Embed Size (px)

Citation preview

Relevant • Independent • Objectivewww.ceri.ca1

Economic Impacts of Low Crude Prices on the Canadian Economy

Canadian Energy Research Institute

Dinara MillingtonCanadian Energy Research Institute

Ryder Scott Canada Reserves ConferenceMay 10, 2016

Relevant • Independent • Objectivewww.ceri.ca2

Canadian Energy Research Institute

Founded in 1975, the Canadian Energy Research Institute (CERI) is an independent, non-profit research institute specializing in the analysis of energy economics and relatedenvironmental policy issues in the energy production, transportation, and consumptionsectors.

Our mission is to provide relevant, independent, and objective economic research ofenergy and environmental issues to benefit business, government, academia and thepublic.

Our core supporters include the Canadian Government (Natural Resources Canada), theGovernment of Alberta (Alberta Energy), and the Canadian Association of PetroleumProducers (CAPP), Chemistry Industry Association of Canada (CIAC), Alberta’s IndustrialHeartland Association (AIHA), and the University of Calgary. In-kind support is alsoprovided by the Alberta Energy Regulator (AER) and Petroleum Services Association ofCanada (PSAC).

All of CERI’s research is placed in the public domain and can be accessed via our websiteat www.ceri.ca .

Relevant • Independent • Objectivewww.ceri.ca3

Agenda

CERI’s Study 156: “Low Crude Oil Prices and Their Impact on the Canadian Economy”:

• Background• Modelling Methodology• Assumptions• Results on National Level• Results for Selected Provinces• Conclusions

Relevant • Independent • Objectivewww.ceri.ca4

Background: Crude Oil Prices (Jan’13 – Mar’16)

$0

$20

$40

$60

$80

$100

$120

$140

US$

/bbl

Cushing, OK WTI Spot Price FOB (US$/bbl)

Europe Brent Spot Price FOB (US$/bbl)

Source: EIA

Relevant • Independent • Objectivewww.ceri.ca5

Modelling Methodology: I/O Model

CERI’s Canada Multi-Regional Input/Output Model (UCMRIO 3.0):

• Addresses the way economic circumstances in one part of an economy can ripple through the rest of it;

• Determines an approximate impact on various economic variables due to the introduction to the economy of a particular set of expenditures or ‘shocks’;

• Models any activity that leads to increased production capacity in an economy: the construction or development of the capacity, and the operation of the capacity to generate outputs.

Relevant • Independent • Objectivewww.ceri.ca6

Modelling Methodology: Scenarios

• Investment:• Reference Case Capital Investment in oil sands

• Operations:• Oil Sands Revenues (Reference Case price and production)

Reference Case

• Investment:• Low Case Capital Investment in oil sands

• Operations:• Oil Sands Revenues (Low Case price and production)• Change in non-energy exports*

Low Case

*Incremental change in non-energy exports as a result of a low exchange rate will only transpire on the operations side of the aforementioned economic sectors. In other words, no capital investment assumption is made to build production capacity in thosefive economic sectors in the 7-year time period.

Relevant • Independent • Objectivewww.ceri.ca7

Assumptions for Two Scenarios

Relevant • Independent • Objectivewww.ceri.ca8

Assumptions for Two Scenarios: Oil Prices

$53.25

$67.58 $69.94 $69.44 $70.43 $71.36 $72.88 $87.63

$102.15 $98.88 $100.36 $93.26

$46.26 $45.94 $46.14 $46.84 $48.61 $50.32 $51.52

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2014

US$

/bb

l

EIA_AEO Ref.Case EIA_AEO Low Case

Source: EIA

Relevant • Independent • Objectivewww.ceri.ca9

Assumptions for Two Scenarios: Oil Sands Production and Capital Investment

2,027 2,078 2,255

2,398 2,602

2,746 2,942

1,338 1,470

1,621 1,752

1,976 2,074 2,230

2,478 2,651

2,801 3,008

3,138

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

('000

b/d

)

Net Bitumen and SCO to Market-Low Case Net Bitumen and SCO to Market-Ref Case

-

5,000

10,000

15,000

20,000

25,000

30,000

2015 2016 2017 2018 2019 2020 2021

(Mln

CDN

$)

Capital Investment-Ref Case Capital Investment-Low Case

Relevant • Independent • Objectivewww.ceri.ca10

Assumptions for Two Scenarios: Non-Energy Exports

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

2015 2016 2017 2018 2019 2020 2021

(CDN

Mln

$)

Other balance of payments adjustments [C24] Special transactions trade [C23]

Consumer goods [C22] Aircraft and other transportation equipment and parts [C21]

Motor vehicles and parts [C19] Electronic and electrical equipment and parts [C18]

Industrial machinery, equipment and parts [C17] Basic and industrial chemical, plastic and rubber products [C15]

Metal and non-metallic mineral products [C14] Metal ores and non-metallic minerals [C13]

Non-Energy Exports in CDN$

Relevant • Independent • Objectivewww.ceri.ca11

Summary of Results: Total Impacts on Canadian Economy (Cumulative 2015-2021)

2015-2021 Unit of Measure Ref.Case Low Case Low vs. Ref.

Case % Change

GDP Growth Mln CDN$ 830,336 626,887 ($203,449) -24.5%

Compensation Mln CDN$ 384,578 297,680 ($86,898) -22.6%

EmploymentThousand person-years

4,109 3,298 (811) -19.7%

Federal Taxes Mln CDN$ 95,063 71,307 ($23,756) -25.0%

Provincial Taxes Mln CDN$ 58,543 45,457 ($13,087) -22.4%

Relevant • Independent • Objectivewww.ceri.ca12

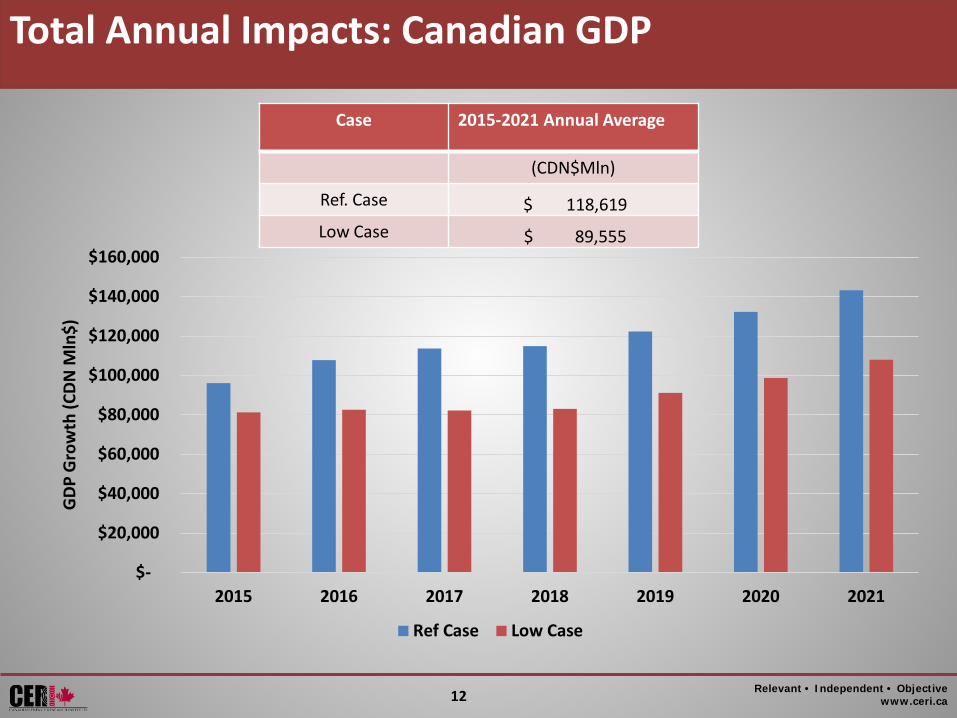

Total Annual Impacts: Canadian GDP

Case 2015-2021 Annual Average

(CDN$Mln)

Ref. Case $ 118,619 Low Case $ 89,555

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

2015 2016 2017 2018 2019 2020 2021

GDP

Gro

wth

(CDN

Mln

$)

Ref Case Low Case

Relevant • Independent • Objectivewww.ceri.ca13

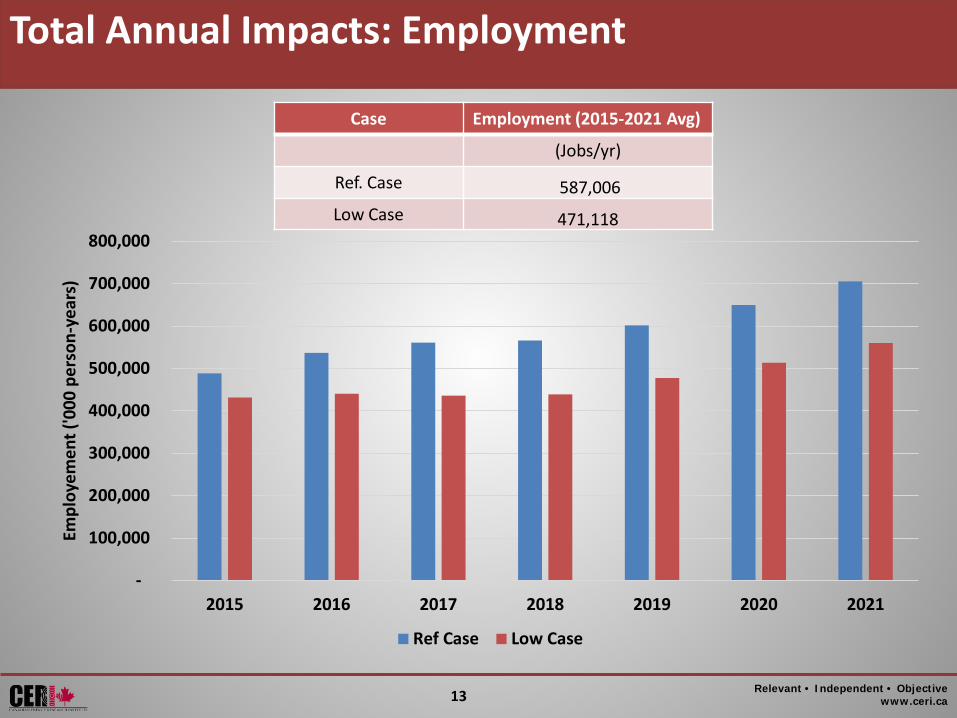

Total Annual Impacts: Employment

Case Employment (2015-2021 Avg)

(Jobs/yr)

Ref. Case 587,006 Low Case 471,118

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2015 2016 2017 2018 2019 2020 2021

Empl

oyem

ent (

'000

per

son-

year

s)

Ref Case Low Case

Relevant • Independent • Objectivewww.ceri.ca14

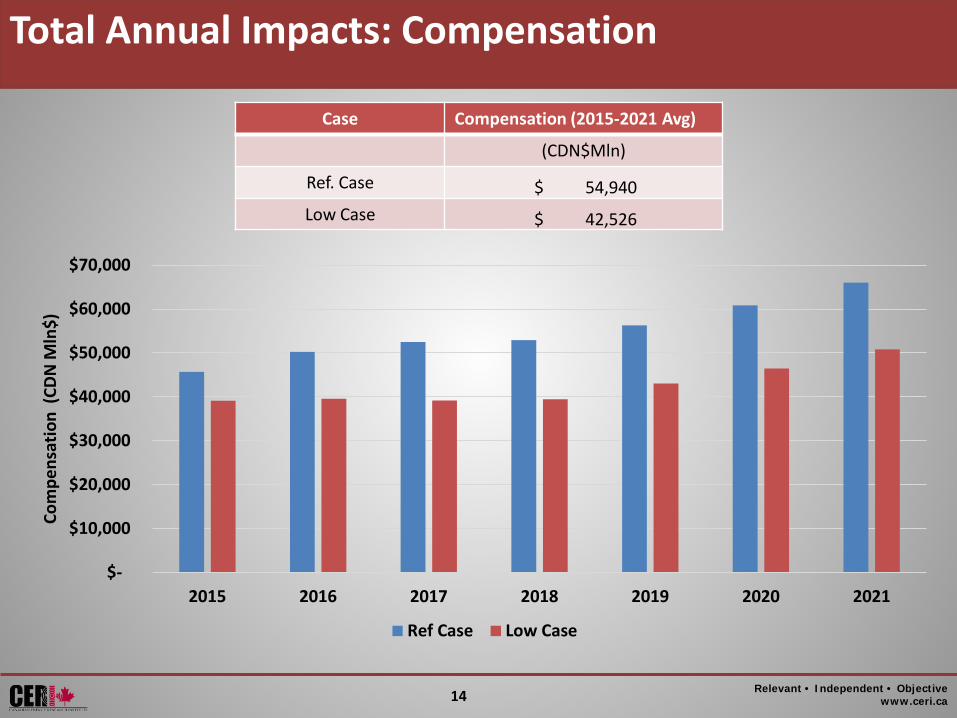

Total Annual Impacts: Compensation

Case Compensation (2015-2021 Avg)

(CDN$Mln)

Ref. Case $ 54,940 Low Case $ 42,526

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

2015 2016 2017 2018 2019 2020 2021

Com

pens

atio

n (C

DN M

ln$)

Ref Case Low Case

Relevant • Independent • Objectivewww.ceri.ca15

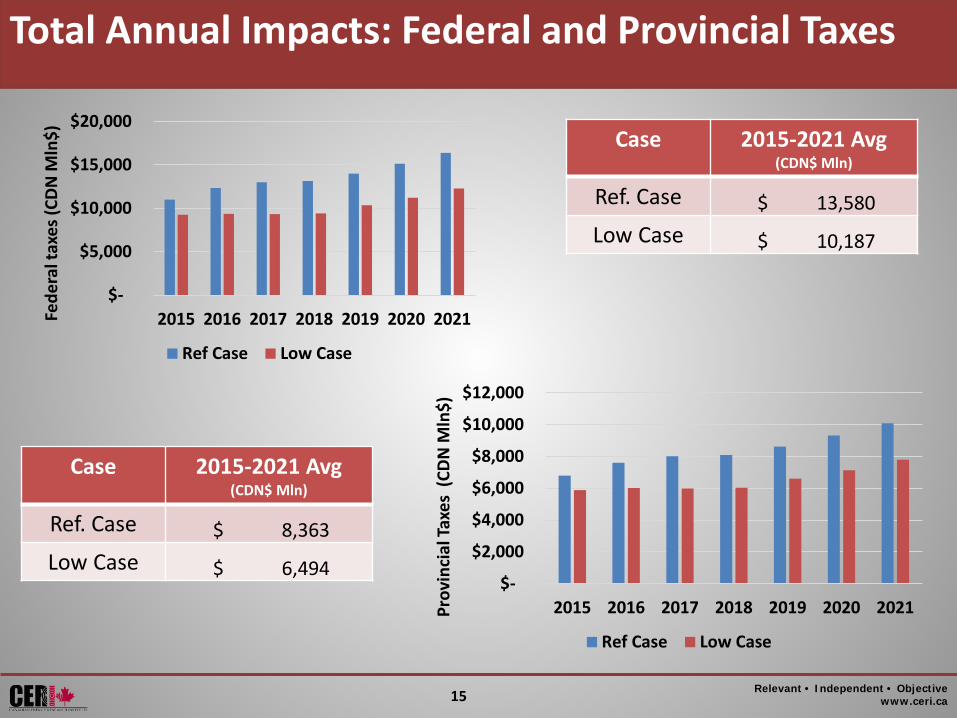

Total Annual Impacts: Federal and Provincial Taxes

Case 2015-2021 Avg (CDN$ Mln)

Ref. Case $ 13,580 Low Case $ 10,187

Case 2015-2021 Avg (CDN$ Mln)

Ref. Case $ 8,363 Low Case $ 6,494

$-

$5,000

$10,000

$15,000

$20,000

2015 2016 2017 2018 2019 2020 2021Fede

ral t

axes

(CD

N M

ln$)

Ref Case Low Case

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2015 2016 2017 2018 2019 2020 2021Prov

inci

al Ta

xes

(CDN

Mln

$)

Ref Case Low Case

Relevant • Independent • Objectivewww.ceri.ca16

Provincial Impacts for AB and ON

Rank Industry % Share of GDP

Ref Case Low Case % change

AB 1 Oil Sands 39.72% $ 331,018 $ 227,898 -31.2%

AB 2 Household 11.71% $ 97,582 $ 67,834 -30.5%

AB 3Finance, Insurance, Real

Estate and Rental and Leasing

7.89% $ 65,755 $ 46,115 -29.9%

AB 4 Conventional Oil 6.13% $ 51,080 $ 36,250 -29.0%

AB 5 Owner occupied dwellings 5.12% $ 42,675 $ 29,665 -30.5%

ON 1Finance, Insurance, Real

Estate and Rental and Leasing

23.22% $ 13,491 $ 16,083 19.2%

ON 2 Wholesale Trade 11.08% $ 3,310 $ 7,678 132.0%

ON 3 Household (Labour) 10.79% $ 5,407 $ 7,476 38.3%

ON 4 Other Manufacturing 10.16% $ 5,460 $ 7,037 28.9%

ON 5 Transportation &Warehousing 7.87% $ 2,893 $ 5,455 88.6%

Relevant • Independent • Objectivewww.ceri.ca17

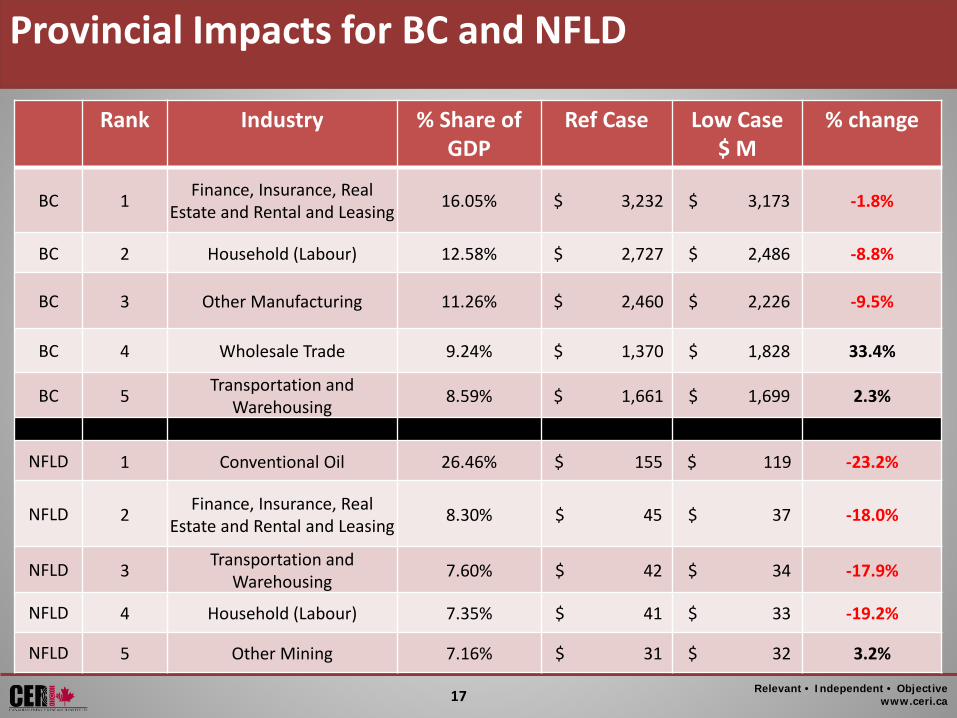

Provincial Impacts for BC and NFLD

Rank Industry % Share of GDP

Ref Case Low Case$ M

% change

BC 1 Finance, Insurance, Real Estate and Rental and Leasing 16.05% $ 3,232 $ 3,173 -1.8%

BC 2 Household (Labour) 12.58% $ 2,727 $ 2,486 -8.8%

BC 3 Other Manufacturing 11.26% $ 2,460 $ 2,226 -9.5%

BC 4 Wholesale Trade 9.24% $ 1,370 $ 1,828 33.4%

BC 5 Transportation and Warehousing 8.59% $ 1,661 $ 1,699 2.3%

NFLD 1 Conventional Oil 26.46% $ 155 $ 119 -23.2%

NFLD 2 Finance, Insurance, Real Estate and Rental and Leasing 8.30% $ 45 $ 37 -18.0%

NFLD 3 Transportation and Warehousing 7.60% $ 42 $ 34 -17.9%

NFLD 4 Household (Labour) 7.35% $ 41 $ 33 -19.2%

NFLD 5 Other Mining 7.16% $ 31 $ 32 3.2%

Relevant • Independent • Objectivewww.ceri.ca18

Conclusions

• Low oil prices are influenced by low economic growth in Asia, Europe and North America. They are also influenced by increased oil production efficiency and high amounts of supply. The low oil price environment is expected to continue for several years.

• As a net oil exporter, Canada is and will be affected by the lower prices, operating through several channels.

• Stronger US growth and a weaker Canadian dollar have boosted non-energy exports. Investment spending and job creation have also begun to pick up in non-energy sectors, although significant slack remains in the labour market.

• Overall, Canadian economic growth could contract by an average of 23 percent if low oil prices persist over the next seven years.

In summary, for the duration of the forecasted time horizon (2015-2021), every dollar gain in the annualized price of WTI, would increase national Canadian GDP by $1.7 billion on average.

Relevant • Independent • Objectivewww.ceri.ca19

Thank you!

www.ceri.ca