Embed Size (px)

Citation preview

ECONOMIC RESEARCH · ENGLISH EDITION FEBRUARY 2004

Nordic OutlookJobless growth: Causes and consequences

Important your attention is drawn to the statement on the back cover of this report which affects your rights.

SEB Economic ResearchNordic Outlook - February 2004

This report was published on February 10, 2004.

Cut-off date for calculations and forecasts was February 4, 2004.

Klas Eklund, Chief Economist +46 8 763 [email protected]

Håkan Frisén, Head of Economic Research [email protected]

Bo Enegren, Economist [email protected]

Ann Enshagen Lavebrink, Research Assistant [email protected]

Ingela Georgii-Hemming, EU Coordinator [email protected]

Olle Holmgren, Economist [email protected]

Mikael Johansson, Economist [email protected]

Fax no. +46 8 763 9300

Contributions to the sections on Germany and Norway in this report have been made by Thomas Köbel fromSEB Frankfurt/M and Tharald Stray Laastad from Trading Strategy, Merchant Banking.

SEB, Economic Research, K A3, SE-106 40 STOCKHOLM

Important: This statement affects your rights

This report is produced for institutional investors (being, in the United Kingdom, persons who fall within Article 9 (3) of the Financial Services Act 1986 (Invest-ment Advertisements) (Exemptions) Order 1988 or other persons to whom this document may lawfully be issued or passed on). This report is produced for privateinformation of recipients and neither Skandinaviska Enskilda Banken AB (publ) (the Bank) nor any identified third party data supplier (“Data Supplier(s)”) aresoliciting any action based upon it. Opinions contained in this research report represent the Bank’s present opinion only and are subject to change without notice.All information contained in this report has been compiled in good faith from sources believed to be reliable. However, no representation or warranty, express orimplied, is made with respect to the completeness or accuracy of the contents by the Bank or any Data Supplier and it is not to be relied upon as authoritative.Recipients are urged to base their investment decisions upon such investigations as they deem necessary. The Bank does not provide legal or tax advice, and whilethe Bank believes the information contained herein to be reliable, it is not intended to be and should not be construed as a legal or tax advice. To the extent permittedby applicable law, no liability whatsoever is accepted by the Bank) or any Data Supplier for any direct or consequential loss arising from use of this document or itscontents. Your attention is drawn to the fact that a member of, or any entity associated with, the Bank or its affiliates, officers, directors, employees or shareholdersof such members may from time to time have a long or short position in, or otherwise participate in the markets for, the securities and the currencies of countriesmentioned herein.

Skandinaviska Enskilda Banken AB (publ) is incorporated in Stockholm Sweden with limited liability and is a member of the Stockholm Stock Exchange.

Skandinaviska Enskilda Banken AB (publ) which is registered in England and Wales No. BR000979 is regulated by The Securities and Futures Authority and is amember of the London Stock Exchange.

Transactions involving debt securities will be executed by or with the Bank unless you are informed otherwise at the time of dealing.

Confidentiality Notice

This report is confidential and may not be reproduced or redistributed to any person other than its recipient from the Bank.

Skandinaviska Enskilda Banken AB (publ), 2004. All rights reserved.

2

SummaryNordic Outlook – February 2004

3

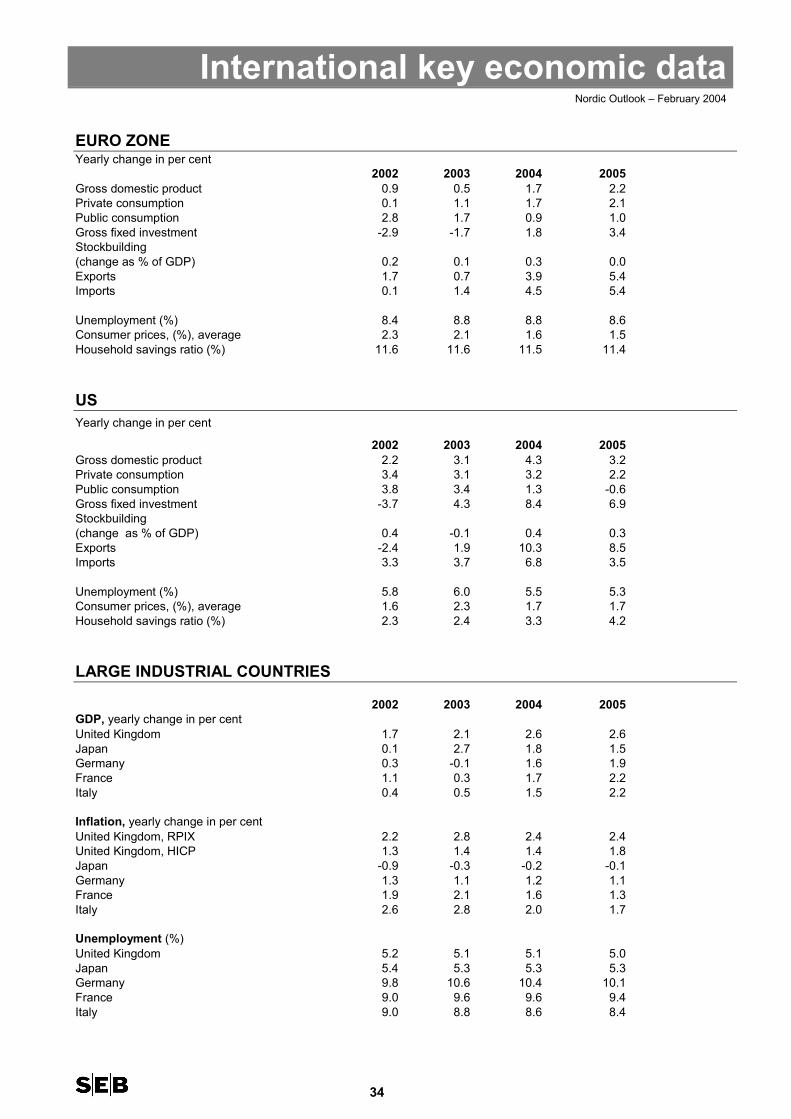

SummaryThe International Economy� The world economy is in a recovery phase. In the US, GDP will grow more than 4 per cent this year but more

slowly in 2005, when fiscal policy is tightened and interest rates will rise.

� The upturn will generate fewer jobs than usual, due to structurally higher productivity growth. Unemploymentwill thus remain relatively high and inflation low. The Fed can proceed slowly with its interest rate hikes and willwait until this autumn for the first one.

� Growth will decelerate somewhat in both Japan and China this year. Japan will continue its foreign exchangeinterventions but the yen will appreciate anyway. China will switch from a US dollar peg to a currency basket,but without drama or foreign exchange turbulence.

� Euro zone recovery will be sluggish, with GDP growth of 1.7 per cent this year. The strong euro will hamperexports. Domestic demand will grow only slowly. The ECB can keep its refi rate unchanged until late autumn.EU enlargement will have little impact during 2004-05.

� Bond yields will remain unchanged this spring and only creep upward slowly, beginning in the autumn. Joblessgrowth and low inflation are the reasons. Asian central banks will continue pumping capital into the US andhelping to hold down interest rates in the West.

� The dollar will weaken to USD 1.30 per euro this spring. As fiscal policy tightening approaches, the Fed beginshiking interest rates and the current account deficit stops growing, the dollar will stabilise. During 2005, it willstrengthen towards USD 1.20 per euro.

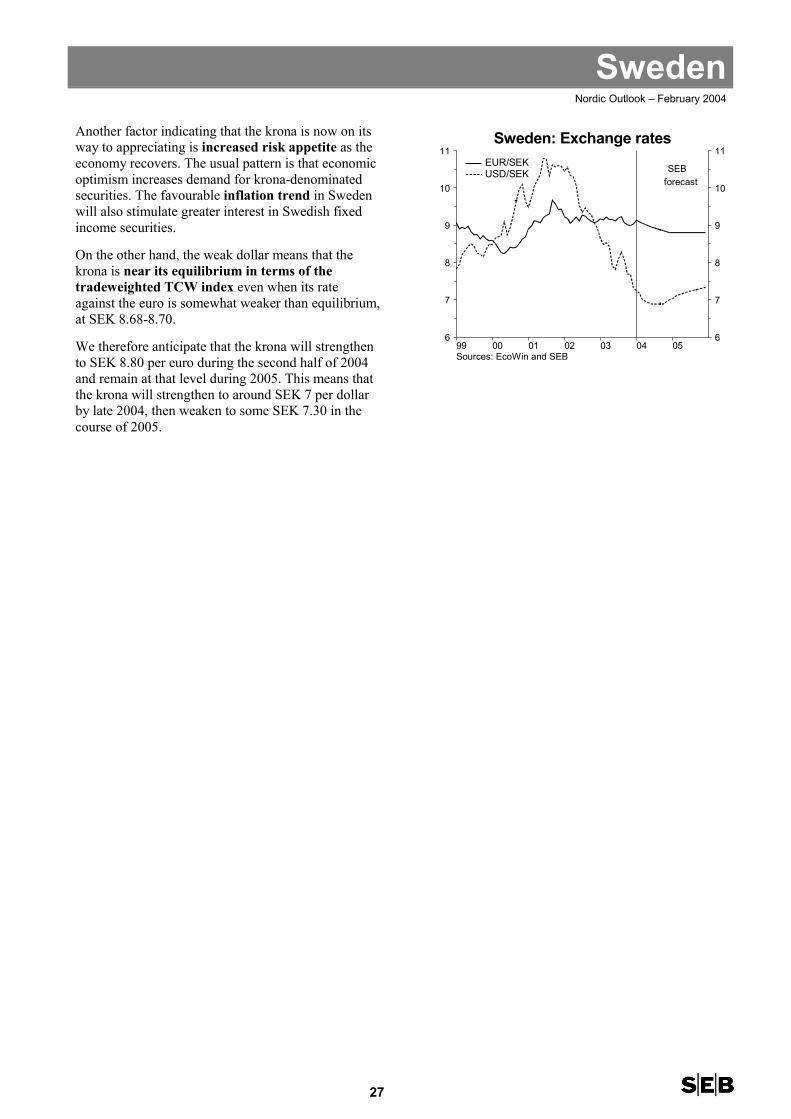

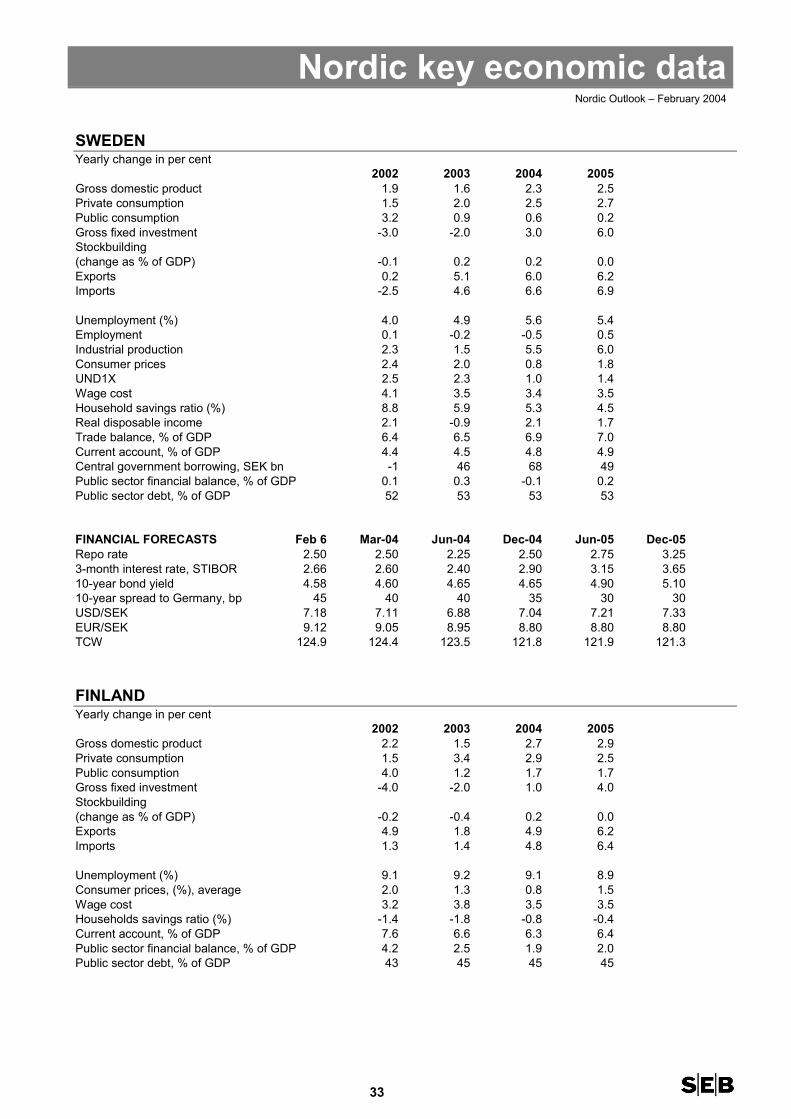

Sweden� Growth will accelerate to 2.3 per cent this year and 2.5 per cent in 2005. Due to a stronger world market and

good productivity, exports will perform decently despite the strong krona. Households will reduce their savingsand keep consumption up, in spite of tax hikes.

� In Sweden, too, higher growth will go hand in hand with weak employment. The reasons are rapidly risingproductivity in the business sector and local government financial problems.

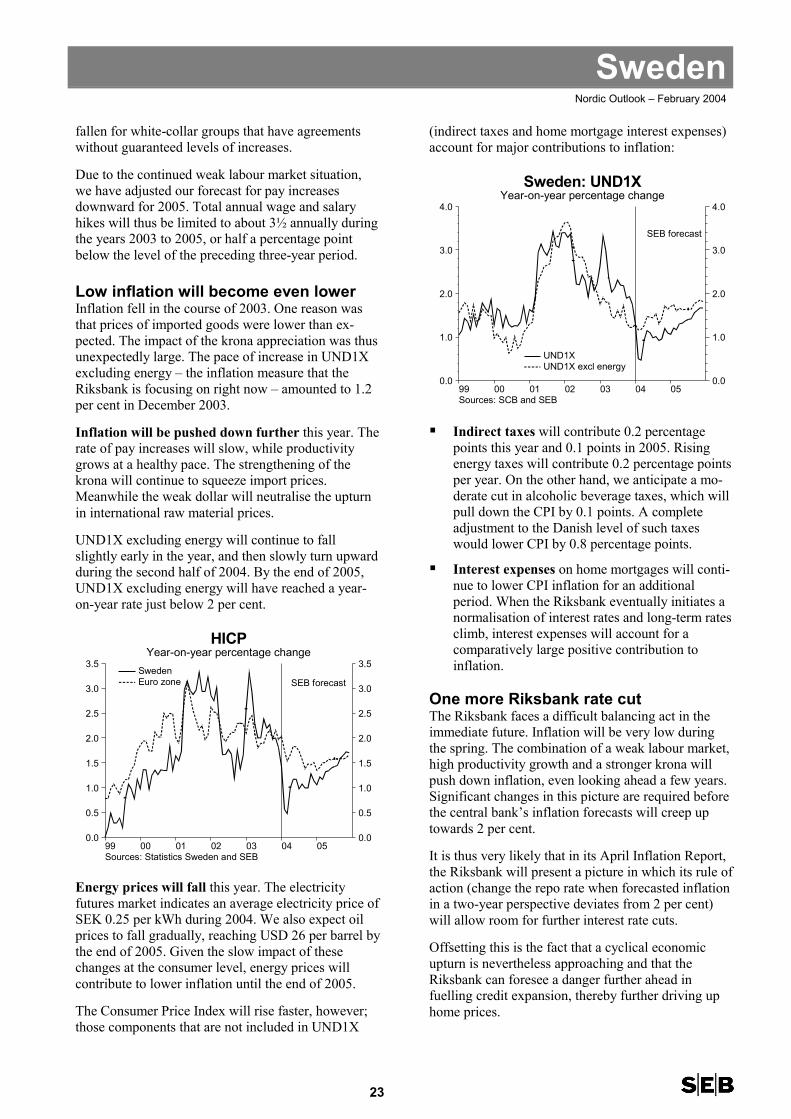

� The wage round will see clashes about distributive principles but lead to modest pay hikes. Inflation will be verylow. Underlying inflation excluding energy will not reach 2 per cent annually over the next couple of years. TheRiksbank will cut the repo rate by another 25 basis points in April. Its rate hike cycle will begin late this year.

� The local government crisis will deepen. Public sector budget targets will not be met, and methods forcircumventing budget expenditure ceilings will become more devious.

� The government’s growth policy will achieve no breakthrough. A desire to preserve its parliamentary alliancewith the Left and Green Parties, while placating internal Social Democratic opinion, will prevent it from takingany major initiatives in taxation policy.

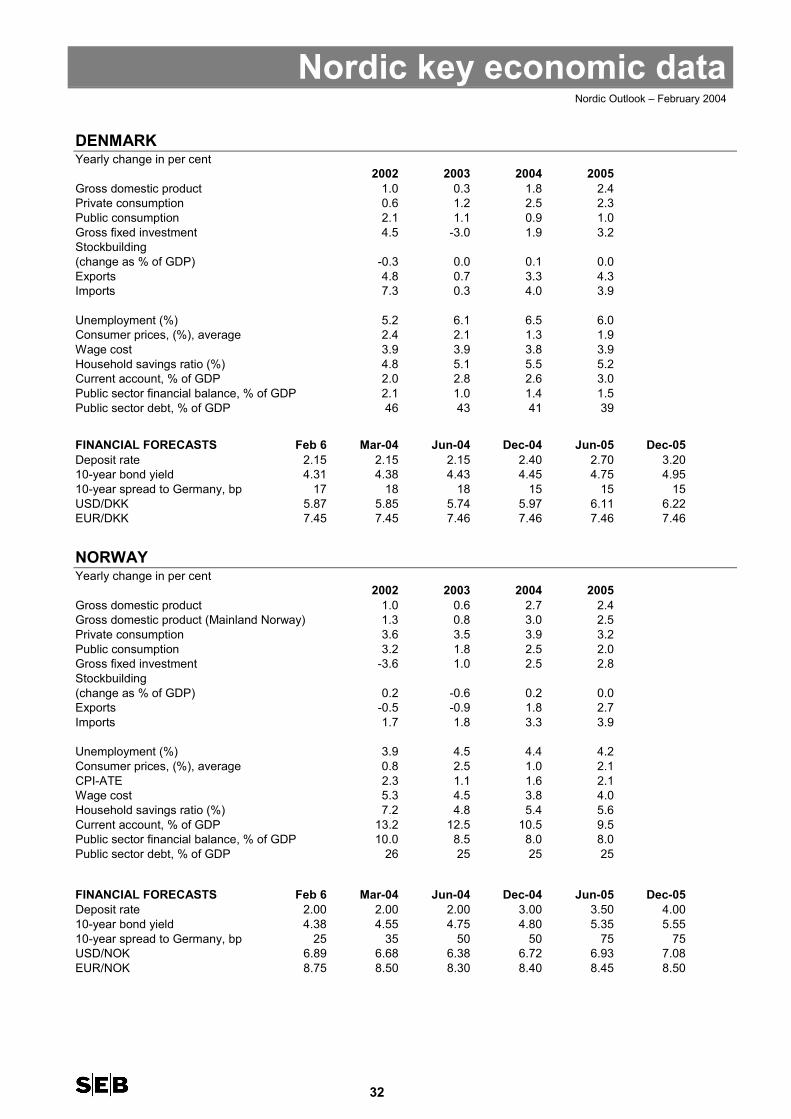

Other Nordic countries� Denmark’s GDP growth will quicken to 1.8 per cent this year with the help of private consumption, while

inflation will fall. The country’s current account surplus will prop up the krone and allow it to maintain a narrowinterest rate margin over the euro zone.

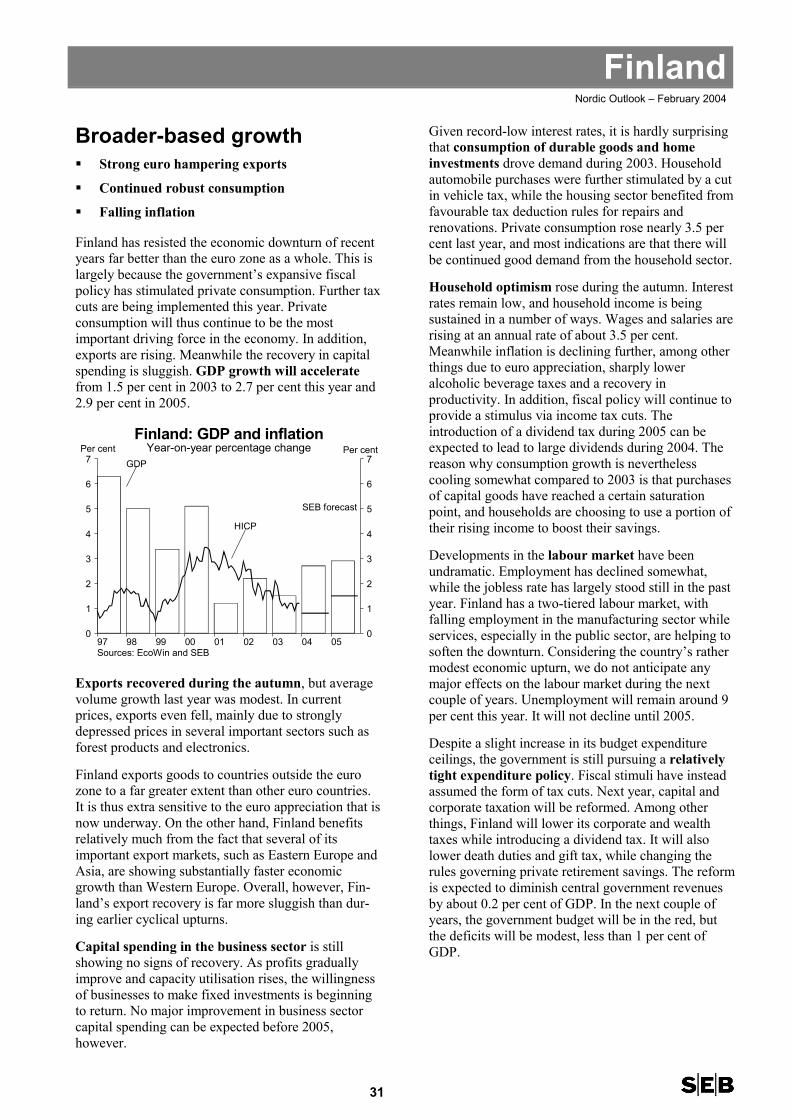

� In Finland, GDP growth will accelerate to 2.7 per cent this year, with private consumption as its main engine.The strong euro will lead to a comparatively sluggish export recovery and falling inflation. Capital and corporatetaxation will be reformed.

� Monetary policy shock therapy is yielding results in Norway. Growth will rise to 2.7 per cent this year, thanks tocapital spending in the oil sector and growing private consumption. Underlying inflation will bottom out thissummer and then climb a bit. Norges Bank will raise its key interest rate during the second half of 2004, and thekrone will strengthen somewhat.

ContentsNordic Outlook – February 2004

4

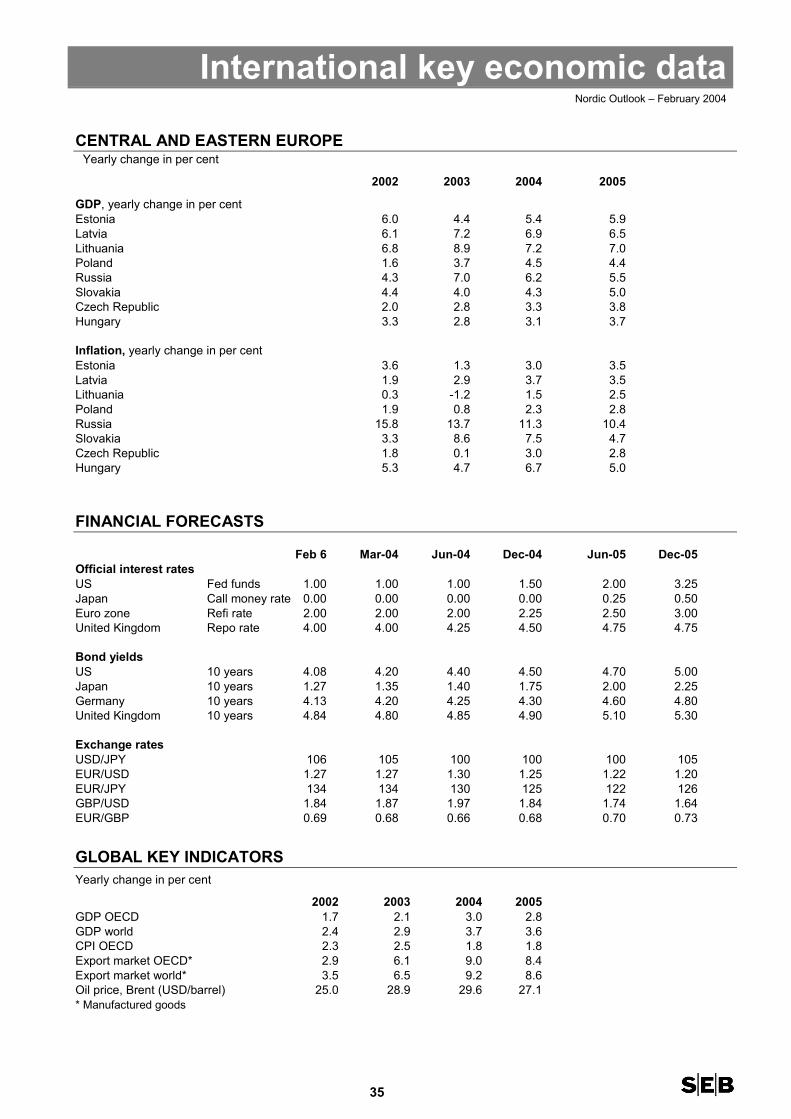

Summary 3International overview 5The United States 6China and Japan 9The euro zone 11The United Kingdom 14Central and Eastern Europe 15International financial markets 16Sweden 19Denmark 28Norway 29Finland 31Nordic key economic data 32International key economic data 34

Boxes

The United States: Jobless growth – for how long? 7Chinese bank and currency reforms 9The euro zone: Stability Pact headed to court 12The euro zone: Enlargement will have small short-term growth impetus 13Sweden: Moderate recovery in the telecom sector 20Sweden: Revised income growth curve 21Sweden: The moment of truth for public finances 25

International overviewNordic Outlook – February 2004

5

Still in the shadow of thebubble� Faster growth – but where are the jobs?

� Continued low interest rates

� Dollar slide hampering the rest of the world

The world economy is now undergoing a perceptiblerecovery, led by the United States. This upturn is dif-ferent from normal cyclical recoveries, however, dueto unusually weak employment and low inflation onthe one hand and major fiscal imbalances in the US onthe other. Although real-term growth hasconsolidated, the world economy is thus stillstruggling with the aftermath of the burst stock marketand capital spending bubble.

Extremely low key interest rates and large tax cutshave stimulated the American economy. But so far,growth has been based on rapid productivityimprovement without new employment. The “neweconomy” has proved more robust than many hadthought. Companies are slimming down andcostcutting, ousourcing jobs to low-cost countries,while placing new technology in service on a largescale. Despite the rapid increase in real GDP, capacityutilisation is thus low compared to potential GDP.

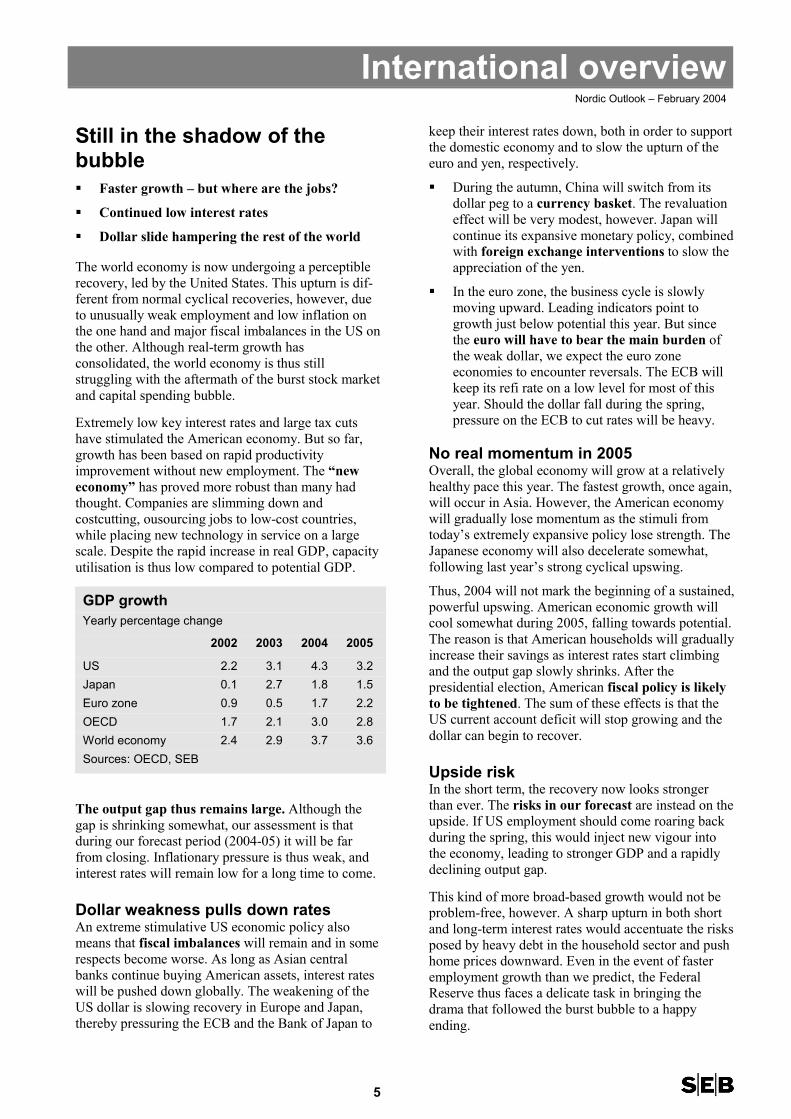

GDP growthYearly percentage change

2002 2003 2004 2005

US 2.2 3.1 4.3 3.2Japan 0.1 2.7 1.8 1.5Euro zone 0.9 0.5 1.7 2.2OECD 1.7 2.1 3.0 2.8World economy 2.4 2.9 3.7 3.6Sources: OECD, SEB

The output gap thus remains large. Although thegap is shrinking somewhat, our assessment is thatduring our forecast period (2004-05) it will be farfrom closing. Inflationary pressure is thus weak, andinterest rates will remain low for a long time to come.

Dollar weakness pulls down ratesAn extreme stimulative US economic policy alsomeans that fiscal imbalances will remain and in somerespects become worse. As long as Asian centralbanks continue buying American assets, interest rateswill be pushed down globally. The weakening of theUS dollar is slowing recovery in Europe and Japan,thereby pressuring the ECB and the Bank of Japan to

keep their interest rates down, both in order to supportthe domestic economy and to slow the upturn of theeuro and yen, respectively.

� During the autumn, China will switch from itsdollar peg to a currency basket. The revaluationeffect will be very modest, however. Japan willcontinue its expansive monetary policy, combinedwith foreign exchange interventions to slow theappreciation of the yen.

� In the euro zone, the business cycle is slowlymoving upward. Leading indicators point togrowth just below potential this year. But sincethe euro will have to bear the main burden ofthe weak dollar, we expect the euro zoneeconomies to encounter reversals. The ECB willkeep its refi rate on a low level for most of thisyear. Should the dollar fall during the spring,pressure on the ECB to cut rates will be heavy.

No real momentum in 2005Overall, the global economy will grow at a relativelyhealthy pace this year. The fastest growth, once again,will occur in Asia. However, the American economywill gradually lose momentum as the stimuli fromtoday’s extremely expansive policy lose strength. TheJapanese economy will also decelerate somewhat,following last year’s strong cyclical upswing.

Thus, 2004 will not mark the beginning of a sustained,powerful upswing. American economic growth willcool somewhat during 2005, falling towards potential.The reason is that American households will graduallyincrease their savings as interest rates start climbingand the output gap slowly shrinks. After thepresidential election, American fiscal policy is likelyto be tightened. The sum of these effects is that theUS current account deficit will stop growing and thedollar can begin to recover.

Upside riskIn the short term, the recovery now looks strongerthan ever. The risks in our forecast are instead on theupside. If US employment should come roaring backduring the spring, this would inject new vigour intothe economy, leading to stronger GDP and a rapidlydeclining output gap.

This kind of more broad-based growth would not beproblem-free, however. A sharp upturn in both shortand long-term interest rates would accentuate the risksposed by heavy debt in the household sector and pushhome prices downward. Even in the event of fasteremployment growth than we predict, the FederalReserve thus faces a delicate task in bringing thedrama that followed the burst bubble to a happyending.

The United StatesNordic Outlook – February 2004

6

Rolling the imbalances over� The forces of growth have been strengthened…

� …at the expense of sustained twin deficits

� Continued spare capacity and low inflation

The American economy is driven by a growingnumber of expansive forces. A weaker dollar, lowerlongterm interest rates and narrowing credit spreadshave reinforced the stimulus of low key interest ratesand large tax cuts. For these reasons, the economy isgrowing at a rapid clip. GDP growth of more than 8per cent (on an annualised basis) in the third quarter of2003 was followed by 4 per cent in the fourth quarter.Growth will remain high during the next sixmonths, then slow as economic policy becomes lessexpansive and households become more cautious.

GDP growth will average 4.3 per cent this year and3.2 per cent next year, implying an upward revision ofour forecast by ½ of one percentage point in bothyears.

2005200420032002200120001999

10

8

6

4

2

0

-2

10

8

6

4

2

0

-2

Sources: EcoWin, SEB

US: Gross domestic productPer cent

forecastSEB

Year-on-year changeAnnualised change

But even if US growth is relatively strong, importantimbalances remain, such as low household savingsand deficits in the federal budget and current account.Meanwhile growth has so far not led to a clearimprovement in the labour market situation.

Crucial to future developments will be how the labourmarket responds to continued growth, as well as howeconomic policy deals with the deficits.

Capital spending has taken overSignificant improvement in the profit situation has ledto a revival of capital spending activity. The corporatesector has thus taken over the role of economiclocomotive from the household sector. Due to theweakening of the dollar, net exports are now alsomaking a positive contribution to growth.

In the short term, consumption trends are largelycontrolled by the timing of federal tax cuts. These cutswere sizeable in the third quarter of 2003, but morerestrained in the fourth. During the first half of 2004there will be a new wave of disbursements, with acertain emphasis on the second quarter. This is oneimportant reason why GDP will continue to growfaster than its potential rate during the first half.

Post-election austerityDuring 2005 the economy will decelerate, due to thebeginnings of fiscal austerity. This is in line with thehistorical pattern. According to the OECD, atightening equivalent to ½-1 per cent of GDP hasoccurred during all post-election years since 1970,with the exception of 2001, a year marked byrecession and terrorism.

This time, however, the realignment of fiscal policymay be less emphatic. Despite setbacks for thepresident in recent opinion polls, in this forecast wehave assumed that George W. Bush will be reelectedfor another term of office and that his strongideological focus on low taxes will continue. On theexpenditure side, certain cuts may indeed occur, butthey will hardly be especially farreaching. The inertiaof the congressional process will also ensure that suchcuts will not have a major impact as early as 2005.

Overall, US public finances have deteriorated byabout 8 per cent of GDP since 2000. Less than half ofthis is attributable to the cyclical downturn, whereasthe rest is due to political decisions − mainly intaxation and defence policy. The cyclical recoveryduring our forecast period will improve the budget byone per cent of GDP or so, at the most. The budgetdeficit will thus remain large over the next couple ofyears.

If the Democrats should strengthen their positionmarkedly in the election, this picture may change. Taxincreases may then lead to more severe belttighteningand to faster deceleration in economic growth.

Continued current account deficitThe large US current account deficit will also persistover the next couple of years. There are two principalfactors behind this:

▪ Expansive economic policy is continuing torestrain household savings. Due to low interestrates, households are continuing to consume andto borrow on the security of their homes. Theupturn in household savings will thus be modest.Corporate savings are instead on their way

The United StatesNordic Outlook – February 2004

7

Jobless growth – for how long?To date, the labour market has reacted on only a smallscale to vigorous US economic growth. In a historicalperspective, this trend is exceptional, both in terms ofthe productivity surge and the long period that haselapsed without the recovery generating new jobs.

New structures will prevail…The question is whether this is merely a temporarydeviation. Will employment soon take off again in thetraditional cyclical way, or are there more profoundchanges behind the low employment level?

We believe that structural factors are of greatimportance. There are several reasons whyproductivity is continuing to grow strongly:

� The “new economy” has led to a shift intechnology. New technology is affecting largeportions of the economy, through greateruserfriendliness and lower IT costs.

� Deregulation in many industries and increasinglytough competition are other important explanations.

� Keener competition is forcing companies toimprove efficiency and relocate less productivemanufacturing operations. “Offshoring” hasbecome an important factor not only inmanufacturing but also in parts of the service sector.

Our conclusion is consequently that productivity willcontinue to climb rapidly during 2004 and 2005 andthat this will hamper job creation.

...but the upturn will create new jobs later However, it is unlikely that strong US growth willgenerate no new jobs at all. A number of signalsindicate that the labour market is on its way towardsbecoming stronger. Employment will grow − albeit witha certain time lag and a weaker tradeoff. The crucialquestions are how strong the upturn will be and howmuch the economy can tolerate without triggering

inflationary forces. Our analysis of both issues leads toencouraging news from an inflation perspective.

Employment has declined by about 2½ million peoplesince the beginning of 2001. Meanwhile many indi-viduals have left the labour market. The underlyingincrease in the labour force is about 1 per centannually. Between the cyclical peak early in 2001 andthe end of our forecast period, the underlyingAmerican labour force should thus have climbed by4-5 per cent, or by 6-7 million people. Altogether, wecould thus argue that an employment increase of 8-9million people will signify that capacity utilisation isback at the same level as during the cyclical peak.

However, this overestimates potential expansion fortwo reasons: Firstly, because there was significantoverheating at the end of the cyclical peak. Secondly,because the long period of weakness in the labourmarket will leave its mark on the labour supply bycausing a certain number of people to withdraw fromthe labour market permanently.

Thus our conclusion is that an employment increase of5-6 million people by the end of 2005 is what the USeconomy needs in order to return to equilibrium andfull capacity utilisation. This is equivalent to an in-crease of about 200-250,000 people per month.

However, such a lasting and quick upturn is highlyunlikely. Our forecast implies that employment will beat its most expansive during the second and thirdquarters of 2004. When GDP growth later cools, inresponse to tighter economic policy conditions, jobgrowth will also slow.

Overall, this forecast means that employment will growby about 3 million people over the next couple ofyears. For this reason, the output gap − thedifference between actual and potential GDP level −will remain considerable, despite rapid GDP growth.This, in turn, will result in continued low inflation.

Year-on-year percentage changeUS: GDP and employment

GDP (LHS) Employment (RHS)Source: EcoWin

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03-3

-2

-1

0

1

2

3

4

5

6

7

8

9

-3

-2

-1

0

1

2

3

4

5

05040302010099

136

134

132

130

128

126

136

134

132

130

128

126

Sources: Bureau of Labor Statistics and SEB

US: EmploymentMillions

Employment (non-farm payroll)Return to normal capacity utilisationForecastTrend

The United StatesNordic Outlook – February 2004

8

downward, since a renewed inclination toundertake capital spending is overshadowingcompanies’ rising profits.

▪ The dollar slide is having only a limited impacton trade. It will require very large exchange rateshifts to turn around trade flows, in order tostrengthen the US current account in a situationwhere the American economy is growing twice asfast as those of Western Europe and Japan. Thisbecomes clear if we consider that Americanexports are only equivalent to about 10 per cent ofGDP and imports 15 per cent. Achieving balancedtrade would thus require a 50 per cent increase inexports. The modest weakening of the dollar thatwe foresee is not sufficient to achieve this.

It thus seems likely that the next couple of years willbe characterised by continued twin deficit problems.In the short term, this is not necessarily a major worry.Longer term, however, issues related to debt levelsand the sustainability of economic trends will becomeincreasingly pivotal.

USD bnUS: Public finance and current account

Federal surplus/deficit Current accountSource: EcoWin

92 93 94 95 96 97 98 99 00 01 02 03

-600

-500

-400

-300

-200

-100

0

100

200

300

-600

-500

-400

-300

-200

-100

0

100

200

300

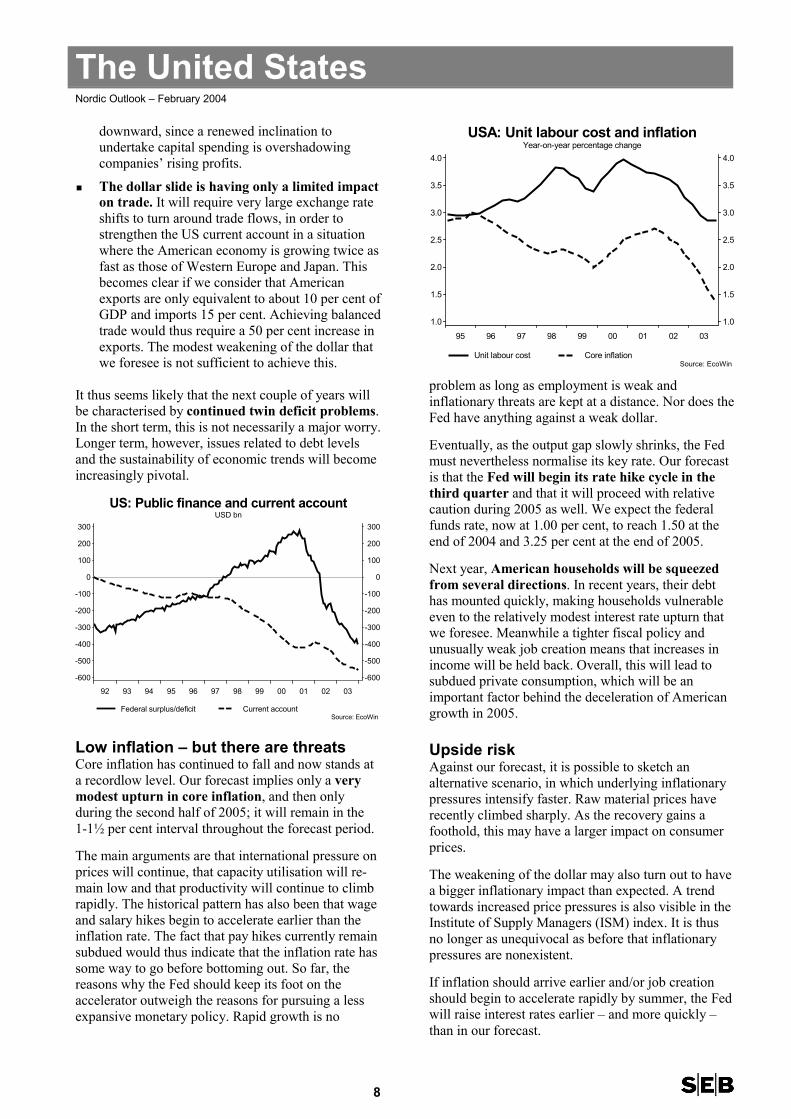

Low inflation – but there are threatsCore inflation has continued to fall and now stands ata recordlow level. Our forecast implies only a verymodest upturn in core inflation, and then onlyduring the second half of 2005; it will remain in the1-1½ per cent interval throughout the forecast period.

The main arguments are that international pressure onprices will continue, that capacity utilisation will re-main low and that productivity will continue to climbrapidly. The historical pattern has also been that wageand salary hikes begin to accelerate earlier than theinflation rate. The fact that pay hikes currently remainsubdued would thus indicate that the inflation rate hassome way to go before bottoming out. So far, thereasons why the Fed should keep its foot on theaccelerator outweigh the reasons for pursuing a lessexpansive monetary policy. Rapid growth is no

Year-on-year percentage changeUSA: Unit labour cost and inflation

Unit labour cost Core inflationSource: EcoWin

95 96 97 98 99 00 01 02 03

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

problem as long as employment is weak andinflationary threats are kept at a distance. Nor does theFed have anything against a weak dollar.

Eventually, as the output gap slowly shrinks, the Fedmust nevertheless normalise its key rate. Our forecastis that the Fed will begin its rate hike cycle in thethird quarter and that it will proceed with relativecaution during 2005 as well. We expect the federalfunds rate, now at 1.00 per cent, to reach 1.50 at theend of 2004 and 3.25 per cent at the end of 2005.

Next year, American households will be squeezedfrom several directions. In recent years, their debthas mounted quickly, making households vulnerableeven to the relatively modest interest rate upturn thatwe foresee. Meanwhile a tighter fiscal policy andunusually weak job creation means that increases inincome will be held back. Overall, this will lead tosubdued private consumption, which will be animportant factor behind the deceleration of Americangrowth in 2005.

Upside riskAgainst our forecast, it is possible to sketch analternative scenario, in which underlying inflationarypressures intensify faster. Raw material prices haverecently climbed sharply. As the recovery gains afoothold, this may have a larger impact on consumerprices.

The weakening of the dollar may also turn out to havea bigger inflationary impact than expected. A trendtowards increased price pressures is also visible in theInstitute of Supply Managers (ISM) index. It is thusno longer as unequivocal as before that inflationarypressures are nonexistent.

If inflation should arrive earlier and/or job creationshould begin to accelerate rapidly by summer, the Fedwill raise interest rates earlier – and more quickly –than in our forecast.

China and JapanNordic Outlook – February 2004

9

China’s cautious deceleration� Japan and China resist currency appreciation

� Somewhat slower expansion in 2004…

� …but Asia still fastest-growing in the world

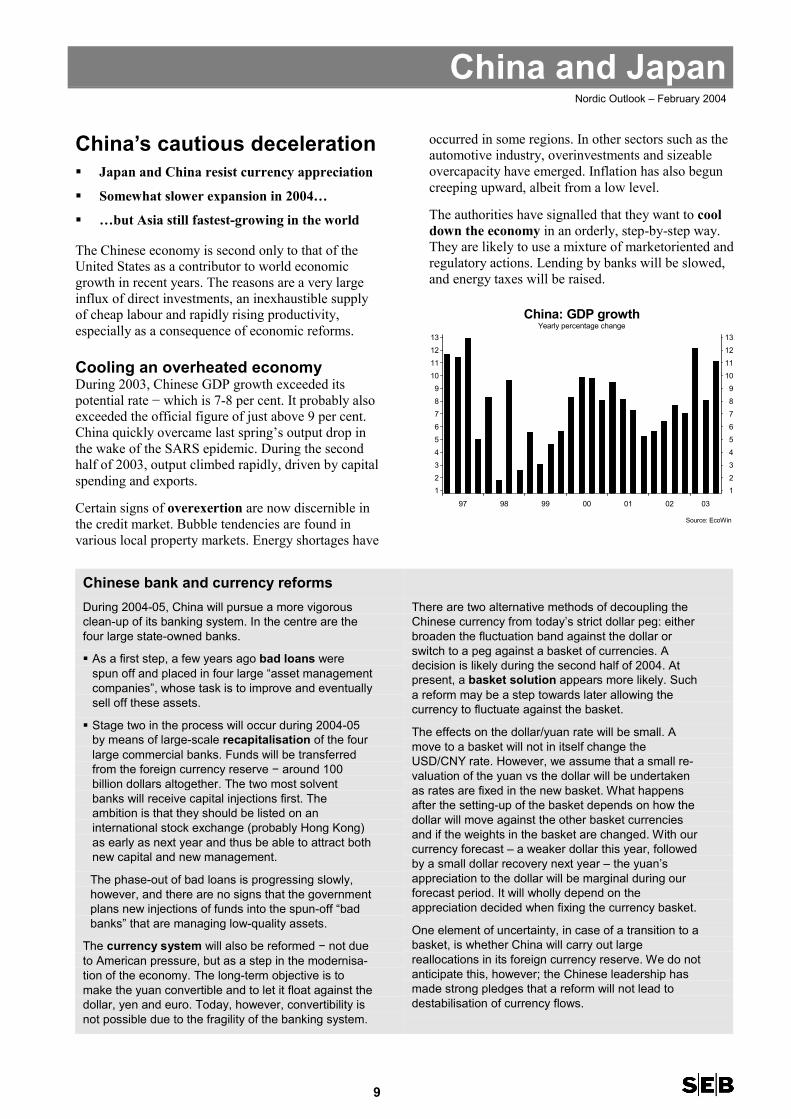

The Chinese economy is second only to that of theUnited States as a contributor to world economicgrowth in recent years. The reasons are a very largeinflux of direct investments, an inexhaustible supplyof cheap labour and rapidly rising productivity,especially as a consequence of economic reforms.

Cooling an overheated economyDuring 2003, Chinese GDP growth exceeded itspotential rate − which is 7-8 per cent. It probably alsoexceeded the official figure of just above 9 per cent.China quickly overcame last spring’s output drop inthe wake of the SARS epidemic. During the secondhalf of 2003, output climbed rapidly, driven by capitalspending and exports.

Certain signs of overexertion are now discernible inthe credit market. Bubble tendencies are found invarious local property markets. Energy shortages have

occurred in some regions. In other sectors such as theautomotive industry, overinvestments and sizeableovercapacity have emerged. Inflation has also beguncreeping upward, albeit from a low level.

The authorities have signalled that they want to cooldown the economy in an orderly, step-by-step way.They are likely to use a mixture of marketoriented andregulatory actions. Lending by banks will be slowed,and energy taxes will be raised.

Yearly percentage changeChina: GDP growth

Source: EcoWin

97 98 99 00 01 02 03

123456789

10111213

123456789

10111213

Chinese bank and currency reformsDuring 2004-05, China will pursue a more vigorousclean-up of its banking system. In the centre are thefour large state-owned banks.

� As a first step, a few years ago bad loans werespun off and placed in four large “asset managementcompanies”, whose task is to improve and eventuallysell off these assets.

� Stage two in the process will occur during 2004-05by means of large-scale recapitalisation of the fourlarge commercial banks. Funds will be transferredfrom the foreign currency reserve − around 100billion dollars altogether. The two most solventbanks will receive capital injections first. Theambition is that they should be listed on aninternational stock exchange (probably Hong Kong)as early as next year and thus be able to attract bothnew capital and new management.

The phase-out of bad loans is progressing slowly,however, and there are no signs that the governmentplans new injections of funds into the spun-off “badbanks” that are managing low-quality assets.

The currency system will also be reformed − not dueto American pressure, but as a step in the modernisa-tion of the economy. The long-term objective is tomake the yuan convertible and to let it float against thedollar, yen and euro. Today, however, convertibility isnot possible due to the fragility of the banking system.

There are two alternative methods of decoupling theChinese currency from today’s strict dollar peg: eitherbroaden the fluctuation band against the dollar orswitch to a peg against a basket of currencies. Adecision is likely during the second half of 2004. Atpresent, a basket solution appears more likely. Sucha reform may be a step towards later allowing thecurrency to fluctuate against the basket.

The effects on the dollar/yuan rate will be small. Amove to a basket will not in itself change theUSD/CNY rate. However, we assume that a small re-valuation of the yuan vs the dollar will be undertakenas rates are fixed in the new basket. What happensafter the setting-up of the basket depends on how thedollar will move against the other basket currenciesand if the weights in the basket are changed. With ourcurrency forecast – a weaker dollar this year, followedby a small dollar recovery next year – the yuan’sappreciation to the dollar will be marginal during ourforecast period. It will wholly depend on theappreciation decided when fixing the currency basket.

One element of uncertainty, in case of a transition to abasket, is whether China will carry out largereallocations in its foreign currency reserve. We do notanticipate this, however; the Chinese leadership hasmade strong pledges that a reform will not lead todestabilisation of currency flows.

China and JapanNordic Outlook – February 2004

10

These actions will slow the GDP growth rate to itspotential during 2004. China’s trade expansion willcontinue, however, and even after this modest coolingprocess the growth rate will be around 7 per cent.

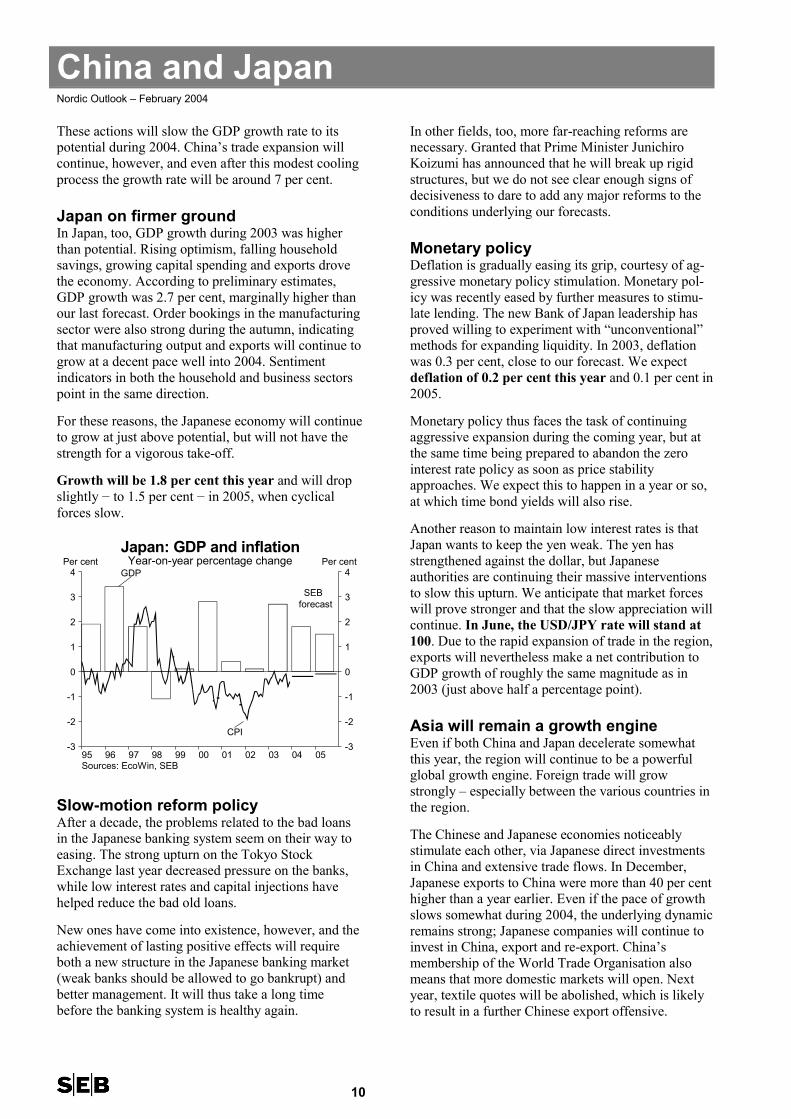

Japan on firmer groundIn Japan, too, GDP growth during 2003 was higherthan potential. Rising optimism, falling householdsavings, growing capital spending and exports drovethe economy. According to preliminary estimates,GDP growth was 2.7 per cent, marginally higher thanour last forecast. Order bookings in the manufacturingsector were also strong during the autumn, indicatingthat manufacturing output and exports will continue togrow at a decent pace well into 2004. Sentimentindicators in both the household and business sectorspoint in the same direction.

For these reasons, the Japanese economy will continueto grow at just above potential, but will not have thestrength for a vigorous take-off.

Growth will be 1.8 per cent this year and will dropslightly − to 1.5 per cent − in 2005, when cyclicalforces slow.

0504030201009998979695

4

3

2

1

0

-1

-2

-3

4

3

2

1

0

-1

-2

-3

Sources: EcoWin, SEB

Japan: GDP and inflationYear-on-year percentage changePer cent Per cent

GDP

CPI

SEB forecast

Slow-motion reform policyAfter a decade, the problems related to the bad loansin the Japanese banking system seem on their way toeasing. The strong upturn on the Tokyo StockExchange last year decreased pressure on the banks,while low interest rates and capital injections havehelped reduce the bad old loans.

New ones have come into existence, however, and theachievement of lasting positive effects will requireboth a new structure in the Japanese banking market(weak banks should be allowed to go bankrupt) andbetter management. It will thus take a long timebefore the banking system is healthy again.

In other fields, too, more far-reaching reforms arenecessary. Granted that Prime Minister JunichiroKoizumi has announced that he will break up rigidstructures, but we do not see clear enough signs ofdecisiveness to dare to add any major reforms to theconditions underlying our forecasts.

Monetary policyDeflation is gradually easing its grip, courtesy of ag-gressive monetary policy stimulation. Monetary pol-icy was recently eased by further measures to stimu-late lending. The new Bank of Japan leadership hasproved willing to experiment with “unconventional”methods for expanding liquidity. In 2003, deflationwas 0.3 per cent, close to our forecast. We expectdeflation of 0.2 per cent this year and 0.1 per cent in2005.

Monetary policy thus faces the task of continuingaggressive expansion during the coming year, but atthe same time being prepared to abandon the zerointerest rate policy as soon as price stabilityapproaches. We expect this to happen in a year or so,at which time bond yields will also rise.

Another reason to maintain low interest rates is thatJapan wants to keep the yen weak. The yen hasstrengthened against the dollar, but Japaneseauthorities are continuing their massive interventionsto slow this upturn. We anticipate that market forceswill prove stronger and that the slow appreciation willcontinue. In June, the USD/JPY rate will stand at100. Due to the rapid expansion of trade in the region,exports will nevertheless make a net contribution toGDP growth of roughly the same magnitude as in2003 (just above half a percentage point).

Asia will remain a growth engineEven if both China and Japan decelerate somewhatthis year, the region will continue to be a powerfulglobal growth engine. Foreign trade will growstrongly – especially between the various countries inthe region.

The Chinese and Japanese economies noticeablystimulate each other, via Japanese direct investmentsin China and extensive trade flows. In December,Japanese exports to China were more than 40 per centhigher than a year earlier. Even if the pace of growthslows somewhat during 2004, the underlying dynamicremains strong; Japanese companies will continue toinvest in China, export and re-export. China’smembership of the World Trade Organisation alsomeans that more domestic markets will open. Nextyear, textile quotes will be abolished, which is likelyto result in a further Chinese export offensive.

The euro zoneNordic Outlook – February 2004

11

The weak link� Stronger euro slowing the recovery

� Inflation will fall towards 1½ per cent

� EU enlargement: little short-term impact

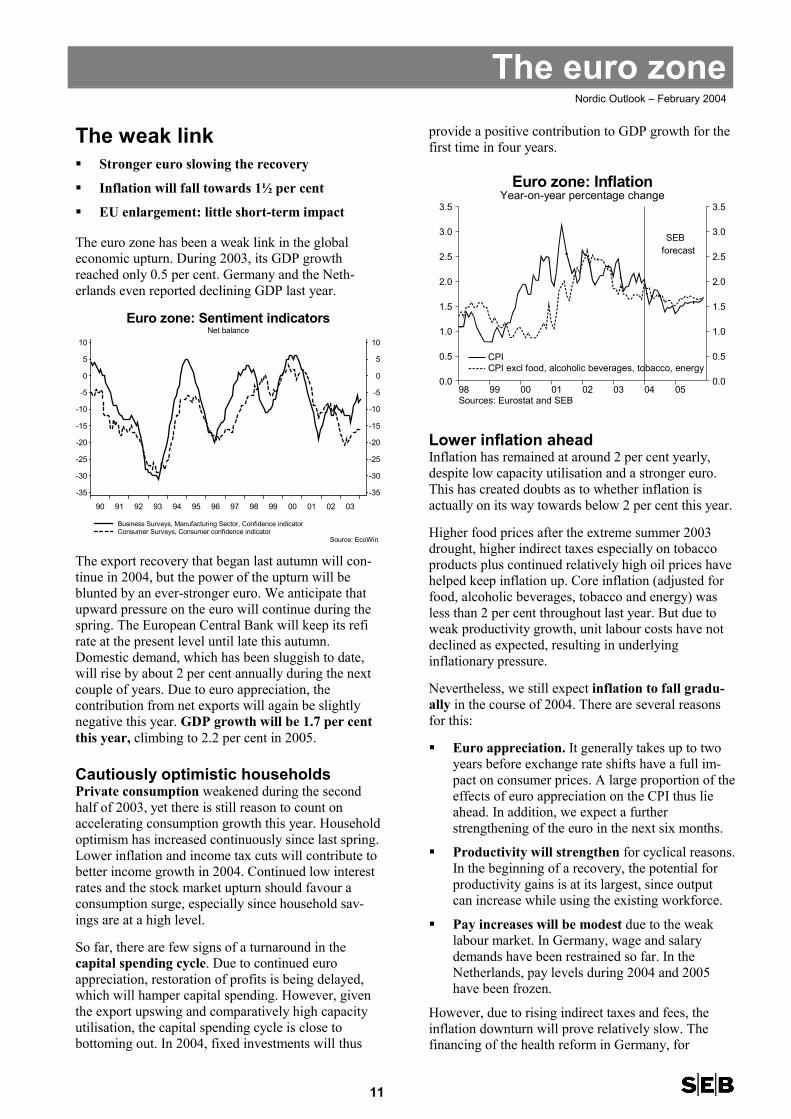

The euro zone has been a weak link in the globaleconomic upturn. During 2003, its GDP growthreached only 0.5 per cent. Germany and the Neth-erlands even reported declining GDP last year.

Net balanceEuro zone: Sentiment indicators

Business Surveys, Manufacturing Sector, Confidence indicator Consumer Surveys, Consumer confidence indicator

Source: EcoWin

90 91 92 93 94 95 96 97 98 99 00 01 02 03

-35

-30

-25

-20

-15

-10

-5

0

5

10

-35

-30

-25

-20

-15

-10

-5

0

5

10

The export recovery that began last autumn will con-tinue in 2004, but the power of the upturn will beblunted by an ever-stronger euro. We anticipate thatupward pressure on the euro will continue during thespring. The European Central Bank will keep its refirate at the present level until late this autumn.Domestic demand, which has been sluggish to date,will rise by about 2 per cent annually during the nextcouple of years. Due to euro appreciation, thecontribution from net exports will again be slightlynegative this year. GDP growth will be 1.7 per centthis year, climbing to 2.2 per cent in 2005.

Cautiously optimistic householdsPrivate consumption weakened during the secondhalf of 2003, yet there is still reason to count onaccelerating consumption growth this year. Householdoptimism has increased continuously since last spring.Lower inflation and income tax cuts will contribute tobetter income growth in 2004. Continued low interestrates and the stock market upturn should favour aconsumption surge, especially since household sav-ings are at a high level.

So far, there are few signs of a turnaround in thecapital spending cycle. Due to continued euroappreciation, restoration of profits is being delayed,which will hamper capital spending. However, giventhe export upswing and comparatively high capacityutilisation, the capital spending cycle is close tobottoming out. In 2004, fixed investments will thus

provide a positive contribution to GDP growth for thefirst time in four years.

0504030201009998

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Sources: Eurostat and SEB

Euro zone: InflationYear-on-year percentage change

forecastSEB

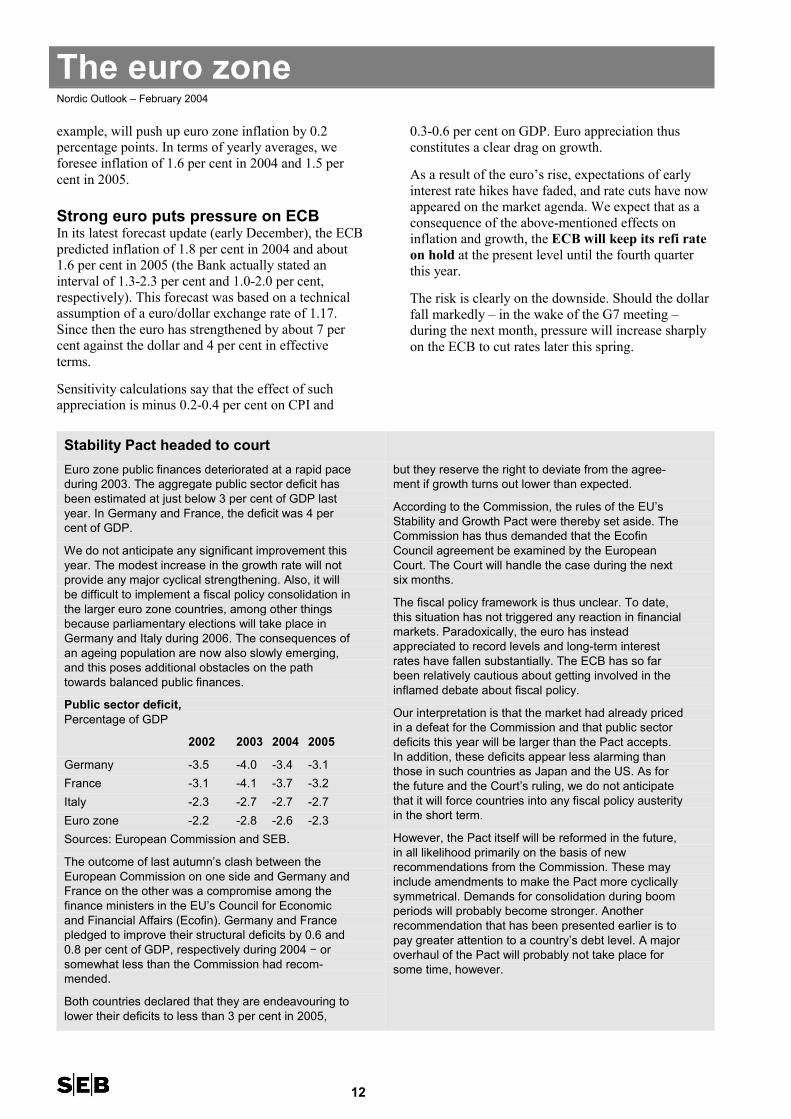

CPICPI excl food, alcoholic beverages, tobacco, energy

Lower inflation aheadInflation has remained at around 2 per cent yearly,despite low capacity utilisation and a stronger euro.This has created doubts as to whether inflation isactually on its way towards below 2 per cent this year.

Higher food prices after the extreme summer 2003drought, higher indirect taxes especially on tobaccoproducts plus continued relatively high oil prices havehelped keep inflation up. Core inflation (adjusted forfood, alcoholic beverages, tobacco and energy) wasless than 2 per cent throughout last year. But due toweak productivity growth, unit labour costs have notdeclined as expected, resulting in underlyinginflationary pressure.

Nevertheless, we still expect inflation to fall gradu-ally in the course of 2004. There are several reasonsfor this:

� Euro appreciation. It generally takes up to twoyears before exchange rate shifts have a full im-pact on consumer prices. A large proportion of theeffects of euro appreciation on the CPI thus lieahead. In addition, we expect a furtherstrengthening of the euro in the next six months.

� Productivity will strengthen for cyclical reasons.In the beginning of a recovery, the potential forproductivity gains is at its largest, since outputcan increase while using the existing workforce.

� Pay increases will be modest due to the weaklabour market. In Germany, wage and salarydemands have been restrained so far. In theNetherlands, pay levels during 2004 and 2005have been frozen.

However, due to rising indirect taxes and fees, theinflation downturn will prove relatively slow. Thefinancing of the health reform in Germany, for

The euro zoneNordic Outlook – February 2004

12

example, will push up euro zone inflation by 0.2percentage points. In terms of yearly averages, weforesee inflation of 1.6 per cent in 2004 and 1.5 percent in 2005.

Strong euro puts pressure on ECBIn its latest forecast update (early December), the ECBpredicted inflation of 1.8 per cent in 2004 and about1.6 per cent in 2005 (the Bank actually stated aninterval of 1.3-2.3 per cent and 1.0-2.0 per cent,respectively). This forecast was based on a technicalassumption of a euro/dollar exchange rate of 1.17.Since then the euro has strengthened by about 7 percent against the dollar and 4 per cent in effectiveterms.

Sensitivity calculations say that the effect of suchappreciation is minus 0.2-0.4 per cent on CPI and

0.3-0.6 per cent on GDP. Euro appreciation thusconstitutes a clear drag on growth.

As a result of the euro’s rise, expectations of earlyinterest rate hikes have faded, and rate cuts have nowappeared on the market agenda. We expect that as aconsequence of the above-mentioned effects oninflation and growth, the ECB will keep its refi rateon hold at the present level until the fourth quarterthis year.

The risk is clearly on the downside. Should the dollarfall markedly – in the wake of the G7 meeting –during the next month, pressure will increase sharplyon the ECB to cut rates later this spring.

Stability Pact headed to courtEuro zone public finances deteriorated at a rapid paceduring 2003. The aggregate public sector deficit hasbeen estimated at just below 3 per cent of GDP lastyear. In Germany and France, the deficit was 4 percent of GDP.

We do not anticipate any significant improvement thisyear. The modest increase in the growth rate will notprovide any major cyclical strengthening. Also, it willbe difficult to implement a fiscal policy consolidation inthe larger euro zone countries, among other thingsbecause parliamentary elections will take place inGermany and Italy during 2006. The consequences ofan ageing population are now also slowly emerging,and this poses additional obstacles on the pathtowards balanced public finances.

Public sector deficit,Percentage of GDP

2002 2003 2004 2005

Germany -3.5 -4.0 -3.4 -3.1France -3.1 -4.1 -3.7 -3.2Italy -2.3 -2.7 -2.7 -2.7Euro zone -2.2 -2.8 -2.6 -2.3Sources: European Commission and SEB.

The outcome of last autumn’s clash between theEuropean Commission on one side and Germany andFrance on the other was a compromise among thefinance ministers in the EU’s Council for Economicand Financial Affairs (Ecofin). Germany and Francepledged to improve their structural deficits by 0.6 and0.8 per cent of GDP, respectively during 2004 − orsomewhat less than the Commission had recom-mended.

Both countries declared that they are endeavouring tolower their deficits to less than 3 per cent in 2005,

but they reserve the right to deviate from the agree-ment if growth turns out lower than expected.

According to the Commission, the rules of the EU’sStability and Growth Pact were thereby set aside. TheCommission has thus demanded that the EcofinCouncil agreement be examined by the EuropeanCourt. The Court will handle the case during the nextsix months.

The fiscal policy framework is thus unclear. To date,this situation has not triggered any reaction in financialmarkets. Paradoxically, the euro has insteadappreciated to record levels and long-term interestrates have fallen substantially. The ECB has so farbeen relatively cautious about getting involved in theinflamed debate about fiscal policy.

Our interpretation is that the market had already pricedin a defeat for the Commission and that public sectordeficits this year will be larger than the Pact accepts.In addition, these deficits appear less alarming thanthose in such countries as Japan and the US. As forthe future and the Court’s ruling, we do not anticipatethat it will force countries into any fiscal policy austerityin the short term.

However, the Pact itself will be reformed in the future,in all likelihood primarily on the basis of newrecommendations from the Commission. These mayinclude amendments to make the Pact more cyclicallysymmetrical. Demands for consolidation during boomperiods will probably become stronger. Anotherrecommendation that has been presented earlier is topay greater attention to a country’s debt level. A majoroverhaul of the Pact will probably not take place forsome time, however.

The euro zoneNordic Outlook – February 2004

13

Enlargement will have small short-termgrowth impetusOn May 1, the European Union will gain ten newmember countries: Poland, the Czech Republic,Hungary, Slovakia, Slovenia, Lithuania, Cyprus,Latvia, Estonia and Malta. The population of the EUwill increase by 20 per cent, from about 380 to 455million. All these new countries intend to join the eurocurrency union before the end of the decade.Enlargement will undoubtedly have major politicalrepercussions for the EU. However, its short-termeconomic consequences have, to a great extent,already taken place.

The new EU economies are small. Together theyaccount for 5 per cent of the EU’s Gross DomesticProduct. Adjusting for lower price levels in the newcountries, their share is still less than 10 per cent. Keyeconomic figures for the enlarged EU thus do notdiffer especially much from those of the old EU.

Key figures for the EU-15 and EU-25, 2004

Growth Inflation Fiscal balance

EU-15 1.9 1.5 -2.6New countries 4.1 3.6 -5.5EU-25 2.0 1.6 -2.7Source: SEBEnlargement will affect the EU economies primarily viatrade and capital spending when the new membercountries are included in the single market. The labourmarket will also be affected by expected migrationfrom east to west. The free labour market will,however, be implemented only in stages. To theextent that enlargement leads to a faster pace ofstructural reforms in existing EU countries, this mayalso boost potential growth. One example is Austria,where recent reform proposals have been motivatedby sharpened competition from the new memberstates.

Different EU countries will be affected in differingdegrees by enlargement. As a result of enlargement,the distribution of the EU’s structural funds willchange. However, this will occur primarily during theEU’s next budget period, 2007-2013. Enlargement willlead to a lowering of average income level, whichmeans that some of the regions receivingdevelopment funds today will lose subsidies they werepreviously entitled to. This will affect Spain, forexample.

1. Migration. Immigration primarily affects countrieslike Germany and Austria, which until now haveabsorbed about 80 per cent of migration from theformer East bloc. Immigration will not become entirelyfree on May 1, 2004, however. The old EU countrieshave permission to apply transitional rules for up tofive years, in the case of Austria and Germany seven

years. All countries with the exception of the UnitedKingdom and Ireland will make use of these transi-tional rules.

Sizeable income differences between east and westare a major incentive for cross-border movement. Theincome level of the new member countries is 20 percent of the level in the old EU, or 40 per cent takingprice levels into account. On the other hand, mobilityis low within the new member states, despite largeregional differences in living standard. Forecasts offuture migration flows indicate annual emigration in therange of 200,000-300,000 people, or 0.1-0.2 per centof the EU labour force. Migration from the east willthus be far from representing any solution to thedemographic problems of Western Europe. However,low-wage competition may push down pay levels inGermany particularly and exert pressure for continuedlabour market reforms.

2. Trade. The new EU countries have been rapidlyintegrated into trade with other countries. In themid1990s, their foreign trade in proportion to GDP wasabout 35 per cent. By 2002 the figure had risen tomore than 50 per cent. A large share of the growingforeign trade of the new EU countries has been withWestern Europe. Today two thirds of their exports goto the EU. This is equivalent to less than 2 per cent ofEU imports and is twice the level of a decade ago.Some trade-related integration effects remain in thefuture. In the long term, the euro common currencymay also provide economic stimulus. The main foreigntrade integration stage has already taken place,however.

3. Direct investments. In recent years, Central andEastern Europe have attracted sizeable foreign directinvestment. One pattern is that the influx of FDI hasbeen clearly higher in EU candidate countries thanin other former east bloc countries. Meanwhilethere are signs of saturation; last year the influxslowed from 22 to 15 billion dollars. One possibleexplanation is that the privatisation process hasprogressed a long way. Since there has already beenan investment rush, we are not counting on anycontinued surge in investment flows, but insteadgradually slower growth at high absolute levels. Overthe next couple of years, EU funds will help keepinvestment up, especially via infrastructure projects.

Overall, we foresee that enlargement will have littleimpact on growth in the existing EU. A continued trendtowards moving production from west to east may beexpected, however, along with a certain pressure onlabour markets in the West.

The United KingdomNordic Outlook – February 2004

14

Recovery on firmer ground� Exports are rebounding

� Modest rate hikes will cool the housing market

� Budget deficit exceeds 3 per cent of GDP

The recovery in the British economy is gaining anever-firmer foothold. An upturn in exports and capitalspending is broadening growth, which was previouslyconsumption-led. We expect GDP to rise by 2.6 percent, both this year and in 2005. The UK will thusachieve its potential growth rate again, after havingfallen below it for three consecutive years. A modesttightening of monetary policy − which will cool theheated housing and credit markets − will limit growth.

Exports have clearly recovered from a weak start in2003. Lingering positive effects from last year’sweakened pound are fuelling the export sector. Inaddition, the international economic outlook hasbrightened. This promises export increases of 4-5 percent annually in 2004-2005. Corporate capitalspending is also beginning to gain momentum, butsince the investment level is relatively high and manycompanies need to make large pension provisions inthe next few years, growth figures will be modest.

Last year, growth in private consumption slowed from3.5 to 2.5 per cent. Due to rising interest rates, con-sumption growth will remain at this calmer level.Home prices are a key factor affecting the con-sumption trend. During the autumn, the rate ofyearon-year price increases cooled to 15-20 per centfrom 30 per cent early in 2003. A major price slidecannot be ruled out, in light of strongly inflated pricelevels. This would lead to clearly lower consumptiongrowth; a slide in home prices is thus the main threatagainst a balanced recovery.

Unemployment will remain unchanged at its currentlow level. Public sector expansion has sustainedemployment to date, and this year the manufacturingsector will again begin recruiting new employees.

Cautious interest rate hikesThe Bank of England recently carried out its secondrepo rate hike since November, from 3.75 to 4.00 percent. But the BoE has good reasons to hurry slowlyand will content itself with 50 basis points during theremainder of 2004.

� Households are deep in debt and highly sensitiveto interest rates. Rate hikes have a relatively rapidimpact, especially in the UK, where more thanthree fourths of home mortgage loans haveadjustable interest rates.

� Inflation risks are small – aside from the housingmarket. Inflation is creeping up slowly, due to lastyear’s depreciation of the pound as well asincreased economic activity. But wage and salaryincreases will be modest and global price pressurewill remain weak, at least this year.

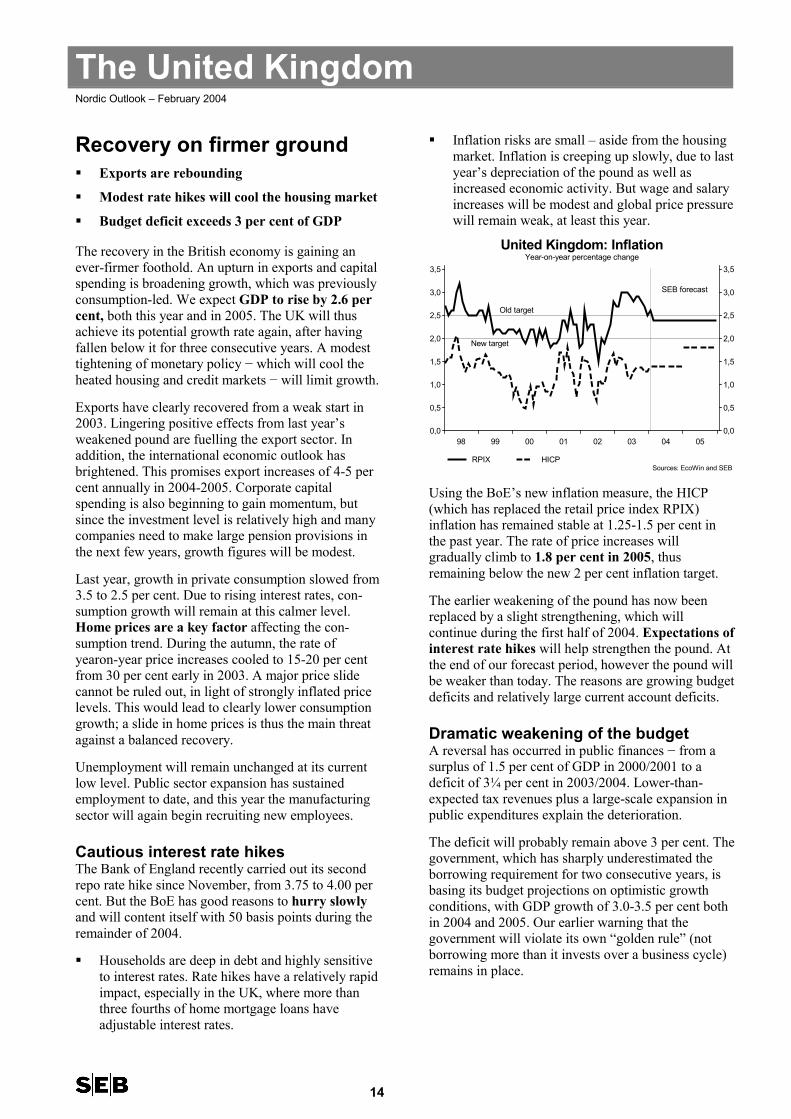

Year-on-year percentage changeUnited Kingdom: Inflation

RPIX HICPSources: EcoWin and SEB

98 99 00 01 02 03 04 050,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

Old target

SEB forecast

New target

Using the BoE’s new inflation measure, the HICP(which has replaced the retail price index RPIX)inflation has remained stable at 1.25-1.5 per cent inthe past year. The rate of price increases willgradually climb to 1.8 per cent in 2005, thusremaining below the new 2 per cent inflation target.

The earlier weakening of the pound has now beenreplaced by a slight strengthening, which willcontinue during the first half of 2004. Expectations ofinterest rate hikes will help strengthen the pound. Atthe end of our forecast period, however the pound willbe weaker than today. The reasons are growing budgetdeficits and relatively large current account deficits.

Dramatic weakening of the budgetA reversal has occurred in public finances − from asurplus of 1.5 per cent of GDP in 2000/2001 to adeficit of 3¼ per cent in 2003/2004. Lower-than-expected tax revenues plus a large-scale expansion inpublic expenditures explain the deterioration.

The deficit will probably remain above 3 per cent. Thegovernment, which has sharply underestimated theborrowing requirement for two consecutive years, isbasing its budget projections on optimistic growthconditions, with GDP growth of 3.0-3.5 per cent bothin 2004 and 2005. Our earlier warning that thegovernment will violate its own “golden rule” (notborrowing more than it invests over a business cycle)remains in place.

Central and Eastern EuropeNordic Outlook – February 2004

15

Good growth − but delaysin joining the euro zone� Exports are recovering

� Inflation is accelerating

� Risk of market instability in Hungary-Poland

Central and Eastern Europe have performed wellduring the economic slowdown in the West. In mostcountries, the growth slump has been mild. Domesticdemand has been fuelled by strong real wageincreases, falling interest rates, expansive fiscal policyand structural transformation.

These positive forces will continue to operate in 2004-2005, although they will diminish in strength. Realwage increases will be high but will slow somewhat.Interest rates will gradually climb, fiscal policy willtighten and the lion’s share of the privatisation processwill have been completed in most places, exceptRussia. On the other hand, exports will grow, drivenby recovering EU economies as well as depreciatingcurrencies in Poland, the Czech Republic and Hun-gary. More export-oriented growth will help easedisturbingly large current account deficits in Estonia,Latvia, the Czech Republic and Hungary.

Inflation will bottom out and climb slowly in the nextcouple of years. The upturn will occur from a verylow level in most countries. In Poland and the CzechRepublic, lower exchange rates along with theshortterm impact of poor harvests on food prices willhelp push inflation upward. For the ten countriesjoining the EU in May − eight of which are in Centraland Eastern Europe − harmonisation of indirect taxeswill also mean upward pressure on inflation. InRussia, however, we anticipate falling inflation.

Lithuania in the front ranksThe three Baltic countries will show fast GDPgrowth, with 5.4-7.2 per cent in 2004. Lithuania is thestar of the class, with higher growth and smallercurrent account deficits than in neighbouringcountries. Estonia needs to tighten its fiscal policy,due to unsustainable current account deficits and rapidcredit expansion.

We are raising our growth forecast for Russia bymore than one percentage point to 6.2 per cent thisyear; in 2005 we predict 5.5 per cent. This is largelydue to high oil prices, but also to faster-than-expectedgrowth in domestic demand. President VladimirPutin’s position was further strengthened by theDecember parliamentary election.

Putin will also win the presidential election in Marchand then resume the economic reform process. Thearrest of former Yukos oil group owner MikhailKhodorkovsky does not seem to be having more thana temporary negative impact on the willingness offoreigners to invest in Russia.

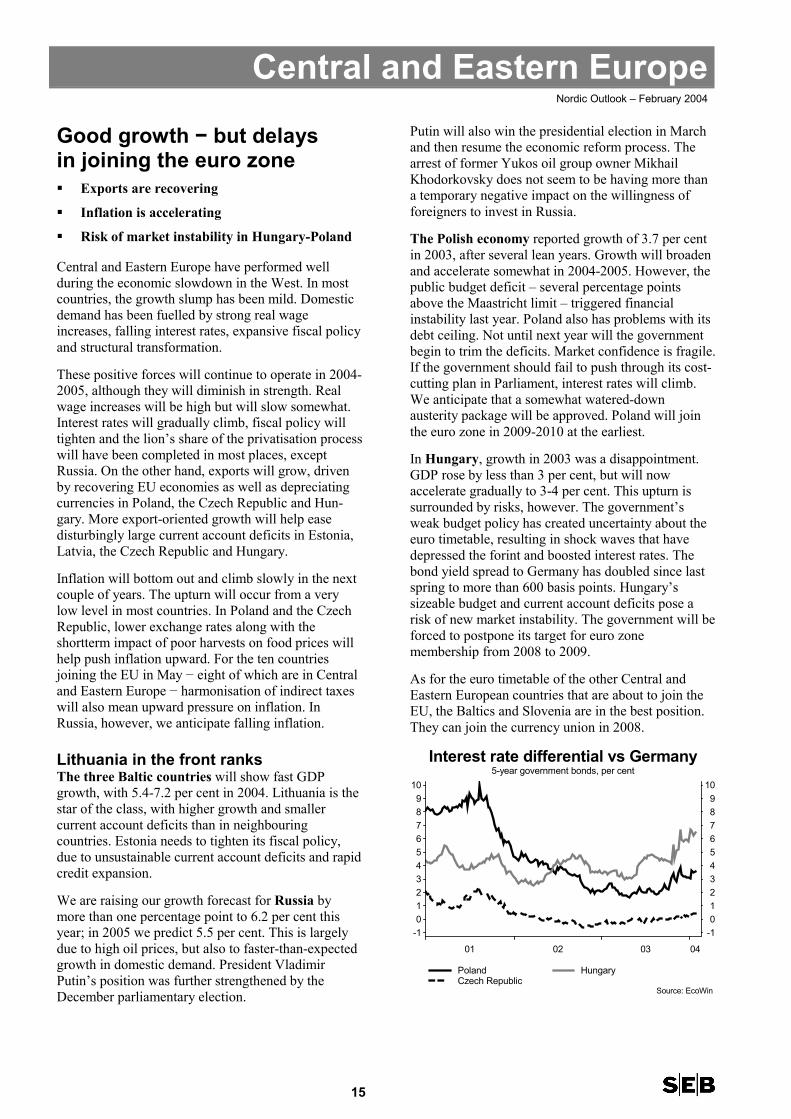

The Polish economy reported growth of 3.7 per centin 2003, after several lean years. Growth will broadenand accelerate somewhat in 2004-2005. However, thepublic budget deficit – several percentage pointsabove the Maastricht limit – triggered financialinstability last year. Poland also has problems with itsdebt ceiling. Not until next year will the governmentbegin to trim the deficits. Market confidence is fragile.If the government should fail to push through its cost-cutting plan in Parliament, interest rates will climb.We anticipate that a somewhat watered-downausterity package will be approved. Poland will jointhe euro zone in 2009-2010 at the earliest.

In Hungary, growth in 2003 was a disappointment.GDP rose by less than 3 per cent, but will nowaccelerate gradually to 3-4 per cent. This upturn issurrounded by risks, however. The government’sweak budget policy has created uncertainty about theeuro timetable, resulting in shock waves that havedepressed the forint and boosted interest rates. Thebond yield spread to Germany has doubled since lastspring to more than 600 basis points. Hungary’ssizeable budget and current account deficits pose arisk of new market instability. The government will beforced to postpone its target for euro zonemembership from 2008 to 2009.

As for the euro timetable of the other Central andEastern European countries that are about to join theEU, the Baltics and Slovenia are in the best position.They can join the currency union in 2008.

5-year government bonds, per centInterest rate differential vs Germany

Poland Czech Republic

Hungary

Source: EcoWin

01 02 03 04

-10123456789

10

-10123456789

10

International financial marketsNordic Outlook – February 2004

16

Weak dollar, low interest rates� Jobless growth will mean low interest rates

� Central banks keep their foot on accelerator

� Imbalances weaken dollar and squeeze ECB

Global financial markets are being driven by partlyopposing forces. Stock markets have risen strongly,propelled by hopes of a continued strong cyclicalupswing. The fixed income market, however, has notfollowed suit. Bond yields have stayed at remarkablylow levels compared to the stock market upturn. Thecrucial issue is whether – and for how long – thisdichotomy can persist. Our view is that the economicrecovery can go on for a while yet without fuellinghigher inflationary pressures in major economies. Ourmain worry as regards stock markets is therefore notinterest rates but valuations. In the foreign exchangemarket, the focus is on global imbalances − withAmerica’s large savings deficits being financed bytransfers from capital accumulation in Asia.

200019801960194019201900

50

40

30

20

10

0

50

40

30

20

10

0

Sources: Smithers & Co, BEA, Thomson Datastream

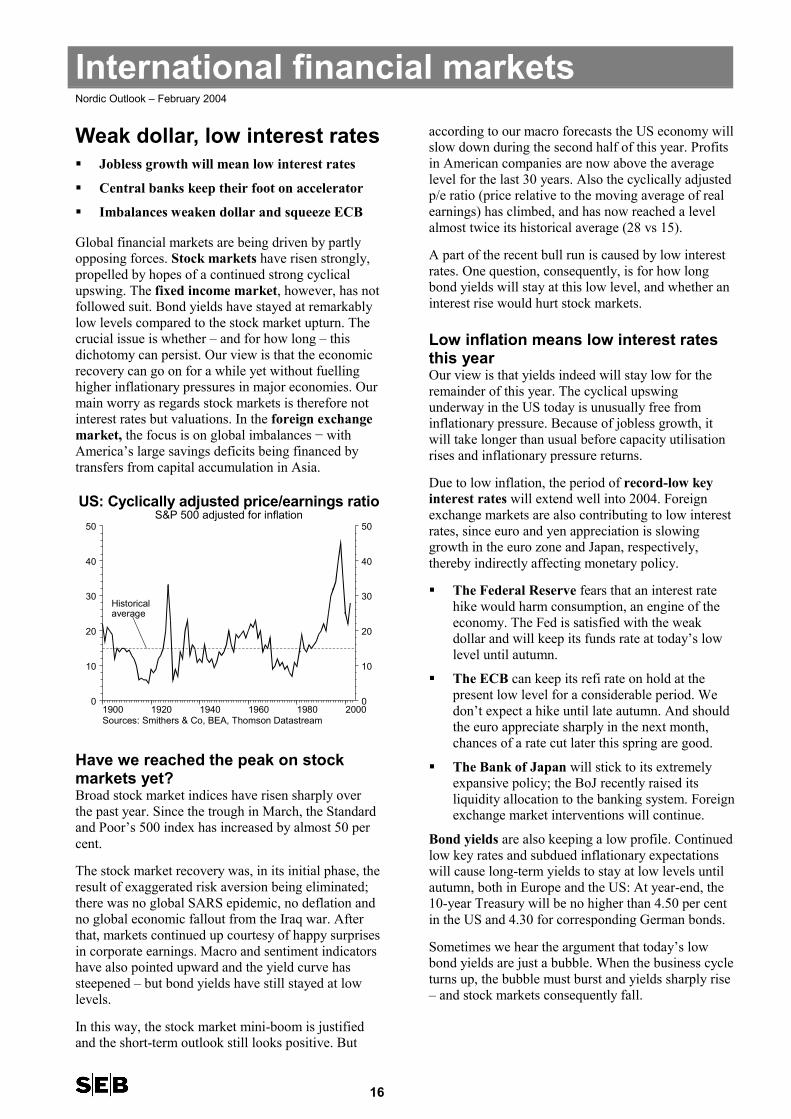

US: Cyclically adjusted price/earnings ratioS&P 500 adjusted for inflation

Historical average

Have we reached the peak on stockmarkets yet?Broad stock market indices have risen sharply overthe past year. Since the trough in March, the Standardand Poor’s 500 index has increased by almost 50 percent.

The stock market recovery was, in its initial phase, theresult of exaggerated risk aversion being eliminated;there was no global SARS epidemic, no deflation andno global economic fallout from the Iraq war. Afterthat, markets continued up courtesy of happy surprisesin corporate earnings. Macro and sentiment indicatorshave also pointed upward and the yield curve hassteepened – but bond yields have still stayed at lowlevels.

In this way, the stock market mini-boom is justifiedand the short-term outlook still looks positive. But

according to our macro forecasts the US economy willslow down during the second half of this year. Profitsin American companies are now above the averagelevel for the last 30 years. Also the cyclically adjustedp/e ratio (price relative to the moving average of realearnings) has climbed, and has now reached a levelalmost twice its historical average (28 vs 15).

A part of the recent bull run is caused by low interestrates. One question, consequently, is for how longbond yields will stay at this low level, and whether aninterest rise would hurt stock markets.

Low inflation means low interest ratesthis yearOur view is that yields indeed will stay low for theremainder of this year. The cyclical upswingunderway in the US today is unusually free frominflationary pressure. Because of jobless growth, itwill take longer than usual before capacity utilisationrises and inflationary pressure returns.

Due to low inflation, the period of record-low keyinterest rates will extend well into 2004. Foreignexchange markets are also contributing to low interestrates, since euro and yen appreciation is slowinggrowth in the euro zone and Japan, respectively,thereby indirectly affecting monetary policy.

� The Federal Reserve fears that an interest ratehike would harm consumption, an engine of theeconomy. The Fed is satisfied with the weakdollar and will keep its funds rate at today’s lowlevel until autumn.

� The ECB can keep its refi rate on hold at thepresent low level for a considerable period. Wedon’t expect a hike until late autumn. And shouldthe euro appreciate sharply in the next month,chances of a rate cut later this spring are good.

� The Bank of Japan will stick to its extremelyexpansive policy; the BoJ recently raised itsliquidity allocation to the banking system. Foreignexchange market interventions will continue.

Bond yields are also keeping a low profile. Continuedlow key rates and subdued inflationary expectationswill cause long-term yields to stay at low levels untilautumn, both in Europe and the US: At year-end, the10-year Treasury will be no higher than 4.50 per centin the US and 4.30 for corresponding German bonds.

Sometimes we hear the argument that today’s lowbond yields are just a bubble. When the business cycleturns up, the bubble must burst and yields sharply rise– and stock markets consequently fall.

International financial marketsNordic Outlook – February 2004

17

050403020100999897

7

6

5

4

3

2

1

0

7

6

5

4

3

2

1

0

Sources: EcoWin and SEB

Key rates

forecast

Per cent Per cent

SEB

Euro zone: Refi rate (Germany until 1999)US: Fed funds

However, we see several factors which indicate thatbond yields will stay low:

� Inflation will remain low, due to jobless growthand continuous swift productivity increases (atleast in the US).

� From a real rate perspective bond yields do notseem particularly low, not even in the US. With along-term inflation of 2-2.5 per cent, it is hard tosee nominal American bond yields of 4 ½-5 percent as a bubble.

� Key rates will remain low, courtesy of lowinflation. On top of that, the Fed wants to avoidexposing the debt-ridden American economy topremature rate hikes. Low short rates willcontinue to support the long end of the yieldcurve.

� Asian central banks will continue to inject li-quidity into the American economy, which is alsohelping to hold back the coming upturn of bondyields.

Rate hike cycle will beginNevertheless, as the recovery gains a foothold, theoutput gap shrinks and global inflation beginscreeping upward, interest rates will start to climb fromtoday’s very low levels.

The Fed will begin a rate hike process in the secondhalf of 2004. Its hikes will be cautious, since debtmakes households vulnerable to higher interest rates.We anticipate that the federal funds rate will stand at1.5 per cent by year-end and climb to 3.25 per cent bythe close of 2005. The BoJ, however, will stick to itszero key rate throughout 2004. The ECB will raise itsrefi rate to 3.0 per cent by late 2005.

Long-term bond yields will climb somewhat too, ascapacity utilisation rises and central banks beginmoving key rates upward. In December 2005, 10-year

Treasury yields in the US will stand at 5.0 per cent,their German equivalents at 4.80 per cent. Comparedto what is priced into the market right now, our yieldtrajectory means lower long-term yields this year, butan upturn towards the level that the market is pricingin during the course of 2005.

Thus, the interest rate rise during our forecast periodwill be moderate. It will not be enough to threaten thestock market.

The fundamental issue raised by our analysis is ratherwhich level of real returns is reasonable in a situationcharacterised by low inflation. When inflation remainslow and stable – and interest rates behave in the sameway – many investors’ hopes for high real returns onfinancial assets seem overly optimistic. They arebased on the faulty presumption that the boomingstock market of the 1990s represent normality. Such aview is a recipe for disappointments – or too riskyinvestments with ensuing high volatility.

Weekly average, per cent10-year government bond yields

US Germany

Sources: EcoWin, SEB

99 00 01 02 03 04 05

3,0

3,5

4,0

4,5

5,0

5,5

6,0

6,5

7,0

3,0

3,5

4,0

4,5

5,0

5,5

6,0

6,5

7,0

SEB forecast

Global imbalances squeezingthe dollarGlobal imbalances and how central banks cope withthem are determining foreign exchange marketdevelopments right now. American stimulus policyimplies that large savings deficits will persist. This ispossible without even heavier pressure on the dollarand longterm yields, due to the large accumulation ofdollar assets in Asian countries.

The US current account deficit was previouslyfinanced primarily by an influx of private capital. Butsince peaking in 2000, this inflow has declined byabout 40 per cent, even though the deficit has grown.Instead, the influx of capital from public sector

International financial marketsNordic Outlook – February 2004

18

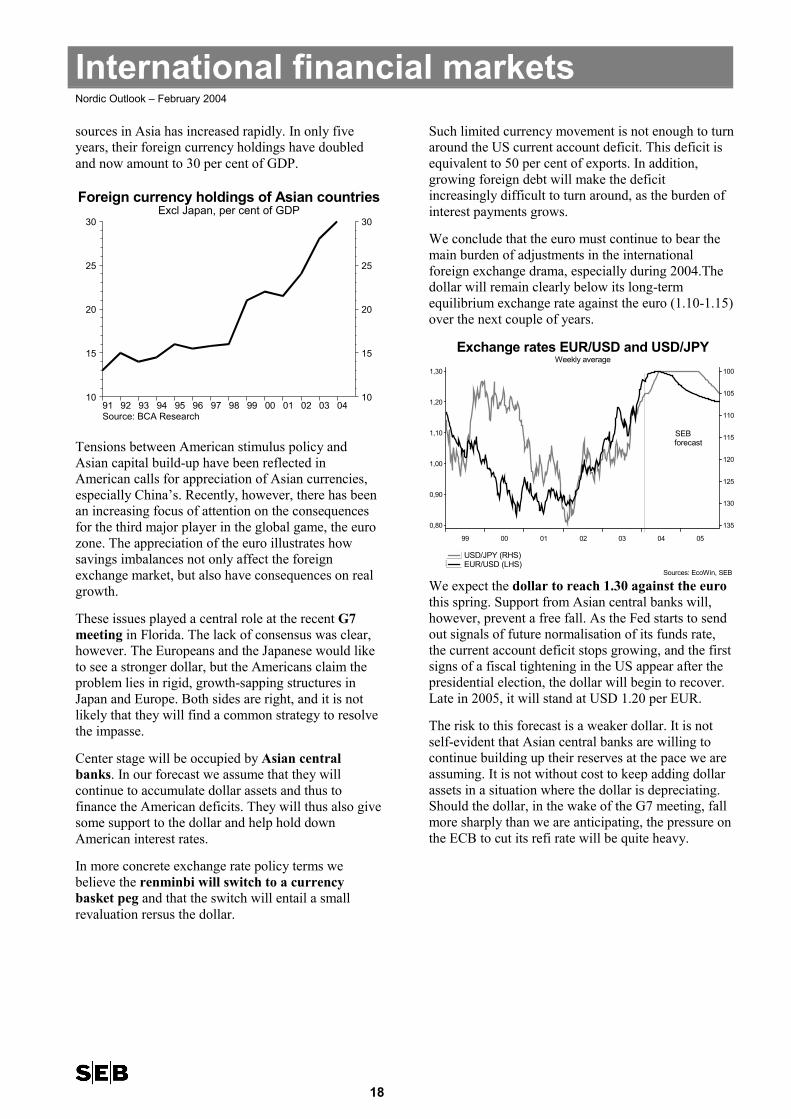

sources in Asia has increased rapidly. In only fiveyears, their foreign currency holdings have doubledand now amount to 30 per cent of GDP.

0403020100999897969594939291

30

25

20

15

10

30

25

20

15

10

Source: BCA Research

Foreign currency holdings of Asian countriesExcl Japan, per cent of GDP

Tensions between American stimulus policy andAsian capital build-up have been reflected inAmerican calls for appreciation of Asian currencies,especially China’s. Recently, however, there has beenan increasing focus of attention on the consequencesfor the third major player in the global game, the eurozone. The appreciation of the euro illustrates howsavings imbalances not only affect the foreignexchange market, but also have consequences on realgrowth.

These issues played a central role at the recent G7meeting in Florida. The lack of consensus was clear,however. The Europeans and the Japanese would liketo see a stronger dollar, but the Americans claim theproblem lies in rigid, growth-sapping structures inJapan and Europe. Both sides are right, and it is notlikely that they will find a common strategy to resolvethe impasse.

Center stage will be occupied by Asian centralbanks. In our forecast we assume that they willcontinue to accumulate dollar assets and thus tofinance the American deficits. They will thus also givesome support to the dollar and help hold downAmerican interest rates.

In more concrete exchange rate policy terms webelieve the renminbi will switch to a currencybasket peg and that the switch will entail a smallrevaluation rersus the dollar.

Such limited currency movement is not enough to turnaround the US current account deficit. This deficit isequivalent to 50 per cent of exports. In addition,growing foreign debt will make the deficitincreasingly difficult to turn around, as the burden ofinterest payments grows.

We conclude that the euro must continue to bear themain burden of adjustments in the internationalforeign exchange drama, especially during 2004.Thedollar will remain clearly below its long-termequilibrium exchange rate against the euro (1.10-1.15)over the next couple of years.

Weekly averageExchange rates EUR/USD and USD/JPY

USD/JPY (RHS) EUR/USD (LHS)

Sources: EcoWin, SEB

99 00 01 02 03 04 05

100

105

110

115

120

125

130

1350,80

0,90

1,00

1,10

1,20

1,30

SEBforecast

We expect the dollar to reach 1.30 against the eurothis spring. Support from Asian central banks will,however, prevent a free fall. As the Fed starts to sendout signals of future normalisation of its funds rate,the current account deficit stops growing, and the firstsigns of a fiscal tightening in the US appear after thepresidential election, the dollar will begin to recover.Late in 2005, it will stand at USD 1.20 per EUR.

The risk to this forecast is a weaker dollar. It is notself-evident that Asian central banks are willing tocontinue building up their reserves at the pace we areassuming. It is not without cost to keep adding dollarassets in a situation where the dollar is depreciating.Should the dollar, in the wake of the G7 meeting, fallmore sharply than we are anticipating, the pressure onthe ECB to cut its refi rate will be quite heavy.

SwedenNordic Outlook – February 2004

19

Higher growth − but withoutjobs and without inflation� Low inflation – one more interest rate cut

� Rocky wage round but low pay agreements

� Weakening budget, growth policy at standstill

The Swedish economy is slowly on the mend. GDPgrowth will accelerate to 2.3 per cent this year and2.5 per cent in 2005. But it will take a long timebefore this manufacturing-led upturn leads to newjobs. The consequence will be a relatively long periodof decent GDP growth, hand in hand with a weaklabour market and low inflation. The government’seconomic policy faces an intricate balancing act:

� Growth is not sufficient to reverse the trendtowards ever-weaker public finances. The fiscalpolicy framework faces tough tests.

� The Riksbank must steer a course between thecoming recovery and the continued decline ininflationary pressure.

04020098969492908886848280

5

4

3

2

1

0

-1

5

4

3

2

1

0

-1

Sources: Statistics Sweden and SEB

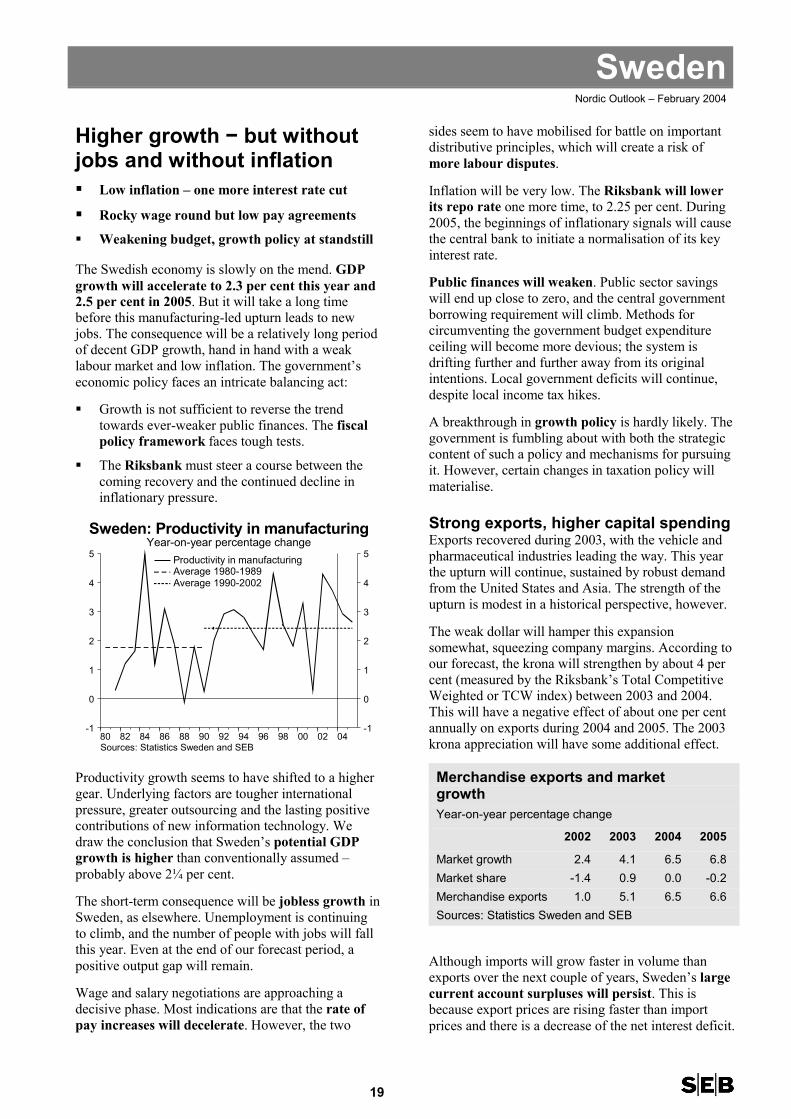

Sweden: Productivity in manufacturingYear-on-year percentage change

Productivity in manufacturingAverage 1980-1989Average 1990-2002

Productivity growth seems to have shifted to a highergear. Underlying factors are tougher internationalpressure, greater outsourcing and the lasting positivecontributions of new information technology. Wedraw the conclusion that Sweden’s potential GDPgrowth is higher than conventionally assumed –probably above 2¼ per cent.

The short-term consequence will be jobless growth inSweden, as elsewhere. Unemployment is continuingto climb, and the number of people with jobs will fallthis year. Even at the end of our forecast period, apositive output gap will remain.

Wage and salary negotiations are approaching adecisive phase. Most indications are that the rate ofpay increases will decelerate. However, the two

sides seem to have mobilised for battle on importantdistributive principles, which will create a risk ofmore labour disputes.

Inflation will be very low. The Riksbank will lowerits repo rate one more time, to 2.25 per cent. During2005, the beginnings of inflationary signals will causethe central bank to initiate a normalisation of its keyinterest rate.

Public finances will weaken. Public sector savingswill end up close to zero, and the central governmentborrowing requirement will climb. Methods forcircumventing the government budget expenditureceiling will become more devious; the system isdrifting further and further away from its originalintentions. Local government deficits will continue,despite local income tax hikes.

A breakthrough in growth policy is hardly likely. Thegovernment is fumbling about with both the strategiccontent of such a policy and mechanisms for pursuingit. However, certain changes in taxation policy willmaterialise.

Strong exports, higher capital spendingExports recovered during 2003, with the vehicle andpharmaceutical industries leading the way. This yearthe upturn will continue, sustained by robust demandfrom the United States and Asia. The strength of theupturn is modest in a historical perspective, however.

The weak dollar will hamper this expansionsomewhat, squeezing company margins. According toour forecast, the krona will strengthen by about 4 percent (measured by the Riksbank’s Total CompetitiveWeighted or TCW index) between 2003 and 2004.This will have a negative effect of about one per centannually on exports during 2004 and 2005. The 2003krona appreciation will have some additional effect.

Merchandise exports and marketgrowthYear-on-year percentage change

2002 2003 2004 2005

Market growth 2.4 4.1 6.5 6.8Market share -1.4 0.9 0.0 -0.2Merchandise exports 1.0 5.1 6.5 6.6Sources: Statistics Sweden and SEB

Although imports will grow faster in volume thanexports over the next couple of years, Sweden’s largecurrent account surpluses will persist. This isbecause export prices are rising faster than importprices and there is a decrease of the net interest deficit.

SwedenNordic Outlook – February 2004

20

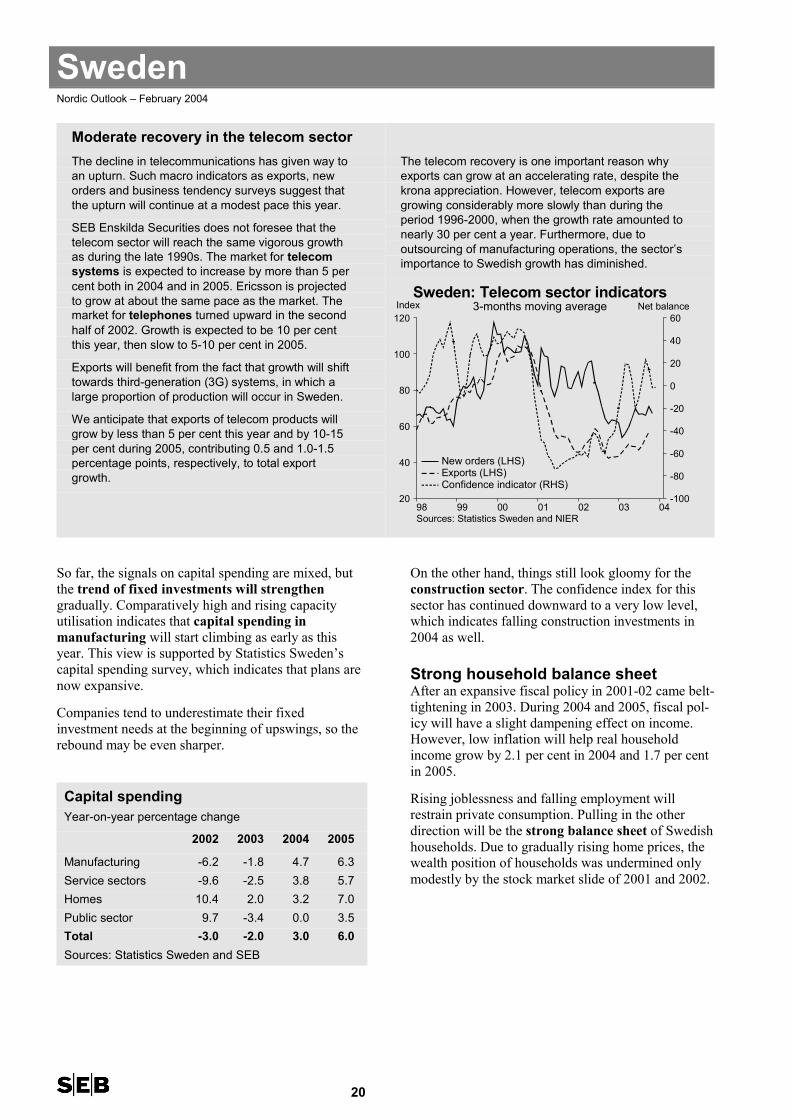

Moderate recovery in the telecom sectorThe decline in telecommunications has given way toan upturn. Such macro indicators as exports, neworders and business tendency surveys suggest thatthe upturn will continue at a modest pace this year.

SEB Enskilda Securities does not foresee that thetelecom sector will reach the same vigorous growthas during the late 1990s. The market for telecomsystems is expected to increase by more than 5 percent both in 2004 and in 2005. Ericsson is projectedto grow at about the same pace as the market. Themarket for telephones turned upward in the secondhalf of 2002. Growth is expected to be 10 per centthis year, then slow to 5-10 per cent in 2005.

Exports will benefit from the fact that growth will shifttowards third-generation (3G) systems, in which alarge proportion of production will occur in Sweden.

We anticipate that exports of telecom products willgrow by less than 5 per cent this year and by 10-15per cent during 2005, contributing 0.5 and 1.0-1.5percentage points, respectively, to total exportgrowth.

The telecom recovery is one important reason whyexports can grow at an accelerating rate, despite thekrona appreciation. However, telecom exports aregrowing considerably more slowly than during theperiod 1996-2000, when the growth rate amounted tonearly 30 per cent a year. Furthermore, due tooutsourcing of manufacturing operations, the sector’simportance to Swedish growth has diminished.

So far, the signals on capital spending are mixed, butthe trend of fixed investments will strengthengradually. Comparatively high and rising capacityutilisation indicates that capital spending inmanufacturing will start climbing as early as thisyear. This view is supported by Statistics Sweden’scapital spending survey, which indicates that plans arenow expansive.

Companies tend to underestimate their fixedinvestment needs at the beginning of upswings, so therebound may be even sharper.

Capital spendingYear-on-year percentage change

2002 2003 2004 2005

Manufacturing -6.2 -1.8 4.7 6.3Service sectors -9.6 -2.5 3.8 5.7Homes 10.4 2.0 3.2 7.0Public sector 9.7 -3.4 0.0 3.5Total -3.0 -2.0 3.0 6.0Sources: Statistics Sweden and SEB

On the other hand, things still look gloomy for theconstruction sector. The confidence index for thissector has continued downward to a very low level,which indicates falling construction investments in2004 as well.

Strong household balance sheetAfter an expansive fiscal policy in 2001-02 came belt-tightening in 2003. During 2004 and 2005, fiscal pol-icy will have a slight dampening effect on income.However, low inflation will help real householdincome grow by 2.1 per cent in 2004 and 1.7 per centin 2005.

Rising joblessness and falling employment willrestrain private consumption. Pulling in the otherdirection will be the strong balance sheet of Swedishhouseholds. Due to gradually rising home prices, thewealth position of households was undermined onlymodestly by the stock market slide of 2001 and 2002.

04030201009998

120

100

80

60

40

20

60

40

20

0

-20

-40

-60

-80

-100

Sources: Statistics Sweden and NIER

Sweden: Telecom sector indicators3-months moving averageIndex Net balance

New orders (LHS)Exports (LHS)Confidence indicator (RHS)

SwedenNordic Outlook – February 2004

21

Revised income growth curveOur analysis of household income has changedappreciably, due to revised calculations from theNational Accounts. The previous picture was that theexpansive fiscal policy of 2001 and 2002 had resultedin annual income increases of about 5 per cent. Whenfiscal policy was tightened in 2003, income growth fellto about 1½ per cent, where it was then projected toremain in 2004 and 2005.

� The new figures show that income rose even fasterin 2001, but considerably more slowly in 2002. Thereasons are primarily of a technical nature, owing tonew principles for accrual of capital gains tax.

� More importantly, household income was squeezedagain in 2003. According to our new calculation,income fell nearly 1 per cent last year; this year it willincrease about 2 per cent.

This sharp reversal raises the question of how weshould interpret the new figures: Can 2004 really be somuch better than 2003? The answer is Yes – in part.Of the 3 per cent reversal, nearly half is explained bythe technical accrual effect. Of the underlyingimprovement, about 1 per cent is explained by higherreal wage growth due to low inflation. A somewhatlooser fiscal policy in 2004 explains more than anotherhalf percentage point of the stronger income growth.

The stock market recovery is now further improvingthe household balance sheet. Lending has admittedlycontinued to increase, and debt as a percentage ofincome is approaching the peak levels of the early1990s. Due to low interest rates, however, the interestburden is far lighter. Given the interest rate forecastswe are presenting here, the interest burden will hardlybe any problem.

The economic situation of householdsYear-on-year percentage change

2002 2003 2004 2005

Disposable income 2.1 -0.9 2.1 1.7Consumption 1.5 2.0 2.5 2.7Household savings 8.8 5.9 5.3 4.5ratio, % of disposable income

Sources: Statistics Sweden and SEB

There are thus many indications that households willcontinue to reduce their savings. We anticipate thatconsumption will climb by around 2½ per cent boththis year and next – clearly faster than income.

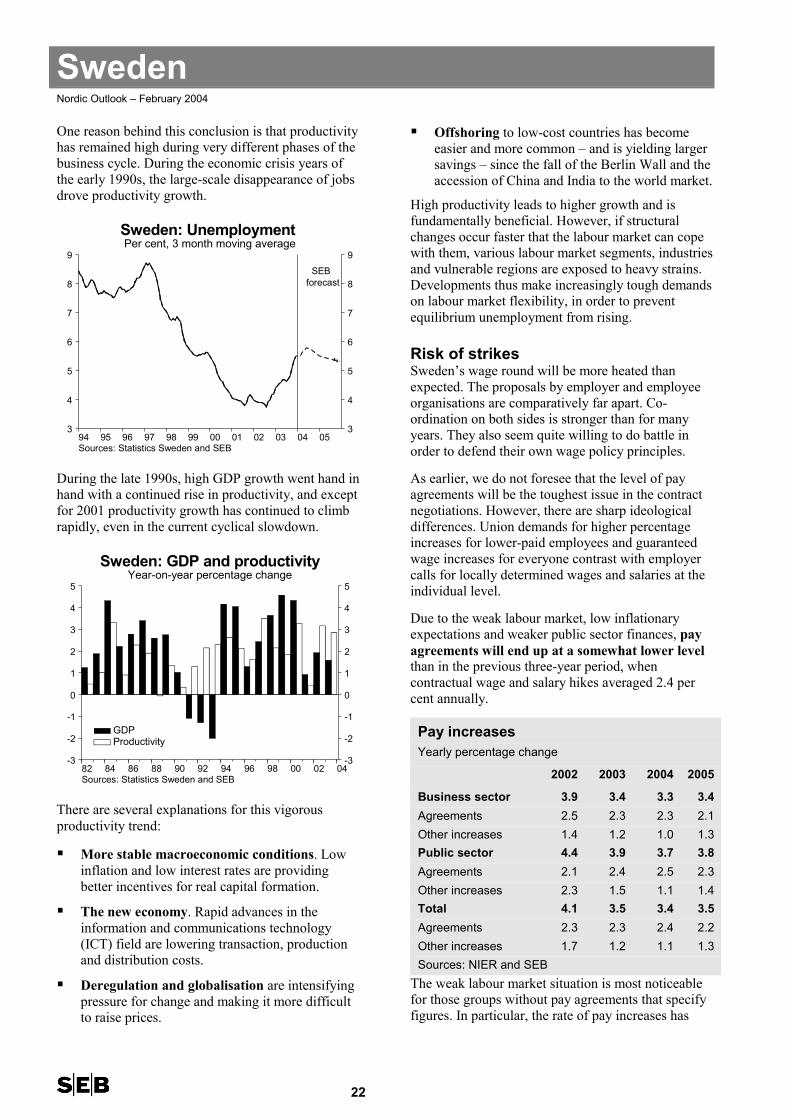

High productivity yields jobless growthUnemployment rose steeply late last year, partlybecause the number of people in government-financedemployment training or temporary jobs (“labourmarket programmes”) declined. Meanwhile, totalemployment showed a downward trend.

Such short-term indicators as lay-off notices, job va-cancies and the business tendency survey of theNational Institute of Economic Research (NIER) pointtowards continued weakening in the labour marketsituation, with rising unemployment and a decliningtotal number of people with jobs during 2004.

The Swedish economy thus exhibits certain featuresreminiscent of the American economy. Despite decentgrowth, not enough jobs are being created to enablethe labour market situation to stabilise. As in the US,it is difficult to determine to what extent productivityhas shifted upward in a long-term perspective. Tosome extent, short-term factors may explaindevelopments: