Embed Size (px)

Citation preview

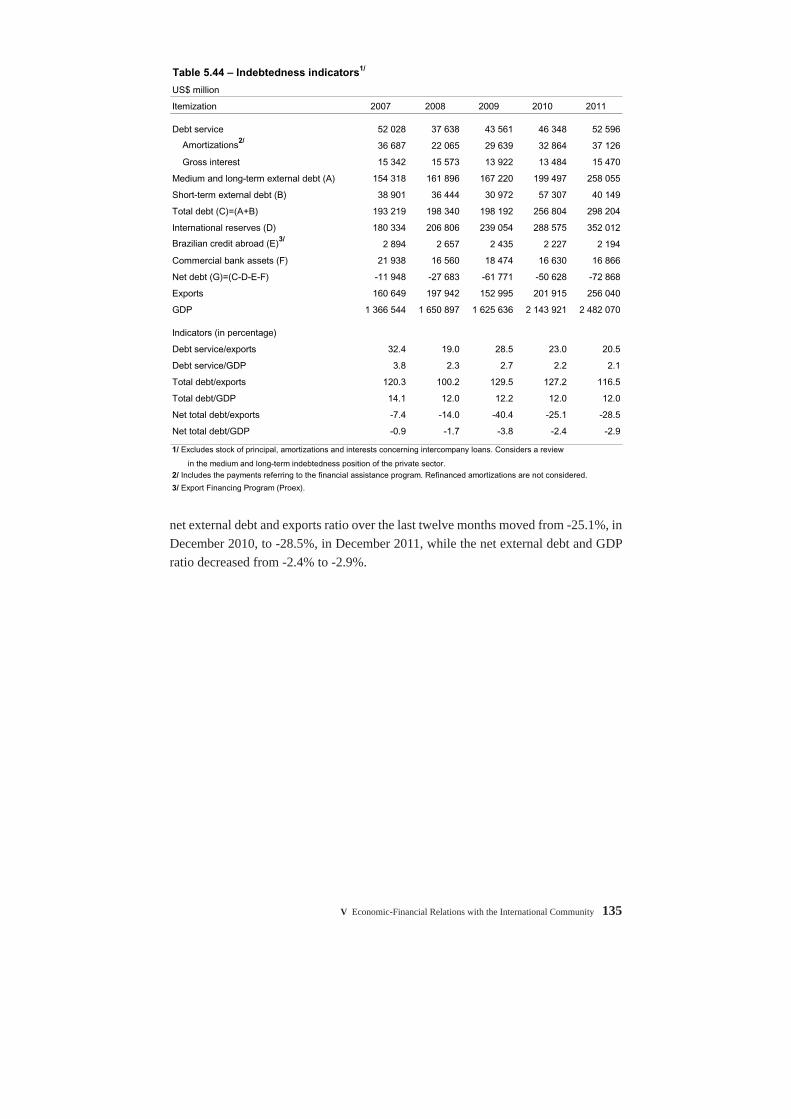

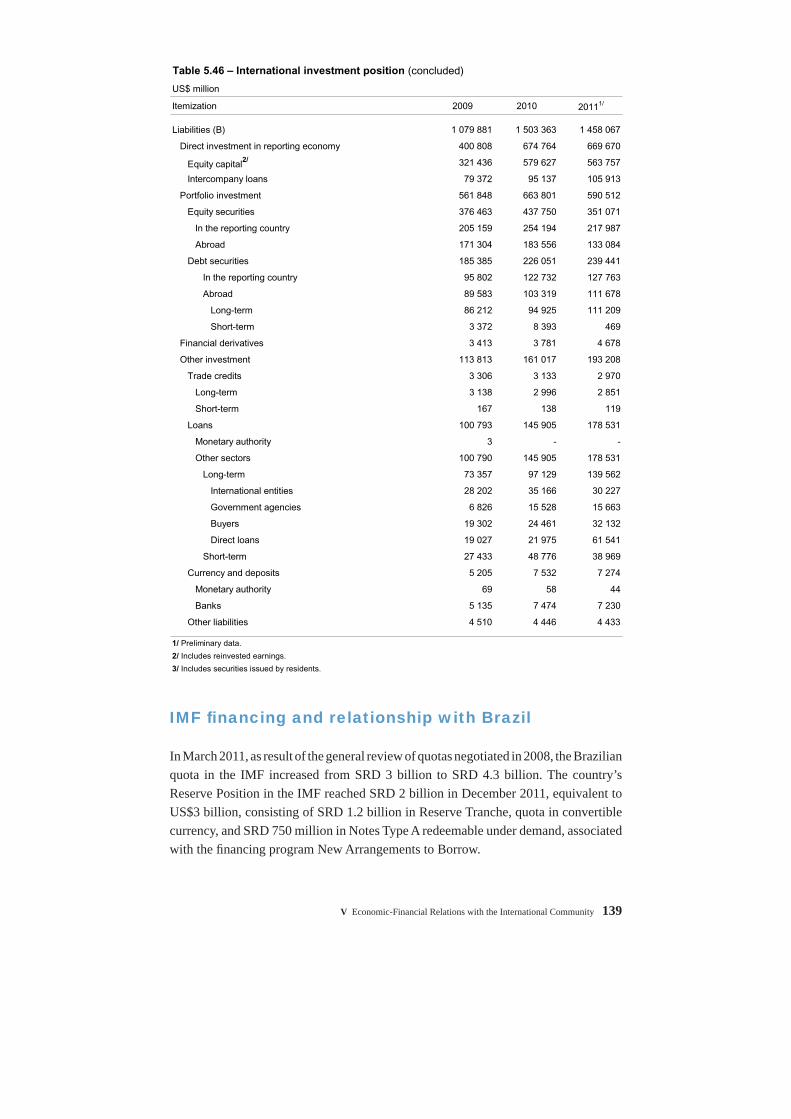

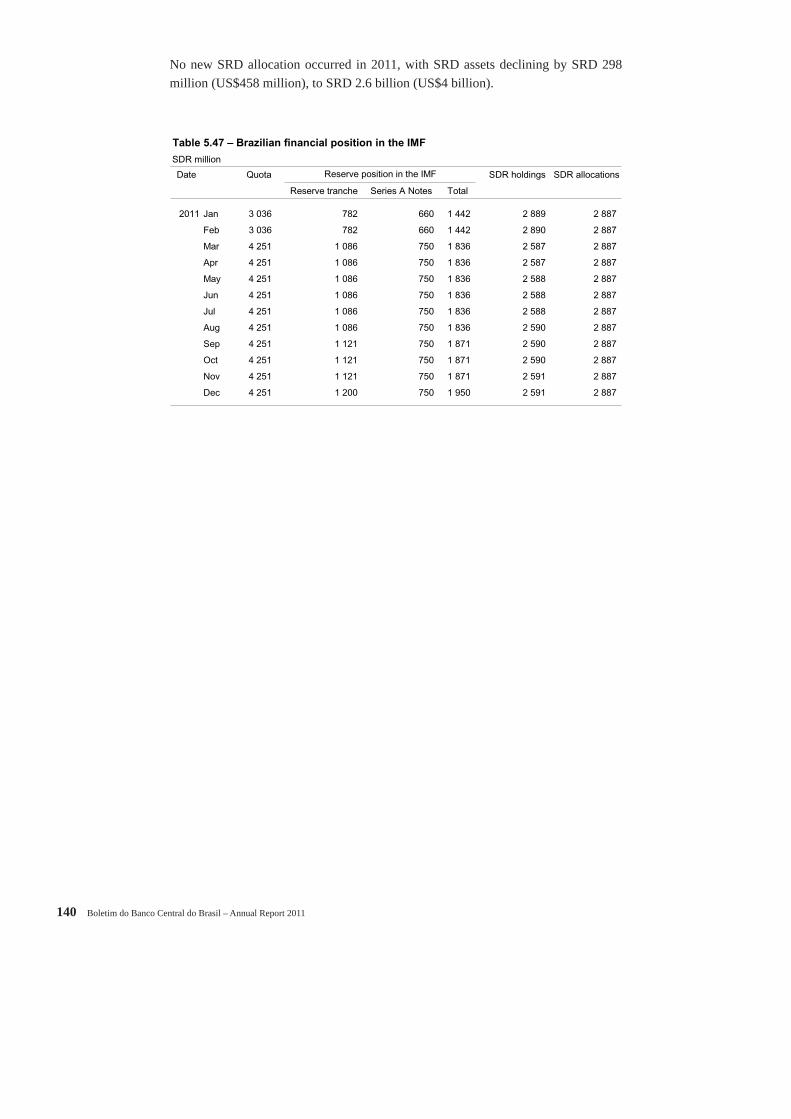

V Economic-Financial Relations with the International Community 77

Economic-Financial Relations with the International Community

Foreign Trade Policy

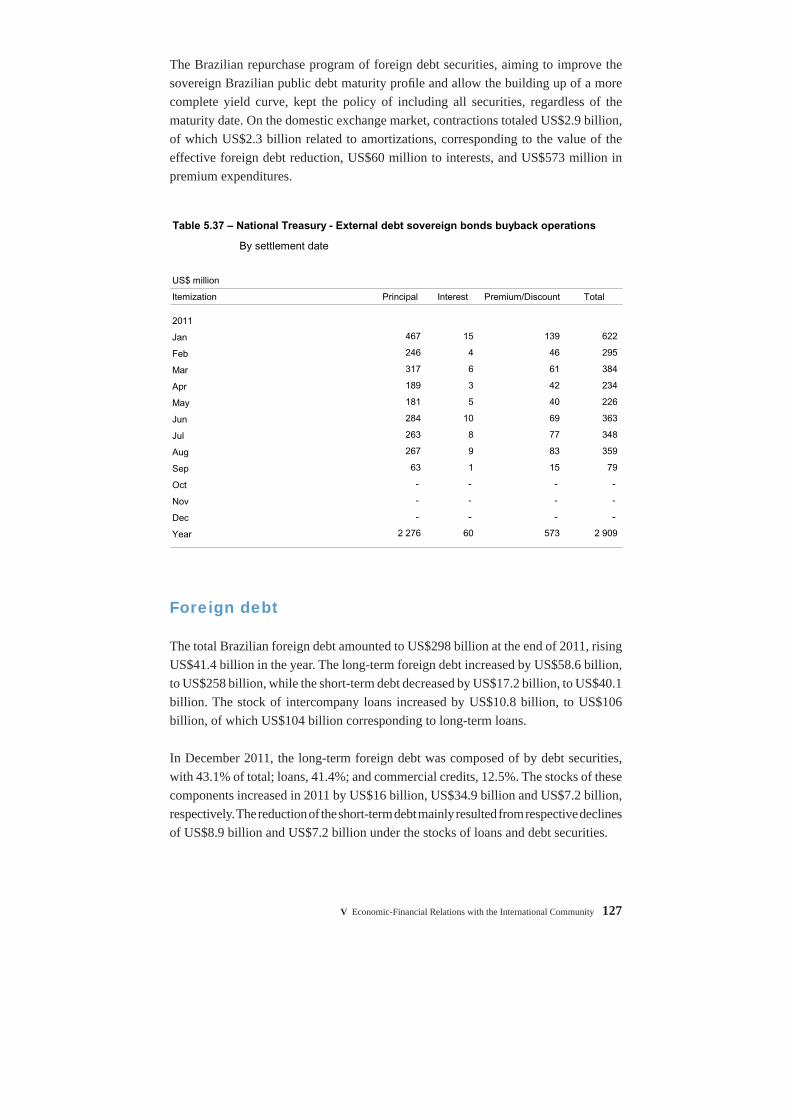

In 2011, the foreign trade policy was guided by two major guidelines: the reinforcement of instruments for commercial protection and stimulus to innovation and national production, aiming to increase the country’s industrial competitiveness in both domestic and foreign markets, an initiative materialized in the Greater Brazil Plan (PBM).

The PBM was established by Decree no. 7,540, dated August 2, 2011, in compliance with the governmental policy of boosting and strengthening the national industry, implemented in May, 2008, through the so-called Productive Development Policy (PDP). The PBM goals are to increase the competitiveness of national goods and services, focusing on the areas of international trade, protection of domestic industry and market, and investment and innovation. Measures concerning the international trade were established with the following purposes:i) Tax relief on exports;ii) Commercial protection;iii) Financing and guaranteeing exports;iv) Commercial promotion.

In the scope of these measures, Provisional Measure no. 540, dated August 2, 2011, converted into Law no. 12,546, dated December 14, established the Reintegra in order to refund values related to residual tax costs. The producer (legal person) who exports manufactured goods in the country will be allowed to calculate the value eligible for the partial or total compensation of residual taxes in the productive chain. This value will be calculated through a percentage established by the Executive Branch on the income associated with exports, varying from zero to 3%, and being differentiated by economic sector and activity category.

This Reintegra regime was regulated by Decree no. 7,633, dated December 1. As a rule, the products for which the costs of imported inputs are not higher than 40% of the export price may be benefi ted, but for high tech goods (pharmaceuticals; machinery, apparatuses and electrical and electronic appliances; airplanes; instruments, apparatuses; clock making) the limit reaches 65%. Products imported with the aim of

V

78 Boletim do Banco Central do Brasil – Annual Report 2011

being re-exported by Brazilian companies are not subject to this system. In addition, inputs imported from the member states of the Southern Common Market (Mercosur) that complies with the origin requirements of the economic bloc will be considered as national inputs for the application of the Reintegra. This regulation also deals with the establishment of a technical group, consisting of the Ministry of Finance and the Ministry of Development, Industry and Foreign Trade (MDIC), whose mission will be to study occasional proposals for changing the refund percentage, the maximum percentage of imported inputs and the list of eligible goods. This system will be effective up to December 31, 2012.

Another PBM initiative, established by Provisional Measure no. 540, dated August 2, converted into Law no. 12,546, dated December 14, was the reduction, from 20% to zero, up to December 2012, of the employer’s contribution on the payroll in the textile, footwear, furniture and software segments, and the implementation of a contribution on revenues of those companies. The rate of 2.5% was defi ned for the software segment, and 1.5% for the other segments. The loss of RGPS’s revenues consequent upon these changes shall be offset with funds provided by the National Treasury. The same regulation determined the gradual reduction, of twelve months, in July of 2011, for immediate appropriation, in July 2012, of the deadline for the refund of the PIS/Cofi ns credits related to capital goods.

Still in the PBM scope, the following commercial protection measures were also announced: reduction, from 15 to 10 months, of the maximum deadline for antidumping investigations, safeguards and compensatory measures, and from 240 to 120 days for the application of provisional rights. Furthermore, it is noteworthy the additional efforts for fi ghting against circumvention (triangulation from which the product is sold by a country, having been produced in another country), false declaration of origin, sub-invoiced products, illegal imports and violation of industrial property.

Commercial protection was defi ned as one of the major foreign trade policy goals throughout the year, by means of several initiatives in this area. The Inter-ministerial Ordinance of the Secretariat of the Federal Revenue of Brazil (RFB) and MDIC no. 149, dated June 16, of the Intelligence Group on Foreign Trade (GI-CEX) allowed the easy identifi cation of administrative instruments of each entity, thus guaranteeing greater effi ciency in the fi ght against disloyal and illegal foreign trade practices. An innovative measure to improve the system of commercial protection with the aim of monitoring the infl ow of goods and avoid anticipated purchases by importers is the inclusion of the product in non-automatic licensing as of the moment in which an antidumping investigation is opened. Other initiative for the cooperation between the two entities was implemented by the Ordinance RFB no. 3,011, dated June 30, authorizing the exchange of data, from the Federal Revenue to the Foreign Trade Secretariat (Secex), in order to analyze requirements to open investigations for extending antidumping measures.

V Economic-Financial Relations with the International Community 79

Moreover, the full-margin was adopted for the calculation of antidumping measures, instead of the Management Executive Committee (Gecex) of the Foreign Trade Council (Camex) guideline suggesting to adopt the rule of the lowest right in effect since 2007. So far, Brazil had opted to impose a surcharge enough to compensate the damage, and the adoption of the full-margin is expected to increase the surcharges applied.

The retroactive charge of antidumping and compensatory rights was established by Camex Resolution no. 64, dated September 14. This regulation authorized the levying of taxes on imported products up to ninety days before the date of the application of provisional antidumping measures. This charge aims to avoid the accumulation of stocks in the period immediately after the beginning of investigations of disloyal commercial practices. The retroactive antidumping right is accepted by the World Trade Organization (WTO) and the Brazilian legislation.

At the end of 2011, a total of 84 antidumping rights, one price commitment and one safeguard measure, related to 52 products associated with 25 countries or blocs took place, with emphasis on those related to China, U.S. and India. It s worth mentioning that the Secex Ordinance no. 39, dated November 11, improved the criteria for the opening of investigation about the fulfi llment of rules established by the Brazilian legislation, and the fi rst investigations about circumvention were opened in the year.

In May, the government decided to apply the non-automatic licensing for the imports of new automotive vehicles. In the scope of the PBM, Provisional Measure no. 540, dated August 2, converted into Law no. 12,546, dated December 14, established a new system for the automotive sector with tax incentives for stimulating investments, value aggregation, employment generation and technological innovation. This regulation was dealt with by Decree no. 7,567, dated September 15. IPI was exempted for vehicles with minimum regional content of 65% in at least 6 of the 11 productive stages in the country, and investment of 0.5% of total gross income on sales of goods and services in research and technological innovation, effective up to December 31, 2012. IPI on vehicles imported from Mercosur member states and Mexico remained unchanged, as long as manufacturers held a plant installed in Brazil. Later on, the Brazilian Government extended, in compliance with the Brazil-Uruguay Automotive Agreement, the benefi ts of the IPI reduction on vehicles from the neighboring country. In view of the Decision of the Supreme Federal Court, stating that the rule would be effective after 90 days, it was established the Decree no. 7,604, dated November 10, which altered the beginning of the IPI increase, effective as of December 16.

In the scope of the Mercosur, the Brazilian government proposed the improvement of the Import Tax tariff structure, including the establishment of a mechanism that would allow tax increases. In the Council’s Meeting of the Mercosur Common Market in Montevideo, held on December 20, through the Decision no. 39/2011, it was implemented a mechanism allowing member states of this economic bloc to increase, temporarily,

80 Boletim do Banco Central do Brasil – Annual Report 2011

import tax rates. This mechanism is an instrument parallel to the List of Exception to the Common External Tariff (TEC), with the difference that TEC rates can be reduced or increased. Each country will be allowed to include one hundred new tariff codes of the Common Mercosur Nomenclature (NCM) apart from those included in the List of Exception, in order to raise rates included in the TEC of the Mercosur for products imported from non member countries.

In the scope of the commercial promotion, the Ata-Carnet came into force through the publication of Decree no. 7,545, dated August 2, 2011. This is a convention that makes it easy the circulation of goods under the regime of temporary admission with no taxes being charged. Additionally, it was reinforced the strategy of commercial promotion by overriding products/services in selected markets.

Regarding the fi nancing and guarantees for exports, it was determined the creation of the Export Financing Fund (FFEX), a fund of private nature established by the Banco do Brasil for companies with revenues up to R$60 million. The Federal Government was authorized by Provisional Measure no. 541, dated August 2, converted into the Law no. 12,545, dated December 14, to initially participate with R$1 billion, but other companies may participate in the fund, which will be also supported by earnings associated with the Proex-Financing.

Furthermore, it was implemented by the BNDES and Banco do Brasil the computerization of the process to issue the Credit Insurance to the Export Guarantee Fund (FGE) Policy. In the case of Proex Equalization operations, the defi nition of reference spreads shall be automatically approved for the exports of goods and services. The FGE will have a revolving ceiling of US$50 million concerning the exports of manufactured products.

With regard to measures aimed to fi nance exports, the Secex Ordinance no. 42, dated December 7, extended the utilization of the Export Financing Program (Proex) for operations carried out through the Simplifi ed Export Declaration (DSE), limited to the value of US$50 thousand. To obtain this fi nancing, it is necessary to fi ll in the Credit Registration (RC) in the Integrated Foreign Trade System (Siscomex), regardless of the Export Registration (RE). When fi nancing is approved by the Banco do Brasil, exporters are only required to present a copy of the DSE and documents related to the shipment of goods in order to release the loan.

Proex operations totaled US$4.1 billion in 2011, of which US$635 million related to fi nancing and US$3.5 billion to interest rates equalization. Funds allocated under the fi nancing modality increased 24.3% as compared to the previous year, while the number of operations decreased from 1,478 to 1,354, and the total of exporters participating in the program decreased from 371 to 312.

V Economic-Financial Relations with the International Community 81

The main economic sectors that took advantage of the Proex-Financing in 2011 were the agribusiness, 58% of total; the segments of textile, leather and footwear, 24%; and machinery and equipment, 9%. The main countries of destination of exports were Cuba, 45% of total; China, 10%; and France, 7%.

Funds allocated to the equalization modality registered stability in the year, while the issue of securities related to operations of interest rates equalization totaled US$185 million, rising 56.6% as compared to 2010. In the year, 2,531 operations were carried out by 34 exporters, as against 2,657 operations carried out by 31 companies in the previous year.

The sectoral analysis reveals that exports involving this modality were focused on machinery and equipment, accounting for 70%, followed by transportation equipment industry, 22%. The main regions of destination of exports carried out by the Proex-Equalization were the North American Free Trade Agreement (Nafta) countries, with 31%; countries of the Latin American Integration Association (Aladi), 20%; and Mercosur member countries, 15%. The main countries of destination were the U.S., with 22% of total; Argentina; 13%; Chile, 8%; Peru, 8%; and Mexico, 7%.

The prorogation of the deadline for the contract of fi nancing in the framework of the BNDES Investment Support Program (ISP), with a budget of R$75 billion, represented an important measure to leverage the productive investment and technological innovation. In March, the PSI was prorogated until December 31, 2011, and, in September, until the end of 2012, being adjusted to the PBM strategies. The National Monetary Council, through Resolution no. 4,009, dated September 14, approved some PSI alterations, with emphasis on the reallocation of fi nancing limits from the BNDES to the Finep, increasing the amount of funds from R$1 billion to R$3 billion; the inclusion as benefi ciaries of national or foreign corporations headquartered in Brazil, in addition to entrepreneurs, associations and foundations with the purpose of developing technological innovation projects in a systematic way.

On June 1, it was announced a partnership between Banco do Brasil and BNDES for the fi nancing of Brazilian exports of capital goods in the Latin America, in the framework of the BNDES Exim automatic. The new credit line, with payment deadlines of up to fi ve years, should contribute to enhance the competitiveness of Brazilian companies abroad, especially in the segment of capital goods. All Banco do Brasil’s branches, in Brazil and overseas, are eligible for negotiating with companies interested in this credit line, limited to US$200 million.

In 2011, disbursements related to BNDES foreign trade operations totaled US$6.7 billion, of which US$5 billion targeted to exports of goods and US$1.7 billion to exports of services. In the scope of the 580 operations involving disbursements for the industry, US$1.4 billion corresponded to exports in the segment of vehicles, tow trucks

82 Boletim do Banco Central do Brasil – Annual Report 2011

and bodyworks; US$1.2 billion in other transportation equipment; US$724 million to machinery and equipment; and US$487 million in electrical machines and apparatuses. These four segments accounted for 77.1% of total disbursements channeled to the manufacturing industry.

Regarding the special import regimes, the Secex Ordinance no. 8, dated February 15, regulated the new regime of Integrated Drawback Exemption. This system permits the replacement of stock of imported inputs acquired in the domestic market with the aim of being utilized in the industrialization of the fi nal exported product. The company may choose between the exemption for the amount imported or acquired in the domestic market, an innovative choice with the goal of improving the competitiveness of Brazilian products on the international market.

Other relevant item was the signing, on October 24, of the Constitutional Amendment Proposal (PEC) in order to prorogate, for more than 50 years, the validity of the Free Economic Zone of Manaus and the extension of benefi ts for that metropolitan region. In addition, through the Inter-Ministerial Ordinance of the Ministry of Science and Technology no. 432, dated June 28, it was defi ned the fi rst company allowed to produce tablets in the country, subject to tax incentives in the framework of the Informatics Law.

Exchange policy

According to Circular no. 3,520, dated January 6, fi nancial institutions should pay to the Central Bank, as compulsory deposit, 60% of the short exchange position exceeding the lowest of the following values: US$3 billion, or the Base Capital (PR). The deadline for fi nancial institutions to adapt to this compulsory deposit paid in cash and without return, totaled 90 days. This prudential measure aimed to reduce banking exchange exposure in foreign currency.

On January 14, the Central Bank resumed reverse exchange swap operations, in which it assumes asset position in exchange variation and liability in domestic interest rates. It is worth mentioning that, in June of 2009, the Central Bank had closed all its open positions in exchange swap contracts. At the end of December 2011, these operations resulted in net exposure of US$3 billion.

Circular no. 3,484, dated January 25, authorized foreign currency auctions with forward settlement, that is, with defi ned deadlines for future payments. Auctions were carried out in February, April and September, totaling US$2.2 billion in the year. Through this measure, the Central Bank obtained the following instruments to intervene on the

V Economic-Financial Relations with the International Community 83

exchange domestic market: direct interventions in the spot market; exchange swap and reverse exchange swap auctions; and forward auctions.

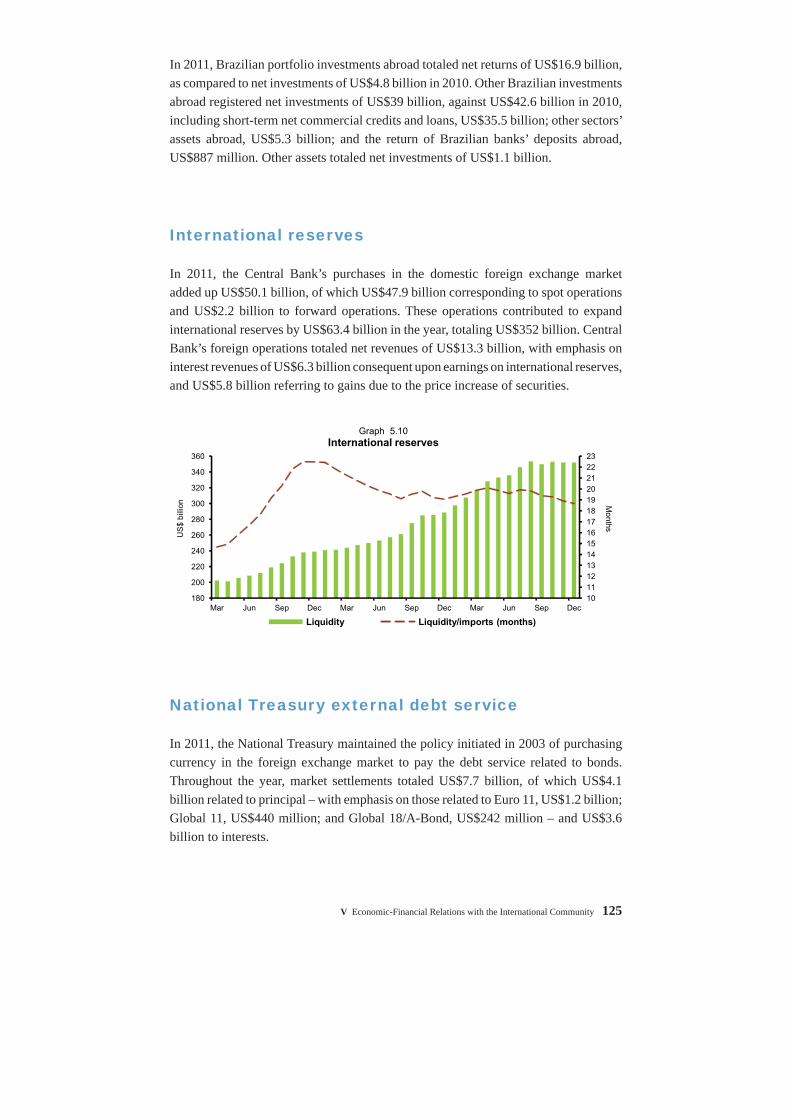

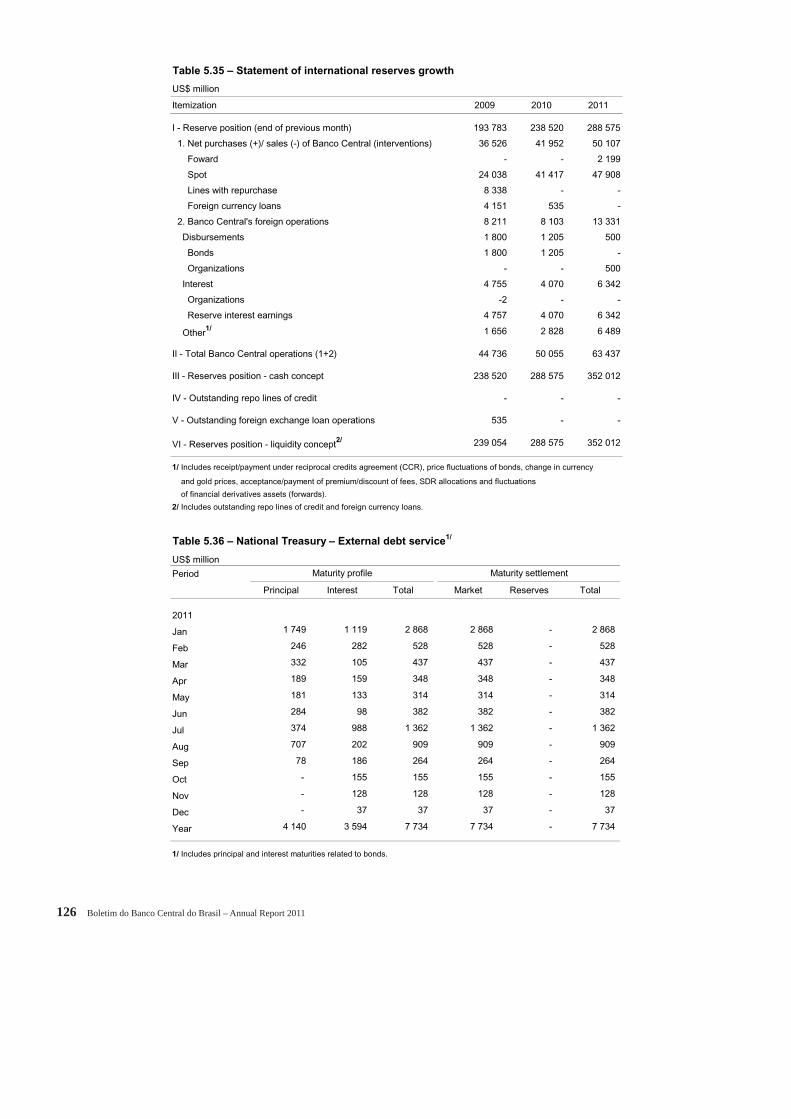

The maintenance of foreign capital infl ows to the Brazilian market allowed the monetary authority to keep the policy of purchasing foreign currency in the spot market, totaling acquisitions of US$47.9 billion from January to September, which, added up to US$2.2 billion related to forward operations, totaled purchases of US$50.1 billion in the year.

According to Decree no. 7,454, the IOF rate on exchange operations for the fulfi llment of obligations of the credit card administrators, commercial or multiple banks in the quality of credit card issuers, resulting from the acquisition of foreign goods and services by their users, increased to 6.38% as of March 25, This measure came into force on the publication’s date, with effects on the exchange operations after the thirtieth day subsequent to the publication’s date.

According to the Decree no. 7,456, dated March 28, the IOF rate on liquidations of exchange operations contracted since March 29, 2011, concerning infl ows of foreign funds under the modality of loans, contracted directly or through the issue of securities on the international market, with minimum average term of 360 days, was raised to 6%. The deadline was increased to 720 days for the settlement of exchange operations contracted since April 7, 2011, according to Decree no. 7,457, dated April 6. The aim of this regulation is to reduce short-term foreign debts, which are subject to higher risks in a crisis scenario.

Aiming to equalize the treatment provided to operations involving conversion operations and transfer between foreign capital registered at the Central Bank of Brazil, the CMN, through Resolution no. 3,967, dated April 4, turned it mandatory the implementation of simultaneous operation in renovations, renegotiations and assumption of obligations related to foreign loans operations, contracted directly or through the issue of securities on the international market. The Central Bank implemented normative changes on this subject through Circular no. 3,531, dated April 13.

Other macro-prudential measure aimed to reduce banking exposure in foreign currency was announced on July 8. Through Circular no. 3,548, the Central Bank redefi ned and consolidated the rules for the compulsory payment on exchange short position. According to this rule, fi nancial institutions should pay to the Central Bank, as compulsory deposit, 60% of the value of the exchange short position exceeding the lowest of the following values: US$1 billion, or the Base Capital (PR). This compulsory deposit should be paid in cash and yields no earnings.

Provisional Measure no. 539, dated July 26, converted into Law no. 12,543, dated December 8, authorized the National Monetary Council to establish specifi c conditions

84 Boletim do Banco Central do Brasil – Annual Report 2011

to negotiate derivatives contracts. According to this Law, operations related to securities, involving derivatives contracts are subjected to the maximum IOF rate, 25%. Additionally, Decree no. 7,536, dated July 26, fi xed the IOF rate in derivatives contracts at 1% on the adjusted value, in the purchase, sale or maturity of contracts of fi nancial derivatives, whose liquidation value had been affected by the variation of the interest rate and resulting in increase of the short net exposure, compared to that calculated at the end of the previous business day. Through Normative Instruction no. 1,207, dated November 3, the Federal Revenue regulated the collection of IOF, but its payment for the triggering events occurred from September 15 to December 31, 2011 was postponed, by means of Ordinance no. 560, dated December 23, to January 31, 2012. In addition, the same Decree determined for the loan operation, contracted by the minimum average deadline higher than 720 days, that if the minimum medium term required is not fulfi lled, the taxpayer will have to pay the tax calculated at a rate of 6%, plus interest on late payments and fi nes.

The IOF rate on foreign investment in shares was reduced from 2% to zero, according to Decree no. 7,632, dated December 1. The reduction reached the initial public offer (IPO) and the secondary market, and included the cancellation and primary issue of depositary receipts of Brazilian companies negotiated abroad. It was also reduced, from 6% to zero, the IOF rate on non-resident investments in securities of medium-term higher than four years, issued by non-fi nancial companies and associated with investment projects.

In the scope of the policy for strengthening the Brazilian companies’ performance on the international market, the CMN, through Resolution no. 4,033, dated November 30, allowed the authorized banks to operate in the exchange market, with minimum base capital of R$5 billion, and to use funds raised in the international market to grant credit abroad. This credit may be only channeled to Brazilian companies, subsidiaries of Brazilian companies and foreign companies, whose shareholder with the majority of voting capital should be, directly or indirectly, an individual or corporation resident in Brazil. In addition, banks were authorized to acquire, in the primary market, securities issued by the referred companies.

In the context of measures aimed to streamline exchange operations, the CMN, through Resolution no. 3,997, dated July 28, regulated the receipt by national exporters of funds associated with sales of goods and services abroad, in an environment of electronic commerce. The measure eliminated the harmful asymmetry for the Brazilian companies, thus allowing national exporters to compete in the environment of electronic commerce under similar conditions with foreign competitors.

V Economic-Financial Relations with the International Community 85

Exchange movement

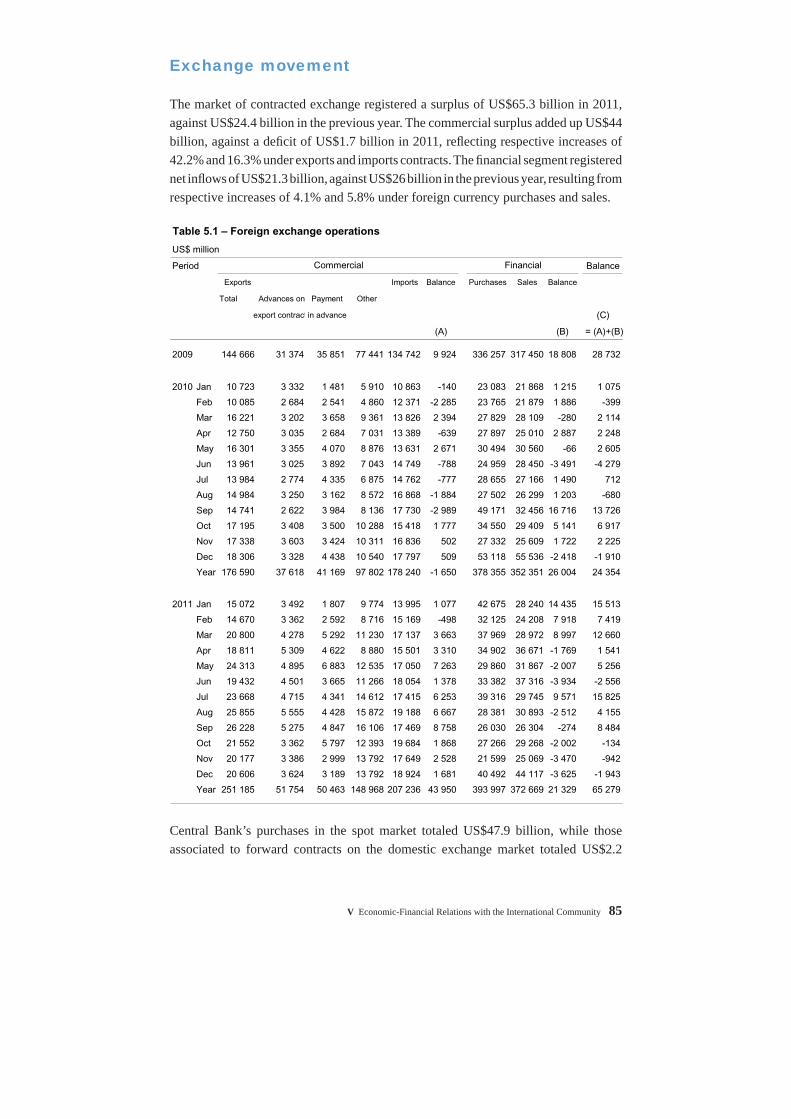

The market of contracted exchange registered a surplus of US$65.3 billion in 2011, against US$24.4 billion in the previous year. The commercial surplus added up US$44 billion, against a defi cit of US$1.7 billion in 2011, refl ecting respective increases of 42.2% and 16.3% under exports and imports contracts. The fi nancial segment registered net infl ows of US$21.3 billion, against US$26 billion in the previous year, resulting from respective increases of 4.1% and 5.8% under foreign currency purchases and sales.

Central Bank’s purchases in the spot market totaled US$47.9 billion, while those associated to forward contracts on the domestic exchange market totaled US$2.2

Table 5.1 – Foreign exchange operations

US$ million

Period Balance

Exports Imports Balance Purchases Sales Balance

Total Advances on Payment Other

export contract in advance (C)

(A) (B) = (A)+(B)

2009 144 666 31 374 35 851 77 441 134 742 9 924 336 257 317 450 18 808 28 732

2010 Jan 10 723 3 332 1 481 5 910 10 863 -140 23 083 21 868 1 215 1 075

Feb 10 085 2 684 2 541 4 860 12 371 -2 285 23 765 21 879 1 886 -399

Mar 16 221 3 202 3 658 9 361 13 826 2 394 27 829 28 109 -280 2 114

Apr 12 750 3 035 2 684 7 031 13 389 -639 27 897 25 010 2 887 2 248

May 16 301 3 355 4 070 8 876 13 631 2 671 30 494 30 560 -66 2 605

Jun 13 961 3 025 3 892 7 043 14 749 -788 24 959 28 450 -3 491 -4 279

Jul 13 984 2 774 4 335 6 875 14 762 -777 28 655 27 166 1 490 712

Aug 14 984 3 250 3 162 8 572 16 868 -1 884 27 502 26 299 1 203 -680

Sep 14 741 2 622 3 984 8 136 17 730 -2 989 49 171 32 456 16 716 13 726

Oct 17 195 3 408 3 500 10 288 15 418 1 777 34 550 29 409 5 141 6 917

Nov 17 338 3 603 3 424 10 311 16 836 502 27 332 25 609 1 722 2 225

Dec 18 306 3 328 4 438 10 540 17 797 509 53 118 55 536 -2 418 -1 910

Year 176 590 37 618 41 169 97 802 178 240 -1 650 378 355 352 351 26 004 24 354

2011 Jan 15 072 3 492 1 807 9 774 13 995 1 077 42 675 28 240 14 435 15 513

Feb 14 670 3 362 2 592 8 716 15 169 -498 32 125 24 208 7 918 7 419

Mar 20 800 4 278 5 292 11 230 17 137 3 663 37 969 28 972 8 997 12 660

Apr 18 811 5 309 4 622 8 880 15 501 3 310 34 902 36 671 -1 769 1 541

May 24 313 4 895 6 883 12 535 17 050 7 263 29 860 31 867 -2 007 5 256

Jun 19 432 4 501 3 665 11 266 18 054 1 378 33 382 37 316 -3 934 -2 556

Jul 23 668 4 715 4 341 14 612 17 415 6 253 39 316 29 745 9 571 15 825

Aug 25 855 5 555 4 428 15 872 19 188 6 667 28 381 30 893 -2 512 4 155

Sep 26 228 5 275 4 847 16 106 17 469 8 758 26 030 26 304 -274 8 484

Oct 21 552 3 362 5 797 12 393 19 684 1 868 27 266 29 268 -2 002 -134

Nov 20 177 3 386 2 999 13 792 17 649 2 528 21 599 25 069 -3 470 -942

Dec 20 606 3 624 3 189 13 792 18 924 1 681 40 492 44 117 -3 625 -1 943

Year 251 185 51 754 50 463 148 968 207 236 43 950 393 997 372 669 21 329 65 279

Commercial Financial

86 Boletim do Banco Central do Brasil – Annual Report 2011

billion. Banks’ exchange position, refl ecting both operations with clients on the primary exchange market and Central Bank’s interventions, decreased from US$16.8 billion, at the end of 2010, to US$1.6 billion, at the end of December 2011.

The Brazilian real depreciated 12.6% against the U.S. dollar in 2011. Effective real exchange rate indices, defl ated by the Extended Price Index (IPA-DI) and the IPCA, registered respective decreases of 10.6% and 5.2% at the end of 2011 and 2010.

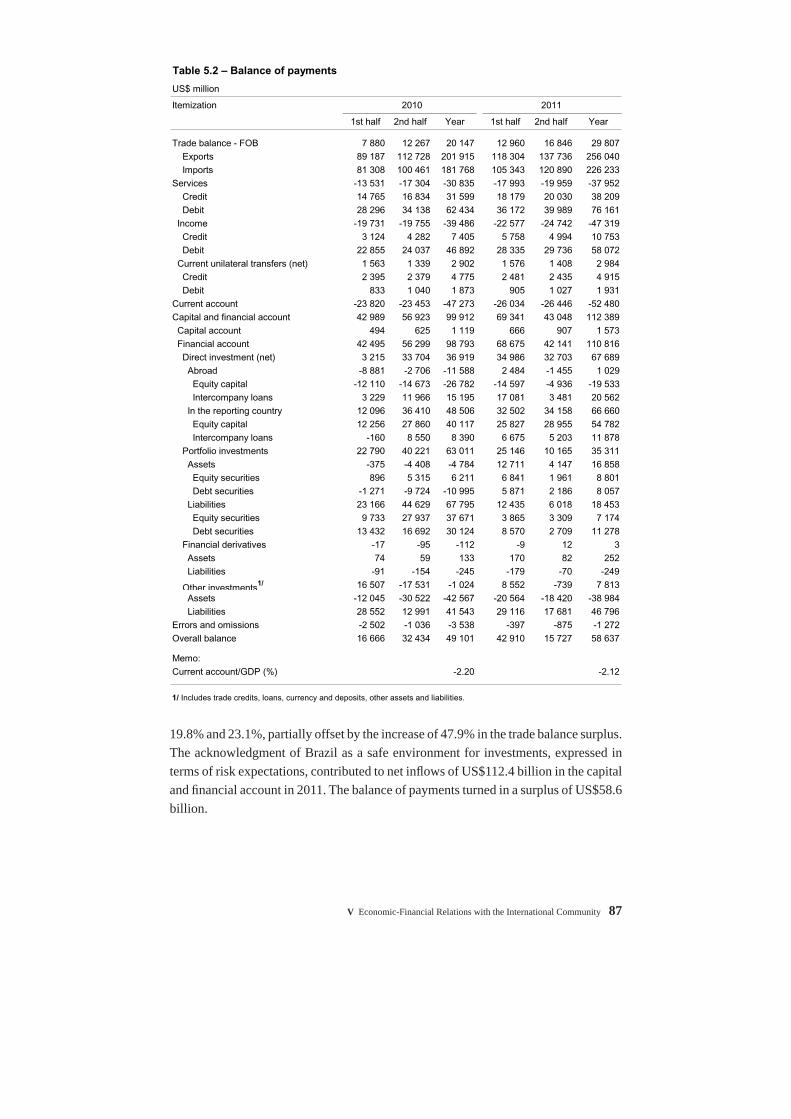

Balance of payments

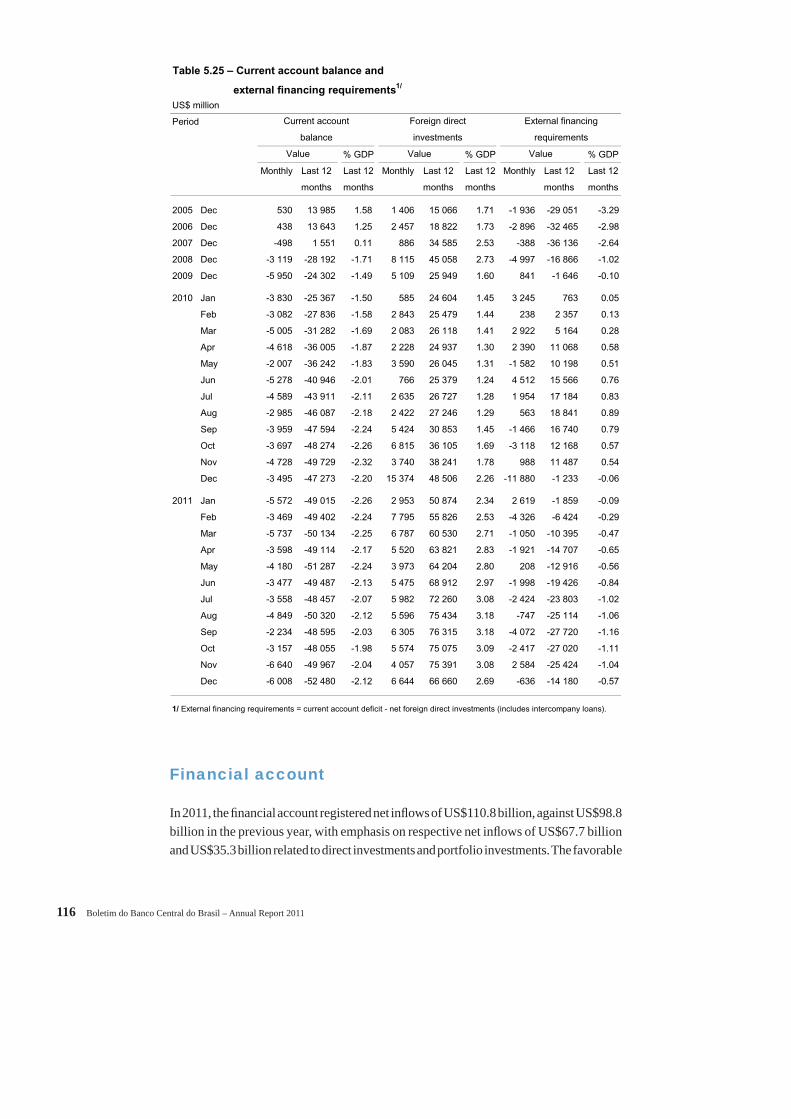

The Brazilian external position was positive in 2011 according to several aspects: the defi cit under current transactions, measured as a proportion of the GDP, decreased as compared to the previous year; the trade fl ow of goods and services expanded; net foreign liability, expressed by the International Investment Position, decreased in absolute terms; and the coverage of debt maturing in twelve months by the stock of international reserves expanded. Therefore, in the scope of the foreign sector, the perception related to the soundness of the Brazilian foreign accounts partially offset the impact of the volatility on international fi nancial markets.

The adoption of a consistent macroeconomic policy, based on three pillars (infl ation targeting, fi scal responsibility and fl oating exchange system) was maintained in 2011. Additionally, the modern National Financial System regulation has been essential to the fi nancial stability. Throughout the year, in spite of the uncertainties in the international scenario, the risk classifi cation agencies increased the country’s sovereign credit rates, in the following order: Fitch, in April, Moody’s, in June, and Standard and Poor’s, in November. The sovereign fi nancing cost in the international market, favored, among other factors, by the strengthened foreign position, hit the lowest level over the last 40 years, in contrast with the environment of sovereign debt crisis in the Eurozone. In the last quarter of the year, the disbursement of bonds by the Brazilian Treasury registered positive records in terms of absolute funding costs and spread as compared to U.S. reference debt securities.

The turmoil arising from the sovereign debt crisis in important European countries did not affect the volumes obtained by the Brazilian private sector, thus positioning Brazil, according to estimates published by the United Nations Conference on Trade and Development (Unctad) in the Global Investment Trends Monitor as the fi fth greatest recipient of net infl ows, behind the U.S., United Kingdom, China and Hong Kong.

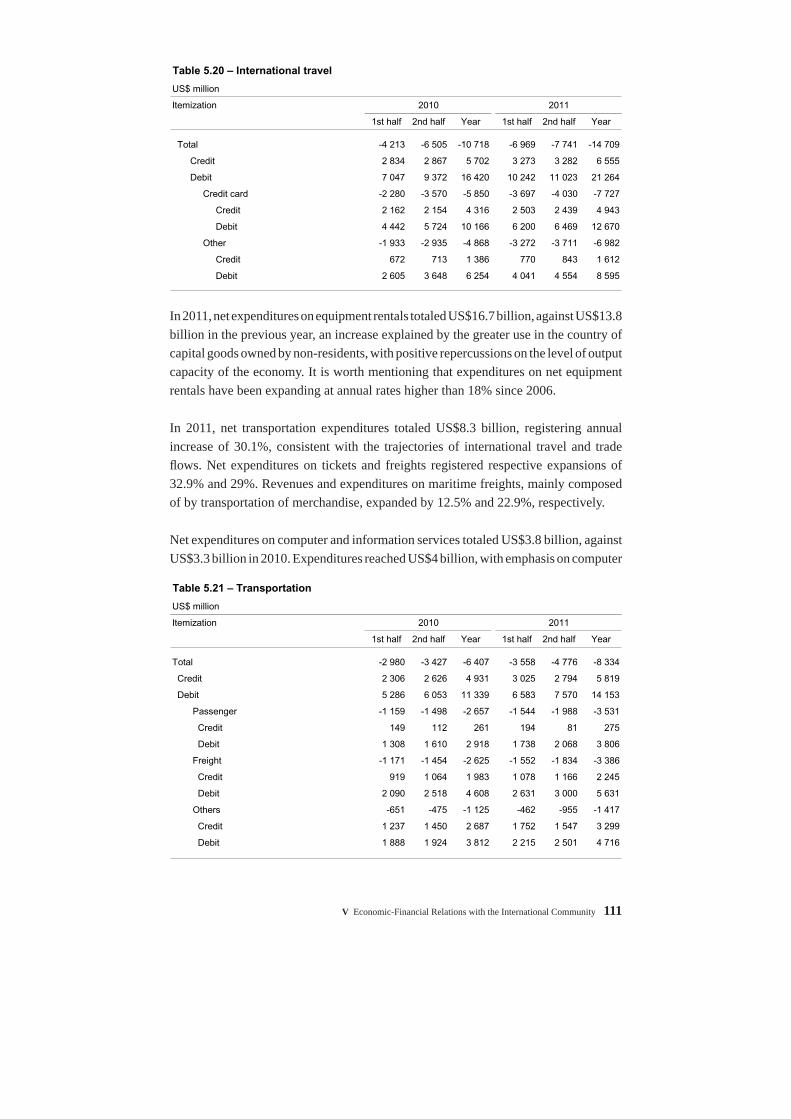

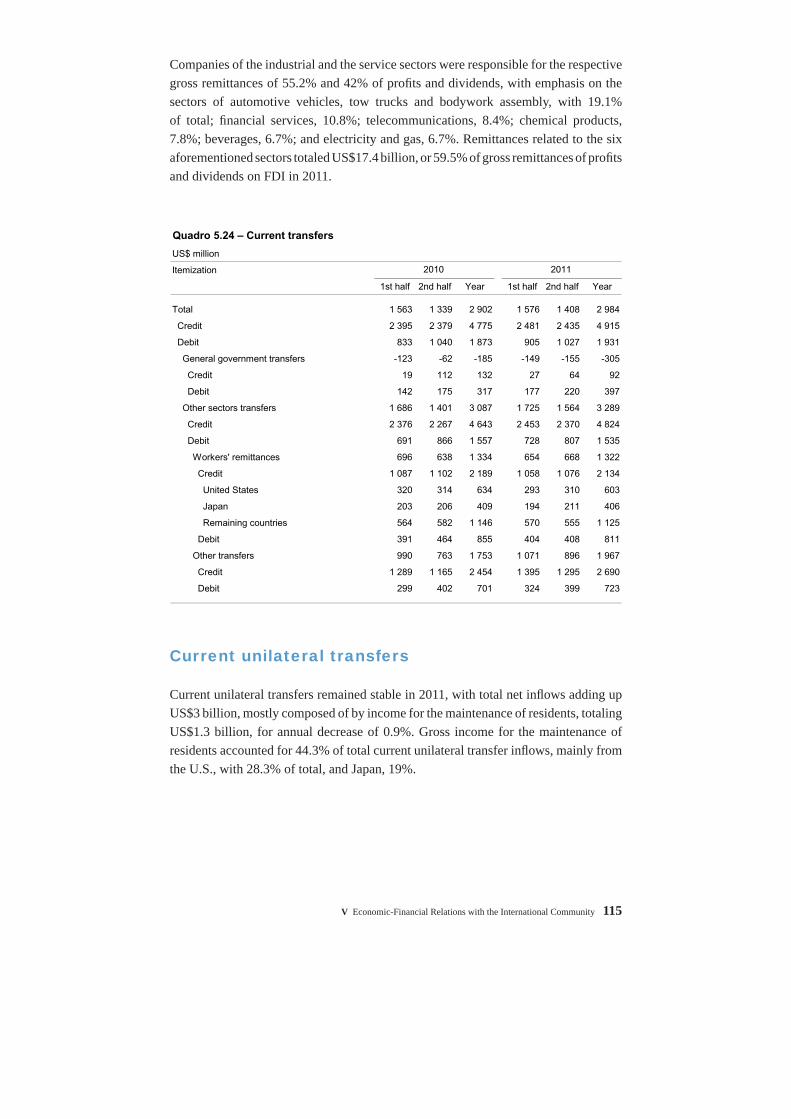

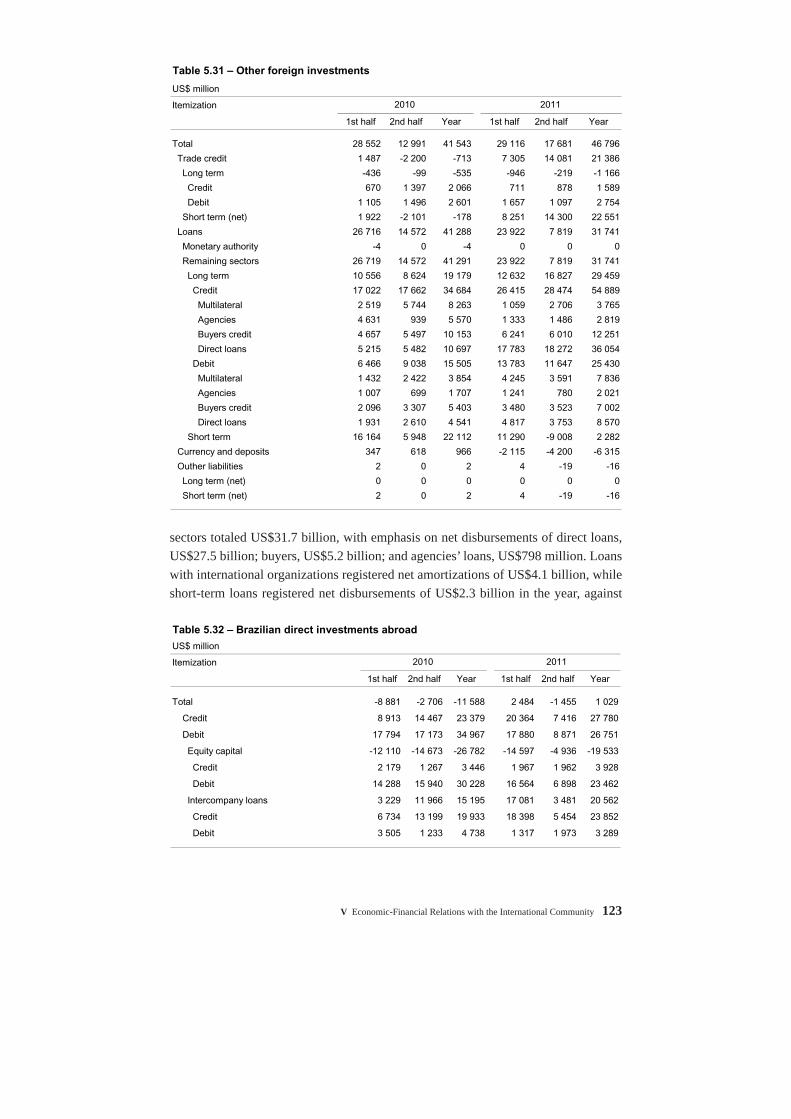

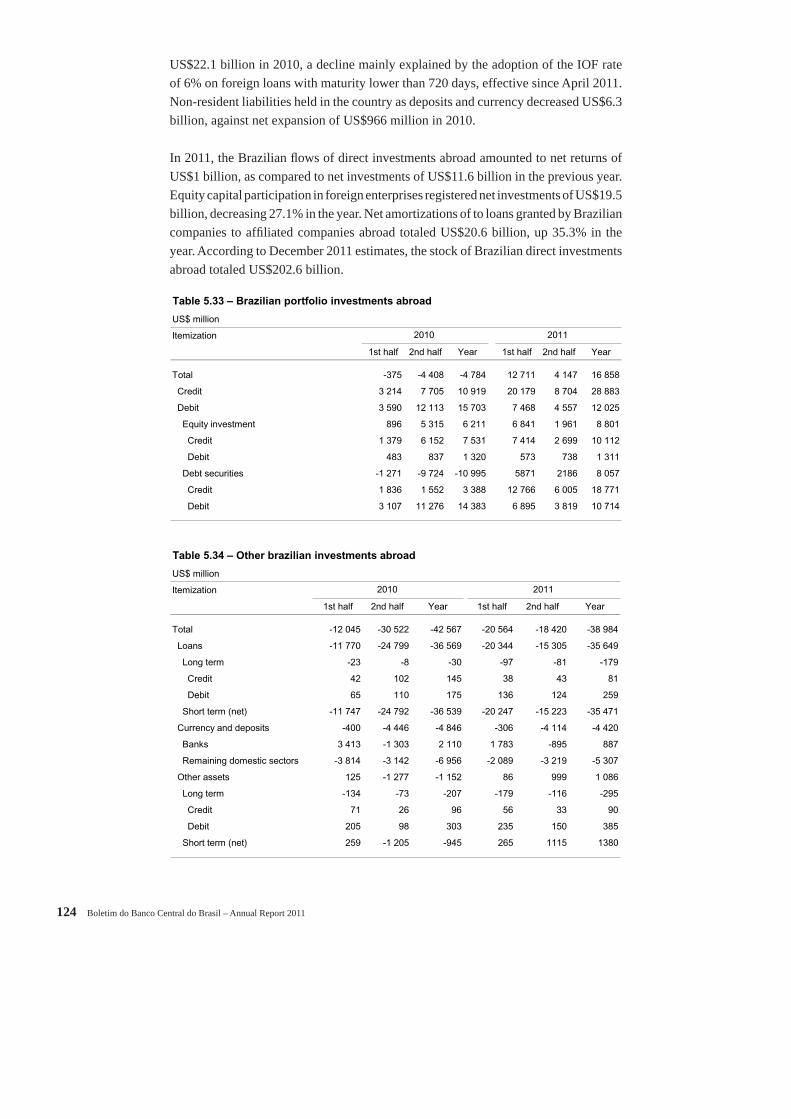

The defi cit in current transactions totaled US$52.5 billion in 2011, against US$47.3 billion in the previous year. Net expenditures on income expanded by US$7.8 billion, while expenditures on services rose US$7.1 billion, for respective annual increases of

V Economic-Financial Relations with the International Community 87

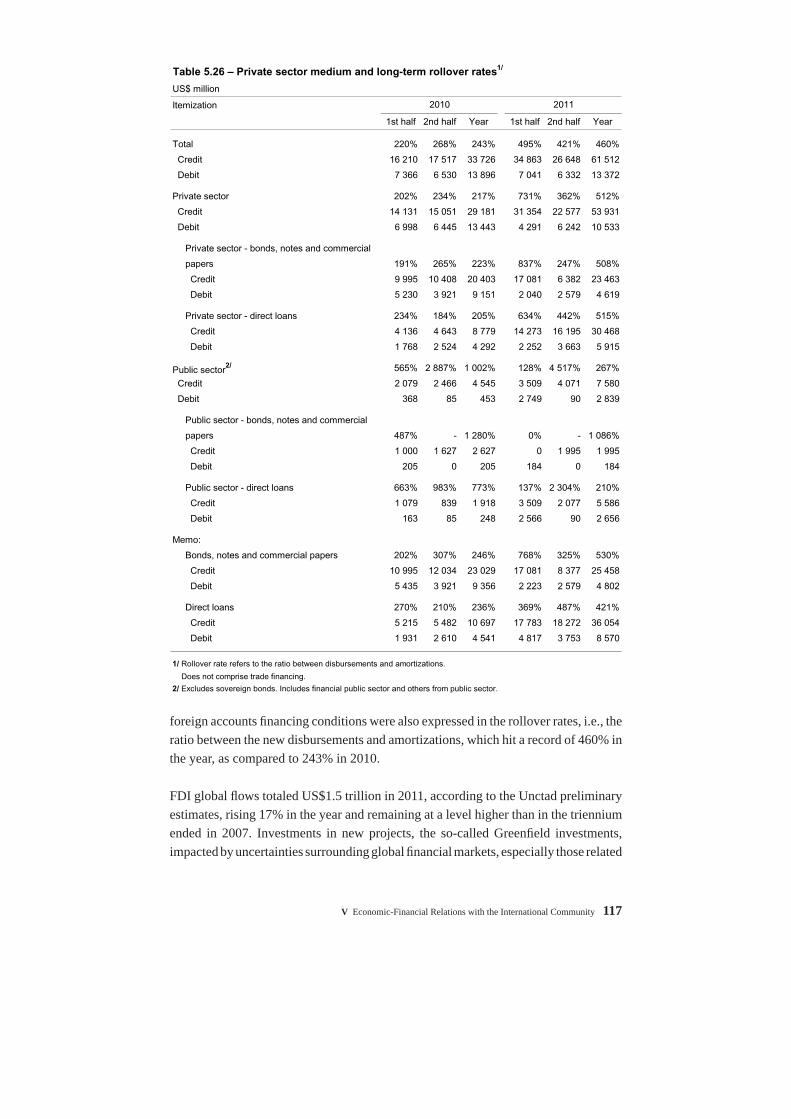

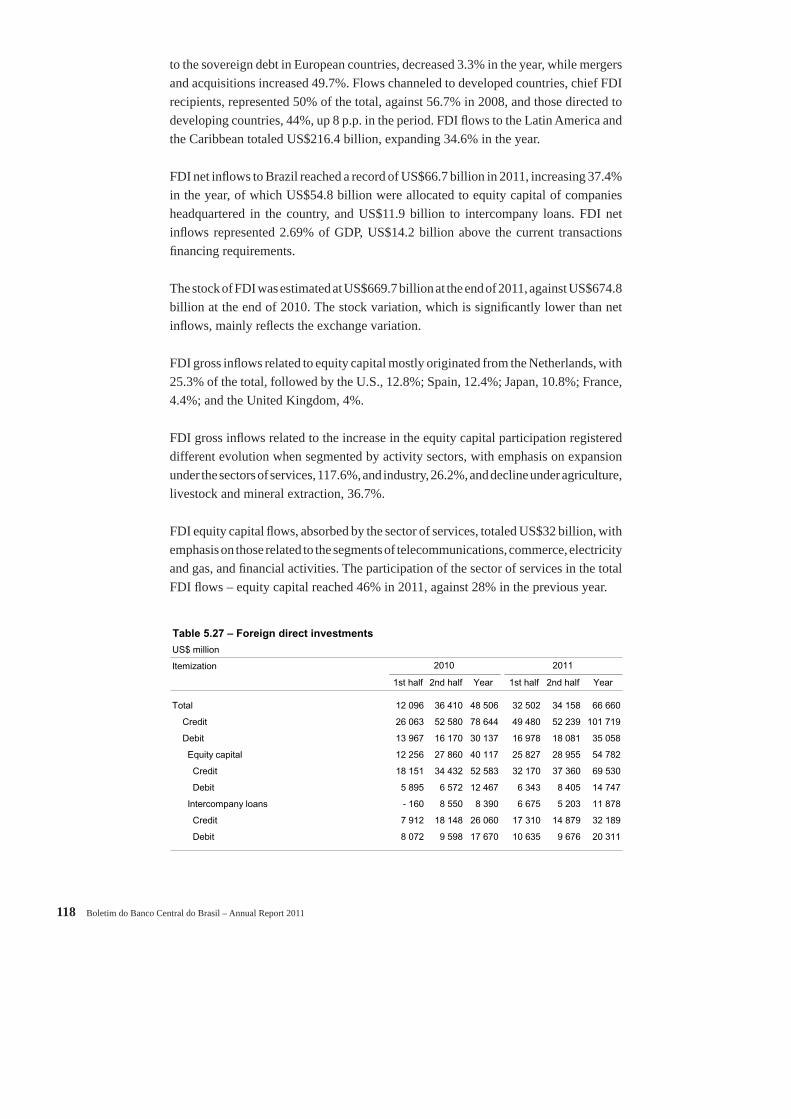

19.8% and 23.1%, partially offset by the increase of 47.9% in the trade balance surplus. The acknowledgment of Brazil as a safe environment for investments, expressed in terms of risk expectations, contributed to net infl ows of US$112.4 billion in the capital and fi nancial account in 2011. The balance of payments turned in a surplus of US$58.6 billion.

Table 5.2 – Balance of payments

US$ million

Itemization 2010 2011

1st half 2nd half Year 1st half 2nd half Year

Trade balance - FOB 7 880 12 267 20 147 12 960 16 846 29 807 Exports 89 187 112 728 201 915 118 304 137 736 256 040 Imports 81 308 100 461 181 768 105 343 120 890 226 233Services -13 531 -17 304 -30 835 -17 993 -19 959 -37 952 Credit 14 765 16 834 31 599 18 179 20 030 38 209 Debit 28 296 34 138 62 434 36 172 39 989 76 161 Income -19 731 -19 755 -39 486 -22 577 -24 742 -47 319 Credit 3 124 4 282 7 405 5 758 4 994 10 753 Debit 22 855 24 037 46 892 28 335 29 736 58 072 Current unilateral transfers (net) 1 563 1 339 2 902 1 576 1 408 2 984 Credit 2 395 2 379 4 775 2 481 2 435 4 915 Debit 833 1 040 1 873 905 1 027 1 931Current account -23 820 -23 453 -47 273 -26 034 -26 446 -52 480Capital and financial account 42 989 56 923 99 912 69 341 43 048 112 389 Capital account 494 625 1 119 666 907 1 573 Financial account 42 495 56 299 98 793 68 675 42 141 110 816 Direct investment (net) 3 215 33 704 36 919 34 986 32 703 67 689 Abroad -8 881 -2 706 -11 588 2 484 -1 455 1 029 Equity capital -12 110 -14 673 -26 782 -14 597 -4 936 -19 533 Intercompany loans 3 229 11 966 15 195 17 081 3 481 20 562 In the reporting country 12 096 36 410 48 506 32 502 34 158 66 660 Equity capital 12 256 27 860 40 117 25 827 28 955 54 782 Intercompany loans -160 8 550 8 390 6 675 5 203 11 878 Portfolio investments 22 790 40 221 63 011 25 146 10 165 35 311 Assets -375 -4 408 -4 784 12 711 4 147 16 858 Equity securities 896 5 315 6 211 6 841 1 961 8 801 Debt securities -1 271 -9 724 -10 995 5 871 2 186 8 057 Liabilities 23 166 44 629 67 795 12 435 6 018 18 453 Equity securities 9 733 27 937 37 671 3 865 3 309 7 174 Debt securities 13 432 16 692 30 124 8 570 2 709 11 278 Financial derivatives -17 -95 -112 -9 12 3 Assets 74 59 133 170 82 252 Liabilities -91 -154 -245 -179 -70 -249

Other investments1/ 16 507 -17 531 -1 024 8 552 -739 7 813 Assets -12 045 -30 522 -42 567 -20 564 -18 420 -38 984 Liabilities 28 552 12 991 41 543 29 116 17 681 46 796Errors and omissions -2 502 -1 036 -3 538 -397 -875 -1 272Overall balance 16 666 32 434 49 101 42 910 15 727 58 637

Memo:Current account/GDP (%) -2.20 -2.12

1/ Includes trade credits, loans, currency and deposits, other assets and liabilities.

88 Boletim do Banco Central do Brasil – Annual Report 2011

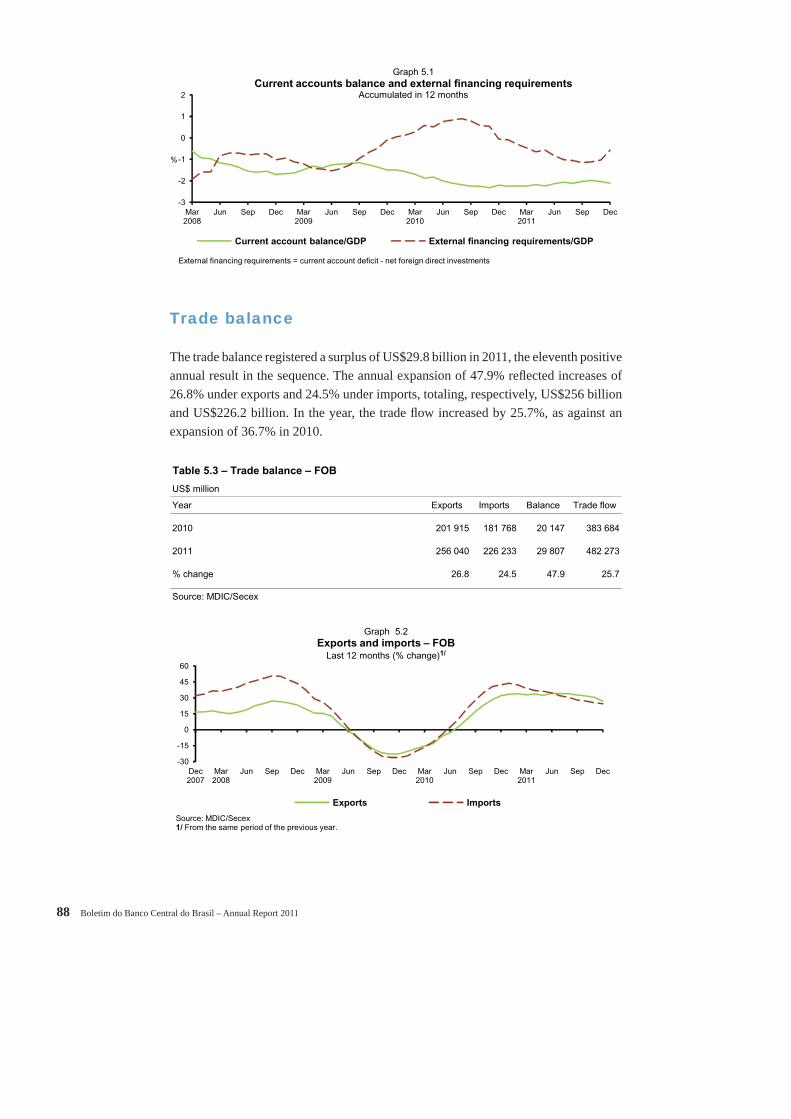

Trade balance

The trade balance registered a surplus of US$29.8 billion in 2011, the eleventh positive annual result in the sequence. The annual expansion of 47.9% refl ected increases of 26.8% under exports and 24.5% under imports, totaling, respectively, US$256 billion and US$226.2 billion. In the year, the trade fl ow increased by 25.7%, as against an expansion of 36.7% in 2010.

Table 5.3 – Trade balance – FOB

US$ million

Year Exports Imports Balance Trade flow

2010 201 915 181 768 20 147 383 684

2011 256 040 226 233 29 807 482 273

% change 26.8 24.5 47.9 25.7

Source: MDIC/Secex

-3

-2

-1

0

1

2

Mar2008

Jun Sep Dec Mar2009

Jun Sep Dec Mar2010

Jun Sep Dec Mar2011

Jun Sep Dec

Graph 5.1Current accounts balance and external financing requirements

Accumulated in 12 months

Current account balance/GDP External financing requirements/GDP

%

External financing requirements = current account deficit - net foreign direct investments

-30

-15

0

15

30

45

60

Dec 2007

Mar 2008

Jun Sep Dec Mar 2009

Jun Sep Dec Mar 2010

Jun Sep Dec Mar 2011

Jun Sep Dec

Source: MDIC/Secex1/ From the same period of the previous year.

Exports Imports

Graph 5.2Exports and imports – FOB

Last 12 months (% change)1/

V Economic-Financial Relations with the International Community 89

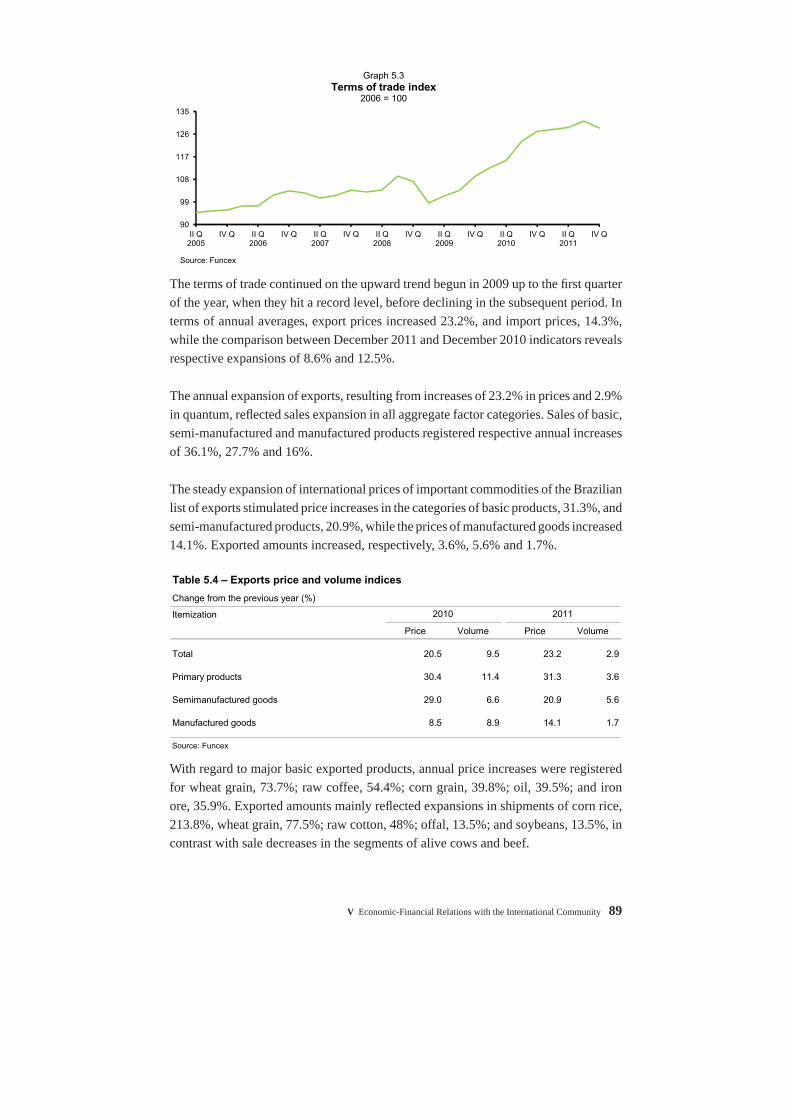

The terms of trade continued on the upward trend begun in 2009 up to the fi rst quarter of the year, when they hit a record level, before declining in the subsequent period. In terms of annual averages, export prices increased 23.2%, and import prices, 14.3%, while the comparison between December 2011 and December 2010 indicators reveals respective expansions of 8.6% and 12.5%.

The annual expansion of exports, resulting from increases of 23.2% in prices and 2.9% in quantum, refl ected sales expansion in all aggregate factor categories. Sales of basic, semi-manufactured and manufactured products registered respective annual increases of 36.1%, 27.7% and 16%.

The steady expansion of international prices of important commodities of the Brazilian list of exports stimulated price increases in the categories of basic products, 31.3%, and semi-manufactured products, 20.9%, while the prices of manufactured goods increased 14.1%. Exported amounts increased, respectively, 3.6%, 5.6% and 1.7%.

With regard to major basic exported products, annual price increases were registered for wheat grain, 73.7%; raw coffee, 54.4%; corn grain, 39.8%; oil, 39.5%; and iron ore, 35.9%. Exported amounts mainly refl ected expansions in shipments of corn rice, 213.8%, wheat grain, 77.5%; raw cotton, 48%; offal, 13.5%; and soybeans, 13.5%, in contrast with sale decreases in the segments of alive cows and beef.

90

99

108

117

126

135

II Q 2005

IV Q II Q 2006

IV Q II Q 2007

IV Q II Q 2008

IV Q II Q 2009

IV Q II Q 2010

IV Q II Q 2011

IV Q

Source: Funcex

Graph 5.3Terms of trade index

2006 = 100

Table 5.4 – Exports price and volume indices

Change from the previous year (%)

Itemization

Price Volume Price Volume

Total 20.5 9.5 23.2 2.9

Primary products 30.4 11.4 31.3 3.6

Semimanufactured goods 29.0 6.6 20.9 5.6

Manufactured goods 8.5 8.9 14.1 1.7

Source: Funcex

2010 2011

90 Boletim do Banco Central do Brasil – Annual Report 2011

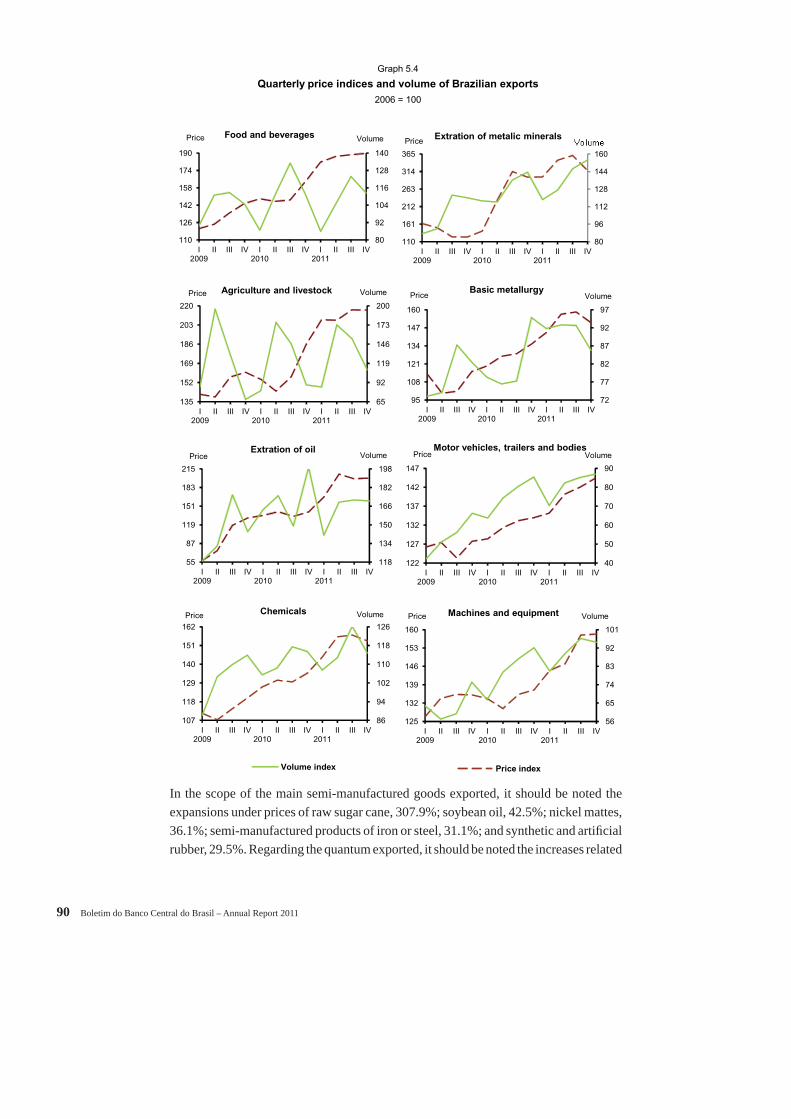

In the scope of the main semi-manufactured goods exported, it should be noted the expansions under prices of raw sugar cane, 307.9%; soybean oil, 42.5%; nickel mattes, 36.1%; semi-manufactured products of iron or steel, 31.1%; and synthetic and artifi cial rubber, 29.5%. Regarding the quantum exported, it should be noted the increases related

Quarterly price indices and volume of Brazilian exports

2006 = 100

Graph 5.4

80

92

104

116

128

140

110

126

142

158

174

190

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice Food and beverages

118

134

150

166

182

198

55

87

119

151

183

215

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePriceExtration of oil

65

92

119

146

173

200

135

152

169

186

203

220

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice Agriculture and livestock

72

77

82

87

92

97

95

108

121

134

147

160

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePriceBasic metallurgy

80

96

112

128

144

160

110

161

212

263

314

365

I2009

II III IV I2010

II III IV I2011

II III IV

Price Extration of metalic minerals

40

50

60

70

80

90

122

127

132

137

142

147

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePriceMotor vehicles, trailers and bodies

86

94

102

110

118

126

107

118

129

140

151

162

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice Chemicals

Volume index

56

65

74

83

92

101

125

132

139

146

153

160

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice Machines and equipment

Price index

V Economic-Financial Relations with the International Community 91

to pig iron and Spiegel iron, 40.6%, semi-manufactured products of iron or steel, 36.4%; copper cathodes, 23%; zinc, 15.2%, and nickel cathodes, 14.4%; in contrast with the decreases in the shipments of aluminum alloys, wood sawn or chipped and vegetable waxes.

In relation to foreign sales of manufactured products, whose prices, in general, are less volatile, it should be noted the annual increases in the segments of ethyl alcohol, 42.4%; fuel oil, 38.1%; frozen orange juice, 37.1%; hydrocarbons and their derivatives, 36%; and refi ned sugar, 33.2%. Regarding the amounts exported in this category, increases were observed in excavation and drilling machinery, 29.9%; tractors, 20.9%; ethylene polymers, propylene and styrene, 17.9%; engines for automotive vehicles, 17.9%; and cargo vehicles, 16.6%. Conversely, decreases higher than 15% were observed in the amounts exported of refi ned sugar, footwear and accessories, and hydrocarbons and their derivatives.

In 2011, according to the Foreign Trade Studies Center Foundation (Funcex), eight of the chief export segments totaled 80% of the country’s foreign sales. In the year, prices increased in all the mentioned segments, with emphasis on those related to oil drilling, 39.7%; metallic minerals, 34.6%; and crop and livestock, 31.9%. Among exports, it should be noted expansions related to basic metallurgy and machinery and equipments; both of them accounting for 11%; and automotive vehicles, tow trucks and bodyworks, 6.8%.

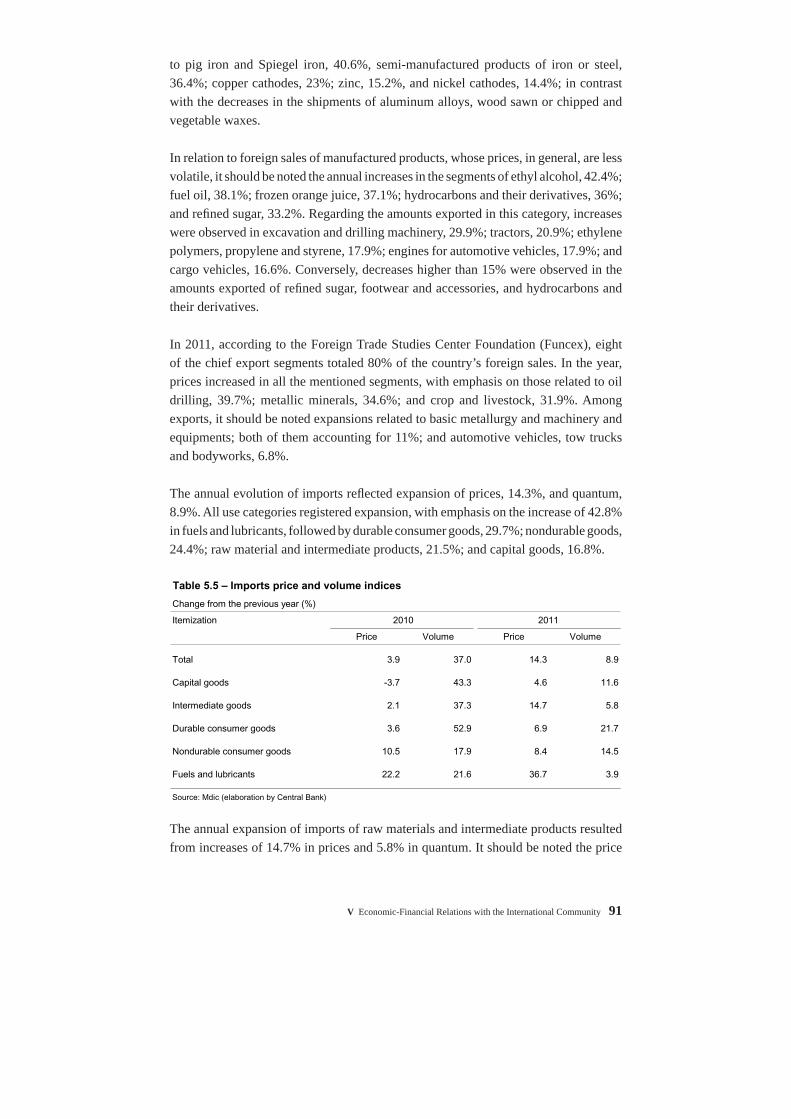

The annual evolution of imports refl ected expansion of prices, 14.3%, and quantum, 8.9%. All use categories registered expansion, with emphasis on the increase of 42.8% in fuels and lubricants, followed by durable consumer goods, 29.7%; nondurable goods, 24.4%; raw material and intermediate products, 21.5%; and capital goods, 16.8%.

The annual expansion of imports of raw materials and intermediate products resulted from increases of 14.7% in prices and 5.8% in quantum. It should be noted the price

Table 5.5 – Imports price and volume indices

Change from the previous year (%)

Itemization 2010 2011

Price Volume Price Volume

Total 3.9 37.0 14.3 8.9

Capital goods -3.7 43.3 4.6 11.6

Intermediate goods 2.1 37.3 14.7 5.8

Durable consumer goods 3.6 52.9 6.9 21.7

Nondurable consumer goods 10.5 17.9 8.4 14.5

Fuels and lubricants 22.2 21.6 36.7 3.9

Source: Mdic (elaboration by Central Bank)

92 Boletim do Banco Central do Brasil – Annual Report 2011

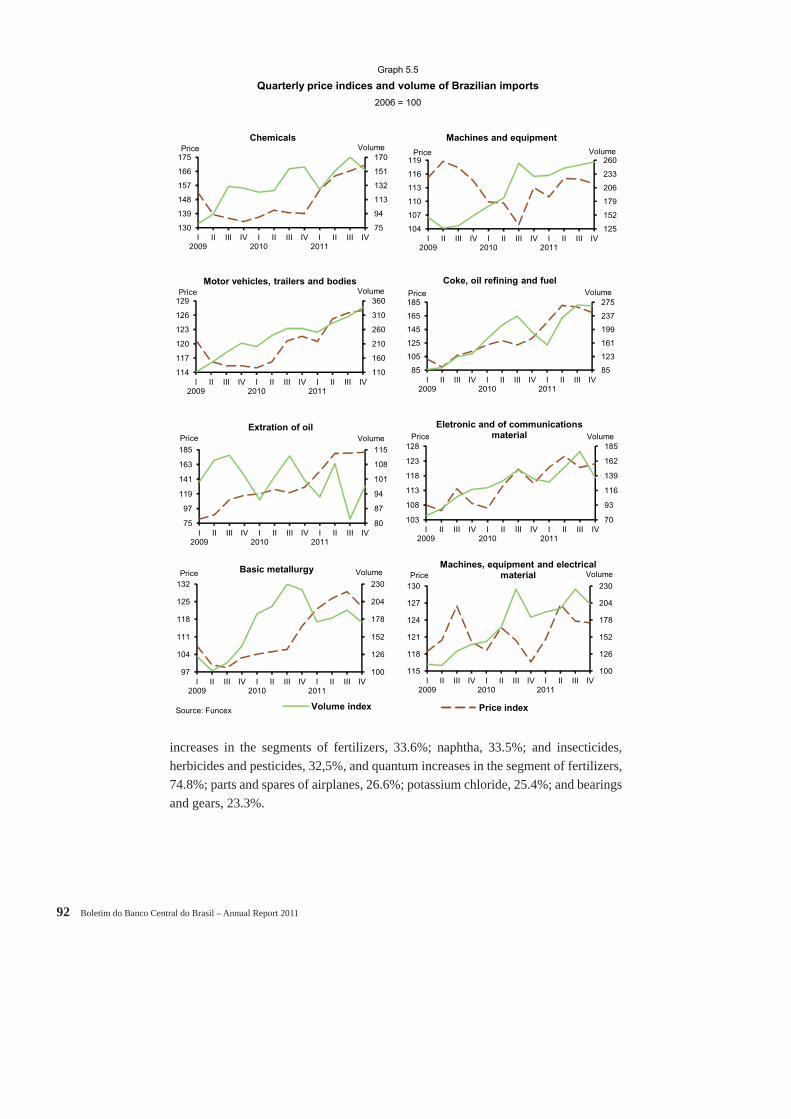

increases in the segments of fertilizers, 33.6%; naphtha, 33.5%; and insecticides, herbicides and pesticides, 32,5%, and quantum increases in the segment of fertilizers, 74.8%; parts and spares of airplanes, 26.6%; potassium chloride, 25.4%; and bearings and gears, 23.3%.

Quarterly price indices and volume of Brazilian imports

2006 = 100

Graph 5.5

75

94

113

132

151

170

130

139

148

157

166

175

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePriceChemicals

100

126

152

178

204

230

115

118

121

124

127

130

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePriceMachines, equipment and electrical

material

Price index

70

93

116

139

162

185

103

108

113

118

123

128

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice

Eletronic and of communications

material

80

87

94

101

108

115

75

97

119

141

163

185

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePriceExtration of oil

125

152

179

206

233

260

104

107

110

113

116

119

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice

Machines and equipment

85

123

161

199

237

275

85

105

125

145

165

185

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice

Coke, oil refining and fuel

100

126

152

178

204

230

97

104

111

118

125

132

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePrice Basic metallurgy

Volume indexSource: Funcex

110

160

210

260

310

360

114

117

120

123

126

129

I2009

II III IV I2010

II III IV I2011

II III IV

VolumePriceMotor vehicles, trailers and bodies

V Economic-Financial Relations with the International Community 93

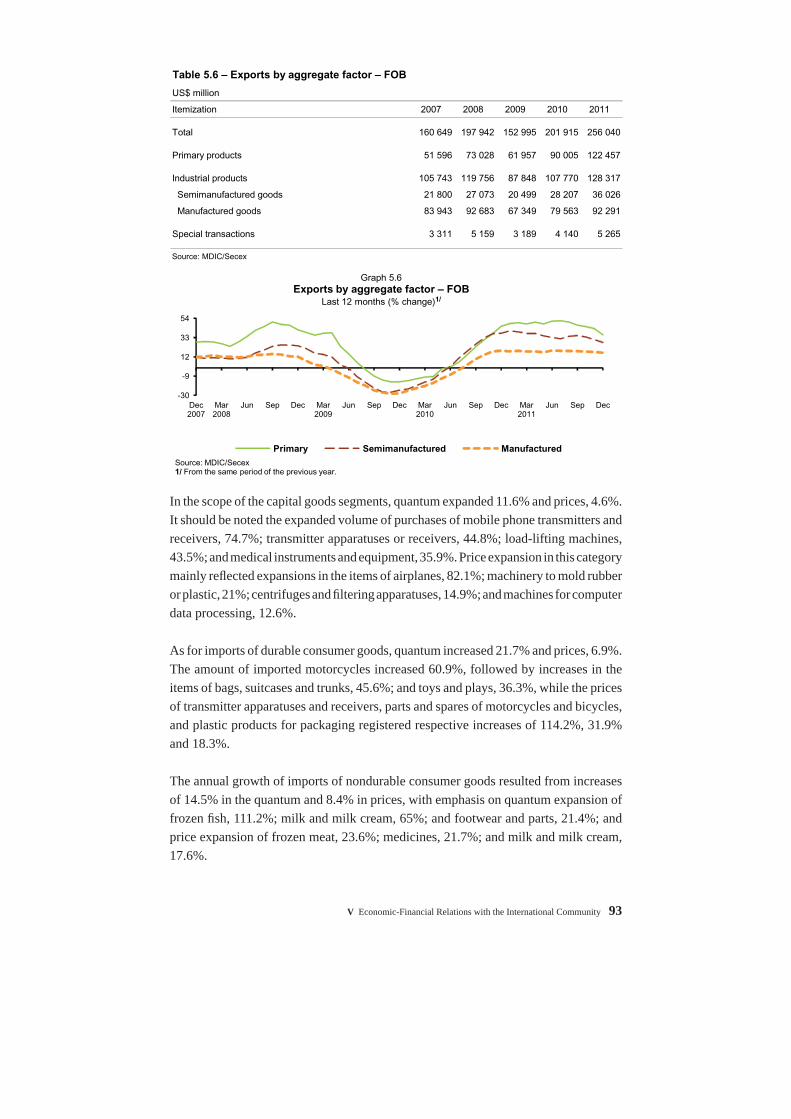

In the scope of the capital goods segments, quantum expanded 11.6% and prices, 4.6%. It should be noted the expanded volume of purchases of mobile phone transmitters and receivers, 74.7%; transmitter apparatuses or receivers, 44.8%; load-lifting machines, 43.5%; and medical instruments and equipment, 35.9%. Price expansion in this category mainly refl ected expansions in the items of airplanes, 82.1%; machinery to mold rubber or plastic, 21%; centrifuges and fi ltering apparatuses, 14.9%; and machines for computer data processing, 12.6%.

As for imports of durable consumer goods, quantum increased 21.7% and prices, 6.9%. The amount of imported motorcycles increased 60.9%, followed by increases in the items of bags, suitcases and trunks, 45.6%; and toys and plays, 36.3%, while the prices of transmitter apparatuses and receivers, parts and spares of motorcycles and bicycles, and plastic products for packaging registered respective increases of 114.2%, 31.9% and 18.3%.

The annual growth of imports of nondurable consumer goods resulted from increases of 14.5% in the quantum and 8.4% in prices, with emphasis on quantum expansion of frozen fi sh, 111.2%; milk and milk cream, 65%; and footwear and parts, 21.4%; and price expansion of frozen meat, 23.6%; medicines, 21.7%; and milk and milk cream, 17.6%.

Table 5.6 – Exports by aggregate factor – FOB

US$ million

Itemization 2007 2008 2009 2010 2011

Total 160 649 197 942 152 995 201 915 256 040

Primary products 51 596 73 028 61 957 90 005 122 457

Industrial products 105 743 119 756 87 848 107 770 128 317

Semimanufactured goods 21 800 27 073 20 499 28 207 36 026

Manufactured goods 83 943 92 683 67 349 79 563 92 291

Special transactions 3 311 5 159 3 189 4 140 5 265

Source: MDIC/Secex

-30

-9

12

33

54

Dec 2007

Mar 2008

Jun Sep Dec Mar 2009

Jun Sep Dec Mar 2010

Jun Sep Dec Mar 2011

Jun Sep Dec

Source: MDIC/Secex1/ From the same period of the previous year.

Primary Semimanufactured Manufactured

Graph 5.6Exports by aggregate factor – FOB

Last 12 months (% change)1/

94 Boletim do Banco Central do Brasil – Annual Report 2011

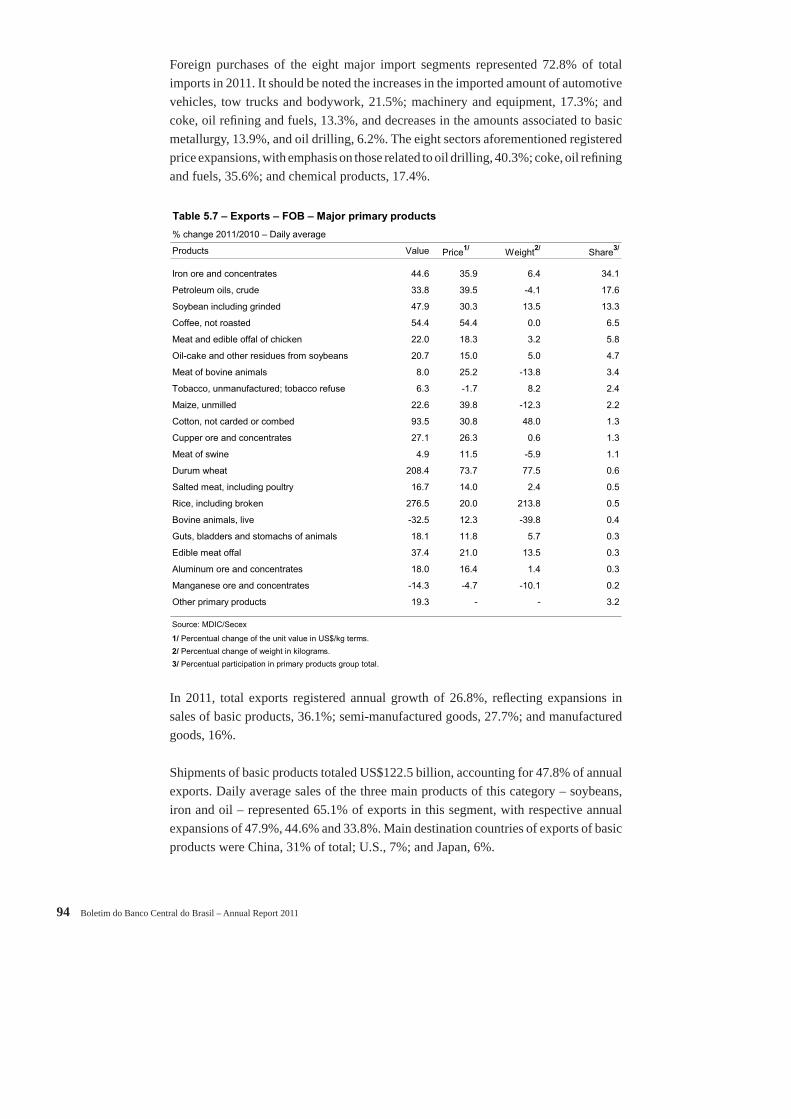

Foreign purchases of the eight major import segments represented 72.8% of total imports in 2011. It should be noted the increases in the imported amount of automotive vehicles, tow trucks and bodywork, 21.5%; machinery and equipment, 17.3%; and coke, oil refi ning and fuels, 13.3%, and decreases in the amounts associated to basic metallurgy, 13.9%, and oil drilling, 6.2%. The eight sectors aforementioned registered price expansions, with emphasis on those related to oil drilling, 40.3%; coke, oil refi ning and fuels, 35.6%; and chemical products, 17.4%.

In 2011, total exports registered annual growth of 26.8%, refl ecting expansions in sales of basic products, 36.1%; semi-manufactured goods, 27.7%; and manufactured goods, 16%.

Shipments of basic products totaled US$122.5 billion, accounting for 47.8% of annual exports. Daily average sales of the three main products of this category – soybeans, iron and oil – represented 65.1% of exports in this segment, with respective annual expansions of 47.9%, 44.6% and 33.8%. Main destination countries of exports of basic products were China, 31% of total; U.S., 7%; and Japan, 6%.

Table 5.7 – Exports – FOB – Major primary products

% change 2011/2010 – Daily average

Products Value Price1/ Weight2/ Share3/

Iron ore and concentrates 44.6 35.9 6.4 34.1

Petroleum oils, crude 33.8 39.5 -4.1 17.6

Soybean including grinded 47.9 30.3 13.5 13.3

Coffee, not roasted 54.4 54.4 0.0 6.5

Meat and edible offal of chicken 22.0 18.3 3.2 5.8

Oil-cake and other residues from soybeans 20.7 15.0 5.0 4.7

Meat of bovine animals 8.0 25.2 -13.8 3.4

Tobacco, unmanufactured; tobacco refuse 6.3 -1.7 8.2 2.4

Maize, unmilled 22.6 39.8 -12.3 2.2

Cotton, not carded or combed 93.5 30.8 48.0 1.3

Cupper ore and concentrates 27.1 26.3 0.6 1.3

Meat of swine 4.9 11.5 -5.9 1.1

Durum wheat 208.4 73.7 77.5 0.6

Salted meat, including poultry 16.7 14.0 2.4 0.5

Rice, including broken 276.5 20.0 213.8 0.5

Bovine animals, live -32.5 12.3 -39.8 0.4

Guts, bladders and stomachs of animals 18.1 11.8 5.7 0.3

Edible meat offal 37.4 21.0 13.5 0.3

Aluminum ore and concentrates 18.0 16.4 1.4 0.3

Manganese ore and concentrates -14.3 -4.7 -10.1 0.2

Other primary products 19.3 - - 3.2

Source: MDIC/Secex

1/ Percentual change of the unit value in US$/kg terms.

2/ Percentual change of weight in kilograms.

3/ Percentual participation in primary products group total.

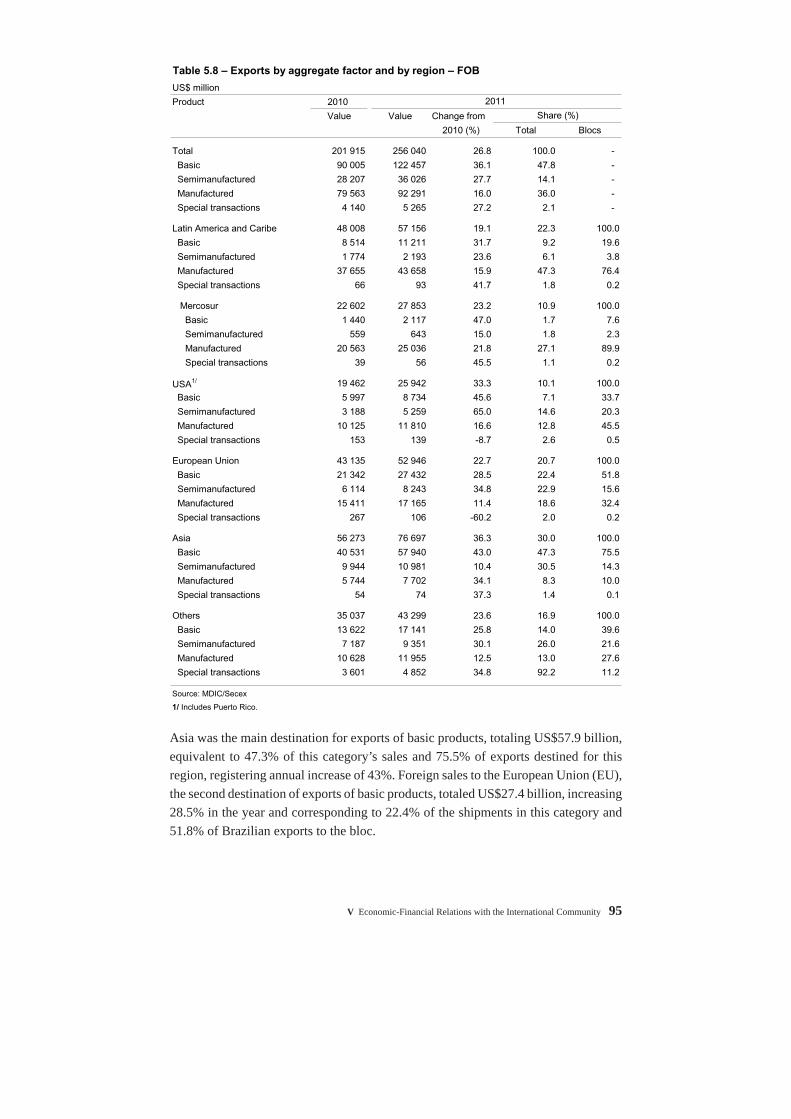

V Economic-Financial Relations with the International Community 95

Asia was the main destination for exports of basic products, totaling US$57.9 billion, equivalent to 47.3% of this category’s sales and 75.5% of exports destined for this region, registering annual increase of 43%. Foreign sales to the European Union (EU), the second destination of exports of basic products, totaled US$27.4 billion, increasing 28.5% in the year and corresponding to 22.4% of the shipments in this category and 51.8% of Brazilian exports to the bloc.

Table 5.8 – Exports by aggregate factor and by region – FOB

US$ million

Product 2010

Value Value Change from

2010 (%) Total Blocs

Total 201 915 256 040 26.8 100.0 -

Basic 90 005 122 457 36.1 47.8 -

Semimanufactured 28 207 36 026 27.7 14.1 -

Manufactured 79 563 92 291 16.0 36.0 -

Special transactions 4 140 5 265 27.2 2.1 -

Latin America and Caribe 48 008 57 156 19.1 22.3 100.0

Basic 8 514 11 211 31.7 9.2 19.6

Semimanufactured 1 774 2 193 23.6 6.1 3.8

Manufactured 37 655 43 658 15.9 47.3 76.4

Special transactions 66 93 41.7 1.8 0.2

Mercosur 22 602 27 853 23.2 10.9 100.0

Basic 1 440 2 117 47.0 1.7 7.6

Semimanufactured 559 643 15.0 1.8 2.3

Manufactured 20 563 25 036 21.8 27.1 89.9

Special transactions 39 56 45.5 1.1 0.2

USA1/ 19 462 25 942 33.3 10.1 100.0

Basic 5 997 8 734 45.6 7.1 33.7

Semimanufactured 3 188 5 259 65.0 14.6 20.3

Manufactured 10 125 11 810 16.6 12.8 45.5

Special transactions 153 139 -8.7 2.6 0.5

European Union 43 135 52 946 22.7 20.7 100.0

Basic 21 342 27 432 28.5 22.4 51.8

Semimanufactured 6 114 8 243 34.8 22.9 15.6

Manufactured 15 411 17 165 11.4 18.6 32.4

Special transactions 267 106 -60.2 2.0 0.2

Asia 56 273 76 697 36.3 30.0 100.0

Basic 40 531 57 940 43.0 47.3 75.5

Semimanufactured 9 944 10 981 10.4 30.5 14.3

Manufactured 5 744 7 702 34.1 8.3 10.0

Special transactions 54 74 37.3 1.4 0.1

Others 35 037 43 299 23.6 16.9 100.0

Basic 13 622 17 141 25.8 14.0 39.6

Semimanufactured 7 187 9 351 30.1 26.0 21.6

Manufactured 10 628 11 955 12.5 13.0 27.6

Special transactions 3 601 4 852 34.8 92.2 11.2

Source: MDIC/Secex

1/ Includes Puerto Rico.

Share (%)

2011

96 Boletim do Banco Central do Brasil – Annual Report 2011

Sales of basic products to the Latin America and the Caribbean totaled US$11.2 billion, of which 18.9% to member states of the Mercosur, corresponding to 9.2% of exports in this category and 19.6% of shipments destined for the region, with annual increase of 31.7%. Exports of basic products to the U.S. totaled US$8.7 billion, increasing 45.6% in the year and representing 7.1% of shipments in this category and 33.7% of the total exported to the country. Sales of basic products to other countries totaled US$17.1 billion, for annual expansion of 25.8%, representing 14% of the total exported and 39.6% of total sales to these countries.

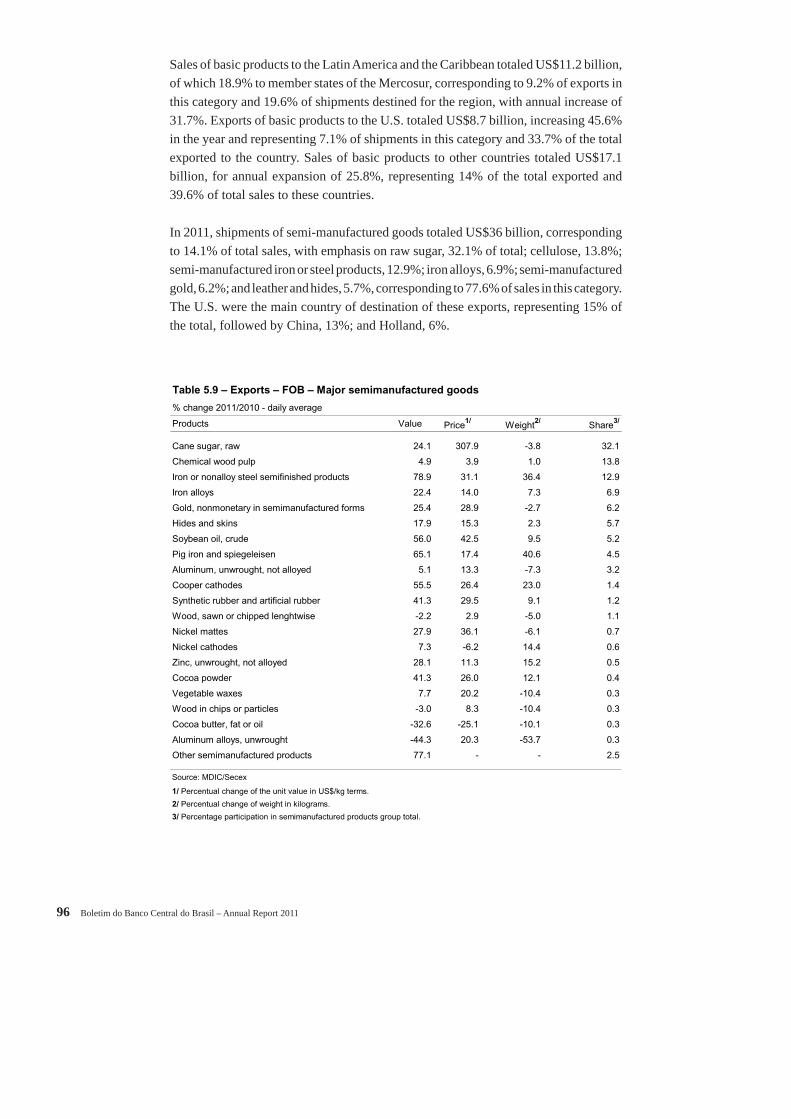

In 2011, shipments of semi-manufactured goods totaled US$36 billion, corresponding to 14.1% of total sales, with emphasis on raw sugar, 32.1% of total; cellulose, 13.8%; semi-manufactured iron or steel products, 12.9%; iron alloys, 6.9%; semi-manufactured gold, 6.2%; and leather and hides, 5.7%, corresponding to 77.6% of sales in this category. The U.S. were the main country of destination of these exports, representing 15% of the total, followed by China, 13%; and Holland, 6%.

Table 5.9 – Exports – FOB – Major semimanufactured goods

% change 2011/2010 - daily average

Products Value Price1/ Weight2/ Share3/

Cane sugar, raw 24.1 307.9 -3.8 32.1

Chemical wood pulp 4.9 3.9 1.0 13.8

Iron or nonalloy steel semifinished products 78.9 31.1 36.4 12.9

Iron alloys 22.4 14.0 7.3 6.9

Gold, nonmonetary in semimanufactured forms 25.4 28.9 -2.7 6.2

Hides and skins 17.9 15.3 2.3 5.7

Soybean oil, crude 56.0 42.5 9.5 5.2

Pig iron and spiegeleisen 65.1 17.4 40.6 4.5

Aluminum, unwrought, not alloyed 5.1 13.3 -7.3 3.2

Cooper cathodes 55.5 26.4 23.0 1.4

Synthetic rubber and artificial rubber 41.3 29.5 9.1 1.2

Wood, sawn or chipped lenghtwise -2.2 2.9 -5.0 1.1

Nickel mattes 27.9 36.1 -6.1 0.7

Nickel cathodes 7.3 -6.2 14.4 0.6

Zinc, unwrought, not alloyed 28.1 11.3 15.2 0.5

Cocoa powder 41.3 26.0 12.1 0.4

Vegetable waxes 7.7 20.2 -10.4 0.3

Wood in chips or particles -3.0 8.3 -10.4 0.3

Cocoa butter, fat or oil -32.6 -25.1 -10.1 0.3

Aluminum alloys, unwrought -44.3 20.3 -53.7 0.3

Other semimanufactured products 77.1 - - 2.5

Source: MDIC/Secex

1/ Percentual change of the unit value in US$/kg terms.

2/ Percentual change of weight in kilograms.

3/ Percentage participation in semimanufactured products group total.

V Economic-Financial Relations with the International Community 97

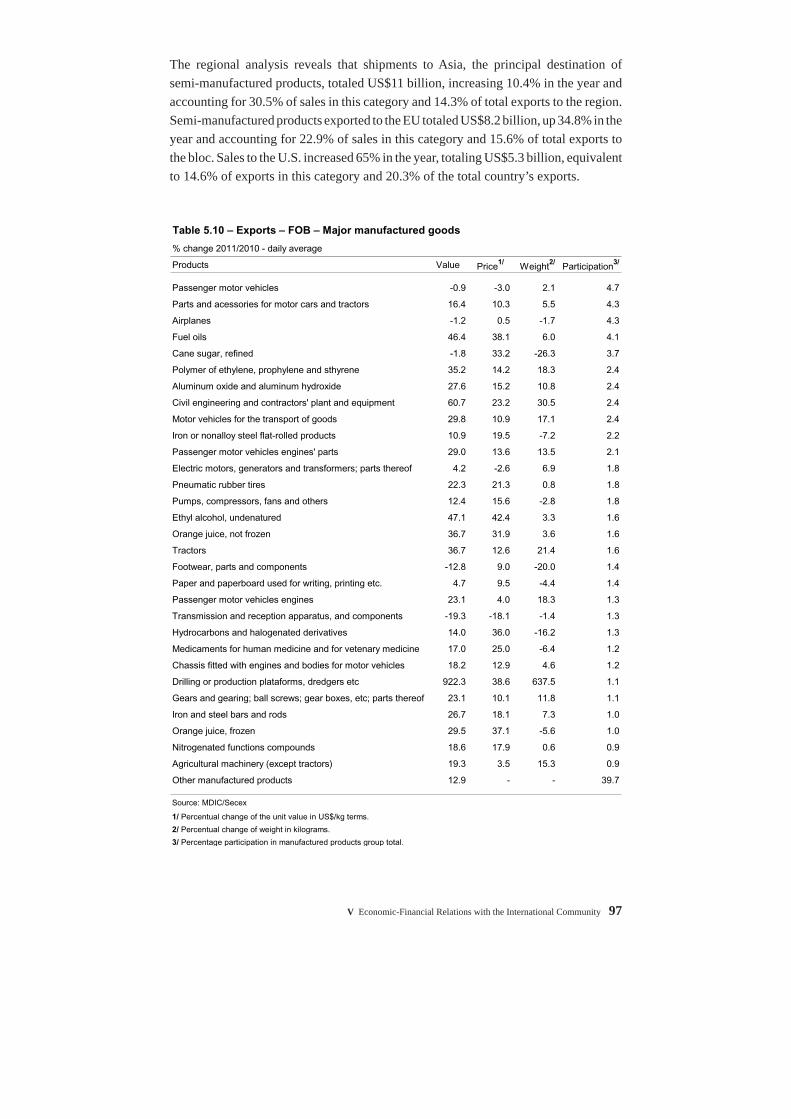

The regional analysis reveals that shipments to Asia, the principal destination of semi-manufactured products, totaled US$11 billion, increasing 10.4% in the year and accounting for 30.5% of sales in this category and 14.3% of total exports to the region. Semi-manufactured products exported to the EU totaled US$8.2 billion, up 34.8% in the year and accounting for 22.9% of sales in this category and 15.6% of total exports to the bloc. Sales to the U.S. increased 65% in the year, totaling US$5.3 billion, equivalent to 14.6% of exports in this category and 20.3% of the total country’s exports.

Table 5.10 – Exports – FOB – Major manufactured goods

% change 2011/2010 - daily average

Products Value Price1/ Weight2/ Participation3/

Passenger motor vehicles -0.9 -3.0 2.1 4.7

Parts and acessories for motor cars and tractors 16.4 10.3 5.5 4.3

Airplanes -1.2 0.5 -1.7 4.3

Fuel oils 46.4 38.1 6.0 4.1

Cane sugar, refined -1.8 33.2 -26.3 3.7

Polymer of ethylene, prophylene and sthyrene 35.2 14.2 18.3 2.4

Aluminum oxide and aluminum hydroxide 27.6 15.2 10.8 2.4

Civil engineering and contractors' plant and equipment 60.7 23.2 30.5 2.4

Motor vehicles for the transport of goods 29.8 10.9 17.1 2.4

Iron or nonalloy steel flat-rolled products 10.9 19.5 -7.2 2.2

Passenger motor vehicles engines' parts 29.0 13.6 13.5 2.1

Electric motors, generators and transformers; parts thereof 4.2 -2.6 6.9 1.8

Pneumatic rubber tires 22.3 21.3 0.8 1.8

Pumps, compressors, fans and others 12.4 15.6 -2.8 1.8

Ethyl alcohol, undenatured 47.1 42.4 3.3 1.6

Orange juice, not frozen 36.7 31.9 3.6 1.6

Tractors 36.7 12.6 21.4 1.6

Footwear, parts and components -12.8 9.0 -20.0 1.4

Paper and paperboard used for writing, printing etc. 4.7 9.5 -4.4 1.4

Passenger motor vehicles engines 23.1 4.0 18.3 1.3

Transmission and reception apparatus, and components -19.3 -18.1 -1.4 1.3

Hydrocarbons and halogenated derivatives 14.0 36.0 -16.2 1.3

Medicaments for human medicine and for vetenary medicine 17.0 25.0 -6.4 1.2

Chassis fitted with engines and bodies for motor vehicles 18.2 12.9 4.6 1.2

Drilling or production plataforms, dredgers etc 922.3 38.6 637.5 1.1

Gears and gearing; ball screws; gear boxes, etc; parts thereof 23.1 10.1 11.8 1.1

Iron and steel bars and rods 26.7 18.1 7.3 1.0

Orange juice, frozen 29.5 37.1 -5.6 1.0

Nitrogenated functions compounds 18.6 17.9 0.6 0.9

Agricultural machinery (except tractors) 19.3 3.5 15.3 0.9

Other manufactured products 12.9 - - 39.7

Source: MDIC/Secex

1/ Percentual change of the unit value in US$/kg terms.

2/ Percentual change of weight in kilograms.

3/ Percentage participation in manufactured products group total.

98 Boletim do Banco Central do Brasil – Annual Report 2011

Sales of semi-manufactured goods to the Latin America and the Caribbean, of which 29.3% to member states of the Mercosur, totaled US$2.2 billion, increasing 23.6% in the year and representing 6.1% of the total of this category and 3.8% of the total exported to these countries. Shipments of semi-manufactured products to the other countries of this area amounted to US$9.4 billion, with annual increase of 30.1%, corresponding to 26% of sales in this category and 21.6% of the total exported to the group.

Exports of manufactured products totaled US$92.3 billion, corresponding to 36% of the Brazilian exports in 2011 and being concentrated in passenger cars, 4.7% of total; auto parts, 4.3%; airplanes, 4.3%; fuel oil, 4.1%; and refi ned sugar, 3.7%. Sales of manufactured goods were mainly shipped to Argentina, 22% of the total in this category; U.S., 13%; and Netherlands, 5%.

Shipments of manufactured goods to the Latin America and the Caribbean totaled US$43.7 billion, increasing 15.9% in the year, corresponding to 47.3% of sales in this category and 76.4% of total shipments to this region. Exports of manufactured products to the EU reached US$17.2 billion, for annual expansion of 11.4%, representing 18.6% of sales in this category and 32.4% of shipments to the bloc.

Exports of manufactured goods to the U.S. registered annual increase of 16.6%, to US$11.8 billion, corresponding to 12.8% of the total of this category and 45.5% of total sales to the country. Shipments to Asia totaled US$7.7 billion, responding for 8.3% of exports of this category and 10% of Brazilian sales to the region, registering annual increase of 34.1%. S sales of manufactured products to the other countries in the region totaled US$12 billion, with annual expansion of 12.5%, representing 13% of the sales of this category and 27.6% of shipments to these countries.

Special operations – including onboard consumption and re-exports – amounted to US$5.3 billion in 2011, increasing 27.2% in the year and corresponding to 2.1% of total exports.

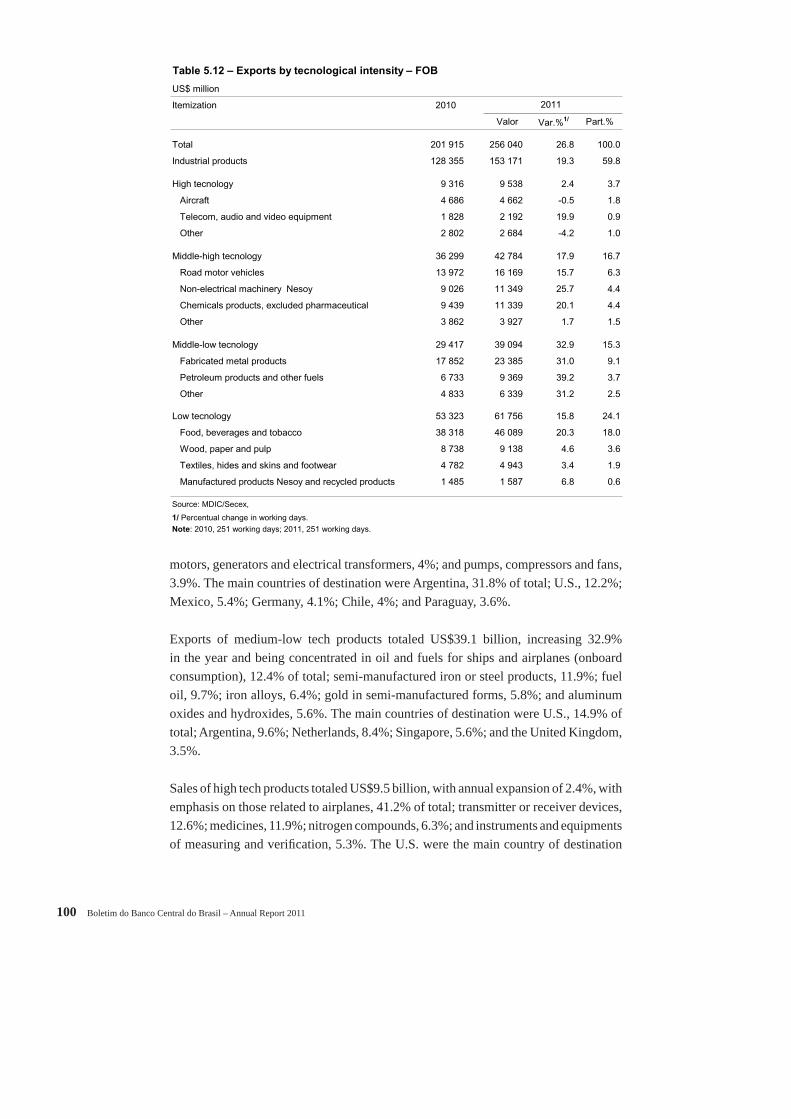

Exports of industrial products totaled US$153.2 billion in 2011, registering annual increase of 19.3%, corresponding to 59.8% of Brazilian exports, being distributed by low technology industries, 24.1% of total exports; medium-high technology, 16.7%, medium-low technology, 15.3%; and high technology, 3.7%.

Sales of low tech products totaled US$61.8 billion, with annual expansion of 15.8%. Shipments were concentrated in the segment of foodstuffs, beverage and tobacco, with emphasis on raw sugarcane, 18.7% of total; chicken meat, 11.4%; soybean meal, 9.2%; cellulose, 8.1%; and beef, 6.8%. The Netherlands was the main destination of these shipments, with 7.9% of total, followed by China, 7.3%; U.S., 7.3%; Russia, 5.7%; and Japan, 3.7%.

V Economic-Financial Relations with the International Community 99

Exports of medium-high tech products increased 17.9% in the year, adding up US$42.8 billion, with emphasis on those related to cars, 10.2% of total; auto parts, 9.3%; ethylene polymers, propylene and styrene, 5.2%; machinery and earthmoving equipments, 5.1%;

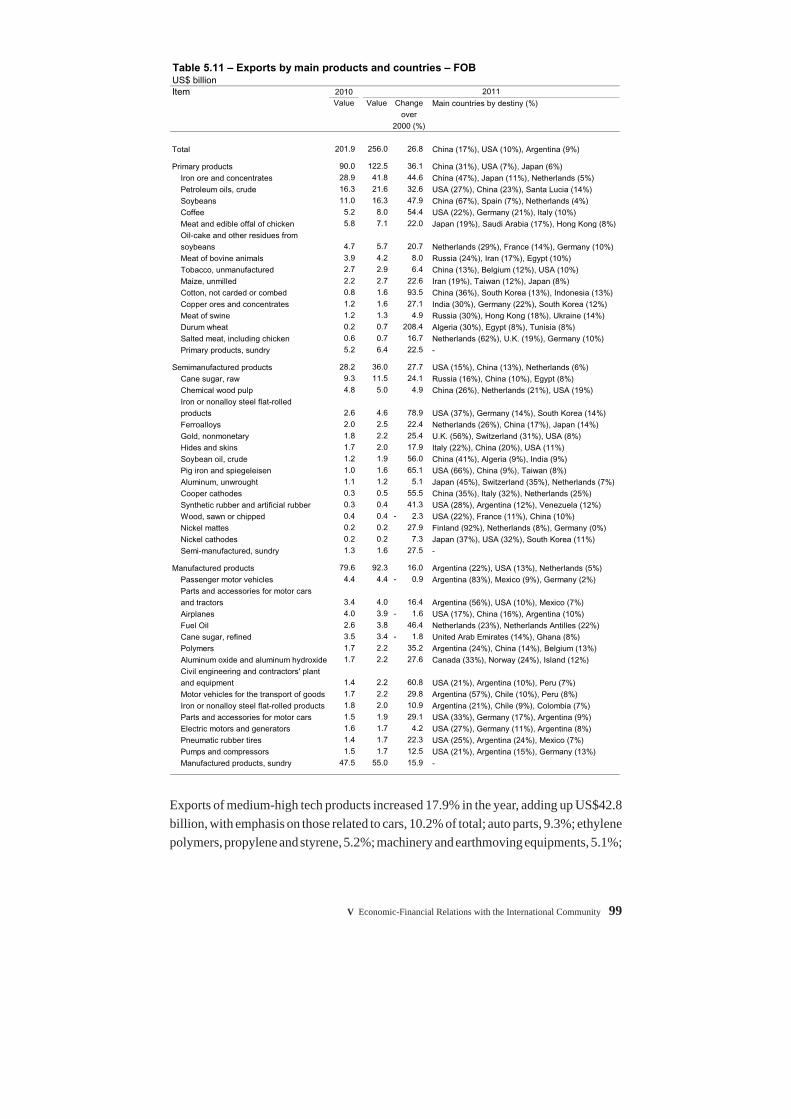

Table 5.11 – Exports by main products and countries – FOB

US$ billionItem 2010

Value Value Change Main countries by destiny (%)over

2000 (%)

Total 201.9 256.0 26.8 China (17%), USA (10%), Argentina (9%)

Primary products 90.0 122.5 36.1 China (31%), USA (7%), Japan (6%)Iron ore and concentrates 28.9 41.8 44.6 China (47%), Japan (11%), Netherlands (5%)Petroleum oils, crude 16.3 21.6 32.6 USA (27%), China (23%), Santa Lucia (14%)Soybeans 11.0 16.3 47.9 China (67%), Spain (7%), Netherlands (4%)Coffee 5.2 8.0 54.4 USA (22%), Germany (21%), Italy (10%)Meat and edible offal of chicken 5.8 7.1 22.0 Japan (19%), Saudi Arabia (17%), Hong Kong (8%)Oil-cake and other residues from soybeans 4.7 5.7 20.7 Netherlands (29%), France (14%), Germany (10%)Meat of bovine animals 3.9 4.2 8.0 Russia (24%), Iran (17%), Egypt (10%)Tobacco, unmanufactured 2.7 2.9 6.4 China (13%), Belgium (12%), USA (10%)Maize, unmilled 2.2 2.7 22.6 Iran (19%), Taiwan (12%), Japan (8%)Cotton, not carded or combed 0.8 1.6 93.5 China (36%), South Korea (13%), Indonesia (13%)Copper ores and concentrates 1.2 1.6 27.1 India (30%), Germany (22%), South Korea (12%)Meat of swine 1.2 1.3 4.9 Russia (30%), Hong Kong (18%), Ukraine (14%)Durum wheat 0.2 0.7 208.4 Algeria (30%), Egypt (8%), Tunisia (8%)Salted meat, including chicken 0.6 0.7 16.7 Netherlands (62%), U.K. (19%), Germany (10%)Primary products, sundry 5.2 6.4 22.5 -

Semimanufactured products 28.2 36.0 27.7 USA (15%), China (13%), Netherlands (6%)Cane sugar, raw 9.3 11.5 24.1 Russia (16%), China (10%), Egypt (8%)Chemical wood pulp 4.8 5.0 4.9 China (26%), Netherlands (21%), USA (19%)Iron or nonalloy steel flat-rolled products 2.6 4.6 78.9 USA (37%), Germany (14%), South Korea (14%)Ferroalloys 2.0 2.5 22.4 Netherlands (26%), China (17%), Japan (14%)Gold, nonmonetary 1.8 2.2 25.4 U.K. (56%), Switzerland (31%), USA (8%)Hides and skins 1.7 2.0 17.9 Italy (22%), China (20%), USA (11%)Soybean oil, crude 1.2 1.9 56.0 China (41%), Algeria (9%), India (9%)Pig iron and spiegeleisen 1.0 1.6 65.1 USA (66%), China (9%), Taiwan (8%)Aluminum, unwrought 1.1 1.2 5.1 Japan (45%), Switzerland (35%), Netherlands (7%)Cooper cathodes 0.3 0.5 55.5 China (35%), Italy (32%), Netherlands (25%)Synthetic rubber and artificial rubber 0.3 0.4 41.3 USA (28%), Argentina (12%), Venezuela (12%)Wood, sawn or chipped 0.4 0.4 - 2.3 USA (22%), France (11%), China (10%)Nickel mattes 0.2 0.2 27.9 Finland (92%), Netherlands (8%), Germany (0%)Nickel cathodes 0.2 0.2 7.3 Japan (37%), USA (32%), South Korea (11%)Semi-manufactured, sundry 1.3 1.6 27.5 -

Manufactured products 79.6 92.3 16.0 Argentina (22%), USA (13%), Netherlands (5%)Passenger motor vehicles 4.4 4.4 - 0.9 Argentina (83%), Mexico (9%), Germany (2%)Parts and accessories for motor carsand tractors 3.4 4.0 16.4 Argentina (56%), USA (10%), Mexico (7%)Airplanes 4.0 3.9 - 1.6 USA (17%), China (16%), Argentina (10%)Fuel Oil 2.6 3.8 46.4 Netherlands (23%), Netherlands Antilles (22%)Cane sugar, refined 3.5 3.4 - 1.8 United Arab Emirates (14%), Ghana (8%)Polymers 1.7 2.2 35.2 Argentina (24%), China (14%), Belgium (13%)Aluminum oxide and aluminum hydroxide 1.7 2.2 27.6 Canada (33%), Norway (24%), Island (12%)Civil engineering and contractors' plantand equipment 1.4 2.2 60.8 USA (21%), Argentina (10%), Peru (7%)Motor vehicles for the transport of goods 1.7 2.2 29.8 Argentina (57%), Chile (10%), Peru (8%)Iron or nonalloy steel flat-rolled products 1.8 2.0 10.9 Argentina (21%), Chile (9%), Colombia (7%)Parts and accessories for motor cars 1.5 1.9 29.1 USA (33%), Germany (17%), Argentina (9%)Electric motors and generators 1.6 1.7 4.2 USA (27%), Germany (11%), Argentina (8%)Pneumatic rubber tires 1.4 1.7 22.3 USA (25%), Argentina (24%), Mexico (7%)Pumps and compressors 1.5 1.7 12.5 USA (21%), Argentina (15%), Germany (13%)Manufactured products, sundry 47.5 55.0 15.9 -

2011

100 Boletim do Banco Central do Brasil – Annual Report 2011

motors, generators and electrical transformers, 4%; and pumps, compressors and fans, 3.9%. The main countries of destination were Argentina, 31.8% of total; U.S., 12.2%; Mexico, 5.4%; Germany, 4.1%; Chile, 4%; and Paraguay, 3.6%.

Exports of medium-low tech products totaled US$39.1 billion, increasing 32.9% in the year and being concentrated in oil and fuels for ships and airplanes (onboard consumption), 12.4% of total; semi-manufactured iron or steel products, 11.9%; fuel oil, 9.7%; iron alloys, 6.4%; gold in semi-manufactured forms, 5.8%; and aluminum oxides and hydroxides, 5.6%. The main countries of destination were U.S., 14.9% of total; Argentina, 9.6%; Netherlands, 8.4%; Singapore, 5.6%; and the United Kingdom, 3.5%.

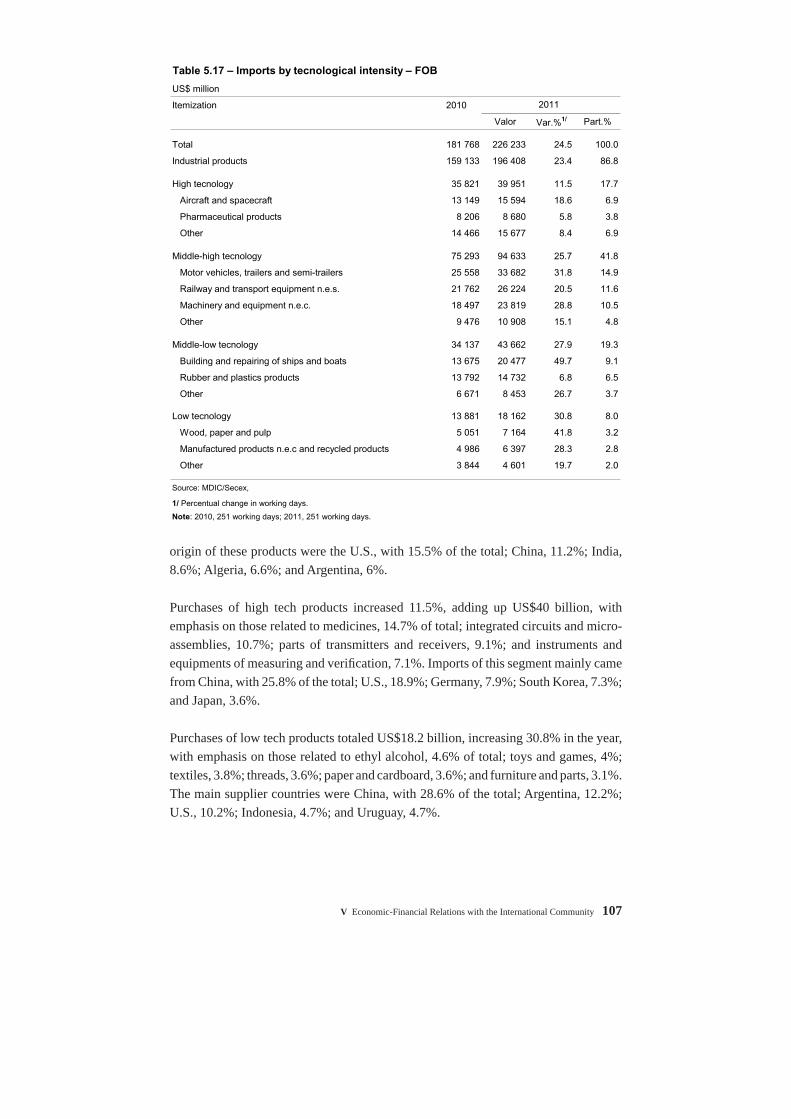

Sales of high tech products totaled US$9.5 billion, with annual expansion of 2.4%, with emphasis on those related to airplanes, 41.2% of total; transmitter or receiver devices, 12.6%; medicines, 11.9%; nitrogen compounds, 6.3%; and instruments and equipments of measuring and verifi cation, 5.3%. The U.S. were the main country of destination

Table 5.12 – Exports by tecnological intensity – FOB

US$ million

Itemization 2010

Valor Var.%1/ Part.%

Total 201 915 256 040 26.8 100.0

Industrial products 128 355 153 171 19.3 59.8

High tecnology 9 316 9 538 2.4 3.7

Aircraft 4 686 4 662 -0.5 1.8

Telecom, audio and video equipment 1 828 2 192 19.9 0.9

Other 2 802 2 684 -4.2 1.0

Middle-high tecnology 36 299 42 784 17.9 16.7

Road motor vehicles 13 972 16 169 15.7 6.3

Non-electrical machinery Nesoy 9 026 11 349 25.7 4.4

Chemicals products, excluded pharmaceutical 9 439 11 339 20.1 4.4

Other 3 862 3 927 1.7 1.5

Middle-low tecnology 29 417 39 094 32.9 15.3

Fabricated metal products 17 852 23 385 31.0 9.1

Petroleum products and other fuels 6 733 9 369 39.2 3.7

Other 4 833 6 339 31.2 2.5

Low tecnology 53 323 61 756 15.8 24.1

Food, beverages and tobacco 38 318 46 089 20.3 18.0

Wood, paper and pulp 8 738 9 138 4.6 3.6

Textiles, hides and skins and footwear 4 782 4 943 3.4 1.9

Manufactured products Nesoy and recycled products 1 485 1 587 6.8 0.6

Source: MDIC/Secex,

1/ Percentual change in working days.Note: 2010, 251 working days; 2011, 251 working days.

2011

V Economic-Financial Relations with the International Community 101

of these products, registering 16.7% of total; followed by Argentina, 12.8%; China, 8.1%; Germany, 5.1%; Mexico, 4.2%; and France, 2.8%.

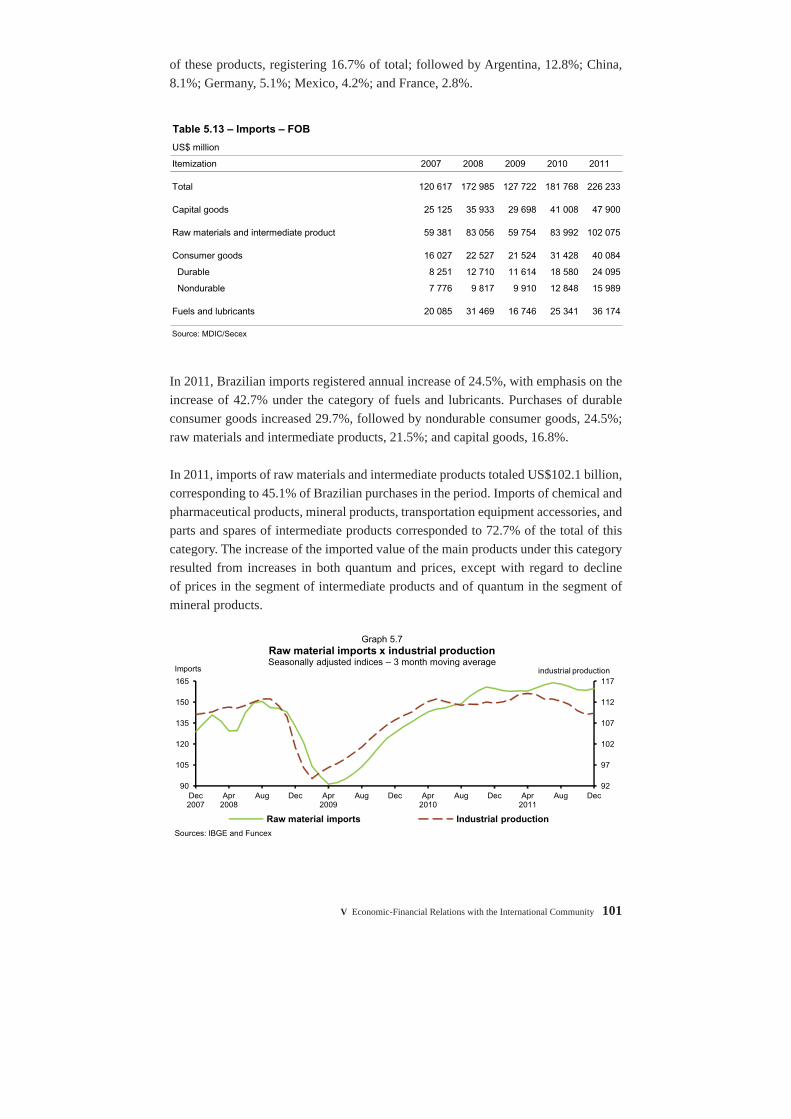

In 2011, Brazilian imports registered annual increase of 24.5%, with emphasis on the increase of 42.7% under the category of fuels and lubricants. Purchases of durable consumer goods increased 29.7%, followed by nondurable consumer goods, 24.5%; raw materials and intermediate products, 21.5%; and capital goods, 16.8%.

In 2011, imports of raw materials and intermediate products totaled US$102.1 billion, corresponding to 45.1% of Brazilian purchases in the period. Imports of chemical and pharmaceutical products, mineral products, transportation equipment accessories, and parts and spares of intermediate products corresponded to 72.7% of the total of this category. The increase of the imported value of the main products under this category resulted from increases in both quantum and prices, except with regard to decline of prices in the segment of intermediate products and of quantum in the segment of mineral products.

Table 5.13 – Imports – FOB

US$ million

Itemization 2007 2008 2009 2010 2011

Total 120 617 172 985 127 722 181 768 226 233

Capital goods 25 125 35 933 29 698 41 008 47 900

Raw materials and intermediate product 59 381 83 056 59 754 83 992 102 075

Consumer goods 16 027 22 527 21 524 31 428 40 084

Durable 8 251 12 710 11 614 18 580 24 095

Nondurable 7 776 9 817 9 910 12 848 15 989

Fuels and lubricants 20 085 31 469 16 746 25 341 36 174

Source: MDIC/Secex

92

97

102

107

112

117

90

105

120

135

150

165

Dec 2007

Apr 2008

Aug Dec Apr 2009

Aug Dec Apr 2010

Aug Dec Apr 2011

Aug Dec

industrial productionImports

Sources: IBGE and Funcex

Raw material imports Industrial production

Graph 5.7Raw material imports x industrial productionSeasonally adjusted indices – 3 month moving average

102 Boletim do Banco Central do Brasil – Annual Report 2011

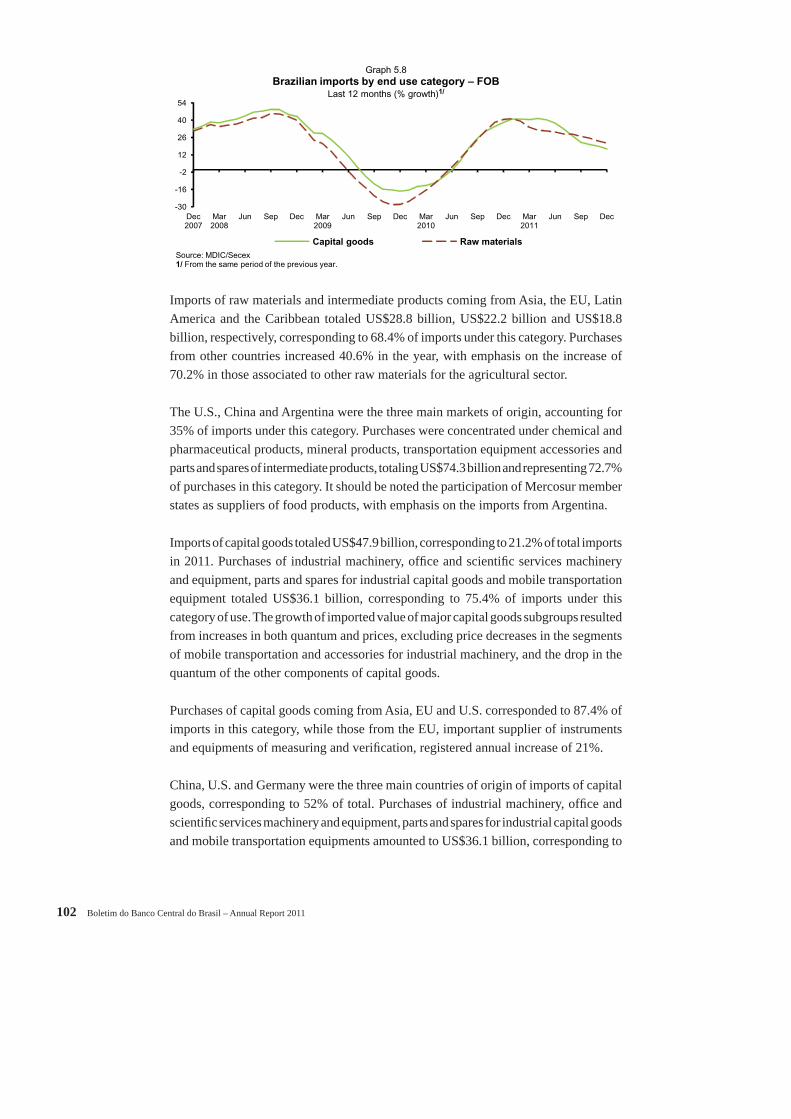

Imports of raw materials and intermediate products coming from Asia, the EU, Latin America and the Caribbean totaled US$28.8 billion, US$22.2 billion and US$18.8 billion, respectively, corresponding to 68.4% of imports under this category. Purchases from other countries increased 40.6% in the year, with emphasis on the increase of 70.2% in those associated to other raw materials for the agricultural sector.

The U.S., China and Argentina were the three main markets of origin, accounting for 35% of imports under this category. Purchases were concentrated under chemical and pharmaceutical products, mineral products, transportation equipment accessories and parts and spares of intermediate products, totaling US$74.3 billion and representing 72.7% of purchases in this category. It should be noted the participation of Mercosur member states as suppliers of food products, with emphasis on the imports from Argentina.

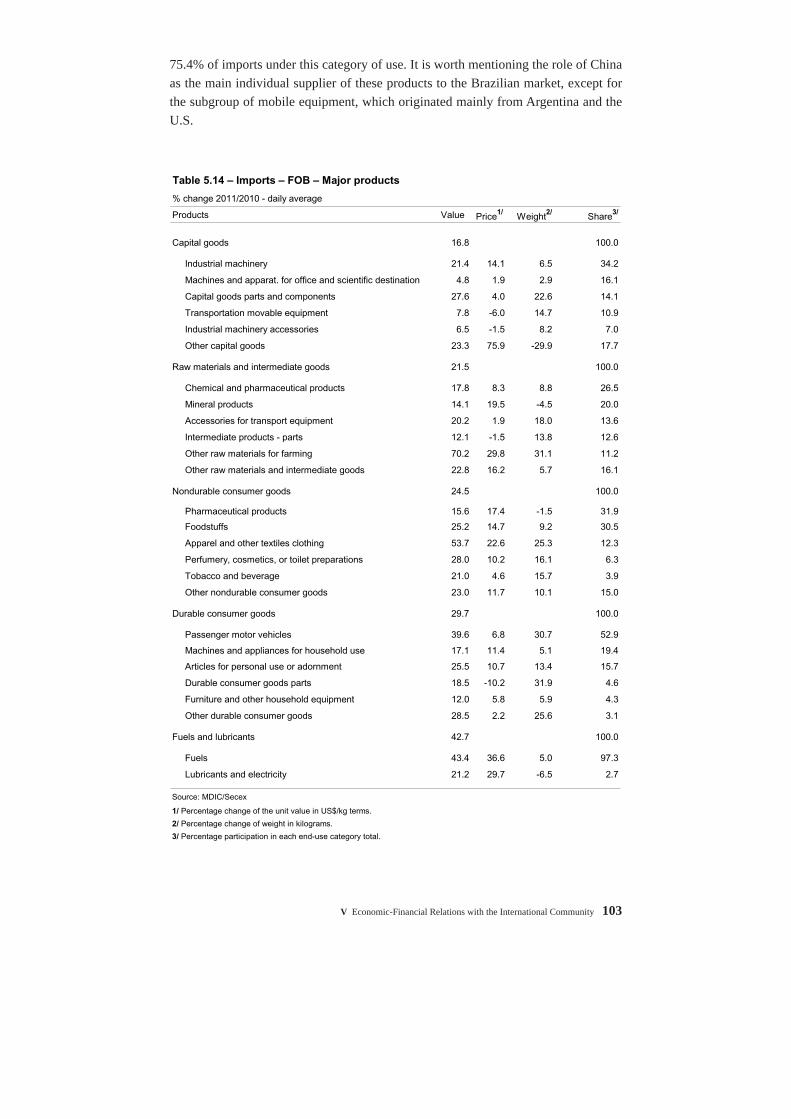

Imports of capital goods totaled US$47.9 billion, corresponding to 21.2% of total imports in 2011. Purchases of industrial machinery, offi ce and scientifi c services machinery and equipment, parts and spares for industrial capital goods and mobile transportation equipment totaled US$36.1 billion, corresponding to 75.4% of imports under this category of use. The growth of imported value of major capital goods subgroups resulted from increases in both quantum and prices, excluding price decreases in the segments of mobile transportation and accessories for industrial machinery, and the drop in the quantum of the other components of capital goods.

Purchases of capital goods coming from Asia, EU and U.S. corresponded to 87.4% of imports in this category, while those from the EU, important supplier of instruments and equipments of measuring and verifi cation, registered annual increase of 21%.

China, U.S. and Germany were the three main countries of origin of imports of capital goods, corresponding to 52% of total. Purchases of industrial machinery, offi ce and scientifi c services machinery and equipment, parts and spares for industrial capital goods and mobile transportation equipments amounted to US$36.1 billion, corresponding to

-30

-16

-2

12

26

40

54

Dec 2007

Mar 2008

Jun Sep Dec Mar 2009

Jun Sep Dec Mar 2010

Jun Sep Dec Mar 2011

Jun Sep Dec

Source: MDIC/Secex1/ From the same period of the previous year.

Capital goods Raw materials

Graph 5.8Brazilian imports by end use category – FOB

Last 12 months (% growth)1/

V Economic-Financial Relations with the International Community 103

75.4% of imports under this category of use. It is worth mentioning the role of China as the main individual supplier of these products to the Brazilian market, except for the subgroup of mobile equipment, which originated mainly from Argentina and the U.S.

Table 5.14 – Imports – FOB – Major products

% change 2011/2010 - daily average

Products Value Price1/ Weight2/ Share3/

Capital goods 16.8 100.0

Industrial machinery 21.4 14.1 6.5 34.2

Machines and apparat. for office and scientific destination 4.8 1.9 2.9 16.1

Capital goods parts and components 27.6 4.0 22.6 14.1

Transportation movable equipment 7.8 -6.0 14.7 10.9

Industrial machinery accessories 6.5 -1.5 8.2 7.0

Other capital goods 23.3 75.9 -29.9 17.7

Raw materials and intermediate goods 21.5 100.0

Chemical and pharmaceutical products 17.8 8.3 8.8 26.5

Mineral products 14.1 19.5 -4.5 20.0

Accessories for transport equipment 20.2 1.9 18.0 13.6

Intermediate products - parts 12.1 -1.5 13.8 12.6

Other raw materials for farming 70.2 29.8 31.1 11.2

Other raw materials and intermediate goods 22.8 16.2 5.7 16.1

Nondurable consumer goods 24.5 100.0

Pharmaceutical products 15.6 17.4 -1.5 31.9

Foodstuffs 25.2 14.7 9.2 30.5

Apparel and other textiles clothing 53.7 22.6 25.3 12.3

Perfumery, cosmetics, or toilet preparations 28.0 10.2 16.1 6.3

Tobacco and beverage 21.0 4.6 15.7 3.9

Other nondurable consumer goods 23.0 11.7 10.1 15.0

Durable consumer goods 29.7 100.0

Passenger motor vehicles 39.6 6.8 30.7 52.9

Machines and appliances for household use 17.1 11.4 5.1 19.4

Articles for personal use or adornment 25.5 10.7 13.4 15.7

Durable consumer goods parts 18.5 -10.2 31.9 4.6

Furniture and other household equipment 12.0 5.8 5.9 4.3

Other durable consumer goods 28.5 2.2 25.6 3.1

Fuels and lubricants 42.7 100.0

Fuels 43.4 36.6 5.0 97.3

Lubricants and electricity 21.2 29.7 -6.5 2.7

Source: MDIC/Secex

1/ Percentage change of the unit value in US$/kg terms.

2/ Percentage change of weight in kilograms.

3/ Percentage participation in each end-use category total.

104 Boletim do Banco Central do Brasil – Annual Report 2011

Table 5.15 – Imports by category of use and by region – FOB

US$ million

Product 2010

Value Value Change from

2010 (%) Category Blocs

Total 181 768 226 233 24.5 100.0 -

Capital goods 41 008 47 900 16.8 21.2 -

Durable consumer goods 18 580 24 095 29.7 10.7 -

Nondurable consumer goods 12 848 15 989 24.5 7.1 -

Fuels and lubricants 25 341 36 174 42.7 16.0 -

Raw material and intermediate goods 83 992 102 075 21.5 45.1 -

Latin America and Caribe 30 919 37 810 22.3 16.7 100.0

Capital goods 2 959 3 339 12.8 7.0 8.8

Durable consumer goods 5 575 6 983 25.2 29.0 18.5

Nondurable consumer goods 3 062 3 834 25.2 24.0 10.1

Fuels and lubricants 3 515 4 846 37.9 13.4 12.8

Raw material and intermediate goods 15 808 18 807 19.0 18.4 49.7

Mercosul 16 620 19 375 16.6 8.6 100.0

Capital goods 2 137 2 451 14.7 5.1 12.7

Durable consumer goods 4 115 4 717 14.6 19.6 24.3

Nondurable consumer goods 2 174 2 720 25.1 17.0 14.0

Fuels and lubricants 343 495 44.5 1.4 2.6

Raw material and intermediate goods 7 851 8 992 14.5 8.8 46.4

USA1/ 27 256 34 225 25.6 15.1 100.0

Capital goods 6 978 8 339 19.5 17.4 24.4

Durable consumer goods 954 1 138 19.3 4.7 3.3

Nondurable consumer goods 1 490 1 764 18.4 11.0 5.2

Fuels and lubricants 4 133 6 225 50.6 17.2 18.2

Raw material and intermediate goods 13 701 16 760 22.3 16.4 49.0

European Union 39 127 46 416 18.6 20.5 100.0

Capital goods 12 067 14 596 21.0 30.5 31.4

Durable consumer goods 2 548 3 392 33.2 14.1 7.3

Nondurable consumer goods 3 702 4 588 23.9 28.7 9.9

Fuels and lubricants 1 497 1 673 11.8 4.6 3.6

Raw material and intermediate goods 19 314 22 166 14.8 21.7 47.8

Asia 56 150 70 076 24.8 31.0 100.0

Capital goods 16 068 18 844 17.3 39.3 26.9

Durable consumer goods 9 184 12 075 31.5 50.1 17.2

Nondurable consumer goods 3 318 4 489 35.3 28.1 6.4

Fuels and lubricants 3 444 5 824 69.1 16.1 8.3

Raw material and intermediate goods 24 137 28 844 19.5 28.3 41.2

Others 28 316 37 706 33.2 16.7 100.0

Capital goods 2 936 2 781 -5.3 5.8 7.4

Durable consumer goods 320 507 58.7 2.1 1.3

Nondurable consumer goods 1 276 1 314 3.0 8.2 3.5

Fuels and lubricants 12 752 17 606 38.1 48.7 46.7

Raw material and intermediate goods 11 032 15 498 40.5 15.2 41.1

Source: MDIC/Secex

1/ Includes Puerto Rico.

2011

Share (%)

V Economic-Financial Relations with the International Community 105

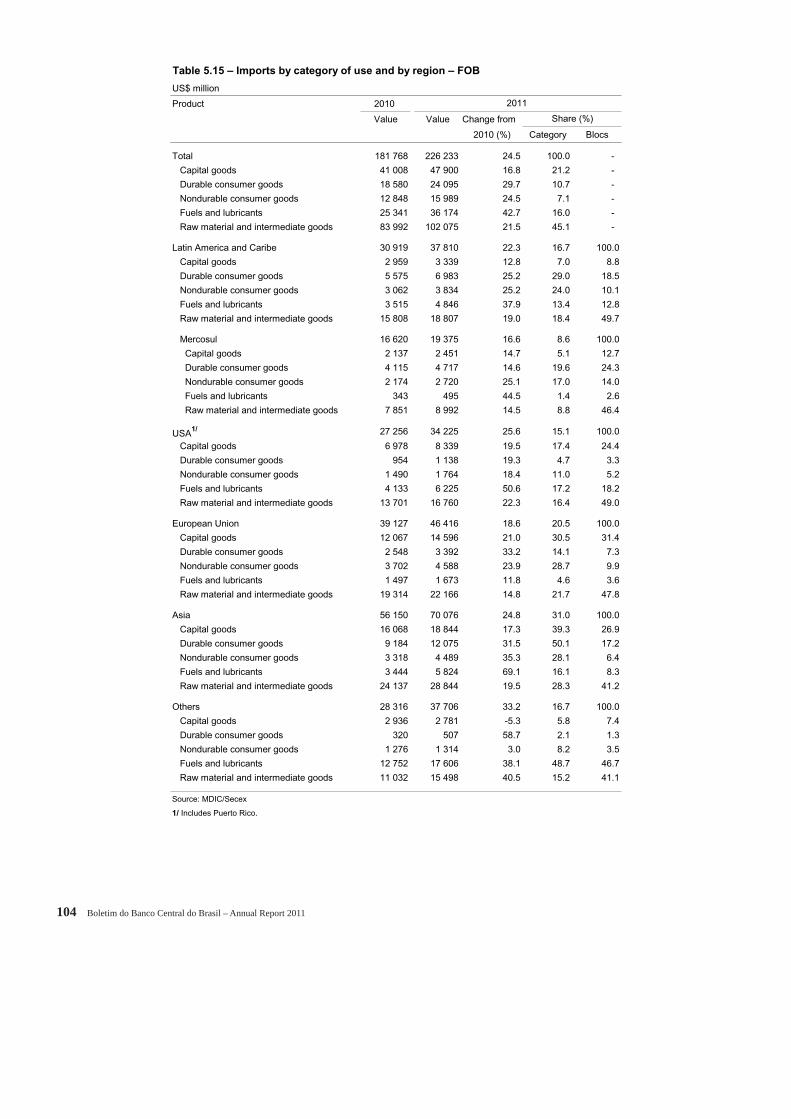

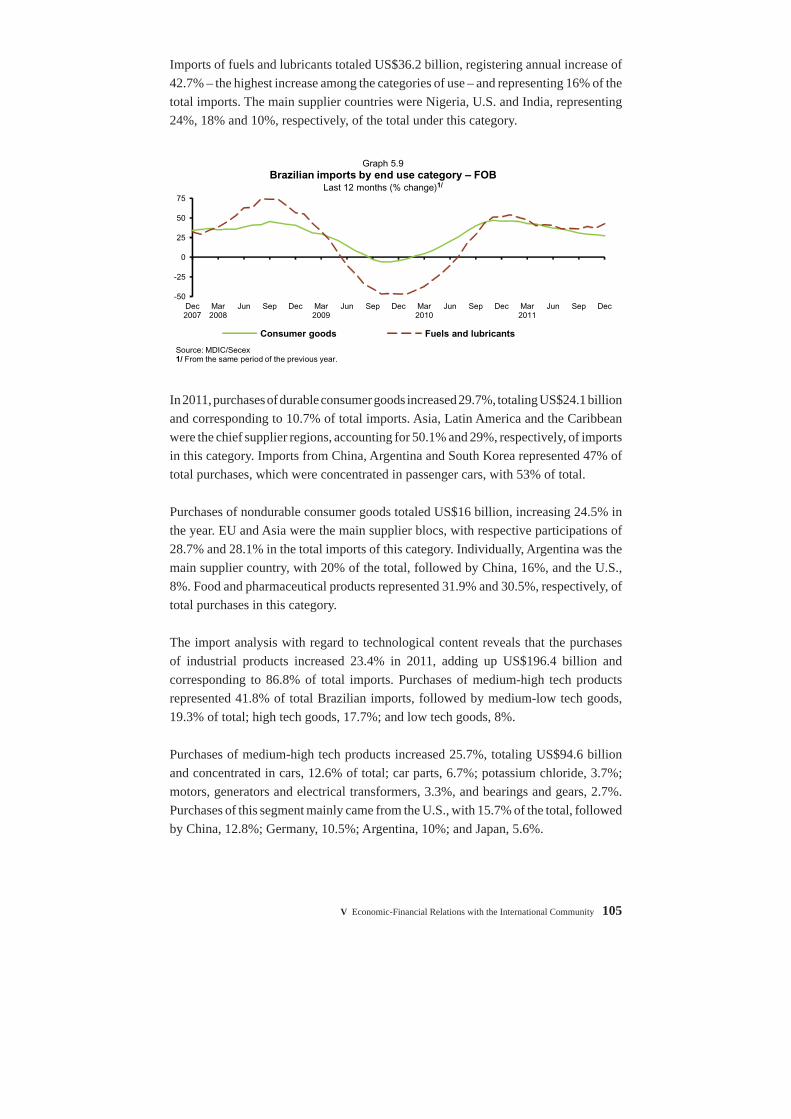

Imports of fuels and lubricants totaled US$36.2 billion, registering annual increase of 42.7% – the highest increase among the categories of use – and representing 16% of the total imports. The main supplier countries were Nigeria, U.S. and India, representing 24%, 18% and 10%, respectively, of the total under this category.

In 2011, purchases of durable consumer goods increased 29.7%, totaling US$24.1 billion and corresponding to 10.7% of total imports. Asia, Latin America and the Caribbean were the chief supplier regions, accounting for 50.1% and 29%, respectively, of imports in this category. Imports from China, Argentina and South Korea represented 47% of total purchases, which were concentrated in passenger cars, with 53% of total.

Purchases of nondurable consumer goods totaled US$16 billion, increasing 24.5% in the year. EU and Asia were the main supplier blocs, with respective participations of 28.7% and 28.1% in the total imports of this category. Individually, Argentina was the main supplier country, with 20% of the total, followed by China, 16%, and the U.S., 8%. Food and pharmaceutical products represented 31.9% and 30.5%, respectively, of total purchases in this category.

The import analysis with regard to technological content reveals that the purchases of industrial products increased 23.4% in 2011, adding up US$196.4 billion and corresponding to 86.8% of total imports. Purchases of medium-high tech products represented 41.8% of total Brazilian imports, followed by medium-low tech goods, 19.3% of total; high tech goods, 17.7%; and low tech goods, 8%.

Purchases of medium-high tech products increased 25.7%, totaling US$94.6 billion and concentrated in cars, 12.6% of total; car parts, 6.7%; potassium chloride, 3.7%; motors, generators and electrical transformers, 3.3%, and bearings and gears, 2.7%. Purchases of this segment mainly came from the U.S., with 15.7% of the total, followed by China, 12.8%; Germany, 10.5%; Argentina, 10%; and Japan, 5.6%.

-50

-25

0

25

50

75

Dec 2007

Mar 2008

Jun Sep Dec Mar 2009

Jun Sep Dec Mar 2010

Jun Sep Dec Mar 2011

Jun Sep Dec

Source: MDIC/Secex1/ From the same period of the previous year.

Consumer goods Fuels and lubricants

Graph 5.9Brazilian imports by end use category – FOB

Last 12 months (% change)1/

106 Boletim do Banco Central do Brasil – Annual Report 2011

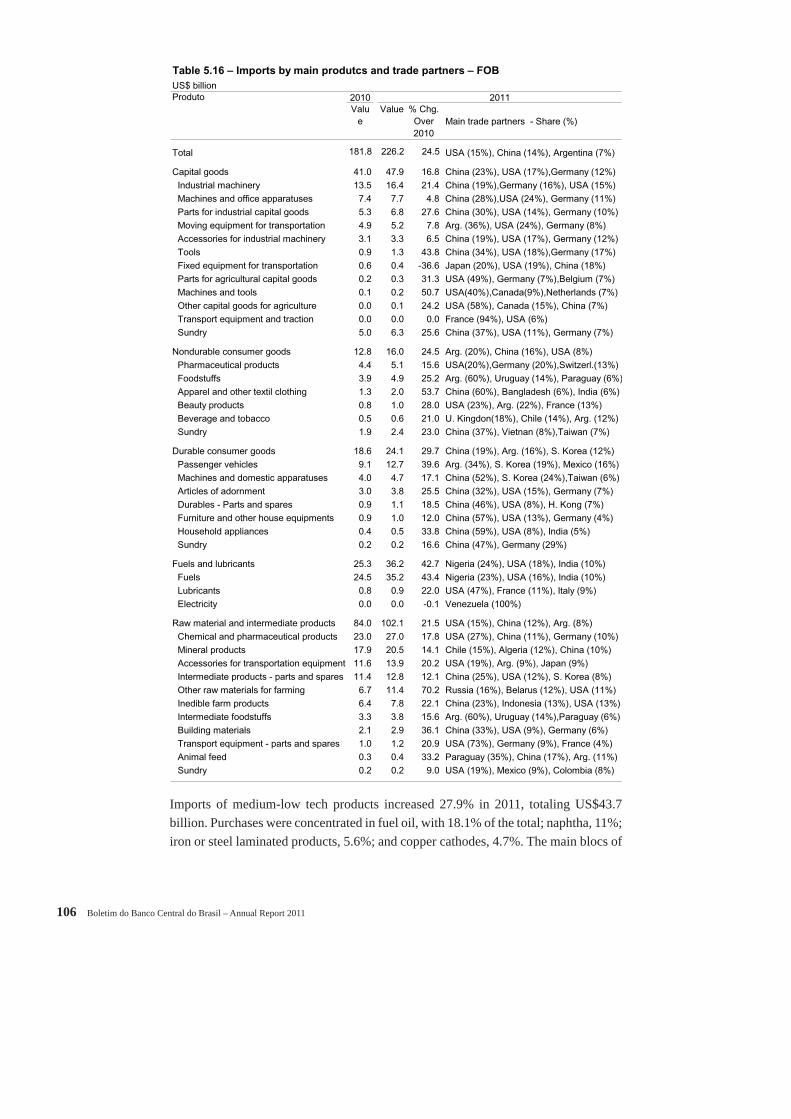

Imports of medium-low tech products increased 27.9% in 2011, totaling US$43.7 billion. Purchases were concentrated in fuel oil, with 18.1% of the total; naphtha, 11%; iron or steel laminated products, 5.6%; and copper cathodes, 4.7%. The main blocs of

Table 5.16 – Imports by main produtcs and trade partners – FOB

US$ billionProduto 2010

Value

Value % Chg. Over 2010

Main trade partners - Share (%)

Total 181.8 226.2 24.5 USA (15%), China (14%), Argentina (7%)

Capital goods 41.0 47.9 16.8 China (23%), USA (17%),Germany (12%)Industrial machinery 13.5 16.4 21.4 China (19%),Germany (16%), USA (15%)Machines and office apparatuses 7.4 7.7 4.8 China (28%),USA (24%), Germany (11%)Parts for industrial capital goods 5.3 6.8 27.6 China (30%), USA (14%), Germany (10%)Moving equipment for transportation 4.9 5.2 7.8 Arg. (36%), USA (24%), Germany (8%)Accessories for industrial machinery 3.1 3.3 6.5 China (19%), USA (17%), Germany (12%)Tools 0.9 1.3 43.8 China (34%), USA (18%),Germany (17%)Fixed equipment for transportation 0.6 0.4 -36.6 Japan (20%), USA (19%), China (18%)Parts for agricultural capital goods 0.2 0.3 31.3 USA (49%), Germany (7%),Belgium (7%)Machines and tools 0.1 0.2 50.7 USA(40%),Canada(9%),Netherlands (7%)Other capital goods for agriculture 0.0 0.1 24.2 USA (58%), Canada (15%), China (7%)Transport equipment and traction 0.0 0.0 0.0 France (94%), USA (6%)Sundry 5.0 6.3 25.6 China (37%), USA (11%), Germany (7%)

Nondurable consumer goods 12.8 16.0 24.5 Arg. (20%), China (16%), USA (8%)Pharmaceutical products 4.4 5.1 15.6 USA(20%),Germany (20%),Switzerl.(13%)Foodstuffs 3.9 4.9 25.2 Arg. (60%), Uruguay (14%), Paraguay (6%)Apparel and other textil clothing 1.3 2.0 53.7 China (60%), Bangladesh (6%), India (6%)Beauty products 0.8 1.0 28.0 USA (23%), Arg. (22%), France (13%)Beverage and tobacco 0.5 0.6 21.0 U. Kingdon(18%), Chile (14%), Arg. (12%)Sundry 1.9 2.4 23.0 China (37%), Vietnan (8%),Taiwan (7%)