Embed Size (px)

Citation preview

Chapter 4

ECONOMICS OF ATM

4.1 INTRODUCTION:

The Automated Teller Machine (ATM) is seen everywhere. This machine has

brought Innovations in the Banking sector all over the world. The advent of the ATM has

made the concept of round the clock banking a reality. The ATM has been helpful to both

the bankers and the customers. The huge crowd of customers in the banking hall of abranch waiting for their tum to collect cash is disappearing. The branch business timings

have lost significance to the customers after the introduction of ATM.

ATM is a device used by the bank customers to process account transactions. The

customer inserts into the ATM, a plastic card i.e. encoded with information on a magnetic

strip. The strip contains an identification code that is transmitted to the bank's central

computer by modem. Every cardholder should be given a PIN (personal identification

number) that he should enter and after verifying the same with the records, ATM would

allow operations.

4.2 ECONOMICS OF ATM:

The cost of ATM has drastically come down over the past 5 years. From an

average original investment of Rs.15 lakh, il has been reduced to Rs. 9lakh. In addition a

recurring cost of Rs.l lakhper month has to be incurred. With this cost pattern, around

180 transactions per day are required to break even. The cost of each transaction at the

branch of the Bank is Rs.60 while it is Rs.10 if carried out through ATM. Nearly 93

percent of UTI Bank's retail cash transactic'rns are done through its ATM'S. This is the

highest compared to other Bank's like ICICI Bank and HDFC bank.

An automated teller machine or automatic teller machine (ATM) is a

computerized telecommunications device that provides a financial institution's customers

a secure method of performing financial transactions in a public space without the need

for a human clerk or bank teller. Using an ATM, customers can access their bank

accounts in order to make cash withdrawals (or credit card cash advances) and check

" 1,26 -

their account balances. Many ATMs also allow people to deposit cash or cheques,transfer money between their bank accounts, pay bills, or purchase goods and services.

A mechanical cash dispenser, arguably an ATM, was developed and built byLuther George Simjian and installed in 1939 in New york by the City Bank of NewYork, but removed after 6 months due to the lack of customer acceptance. Don Wetzelwas the co-patentee and chief conceptualist of the automated teller machine, an idea hethought of while waiting in line at a Dallas bank. At the time (196g) Wetzel was the vicePresident of Product Planning at Docutel, the company that developed automatedbaggage-handling equipment. The other tw'o inventors listed on the patent were TomBarnes, the chief mechanical engineer and George Chastain, the electrical engineer. Ittook five million dollars to develop the ATM. The concept of the ATM first began in1968; a working prototlpe came about in 1969 and was issued a patent in 1973. The firstworking ATM was installed in a New York based Chemical Bank though there aredifferent claims to which bank had the first ATM.

There are no hard international or governmental-compiled numbers totaling thecomplete number of ATMs in use worldwide. Estimates developed by ATMIA (ATMIndustry Association) place the number of ATMs in use at over 1.5 million as of August2006' Transacting business through either the ATMs or the Internet in India has just tenyears of operational history to refer to, with the bulk of strategic activity having takenplace during the past two years or so. The market is yet untapped. There are about 32,000ATMs in the country now. A little more than half that number is installed off-site. Largesize banks have a target of setting up at least l0 ATMs each in 2006-07.4 recent RBIreview states that one third of all commercial banking outlets are ATMs. private Bankshave at least three ATMs for one branch. With around 3,160 branches, Central Bank hasthe third largest network in the country. It is targeting to double its business from thecurrent Rs I lakh crore over three years. It is also planning to set up about 500 ATMs bythe end-March 20oi as said by Mr. K. Subbaraman, Executive Director, Central Bank ofIndia' The basic cost of an ATM linked to a branch, independent of other costs. is aboutRs 7'5 lakh' The hardware costs about Rs 3 lakh, the UpS and software another Rs 4

-L27-

lakh, says Mr. B. Rajagopalan, AGM, Technology & communications, State Bank ofIndia. About two years ago the basic cost of an ATM was Rs 20 lakhs.

4.2.1AT}.I Expansion In India:

The technological advancements is been proved beneficial to the customers and

even the banks with the introduction of the Automated Teller Machine (ATM). ATMshave been used by banks not only to expand their reach to customers, but also to offervalue-added services. The ATMs offer convenience to customers and provide bankingservices well beyond the traditional banking.

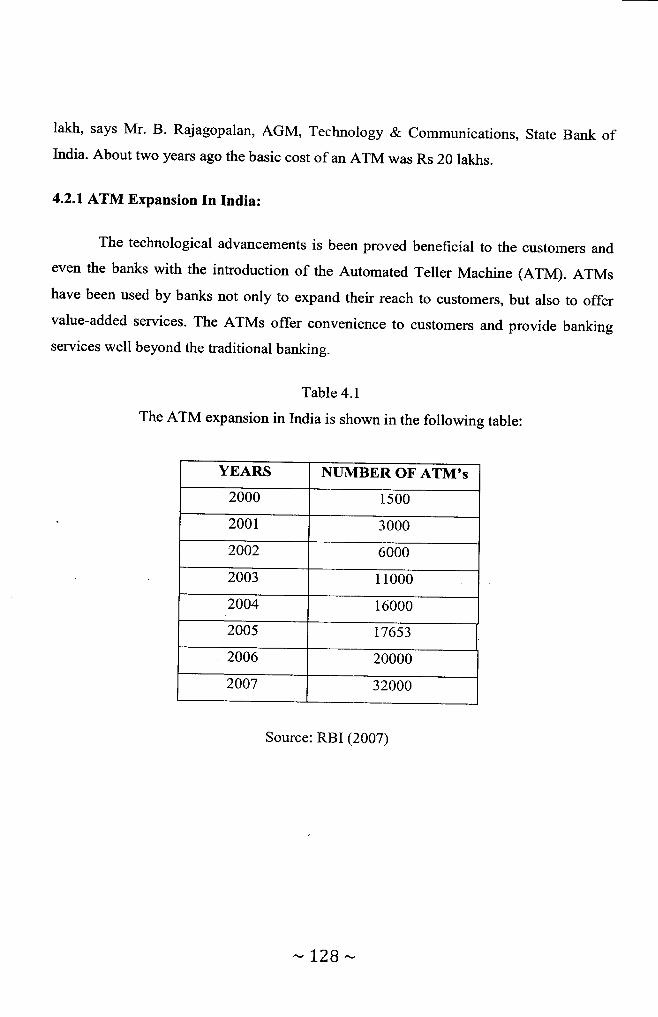

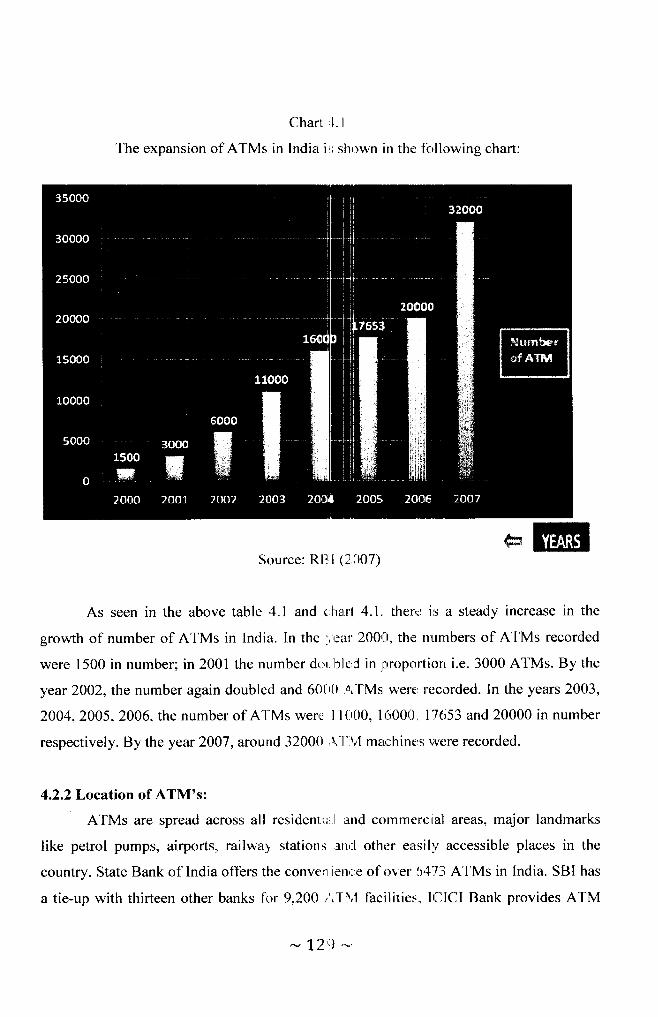

Table 4.1

The ATM expansion in India is shown in the following table:

YEARS NUMBER OF ATM's2000 1500

2001 3000

2002 6000

2003 I 1000

2004 16000

2005 17653

2006 20000

2007 32000

Source: RBI (2007)

- 1.28 -

Chart

The expansion of ATMs in India

,[. ]

is shr:wn in thrl {trlL:wing chart:

*. I?lltlSource: RII I (2007)

As seen in the above table.4.l and <:harl 4.1. therr,r ir; a steady increase in the

growth of number of ATMs in India. In the',,ear'200r"1, thr: numbers of ATMs recorded

were 1500 in number; in 2001 the nurnber dor. bleC in proportion i.e. 3000 ATMs. By the

year 2002, the number again doubled :rnd 60(t0 ^r'l'Ms were, recorded. In the years 2003,

2004,2005,2006, the number of A1-lt4s wer,e I l(t00, 11500(), 17653 and 20000 in number

respectively. By the year 2007, arouncl 320()0 ,\'l'\vl marchine's were recorded.

4.2.2 Location of ATM's:

ATMs are spread across all re'sident"u,.l and comm'ercial areas, major landmarks

like petrol pumps, airports, railwal' sitations an'J other easil;l accessible places in the

country. State Bank of tndia offers the conl'en ien,.;e of-ol er '6,I',t3 ATMs in lndia. SBI has

a tie-up with thirteen other banks fcrr 9,200 ,r,Tl,l facilitie-s" ltllCI Bank provides ATM

- I',2':.1 .-

cum debit cards to its customers that enable them to access the banking services through

a network of over 3469 ATMs. Other than this HDFC Bank, United Bank of India. Bank

of Baroda etc also provides the service of ATM cards.

The number of people using ATMs is incessantly increasing day by day. Today

the banls have reached the rural masses also. According to the 'ATM user survey 2008'

the number of ATMs installed in India grew by 28%o. Despite the regular growth, India

scores very low in ATM penetration even by Asian standards. While we have 23 ATMsper million people, China has 55 and South Korea has 1600. Industry estimates are that

for ATMs to be viable, at least 10,000 transactions a month or 300 a day should be the

target. Total cash movement through ATMs across India was around Rs. 70,000 crore.

lndia along with other BRIC countries will invest heavily in ATMs till 2011.

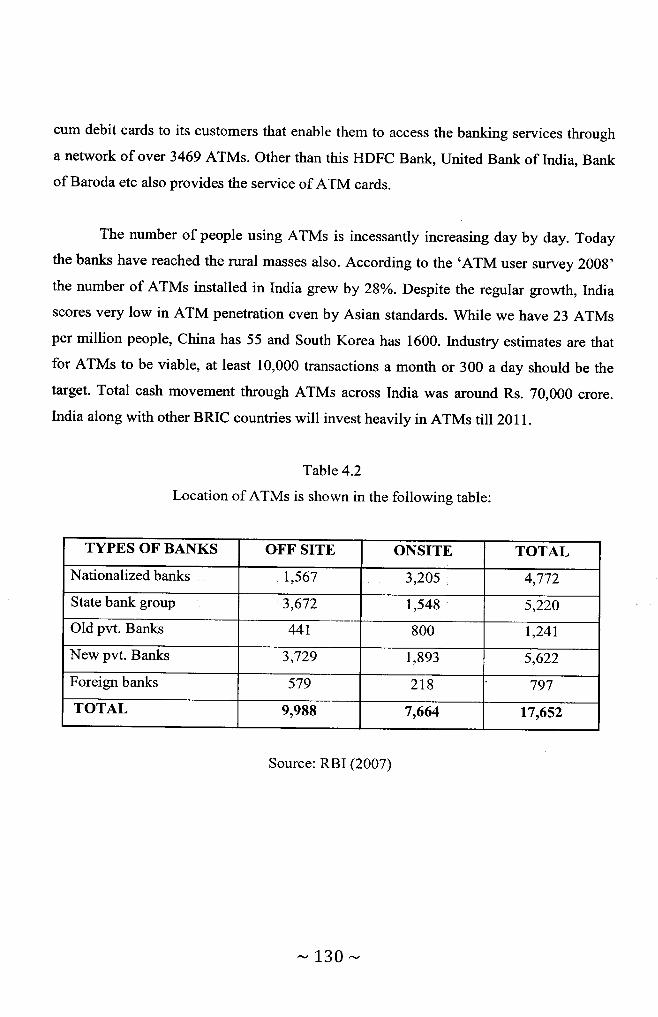

Table 4.2

Location of ATMs is shown in the following table:

Source: RBI (2007)

TYPES OF BANKS OFF SITE ONSITE TOTALNationalized banks r,567 3,205 4,772

State bank group 3,672 1,548 5,220

Old pvt. Banks 441 800 I,241

New pvt. Banks 3,729 1,893 5,622

Foreign banks 579 218 797

TOTAL 9,ggg 7,664 17,652

-130-

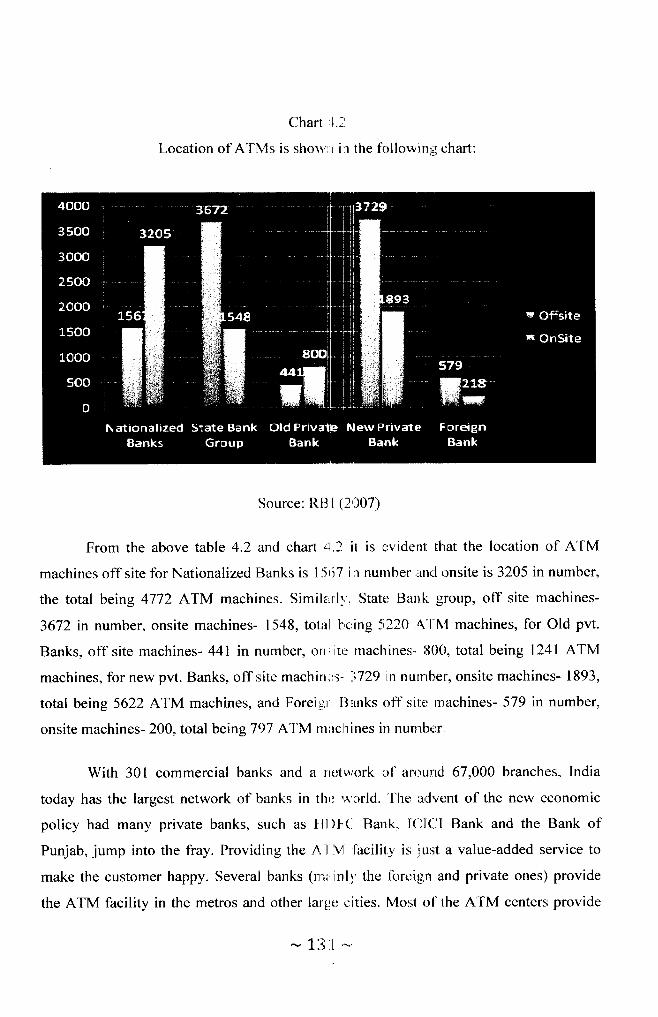

Chart ,l.l

Location of ATMs is shou,r.r ir the followinsl chart:

Source: RII I (2,007)

From the above table 4.2 andl chart rl.2 it is ::vidcnl. that the location of ATM

machines off site for Nationalized []arrl<s is I 5rj,7 i n nurnber ancl onsite is 3205 in number,

the total being 4772 ATM machines. Simile'rl1 . Statr: []a"rr[r group, off site machines-

3672 in number, onsite machines- l5zl8, tolal he:ing j;220.{l-l\'1 machines, for Old pvt.

Banks, off site machines- 441 in nunrber, on,itr: machines- 130(t, total being 1241 ATM

machines, for new pvt. Banks, off site;machin.:s- :i729 in nutnber, onsite machines- 1893,

total being 5622 ATM machines, anrdl Foreigurllanks of{'site machines- 579 in number,

onsite machines- 200, total being 797 l\TM tnttchines in nunrbe:r.

With 301 commercial banks and a nt,:tiriork of around 67,000 branches, India

today has the largest network of banl:s in thr: ',r'orld. 'Ihe a,C.rent of the new economic

policy had many private banks, s;uch as tll)F(.l llank. I(.llCI Bank and the Bank of

Punjab, jump into the fray. Providing the.A.l lV lacility is just a value-added service to

make the customer happy.Several ba;nks (mi,inl1'the foreign and private ones) provide

the ATM facility in the metros and other larlre ,;ities. Mosl ol'rhe ATM centers provide

- 1.3.[ '-'

24-hout service to their customers. More than 20 nationalized banks and a few privateones have pooled in their resources to launch a consortium of more than 500 ATMs inMumbai. Dubbed "Swadhan scheme," this means a client from any of the listed bankscan withdraw cash from any of the outlets, which could even be of any other privatebank.

4.3 ATM PENETRATION IN ASIAN COUNTRIES:

The Reserve Bank of India's (RBD plan to make ATM usage free from April2009 is well on track, if business at India's largest ATM machine manufacturer isanything to go by. A senior official of NCR Corporation says that his firm has not seen

any significant slowdown in sales compared with large banks recently. Fears ofimpending recession and resistance from some banks to co-operate with RBI,s plan hadled to market speculation that ATM penetration would hit a plateau in the comingmonths. "We have not seen any significant drop in demand from banks for ATMmachines," said NCR Corporation India MD India area Pradeep Sen on the sidelines of apress conference. "Embracing technology is perhaps the best way to acquire newcustomers for banks, especially since there is still demand for cost-efficient solutions inthe market," he added. However, he warns that if the demand drastically slips from here,

things can worsen any moment.

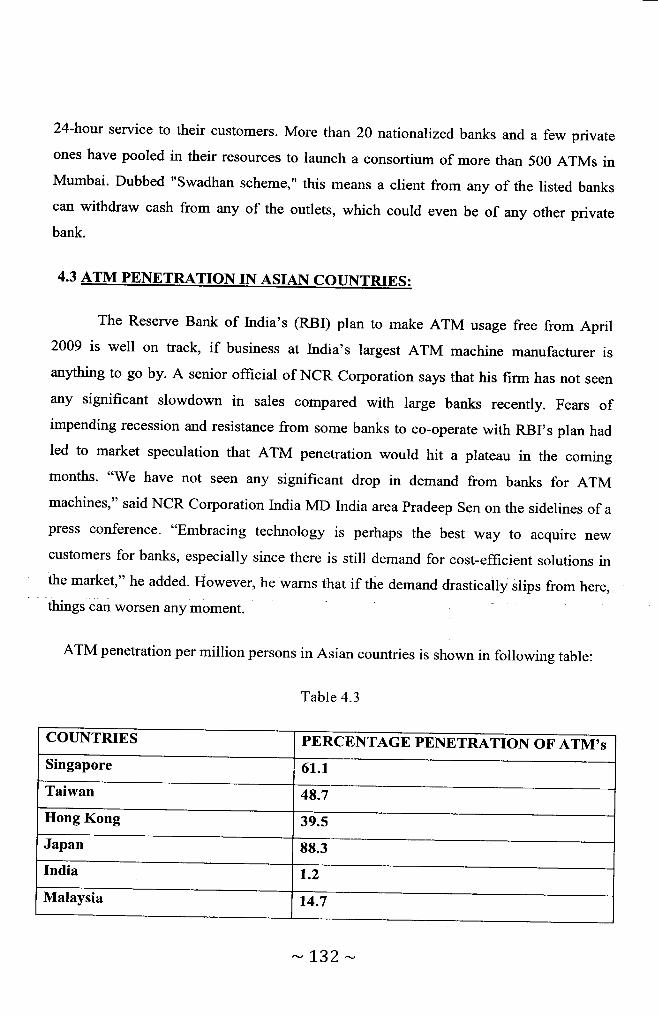

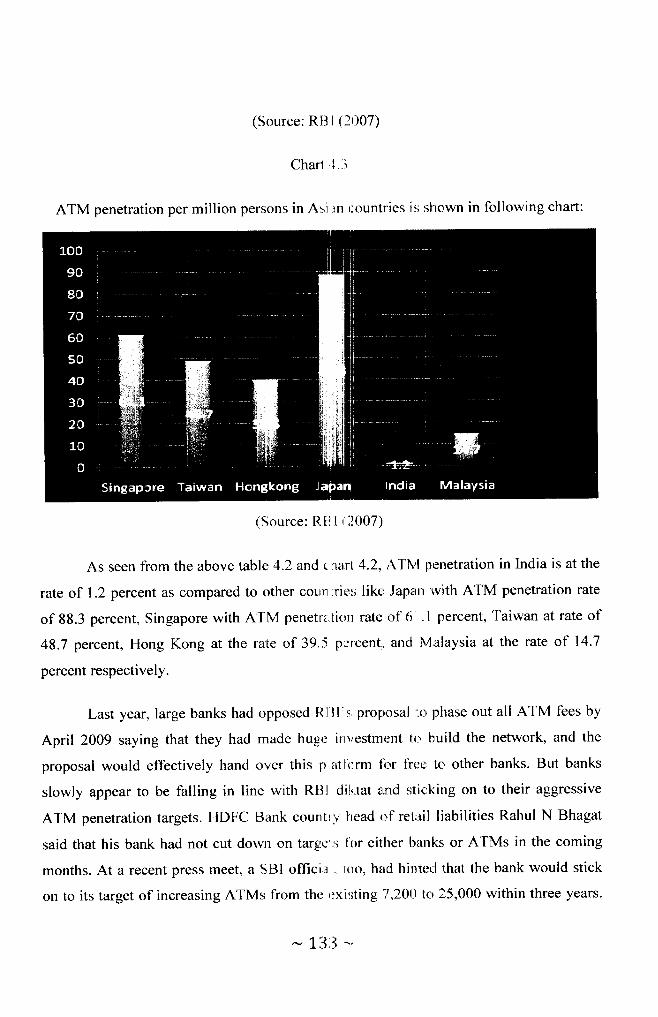

ATM penetration per million persons in Asian countries is shown in followins table:

Table 4.3

COUNTRIES PERCENTAGE PENETRATION OF ATM'sSingapore 61.1

Taiwan 48.7

Hong Kong 39.s

Japan 88.3

India 1.2

Malaysia 14.7

- 1-32 -

ATM penetration per million persons in Asirn r:;ountries is sfLown in following chart:

(Source: Rtl I (lrl07)

Charl ,1..i

(SouLrce: Rtil r.1007)

As seen from the above table 4f.2 and c harl 4.2, A-flrl penetration in India is at the

rate of 1.2 percent as aompared to other coun :rier; like, Jap;an rvith ATM penetration rate

of 88.3 percent, Singapore with A'Tlvl. penetri.ti(frr rate of'6 .l percent, Taiwan at rate of

48.7 percent, Hong Kong at the rirte of 39.5 p.'rcent. ancl lr/;alaysia at the rate of 14.7

percent respectively.

Last year, large banks had opp,osed tlltl's; proprosal 'io, phase out all ATM fees by

April 2009 saying that they had made hugre irrvestment to build the network, and the

proposal would effectively hand over this prratiirrm lirr fi'ee, to other banks. But banks

slowly appear to be falling in line vrith RIll diL:tat a.nd sticking on to their aggressive

ATM penetration targets. HDFC EfarLl< country head of retitil liabilities Rahul N Bhagat

said that his bank had not cut dorvn on tar€lelrs f'or either batrks or ATMs in the coming

months. At a recent press meet, a SBI offici,a ,, oo, htrd hi:nted that the bank would stick

on to its target of increasing ATMs from the r:xir;ting ,t,2,01J to 25,000 within three years.

- 13,1 -.

Four banks - SBI, ICICI Bank, HDFC Bank and Axis Bank make up for more than60%o

of the 35,000 ATMs in India. Mr. Sen said the ATM sharing proposal should nor srop

from banks from setting up their own ATMs. He points out that banks would have to pay

fees for using somebody else's services. Besides the all important brand visibility is at

stake when you allow a customer to visit a competitor's ATM. 'oThere's a trade offbetween the costs of setting up an ATM and these fwo factors," he said. Market experts

point out that ATM is one of the easiest ways by which banks can contribute to financial

inclusion (59% of rural India does not have financial assistance). When costs of sefting

up a branch are high and prospects of business are uncertain, banks would do best to

make use of technology like ATMs.

4.4 FACILITIES AT ATMs:

Capable of handling rough weather and sub-zero temperatures, the ATM caters to

Indian army personnel especially of the 63rd Mountain Brigade, which has itsheadquarters there and tourists.

Following facilities are provided at ATM's:

l. There are Round-the-clock Cash Withdrawals with conveniently located 24 hour

ATMs at key locations.

cash and cheque can be deposited anytime within 24 hours of the day. Just

deposit it at ATMs and it will be credited into the account on the next workins

day.

Balance enquiry & statement of account can be done at ATM's absolutely free.

ATM screen will reveal the balance in the account. A mini statement comprising

last few transactions can also be obtained from the ATM.

Drop in your request for a cheque book at the ATM and it will be delivered to

you.

2.

J.

4.

- 1,34 -

5. Fabulous and amazing discounts against your purchases at department stores,

textile shops, jewellery stores, food outlets, electronic shops, theme parks can be

availed by making payments through ATM cards.

4.5 ADVANTAGES OF ATM TO BANKS:

ATMs have eradicated the massive paper work in the banks, and have provided

convenience not only to the customers but also to the bankers.

Following are the advantages of ATM to banks:

1. Less space required

2. Capital expenditure is lower as compared to Branch

3. Bank's staff gets more time to do marketing

4. Lower transaction cost.

5. one more means for advertising Bank's products to customers.

6. Convenience of shopping-no need to carry cash

7. No need to visit branch for transaction

8. AAA Banking-Any time, Anywhere, Anyhow.

9. Fast and efficient service.

10. Good currency notes.

4.6 PRECAUTIONS TO BE TAKEN BY ATM USERS:

Although ATMs provide convenience to the customers, still there are some safety

measures that have to be taken care of.

Following are the precautions to be taken by ATM users:

1. Always keep your card in your purse/wallet where it won't get scratched.

2. Remove your card after you enter the ATM cubicle.

3. Make your PIN series of letters or numbers that you can easily remember but that

cannot be easily associated with you personally.

4. After your transaction, take your money along with receipt and card.

-135-

5. Position your hand and body in such a way that the PIN entry cannot be recorded bycamera.

6. If you find that cash received from ATM is short, complain to the security if there isone' or else phone up your branch and inform immediately so that they would lookinto your grievance.

7. If some one picks your pocket and you loose the card, inform the card issuing Bank

immediately and also file an FIR with the nearest police station.

8. Check your monthly statement to make certain all charges are your own and

immediately notify the card issuer of any error or unauthorized changes.

9. Do not write your PIN on the card or any other paper. If you still feel it necessary, do

not keep this along with the wallet in which the card is kept.

10. Avoid using birth dates, initials, house number, phone number as pIN.

11. Do not reveal your PIN to any one, including close friends.

12. Do not trough the receipt in and around ATM area. It is suggested that you destroy itby tearing into pieces since it contains your account number and card number whichmight be misused.

4.7 TYPES OF PLASTIC MONEY:

Following are the different form of plastic money:

1. ATM Card: This card is useful only to operate the ATM for withdrawal of cash and

other facilities provided at ATM centers.

2. Debit Card: This Card is useful to make payments for purchase from member

establishments who have arrangements with the card issuingbank/agency. All Card

issuers are affiliated to two major issuers - VISA and Master Card. This is a Card

similar to Credit Card.

3. Debit-cum-ATM Card: This is the most common these days. The same Debit Card

is used to draw cash from ATM and also make payments to shops for purchases. This

is Two-in-one Card.

-L36-

4. Credit Card: This Card enable the client to obtain goods or services from various

shops having arrangements with the issuing agency even when there is no balance in

his savings or current account. Normally a limit is fixed based on the net worth of the

client up to which the client can use the Card. The same card is used even to draw

cash from ATM's with in the cash limit approved to that client. Normally, at the time

of issuing the Card, the Bank intimates the client two limits (spending limits) - one

the total spending limit (based on the net worth of the client) and the other sub limit

within the total spending limit for the purpose of drawing cash, e.g. a Card has a total

spending limit of Rs.l lakh with a sub limit for cash withdrawal of Rs. 20,000. The

functions performed by Debit and Credit Cards are nearly the same. The only

difference is that in case of Debit Cards the transactions can be put through if and

only if balance is available in customers account but in Credit Cards even without

balance in the account the client can operate-subject of course to the maximum limit

fixed. Credit Cards are normally valid in the country of issue. For example, the Credit

Card issued by Banks in India, is valid through out India. If the Bank has arrangement

with agencies in foreign countries, it may issue a Credit Card to selected clients,

which is valid abroad as well. Such Cards are termed as International Credit Card.

Charge Card: A Charge Card is similar to a Credit Card with one major difference,

with a Charge Card you have to pay the entire dues within the credit period and

cannot carry over any balance like Credit Card.

Co-Branded Cards: Some times Banks that issues Cards enter into agreement with

other entities (air lines, hotels) etc. So that both are in win-win situation i.e. the no:

of Cards of the issuing Bank increase by which their fee based income goes up and

the sales of the Co-branded Company's product also increases. Co-Branded Cards,

which are affiliated with merchants such as airlines and retailers. use rewards

programmes and special offers including rebates, discounts and gifts certificates to

attract new customers, generate loyalty among existing customers and ultimately

f,.

6.

-L37 -

increase Card usages. The future of Co-Branded Cards across all industries seems

brieht.

4.8 FUTURE OF ATM:

Although ATM machines were originally developed as cash dispensers, they have

evolved to include many other Bank related functions. In future, ATM may perform

functions that are not directly related to management of one's own Bank account such as

paylng routine bills, fees and taxes.

ATM's have a great role to play in .lndia. All Banks have come together through

an arrangement by which each Bank's customer can access the ATM of other member

Banks without any extra cost. This would ensure lower cost to the Bank and higher and

efficient utilization of already installed ATM's. The National Financial Switch CNFS)

network, which is aimed and maintained by the Institute for Development and Research

in Banking Technology is the technical aim of the RBI and aims at linking all ATM's inthe country for providing efficient and cheaper ATM operations. Many public and

private sector Bank's are becoming members of NFS to get the benefit of over 9000

ATM's. Efforts are on to manufacture ATM's that would be supplied at around Rs. 2

lakh. This would help in taking the ATM to the rural areas of the country to suit the rural

people and also as an additional security device innovations are being made in the form

of using camera inside the ATM, which would picture the client and compare with the

records or use thumb impressions of the client for identification etc.

Thus the ATM's would be the 'Banking of the future' and the brick and mortar

branches would slowly disappear. Both Bankers and the clients. due to the various

benefits have adapted themselves to the ATM culture.

-138-

4.9 PROBLEMS WITH ATM USAGE IN INDIA:

There are several problems with ATM usage in India. The issues include the

instructions displayed during a transaction, physical security at ATMs and ATM-sharing.

ATMs were treated to be a boon for the general public when came in existence. There

was no need to stand in queues in banks to withdraw money, no need to go the branch foryears even to get a cheque deposited, cash deposited or for getting the cheque book

issued. ATMs offer almost every service for which a customer goes to the bank. But as

for all services in India, basic habit of not keeping up with advances has shown its effect

in this matter also.

Some ATMs display the message "Your request cannot be processed now", the

meaning of which has to be interpreted by the customer only. It can mean that the ATMdoes not have suflicient funds, or that your account has some problem or it may also

mean that the server of the bank is not working. When an attendant of an ATM of a

private bank was asked about it, he said that as soon as any problem is found in the ATMmachine, a cornplaint is lodged immediately but the same is attended to in as long as 15

days in some cases. The seryers of the banks working so slo-wly that it is difficult to

understand if the problem is with the machine or the bank?s seryer.

It has become a practice in many ATMs to not keep deposit slips and envelops whichare necessary for depositing cheques and cash. Any person seeking to deposit the cheque

has to write his account details at the back of the cheque and drop the same in the cheque

box without being provided any proof for having dropped the cheque. The person should

get the details of the cheque deposited b1' him because, in case of non-credit of the

cheque, he cannot enquire the bank about it if he has no receipt with him. The ATM of aprivate bank has a layout which does not allow sufficient room for a person to drop a

cheque in the drop box without obstructing a person making a cash transaction. Withrespect to the transparency of the glass at the ATM gate, anyone can get a full view of the

cash transaction and even the counting of the notes at the ATM. As per the provisions at

-L39-

the ATM, only one person should be there at a time to operate the ATM machine. Butthis rule is a most violated one.

Security guards at ATMs are not up to the standards of a guard but that of a peon.

They are neither good for the bank nor for the public. Housekeeping standards, themaintenance of the ATM machines are also not of good standard. It seems that the banksare not able to maintain the standards expected from them. An overall overview of thesituation is highly required. On one hand, there is talk of matching the world standardbut, on the other hand, the basic infrastructure at ATMs is becoming difficult to bemaintained. The govetnment has also not linalized the rules for the sharing of ATMs,something that will help people to use any ATM without any charge, irrespective of thebank in which he has an account. This will at least enable people to get their jobcompleted without being intemrpted by the non-working of the ATM machine.

- 1,40 -