mainconditions: environmental degradation,resources reduction and user conflicts.

The coastal situation in India mirrorsglobal trends where unsustainable use ofnatural resources, pollution and habitatdestruction are resulting in significant, ifnot fully irreversible, loss of the marineand coastal life support systems. Overfishing and the use of destructive fishingpractices and habitat conversion haveresulted in alarming degradation ofcoastal areas.

Coastal regions in India areexperiencing:

• Population growth in the coastal areasis mainly due to migration of job lessvillagers who were once working inagricultural fields.

• Widespread poverty in coastal areasfishers in particular among the poorestof the poor;

• Declining fisheries productivity in Indiais due to over harvesting and loss ofhabitats. Increasing population andpoverty have put additional pressureon resources.

• Fish production has increased over adecade but per capita consumption offish has declined.

• Increasing environmental damagesdue to human induced activities.

Pollution from land-based activities,Industrial and Urban Development:India stands at the threshold of this new

The description of the areas of coastline in different coastal states in India.

The increasedpopulation pressurehas led to resourcedepletion andenvironmentaldegradation due tocoastal pollution,disposal of domesticwastes and industrialwastes

11

BIODIVERSITY

millennium probably with a bleak pictureof the status of coastal resources andmuch to do to reverse the current trend.Without the sincere efforts of managersand scientists this cannot be achieved.In order to sustain and eventuallyimprove the benefits we derive fromcoastal resources, momentouscommitments and investments must bemade by local coastal communities.Government of India, StateGovernments, and Non GovernmentOrganizations should put in additionaleffort in conservation and sustainable useof coastal resources. Furthermore, theseefforts and initiatives must becoordinated and harmonized to achievethe goal of carrying these benefits tofuture generations. Coastal and marinemanagement provides the tools forslowing and hopefully reversing thenegative impacts of uncontrolled use ofthese resources. Coastal and marinemanagement also provides the essentialprocesses for integration of all sectoral,spatial, temporal, policy and institutionalcomponents crucial to achieve the goalof sustainable development.

Resource use Conflicts: Naturalresources are those products readilybestowed to us by nature from whichhumans derive value. Forests, fisheries,minerals, water, and land resources arevaluable commodities in India. Resourceuse conflicts arise when the benefitsderived by one group of people using oneresource have an impact on the benefitsderived by another group using the same

or another resource (Devaraj andVivekanandan, 1999). Similarly, overuseof one resource may affect the relativehealth or abundance of another resourcewithin an environmental system. Suchimpacts are not always obvious and mustbe understood.

Examples of resource conflicts that canbe addressed by coastal and marinemanagement include:

• Siltation from deforestation byresource users in upland areasnegatively impacts coastal habitats andfisheries in coastal areas;

• Intrusion of commercial fishing incontinental shelf regions results inoverexploitation of limited fisheriesresources where relatively fewindividuals benefit; and

• A probable lack of specific regulations(local and national) for fishing activitieswithin known productive fishinggrounds where small-scale fishers aredirectly dependent for livelihood.

Coastal areas all over India aredeveloping rapidly because, people liketo live near the sea. The consequence isthat beaches, coastal land areas, and nearshore coastal habitats are in greatdemand and are being utilized for a widevariety of conflicting human usesincluding industry, construction,dumping, boat landings, tourism, andhabitation. Many user conflicts betweentraditional and mechanized fishers stillpersist within the 10 and 15 km limits.

While commercial fishing is strictlyprohibited within coastal waters bynational laws, intrusion of large, highlyefficient, mechanized fishing boats isprevalent. One result of the conflictbetween the mechanized and traditionalsectors is decreasing catches. Asindicated, catch from the traditionalsector is being overtaken by catch fromthe mechanized and aquaculture sectors;meanwhile, traditional fishers aregrowing in number. The willingness offishers to continue fishing when catchesare declining indicates the relative lackof alternatives and the small value fishersenforcing time. If properly implemented,reserving the use of traditional fishinggrounds by state and central law servesas a strategy for restricting access,reducing fishing pressure, and improvingthe condition of traditional fisheries formore fishers for a longer time. Localmanagement regimes that clarify andlimit user rights will improve sustainabilityof fisheries. An increasingly commonsituation is some of the recentdevelopmental projects. These projectsare encroaching large areas of coastalhabitats, such as seagrass beds, coral reefand mangrove forests, thus permanentlyeliminating nursery grounds for fisherieswithout mitigation measures.

Population growth and Poverty:Population growth in coastal areasintensifies resource use conflicts in many

Fish Production in India (lakh tones)

Coastal areas all overIndia are developing

rapidly because, peoplelike to live near the sea.The consequence is that

beaches, coastal landareas, and near shorecoastal habitats are ingreat demand and are

being utilized for a widevariety of conflicting

human uses includingindustry, construction,

dumping, boat landings,tourism, and habitation

12

BIODIVERSITY

ways. The coastal areas are under increasing pressure fromrapid population growth and the consequent concentration ofdevelopment activities in the coastal strip (Whittingham et al.,2003). More than 25 percent of Indian population lives incoastal areas because all major cities such as Mumbai, Chennaiand Kolkata are situated in the coastal region and most largeindustries are located close to the sea. In addition, the mostproductive natural ecosystems in the country situated alongthe coast and support many people. As the population densityincreases the quality of life and the environment declines forthe average person living in a coastal area.

Illegal Activities: The destruction of coastal habitats and declineof fisheries are to a large extent due to the proliferation ofillegal activities. While national policies and laws existprohibiting a wide range of activities in coastal and marineareas, without swift and enforcement of these laws, illegalactivities still continue. Examples of illegal and damagingactivities that can be addressed by coastal management include:

• Use of destructive and illegal fishing methods such as blastfishing, poisons, super lights, and others such as intrusion ofcommercial fishing into traditional fishing grounds, lack ofregulations resulting in damaging construction anddevelopmental activities in the coastal zone;

• Conversion of mangrove and seagrass habitats to land orother uses resulting in decline of near shore catch;

• Harvesting of banned species including corals, whale sharks,manta rays, giant clams and other endangered marinespecies; and

• Habitat destruction from other sources.

Enforcement of different acts promulgated by the parliamentof India needs to be encouraged and become accepted as animportant means to improve the status and productivity ofcoastal ecosystems. Fisheries will improve significantly if illegalfishing is stopped. Public education and better enforcement

are two strategies that have proven to be effective.

Although it is a fact that the coastal areas from mean high tideto 500 m inland are protected by law and reserved as openaccess space where no building or private ownership is allowed(Coastal Zone Regulation), this law is not being enforced strictlyby many states. Enforcing this law will prevent overcrowdingand environmental degradation in coastal areas. Coastal landuse and coastal areas all over India are being developed rapidlysince people like to live and do business near the sea. Theconsequence is that beaches and coastal land areas are indemand and are being utilized for industry, construction,dumping, boat landings, recreation, habitation, and many otheractivities.

Illegal fishing methods, such as blast fishing that are known todestroy or shatter the physical structure of the coral reef, createconsiderable losses to society (Venkataraman and Wafar, 2005).The impacts of illegal and destructive fishing practices on theenvironment are long term and irreversible, with continuingreductions in net returns for all types of fishing methods.

Aquaculture Development: Aquaculture activity got a boostin the early 1990s in the coastal parts of India on account ofeconomic liberalization policies initiated by the Governmentof India. The increased production was both a result of increasedarea under expansion and increased productivity. Coastalaquaculture in India is mainly related to shrimp farming. Thecontribution of cultured shrimps to the total shrimp exportincreased from 48.78 percent in 1988-89 to 75.07 percent in1998-99. However, it suffered a setback with the SupremeCourt declaring it contrary to the Coastal Regulation Zonenotification and banning all aquaculture activities, excepttraditional and improved traditional within up to 500 m of theHigh Tide Line (HTL) in most coastal areas.

The primary concern in India related to aquaculturedevelopment is the conversion of coastal ecosystems, primarilymangrove, to fish, seaweed or shrimp ponds (Nanda Kumar etal., 2001). This activity has replaced original mangrove forestin the country. Another significant impact results from variouskinds of pollution generated by aquaculture because it isessentially a farming system that uses fertilizer, feeds, andchemicals. In concentrated form, they are detrimental to nearshore water quality, natural fisheries, and human health.Considering the environmental damages of aquaculture

13

BIODIVERSITY

practices, the Supreme Court of Indiabanned aquaculture within CRZ andentrusted the job of issuing clearance tothe farms for the existing/proposed farmsoutside the CRZ to the AquacultureAuthority constituted as per thedirections of the Supreme Court of Indiawith headquarters at Chennai. To assistthe Authority in regularizing shrimpfarming, State level committee andDistrict level committees have beenconstituted in the State.

Inadequately regulated coastaldevelopment has resulted in severalissues: Adequate measures are essentialto create an open space for access, tominimize negative impacts on the nearshore marine systems such as reefs and

or near the beach. Although sandybeaches normally replenish themselvesafter a storm, once a beach wall orperpendicular jetty is in place, the naturalmovement and return of the sand isprevented. Thus there is a need toprevent all construction in the coastalareas. Examples of this problem caneasily be seen along developed shorelinessuch as on Lakshadweep Island or insome islands of Andaman, where naturalbeaches have disappeared; squattingshould also be prevented in the coastalareas. Such settlements are difficult toget rid of. They have the excuse that theyare poor, landless people with fewalternatives. Unfortunately, thecontinued prevalence of squatting onlyencourages more people to do the same,mostly detrimental to coastal and beachareas and any hope of environmentalintegrity.

(To be continued……)

seagrass beds, to minimize erosioncaused by structures on the beach, toeffectively control dumping into the sea,and to create a visually attractive area,uncluttered with haphazard devel-opment. Increased pollution in near shorewaters is often emanated from shorelineareas where there is a lack of control onactivities. Domestic waste generated inshoreline communities enters in to thesea. Septic systems constructed too closeto the beach drain in to the sea andpollute the near shore areas, especiallyin densely populated areas and islandssuch as Lakshadweep and Andaman.Dumping of solid waste in near shoreareas is a related problem. Constructionactivities near the beach and sea oftencause silt to wash into marine waters andsmother reefs and seagrasses or affectnear shore fisheries.

Erosion of beach sand, usually resultsfrom the construction of structures on

Increased pollution innear shore waters is oftenemanated from shorelineareas where there is a lack

of control on activities.Domestic waste

generated in shorelinecommunities enters in to

the sea. Septic systemsconstructed too close tothe beach drain in to thesea and pollute the nearshore areas, especially indensely populated areas

and islands such asLakshadweep and

Andaman

14

ANALYSIS

Marketing Analysis ofMilk Production in

Shirpur Tehsil of Dhule Districtof Maharashtra (India)

By Vijay Gorakh Patil*

Introduction

Dairy farming has been recognized as animportant source of income and is moreremunerative in comparison to cropproduction in India. Milk production inIndia is predominantly the domain ofsmall farmers in mixed farming system.Scientific dairy management helps thefarmer to channelize his limited resourcesto maximize returns from his dairy farm.

The importance of dairying lies not onlyin products but also it brings aboutsignificant changes in socio-economicstructure of rural economy. The NationalCommission on Agriculture (1976)observed dairying as an additionalenterprise for improving the status of

profession of their own choice. Thelargest part of Indian population isengaged in agriculture as a mainoccupation. However, the mainoccupation of agriculture does not seemto meet the need of an individual, as thepressure on land holdings is mountingday-by-day due to population explosion.A subsidiary income source is necessaryto contemplate with the situation, so thatour farmers can achieve enough foodsecurity. Indian farmers have adoptedanimal husbandry as a subsidiaryoccupation. Dairying is recognized as thebest alternative to provide employmentto rural people in order to improve theirliving condition. Dairy enterprise providesready cash in hand to rural householdsfor fulfilling their daily requirements.Therefore, it was essential to bring thecost structure of milk production in frontof dairy farmers enabling them to decideat what price the milk should be sold.The investigator also focused on the factthat the farmers should understand howthe input cost would be reduced and theprofit increased.

Selection of Respondents

Primary data were collected from therandomly selected farmers from eightvillages of Shirpur Tehsil. Thus a sampleof 50 dairy farmers was drawn for thestudy.

The random sample survey study on fifty dairy farmers from eight villages ofShirpur Tehsil of Dhule District of Maharashtra (India) was undertaken to knowthe cost of production of milk in the study area. The total cost of milk productionper cow/buffalo was Rs. 113.87 in which the variable cost was 83.76 percent(Rs. 95.38) and remaining Rs. 16.24 percent (Rs. 18.49) was fixed cost. In variablecost, the cost of feed stuff was 73.39 percent (Rs. 70). Labour cost was 15.73percent (Rs. 15.00), the cost of medical treatment was 2.62 percent (Rs. 2.50)and interest on working capital was 8.26 percent (7.88). Finally it was foundthat the cost of milk was Rs. 9.10 per liter in the study area.

rural masses especially weaker sectionsconsisting of small, medium & landlesslaborers. It is therefore, becomesessential to examine the production costof milk.

Explanation of the problem

In this research the investigator hadstudied the production cost of milk at thefarmer level in Shirpur Tehsil of DhuleDistrict of Maharashtra state (India). Theinvestigator had selected fifty dairyfarmers from eight villages from ShirpurTehsil, District Dhule. In thequestionnaire, questions related to fixedand variable cost were asked. It wasdistributed to dairy farmers for collectingprimary data. The collected data wasanalyzed by using the statistical toolpercentage and conclusions were drawn.

Objectives of Assignment

To estimate the cost of milk production.

Hypothesis

The hypotheses were formulated fortesting through empirical data on theobjectives of the present study.

The cost of milk production would beestimated.

Significance of the Study

Our country being the largest democraticone in the world, any person can have a

15

ANALYSIS

Preparation of InterviewSchedule

A structural interview schedule,consisting of relevant questions relatedwith the objectives of the study wasprepared. Every precaution was taken tokeep the language simple so as to getdesired responses from the respondents.The interview schedule was developedin Marathi (Local Language) for betterunderstanding for the dairy farmers. Itcontained questions related to the costof milk production, cost of feed etc.

Pre-testing of Interview schedule

The Interview schedule so developed waspre-tested for its accuracy, simplicity andpracticability with a group of 10 dairyfarmers in village Dahiwad. Consideringthe experience of pre - testing, relatedquestions were put together to haveconsistency in response. The language ofa few questions was modified for easein understanding and eliciting accurateresponse. Sufficient number of copies ofinterview schedule were then preparedand used for collection of data.

Collection of Data

The primary data were collectedpersonally from the sample respondentby adopting personal interview methodwith the help of interview scheduledeveloped for this purpose. Therespondents were contacted at their timeon farm as per their convenience. Therapport was established by explainingthem the objective of study.

Tabulation and Analysis of data

The data were analyzed on the basis ofspecific objectives of the study andhypothesis formulated for the study. Thedata in the primary table were used forthe categorization of parametersaccording to the objective of the study,preparation of secondary table and theapplication of statistical tools.

The statistical tools used in the presentresearch study were Arithmetic mean,percentage.

Result and Discussion

Research methodology of this study ispresented in the following subheads.

The cost of milk production included

a) Fixed cost as well asb) variable cost.

Fixed cost, includes i) Depreciation onshed ii) Depreciation on Live Stock iii)Depreciation on miscellaneous items andiv) Interest on fixed capital. Variable costincludes. – i) Cost of feed stuff ii) Labourcost iii) Cost of treatment and iv) Intereston working capital. The cost of milkproduction was Rs. 9.10 per liter in thestudy area.

The total cost of milk production per farmwas Rs. 113.87 in which the variable costwas 83.76 percent (Rs. 95.38) andremaining 16.24 percent (Rs. 18.49) wasfixed cost. In variable cost, cost of feedstuff was 73.39 percent (Rs.70), Labourcost was 15.73 percent (Rs. 15.00), thecost of treatment was 2.62 percent (Rs.2.50) and interest on working capital was8.26 percent (Rs. 7.88). From the abovediscussion it was concluded that the costof labour and cost of feed stuff was themain component in the production of milkin the study area. These findings are alsoin conformation to Prashant Khare (2003)

Summary

1) Cost of Milk production- The Costof milk production was 9.10 per liter inthe study area. The total cost of milkproduction per farm was Rs. 113.87 inwhich the variable cost was 83.76percent (Rs. 95.38) and remaining 16.24percent (Rs.18.49) was fixed cost.

S.N. Particulars Milk Production Percentage toCost (Rs.) Total

1 Fixed Cost 16.24

a) Depreciation on cattle shed 1.66 08.98

b) Depreciation on Livestock 8.33 45.05

c) Depreciation on Misc. Expenses 1.00 05.40

d) Interest on Fixed Cost 7.50 40.57

Total Fixed Cost 18.49 100.00

2 Variable Cost 83.76

a) Cost of feed stuff 70.00 73.39

b) Labour Cost 15.00 15.73

c) Cost of treatment 02.50 2.62

d) Interest on working capital 07.88 8.26

Total of Variable Cost 95.38 100.00

Total Cost of Production 113.87 -

Value of dung 10.00 -

Net Cost of Production 103.87 -

Milk Production Per day ( Lit) 12.5 -

Per Liter Cost of Production 9.10 -

Table 1: Cost of milk production

Conclusion and suggestion

The variable cost was the maincomponent of the cost of production. Invariable cost, the cost of feed stuff andthe cost of Labour are the main.Therefore effort should be made toensure that farmers share some of theirland in the cultivation of the fodder andproper management of labour should bethe focus.

Implications

1. The study analyzed the cost of milkproduction which will help the dairyfarmers to minimize the variable costand to increase the profit.

2. The investigation made it clear thatlow price is the major problem of thefarmers. The investigation should helpthe farmers to produce better qualityof milk which will be given high price.

3. The study would be helpful foremployment generation

4. The findings of the study would behelpful in deciding “At what cost themilk should be sold?”.

5. The findings of the study would behelpful in reducing the input cost.

*Vijay Gorakh Patil-Ph. D. ResearchFellow YCMOU, Nashika

16

MARKET

A Road Map to Wholesale MarketInfrastructure – PPP Mode

By Satyaveer Singh* and Subah Singh Yadav**

Background

As per the Census (2001), about 228million people in rural India (equivalentto 56 percent of the total labor force) arefarmers and agricultural laborers. TheNational Sample Survey Organization(NSSO) in 2005 had estimated that whilefarming households accounted for 60percent of households in rural areas, directincome from farming activities accountedfor over 50 percent of farm householdincomes. As agricultural growth appearsto be decelerating, policy makers areconcerned about its impact on theNational economy. The average annualrate of growth of agricultural GDPdeclined from 3.4 percent during 1985/86 - 1994/95 to 1.8 percent in 1995/96- 2002/03.

Need for a Holistic DevelopmentApproach and Significance of Agricultural

Markets

In such a situation a vibrant agriculturalsector is needed not only for raising theincome levels of the people dependanton agriculture but also for acceleratingthe growth of other sectors of theeconomy as both are mutuallyreinforcing. At the current stage of India’sdevelopment, while looking at theoptions for strengthening agriculturalsector, there is a need to addressagriculture in a holistic manner coveringproduction, processing, marketing,distribution, utilization and trade of food,feed and other agricultural products. Theagricultural development strategy mustaddress not only farmers but all otherstakeholders engaged in marketing,trade, processing and agri-business, i.e.total supply chain right from ‘the Farmgate to the Food plate’. In this context,

agricultural marketing system obviouslyassumes added importance.

Agricultural marketing system is thecritical link between farm productionsector on the one hand and non-farmsector, industry, and urban economy onthe other. Apart from performing physicaland facilitating functions of transferringthe goods from producers to consumers,the marketing system also performs thefunction of discovering the prices atdifferent stages of marketing andtransmitting the price signals in themarketing chain. An efficient marketingsystem helps in optimization of resourceuse, output management, increase infarm incomes, widening of markets,growth of agro-based industry, additionto national income through valueaddition, and employment creation. Theissues and concerns in marketing relate

17

MARKET

mainly to the performance (efficiency)of the marketing system, which dependson the structure and conduct of themarket and infrastructure available forperforming marketing functions. These,in turn are influenced by the extent andform of government intervention.

Classification of AgriculturalMarkets

Markets in India can be broadly groupedunder three main categories – primary,secondary and terminal. Markets differconsiderably from one another as regardsthe functions they perform, the facilitiesthey offer and the services they render.

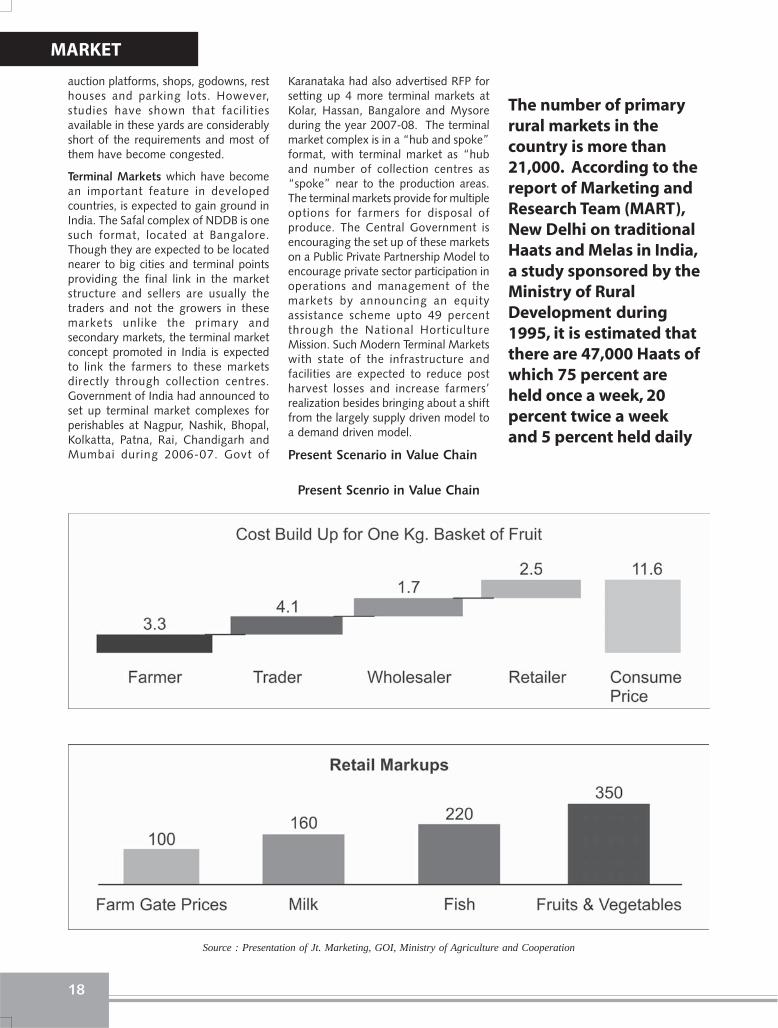

Rural Primary Markets include mainlythe periodical markets known as haats,shandies or painths and fairs which areestimated to be more than 21,000 to amaximum of 47,000 in number. Theseare located in rural and interior areas andserve as focal points to a great majorityof the farmers – mostly small andmarginal for marketing their farmproduce and for purchase of theirconsumption needs. These markets mayalso function as collection canters toadjoining secondary markets and aredevoid of most of the marketing facilitiesand look like strips of land serving asmeeting place between sellers and

buyers. The commodities collected inthese markets find their way to thewholesale assembling markets.

The number of primary rural markets inthe country is more than 21,000.According to the report of Marketing andResearch Team (MART), New Delhi ontraditional Haats and Melas in India, astudy sponsored by the Ministry of RuralDevelopment during 1995, it isestimated that there are 47,000 Haatsof which 75 percent are held once aweek, 20 percent twice a week and 5percent held daily. The study indicatesthat on an average, one haat caters toapproximately 14 villages. Therelationship between the distribution ofvillages according to population or rangeand the availability of haats, smallestvillage (population less than 500) heldthe fewest haats (only 1.6 percent).Majority of haats (47.9percent) are heldin the largest villages (those with apopulation of over 5000 persons). Thestudy reveals that nearly 2/3 of the haatsare held at a distance of 16 kms are more,23 percent are held at 6 to 15 kmsdistance and 9 percent within a distanceof 1 to 5 kms. The amenities and facilitiesavailable in these haats are far fromsatisfactory.

Wholesale/assembling markets or thesecondary markets numbering 6359constitute the cardinal link in the marketstructure in the country. Although betterorganized than the primary markets,these markets present divergent pictureswith regard to facilities offered andservices provided. Most of these arelocated in the district and talukheadquarters, important trade centresand nearby railway stations and performassembling and distribution functions. Inmost of these markets, a number ofcommodities are traded. Specializedsingle commodity markets are not manyexcept a few markets for cotton, jute,oilseeds, fruit and vegetables. The layoutof most of the secondary markets isinconvenient and unsatisfactory. Thebusiness is conducted according tomarket practices established by age oldcustoms, or as per the regulations ofAPM committees wherever regulated.These markets play an important role indetermining the prices of agriculturalproduce assembled there and as suchhave a governing impact on terms oftrade between agriculture vs. othersectors of economy. The users of thesemarkets, either buyers or sellers have topay fee to the managers of the marketplaces. Facilities in the places varyextensively. Nearly 2/3 of market yardsand sub yards were laid out initially onvast land area with such facilities as

Specialized singlecommodity markets arenot many except a fewmarkets for cotton, jute,oilseeds, fruit andvegetables. The layout ofmost of the secondarymarkets is inconvenientand unsatisfactory. Thebusiness is conductedaccording to marketpractices established byage old customs, or as perthe regulations of APMcommittees whereverregulated

18

auction platforms, shops, godowns, resthouses and parking lots. However,studies have shown that facilitiesavailable in these yards are considerablyshort of the requirements and most ofthem have become congested.

Terminal Markets which have becomean important feature in developedcountries, is expected to gain ground inIndia. The Safal complex of NDDB is onesuch format, located at Bangalore.Though they are expected to be locatednearer to big cities and terminal pointsproviding the final link in the marketstructure and sellers are usually thetraders and not the growers in thesemarkets unlike the primary andsecondary markets, the terminal marketconcept promoted in India is expectedto link the farmers to these marketsdirectly through collection centres.Government of India had announced toset up terminal market complexes forperishables at Nagpur, Nashik, Bhopal,Kolkatta, Patna, Rai, Chandigarh andMumbai during 2006-07. Govt of

Karanataka had also advertised RFP forsetting up 4 more terminal markets atKolar, Hassan, Bangalore and Mysoreduring the year 2007-08. The terminalmarket complex is in a “hub and spoke”format, with terminal market as “huband number of collection centres as“spoke” near to the production areas.The terminal markets provide for multipleoptions for farmers for disposal ofproduce. The Central Government isencouraging the set up of these marketson a Public Private Partnership Model toencourage private sector participation inoperations and management of themarkets by announcing an equityassistance scheme upto 49 percentthrough the National HorticultureMission. Such Modern Terminal Marketswith state of the infrastructure andfacilities are expected to reduce postharvest losses and increase farmers’realization besides bringing about a shiftfrom the largely supply driven model toa demand driven model.

Present Scenario in Value Chain

Source : Presentation of Jt. Marketing, GOI, Ministry of Agriculture and Cooperation

Present Scenrio in Value Chain

The number of primaryrural markets in thecountry is more than21,000. According to thereport of Marketing andResearch Team (MART),New Delhi on traditionalHaats and Melas in India,a study sponsored by theMinistry of RuralDevelopment during1995, it is estimated thatthere are 47,000 Haats ofwhich 75 percent areheld once a week, 20percent twice a weekand 5 percent held daily

MARKET

19

MARKET

Cost-plus model at every stage in terms of share of farmers, trader wholesalers,retailer in consumer’s rupee.

Terminal Market Eligibility

Terminal Market Complex project is built, owned and operated by the selected PrivateEnterprise (PE) through Competitive Bidding process. PE includes individual orconsortium, Group of Farmers/Growers/Consumers/Producer Organisations/ProducerCompany, Partnership/ Proprietary firms, Companies, Marketing Boards, Public SectorUndertaking, Co-operatives, registered NGOs empanelled with GOI/State Govt./Planning Commission, recognized Self Help Groups under the schemes of GOI/StateGovts. and other registered bodies engaged in production and trading of agriculturalproduce. The PE could also be a consortium of entrepreneurs from, inter-alia, agri-business, cold chain, logistics, warehousing, agri-infrastructure and relatedbackground.

Infrastructure at Terminal Markets

Source: Guidelines of Terminal Market, Ministry of Agriculture and Cooperation, GoI

Expected Outcome from the Modern Terminal Markets

Parameters Present Status Expected Outcome

Trade Transparency Non Existing Transparent Auction through Electronic Auction System

Cold Chain Infrastructure Very Poor Setting up of cold storage at each market ranging from 2000 to15000 MT capacity

Backward-forward linkages No Linkages Minimum of 20 collection centers nearer to the farmers field willbe set up. The farmer will have alternative options to supply tothe supply chains, processing, export of commodities etc.

Monopoly of APMC Markets Prevailing Farmer is provided with alternative option of taking his produceto terminal markets

Multiple intermediaries Prevailing Length of the chain of commission agents will substantially bereduced with an ideal situation of eliminating thecommission agents completely

Beneficiary farmers - 16000 to 20000 farmers under each terminal market

Share of the farmer in Varies from 30 to 60% Farmer’s share is expected to increase to 50 tothe consumer price for perishables 70% of the consumer price

depending on thelocation, season,demand and supply etc.

Private Enterpriseincludes individual orconsortium, Group ofFarmers/Growers/Consumers/ProducerOrganisations/ProducerCompany, Partnership/Proprietary firms,Companies, MarketingBoards, Public SectorUndertaking, Co-operatives, registeredNGOs empanelled withGOI/State Govt./PlanningCommission, recognizedSelf Help Groups underthe schemes of GOI/StateGovts. and otherregistered bodiesengaged in productionand trading ofagricultural produce

20

MARKET

Wholesale Facilities:

• Cash and carry

• Transporters shops

• Exporters shops

• ATM Counters

• Price display boards

• Conference rooms

• Multipurpose halls

• Counseling centre

• Laboratories

• Research centre

• Electronic auctioning

• Packaging units

• Electronic grading and sorting lines

• Labeling of produce

• Pre-cooling unit

• Cold storage

• Ripening chambers

• Washing areas

• Quality testing facility

• Temperature controlled warehouses

Non Marketing Services:

• Freight consolidation

• Logistic centres

• Fertilizers and manure shops

• Nurseries/plant shops

• Storage area for plastic crates, trolley/forklifts, wooden palates

• Information cell

• Fire fighting services

• Maintenance and repair shops

• Rain water harvesting

• Garbage composting

• Sewage treatment plant

Expectation from the PrivatePlayer

1. Establish collection centre in thecatchment area of the terminalmarket.

2. Provide cleaning, washing andsorting (Grading) facilities at thecollection centre

3. Provide transportation facilities fromCC to TM or CC to Forward Marketsand Processing Units

4. Provide Transparent Electronic uctionSystem in TM and Electronic Display

Boards at Collection Centre

5. Plastic crates for Fruits and Vegetableon reasonable rent

6. Agri-clinic facilities for goodagriculture practices, input seeds,fertilizer and pesticides etc.

7. Support in crop insurance andfarmers insurance

8. Provide a corpus fund for educationof farmers’ kids (1% less rate ofinterest than to commercial banks)

9. Grading and certification laboratoryfacilities at TM

10. Cold storage and cool chainmanagement at TM

11. Ripening Chambers/VHT plant etc.as per the need of the commodityspecific TM

12. Organic Solid Waste ManagementPlant for de-bio-gradation of wastein organic compost

13. Market Intelligence System at TM fordemand and supply analysts andprice discovery mechanism

14. World class hygienic environment inthe TM

15. E-trading facilities at TM

*Policy Change could delay the project; people may not be so clear with new processes which will affect their ability to utilize the solution;Possibly new process will not be fully integrated initially; Possible void if new process don’t fully cover all contingencies.

Risk Categories Phase of Dominance Allocation of Risk

Land Acquisition Project Development State Govt/Private party

Political and Social Risk Throughout Project Cycle State Govt/Private party

Delays in Project Development Project Development Private Party -Design- Planning Risk

Project Construction Risk Construction Period Private Party

Project Cost risk/Cost Over-Runs Construction Period Private Party

Technology Risk Construction/Operations Period Private Party

Regulatory & Administrative Operation Period State Govt/Private party

Commercial Risk Operation Period Private Party*Business Process and Policies

Operation and Maintenance Operation Period Private party

Financial Risk Operation Period Private PartyInterest Rate, Tax Rate, Inflation

Termination Risk Operation Period Private Party

Environment Risk Construction/Operation Period State Govt/Private party

21

MARKET

Expectation from the Government

1. Single license to operate in the state

2. Autonomy in commercial operation ofTM

3. Single point levy/Collection of Marketfee

Public Private Partnership Model(PPP)

Infrastructure shortages are proving akey constraint in sustaining andexpanding country’s economic growthand ensuring that all citizens are able toshare its benefits. To meet this challenge,the Government is committed to raisinginvestment through Public PrivatePartnership activities in all keyinfrastructure sectors includingagricultural marketing. It is importantthat to understand the PPPs are notcatch-all solutions to the persistentdifficulties of under-investment and lackof resources for development. PPPs areoften complex transactions, needing aclear specification of the services to beprovided and understanding of the wayrisks are allocated between theGovernment and Private Sector. Most ofthe PPPs are in nature of long termproject and therefore, Government hasto develop and manage the relationshipwith the private providers to overcomeunexpected events that can disrupt eventhe best design contracts. And ultimately,PPPs always involve projects for which,in the eyes of the citizens, governmentultimately bears responsibility- even if thetask of delivery has been contacted out.

Project Risks and allocation ofRisks

1. Regulatory

2. Political

3. Commercial

4. Financial Risk

5. Market Risk

6. Land Acquisition Risk

7. Construction Risk

8. Technology Risk

9. Cost Overrun Risk

10. Force Majeure Risk

11. Operation and Maintenance

Risk Mitigation Steps

Identifying the events or actions whichaffect the viability of the project. In caseany such event occurs, the effect of thesame on the cost and time of the project.Identify and allocating the risk to theparty who can manage it best. Steps oractions which can be taking to reducethe chances of the event occurring. Costsof addressing the risk have to bedetermined.

* Satyaveer Singh, MIS Expert, AsianDevelopment Bank, TA-4890 IND,Mainstreaming of Public Private Partner-ships at State Level

** Subah Singh Yadav, Chief Manager,Bank of Baroda, Zonal Officer, Lucknow

PPPs are oftencomplex transactions,needing a clearspecification of theservices to be providedand understanding ofthe way risks areallocated between theGovernment andPrivate Sector. Most ofthe PPPs are in natureof long term projectand therefore,Government has todevelop and managethe relationship withthe private providersto overcomeunexpected eventsthat can disrupt eventhe best designcontracts

22

FOCUS

Agriculture continues to play apredominant role in influencingthe overall performance of the

Indian economy. In spite of theadvancement in chemical, biological andinformation fields, there has been adistinct slowdown in agricultural growthduring the past two decades. By the year2003-04, only 35.3 percent of the netsown area of 140.9 million hectares wasutilized for double cropping. Further,even after five decades of planning, cropdiversification in favour of remunerativecash crops is quite insignificant, whichcan be understood from the highproportion of area under different foodgrain crops1. Between 1990-91 and2006-07, the annual rate of growth offood grains production at 1.2 percentwas lower than that of population at 1.9percent. The share of agriculture in theGDP has registered a steady decline from36.4 percent in 1982-83 to 18.5 percentin 2006-07. Extension and other supportservices to crop cultivation haveweakened. All these have resulted inpoor performance of the sector leadingto agrarian distress, manifested throughmigration, farmers’ suicides and reduced

participation in agricultural activities.Keeping this in view, an attempt has beenmade to focus on the current status offarmers and the likely strategies toaddress the constraints to development.

Agrarian Distress

There are many dimensions of thepresent agrarian crisis. In terms ofpopulation, India stands at number two,but in terms of area, it stands at numberseven in the world. By the year 2003-04, only 67.3 million hectares, which is35.3 percent of the total cropped area,were under non-food grain crops2. Whilethe workforce in agriculture hasremained more or less stagnant3, itscontribution to nation’s GDP has beensteadily declining. It has also resulted ina declining ratio of worker productivityin agriculture to non-agriculture. Onaccount of an increasing number ofholdings and constant, and evendeclining cultivable land area, the burdenof farmers has been increasing4. Theland-to-labour ratio as well as incomegains per capita have been reducingsignificantly.

India, in the second decade of planning,saw the advent of the green revolution.It encouraged undertaking massiveinvestments in the agriculture sector andpursuing policies to accelerate thegrowth process. The expansion inirrigation, impressive technologicaladvances and policies, and institutionalsupport agriculture led to a sustainedoverall increase in agriculturalproduction. The decade of the 1980s sawthe diversification of agriculture fromcereal to cash crops like cotton, oilseedsand also to horticulture and livestock.Thus, the major policy goals during theperiod between the 60s and 80s wereon achieving self-sufficiency in foodgrains production, but it lost its flamestowards the last part of the 80s. Since1982-83 the public investment inirrigation, rural infrastructure andagricultural research has started decliningand this declining trend dampened thegrowth perspective in agriculture sector.As a result, some of the positive gains ofgreen revolution got erased and theconstraints arising from the patterns ofland ownership5 and unequal access toirrigation water began to surface.

Agrarian Crisis:

By Dr. B.B. Sahoo*

Distress & Suicide

23

FOCUS

The crisis has been exacerbated furtherby rapid environmental degradation andplateauing of the existing agriculturaltechnology. These factors impingeadversely on the production potential ofthe agricultural sector. The slowing downand stagnation of agricultural growth hasadversely affected the income andemployment of a vast majority of ruralpeople dependent on agriculture. Scantyirrigation facility for the agriculture sectoris another cause of concern. Out of thetotal 190.6 million hectares of gross sownarea, only 76.8 million hectares of landhave irrigation facilities and theremaining 113.8 million hectares havebeen cultivated in rain-fed conditions bythe year 2003-04. Unlike irrigatedagriculture, rain-fed agriculture ischaracterized by low levels ofproductivity. The existing irrigated areasare also experiencing serious water stressas both reservoir and ground waterresources are depleting in many parts ofthe country. The growing demand fordrinking water and other needsassociated with rapid urbanization andindustrialization further increases stresson available irrigation resources.

Soil erosion, water logging and shiftingcultivation also cause land degradation.Similarly, excessive and unbalanced useof fertilisers and pesticides reduces soilfertility due to soil nutrient depletion.Among states, there are a few peakachievers in agricultural productivity. Forinstance, the worker’s productivity inPunjab at Rs.35,087 during 2004-05 was7.2 times that of Bihar and 5.3 times thatof Madhya Pradesh. The workers’productivities in 11 major states arebelow the national average ofRs.12,3716. Thus, regional disparity isanother factor increasing agrariandistress. This is further exacerbated bythe growing differences in workers’productivity in agricultural activities andnon-agriculture activities. For instance,at an all India level, the workers’productivity in non-agricultural activitiesat Rs.61,432 was 4.96 times higher thanthat of agricultural activities at Rs.12,371in the year 2004-057. All the more,income from agriculture is increasinglybecoming inadequate to meet the basicconsumption requirements of the farmfamily and it is more so for marginalfarmers.

Since the early 90s, in order to benefit

from global trade, some farmers haveembarked on the production ofremunerative cash crops withoutadequate knowledge on grades andstandards. As big farmers are the mostimportant information source for thecommon farmers, some of the smallfarmers are tempted to cultivate highvalued commercial crops. Because of theimplied investment requirements, thesechanges have tended to exclude most ofthe small farmers from participating inmarket growth. It is a fact that everyfarmer wants to sell his produce near thetop price and when he is unable toachieve the goal of selling his produce,he becomes confused and this confusionleads to frustration. Many a time, whenthe prices of his produce sinks8, he findsit difficult to manage the situation.Further, adverse weather conditions,unstable markets and poor profit marginsare weakening the ability of farmers inproducing traditional crops.Inappropriate application of inputs mix,ignorance on technical know-how andspurious use of fertilizer and pesticideadd to farmers’ woes. Inappropriate farmcredit policy, support services andinfrastructure base further accentuate thesituation. As a result, most farmers arelooking for alternatives. As the cost ofcultivation of most of the commercialcrops are relatively high, shortfall in yieldand price of these crops has broughtmisery to the farmers in the form ofincreasing debt burden, distress sale andeven, the extreme step of committingsuicide. Some such incidents have beenrecently witnessed in states likeMaharashtra, Andhra Pradesh andKarnataka. On the overall, agrariandistress is increasing.

Studies on Agrarian Distress

Of late, some studies on agrarian distresshave been conducted in the country.Major factors common to most of thefindings on increasing agrarian distressare the following:

Crop Related: Based on their study, Rao& Suri9 have shown that farmers inAndhra Pradesh, knowing well the risksinvolved in the cultivation of cotton andchillies, had taken up the cultivation ofthese two crops. Every year, they wereloosing one or the other crop either dueto bad monsoon, lack of water or pestattack. They were not able to recovertheir investments in the cultivation of

these crops. Both paddy and cottonshowed negative returns and chillies gavemarginal return. While estimating loss,it was observed that small farmersfollowed by marginal farmers sufferedthe most. As the small and marginalfarmers are more vulnerable to risk anduncertainty, when crop fails, debt burdengets accumulated and they findthemselves in a difficult situation.

Credit Related: Rural areas are lessorganized in terms of available financialproducts. Low demand for credit, no/less documentation of property and smallsized loan demand by the rural customersmake the fund flow costly. A high costof handling transactions by banks andincreased travel requirement bycustomers (bankers also) furtheraggravates the situation. As a result, thenumber of bank branches in rural areashas been declining. For instance, in1991, there were 35,206 rural branches,which was 58.4 percent of the total bankbranches in the country, but in 2006, itsnumber decreased to 30,579, i.e., 44percent of the total bank branches. Inthe present liberalized era, farmers areinfluenced by the market forces ofdemand and supply and have startedcultivating commercial crops. When thecultivation of commercial crops requiresmore investment and bankers have beenshying away from financing agriculture,the farmers are forced to depend oninformal sources. But the high cost ofdebt servicing and harassment forrepayment of loans make the life of thecommon farmer miserable.

Marketing & Price Related: Marketingis another factor increasing farmers’worry. In the absence of secure and readymarkets, farmers are forced to opt fordistress sale. When the cost ofinvestment in producing agriculturalcommodities is rising and the profitmargin is declining, the farmer’s abilityto continue as a farmer gets shattered.In the process, the middlemen reap thebenefit and the common farmers areexploited. The Minimum Support Price(MSP) given to farmer is also found tobe inadequate. In some cases, farmerssell their produce to middlemen at lowerprices than the MSP.

Extension Services Related: Theextension services provided to farmersare very poor. They do not get properinformation on package of practices,

24

FOCUS

demand for their produces and benefitsof crop diversification. In a piece-mealmanner, they get the technical advicefrom the local input dealers, who are nottechnically qualified, and theirprescriptions are guided by the availablestock of seeds, fertilizers and pesticideswith them.

Other Factors: Besides cultivation, thesmall and marginal farmers do not haveany other option for earning theirlivelihood. Although from time to time,the Government has taken manydevelopmental initiatives, they areinsufficient to provide meaningful livingto the commoners. Many times, the realrecipients are not necessarily those whoactually require it. Other factors, whichadversely impact on the small farmers,are the following:

• No supplementary livelihood optionsin non-farm sector;

• Absence of safety nets for the smalland marginal farmers;

• Increasing expenditure on marriageand other social functions;

• Increasing expenditure on illness; and,

• Inadequate risk mitigation measures

State Causes

Andhra Pradesh Monsoon failure, increasing cost of cultivation, mono-cropping1, lower yield and non-remunerativeprices2

Punjab Crop failure, lower yield, mounting debt burden, alcoholism, domestic discord, drug addiction3

Maharashtra Crop failure, indebtedness, price fluctuation, poor extension network, decline in social position, conflicts,drug addiction, alcoholism and health problems4

Kerala Crop failure, drought, flood, water logging, deficit rainfall, pest attack, decline in yield, increase inexpenditure on fertilizer and pesticide, sharp drop in price of crops and decline in the quantity exported5

Table 1: Causes of agrarian distress and farmers’ suicides

Table 1 presents the major findings ofsome studies on increasing agrariandistress and farmers’ suicides in someselected states like Andhra Pradesh,Punjab, Maharashtra and Kerala.

Farmers’ Suicides

Suicides are normally influenced bystrains on an individual due to a varietyof psychological, social and economicreasons. The number of suicides in thecountry during the decade 1996-2006increased from 88,241 in 1996 to1,18,112 in 2006, which was 33.8percent. During 2006, collectively 7states, i.e., West Bengal, Maharashtra,Andhra Pradesh, Tamil Nadu, Karnataka,Kerala and Madhya Pradesh, witnessed71.4 percent of the total suicides in thecountry. Family problems and illness werereported as the main causes of suicide.While studying suicides by profession, itis observed that 41 percent of the totalsuicide victims were self-employedfollowed by housewives at 21.2 percent.Similarly, 69.9 percent of the total suicidevictims had an education up to themiddle level1.

Table 2 presents year-wise farmers’suicide rates during the period between2001 and 2006 in the top five states in

Year Chhatisgarh Maharashtra Andhra Pradesh Karnataka Madhya Pradesh

2001 6.97 3.65 1.98 4.74 2.27

2002 5.83 3.76 2.46 4.21 2.25

2003 4.93 3.84 2.31 4.58 2.46

2004 6.33 4.10 3.39 3.21 2.83

2005 6.29 3.82 3.13 2.94 2.19

2006 6.49 4.28 3.24 2.57 2.45

the country. It is observed from the tablethat during the period, farmers’ suiciderate was the highest in Chhatisgarh,followed by Maharashtra and AndhraPradesh. Experts say that rising cost ofinvestment, repetitive crop failure, highindebtedness, price volatility and distresssale are some of the factors increasingagrarian distress.

Table 2: Top five states with year-wise figure on farmers’ suicide(Farmer suicide rate per one lakh farmer population)

Source: National Crime Records Bureau; Sourced from the website

Soil erosion, waterlogging and shiftingcultivation also causeland degradation.Similarly, excessive andunbalanced use offertilisers andpesticides reduces soilfertility due to soilnutrient depletion.Among states, there area few peak achievers inagriculturalproductivity

25

FOCUS

A State-Wise Analysis

In order to understand the drivers ofagrarian distress and farmers suicides, 20major states are selected and based onthe incidence of farmers’ suicides, theyare divided into ‘distressed states’ and‘non-distressed states’. As the highestnumber of farmers’ suicides (in terms ofthe farmers’ suicide rate) has beenreported in the states of Chhatisgarh,Maharashtra, Andhra Pradesh,Karnataka, Madhya Pradesh, Punjab andKerala during 2001 and 2006, these 7states have been categorized as‘distressed states’ (DS). The remaining13 states have been considered as ‘non-distressed states’ (NDS).

While analysing area and productivity offood grain crops, it is observed that botharea and productivity have beendeclining in distressed and non-distressed

states. However, the decline in distressedstates is relatively high1. Similarobservations were seen in the case of theproductivity of food grain crops2. Table 3presents some selected parametersrelating to agriculture in both ‘distressed’and ‘non-distressed’ states. To avoidirregularities, three year average data, i.e.,from 2001-02 to 2003-04, has been usedfor the analysis. While analyzing perhousehold data, it is observed that in spiteof comparatively lower irrigated area,farmers in distressed states producerelatively more non-food grain crops.Further, the households in distressed stateshave the maximum increment in credit.When the situation is analysed from perhectare of land, it is observed that in spiteof lower area under non-food grain cropsand farm credit disbursement, the farmersin ‘non-distressed’ states could increasethe crop output.

Table 3: Selected parameters relating to agriculture in ‘Distressed’and ‘Non-Distressed’ states.

In order to understand the relativeimportance of factors influencingagricultural income of the farmers’households, a regression equation hasbeen fitted. In the absence of relevantinformation on value of crop output, thenet state domestic product (NSDP) atfactor cost from agriculture has beentaken as the proxy for the value ofoutput. Further, to arrive at the value ofcrop output per household, the NSDPfrom agriculture has been divided withthe total farmers’ household. Althoughthere are a large number of variables,which influence the value of crop output,in the present exercise, four variables,i.e., gross sown area, gross irrigated area,area under non-foodgrain crops andinstitutional credit, which impact the cropoutput the most, are considered as theindependent variables and a linearequation1 has been used for the analysis.

In the case of ‘distressed states’, all theselected variables, except amount ofcredit disbursed, are found to havesignificant association with the value ofoutput and collectively they explain 99percent of the variations in thedependent variable. While the grosssown area and area under non-food graincrops are found to be significant at 10percent level, gross irrigated area is foundto be significant at 5 percent level2.When all other factors are constant, anincrease in gross sown area by onehectare increases the value of agricultural

Per household

Value of crop output (Rs.000) 17.28 14.65 15.22

Gross Sown Area (Hectare) 1.51 1.09 27.81

Gross Irrigated Area (Hectare) 0.48 0.52 -8.33

Area under non-food grain crops 0.60 0.36 40.00(Hectare)

Institutional credit (Rs.000) 7.10 3.78 46.76

Per hectare

Value of crop output (Rs.000) 11.42 13.49 -18.13

Gross Sown Area (Hectare) 1.28 1.39 -8.59

Gross Irrigated Area (Hectare) 0.32 0.48 -50.00

Area under non-food grain crops 0.40 0.33 17.50(Hectare)

Institutional credit (Rs.000) 4.69 3.47 26.01

Particulars DistressedStates1

Non-Distressed

States2

% Change

As the highest numberof farmers’ suicides (interms of the farmers’

suicide rate) has beenreported in the states

of Chhatisgarh,Maharashtra, AndhraPradesh, Karnataka,

Madhya Pradesh,Punjab and Kerala

during 2001 and 2006,these 7 states have

been categorized as‘distressed states’ (DS)

26

FOCUS

output by Rs.720. Similarly, keepingother factors constant, when irrigatedarea increases by one hectare, the valueof agricultural output increases byRs.11,940. It is disturbing to note thatinstitutional credit, which is alwaysconsidered to be an important factorinfluencing output, has turned out to beinsignificant in influencing agriculturalincome. The inferences of such findingsare that either the farmers have beeninfluenced by a handful of progressivefarmers for the cultivation of cash cropsor they are influenced by the marketforces of demand and supply. Theinferences regarding credit may be thatfarmers in ‘distressed states’ are eitherproducing high valued non-food grainsin the land, which are not fit for theircultivation or not making proper end useof the credit. As a result, benefit-costratios in the cultivation of non-food graincrops are not remunerative. However,these observations are based on statelevel analysis. Location specific studiesin areas like the Vidarbha region inMaharashtra and the Telengana regionin Andhra Pradesh could throwmeaningful insight into these issues.

In ‘non-distressed states’ all the selectedindependent variables are found to havesignificant association with the value ofoutput and collectively they explain 74percent of the variations in thedependent variable. While gsa, gia andcrd are found to have positive associationwith the dependent variable, anfc isfound to have negative association.Keeping other factors constant, when thegross sown area is increased by onehectare, the agricultural income increasesby Rs.2,140 and when irrigated areaincreases by one hectare, value ofagricultural output would increase byRs.9,100. Similarly, when credit foragricultural purposes increases byRs.1,000, value of output increases byRs.2,100. However, the variable anfc isfound to have negative association withoutput, which infers that farmers in ‘non-distressed states’ may be producing non-food grain crops in the land, which arenot fit for the production of food grains.As a result, non-food grains cultivatedin non-distressed states are notprofitable. Further, the value of theelasticity for anfc is found to be (-) 0.04,which is very insignificant. When bothdistressed and non-distressed states arecompared in terms of productivity, it is

observed that per hectare yield in non-distressed states is 18.1 percent higherthan that in the distressed states. Table4 presents the details of the regressionresult.

Particulars Distress States Non-Distress States

Coefficient Std. Error Coefficient Std. Error

Intercept 2.26 9.20

Gross Sown Area 0.72*** 3.04 2.14*** 7.65