Embed Size (px)

DESCRIPTION

economy

Citation preview

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 1/48

ECONOMICS

20 1 32 0 1 4E D I T I O N

Introduction to

Economics

Y E A R S

1 9 D O I N G O U R B E S T , S O Y O U C A N D O Y O

U R

the WorldScholar’s Cup®

®

ECONOMICSCRAM KIT

ALPA CA- IN-CH IEF

Daniel Berdichevsky

EDITOR

Tania Asnes

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 2/48

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 3/48

ECONOMICS CRAM KIT | 2

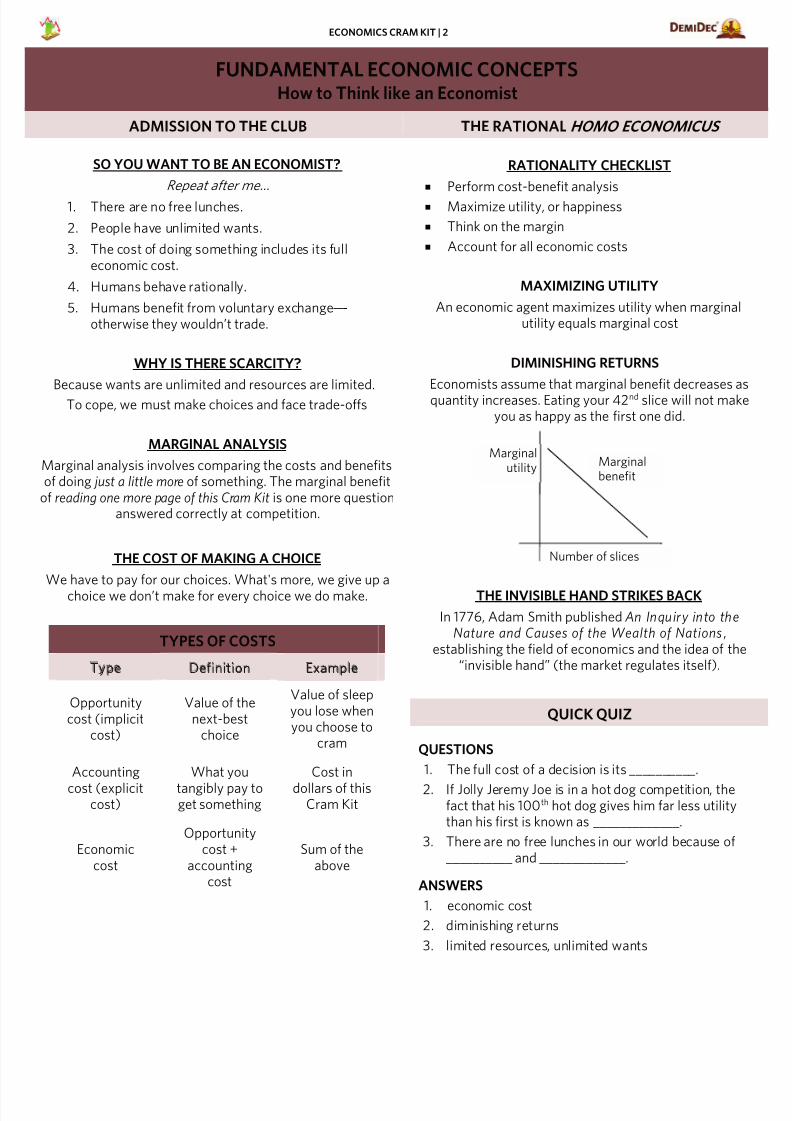

FUNDAMENTAL ECONOMIC CONCEPTSHow to Think like an Economist

ADMISSION TO THE CLUB THE RATIONAL HOMO ECONOMICUS

SO YOU WANT TO BE AN ECONOMIST?

Repeat after me…

1. There are no free lunches.

2. People have unlimited wants.

3. The cost of doing something includes its fulleconomic cost.

4. Humans behave rationally.

5. Humans benefit from voluntary exchange-----otherwise they wouldn’t trade.

WHY IS THERE SCARCITY?

Because wants are unlimited and resources are limited.

To cope, we must make choices and face trade-offs

MARGINAL ANALYSIS

Marginal analysis involves comparing the costs and benefitsof doing just a little more of something. The marginal benefit

of reading one more page of this Cram Kit is one more questionanswered correctly at competition.

THE COST OF MAKING A CHOICE

We have to pay for our choices. What's more, we give up achoice we don’t make for every choice we do make.

TYPES OF COSTS

Type Definition Example

Opportunitycost (implicit

cost)

Value of thenext-best

choice

Value of sleepyou lose whenyou choose to

cram

Accounting

cost (explicitcost)

What you

tangibly pay toget something

Cost in

dollars of thisCram Kit

Economiccost

Opportunitycost +

accountingcost

Sum of theabove

RATIONALITY CHECKLIST

Perform cost-benefit analysis

Maximize utility, or happiness

Think on the margin

Account for all economic costs

MAXIMIZING UTILITY

An economic agent maximizes utility when marginalutility equals marginal cost

DIMINISHING RETURNS

Economists assume that marginal benefit decreases aquantity increases. Eating your 42nd slice will not mak

you as happy as the first one did.

THE INVISIBLE HAND STRIKES BACK

In 1776, Adam Smith published An Inquiry into theNature and Causes of the Wealth of Nations,

establishing the field of economics and the idea of th“invisible hand” (the market regulates itself).

QUICK QUIZ

QUESTIONS

1. The full cost of a decision is its __________.

2. If Jolly Jeremy Joe is in a hot dog competition, thefact that his 100th hot dog gives him far less utilitythan his first is known as _____________.

3. There are no free lunches in our world because of__________ and _____________.

ANSWERS

1. economic cost

2. diminishing returns

3. limited resources, unlimited wants

Number of slices

Marginalbenefit

Marginalutility

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 4/48

ECONOMICS CRAM KIT | 3

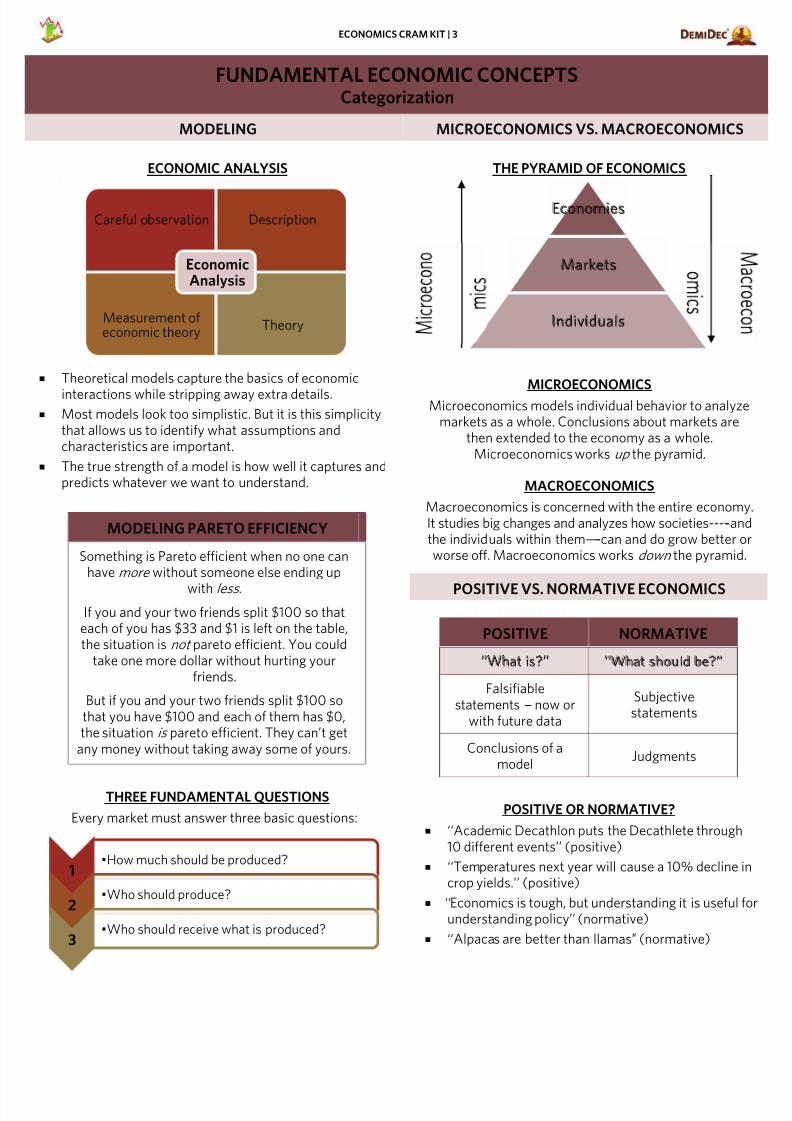

FUNDAMENTAL ECONOMIC CONCEPTSCategorization

MODELING MICROECONOMICS VS. MACROECONOMICS

ECONOMIC ANALYSIS`

Theoretical models capture the basics of economic

interactions while stripping away extra details.

Most models look too simplistic. But it is this simplicitythat allows us to identify what assumptions andcharacteristics are important.

The true strength of a model is how well it captures andpredicts whatever we want to understand.

MODELING PARETO EFFICIENCY

Something is Pareto efficient when no one canhave more without someone else ending up

with less .

If you and your two friends split $100 so thateach of you has $33 and $1 is left on the table,the situation is not pareto efficient. You could

take one more dollar without hurting yourfriends.

But if you and your two friends split $100 sothat you have $100 and each of them has $0,the situation is pareto efficient. They can’t get

any money without taking away some of yours.

THREE FUNDAMENTAL QUESTIONS

Every market must answer three basic questions:

THE PYRAMID OF ECONOMICS

MICROECONOMICS

Microeconomics models individual behavior to analyzmarkets as a whole. Conclusions about markets are

then extended to the economy as a whole.Microeconomics works up the pyramid.

MACROECONOMICS

Macroeconomics is concerned with the entire economIt studies big changes and analyzes how societies-----anthe individuals within them-----can and do grow better oworse off. Macroeconomics works down the pyramid

POSITIVE VS. NORMATIVE ECONOMICS

POSITIVE NORMATIVE

‘‘What is?’’ ‘‘What should be?’’

Falsifiablestatements --- now or

with future data

Subjectivestatements

Conclusions of amodel

Judgments

POSITIVE OR NORMATIVE?

‘‘Academic Decathlon puts the Decathlete through10 different events’’ (positive)

‘‘Temperatures next year will cause a 10% decline crop yields.’’ (positive)

‘‘Economics is tough, but understanding it is useful understanding policy’’ (normative)

‘‘Alpacas are better than llamas’’ (normative)

Economies

Markets

Individuals

Careful observation Description

Measurement ofeconomic theory

Theory

EconomicAnalysis

1•How much should be produced?

2•Who should produce?

3•Who should receive what is produced?

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 5/48

ECONOMICS CRAM KIT | 4

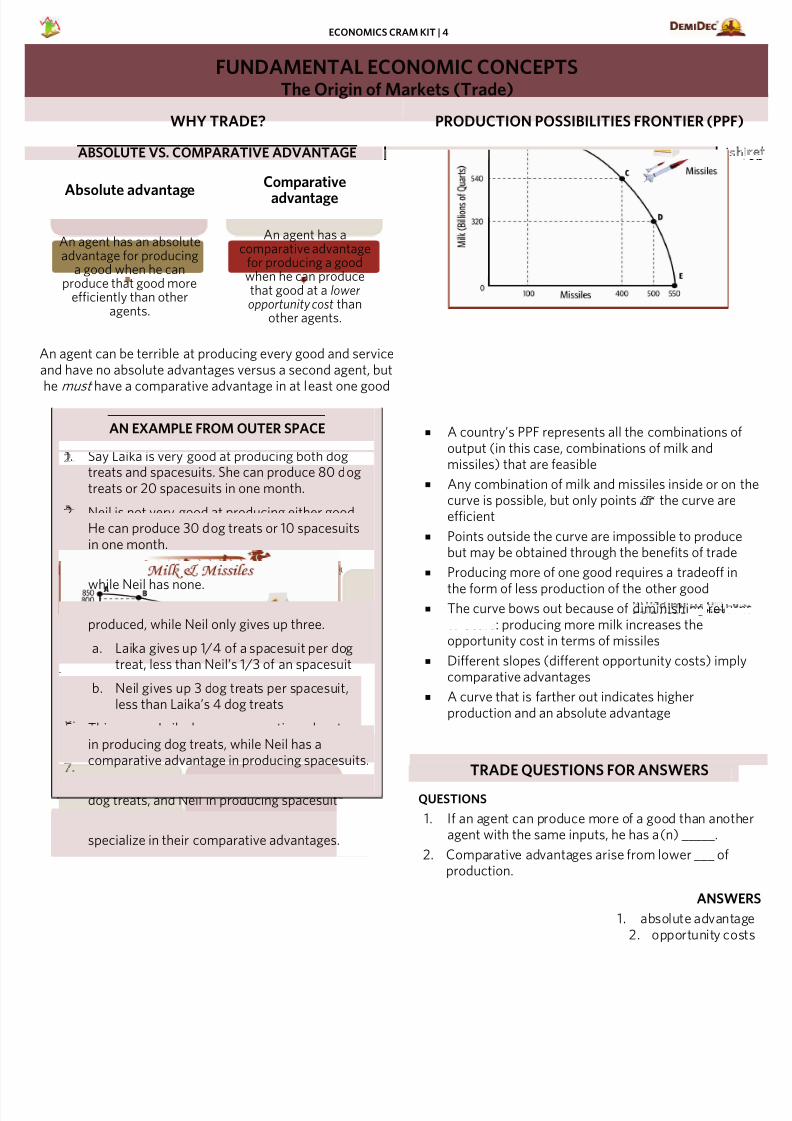

FUNDAMENTAL ECONOMIC CONCEPTSThe Origin of Markets (Trade)

WHY TRADE? PRODUCTION POSSIBILITIES FRONTIER (PPF)

ABSOLUTE VS. COMPARATIVE ADVANTAGE

An agent can be terrible at producing every good and serviceand have no absolute advantages versus a second agent, but

he must have a comparative advantage in at least one good

AN EXAMPLE FROM OUTER SPACE

1. Say Laika is very good at producing both dogtreats and spacesuits. She can produce 80 dogtreats or 20 spacesuits in one month.

2. Neil is not very good at producing either good.He can produce 30 dog treats or 10 spacesuitsin one month.

3. Laika has absolute advantages for both goods,

while Neil has none.4. Laika gives up four dog treats for each spacesuit

produced, while Neil only gives up three.

a. Laika gives up 1/4 of a spacesuit per dogtreat, less than Neil’s 1/3 of an spacesuit

b. Neil gives up 3 dog treats per spacesuit,less than Laika’s 4 dog treats

5. This means Laika has a comparative advantagein producing dog treats, while Neil has acomparative advantage in producing spacesuits.

6. Therefore, Laika should specialize in producingdog treats, and Neil in producing spacesuits.

7. Trade benefits both because they are able tospecialize in their comparative advantages.

A country’s PPF represents all the combinations ofoutput (in this case, combinations of milk andmissiles) that are feasible

Any combination of milk and missiles inside or on curve is possible, but only points on the curve areefficient

Points outside the curve are impossible to producebut may be obtained through the benefits of trade

Producing more of one good requires a tradeoff in

the form of less production of the other good The curve bows out because of diminishing return

to scale: producing more milk increases theopportunity cost in terms of missiles

Different slopes (different opportunity costs) implcomparative advantages

A curve that is farther out indicates higherproduction and an absolute advantage

TRADE QUESTIONS FOR ANSWERS

QUESTIONS

1. If an agent can produce more of a good than anothagent with the same inputs, he has a(n) _____.

2. Comparative advantages arise from lower ___ ofproduction.

ANSWE

1. absolute advanta2. opportunity cos

Absolute advantage

An agent has an absoluteadvantage for producing

a good when he canproduce that good more

efficiently than otheragents.

Comparative

advantage

An agent has acomparative advantage

for producing a goodwhen he can producethat good at a loweropportunity cost than

other agents.

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 6/48

ECONOMICS CRAM KIT | 5

MICROECONOMICSIntroduction to Markets

PERFECT COMPETITON MARKET MODEL MARKETS

ASSUMING MAKES…

The perfectly competitive market model relies on several keyassumptions. These assumptions mark the boundarybetween perfect competition and other market types:

WE ALL COME TOGETHER

Markets occur when producers and consumersexchange a certain good or service voluntarily

Markets do not have to be explicitly created by acentral body (like a government)

Markets are not always highly organized

As long as the transactions are voluntary, everyoninvolved will be better off

THE PRICE IS RIGHT

A market price conveys the value of a good toproducers and consumers

In perfect competition, the price represents theopportunity cost of a good’s production

Price also signals the value of the good to allproducers and consumers

All buyers and sellers are price takers, not makers

AGGREGATION

Prices are good indicators of a product’s value in acompetitive market. Adding up prices allows us to

compare different goods. This process is calledaggregation and allows firms and consumers to make

good market decisions.

MARKET MENTALITY

QUESTIONS

1. What does “no agent has market power” mean incontext of a perfectly competitive market?

2. In a competitive market, market price reflects the______________.

3. Aggregation is the process of ____________.

ANSWE

1. No individual agent can affect the market price.economic agents must accept the market price as

determined by the market as a wh

2. value consumers and producers place on the go

3. comparing different goods using a common measurstick, such as market p

•No individual has marketpower

•No producer can set pricesother than the market price

All agents acceptprices as given

•All producers produce anidentical product or service

One

homogenousproduct

•Consuming more of aproduct eventually offersless utility to consumers

•Inputs eventually grow lessuseful as production rises

Diminishingreturns

•Entry costs are the costs ofstarting a certain business

•Exit costs are costs ofshutting down a business

Entry and exitcosts are zero

•The process of exchangedoes not add more costs

•The market price is thesame for all consumers

Transactioncosts are zero

•Consumers are aware of allproducers and vice versa

•Everyone has access to themarket price

Perfect

information

•Firms maximize profits

•Consumers maximizeutility

Rational behavior

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 7/48

ECONOMICS CRAM KIT | 6

MICROECONOMICSDemand

THEORY OF THE CONSUMER SHIFTING ALL OVER THE PLACE

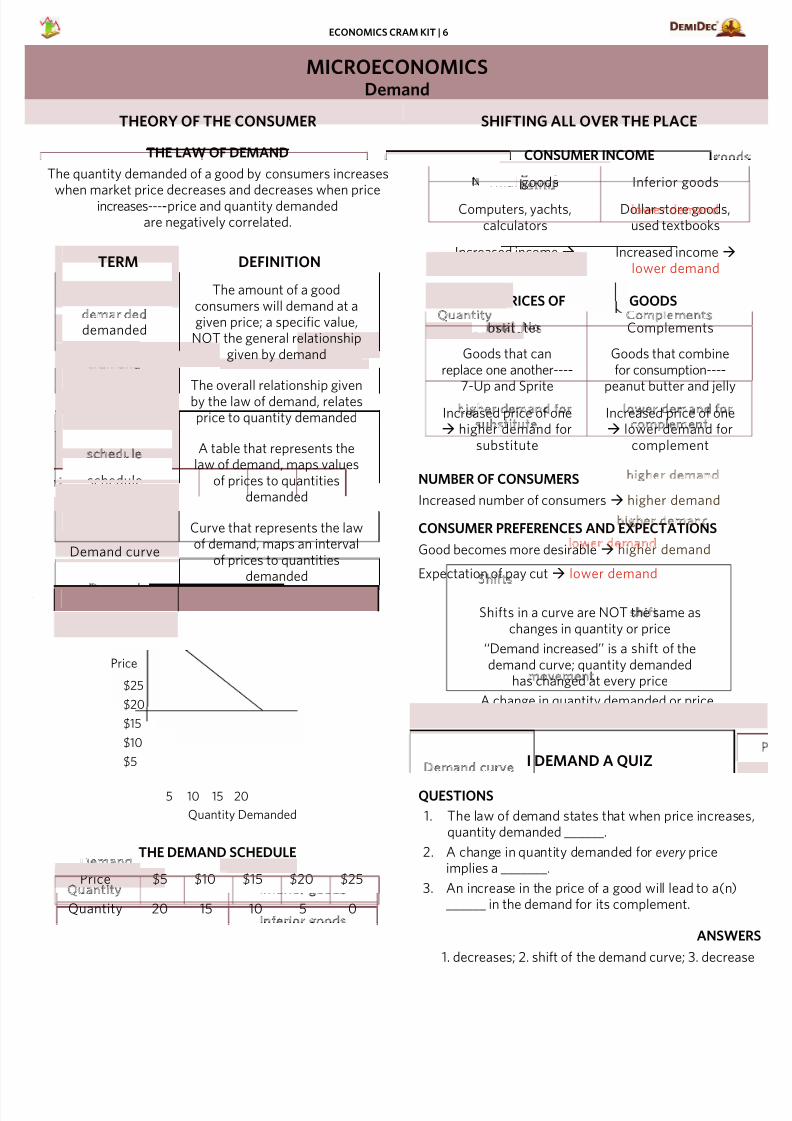

THE LAW OF DEMAND

The quantity demanded of a good by consumers increases

when market price decreases and decreases when priceincreases-----price and quantity demandedare negatively correlated.

TERM DEFINITION

Quantity demanded

The amount of a goodconsumers will demand at agiven price; a specific value,

NOT the general relationshipgiven by demand

Demand The overall relationship givenby the law of demand, relatesprice to quantity demanded

Demand schedule

A table that represents thelaw of demand, maps values

of prices to quantitiesdemanded

Demand curve

Curve that represents the lawof demand, maps an interval

of prices to quantitiesdemanded

[

THE DEMAND CURVE

THE DEMAND SCHEDULE

Price $5 $10 $15 $20 $25

Quantity 20 15 10 5 0

CONSUMER INCOME

Normal goods Inferior goods

Computers, yachts,calculators

Dollar store goods,used textbooks

Increased incomehigher demand

Increased income lower demand

PRICES OF RELATED GOODS

Substitutes Complements

Goods that canreplace one another-----

7-Up and Sprite

Goods that combinefor consumption-----

peanut butter and jellyIncreased price of one higher demand for

substitute

Increased price of one lower demand for

complement

NUMBER OF CONSUMERS

Increased number of consumers higher demand

CONSUMER PREFERENCES AND EXPECTATIONS

Good becomes more desirable higher demand

Expectation of pay cut lower demand

Shifts in a curve are NOT the same aschanges in quantity or price

‘‘Demand increased’’ is a shift of thedemand curve; quantity demanded

has changed at every price

A change in quantity demanded or priceis a movement along the curve

I DEMAND A QUIZ

QUESTIONS

1. The law of demand states that when price increasequantity demanded ______.

2. A change in quantity demanded for every priceimplies a _______.

3. An increase in the price of a good will lead to a(n)______ in the demand for its complement.

ANSWE

1. decreases; 2. shift of the demand curve; 3. decrea

Price

Quantity Demanded

$25

$20

$15

$10

$5

5 10 15 20

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 8/48

ECONOMICS CRAM KIT | 7

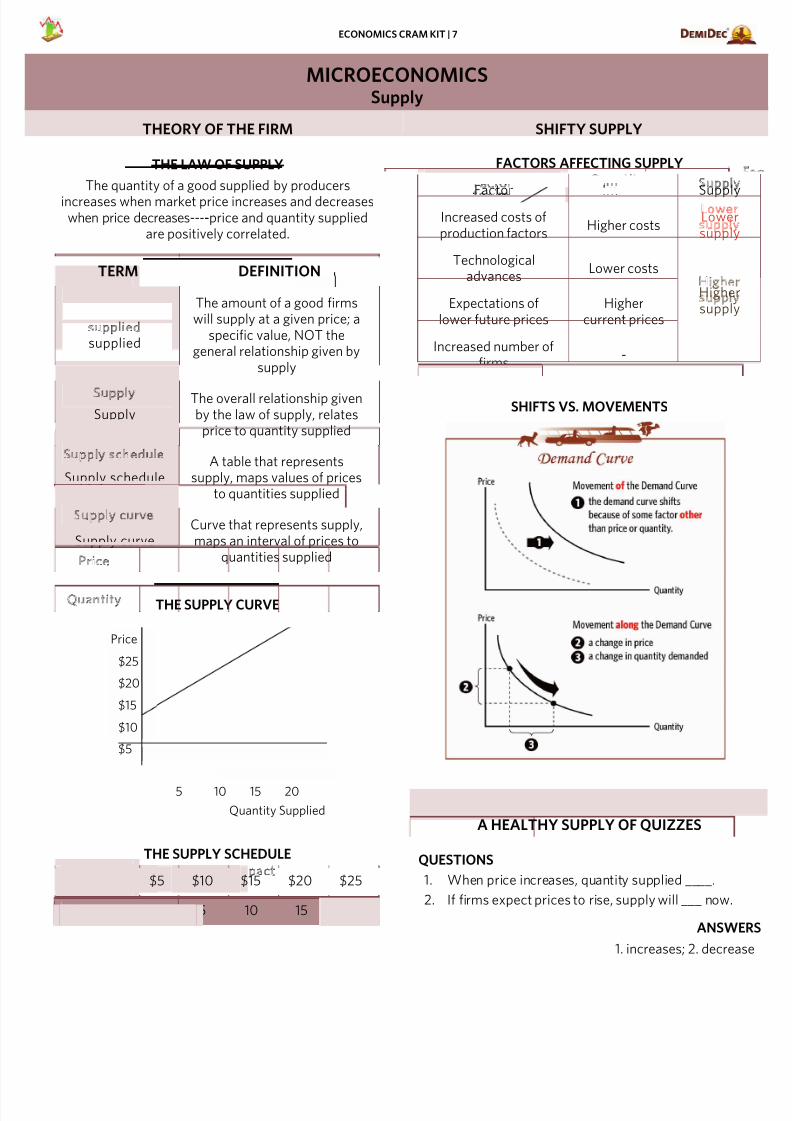

MICROECONOMICSSupply

THEORY OF THE FIRM SHIFTY SUPPLY

THE LAW OF SUPPLY

The quantity of a good supplied by producers

increases when market price increases and decreaseswhen price decreases-----price and quantity supplied

are positively correlated.

TERM DEFINITION

Quantity supplied

The amount of a good firmswill supply at a given price; a

specific value, NOT thegeneral relationship given by

supply

Supply The overall relationship givenby the law of supply, relates

price to quantity supplied

Supply schedule A table that represents

supply, maps values of pricesto quantities supplied

Supply curve Curve that represents supply,maps an interval of prices to

quantities supplied

THE SUPPLY CURVE

THE SUPPLY SCHEDULE

Price $5 $10 $15 $20 $25

Quantity 0 5 10 15 20

FACTORS AFFECTING SUPPLY

Factor Impact SupplyIncreased costs ofproduction factors

Higher costsLower supply

Technologicaladvances

Lower costs

HighersupplyExpectations of

lower future pricesHigher

current prices

Increased number offirms

-

SHIFTS VS. MOVEMENTS

A HEALTHY SUPPLY OF QUIZZES

QUESTIONS

1. When price increases, quantity supplied ____.

2. If firms expect prices to rise, supply will ___ now.

ANSWE

1. increases; 2. decrea

Price

Quantity Supplied

$25

$20

$15

$10

$5

5 10 15 20

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 9/48

ECONOMICS CRAM KIT | 8

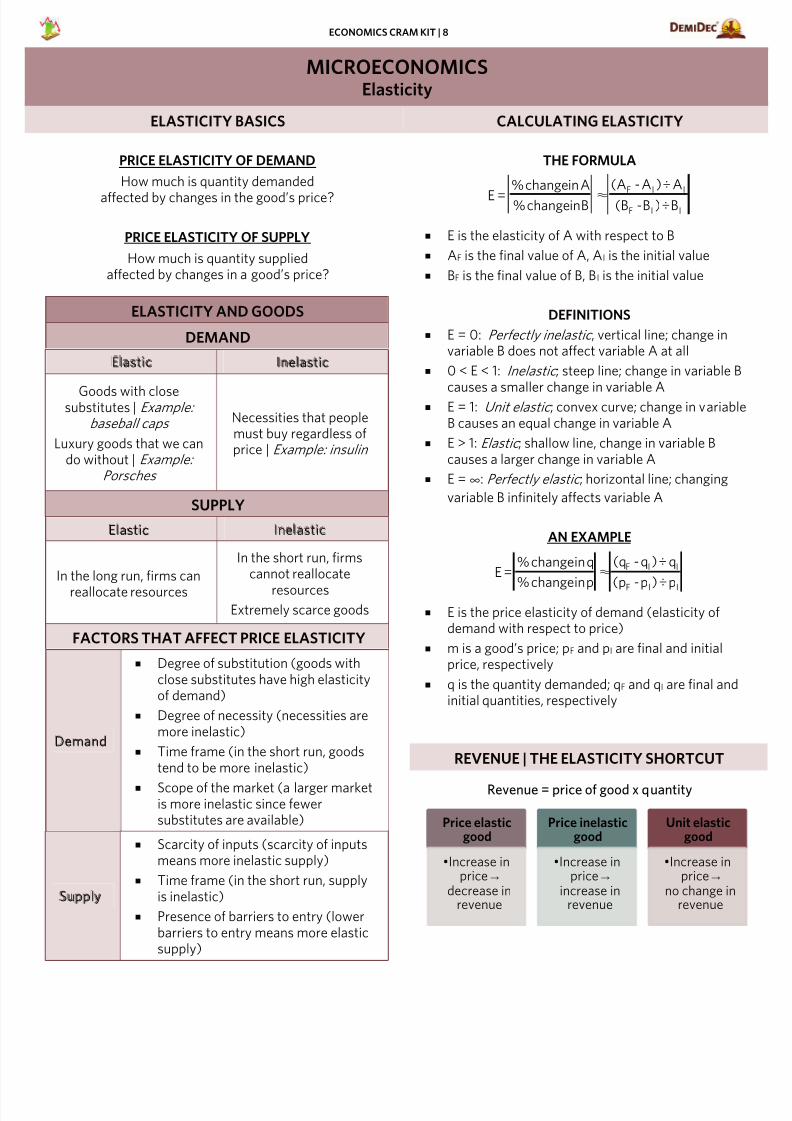

MICROECONOMICSElasticity

ELASTICITY BASICS CALCULATING ELASTICITY

PRICE ELASTICITY OF DEMAND

How much is quantity demanded

affected by changes in the good’s price?

PRICE ELASTICITY OF SUPPLY

How much is quantity suppliedaffected by changes in a good’s price?

ELASTICITY AND GOODS

DEMAND

Elastic Inelastic

Goods with closesubstitutes | Example:

baseball caps

Luxury goods that we cando without | Example:

Porsches

Necessities that peoplemust buy regardless ofprice | Example: insulin

SUPPLY

Elastic Inelastic

In the long run, firms can

reallocate resources

In the short run, firmscannot reallocate

resourcesExtremely scarce goods

FACTORS THAT AFFECT PRICE ELASTICITY

Demand

Degree of substitution (goods withclose substitutes have high elasticityof demand)

Degree of necessity (necessities aremore inelastic)

Time frame (in the short run, goodstend to be more inelastic)

Scope of the market (a larger marketis more inelastic since fewersubstitutes are available)

Supply

Scarcity of inputs (scarcity of inputsmeans more inelastic supply)

Time frame (in the short run, supplyis inelastic)

Presence of barriers to entry (lowerbarriers to entry means more elasticsupply)

THE FORMULA

E is the elasticity of A with respect to B

AF is the final value of A, AI is the initial value

BF is the final value of B, B I is the initial value

DEFINITIONS

E = 0: Perfectly inelastic , vertical line; change invariable B does not affect variable A at all

0 < E < 1: Inelastic ; steep line; change in variable B

causes a smaller change in variable A E = 1: Unit elastic ; convex curve; change in variabl

B causes an equal change in variable A

E > 1: Elastic ; shallow line, change in variable Bcauses a larger change in variable A

E =∞: Perfectly elastic ; horizontal line; changing

variable B infinitely affects variable A

AN EXAMPLE

E is the price elasticity of demand (elasticity ofdemand with respect to price)

m is a good’s price; pF and pI are final and initialprice, respectively

q is the quantity demanded; qF and qI are final andinitial quantities, respectively

REVENUE | THE ELASTICITY SHORTCUT

Revenue = price of good x quantity

IIF

IIF

B÷)B-(B

A÷)A-(A

Binchange%

Ainchange%

=E ≈

IIF

IIF

p÷)p-(p

q÷)q-(q

pinchange%

qinchange%=E ≈

Price elasticgood

•Increase inprice ®

decrease inrevenue

Price inelasticgood

•Increase inprice ®

increase inrevenue

Unit elasticgood

•Increase inprice ®

no change inrevenue

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 10/48

ECONOMICS CRAM KIT | 9

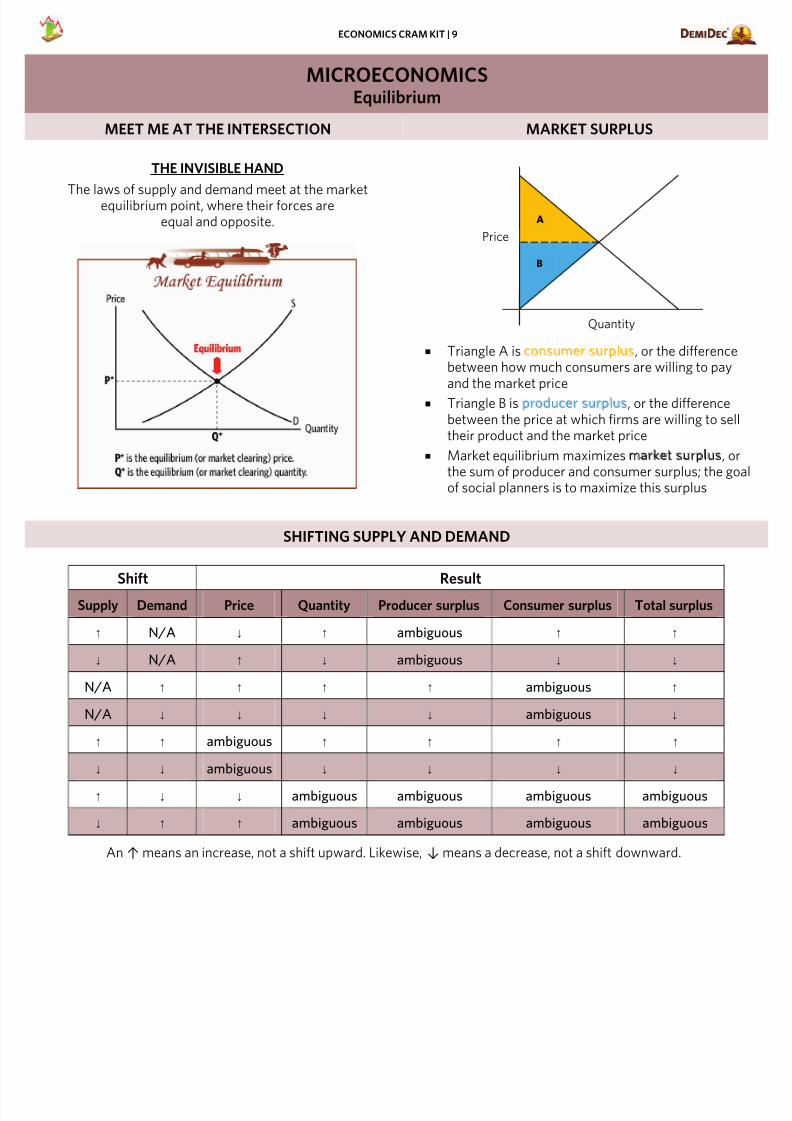

MICROECONOMICSEquilibrium

MEET ME AT THE INTERSECTION MARKET SURPLUS

THE INVISIBLE HAND

The laws of supply and demand meet at the marketequilibrium point, where their forces areequal and opposite.

Triangle A is consumer surplus, or the differencebetween how much consumers are willing to payand the market price

Triangle B is producer surplus, or the differencebetween the price at which firms are willing to selltheir product and the market price

Market equilibrium maximizes market surplus, orthe sum of producer and consumer surplus; the goof social planners is to maximize this surplus

SHIFTING SUPPLY AND DEMAND

Shift Result

Supply Demand Price Quantity Producer surplus Consumer surplus Total surplus

- N/A ¯ - ambiguous - -

¯ N/A - ¯ ambiguous ¯ ¯

N/A - - - - ambiguous -

N/A ¯ ¯ ¯ ¯ ambiguous ¯

- - ambiguous - - - -

¯ ¯ ambiguous ¯ ¯ ¯ ¯

- ¯ ¯ ambiguous ambiguous ambiguous ambiguous

¯ - - ambiguous ambiguous ambiguous ambiguous

An- means an increase, not a shift upward. Likewise, ¯ means a decrease, not a shift downward.

A

B

Price

Quantity

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 11/48

ECONOMICS CRAM KIT | 10

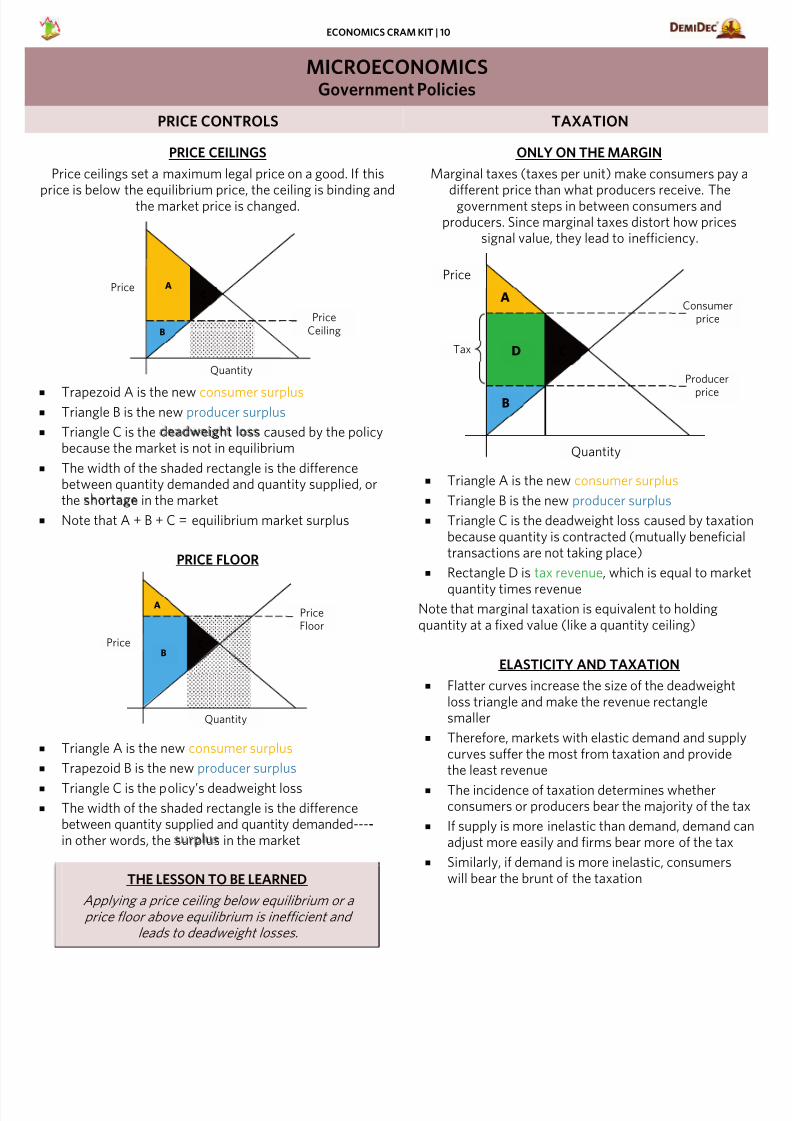

MICROECONOMICSGovernment Policies

PRICE CONTROLS TAXATION

PRICE CEILINGS

Price ceilings set a maximum legal price on a good. If this

price is below the equilibrium price, the ceiling is binding andthe market price is changed.

Trapezoid A is the new consumer surplus Triangle B is the new producer surplus

Triangle C is the deadweight loss caused by the policybecause the market is not in equilibrium

The width of the shaded rectangle is the differencebetween quantity demanded and quantity supplied, orthe shortage in the market

Note that A + B + C = equilibrium market surplus

PRICE FLOOR

Triangle A is the new consumer surplus

Trapezoid B is the new producer surplus

Triangle C is the policy’s deadweight loss

The width of the shaded rectangle is the differencebetween quantity supplied and quantity demanded-----in other words, the surplus in the market

THE LESSON TO BE LEARNED

Applying a price ceiling below equilibrium or a

price floor above equilibrium is inefficient andleads to deadweight losses.

ONLY ON THE MARGIN

Marginal taxes (taxes per unit) make consumers pay

different price than what producers receive. Thegovernment steps in between consumers andproducers. Since marginal taxes distort how prices

signal value, they lead to inefficiency.

Triangle A is the new consumer surplus

Triangle B is the new producer surplus

Triangle C is the deadweight loss caused by taxatiobecause quantity is contracted (mutually beneficiatransactions are not taking place)

Rectangle D is tax revenue, which is equal to mark

quantity times revenueNote that marginal taxation is equivalent to holdingquantity at a fixed value (like a quantity ceiling)

ELASTICITY AND TAXATION

Flatter curves increase the size of the deadweightloss triangle and make the revenue rectanglesmaller

Therefore, markets with elastic demand and supplcurves suffer the most from taxation and providethe least revenue

The incidence of taxation determines whetherconsumers or producers bear the majority of the ta

If supply is more inelastic than demand, demand cadjust more easily and firms bear more of the tax

Similarly, if demand is more inelastic, consumerswill bear the brunt of the taxation

A

PriceB

PriceFloor

Quantity

C

APrice

B

C

PriceCeiling

Quantity

A

Price

B

Producer

price

Quantity

Consumerprice

Tax D C

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 12/48

ECONOMICS CRAM KIT | 11

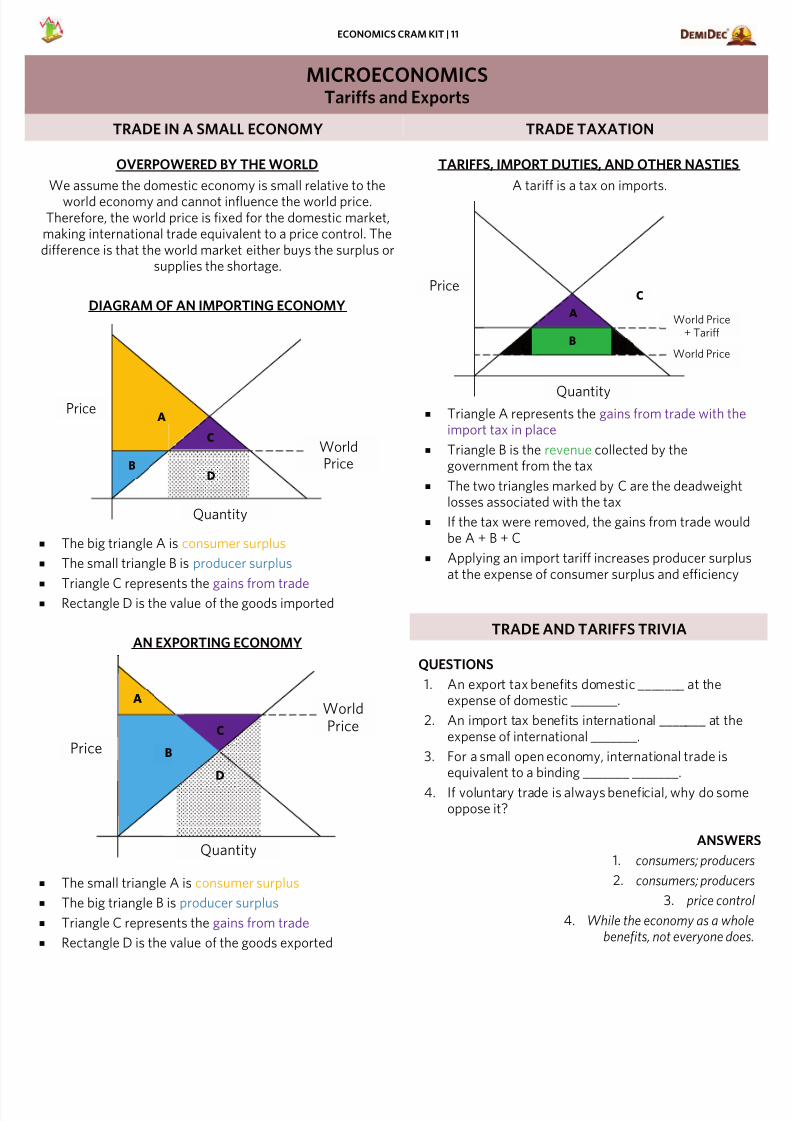

MICROECONOMICSTariffs and Exports

TRADE IN A SMALL ECONOMY TRADE TAXATION

OVERPOWERED BY THE WORLD

We assume the domestic economy is small relative to the

world economy and cannot influence the world price.Therefore, the world price is fixed for the domestic market,

making international trade equivalent to a price control. Thedifference is that the world market either buys the surplus or

supplies the shortage.

DIAGRAM OF AN IMPORTING ECONOMY

The big triangle A is consumer surplus

The small triangle B is producer surplus

Triangle C represents the gains from trade Rectangle D is the value of the goods imported

AN EXPORTING ECONOMY

The small triangle A is consumer surplus

The big triangle B is producer surplus

Triangle C represents the gains from trade

Rectangle D is the value of the goods exported

TARIFFS, IMPORT DUTIES, AND OTHER NASTIES

A tariff is a tax on imports.

Triangle A represents the gains from trade with theimport tax in place

Triangle B is the revenue collected by thegovernment from the tax

The two triangles marked by C are the deadweightlosses associated with the tax

If the tax were removed, the gains from trade woube A + B + C

Applying an import tariff increases producer surpluat the expense of consumer surplus and efficiency

TRADE AND TARIFFS TRIVIA

QUESTIONS

1. An export tax benefits domestic _______ at theexpense of domestic _______.

2. An import tax benefits international _______ at theexpense of international _______.

3. For a small open economy, international trade isequivalent to a binding _______ _______.

4. If voluntary trade is always beneficial, why do somoppose it?

ANSWE

1. consumers; produce

2. consumers; produce

3. price cont

4. While the economy as a whobenefits, not everyone do

A

Price B

WorldPrice

Quantity

D

C

APrice

B

WorldPrice

Quantity

C

D

A

Price

World Price+ Tariff

Quantity

World PriceB

C

C C

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 13/48

ECONOMICS CRAM KIT | 12

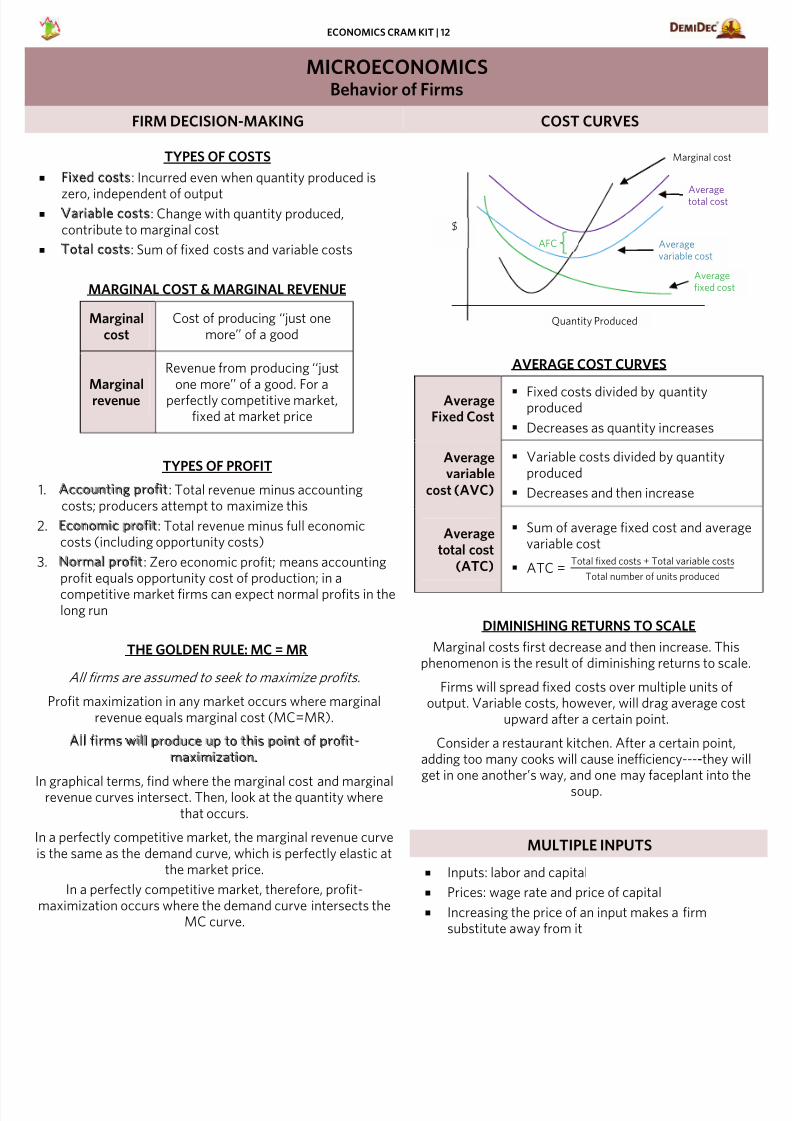

MICROECONOMICSBehavior of Firms

FIRM DECISION-MAKING COST CURVES

TYPES OF COSTS

Fixed costs: Incurred even when quantity produced is

zero, independent of output Variable costs: Change with quantity produced,

contribute to marginal cost

Total costs: Sum of fixed costs and variable costs

MARGINAL COST & MARGINAL REVENUE

Marginalcost

Cost of producing ‘‘just onemore’’ of a good

Marginalrevenue

Revenue from producing ‘‘justone more’’ of a good. For a

perfectly competitive market,fixed at market price

TYPES OF PROFIT

1. Accounting profit: Total revenue minus accountingcosts; producers attempt to maximize this

2. Economic profit: Total revenue minus full economiccosts (including opportunity costs)

3. Normal profit: Zero economic profit; means accountingprofit equals opportunity cost of production; in a

competitive market firms can expect normal profits in thelong run

THE GOLDEN RULE: MC = MR

All firms are assumed to seek to maximize profits.

Profit maximization in any market occurs where marginalrevenue equals marginal cost (MC=MR).

All firms will produce up to this point of profit-maximization.

In graphical terms, find where the marginal cost and marginalrevenue curves intersect. Then, look at the quantity wherethat occurs.

In a perfectly competitive market, the marginal revenue curveis the same as the demand curve, which is perfectly elastic at

the market price.

In a perfectly competitive market, therefore, profit-maximization occurs where the demand curve intersects the

MC curve.

AVERAGE COST CURVES

AverageFixed Cost

Fixed costs divided by quantityproduced

Decreases as quantity increases

Averagevariable

cost (AVC)

Variable costs divided by quantityproduced

Decreases and then increase

Averagetotal cost

(ATC)

Sum of average fixed cost and averagvariable cost

ATC =Total fixed costs + Total variable costs

Total number of units produced

DIMINISHING RETURNS TO SCALE

Marginal costs first decrease and then increase. Thisphenomenon is the result of diminishing returns to scal

Firms will spread fixed costs over multiple units ofoutput. Variable costs, however, will drag average cos

upward after a certain point.

Consider a restaurant kitchen. After a certain point,adding too many cooks will cause inefficiency-----they wget in one another’s way, and one may faceplant into th

soup.

MULTIPLE INPUTS

Inputs: labor and capital

Prices: wage rate and price of capital

Increasing the price of an input makes a firmsubstitute away from it

Quantity Produced

Averagefixed cost

Marginal cost

AFC Averagevariable cost

Averagetotal cost

$

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 14/48

ECONOMICS CRAM KIT | 13

MICROECONOMICSFailures of Perfect Competition

IMPERFECT MARKETS: MONOPOLY I HAVE THE POWER

FAILURES OF PERFECT COMPETITION

Removing any assumptions of perfect competition creates a

new market type. All of these market types are inefficientand create deadweight loss. All firms face downward sloping

demand curves.

MONOPOLY BASICS

Only one firm supplies (example: De Beers diamonds)

This firm has full market power to set prices

Arise from barriers to entry or economies of scale (aftera certain point, producing more of a good will increasecosts due to increasing inefficiency)

Faces a downward sloping demand curve (for the entiremarket)

DEALING WITH MONOPOLIES

The United States government has devised severalmethods of dealing with monopolies.

RegulationLegislation (Sherman

Anti-Trust Act)Public

Ownership

MARKET POWER

Market power is the ability of an individual to influenc

market price. Perfect competitors have no marketpower and must accept the market price.

CAUSES OF MARKET POWER

PRICE DISCRIMINATION

Price discrimination involves sellingthe same product to different consumers at different

prices-----such as airline seats or movie tickets.

This practice increases producer surplus at the expenseconsumer surplus. Monopolies price discriminate tocapture new consumers without losing current ones

BARRIERS TO ENTRY

Monopolies arise due to barriers that keep competitorsfrom entering the market. Barriers include:

Ownership of a key resource

Government-created barriers (patents, copyrightsand other property protections)

Natural monopolies: emerge when it is practical foonly one seller to operate in a given market

YOU SHALL NOT MATCH

1. Market power2. Economies of scale

3. Sherman Anti-Trust Act

4. Barriers to entry

5. Only one supplier

A. After a certain pointproducing more gooincreases costs

B. Monopoly

C. Ability to influencemarket price

D. Legislation that dealwith monopolies

E. Prevent more firmsfrom entering

Answers: 1. C; 2. A; 3. D; 4. E; 5

•Monopolies can produce less than what isdemanded to increase profits

•This leaves some consumer demand unmet,decreasing general welfare

•Some consumer surplus becomes producersurplus, but part of it vanishes as deadweightloss

Deliberate scarcity

•Monopolists are sometimes lazy, incompetent,or just lack incentive to raise standards due tono competition

•This inefficiency can result in wasted resources,higher production costs, and higher prices

Inefficiency

•A monopoly will set price and quantity suppliedwhere marginal revenue equals marginal cost

•Unlike a perfectly competitive firm, increasingsupply to reach that point increases economicprofits

Positive economic profit

High entrycosts

Policies thatrestrict entry

Economies ofscale

Control ofnatural

resources

Rent seeking(see later)

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 15/48

ECONOMICS CRAM KIT | 14

Harm others

They are the costs

of an action thatare not passedalong to the agenttaking that action

Since the agentdoes not face thecost, he willperform more ofthe action than isoptimal

Negativeexternalities

Benefit others

They are the

benefits of anaction not felt bythe agent takingthat action

Since the agentdoes not enjoy thbenefit, he willperform less of taction than isoptimal

Positiveexternalities

MICROECONOMICSFailures of Perfect Competition

IMPERFECT MARKETS CONTINUED MARKET FAILURES

OLIGOPOLY

Only a few firms (suppliers) exist

Each firm has some degree of market power

Goods are either homogenous or differentiated

Firms primarily face non-price competition

Producers often collude and form cartels

Examples: Market for mobile phone service, OPEC

Collusion occurs when firms in an oligopoly cooperate toraise market prices artificially. A group of firms that colludesto control prices is a cartel, which is illegal under U.S. anti-

trust law.

The incentive to cheat in a cartel is strong, so cartels tend to

break down even without government intervention.

THE BOTTOM LINE

An oligopoly will be more efficient and benefitmore people than a monopoly, but will be less

efficient and benefit fewer people than aperfectly competitive market.

MONOPOLISTIC COMPETITION

Goods no longer homogenous

Large number of firms, just like perfect competition

Firms compete by differentiating their products, oftenartificially

Producers often engage in non-price competition (forexample, through advertising)

Firms face a downward sloping demand curve

Examples: Blue jeans, restaurants, toothbrushes

The diversification of products in a monopolisticallycompetitive market gives consumers more choices than in a

perfectly competitive market, where all products arehomogenous.

However, since market price is greater than marginal cost, themarkets will experience some social inefficiency.

THE BOTTOM LINE

You can spot a monopolistically competitivemarket whenever multiple companies are using

ads to convince you that their products aredifferent when they are actually pretty similar.

Market failures occur when competitive markets fail tproduce socially desirable outcomes.

The two main forms of market failures are linked toexternalities and public goods.

Externalities are costs or benefits associatedwith a decision not factored into the decision-making

process. They do not affectthe decision maker directly.

INTERNALIZE IT!

One way to address externalities is to internalize themby incorporating the cost of the externality into the

market. For instance, if companies are taxed for eachpound of pollution they emit-----and the tax is set to equ

the cost of that pollution to society-----companies wilmake choices based on true social cost.

THE COASE THEOREM

As long as the parties involved in a dispute cannegotiate and property rights are clearly defined, the

private market can settle any disputes.

PLEASE DON’T FAIL THIS TRUTH TEST

TRUE/FALSE

1. Oligopolies are more efficient than monopolies

2. Externalities are the only area of market failure

ANSWE

1. Tr

2. False; public goods are alassociated with market failu

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 16/48

ECONOMICS CRAM KIT | 15

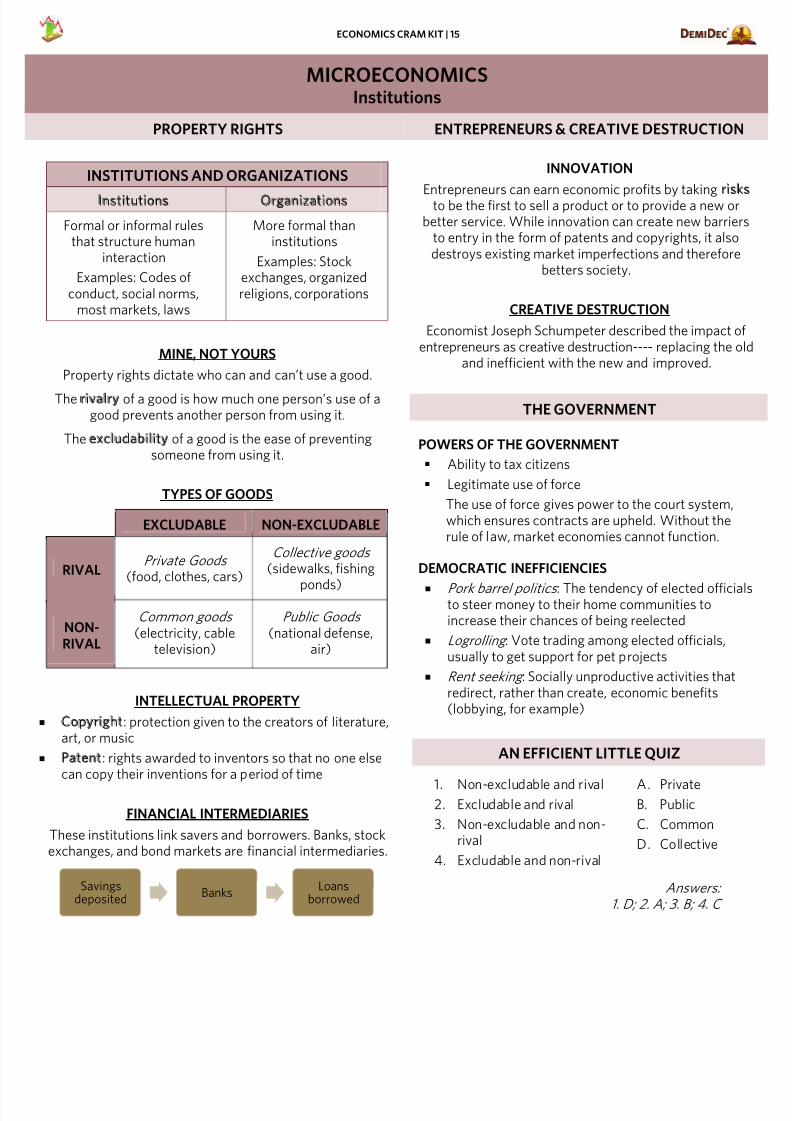

MICROECONOMICSInstitutions

PROPERTY RIGHTS ENTREPRENEURS & CREATIVE DESTRUCTION

INSTITUTIONS AND ORGANIZATIONS

Institutions Organizations

Formal or informal rulesthat structure human

interaction

Examples: Codes ofconduct, social norms,

most markets, laws

More formal thaninstitutions

Examples: Stockexchanges, organizedreligions, corporations

MINE, NOT YOURS

Property rights dictate who can and can’t use a good.

The rivalry of a good is how much one person’s use of agood prevents another person from using it.

The excludability of a good is the ease of preventingsomeone from using it.

TYPES OF GOODS

EXCLUDABLE NON-EXCLUDABLE

RIVALPrivate Goods

(food, clothes, cars)

Collective goods (sidewalks, fishing

ponds)

NON-

RIVAL

Common goods

(electricity, cabletelevision)

Public Goods

(national defense,air)

INTELLECTUAL PROPERTY

Copyright: protection given to the creators of literature,art, or music

Patent: rights awarded to inventors so that no one elsecan copy their inventions for a period of time

FINANCIAL INTERMEDIARIES

These institutions link savers and borrowers. Banks, stockexchanges, and bond markets are financial intermediaries.

INNOVATION

Entrepreneurs can earn economic profits by taking riskto be the first to sell a product or to provide a new orbetter service. While innovation can create new barrier

to entry in the form of patents and copyrights, it alsodestroys existing market imperfections and therefore

betters society.

CREATIVE DESTRUCTION

Economist Joseph Schumpeter described the impact oentrepreneurs as creative destruction----- replacing the o

and inefficient with the new and improved.

THE GOVERNMENT

POWERS OF THE GOVERNMENT

Ability to tax citizens

Legitimate use of force

The use of force gives power to the court system,which ensures contracts are upheld. Without therule of law, market economies cannot function.

DEMOCRATIC INEFFICIENCIES

Pork barrel politics : The tendency of elected officiato steer money to their home communities toincrease their chances of being reelected

Logrolling : Vote trading among elected officials,usually to get support for pet projects

Rent seeking : Socially unproductive activities thatredirect, rather than create, economic benefits(lobbying, for example)

AN EFFICIENT LITTLE QUIZ

1. Non-excludable and rival2. Excludable and rival

3. Non-excludable and non-rival

4. Excludable and non-rival

A. PrivateB. Public

C. Common

D. Collective

Answers:

1. D; 2. A; 3. B; 4. C

Savingsdeposited

BanksLoans

borrowed

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 17/48

ECONOMICS CRAM KIT | 16

MACROECONOMICSBasics of Macroeconomics

MACROECONOMICS ISSUES THE STATE OF THE ECONOMY

Macroeconomics is concerned with two main issues:

Factors that affect things in the long run (the size of

economies, standard of living, and price level) The causes and consequences of short-run economic

fluctuations (especially unemployment and inflation)

REAL GDP

Real Gross Domestic Product (GDP) measures the totalquantity of goods and services produced in an economy in agiven year, adjusted for the effects of inflation.

REAL GDP PER CAPITA

‘‘Per capita’’ is a Latin phrase meaning ‘‘per head.’’ GDP per

capita is the GDP per person in the economy; it indicates whatthe average person is able to consume in an economy.

If the population were suddenly to double, GDP per capitawould be cut in half. (Technically, the same would be true ifevery person in the economy were to grow a second head.)

AVERAGE LABOR PRODUCTIVITY

Average labor productivity measures how much the typicalworker can produce.

Divide the economy’s total output (GDP) by the total number

of workers employed.

Average labor productivity =Economy's output (GDP)

Total number of workers

Greater levels of production and average labor productivityenable consumption that improves the standard of living.

HUMAN HAPPINESS

Human happiness depends on more than just material levelsof consumption. Other important factors:

A long, healthy life

Access to education

Clean environment

Possession of alpacas

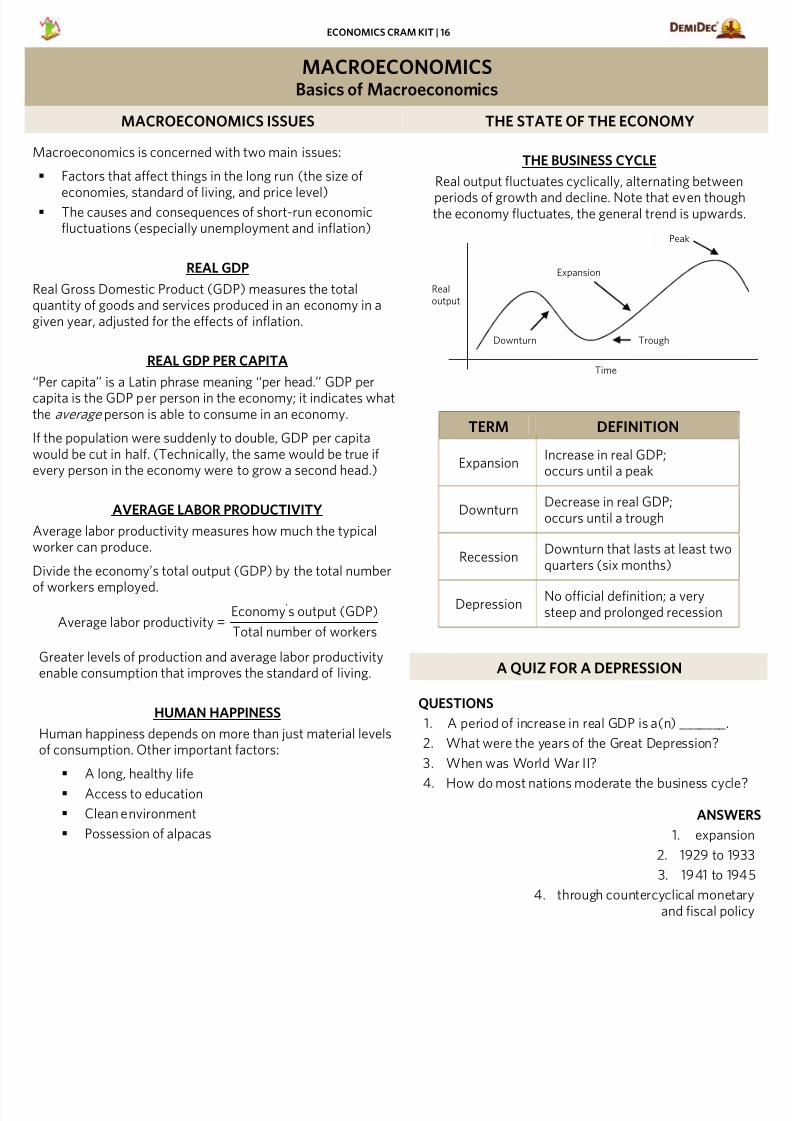

THE BUSINESS CYCLE

Real output fluctuates cyclically, alternating between

periods of growth and decline. Note that even thoughthe economy fluctuates, the general trend is upwards

TERM DEFINITION

ExpansionIncrease in real GDP;occurs until a peak

DownturnDecrease in real GDP;occurs until a trough

RecessionDownturn that lasts at least twoquarters (six months)

DepressionNo official definition; a verysteep and prolonged recession

A QUIZ FOR A DEPRESSION

QUESTIONS

1. A period of increase in real GDP is a(n) _______.

2. What were the years of the Great Depression?

3. When was World War II?

4. How do most nations moderate the business cycle

ANSWE

1. expansi

2. 1929 to 19

3. 1941 to 194

4. through countercyclical monetaand fiscal poli

Peak

Trough

Expansion

Downturn

Realoutput

Time

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 18/48

ECONOMICS CRAM KIT | 17

MACROECONOMICSUnemployment

EMPLOYMENT TYPES OF UNEMPLOYMENT

THE LABOR FORCE

The labor force includes all members of the populationwho have a job (employed) or are actively seekingemployment (unemployed).

To be in the labor force, you cannot be:

Younger than 16 or retired

In jail, in the military, or a homemaker

A discouraged worker : you must have worked in the pastweek or looked for work in the past four weeks

TERM DEFINITION

Employmentrate

Percentage of the labor force thathas a job; number of persons

employed divided by the laborforce; never 100%

Unemploymentrate

Percentage of the labor force thatlacks a job but is searching for one.

The Bureau of Labor Statisticsmeasures unemployment.

Participationrate

Percentage of the population inthe labor force-----about 66%

Employed Worked for pay in the past week,or on vacation or sick leave

UnemployedDid not work during the past

week but did look for paid worksometime in the past four weeks

Discouragedworker / out ofthe labor force

Did not work in the past week orlook for work in the past four

weeks

THE NATURAL RATE OF UNEMPLOYMENT

Key fact: Full employment is NOT 0% unemployment.

There is always unemployment-----some people arealways between jobs, or just joining the labor force

The unemployment rate of an economy at full output isthe natural rate of unemployment

Okun’s law relates unemployment to GDP; every 1%increase in unemployment above the natural rate resultsin a 2% drop in real GDP

No one knows exactly what the natural rate is in 21st

century America-----it might be higher than it used to be

d

QUIZ FOR EMPLOYMENT

QUESTIONS

1. Unemployed workers must be _______, but nothave a _______.

2. Unemployment due to a mismatch between skillsdemanded and skills supplied is _______.

3. No one knows the ____ rate of unemployment.

4. The percentage of the population that is in the laboforce is known as the _______.

ANSWE

1. looking for work; j

2. structural unemployme

3. natu

4. labor participation ra

•Mismatch between skills demanded and skillssupplied

•Spurred by changes in technology or consumerpreferences

•Would be zero if retraining was instant wasinstant and free

•Factors into the natural rate of unemployment

Structural

•Unemployment resulting from movement alongthe business cycle

•Increases with recessions and decreases withexpansions

•Does not factor into the natural rate ofunemployment

Cyclical

•Caused by time-lag between jobs

•Inevitable

•Factors into the natural rate of unemployment

Frictional

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 19/48

ECONOMICS CRAM KIT | 18

MACROECONOMICSGross Domestic Product

THE ‘‘BIG’’ PART OF MACRO HISTORY OF GDP

GROSS DOMESTIC PRODUCT (GDP)

GDP is the market value of all final goods and services

produced within a country in a given period of time.

WHAT’S NOT INCLUDED IN GDP

Intermediate goods: goods used for the production ofother goods, value is reflected in its final good

Example: bolts

Goods not sold on the open market: illegal ‘‘blackmarket’’ goods, as well as goods produced for personalconsumption

Example: home-knit sweaters

Used goods: the value of the good was already counted

in GDP when the good was sold newExample: a used car

Transfer payments: moving money between thegovernment and people

Example: a Social Security check

LIMITATIONS OF GDP

HEY, YOU MISSED ME!

GDP misses out on a lot of economic activity.

It can be difficult to determine what is a ‘‘final’’ goo GDP excludes goods and services not bought or so

in ‘official’ markets (such as work done by stay-at-home spouses)

GDP usually ignores the fact that certain activitiesdeplete natural resources , pollute, or have othercostly externalities

•The total value of differentgoods (add up dollar values)

“the marketvalue”

•Only final goods are counted

•Capital goods (made to makeother goods) are counted theyear they are produced

“of all finalgoods andservices”

•All goods produced within acountry’s borders, even if aforeigner owns the factory

“producedwithin acountry"

•Typically a specific quarter oryear

“in a givenperiod of

time”

Development of GDP

In the mid-17th century, Sir William Petty wasassigned by the British government to assess

the Irish people’s ability to pay taxes.

In 1932, the U.S. Department of Commercecommissioned Simon Kuznets to develop a

system to measure national output.

Kuznets presented his findings in 1934 to theU.S. Senate.

When the U.S. entered World War II (whicheffectively ended the Great Depression) it

continued to refine techniques for measuringoutput.

For his efforts, Kuznets received the NobelPrize in Economic Science in 1971.

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 20/48

ECONOMICS CRAM KIT | 19

MACROECONOMICSMeasuring GDP

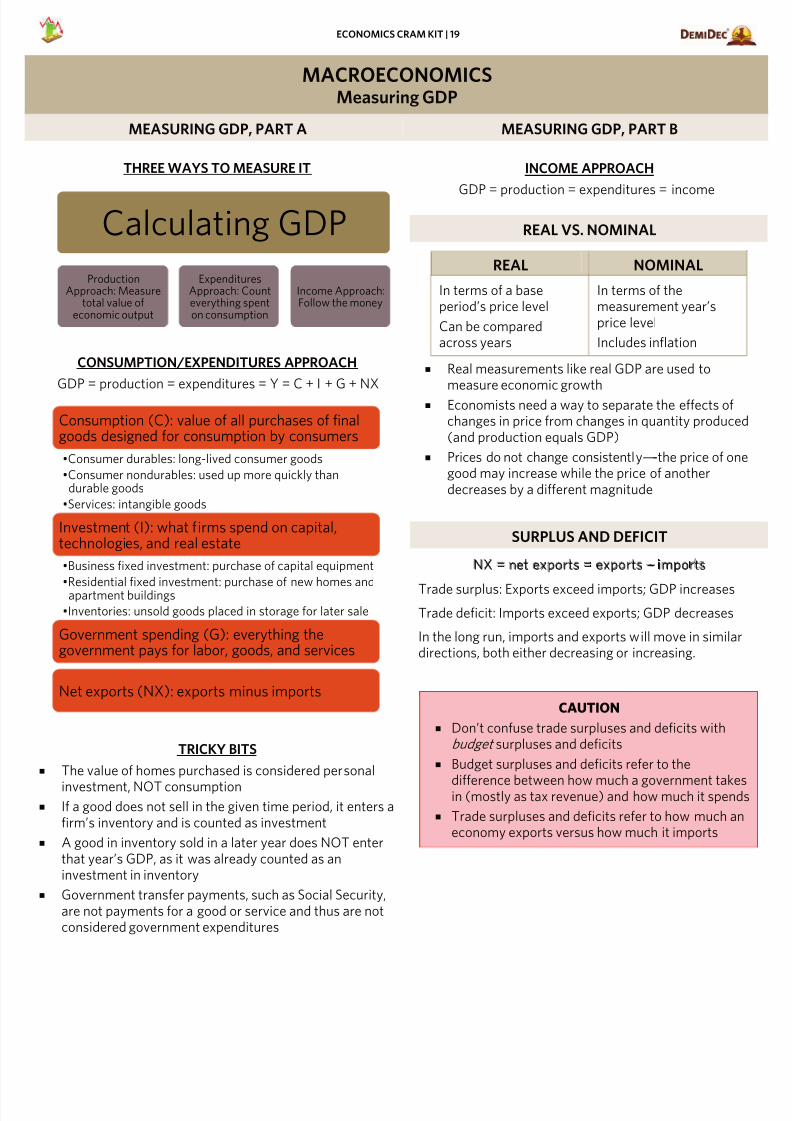

MEASURING GDP, PART A MEASURING GDP, PART B

THREE WAYS TO MEASURE IT

CONSUMPTION/EXPENDITURES APPROACH

GDP = production = expenditures = Y = C + I + G + NX

TRICKY BITS

The value of homes purchased is considered personal

investment, NOT consumption If a good does not sell in the given time period, it enters a

firm’s inventory and is counted as investment

A good in inventory sold in a later year does NOT enterthat year’s GDP, as it was already counted as aninvestment in inventory

Government transfer payments, such as Social Security,are not payments for a good or service and thus are notconsidered government expenditures

INCOME APPROACH

GDP = production = expenditures = income

REAL VS. NOMINAL

REAL NOMINAL

In terms of a baseperiod’s price level

Can be comparedacross years

In terms of themeasurement year’sprice level

Includes inflation

Real measurements like real GDP are used tomeasure economic growth

Economists need a way to separate the effects ofchanges in price from changes in quantity produce(and production equals GDP)

Prices do not change consistently-----the price of ongood may increase while the price of anotherdecreases by a different magnitude

SURPLUS AND DEFICIT

NX = net exports = exports --- imports

Trade surplus: Exports exceed imports; GDP increases

Trade deficit: Imports exceed exports; GDP decreases

In the long run, imports and exports will move in similardirections, both either decreasing or increasing.

CAUTION

Don’t confuse trade surpluses and deficits withbudget surpluses and deficits

Budget surpluses and deficits refer to the

difference between how much a government takein (mostly as tax revenue) and how much it spend

Trade surpluses and deficits refer to how much aneconomy exports versus how much it imports

Consumption (C): value of all purchases of finalgoods designed for consumption by consumers

•Consumer durables: long-lived consumer goods

•Consumer nondurables: used up more quickly thandurable goods

•Services: intangible goods

Investment (I): what firms spend on capital,technologies, and real estate

•Business fixed investment: purchase of capital equipment

•Residential fixed investment: purchase of new homes andapartment buildings

•Inventories: unsold goods placed in storage for later sale

Government spending (G): everything thegovernment pays for labor, goods, and services

Net exports (NX): exports minus imports

Calculating GDP

ProductionApproach: Measure

total value ofeconomic output

ExpendituresApproach: Counteverything spenton consumption

Income Approach:Follow the money

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 21/48

ECONOMICS CRAM KIT | 20

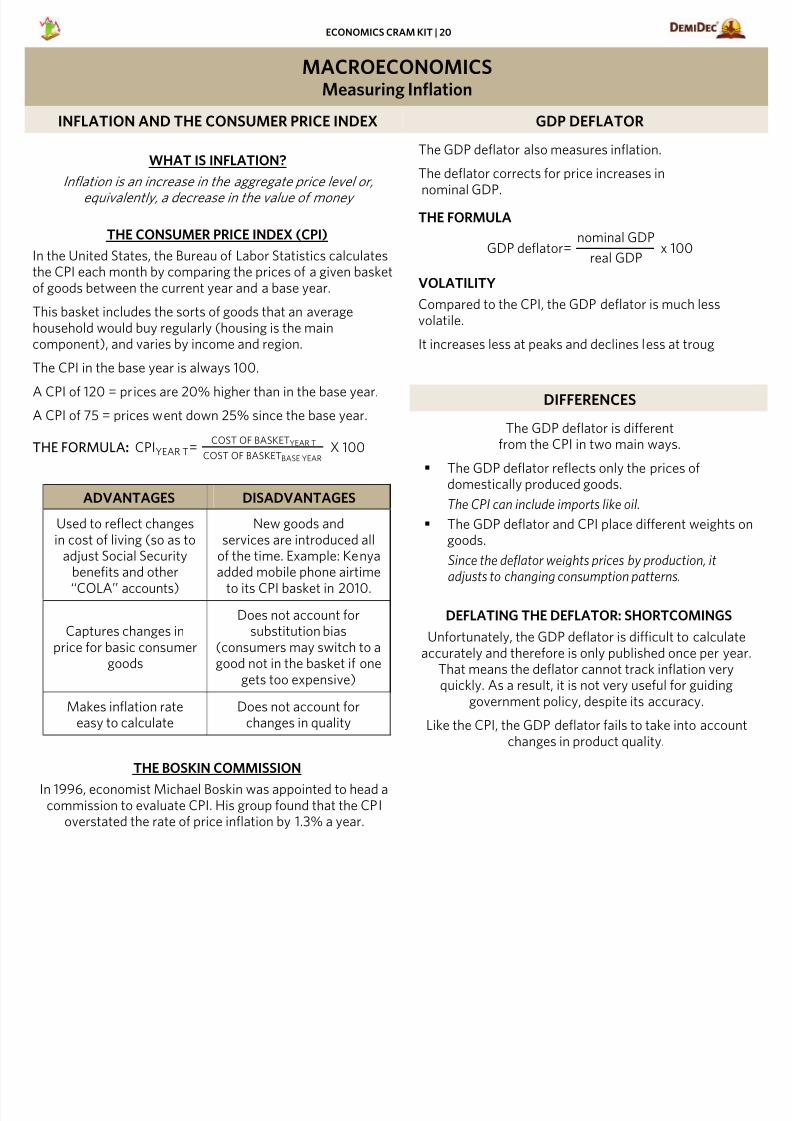

MACROECONOMICSMeasuring Inflation

INFLATION AND THE CONSUMER PRICE INDEX GDP DEFLATOR

WHAT IS INFLATION?

Inflation is an increase in the aggregate price level or,

equivalently, a decrease in the value of money

THE CONSUMER PRICE INDEX (CPI)

In the United States, the Bureau of Labor Statistics calculatesthe CPI each month by comparing the prices of a given basketof goods between the current year and a base year.

This basket includes the sorts of goods that an averagehousehold would buy regularly (housing is the maincomponent), and varies by income and region.

The CPI in the base year is always 100.

A CPI of 120 = prices are 20% higher than in the base year.A CPI of 75 = prices went down 25% since the base year.

THE FORMULA: CPIYEAR T=COST OF BASKETYEAR T

COST OF BASKETBASE YEAR X 100

ADVANTAGES DISADVANTAGES

Used to reflect changesin cost of living (so as to

adjust Social Securitybenefits and other

‘‘COLA’’ accounts)

New goods andservices are introduced all

of the time. Example: Kenyaadded mobile phone airtime

to its CPI basket in 2010.

Captures changes inprice for basic consumer

goods

Does not account forsubstitution bias

(consumers may switch to agood not in the basket if one

gets too expensive)

Makes inflation rateeasy to calculate

Does not account forchanges in quality

THE BOSKIN COMMISSION

In 1996, economist Michael Boskin was appointed to head acommission to evaluate CPI. His group found that the CPI

overstated the rate of price inflation by 1.3% a year.

The GDP deflator also measures inflation.

The deflator corrects for price increases in

nominal GDP.THE FORMULA

GDP deflator=nominal GDP

real GDP x 100

VOLATILITY

Compared to the CPI, the GDP deflator is much lessvolatile.

It increases less at peaks and declines less at troug

DIFFERENCES

The GDP deflator is differentfrom the CPI in two main ways.

The GDP deflator reflects only the prices ofdomestically produced goods.

The CPI can include imports like oil.

The GDP deflator and CPI place different weights ogoods.

Since the deflator weights prices by production, itadjusts to changing consumption patterns.

DEFLATING THE DEFLATOR: SHORTCOMINGS

Unfortunately, the GDP deflator is difficult to calculateaccurately and therefore is only published once per yea

That means the deflator cannot track inflation veryquickly. As a result, it is not very useful for guiding

government policy, despite its accuracy.

Like the CPI, the GDP deflator fails to take into accounchanges in product quality.

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 22/48

ECONOMICS CRAM KIT | 21

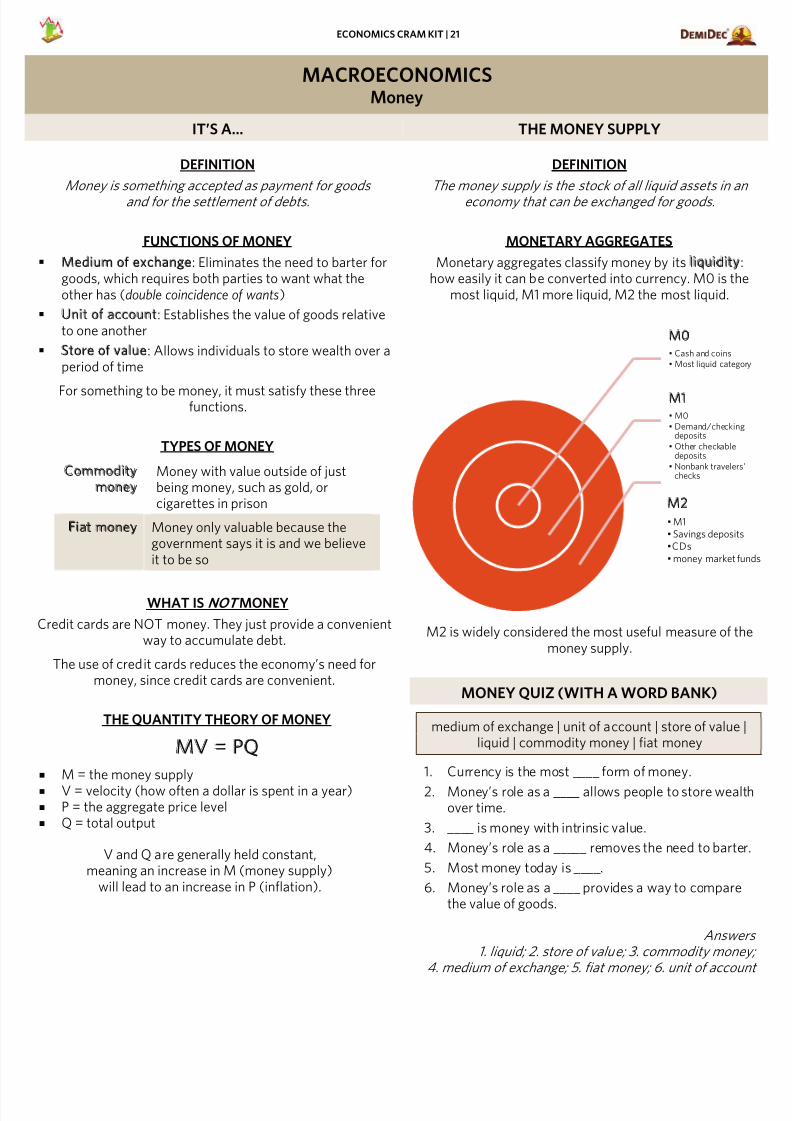

MACROECONOMICSMoney

IT’S A… THE MONEY SUPPLY

DEFINITION

Money is something accepted as payment for goods

and for the settlement of debts.

FUNCTIONS OF MONEY

Medium of exchange: Eliminates the need to barter forgoods, which requires both parties to want what theother has (double coincidence of wants)

Unit of account: Establishes the value of goods relativeto one another

Store of value: Allows individuals to store wealth over aperiod of time

For something to be money, it must satisfy these threefunctions.

TYPES OF MONEY

Commodity money

Money with value outside of justbeing money, such as gold, orcigarettes in prison

Fiat money Money only valuable because thegovernment says it is and we believeit to be so

WHAT IS NOT MONEY

Credit cards are NOT money. They just provide a convenientway to accumulate debt.

The use of credit cards reduces the economy’s need formoney, since credit cards are convenient.

THE QUANTITY THEORY OF MONEY

MV = PQ

M = the money supply

V = velocity (how often a dollar is spent in a year)

P = the aggregate price level

Q = total output

V and Q are generally held constant,meaning an increase in M (money supply)

will lead to an increase in P (inflation).

DEFINITION

The money supply is the stock of all liquid assets in a

economy that can be exchanged for goods.

MONETARY AGGREGATES

Monetary aggregates classify money by its liquidityhow easily it can be converted into currency. M0 is th

most liquid, M1 more liquid, M2 the most liquid.

M2 is widely considered the most useful measure of thmoney supply.

MONEY QUIZ (WITH A WORD BANK)

medium of exchange | unit of account | store of valueliquid | commodity money | fiat money

1. Currency is the most ____ form of money.

2. Money’s role as a ____ allows people to store weaover time.

3. ____ is money with intrinsic value.

4. Money’s role as a _____ removes the need to barte

5. Most money today is ____.

6. Money’s role as a ____ provides a way to comparethe value of goods.

Answe1. liquid; 2. store of value; 3. commodity mon

4. medium of exchange; 5. fiat money; 6. unit of accou

M0• Cash and coins• Most liquid categ

M1• M0

• Demand/checkindeposits

• Other checkabledeposits

• Nonbank travelerschecks

M2

• M1

• Savings deposit

•CDs

• money market f

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 23/48

ECONOMICS CRAM KIT | 22

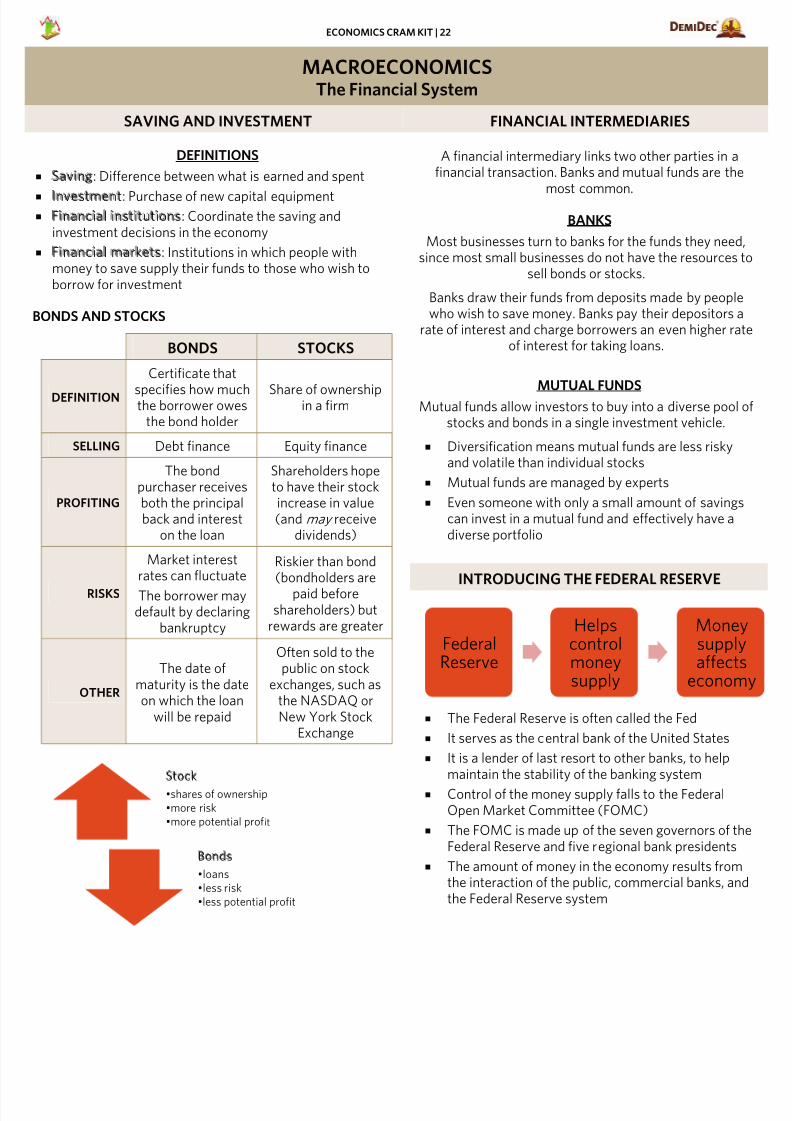

MACROECONOMICSThe Financial System

SAVING AND INVESTMENT FINANCIAL INTERMEDIARIES

DEFINITIONS

Saving: Difference between what is earned and spent

Investment: Purchase of new capital equipment Financial institutions: Coordinate the saving and

investment decisions in the economy

Financial markets: Institutions in which people withmoney to save supply their funds to those who wish toborrow for investment

BONDS AND STOCKS

BONDS STOCKS

DEFINITION

Certificate that

specifies how muchthe borrower owesthe bond holder

Share of ownershipin a firm

SELLING Debt finance Equity finance

PROFITING

The bondpurchaser receivesboth the principalback and interest

on the loan

Shareholders hopeto have their stockincrease in value(and may receive

dividends)

RISKS

Market interestrates can fluctuate

The borrower maydefault by declaring

bankruptcy

Riskier than bond(bondholders are

paid beforeshareholders) but

rewards are greater

OTHER

The date ofmaturity is the dateon which the loan

will be repaid

Often sold to thepublic on stock

exchanges, such asthe NASDAQ orNew York Stock

Exchange

A financial intermediary links two other parties in afinancial transaction. Banks and mutual funds are the

most common.

BANKS

Most businesses turn to banks for the funds they needsince most small businesses do not have the resources

sell bonds or stocks.

Banks draw their funds from deposits made by peoplewho wish to save money. Banks pay their depositors a

rate of interest and charge borrowers an even higher raof interest for taking loans.

MUTUAL FUNDS

Mutual funds allow investors to buy into a diverse pool stocks and bonds in a single investment vehicle.

Diversification means mutual funds are less riskyand volatile than individual stocks

Mutual funds are managed by experts

Even someone with only a small amount of savingscan invest in a mutual fund and effectively have adiverse portfolio

INTRODUCING THE FEDERAL RESERVE

The Federal Reserve is often called the Fed

It serves as the central bank of the United States

It is a lender of last resort to other banks, to helpmaintain the stability of the banking system

Control of the money supply falls to the FederalOpen Market Committee (FOMC)

The FOMC is made up of the seven governors of thFederal Reserve and five regional bank presidents

The amount of money in the economy results fromthe interaction of the public, commercial banks, anthe Federal Reserve system

Stock

•shares of ownership

•more risk

•more potential profit

Bonds

•loans

•less risk

•less potential profit

FederalReserve

Helpscontrolmoneysupply

Monesupplyaffects

econom

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 24/48

ECONOMICS CRAM KIT | 23

MACROECONOMICSMonetary Policy

SHOW ME THE MONEY THE FED IN SLIGHTLY MORE DETAIL

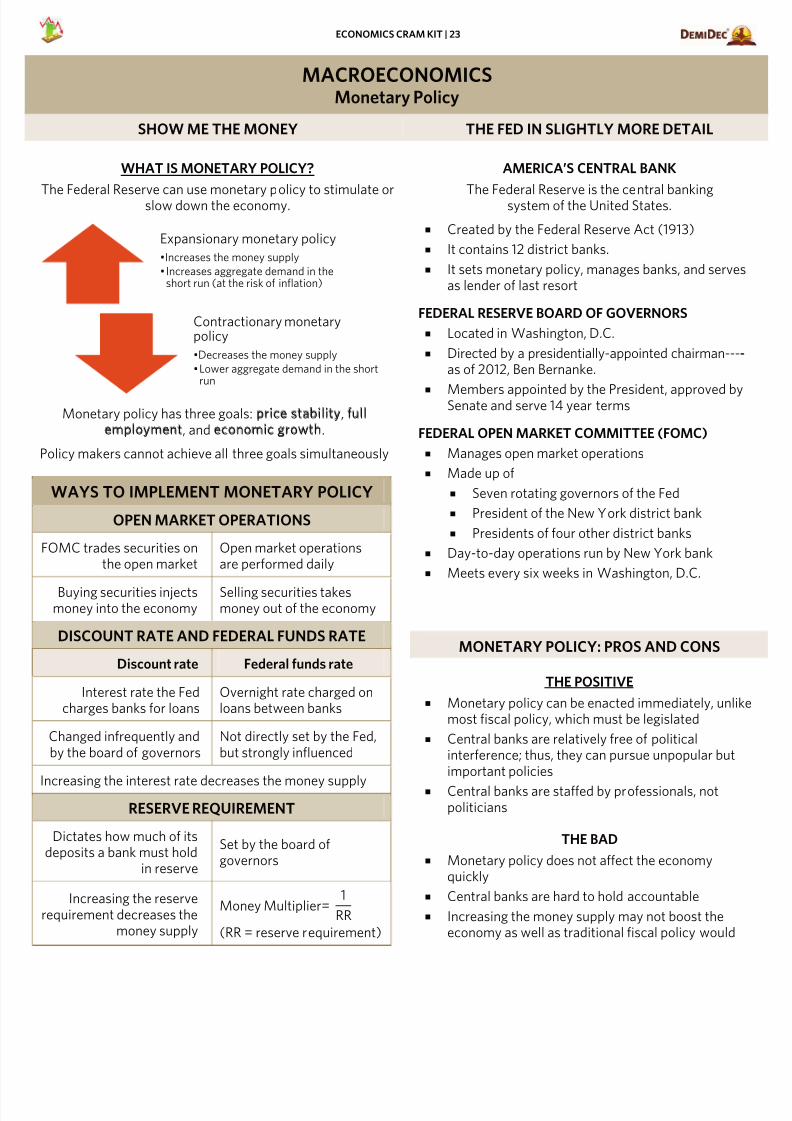

WHAT IS MONETARY POLICY?

The Federal Reserve can use monetary policy to stimulate orslow down the economy.

Monetary policy has three goals: price stability, full employment, and economic growth.

Policy makers cannot achieve all three goals simultaneously

WAYS TO IMPLEMENT MONETARY POLICY

OPEN MARKET OPERATIONS

FOMC trades securities onthe open market

Open market operationsare performed daily

Buying securities injectsmoney into the economy

Selling securities takesmoney out of the economy

DISCOUNT RATE AND FEDERAL FUNDS RATE

Discount rate Federal funds rate

Interest rate the Fedcharges banks for loans

Overnight rate charged onloans between banks

Changed infrequently andby the board of governors

Not directly set by the Fed,but strongly influenced

Increasing the interest rate decreases the money supply

RESERVE REQUIREMENT

Dictates how much of itsdeposits a bank must hold

in reserve

Set by the board ofgovernors

Increasing the reserverequirement decreases the

money supply

Money Multiplier=1

RR

(RR = reserve requirement)

AMERICA’S CENTRAL BANK

The Federal Reserve is the central bankingsystem of the United States.

Created by the Federal Reserve Act (1913)

It contains 12 district banks.

It sets monetary policy, manages banks, and serveas lender of last resort

FEDERAL RESERVE BOARD OF GOVERNORS

Located in Washington, D.C.

Directed by a presidentially-appointed chairman---as of 2012, Ben Bernanke.

Members appointed by the President, approved bySenate and serve 14 year terms

FEDERAL OPEN MARKET COMMITTEE (FOMC)

Manages open market operations

Made up of

Seven rotating governors of the Fed

President of the New York district bank

Presidents of four other district banks

Day-to-day operations run by New York bank

Meets every six weeks in Washington, D.C.

MONETARY POLICY: PROS AND CONS

THE POSITIVE

Monetary policy can be enacted immediately, unlikmost fiscal policy, which must be legislated

Central banks are relatively free of politicalinterference; thus, they can pursue unpopular butimportant policies

Central banks are staffed by professionals, notpoliticians

THE BAD

Monetary policy does not affect the economyquickly

Central banks are hard to hold accountable

Increasing the money supply may not boost theeconomy as well as traditional fiscal policy would

Expansionary monetary policy

•Increases the money supply

•Increases aggregate demand in theshort run (at the risk of inflation)

Contractionary monetarypolicy

•Decreases the money supply

•Lower aggregate demand in the shortrun

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 25/48

ECONOMICS CRAM KIT | 24

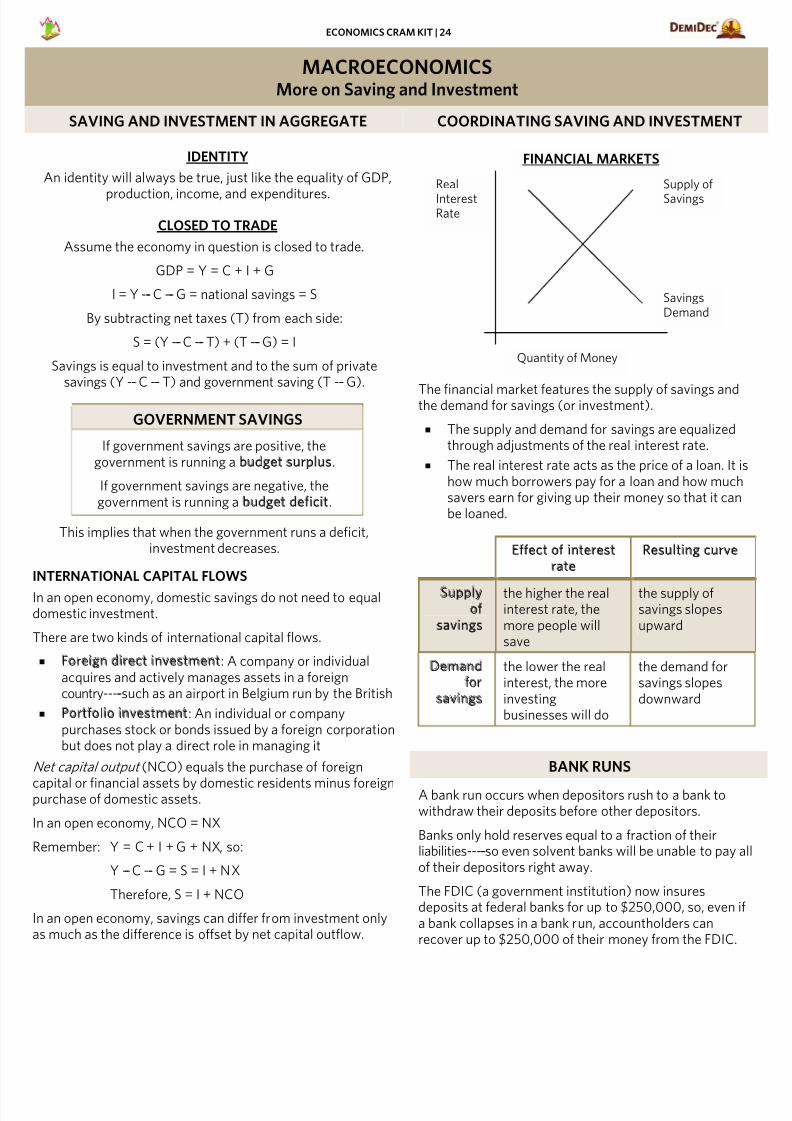

MACROECONOMICSMore on Saving and Investment

SAVING AND INVESTMENT IN AGGREGATE COORDINATING SAVING AND INVESTMENT

IDENTITY

An identity will always be true, just like the equality of GDP,

production, income, and expenditures.

CLOSED TO TRADE

Assume the economy in question is closed to trade.

GDP = Y = C + I + G

I = Y --- C --- G = national savings = S

By subtracting net taxes (T) from each side:

S = (Y --- C --- T) + (T --- G) = I

Savings is equal to investment and to the sum of privatesavings (Y --- C --- T) and government saving (T --- G).

GOVERNMENT SAVINGS

If government savings are positive, thegovernment is running a budget surplus.

If government savings are negative, thegovernment is running a budget deficit.

This implies that when the government runs a deficit,investment decreases.

INTERNATIONAL CAPITAL FLOWS

In an open economy, domestic savings do not need to equaldomestic investment.

There are two kinds of international capital flows.

Foreign direct investment: A company or individualacquires and actively manages assets in a foreigncountry-----such as an airport in Belgium run by the British

Portfolio investment: An individual or companypurchases stock or bonds issued by a foreign corporationbut does not play a direct role in managing it

Net capital output (NCO) equals the purchase of foreign

capital or financial assets by domestic residents minus foreignpurchase of domestic assets.

In an open economy, NCO = NX

Remember: Y = C + I + G + NX, so:

Y --- C --- G = S = I + NX

Therefore, S = I + NCO

In an open economy, savings can differ from investment onlyas much as the difference is offset by net capital outflow.

The financial market features the supply of savings andthe demand for savings (or investment).

The supply and demand for savings are equalizedthrough adjustments of the real interest rate.

The real interest rate acts as the price of a loan. It ihow much borrowers pay for a loan and how muchsavers earn for giving up their money so that it canbe loaned.

Effect of interest rate

Resulting curve

Supply of

savings

the higher the realinterest rate, themore people willsave

the supply ofsavings slopesupward

Demand for

savings

the lower the realinterest, the moreinvestingbusinesses will do

the demand forsavings slopesdownward

BANK RUNS

A bank run occurs when depositors rush to a bank towithdraw their deposits before other depositors.

Banks only hold reserves equal to a fraction of theirliabilities-----so even solvent banks will be unable to pay aof their depositors right away.

The FDIC (a government institution) now insuresdeposits at federal banks for up to $250,000, so, even ia bank collapses in a bank run, accountholders canrecover up to $250,000 of their money from the FDIC.

Quantity of Money

FINANCIAL MARKETS

Real

InterestRate

SavingsDemand

Supply of

Savings

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 26/48

ECONOMICS CRAM KIT | 25

MACROECONOMICSMoney Market in the Long Run

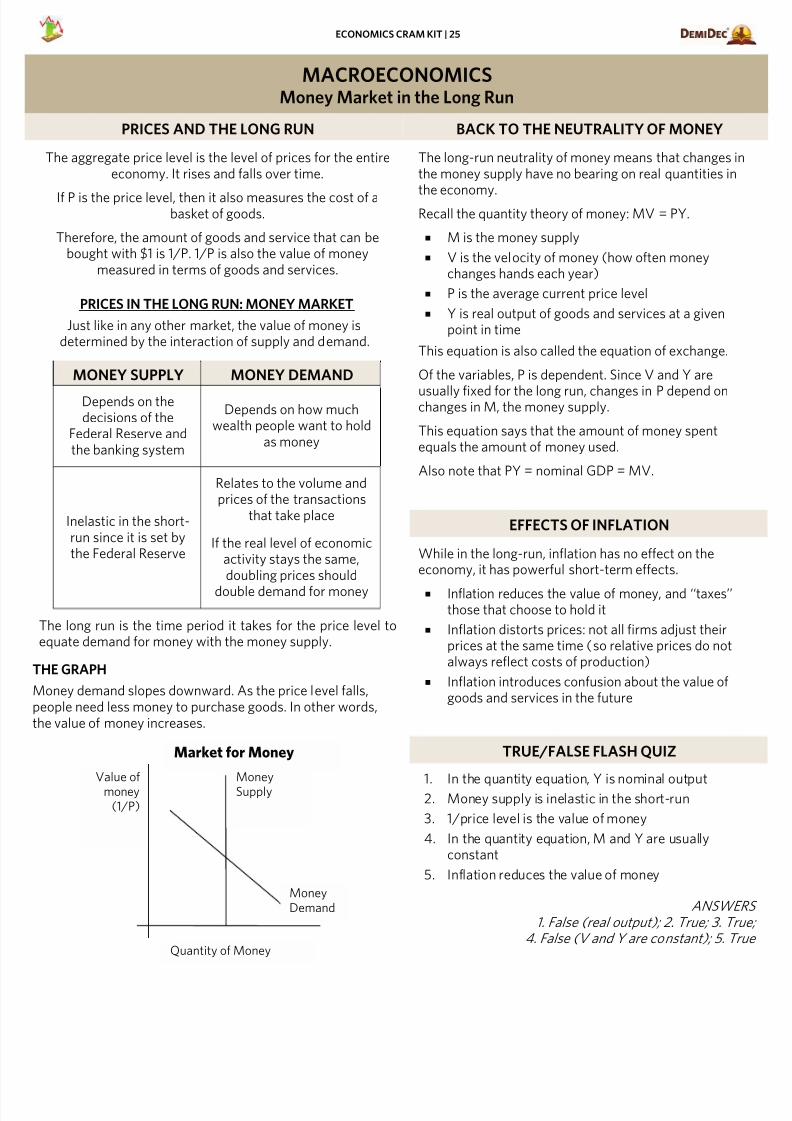

PRICES AND THE LONG RUN BACK TO THE NEUTRALITY OF MONEY

The aggregate price level is the level of prices for the entireeconomy. It rises and falls over time.

If P is the price level, then it also measures the cost of abasket of goods.

Therefore, the amount of goods and service that can bebought with $1 is 1/P. 1/P is also the value of money

measured in terms of goods and services.

PRICES IN THE LONG RUN: MONEY MARKET

Just like in any other market, the value of money isdetermined by the interaction of supply and demand.

MONEY SUPPLY MONEY DEMAND

Depends on thedecisions of the

Federal Reserve andthe banking system

Depends on how muchwealth people want to hold

as money

Inelastic in the short-run since it is set bythe Federal Reserve

Relates to the volume andprices of the transactions

that take place

If the real level of economicactivity stays the same,doubling prices should

double demand for money

The long run is the time period it takes for the price level toequate demand for money with the money supply.

THE GRAPH

Money demand slopes downward. As the price level falls,people need less money to purchase goods. In other words,the value of money increases.

The long-run neutrality of money means that changes inthe money supply have no bearing on real quantities in

the economy.Recall the quantity theory of money: MV = PY.

M is the money supply

V is the velocity of money (how often moneychanges hands each year)

P is the average current price level

Y is real output of goods and services at a givenpoint in time

This equation is also called the equation of exchange.

Of the variables, P is dependent. Since V and Y are

usually fixed for the long run, changes in P depend onchanges in M, the money supply.

This equation says that the amount of money spentequals the amount of money used.

Also note that PY = nominal GDP = MV.

EFFECTS OF INFLATION

While in the long-run, inflation has no effect on theeconomy, it has powerful short-term effects.

Inflation reduces the value of money, and ‘‘taxes’’those that choose to hold it

Inflation distorts prices: not all firms adjust theirprices at the same time (so relative prices do notalways reflect costs of production)

Inflation introduces confusion about the value ofgoods and services in the future

TRUE/FALSE FLASH QUIZ

1. In the quantity equation, Y is nominal output2. Money supply is inelastic in the short-run

3. 1/price level is the value of money

4. In the quantity equation, M and Y are usuallyconstant

5. Inflation reduces the value of money

ANSWE

1. False (real output); 2. True; 3. Tru4. False (V and Y are constant); 5. Tr

Quantity of Money

Market for Money

Value ofmoney

(1/P)

MoneyDemand

MoneySupply

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 27/48

ECONOMICS CRAM KIT | 26

MACROECONOMICSModeling the Economy

THE CIRCULAR FLOW MODEL FLOWS

GOODS AND SERVICES (CLOCKWISE)

MONEY (COUNTER-CLOCKWISE)

THE ACTORS

FIRMSProduce goods and services usingthe factors of production ownedby households

HOUSEHOLDS

Rent the factors of production(land, labor, capital,entrepreneurship) to firms

Consume goods produced by firms

GOVERNMENT

Ability to tax to earn income

Can borrow from financial marketsto produce goods for society

GDP AS FLOW

GDP is equal to the flow around the model at any

given point The expenditure approach is the sum of consumpt

and government purchases (since investment andexports are not counted in this model)

The income approach uses the flow of income tohouseholds

Totaling the flow in the money diagram yieldsnominal GDP

Totaling the flow in the goods and services diagramyields real GDP

ENTERING THE CIRCULAR FLOW MODELNew wealth enters the cycle through households.

Households provide the human labor used to work. Eveinputs such as land belong to individuals, which in turnbelong to households. These land-owning individuals retheir land to businesses.

CIRCULAR FLOW FLASH QUIZ

QUESTIONS

1. The three actors in the circular flow model are_______, _______, and _______.

2. The two markets in the circular flow model are themarkets for _______ and _______.

3. All factors of production are owned by _______.

4. With regard to the circular flow, nominal GDP isequal to the _______.

5. ______ sits between households and the goods andservices market.

ANSWERS

1. households; firms; government

2. goods and services; factors of production

3. households

4. flow around the money diagram

5. government

FactorMarkets

Firms

Goods andServicesMarkets

Households

FactorMarkets

Households

Goods andServicesMarkets

FirmsGovernment

Governmentpurchases

Income Wages andrent

RevenueConsumption

Taxes

Government

Goods andservices

Land, capitallabor

Factors ofproduction

Goods andservices

Goods andservices

Transfers

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 28/48

ECONOMICS CRAM KIT | 27

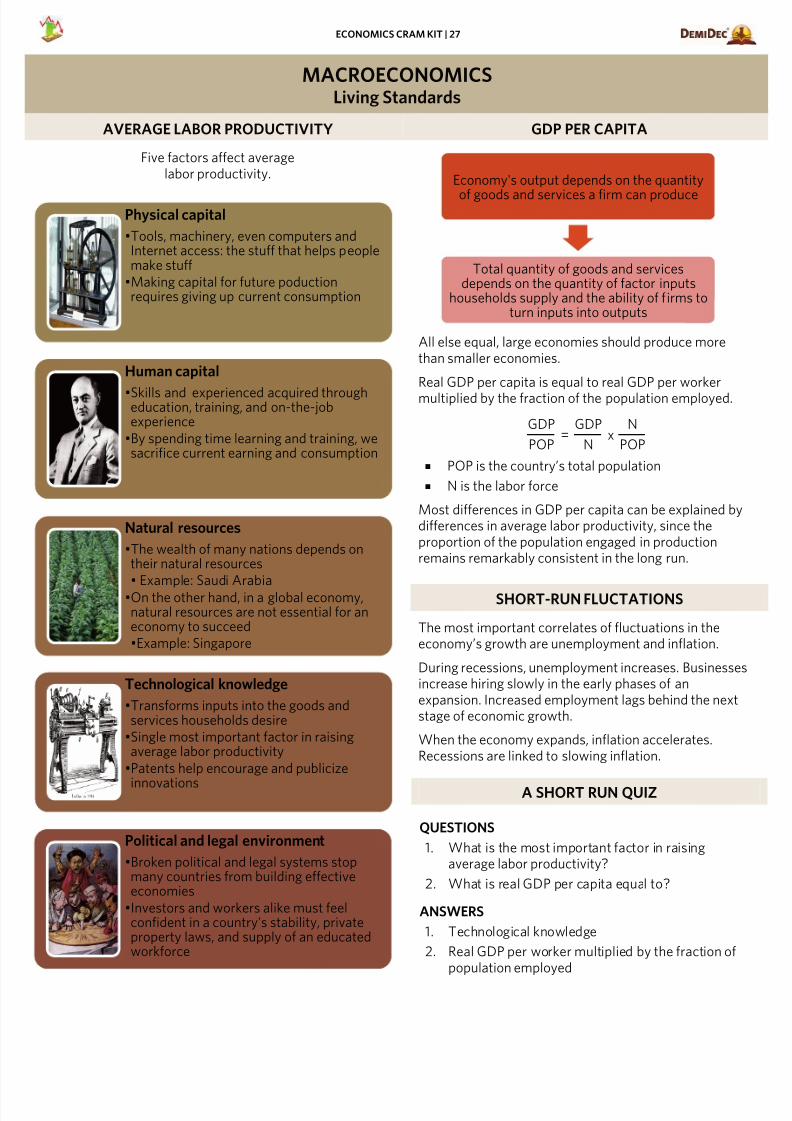

MACROECONOMICSLiving Standards

AVERAGE LABOR PRODUCTIVITY GDP PER CAPITA

Five factors affect averagelabor productivity.

All else equal, large economies should produce morethan smaller economies.

Real GDP per capita is equal to real GDP per workermultiplied by the fraction of the population employed.

GDP

POP =

GDP

N x

N

POP

POP is the country’s total population

N is the labor force

Most differences in GDP per capita can be explained bydifferences in average labor productivity, since theproportion of the population engaged in productionremains remarkably consistent in the long run.

SHORT-RUN FLUCTATIONS

The most important correlates of fluctuations in theeconomy’s growth are unemployment and inflation.

During recessions, unemployment increases. Businesseincrease hiring slowly in the early phases of anexpansion. Increased employment lags behind the nextstage of economic growth.

When the economy expands, inflation accelerates.Recessions are linked to slowing inflation.

A SHORT RUN QUIZ

QUESTIONS

1. What is the most important factor in raisingaverage labor productivity?

2. What is real GDP per capita equal to?

ANSWERS

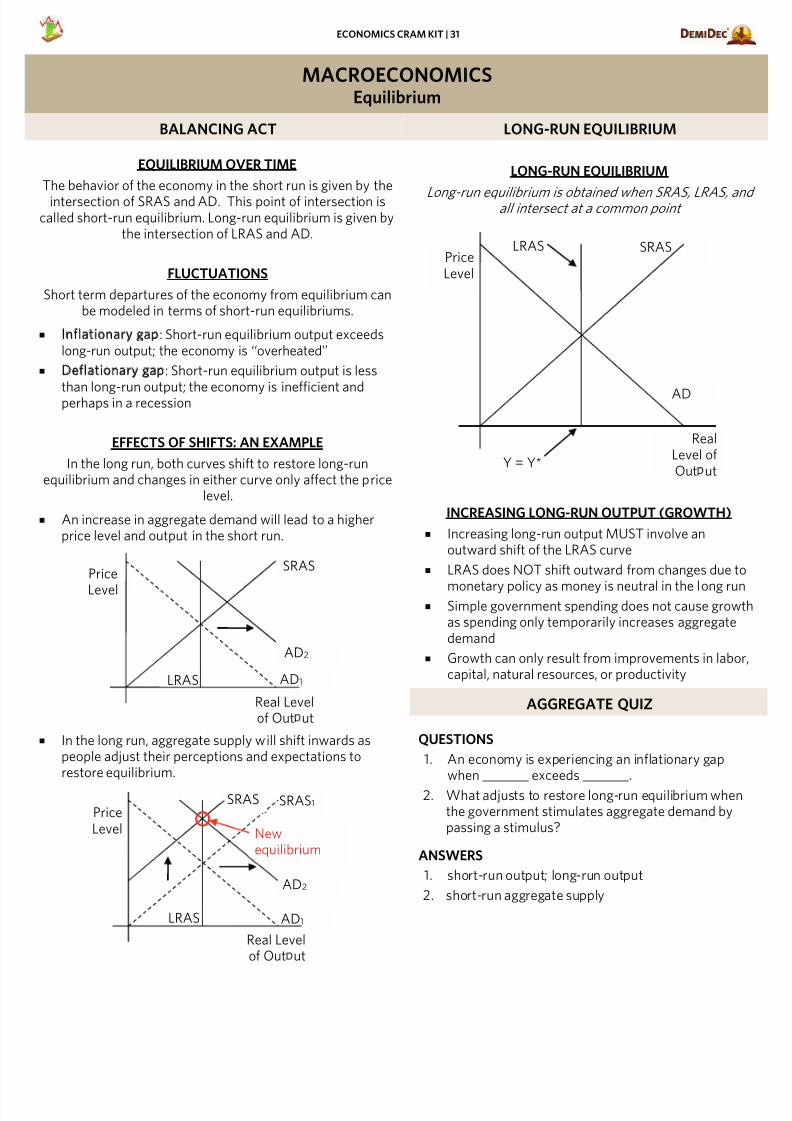

1. Technological knowledge

2. Real GDP per worker multiplied by the fraction ofpopulation employed

Physical capital

•Tools, machinery, even computers andInternet access: the stuff that helps peoplemake stuff

•Making capital for future poductionrequires giving up current consumption

Human capital

•Skills and experienced acquired througheducation, training, and on-the-jobexperience

•By spending time learning and training, wesacrifice current earning and consumption

Natural resources

•The wealth of many nations depends ontheir natural resources• Example: Saudi Arabia

•On the other hand, in a global economy,natural resources are not essential for aneconomy to succeed•Example: Singapore

Technological knowledge

•Transforms inputs into the goods andservices households desire

•Single most important factor in raisingaverage labor productivity

•Patents help encourage and publicize

innovations

Political and legal environment

•Broken political and legal systems stopmany countries from building effectiveeconomies

•Investors and workers alike must feelconfident in a country's stability, privateproperty laws, and supply of an educatedworkforce

Economy's output depends on the quantity

of goods and services a firm can produce

Total quantity of goods and servicesdepends on the quantity of factor inputs

households supply and the ability of firms toturn inputs into outputs

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 29/48

ECONOMICS CRAM KIT | 28

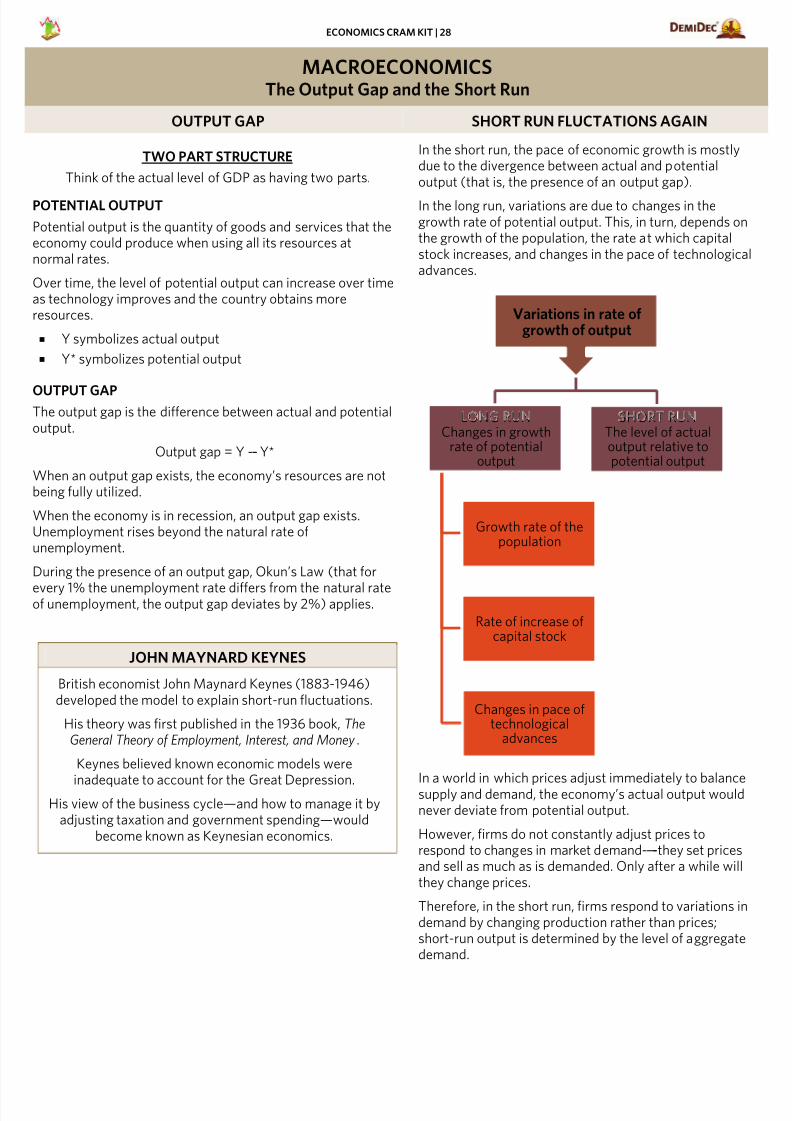

MACROECONOMICSThe Output Gap and the Short Run

OUTPUT GAP SHORT RUN FLUCTATIONS AGAIN

TWO PART STRUCTURE

Think of the actual level of GDP as having two parts.

POTENTIAL OUTPUT

Potential output is the quantity of goods and services that theeconomy could produce when using all its resources atnormal rates.

Over time, the level of potential output can increase over timeas technology improves and the country obtains moreresources.

Y symbolizes actual output

Y* symbolizes potential output

OUTPUT GAPThe output gap is the difference between actual and potentialoutput.

Output gap = Y --- Y*

When an output gap exists, the economy’s resources are notbeing fully utilized.

When the economy is in recession, an output gap exists.Unemployment rises beyond the natural rate ofunemployment.

During the presence of an output gap, Okun’s Law (that for

every 1% the unemployment rate differs from the natural rateof unemployment, the output gap deviates by 2%) applies.

JOHN MAYNARD KEYNES

British economist John Maynard Keynes (1883-1946)developed the model to explain short-run fluctuations.

His theory was first published in the 1936 book, TheGeneral Theory of Employment, Interest, and Money .

Keynes believed known economic models were

inadequate to account for the Great Depression.His view of the business cycle—and how to manage it by

adjusting taxation and government spending—wouldbecome known as Keynesian economics.

In the short run, the pace of economic growth is mostlydue to the divergence between actual and potentialoutput (that is, the presence of an output gap).

In the long run, variations are due to changes in thegrowth rate of potential output. This, in turn, depends othe growth of the population, the rate at which capitalstock increases, and changes in the pace of technologicadvances.

In a world in which prices adjust immediately to balancesupply and demand, the economy’s actual output wouldnever deviate from potential output.

However, firms do not constantly adjust prices torespond to changes in market demand-----they set pricesand sell as much as is demanded. Only after a while wilthey change prices.

Therefore, in the short run, firms respond to variations idemand by changing production rather than prices;short-run output is determined by the level of aggregatedemand.

Variations in rate ofgrowth of output

LONG RUNChanges in growth

rate of potentialoutput

Growth rate of thepopulation

Rate of increase ofcapital stock

Changes in pace oftechnological

advances

SHORT RUNThe level of actualoutput relative topotential output

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 30/48

ECONOMICS CRAM KIT | 29

MACROECONOMICSAggregate Demand

INTRODUCING THE AD/AS MODEL AGGREGATE SHIFTS RESULT FROM…

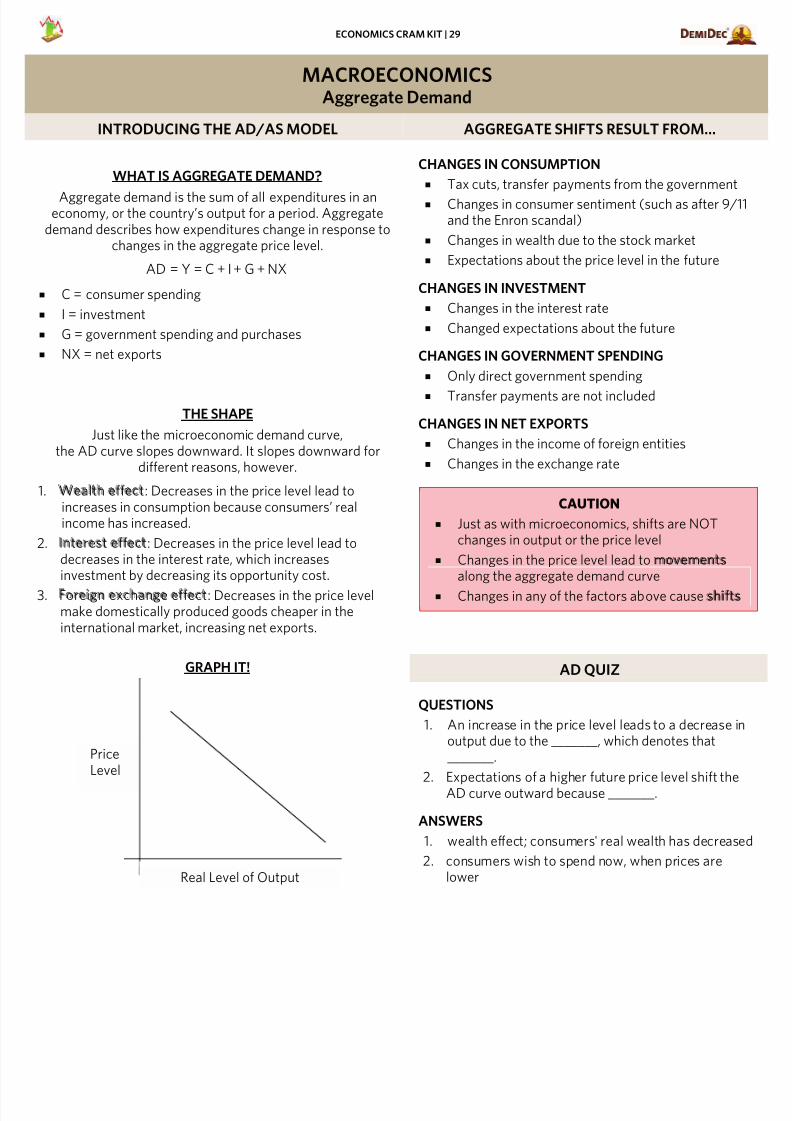

WHAT IS AGGREGATE DEMAND?

Aggregate demand is the sum of all expenditures in aneconomy, or the country’s output for a period. Aggregate

demand describes how expenditures change in response tochanges in the aggregate price level.

C = consumer spending

I = investment

G = government spending and purchases

NX = net exports

THE SHAPE

Just like the microeconomic demand curve,the AD curve slopes downward. It slopes downward for

different reasons, however.

1. Wealth effect: Decreases in the price level lead toincreases in consumption because consumers’ realincome has increased.

2. Interest effect: Decreases in the price level lead todecreases in the interest rate, which increasesinvestment by decreasing its opportunity cost.

3. Foreign exchange effect: Decreases in the price levelmake domestically produced goods cheaper in theinternational market, increasing net exports.

GRAPH IT!

CHANGES IN CONSUMPTION

Tax cuts, transfer payments from the government

Changes in consumer sentiment (such as after 9/1and the Enron scandal)

Changes in wealth due to the stock market

Expectations about the price level in the future

CHANGES IN INVESTMENT

Changes in the interest rate

Changed expectations about the future

CHANGES IN GOVERNMENT SPENDING

Only direct government spending

Transfer payments are not included

CHANGES IN NET EXPORTS

Changes in the income of foreign entities

Changes in the exchange rate

CAUTION

Just as with microeconomics, shifts are NOTchanges in output or the price level

Changes in the price level lead to movements along the aggregate demand curve

Changes in any of the factors above cause shifts

AD QUIZ

QUESTIONS

1. An increase in the price level leads to a decrease inoutput due to the _______, which denotes that_______.

2. Expectations of a higher future price level shift theAD curve outward because _______.

ANSWERS

1. wealth effect; consumers' real wealth has decrease

2. consumers wish to spend now, when prices arelower

NX+G+I+C=Y=AD

PriceLevel

Real Level of Output

7/18/2019 Economics Cram Kit

http://slidepdf.com/reader/full/economics-cram-kit-56d6a0b3cdef5 31/48

ECONOMICS CRAM KIT | 30

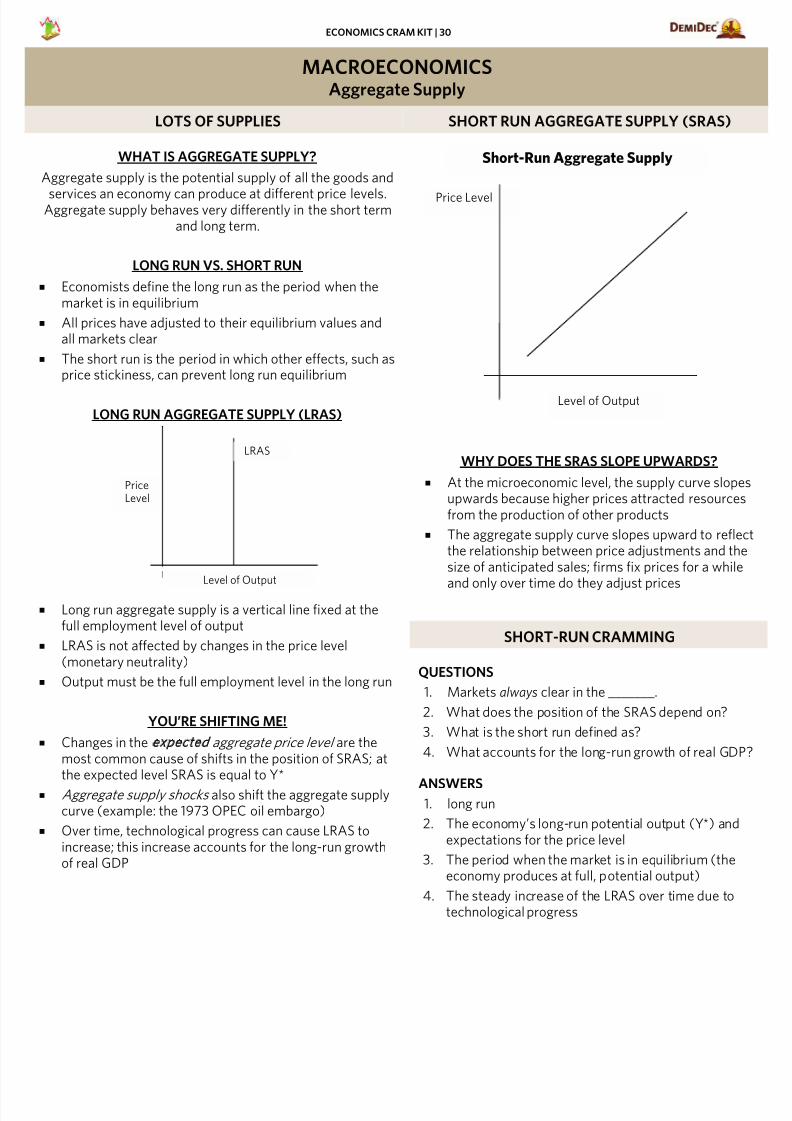

MACROECONOMICSAggregate Supply

LOTS OF SUPPLIES SHORT RUN AGGREGATE SUPPLY (SRAS)

WHAT IS AGGREGATE SUPPLY?

Aggregate supply is the potential supply of all the goods and

services an economy can produce at different price levels.Aggregate supply behaves very differently in the short term

and long term.

LONG RUN VS. SHORT RUN

Economists define the long run as the period when themarket is in equilibrium

All prices have adjusted to their equilibrium values andall markets clear

The short run is the period in which other effects, such asprice stickiness, can prevent long run equilibrium

LONG RUN AGGREGATE SUPPLY (LRAS)

Long run aggregate supply is a vertical line fixed at thefull employment level of output

LRAS is not affected by changes in the price level(monetary neutrality)

Output must be the full employment level in the long run

YOU’RE SHIFTING ME!

Changes in the expected aggregate price level are themost common cause of shifts in the position of SRAS; atthe expected level SRAS is equal to Y*

Aggregate supply shocks also shift the aggregate supplycurve (example: the 1973 OPEC oil embargo)

Over time, technological progress can cause LRAS toincrease; this increase accounts for the long-run growthof real GDP

WHY DOES THE SRAS SLOPE UPWARDS?