Embed Size (px)

Citation preview

ECONOMIC RECOVERY

PATHWAYS FOR

CANADA'S ENERGY

INDUSTRY: PART 2 -

CANADIAN CRUDE OIL

AND NATURAL GAS

STUDY NO. 192B SEPTEMBER 2020

3512 - 33 Street NW, #150, Calgary, AB T2L 2A6350 Sparks Street, #805, Ottawa, ON K1R 7S8

403.282.1231 | www.ceri.ca | [email protected]

@ceri_canada

Canadian Energy Research Institute

ECONOMIC RECOVERY PATHWAYS FOR CANADA’S ENERGY INDUSTRY: PART 2 – CANADIAN CRUDE OIL AND NATURAL GAS

Economic Recovery Pathways for Canada's Energy Industry: Part 2 - Canadian Crude Oil and Natural Gas

Authors: Mohamed Refaei, Tosin Adeyemo, Toufigh Bararpour, Eranda Bartholameuz, Nurul Hossain, Dinara Millington, Marc Mikhail, Hamid Rahmanifard Recommended Citation (Author-date style): Refaei, Mohamed, Tosin Adeyemo, Toufigh Bararpour, Eranda Bartholameuz, A K M Nurul Hossain, Dinara Millington, Marc Mikhail and Hamid Rahmanifard. 2020. “Economic Recovery Pathways for Canada's Energy Industry: Part 2 - Canadian Crude Oil and Natural Gas.” Study No. 192B. Calgary, AB: Canadian Energy Research Institute. https://ceri.ca/assets/files/Study_192B_Full_Report.pdf Recommended Citation (Numbered style): M. Refaei, T. Adeyemo, T. Bararpour, E. Bartholameuz, A.N. Hossain, D. Millington, M. Mikhail, and H. Rahmanifard, “Economic Recovery Pathways for Canada's Energy Industry: Part 2 - Canadian Crude Oil and Natural Gas,” Canadian Energy Research Institute, Calgary, AB, Study No. 192B, 2020. URL: https://ceri.ca/assets/files/Study_192B_Full_Report.pdf Copyright © Canadian Energy Research Institute, 2020 Sections of this study may be reproduced in magazines and newspapers with acknowledgment to the Canadian Energy Research Institute

September 2020 Printed in Canada

Acknowledgements: The authors of this report would like to extend their thanks and sincere gratitude to all CERI staff, the Board of Directors and the Research Advisory Committee involved in the production and editing of the material. The authors would also like to acknowledge the following reviewers for providing helpful and valuable insights for this study:

• Randy Green, Sproule • Elizabeth Aquin, PSAC • GLJ Ltd.

Responsibility for any errors, interpretations, or omissions lies solely with CERI.

ABOUT THE CANADIAN ENERGY RESEARCH INSTITUTE Founded in 1975, the Canadian Energy Research Institute (CERI) is an independent, registered charitable organization specializing in the analysis of energy economics and related environmental policy issues in the energy production, transportation, and consumption sectors. Our mission is to provide relevant, independent, and objective economic research of energy and environmental issues to benefit business, government, academia, and the public.

For more information about CERI, visit www.ceri.ca

CANADIAN ENERGY RESEARCH INSTITUTE 150, 3512 – 33 Street NW, Calgary, Alberta T2L 2A6, Email: [email protected], Phone: 403-282-1231

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas iii

Table of Contents List of Figures ................................................................................................................................................ v

List of Tables ............................................................................................................................................... vii

Acronyms and Abbreviations ....................................................................................................................... ix

Executive Summary ...................................................................................................................................... xi

Chapter 1: Introduction and Background ..................................................................................................... 1

Introduction .............................................................................................................................................. 1

Background - Summary Statistics ............................................................................................................. 1

Chapter 2: Modelling Methodology and Assumptions ................................................................................. 5

Modelling Methodology and Assumptions .............................................................................................. 5

Economic Model ................................................................................................................................... 5

Economic Impacts ................................................................................................................................ 6

Federal Programs ................................................................................................................................. 9

Provincial Programs ............................................................................................................................ 11

Oil and Gas Operations and Revenues ............................................................................................... 13

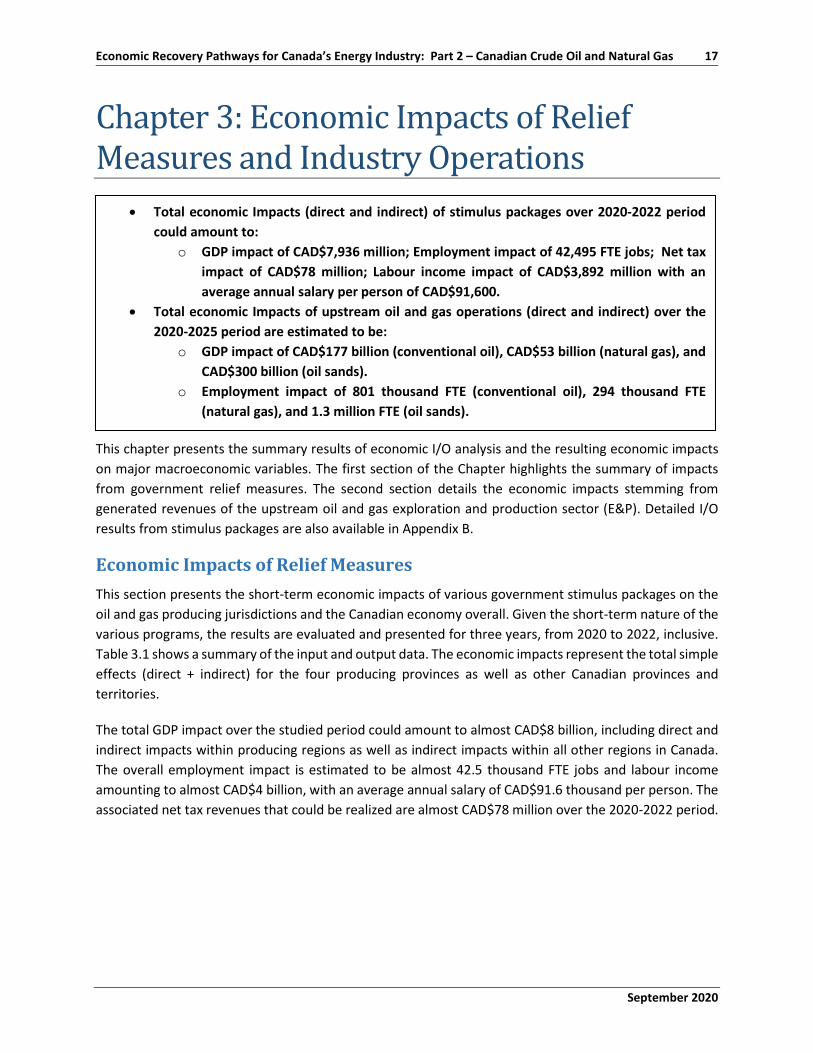

Chapter 3: Economic Impacts of Relief Measures and Industry Operations .............................................. 17

Economic Impacts of Relief Measures .................................................................................................... 17

Gross Domestic Product Impact ......................................................................................................... 19

Employment Impact ........................................................................................................................... 20

Net Tax Impact ................................................................................................................................... 21

Labour Income Impact ....................................................................................................................... 22

Economic Impacts of Oil and Gas Revenues ........................................................................................... 23

Economic Impacts of Conventional Crude Oil Development ............................................................. 23

Economic Impacts of Natural Gas Production ................................................................................... 25

Economic Impacts of Oil Sands Production ........................................................................................ 28

Chapter 4: Challenges and Opportunities for the Recovery of Canada's Oil and Gas Sector ..................... 33

Chapter 5: Conclusions ............................................................................................................................... 37

Bibliography ................................................................................................................................................ 39

Appendix A: Federal and Provincial Relief Measures ................................................................................. 43

Relief Measures by Categories ............................................................................................................... 43

Credit-Loans ....................................................................................................................................... 43

iv Canadian Energy Research Institute

September 2020

Subsidies ............................................................................................................................................. 45

Tax Deferrals ...................................................................................................................................... 46

Grants ................................................................................................................................................. 48

Appendix B: Input/output Results .............................................................................................................. 53

Credit Loans ............................................................................................................................................ 53

Canada Emergency Business Account (CEBA) .................................................................................... 53

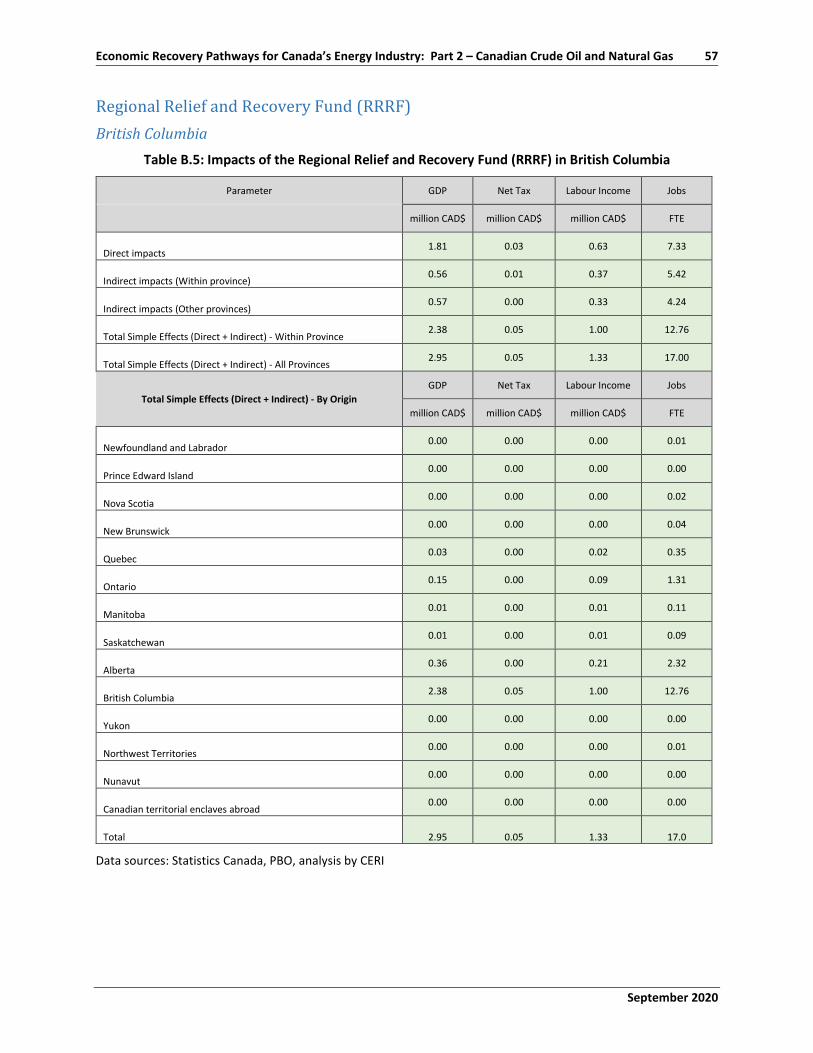

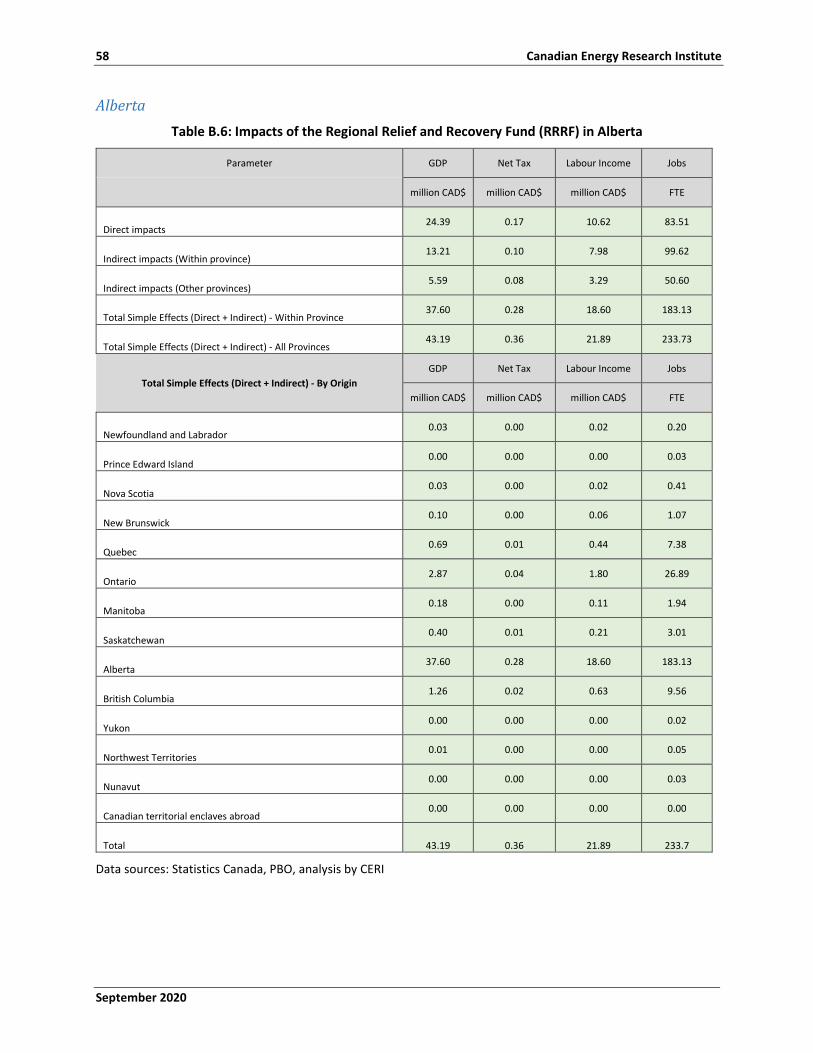

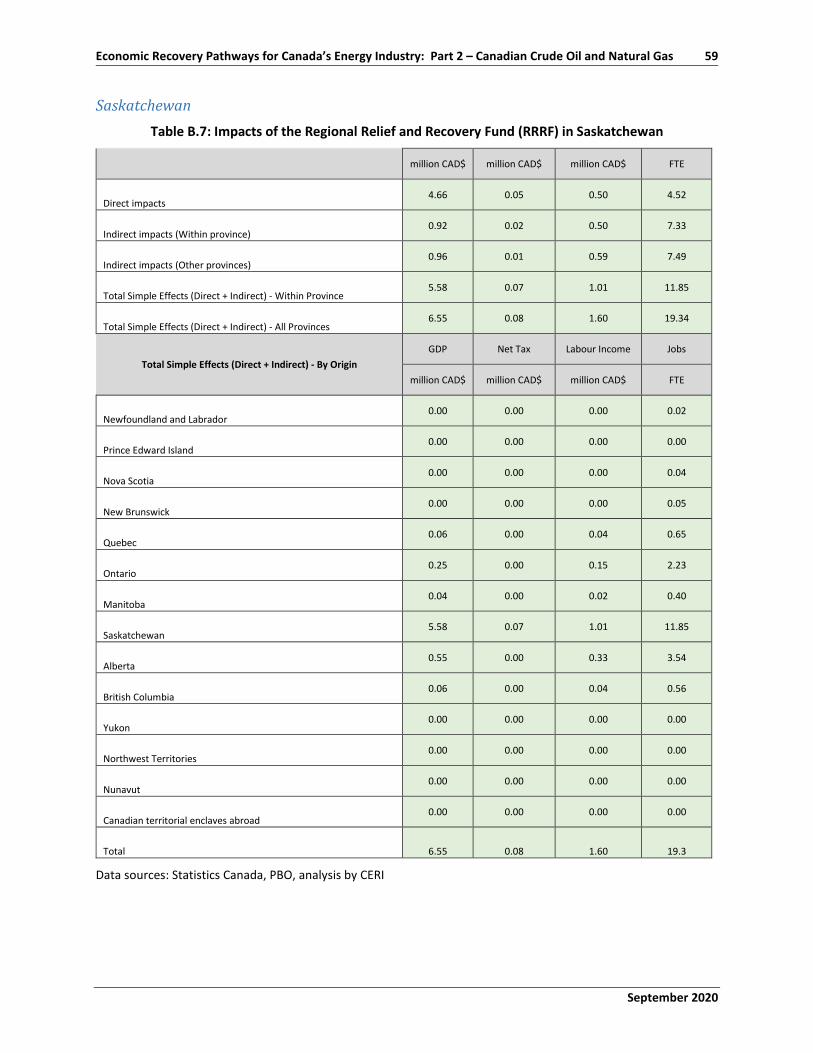

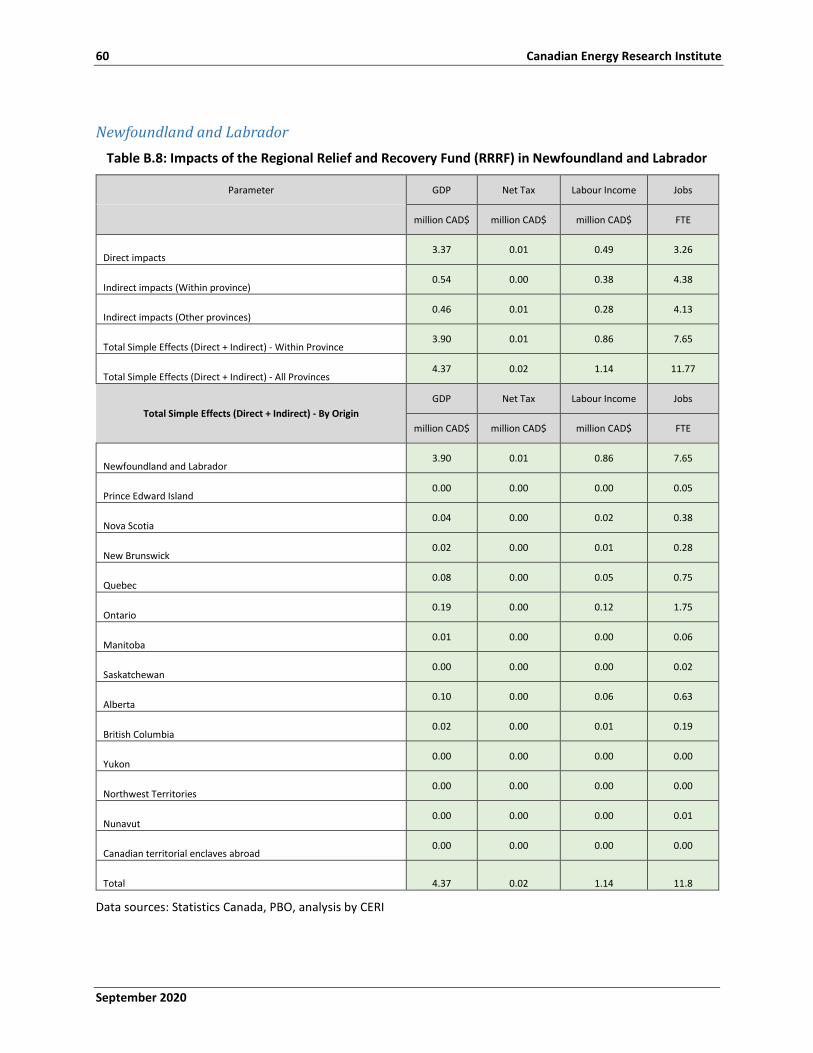

Regional Relief and Recovery Fund (RRRF) ........................................................................................ 57

Business Credit Availability Program (BCAP) ...................................................................................... 61

Subsidies ................................................................................................................................................. 65

Canada Emergency Wage Subsidy (CEWS) ......................................................................................... 65

Canada Emergency Commercial Rent Assistance (CECRA) ................................................................ 69

Temporary Wage Subsidy for Employers (TWS) ................................................................................ 73

Tax Deferrals ........................................................................................................................................... 77

Deferral of Sales Tax Remittance and Customs Duty ......................................................................... 77

Income Tax (Federal, provincial, and other related provincial taxes) ................................................ 81

Grants ..................................................................................................................................................... 85

Orphan and Inactive Oil and Gas Wells Grant .................................................................................... 85

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas v

List of Figures Figure 1.1: Oil and Gas Sector Employment by Province (Number of Jobs) ................................................. 2

Figure 1.2: Oil and Gas GDP Contribution by Subsector (Million CAD$)....................................................... 3

Figure 2.1: Input-Output Framework ............................................................................................................ 6

Figure 2.2: FTE Job Multipliers by Province and Sector ................................................................................ 7

Figure 2.3: GDP Multipliers by Province and Sector ..................................................................................... 8

Figure 2.4: 2020-2025 Canadian Oil and Gas Production Forecast ............................................................ 14

Figure 2.5: Oil and Gas Price Forecasts ....................................................................................................... 15

Figure 3.1: GDP Impacts of Stimulus Packages ........................................................................................... 19

Figure 3.2: Employment Impacts of Stimulus Packages ............................................................................. 20

Figure 3.3: Net Tax Impacts of Stimulus Packages ...................................................................................... 21

Figure 3.4: Labor Income Impacts of Stimulus Packages ............................................................................ 22

Figure 3.5: Annual GDP Impacts of Crude Oil Production, 2020-2025 ....................................................... 23

Figure 3.6: Annual Net Tax Impacts of Crude Oil Production, 2020-2025 .................................................. 24

Figure 3.7: Labour income (A) and the Employment (B) Impacts of Crude Oil Production, 2020-2025 ........................................................................................ 25

Figure 3.8: Annual GDP Impacts of Natural Gas Production, 2020-2025 ................................................... 26

Figure 3.9: Annual Net Tax Impacts of Natural Gas Production, 2020-2025 .............................................. 27

Figure 3.10: Labour income (A) and the Employment (B) Impacts of Natural Gas Production, 2020-2025 .................................................................................... 28

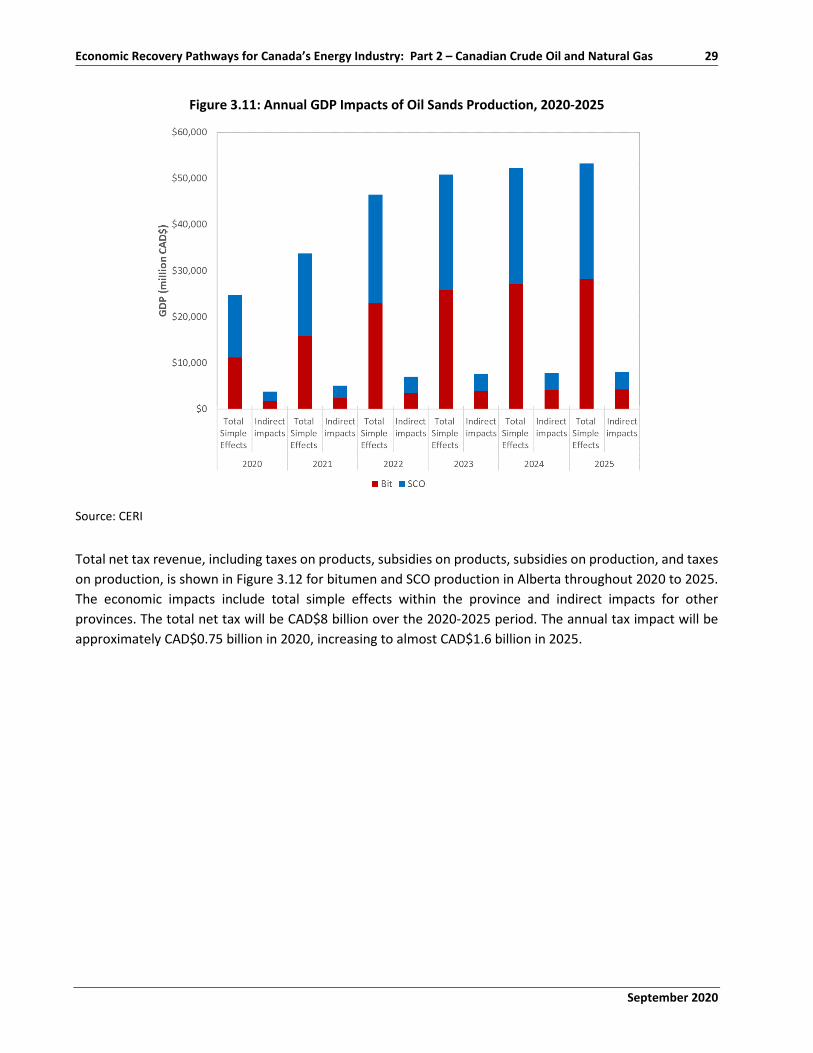

Figure 3.11: Annual GDP Impacts of Oil Sands Production, 2020-2025 ..................................................... 29

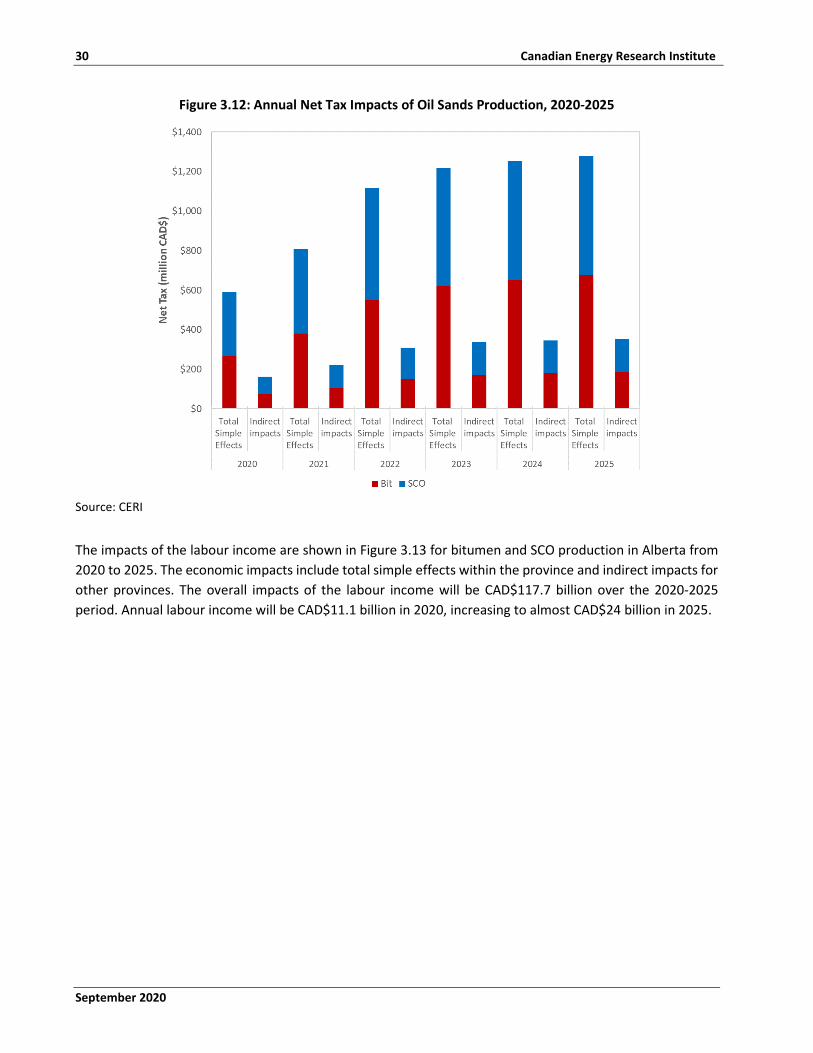

Figure 3.12: Annual Net Tax Impacts of Oil Sands Production, 2020-2025 ................................................ 30

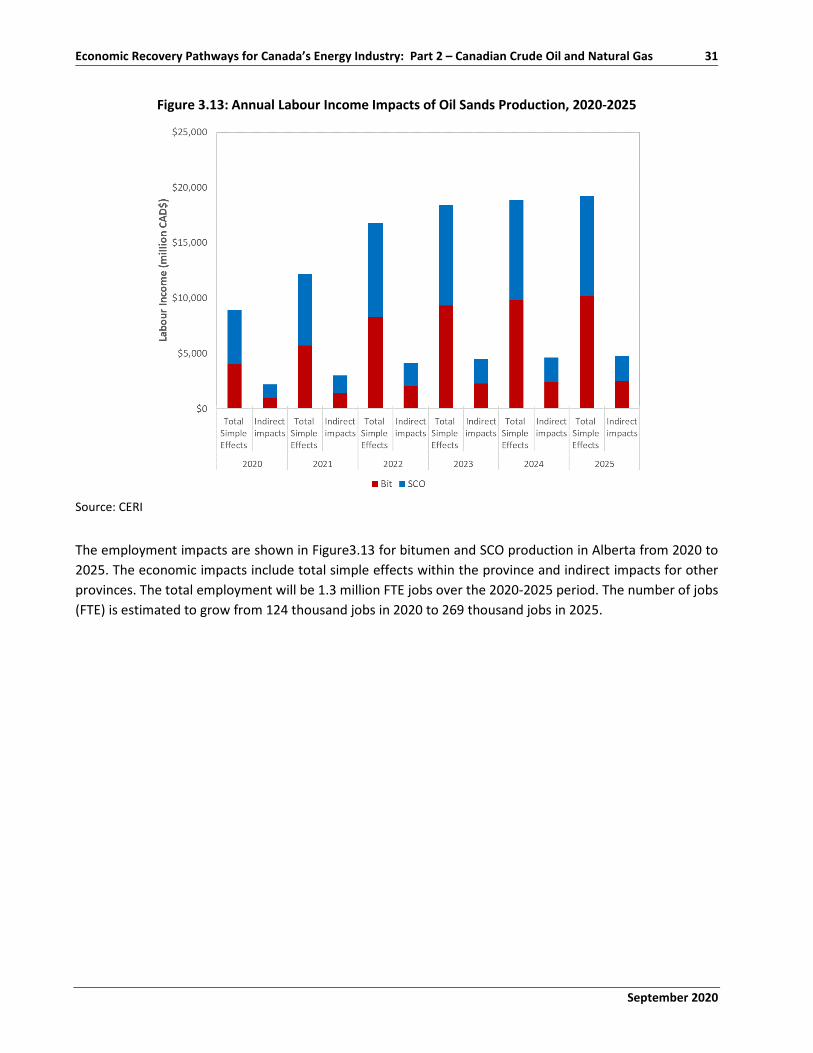

Figure 3.13: Annual Labour Income Impacts of Oil Sands Production, 2020-2025 .................................... 31

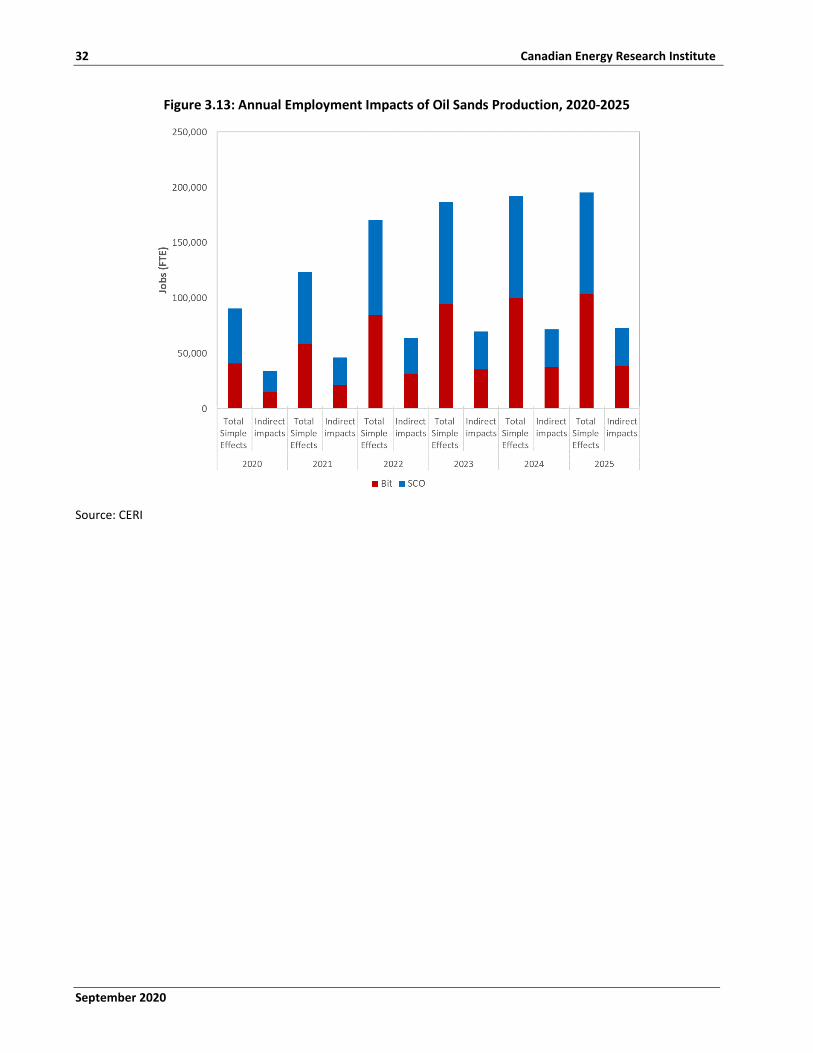

Figure 3.13: Annual Employment Impacts of Oil Sands Production, 2020-2025 ........................................ 32

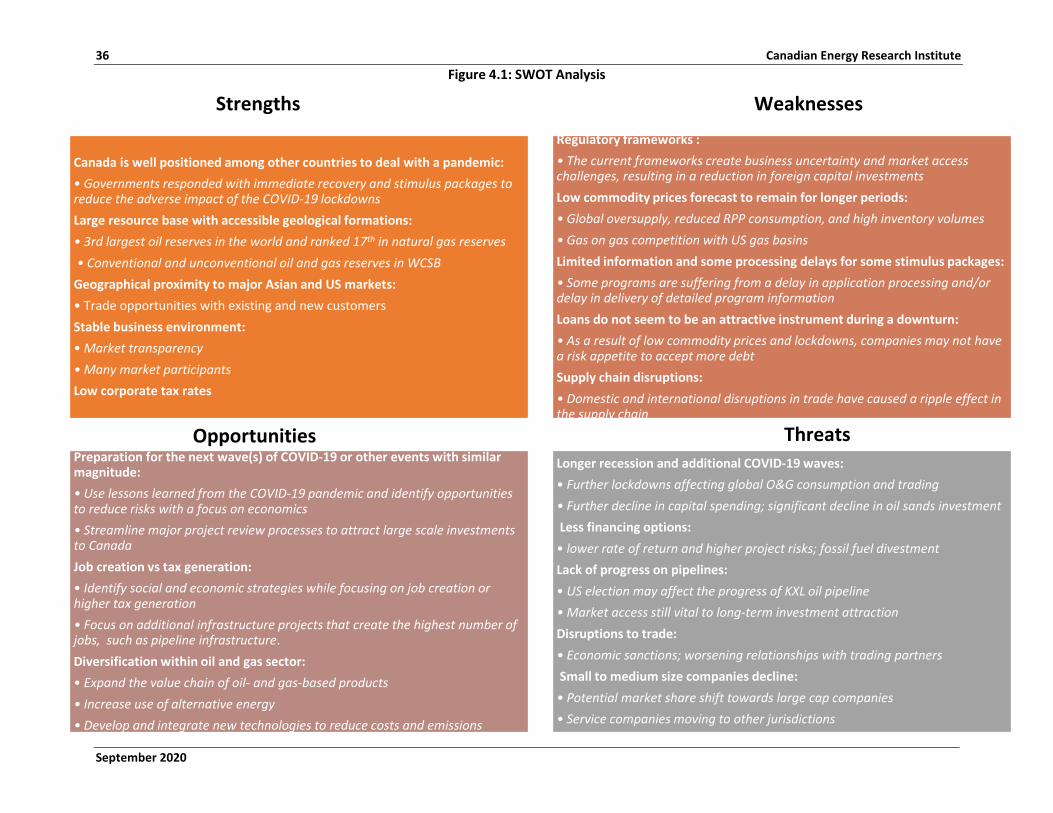

Figure 4.1: SWOT Analysis........................................................................................................................... 36

vi Canadian Energy Research Institute

September 2020

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas vii

List of Tables Table E.1: Annualized Economic Impact Gap for the E&P Sector .............................................................. xii

Table 1.1: Oil and Gas Sector’s Employment Changes (Month over Month) ............................................... 2

Table 1.2: Oil and Gas Sector’s GDP Changes (Month over Month) ............................................................. 3

Table 2.1: Stimulus Programs and Funds for all Sectors ............................................................................... 9

Table 2.2: Stimulus Programs and Fund Allocation for O&G Sector in BC, AB, SK, NL ............................... 11

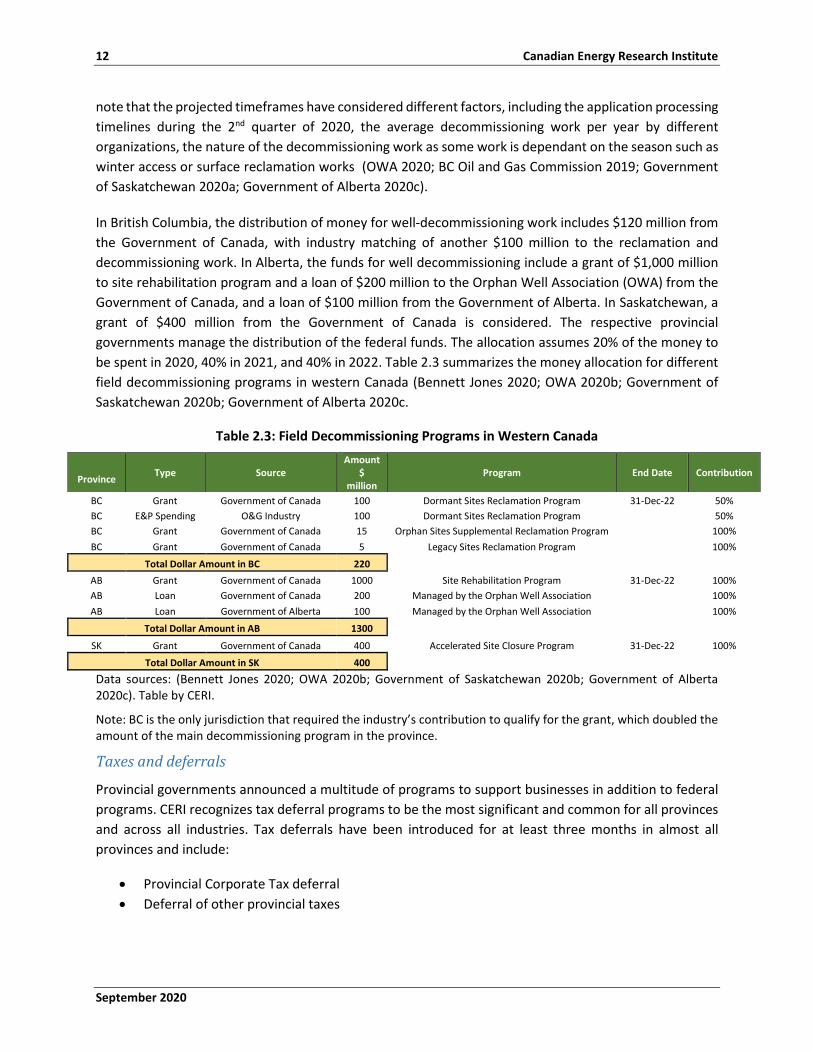

Table 2.3: Field Decommissioning Programs in Western Canada .............................................................. 12

Table 3.1: Summary Table........................................................................................................................... 18

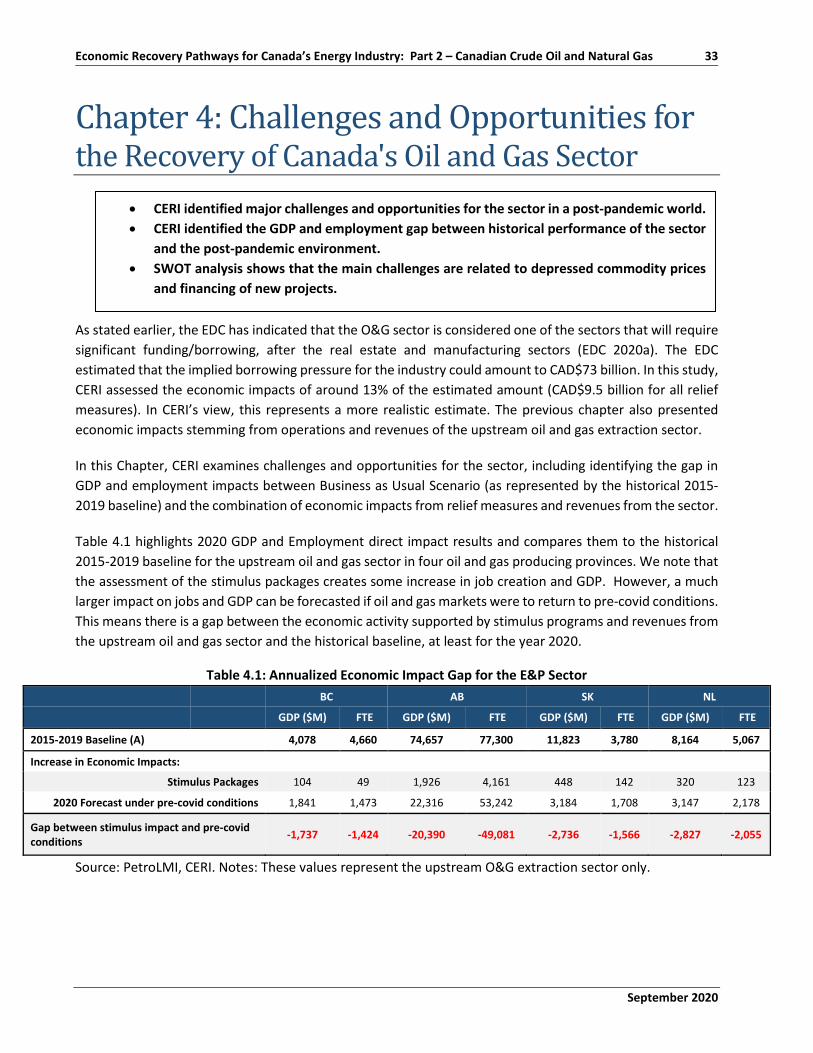

Table 4.1: Annualized Economic Impact Gap for the E&P Sector ............................................................... 33

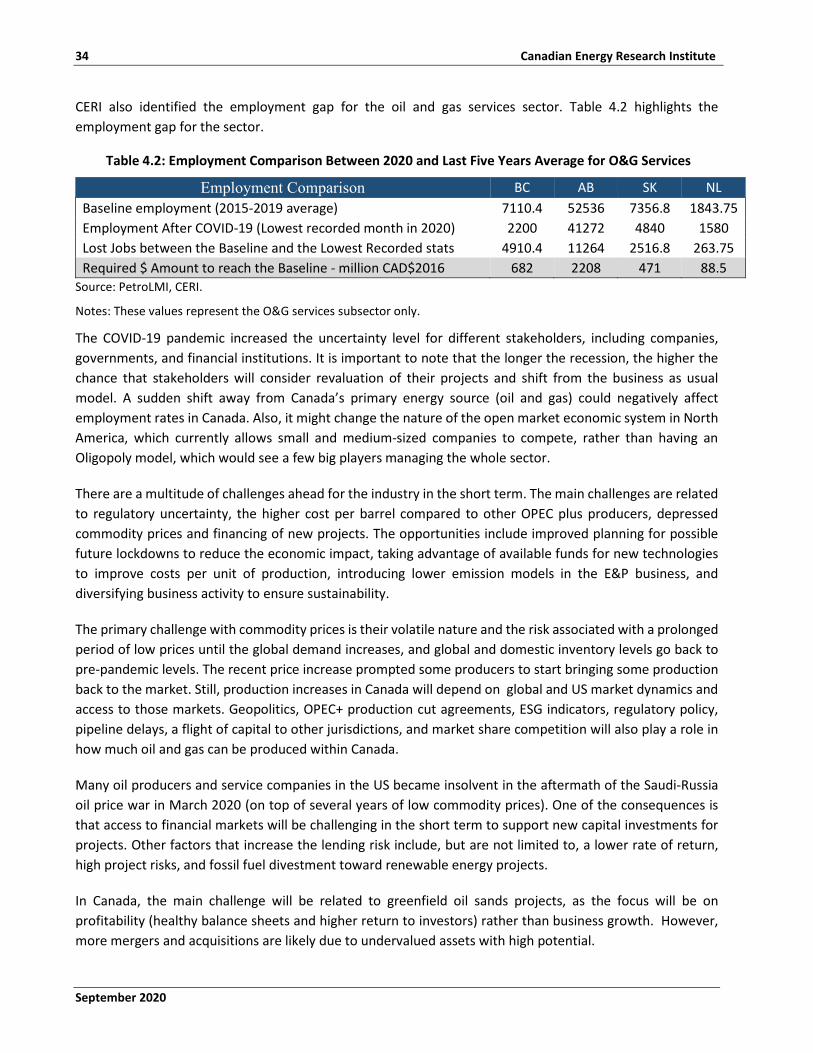

Table 4.2: Employment Comparison Between 2020 and Last Five Years Average for O&G Services ........ 34

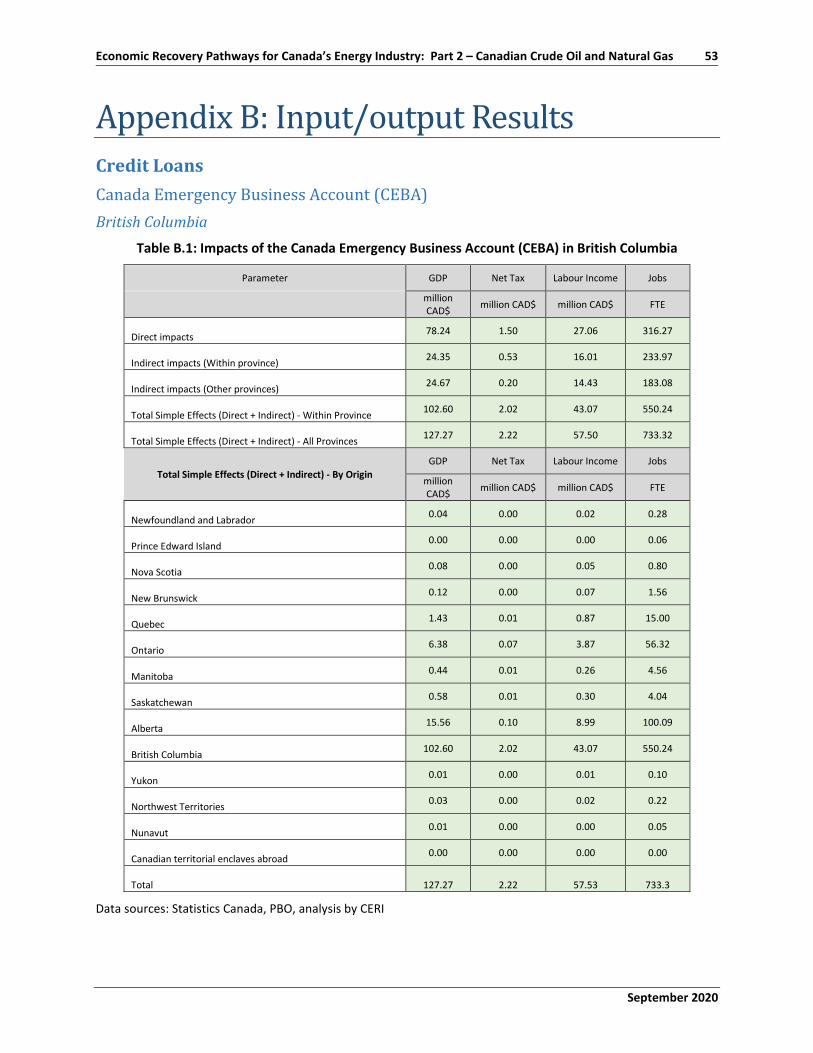

Table B.1: Impacts of the Canada Emergency Business Account (CEBA) in British Columbia .................... 53

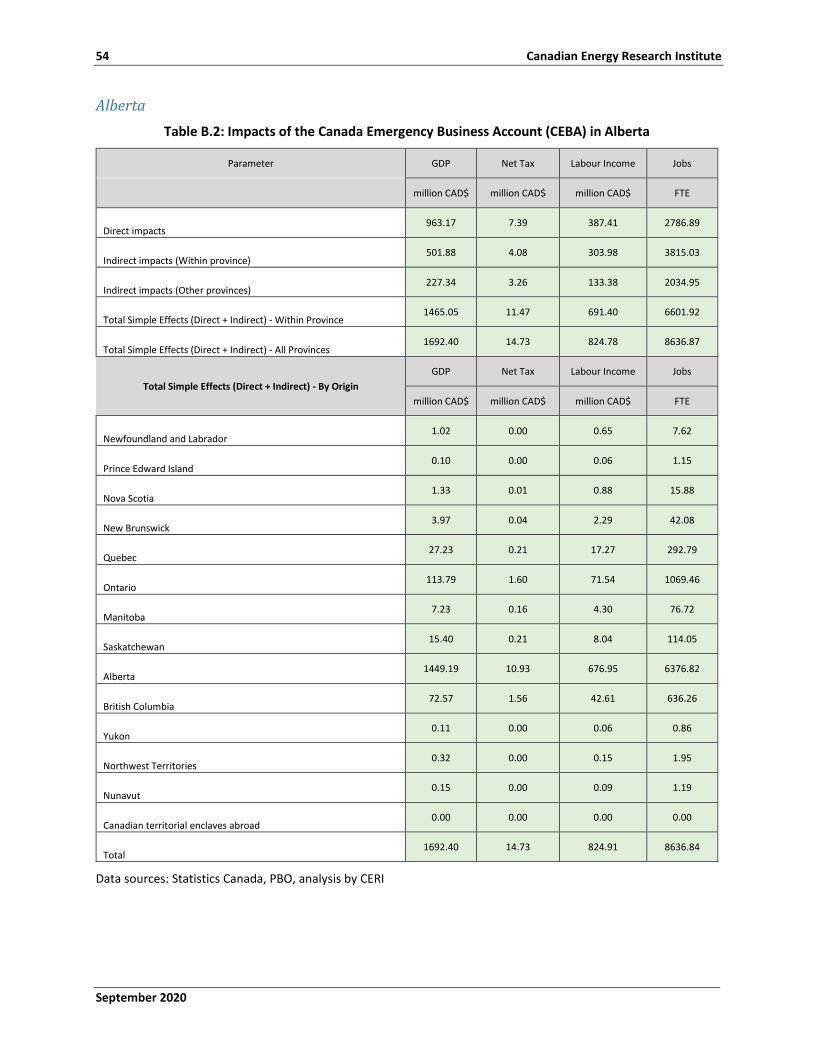

Table B.2: Impacts of the Canada Emergency Business Account (CEBA) in Alberta ................................... 54

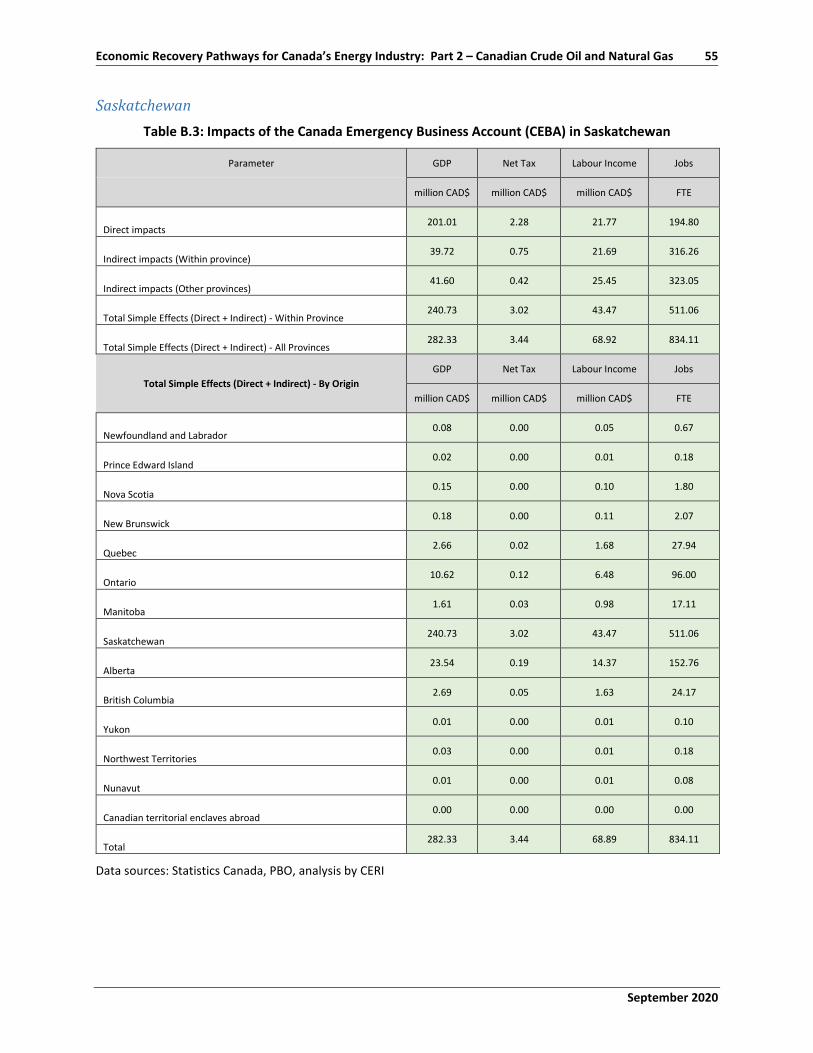

Table B.3: Impacts of the Canada Emergency Business Account (CEBA) in Saskatchewan ........................ 55

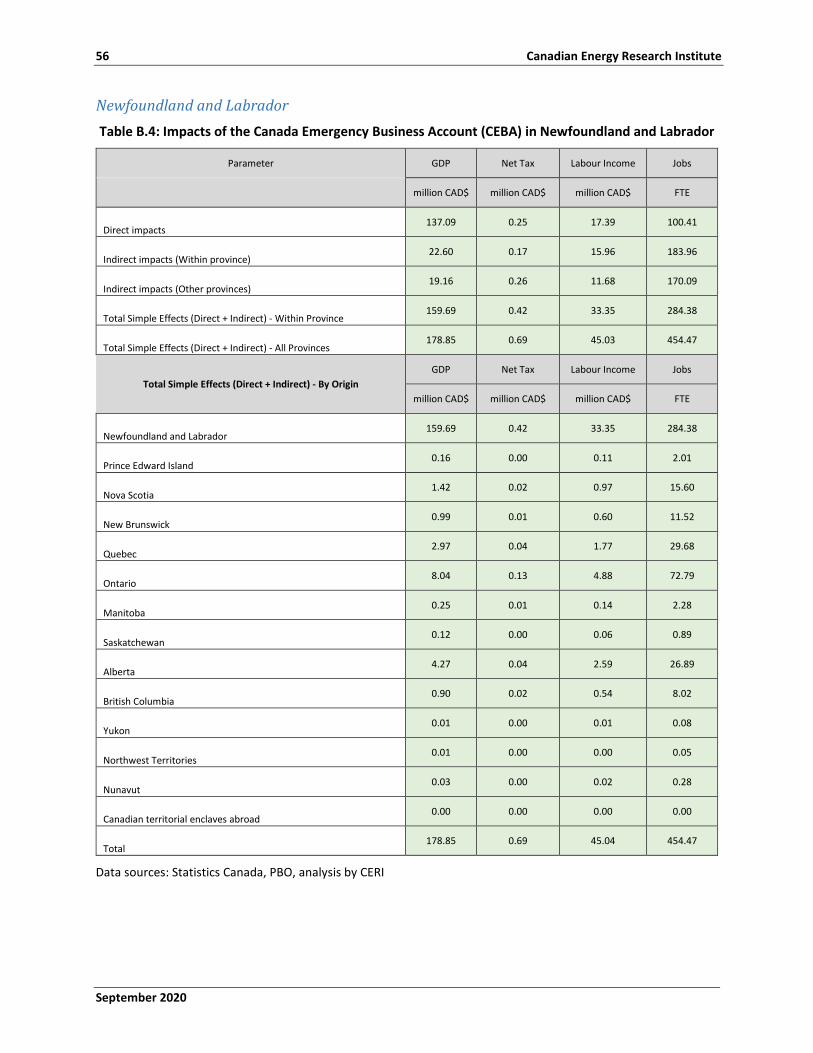

Table B.4: Impacts of the Canada Emergency Business Account (CEBA) in Newfoundland and Labrador 56

Table B.5: Impacts of the Regional Relief and Recovery Fund (RRRF) in British Columbia ........................ 57

Table B.6: Impacts of the Regional Relief and Recovery Fund (RRRF) in Alberta ....................................... 58

Table B.7: Impacts of the Regional Relief and Recovery Fund (RRRF) in Saskatchewan ............................ 59

Table B.8: Impacts of the Regional Relief and Recovery Fund (RRRF) in Newfoundland and Labrador ..... 60

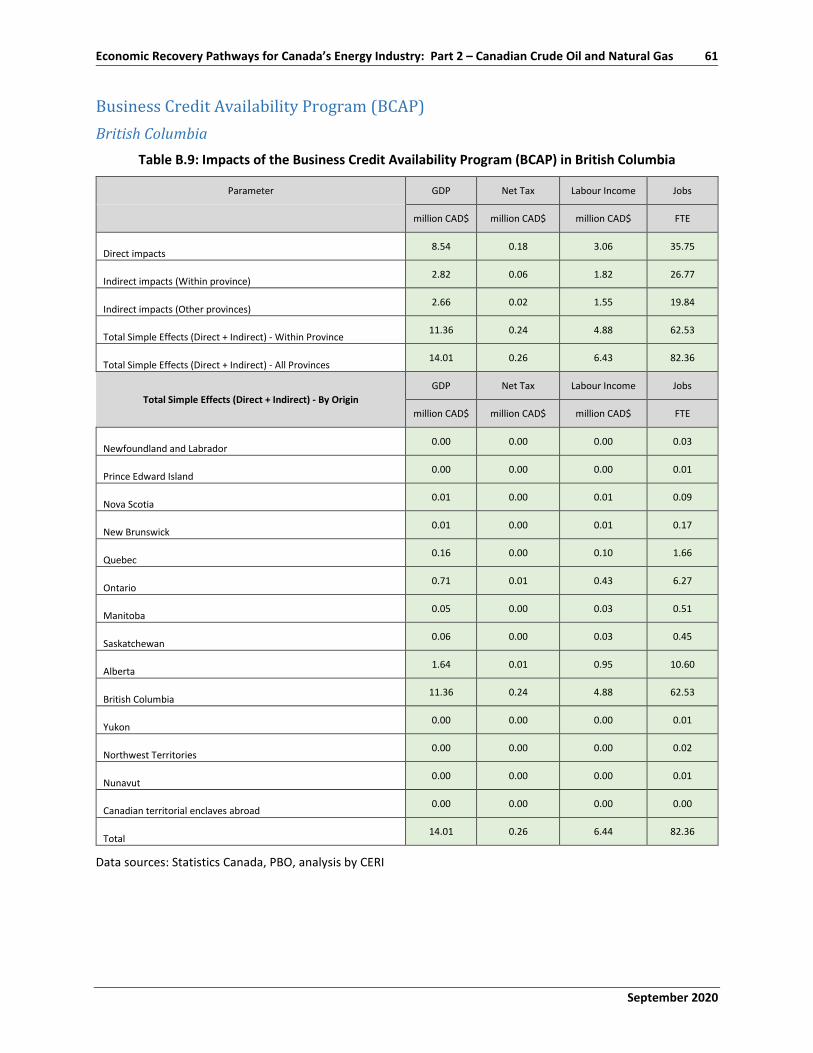

Table B.9: Impacts of the Business Credit Availability Program (BCAP) in British Columbia ...................... 61

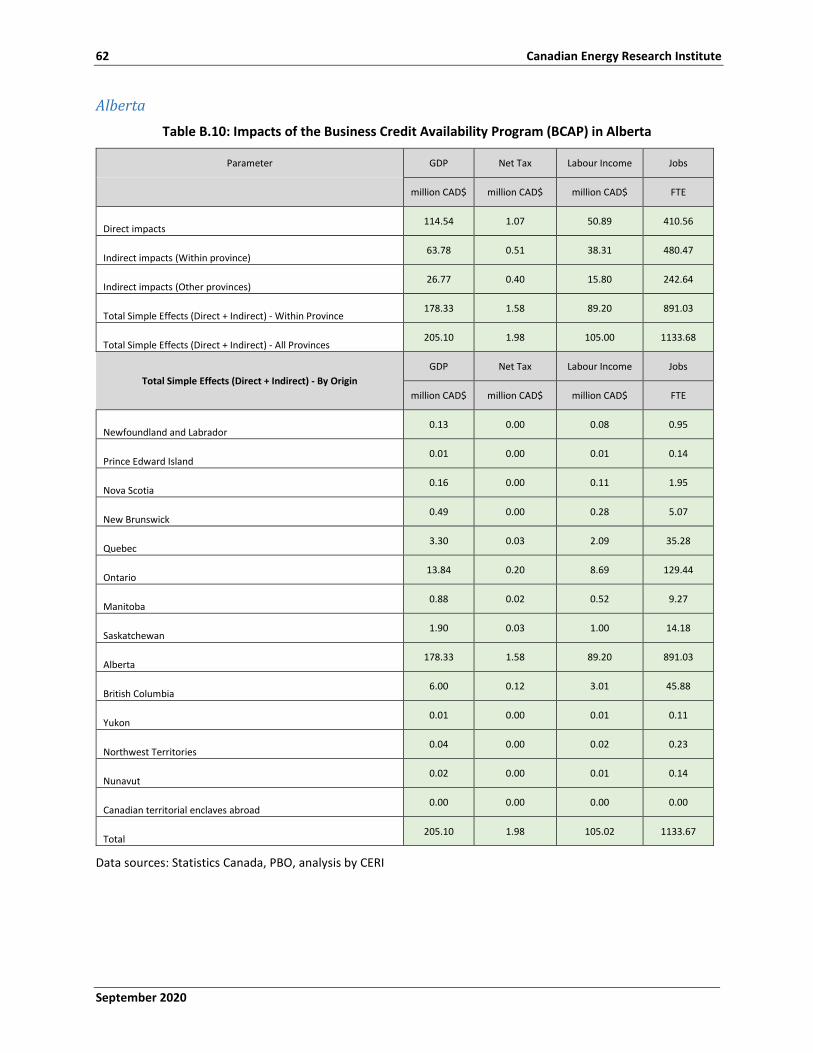

Table B.10: Impacts of the Business Credit Availability Program (BCAP) in Alberta .................................. 62

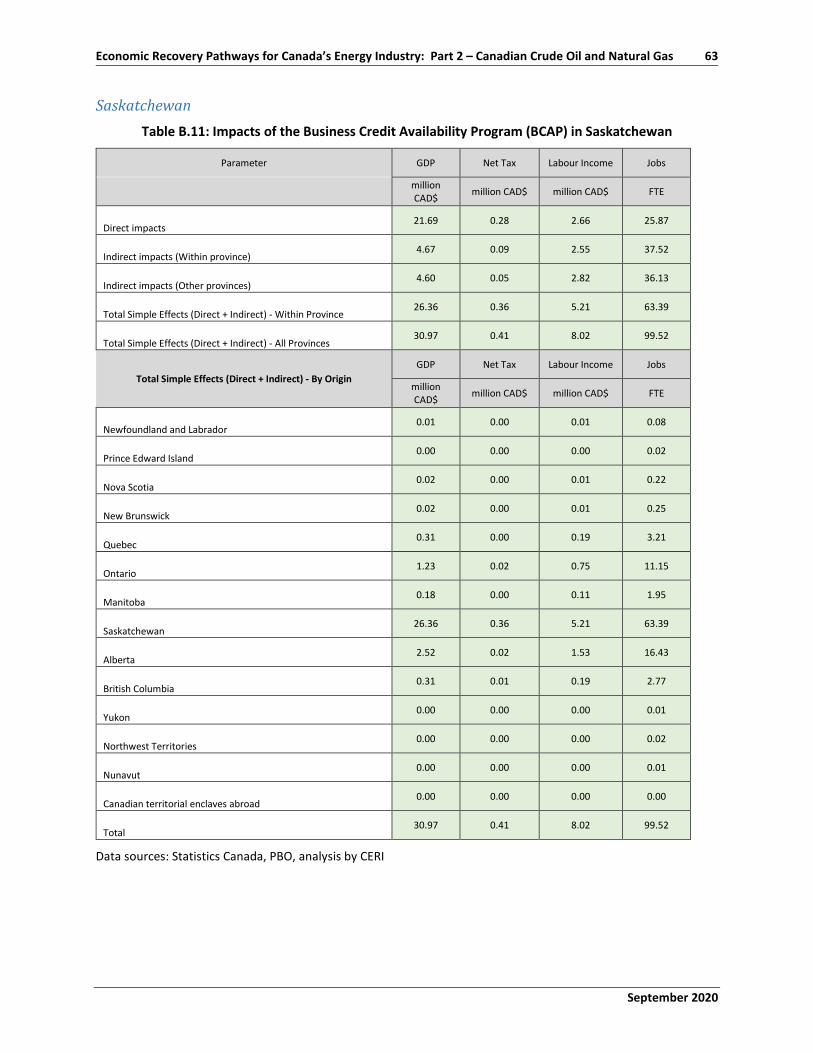

Table B.11: Impacts of the Business Credit Availability Program (BCAP) in Saskatchewan ....................... 63

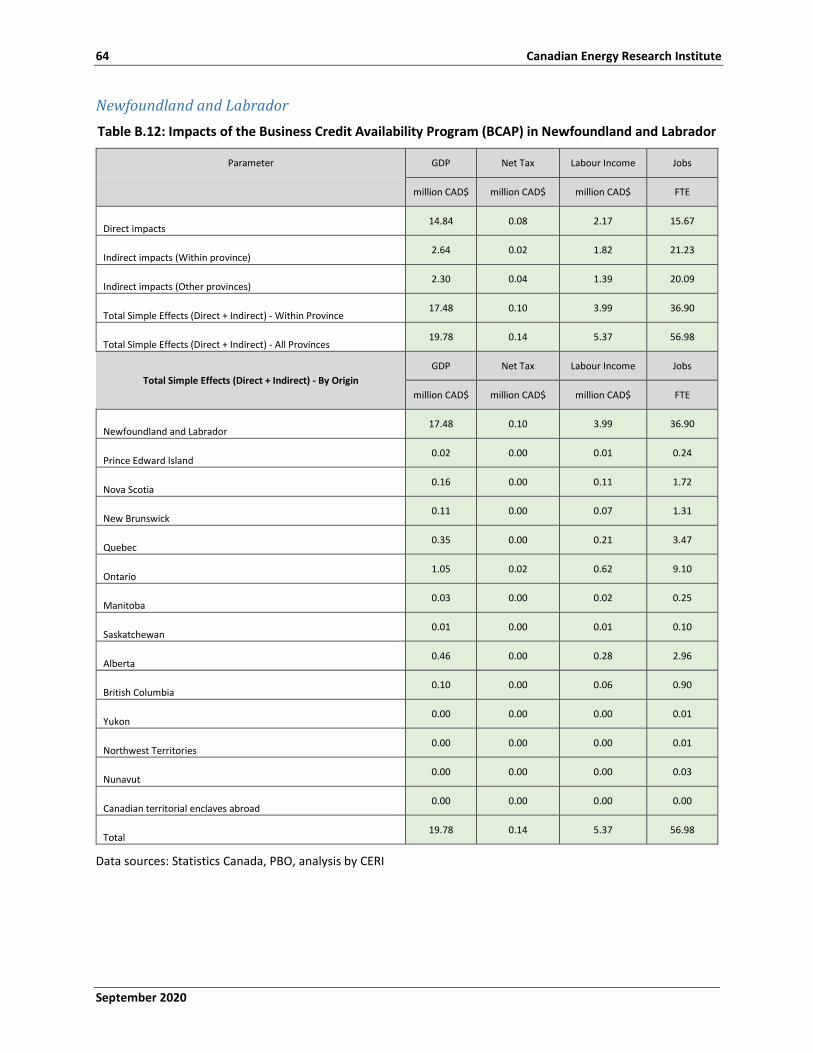

Table B.12: Impacts of the Business Credit Availability Program (BCAP) in Newfoundland and Labrador 64

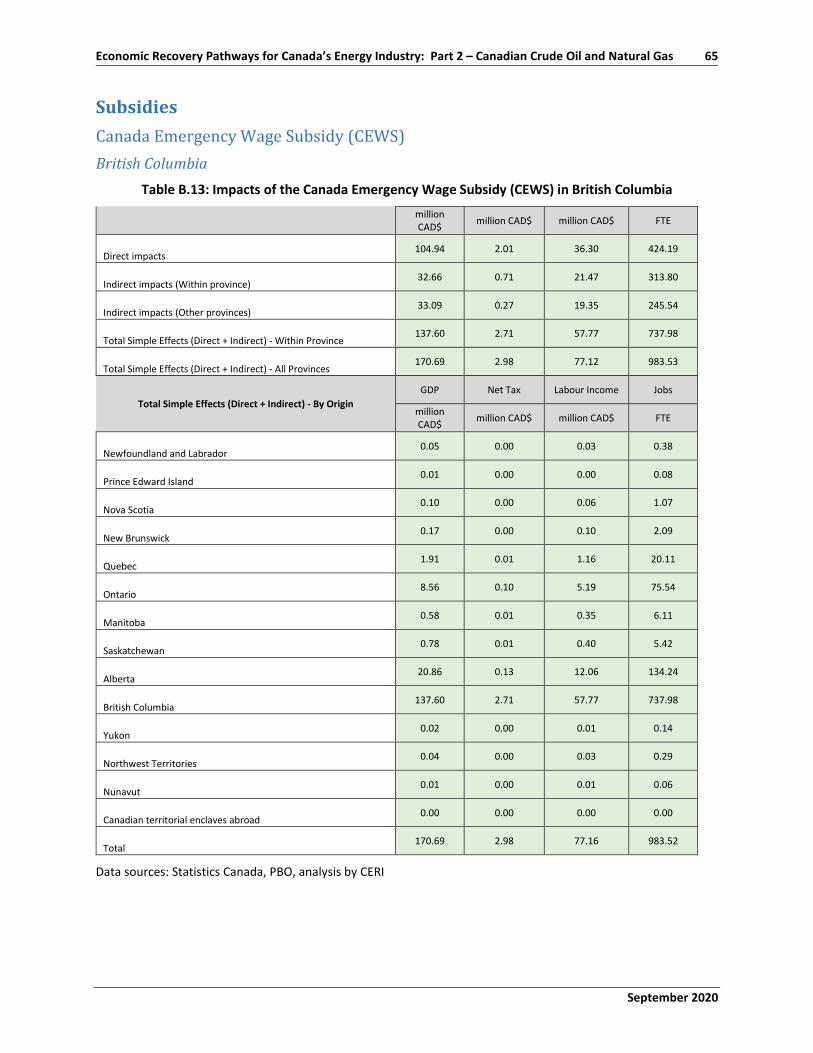

Table B.13: Impacts of the Canada Emergency Wage Subsidy (CEWS) in British Columbia ....................... 65

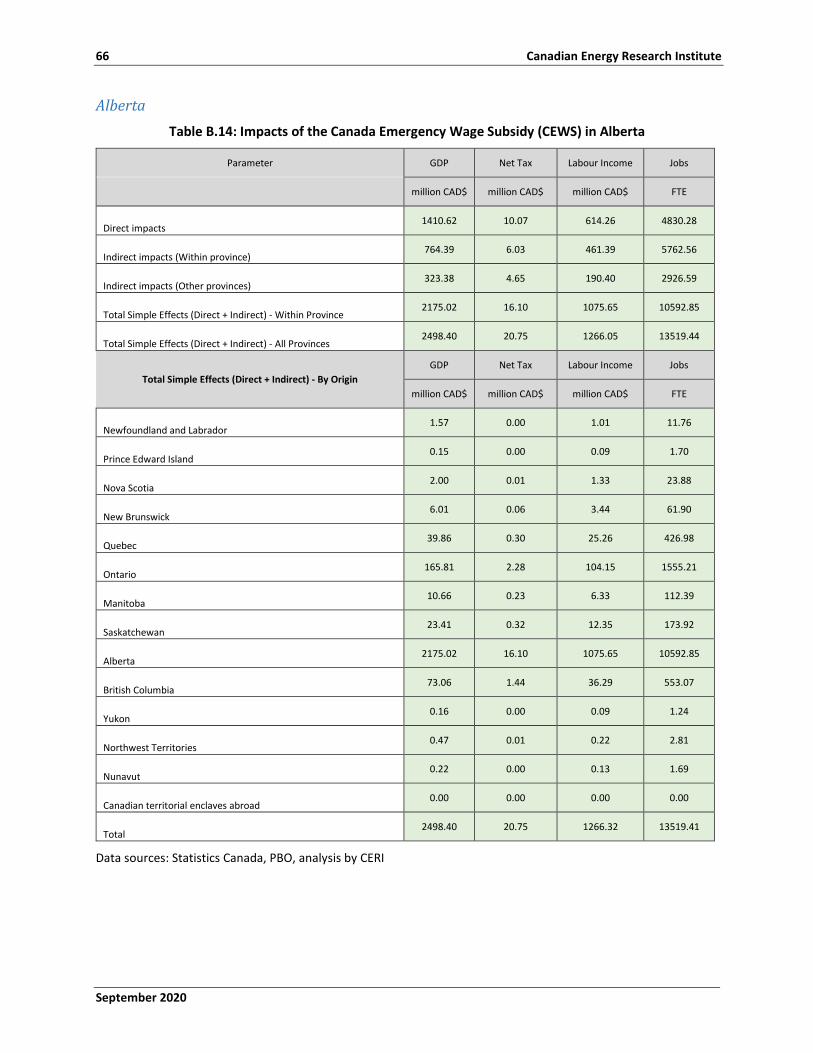

Table B.14: Impacts of the Canada Emergency Wage Subsidy (CEWS) in Alberta ..................................... 66

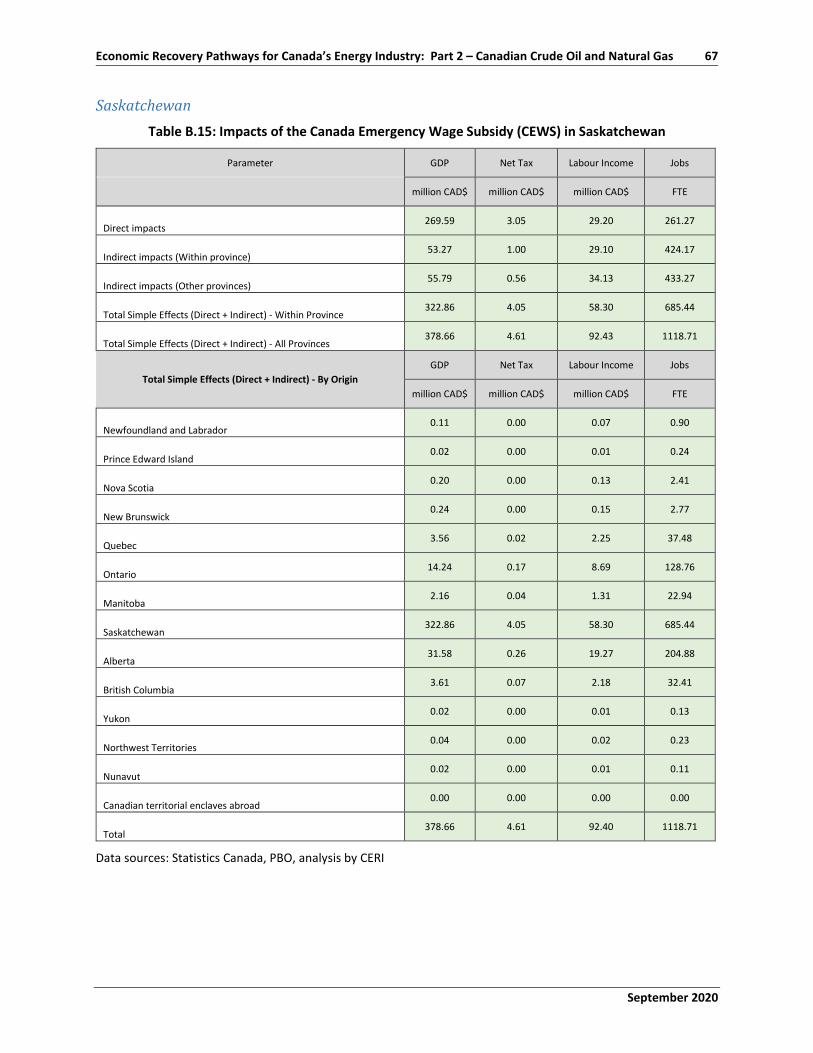

Table B.15: Impacts of the Canada Emergency Wage Subsidy (CEWS) in Saskatchewan .......................... 67

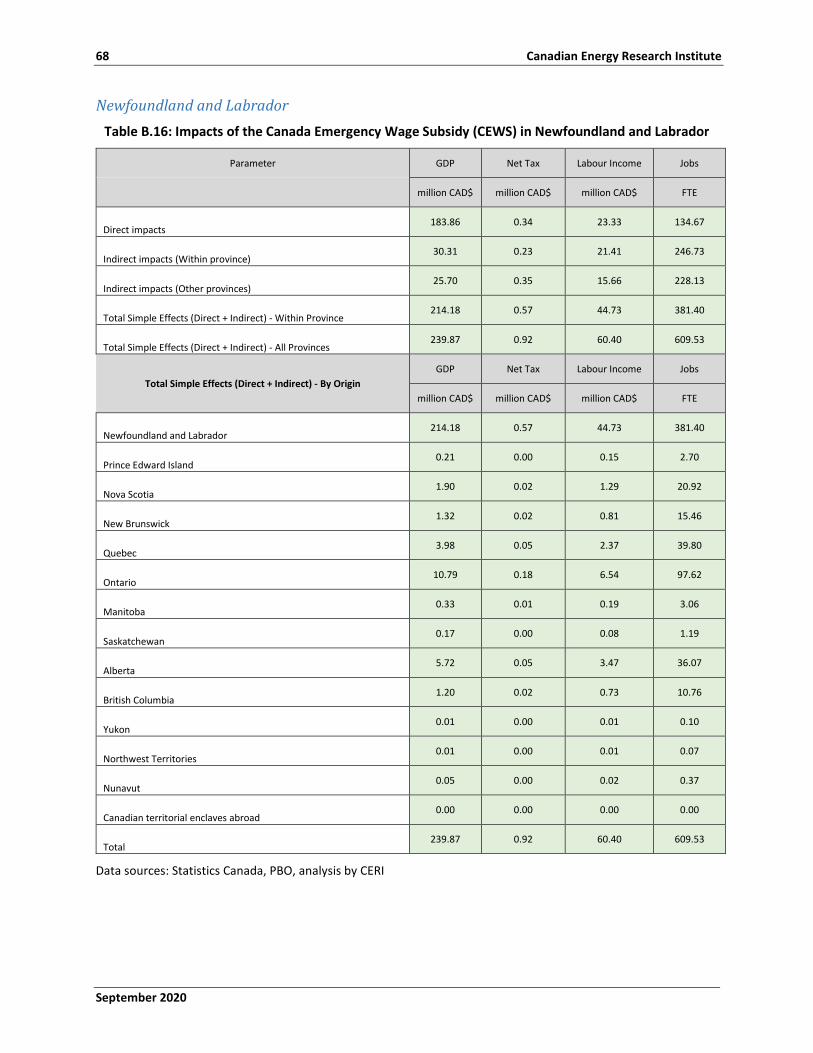

Table B.16: Impacts of the Canada Emergency Wage Subsidy (CEWS) in Newfoundland and Labrador ... 68

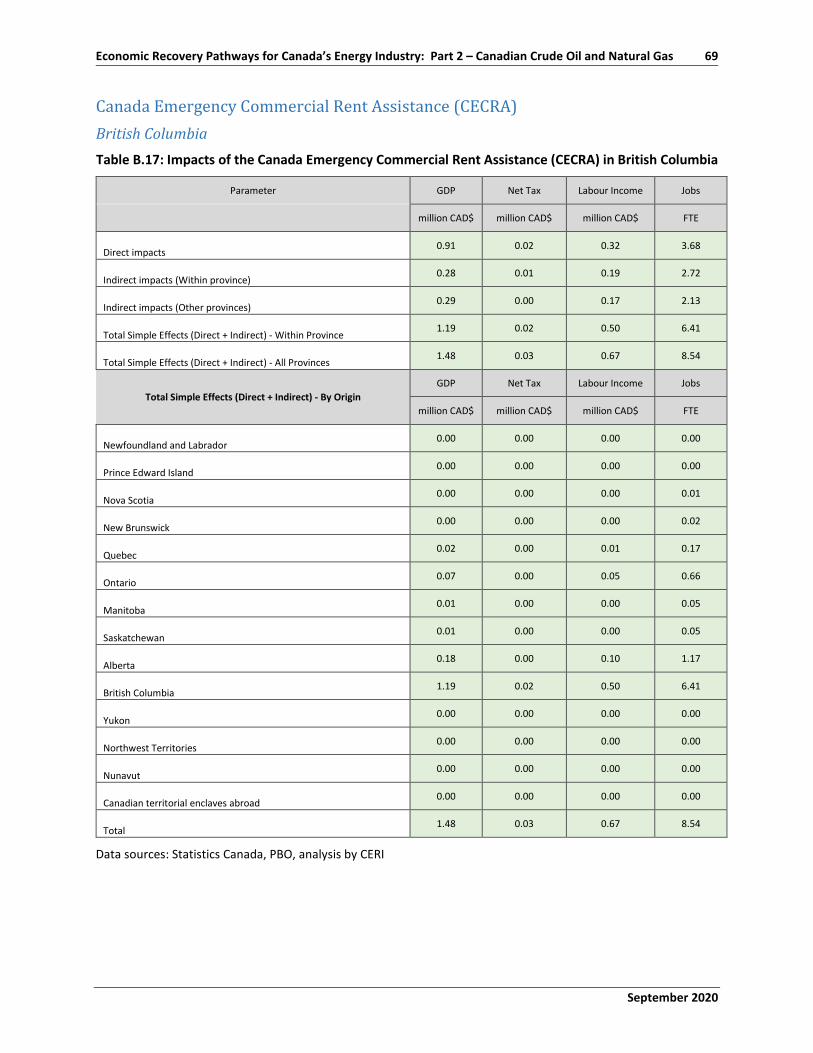

Table B.17: Impacts of the Canada Emergency Commercial Rent Assistance (CECRA) in British Columbia .................................................................................................................................................................... 69

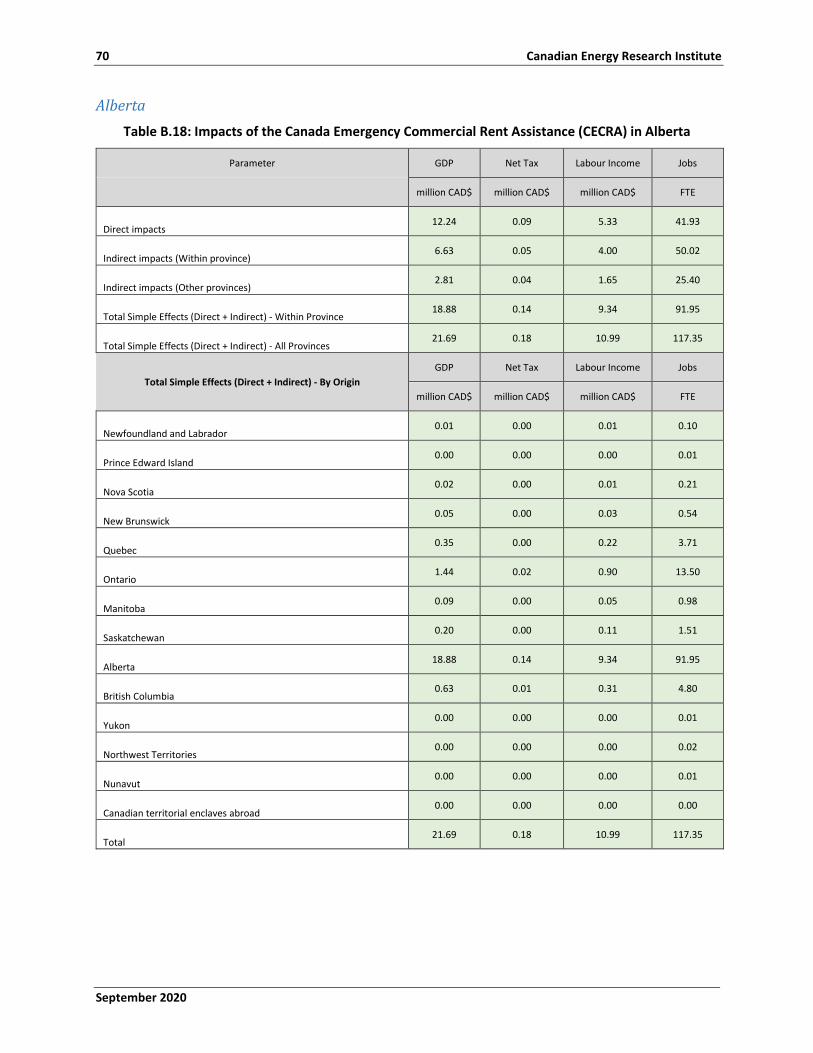

Table B.18: Impacts of the Canada Emergency Commercial Rent Assistance (CECRA) in Alberta ............. 70

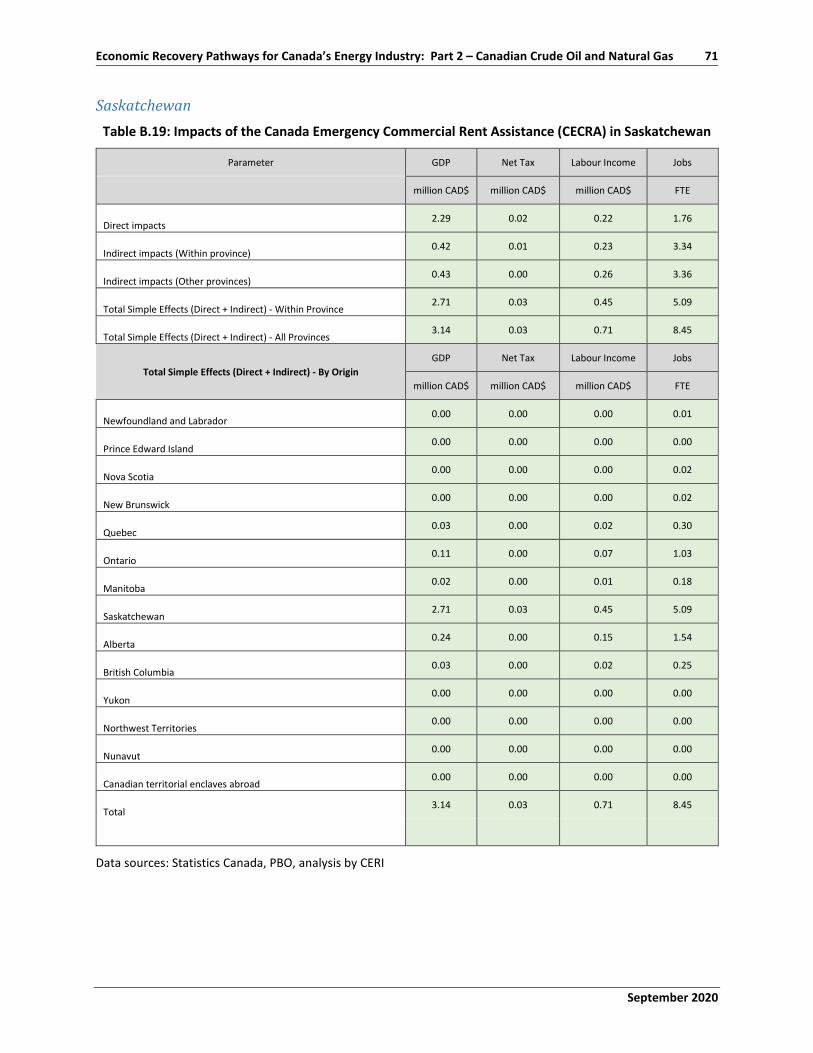

Table B.19: Impacts of the Canada Emergency Commercial Rent Assistance (CECRA) in Saskatchewan .. 71

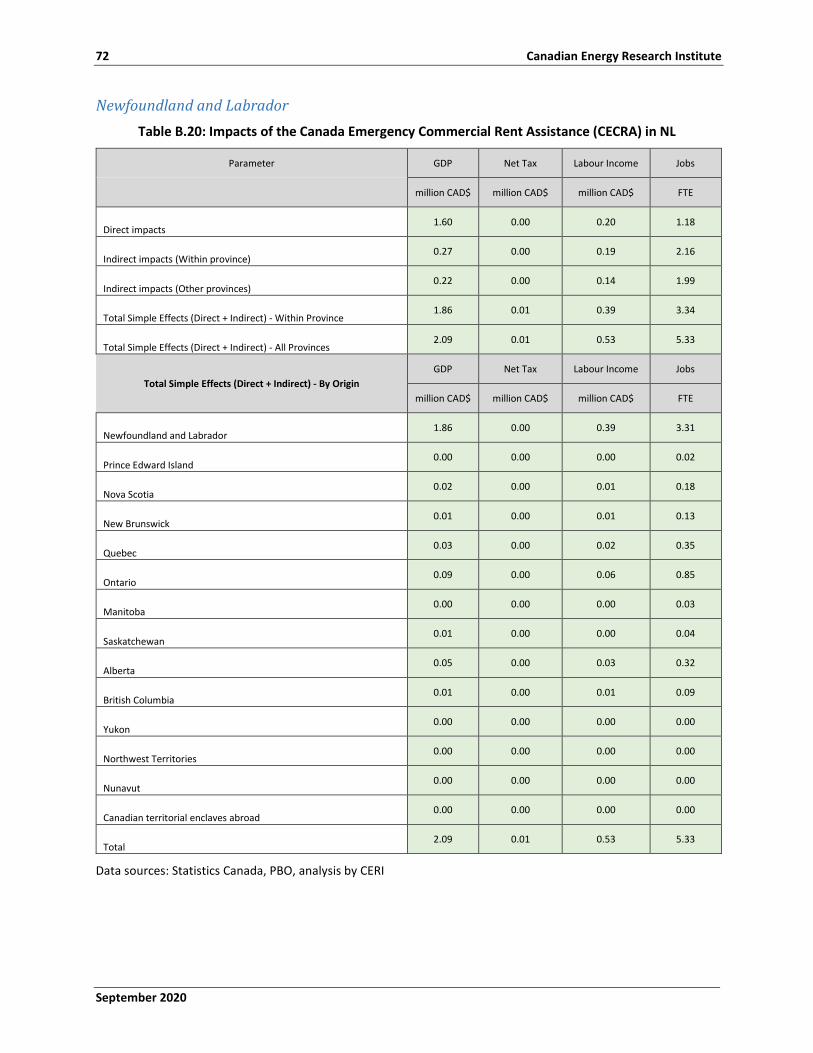

Table B.20: Impacts of the Canada Emergency Commercial Rent Assistance (CECRA) in NL ..................... 72

viii Canadian Energy Research Institute

September 2020

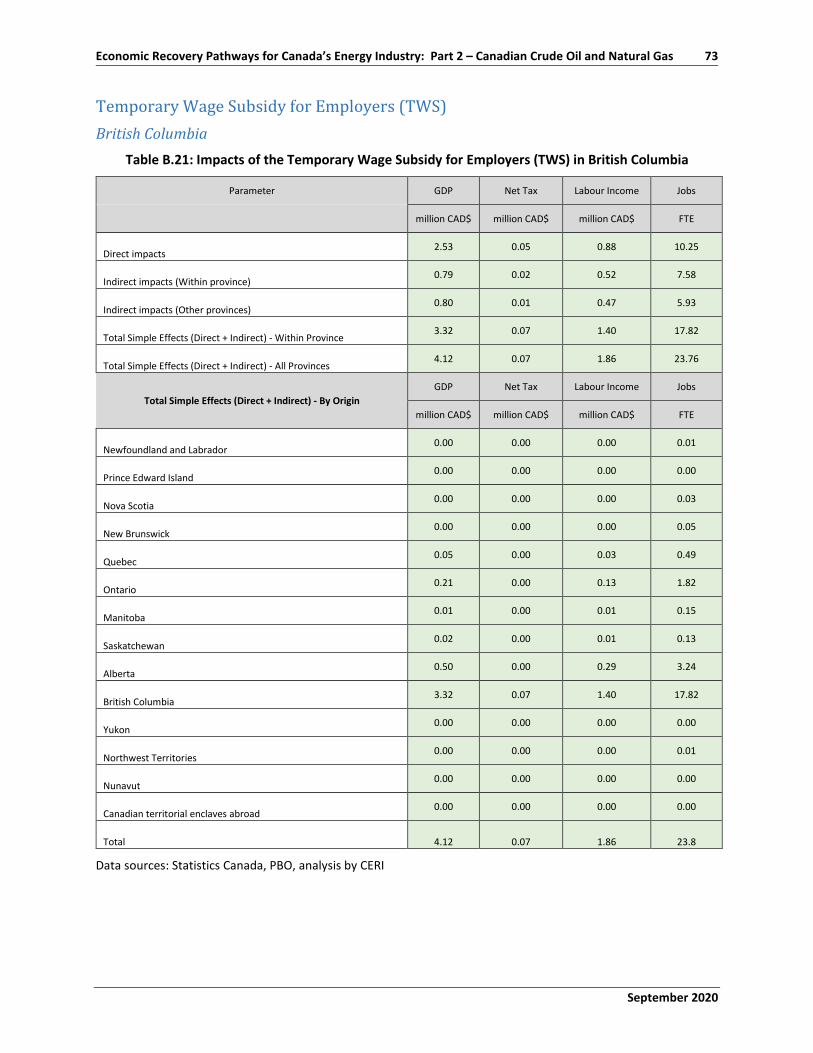

Table B.21: Impacts of the Temporary Wage Subsidy for Employers (TWS) in British Columbia .............. 73

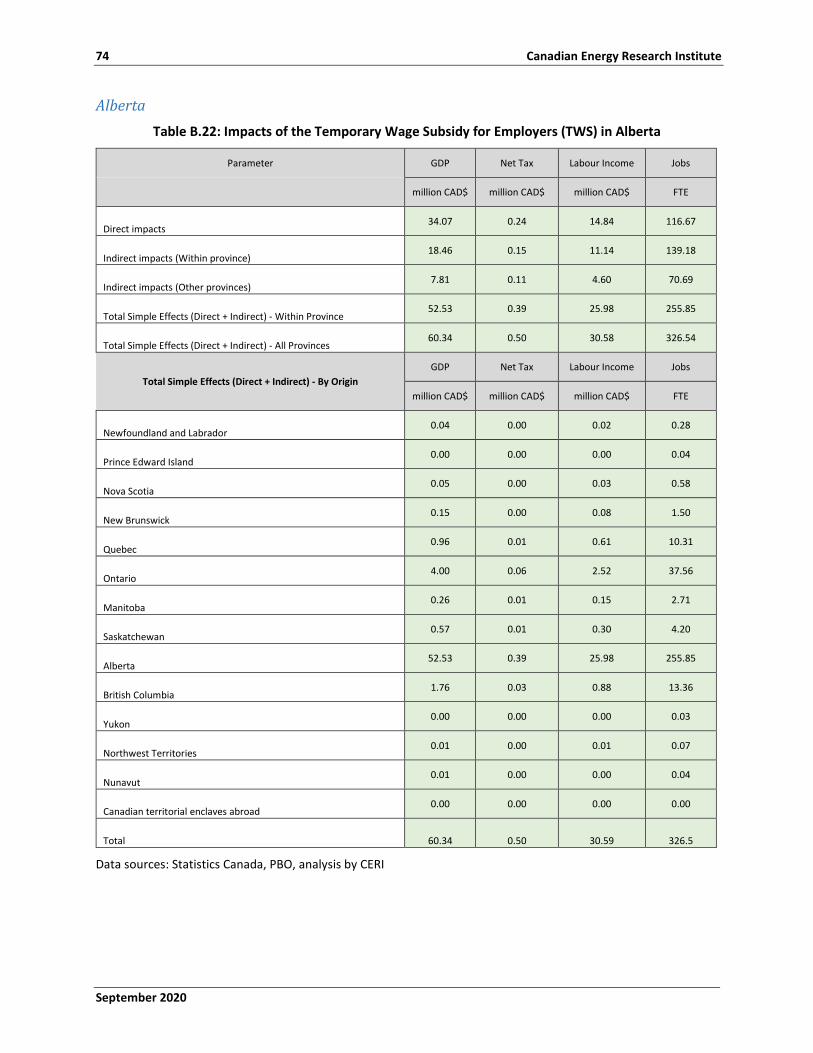

Table B.22: Impacts of the Temporary Wage Subsidy for Employers (TWS) in Alberta ............................. 74

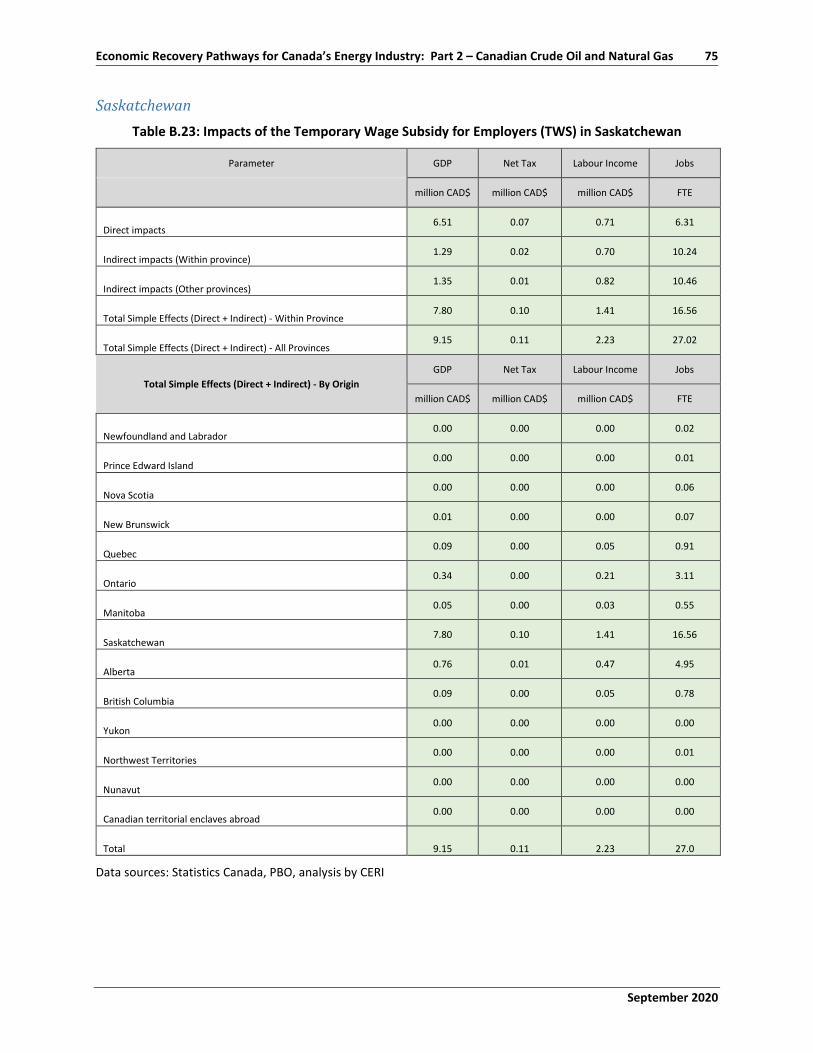

Table B.23: Impacts of the Temporary Wage Subsidy for Employers (TWS) in Saskatchewan .................. 75

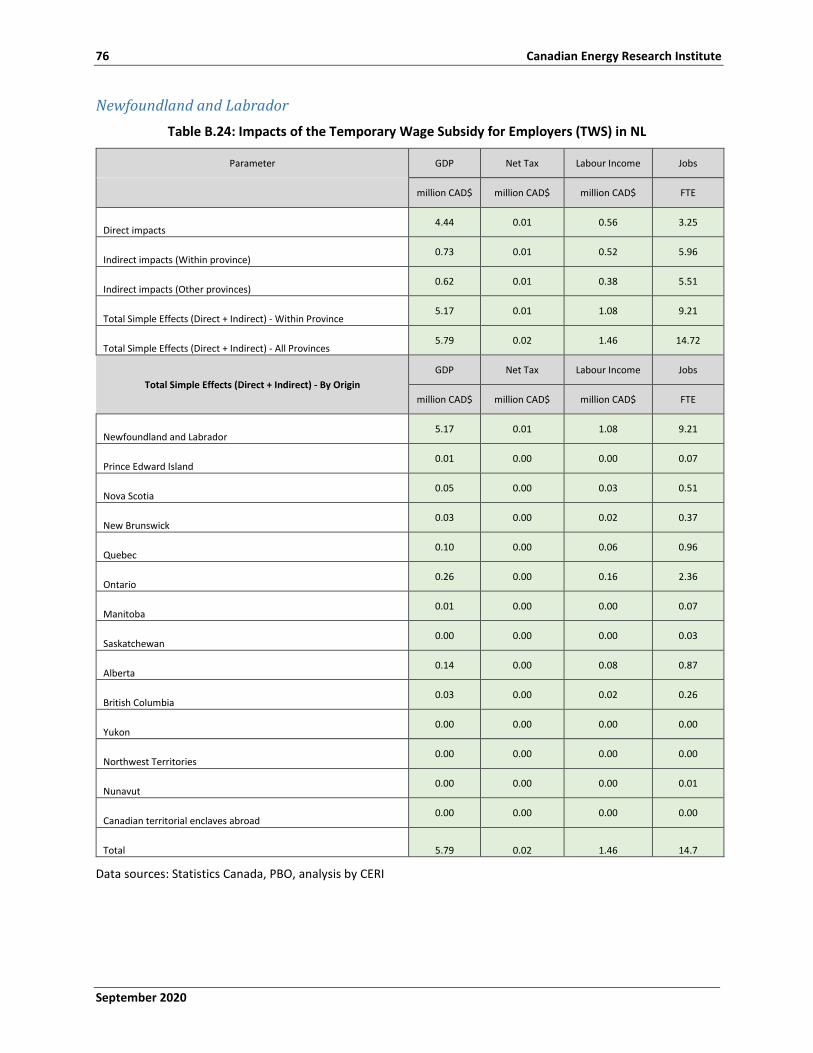

Table B.24: Impacts of the Temporary Wage Subsidy for Employers (TWS) in NL ..................................... 76

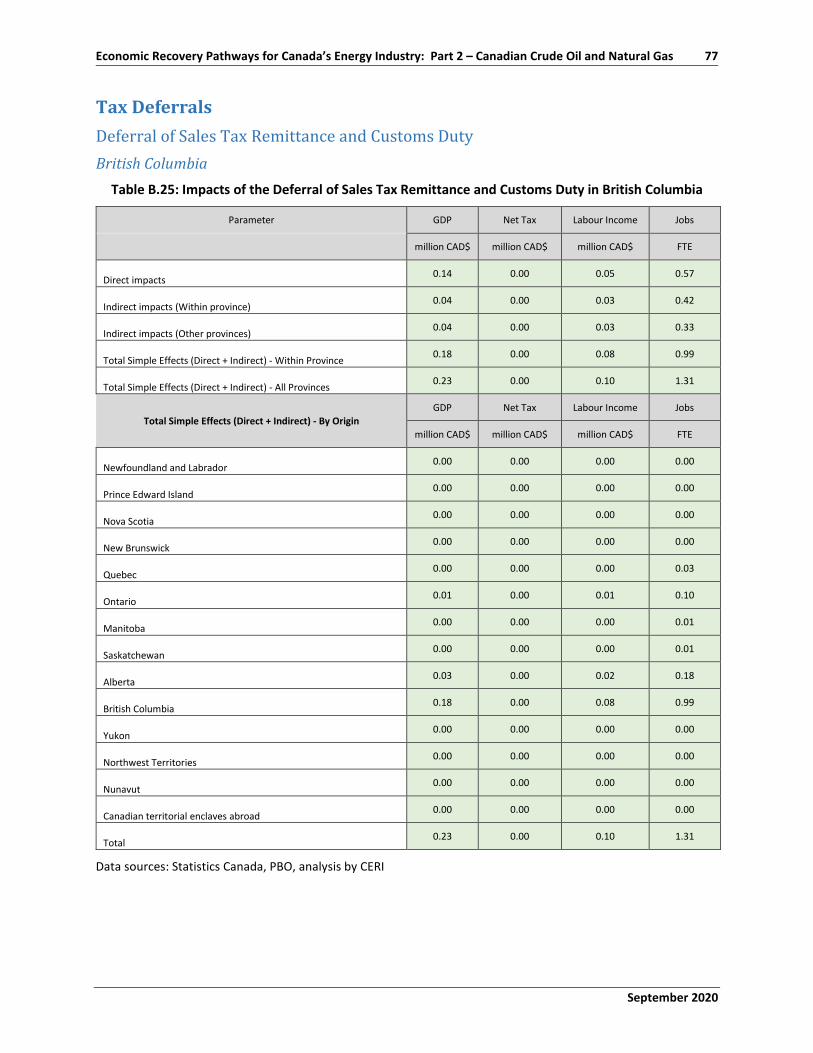

Table B.25: Impacts of the Deferral of Sales Tax Remittance and Customs Duty in British Columbia ....... 77

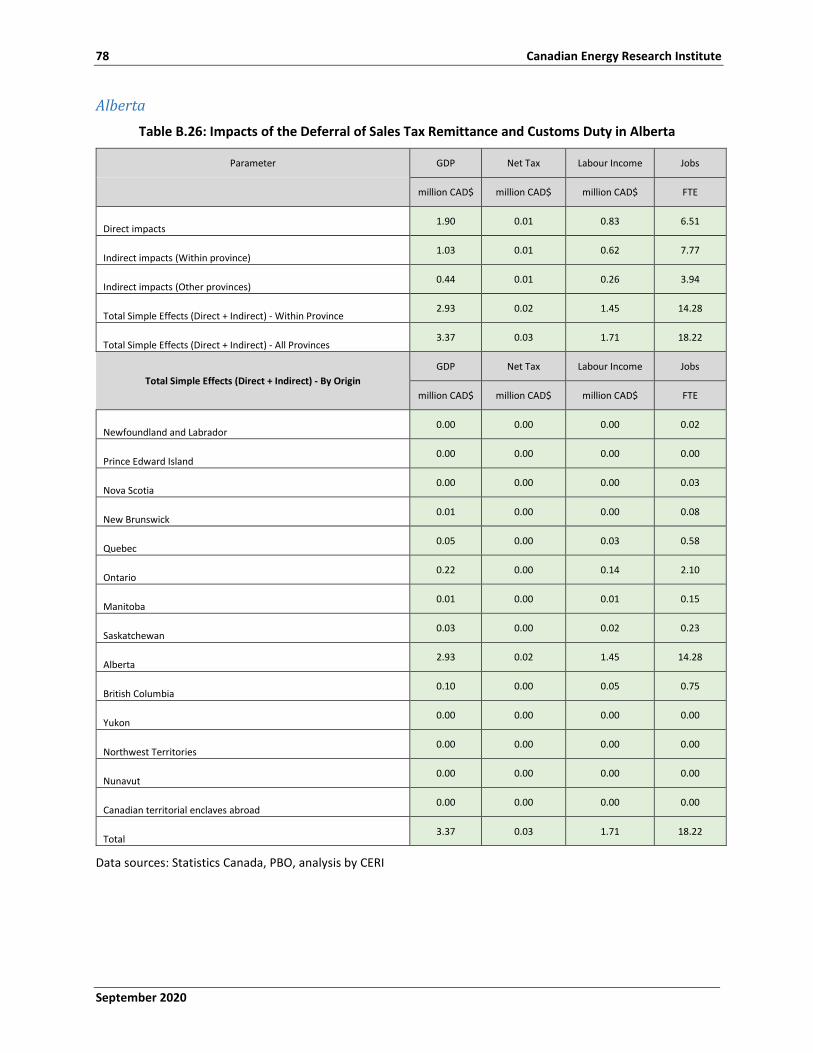

Table B.26: Impacts of the Deferral of Sales Tax Remittance and Customs Duty in Alberta ...................... 78

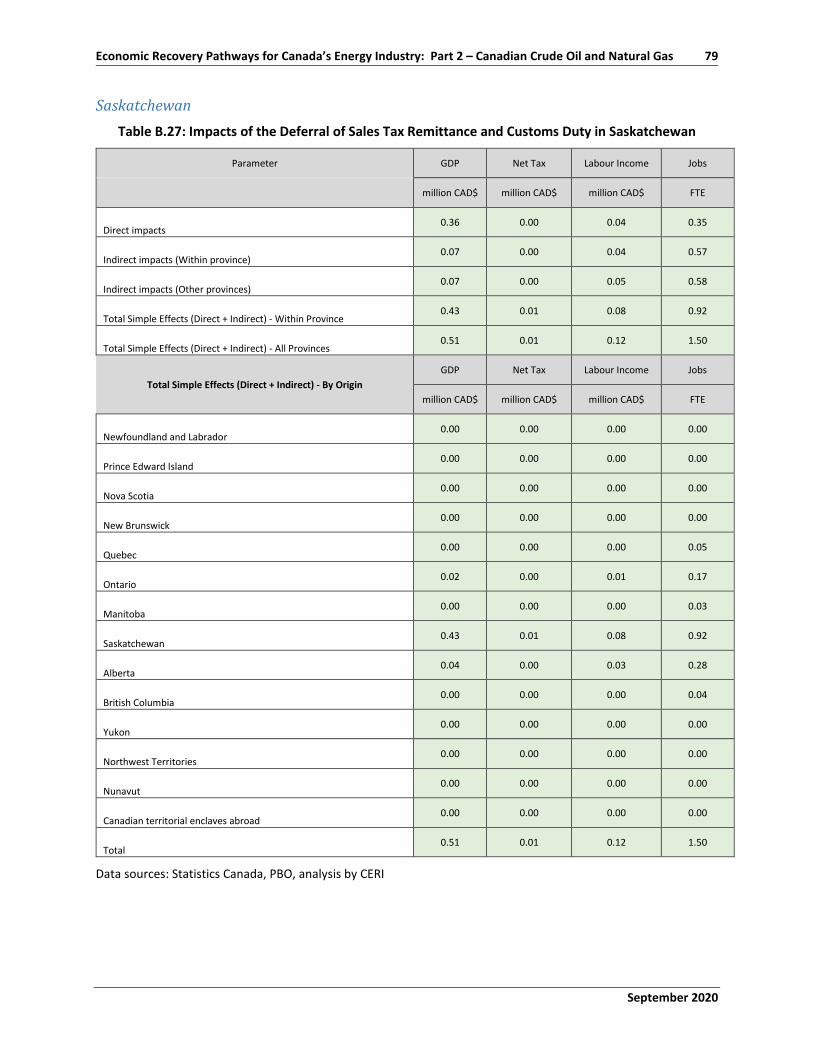

Table B.27: Impacts of the Deferral of Sales Tax Remittance and Customs Duty in Saskatchewan ........... 79

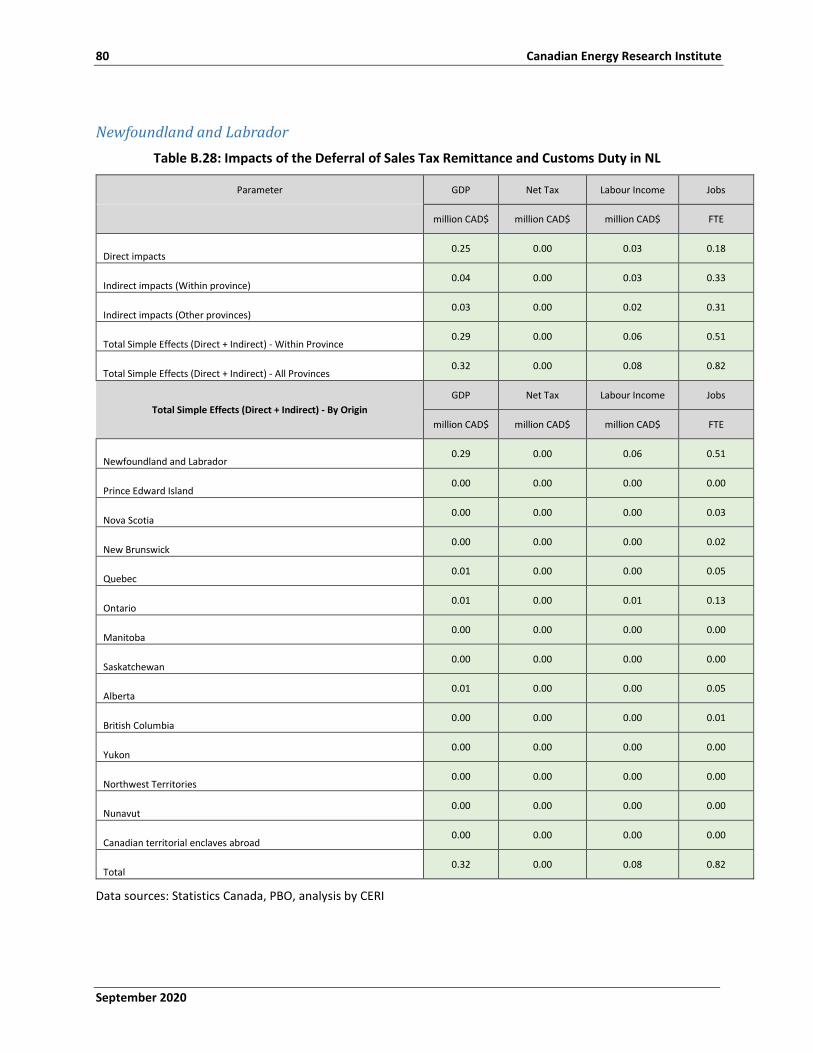

Table B.28: Impacts of the Deferral of Sales Tax Remittance and Customs Duty in NL ............................. 80

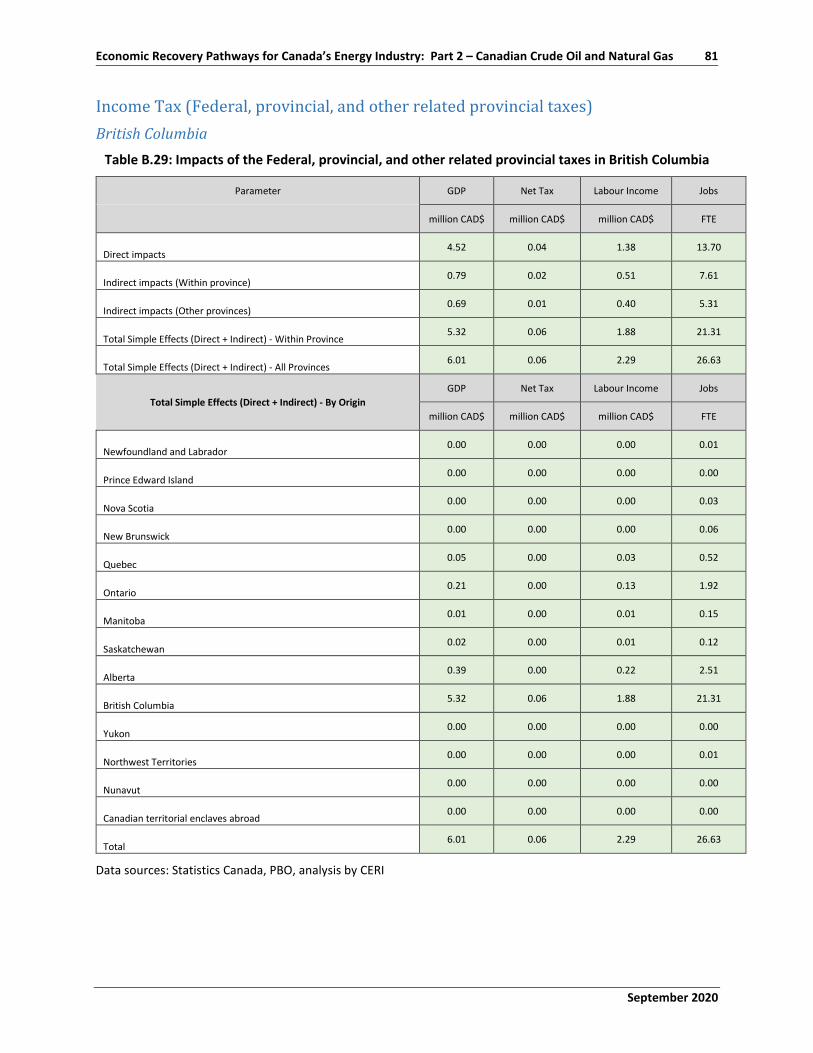

Table B.29: Impacts of the Federal, provincial, and other related provincial taxes in British Columbia .... 81

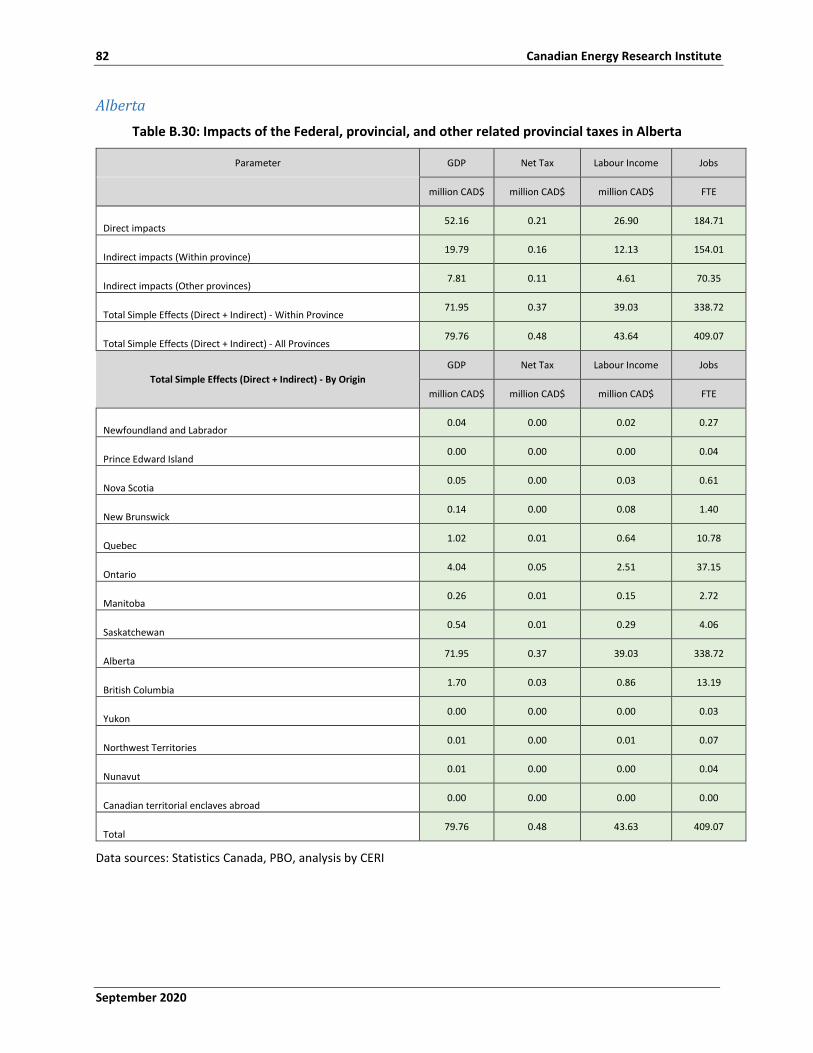

Table B.30: Impacts of the Federal, provincial, and other related provincial taxes in Alberta .................. 82

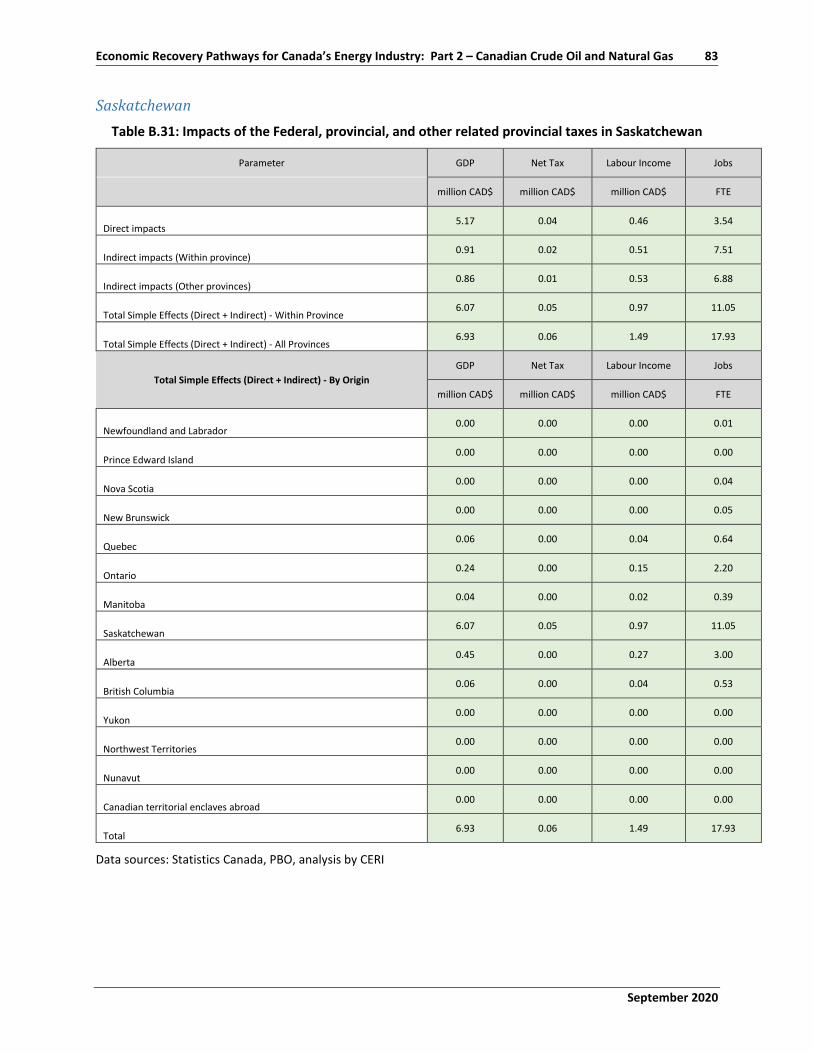

Table B.31: Impacts of the Federal, provincial, and other related provincial taxes in Saskatchewan ....... 83

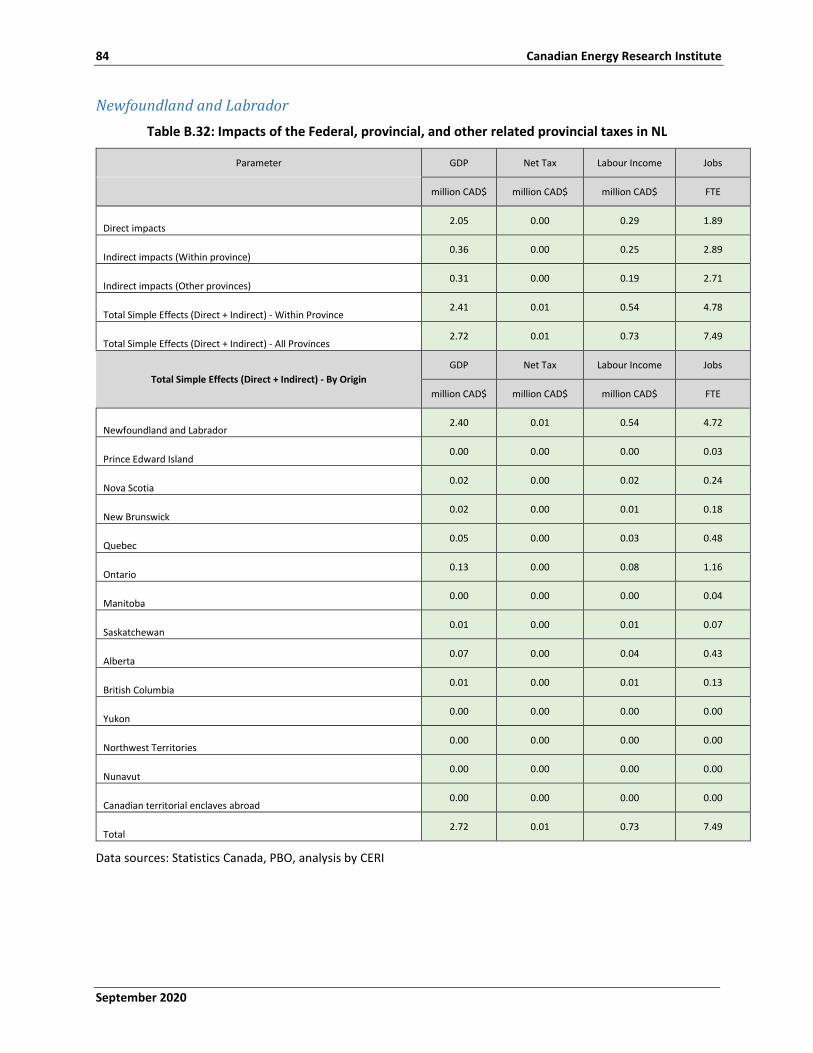

Table B.32: Impacts of the Federal, provincial, and other related provincial taxes in NL .......................... 84

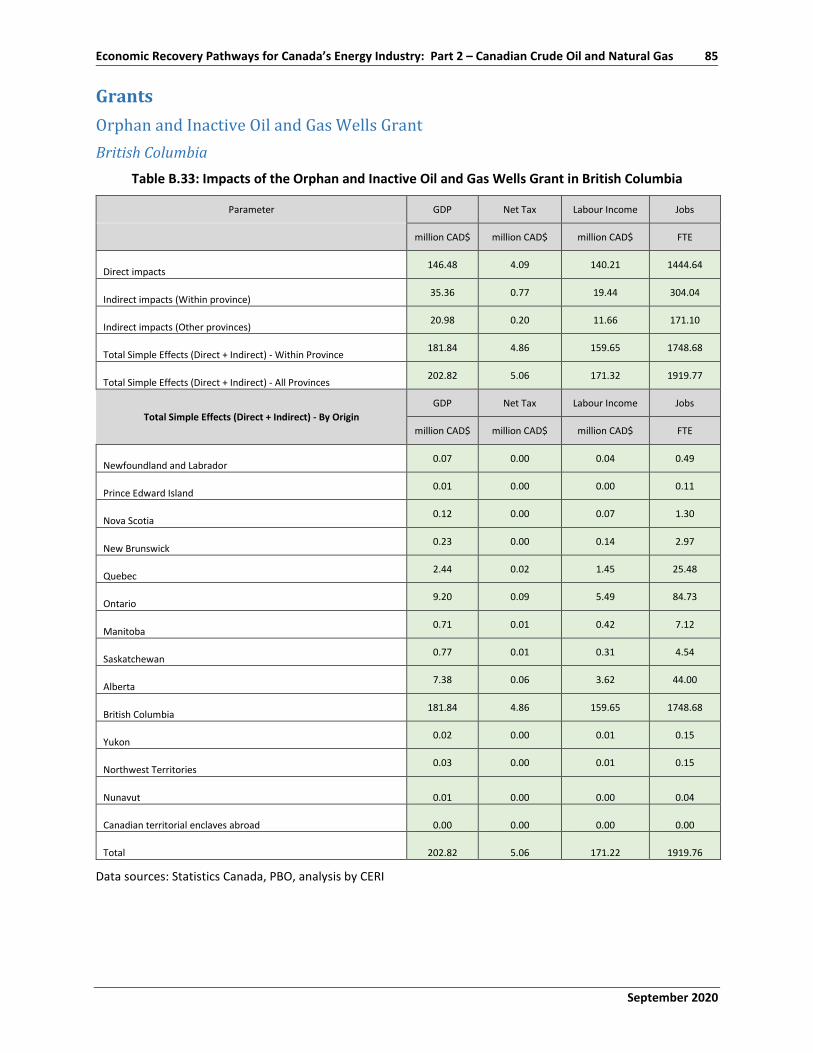

Table B.33: Impacts of the Orphan and Inactive Oil and Gas Wells Grant in British Columbia .................. 85

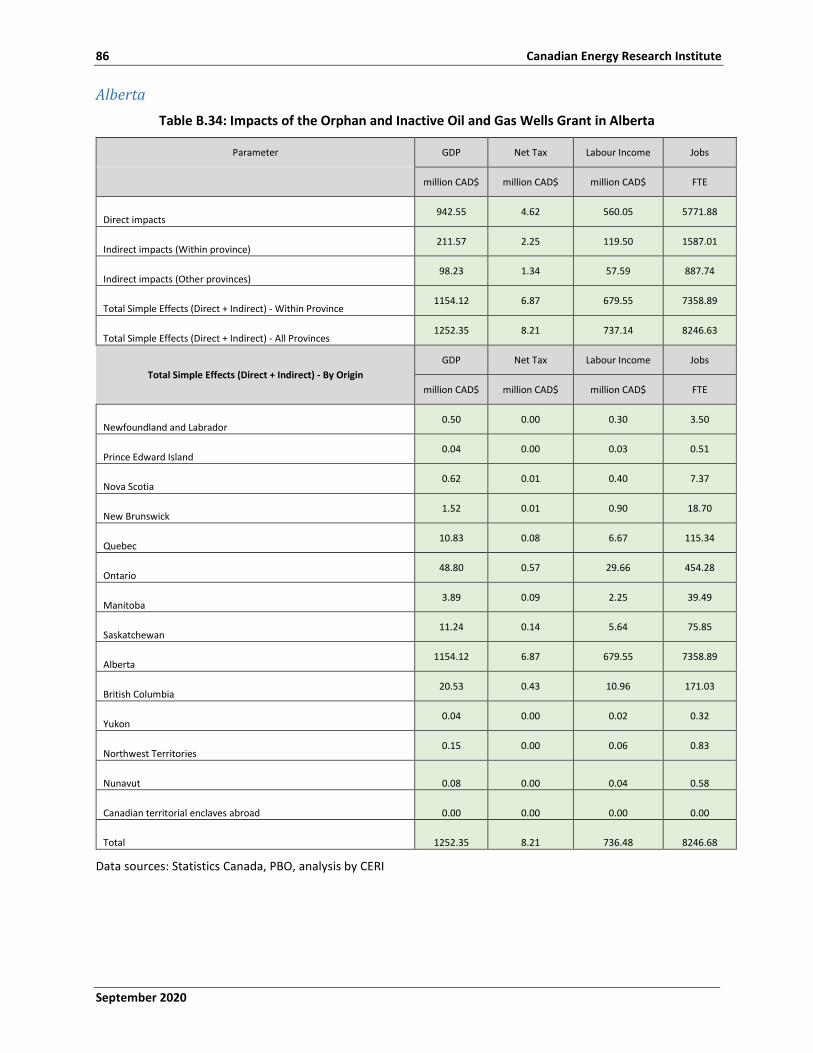

Table B.34: Impacts of the Orphan and Inactive Oil and Gas Wells Grant in Alberta ................................ 86

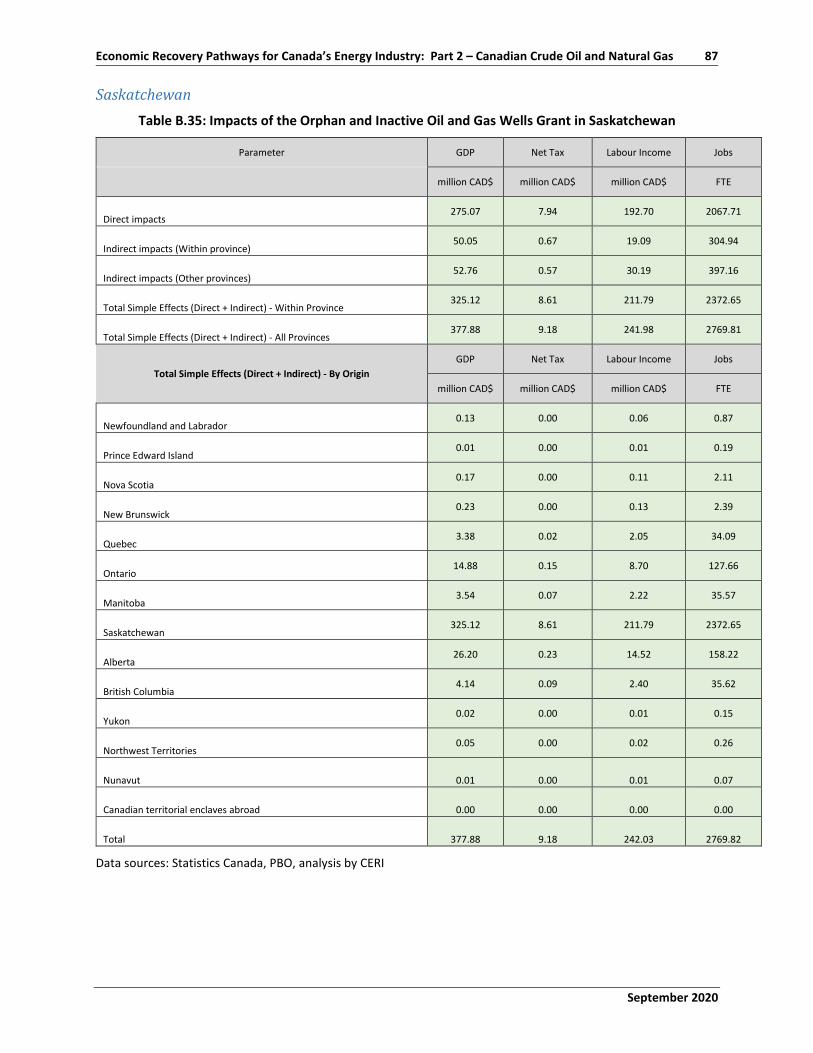

Table B.35: Impacts of the Orphan and Inactive Oil and Gas Wells Grant in Saskatchewan ..................... 87

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas ix

Acronyms and Abbreviations AB Alberta

ACOA Atlantic Canada Opportunities Agency

AECO Alberta Energy Company

AT1 Additional Tier 1

BC British Columbia

BCAP Business Credit Availability Program

BDC Business Development Bank of Canada

CAD Canadian Dollars

CanNor Canadian Northern Economic Development Agency

CBC Canadian Broadcasting Corporation

CBSA Canada Board Services Agency

CEBA Canada Emergency Business Account

CECRA Canada Emergency Commercial Rent Assistance

CEDQ Canada Economic Development for Quebec Regions

CERI Canadian Energy Research Institute

CEWS Canada Emergency Wage Subsidy

COVID-19 Corona Virus Disease 2019

CPA Chartered Professional Accountant

CRA Canada Revenue Agency

DWF Decommissioning Work Funding

EDC Export Development Canada

ERF Emissions Reduction Fund

E&P Exploration and Production

FedDev Federal Economic Development Agency for Southern Ontario

FedNor Federal Economic Development Initiative in Northern Ontario

FTE Full-Time Equivalent

GDP Gross Domestic Product

IEA International Energy Agency

x Canadian Energy Research Institute

September 2020

I-O Input-Output

kbpd Thousand barrels per day

KXL Keystone Export Limited

LEEFF Large Employer Emergency Financing Facility

LMI Labour Market Information

LNG Liquified Natural Gas

MMbpd Million barrels per day

MMcf/d Million cubic feet per day

MRIO Multi-regional Input-Output

NEB National Energy Board

NL Newfoundland and Labrador

O&G Oil and Gas

OWA Orphan Well Association

PBO Parliamentary Budget Officer

Petro LMI Petroleum Labour Market Information

PLCAC Pipeline Contractors Association of Canada

PNG Petroleum and Natural Gas

PPE Personal Protective Equipment

PSAC Petroleum Services Association of Canada

Q1 First Quarter

Q2 Second Quarter

RRRF Regional Relief Recovery Fund

SK Saskatchewan

SWOT Strengths, Weaknesses, Opportunities and Threats

TWS Temporary Wage Subsidy

USD United States Dollar

WCB Workers' Compensation Board

WD Western Economic Diversification Canada

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas xi

Executive Summary Part 1 of the four part series, Economic Recovery Pathways for Canada’s Energy Industry, provided an overview of COVID-19 impacts on the energy sector. In Part 2, the Canadian Energy Research Institute (CERI) will review some of the central government assistance programs and assess how they can aid in the recovery of the oil and gas sector in Canada.

CERI’s Canadian Multi-regional Input-Output (MRIO) model was used to analyze the economic impacts of various relief measures for the sector as well as the economic impacts of oil and gas revenues generated from their operations. The economic impacts are determined in terms of major macroeconomic indicators such as impacts on GDP, employment, tax revenues and labour income. This report focuses on major oil and gas producing provinces. It is important to note that the economic impacts in this report are not limited to the producing provinces. The results include direct and indirect impacts on all Canadian provinces and territories (i.e. producing and non-producing).

The economic impacts of government relief measures are evaluated over the three years of 2020-2022. The results of the total economic impacts are as follows:

• The GDP impact of the stimulus packages over the period (Direct + Indirect) is CAD$7,936 million. • The total number of FTE jobs (Direct + Indirect) is 42,495 across Canada, with the most significant

impact to be felt in provinces where oil and gas is extracted. • The overall net tax impact is CAD$78 million. • The average annual income per person for the job created or preserved is CAD$91,600/year.

We show that relief measures could aid in the recovery of the oil and gas sector in the short term1. Still, it is not a panacea for the sector as there are broader market challenges.

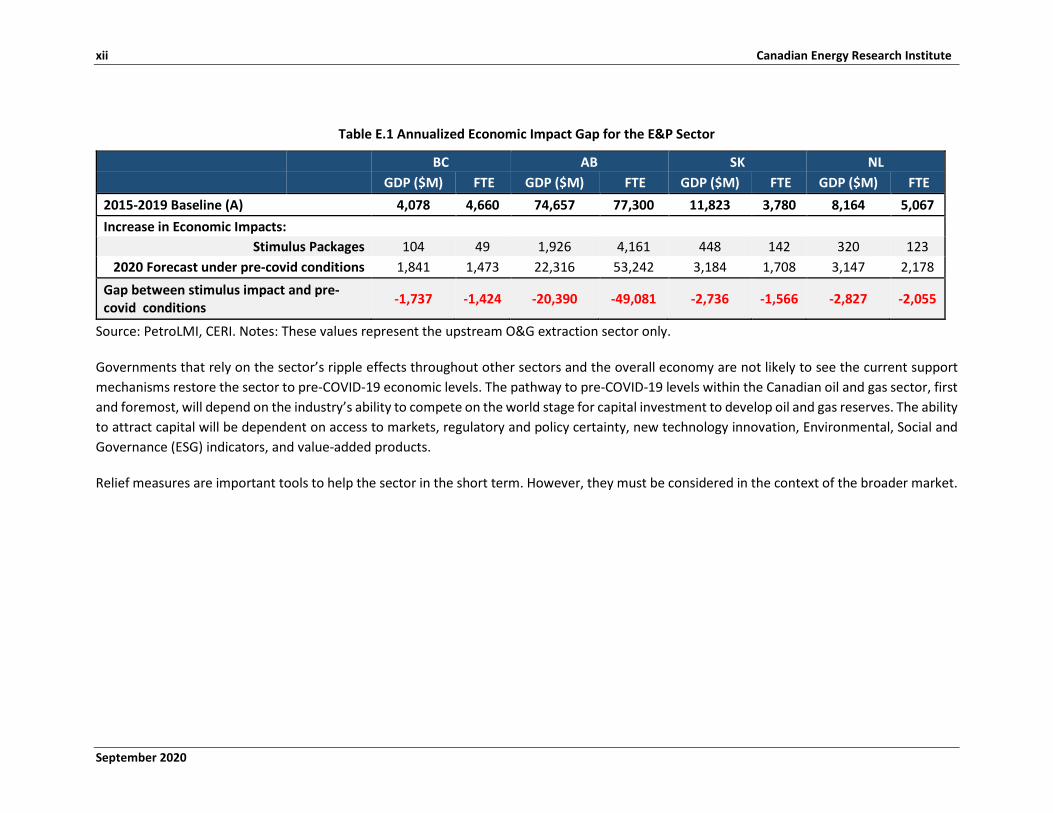

An illustrative example shown in Table E.1 highlights 2020 GDP and Employment direct impacts from both stimulus packages plus revenues and compares them to the historical 2015-2019 baseline for the upstream oil and gas sector in four oil and gas producing provinces. We note that the assessment of the stimulus packages creates some increase in job creation and GDP. However, a much larger impact on jobs and GDP can be forecasted if oil and gas markets were to return to pre-covid conditions. This means there is a gap between the economic activity supported by stimulus programs and revenues from the upstream oil and gas sector and the historical baseline, at least for the year 2020.

1 Two programs that CERI did not evaluate due to the nature of the programs are Large Employer Emergency Financing Facility (LEEFF) and the Emission Reduction Fund (ERF).

xii Canadian Energy Research Institute

September 2020

Table E.1 Annualized Economic Impact Gap for the E&P Sector

BC AB SK NL GDP ($M) FTE GDP ($M) FTE GDP ($M) FTE GDP ($M) FTE

2015-2019 Baseline (A) 4,078 4,660 74,657 77,300 11,823 3,780 8,164 5,067 Increase in Economic Impacts:

Stimulus Packages 104 49 1,926 4,161 448 142 320 123 2020 Forecast under pre-covid conditions 1,841 1,473 22,316 53,242 3,184 1,708 3,147 2,178

Gap between stimulus impact and pre-covid conditions -1,737 -1,424 -20,390 -49,081 -2,736 -1,566 -2,827 -2,055

Source: PetroLMI, CERI. Notes: These values represent the upstream O&G extraction sector only.

Governments that rely on the sector’s ripple effects throughout other sectors and the overall economy are not likely to see the current support mechanisms restore the sector to pre-COVID-19 economic levels. The pathway to pre-COVID-19 levels within the Canadian oil and gas sector, first and foremost, will depend on the industry’s ability to compete on the world stage for capital investment to develop oil and gas reserves. The ability to attract capital will be dependent on access to markets, regulatory and policy certainty, new technology innovation, Environmental, Social and Governance (ESG) indicators, and value-added products.

Relief measures are important tools to help the sector in the short term. However, they must be considered in the context of the broader market.

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 1

Chapter 1: Introduction and Background Introduction The COVID-19 pandemic has adversely impacted Canada's oil and natural gas industry (O&G), in addition to already limited egress for exports, volatile crude oil prices, and increased competition even before the pandemic. By all internationally accepted analyses, fossil fuels will continue to be in demand for the foreseeable future.

Part 1 of this four-part series, Economic Recovery Pathways of Canada’s Energy Industry, introduced many of the COVID-19 impacts on the oil and gas sector. In Part 2), the Canadian Energy Research Institute (CERI) will review central government assistance programs and assess how they can aid in the recovery of the oil and gas sector in Canada. Government aid programs have been organized into four major categories: credit loans, subsidies, tax deferrals, and grants. The analysis includes an assessment of the economic impacts of oil and gas revenues generated from the sector’s operations.

Background - Summary Statistics Prior to the COVID-19 pandemic, market access, regulatory uncertainty, and the actions of OPEC+ were already having a negative impact on employment rates and performance within the O&G sector.

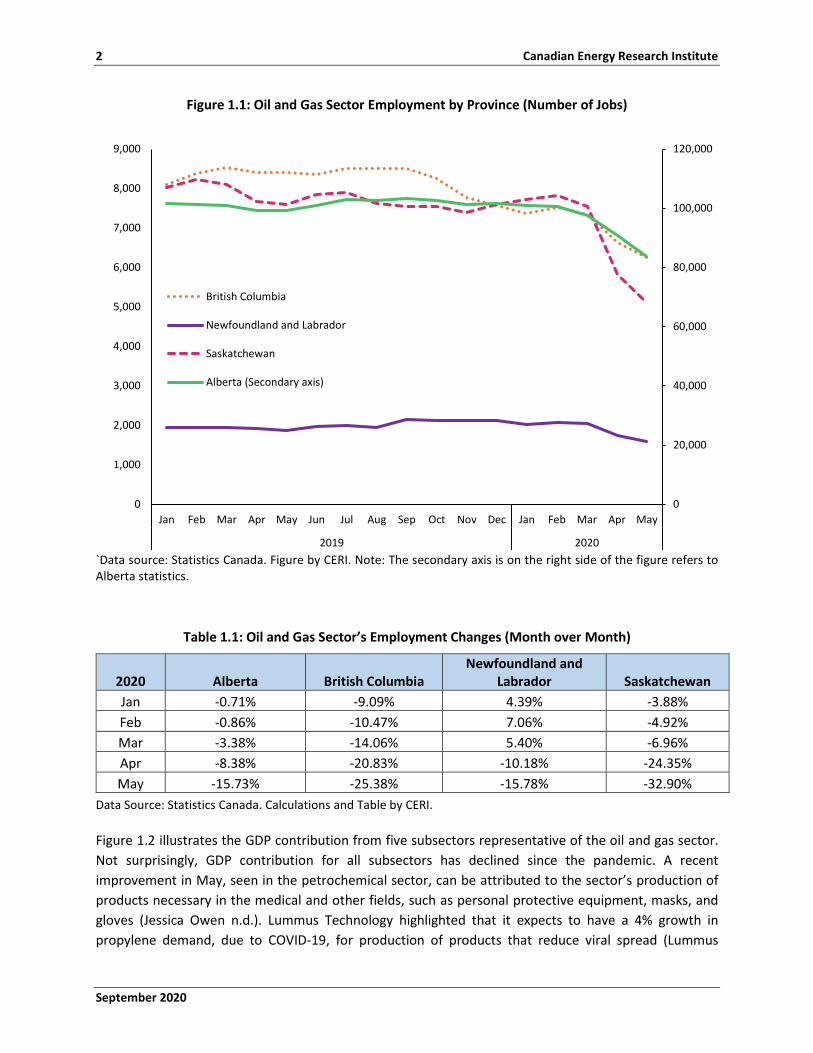

Figure 1.1 shows monthly provincial employment rates within the oil and gas sector from January 2019 to May 2020 (the most recent monthly data available at the time of writing). Alberta saw the highest decline in number of jobs with a loss of almost 14,000 jobs from March to May 2020. Since the pandemic, and the ensuing country-wide lock-down introduced in March, unemployment rates have increased in all oil and gas producing provinces. It is uncertain how long it will be before the sector returns to pre-pandemic employment levels (Statistics Canada 2020a). The steepest rate of decline in employment was observed in Saskatchewan, with a -17.39% drop in employment from March to May 2020, followed by British Columbia and Alberta. (see Table 1.1 for provincial percentage change in employment).

2 Canadian Energy Research Institute

September 2020

Figure 1.1: Oil and Gas Sector Employment by Province (Number of Jobs)

`Data source: Statistics Canada. Figure by CERI. Note: The secondary axis is on the right side of the figure refers to Alberta statistics.

Table 1.1: Oil and Gas Sector’s Employment Changes (Month over Month)

2020 Alberta British Columbia Newfoundland and

Labrador Saskatchewan Jan -0.71% -9.09% 4.39% -3.88% Feb -0.86% -10.47% 7.06% -4.92% Mar -3.38% -14.06% 5.40% -6.96% Apr -8.38% -20.83% -10.18% -24.35% May -15.73% -25.38% -15.78% -32.90%

Data Source: Statistics Canada. Calculations and Table by CERI.

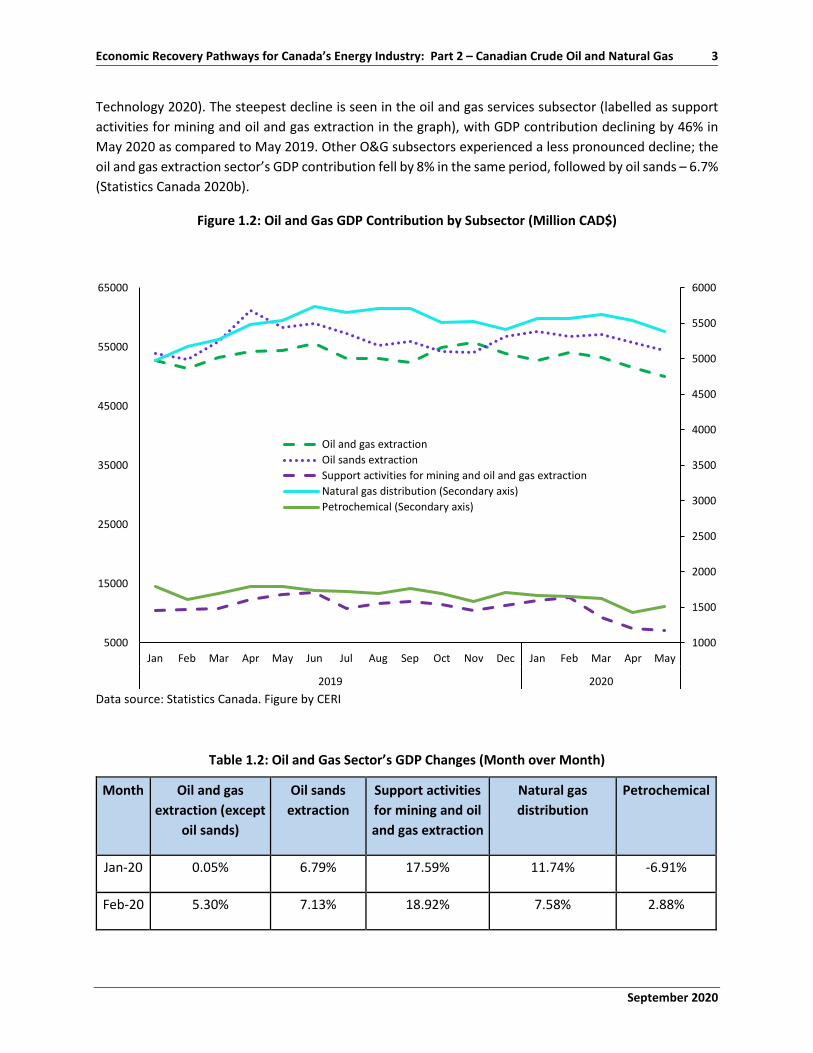

Figure 1.2 illustrates the GDP contribution from five subsectors representative of the oil and gas sector. Not surprisingly, GDP contribution for all subsectors has declined since the pandemic. A recent improvement in May, seen in the petrochemical sector, can be attributed to the sector’s production of products necessary in the medical and other fields, such as personal protective equipment, masks, and gloves (Jessica Owen n.d.). Lummus Technology highlighted that it expects to have a 4% growth in propylene demand, due to COVID-19, for production of products that reduce viral spread (Lummus

0

20,000

40,000

60,000

80,000

100,000

120,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

2019 2020

British Columbia

Newfoundland and Labrador

Saskatchewan

Alberta (Secondary axis)

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 3

Technology 2020). The steepest decline is seen in the oil and gas services subsector (labelled as support activities for mining and oil and gas extraction in the graph), with GDP contribution declining by 46% in May 2020 as compared to May 2019. Other O&G subsectors experienced a less pronounced decline; the oil and gas extraction sector’s GDP contribution fell by 8% in the same period, followed by oil sands – 6.7% (Statistics Canada 2020b).

Figure 1.2: Oil and Gas GDP Contribution by Subsector (Million CAD$)

Data source: Statistics Canada. Figure by CERI

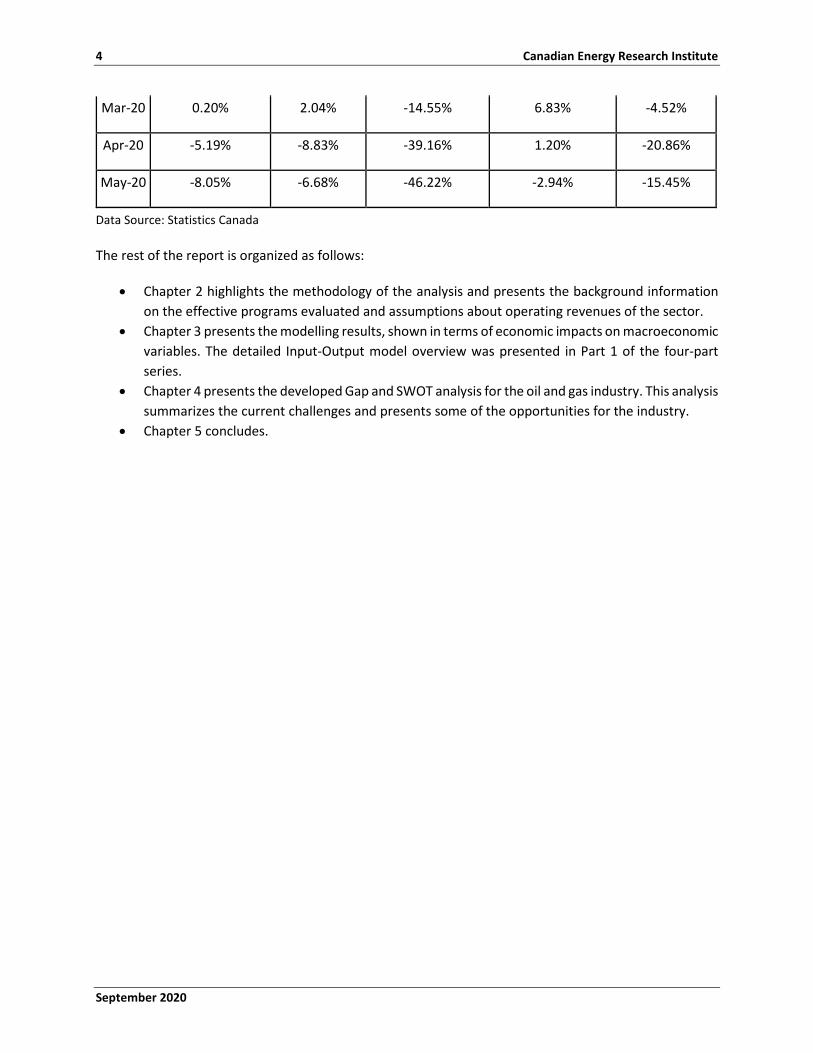

Table 1.2: Oil and Gas Sector’s GDP Changes (Month over Month)

Month Oil and gas extraction (except

oil sands)

Oil sands extraction

Support activities for mining and oil and gas extraction

Natural gas distribution

Petrochemical

Jan-20 0.05% 6.79% 17.59% 11.74% -6.91%

Feb-20 5.30% 7.13% 18.92% 7.58% 2.88%

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

5000

15000

25000

35000

45000

55000

65000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

2019 2020

Oil and gas extractionOil sands extractionSupport activities for mining and oil and gas extractionNatural gas distribution (Secondary axis)Petrochemical (Secondary axis)

4 Canadian Energy Research Institute

September 2020

Mar-20 0.20% 2.04% -14.55% 6.83% -4.52%

Apr-20 -5.19% -8.83% -39.16% 1.20% -20.86%

May-20 -8.05% -6.68% -46.22% -2.94% -15.45%

Data Source: Statistics Canada

The rest of the report is organized as follows:

• Chapter 2 highlights the methodology of the analysis and presents the background information on the effective programs evaluated and assumptions about operating revenues of the sector.

• Chapter 3 presents the modelling results, shown in terms of economic impacts on macroeconomic variables. The detailed Input-Output model overview was presented in Part 1 of the four-part series.

• Chapter 4 presents the developed Gap and SWOT analysis for the oil and gas industry. This analysis summarizes the current challenges and presents some of the opportunities for the industry.

• Chapter 5 concludes.

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 5

Chapter 2: Modelling Methodology and Assumptions

The CERI Canadian Multi-regional Input-Output (MRIO) model was used to analyze the economic impacts of various government relief measures as well as impacts resulting from revenue generated by daily operations in the upstream oil and gas sector. The model is based on the most recent Statistics Canada 2016 Supply and Use tables data. The economic impacts are determined in terms of major macroeconomic indicators such as impacts on GDP, employment, net tax revenues and labour income.

A detailed description and the mathematical framework of the model were presented in Part 1 of this four-part series. A detailed description of various stimulus and relief packages from the federal and provincial governments is available in Appendix A.

Modelling Methodology and Assumptions Economic Model Input-Output (I/O) models are used to estimate the impact that discrete changes in the economic activities within an economic sector or industry could have across the whole economy, given the interdependence that exists among industries. Notably, the use of outputs from one industry as inputs into another industry’s production process. I/O models provide estimates on the impact of various economic variables due to the introduction of a set of expenditures or ‘shocks.’ However, as mentioned by Poole (2005), the I/O model "shocks" are only capable of reproducing the average structure of the economy and not the marginal effects due to the linearity of the model and absence of feed-back effects (Poole 2005).

The estimates in this report are primarily used over short-term time horizons. Given that the most recent Supply and Use tables (Statistics Canada 2018), which are required to build the model, contain 2016 data, the economic impacts are based on the relationships prevailing in that year. Any structural changes that have happened since the collection of the data have been left out of the model, and the results could be either over- or under-estimated.

As shown in Figure 2.1, the analysis investigated the macroeconomic impacts of different stimulus programs or “shocks” on the following economic sectors in major oil and gas producing provinces of British Columbia (BC), Alberta (AB), Saskatchewan (SK), and Newfoundland and Labrador (NL):

• CERI’s MRIO model is used to analyse economic impacts. • The economic impacts are determined in terms of major macroeconomic indicators such as

impacts on GDP, employment, tax revenues and labour income. • CERI has identified 9 federal programs relevant to the oil and gas sector in addition to

provincial tax deferrals. • CERI estimated economic impacts of daily operations of the upstream oil and gas sector

(based on estimated revenues) to compare the results to a historical baseline.

6 Canadian Energy Research Institute

September 2020

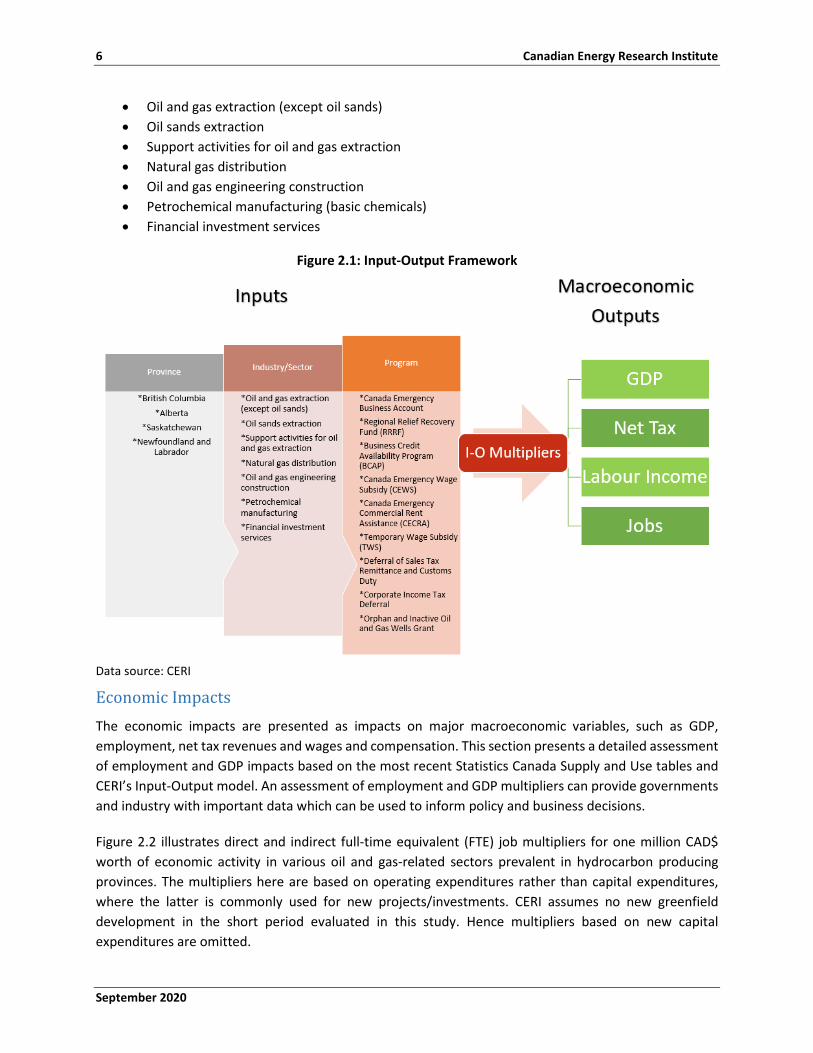

• Oil and gas extraction (except oil sands) • Oil sands extraction • Support activities for oil and gas extraction • Natural gas distribution • Oil and gas engineering construction • Petrochemical manufacturing (basic chemicals) • Financial investment services

Figure 2.1: Input-Output Framework

Data source: CERI

Economic Impacts The economic impacts are presented as impacts on major macroeconomic variables, such as GDP, employment, net tax revenues and wages and compensation. This section presents a detailed assessment of employment and GDP impacts based on the most recent Statistics Canada Supply and Use tables and CERI’s Input-Output model. An assessment of employment and GDP multipliers can provide governments and industry with important data which can be used to inform policy and business decisions.

Figure 2.2 illustrates direct and indirect full-time equivalent (FTE) job multipliers for one million CAD$ worth of economic activity in various oil and gas-related sectors prevalent in hydrocarbon producing provinces. The multipliers here are based on operating expenditures rather than capital expenditures, where the latter is commonly used for new projects/investments. CERI assumes no new greenfield development in the short period evaluated in this study. Hence multipliers based on new capital expenditures are omitted.

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 7

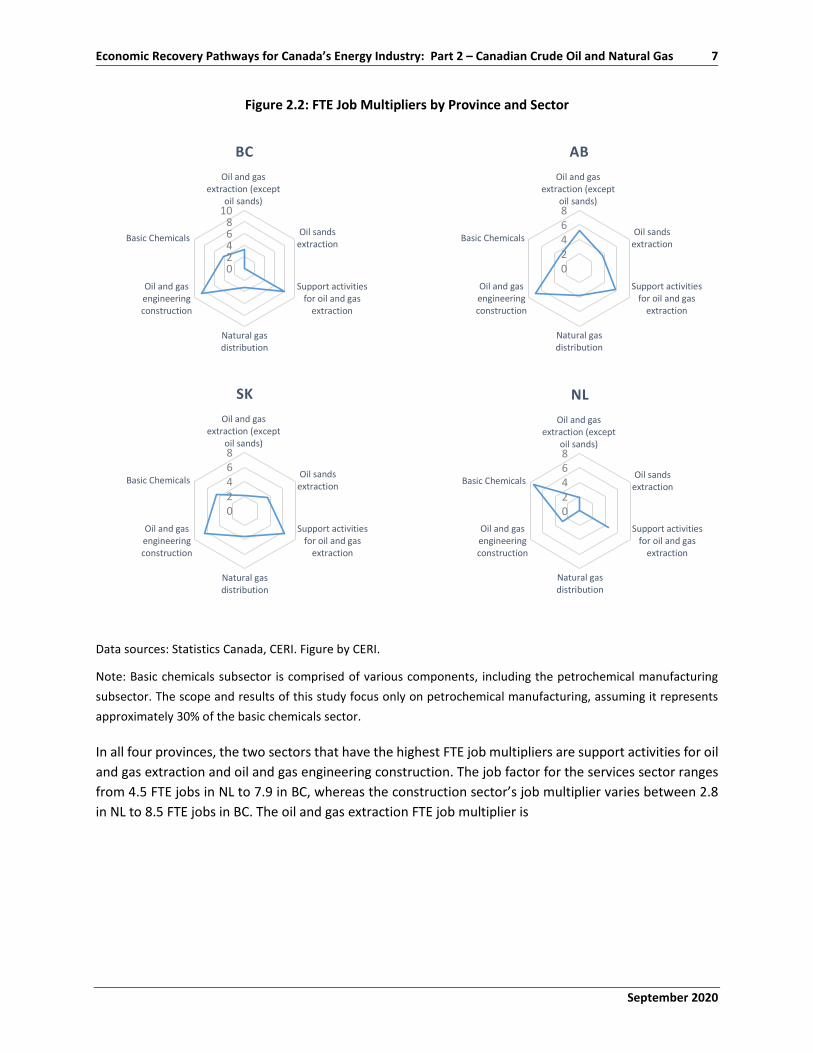

Figure 2.2: FTE Job Multipliers by Province and Sector

Data sources: Statistics Canada, CERI. Figure by CERI.

Note: Basic chemicals subsector is comprised of various components, including the petrochemical manufacturing subsector. The scope and results of this study focus only on petrochemical manufacturing, assuming it represents approximately 30% of the basic chemicals sector.

In all four provinces, the two sectors that have the highest FTE job multipliers are support activities for oil and gas extraction and oil and gas engineering construction. The job factor for the services sector ranges from 4.5 FTE jobs in NL to 7.9 in BC, whereas the construction sector’s job multiplier varies between 2.8 in NL to 8.5 FTE jobs in BC. The oil and gas extraction FTE job multiplier is

02468

10

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

BC

02468

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

AB

02468

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

SK

02468

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

NL

8 Canadian Energy Research Institute

September 2020

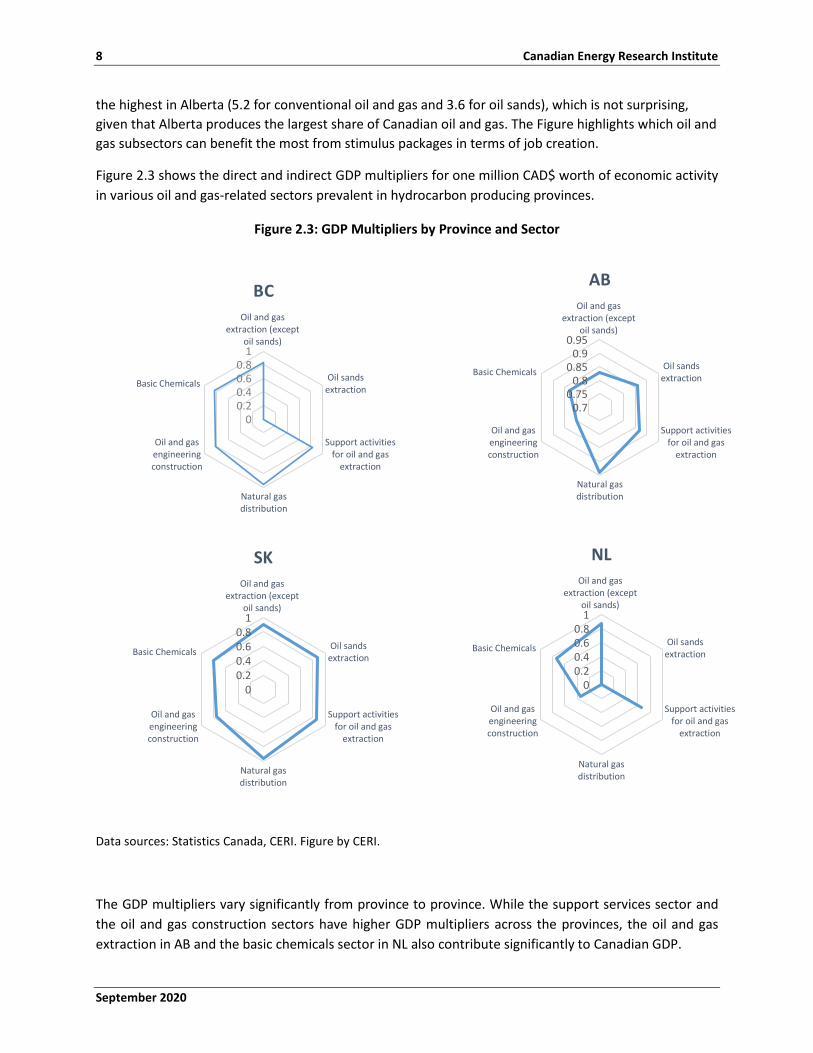

the highest in Alberta (5.2 for conventional oil and gas and 3.6 for oil sands), which is not surprising, given that Alberta produces the largest share of Canadian oil and gas. The Figure highlights which oil and gas subsectors can benefit the most from stimulus packages in terms of job creation.

Figure 2.3 shows the direct and indirect GDP multipliers for one million CAD$ worth of economic activity in various oil and gas-related sectors prevalent in hydrocarbon producing provinces.

Figure 2.3: GDP Multipliers by Province and Sector

Data sources: Statistics Canada, CERI. Figure by CERI.

The GDP multipliers vary significantly from province to province. While the support services sector and the oil and gas construction sectors have higher GDP multipliers across the provinces, the oil and gas extraction in AB and the basic chemicals sector in NL also contribute significantly to Canadian GDP.

00.20.40.60.8

1

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

NL

00.20.40.60.8

1

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

BC

0.70.75

0.80.85

0.90.95

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

AB

00.20.40.60.8

1

Oil and gasextraction (except

oil sands)

Oil sandsextraction

Support activitiesfor oil and gas

extraction

Natural gasdistribution

Oil and gasengineeringconstruction

Basic Chemicals

SK

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 9

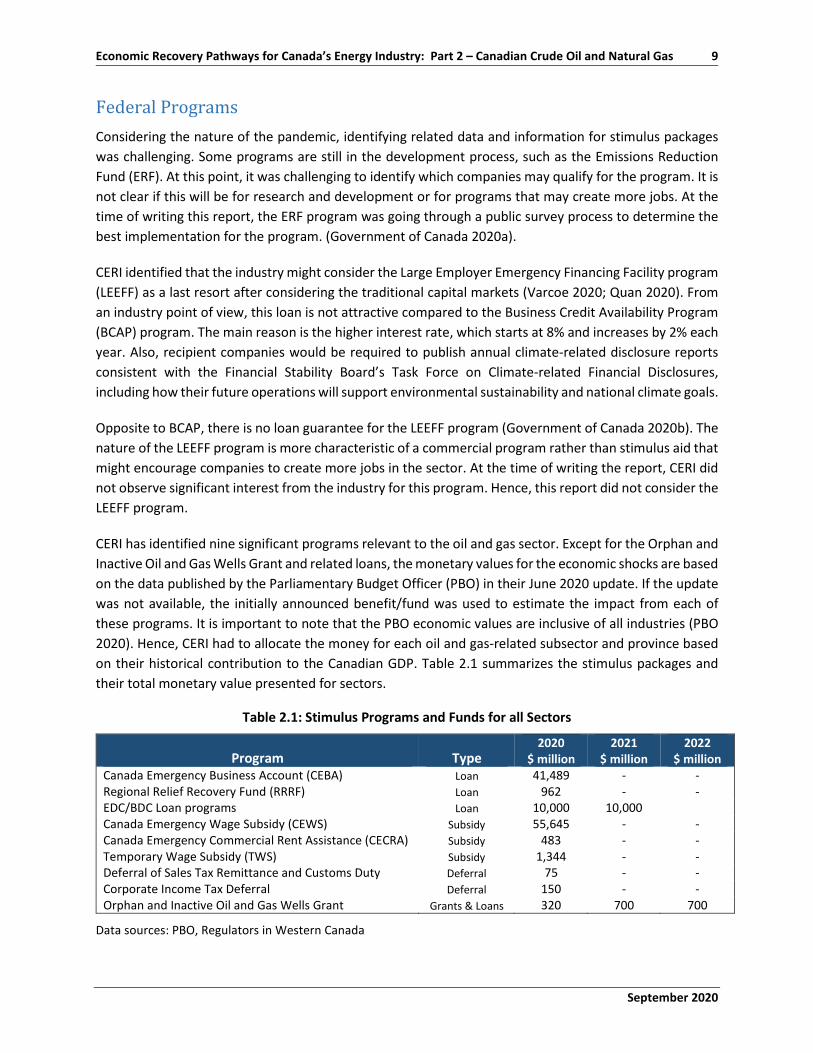

Federal Programs Considering the nature of the pandemic, identifying related data and information for stimulus packages was challenging. Some programs are still in the development process, such as the Emissions Reduction Fund (ERF). At this point, it was challenging to identify which companies may qualify for the program. It is not clear if this will be for research and development or for programs that may create more jobs. At the time of writing this report, the ERF program was going through a public survey process to determine the best implementation for the program. (Government of Canada 2020a).

CERI identified that the industry might consider the Large Employer Emergency Financing Facility program (LEEFF) as a last resort after considering the traditional capital markets (Varcoe 2020; Quan 2020). From an industry point of view, this loan is not attractive compared to the Business Credit Availability Program (BCAP) program. The main reason is the higher interest rate, which starts at 8% and increases by 2% each year. Also, recipient companies would be required to publish annual climate-related disclosure reports consistent with the Financial Stability Board’s Task Force on Climate-related Financial Disclosures, including how their future operations will support environmental sustainability and national climate goals.

Opposite to BCAP, there is no loan guarantee for the LEEFF program (Government of Canada 2020b). The nature of the LEEFF program is more characteristic of a commercial program rather than stimulus aid that might encourage companies to create more jobs in the sector. At the time of writing the report, CERI did not observe significant interest from the industry for this program. Hence, this report did not consider the LEEFF program.

CERI has identified nine significant programs relevant to the oil and gas sector. Except for the Orphan and Inactive Oil and Gas Wells Grant and related loans, the monetary values for the economic shocks are based on the data published by the Parliamentary Budget Officer (PBO) in their June 2020 update. If the update was not available, the initially announced benefit/fund was used to estimate the impact from each of these programs. It is important to note that the PBO economic values are inclusive of all industries (PBO 2020). Hence, CERI had to allocate the money for each oil and gas-related subsector and province based on their historical contribution to the Canadian GDP. Table 2.1 summarizes the stimulus packages and their total monetary value presented for sectors.

Table 2.1: Stimulus Programs and Funds for all Sectors

Program Type 2020

$ million 2021

$ million 2022

$ million Canada Emergency Business Account (CEBA) Loan 41,489 - - Regional Relief Recovery Fund (RRRF) Loan 962 - - EDC/BDC Loan programs Loan 10,000 10,000 Canada Emergency Wage Subsidy (CEWS) Subsidy 55,645 - - Canada Emergency Commercial Rent Assistance (CECRA) Subsidy 483 - - Temporary Wage Subsidy (TWS) Subsidy 1,344 - - Deferral of Sales Tax Remittance and Customs Duty Deferral 75 - - Corporate Income Tax Deferral Deferral 150 - - Orphan and Inactive Oil and Gas Wells Grant Grants & Loans 320 700 700

Data sources: PBO, Regulators in Western Canada

10 Canadian Energy Research Institute

September 2020

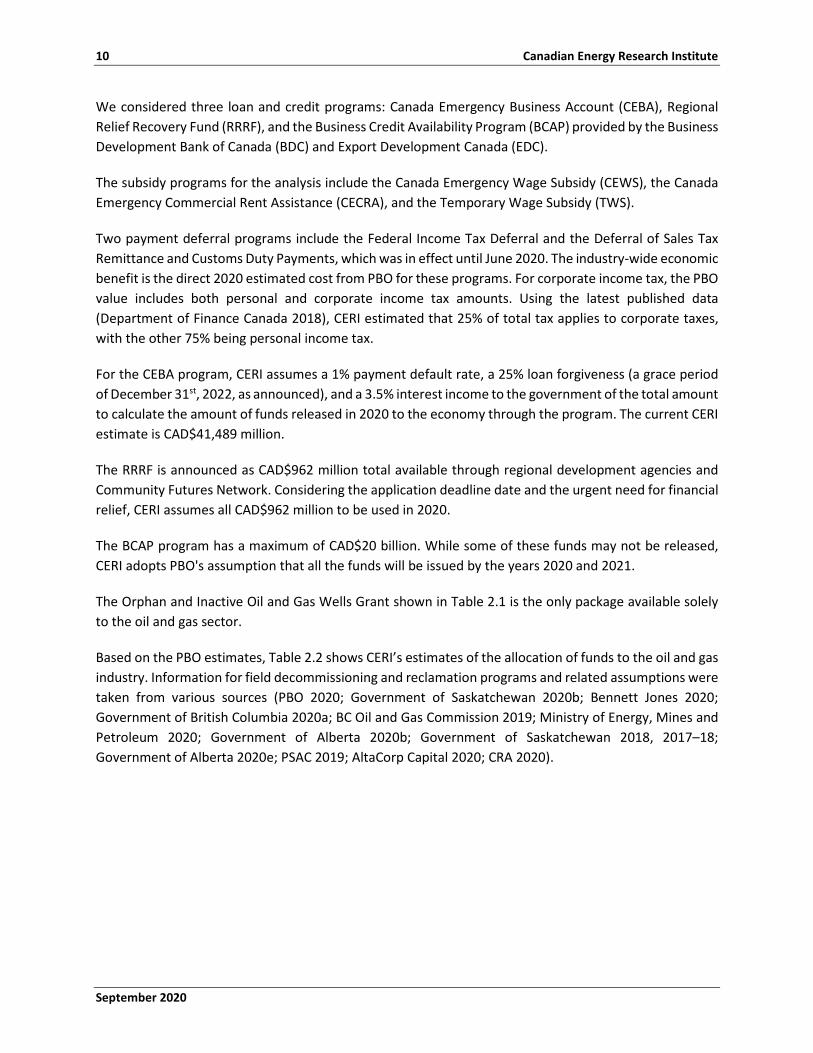

We considered three loan and credit programs: Canada Emergency Business Account (CEBA), Regional Relief Recovery Fund (RRRF), and the Business Credit Availability Program (BCAP) provided by the Business Development Bank of Canada (BDC) and Export Development Canada (EDC).

The subsidy programs for the analysis include the Canada Emergency Wage Subsidy (CEWS), the Canada Emergency Commercial Rent Assistance (CECRA), and the Temporary Wage Subsidy (TWS).

Two payment deferral programs include the Federal Income Tax Deferral and the Deferral of Sales Tax Remittance and Customs Duty Payments, which was in effect until June 2020. The industry-wide economic benefit is the direct 2020 estimated cost from PBO for these programs. For corporate income tax, the PBO value includes both personal and corporate income tax amounts. Using the latest published data (Department of Finance Canada 2018), CERI estimated that 25% of total tax applies to corporate taxes, with the other 75% being personal income tax.

For the CEBA program, CERI assumes a 1% payment default rate, a 25% loan forgiveness (a grace period of December 31st, 2022, as announced), and a 3.5% interest income to the government of the total amount to calculate the amount of funds released in 2020 to the economy through the program. The current CERI estimate is CAD$41,489 million.

The RRRF is announced as CAD$962 million total available through regional development agencies and Community Futures Network. Considering the application deadline date and the urgent need for financial relief, CERI assumes all CAD$962 million to be used in 2020.

The BCAP program has a maximum of CAD$20 billion. While some of these funds may not be released, CERI adopts PBO's assumption that all the funds will be issued by the years 2020 and 2021.

The Orphan and Inactive Oil and Gas Wells Grant shown in Table 2.1 is the only package available solely to the oil and gas sector.

Based on the PBO estimates, Table 2.2 shows CERI’s estimates of the allocation of funds to the oil and gas industry. Information for field decommissioning and reclamation programs and related assumptions were taken from various sources (PBO 2020; Government of Saskatchewan 2020b; Bennett Jones 2020; Government of British Columbia 2020a; BC Oil and Gas Commission 2019; Ministry of Energy, Mines and Petroleum 2020; Government of Alberta 2020b; Government of Saskatchewan 2018, 2017–18; Government of Alberta 2020e; PSAC 2019; AltaCorp Capital 2020; CRA 2020).

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 11

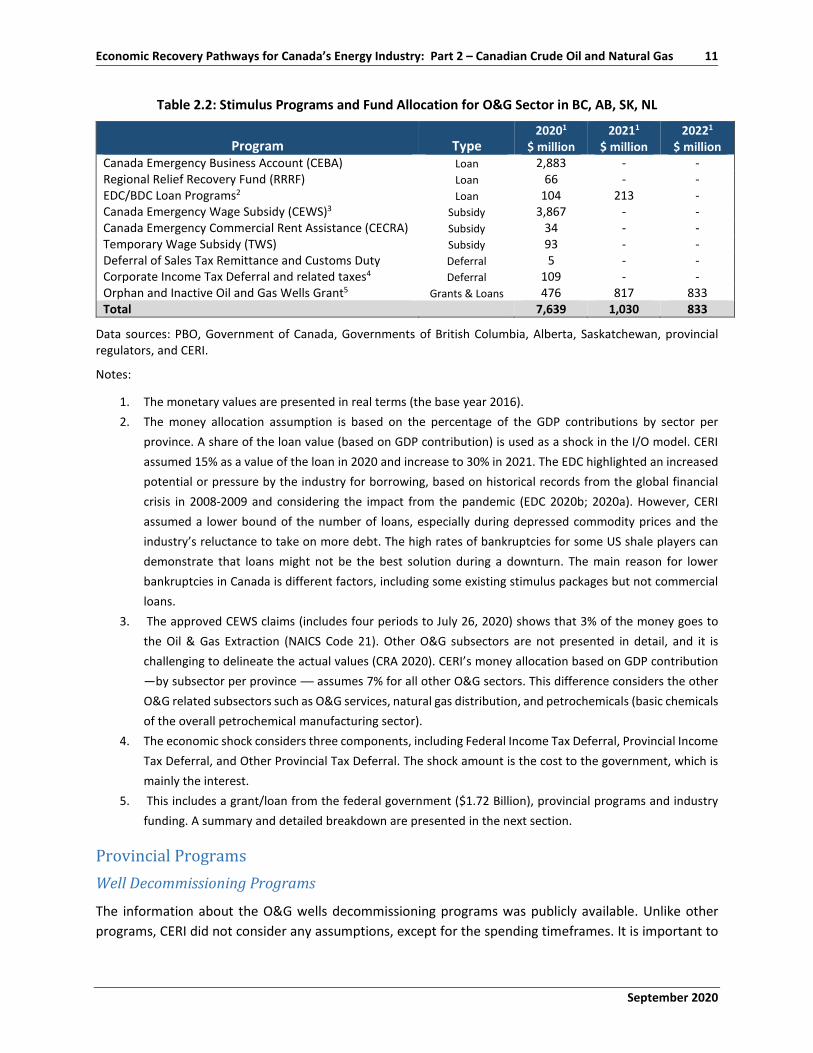

Table 2.2: Stimulus Programs and Fund Allocation for O&G Sector in BC, AB, SK, NL

Program Type 20201

$ million 20211

$ million 20221

$ million Canada Emergency Business Account (CEBA) Loan 2,883 - - Regional Relief Recovery Fund (RRRF) Loan 66 - - EDC/BDC Loan Programs2 Loan 104 213 - Canada Emergency Wage Subsidy (CEWS)3 Subsidy 3,867 - - Canada Emergency Commercial Rent Assistance (CECRA) Subsidy 34 - - Temporary Wage Subsidy (TWS) Subsidy 93 - - Deferral of Sales Tax Remittance and Customs Duty Deferral 5 - - Corporate Income Tax Deferral and related taxes4 Deferral 109 - - Orphan and Inactive Oil and Gas Wells Grant5 Grants & Loans 476 817 833 Total 7,639 1,030 833

Data sources: PBO, Government of Canada, Governments of British Columbia, Alberta, Saskatchewan, provincial regulators, and CERI.

Notes:

1. The monetary values are presented in real terms (the base year 2016). 2. The money allocation assumption is based on the percentage of the GDP contributions by sector per

province. A share of the loan value (based on GDP contribution) is used as a shock in the I/O model. CERI assumed 15% as a value of the loan in 2020 and increase to 30% in 2021. The EDC highlighted an increased potential or pressure by the industry for borrowing, based on historical records from the global financial crisis in 2008-2009 and considering the impact from the pandemic (EDC 2020b; 2020a). However, CERI assumed a lower bound of the number of loans, especially during depressed commodity prices and the industry’s reluctance to take on more debt. The high rates of bankruptcies for some US shale players can demonstrate that loans might not be the best solution during a downturn. The main reason for lower bankruptcies in Canada is different factors, including some existing stimulus packages but not commercial loans.

3. The approved CEWS claims (includes four periods to July 26, 2020) shows that 3% of the money goes to the Oil & Gas Extraction (NAICS Code 21). Other O&G subsectors are not presented in detail, and it is challenging to delineate the actual values (CRA 2020). CERI’s money allocation based on GDP contribution —by subsector per province — assumes 7% for all other O&G sectors. This difference considers the other O&G related subsectors such as O&G services, natural gas distribution, and petrochemicals (basic chemicals of the overall petrochemical manufacturing sector).

4. The economic shock considers three components, including Federal Income Tax Deferral, Provincial Income Tax Deferral, and Other Provincial Tax Deferral. The shock amount is the cost to the government, which is mainly the interest.

5. This includes a grant/loan from the federal government ($1.72 Billion), provincial programs and industry funding. A summary and detailed breakdown are presented in the next section.

Provincial Programs Well Decommissioning Programs

The information about the O&G wells decommissioning programs was publicly available. Unlike other programs, CERI did not consider any assumptions, except for the spending timeframes. It is important to

12 Canadian Energy Research Institute

September 2020

note that the projected timeframes have considered different factors, including the application processing timelines during the 2nd quarter of 2020, the average decommissioning work per year by different organizations, the nature of the decommissioning work as some work is dependant on the season such as winter access or surface reclamation works (OWA 2020; BC Oil and Gas Commission 2019; Government of Saskatchewan 2020a; Government of Alberta 2020c).

In British Columbia, the distribution of money for well-decommissioning work includes $120 million from the Government of Canada, with industry matching of another $100 million to the reclamation and decommissioning work. In Alberta, the funds for well decommissioning include a grant of $1,000 million to site rehabilitation program and a loan of $200 million to the Orphan Well Association (OWA) from the Government of Canada, and a loan of $100 million from the Government of Alberta. In Saskatchewan, a grant of $400 million from the Government of Canada is considered. The respective provincial governments manage the distribution of the federal funds. The allocation assumes 20% of the money to be spent in 2020, 40% in 2021, and 40% in 2022. Table 2.3 summarizes the money allocation for different field decommissioning programs in western Canada (Bennett Jones 2020; OWA 2020b; Government of Saskatchewan 2020b; Government of Alberta 2020c.

Table 2.3: Field Decommissioning Programs in Western Canada

Province Type Source

Amount $

million Program End Date Contribution

BC Grant Government of Canada 100 Dormant Sites Reclamation Program 31-Dec-22 50% BC E&P Spending O&G Industry 100 Dormant Sites Reclamation Program 50% BC Grant Government of Canada 15 Orphan Sites Supplemental Reclamation Program 100% BC Grant Government of Canada 5 Legacy Sites Reclamation Program 100%

Total Dollar Amount in BC 220 AB Grant Government of Canada 1000 Site Rehabilitation Program 31-Dec-22 100% AB Loan Government of Canada 200 Managed by the Orphan Well Association 100% AB Loan Government of Alberta 100 Managed by the Orphan Well Association 100%

Total Dollar Amount in AB 1300 SK Grant Government of Canada 400 Accelerated Site Closure Program 31-Dec-22 100%

Total Dollar Amount in SK 400 Data sources: (Bennett Jones 2020; OWA 2020b; Government of Saskatchewan 2020b; Government of Alberta 2020c). Table by CERI.

Note: BC is the only jurisdiction that required the industry’s contribution to qualify for the grant, which doubled the amount of the main decommissioning program in the province.

Taxes and deferrals

Provincial governments announced a multitude of programs to support businesses in addition to federal programs. CERI recognizes tax deferral programs to be the most significant and common for all provinces and across all industries. Tax deferrals have been introduced for at least three months in almost all provinces and include:

• Provincial Corporate Tax deferral • Deferral of other provincial taxes

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 13

Other government payment deferrals include sales tax deferral, carbon tax deferral, workers compensation deferral, etc. More detail about the provincial programs is available in Appendix A.

To estimate the provincial level tax deferral benefits, CERI uses the federal corporate income tax deferral value estimated by the PBO and calculates the provincial tax deferral amounts based on tax rates between federal and provincial governments. Once the provincial and federal corporate income taxes are estimated, CERI uses Statistics Canada Supply Use Tables to estimate other taxes on production. CERI assumes all other taxes on production represents all deferred provincial taxes, excluding corporate income tax.

Although CERI focuses only on deferral of provincial taxes and payments, some other provincial programs that may be of significance are as follows:

• The delayed carbon tax increase in BC • Corporate Tax reduction in AB (from 10% to 8% in July 2020) • Small Business relaunch and emergency payments in AB and SK

Oil and Gas Operations and Revenues This section highlights the methodology for evaluating the oil and gas producer’s gross revenues (operations), which are used as inputs, or injections, into the CERI MRIO model to estimate the economic impacts of the upstream oil and gas sectors. The revenues are calculated based on CERI’s most recent production outlooks published in CERI Studies 190 and 191 (CERI 2020a; 2020b). In particular, we only consider Scenario II production levels for the period of 2020-2025, inclusive2.

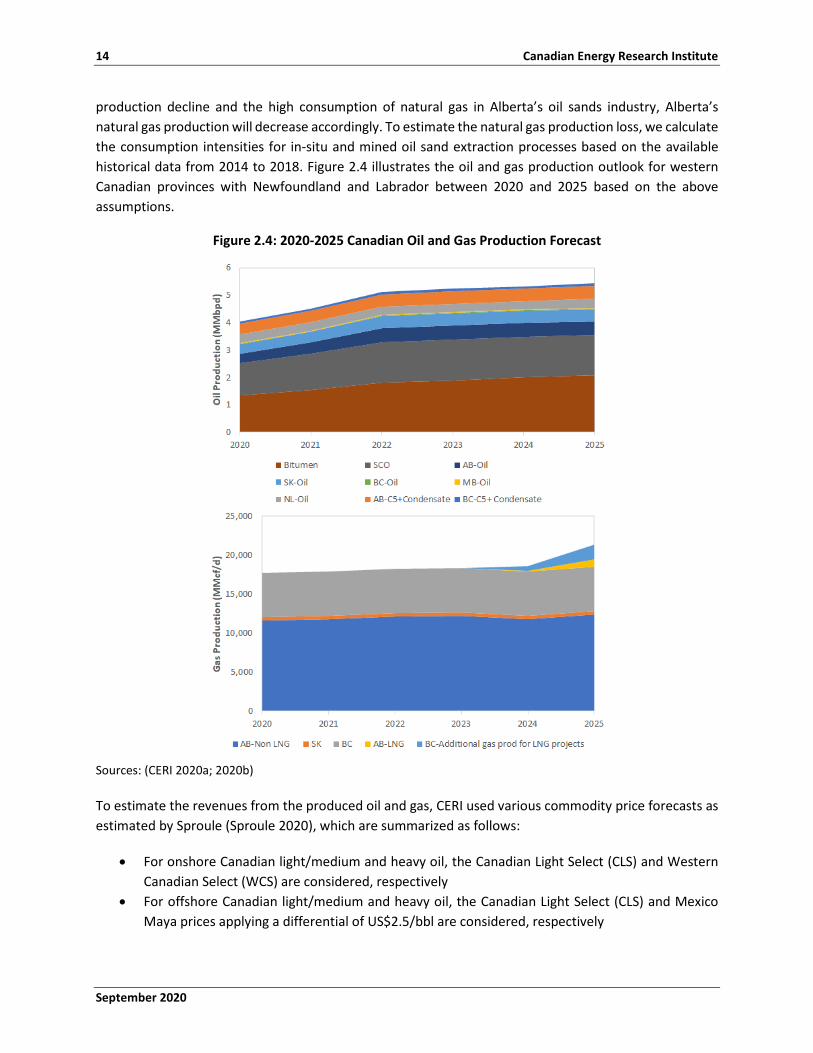

For ease of reference, CERI estimated a crude oil production loss of 1 million barrels per day (MMbpd) in 2020 and 700 thousand barrels per day (kbpd) in 2021. After 2021, a permanent production loss of 200 kbpd is considered, meaning that between 2022 and 2025, the annual oil production in Canada will decrease by 200 kbpd compared to the respective values forecasted in CERI’s 2019 production forecasts (CERI 2019a; 2019b).

It is assumed that the following major oil-producing provinces, i.e., British Columbia (BC), Alberta (AB), Saskatchewan (SK), and Manitoba (MB), are affected by the production cuts. We exempt Newfoundland and Labrador (NL) because of its specific geographical situation and market structure and its ability to access global Brent prices. Additionally, data for March and April 2020 does not show a significant change in the crude oil production in NL (C-NLOPB 2020).

The production loss is split among oil and gas producing provinces based on historical production shares. We consider the average shares between the years of 2014-2018 as the production share of each province of the total crude oil production in Canada (CAPP 2019).

We assume that the natural gas exports to the US and the domestic natural gas consumption will not alter significantly in different industrial sectors except for Alberta’s oil sands industry. However, owing to the

2 Readers are encouraged to familiarize themselves with the abovementioned studies to understand the production forecasts, production losses and provincial shares assignment.

14 Canadian Energy Research Institute

September 2020

production decline and the high consumption of natural gas in Alberta’s oil sands industry, Alberta’s natural gas production will decrease accordingly. To estimate the natural gas production loss, we calculate the consumption intensities for in-situ and mined oil sand extraction processes based on the available historical data from 2014 to 2018. Figure 2.4 illustrates the oil and gas production outlook for western Canadian provinces with Newfoundland and Labrador between 2020 and 2025 based on the above assumptions.

Figure 2.4: 2020-2025 Canadian Oil and Gas Production Forecast

Sources: (CERI 2020a; 2020b)

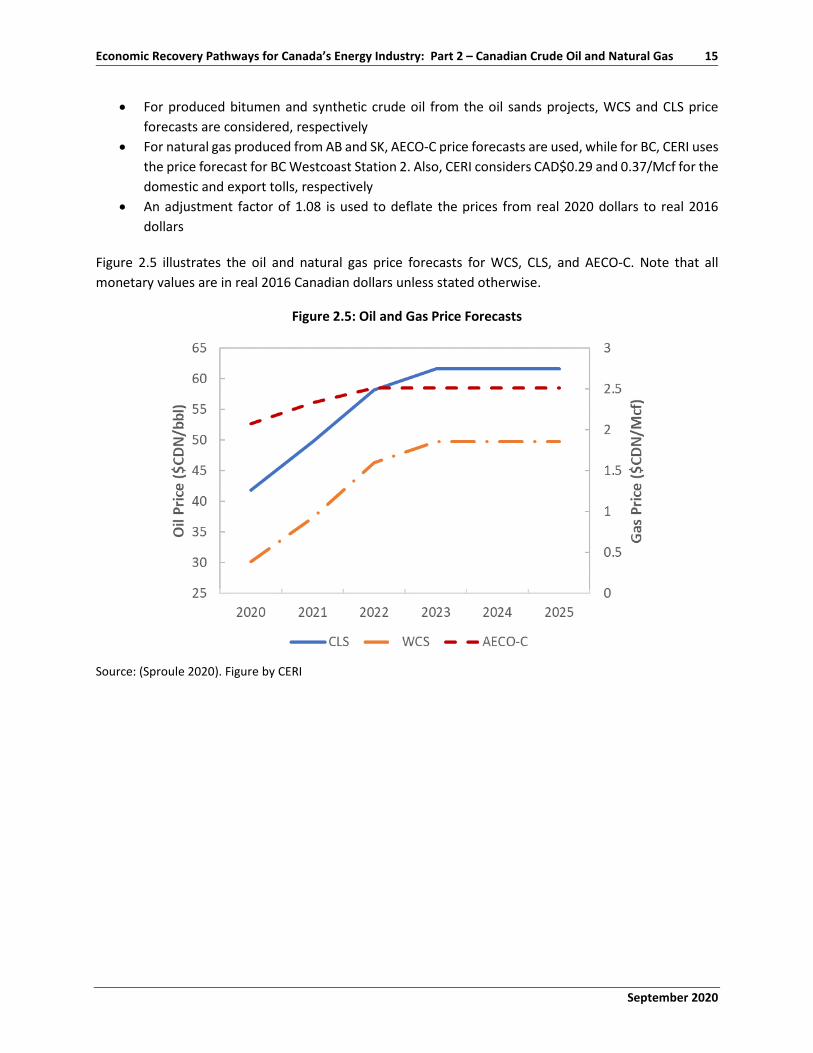

To estimate the revenues from the produced oil and gas, CERI used various commodity price forecasts as estimated by Sproule (Sproule 2020), which are summarized as follows:

• For onshore Canadian light/medium and heavy oil, the Canadian Light Select (CLS) and Western Canadian Select (WCS) are considered, respectively

• For offshore Canadian light/medium and heavy oil, the Canadian Light Select (CLS) and Mexico Maya prices applying a differential of US$2.5/bbl are considered, respectively

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 15

• For produced bitumen and synthetic crude oil from the oil sands projects, WCS and CLS price forecasts are considered, respectively

• For natural gas produced from AB and SK, AECO-C price forecasts are used, while for BC, CERI uses the price forecast for BC Westcoast Station 2. Also, CERI considers CAD$0.29 and 0.37/Mcf for the domestic and export tolls, respectively

• An adjustment factor of 1.08 is used to deflate the prices from real 2020 dollars to real 2016 dollars

Figure 2.5 illustrates the oil and natural gas price forecasts for WCS, CLS, and AECO-C. Note that all monetary values are in real 2016 Canadian dollars unless stated otherwise.

Figure 2.5: Oil and Gas Price Forecasts

Source: (Sproule 2020). Figure by CERI

16 Canadian Energy Research Institute

September 2020

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 17

Chapter 3: Economic Impacts of Relief Measures and Industry Operations

This chapter presents the summary results of economic I/O analysis and the resulting economic impacts on major macroeconomic variables. The first section of the Chapter highlights the summary of impacts from government relief measures. The second section details the economic impacts stemming from generated revenues of the upstream oil and gas exploration and production sector (E&P). Detailed I/O results from stimulus packages are also available in Appendix B.

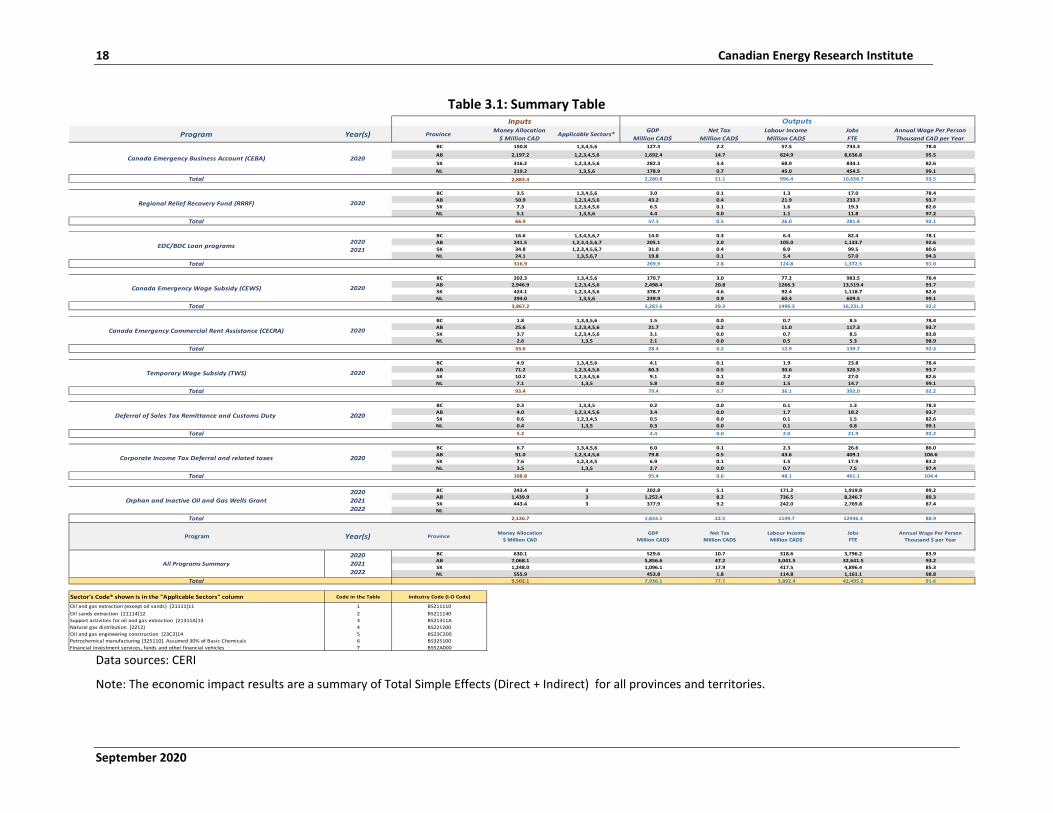

Economic Impacts of Relief Measures This section presents the short-term economic impacts of various government stimulus packages on the oil and gas producing jurisdictions and the Canadian economy overall. Given the short-term nature of the various programs, the results are evaluated and presented for three years, from 2020 to 2022, inclusive. Table 3.1 shows a summary of the input and output data. The economic impacts represent the total simple effects (direct + indirect) for the four producing provinces as well as other Canadian provinces and territories.

The total GDP impact over the studied period could amount to almost CAD$8 billion, including direct and indirect impacts within producing regions as well as indirect impacts within all other regions in Canada. The overall employment impact is estimated to be almost 42.5 thousand FTE jobs and labour income amounting to almost CAD$4 billion, with an average annual salary of CAD$91.6 thousand per person. The associated net tax revenues that could be realized are almost CAD$78 million over the 2020-2022 period.

• Total economic Impacts (direct and indirect) of stimulus packages over 2020-2022 period could amount to:

o GDP impact of CAD$7,936 million; Employment impact of 42,495 FTE jobs; Net tax impact of CAD$78 million; Labour income impact of CAD$3,892 million with an average annual salary per person of CAD$91,600.

• Total economic Impacts of upstream oil and gas operations (direct and indirect) over the 2020-2025 period are estimated to be:

o GDP impact of CAD$177 billion (conventional oil), CAD$53 billion (natural gas), and CAD$300 billion (oil sands).

o Employment impact of 801 thousand FTE (conventional oil), 294 thousand FTE (natural gas), and 1.3 million FTE (oil sands).

18 Canadian Energy Research Institute

September 2020

Table 3.1: Summary Table

Data sources: CERI

Note: The economic impact results are a summary of Total Simple Effects (Direct + Indirect) for all provinces and territories.

Inputs

Program Year(s) Province Money Allocation $ Million CAD

Applicable Sectors* GDPMillion CAD$

Net TaxMillion CAD$

Labour IncomeMillion CAD$

JobsFTE

Annual Wage Per PersonThousand CAD per Year

BC 150.8 1,3,4,5,6 127.3 2.2 57.5 733.3 78.4

AB 2,197.2 1,2,3,4,5,6 1,692.4 14.7 824.9 8,636.8 95.5

SK 316.2 1,2,3,4,5,6 282.3 3.4 68.9 834.1 82.6NL 219.2 1,3,5,6 178.9 0.7 45.0 454.5 99.1

Total 2,883.4 2,280.8 21.1 996.4 10,658.7 93.5Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 3.5 1,3,4,5,6 3.0 0.1 1.3 17.0 78.4AB 50.9 1,2,3,4,5,6 43.2 0.4 21.9 233.7 93.7SK 7.3 1,2,3,4,5,6 6.5 0.1 1.6 19.3 82.6NL 5.1 1,3,5,6 4.4 0.0 1.1 11.8 97.2

Total 66.9 57.1 0.5 26.0 281.8 92.1Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 16.6 1,3,4,5,6,7 14.0 0.3 6.4 82.4 78.1AB 241.5 1,2,3,4,5,6,7 205.1 2.0 105.0 1,133.7 92.6SK 34.8 1,2,3,4,5,6,7 31.0 0.4 8.0 99.5 80.6NL 24.1 1,3,5,6,7 19.8 0.1 5.4 57.0 94.3

Total 316.9 269.9 2.8 124.8 1,372.5 91.0Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 202.3 1,3,4,5,6 170.7 3.0 77.2 983.5 78.4AB 2,946.9 1,2,3,4,5,6 2,498.4 20.8 1266.3 13,519.4 93.7SK 424.1 1,2,3,4,5,6 378.7 4.6 92.4 1,118.7 82.6NL 294.0 1,3,5,6 239.9 0.9 60.4 609.5 99.1

Total 3,867.2 3,287.6 29.3 1496.3 16,231.2 92.2Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 1.8 1,3,4,5,6 1.5 0.0 0.7 8.5 78.4AB 25.6 1,2,3,4,5,6 21.7 0.2 11.0 117.3 93.7SK 3.7 1,2,3,4,5,6 3.1 0.0 0.7 8.5 83.8NL 2.6 1,3,5 2.1 0.0 0.5 5.3 98.9

Total 33.6 28.4 0.2 12.9 139.7 92.3Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 4.9 1,3,4,5,6 4.1 0.1 1.9 23.8 78.4AB 71.2 1,2,3,4,5,6 60.3 0.5 30.6 326.5 93.7SK 10.2 1,2,3,4,5,6 9.1 0.1 2.2 27.0 82.6NL 7.1 1,3,5 5.8 0.0 1.5 14.7 99.1

Total 93.4 79.4 0.7 36.1 392.0 92.2Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 0.3 1,3,4,5 0.2 0.0 0.1 1.3 78.3AB 4.0 1,2,3,4,5,6 3.4 0.0 1.7 18.2 93.7SK 0.6 1,2,3,4,5 0.5 0.0 0.1 1.5 82.6NL 0.4 1,3,5 0.3 0.0 0.1 0.8 99.1

Total 5.2 4.4 0.0 2.0 21.9 92.2Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 6.7 1,3,4,5,6 6.0 0.1 2.3 26.6 86.0AB 91.0 1,2,3,4,5,6 79.8 0.5 43.6 409.1 106.6SK 7.6 1,2,3,4,5 6.9 0.1 1.5 17.9 83.2NL 3.5 1,3,5 2.7 0.0 0.7 7.5 97.4

Total 108.8 95.4 0.6 48.1 461.1 104.4Program Province Money Allocation Applicable Sectors GDP Net Tax Labour Income Jobs

BC 243.4 3 202.8 5.1 171.2 1,919.8 89.2AB 1,439.9 3 1,252.4 8.2 736.5 8,246.7 89.3SK 443.4 3 377.9 9.2 242.0 2,769.8 87.4NL

Total 2,126.7 1,833.1 22.5 1149.7 12936.3 88.9

Program Year(s) Province Money Allocation $ Million CAD

GDPMillion CAD$

Net TaxMillion CAD$

Labour IncomeMillion CAD$

JobsFTE

Annual Wage Per PersonThousand $ per Year

BC 630.1 529.6 10.7 318.6 3,796.2 83.9AB 7,068.1 5,856.6 47.2 3,041.5 32,641.5 93.2SK 1,248.0 1,096.1 17.9 417.5 4,896.4 85.3NL 555.9 453.8 1.8 114.8 1,161.1 98.8

Total 9,502.1 7,936.1 77.7 3,892.4 42,495.2 91.6

Sector's Code* shown is in the "Applicable Sectors" column Code in the Table Industry Code (I-O Code)

Oil and gas extraction (except oil sands) [21111]11 1 BS211110Oil sands extraction [21114]12 2 BS211140Support activities for oil and gas extraction [21311A]13 3 BS21311ANatural gas distribution [2212] 4 BS221200Oil and gas engineering construction [23C2]14 5 BS23C200Petrochemical manufacturing [325110]. Assumed 30% of Basic Chemicals 6 BS325100Financial investment services, funds and other financial vehicles 7 BS52A000

2020

2020

2020

202020212022

202020212022

Canada Emergency Business Account (CEBA)

Regional Relief Recovery Fund (RRRF)

Outputs

2020

2020

20202021

2020

2020

Orphan and Inactive Oil and Gas Wells Grant

All Programs Summary

EDC/BDC Loan programs

Canada Emergency Wage Subsidy (CEWS)

Canada Emergency Commercial Rent Assistance (CECRA)

Temporary Wage Subsidy (TWS)

Deferral of Sales Tax Remittance and Customs Duty

Corporate Income Tax Deferral and related taxes

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 19

The next four sections describe the direct and indirect impacts on GDP, employment, tax revenues and labour income within each producing province. The indirect impacts on other provinces and territories are aggregated.

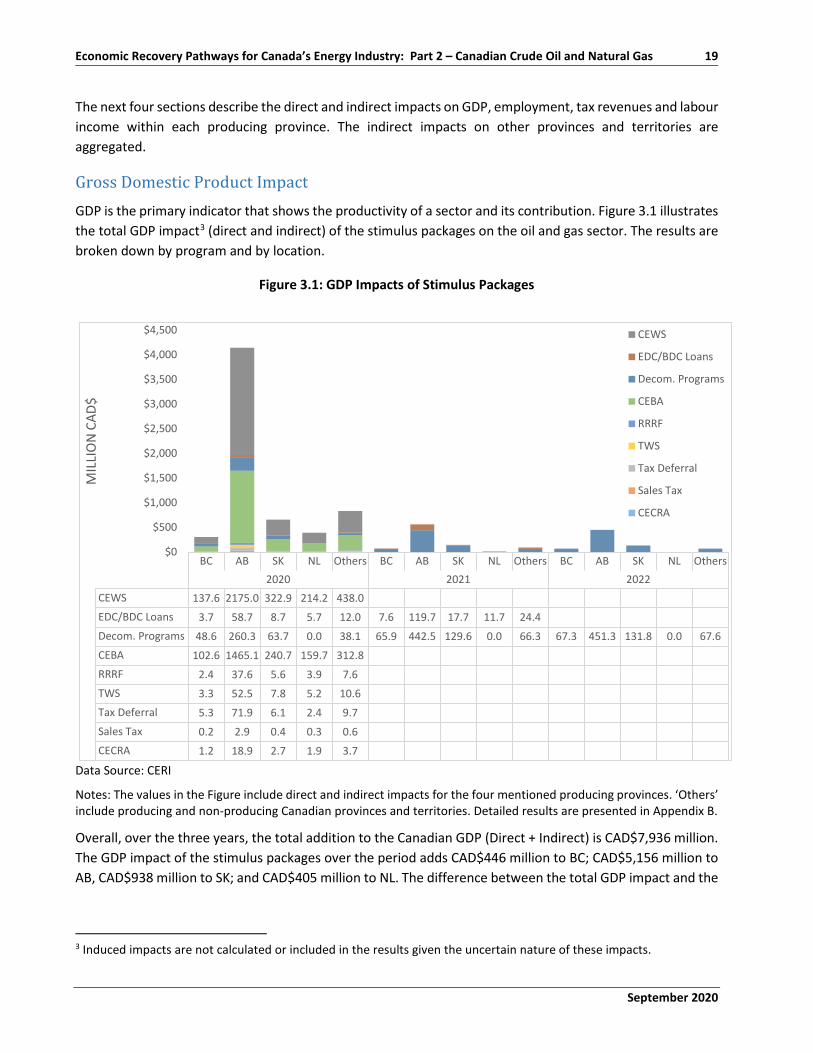

Gross Domestic Product Impact GDP is the primary indicator that shows the productivity of a sector and its contribution. Figure 3.1 illustrates the total GDP impact3 (direct and indirect) of the stimulus packages on the oil and gas sector. The results are broken down by program and by location.

Figure 3.1: GDP Impacts of Stimulus Packages

Data Source: CERI

Notes: The values in the Figure include direct and indirect impacts for the four mentioned producing provinces. ‘Others’ include producing and non-producing Canadian provinces and territories. Detailed results are presented in Appendix B.

Overall, over the three years, the total addition to the Canadian GDP (Direct + Indirect) is CAD$7,936 million. The GDP impact of the stimulus packages over the period adds CAD$446 million to BC; CAD$5,156 million to AB, CAD$938 million to SK; and CAD$405 million to NL. The difference between the total GDP impact and the

3 Induced impacts are not calculated or included in the results given the uncertain nature of these impacts.

BC AB SK NL Others BC AB SK NL Others BC AB SK NL Others2020 2021 2022

CEWS 137.6 2175.0 322.9 214.2 438.0EDC/BDC Loans 3.7 58.7 8.7 5.7 12.0 7.6 119.7 17.7 11.7 24.4Decom. Programs 48.6 260.3 63.7 0.0 38.1 65.9 442.5 129.6 0.0 66.3 67.3 451.3 131.8 0.0 67.6CEBA 102.6 1465.1 240.7 159.7 312.8RRRF 2.4 37.6 5.6 3.9 7.6TWS 3.3 52.5 7.8 5.2 10.6Tax Deferral 5.3 71.9 6.1 2.4 9.7Sales Tax 0.2 2.9 0.4 0.3 0.6CECRA 1.2 18.9 2.7 1.9 3.7

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

MIL

LIO

N C

AD$

CEWS

EDC/BDC Loans

Decom. Programs

CEBA

RRRF

TWS

Tax Deferral

Sales Tax

CECRA

20 Canadian Energy Research Institute

September 2020

impacts for the four producing provinces is attributed to GDP impacts that could be felt in other provinces and territories.

While CEWS will provide the most significant short-term benefit, the field decommissioning and reclamation programs in western Canada will be the primary source of government stimulus for the sector, in particular, the oil and gas services sector over the next two years.

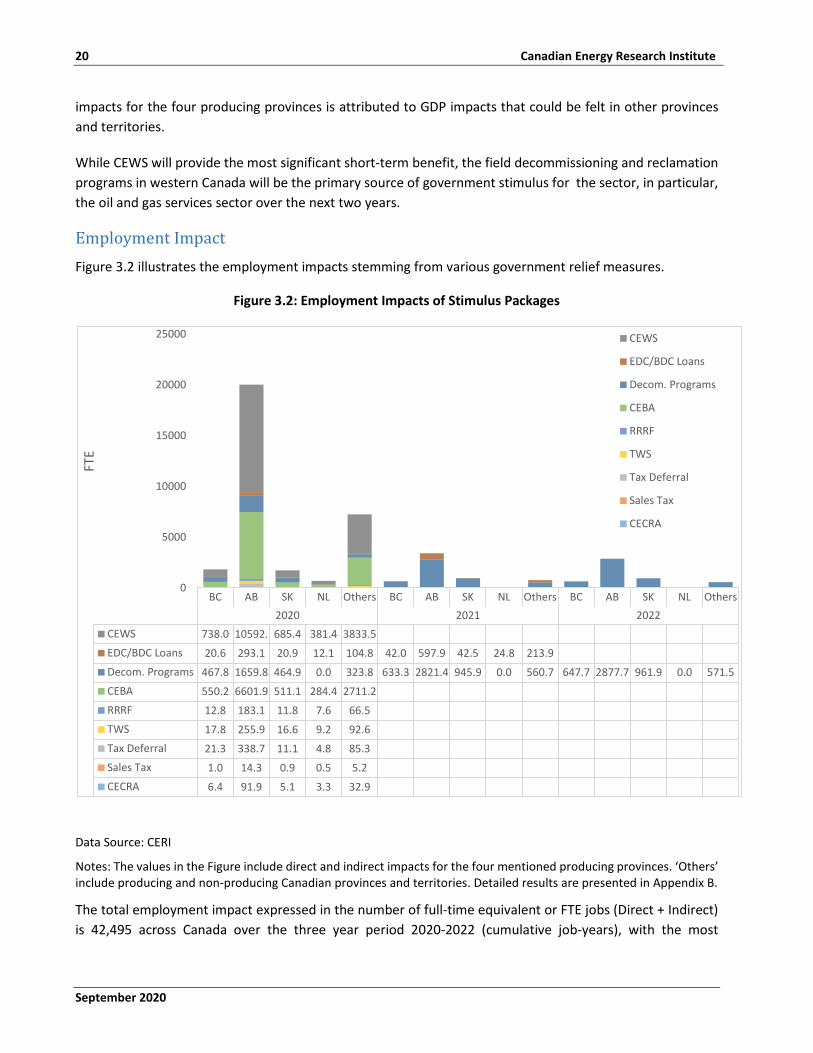

Employment Impact Figure 3.2 illustrates the employment impacts stemming from various government relief measures.

Figure 3.2: Employment Impacts of Stimulus Packages

Data Source: CERI

Notes: The values in the Figure include direct and indirect impacts for the four mentioned producing provinces. ‘Others’ include producing and non-producing Canadian provinces and territories. Detailed results are presented in Appendix B.

The total employment impact expressed in the number of full-time equivalent or FTE jobs (Direct + Indirect) is 42,495 across Canada over the three year period 2020-2022 (cumulative job-years), with the most

BC AB SK NL Others BC AB SK NL Others BC AB SK NL Others2020 2021 2022

CEWS 738.0 10592. 685.4 381.4 3833.5EDC/BDC Loans 20.6 293.1 20.9 12.1 104.8 42.0 597.9 42.5 24.8 213.9Decom. Programs 467.8 1659.8 464.9 0.0 323.8 633.3 2821.4 945.9 0.0 560.7 647.7 2877.7 961.9 0.0 571.5CEBA 550.2 6601.9 511.1 284.4 2711.2RRRF 12.8 183.1 11.8 7.6 66.5TWS 17.8 255.9 16.6 9.2 92.6Tax Deferral 21.3 338.7 11.1 4.8 85.3Sales Tax 1.0 14.3 0.9 0.5 5.2CECRA 6.4 91.9 5.1 3.3 32.9

0

5000

10000

15000

20000

25000

FTE

CEWS

EDC/BDC Loans

Decom. Programs

CEBA

RRRF

TWS

Tax Deferral

Sales Tax

CECRA

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 21

substantial impact to be felt in provinces where oil and gas is extracted. The peak year is 2020, which results in 31,554 FTE due to the CEWS program. Within the total employment impact, the employment impact of decommissioning and reclamation programs could yield almost 13 thousand FTE jobs. Field decommissioning programs have become the leading employment contributors for 2021 and 2022.

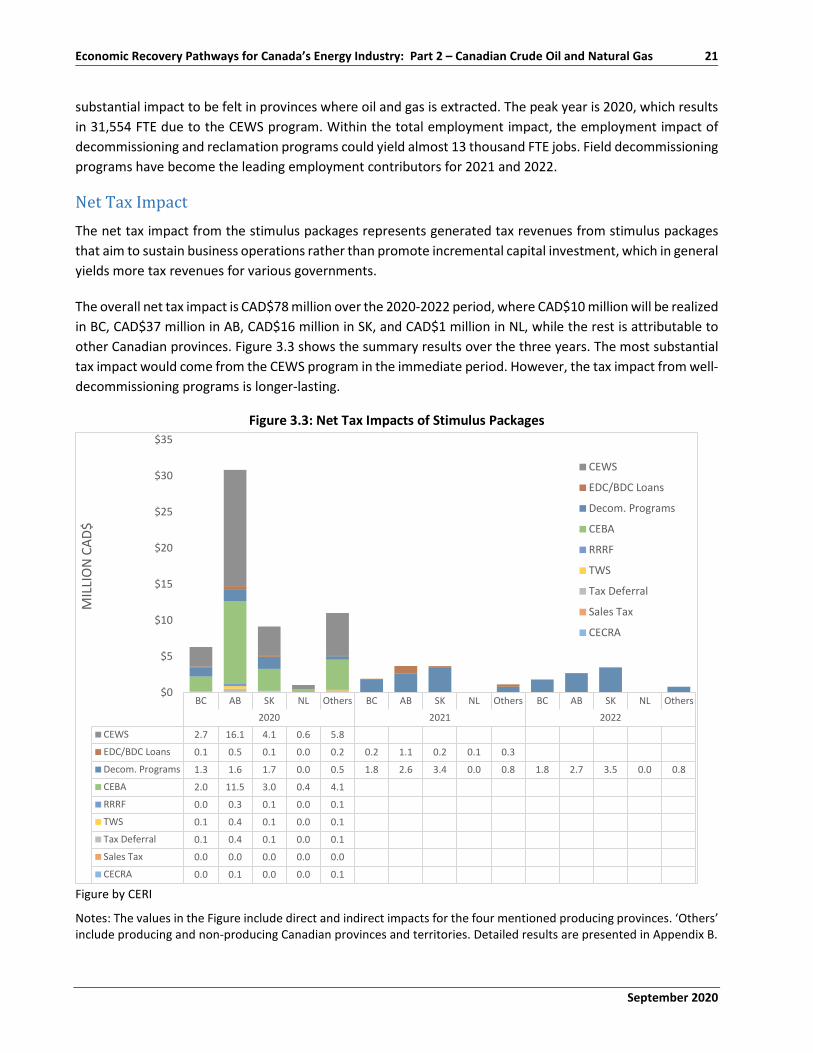

Net Tax Impact The net tax impact from the stimulus packages represents generated tax revenues from stimulus packages that aim to sustain business operations rather than promote incremental capital investment, which in general yields more tax revenues for various governments.

The overall net tax impact is CAD$78 million over the 2020-2022 period, where CAD$10 million will be realized in BC, CAD$37 million in AB, CAD$16 million in SK, and CAD$1 million in NL, while the rest is attributable to other Canadian provinces. Figure 3.3 shows the summary results over the three years. The most substantial tax impact would come from the CEWS program in the immediate period. However, the tax impact from well-decommissioning programs is longer-lasting.

Figure 3.3: Net Tax Impacts of Stimulus Packages

Figure by CERI

Notes: The values in the Figure include direct and indirect impacts for the four mentioned producing provinces. ‘Others’ include producing and non-producing Canadian provinces and territories. Detailed results are presented in Appendix B.

BC AB SK NL Others BC AB SK NL Others BC AB SK NL Others2020 2021 2022

CEWS 2.7 16.1 4.1 0.6 5.8

EDC/BDC Loans 0.1 0.5 0.1 0.0 0.2 0.2 1.1 0.2 0.1 0.3

Decom. Programs 1.3 1.6 1.7 0.0 0.5 1.8 2.6 3.4 0.0 0.8 1.8 2.7 3.5 0.0 0.8

CEBA 2.0 11.5 3.0 0.4 4.1

RRRF 0.0 0.3 0.1 0.0 0.1

TWS 0.1 0.4 0.1 0.0 0.1

Tax Deferral 0.1 0.4 0.1 0.0 0.1

Sales Tax 0.0 0.0 0.0 0.0 0.0

CECRA 0.0 0.1 0.0 0.0 0.1

$0

$5

$10

$15

$20

$25

$30

$35

MIL

LIO

N C

AD$

CEWS

EDC/BDC Loans

Decom. Programs

CEBA

RRRF

TWS

Tax Deferral

Sales Tax

CECRA

22 Canadian Energy Research Institute

September 2020

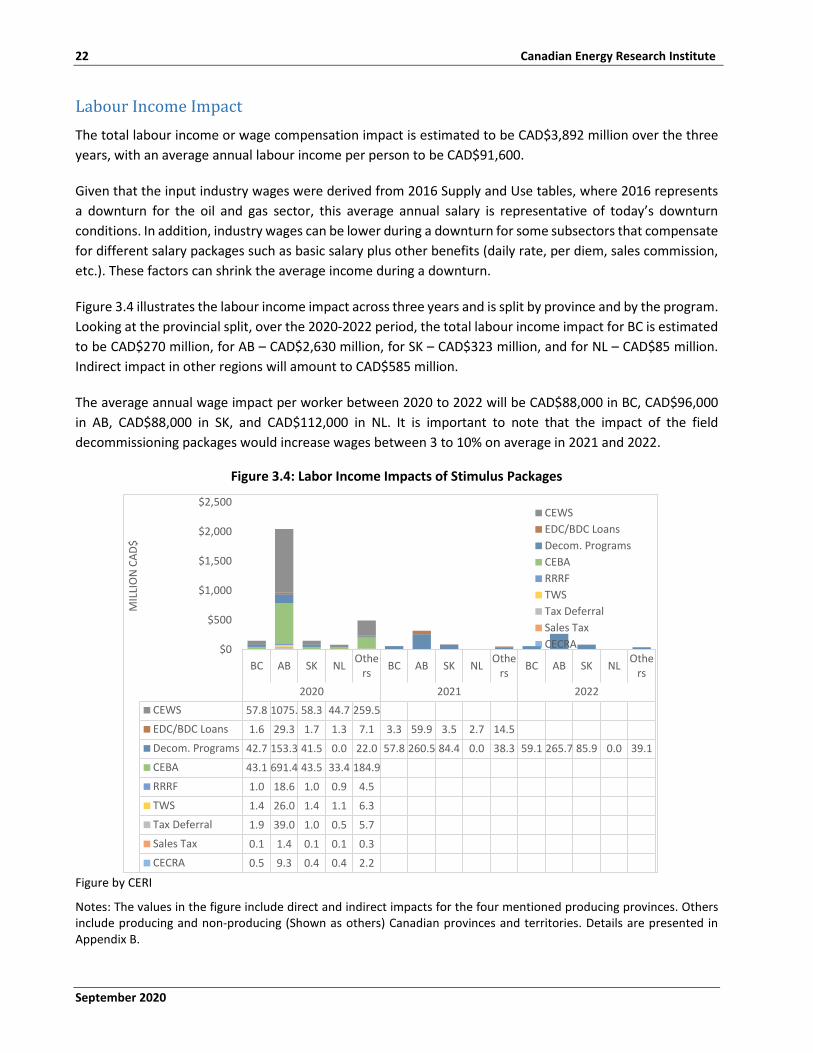

Labour Income Impact The total labour income or wage compensation impact is estimated to be CAD$3,892 million over the three years, with an average annual labour income per person to be CAD$91,600.

Given that the input industry wages were derived from 2016 Supply and Use tables, where 2016 represents a downturn for the oil and gas sector, this average annual salary is representative of today’s downturn conditions. In addition, industry wages can be lower during a downturn for some subsectors that compensate for different salary packages such as basic salary plus other benefits (daily rate, per diem, sales commission, etc.). These factors can shrink the average income during a downturn.

Figure 3.4 illustrates the labour income impact across three years and is split by province and by the program. Looking at the provincial split, over the 2020-2022 period, the total labour income impact for BC is estimated to be CAD$270 million, for AB – CAD$2,630 million, for SK – CAD$323 million, and for NL – CAD$85 million. Indirect impact in other regions will amount to CAD$585 million.

The average annual wage impact per worker between 2020 to 2022 will be CAD$88,000 in BC, CAD$96,000 in AB, CAD$88,000 in SK, and CAD$112,000 in NL. It is important to note that the impact of the field decommissioning packages would increase wages between 3 to 10% on average in 2021 and 2022.

Figure 3.4: Labor Income Impacts of Stimulus Packages

Figure by CERI

Notes: The values in the figure include direct and indirect impacts for the four mentioned producing provinces. Others include producing and non-producing (Shown as others) Canadian provinces and territories. Details are presented in Appendix B.

BC AB SK NL Others BC AB SK NL Othe

rs BC AB SK NL Others

2020 2021 2022CEWS 57.8 1075. 58.3 44.7 259.5EDC/BDC Loans 1.6 29.3 1.7 1.3 7.1 3.3 59.9 3.5 2.7 14.5Decom. Programs 42.7 153.3 41.5 0.0 22.0 57.8 260.5 84.4 0.0 38.3 59.1 265.7 85.9 0.0 39.1CEBA 43.1 691.4 43.5 33.4 184.9RRRF 1.0 18.6 1.0 0.9 4.5TWS 1.4 26.0 1.4 1.1 6.3Tax Deferral 1.9 39.0 1.0 0.5 5.7Sales Tax 0.1 1.4 0.1 0.1 0.3CECRA 0.5 9.3 0.4 0.4 2.2

$0

$500

$1,000

$1,500

$2,000

$2,500

MIL

LIO

N C

AD$

CEWSEDC/BDC LoansDecom. ProgramsCEBARRRFTWSTax DeferralSales TaxCECRA

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 23

Economic Impacts of Oil and Gas Revenues The economic impacts stemming from oil and gas revenues are highly dependent on production and price levels. Hence any variation to either or both of those variables will alter the economic impacts estimated and presented in this section.

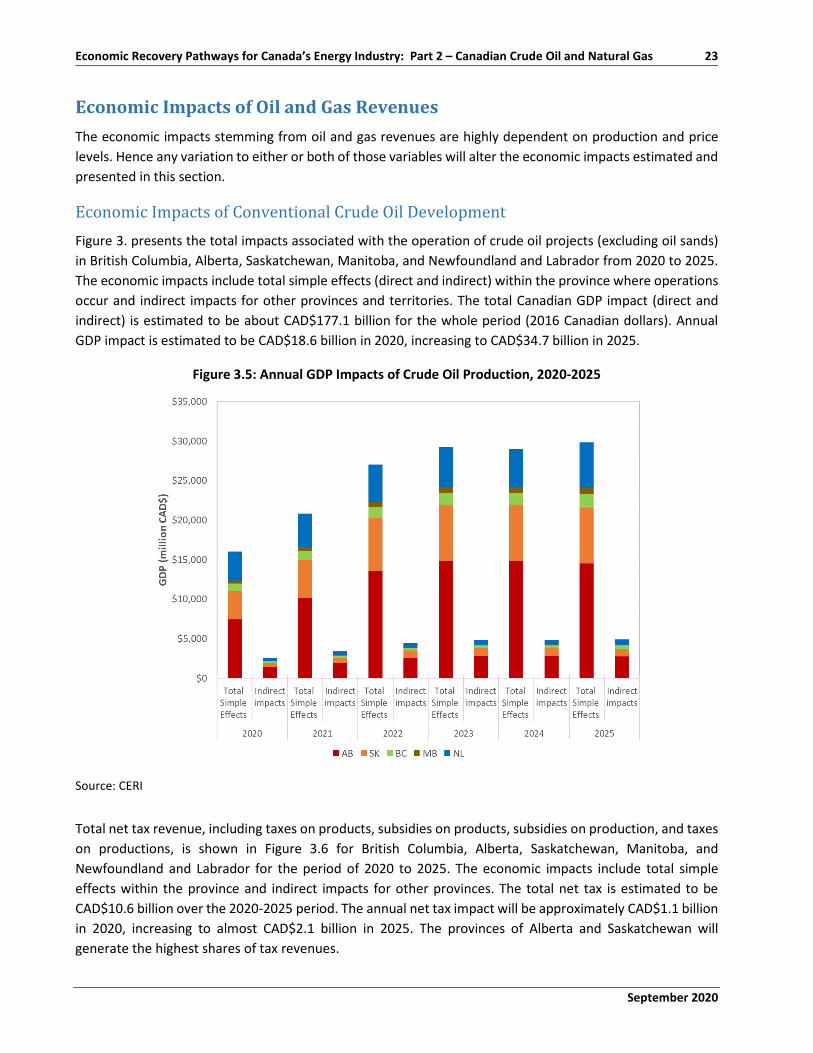

Economic Impacts of Conventional Crude Oil Development Figure 3. presents the total impacts associated with the operation of crude oil projects (excluding oil sands) in British Columbia, Alberta, Saskatchewan, Manitoba, and Newfoundland and Labrador from 2020 to 2025. The economic impacts include total simple effects (direct and indirect) within the province where operations occur and indirect impacts for other provinces and territories. The total Canadian GDP impact (direct and indirect) is estimated to be about CAD$177.1 billion for the whole period (2016 Canadian dollars). Annual GDP impact is estimated to be CAD$18.6 billion in 2020, increasing to CAD$34.7 billion in 2025.

Figure 3.5: Annual GDP Impacts of Crude Oil Production, 2020-2025

Source: CERI

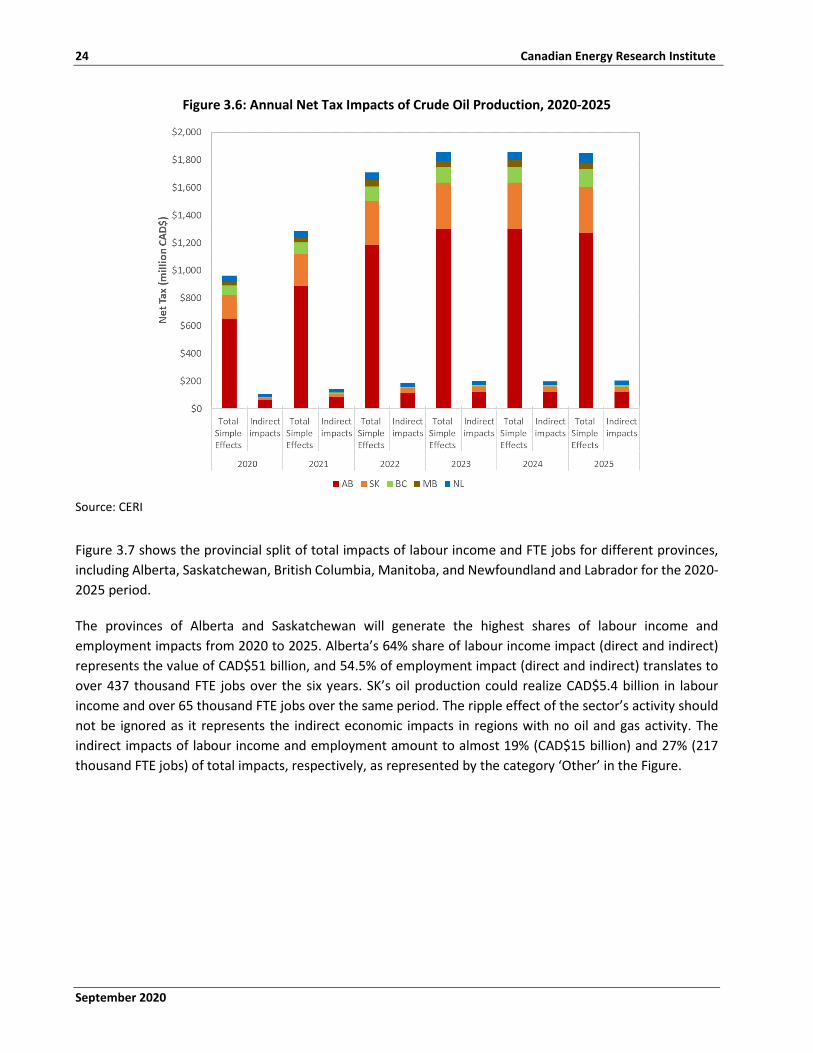

Total net tax revenue, including taxes on products, subsidies on products, subsidies on production, and taxes on productions, is shown in Figure 3.6 for British Columbia, Alberta, Saskatchewan, Manitoba, and Newfoundland and Labrador for the period of 2020 to 2025. The economic impacts include total simple effects within the province and indirect impacts for other provinces. The total net tax is estimated to be CAD$10.6 billion over the 2020-2025 period. The annual net tax impact will be approximately CAD$1.1 billion in 2020, increasing to almost CAD$2.1 billion in 2025. The provinces of Alberta and Saskatchewan will generate the highest shares of tax revenues.

24 Canadian Energy Research Institute

September 2020

Figure 3.6: Annual Net Tax Impacts of Crude Oil Production, 2020-2025

Source: CERI

Figure 3.7 shows the provincial split of total impacts of labour income and FTE jobs for different provinces, including Alberta, Saskatchewan, British Columbia, Manitoba, and Newfoundland and Labrador for the 2020-2025 period.

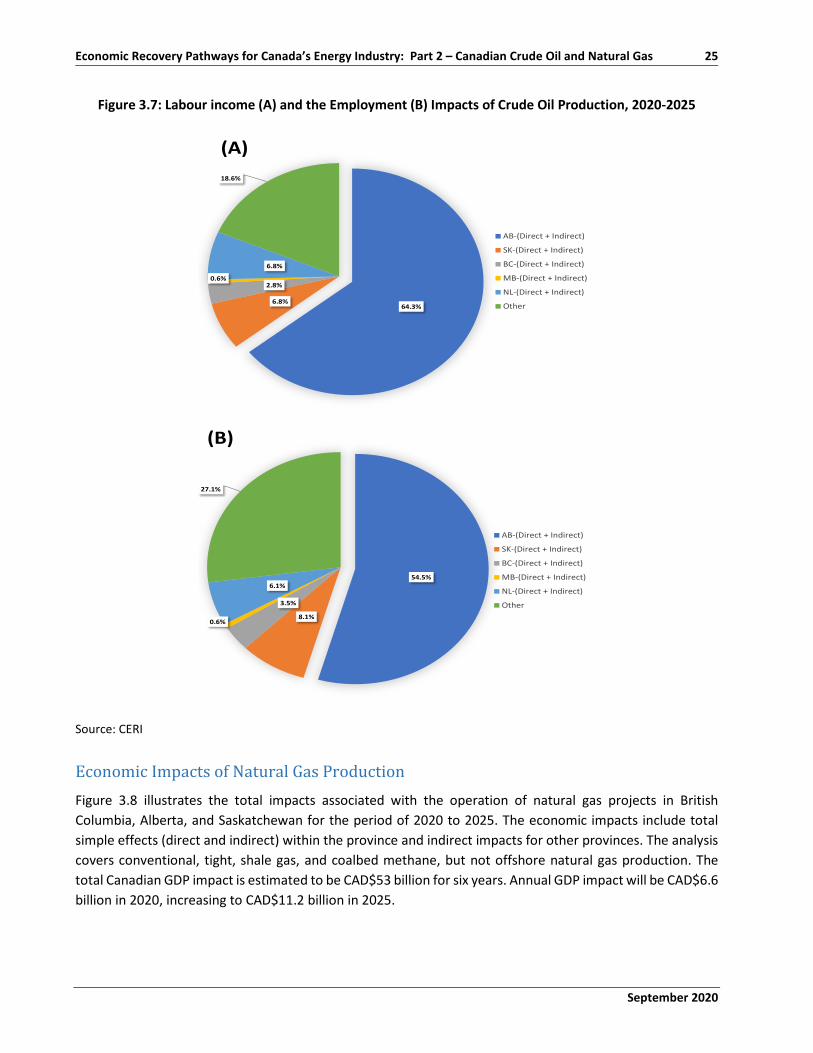

The provinces of Alberta and Saskatchewan will generate the highest shares of labour income and employment impacts from 2020 to 2025. Alberta’s 64% share of labour income impact (direct and indirect) represents the value of CAD$51 billion, and 54.5% of employment impact (direct and indirect) translates to over 437 thousand FTE jobs over the six years. SK’s oil production could realize CAD$5.4 billion in labour income and over 65 thousand FTE jobs over the same period. The ripple effect of the sector’s activity should not be ignored as it represents the indirect economic impacts in regions with no oil and gas activity. The indirect impacts of labour income and employment amount to almost 19% (CAD$15 billion) and 27% (217 thousand FTE jobs) of total impacts, respectively, as represented by the category ‘Other’ in the Figure.

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 25

Figure 3.7: Labour income (A) and the Employment (B) Impacts of Crude Oil Production, 2020-2025

Source: CERI

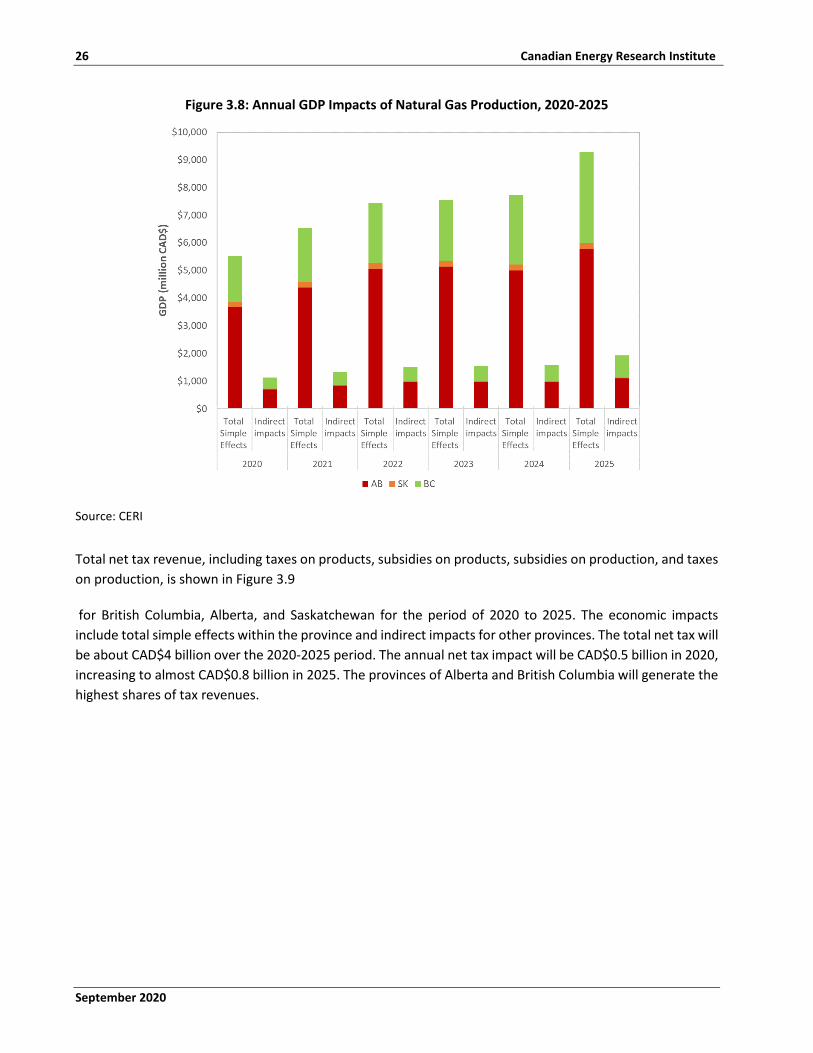

Economic Impacts of Natural Gas Production Figure 3.8 illustrates the total impacts associated with the operation of natural gas projects in British Columbia, Alberta, and Saskatchewan for the period of 2020 to 2025. The economic impacts include total simple effects (direct and indirect) within the province and indirect impacts for other provinces. The analysis covers conventional, tight, shale gas, and coalbed methane, but not offshore natural gas production. The total Canadian GDP impact is estimated to be CAD$53 billion for six years. Annual GDP impact will be CAD$6.6 billion in 2020, increasing to CAD$11.2 billion in 2025.

64.3%6.8%

2.8%0.6%

6.8%

18.6%

AB-(Direct + Indirect)

SK-(Direct + Indirect)

BC-(Direct + Indirect)

MB-(Direct + Indirect)

NL-(Direct + Indirect)

Other

(A)

54.5%

8.1%

3.5%

0.6%

6.1%

27.1%

AB-(Direct + Indirect)

SK-(Direct + Indirect)

BC-(Direct + Indirect)

MB-(Direct + Indirect)

NL-(Direct + Indirect)

Other

(B)

26 Canadian Energy Research Institute

September 2020

Figure 3.8: Annual GDP Impacts of Natural Gas Production, 2020-2025

Source: CERI

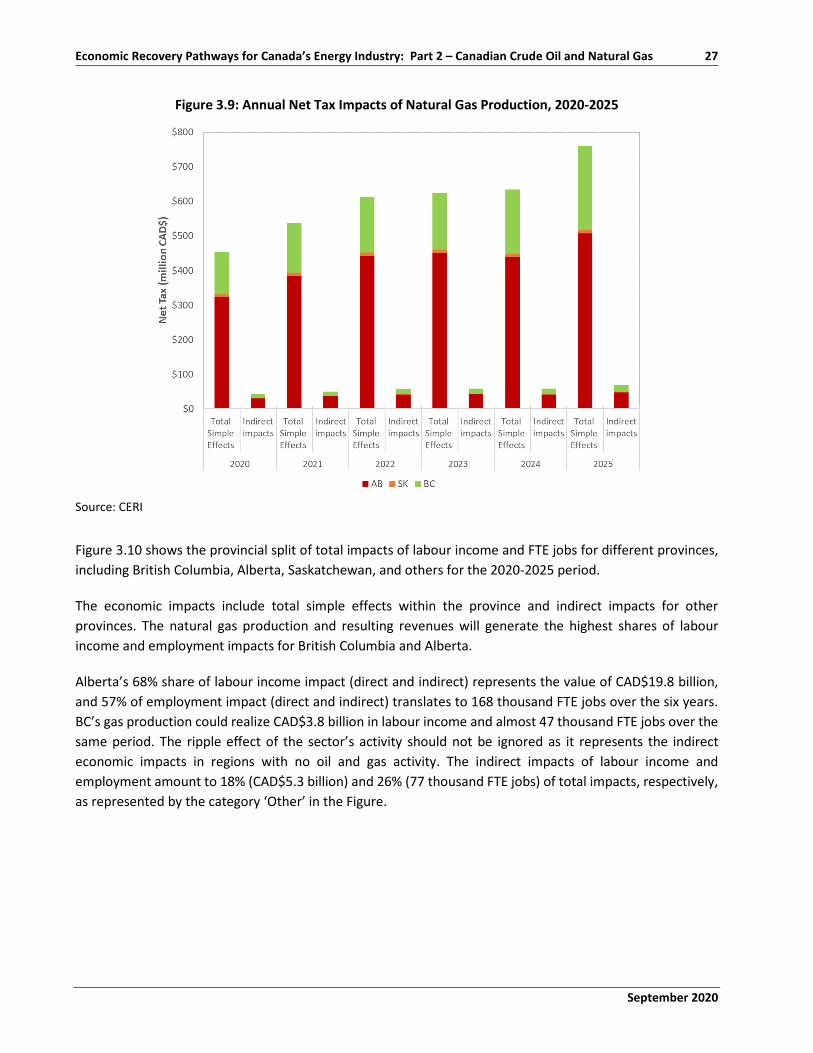

Total net tax revenue, including taxes on products, subsidies on products, subsidies on production, and taxes on production, is shown in Figure 3.9

for British Columbia, Alberta, and Saskatchewan for the period of 2020 to 2025. The economic impacts include total simple effects within the province and indirect impacts for other provinces. The total net tax will be about CAD$4 billion over the 2020-2025 period. The annual net tax impact will be CAD$0.5 billion in 2020, increasing to almost CAD$0.8 billion in 2025. The provinces of Alberta and British Columbia will generate the highest shares of tax revenues.

September 2020

Economic Recovery Pathways for Canada’s Energy Industry: Part 2 – Canadian Crude Oil and Natural Gas 27

Figure 3.9: Annual Net Tax Impacts of Natural Gas Production, 2020-2025

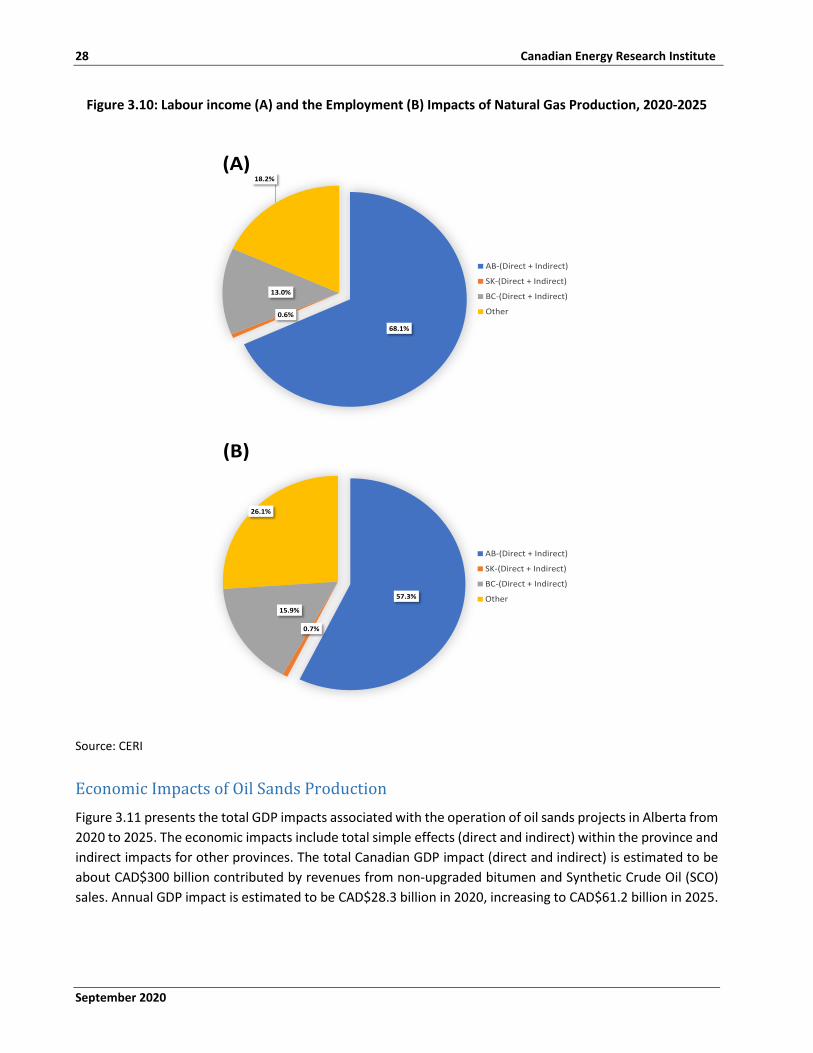

Source: CERI