Embed Size (px)

Citation preview

Economic Theory for Environmentalists

John Gowdy and Sabine O’Hara

Review by Gary Lynne

Acknowledgments

• Commenting on students from other disciplines first exposed to NREE: “…sheer amazement at the worldview of mainline economists planted the seed for the project” (p. xiii)

• Help dialogue with and among the many committed individuals in environmental organizations, community groups, government agencies

Quote from Joan Robinson:

• “The purpose of studying economics is not to acquire a set of ready made answers to economic questions, but to learn how to avoid being deceived by economists” (p. xv)

1. Introduction

• Most serious problem civilization faces: Conflict between economic activity and biological world

• Focus here on neoclassical economics:– Shows why market and biology are often in

conflict– Dominates environmental policy debate:

Need to understand this framework in order to engage this dialogue

1…

• Centuries of history drawing heavily on Adam Smith, Ricardo, Malthus (mid-1700s to early 1800s)

• Dubbed “neoclassical” by Veblen in the late 1800s, early 1900s

• G&O also claim it can be traced to the marginalist revolution in 1870s

• Economists of that late 19th century era, e.g. Marshall, started the process of thinking about small changes, using the calculus

• Keynesian ideas brought into the model from the 1930s through the 1950s, 1960s

1…

• By the 1960s, Samuelson (who contributed heavily to the mathematization of economics) claimed that only those on extreme left or extreme right were not NC

• Had become the “Queen of the Social Sciences” due to its internal precision, use of formal mathematics: Still is, to a degree

• Began to breakdown in the 1970s during the energy crisis; in 1980s due to slow economic growth

Markets and Models: The Circular Flow…

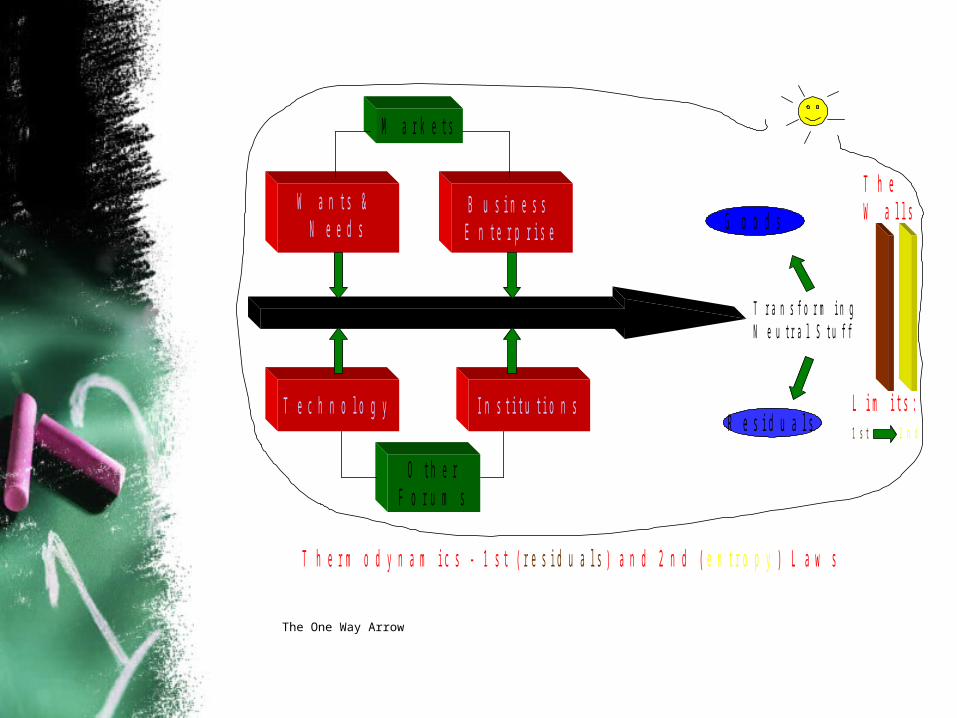

• G&O highlight the standard flow diagram… material and goods in one direction, money in the other, with the flow presumed ongoing as though disconnected from the natural system

• Markets coordinate this flow; markets referred to as “mechanisms”

• “Factors” or “Inputs” go into production• Outputs or Products emerge, to be

consumed as Goods

In GNP terms…

• Base inputs such as land, water, fuel, raw materials (e.g. iron ore, bauxite, phosphorus, sand) go to produce intermediate products, e.g. windshields in cars; corn to produce corn syrup, corn flakes and ethanol as a component of motor fuel

• In most general terms, there is land, labor and capital (human-made)

• Rents, wages, interest and profit are earned• Income is used by consumers to purchase the

final goods• Value is added at each step• Sum the base value plus added value at each

stage in production to final consumption to obtain the GNP

Economic Efficiency and Pareto Optimality

• Concept of efficiency is central• Consumers buy much like in an English auction• Producers sell, also, much like in an English

auction• Both guided by Adam Smith’s “invisible hand”

presumed achieved by each individual maximizing their own self-interest

• Fairness of the outcomes not considered; justice not considered in any direct sense; waste into the ecosystem also not considered directly

Pareto Optimality…

• Is achieved when noone can be made better off without someone being made worse off from the next step in the exchange process

• Pareto optimality is what an economist is referring to when speaking of “efficiency”

PO… (p. 6)

• In the goods market, Pareto opted malady is achieved when “no further trading of consumer goods can make one individual better off without making another individual worse off.”

• In production, Pareto opted malady means that “no further trading of inputs between firms can increase the production of one good without decreasing the production of another good.”

• Presumed “value neutrality”

A “price theory”… (p. 6)

• NC theory sometimes referred to as “price theory”; prices and money simply eliminate the need for barter; provides a common unit of exchange

Context of Market Exchange

• Market embedded in economy

• Economy embedded in biophysical world

• Ecological Economics perspective that NREE is “abstracted from time, place, and social and environmental context (p. 9)”

NREE sees MarketExchange as the large Box…

B u s i n e s s E n t e r p r i s e

T e c h n o l o g y I n s t i t u t i o n s

W a n t s &N e e d s

T r a n s f o r m i n g N e u t r a l S t u f f

G o o d s

R e s i d u a l s

M a r k e t sM a r k e t s

O t h e rF o r u m s

T h e r m o d y n a m i c s - 1 s t ( r e s i d u a l s ) a n d 2 n d ( e n t r o p y ) L a w s

T h e W a l l s

L i m i t s :1 s t 2 n d

The One Way Arrow

Notes how environmentalists generally critical of NC theory

• Unrealistic assumptions– Perfect information– Absence of barriers to trade– Homogeneity of goods in particular markets– Individual rationality – “and so on” (p. 11)

• G&O claim “economy/environmental conflict ultimately arises from the impossibility of economic markets to place ecologically meaningful values on the functions and attributes of the biophysical world.”

Need more focus on

• Quality of life• Long-term sustainability of the

biosphere• Larger human and nonhuman

context of economic activity• “…it is essential to understand the

theories and concepts behind economic cost–benefit calculations.”

Chp 2 The Theory of the Consumer

“What’s behind the demand curve?”

2 Fundamentals

• The consumer is deemed “sovereign”… consumer knows best

• Goods move to consumers in response to consumer preferences

The indifference curve

• Most fundamental idea in economics

• Consumers can “trade-off” goods and maintain a level of utility, as shown in these “iso-utility” curves

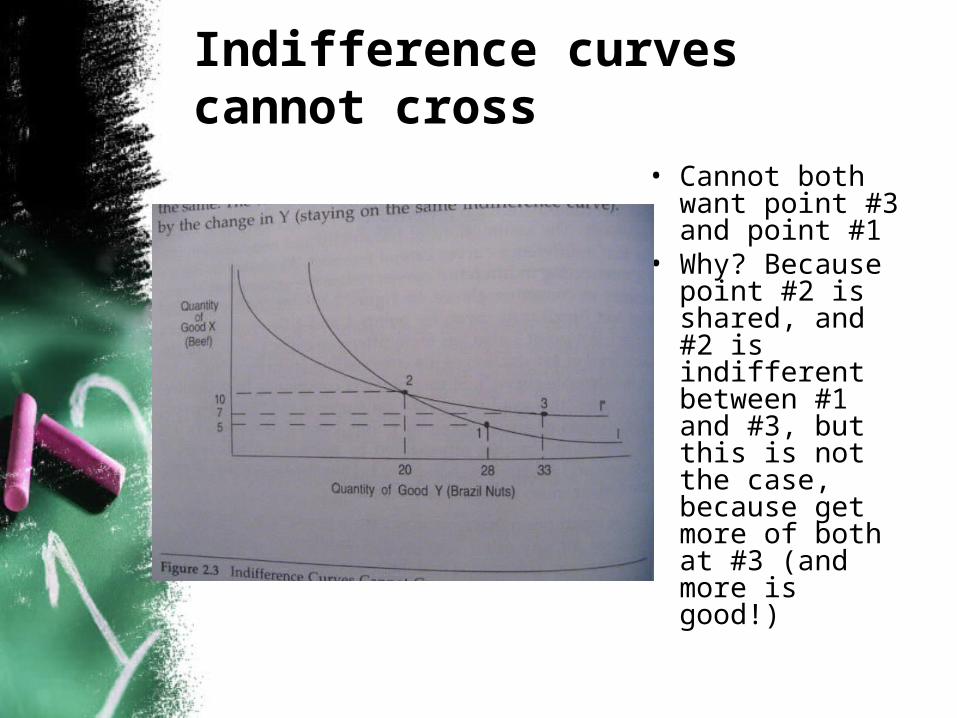

Indifference curves cannot cross

• Cannot both want point #3 and point #1

• Why? Because point #2 is shared, and #2 is indifferent between #1 and #3, but this is not the case, because get more of both at #3 (and more is good!)

Marginal rate of substitution

• MRS is about trade-offs along an iso-curve

• To increase Brazil nuts by one unit from 2 to 3, willing to give up 7-5= 2 units of beef

• Notice how MRS declines (moves to a smaller negative)

Relates to the marginal utility

• |MRS| is the ratio of the marginal utilities, or the additional pleasure one enjoys for one more unit of the good

• For the previous diagram, MRSYX is equal to the negative ratio of –(MUY / MUX)

• So, as one obtains more Y relative to X, the MUY declines relative to the increase in the MUX, causing the ratio to become a smaller (less) negative

• The notion of a “willingness to trade” is captured in this idea

Edgeworth Box and Pareto Optimality in Consumption

• Think of picking up one set of indifference curves for an individual B, by the origin, rotating same to the right

• Set them down on the other set indifference curves for A

Conditions along the “contract curve”

• MRSAYX = MRSB

YX

• This is the goal of economic policy– Make small changes at the margin– Continue to make changes until someone

would be made worse-off – When noone can improve their state in life

from further trading without making someone worse off, we have achieved economic efficiency

– This is true at every point on the contract curve

– There are infinite number of economically efficient points in consumer trading activities

How relate to information about the natural world?

• G&O point out markets may be populated with consumer participants who know little or nothing of the natural world

• For example, consumers may buy aerosol sprays that are destroying the ozone layer quite oblivious to even the notion of such a layer being essential for long term survival

• Consequences for biodiversity may not be known, in the purchase decision

Assumption of substitutability

• NC theory sees no need for concern, as there are always substitutes

• Only concern is balancing, trading-off human satisfaction from one good versus another

• All other factors are “external” to the market

Irreversibility, Thresholds, Interconnectedness

• The idea of MRS being equal across all consumers for all time presumes everything is reversible, e.g. consumption decisions driving a species to extinction could be somehow overcome, “reversed”

• There are no thresholds to be avoided• Connectedness between consumers,

and with the environment, is assumed away; no complementarity

Discounting

• Consumer theory focuses on the “now” represented in the life-span of homo sapiens, assumed roughly to be no more than 100-years, of each consumer

• Individuals are presumed to always discount the future, wanting it now, rather than willing to wait very long for it, and certainly not leave it for future generations

Models and Reality

• G&O note how models are always abstractions

• Yet, they are calling for an economic model that is not quite so abstract, recognizing:– Connections and feedbacks need to be

better represented– Absolute scarcity of resources is real– Need for a better representation of the life

support systems of the planet– Perhaps need more value placed on distant

consumption, beyond “the next 100-years”

3 The Theory of the Firm

“What is behind supply?”

3 Fundamentals

• Refer to each firm having inputs or “factors” to be used in production, e.g. land, tractors, feed yards to produce beef

• Firms have production functions and isoquants

• Motivation: Maximize profits, in response to consumers who are sovereign

Households provide Inputs

• Notice that the natural system is presumed made available through households: Natural resources are presumed privatized/ owned by individuals

• One way movement of materials: No residuals

The Isoquant

• Capital and labor provided by the households is combined to produce “goods”

• The “iso-quant” shows equal quantities for each combination of inputs

• Presumed that one can always find a substitute input

• Increasing rate of substitution as move to the left: Takes ever more capital to replace labor as reduce labor to smaller amounts, e.g. eventually using human-like robots!

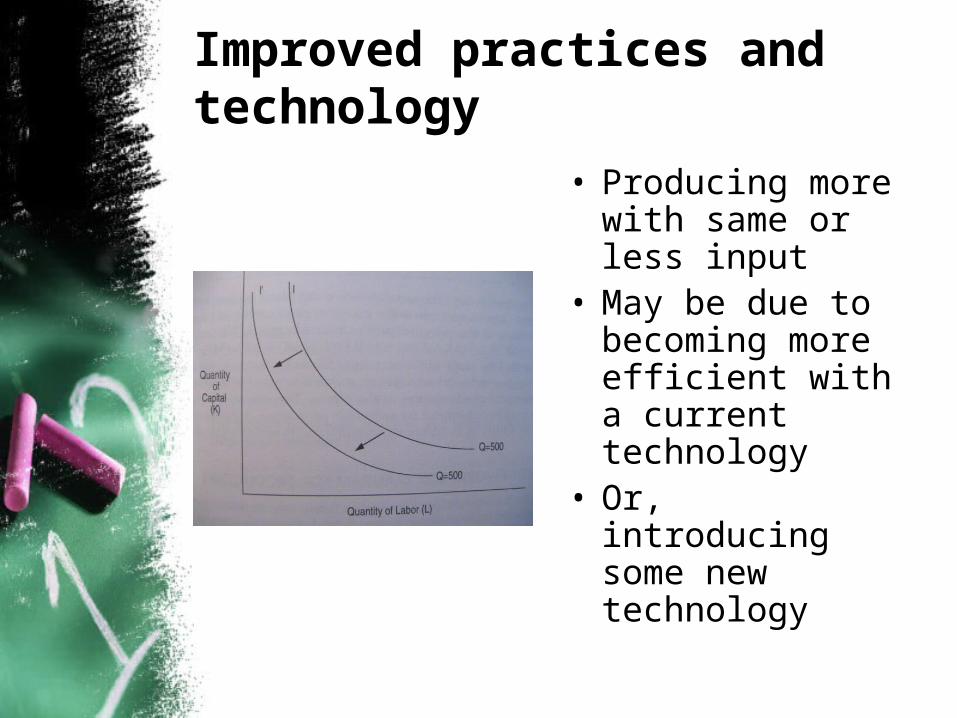

Improved practices and technology

• Producing more with same or less input

• May be due to becoming more efficient with a current technology

• Or, introducing some new technology

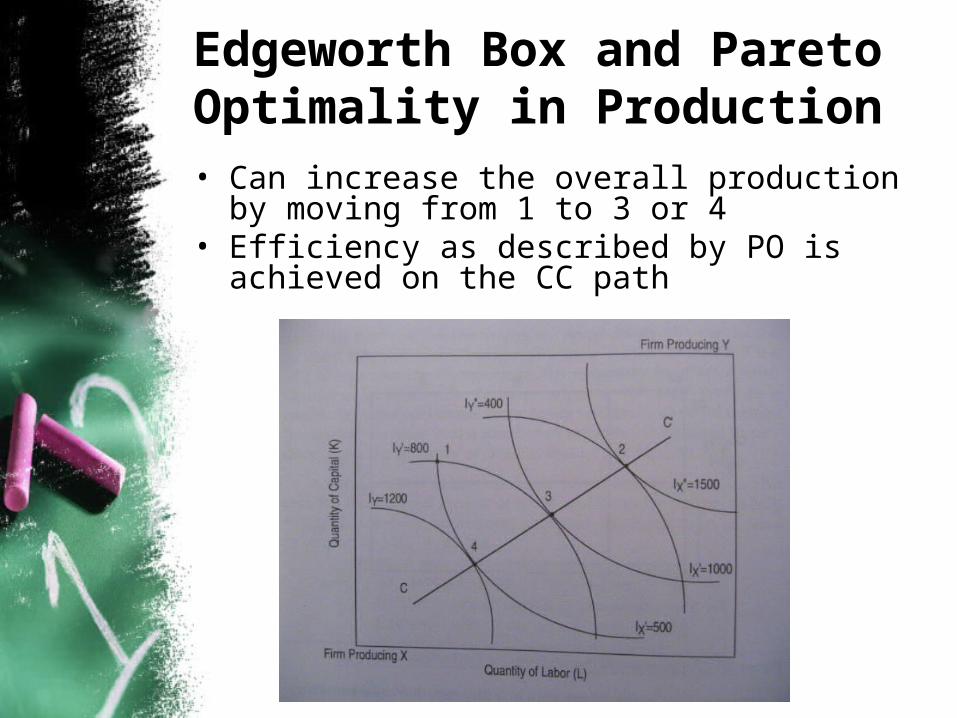

Edgeworth Box and Pareto Optimality in Production• Can increase the overall production by moving

from 1 to 3 or 4• Efficiency as described by PO is achieved on

the CC path

Production Possibilities

• Moving along CC in the previous diagram we can trace this curve showing the most efficient way to produce X and Y

• Some point 1 inside CC would correspond to point 1 in the previous diagram, an inefficient way to produce

Critique of Production Theory

• G&O claim the foregoing has little to do with real production (p. 48)

• Does not describe the actual transformation of inputs into goods; only explores possibilities in resource allocation

• No sense of priorities set on what goods (and bads) to be produced; efficiency is the only concern

G&O Critique…

• Says nothing of resource scarcity in an absolute sense; concerned only with relative scarcity (p. 49)

• Does not address the by-products, the wastes• No notion of optimal scale relative to the

resource base on which it depends (p. 49)• Substitutions ongoing in the economy take

place outside these “boxes,” just like the side effects also occur outside the boxes (p. 49)

• Does not adequately model the longer term questions of limits

G&O Critique…

• Perhaps most importantly: Presumes essentially not problems with substitutes… there will always be something

• G&O highlight the Cobb Douglas function as having special problems due to isoquants never touching the axis, and displaying a constant elasticity of substitution at a value of 1 (pp. 52-55)

• Created special problems with capital to natural resource substitution studies

4 General Equilibrium and Welfare Economics

“What’s behind social value, equilibrium?”

Chp 4 General Equilibrium

• Bring firms and households (consumers) together

• Inputs provided by the households• Goods provided by the firms

General Equilibrium in Exchange

• Bring the Edgeworth box into the Production Possibilities diagram

• Allocate this much of each good• Rule: MRSy-for-x = RPTy-for-x … “barter”

economy

Grand Utility Possibilities Frontier

• Move along such paths through “2” in the previous figure

• As many of these as there are combinations of X and Y

• Connect all the highest points, defined by situation where MRS=RPT for each case

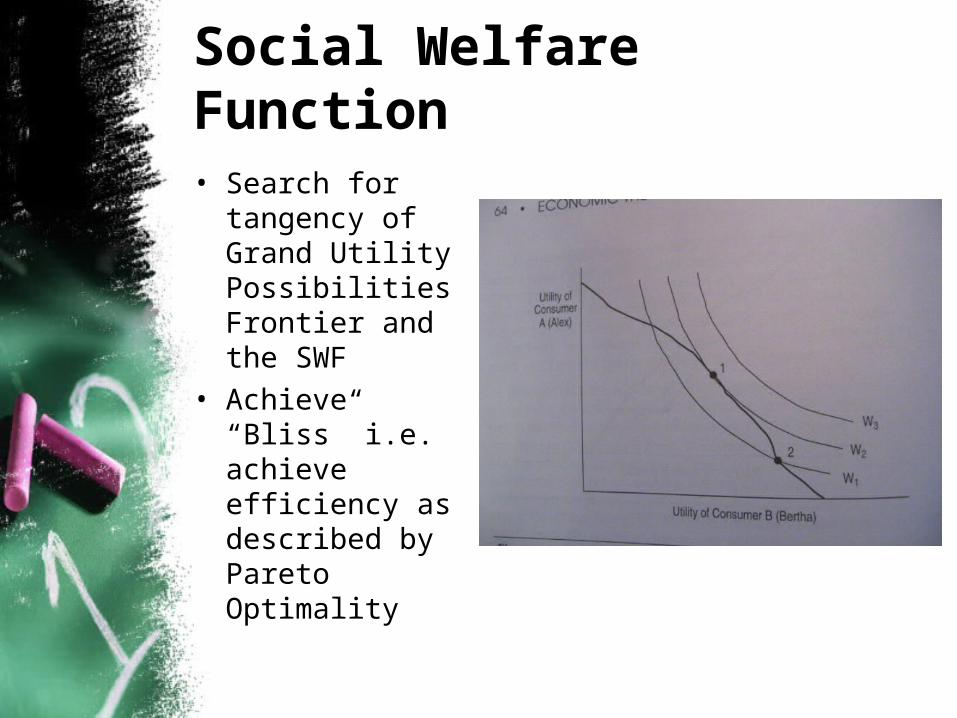

Social Welfare Function

• Search for tangency of Grand Utility Possibilities Frontier and the SWF

• Achieve “Bliss” i.e. achieve efficiency as described by Pareto Optimality

General Equilibrium Theory and the Biophysical World (p. 66)

• Relevant time frame is immediate, the present and current situation

• Place not considered, i.e. the ecological context, the social context is not in the model

• Initial start-up conditions, like who is controlling how much of what natural resources is outside the model

• No feedbacks, so no need for caution• Success is measured by individual, material

accumulation (p. 67)• Denies any role of social context, community

support, families… other than as the sum of individual parts

General… cont

• Cannot compare utility from individuals… so the utility of 1-more pound of beef to the wealthy cannot be compared to the utility of 1-more pound of Brazil nuts to the poor

Social Welfare and Ethics

• G&O contend that humans are social beings, “social agents embedded in a social context” (p. 68)

• G&O note how some economists, in trying to respond to this issue, have considered altruism as a kind of preference

• G&O mention Rawls… as a way to address intergenerational issues

Social… cont

• G&O claim that Adam Smith saw only self(ish)-interest leading to the best interest of society as a whole

• G&O claim: “The individual’s well-being is intricately connected to the well-being of the community, and thus the welfare of the whole is decisive. Examples of a mutual and reciprocal understanding of the individual as part of a larger social and ecological context are found in the belief systems of indigenous peoples. What happens to nature is inseparably connected to the fate of humans. The neoclassical framework asserts not only a particular kind of economic understanding but also a particular cultural perspective of the relationship between individuals and their social and ecological context… In many ways the global environmental problems we face have added new fuel to the welfare discussion… added a new dimension to the interconnectedness between individual and social context.” (p. 69) (italics added)

Beyond Human Welfare

• How consider the welfare of non-human, biophysical elements of planet earth

• Leopold, 1930s, called for a “land ethic”… today’s environmental movement

• Eco-feminism, ego-justice, responsibility-based ethic

G&O Summarize

• In organizing consumption and production, demand and supply, ultimately need to consider the SWF

• It is essential, but impossible, due to not being able to compare utilities

• Yet, all societies implicitly construct a SWF through cultural, political processes

• Really requires the moral dimension… moral and ethical considerations… to be brought to the table

• The implicit SWF of NREE makes a particular moral, ethical statement

• As the next chapter shows, whatever the market produces is deemed an expression of the SWF; the market is implicitly deemed moral and ethical

5 Introducing Prices: Pareto Optimality and Perfect

Competition“Does the market

achieve peace of mind?”

Introduction• Money is added• Reason: to move away from bartering and

achieve efficiency more easily• Market is conceived as an auction

Prices in Consumption: The Budget Constraint

• Maximize utility subject to one’s budget• Move up the path 4 2 3 (if can, but budget

stops this consumer at 2)• Path has characteristic that

|MRSYX | = MUY/MUX = PY/PX

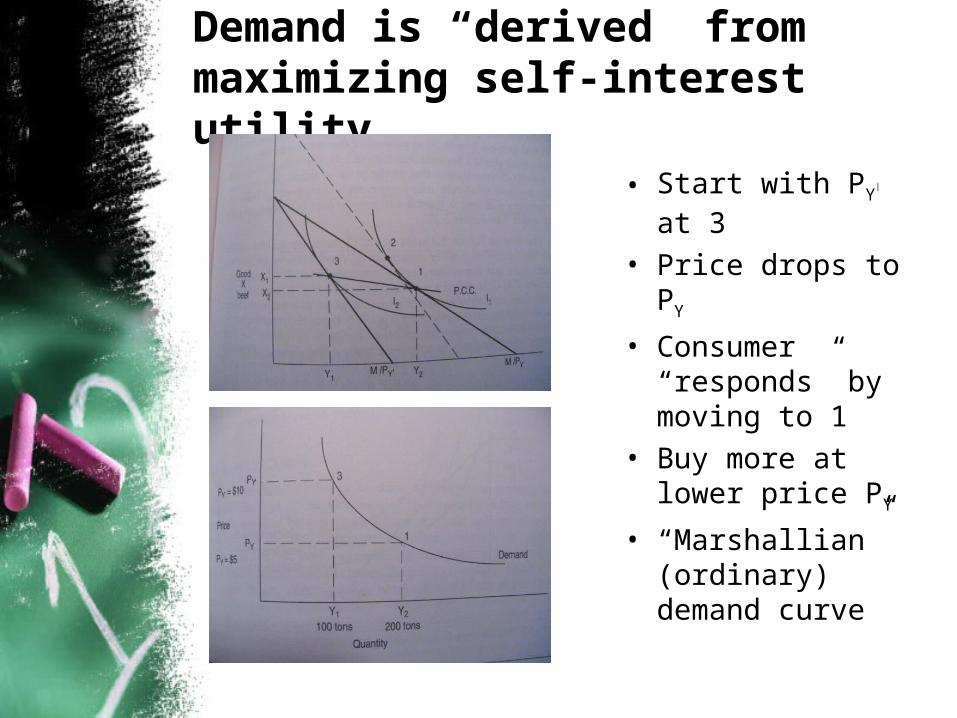

Demand is “derived” from maximizing self-interest utility

• Start with PY| at 3

• Price drops to PY

• Consumer “responds” by moving to 1

• Buy more at lower price PY

• “Marshallian” (ordinary) demand curve

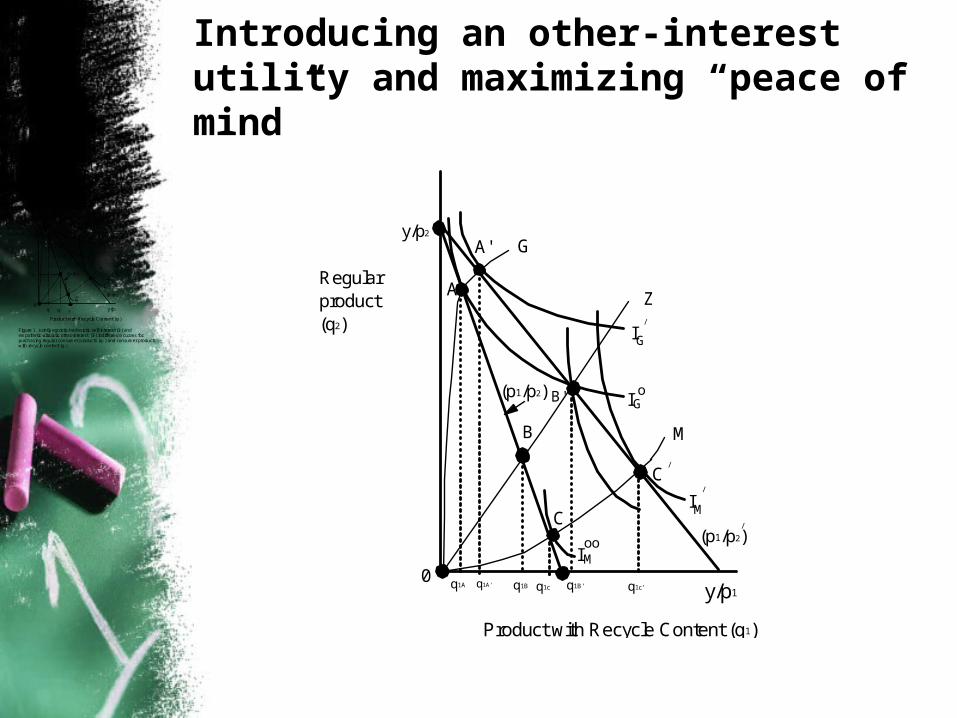

Introducing an other-interest utility and maximizing “peace of mind”

Z

y

q2

0y

I

C

A'

I

Io

I

/

/

Figure 1. Jointly egoistic-hedonistic self-interest (IG) and empathetic-altruistic other-interest (IM) indifference curves for purchasing regular consumer products (q2 ) and consumer products with recycle content (q1).

Product with Recycle Content (q1)

Regularproduct(q2)

//

G

M

y/p1

B

y/p2

//

A

C(p1/p2)

(p1/p2) q2

q1 q1

G

G

M

Mo

/

/

/

/

/ Z

0

I

C

A'

I

Io

I

Product with Recycle Content (q1)

Regularproduct(q2)

G

M

y/p1

B

y/p2

A

C(p1/p2)

(p1/p2)

q1A' q1B

G

G

M

Moo

/

/

/

/

B'

q1A q1B'q1c q1c'

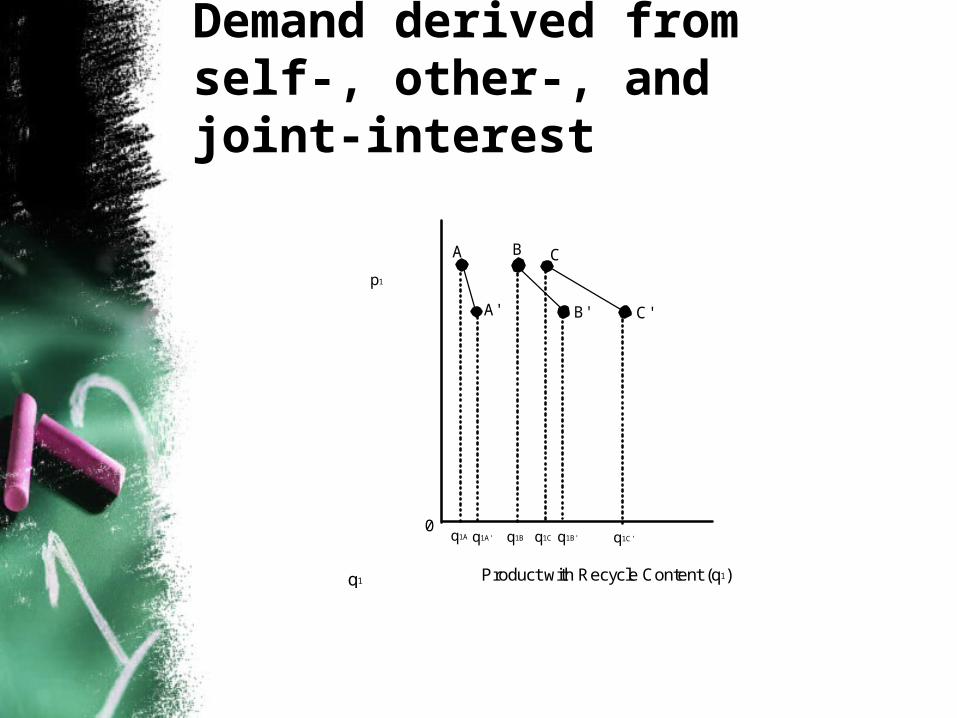

Demand derived from self-, other-, and joint-interest

0

C'A'

Product with Recycle Content (q1)

B

p1

A C

q1A

q1

B'

q1C'q1B'q1Cq1Bq1A'

Prices in Production: The Cost Constraint

• Entire capital budget along C

• Use it mainly on labor or mainly on machinery

• Least cost at point 1

“No-limits” expansionpath

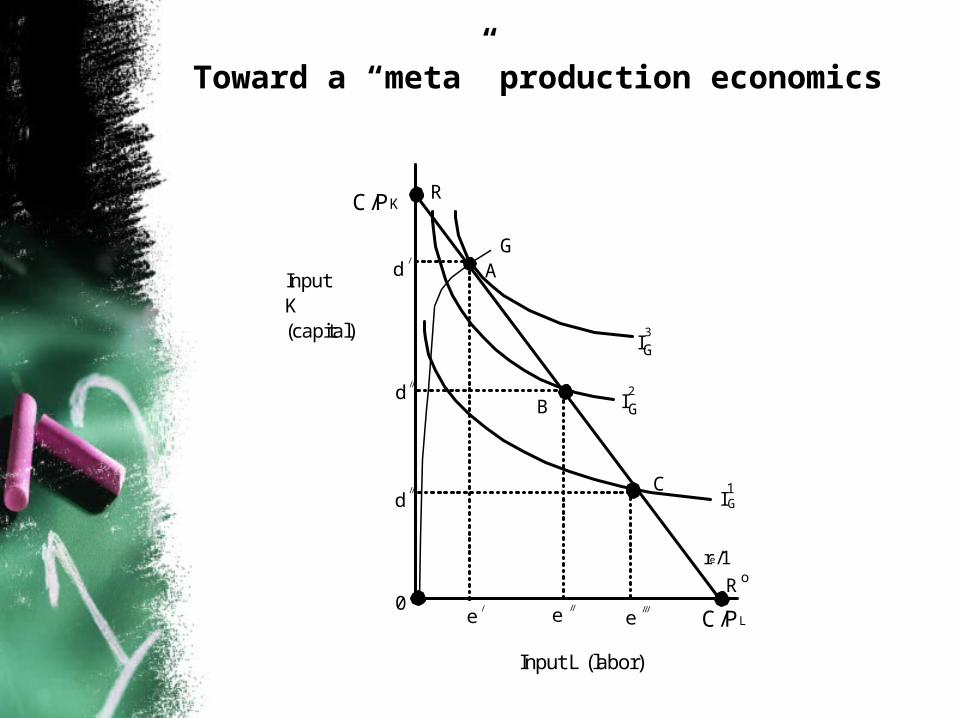

Toward a “meta” production economics

R

d

d

0e

C

A

I

I G

G

/

/

Input L (labor)

Input K(capital)

///

G

C/PL

C/PK

2

1

e

//

re/1

B

GId///

e //

3

Ro

Meta-isoquants

Z

R

d

d

0e

I

C

A

I

I G

G

M

IM

/

/

Input L (labor)

Input K(capital)

///

G

M

R/re

R/rd

2

1

3

1

e

//

re/1

B

GI

2

d///

e //

MI

3

Ro

Total cost and total revenue: Moving toward the “supply” fn

• Moving along the “expansion path” can trace off a total cost (TC) function

• Can also measure total revenue in this same space; a linear TR suggests a constant price (slope is that price)

Corrected TR

Marginal revenue and cost

• Move along some TC curve and plot the slope of it = MC• Move along TC and plot the slope of a ray out of the origin = AC• Earn normal, maximum profits at point where MR=MC at the low point of AC curve• Economic profit is zero, i.e. are earning a normal return on all inputs (with MR=AR=AC)• Supply curve is the MC curve at and on either side of this point (above it for long run; starts

somewhat below it, at average variable costs (AVC), in short run• “Add-up” all such points to develop the industry supply curve, “the supply”

AVC

Perfect Competition

• Now know the origin of the “supply-demand” diagram • Special case in supply-demand: Large number of buyers and sellers • As G&O describe it, this is the “heart and soul” of NREE economics • If competition prevails, each firm has little market power, so MR = price• If competition prevails, each consumer pays that (same) price

Efficiency: Competitive Firm

• As noted in addressing supply, firms operate where MR = p = MC

• This is a long run MC

• This is at the minimum of LRAC

• Only “normal” profits being earned

Perfect Competition and Pareto Optimality

• Notice the similarity between the results in perfect competition and the social welfare model

• Introduce money, and observe evolution of prices, find that competition “maximizes welfare” = “sum is sum of parts” = utilitarian philosophy

• MRSXY = PY/PX

• MRTSKL = PL/PK

• MCX = PX, MCY=PY

• MCY/MCX = PY/PX = RPT• MRS = RPT