Embed Size (px)

Citation preview

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 1/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 1

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

Topic 5: WelfareTopic 5: Welfare

Economics 1, Fall 2002Andreas Bentz

Based Primarily on Frank Chapters 16 - 18

2

Review: EquilibriumReview: EquilibriumTopic 3, Consumer Theory :

foundations of Classical Demand Theoryutility maximisation

» gives us individual demand

Topic 4, Firms :profit maximisation (gives us factor demands)cost minimisation (gives us cost curves)

» recall: a firm’s supply curve is its marginal cost curve

The Equilibrium Principle :In a competitive market, price adjusts to equilibrate demandand supply: D(p*) = S(p*), p* is the equilibrium price.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 2/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 2

3

Partial and General EquilibriumPartial and General EquilibriumSo far, this study has been partial equilibriumanalysis :

this ignores the fact that changes in the price of onegood generally change the demand for other goods,and it ignores the fact that changes in the prices of goods that people sell change a person’s incomeand therefore their demand for other goods.

General equilibrium analysis studies theinteraction between supply and demand inseveral markets.

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

General EquilibriumGeneral Equilibrium

When everything’s fine:the Two Fundamental Theorems and

other Nice Results.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 3/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 3

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

ExchangeExchange

Wanna trade?

6

General Equilibrium: ExchangeGeneral Equilibrium: ExchangeSimplest setting:

two consumers: person A, person Btwo goods: x 1, x2

pure exchange (no production)

In a pure exchange economy, a fixed amount of goodsis exchanged.

Initially, every consumer is endowed with some of each good;then they may engage in trade.

This allows us to study how prices change in response torelative scarcity.

How do we represent the possible allocations of thetwo goods between the two consumers?

We can represent this in an Edgeworth box.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 4/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 4

7

Exchange, cont’dExchange, cont’dSome definitions:

an allocation X of goods:» bundle (x 1

A, x2A) (person A); bundle (x 1

B, x2B) (person B)

» This is any distribution of the two goods between the twoconsumers.

» Any allocation is feasible if the amount of good 1 thatperson A holds and the amount of good 1 that person Bholds add up to the total amount of good 1 in theeconomy, and similarly for good 2.

an endowment W (or, initial allocation) of goods:» bundle ( ω 1

A, ω 2A) (person A); bundle ( ω 1

B, ω 2B) (person B)

8

Feasible AllocationsFeasible AllocationsAll allocations in the Edgeworth box are feasible:

W

X

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 5/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 5

9

Edgeworth BoxEdgeworth BoxDefinition: An allocation X is feasible if the totalamount of each good consumed is equal tothe total amount available:

x1A + x1

B = ω 1A + ω 1

B

x2A + x2

B = ω 2A + ω 2

B

Any allocation in the Edgeworth box isfeasible.The initial endowment allocation ( ω 1

A, ω 2A)

(person A) and ( ω 1B, ω 2B) (person B)determines the size of the Edgeworth box.

10

Edgeworth Box, cont’dEdgeworth Box, cont’dNow we know how to illustrate all feasibleallocations in our two-consumer economy.How do we represent preferences?

Each consumer has preferences over the twogoods.Preferences are represented by indifferencecurves, in the way in which we have introducedthem in topic 3.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 6/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 6

11

Building an Edgeworth BoxBuilding an Edgeworth Box

A’s quantity of good 1

A’ s

q u an

t i t y of

g o o d 2

B’s quantity of good 1

B’ s

q u an

t i t y of

g o o d 2

12

At allocation W (endowment), welfare gains for bothconsumers are possible:

Gains from ExchangeGains from Exchange

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 7/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 7

13

Pareto EfficiencyPareto EfficiencyAt X, there are no further gains from trade:

X is Pareto efficient.

14

Pareto Efficiency, cont’dPareto Efficiency, cont’dDefinition: Allocation X is a Paretoimprovement over allocation Y if:

every agent prefers (or is indifferent between) her consumption bundle under X to her bundle under Y;that is: if for every agent allocation X is on a higher (or at least the same) indifference curve.

Definition: Allocation X is Pareto efficient if there is no other allocation that is a Paretoimprovement over X.

The locus of all Pareto efficient allocations is thecontract curve .

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 8/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 8

15

Contract CurveContract CurveThe locus of all Pareto efficient allocations is thecontract curve .

The contract curve joins all the tangencies between A’s andB’s indifference curves.

A’s quantity of good 1

A’ s

q u an

t i t y of

g o

o d 2

B ’ s q u a n t i t y o f g o o d 1

B’squantityof good 2

16

Pareto Efficiency, cont’dPareto Efficiency, cont’dThe definitions are in terms of preferences .

We want a criterion that tells us whether anallocation is “good” in some sense.

Definition: According to the Pareto welfarecriterion , an allocation X is (socially) better than Y if X is a Pareto improvement over Y.

What is attractive about this definition:» requires only a weak value judgement, and is powerful

and uncontentious;» most other welfare criteria are contentious.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 9/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 9

17

Pareto Efficiency, cont’dPareto Efficiency, cont’dBut: The Pareto criterion ranks allocations onlyincompletely.

Example 1: If some agents “prefer allocation X to Y”, andsome agents “prefer Y to X”, the Pareto criterion cannot tell uswhich is better.Example 2: Two Pareto efficient allocations cannot becompared by the Pareto criterion.

And: A Pareto efficient allocation may not have anyother nice properties.

Example: Distribution: typically, an allocation where one

individual has everything and everyone else has nothing isPareto efficient.

18

Market TradeMarket Trade

Given endowment W, what is the outcome of trade ina competitive market?

Can prices p 1, p2 be equilibrium prices?At prices p 1, p2, there is excess supply of good 1 and excessdemand for good 2 (p 1 is “too high” and p 2 is “too low”).Lower p 1 and raise p 2 (recall slope of the budget line is -p 1/p2).

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 10/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 10

19

Market Trade, cont’dMarket Trade, cont’dAt the competitive market equilibrium (or,Walrasian equilibrium), there is no excessdemand or excess supply. Prices equilibratesupply and demand.And this equilibrium has nice properties: it isPareto efficient.This is a general property of competitivemarket (Walrasian) equilibria. We thus havethe following:

20

The First TheoremThe First TheoremTheorem: All competitive market equilibria (or,Walrasian equilibria) are Pareto efficient.

The First Fundamental Theorem of WelfareEconomics (Adam Smith’s “invisible hand”):“[Every individual] generally, indeed, neither intendsto promote the public interest, nor knows how muchhe is promoting it. … he intends only his own gain,

and he is in this, as in many other cases, led by aninvisible hand to promote an end which was no partof his intention.”

» [Smith A (1776) An Inquiry into the Nature and Causes of the Wealth of Nations Book IV]

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 11/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 11

21

Alexander Pope, Essay on ManAlexander Pope, Essay on ManOn their own axis as the planets run,Yet make at once their circle round the sun;So two consistent motions act the soul;And one regards itself and one the whole.Thus God and Nature link’d the gen’ral frame,And bade self-love and social be the same.

Epistle III, An Essay on Man (1733)

22

First Theorem: DiscussionFirst Theorem: DiscussionInformational economy: agents only need toknow the prices they face. Then, the outcomeof market trade will be efficient.In a two-agent world, this is not an excitingresult. But it holds for large numbers of agents:

a strong case for the market as an allocationmechanism.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 12/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 12

23

The Second TheoremThe Second TheoremTheorem: If preferences are convex, everyPareto efficient allocation can be achieved asthe equilibrium outcome of competitive markettrade.

“The Second Fundamental Theorem of WelfareEconomics”Or: Given convexity of preferences, we can alwaysfind a set of prices that supports any Paretoefficient allocation as a market equilibrium for anappropriately chosen endowment allocation.

24

Second Theorem: IllustrationSecond Theorem: Illustration

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 13/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 13

25

Second Theorem: DiscussionSecond Theorem: DiscussionThe second theorem is a theorem about theseparation of efficiency (a property of theallocation), and distribution.Redistribution need not be concerned withefficiency:

We can pick any (Pareto efficient) allocation, andredistribute to an appropriate (not necessarilyPareto efficient) allocation. The market will then

achieve efficiency autonomously.

26

SecondSecond Th’mTh’m: Discussion, cont’d: Discussion, cont’d

Redistribution: all we need to do is:choose the allocation X we like (by some welfare criterion),calculate the corresponding equilibrium prices,redistribute endowments to anywhere along the (constructed) budgetline,then, market trade will automatically achieve efficiency (by the firsttheorem ).

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 14/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 14

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

ProductionProduction

… more opportunities …

28

General Equilibrium: ProductionGeneral Equilibrium: ProductionIn the pure exchange model, the amounts of good 1 and good 2 in the economy weregiven.We now study general equilibrium inproduction: how do producers decide howmuch (and using which input mix) to produce?

The quantities of the inputs capital (k) and labor (l)are given: how do firms produce output?

The Edgeworth (production) box contains allfeasible input combinations.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 15/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 15

29

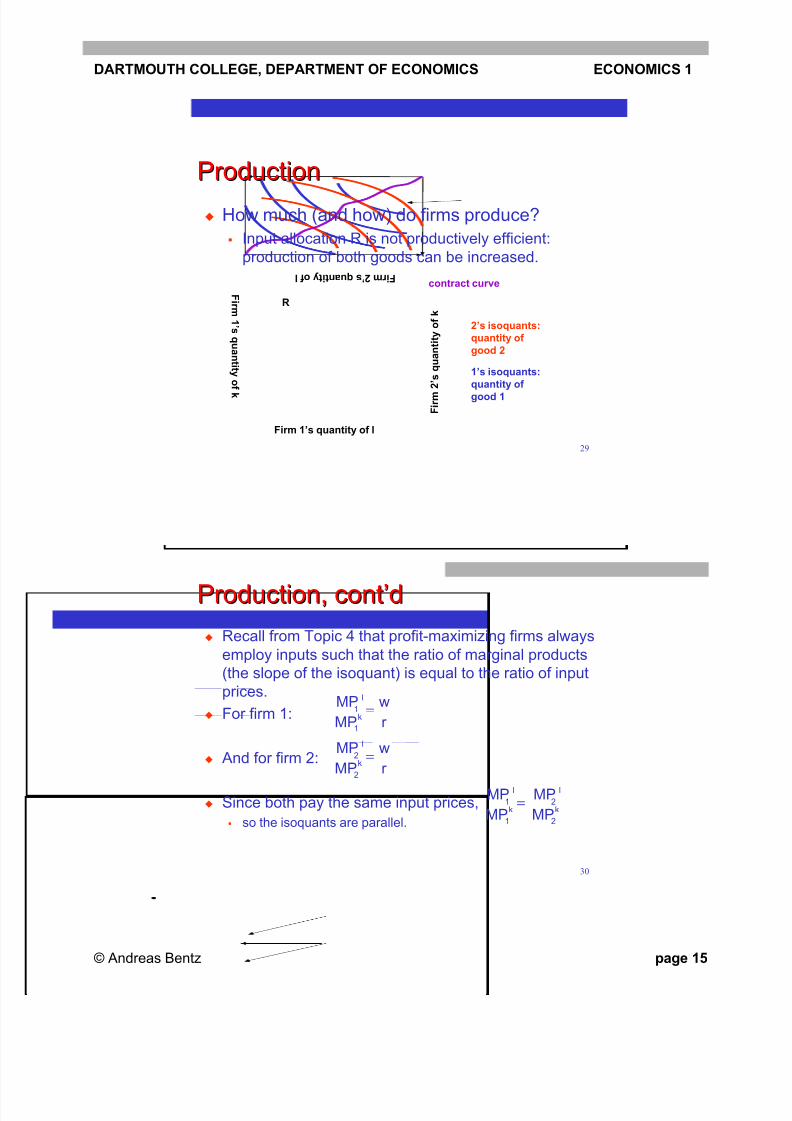

ProductionProductionHow much (and how) do firms produce?

Input allocation R is not productively efficient:production of both goods can be increased.

Firm 1’s quantity of l

F i r m 1 ’ s

q u an

t i t y of k

F i r m 2 ’ s q u a n t i t y o f l

Firm 2’squantityofk

contract curve

2’s isoquants:quantity of good 2

1’s isoquants:quantity of good 1

R

30

Production, cont’dProduction, cont’dRecall from Topic 4 that profit-maximizing firms alwaysemploy inputs such that the ratio of marginal products(the slope of the isoquant) is equal to the ratio of inputprices.For firm 1:

And for firm 2:

Since both pay the same input prices,so the isoquants are parallel.

r w

MPMP

k

l=

1

1

r w

MPMP

k

l=

2

2

MPMP

k

l=

1

1

MPMP

k

l

2

2

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 16/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 16

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

Product MixProduct Mix

Are you being served?

32

Production Possibilities Frontier Production Possibilities Frontier What are the combinations of outputs thiseconomy could (at best) produce (with givenamounts of inputs)?

For every quantity of good 2, what is the largestquantity of good 1 that can be produced (whenfactors are employed optimally)?

This gives us a schedule of an economy’sproduction possibilities: the different outputcombinations the economy can maximallyproduce.

This is the Production Possibilities Frontier (PPF ).

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 17/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 17

33

PPF, cont’dPPF, cont’dThe contract curve in theEdgeworth (production)box tells us where it isnot possible to increaseproduction of one goodwithout reducingproduction of the other.It has all the informationwe need for the PPF:

Given any quantity of good 2, what is themaximum that can beproduced of good 1?

Firm 1’s quantity of l

F i r m 1 ’ s

q u an

t i t y of k

F i r m 2 ’ s q u a n t i t y o f l

Firm 2’squantityof k

1

2

PPF

34

PPF, cont’dPPF, cont’dAs we move down the PPF, we gain more of good 1,but have to give up some of good 2.

The absolute value of this ratio (the slope of the PPF) is themarginal rate of transformation (MRT ).

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 18/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 18

35

PPF, cont’dPPF, cont’dWhat is MRT?

As we gain one more unit of good 1, we need resources (kand l) costing MC 1.How much of good 2 do we need to give up to “free up”enough to buy inputs worth MC 1 (to produce this one unit of good 1)?

» If we produce one unit of good 2 less, we free up MC 2.» If we produce 1 / MC 2 units of good 2 less, we free up $1.» If we produce MC 1 / MC2 units of good 2 less, we free up

MC1.

So MRT = MC 1 / MC2. In a competitive market, this is equal top1 / p2.

36

PPF and ExchangePPF and ExchangeThe economy is productively efficient (it produces on ,not inside the PPF):

which point on the PPF is chosen (the product mix)determines the size of the Edgeworth (exchange) box.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 19/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 19

37

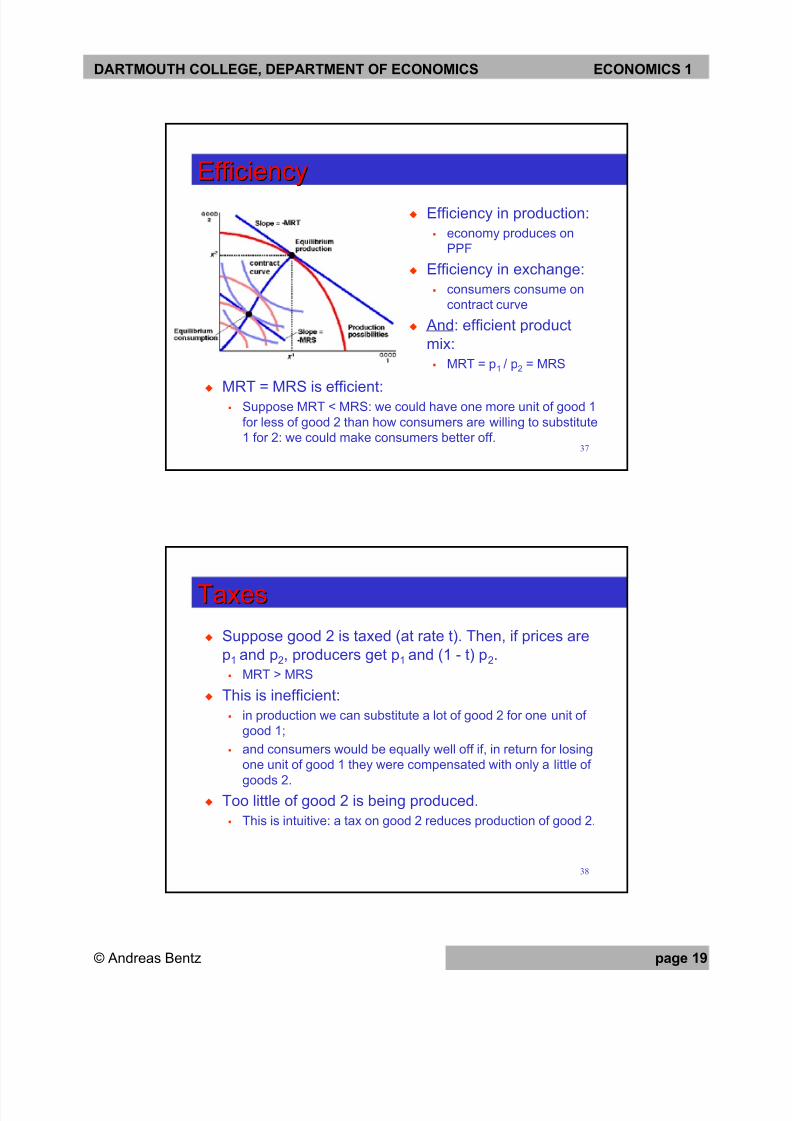

EfficiencyEfficiency

MRT = MRS is efficient:Suppose MRT < MRS: we could have one more unit of good 1for less of good 2 than how consumers are willing to substitute1 for 2: we could make consumers better off.

Efficiency in production:economy produces onPPF

Efficiency in exchange:consumers consume oncontract curve

And: efficient productmix:

MRT = p 1 / p2 = MRS

38

TaxesTaxesSuppose good 2 is taxed (at rate t). Then, if prices arep1 and p 2, producers get p 1 and (1 - t) p 2.

MRT > MRS

This is inefficient:in production we can substitute a lot of good 2 for one unit of good 1;and consumers would be equally well off if, in return for losingone unit of good 1 they were compensated with only a little of

goods 2.Too little of good 2 is being produced.

This is intuitive: a tax on good 2 reduces production of good 2.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 20/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 20

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

ExternalitiesExternalities

When things can go wrong.

40

Externalities: ProductionExternalities: ProductionDefinition: When an agent’s productionpossibilities depend on another agent’sconsumption or production decisions, we havea production externality .

Example: The noise coming into my office fromTabard puts me off work. (Negative externality)Example: Professor Scott talking to me makes me

more productive. (Positive externality)

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 21/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 21

41

Externalities: ConsumptionExternalities: ConsumptionDefinition: When an agent has preferencesover another agent’s consumption or production decisions, we say that there is aconsumption externality .

Example: I dislike your consumption of cigarettes inmy office. (Negative externality)Example: I enjoy teaching an interested class thatasks lots of questions. (Positive externality)

42

Externalities, cont’dExternalities, cont’dIn each case, there is a cost (for negativeexternalities) or a benefit (for positiveexternalities) imposed on someone other thanthe decision-maker.

Since the decision-maker does not bear this cost(benefit) herself, she does not take it into account inher decision.

There will be “too much” of a negativeexternality and “too little” of a positiveexternality (relative to what is socially optimal).

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 22/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 22

43

Example: NoiseExample: NoiseSocial and private costdiverge: the externalityimposes an externalcost on “society” (agentsother than the decision-maker)Decision rule:

marginal cost = marginalbenefit.

Implication: privately andsocially optimalquantities differ.

decibels

cost / benefit

private=socialbenefit

socialcost

privatecost

soc.opti. priv.opti.

44

What’s the Problem?What’s the Problem?What goes wrong in the presence of externalities is that external costs and benefitsare not taken into account by the decision-maker:

She does not face the full price (opportunity cost) of her actions:

» I would be willing to bribe you not to play loud music; or: I

would be willing to put up with your music if you paid me.There is no market in which the externality istraded (and which would result in a price).Externalities are an example of market failure .

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 23/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 23

45

What’s the Problem, cont’dWhat’s the Problem, cont’dIf all parties affected by an external cost or anexternal benefit could negotiate with thedecision-maker at no transaction cost , thesocially optimal solution could be obtained.

Costless negotiation would institute a price.If negotiation is not costless, the transaction costfrom negotiation may outweigh the benefit to thoseaffected by the externality. (No negotiation will takeplace.)

46

Example: SmokeExample: SmokeSetup:

For person A, smoke is agood, for person B, a bad;both have equal amountsof money.

If there is a market for smoke, everything’sfine …

the equilibrium depends on

who has the property rightto clean air

If there is no market for smoke, things gowrong …

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 24/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 24

47

CoaseCoase ’s’s TheoremTheoremIn 1960, Ronald Coase argued precisely whatwe have just seen:

If negotiation is costless, the (socially) optimalallocation can be attained without action by thestate.

How likely is negotiation to be costless?The more people are affected by the externality, thehigher the transaction cost.

» Example: polluted air

What if negotiation is too costly?

48

Is there a Case for Intervention?Is there a Case for Intervention?The first section of Topic 5 (… wheneverything’s fine) is about why competitivemarkets do the best job at efficiency if they are

perfectly competitive .For externalities, there exists no market (themarket fails).

Only when markets fail do economists see acase for state intervention.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 25/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 25

49

What can the State Do?What can the State Do?Institute an artificial price for the externality:

introduce a (“Pigouvian”) tax.

decibels

cost / benefit

private=social

benefit

socialcost

privatecost

soc.opti.

priv.opti.

Example: Noise.Tax emission of each decibel so thatthe private costrises sufficiently sothat it is equal to thesocial cost.

But how dogovernments knowwhat the right tax is?

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

Public Goods and GovernmentPublic Goods and Government

“Why national defense is run by thegovernment” and other stories.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 26/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 26

51

Public GoodsPublic GoodsPublic goods are goods that have twocharacteristics:

non-diminishability : if I consume some of the goodthere isn’t any less of it there for younon-excludability : it is impossible or prohibitivelyexpensive to exclude anyone from consuming thegood

Examples:

public parksstreet lightingnational defense

52

What’s the Problem?What’s the Problem?What can go wrong with public goods is this:

Once a public good is provided, everyone (by non-excludability) can consume it.So I would rather have you provide the public good(and you pay for it), than to provide it myself.

This is a “ free rider problem :” I want to free-ride on your effort.

There is no reason to believe that profit-maximizersprovide (the efficient level of) public goods.

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 27/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 27

53

What’s the Problem, cont’dWhat’s the Problem, cont’dAgain, there is market failure :

If there were a price for the public good (whichusers pay and which the provider can collect), therewould be an incentive to provide the public good if benefit > cost.

Since, by definition (non-excludability), there isno price that can be collected, the market fails.

There is a case for state intervention.

54

Willingness to PayWillingness to PayThe marginal-willingness-to-pay curvefor a public good tellsyou how much you value(would just be preparedto pay for) eachadditional unit of thegood. (cf. Topic 3)

(This is just an inversedemand curve.)

p

q

marginal-willingness-to-pay

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 28/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 28

55

Willingness to Pay, cont’dWillingness to Pay, cont’dTo derive an inverse demand curve for the public good,or aggregate (marginal-) willingness-to-pay curve , weadd the individual marginal-willingness-to-pay curvesvertically. Why?

A fixed amount of thepublic good will beprovided. Suppose thisamount is q*. How badlydo people want q*? At themargin, person A wouldbe willing to pay p

A*, and

person B, p B*. Together,they are willing to pay(value at) p A* + pB*.

p

q

person A

person B

aggregatewillingness-to-pay curve

q*

p A*

p B*

p A*+pB*

56

Optimal ProvisionOptimal ProvisionHow much of the publicgood should be providedoptimally?

The quantity at whichaggregate marginal-willingness-to-pay =marginal cost of provision.Why? Suppose MC >AMWTP. Then the lastunit of the public goodcosts more to producethan it is valued bysociety, so there shouldbe less of it. (etc.)

p

q

person A

person B

aggregatewillingness-to-pay curve

q*

p A*

pB

*

p A*+pB*

MC

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 29/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 29

57

Public Provision of Public GoodsPublic Provision of Public Goods

If a person’s total WTP

is less than the taximposed on her, she willvote against provision.

Taxation:Suppose governmentscan only impose “lump-sum” taxes .The total cost of providingthe public good is thearea under MC (up to q*).Each person’s valuationof (or, total willingness topay for) a level of publicgood provision of q* is thearea under her marginalwillingness to pay curve.

p

q

person A

person B

aggregatewillingness-to-pay curve

q*

p A*

p B*

p A*+pB*

MC

58

Public Provision, cont’dPublic Provision, cont’dHow should we tax (in order to finance publicgoods)?

A tax on prices is inefficient:» expenditure tax (VAT)» income tax (changes the price of leisure)

We should tax in a lump-sum way:» but if everyone pays the same, we may get the inefficiency

on the previous slide;» and: it may seem inequitable.» We should impose a lump-sum tax on each person’s

endowment (what they have) … largely, everyone’scapacity to earn income (not actual income earned).

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 30/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 30

59

Public Provision, cont’dPublic Provision, cont’dBut how do we tax earning potential?

If we ask people (and they know they will be taxedon their reply), they will understate their earningpotential.This is an asymmetric information problem :individuals have more information about their potential than the state.The theory of optimal taxation is about constructinga tax schedule that elicits the “right” labor/leisurechoice from people, while imposing the “right” tax.

60

Private Provision of Public GoodsPrivate Provision of Public GoodsPrivate provision of public goods:

donations» social reward/stigma» large private benefit may be sufficient for provision

sale of by-products» Example: TV: access to audience (advertising). But: distortion to

programming?exclusion of non-payers

» Example: pay-TV: paying for programming improvesprogramming. But: people with low (but positive) WTP areexcluded (although MC of provision for them is zero)

private contracts» Example: maintenance fee in condos

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 31/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 31

Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02Dartmouth College, Department of Economics: Economics 1, Fall ‘02

Public ChoicePublic Choice

The Economics of Politics.

62

Social ChoicesSocial ChoicesIf social choices (about public good provision) have tobe made, how do we decide?

Individual agents’ preferences are fundamental.

How do we aggregate individual preferences into“social preferences”?

Dictatorship: only one person’s preferences count.Utilitarianism: maximize the sum of everyone’s utility (“thebalance of pleasure over pain”) (Bentham, Mill)

“Maximin:” maximize the utility of the least well-off person insociety (Rawls)Democracy: majority voting

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 32/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 32

63

Voting and theVoting and the CondorcetCondorcet ParadoxParadoxOne possible way of aggregating individualpreferences into “social preferences” is voting : Rank: Person A Person B Person C

1 X Y Z2 Y Z X3 Z X Y

But: Social preferences from majority votingare intransitive : X f Y, Y f Z, Z f X

The outcome of voting depends on the order inwhich votes are taken.

64

The Median Voter TheoremThe Median Voter TheoremExample: Voting over taxes (i.e. the level of public good provision)

Individual’s tastes are distributed along a line: somepeople prefer low taxes (and low levels of publicgoods), others prefer high taxes (and high levels of public goods).

lo hi

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 33/35

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 34/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

© Andreas Bentz page 34

67

Costs and BenefitsCosts and BenefitsSo far we have answered the question: Whoprefers what?We have not addressed the question: Whoprefers what by how much ?

Measure: total willingness to pay (consumer surplus).Obviously this is important: if the people who prefer high taxation (and high public good provision)

prefer this by a lot; and those preferring lowtaxation, prefer this by only a little, you should thinkthat the outcome “should” be influenced by this.

68

Costs and Benefits, cont’dCosts and Benefits, cont’dWhat we would like to do is weigh up the costs(loss of consumer surplus from having the hightaxation option rather than the low taxationoption) to some people against the benefits toothers.If we have econometric estimates of consumer surplus (willingness to pay), we can pursuecost-benefit analysis.

Back to the question: What do we want to (socially)maximize? Overall happiness (utilitarianism)?

8/4/2019 Economics 1 Bentz Fall 2002 Topic 5

http://slidepdf.com/reader/full/economics-1-bentz-fall-2002-topic-5 35/35

DARTMOUTH COLLEGE, DEPARTMENT OF ECONOMICS ECONOMICS 1

69

Positive and Normative EconomicsPositive and Normative EconomicsWe have now started to delve deep intonormative questions: how should society beorganized?Economics itself cannot answer thesequestions …… but it can help us understand what theeconomic consequences are of adopting anyone way of organizing social decision-making:it can answer positive questions .

70

Sadly ...Sadly ...

The End.

![Annie Unsworth - Economics Notes Topic 3.Docx[1]](https://img.pdfslide.us/doc/110x75/577d255b1a28ab4e1e9e9a17/annie-unsworth-economics-notes-topic-3docx1.jpg)

![Annie Unsworth - Economics Topic 1.Docx[1]](https://img.pdfslide.us/doc/110x75/577d254d1a28ab4e1e9e7ad5/annie-unsworth-economics-topic-1docx1.jpg)