Embed Size (px)

Citation preview

Bureau of Economic Geology, The University of Texas at Austin

Economic & Policy ConsiderationsReserves Symposium, July 19, 2011

©CEE-UT, 2

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

Do You Believe???

• Reserves estimation is “science + art”• Usefulness of reserves is contingent on

confidence– Reliability, quality of reporting– Due diligence is equal opportunity, but costly

• Frontier, unconventional plays raise new challenges

• FD cost, commodity price variability

©CEE-UT, 3

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

“Art”: A Proposed Definition

The ability to visualize, build and executea concept for optimal commercialization of upstream assets based on valuations using thorough analysis of, and reasonable and sound scientific interpretation of, G&G and engineering data and information.

©CEE-UT, 4

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

Project Based

http://www.spe.org/industry/docs/PRMS_Development_Process_Slides.pdf

©CEE-UT, 5

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

SPE Description of Uncertainty

http://www.spe.org/industry/docs/PRMS_Development_Process_Slides.pdf

©CEE-UT, 6

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

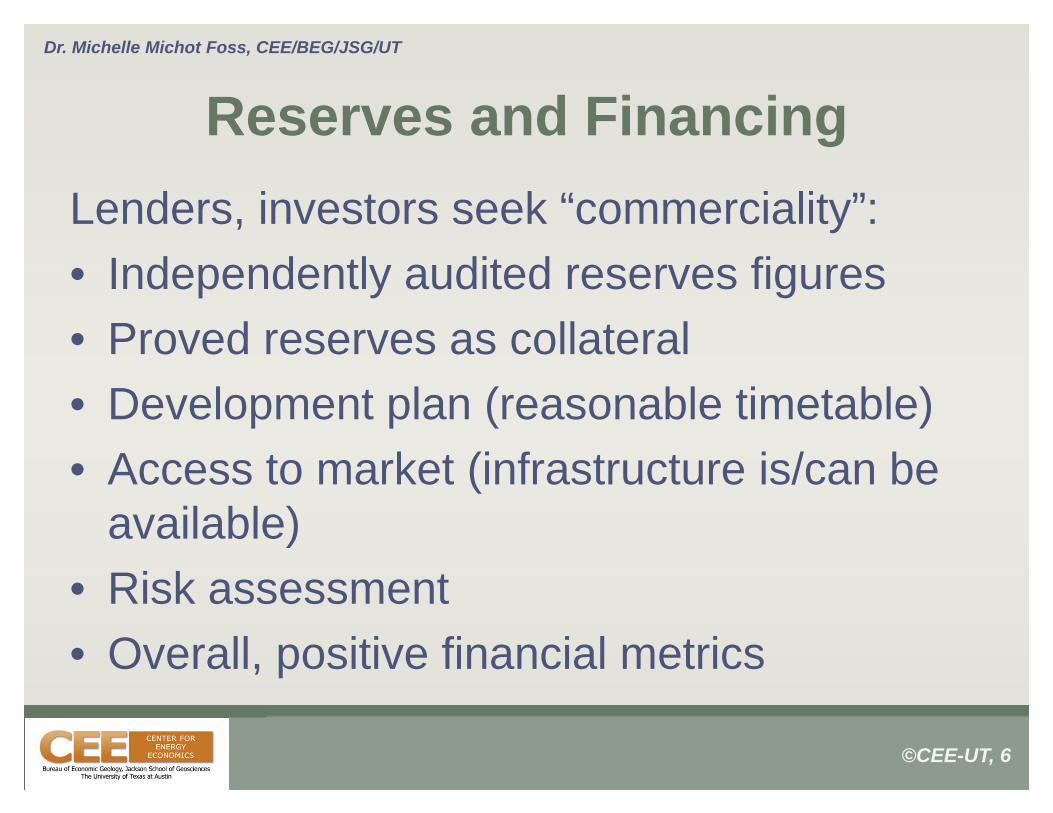

Reserves and FinancingLenders, investors seek “commerciality”:• Independently audited reserves figures• Proved reserves as collateral• Development plan (reasonable timetable)• Access to market (infrastructure is/can be

available)• Risk assessment• Overall, positive financial metrics

©CEE-UT, 7

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

Reserves Definitions Matter• IOCs investing globally have to comply with

regulations and market expectations– Fiscal regimes have to be conducive to

reporting and revenues to shareholders• Governments and NOCs

– Petrobras pays Brazilian government about 50% of value it generates

– Pemex pays Mexican government about 80% of value it generates

©CEE-UT, 8

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

CEE analysis based on U.S. EIA FRS

©CEE-UT, 9

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

U.S. Nat Gas Cost Structure, 1

©CEE-UT, 10

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

U.S. Nat Gas Cost Structure, 2

$(3.00)

$(2.50)

$(2.00)

$(1.50)

$(1.00)

$(0.50)

$‐

$0.50

$1.00

$1.50

$2.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14

U.S. 09 Cash Exploration Costs $/MCFE

U.S. Cash Operating Costs $/MCFE

U.S. All Source FD Costs, $/MCFE

Differences, 2009‐2010

Avg.

Challenges:•High variability in geology (matrix porosity)•High variability in cost structure

©CEE-UT, 11

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

API

©CEE-UT, 12

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

API

©CEE-UT, 13

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

Fiscal Agreements Decisions

©CEE-UT, 14

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

Upstream Regimes

Approximations based on Foss, et.al., 1998, Best Practices in Energy Sector Reform (CEE-UT).

Recent fiscal regime changes (up is more favorable)

Relative Risk, Reserve Position (Prospectivity)

Qua

lity

of C

omm

erci

al

Fram

ewor

ks

Favorable

Colombia

Canada

Saudi Arabia

VenezuelaRussia

United States (all)

ChinaIndiaBrazil

Mexico

Norway

FavorableKuwait

United Kingdom

U.S. Gulf of Mexico(Federal, non-moratoria)

Iraq

Nigeria

UAE

Iran Other FSU

2001

2007

(Alberta)

Note: Investor (oil company) perspective

©CEE-UT, 15

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

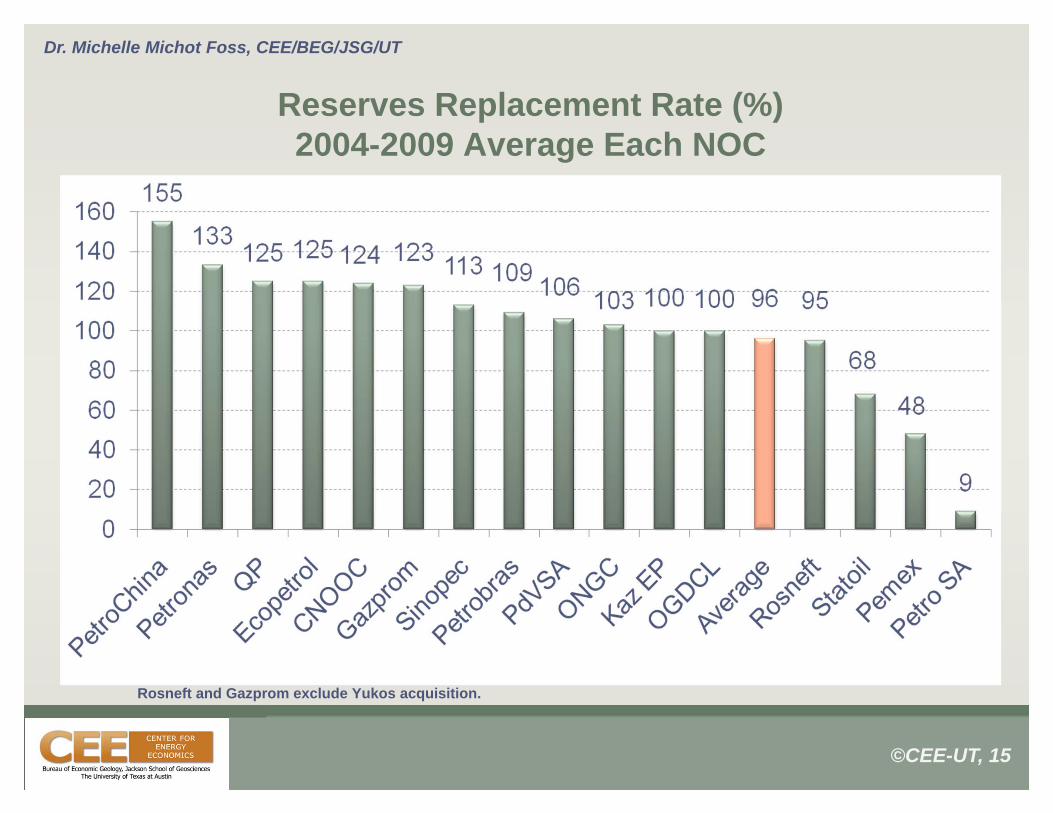

Reserves Replacement Rate (%)2004-2009 Average Each NOC

Rosneft and Gazprom exclude Yukos acquisition.

©CEE-UT, 16

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

All Source Reserve Replacement Cost US$/BOE2004-2009 Average Each NOC

* Companies with less than 6 years of data

Challenges:•High variability in cost structure•Maturity and regime

©CEE-UT, 17

Dr. Michelle Michot Foss, CEE/BEG/JSG/UT

Conclusions

• It’s not a perfect world– Transparency is critical

• Technical challenges need to be addressed– Everyone loses if envelope pushed too far

• Substitutes to reserves are not attractive