Embed Size (px)

Citation preview

World Development, Vol. 17, No. 4, pp. 491-502. 1989. 0305-750X/89 $3.00 + 0.00 Printed in Great Britain. 0 1989 Pergamon Press plc

Economic Stabilization and Structural Transformation: Lessons from the Chilean

Experience, 1973-87

CRISTIAN MORAN* The World Bank, Washington, DC

Summary. -This paper evaluates the experience of economic reforms and stabilization efforts in Chile during 1973-87. The paper presents a brief historical background, and then reviews the main goals, policy tools, and results of the economic program implemented since the military government came to power in September 1973. The paper discusses in detail the stabilization and structural transformation aspects of the economic program - including the privatization of the economy and the trade and financial liberalization. The main conclusion is that, despite a healthy improvement in the economic situation during 1985-87, the future of the Chilean economy remains uncertain and vulnerable to external shocks. The paper concludes by summarizing the main policy lessons of the Chilean experience.

1. INTRODUCTION

This paper evaluates the experience of econo- mic reforms and stabilization efforts in Chile during 1973-87. Its objective is to answer three main questions: (i) what were the objectives of and motivations for the economic policy changes introduced in Chile during this period? (ii) what are the main results - both in comparison to Chile’s own historical record and in comparison to the record of other developing countries during the same period? and (iii) what are the main policy lessons from this experience?

The emphasis adopted here is mostly nontech- nical, and covers exclusively the economic dimension of the changes introduced since 1973. The paper discusses the essential features of the economic program in a way that permits a comprehensive analysis of the whole period, but does not discuss the socio-political aspects of the changes introduced in Chile - although it recognizes that the economic program was closely linked to the political philosophy of the new regime. By focusing exclusively on the eco- nomic dimension of these changes, however, the paper provides a more detailed analysis of the economic program. It also gives references to guide the interested reader into other material that describes more fully topics which are only touched upon here. The limitations of this analysis should be borne in mind.

Section 2 provides a brief historical back- ground to Chile’s policy experiment, and states the main objectives of the economic program. Section 3 describes the stabilization aspects of the program, which focused on the control of infla- tion and the associated fiscal and balance-of- payments imbalances. It also discusses the events leading to the crisis of 1982-83 and the economic adjustment program implemented since 1985. Section 4 discusses the structural transformation aspects of the program. It distinguishes three key components: the privatization of the economy, the trade liberalization, and the financial liberali- zation. Finally, Section 5 summarizes the main economic lessons of the Chilean experience.

2. BRIEF HISTORICAL BACKGROUND AND OBJECTIVES OFTHE ECONOMIC

PROGRAM

During most of the present century, the

*An earlier version of this paper was presented at a conference on “Chile Now,” at Haverford College, Pennsylvania, February 28, 1987. I am grateful to Patricia Meller and sev ral World Bank colleagues for helpful comments.

This paper represents the author’s view, and should not be attributed to the World Bank, its Board of Directors, its management, or any of its member countries.

491

492 WORLD DEVELOPMENT

Chilean economy depended on one or two mineral exports (first nitrates and copper, then mostly copper) to generate the foreign exchange it needed to finance development efforts. These exports also generated a substantial part of tax revenue. Continuous fluctuations in the prices of these commodities led to recurrent balance-of- payments crises, and had drastic effects on the government budget. To insulate the economy from these effects, Chile adopted an import substitution strategy, a process that was de- lineated during the late 1940s and which gained strength in the 1950s.

The import substitution strategy failed in two main respects. First, the government lacked the political stability and coherence needed to im- pose some economic rationale on the whole process. Second, the strategy was biased toward the protection of the domestic industrial sector, and discriminated heavily against exportable goods in general, and against agricultural goods in particular. This led to an overvalued domestic currency, drastic restrictions on imports, and a system of taxes and subsidies that gave arbitrary and ad hoc protection to specific sectors. On top of this, price controls for essential commodities and domestic interest rates coexisted with an elaborate array of social benefits, perpetuating the budget deficits which were financed by inflationary monetary expansion and foreign borrowing. While some of these ills were cor- rected during the 1960s they regained full force during the Allende administration (1970-73).

By late 1973, Chile badly needed a stabiliza- tion program that could control inflation and correct an acute fiscal and balance-of-payments crisis. The new government designed an emergency program that dealt with these issues, and later broadened the scope of the program and attempted a full-scale restructuring of the foundations of Chilean society.

The economic team called upon to design the program and carry full responsibility for its implementation was a group of young economists heavily influenced by the orthodox monetary theories taught at the University of Chicago. This group of economists (which took control of economic policy making in 1975 and, for the most part, retained that control through 1987) firmly believed that the economic problems that had afflicted Chile in the 20th century stemmed from two main characteristics of its development process: (i) it was a closed and highly protected economy; and (ii) the government interfered excessively in economic matters. They therefore decided to move quickly to limit the role of the government, to open up the economy to inter- national trade and capital flows, to establish a set

of free market-oriented policies, and to declare that the principle of “neutrality” (I.e.. of nondis- crimination) would determine all economic deci- sions. The main emphasis of the program was on economic efficiency. Considerations of the distri- bution of income or wealth were notably de- emphasized, on grounds that the higher growth rate that would result from the new development strategy would automatically yield an improved situation for all economic agents - the “trickle down” effect.

The economic program had two main com- ponents: the stabilization program and the struc- tural transformation program.

3. THE STABILIZATION PROGRAM

In the first few years of the military govern- ment, controlling the balance-of-payments crisis received high priority. This priority became even more urgent as the negative external effects of the first oil shock unfolded in 197-l-75. After these events receded, controlling inflation be- came the main goal of the stabilization program.

Initially, inflation was diagnosed as being caused primarily by the monetary expansion used to finance the fiscal deficit. Thus, an orthodox set of deflationary policies was implemented, focus- ing on the control of domestic monetary expan- sion and the government deficit. Despite the slow growth of domestic credit, however, inflation proved more stubborn than initially envisioned. At the end of 1975, inflation was still running at about 300% per year - after having peaked at 1000% at the end of 1973. Output declined 12% in 1975 and unemployment increased to about 20% that year, compared to an average unem- ployment rate of about 5-6% in the 1960s.’

In early 1976, the government changed its diagnosis of inflation and argued that. since Chile was on its way to becoming a small, open economy, the rate of inflation was mostly deter- mined by external inflation and by the rate of change in the exchange rate - although it recognized that inflationary expectations played a pervasive role in the short run. The strategy was then changed, and the exchange rate policy became the main stabilization tool to control inflation. In June 1976 and again in early 1977, the government revalued the domestic currency, and then subsequently devalued it through a sequence of preannounced exchange rate changes. The rate of devaluation, however, was kept below the difference between the rate of domestic and foreign inflation, in an effort to break inflationary expectations and to set a ceil- ing to the domestic rate of inflation. This process was completed in June 1979, when the exchange

rate was fixed against the US dollar. A few months later, the government announced that the new rate would be maintained indefinitely.

Inflation was ultimately controlled, but it took much longer than originally anticipated. In 1981, Chile achieved an inflation rate of 9%, similar to the local currency inflation of the major indus- trial countries. By that time, however, the peso was grossly overvalued, stimulating imports to unprecedented levels, discouraging exports, and maintaining an unsustainable domestic consump- tion boom financed by foreign borrowing.* On top of this, the second oil shock and a reduction in real copper prices had triggered a new decline in the terms of trade, and international real interest rates had started to rise. At the end of 1981, there were signs that the economy was already in a weak position, both domestically and in its external accounts. As a consequence, net capital inflows started to decline - although they were still positive. By mid-1982, net capital flows had turned negative, a process that was rein- forced by the global debt crisis that afflicted most of the Latin American countries.

few others. Bank deposits were publicly guaran- teed, upper limits on passive nominal interest rates were imposed, and emergency credit pro- grams established. Two of these programs - the provision of subsidized credit lines to reschedule peso private debts, and the preferential exchange rate to US dollar debtors - involved massive increases in Central Bank credit to financial intermediaries. These programs were later com- plemented by Central Bank purchases of the nonperforming portfolios of commercial banks.

The Chilean economic authorities were slow to react to these events, however, since they were convinced that the adjustment process would be automatic and short lived. But the adjustment was neither. In fact, the adjustment did not occur because a policy inconsistency had been built into the system. To correct the real overvaluation of the peso (given a fixed nominal exchange rate) nominal wages and/or profits had to decline. But wages were prevented from declining by a re- cently enacted labor law that put a floor on wage changes, limiting wage adjustments to past changes in inflation.

By 1985, it became clear that the problems Chile faced were much more serious than initially envisioned, and that a longer-term strategy was needed to address them. The government decided to initiate a new adjustment program, which emphasized three key areas: (i) export incentives and the balance of payments; (ii) domestic resource mobilization; and (iii) rehabi- litation of the financial and corporate sectors. This program was complemented with an ortho- dox stabilization package and an explicit attempt to restructure the external debt. It also received the support of the International Monetary Fund (IMF), through a three-year Extended Fund Facility arrangement, and the World Bank, through three consecutive structural adjustment loans.

As a result, the economy went into a drastic recession. The government was forced to devalue the peso in June 1982. It continued a series of devaluations for the next two years. With the devaluations, the price of domestic assets in dollar terms fell drastically and large capital losses occurred. This aggravated the crisis and prompted further speculation against the peso. Real GDP fell 14% in 1982 and another 1% in 1983. Unemployment reached 28% of the labor force in 1983, including those enrolled in the government’s two emergency programs: the Minimum Employment Program (PEM) and the Program for Heads of Households (POJH). Fixed real investment declined 44% during 1981- 83, and import volumes declined 46%. It was Chile’s worst depression since the 1930s.

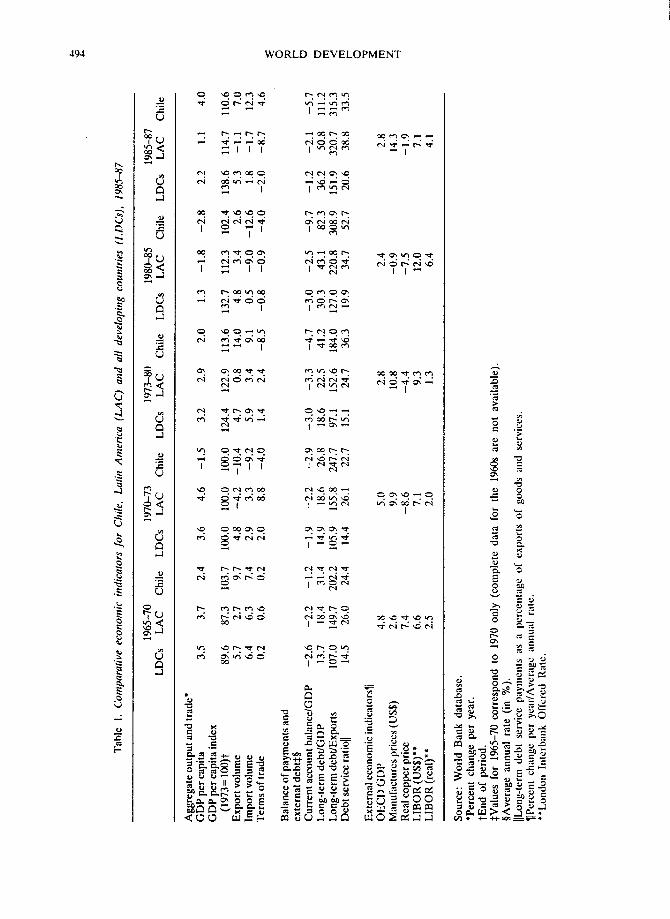

The new adjustment program was well de- signed and avoided previous policy mistakes. It also benefited from a moderate improvement in the external environment. As a result, GDP growth averaged 5.6% per year during 1985-87 (or 4.0% per year in per capita terms), led by increases in exports and investment. With strong output growth, unemployment decreased at a significant pace: from 22.3% in 1984 to 10.6% in 1987, the lowest level since 1974. The current account deficit, finally, declined from US$2.1 billion (10.7% of GDP) in 1984, to US$l.O billion (4.8% of GDP) in 1987. This was due to significant increases in exports, and helped by reductions in international interest rates and improvements in the terms of trade (Table 1).

TO avoid a complete breakdown of the entire economic system, the Central Bank provided financial support. In January 1983, it intervened in the five largest private banks. and liauidated a

Even though Chile’s recent economic recovery has been strong, per capita consumption is still below the level attained in 1970-73. GDP per capita in 1987 was below the previous peak of 1981, although it was 10% above the level of 1973 and 7% above that of 1970. But GNP per capita in 1987 - which excludes interest payments on the external debt - had barely recuperated to the level of 1970. Private consumption per capita was 15% below the level of 1973, and 8% below the level of 1970.

_ .

Note that the decline in consumption between 1970 and 1987 coincides with the decline in real wages, but the comparison may be somewhat

STABILIZATION AND STRUCTURAL TRANSFORMATION IN CHILE 493

Tab

le

1. C

ompa

rativ

e ec

onom

ic

indi

cato

rs

for

Chi

le,

Lat

in

Am

eric

a (L

AC

) an

d al

l de

velo

ping

co

untr

ies

(LD

Cs)

, 19

85-8

7

1965

-70

1970

-73

1973

-80

1980

-85

1985

-87

LD

Cs

LA

C

Chi

le

LD

Cs

LA

C

Chi

le

LD

Cs

LA

C

Chi

le

LD

Cs

LA

C

Chi

le

LD

Cs

LA

C

Chi

le

Agg

rega

te

outp

ut a

nd t

rade

* G

DP

per

capi

ta

GD

P pe

r ca

pita

ind

ex

(197

3=1O

O)t

E

xpor

t vo

lum

e Im

port

vol

ume

Ter

ms

of t

rade

Bal

ance

of

paym

ents

an

d ex

tern

al

debt

$§

Cur

rent

ac

coun

t ba

lanc

e/G

DP

Lon

g-te

rm

debt

/GD

P L

ong-

term

de

bt/E

xpor

ts

Deb

t se

rvic

e ra

tio1

1

Ext

erna

l ec

onom

ic

indi

cato

rs11

O

EC

D

GD

P M

anuI

actu

res

pric

es (

USS

) R

eal

copp

er

pric

e L

IBO

R (

US$

)**

LIB

OR

(r

eal)

**

3.5

3.7

2.4

3.6

4.6

-1.5

3.

2 2.

9 2.

0 1.

3 -1

.8

-2.8

2.

2 1.

1 4.

0

89.6

87

.3

103.

7 10

0.0

5.7

2.7

9.7

4.8

6.4

6.3

7.4

0.2

0.6

0.2

-2.6

-2

.2

-1.2

-1

.9

-2.2

13

.7

18.4

31

.4

14.9

18

.6

107.

0 14

9.7

202.

2 10

5.9

155.

8 14

.5

26.0

24

.4

14.4

26

.1

4.8

5.0

2.6

9.9

7.4

-8.6

6.

6 7.

1 2.

5 2.

0

100.

0 -4

.2

3.3

8.8

100.

0 12

4.4

122.

9 11

3.6

132.

7 11

2.3

102.

4 13

8.6

114.

7 11

0.6

-10.

4 4.

7 0.

8 14

.0

4.8

3.4

2.6

5.3

-1.1

7.

0 -9

.2

5.9

3.4

9.1

0.5

-9.0

-1

2.6

1.8

-1.7

12

.3

-4.0

1.

4 2.

4 -8

.5

-0.8

-0

.9

-4.0

-2

.0

-8.7

4.

6

E

r -2

.9

-3.0

-3

.3

-4.7

-3

.0

-2.5

-9

.7

-1.2

-2

.1

-5.7

b

26.8

18

.6

22.5

41

.2

30.3

43

.1

82.3

36

.2

50.8

11

1.2

z 24

7.7

97.1

15

2.6

184.

0 12

7.0

220.

8 30

8.9

151.

9 32

0.7

315.

3 2

22.7

15

.1

24.7

36

.3

19.9

34

.7

52.7

20

.6

38.8

33

.5

F!

g

2.x

2.4

2.8

K

10.8

-0

.9

14.3

$

-4.4

-7

.5

-1.9

9.

3 12

.0

7.1

1.3

6.4

4.1

Sour

ce:

Wor

ld

Ban

k da

taba

se.

*Per

cent

ch

ange

pe

r ye

ar.

tEnd

of

pe

riod

. $V

alue

s fo

r 19

65-7

0 co

rres

pond

to

19

70 o

nly

(com

plet

e da

ta

for

the

1960

s ar

e no

t av

aila

ble)

. §A

vera

ge

annu

al

rate

(i

n %

).

/Lon

g-te

rm

debt

se

rvic

e pa

ymen

ts

as

a pe

rcen

tage

of

ex

port

s of

go

ods

and

serv

ices

. II

Perc

ent

chan

ge

per

year

/Ave

rage

an

nual

ra

te.

**L

ondo

n In

terb

ank

Off

ered

R

ate.

STABILIZATION AND STRUCTURAL TRANSFORMATION IN CHILE 495

misleading because of the drastic changes in composition. After increasing moderately in the second half of the 1970s real wages declined by 145% between 1981-85, and increased slightly during 1985-87 (by 1.8%). As a consequence, average real wages in 1987 were 15% below the level achieved in 1970.3 But since the price of imports relative to nontradeables declined as a consequence of the trade liberalization (dis- cussed below), import consumption almost cer- tainly increased during 197&87, despite similar income levels (GNP per capita). Thus, if the consumption weight given to imports, and parti- cularly to consumer durables, is higher than the weight given to nontradeables - an hypothesis consistent with the higher income elasticity for the former group of commodities - then the gap in the appropriately resealed consumption figures between 1970 and 1987 may be smaller than what the aggregate consumption figures suggest.

Despite this caveat, Chile’s economic perfor- mance during 1973-87 did not produce an im- provement in average living standards (income and consumption per capita) over that achieved in 1970 - and may have made the living standards of the poor deteriorate. The available evidence indicates two things. First, the percen- tage of poor households (defined as those whose per capita income is below two times the cost of a basic basket of food items) in the Greater Santiago area increased from 29% in 1969 to 46% in 1985, having peaked at 57% in 1976 (Pollack and Uthoff, 1987). Second, the concen- tration of income increased significantly between 1968-73 and 1980-84, as measured by the Gini coefficient - which increased from 48.0% in the first period to 53.6% in the second (see Torche, 1988, Table 12, p. 186).

It may be inappropriate to make a mechanical comparison of Chile’s performance during 197F 87 with its own historical record, as changes in the external environment (e.g., smaller increases in world trade and declining terms of trade) may well explain this deterioration. Still, when one looks at the experience of the average developing country, one finds that Chile’s economic per- formance during the last 14 years - and particu- larly during 1973-85 - is indeed poor. More recently, however, things have changed. While the average developing country grew at rates of 3.2 and 1.3% per year during 1973-80 and 198O- 85, respectively, Chile’s record indicates increases of 2.0 and -2.8% per year. The difference between Chile and the average Latin American country (which grew at rates of 2.9 and -1.8%) is not as marked, but Chile still shows a poorer performance. In contrast to the sluggish growth of other developing countries, however,

Chile’s economy grew strongly during 1985-87. This helped narrow the gap in per capita income growth, but did not eliminate it. By 1987, Chile’s GDP per capita level, using 1973 as a basis for comparison, was still 4% below that of other Latin American countries, and 20% below that of the average developing country (Table 1). Thus, both in absolute and in relative terms, Chile’s economic record is disappointing.4

In sum, although Chile’s stabilization efforts produced some positive results, the costs asso- ciated with these policies may have been un- necessarily harsh. On the positive side, inflation did come down after eight years of policy experimentation, and public finances, including public enterprises, were brought under control. The latter result was, in part, a direct conse- quence of the privatization process (discussed in detail below), but was also brought about by comprehensive tax reform initiated in the early years of the stabilization program. On the negative side, the poor growth performance and the dramatic rise in unemployment throughout the past 14 years are evidence of an enormous economic waste that should have been dealt with more decisively. While there are different reasons for the increase in unemployment rates (including the reduction in government employ- ment, the low growth of aggregate demand, and the restructuring of the economy in conditions of labor market rigidity), the government’s drastic cutback in public investment programs during 1973-83 may have unnecessarily tightened the resources needed for a smoother transition to- ward a more open and modern economy.

Finally, and perhaps most important, it is possible that the negative effects of the drastic recessions in 1975 and 1982-83 will significantly impair Chile’s long-term growth prospects. There are clear indications that severe recessions not only cause unnecessary bankruptcies - as they destroy productive units which would be profit- able under normal conditions - but also that the associated cutbacks in social programs severely hurt the formation of human capital, although the effects may be quite delayed.5 In Chile, while the government has made progress toward im- proving the targeting of social programs to the poor, prolonged unemployment and under- employment, and the associated increase in the poor population, coupled with a reduction in health and education expenditures, may cause a slowdown of future growth. One hypothesis, which should be the subject of future investiga- tions, is that the costs and benefits of drastic booms and busts may be asymmetric, as the scrapping of physical capital and the social hardships suffered by the poorest segments of

196 WORLD DEVELOPMENT

society in economic downturns may not be easily redeemable in economic upswings.

4. THE STRUCTURAL TRANSFORMATION PROGRAM

For expository purposes, it is convenient to distinguish three key components of the struc- tural transformation program implemented in Chile, all of which are clearly interrelated: (a) the privatization process; (b) the international trade liberalization process; and (c) the financial liber- alization process.

(a) The privatization process

The Chilean economy witnessed two distinct episodes of privatization during the period of 1973-87. The first episode occurred during 1974- 81, but was mostly complete by 1978. The second episode started in 1985 and still continues, although a significant part of it was completed during 1986. The motivation behind these two episodes was the same, however, as the govern- ment attempted to transfer state-controlled assets to the private sector in its overall effort to reduce the size of the public sector, and to restructure the economy so as to increase effi- ciency.

As soon as the new government took control in 1973, rapid steps were taken to return to the private sector the firms and agricultural plots illegally seized during the previous administra- tion. In the first phase (1973-78) of this privatiza- tion episode, about 3,700 farms (a total of 2.9 million hectares) and 257 firms (out of a total of 259 that had been seized during 1970-73) were returned to their previous owners. This process was relatively expeditious and encountered little resistance. No money was involved, and the previous owners were asked to renounce any legal claims against the government.

During the second phase (1974-81) of this privatization episode, the government initiated a process of divestiture of the firms controlled by CORFO, the State Development Corporation. CORFO was created in 1939 to support produc- tive activities - through credit and incentives for research and development - and to undertake certain projects considered to be of national interest. CORFO was directly involved in about 50 firms in 1970, but this number had increased to 180 by 1973. The new government declared that it had no intention of retaining control over these firms, and started to transfer them to the private sector through public auctions. A direct

negotiation process was started when the private sector began to make attractive offers.

The speed, timing, sequence, and implementa- tion strategy adopted for the latter phase of this privatization episode contained serious policy mistakes, however. A total of 115 firms and 13 banks were privatized during 1974-76, with a total sales value of US$336 million. In 1975 alone, in the midst of a severe recession, 39 firms and 9 banks were privatized for a total sales value of USS228 million, or 2.6% of GDP. Although only a small downpayment (generally lO-20% of the sale value) was given for these enterprises - the rest being financed with credit extended by CORFO - these sales exerted significant pres- sure on the incipient financial market, explaining at least in part the high real interest rates during this period. This pressure was particularly strong because the firms and farms that had been returned to their previous owners during the first phase of the privatization were heavily decapital- ized, and were also pressing the market for working and investment capital. This was all at a time when the government was pursuing a strongly contractionary policy in order to stabil- ize the economy and cope with the first oil shock. Partly as a result of these pressures, real interest rates averaged 40% per year during 1975-79. In addition, the recession of 1975 probably had a significant depressive effect on the prices of these companies, and thus the government may have received a lower price for them than under more normal conditions. The privatization process was also pursued at a time when the restructuring of the economy - particularly the trade and finan- cial liberalization - had not been completed. The restructuring would induce significant changes in the conditions under which firms operated, and hence affect their profitability. Finally, because the firms were acquired with heavy debts and the screening process on the financial strength and cross-ownership of the prospective buyers was not adequate, privatiza- tion facilitated the concentration of assets into the hands of a few industrial and financial conglomerates with a weak, and hence highly vulnerable, capital base.6

Thus, when the external conditions deterio- rated in the early 1980s and the domestic economy lost strength, a drastic financial crisis emerged that forced massive intervention by the Central Bank. The control of the banks in financial trouble, however, also implied de facto control of all the firms that were heavily indebted to these banks and could not service their debts. Thus, at the end of 1983, the first privatization process had come full circle, with many of the same firms and banks that had been in the hands

STABILIZATION AND STRUCTURAL TRANSFORMATION IN CHILE 497

of the government 10 years before again con- trolled by the state. After a brief transitory period, however, the government started a new privatization effort in 1985 - an ongoing pro- cess.

This new privatization episode has also had two different phases. In the first phase (1985-86). the government tried to return to the private sector those firms that had come under its control due to the financial crisis of 1982-83 -and which constituted the “odd sector” of the economy. This process was mostly complete by mid-1986. The second phase continued with the govern- ment’s attempt to privatize the remaining state enterprises, a process which had been inter- rupted by the crisis of 1982-83. As of mid-1986, these enterprises numbered about 40,2.5 of which were in the hands of CORFO. This second phase started in 1986 and is not yet completed.

During this second privatization episode, the government deliberately diffused property widely and enforced a more careful screening of prospective buyers, emphasizing their finan- cial strength. New financial legislation was also drafted to avoid excessive concentration, but the consolidation of financial data has not been adequately resolved. The diffusion of property has been achieved through several methods, but the one that has attracted the most attention is the system of “popular capitalism.” This system imposes limits on the maximum stock ownership of individual agents, giving credits to enable small investors to participate. It has also involved heavy subsidies, providing tax breaks that favor wealthy individuals. Other forms of divestiture include auctions to a selected group of investors, both domestic and foreign; sales in the stock exchange; sales to institutional investors, domin- ated by private social security corporations; and sales to employees of the companies being privatized.

Although this second privatization episode benefited from the experience of the first privati- zation, three issues remain. First, this new process has not followed a phased and carefully planned program. The government has again proceeded to privatize these firms in a very short period of time, announcing different amounts to be privatized at different stages. Second, the government has not clarified the regulatory framework for the new companies being priva- tized (some of which are natural monopolies), nor the final role that institutional investors will be allowed to play. Both of these issues may have had a negative effect on the prices of the companies being privatized. Third, and perhaps most important for the future, is the issue of how the government will utilize the proceeds from the

sale of these firms. The question here is whether these proceeds will be used to finance current expenditures, in which case their net effect on government finances is likely to be negative. or be used to finance new investment, particularly in infrastructure and human capital (Larrain, 1988).

(b) The trade liberalization process

The trade liberalization process was a key component of the government’s attempt to im- pose market discipline. The economic authorities argued that opening up the economy would force domestic firms to specialize in the production of those goods and services in which the country had comparative advantage, thus improving eco- nomic efficiency. This result followed from com- parative static considerations in an economy with fixed resource endowments. Moreover, the accu- mulated evidence from past experiences with trade restrictions (Little, Scitovsky and Scott, 1970; Bhagwati, 1978; Krueger, 1977) tended to underscore the economic advantages and per- formance of countries following outward- oriented policies - most notably those in East Asia, which continue to enjoy a remarkable performance even today. Thus, from both theoretical and practical considerations, a deci- sion was made relatively early to open up the economy to external trade and capital flows.

The opening of the economy was pursued sequentially. First, the trade account was opened while external capital flows remained restricted. A set of low and uniform tariffs (set at lo%, with minor exceptions) and a unique exchange rate were imposed, and all nontariff barriers were eliminated. This process started in 1974 and was mostly complete by mid-1979. Then, external capital flows were liberalized by deregulating progressively long-term flows - eliminating global limits on borrowing in 1979 and restric- tions on monthly inflows in 1980 - and finally liberalizing short-term flows in 1981.

As a result, the country did achieve a substan- tial rise in exports, particularly nontraditional ones. Imports, however, grew much faster than exports after the first recession (1976-79), and they grew at even higher rates in 1980-81 when the exchange rate was fixed and capital inflows liberalized. After the recession of 1982-83 and the associated cutback in foreign lending, the government partly reversed its previous trade policies, but later reestablished an open trading environment.

In order to rapidly cope with the external imbalance and the loss of international reserves,

198 WORLD DEVELOPMEKT

the government increased tariffs from 10 to 20% in 1983, and added a 15% surtax on 235 import items in March 1984. Finally, in September 1984, the government leveled off import tariffs at 35%. With the introduction of the adjustment program in 1985, however, a new emphasis was given to export incentives and the reduction of trade restrictions. Import tariffs were reduced from 35 to 30% in March 1985, and to 20% in July 1985.’ These measures were complemented with the establishment of a passive crawling peg system (which resulted in a further depreciation of the real effective exchange between 1985 and 1987) and several export incentives. These included (i) the elimination of a stamp tax on exports and of the value-added tax on investment for exports; (ii) the elimination of export credit restrictions and the establishment of a privately-run export credit insurance program; (iii) the introduction of measures to offset the uniform tariffs on the purchase of intermediate inputs and capital goods; (iv) the strengthening of the state’s export development agency, PROCHILE; and (v) the establishment of a pilot copper stabilization fund to smooth out copper revenues when prices deviated from their long-run trend.

The new measures quickly yielded positive results. Merchandise exports increased by 7.9% per year in volume terms during 1984-87, com- pared to an increase of 3.7% per year during 1980-84. Agricultural and industrial exports in- creased even more (by 19 and 15% per year during 1984-86, respectively, compared to 8.4 and 4.2% per year during 198O-84), helped by a favorable exchange rate and other incentives which effectively redressed the mild anti-export bias which prevailed during 1974-81. While no direct evidence is available, there are indications that investments in export-oriented activities - particularly in fruits, forestry, agro-industry, and mining - have increased at a significant pace in the last few years. Imports, on the other hand, increased by 12% per year in volume terms during 1985-87, but after a significant decline in previous years. Thus, at the end of 1987, the volume of merchandise imports was about 30% below the previous peak of 1981. In sum, and mostly as a result of the increase in exports (but partly helped by favorable terms-of-trade de- velopments) the trade surplus increased signifi- cantly, from 1.5% of GDP (or US$O.3 billion) in 1984, to 5.8% (or US$l.l billion) in 1987.

The opening of the economy was undoubtedly an area where important progress was made, although policy biases and inconsistencies may initially have clouded these achievements. The policy mix proved inconsistent, as the govern- ment allowed the exchange rate to appreciate

significantly in the late 1970s - a process which was reinforced by the massive inflows of external capital which followed the opening of the capital account in 1979. A mild anti-export bias was also introduced, as the government initially failed to compensate exporters for the 10% import tariffs. In recent years, however, this bias has been reversed and the exchange rate policy. has clearly benefited exporting and import substituting acti- vities, while the maintenance of an open trading environment has provided competitive pressures and induced increases in economic efficiency.’

(c) The financial liberalization process

The financial liberalization was the final piece of the key set of domestic policies implemented in Chile during the mid-1970s to restructure the economy. Its main objective was to promote domestic savings - a result which aas expected as an immediate consequence of the freeing of interest rates - and to permit an efficient allocation of financial resources to\vard produc- tive investment. While the liberalization of domestic financial markets was implemented quite rapidly and was mostly complete by 1977, external financial flows remained restricted until mid-1979. These restrictions were subsequently eliminated, however, as I have already noted.

A major shortcoming of the financial liberali- zation process was the excessively permissive legislation. which left banking practices unreg- ulated in an environment where assets were heavily concentrated in the hands of highly leveraged financial conglomerates. These condi- tions permitted continued bank lending to risky projects and - during the early 1980s - to insolvent firms associated with the same groups that owned the banks. Three main problems resulted. First, the available credit was channeled to unprofitable but affiliated firms. and hence less credit was available to profitable but inde- pendent firms (Galvez and Tybout, 1985). Second, the prevailing conditions encouraged an “adverse selection process,” which attracted high-risk borrowers who could temporarily afford the high real interest rates, driving low- risk, low-return activities out of the market. Finally, de facto deposit insurance - provided by the bailout of financial institutions prior to the crisis - gave incentives for undue risk taking (Corbo and de Melo, 1987).

The implementation of the financial liberaliza- tion process made possible large capital inflows, but did not increase savings and investment. In just three years, from 1978 to 1981. Chile’s total external debt increased from USS7.0 billion to

STABILIZATION AND STRUCTURAL TRANSFORMATION IN CHILE 499

US$15.6 billion, and most of this debt was not guaranteed by the public sector. By 1981.65% of Chile’s total long-term debt was private and without government guarantee, compared to 27% in 1978. Despite these large inflows, invest- ment remained depressed. As a proportion of GDP, fixed investment (at constant prices) in- creased from 14.6% during 1974-78 to 17.6% during 1979-81, but was still below the level of 19.2% achieved during 1966-70. These low investment rates were early indications that the growth process of the late 1970s and early 1980s was unsustainable (Foxley. 1982).

Part of the poor investment performance can be explained by the high real interest rates during this period, but this does not explain the poor savings behavior. Private savings averaged 3.1% of GDP during 1979-81. compared to 7.9% in 1970. Although the increase in real asset prices during 1979-81 may partly explain the poor savings performance - since an increase in perceived wealth decreases the stimulus to save more - private savings remained exceedingly low.

After the economic and financial crisis of 1982-83, the government designed a program to rehabilitate the corporate and financial sectors. This program was important to the economic recovery, but entailed heavy losses which will take many years to absorb. The Central Bank intervention and the various subsidy schemes it introduced allowed many banks and firms to continue operating - although many others were liquidated - thus avoiding complete bankruptcy with devastating economic consequences. But the losses so far have been enormous. Estimates of these losses average over 6% of GDP during 1983-84, and 11% during 1985-86 - for an accumulated total of USS6.0 billion.’ Moreover, these estimates omit the losses incurred by the State Bank (Bunco de1 Emdo), which absorbed the debts of two banks - BUF and BHC - which had faced intervention. These debts were valued at USS360 million (Larrain, 1988). Losses for 1987 and beyond are expected to be substan- tially lower than the amounts involved in pre- vious years - as most of the subsidy schemes have been phased out - but they depend to a significant extent on the continued economic recovery.

Finally, it is important to note recent develop- ments in external debt instruments in Chile. The financial rehabilitation package introduced in 1985 was complemented with an innovative debt conversion program. Two different debt conver- sion mechanisms were introduced. The first, regulated under Chapter 18 of the Central Bank’s Rules on International Exchange, permits con-

version of Chilean external debt instruments into domestic debt certificates. This mechanism is open to both residents and nonresidents and may be used for any purpose; the certificates may be sold in the domestic capital market. The second, regulated under Chapter 19. permits conversion of external debt instruments into domestic debt certificates to be used for equity investment, and is only open to foreign investors. The external debt certificates are bought at a discount in the international secondary market, but are recog- nized at near par value in Chile. The external discounts fluctuated between 3@-35% between 1985 and mid-1987, but increased to 1M5% in the second half of 1987 after a significant increase in the supply of these certificates.

The debt conversion program proved useful in restricting the growth of Chile’s external debt, but its benefits have been limited. At the end of 1987, Chile had retired US$2.2 billion in princi- pal through the use of Chapters 18 and 19.‘” Slightly more than half of this amount (US$1.2 billion) was retired through Chapter IS. which does not carry remittance rights. There are basically two benefits under this scheme: (i) interest payments associated with the reduction in principal are consequently eliminated (in this case the total reduction in interest payments amounts to USSllO million); and (ii) part of the external discount is appropriated by the Central Bank (in this case averaging 15% during 1985- 87, or about half of the discount prevailing in international secondary markets) through licens- ing the right to participate in these operations (Ffrench-Davis, 1987). The remaining portion of the principal retired during 1985-87 (a total of US$l.O billion) made use of Chapter 19. The benefits Chile obtained under this plan may have been even smaller than under the previous scheme, because the reduction in interest pay- ments may be compensated by future profit remittances, and because the external discount is now shared between foreign investors, who effectively receive a preferential exchange rate, and commercial banks who act as intermediaries.

Two other potential benefits of the debt conversion mechanisms need to be mentioned. First, both conversion mechanisms helped slow the expansion of Chile’s external debt, improving the debt ratios and positively affecting Chile’s creditworthiness. Second, the Chapter 19 scheme has permitted an increase in the flow of foreign funds to Chile, most of which have been used in the reprivatization of firms discussed above. This increase, however, has been partly offset by a reduction in foreign direct investment. from an average of USS220 million per year in 1980-84 to US$60 million in 1985-86.

500 WORLD DEVELOPMENT

5. CONCLUSIONS

Five main lessons emerge from the analysis of this paper.

major private losses. It may also be advisable to control the extent of foreign indebtedness, which ultimately affects the entire country’s credit- worthiness - not just that of the borrowers.

First, rigid orthodoxy in economics - particu- larly as applied to policy making in less devel- oped countries - is most likely destined to produce poor economic results. Although the recent experience of Chile may be quite special in that it highlights the results obtained from ap- plying one version of monetarism, it is doubtful whether any other orthodoxy - applied with the same dogmatism - would have produced much better results. In sum, economists still have much to learn about the functioning of real economies, and about the impact of economic policies on economic behavior and performance. This sug- gests a cautious approach, and one of very pragmatic and highly selective government inter- vention when there are clear signs that action is required.

Second, the verdict about the adequate speed, intensity, and sequence of the stabilization efforts and structural transformation attempts is not yet clear. While consideration of the costs of adjusting to the new policy regime would favor a more gradual approach, the credibility of the new set of policies seems to be greater when there is a big policy change, favoring a sudden approach (or “shock treatment”). What is clear, however, is that adjustment costs and lags in economic behavior should be recognized in economic policy decisions, and adequately taken into consideration.

Fourth, although external developments played a negative role in Chile’s economic performance during 1973-87, domestic policy mistakes and the inability of the government to act quickly when the conditions clearly warranted it amplified the negative effects - particularly during 1973-85. As a result, the performance of the economy deteriorated drastically, both in comparison with Chile’s own history and with the average performance of developing countries during the same period. Moreover, the distribu- tion of income and wealth became more regres- sive. By the end of 1987, and as a result of low investment rates, the heavy debt burden, con- tinued political polarization, and the delayed effects of a marked increase in unemployment and recent cutbacks in health and education pro- grams, the future of the economy seemed uncer- tain and vulnerable to external shocks.

Third, it is not obvious from Chile’s experience that the private sector, unregulated, will be much more efficient than the public sector.” An effective monitoring procedure should therefore be established to avoid major crises affecting the whole economy, and to protect the government, and ultimately the taxpayer, from absorbing

Finally, and despite the heavy economic and social costs, the economic program implemented in Chile has had several positive achievements. Among these, the opening of the economy to international trade - i.e., the introduction of a relatively undistorted set of trade policies - must be considered an important step forward, even though its initial implementation lacked consistency. In addition, the government’s con- trol of the budget deficit and of inflation, and the elimination of domestic price controls are also positive achievements. One can hope that these positive features will be maintained, while new and complementary efforts will be made to address the shortcomings of the past, so that Chile’s experience of the last 14 years will prove valuable for its future economic devel- opment.

NOTES

1. Note that the severity of the deflationary package imposed in 1975 was also motivated by negative external events - declining terms of trade and export volumes - that Chile suffered as a result of the first oil shock.

2. The real effective exchange rate appreciated by 37% between 1979 and 1981. according to IMF figures.

3. Real minimum wages declined even more; see Arellano (1988), Table 3.

4. Several studies have analyzed the links between recent external shocks and economic performance in

LDCs (see, e.g., Balassa and McCarthy, 1984). They invariably conclude that there is no correlation between the magnitude of the external shocks and indicators of economic performance. Thus, domestic policy responses and the characteristics of the countries (e.g., level of development, degree of openness) are para- mount in “explaining” these links. A more detailed study about Chile has suggested that external events played a minor role in the country’s poor economic performance during the early 198Os, in comparison with the shocks it suffered during the mid-1970s (Balassa. 1985).

5. Studies attempting to analyze the links between

STABILIZATION AND STRUCTURAL TRANSFORMATION IN CHILE 501

deteriorating social indicators and economic growth have faced two formidable problems. First, the avail- able evidence is scarce and rather weak. Second. the lags involved may be very long indeed. Yet, neither of these should be a cause of contempt (see Helleiner. 1986, and the references cited therein). Note also that short-term losses can, in principle, be covered by borrowing - but “market failures” are likely to become patently clear during drastic recessions.

6. See Marshall and Montt (1987) and Larrain (1988) for a more detailed description of Chile’s privatization process.

7. A new tariff reduction - to 15% -was instituted in January 1988.

8. See Corbo. de Melo, and Tybout (1988) for recent evidence on the efficiency gains of the trade liberaliza- tion in Chile.

9. See Moran (1988), Table 2. I am grateful to E. Barandiaran for providing me with these figures.

10. These amounts exclude USSO. billion of capital entered under Decree Law 600. which regulates foreign direct investment, and other operations (such as partial write offs or direct buy backs’of private‘unguaranteed foreign debt) for about US$O.8 billion.

11. In fact, if the comparison is limited to the banking sector, the Chilean experience of 1974-85 suggests the opposite to be true. It would be unwise to generalize from this experience, however.

REFERENCES

Arellano, J. P., “La situation social en Chile,” Notas Tecnicas No. 94 (Santiago, Chile: CIEPLAN, June 1988).

Balassa, B., “Policy experiments in Chile, 1973-83,” in G. M. Walton (Ed.). The National Economic Poli- ties of Chile (Greenwich, CT: Jai Press, 1985). pp. 203-238.

Balassa, B., and D. McCarthy, “Adjustment policies in developing countries, 1979-82,” World Bank Staff Working Paper No. 675 (Washington, DC: World Bank, April 1984).

Bhagwati, J., Foreign Trade Regimes and Economic Development: Anatomy and Consequences of Ex- change Control Regimes (Cambridge, MA: Ballinger, 1978).

Corbo, V., J. de Melo, and J. Tybout, “The effects of trade policy on scale and technical efficiencv: New evidence from Chile,” processed (Washington, DC: World Bank, Trade Policv Division. Mav 1988).

Corbo, V., and J. de Melo, “Lessons from the Southern Cone policy reforms,” The World Bank Research Observer, Vol. 2, No. 2 (July 1987). pp. 111-142.

Diaz-Alejandro, C., “Southern Cone stabilization plans,” in W. Cline, and S. Weintraub (Eds.), Economc Stabilization in Developing Countries (Washington, DC: The Brookings Institution, 1981). pp. 119-146.

Edwards, S., and A. Cox-Edwards, Monetarism and Liberalization, the Chilean Experiment (Cambridge, MA: Ballinger, 1987).

Foxley, A., “Towards a free market economy,” Journal of Development Economics, Vol. 10, No. 1 (February 1982). pp. 3-29.

Ffrench-Davis, R., “Conversion de pagares de la deuda externa en Chile,” Coleccion Estudios CIEPLAN, No. 22 (December 1987). pp. 41-62.

Helleiner, G., “Balance-of-payments experience and growth prospects of developing countries: A syn- thesis.” World Development, Vol. 14, No. 8 (August 1986). pp. 877-908.

Galvez, J., and J. Tybout, “Microeconomic adjustment in Chile during 1977-81: The importance of being a grupo,” World Development, Vol. 13, No. 8 (August 1985). pp. 969-994.

Krueger, A., “Growth, distortions, and patterns of trade among many countries,” Princeton Studies in International Finance, No. 40 (Princeton, NJ: Inter- national Finance Section. 1977).

Larrain, F., -‘Public sector behavior in a highly indebted country: The contrasting Chilean experi- ence 197&85,” processed (Washington, DC: World Bank, January 1988).

Little, I., T. Scitovsky, and M. Scott, Industry and Trade in Some Developing Countries. A Comparative Study (London: Oxford University Press, 1970).

Marshall, J., and F. Montt, “Privatization in Chile,” processed (Washington, DC: World Bank, March 1987).

Meller, P., “Una reflexion critica en torno al modelo economico Chileno,” Coleccion Estudios CIEPLAN, No. 10 (June 1983), pp. 125-136.

Moran, C., “Chile in the 1980s: Crisis and recovery,” Background Country Study for the Adjustment Lending Policy Paper (Washington, DC: World Bank, Trade Policy Division, April 1988).

Pollack, IM., and A. Uthoff, “Pobreza y mercado de trabajo en el Gran Santiago: 1969-85,” Esrudios de Economia, Vol. 14, No. 1 (May 1987). pp. 141-191.

Torche, A., “Distribuir el ingreso para satisfacer las necesidades basicas,” in F. Larrain (Ed.), Desarrollo Economico en Democracia (Santiago, Chile: Edit. U. Catolica de Chile, 1988).

World Bank, “Poverty in LatinAmerica: The impact of depression,” World Bank Report (Washington, DC: World Bank, September 1986).

Zahler, R., “The monetary and real effects of the financial opening up of national economies to the exterior. The case of Chile, 197>78,” in Latin America: International Monetary System and External Financing, Project UNDP/ECLAC RLA/ 771021 (Santiago, Chile: Economic Commission for

502 WORLD DEVELOPLLIENT

Latin America, 1986a). pp. 195-226. System and External Financing, Project UNDPI Zahler, R.. “Recent Southern Cone liberalization ECLAC RLA/77/021 (Santiago, Chile: Economic

reform and stabilization policies. The Chilean case. Commission for Latin America, 1986b). pp. 301- 197182,” in Latin America: International Monetary 336.