Embed Size (px)

Citation preview

Major Economic Problems facing PakistanBy: Suleman Ahmad -

10254

Presentation Part: 1HISTORICAL PERSPECTIVE

Nineties - A lost Decade•Each Government, in reality, adhering to

similar short term, and short sighted, approach to economic management with similar results.

•Still in the Ricardian era of saving/investment deficiency rather than in the Keynesian period of idle capacity and lack of effective demand.

Natural Calamities•Floods – failure to build dams

•Earthquakes – a lost opportunity to utilize the foreign aid flows.

IMF and World Bank•Showed support of short term economic

policy patchwork - accommodated lapses in policy promises and commitments.

•Additional Foreign Loans – provided support but took Pakistan in deeper long term debt difficulties. The conditionality varied from time to time.

IMF and World Bank• Resulted in increasing foreign debt servicing

liability, without a corresponding expansion in foreign exchange earning capacity.

• The way to economic welfare is through concessional rescheduling, restructuring and write offs but the Government should first decide and demonstrate determination to move on a self sustaining, and self respecting, path of economic and social development.

Good Governance•One of the biggest problems of the

country.

•There can be no real breakthrough in the economic management of the country without the emergence of good governance and stable institutional foundation.

Presentation Part: 2MACRO ECONOMIC PROBLEMS

OF PAKISTAN

Introduction•Implementation of difficult policy choices,

and not their diagnosis, is the real problem of economic management in Pakistan.

•Poor governance is giving birth to mismanagement of public finances which, in turn, has become the mother of all economic ills.

Savings and Investments Relation with GDP

Savings and Investments Relation with GDP• If we see the graph, it could be seen easily that the three are

positively correlated. The slopes where the GDP growth has fallen are those periods when the saving and investment have gone down as well.

• For example in 1981-82, with GDP growth rate of 7.56% the simultaneous growth rates of savings were 9.9% and that of investment were 19.62% (7.71% growth of GDP in 1991-92, combined with a growth rate of 41.91% for Savings growth and 26.16% for national investment).

• This correlation is stronger between GDP growth and investment and less strong for national savings growth rate where more lagged relation is present.

Gross Domestic Savings (% of GDP)

Gross Capital Formation (% of GDP)

Saving and Investment Stimulus• The saving and investment are the stimulus which is

lacking in Pakistan for its desired economic growth.

• In 60’s Pakistan’s Domestic investment was almost the same as that of Korea, Malaysia and Thailand. Only Japan had 29.1% of GFC as a percentage of GDP, then in 1965 still Pakistan was ahead of them, but afterwards it dropped. In 1995 Pakistan’s closest country was almost spending twice as much as Pakistan for her investment expenditure (Indonesia with 28.4% of GDP vs. Pakistan’s 17.1% of GDP).

Saving and Investment(% of GDP)

Aggregate Investment Gap with Competitors

3.14%

-9.18%

-0.91%

-6.81%

-0.26%

-6.31%

0.93%

-2.75%

2.92%

-3.54%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Pakistan-Bangladesh

Pakistan-India Pakistan-South Asia

Pakistan-LowIncome

Pakistan-LowMiddle Income

1982-1991

1992-2001

TRENDS IN PRIVATE INVESTMENTS

Figure 2.2b: Trends in Private Investment (% of GDP)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

IndiaPakistanBangladesh

POLITICAL INSTABILITY• A systematic approach has been adopted by these

countries to isolate Pakistan in the global arena. But instead of unity, our political parties are playing dirty games against one another.

• These parties are least bothered about the security situation of Pakistan. Their vision is just to secure the supreme office for next five years; they are unaware of the agendas of the foreign powers who prepare plan for next 50 years.

• Political stability in the country will attract the foreign investors and boost our national economy

LAW AND ORDER - TERRORISM• Foreign investors are afraid of investing

their money in establishing new industries. On the other hand, those who have well-established businesses try to withdraw their money.

• Statistical data shows that damage to the Pakistani economy is estimated at $68 billion over the last ten years.

NEED OF ENTREPRENURIAL INITIATIVES• The role of the entrepreneur in economic development is

central; he starts businesses and provides jobs. In Pakistan this sector provides 80% of non-farm employment, contributes 40% to GDP and has a 25% share in the country's exports.

• In the case of Pakistan, the green revolution in agriculture, the industrialization of the '60s and the development of the textile industry in the ‘80s and '90s are some of the examples of transformative entrepreneurial activity.

• The quality of entrepreneurial activity in Pakistan will improve as the overall context will become better, the quality and spread of education being the primary driver and the development of the physical infrastructure a very important element.

INFLATION

INFLATION

FISCAL IMBALANCE

FISCAL IMBALANCE•A large part of the fiscal slippage was due

to a heavy payment for the resolution of the circular debt that was not initially budgeted for. Excluding these payments, the budget deficit for FY13 declines to 6.6 percent of GDP, slightly lower than the 6.8 percent deficit recorded in FY12.

REASONS FOR THE IMBALANCE(1) underestimation of subsidies(2) underestimation of interest payments;

and(3)overestimation of FBR tax revenue.

Tax to GDP Ratio

Expenditure and Debt Servicing

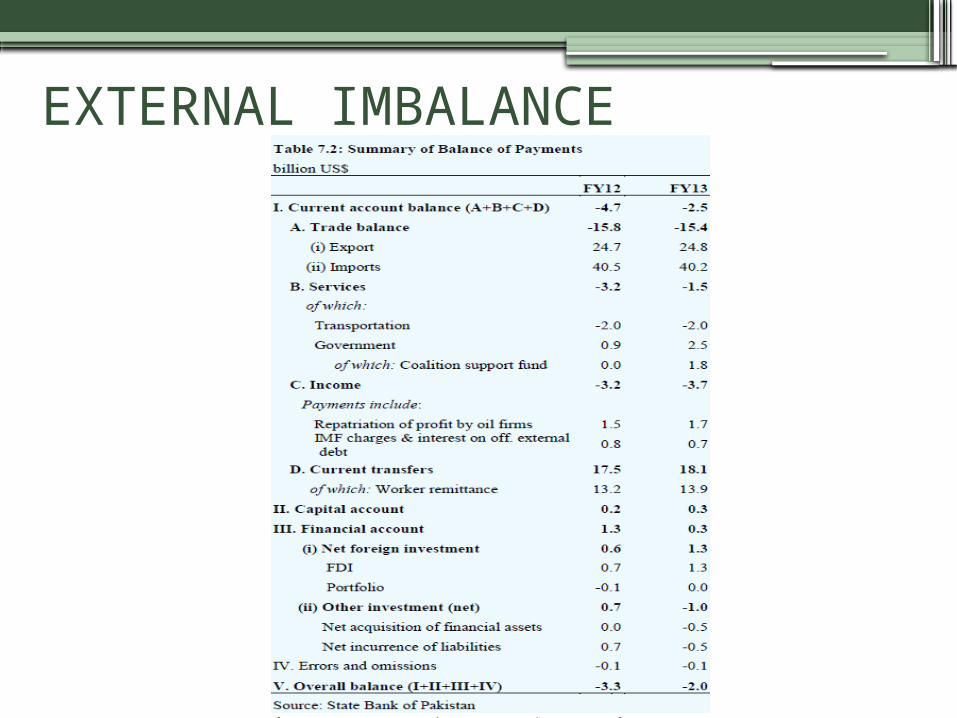

External Imbalance•The current account posted a deficit of

US$ 2.5 billion in FY13, which was nearly half the deficit seen last year. As mentioned before, this improvement can be traced to the CSF inflows of US$ 1.8 billion in FY13.

•Workers Remittances continued their upward trend by posting a figure of 13.9b$ for the FY13 almost meeting the target of 14billion$.

EXTERNAL IMBALANCE

FOREIGN DIRECT INVESTMENT• Foreign investments picked up in FY13 to

reach US$ 1.3 billion, compared with just US$ 0.6 billion last year. This is a welcome increase, but the level of FDI remains glaringly low due to: election-related political uncertainty; security concerns; and the vulnerability of Pakistan’s external account. In addition to domestic factors, the global investment environment was not conducive: FDI in both developed and developing countries has struggled to recover.

DOMESTIC AND EXTERNAL DEBT•Despite the one percentage point

reduction during FY13, Pakistan’s public debt is still 63.3 percent of GDP – higher than the ceiling of 60 percent under the Fiscal Responsibility and Debt Limitation Act (FRDL) of 2005.

•Pakistan is already involved in a debt trap.

FURTHER IMPLICATIONS•More importantly, the mounting domestic

debt (which now makes up around two-third of the entire public debt, compared to 59 percent last year) entails significant risks to Pakistan’s fiscal and debt outlook. Two of the most important issues are:

(1) Rise in the debt servicing burden(2)Worsening maturity profile increases

roll-over and interest-rate risk

TOTAL DEBT

IMPLICATIONS OF OVERBURDENING DEBTSuch mounting debt will have adverse consequences for the economy: • it will hold back economic growth•limit the scope for discretionary (monetary

and fiscal) policies• increase vulnerability to exogenous shocks•raise the tax burden on captive payers,

which will discourage investment •create more uncertainty in the economy.

IMPACT OF RECESSION• The surge in commodity prices that preceded the

recession had taken its toll on Pakistan and precluded the use of a comparable stimulus package. The then regime in Pakistan had chosen not to pass the full impact of the rise in commodity prices in 2007 to the consumers. This among other policies had contributed to a sudden increase in the fiscal deficit for FY 2007-08. When the recession set in the fiscal deficit was already high and the external account was in poor shape. Pakistan requested IMF financing to stay afloat and in turn agreed to implement fiscal tightening.

Presentation Part: 3POLICY ALTERNATIVES

RECOMMENDATIONS Mobilization of Domestic Savings

• The country needs to have a policy framework to sustain an annual rate of growth of 6- 8 per cent with growth impulses emanating from all the productive sectors of the economy, and fruits of growth being shared by all segments of society.

• It can ensure an environment of relative price stability, soundness of the financial and fiscal systems, balance of payment viability, and efficient resource utilization that increases agricultural yield and improves industrial efficiency. The real long run policy issue, therefore, is as to what can be done to raise the domestic low rate of saving, which in combination with external non debt creating inflows, can match up with the required rate of investment.

RECOMMENDATIONS•Implementation of a sound Budget Budgetary measures should include

mobilization of additional revenue resources, severe curtailment of inessential and unproductive government expenditure, and honest and efficient use of development expenditure to facilitate economic development and improve the economic wellbeing of the majority of the population.

RECOMMENDATIONS• Tight Monetary Policy: The SBP should implement a prudent monetary policy

that is not hostage to the financing needs of the government.

• Fiscal Reforms: In order to raise revenues, restructure loss-making

PSEs, and contain untargeted subsidies. In this regard, one of the key areas to focus on is the energy sector. Untargeted energy subsidies were responsible for the persistently large fiscal deficits in the past several years, and growth in the country’s domestic debt

RECOMMENDATIONS• Taxation Reforms

To increase the revenues the tax to GDP ratio must be increased and tax base broadened to include more tax payers.

• Implementation of Policies Whatever policy is made, good governance and

implementation is required to make any kind of change in the present scenario of the Pakistan Economy.

RECOMMENDATIONS• Tight Monetary Policy: The SBP should implement a prudent monetary policy

that is not hostage to the financing needs of the government.

• Fiscal Reforms: In order to raise revenues, restructure loss-making

PSEs, and contain untargeted subsidies. In this regard, one of the key areas to focus on is the energy sector. Untargeted energy subsidies were responsible for the persistently large fiscal deficits in the past several years, and growth in the country’s domestic debt

RECOMMENDATIONS• Bring down the Interest Rate Spread

The SBP has the institutional responsibility and legal authority to bring down this spread within the normal limits obtaining in other countries and on that basis to ensure a higher nominal rate of return on deposits and lower cost of borrowing of the private sector.

• Increase Private Sector Savings• contributory retirement schemes • Tax incentives • Austerity in government expenditures• Development of capital markets and discouragement

of conspicuous consumption

CONCLUSION•Pakistan is rich in human and material

resources but poor governance of the country has impeded the process of exploitation of these resources. Among macroeconomic problems faced by the country, budget mismanagement is the mother of most economic ills in Pakistan. Pakistan has the potential to change, it just needs the will and the leadership needs to set the trends.

Thank You!