Embed Size (px)

DESCRIPTION

introduction to corporate restructuring

Citation preview

Corporate Restructuring

• Restructuring is a catch-all term, used by companies in trouble who need to change or risk losing business as well as successful ones who want to keep their edge.

• Many try to turn the business around by cutting jobs, buying companies, selling off or closing unprofitable divisions or even splitting the company up.

Restructuring

Bringing about a drastic or fundamental internal change that alters the relationship between different components of an organisation or system

Restructuring

Restructuring is the corporate management term for the act of reorganizing the legal, ownership, operational, or other structures of a company for the purpose of making it more profitable, or better organized for its present needs. Other reasons for restructuring include a change of ownership or ownership structure, demerger, or a response to a crisis or major change in the business such as bankruptcy, repositioning, or buyout. Restructuring may also be described as corporate restructuring, debt restructuring and financial restructuring.

Corporate Restructuring

• Corporate restructuring is the process of redesigning one or more aspects of a company. The process of reorganizing a company may be implemented due to a number of different factors, such as positioning the company to be more competitive, survive a currently adverse economic climate, or poise the corporation to move in an entirely new direction.

Symptoms for Restructuring 1. The market(s) perception about the organization is deteriorating. 2. The company has difficulties in paying or is unable to pay off its debts. 3. Sales are declining. 4. Stock price is falling. 5. New skills and capabilities are required to meet operational requirements. 6. Accountability for results are not clearly communicated and measurable

resulting in 7. subjective and biased performance appraisals. 8. Parts of the organization are significantly over or under staffed. 9. Organizational communications are inconsistent, fragmented, and inefficient. 10. Technology and innovation are creating changes in workflow and production

processes. 11. Significant staffing increases or decreases are contemplated. 12. Personnel retention and turnover is a significant problem. 13. Workforce productivity is stagnant or deteriorating. 14. Morale is deteriorating.

Reasons for restructuring• Globalization – pressure from markets; rise of Asian companies

especially Chinese and Indians;• Technological Innovation- the necessity of new technologies, lower

energy and raw material consumption, higher use of renewable resources;

• Research and Development – development of new and innovative products; broadening of product range especially high-tech products, specialties,

• Regulative – new and/or tougher regulations• Image – sector not well branded, image in society not good, sector

not attractive as career choices(Restructuring, Managing Change Competitiveness and Employment in

the EU Chemical Industry – Workshop - Sept, 2007)

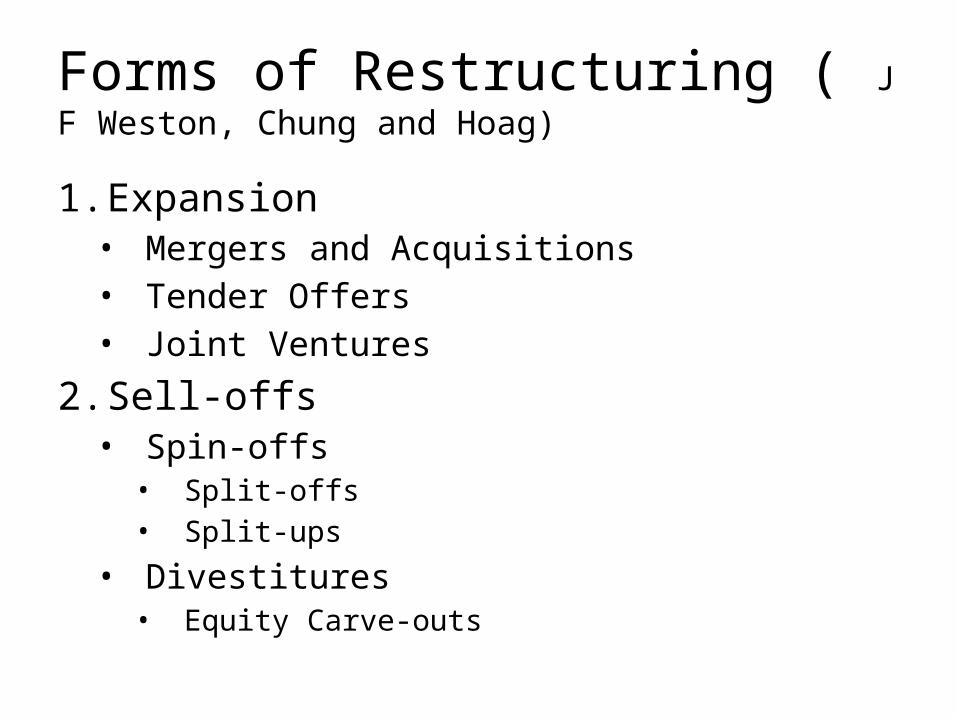

Forms of Restructuring ( J F Weston, Chung and Hoag)

1. Expansion• Mergers and Acquisitions• Tender Offers• Joint Ventures

2. Sell-offs• Spin-offs• Split-offs• Split-ups

• Divestitures• Equity Carve-outs

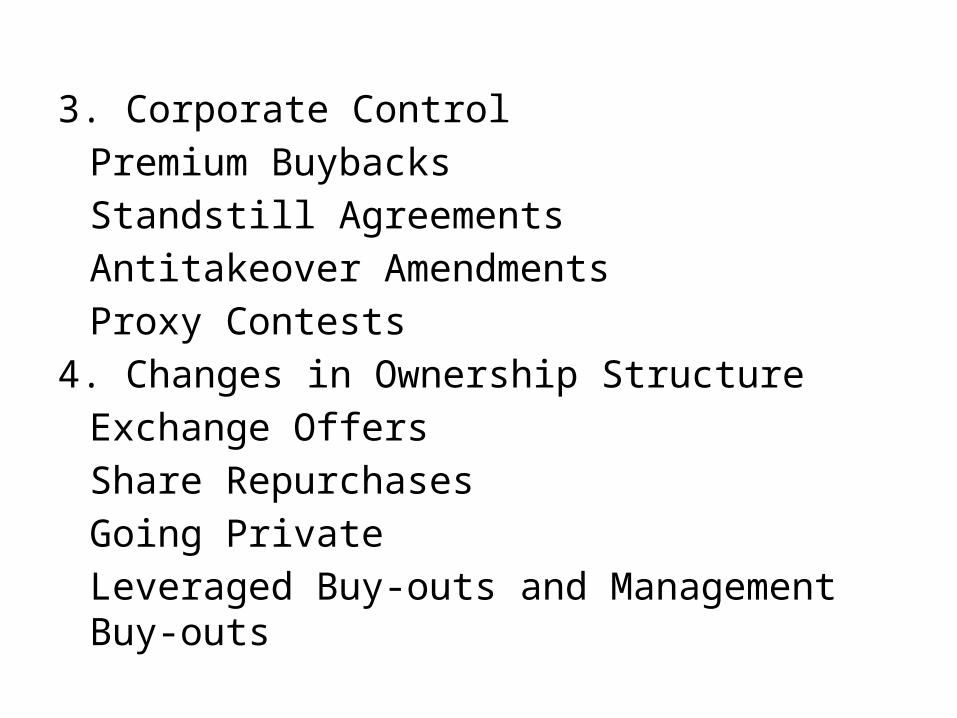

3. Corporate ControlPremium BuybacksStandstill AgreementsAntitakeover AmendmentsProxy Contests

4. Changes in Ownership StructureExchange OffersShare RepurchasesGoing PrivateLeveraged Buy-outs and Management Buy-outs

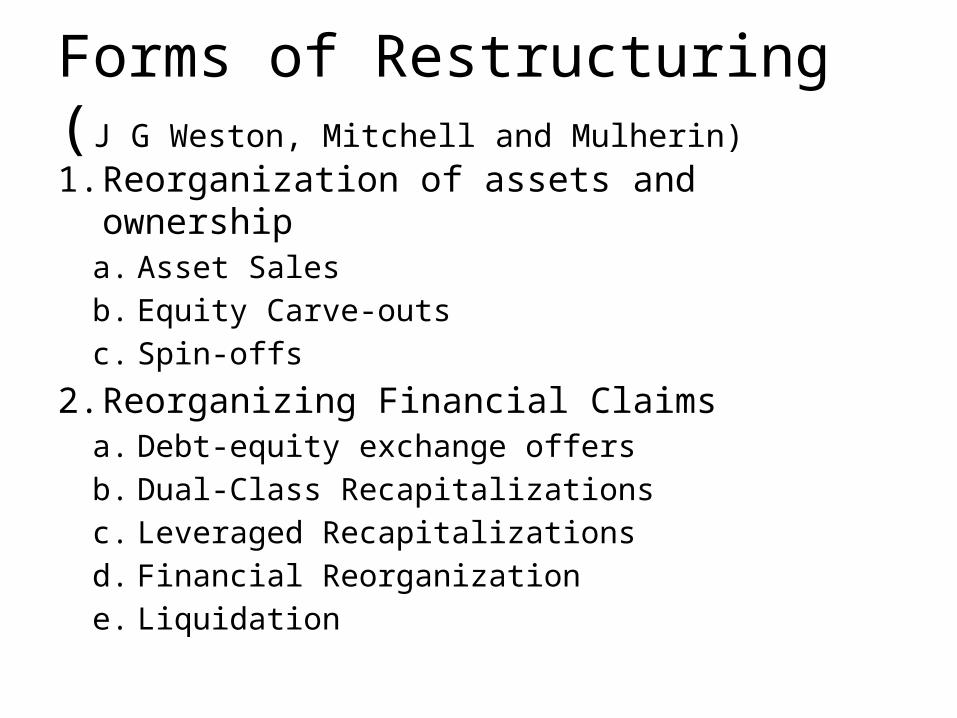

Forms of Restructuring (J G Weston, Mitchell and Mulherin)

1. Reorganization of assets and ownershipa. Asset Salesb. Equity Carve-outsc. Spin-offs

2. Reorganizing Financial Claimsa. Debt-equity exchange offersb. Dual-Class Recapitalizationsc. Leveraged Recapitalizationsd. Financial Reorganizatione. Liquidation

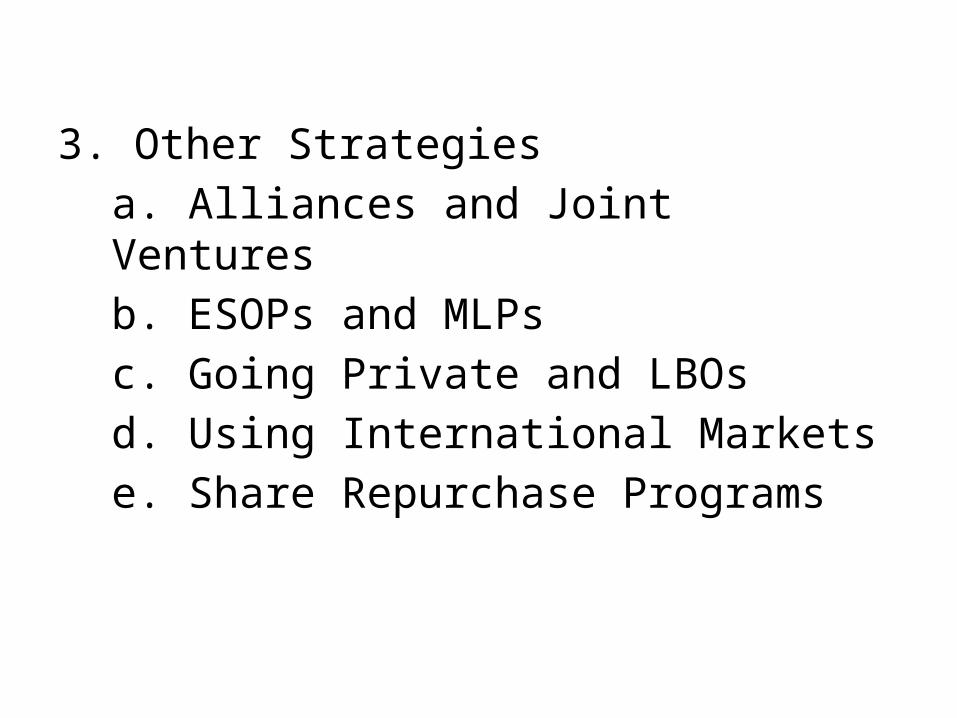

3. Other Strategiesa. Alliances and Joint Venturesb. ESOPs and MLPsc. Going Private and LBOsd. Using International Marketse. Share Repurchase Programs

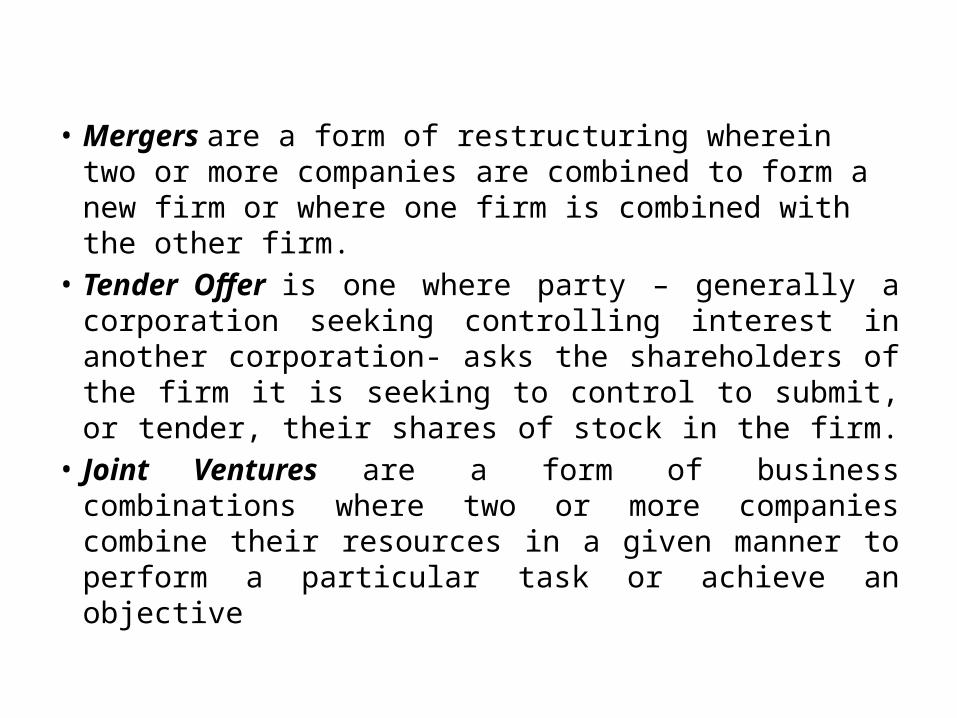

• Mergers are a form of restructuring wherein two or more companies are combined to form a new firm or where one firm is combined with the other firm.

• Tender Offer is one where party – generally a corporation seeking controlling interest in another corporation- asks the shareholders of the firm it is seeking to control to submit, or tender, their shares of stock in the firm.

• Joint Ventures are a form of business combinations where two or more companies combine their resources in a given manner to perform a particular task or achieve an objective

Spin off and Split-offIn a spin-off, the parent company (ParentCo) distributes to its existing shareholders new shares in a subsidiary, thereby creating a separate legal entity with its own management team and board of directors. The distribution is conducted pro-rata, such that each existing shareholder receives stock of the subsidiary in proportion to the amount of parent company stock already held. No cash changes hands, and the shareholders of the original parent company become the shareholders of the newly spun company (SpinCo).In a split-off, the parent company offers its shareholders the opportunity to exchange their ParentCo shares for new shares of a subsidiary (SplitCo). This tender offer often includes a premium to encourage existing ParentCo shareholders to accept the offer. For example, ParentCo might offer its shareholders $11.00 worth of SplitCo stock in exchange for $10.00 of ParentCo stock (a 10% premium).

Objectives of spin-off• Unlocking hidden value – Establish a public market

valuation for undervalued assets and create a pure-play entity that is transparent and easier to value

• Un-diversification – Divest non-core businesses and sharpen strategic focus when direct sale to a strategic or financial buyer is either not compelling or not possible

• Institutional sponsorship – Promote equity research coverage and ownership by sophisticated institutional investors, either of which tend to validate Spin Co as a standalone business

• Public currency – Create a public currency for acquisitions and stock-based compensation programs

• Motivating management – Improve performance by better aligning management incentives with SpinCo's performance (using SpinCo, rather than ParentCo, stock-based awards), creating direct accountability to public shareholders, and increasing transparency into management performance

• Eliminating dissynergies – Reduce bureaucracy and give SpinCo management complete autonomy

• Anti-trust – Break up a business in response to anti-trust concerns

• Corporate defense – Divest "crown jewel" assets to make a hostile takeover of ParentCo less attractive

Divestiture • In contrast to the class of spin-offs in which

only shares are transferred or exchanged is another group of transactions in which cash comes into the firm – divestitures. Basically, a divestiture involves the sale of a portion of the firm to an outside third party. Cash or equivalent consideration is received by the divesting firm.

• A variation on divestiture is the equity carve-out

EQUITY CARVE OUT:

• Equity Carve-OutAn equity carve-out is defined as the offering of a full or partial interest in a subsidiary to the investment public. In effect, an equity carve-out is an IPO of a corporate subsidiary or a split-off IPO.

. An equity carve-out involves the sale of a portion of the firm via an equity offering to outsiders. In other words, new shares of equity are sold to outsiders which give them ownership of a portion of the previously existing firm.

Equity carve outs

• Also called partial IPO• Parent company sells a percentage of the

equity of a subsidiary to the public stock market

• Receives cash for the percentage sold• Can sell any percentage, often just less than

20%, just less than 50%, are chosen.

Asset sale/Divestiture/Divestment

An asset sale is defined as the sale of a division, subsidiary, product line, or other assets directly to another firm. • Sell businesses that are not part of core operations, e.g.,

Raymond, L&T, Eastman Kodak, Ford Motor Company,• Generate additional Funds• Unlock the hidden value• Create stability• Sale an under-performing division• Comply with legal provisions

Corporate Control

• Control is the power/right/ability to control the composition of board of directors of a firm

• Control vests with the holding of ownership shares• Existing managements always desire to retain the corporate

control• Like all other commodities, the right to control can be bought

or sold. The market is known as ‘market for corporate control’ or ‘takeover market’ or ‘stock market’. Acquiring adequate number of shares will give controlling interest.

• Existing management would normally resist the takeover attempts or devise defenses enough to prevent hostile takeovers.

• Premium buy-backs – represent the repurchase of a substantial stockholder’s ownership interest at a premium above the market price (greenmail).

• Such buy-backs is generally accompanied ‘standstill agreements.’ They represent voluntary contracts in which the stockholders who are bought out agree not to make further attempts to takeover the company in future. When a standstill agreement is made without a buyback, the substantial stockholder is simply agrees not to increase his or her ownership which presumably would put him or her in an effective control position.

• Antitakeover amendments are changes in the corporate bylaws to make an acquisition of the company more difficult or more expensive. These include:• Supermajority voting provisions requiring a high percentage of

stockholders to approve a merger• Staggered terms for directors which can delay change of control

for a number of years, and• Golden parachutes which award large termination payments to

existing management if control of the firm is changed and management is terminated.

• In a proxy contest, an outside group seeks to obtain representation on the firm’s board of directors. The outsiders are referred to as ‘dissidents’ or ‘insurgents’ who seek to reduce the control position of the incumbents or existing board of directors.

Changes in Ownership Structure

• Ownership structure means the distribution of voting powers or ownership of the firm. The firm may be closely held or widely held. In closely held firm the insiders stake would be higher than outsiders (general public) stake than in case of widely held.

• Actions initiated to change this pattern of ownership are known as ‘Changes in Ownership Structure’.

• Some of the actions are:

• Exchange Offers – which may be the exchange of debt or preferred stock for common stock or conversely, of common stock for the more senior claims. Exchanging debt for common stock increases leverage; exchanging common stock for debt decreases leverage.

• A second form is share repurchase, which simply means that the corporation buys back some fraction of its outstanding shares of equity. Tender offers may be made for share repurchase.

• In a going-private transaction, the entire equity interest in a previously public corporation is purchased by a small group of investors. The firm is not longer subject to the regulations of SEBI.

• Going private transactions typically include members of the incumbent management group who obtain a substantial proportion of the equity ownership of the newly private company. When the transaction is initiated by the incumbent management, it is referred to as MBO.

• When financing from third parties involve substantial borrowing by the private company, such transactions are referred to as ‘Leveraged Buyouts (LBOs)’.

Other Classifications• Financial Restructuring• Technological Restructuring• Market Restructuring• Manpower Restructuring• Management Restructuring• Board Restructuring• Product Restructuring• Organizational Restructuring• Portfolio Restructuring

Dual Class Recapitalisation

• The issuing of various types of shares by a single company• A dual class stock structure can consist of stocks such as

Class A and Class B shares, and where the different classes have distinct voting rights and dividend payments. Two share classes are typically issued

• one share class is offered to the general public, and the other is offered to company founders, executives and family. The class offered to the general public has limited voting rights, while the class available to founders and executives has more voting power and often provides a majority control of the company.

Reasons for Dual class recapitalisation

• It helps management to retain corporate control

• Helps management to innovate (concentrate on innovation)

Employee stock ownership plan (ESOP)

An employee stock ownership plan (ESOP) is an employee-owner scheme that provides a company's workforce with an ownership interest in the company. In an ESOP, companies provide their employees with stock ownership, often at no up-front cost to the employees. ESOP shares, however, are part of employees' compensation for work performed. Shares are allocated to employees and may be held in an ESOP trust until the employee retires or leaves the company. The shares are then sold.

Does Corporate Restructuring Creates Value?

• Do all firms use all restructuring forms?• Which forms of restructuring are widely

employed?• Does Restructuring Creates value? • Do all forms of restructuring create

similar value?

Does Corporate Restructuring Creates Value?

• Jensen and Meckling (1976) argue that a company can be viewed as a collection of contracting relationship among individuals - a nexus of contracts. These contracts are what make it possible for the company to conduct business. The parties to these contracts include shareholders, creditors, managers, employees, suppliers and customers - in other words, anyone who has a claim on the firm’s profits and cash flows. Restructuring is a process by which firms change these contracts (Gilson, 2010).

• Firms restructure to overcome some of these market imperfections, rigidities, or in-built inefficiencies crept in various contracts. The objective is to emerge out of suffocating environment and have more focused and stronger firms.

• A growing body of research indicates that corporate restructuring generates value for stockholders and recent empirical evidence points to improvements in operating performance as a primary source of these gains.

• According to a study by the Harvard Business School corporate restructuring has enabled thousands of organizations around the world to respond more quickly and effectively to new opportunities and unexpected pressures, thereby re-establishing their competitive advantage.

• Kaplan (1989) and Lichtenberg and Siegel (1989) study firms taken private in MBOs and find that both financial (sales, income, etc) and real (factory productivity) performance measures improve after the buyout

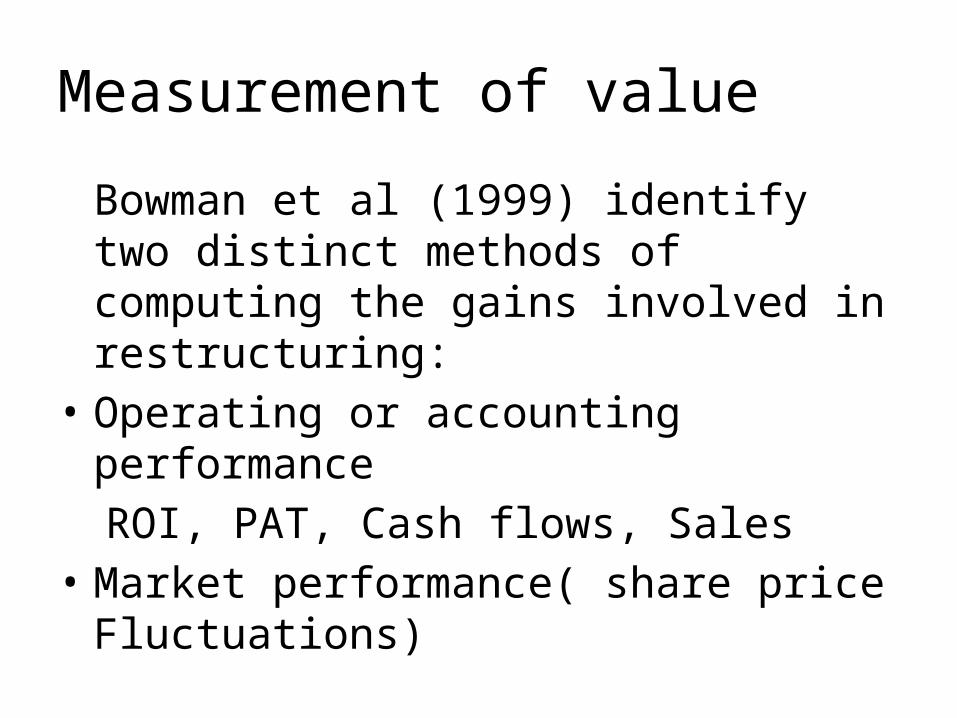

Measurement of value

Bowman et al (1999) identify two distinct methods of computing the gains involved in restructuring:

• Operating or accounting performanceROI, PAT, Cash flows, Sales

• Market performance( share price Fluctuations)

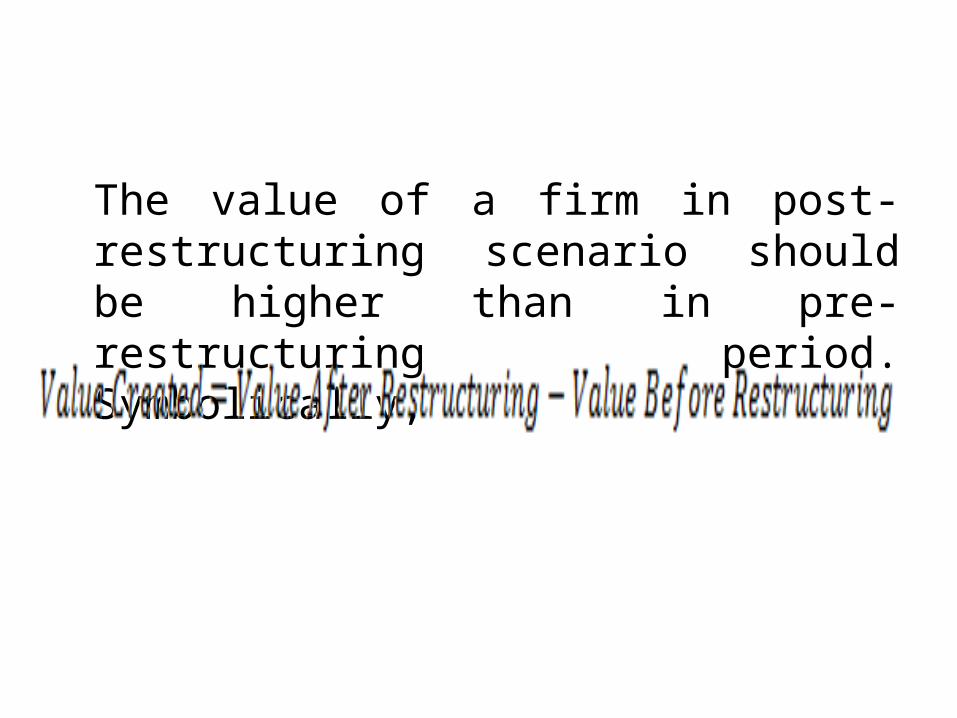

The value of a firm in post-restructuring scenario should be higher than in pre-restructuring period. Symbolically,

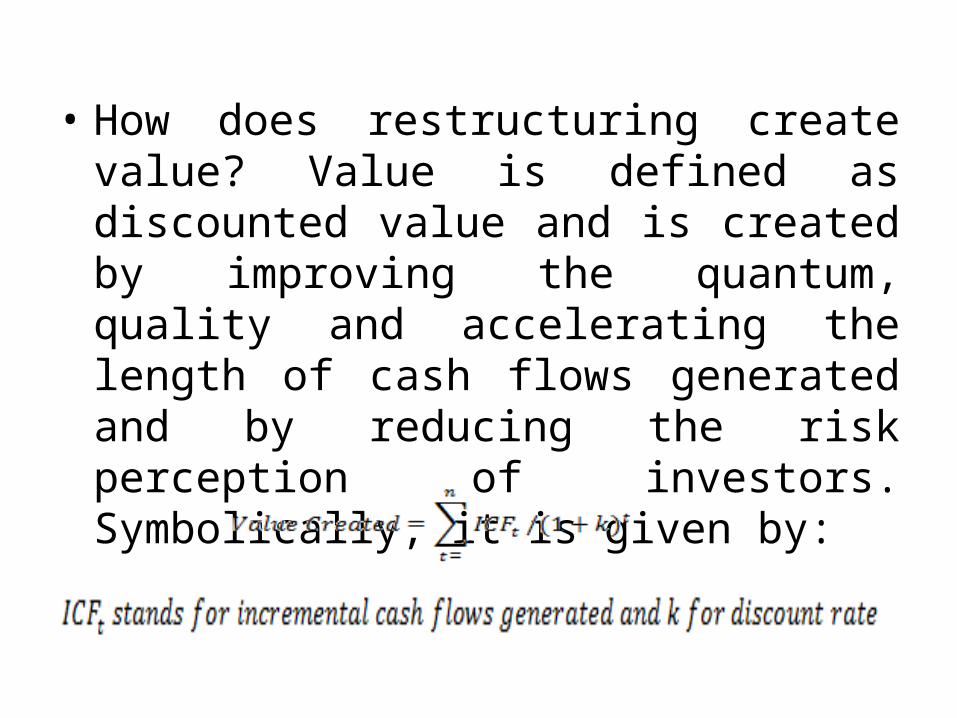

• How does restructuring create value? Value is defined as discounted value and is created by improving the quantum, quality and accelerating the length of cash flows generated and by reducing the risk perception of investors. Symbolically, it is given by:

Sources of value creation

• Reduction in reported cash losses due to sale of loss-making divisions, segments, etc

• Acquisition of related businesses and strengthening the core competency levels

• Savings in labour cost on account of reducing the labour force and revamping HR policies

• Reduction in rejection rate and reworks cost• Reduction in interest burden through appropriate debt recast

measures• Reduction in management expenses through a process of

portfolio restructuring• Savings in servicing costs on account of share buyback method

• Greater ability to raise large funds with minimum flotation costs

• Improved industrial relations• Improvement in relations with suppliers, bankers,

customers and general public at large• Focused approach resulting in clear vision and

mission statements• A responsive organizational structure• Improvement in performance of divisions,

segments, etc spun off as separate firms• Greater flow of information to market and

improving the valuations

Suggested Readings

• Books1. Weston, Chung and Hoag, Mergers, Restructuring and Corporate Control, PHI,

New Delhi.2. Weston, Mitchell and Mulherin, Takeovers, Restructuring and Corporate

Governance, Pearson, New Delhi.3. Donald DePamphilis, Mergers, Acquistions and Other Restructuring, Elsevier,

New Delhi4. Stuart Gilson, Creating Value through Corporate Restructuring, John Wiley,

New Delhi.• Articles

1. Jensen and Meckling (1976), The Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure, Journal of Financial Economics, Vol.3, No.1.

2. Lopez, Regier and Webb (2001), Do Restructuring Improve Operating Performance, Financial Markets Research

3. Bowman, Singh, Useem and Bhadury (1999), When Does Restructuring Improve Economic Performance? California Management Review, Vol. 41, No. 2